Embed Size (px)

Citation preview

From Business Planning to Financial Modelling and Valuation

10 October 2008(You will remember what you were doing

the day of The Crash)

Michel ALLÉYvan de BEAUFFORTGEST D-422

|1

From Business Planning to Financial Modelling and Valuation

Agenda of the evening

• 18h00 – 18h15 Agenda alignment– Excel session 1st or 8th November from 10h to 13h (with laptop)

– Meetings with experts 7th November

– Final presentation 10th December

• 18h15 – 20h00 Business planning & valuation

• 20h15 – 21h15 The airlines universe

|2

From Business Planning to Financial Modelling and Valuation

1. Introductiona. Objective of the courseb. Concept of business strategyc. The Business Pland. Scope and contexte. Use of the Business Planf. Financial Model as part of the Business Plang. Elaborating the plan = An iterative process

Table of content (1/5)

|3

From Business Planning to Financial Modelling and Valuation

2. Business Planninga. Source of informationb. What does the Company do?c. Economic environmentd. Underlying marketse. Competitorsf. Cost structure and sales priceg. Capex requirementh. Working capital requirementsi. Porter analysis j. SWOT analysisk. Human resources

Table of content (2/5)

|4

From Business Planning to Financial Modelling and Valuation

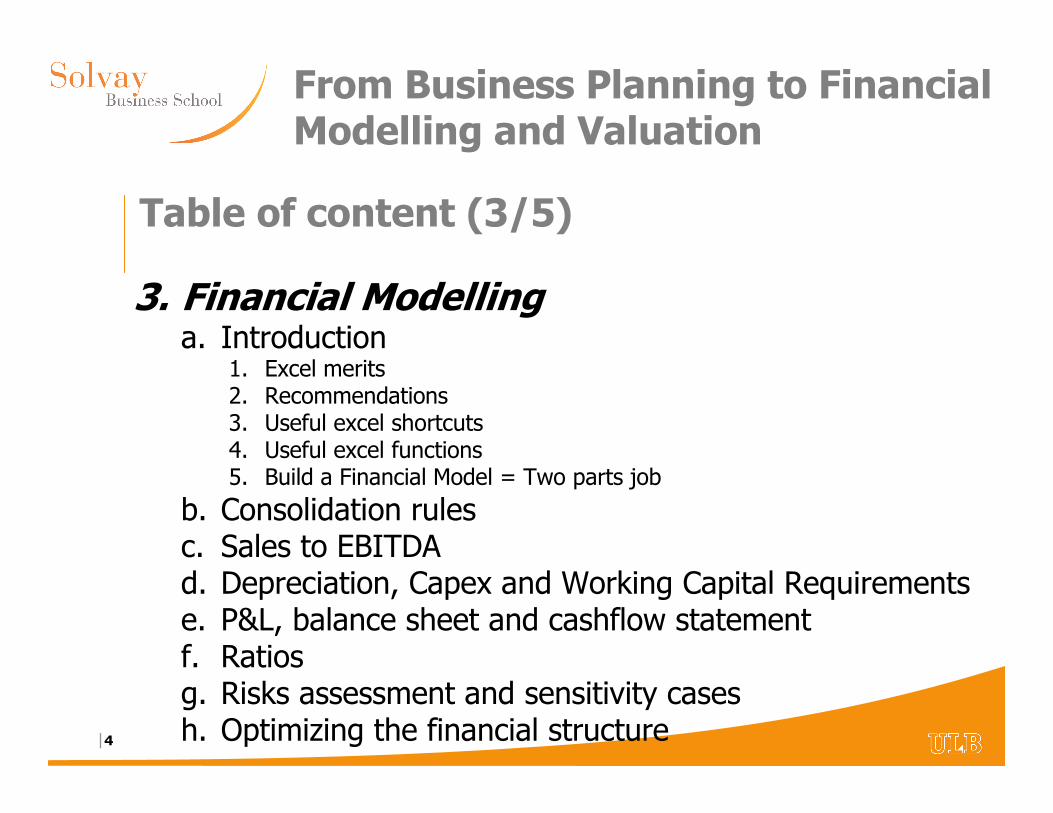

3. Financial Modellinga. Introduction

1. Excel merits2. Recommendations3. Useful excel shortcuts4. Useful excel functions5. Build a Financial Model = Two parts job

b. Consolidation rulesc. Sales to EBITDAd. Depreciation, Capex and Working Capital Requirementse. P&L, balance sheet and cashflow statementf. Ratiosg. Risks assessment and sensitivity casesh. Optimizing the financial structure

Table of content (3/5)

|5

From Business Planning to Financial Modelling and Valuation

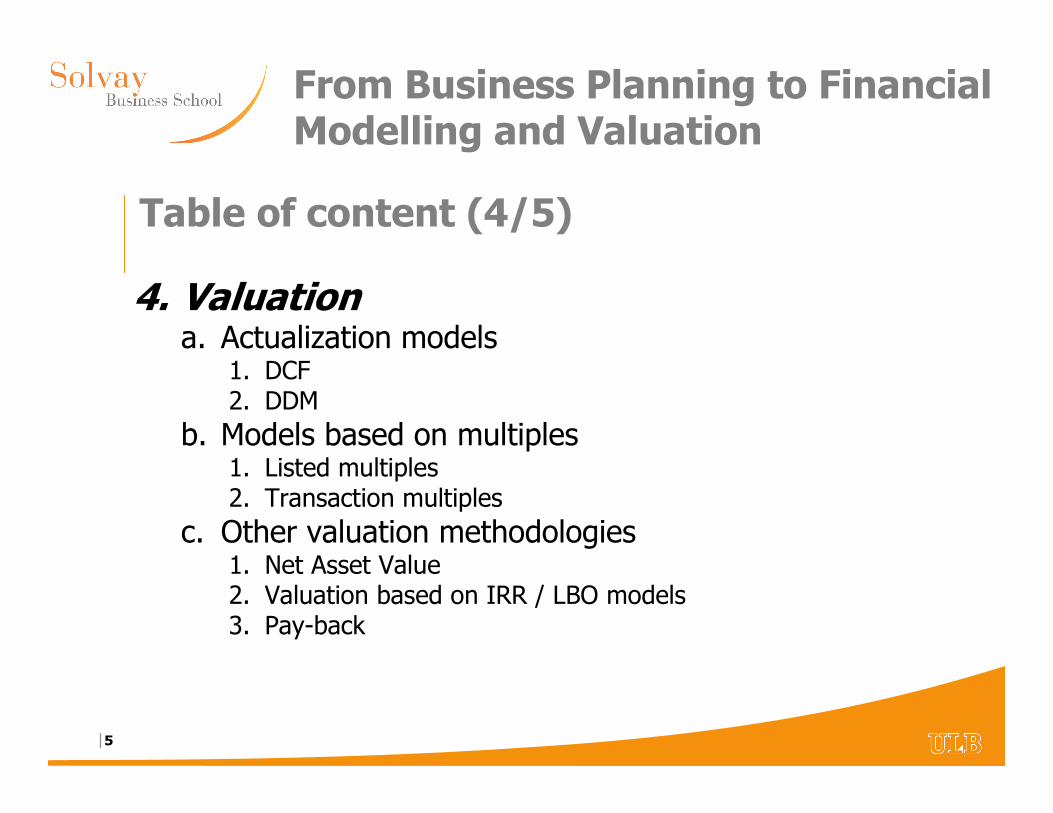

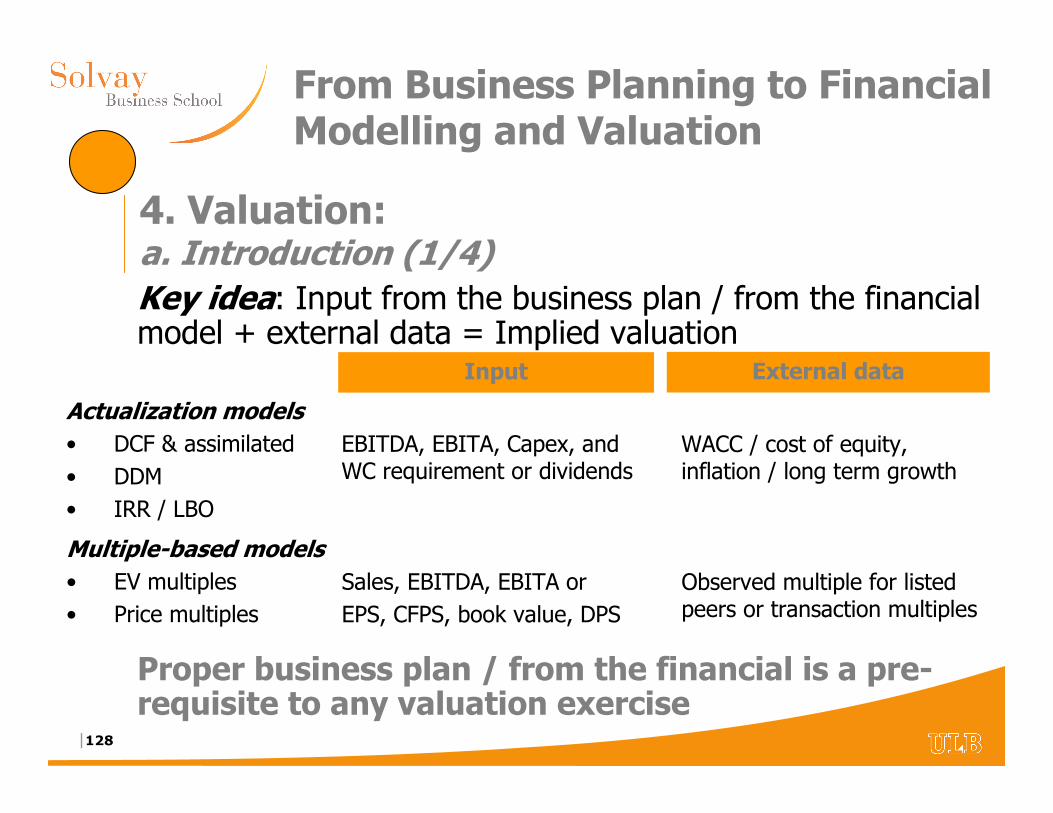

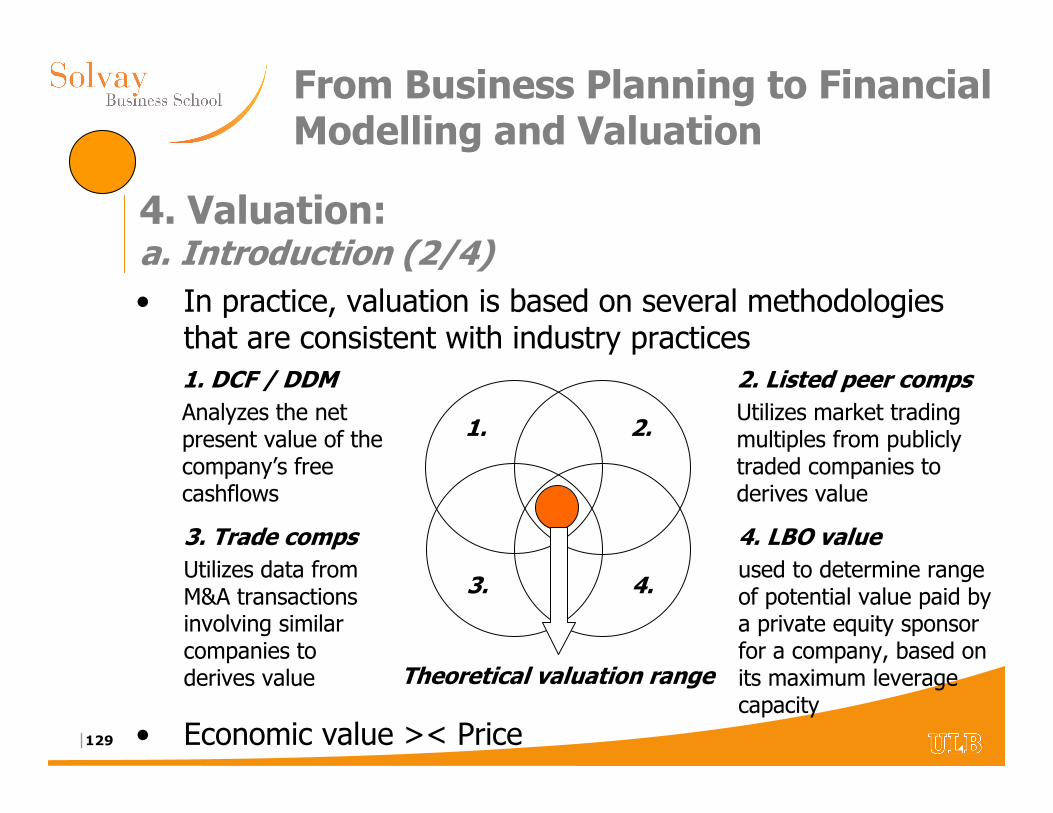

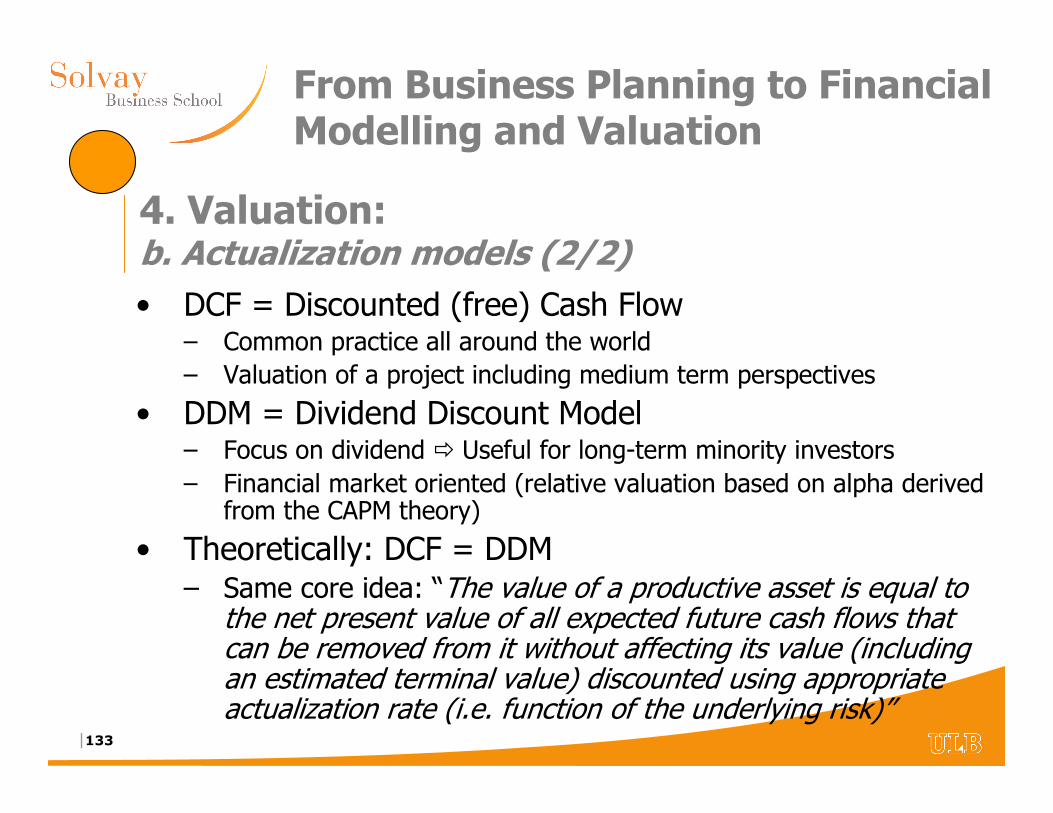

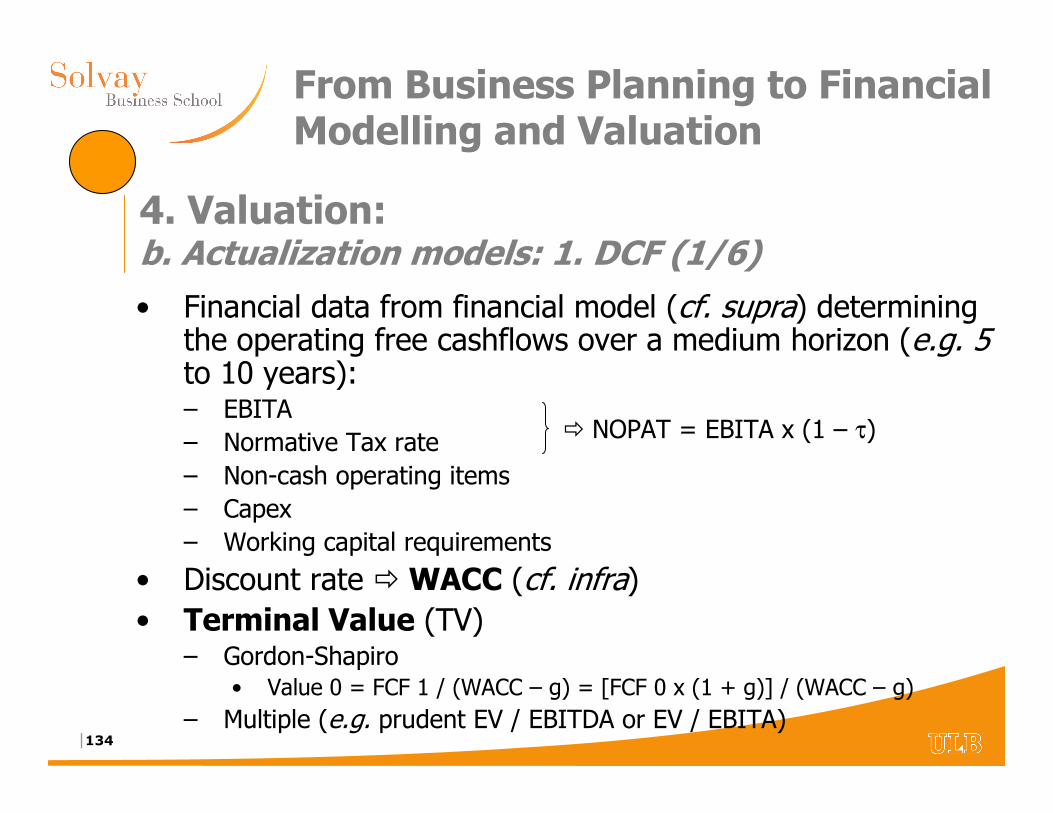

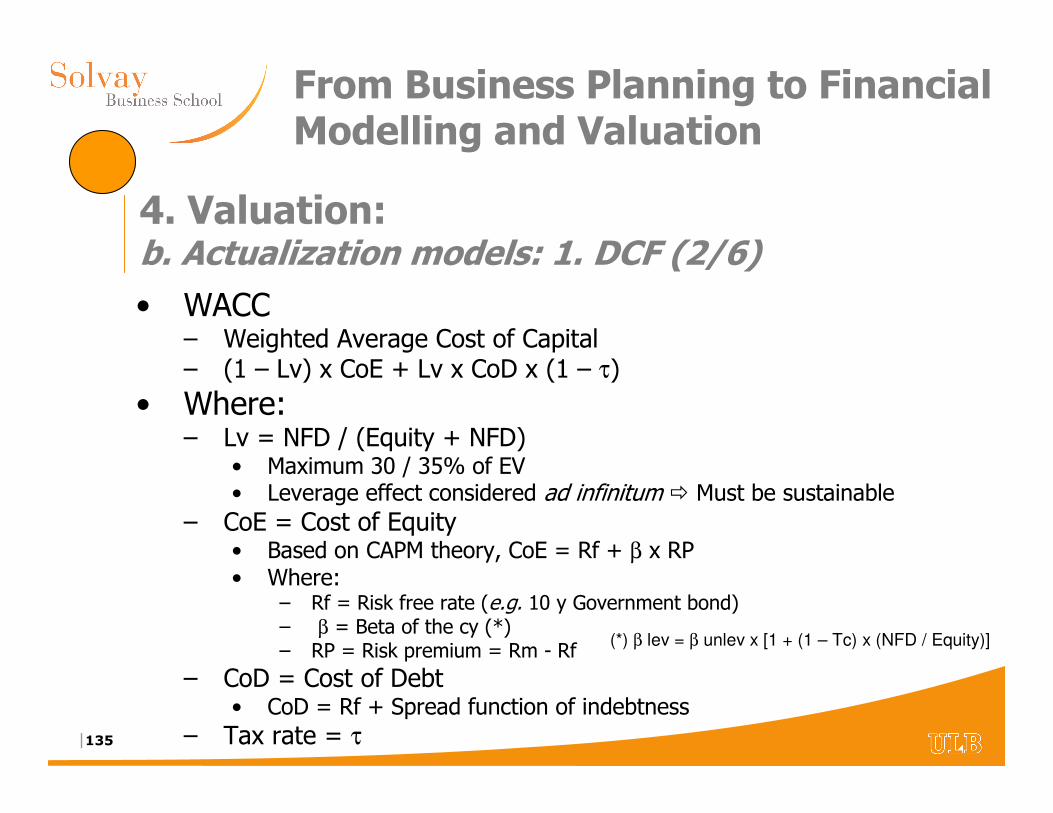

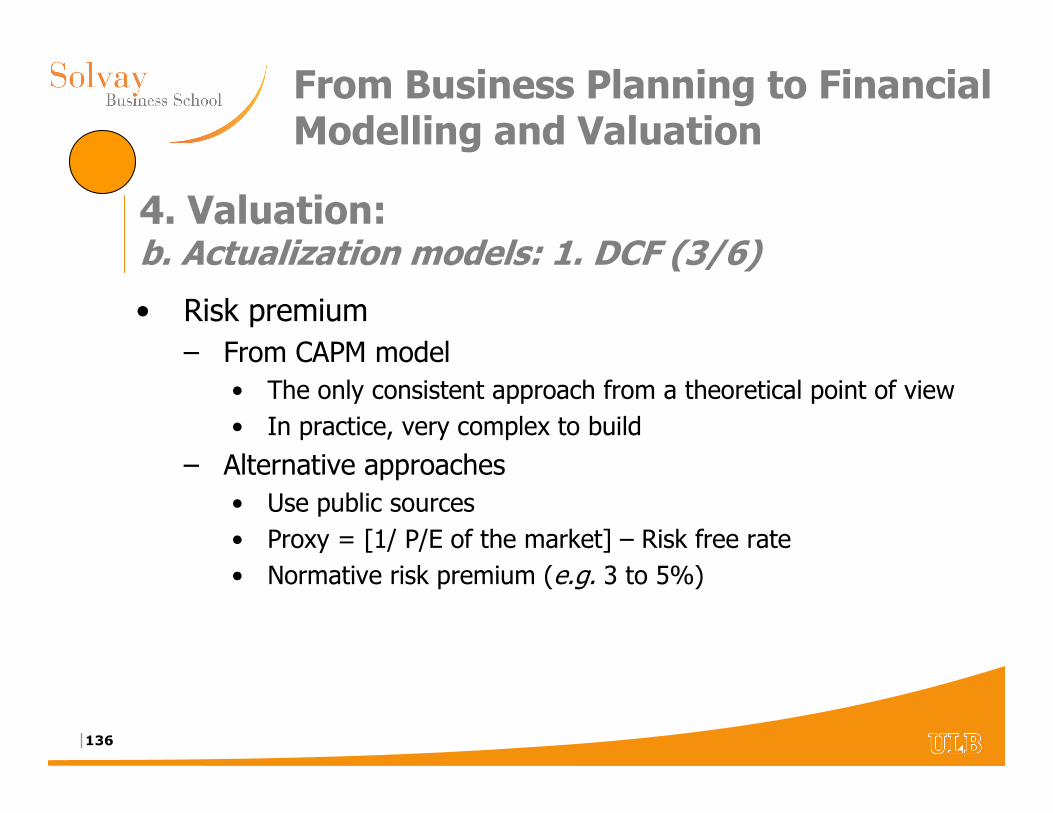

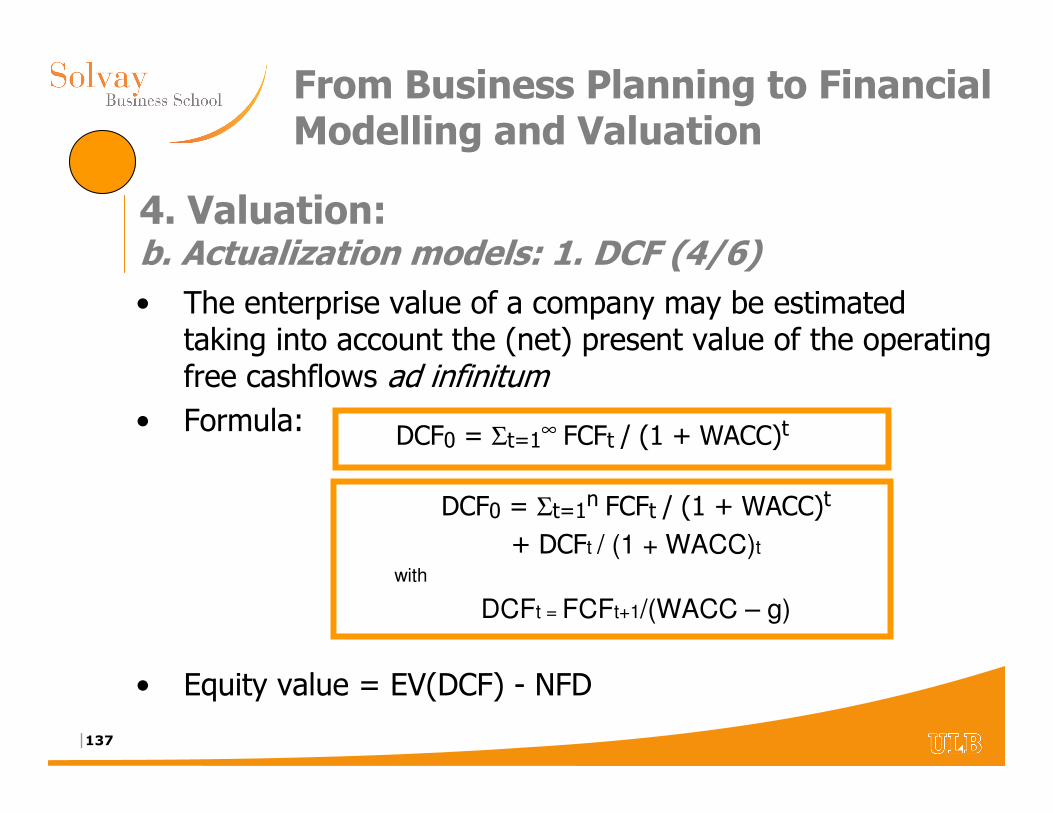

4. Valuationa. Actualization models

1. DCF2. DDM

b. Models based on multiples1. Listed multiples2. Transaction multiples

c. Other valuation methodologies1. Net Asset Value2. Valuation based on IRR / LBO models3. Pay-back

Table of content (4/5)

|6

From Business Planning to Financial Modelling and Valuation

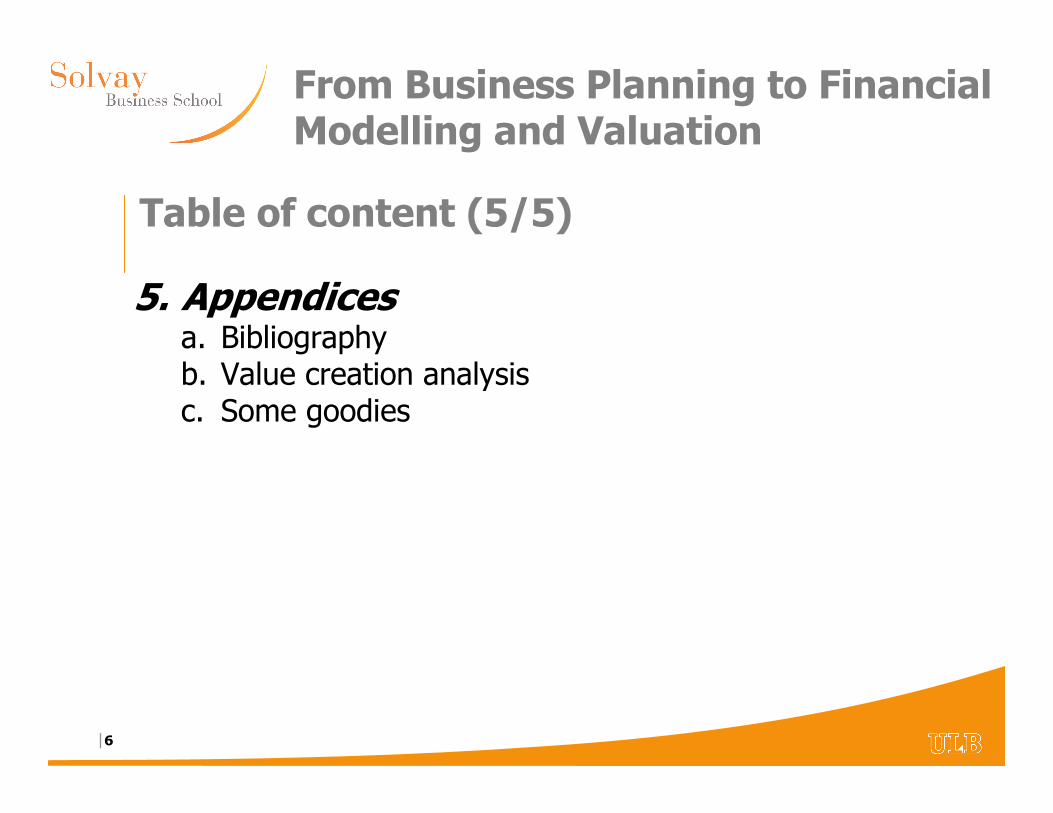

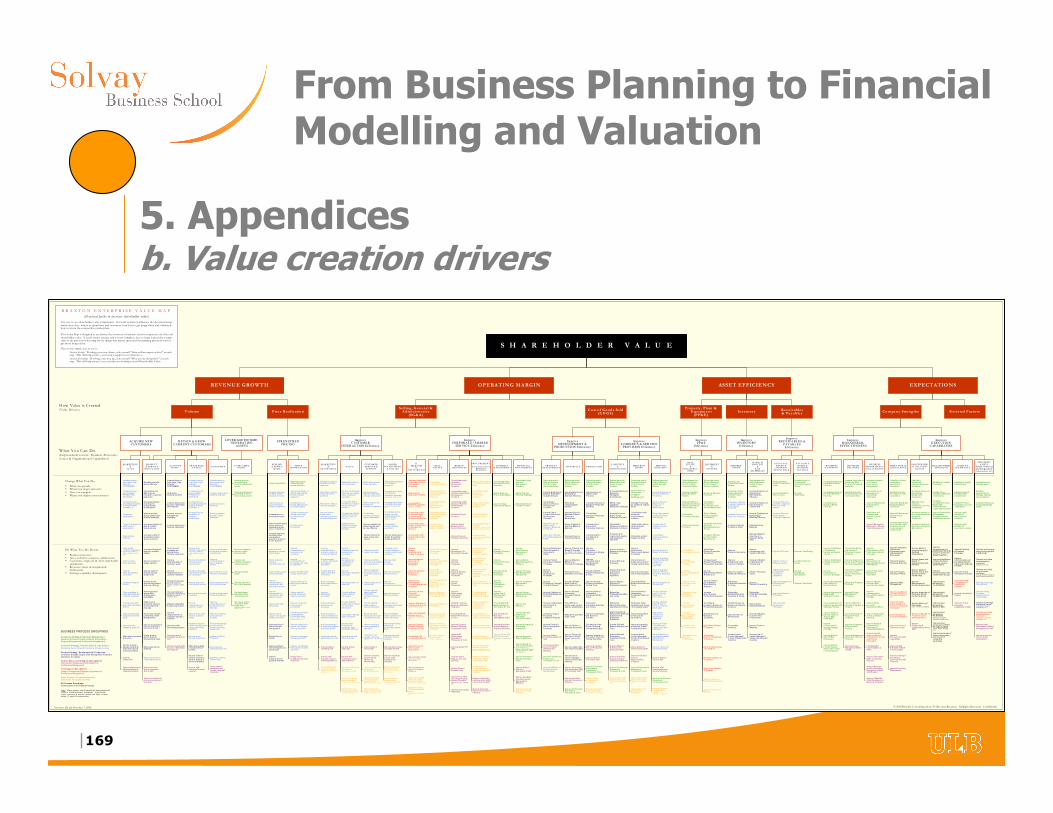

5. Appendicesa. Bibliographyb. Value creation analysisc. Some goodies

Table of content (5/5)

|7

From Business Planning to Financial Modelling and Valuation

1. Introduction

|8

From Business Planning to Financial Modelling and Valuation

1. Introduction: a. Objectives of the course

To get yourself familiar with…

• How to produce a set of viable business assumptions?

• How to input these in a financial model?

• How to derive a valuation?

• Where to find hidden jewels?

• How to determine the appropriate financial structure of a company?

|9

From Business Planning to Financial Modelling and Valuation

1. Introduction: b. Concept of business strategy (1/5)

• « Strategy is a concept by which we are trying to bring coherence to a multitude of actions by different actors in the organization. As such it is a complement to both organization, and corporate culture which perform the same function »

• The de facto strategy of a company corresponds to the underlying pattern in its resource allocation decisions – the way it deploys not only financial resources, but also its best people, and senior manager’s time. In that sense ALL companies have a strategy, through not always a conscious one

|10

From Business Planning to Financial Modelling and Valuation

1. Introduction: b. Concept of business strategy (2/5)

• Most companies develop however a formal and explicit strategy

• The starting point of such strategic thinking is an assessment of the fit between:– the company environment (i.e. what might be done?)

– its capabilities (i.e. what can be done?)

– and its identity (i.e. what one want to do?)

• Such strategy formulation implies not only a phase of analysis, but also the more creative generation of options and the need for choices

|11

From Business Planning to Financial Modelling and Valuation

1. Introduction: b. Concept of business strategy (3/5)

• The strategy which results from an assessment can be defined as « a set of deliberate priorities in resource allocation which, by building and maintaining the company’s competitive advantage, will allow it to reach its objectives »

• Difference between a “strategy” and a “tactic”– Strategy involves the “big picture”. The overall plan, how the

campaign will achieve organizational goals and objectives. Strategic planning helps to determine how the organization will be positioned

– Tactics are activities specifically created and selected to reach specific and measurable objectives. Tactics are the actual ways in which the strategies are executed

– “Strategy is an art. Tactics are science” Carl von Clausewitz

|12

From Business Planning to Financial Modelling and Valuation

1. Introduction: b. Concept of business strategy (4/5)

• A statement of business strategy typically consists of the following elements:– a set of objectives– a business definition– a competitive positioning (e.g. dominance, differentiation or

focus)

– a consistent set of functional policies– priorities in resources allocation

• Mostly, strategies are interacting with daily operations

|13

From Business Planning to Financial Modelling and Valuation

1. Introduction: b. Concept of business strategy (5/5)

• Apart from the socio-economic-political environment, the starting point of the environmental analysis is to focus on the immediate industry competitive environment as it is today.

• Four elements need to be analyzed in terms of the current situation and of trends:1. Market (segments, customers,…)

2. Competition (direct and indirect)

3. Cost structure (value chain composition and drivers)

4. Technology (underlies cost structure)

Goal = Determination of key success factors

|14

From Business Planning to Financial Modelling and Valuation

• The Business Plan (BP) describes and quantifies the long term project of the management for the company– Describes

• Facts • In a coherent vision

– Quantifies• Figures• In a coherent framework

– This, over a long period of time• Extended period of time (3 to 10 years)

• Where periodicity is a function of the situation (year, half year, quarter, …)

1. Introduction:c. The Business Plan

|15

From Business Planning to Financial Modelling and Valuation

1. Introduction:d. Scope and context

• The BP refers to all dimensions of the Company– Products

– Marketing

– Production

– R&D

– Human Resources

– Finance

• The BP depends on the business context– Integrating the overall and industry business trends

– Integrating the present and future competition

– Integrating the specific constraints (e.g. shareholders, investment bankers, debt providers, …)

|16

From Business Planning to Financial Modelling and Valuation

1. Introduction:e. Use of the Business Plan

� The BP is an essential work in the life of a company� Start-up or existing businesses

� Opportunity to stand back from the day-to-day activities

� The BP gives guidelines for the management � A contract between management and shareholders / bankers

� The BP is an assessment tool for the shareholders in investment decisions� It shows the profitability and the dividend yield prospects

� It shows how much value can be created

� The BP is a tool to evaluate the performances of the management� Are the goals achieved or not?

|17

From Business Planning to Financial Modelling and Valuation

1. Introduction:f. Financial Model as part of the Business Plan (1/3)

� The Financial Model is the rational translation in financial terms of the content of the BP� Forecasts for Profit & Loss account (P&L), Balance Sheet (BS) and

CashFlow Statement (CFS)� Link to be made with historical accounts (if any >< Start-up)� Put in simple equation an ever more complex reality

� Its quality relies on the quality of the BP’s assumptions (as well as coherent building)

� Objective tool � From P&L to CFS (through BS) �Identification of the cash needs / surplus � Determination of the optimal financial structure (maximisation under constraints)

� Prerequisite material support to assess the company’s value in a second step

|18

From Business Planning to Financial Modelling and Valuation

1. Introduction:f. Financial Model components: quick reminder (2/3)• P&L or “Profit and Losses” statement or income statement :

– It summarizes a firm's financial transactions over an interval of time– It starts from sales (top line) and ends up at net profit (bottom line), taking into

consideration costs, amortization, financial charges

• Balance Sheet:– It is the picture of the assets and liabilities of a company, a snapshot of a firm's

financial resources and obligations at a single point in time– At the right side (Liabilities) is the inventory of how the company is financed from

long term to short term (top right: equity then long term financial debt, bottom right: short term suppliers debt)

– The left side (Assets) registers how the financing is employed, from long term assets (e.g. buildings or intangibles) to short term ones (e.g. cash)

– Hence,

• Cash Flow statement: – Shows a company's flow of cash– The money coming into the business is called cash inflow, and money going out

from the business is called cash outflow– The statement shows how changes in balance sheet and income accounts affect

cash and cash equivalents, and breaks the analysis down to operating, investing, and financing activities

|19

From Business Planning to Financial Modelling and Valuation

1. Introduction:f. Financial Model as part of the Business Plan (2/2)

� If the results of the Financial Model do not meet the expectations of the shareholders� Review all the drivers to see how to improve the value creation

dynamics

� See if you can change the assumptions of the BP through an alternative strategy (and an alternative management team if necessary)

� Do not invest in the company or in the project!!!

|20

From Business Planning to Financial Modelling and Valuation

1. Introduction:g. Elaborating the plan = An iterative process (1/2)

• Permanent discussions between the CFO and the other managers– What happens from the financial point of view when we want to

change some assumptions?

– Why is it interesting or impossible from the financial point of view to make other assumptions / strategy?

• Frequent discussions between the management and the shareholders

• Follow-up of an acquisition or of a restructuring process

• Negotiation tool for the company and its bankers

• Essential tool under a bankruptcy context

• Need to be a dynamic and continuous exercise

|21

From Business Planning to Financial Modelling and Valuation

1. Introduction:g. Elaborating the plan = An iterative process (2/2)

Define the fundamental

business questions

within a specific scope

of analysis

Identify the outputs

required from the model

to help to answer the

questions

Identify the key inputs

variables that determine

the outputs

Describe how the

variables will behave

over time

Develop the logical

arguments that explain

how the outputs are

derived from the inputs

Build spreadsheet model

in Excel

Enter data assumptions

Test alternative

scenarios

and sensitivities of the

outputs

Valuation based on

various methodologies

Editing the

memorandum

explaining your work

and your conclusions

Revise outputs

in the light of data

availability

Data collection

Try alternative

data if

necessary

Analysis of the value

implied by

alternative

scenarios

Next steps: implemen-tation andcontrol the business strategy

|22

From Business Planning to Financial Modelling and Valuation

2. Business Planning

|23

From Business Planning to Financial Modelling and Valuation

2. Business Planning:a. Source of information (1/2)

� Public sources of information about the business landscape as a starting point:� Industry studies (cf. Books, investment analysts, market research, ...)

� Company public information (cf. Annual reports, SEC filings, websites, bonds memorandum, IPO memorandum, promotional material, company histories, …)

� Business press: General newspapers (e.g. Wall Street Journal, Financial Times, ...), specialized industry trade journals, …

� Online services (e.g. Standards and Poor’s, Bloomberg, Reuters, JCF Group / Factset, Bureau van Dijk / Amadeus, Compustat, ...)

� Government sources (cf. Legal or tax documents, releases from antitrust or regulatory bodies)

� Trade associations, industry and company directories

|24

From Business Planning to Financial Modelling and Valuation

2. Business Planning:a. Source of information (2/3)

• A direct access to the company’s management is key:– Challenge preliminary conclusions about the business landscape

made on the basis of public information (bi-directional exercise)

– Further identification of business drivers and assumptions

• If a direct access to the company’s management is not possible, indirect contacts may be useful– Investment bankers

– Strategic consultants

– Accountants

– Lawyers

• Be careful with Non-Disclosure Agreements (NDA)

– Insurance brokers

– Competitors

– Suppliers

– Customers

|25

From Business Planning to Financial Modelling and Valuation

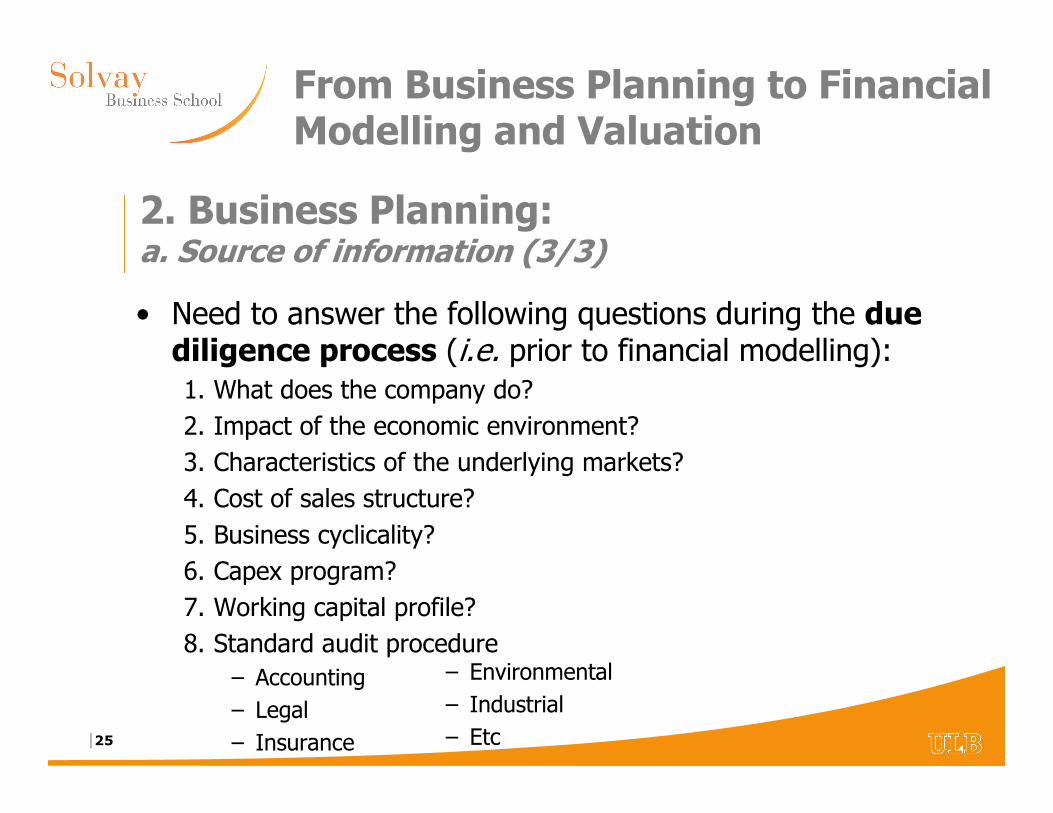

2. Business Planning:a. Source of information (3/3)

• Need to answer the following questions during the due diligence process (i.e. prior to financial modelling):1. What does the company do?

2. Impact of the economic environment?

3. Characteristics of the underlying markets?

4. Cost of sales structure?

5. Business cyclicality?

6. Capex program?

7. Working capital profile?

8. Standard audit procedure

– Accounting

– Legal

– Insurance

– Environmental

– Industrial

– Etc

|26

From Business Planning to Financial Modelling and Valuation

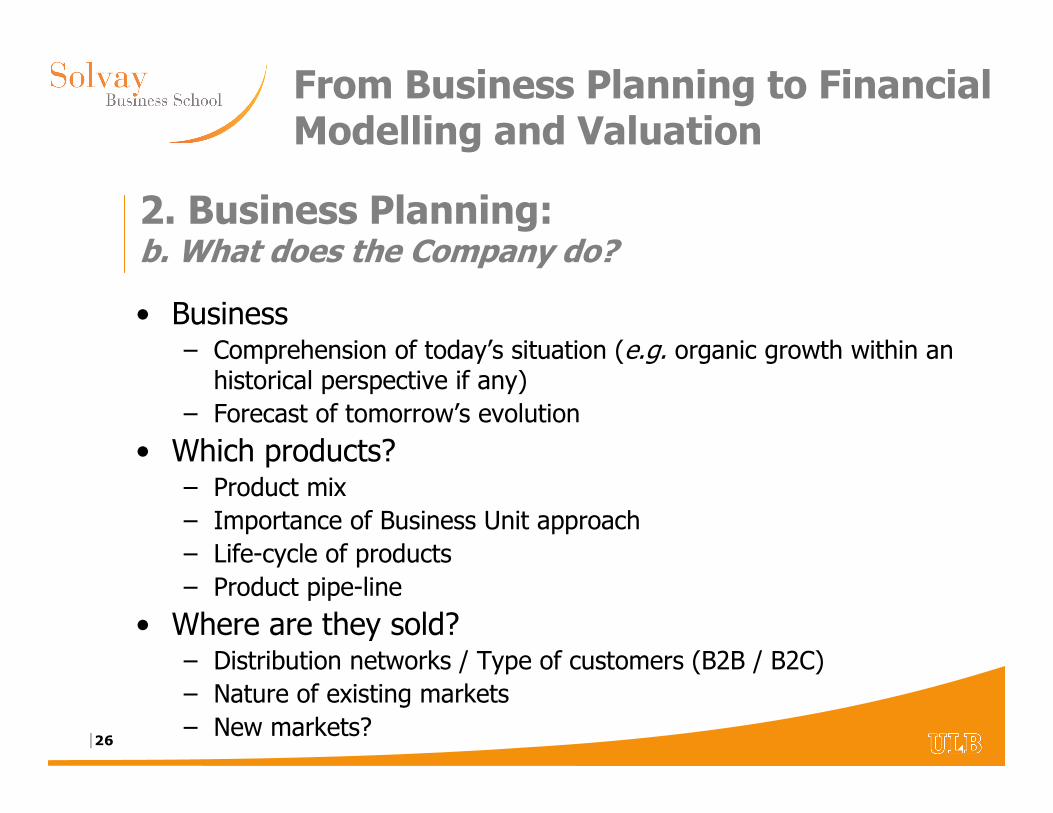

2. Business Planning:b. What does the Company do?

• Business– Comprehension of today’s situation (e.g. organic growth within an

historical perspective if any)

– Forecast of tomorrow’s evolution

• Which products?– Product mix

– Importance of Business Unit approach

– Life-cycle of products

– Product pipe-line

• Where are they sold?– Distribution networks / Type of customers (B2B / B2C)

– Nature of existing markets

– New markets?

|27

From Business Planning to Financial Modelling and Valuation

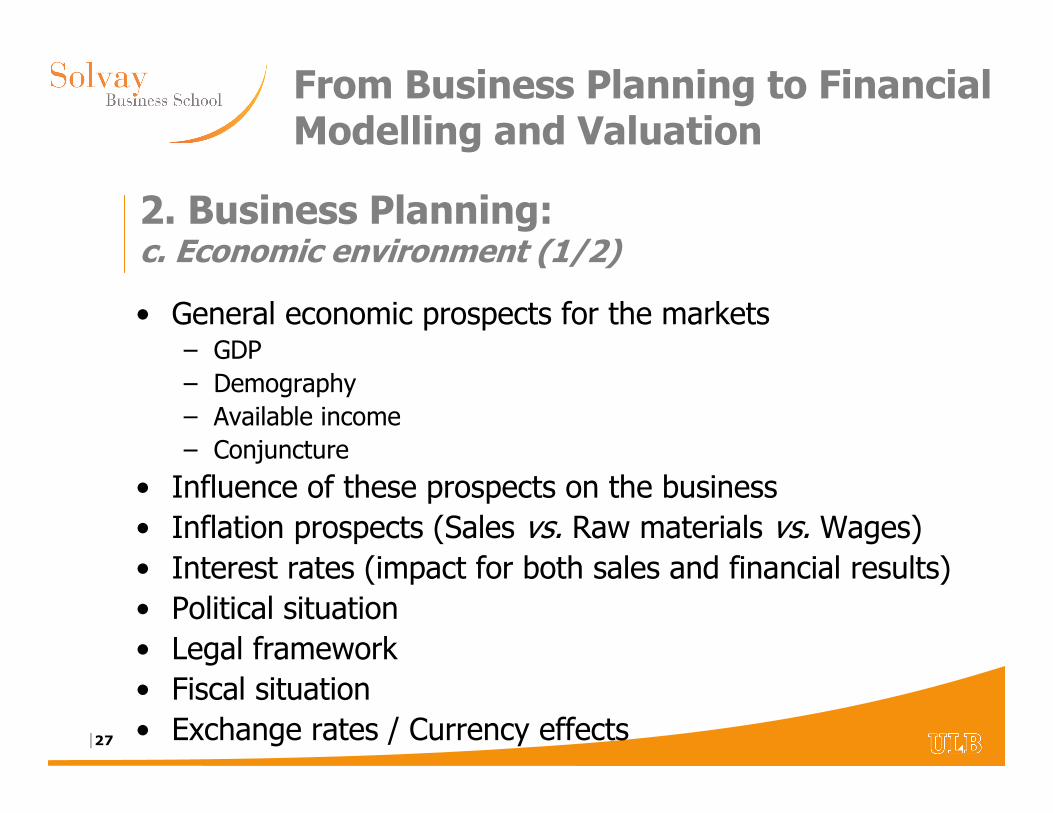

2. Business Planning:c. Economic environment (1/2)

• General economic prospects for the markets– GDP

– Demography

– Available income

– Conjuncture

• Influence of these prospects on the business

• Inflation prospects (Sales vs. Raw materials vs. Wages)

• Interest rates (impact for both sales and financial results)

• Political situation

• Legal framework

• Fiscal situation

• Exchange rates / Currency effects

|28

From Business Planning to Financial Modelling and Valuation

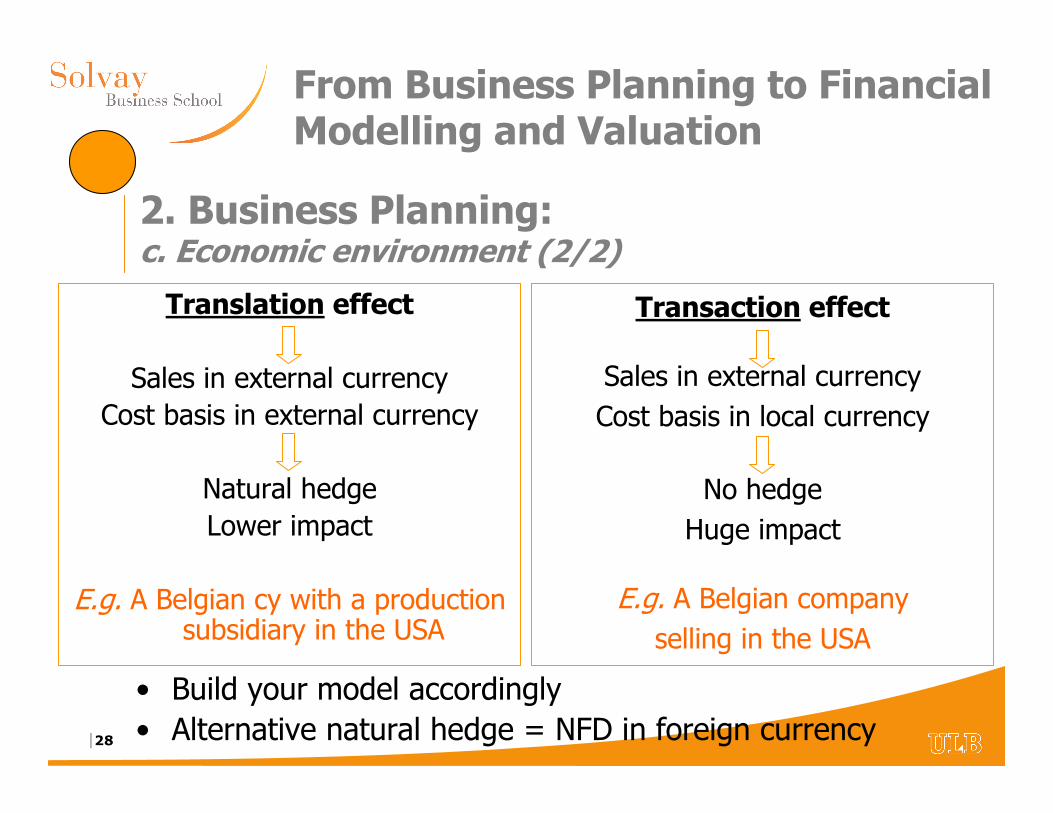

2. Business Planning:c. Economic environment (2/2)

Translation effect

Sales in external currency

Cost basis in external currency

Natural hedge

Lower impact

E.g. A Belgian cy with a production subsidiary in the USA

Transaction effect

Sales in external currency

Cost basis in local currency

No hedge

Huge impact

E.g. A Belgian company

selling in the USA

• Build your model accordingly

• Alternative natural hedge = NFD in foreign currency

|29

From Business Planning to Financial Modelling and Valuation

2. Business Planning:d. Underlying markets (1/2)

• Size of the markets– Today and in the future

– Historic and prospective evolution of prices and volumes

• Major customers (relative size)

• Major suppliers (relative size)

• Why and how are the markets changing?– Taste of the customers

– Innovative products and new technologies

• Segmentation of the markets

• Use of market studies (internal and / or external)

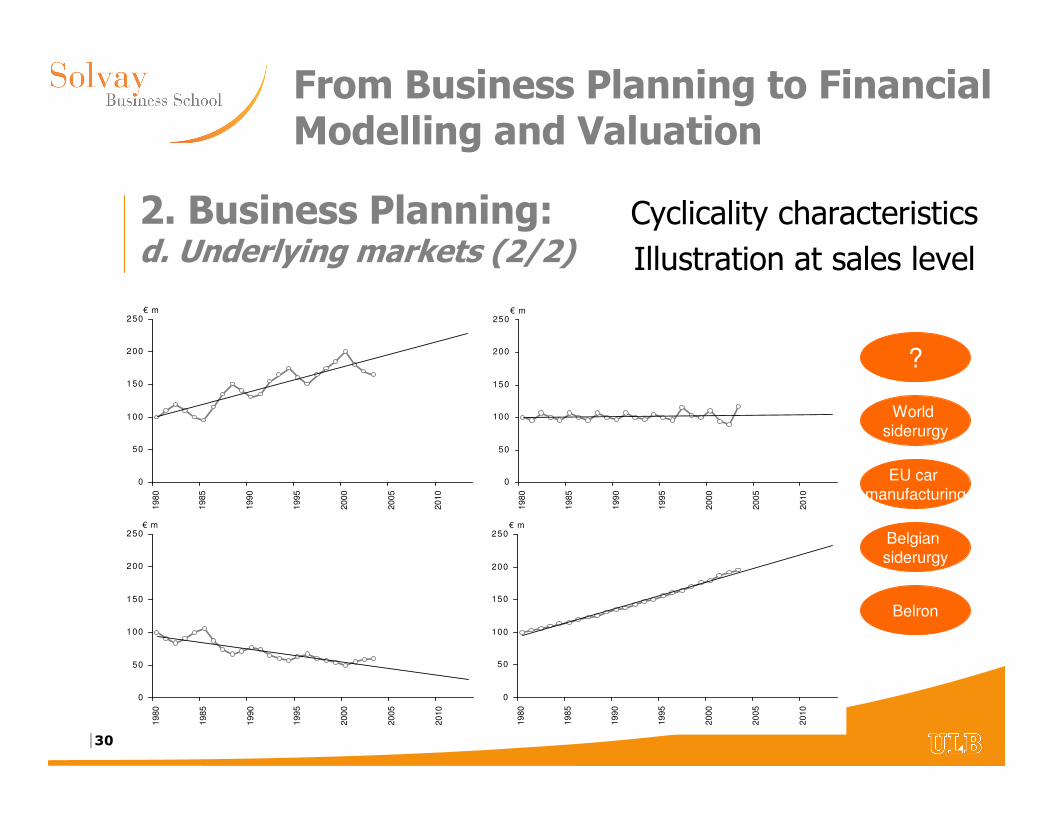

• Cyclicality characteristics

|30

From Business Planning to Financial Modelling and Valuation

2. Business Planning:d. Underlying markets (2/2)

0

50

100

150

200

250

1980

1985

1990

1995

2000

2005

2010

€ m

0

50

100

150

200

250

19

80

19

85

19

90

19

95

20

00

20

05

20

10

€ m

0

50

100

150

200

250

1980

1985

1990

1995

2000

2005

2010

€ m

0

50

100

150

200

250

1980

1985

1990

1995

2000

2005

2010

€ m

Cyclicality characteristics

Illustration at sales level

World

siderurgy

EU car

manufacturing

Belgian

siderurgy

Belron

?

|31

From Business Planning to Financial Modelling and Valuation

2. Business Planning:e. Competitors (1/2)

• Who are they?• Where are they?• What is their market share (dynamic perspective)?• New entrants?

– Barriers to entry– Backward or downward integration dynamics– Sister industries

• Why should the customers go to competitors?• Present and future overcapacity?• Comparison of the products

– Price– Quality– Product range

|32

From Business Planning to Financial Modelling and Valuation

2. Business Planning:e. Competitors (2/2)

• What are the projects of the competitors?– Innovation– Price strategy– Financial situation

• Benchmarking is key– Operational – Financial

|33

From Business Planning to Financial Modelling and Valuation

2. Business Planning:f. Cost structure and sales price (1/2)

• Nature of the operating costs?– Fixed costs vs. variable costs– Sensitivity to external elements (currencies, raw materials, …)

– Translation effect vs. transaction effect

• What are the prices asked by the suppliers?– Today and tomorrow

– Can we buy cheaper or better?

• Ability to pass price increase through to clients?

• How fast will the salaries increase?

• Can we use new technologies?– To improve the productivity and to reduce the costs

– To improve the quality

|34

From Business Planning to Financial Modelling and Valuation

2. Business Planning:f. Cost structure and sales price (2/2)

(Q2 – Q1) / Q1(P2 – P1) / P1

• At what price can we sell our products ?– Costs + margin

– Volume effect on cost base

– Price elasticity of the volume sold �

– Reactions of the competitors

– Consequences on the margin

– Which product: base or add-ons?

|35

From Business Planning to Financial Modelling and Valuation

2. Business Planning:g. Capex requirements (1/2)

• Which new fixed assets do we need / do you want?– Current status of the asset base

– Production facility requirements (size, layout, capacity, location)

– Amount / Timing / Flexibility

– Cost of opportunity

• Capex nature– Equipment requirements

– Maintenance capex vs. Expansion capex vs. Acquisitions / Disposals– Tangible vs. Intangible (IT)

• Research & Development?

• Commercial Investments– Advertising

– Start-up losses

|36

From Business Planning to Financial Modelling and Valuation

2. Business Planning:g. Capex requirements (2/2)

• Alternative scenarios– Financial or operational leasing

– Outsourcing

– Acquisitions

• Consequences on the P&L– Depreciation duration vs. life-time

– Tax considerations

|37

From Business Planning to Financial Modelling and Valuation

2. Business Planning:h. Working capital requirements (1/3)

• Inventory requirements– Raw materials inventory

– Finished goods inventory

– Warehouse space requirements

– Supply chain requirements

• Specific to each industry– Manufacturing >< Retail

• How can we reduce the inventories?– Logistic optimization

– Subcontracting

• Are we able to let the customers pay quicker?

• Can we pay the suppliers later?

|38

From Business Planning to Financial Modelling and Valuation

2. Business Planning:h. Working capital requirements (2/3)

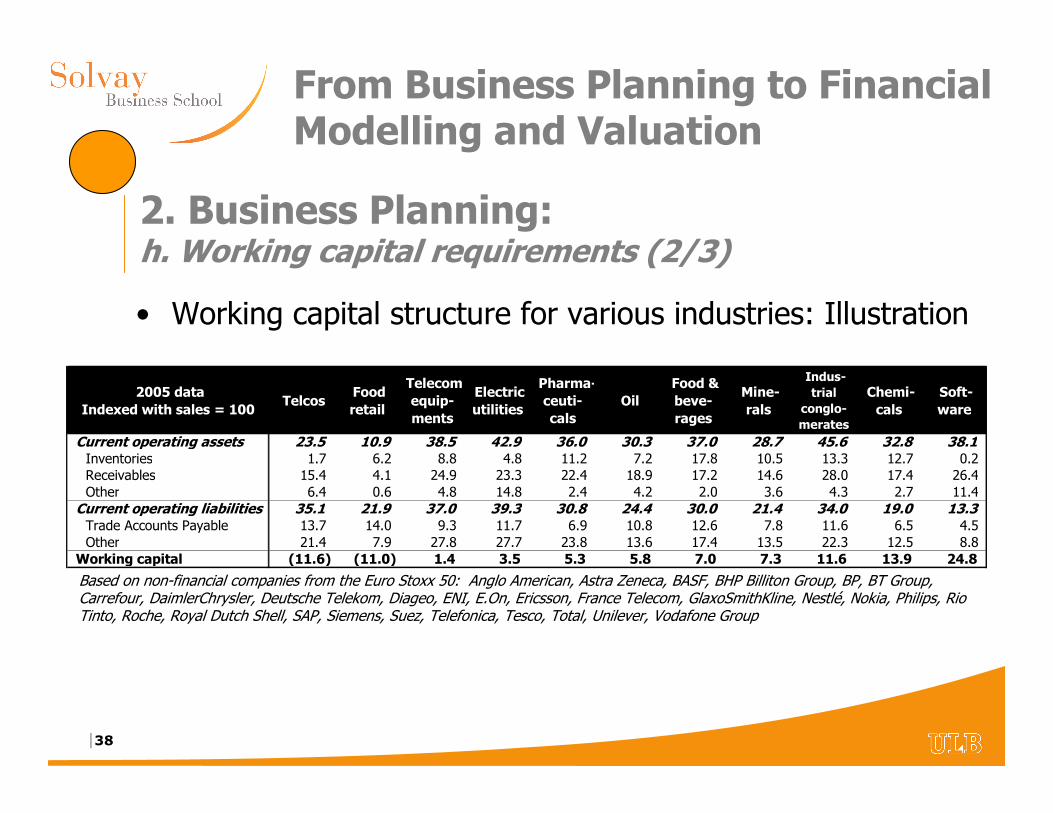

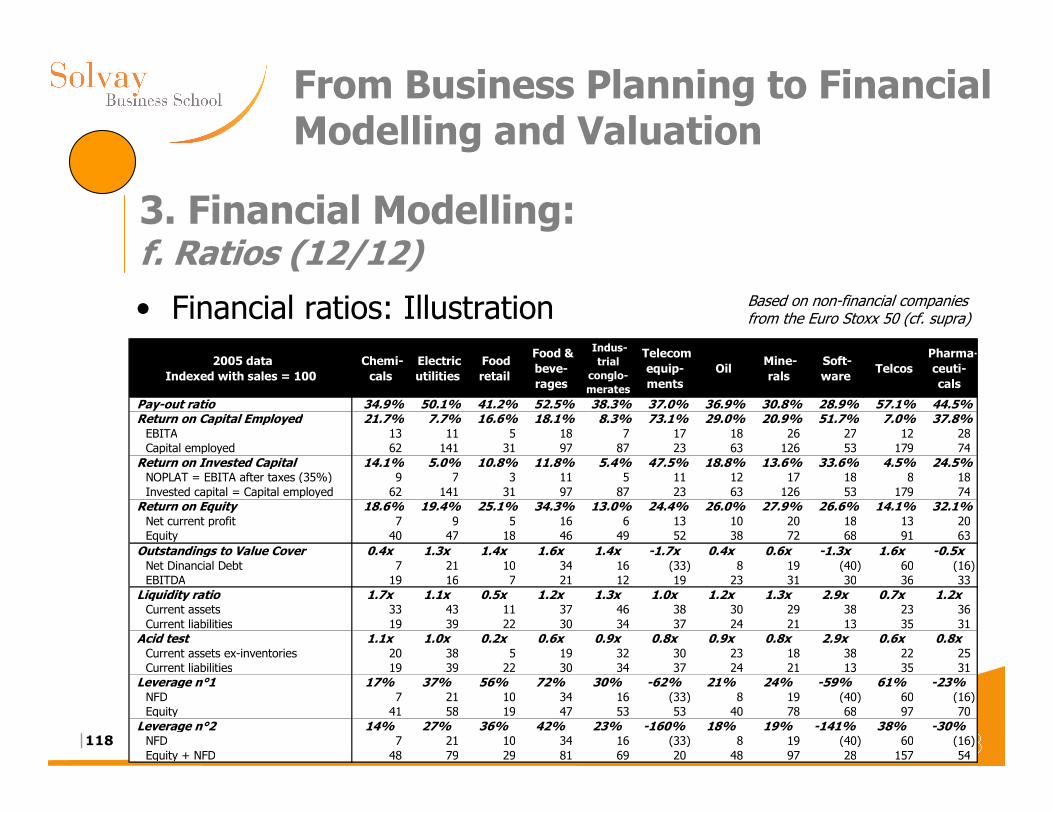

• Working capital structure for various industries: Illustration

Based on non-financial companies from the Euro Stoxx 50: Anglo American, Astra Zeneca, BASF, BHP Billiton Group, BP, BT Group, Carrefour, DaimlerChrysler, Deutsche Telekom, Diageo, ENI, E.On, Ericsson, France Telecom, GlaxoSmithKline, Nestlé, Nokia, Philips, Rio Tinto, Roche, Royal Dutch Shell, SAP, Siemens, Suez, Telefonica, Tesco, Total, Unilever, Vodafone Group

2005 data Indexed with sales = 100

Telcos Food retail

Telecom equip-ments

Electric utilities

Pharma-ceuti-cals

Oil Food & beve-rages

Mine-rals

Indus-trial

conglo-merates

Chemi-cals

Soft-ware

Current operating assets 23.5 10.9 38.5 42.9 36.0 30.3 37.0 28.7 45.6 32.8 38.1 Inventories 1.7 6.2 8.8 4.8 11.2 7.2 17.8 10.5 13.3 12.7 0.2 Receivables 15.4 4.1 24.9 23.3 22.4 18.9 17.2 14.6 28.0 17.4 26.4 Other 6.4 0.6 4.8 14.8 2.4 4.2 2.0 3.6 4.3 2.7 11.4

Current operating liabilities 35.1 21.9 37.0 39.3 30.8 24.4 30.0 21.4 34.0 19.0 13.3 Trade Accounts Payable 13.7 14.0 9.3 11.7 6.9 10.8 12.6 7.8 11.6 6.5 4.5 Other 21.4 7.9 27.8 27.7 23.8 13.6 17.4 13.5 22.3 12.5 8.8

Working capital (11.6) (11.0) 1.4 3.5 5.3 5.8 7.0 7.3 11.6 13.9 24.8

|39

From Business Planning to Financial Modelling and Valuation

2. Business Planning:h. Working capital requirements (3/3)

• New techniques to reduce the working capital– Just-in time

– Zero inventories

– Factoring

|40

From Business Planning to Financial Modelling and Valuation

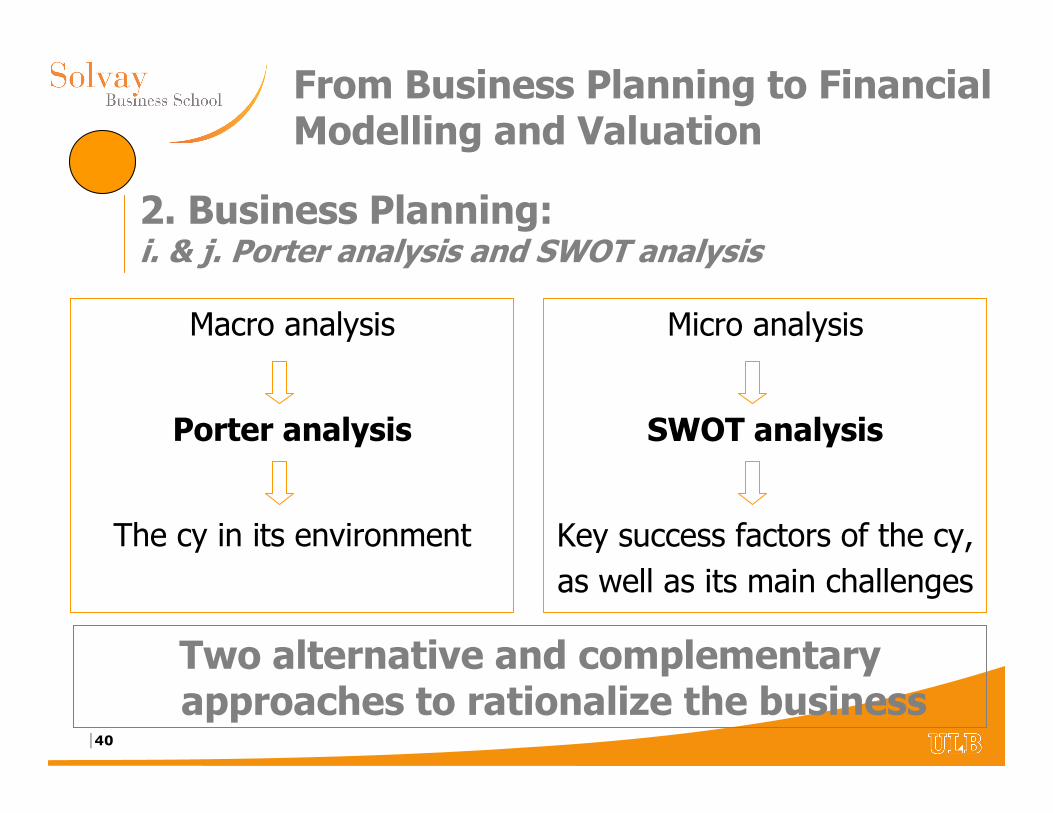

2. Business Planning:i. & j. Porter analysis and SWOT analysis

Macro analysis

Porter analysis

The cy in its environment

Micro analysis

SWOT analysis

Key success factors of the cy,

as well as its main challenges

Two alternative and complementary approaches to rationalize the business

|41

From Business Planning to Financial Modelling and Valuation

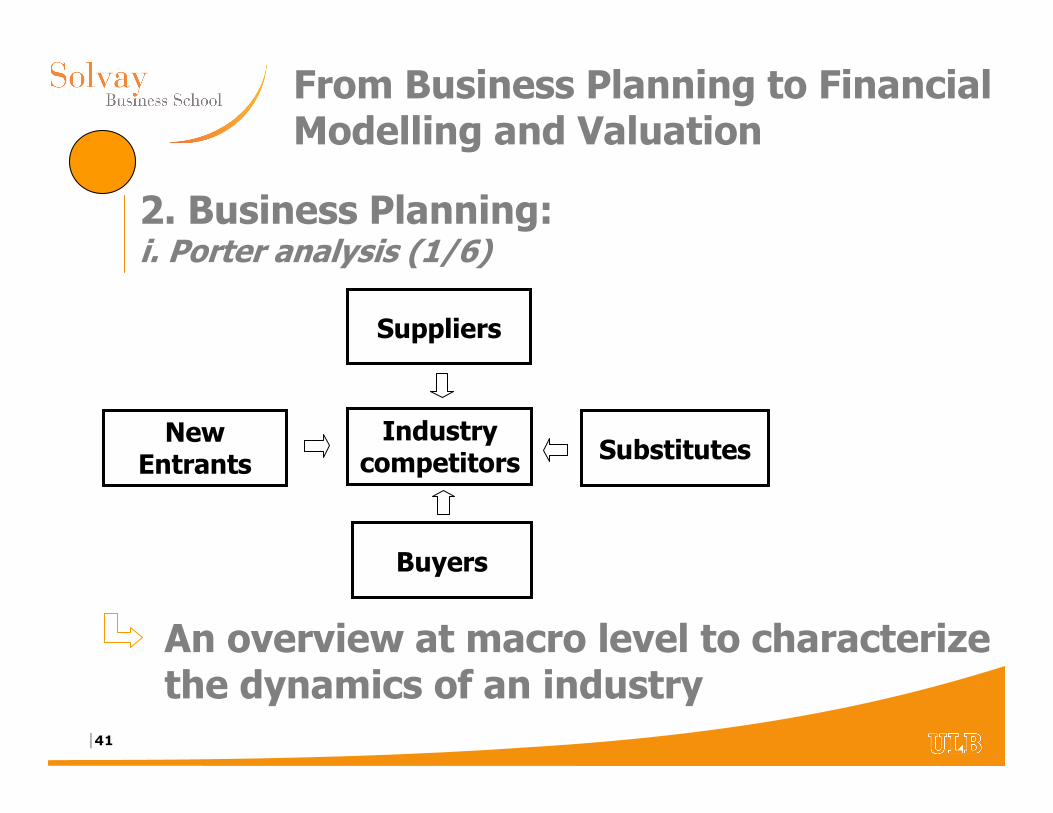

2. Business Planning:i. Porter analysis (1/6)

Suppliers

Industry competitors

Buyers

SubstitutesNew

Entrants

An overview at macro level to characterize the dynamics of an industry

|42

From Business Planning to Financial Modelling and Valuation

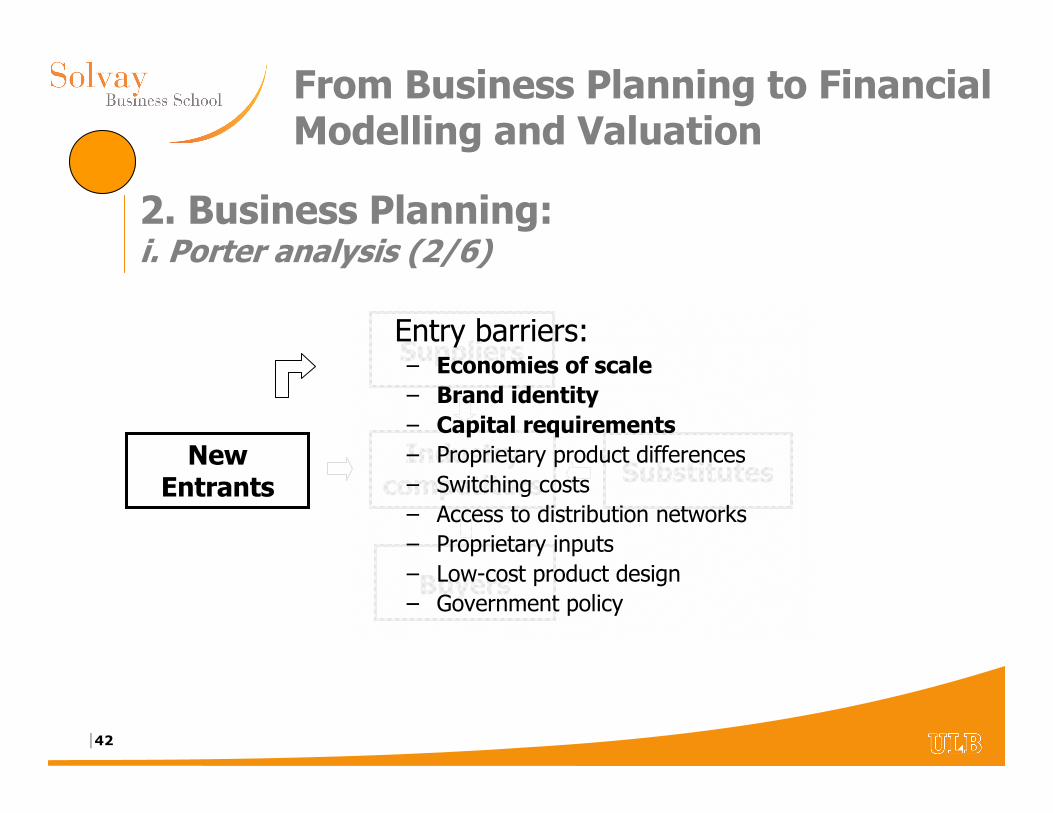

2. Business Planning:i. Porter analysis (2/6)

Suppliers

Industry competitors

Buyers

Substitutes

Entry barriers:– Economies of scale– Brand identity– Capital requirements– Proprietary product differences

– Switching costs

– Access to distribution networks

– Proprietary inputs

– Low-cost product design

– Government policy

New Entrants

|43

From Business Planning to Financial Modelling and Valuation

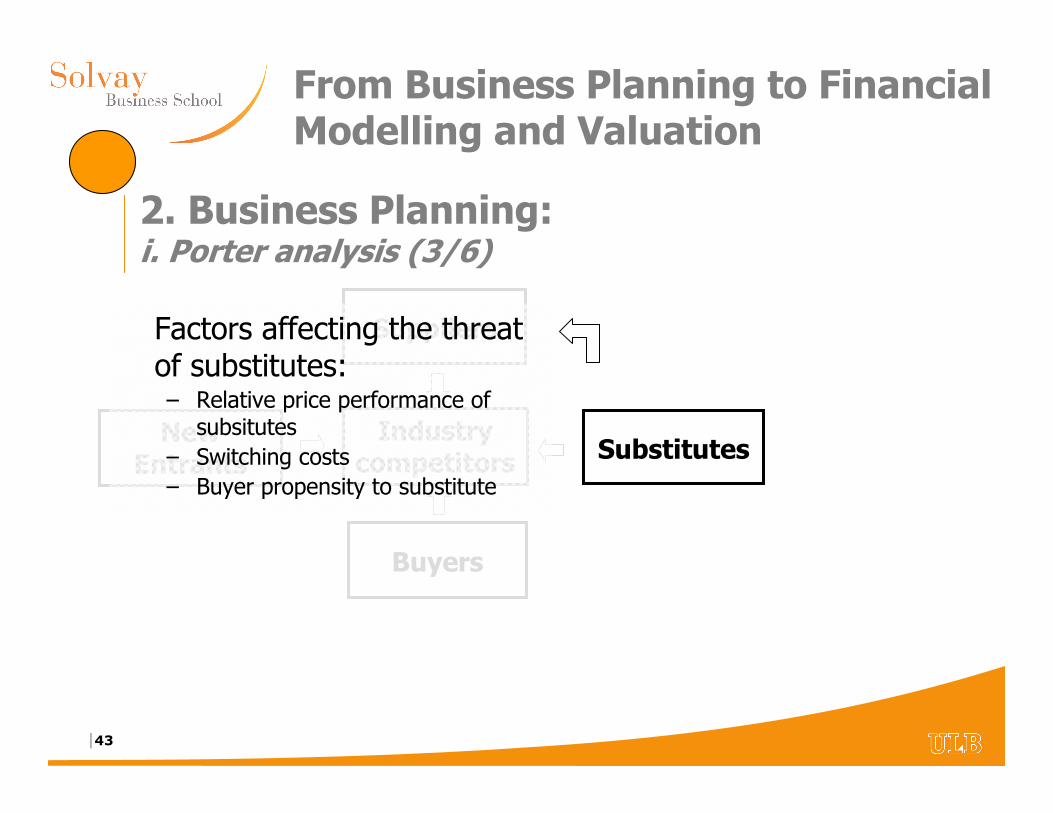

2. Business Planning:i. Porter analysis (3/6)

Suppliers

Industry competitors

Buyers

New Entrants

Factors affecting the threat of substitutes:– Relative price performance of

subsitutes

– Switching costs

– Buyer propensity to substitute

Substitutes

|44

From Business Planning to Financial Modelling and Valuation

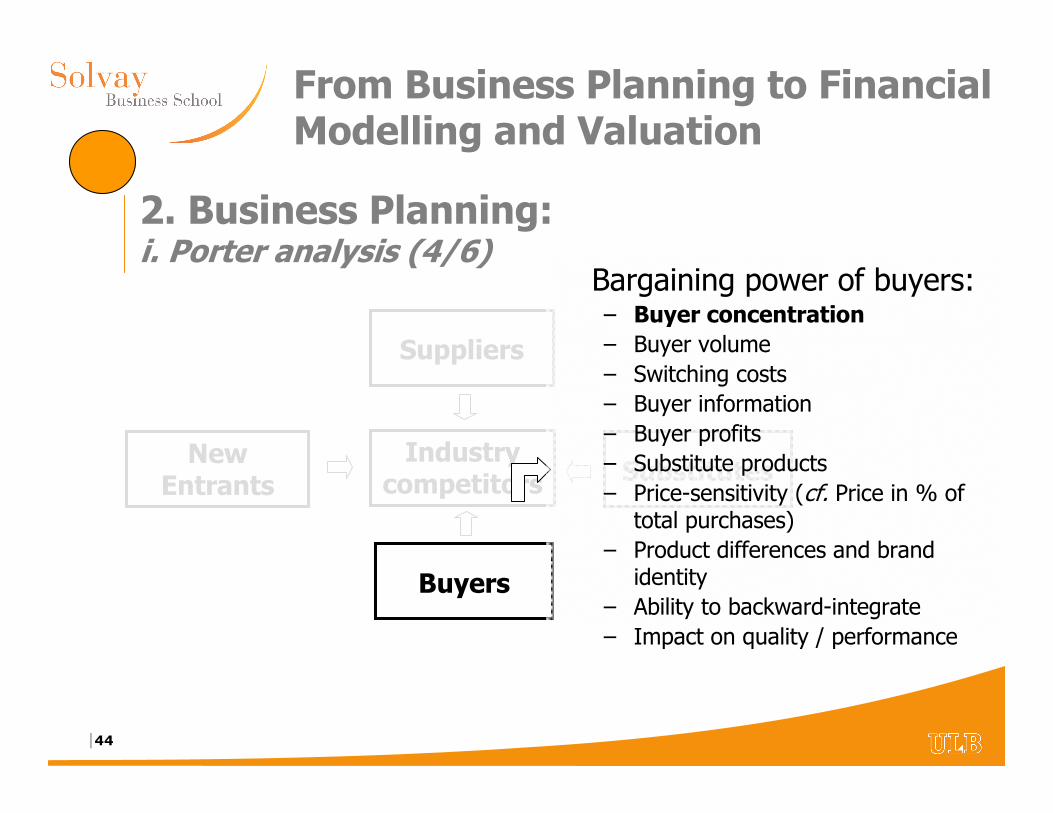

2. Business Planning:i. Porter analysis (4/6)

Suppliers

Industry competitors

Buyers

SubstitutesNew

Entrants

Bargaining power of buyers:– Buyer concentration– Buyer volume

– Switching costs

– Buyer information

– Buyer profits

– Substitute products

– Price-sensitivity (cf. Price in % of total purchases)

– Product differences and brand identity

– Ability to backward-integrate

– Impact on quality / performance

|45

From Business Planning to Financial Modelling and Valuation

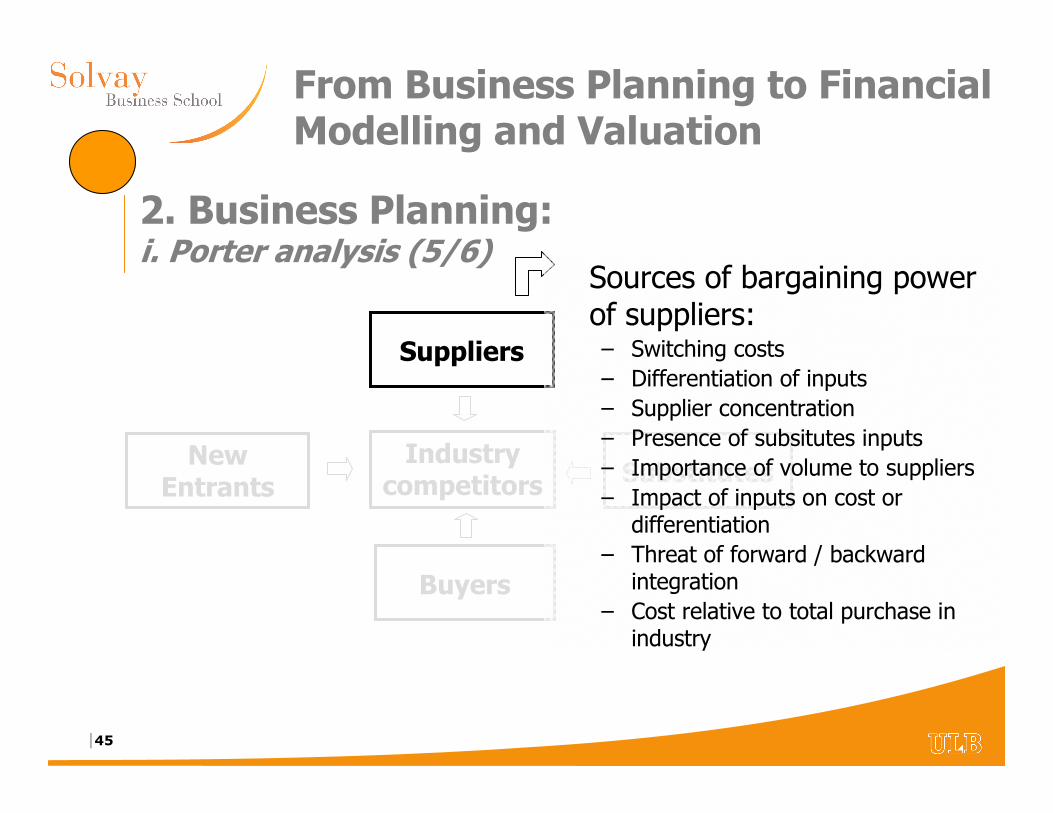

2. Business Planning:i. Porter analysis (5/6)

Suppliers

Industry competitors

Buyers

SubstitutesNew

Entrants

Sources of bargaining power of suppliers:– Switching costs

– Differentiation of inputs

– Supplier concentration

– Presence of subsitutes inputs

– Importance of volume to suppliers

– Impact of inputs on cost ordifferentiation

– Threat of forward / backwardintegration

– Cost relative to total purchase in industry

|46

From Business Planning to Financial Modelling and Valuation

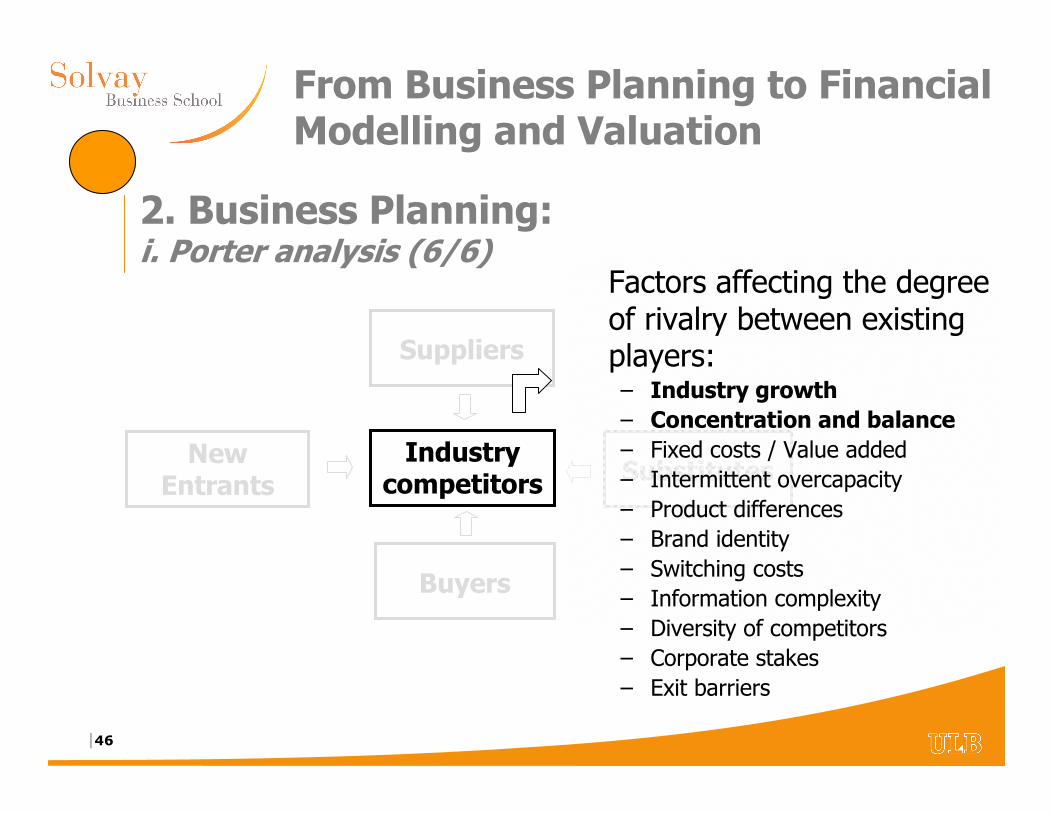

2. Business Planning:i. Porter analysis (6/6)

Suppliers

Industry competitors

Buyers

SubstitutesNew

Entrants

Factors affecting the degree of rivalry between existing players:– Industry growth– Concentration and balance– Fixed costs / Value added

– Intermittent overcapacity

– Product differences

– Brand identity

– Switching costs

– Information complexity

– Diversity of competitors

– Corporate stakes

– Exit barriers

|47

From Business Planning to Financial Modelling and Valuation

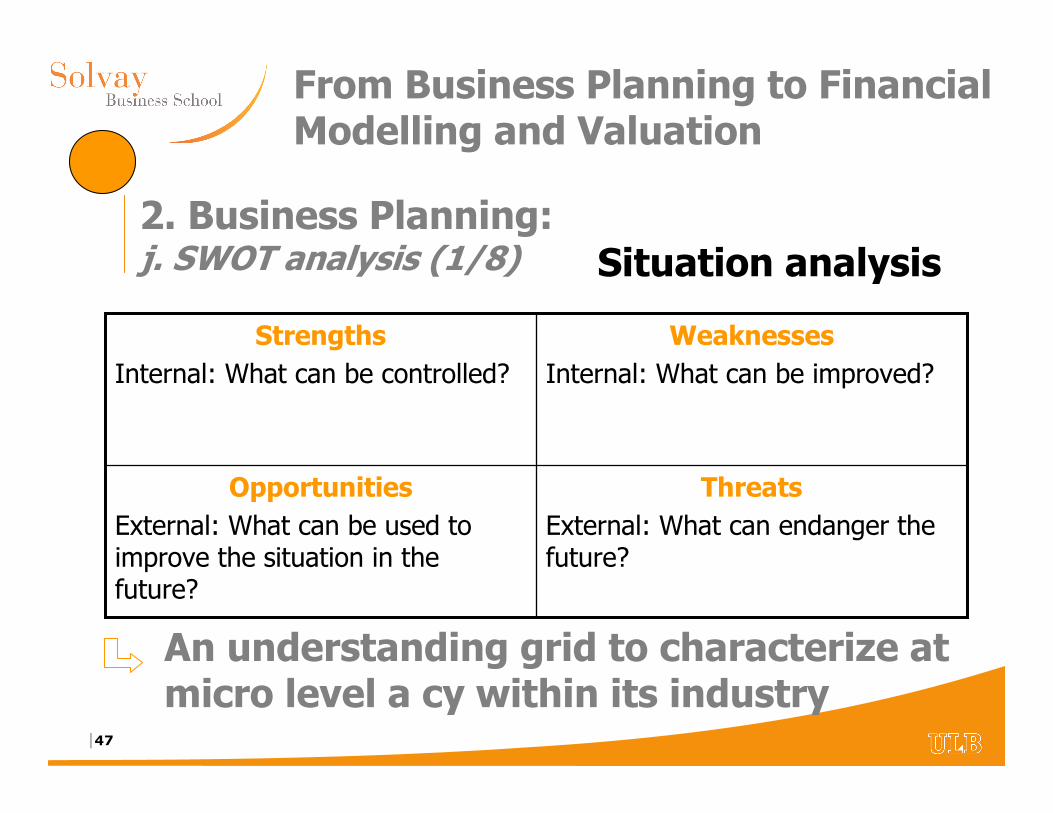

An understanding grid to characterize at micro level a cy within its industry

ThreatsExternal: What can endanger the future?

OpportunitiesExternal: What can be used to improve the situation in the future?

WeaknessesInternal: What can be improved?

StrengthsInternal: What can be controlled?

2. Business Planning:j. SWOT analysis (1/8) Situation analysis

|48

From Business Planning to Financial Modelling and Valuation

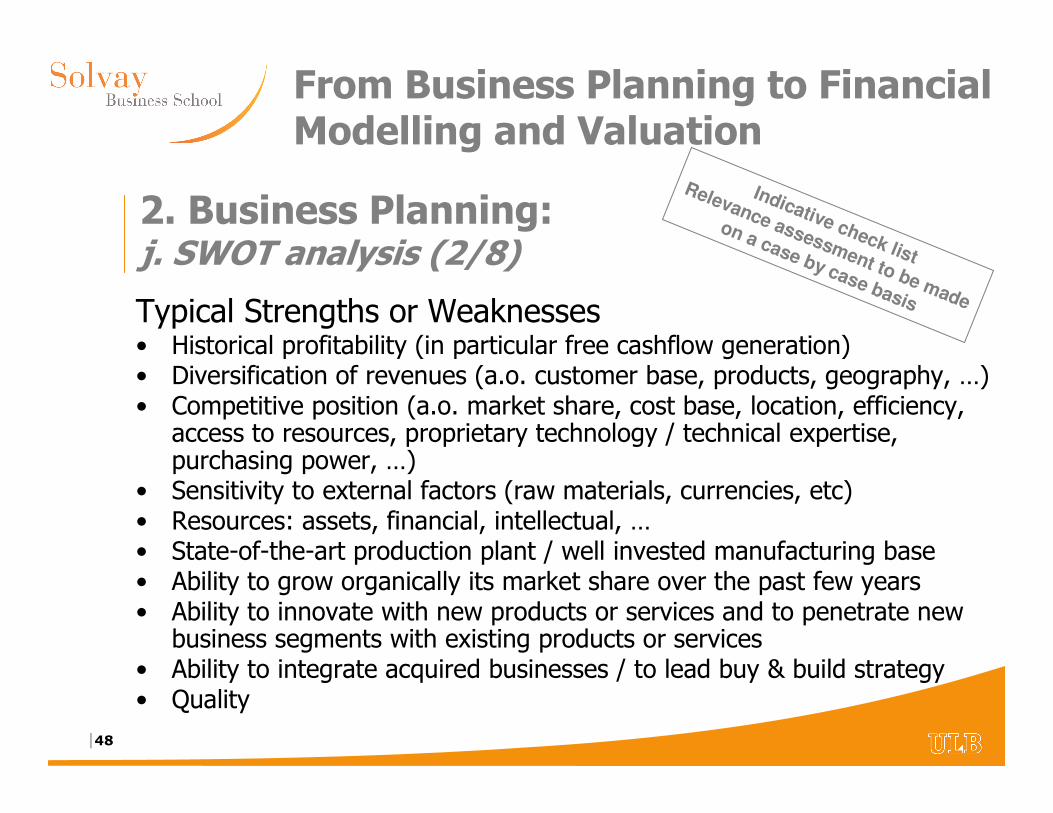

2. Business Planning:j. SWOT analysis (2/8)

Typical Strengths or Weaknesses• Historical profitability (in particular free cashflow generation)• Diversification of revenues (a.o. customer base, products, geography, …)• Competitive position (a.o. market share, cost base, location, efficiency,

access to resources, proprietary technology / technical expertise, purchasing power, …)

• Sensitivity to external factors (raw materials, currencies, etc)• Resources: assets, financial, intellectual, …• State-of-the-art production plant / well invested manufacturing base• Ability to grow organically its market share over the past few years• Ability to innovate with new products or services and to penetrate new

business segments with existing products or services• Ability to integrate acquired businesses / to lead buy & build strategy• Quality

Indicative check list

Relevance assessment to be made

on a case by case basis

|49

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (3/8)

Typical Strengths or Weaknesses (…)• Sales inflation vs. cost inflation• Price positioning (relative to the competition)

• Mix of mature and growing markets

• Staff (sales, back-office, turnover, …)

• Management team / Track record of the team

• Customer service / Delivery time (relative to the competition)

• Relationships with key industry customers

• Brand names (vs. B brands or private labels)• First mover advantage

• Capacity & planning

• Capital intensity

Indicative check list

Relevance assessment to be made

on a case by case basis

|50

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (4/8)

Typical Strengths or Weaknesses (…)• Seasonality / Weather effects / Fashion influences

• Accreditations / Qualifications / Certifications

• Corporate brand / Reputation / Image

• Ethics

• Environment

• Communication

• Corporate governance

Indicative check list

Relevance assessment to be made

on a case by case basis

|51

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (5/8)

Typical Opportunities or Threats• Political / legal / social / tax / environmental framework

• Market trends

• Demography

• Economic outlook

• Expectations of stakeholders

• Technology trends, innovation, breakthrough

• Identified efficiency / productivity improvement initiatives

• Competitors and competitive actions

• Supplier move

• Customer expectations, customer’s customer expectations

• Product pipe line (company vs. competition)

• Substitutes / Penetration of new markets

Indicative check list

Relevance assessment to be made

on a case by case basis

|52

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (6/8)

Typical Opportunities or Threats• Disposal of non-core assets

• Low Cost Countries (LCC)

• Use of unexploited capacities

• Management team (in a context of succession or expansion strategy)

• Vital contracts and partners

• Loss of key staff

• Sustaining internal capabilities

Indicative check list

Relevance assessment to be made

on a case by case basis

|53

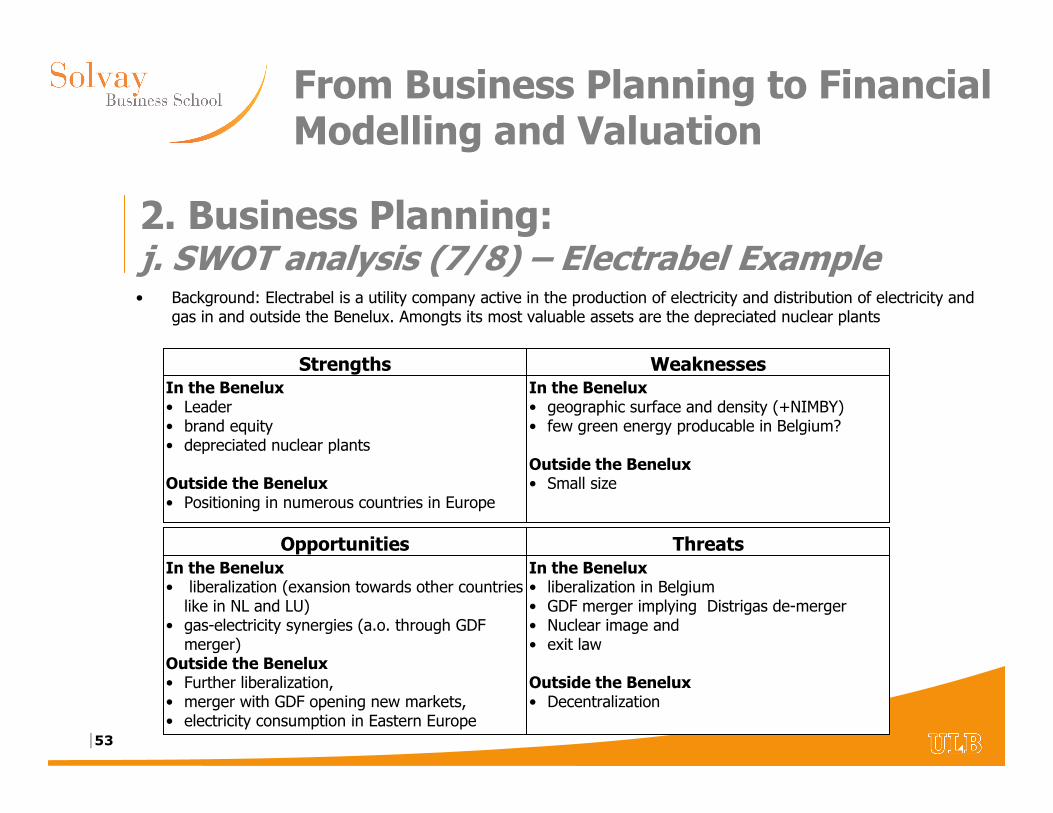

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (7/8) – Electrabel Example• Background: Electrabel is a utility company active in the production of electricity and distribution of electricity and

gas in and outside the Benelux. Amongts its most valuable assets are the depreciated nuclear plants

StrengthsIn the Benelux• Leader• brand equity• depreciated nuclear plants

Outside the Benelux• Positioning in numerous countries in Europe

OpportunitiesIn the Benelux• liberalization (exansion towards other countries

like in NL and LU)• gas-electricity synergies (a.o. through GDF

merger)Outside the Benelux• Further liberalization, • merger with GDF opening new markets,• electricity consumption in Eastern Europe

ThreatsIn the Benelux• liberalization in Belgium• GDF merger implying Distrigas de-merger• Nuclear image and • exit law

Outside the Benelux• Decentralization

WeaknessesIn the Benelux• geographic surface and density (+NIMBY)• few green energy producable in Belgium?

Outside the Benelux• Small size

|54

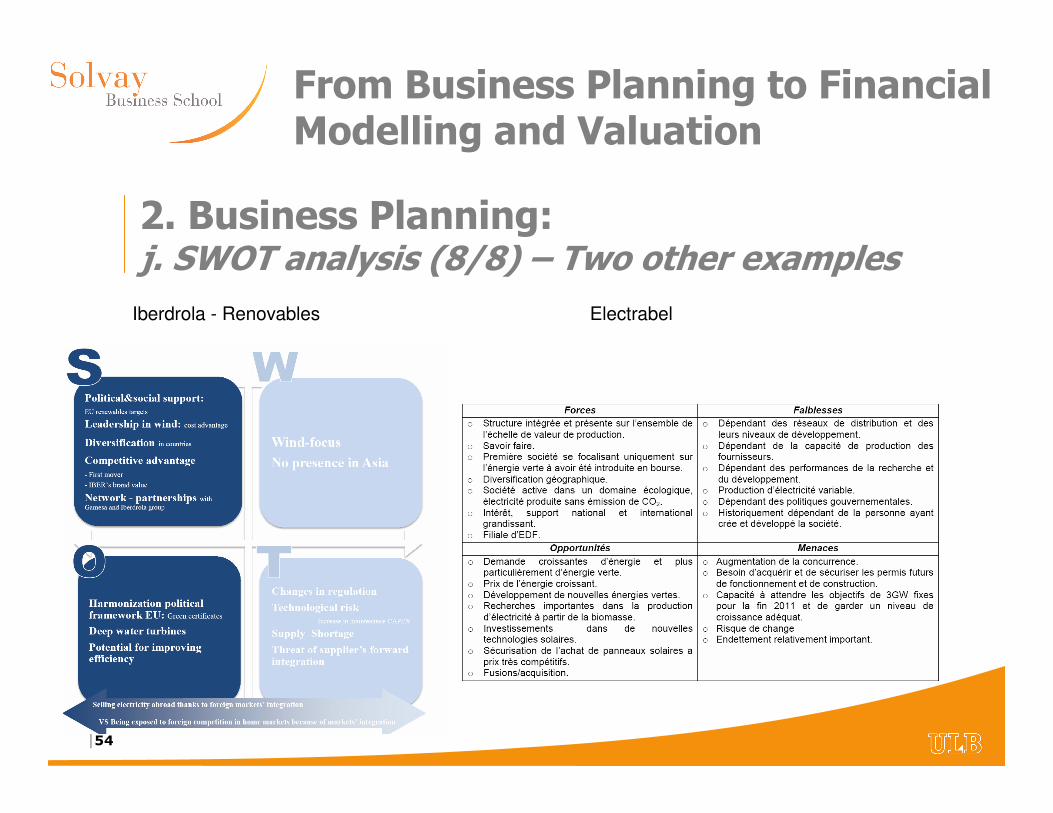

From Business Planning to Financial Modelling and Valuation

2. Business Planning:j. SWOT analysis (8/8) – Two other examples

Iberdrola - Renovables Electrabel

|55

From Business Planning to Financial Modelling and Valuation

2. Business Planning:k. Human resources

• Understand the existing organizational structure and key people

• Assign responsibilities

• Evaluate training required

• List skills required

• Prepare union issues

• Estimate compensation

• Gauge skills availability

• Consider new hiring

|56

From Business Planning to Financial Modelling and Valuation

3. Financial Modelling

|57

From Business Planning to Financial Modelling and Valuation

• Put the BP in an Excel workbook

• Advantages:– Quicker calculations

– Check that everything is OK

• Assets = Liabilities

• Cash flow Statement equation

– Easy modification of one or some assumptions (cf. sensitivity analysis)

– Data base for illustration (cf. table and graph for memorandum)

– Frequent update

• Disadvantages:– May easily become a black-box

3. Financial Modelling:a. Introduction (1/5): Excel merits

|58

From Business Planning to Financial Modelling and Valuation

• Do it yourself is always better >< Standardised template

• Make it simple (for you and for the external parties)– Regroup all the assumptions

– Use colours (assumptions in green, formulas in blue, …)

– Use various pages

– Use comments

• Avoid– Conceptual errors and links with other files

– Circular references

• Synthesis and graphic presentation– Always mention units (€ vs. € m, $, £, #, …)!

– Summary tables / Graphs

3. Financial Modelling:a. Introduction (2/5): Recommendations

|59

From Business Planning to Financial Modelling and Valuation

• Ctrl + C = Copy

• Ctrl + V = Paste

• Ctrl + P = Print

• Ctrl + Spacebar = Select a column

• Shift + Spacebar = Select a row

• Ctrl + A = Select a whole table, then the whole sheet

3. Financial Modelling:a. Introduction (3/5): Useful excel shortcuts

Will be further analyzed during Excel Training

|60

From Business Planning to Financial Modelling and Valuation

• ABS() = Returns the absolute value of a number

• AVERAGE() or MEAN() = Returns the arithmetic average or the mean of as series of arguments

• ISERROR()

• CONCATENATE() = Joins a number of strings (text) variables into a single text variable

• IF() = Returns one value if a specified condition is true and another value if the condition is false

• MAX() = Provides the largest value amongst a set of values

• MIN() = Provides the smallest value amongst a set of values

• ROUND() = Rounds a number to the specified number of digit

• VLOOKUP() = Searches for a value in the left-most column of a table and then returns a value from the same row in a column from within the table specified by the user

3. Financial Modelling:a. Introduction (4/5): Useful excel functions

Will be further analyzed during Excel Training

|61

From Business Planning to Financial Modelling and Valuation

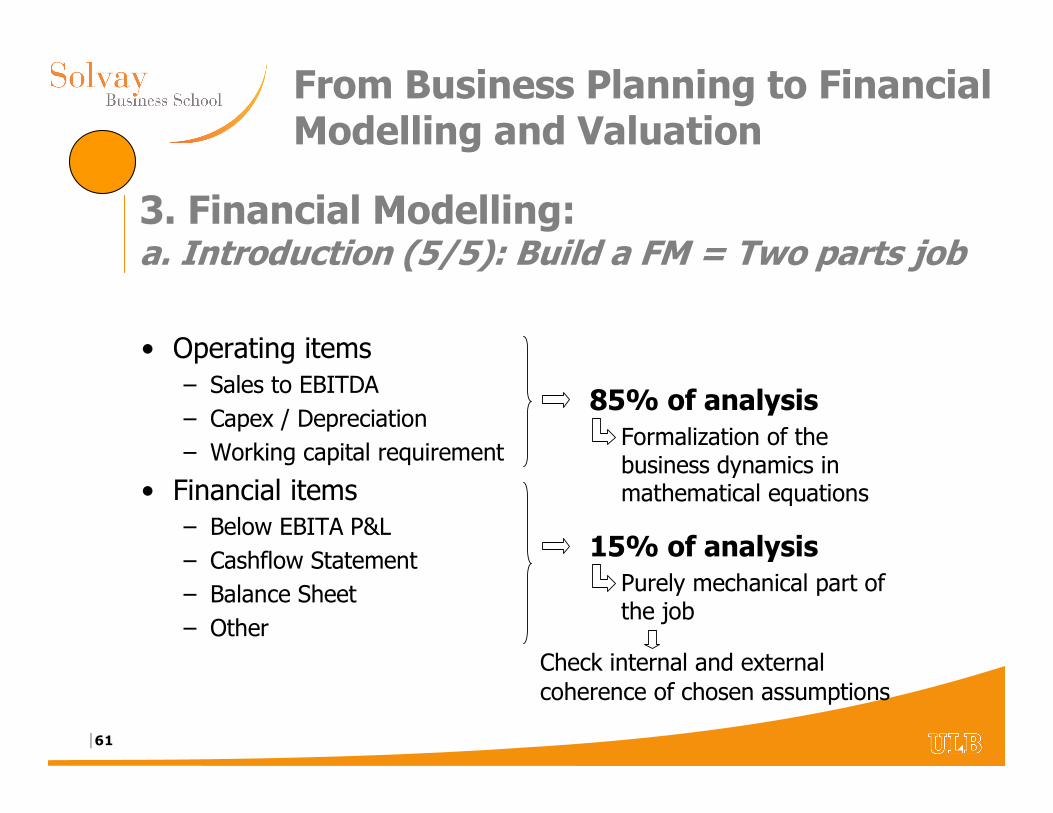

• Operating items– Sales to EBITDA

– Capex / Depreciation

– Working capital requirement

• Financial items– Below EBITA P&L

– Cashflow Statement

– Balance Sheet

– Other

85% of analysisFormalization of the business dynamics in mathematical equations

15% of analysisPurely mechanical part of the job

Check internal and external coherence of chosen assumptions

3. Financial Modelling:a. Introduction (5/5): Build a FM = Two parts job

|62

From Business Planning to Financial Modelling and Valuation

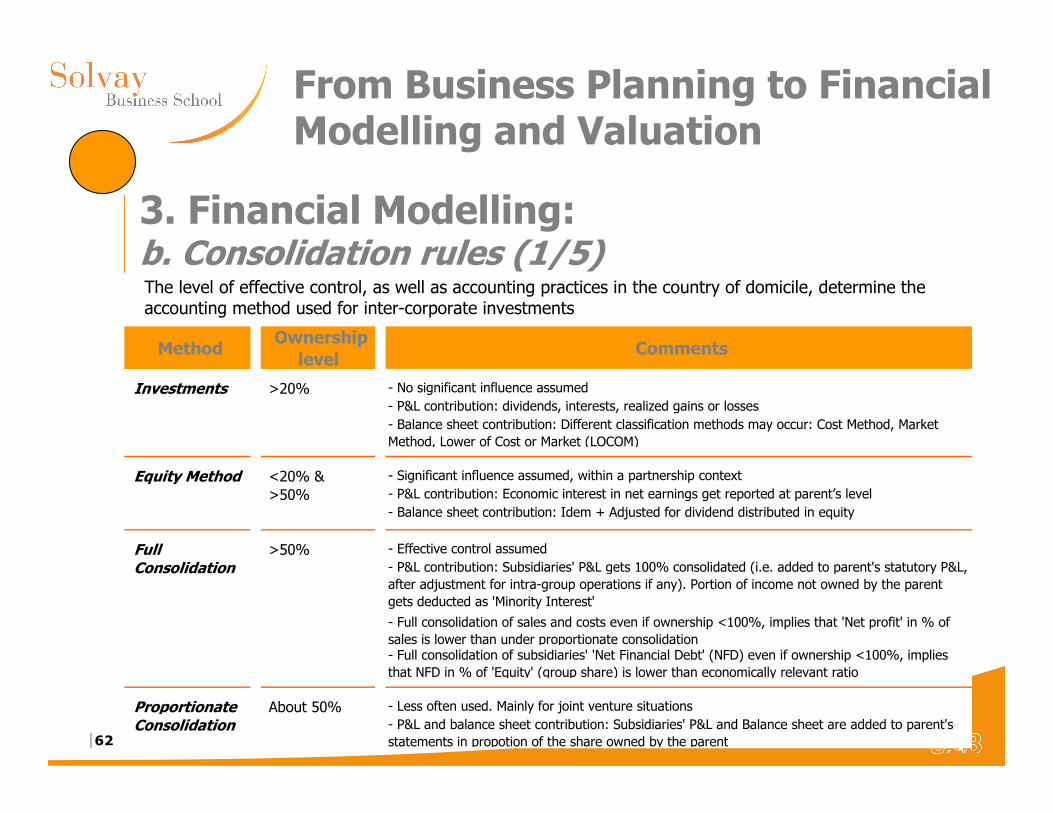

3. Financial Modelling:b. Consolidation rules (1/5)The level of effective control, as well as accounting practices in the country of domicile, determine the accounting method used for inter-corporate investments

Method Ownership

level Comments

Investments >20% - No significant influence assumed

- P&L contribution: dividends, interests, realized gains or losses

- Balance sheet contribution: Different classification methods may occur: Cost Method, Market

Method, Lower of Cost or Market (LOCOM)

Equity Method <20% & - Significant influence assumed, within a partnership context

>50% - P&L contribution: Economic interest in net earnings get reported at parent’s level

- Balance sheet contribution: Idem + Adjusted for dividend distributed in equity

Full >50% - Effective control assumed

Consolidation - P&L contribution: Subsidiaries' P&L gets 100% consolidated (i.e. added to parent's statutory P&L,

after adjustment for intra-group operations if any). Portion of income not owned by the parent

gets deducted as 'Minority Interest'

- Full consolidation of sales and costs even if ownership <100%, implies that 'Net profit' in % of

sales is lower than under proportionate consolidation- Full consolidation of subsidiaries' 'Net Financial Debt' (NFD) even if ownership <100%, implies

that NFD in % of 'Equity' (group share) is lower than economically relevant ratio

Proportionate About 50% - Less often used. Mainly for joint venture situations

Consolidation - P&L and balance sheet contribution: Subsidiaries' P&L and Balance sheet are added to parent's

statements in propotion of the share owned by the parent

|63

From Business Planning to Financial Modelling and Valuation

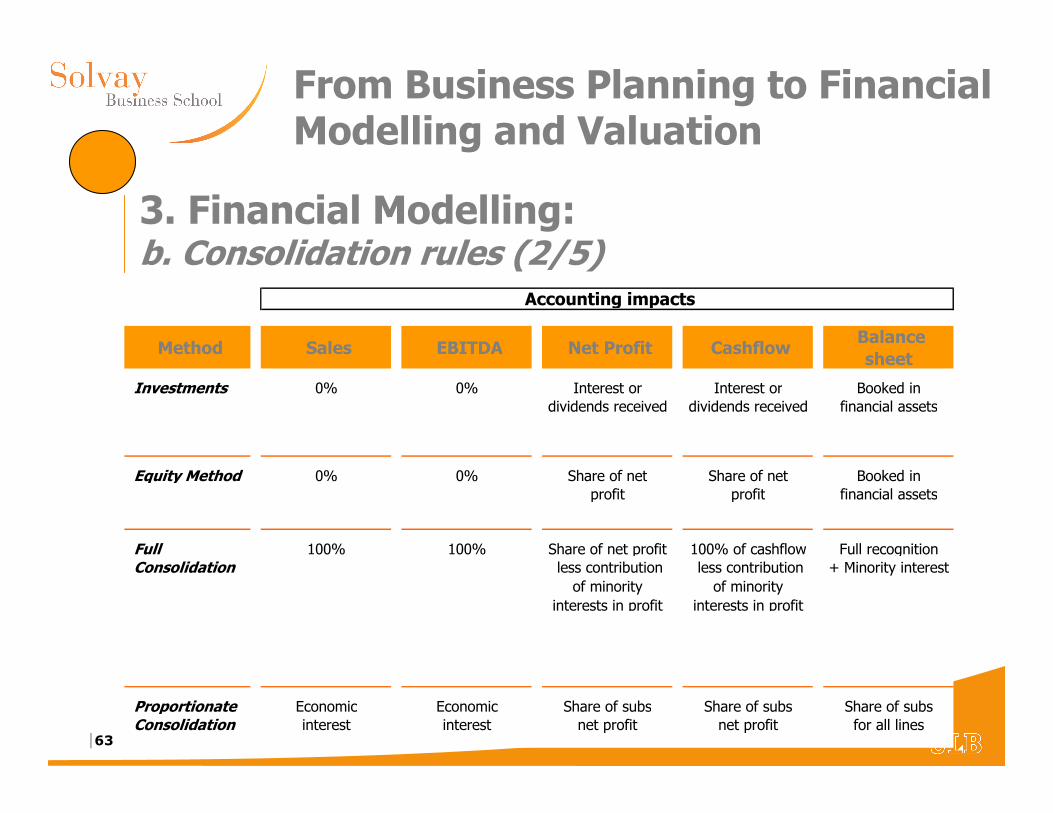

3. Financial Modelling:b. Consolidation rules (2/5)

Method Sales EBITDA Net Profit Cashflow Balance sheet

Investments 0% 0% Interest or Interest or Booked individends received dividends received financial assets

Equity Method 0% 0% Share of net Share of net Booked inprofit profit financial assets

Full 100% 100% Share of net profit 100% of cashflow Full recognitionConsolidation less contribution

of minority

interests in profit

less contribution

of minority

interests in profit

+ Minority interest

Proportionate Economic Economic Share of subs Share of subs Share of subsConsolidation interest interest net profit net profit for all lines

Accounting impacts

|64

From Business Planning to Financial Modelling and Valuation

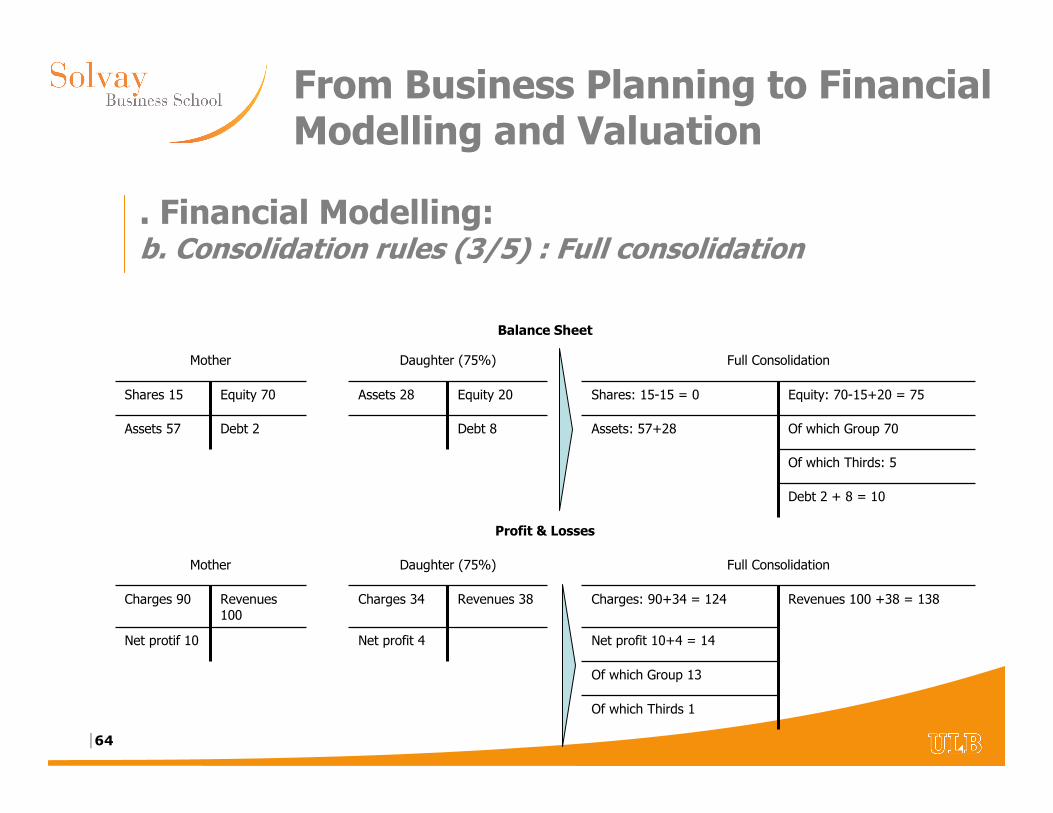

. Financial Modelling:b. Consolidation rules (3/5) : Full consolidation

Balance Sheet

Revenues 100

Debt 2

Equity 70

Net protif 10

Charges 90

Mother

Profit & Losses

Assets 57

Shares 15

Mother

Revenues 38

Debt 8

Equity 20

Net profit 4

Charges 34

Daughter (75%)

Assets 28

Daughter (75%)

Of which Thirds 1

Of which Group 13

Net profit 10+4 = 14

Charges: 90+34 = 124

Full Consolidation

Assets: 57+28

Shares: 15-15 = 0

Full Consolidation

Revenues 100 +38 = 138

Debt 2 + 8 = 10

Of which Thirds: 5

Of which Group 70

Equity: 70-15+20 = 75

|65

From Business Planning to Financial Modelling and Valuation

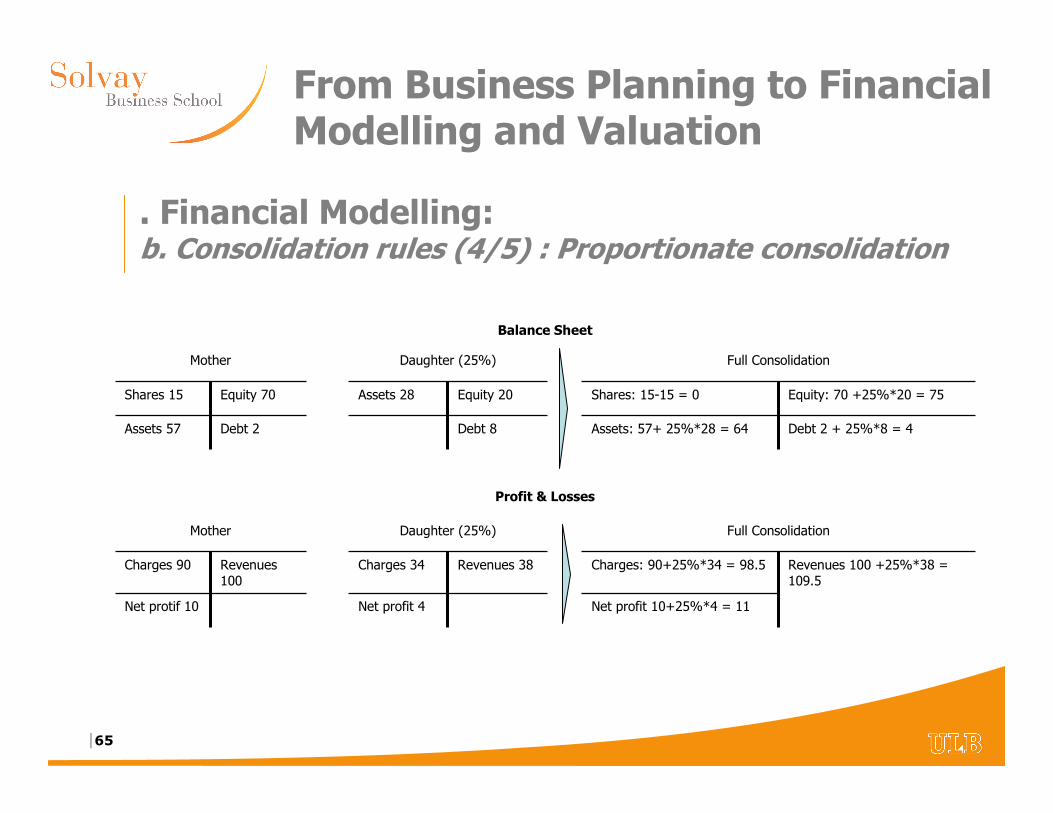

. Financial Modelling:b. Consolidation rules (4/5) : Proportionate consolidation

Balance Sheet

Revenues 100

Debt 2

Equity 70

Net protif 10

Charges 90

Mother

Profit & Losses

Assets 57

Shares 15

Mother

Revenues 38

Debt 8

Equity 20

Net profit 4

Charges 34

Daughter (25%)

Assets 28

Daughter (25%)

Net profit 10+25%*4 = 11

Charges: 90+25%*34 = 98.5

Full Consolidation

Assets: 57+ 25%*28 = 64

Shares: 15-15 = 0

Full Consolidation

Revenues 100 +25%*38 = 109.5

Debt 2 + 25%*8 = 4

Equity: 70 +25%*20 = 75

|66

From Business Planning to Financial Modelling and Valuation

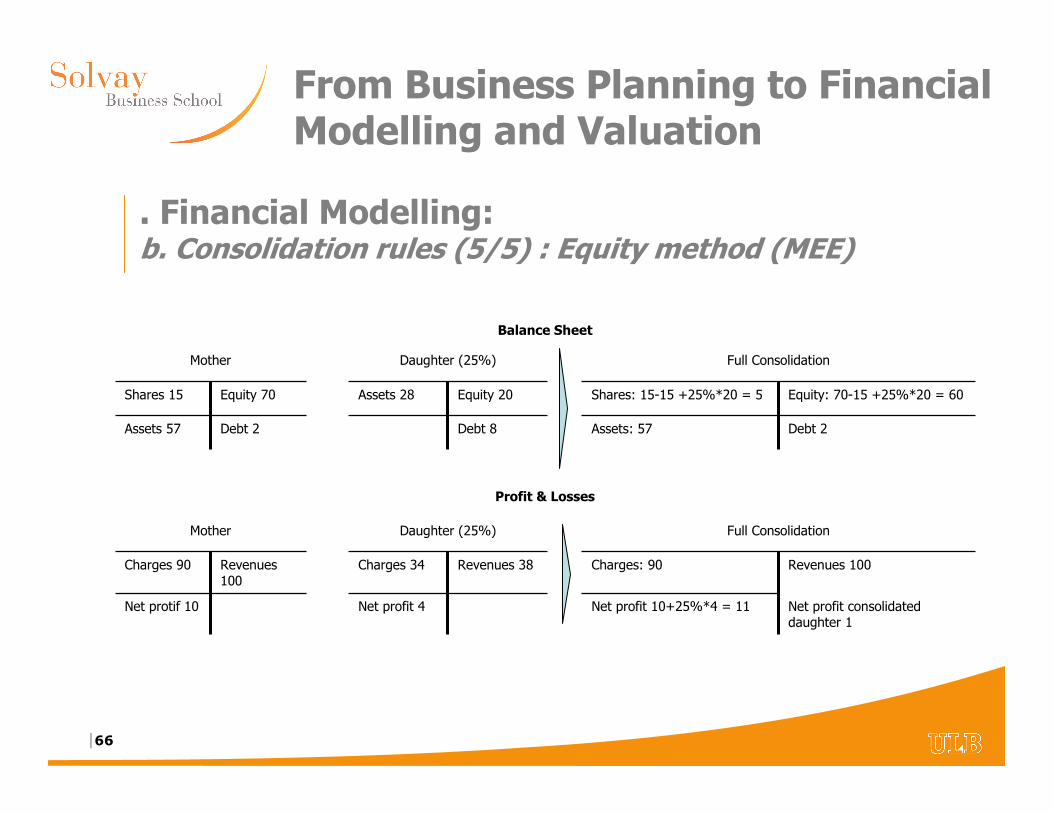

. Financial Modelling:b. Consolidation rules (5/5) : Equity method (MEE)

Balance Sheet

Revenues 100

Debt 2

Equity 70

Net protif 10

Charges 90

Mother

Profit & Losses

Assets 57

Shares 15

Mother

Revenues 38

Debt 8

Equity 20

Net profit 4

Charges 34

Daughter (25%)

Assets 28

Daughter (25%)

Net profit 10+25%*4 = 11

Charges: 90

Full Consolidation

Assets: 57

Shares: 15-15 +25%*20 = 5

Full Consolidation

Net profit consolidated daughter 1

Revenues 100

Debt 2

Equity: 70-15 +25%*20 = 60

|67

From Business Planning to Financial Modelling and Valuation

• Sales– Sales vs. Turnover vs. Revenues

– Revenue recognition rules to be carefully understood (e.g. discounts, allowances and returns, cross-sales, …)

• Gross Margin– Gross Margin ≡ Sales – Cost of goods sold

– Cost of goods sold = Direct costs

– Depreciation and amortization often included here (adjustment isneeded if any)

3. Financial Modelling:c. Sales to EBITDA (1/7)

|68

From Business Planning to Financial Modelling and Valuation

• EBITDA– EBITDA ≡ Earning Before Interest, Taxes, Depreciation and

Amortization

– Operating cashflow

– Most comparable valuation or benchmarking metric• Independent of the financial structure

• Common concept around the world (no impact of accounting rules regarding depreciation matters)

• EBITA– EBITA ≡ Earning Before Interest, Taxes and Amortization

– Operating profit

– After depreciation of fixed tangible assets but before goodwill amortization, since the later is not, as such, an effective operating charge

3. Financial Modelling:c. Sales to EBITDA (2/7)

|69

From Business Planning to Financial Modelling and Valuation

• Financials have to be considered based on their continuing normalized operations– Exceptional items are characterized by

• their unusual nature (unrelated to ordinary business activities) and

• By the infrequence of occurrence (i.e. not expected to happen again)

– Exceptional items include

• Restructuring charges

• Impact of disposed / acquired assets. Proforma data are better within the context of valuation based on multiples (cf. infra)

3. Financial Modelling:c. Sales to EBITDA (3/7)

|70

From Business Planning to Financial Modelling and Valuation

• Definition of the adequate degree of detail:– At consolidated level for mono-product / mono-market business

– Per business unit / per division

– Per product, per market, per plant, per shop, …

• Depend on data availability– Difference between an internal analyst and an external analyst

– Standard information package for listed companies

– Issues related to private companies

– Existing company vs. Start-up project

• Creativity is a key– Delta analysis or % analysis = simplest way

– Exhaustive analysis

– 80 / 20 rule

3. Financial Modelling:c. Sales to EBITDA (4/7)

|71

From Business Planning to Financial Modelling and Valuation

• Estimate revenues following a top-down approach:– Sizing the total market

– Determining the market share dynamics

– Forecasting prices

• Importance of considering the point in the cycle

• If possible breakdown between: – Price effect (to be compared to general inflation)

– Volume effect (to be compared to real GDP growth rate)

– Product-mix effect

– Currency effect (transaction impact vs. translation impact)

– Perimeter effect (cf. organic growth vs. mechanical growth implied acquisitions)

– Accounting changes

3. Financial Modelling:c. Sales to EBITDA (5/7)

|72

From Business Planning to Financial Modelling and Valuation

• When revenue growth forecasts have been built, then implied operating costs may be derived:– Classical breakdown = Cost of goods, Selling general and

administration costs (SG&A) and depreciation

– By default = % of sales but a more detailed approach should be followed: e.g.• Wages should take into account # of FTE and unit wage cost

• Advertizing per category

• Details over P&L impacts from R&D and start-up losses of new activities if any

– If expansion is important, a detailed capex / depreciation model is needed

– Historical and sectorial benchmark is key

3. Financial Modelling:c. Sales to EBITDA (6/7)

|73

From Business Planning to Financial Modelling and Valuation

• Distinction between variable and fixed costs

• Distinction between cash and non-cash operating costs

• Economic segmentation >< Accounting segmentation

• Coherence with revenue model:– Integration of plateau effects if any

– Link between marketing investment and sales evolution

• Analysis of non accounting set of data:– Productivity at production level (e.g. productivity per plant, …) and

capacity evolution

– Productivity evolution employee levels (to be compared to salaryevolution)

• Wage inflation > Sales inflation (normally)

3. Financial Modelling:c. Sales to EBITDA (7/7)

|74

From Business Planning to Financial Modelling and Valuation

• Depreciation are driven by past investments and amortization rules– Real estate

– Equipment

• Assets to be depreciated based on their effective economic life-time– Some significant differences may occur between accounting

amortization rhythm and economic amortization rhythm

– Management conservatism

– Tax considerations

3. Financial Modelling:d. Depreciation, Capex & Working Cap. Req. (1/2)

|75

From Business Planning to Financial Modelling and Valuation

• Capex may be expressed in % of sales (especially maintenance capex)

• Normally (excluding impact of high inflation context), within a medium term perspective, capex and depreciation should tend to be equivalent (in % of sales)

• If expansion is important, a detailed capex / depreciation model is needed (cf. supra for Depreciation in EBITA)

• Working capital items sometimes expressed in # of days of sales (for receivables and accrued items) or in # of days of cost of goods sold (for inventories and payables). Except in case of distinctive price evolution between sales and CoGs, % of sales for each item is easier to take into consideration

• Realism of evolution also to be validated in historical and sectorial perspectives

3. Financial Modelling:d. Depreciation, Capex & Working Cap. Req. (2/2)

|76

From Business Planning to Financial Modelling and Valuation

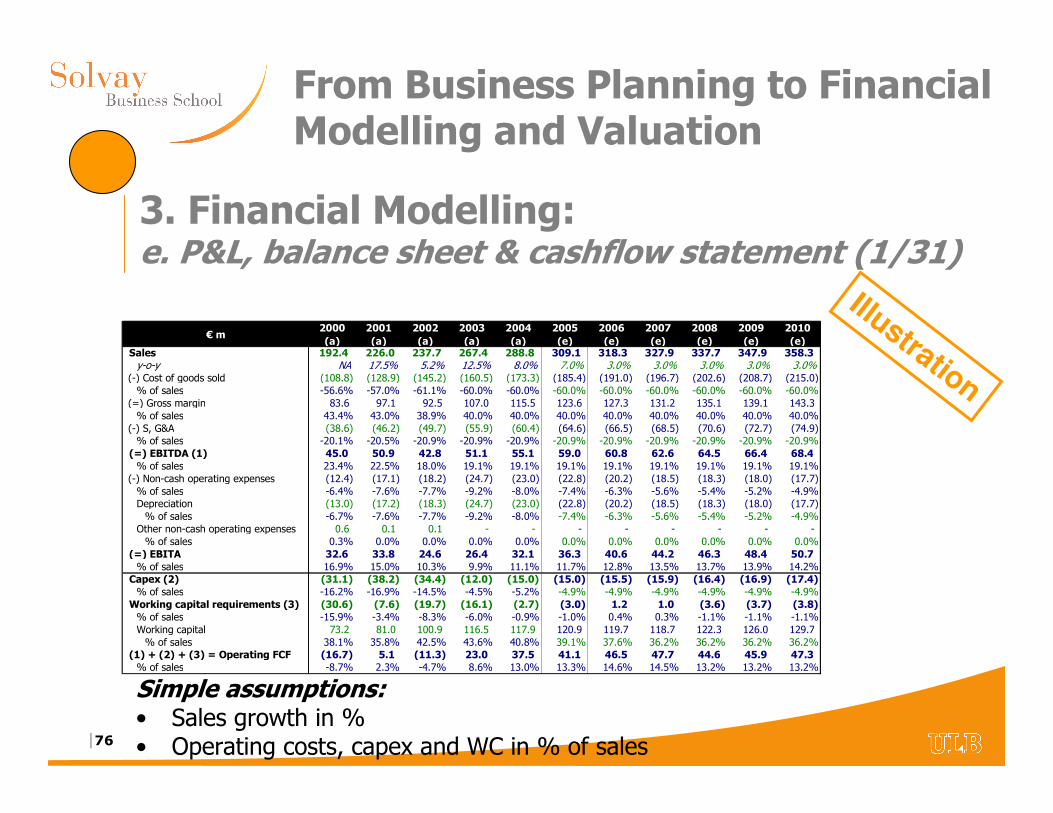

Illustration

€ m2000 (a)

2001 (a)

2002 (a)

2003 (a)

2004 (a)

2005 (e)

2006 (e)

2007 (e)

2008 (e)

2009 (e)

2010 (e)

Sales 192.4 226.0 237.7 267.4 288.8 309.1 318.3 327.9 337.7 347.9 358.3 y-o-y NA 17.5% 5.2% 12.5% 8.0% 7.0% 3.0% 3.0% 3.0% 3.0% 3.0%

(-) Cost of goods sold (108.8) (128.9) (145.2) (160.5) (173.3) (185.4) (191.0) (196.7) (202.6) (208.7) (215.0) % of sales -56.6% -57.0% -61.1% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0%

(=) Gross margin 83.6 97.1 92.5 107.0 115.5 123.6 127.3 131.2 135.1 139.1 143.3 % of sales 43.4% 43.0% 38.9% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

(-) S, G&A (38.6) (46.2) (49.7) (55.9) (60.4) (64.6) (66.5) (68.5) (70.6) (72.7) (74.9) % of sales -20.1% -20.5% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9%

(=) EBITDA (1) 45.0 50.9 42.8 51.1 55.1 59.0 60.8 62.6 64.5 66.4 68.4 % of sales 23.4% 22.5% 18.0% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1%

(-) Non-cash operating expenses (12.4) (17.1) (18.2) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.4% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%Depreciation (13.0) (17.2) (18.3) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.7% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%

Other non-cash operating expenses 0.6 0.1 0.1 - - - - - - - - % of sales 0.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

(=) EBITA 32.6 33.8 24.6 26.4 32.1 36.3 40.6 44.2 46.3 48.4 50.7 % of sales 16.9% 15.0% 10.3% 9.9% 11.1% 11.7% 12.8% 13.5% 13.7% 13.9% 14.2%

Capex (2) (31.1) (38.2) (34.4) (12.0) (15.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) % of sales -16.2% -16.9% -14.5% -4.5% -5.2% -4.9% -4.9% -4.9% -4.9% -4.9% -4.9%

Working capital requirements (3) (30.6) (7.6) (19.7) (16.1) (2.7) (3.0) 1.2 1.0 (3.6) (3.7) (3.8) % of sales -15.9% -3.4% -8.3% -6.0% -0.9% -1.0% 0.4% 0.3% -1.1% -1.1% -1.1%Working capital 73.2 81.0 100.9 116.5 117.9 120.9 119.7 118.7 122.3 126.0 129.7 % of sales 38.1% 35.8% 42.5% 43.6% 40.8% 39.1% 37.6% 36.2% 36.2% 36.2% 36.2%

(1) + (2) + (3) = Operating FCF (16.7) 5.1 (11.3) 23.0 37.5 41.1 46.5 47.7 44.6 45.9 47.3 % of sales -8.7% 2.3% -4.7% 8.6% 13.0% 13.3% 14.6% 14.5% 13.2% 13.2% 13.2%

Simple assumptions:• Sales growth in %• Operating costs, capex and WC in % of sales

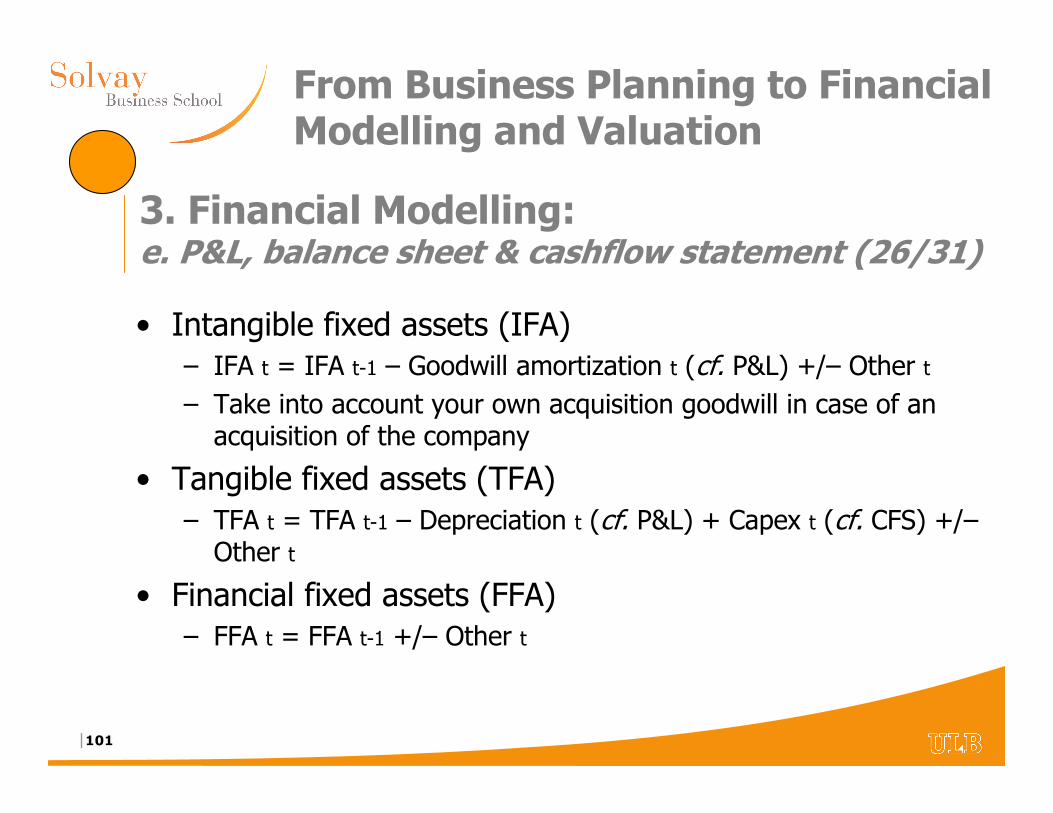

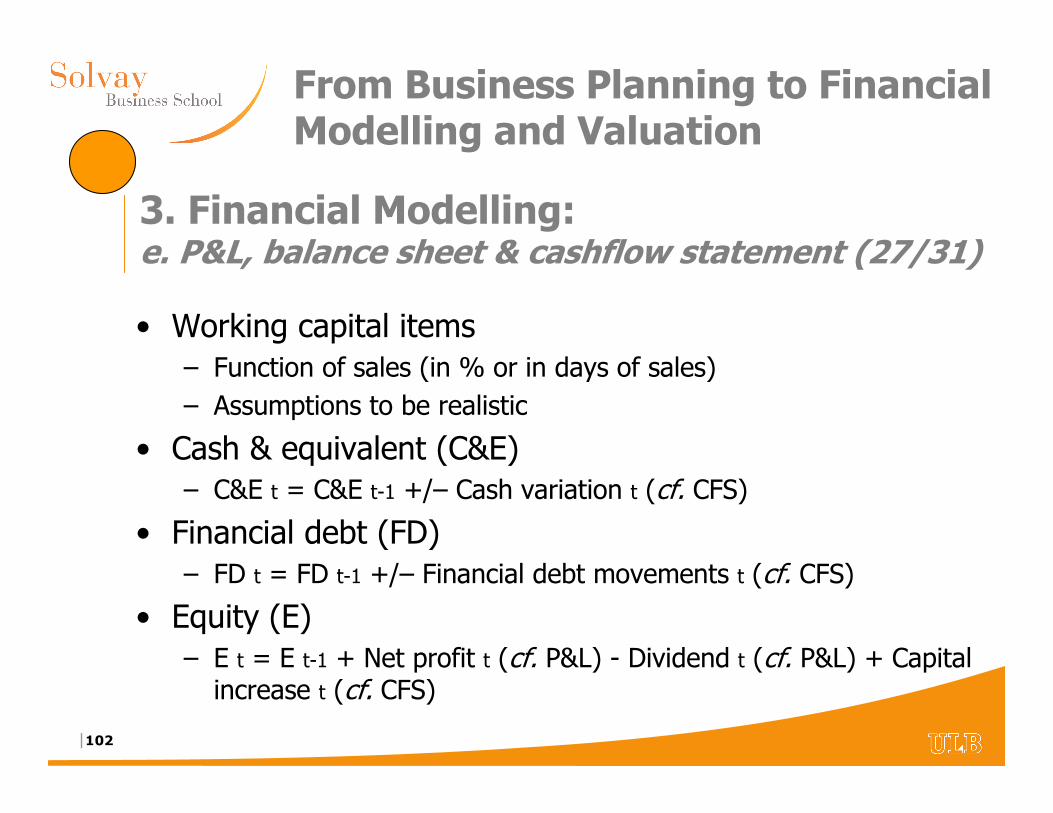

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (1/31)

|77

From Business Planning to Financial Modelling and Valuation

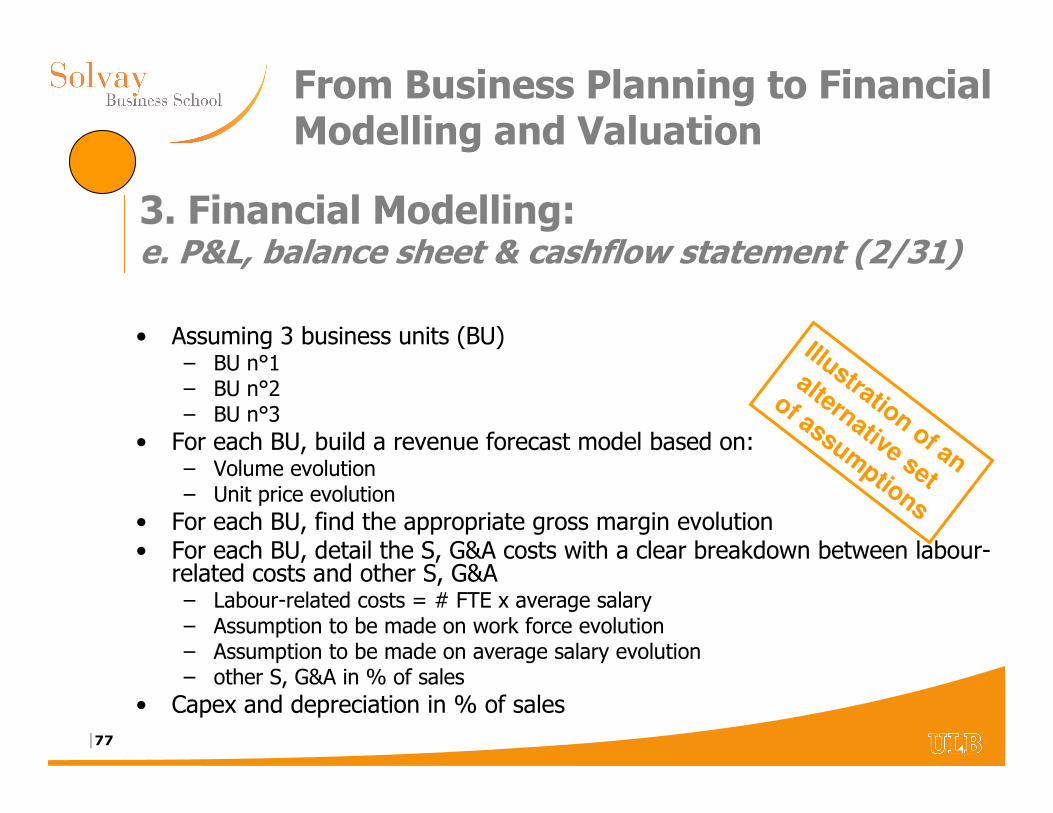

• Assuming 3 business units (BU)– BU n°1– BU n°2– BU n°3

• For each BU, build a revenue forecast model based on:– Volume evolution– Unit price evolution

• For each BU, find the appropriate gross margin evolution• For each BU, detail the S, G&A costs with a clear breakdown between labour-

related costs and other S, G&A– Labour-related costs = # FTE x average salary– Assumption to be made on work force evolution– Assumption to be made on average salary evolution– other S, G&A in % of sales

• Capex and depreciation in % of sales

Illustration of an

alternative set

of assumptions

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (2/31)

|78

From Business Planning to Financial Modelling and Valuation

Illustration of an

alternative set

of assumptions

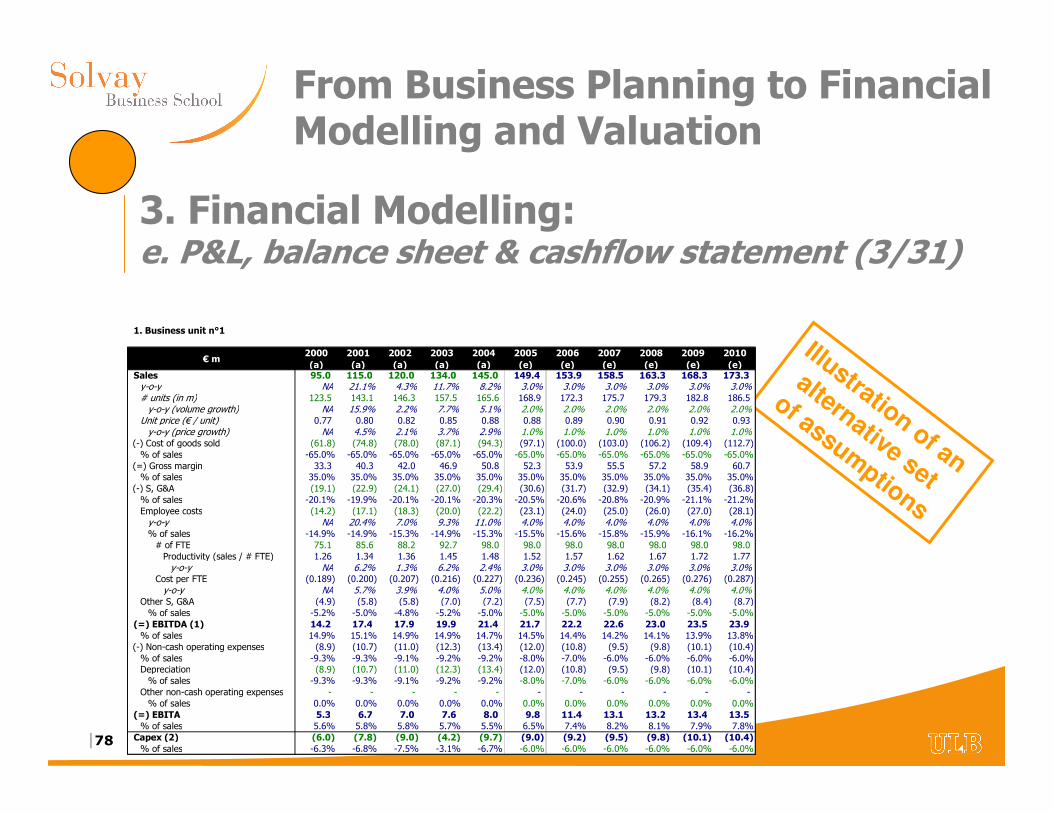

1. Business unit n°1

€ m2000 (a)

2001 (a)

2002 (a)

2003 (a)

2004 (a)

2005 (e)

2006 (e)

2007 (e)

2008 (e)

2009 (e)

2010 (e)

Sales 95.0 115.0 120.0 134.0 145.0 149.4 153.9 158.5 163.3 168.3 173.3 y-o-y NA 21.1% 4.3% 11.7% 8.2% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%# units (in m) 123.5 143.1 146.3 157.5 165.6 168.9 172.3 175.7 179.3 182.8 186.5 y-o-y (volume growth) NA 15.9% 2.2% 7.7% 5.1% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

Unit price (€ / unit) 0.77 0.80 0.82 0.85 0.88 0.88 0.89 0.90 0.91 0.92 0.93 y-o-y (price growth) NA 4.5% 2.1% 3.7% 2.9% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

(-) Cost of goods sold (61.8) (74.8) (78.0) (87.1) (94.3) (97.1) (100.0) (103.0) (106.2) (109.4) (112.7) % of sales -65.0% -65.0% -65.0% -65.0% -65.0% -65.0% -65.0% -65.0% -65.0% -65.0% -65.0%

(=) Gross margin 33.3 40.3 42.0 46.9 50.8 52.3 53.9 55.5 57.2 58.9 60.7 % of sales 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

(-) S, G&A (19.1) (22.9) (24.1) (27.0) (29.4) (30.6) (31.7) (32.9) (34.1) (35.4) (36.8) % of sales -20.1% -19.9% -20.1% -20.1% -20.3% -20.5% -20.6% -20.8% -20.9% -21.1% -21.2%Employee costs (14.2) (17.1) (18.3) (20.0) (22.2) (23.1) (24.0) (25.0) (26.0) (27.0) (28.1) y-o-y NA 20.4% 7.0% 9.3% 11.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%% of sales -14.9% -14.9% -15.3% -14.9% -15.3% -15.5% -15.6% -15.8% -15.9% -16.1% -16.2%# of FTE 75.1 85.6 88.2 92.7 98.0 98.0 98.0 98.0 98.0 98.0 98.0 Productivity (sales / # FTE) 1.26 1.34 1.36 1.45 1.48 1.52 1.57 1.62 1.67 1.72 1.77 y-o-y NA 6.2% 1.3% 6.2% 2.4% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Cost per FTE (0.189) (0.200) (0.207) (0.216) (0.227) (0.236) (0.245) (0.255) (0.265) (0.276) (0.287) y-o-y NA 5.7% 3.9% 4.0% 5.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Other S, G&A (4.9) (5.8) (5.8) (7.0) (7.2) (7.5) (7.7) (7.9) (8.2) (8.4) (8.7) % of sales -5.2% -5.0% -4.8% -5.2% -5.0% -5.0% -5.0% -5.0% -5.0% -5.0% -5.0%

(=) EBITDA (1) 14.2 17.4 17.9 19.9 21.4 21.7 22.2 22.6 23.0 23.5 23.9 % of sales 14.9% 15.1% 14.9% 14.9% 14.7% 14.5% 14.4% 14.2% 14.1% 13.9% 13.8%

(-) Non-cash operating expenses (8.9) (10.7) (11.0) (12.3) (13.4) (12.0) (10.8) (9.5) (9.8) (10.1) (10.4) % of sales -9.3% -9.3% -9.1% -9.2% -9.2% -8.0% -7.0% -6.0% -6.0% -6.0% -6.0%Depreciation (8.9) (10.7) (11.0) (12.3) (13.4) (12.0) (10.8) (9.5) (9.8) (10.1) (10.4) % of sales -9.3% -9.3% -9.1% -9.2% -9.2% -8.0% -7.0% -6.0% -6.0% -6.0% -6.0%

Other non-cash operating expenses - - - - - - - - - - - % of sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

(=) EBITA 5.3 6.7 7.0 7.6 8.0 9.8 11.4 13.1 13.2 13.4 13.5 % of sales 5.6% 5.8% 5.8% 5.7% 5.5% 6.5% 7.4% 8.2% 8.1% 7.9% 7.8%

Capex (2) (6.0) (7.8) (9.0) (4.2) (9.7) (9.0) (9.2) (9.5) (9.8) (10.1) (10.4) % of sales -6.3% -6.8% -7.5% -3.1% -6.7% -6.0% -6.0% -6.0% -6.0% -6.0% -6.0%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (3/31)

|79

From Business Planning to Financial Modelling and Valuation

Illustration of an

alternative set

of assumptions

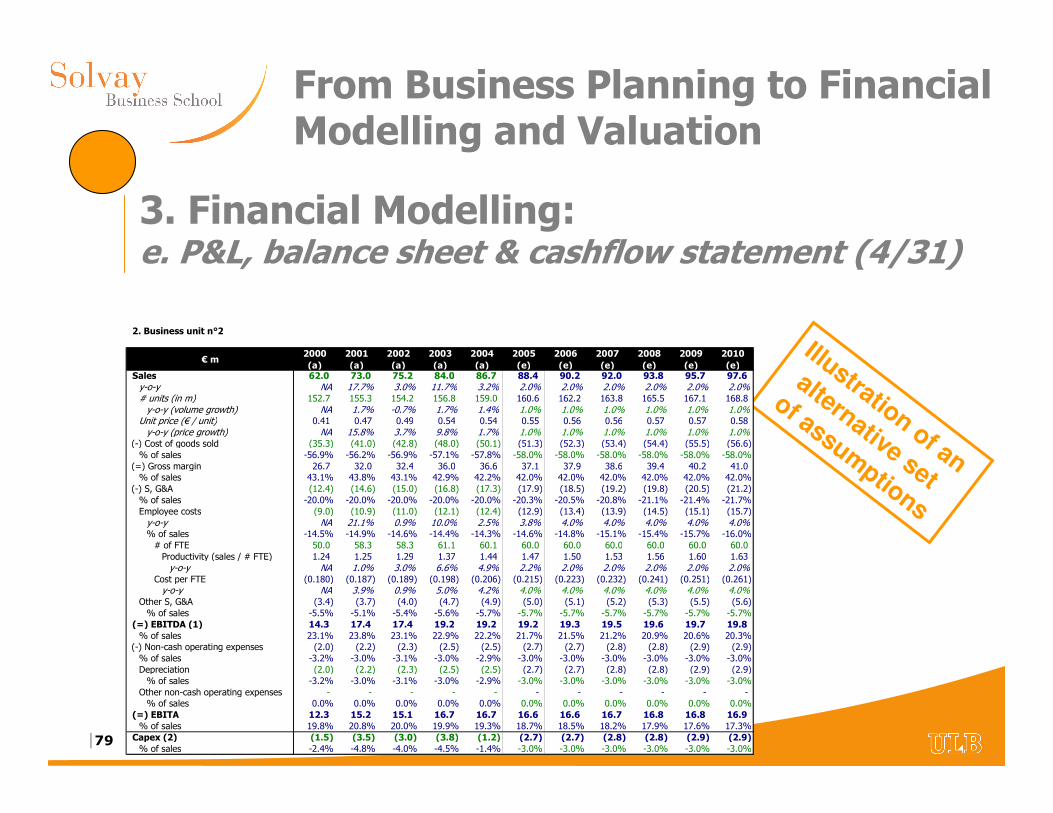

2. Business unit n°2

€ m2000 (a)

2001 (a)

2002 (a)

2003 (a)

2004 (a)

2005 (e)

2006 (e)

2007 (e)

2008 (e)

2009 (e)

2010 (e)

Sales 62.0 73.0 75.2 84.0 86.7 88.4 90.2 92.0 93.8 95.7 97.6 y-o-y NA 17.7% 3.0% 11.7% 3.2% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%# units (in m) 152.7 155.3 154.2 156.8 159.0 160.6 162.2 163.8 165.5 167.1 168.8 y-o-y (volume growth) NA 1.7% -0.7% 1.7% 1.4% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Unit price (€ / unit) 0.41 0.47 0.49 0.54 0.54 0.55 0.56 0.56 0.57 0.57 0.58 y-o-y (price growth) NA 15.8% 3.7% 9.8% 1.7% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

(-) Cost of goods sold (35.3) (41.0) (42.8) (48.0) (50.1) (51.3) (52.3) (53.4) (54.4) (55.5) (56.6) % of sales -56.9% -56.2% -56.9% -57.1% -57.8% -58.0% -58.0% -58.0% -58.0% -58.0% -58.0%

(=) Gross margin 26.7 32.0 32.4 36.0 36.6 37.1 37.9 38.6 39.4 40.2 41.0 % of sales 43.1% 43.8% 43.1% 42.9% 42.2% 42.0% 42.0% 42.0% 42.0% 42.0% 42.0%

(-) S, G&A (12.4) (14.6) (15.0) (16.8) (17.3) (17.9) (18.5) (19.2) (19.8) (20.5) (21.2) % of sales -20.0% -20.0% -20.0% -20.0% -20.0% -20.3% -20.5% -20.8% -21.1% -21.4% -21.7%Employee costs (9.0) (10.9) (11.0) (12.1) (12.4) (12.9) (13.4) (13.9) (14.5) (15.1) (15.7) y-o-y NA 21.1% 0.9% 10.0% 2.5% 3.8% 4.0% 4.0% 4.0% 4.0% 4.0%% of sales -14.5% -14.9% -14.6% -14.4% -14.3% -14.6% -14.8% -15.1% -15.4% -15.7% -16.0%# of FTE 50.0 58.3 58.3 61.1 60.1 60.0 60.0 60.0 60.0 60.0 60.0 Productivity (sales / # FTE) 1.24 1.25 1.29 1.37 1.44 1.47 1.50 1.53 1.56 1.60 1.63 y-o-y NA 1.0% 3.0% 6.6% 4.9% 2.2% 2.0% 2.0% 2.0% 2.0% 2.0%

Cost per FTE (0.180) (0.187) (0.189) (0.198) (0.206) (0.215) (0.223) (0.232) (0.241) (0.251) (0.261) y-o-y NA 3.9% 0.9% 5.0% 4.2% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Other S, G&A (3.4) (3.7) (4.0) (4.7) (4.9) (5.0) (5.1) (5.2) (5.3) (5.5) (5.6) % of sales -5.5% -5.1% -5.4% -5.6% -5.7% -5.7% -5.7% -5.7% -5.7% -5.7% -5.7%

(=) EBITDA (1) 14.3 17.4 17.4 19.2 19.2 19.2 19.3 19.5 19.6 19.7 19.8 % of sales 23.1% 23.8% 23.1% 22.9% 22.2% 21.7% 21.5% 21.2% 20.9% 20.6% 20.3%

(-) Non-cash operating expenses (2.0) (2.2) (2.3) (2.5) (2.5) (2.7) (2.7) (2.8) (2.8) (2.9) (2.9) % of sales -3.2% -3.0% -3.1% -3.0% -2.9% -3.0% -3.0% -3.0% -3.0% -3.0% -3.0%Depreciation (2.0) (2.2) (2.3) (2.5) (2.5) (2.7) (2.7) (2.8) (2.8) (2.9) (2.9) % of sales -3.2% -3.0% -3.1% -3.0% -2.9% -3.0% -3.0% -3.0% -3.0% -3.0% -3.0%

Other non-cash operating expenses - - - - - - - - - - - % of sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

(=) EBITA 12.3 15.2 15.1 16.7 16.7 16.6 16.6 16.7 16.8 16.8 16.9 % of sales 19.8% 20.8% 20.0% 19.9% 19.3% 18.7% 18.5% 18.2% 17.9% 17.6% 17.3%

Capex (2) (1.5) (3.5) (3.0) (3.8) (1.2) (2.7) (2.7) (2.8) (2.8) (2.9) (2.9) % of sales -2.4% -4.8% -4.0% -4.5% -1.4% -3.0% -3.0% -3.0% -3.0% -3.0% -3.0%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (4/31)

|80

From Business Planning to Financial Modelling and Valuation

Illustration of an

alternative set

of assumptions

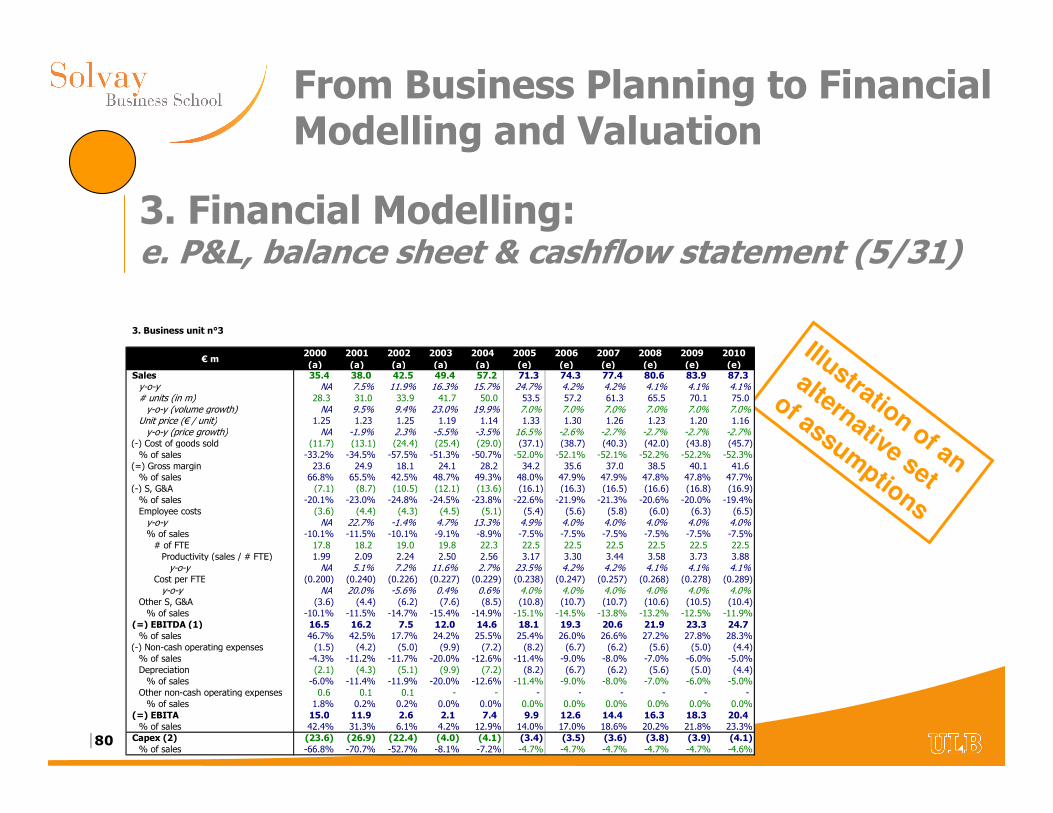

3. Business unit n°3

€ m2000 (a)

2001 (a)

2002 (a)

2003 (a)

2004 (a)

2005 (e)

2006 (e)

2007 (e)

2008 (e)

2009 (e)

2010 (e)

Sales 35.4 38.0 42.5 49.4 57.2 71.3 74.3 77.4 80.6 83.9 87.3 y-o-y NA 7.5% 11.9% 16.3% 15.7% 24.7% 4.2% 4.2% 4.1% 4.1% 4.1%# units (in m) 28.3 31.0 33.9 41.7 50.0 53.5 57.2 61.3 65.5 70.1 75.0 y-o-y (volume growth) NA 9.5% 9.4% 23.0% 19.9% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0%

Unit price (€ / unit) 1.25 1.23 1.25 1.19 1.14 1.33 1.30 1.26 1.23 1.20 1.16 y-o-y (price growth) NA -1.9% 2.3% -5.5% -3.5% 16.5% -2.6% -2.7% -2.7% -2.7% -2.7%

(-) Cost of goods sold (11.7) (13.1) (24.4) (25.4) (29.0) (37.1) (38.7) (40.3) (42.0) (43.8) (45.7) % of sales -33.2% -34.5% -57.5% -51.3% -50.7% -52.0% -52.1% -52.1% -52.2% -52.2% -52.3%

(=) Gross margin 23.6 24.9 18.1 24.1 28.2 34.2 35.6 37.0 38.5 40.1 41.6 % of sales 66.8% 65.5% 42.5% 48.7% 49.3% 48.0% 47.9% 47.9% 47.8% 47.8% 47.7%

(-) S, G&A (7.1) (8.7) (10.5) (12.1) (13.6) (16.1) (16.3) (16.5) (16.6) (16.8) (16.9) % of sales -20.1% -23.0% -24.8% -24.5% -23.8% -22.6% -21.9% -21.3% -20.6% -20.0% -19.4%Employee costs (3.6) (4.4) (4.3) (4.5) (5.1) (5.4) (5.6) (5.8) (6.0) (6.3) (6.5) y-o-y NA 22.7% -1.4% 4.7% 13.3% 4.9% 4.0% 4.0% 4.0% 4.0% 4.0%% of sales -10.1% -11.5% -10.1% -9.1% -8.9% -7.5% -7.5% -7.5% -7.5% -7.5% -7.5%# of FTE 17.8 18.2 19.0 19.8 22.3 22.5 22.5 22.5 22.5 22.5 22.5 Productivity (sales / # FTE) 1.99 2.09 2.24 2.50 2.56 3.17 3.30 3.44 3.58 3.73 3.88 y-o-y NA 5.1% 7.2% 11.6% 2.7% 23.5% 4.2% 4.2% 4.1% 4.1% 4.1%

Cost per FTE (0.200) (0.240) (0.226) (0.227) (0.229) (0.238) (0.247) (0.257) (0.268) (0.278) (0.289) y-o-y NA 20.0% -5.6% 0.4% 0.6% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Other S, G&A (3.6) (4.4) (6.2) (7.6) (8.5) (10.8) (10.7) (10.7) (10.6) (10.5) (10.4) % of sales -10.1% -11.5% -14.7% -15.4% -14.9% -15.1% -14.5% -13.8% -13.2% -12.5% -11.9%

(=) EBITDA (1) 16.5 16.2 7.5 12.0 14.6 18.1 19.3 20.6 21.9 23.3 24.7 % of sales 46.7% 42.5% 17.7% 24.2% 25.5% 25.4% 26.0% 26.6% 27.2% 27.8% 28.3%

(-) Non-cash operating expenses (1.5) (4.2) (5.0) (9.9) (7.2) (8.2) (6.7) (6.2) (5.6) (5.0) (4.4) % of sales -4.3% -11.2% -11.7% -20.0% -12.6% -11.4% -9.0% -8.0% -7.0% -6.0% -5.0%Depreciation (2.1) (4.3) (5.1) (9.9) (7.2) (8.2) (6.7) (6.2) (5.6) (5.0) (4.4) % of sales -6.0% -11.4% -11.9% -20.0% -12.6% -11.4% -9.0% -8.0% -7.0% -6.0% -5.0%

Other non-cash operating expenses 0.6 0.1 0.1 - - - - - - - - % of sales 1.8% 0.2% 0.2% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

(=) EBITA 15.0 11.9 2.6 2.1 7.4 9.9 12.6 14.4 16.3 18.3 20.4 % of sales 42.4% 31.3% 6.1% 4.2% 12.9% 14.0% 17.0% 18.6% 20.2% 21.8% 23.3%

Capex (2) (23.6) (26.9) (22.4) (4.0) (4.1) (3.4) (3.5) (3.6) (3.8) (3.9) (4.1) % of sales -66.8% -70.7% -52.7% -8.1% -7.2% -4.7% -4.7% -4.7% -4.7% -4.7% -4.6%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (5/31)

|81

From Business Planning to Financial Modelling and Valuation

Illustration of an

alternative set

of assumptions

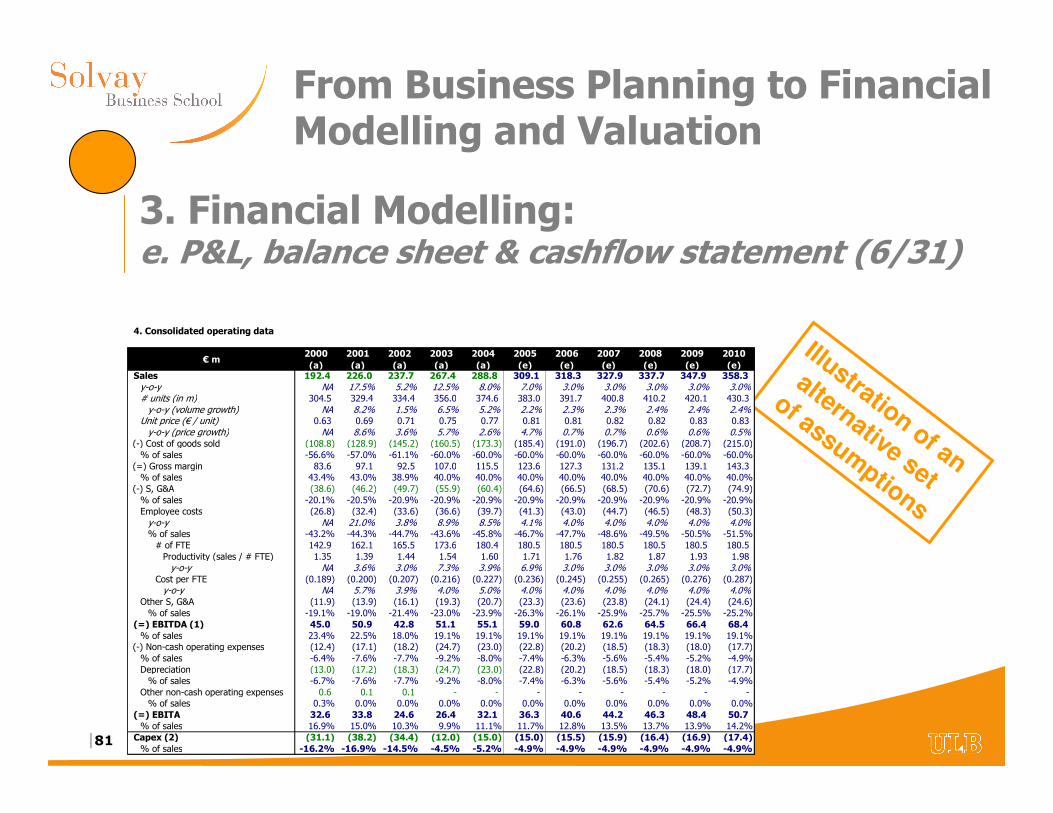

4. Consolidated operating data

€ m2000 (a)

2001 (a)

2002 (a)

2003 (a)

2004 (a)

2005 (e)

2006 (e)

2007 (e)

2008 (e)

2009 (e)

2010 (e)

Sales 192.4 226.0 237.7 267.4 288.8 309.1 318.3 327.9 337.7 347.9 358.3 y-o-y NA 17.5% 5.2% 12.5% 8.0% 7.0% 3.0% 3.0% 3.0% 3.0% 3.0%# units (in m) 304.5 329.4 334.4 356.0 374.6 383.0 391.7 400.8 410.2 420.1 430.3 y-o-y (volume growth) NA 8.2% 1.5% 6.5% 5.2% 2.2% 2.3% 2.3% 2.4% 2.4% 2.4%

Unit price (€ / unit) 0.63 0.69 0.71 0.75 0.77 0.81 0.81 0.82 0.82 0.83 0.83 y-o-y (price growth) NA 8.6% 3.6% 5.7% 2.6% 4.7% 0.7% 0.7% 0.6% 0.6% 0.5%

(-) Cost of goods sold (108.8) (128.9) (145.2) (160.5) (173.3) (185.4) (191.0) (196.7) (202.6) (208.7) (215.0) % of sales -56.6% -57.0% -61.1% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0%

(=) Gross margin 83.6 97.1 92.5 107.0 115.5 123.6 127.3 131.2 135.1 139.1 143.3 % of sales 43.4% 43.0% 38.9% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

(-) S, G&A (38.6) (46.2) (49.7) (55.9) (60.4) (64.6) (66.5) (68.5) (70.6) (72.7) (74.9) % of sales -20.1% -20.5% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9%Employee costs (26.8) (32.4) (33.6) (36.6) (39.7) (41.3) (43.0) (44.7) (46.5) (48.3) (50.3) y-o-y NA 21.0% 3.8% 8.9% 8.5% 4.1% 4.0% 4.0% 4.0% 4.0% 4.0%% of sales -43.2% -44.3% -44.7% -43.6% -45.8% -46.7% -47.7% -48.6% -49.5% -50.5% -51.5%# of FTE 142.9 162.1 165.5 173.6 180.4 180.5 180.5 180.5 180.5 180.5 180.5 Productivity (sales / # FTE) 1.35 1.39 1.44 1.54 1.60 1.71 1.76 1.82 1.87 1.93 1.98 y-o-y NA 3.6% 3.0% 7.3% 3.9% 6.9% 3.0% 3.0% 3.0% 3.0% 3.0%

Cost per FTE (0.189) (0.200) (0.207) (0.216) (0.227) (0.236) (0.245) (0.255) (0.265) (0.276) (0.287) y-o-y NA 5.7% 3.9% 4.0% 5.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Other S, G&A (11.9) (13.9) (16.1) (19.3) (20.7) (23.3) (23.6) (23.8) (24.1) (24.4) (24.6) % of sales -19.1% -19.0% -21.4% -23.0% -23.9% -26.3% -26.1% -25.9% -25.7% -25.5% -25.2%

(=) EBITDA (1) 45.0 50.9 42.8 51.1 55.1 59.0 60.8 62.6 64.5 66.4 68.4 % of sales 23.4% 22.5% 18.0% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1%

(-) Non-cash operating expenses (12.4) (17.1) (18.2) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.4% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%Depreciation (13.0) (17.2) (18.3) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.7% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%

Other non-cash operating expenses 0.6 0.1 0.1 - - - - - - - - % of sales 0.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

(=) EBITA 32.6 33.8 24.6 26.4 32.1 36.3 40.6 44.2 46.3 48.4 50.7 % of sales 16.9% 15.0% 10.3% 9.9% 11.1% 11.7% 12.8% 13.5% 13.7% 13.9% 14.2%

Capex (2) (31.1) (38.2) (34.4) (12.0) (15.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) % of sales -16.2% -16.9% -14.5% -4.5% -5.2% -4.9% -4.9% -4.9% -4.9% -4.9% -4.9%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (6/31)

|82

From Business Planning to Financial Modelling and Valuation

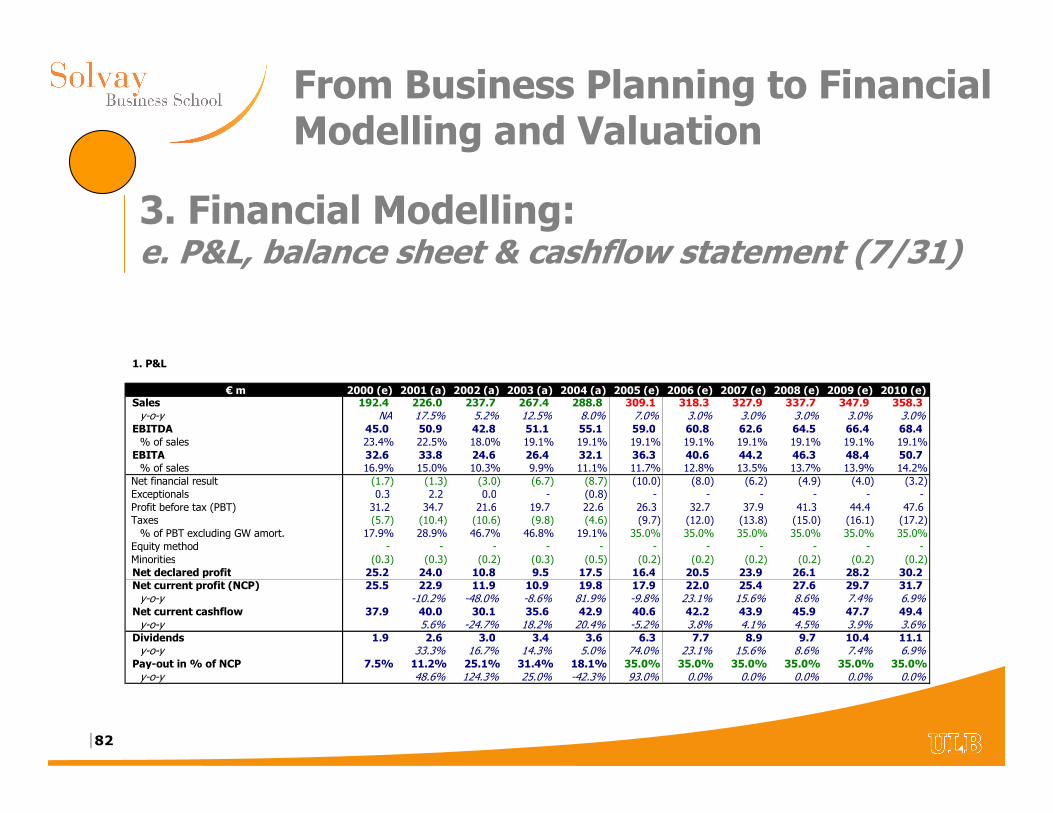

1. P&L

€ m 2000 (e) 2001 (a) 2002 (a) 2003 (a) 2004 (a) 2005 (e) 2006 (e) 2007 (e) 2008 (e) 2009 (e) 2010 (e)Sales 192.4 226.0 237.7 267.4 288.8 309.1 318.3 327.9 337.7 347.9 358.3 y-o-y NA 17.5% 5.2% 12.5% 8.0% 7.0% 3.0% 3.0% 3.0% 3.0% 3.0%

EBITDA 45.0 50.9 42.8 51.1 55.1 59.0 60.8 62.6 64.5 66.4 68.4 % of sales 23.4% 22.5% 18.0% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1%

EBITA 32.6 33.8 24.6 26.4 32.1 36.3 40.6 44.2 46.3 48.4 50.7 % of sales 16.9% 15.0% 10.3% 9.9% 11.1% 11.7% 12.8% 13.5% 13.7% 13.9% 14.2%

Net financial result (1.7) (1.3) (3.0) (6.7) (8.7) (10.0) (8.0) (6.2) (4.9) (4.0) (3.2) Exceptionals 0.3 2.2 0.0 - (0.8) - - - - - - Profit before tax (PBT) 31.2 34.7 21.6 19.7 22.6 26.3 32.7 37.9 41.3 44.4 47.6 Taxes (5.7) (10.4) (10.6) (9.8) (4.6) (9.7) (12.0) (13.8) (15.0) (16.1) (17.2) % of PBT excluding GW amort. 17.9% 28.9% 46.7% 46.8% 19.1% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

Equity method - - - - - - - - - - - Minorities (0.3) (0.3) (0.2) (0.3) (0.5) (0.2) (0.2) (0.2) (0.2) (0.2) (0.2) Net declared profit 25.2 24.0 10.8 9.5 17.5 16.4 20.5 23.9 26.1 28.2 30.2 Net current profit (NCP) 25.5 22.9 11.9 10.9 19.8 17.9 22.0 25.4 27.6 29.7 31.7 y-o-y -10.2% -48.0% -8.6% 81.9% -9.8% 23.1% 15.6% 8.6% 7.4% 6.9%

Net current cashflow 37.9 40.0 30.1 35.6 42.9 40.6 42.2 43.9 45.9 47.7 49.4 y-o-y 5.6% -24.7% 18.2% 20.4% -5.2% 3.8% 4.1% 4.5% 3.9% 3.6%

Dividends 1.9 2.6 3.0 3.4 3.6 6.3 7.7 8.9 9.7 10.4 11.1 y-o-y 33.3% 16.7% 14.3% 5.0% 74.0% 23.1% 15.6% 8.6% 7.4% 6.9%

Pay-out in % of NCP 7.5% 11.2% 25.1% 31.4% 18.1% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%y-o-y 48.6% 124.3% 25.0% -42.3% 93.0% 0.0% 0.0% 0.0% 0.0% 0.0%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (7/31)

|83

From Business Planning to Financial Modelling and Valuation

• Cost of debt – Existing financial (bank) facilities may be maintained (if any)– Estimated cost estimated as follows:

• Risk free (short term) + corporate spread + hedging costs (if any)• Corporate spread of debt via rating or via function of ‘NFD / EBITDA’ ratio• Hedging cost depending of the yield curve (cf. short term vs. long term rates)

– Calculation to be made in a separate table (cf. infra)

• Interest on cash– Always be prudent (e.g. 1% x Cash t-1)– Try to minimize cash by choosing an appropriate debt level and

dividend policy

• Other financial results– To be determined. Normally = 0 if there is no unconsolidated

shareholdings

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (8/31)

|84

From Business Planning to Financial Modelling and Valuation

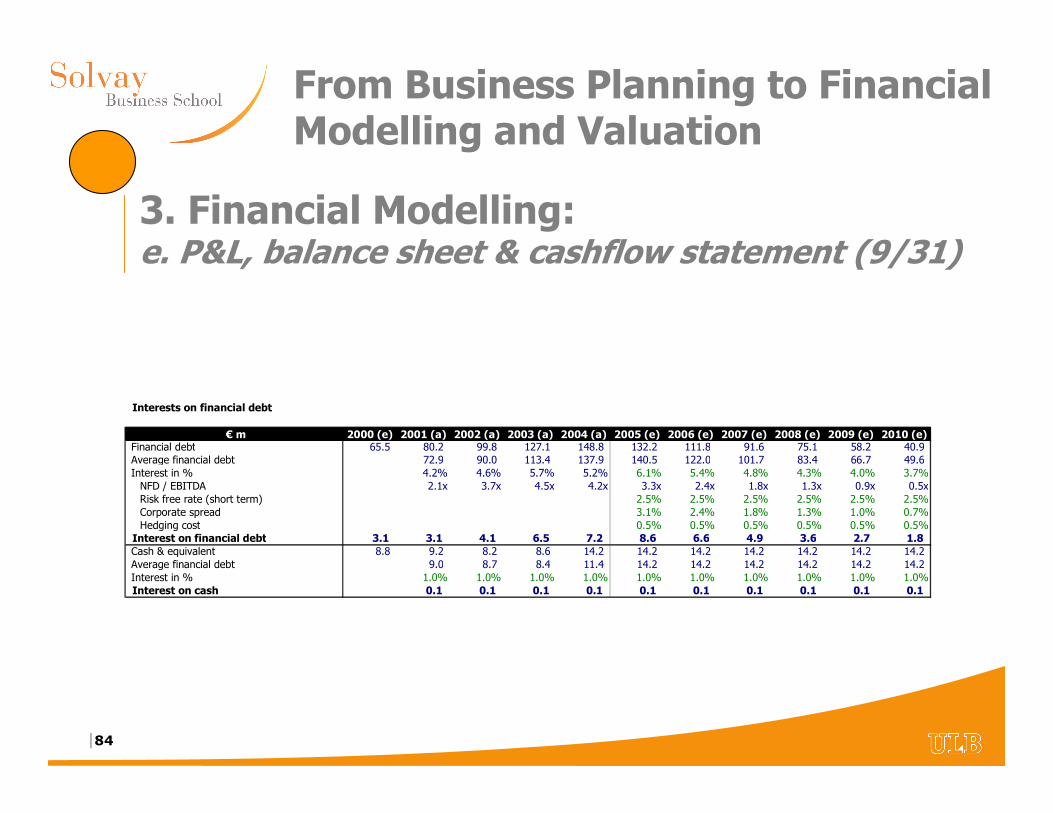

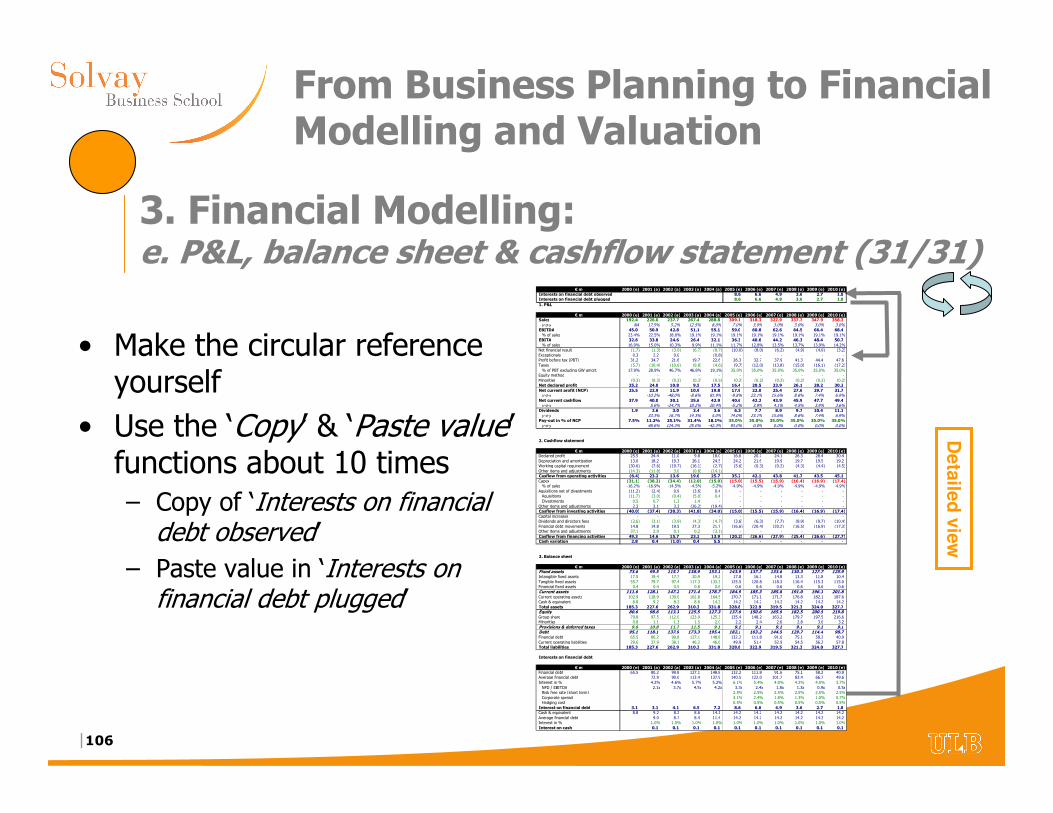

Interests on financial debt

€ m 2000 (e) 2001 (a) 2002 (a) 2003 (a) 2004 (a) 2005 (e) 2006 (e) 2007 (e) 2008 (e) 2009 (e) 2010 (e)Financial debt 65.5 80.2 99.8 127.1 148.8 132.2 111.8 91.6 75.1 58.2 40.9 Average financial debt 72.9 90.0 113.4 137.9 140.5 122.0 101.7 83.4 66.7 49.6 Interest in % 4.2% 4.6% 5.7% 5.2% 6.1% 5.4% 4.8% 4.3% 4.0% 3.7%NFD / EBITDA 2.1x 3.7x 4.5x 4.2x 3.3x 2.4x 1.8x 1.3x 0.9x 0.5xRisk free rate (short term) 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%Corporate spread 3.1% 2.4% 1.8% 1.3% 1.0% 0.7%Hedging cost 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Interest on financial debt 3.1 3.1 4.1 6.5 7.2 8.6 6.6 4.9 3.6 2.7 1.8 Cash & equivalent 8.8 9.2 8.2 8.6 14.2 14.2 14.2 14.2 14.2 14.2 14.2 Average financial debt 9.0 8.7 8.4 11.4 14.2 14.2 14.2 14.2 14.2 14.2 Interest in % 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%Interest on cash 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (9/31)

|85

From Business Planning to Financial Modelling and Valuation

• Extraordinary items– Excluding specific information = 0

• Taxes– Application of a % on PBT (excluding goodwill amortization)

– Tax loss carry forward has to be considered

– Tax optimization has to be considered

• Equity accounted shareholdings and minorities– To be determined on a case by case basis

– Be careful if 100% of earnings are not paid in dividend (cf. important for the establishment of the cashflow statement)

• Dividend policy– To be considered in the overall perspective

– Based on pay-out on ‘Net current profit’

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (10/31)

|86

From Business Planning to Financial Modelling and Valuation

• NCP= Net Profit + Amortization Goodwill + Exceptionals

• Net current profit has to be adjusted for– Financing one-offs (e.g. debt refinancing)

– Parent’s share in a subsidiary’s exceptional item when parent uses the equity method

– Tax impact also has to be considered

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (11/31)

|87

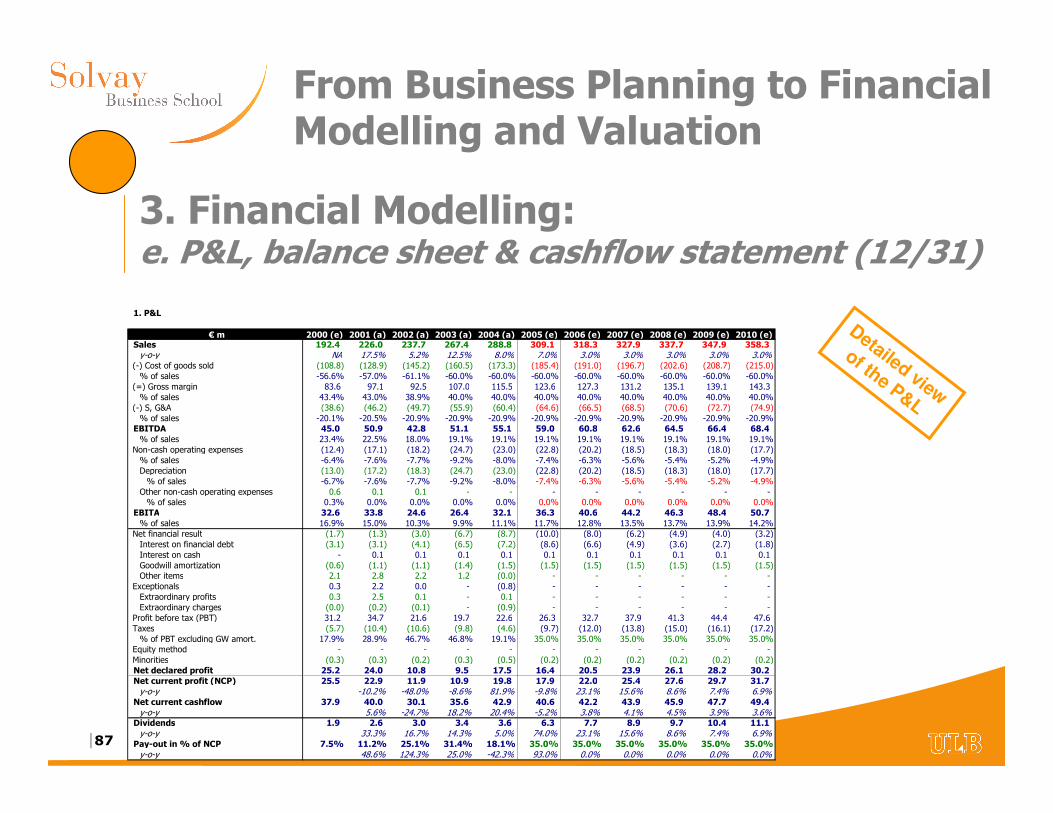

From Business Planning to Financial Modelling and Valuation

Detailed view

of the P&L

1. P&L

€ m 2000 (e) 2001 (a) 2002 (a) 2003 (a) 2004 (a) 2005 (e) 2006 (e) 2007 (e) 2008 (e) 2009 (e) 2010 (e)Sales 192.4 226.0 237.7 267.4 288.8 309.1 318.3 327.9 337.7 347.9 358.3 y-o-y NA 17.5% 5.2% 12.5% 8.0% 7.0% 3.0% 3.0% 3.0% 3.0% 3.0%

(-) Cost of goods sold (108.8) (128.9) (145.2) (160.5) (173.3) (185.4) (191.0) (196.7) (202.6) (208.7) (215.0) % of sales -56.6% -57.0% -61.1% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0% -60.0%

(=) Gross margin 83.6 97.1 92.5 107.0 115.5 123.6 127.3 131.2 135.1 139.1 143.3 % of sales 43.4% 43.0% 38.9% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

(-) S, G&A (38.6) (46.2) (49.7) (55.9) (60.4) (64.6) (66.5) (68.5) (70.6) (72.7) (74.9) % of sales -20.1% -20.5% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9% -20.9%

EBITDA 45.0 50.9 42.8 51.1 55.1 59.0 60.8 62.6 64.5 66.4 68.4 % of sales 23.4% 22.5% 18.0% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1%

Non-cash operating expenses (12.4) (17.1) (18.2) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.4% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%Depreciation (13.0) (17.2) (18.3) (24.7) (23.0) (22.8) (20.2) (18.5) (18.3) (18.0) (17.7) % of sales -6.7% -7.6% -7.7% -9.2% -8.0% -7.4% -6.3% -5.6% -5.4% -5.2% -4.9%

Other non-cash operating expenses 0.6 0.1 0.1 - - - - - - - - % of sales 0.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

EBITA 32.6 33.8 24.6 26.4 32.1 36.3 40.6 44.2 46.3 48.4 50.7 % of sales 16.9% 15.0% 10.3% 9.9% 11.1% 11.7% 12.8% 13.5% 13.7% 13.9% 14.2%

Net financial result (1.7) (1.3) (3.0) (6.7) (8.7) (10.0) (8.0) (6.2) (4.9) (4.0) (3.2) Interest on financial debt (3.1) (3.1) (4.1) (6.5) (7.2) (8.6) (6.6) (4.9) (3.6) (2.7) (1.8) Interest on cash - 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 Goodwill amortization (0.6) (1.1) (1.1) (1.4) (1.5) (1.5) (1.5) (1.5) (1.5) (1.5) (1.5) Other items 2.1 2.8 2.2 1.2 (0.0) - - - - - -

Exceptionals 0.3 2.2 0.0 - (0.8) - - - - - - Extraordinary profits 0.3 2.5 0.1 - 0.1 - - - - - - Extraordinary charges (0.0) (0.2) (0.1) - (0.9) - - - - - -

Profit before tax (PBT) 31.2 34.7 21.6 19.7 22.6 26.3 32.7 37.9 41.3 44.4 47.6 Taxes (5.7) (10.4) (10.6) (9.8) (4.6) (9.7) (12.0) (13.8) (15.0) (16.1) (17.2) % of PBT excluding GW amort. 17.9% 28.9% 46.7% 46.8% 19.1% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

Equity method - - - - - - - - - - - Minorities (0.3) (0.3) (0.2) (0.3) (0.5) (0.2) (0.2) (0.2) (0.2) (0.2) (0.2) Net declared profit 25.2 24.0 10.8 9.5 17.5 16.4 20.5 23.9 26.1 28.2 30.2 Net current profit (NCP) 25.5 22.9 11.9 10.9 19.8 17.9 22.0 25.4 27.6 29.7 31.7 y-o-y -10.2% -48.0% -8.6% 81.9% -9.8% 23.1% 15.6% 8.6% 7.4% 6.9%

Net current cashflow 37.9 40.0 30.1 35.6 42.9 40.6 42.2 43.9 45.9 47.7 49.4 y-o-y 5.6% -24.7% 18.2% 20.4% -5.2% 3.8% 4.1% 4.5% 3.9% 3.6%

Dividends 1.9 2.6 3.0 3.4 3.6 6.3 7.7 8.9 9.7 10.4 11.1 y-o-y 33.3% 16.7% 14.3% 5.0% 74.0% 23.1% 15.6% 8.6% 7.4% 6.9%

Pay-out in % of NCP 7.5% 11.2% 25.1% 31.4% 18.1% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%y-o-y 48.6% 124.3% 25.0% -42.3% 93.0% 0.0% 0.0% 0.0% 0.0% 0.0%

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (12/31)

|88

From Business Planning to Financial Modelling and Valuation

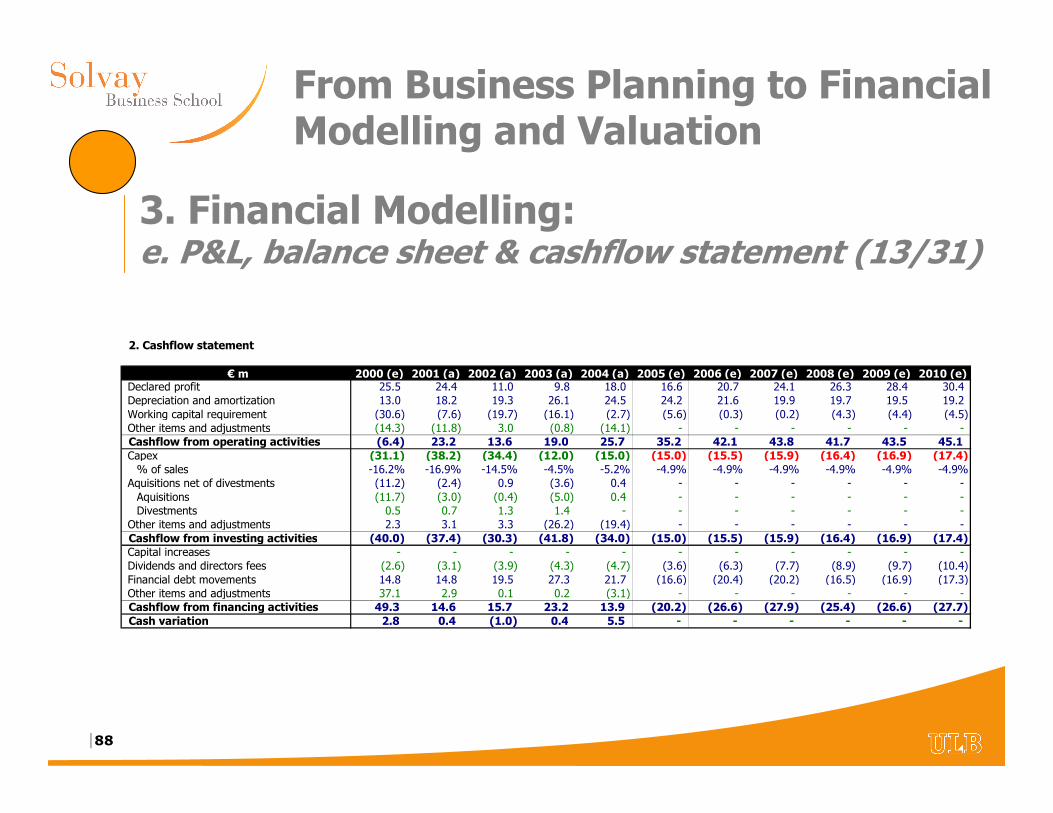

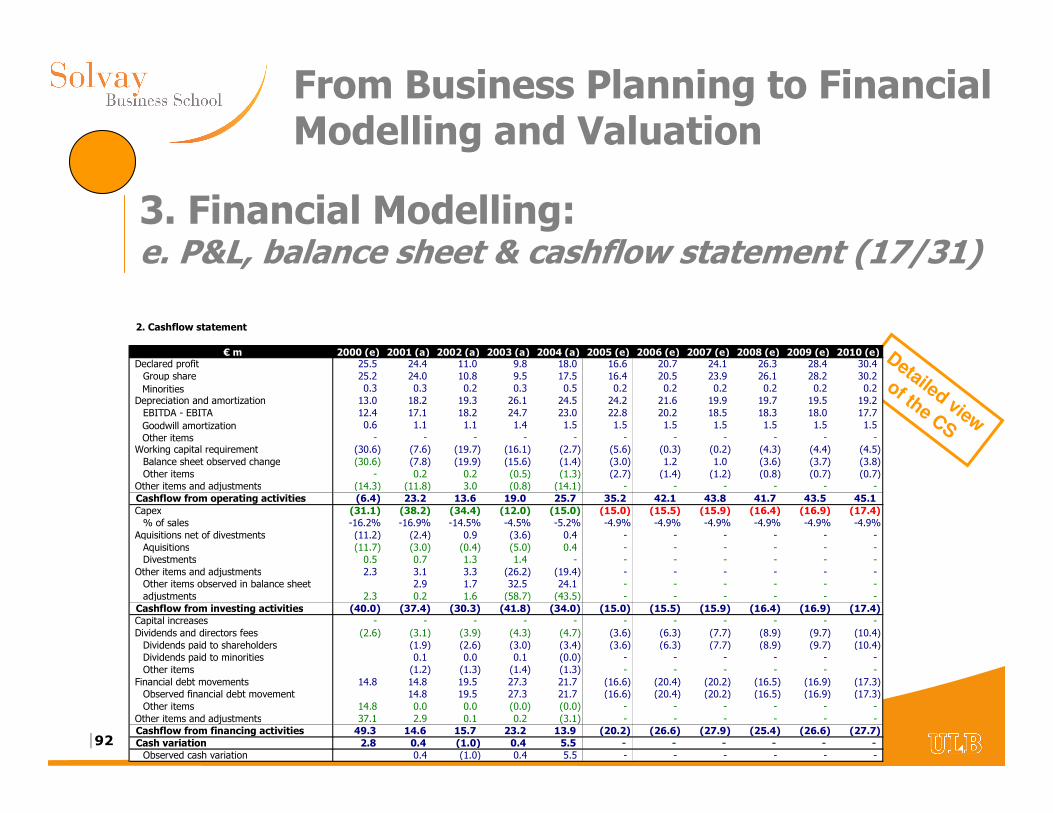

2. Cashflow statement

€ m 2000 (e) 2001 (a) 2002 (a) 2003 (a) 2004 (a) 2005 (e) 2006 (e) 2007 (e) 2008 (e) 2009 (e) 2010 (e)Declared profit 25.5 24.4 11.0 9.8 18.0 16.6 20.7 24.1 26.3 28.4 30.4 Depreciation and amortization 13.0 18.2 19.3 26.1 24.5 24.2 21.6 19.9 19.7 19.5 19.2 Working capital requirement (30.6) (7.6) (19.7) (16.1) (2.7) (5.6) (0.3) (0.2) (4.3) (4.4) (4.5) Other items and adjustments (14.3) (11.8) 3.0 (0.8) (14.1) - - - - - - Cashflow from operating activities (6.4) 23.2 13.6 19.0 25.7 35.2 42.1 43.8 41.7 43.5 45.1 Capex (31.1) (38.2) (34.4) (12.0) (15.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) % of sales -16.2% -16.9% -14.5% -4.5% -5.2% -4.9% -4.9% -4.9% -4.9% -4.9% -4.9%

Aquisitions net of divestments (11.2) (2.4) 0.9 (3.6) 0.4 - - - - - - Aquisitions (11.7) (3.0) (0.4) (5.0) 0.4 - - - - - - Divestments 0.5 0.7 1.3 1.4 - - - - - - -

Other items and adjustments 2.3 3.1 3.3 (26.2) (19.4) - - - - - - Cashflow from investing activities (40.0) (37.4) (30.3) (41.8) (34.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) Capital increases - - - - - - - - - - - Dividends and directors fees (2.6) (3.1) (3.9) (4.3) (4.7) (3.6) (6.3) (7.7) (8.9) (9.7) (10.4) Financial debt movements 14.8 14.8 19.5 27.3 21.7 (16.6) (20.4) (20.2) (16.5) (16.9) (17.3) Other items and adjustments 37.1 2.9 0.1 0.2 (3.1) - - - - - - Cashflow from financing activities 49.3 14.6 15.7 23.2 13.9 (20.2) (26.6) (27.9) (25.4) (26.6) (27.7) Cash variation 2.8 0.4 (1.0) 0.4 5.5 - - - - - -

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (13/31)

|89

From Business Planning to Financial Modelling and Valuation

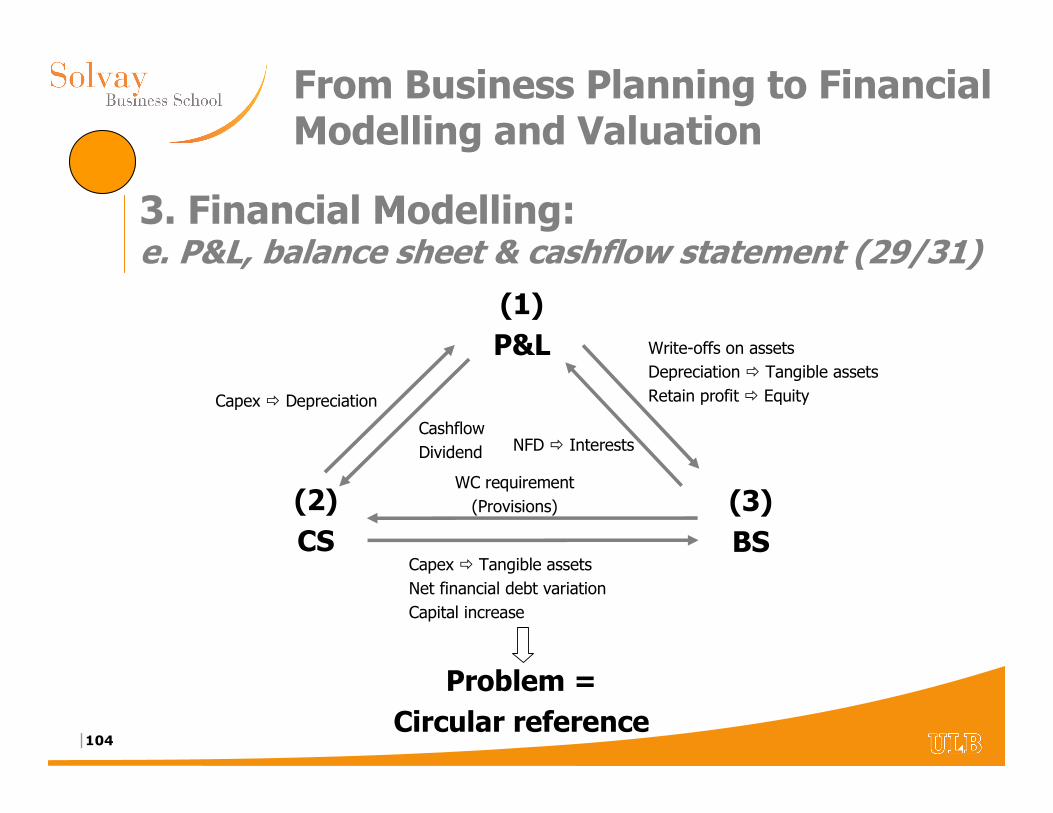

• ‘Declared profit’ and ‘Depreciation and amortization’– Derived from P&L

– Declared profit = Group share profit + Profit from minorities

• Working capital (WC) requirement– Derived from balance sheet (BS)

– WC requirement t = – (WC t – WC t-1)

– Be careful with change of perimeter (cf. acquisition and disposals)

• Other items and adjustments– Derived from historical cashflow statement for past financials

– Non-cash items due to changes in perimeter and currency impacts

– Adjustment to be considered if 100% of profit coming from equityaccounted shareholdings are received in dividend

– Prospectively = 0

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (14/31)

|90

From Business Planning to Financial Modelling and Valuation

• Capex– In an ideal world = Detailed assumptions

– Distinction between maintenance capex and expansion

– In absence of satisfactory information % of sales consistent with industrial benchmarks

• Acquisitions and disposals– Prospective data to be considered first without change of perimeter

– In a second step, test the impact associated with acquisition and disposal

• Other items and adjustments– Derived from historical cashflow statement for past financials

– Non-cash items related to change in perimeter and currency impacts

– Prospectively = 0

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (15/31)

|91

From Business Planning to Financial Modelling and Valuation

• Capital increase and dividend policy– Dividends to be considered = dividends paid to the company

shareholders and dividends paid to minorities – Assumptions to be considered carefully in the financial optimization /

value creation perspectives (cf. infra)– Fine tuning of those assumptions in other assumptions change

• Financial debt movements– Take into account reimbursement of existing credit line facilities– Automatic result (cf. equilibrium line)

• Other items and adjustments– Derived from historical cashflow statement (CFS) for past financials– Normally non-cash items related to change in perimeter and currency

impacts– Prospectively = 0

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (16/31)

|92

From Business Planning to Financial Modelling and Valuation

Detailed view

of the CS

2. Cashflow statement

€ m 2000 (e) 2001 (a) 2002 (a) 2003 (a) 2004 (a) 2005 (e) 2006 (e) 2007 (e) 2008 (e) 2009 (e) 2010 (e)Declared profit 25.5 24.4 11.0 9.8 18.0 16.6 20.7 24.1 26.3 28.4 30.4 Group share 25.2 24.0 10.8 9.5 17.5 16.4 20.5 23.9 26.1 28.2 30.2

Minorities 0.3 0.3 0.2 0.3 0.5 0.2 0.2 0.2 0.2 0.2 0.2 Depreciation and amortization 13.0 18.2 19.3 26.1 24.5 24.2 21.6 19.9 19.7 19.5 19.2 EBITDA - EBITA 12.4 17.1 18.2 24.7 23.0 22.8 20.2 18.5 18.3 18.0 17.7

Goodwill amortization 0.6 1.1 1.1 1.4 1.5 1.5 1.5 1.5 1.5 1.5 1.5

Other items - - - - - - - - - - - Working capital requirement (30.6) (7.6) (19.7) (16.1) (2.7) (5.6) (0.3) (0.2) (4.3) (4.4) (4.5) Balance sheet observed change (30.6) (7.8) (19.9) (15.6) (1.4) (3.0) 1.2 1.0 (3.6) (3.7) (3.8) Other items - 0.2 0.2 (0.5) (1.3) (2.7) (1.4) (1.2) (0.8) (0.7) (0.7)

Other items and adjustments (14.3) (11.8) 3.0 (0.8) (14.1) - - - - - - Cashflow from operating activities (6.4) 23.2 13.6 19.0 25.7 35.2 42.1 43.8 41.7 43.5 45.1 Capex (31.1) (38.2) (34.4) (12.0) (15.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) % of sales -16.2% -16.9% -14.5% -4.5% -5.2% -4.9% -4.9% -4.9% -4.9% -4.9% -4.9%

Aquisitions net of divestments (11.2) (2.4) 0.9 (3.6) 0.4 - - - - - - Aquisitions (11.7) (3.0) (0.4) (5.0) 0.4 - - - - - - Divestments 0.5 0.7 1.3 1.4 - - - - - - -

Other items and adjustments 2.3 3.1 3.3 (26.2) (19.4) - - - - - - Other items observed in balance sheet 2.9 1.7 32.5 24.1 - - - - - - adjustments 2.3 0.2 1.6 (58.7) (43.5) - - - - - -

Cashflow from investing activities (40.0) (37.4) (30.3) (41.8) (34.0) (15.0) (15.5) (15.9) (16.4) (16.9) (17.4) Capital increases - - - - - - - - - - - Dividends and directors fees (2.6) (3.1) (3.9) (4.3) (4.7) (3.6) (6.3) (7.7) (8.9) (9.7) (10.4) Dividends paid to shareholders (1.9) (2.6) (3.0) (3.4) (3.6) (6.3) (7.7) (8.9) (9.7) (10.4) Dividends paid to minorities 0.1 0.0 0.1 (0.0) - - - - - - Other items (1.2) (1.3) (1.4) (1.3) - - - - - -

Financial debt movements 14.8 14.8 19.5 27.3 21.7 (16.6) (20.4) (20.2) (16.5) (16.9) (17.3) Observed financial debt movement 14.8 19.5 27.3 21.7 (16.6) (20.4) (20.2) (16.5) (16.9) (17.3) Other items 14.8 0.0 0.0 (0.0) (0.0) - - - - - -

Other items and adjustments 37.1 2.9 0.1 0.2 (3.1) - - - - - - Cashflow from financing activities 49.3 14.6 15.7 23.2 13.9 (20.2) (26.6) (27.9) (25.4) (26.6) (27.7) Cash variation 2.8 0.4 (1.0) 0.4 5.5 - - - - - - Observed cash variation 0.4 (1.0) 0.4 5.5 - - - - - -

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (17/31)

|93

From Business Planning to Financial Modelling and Valuation

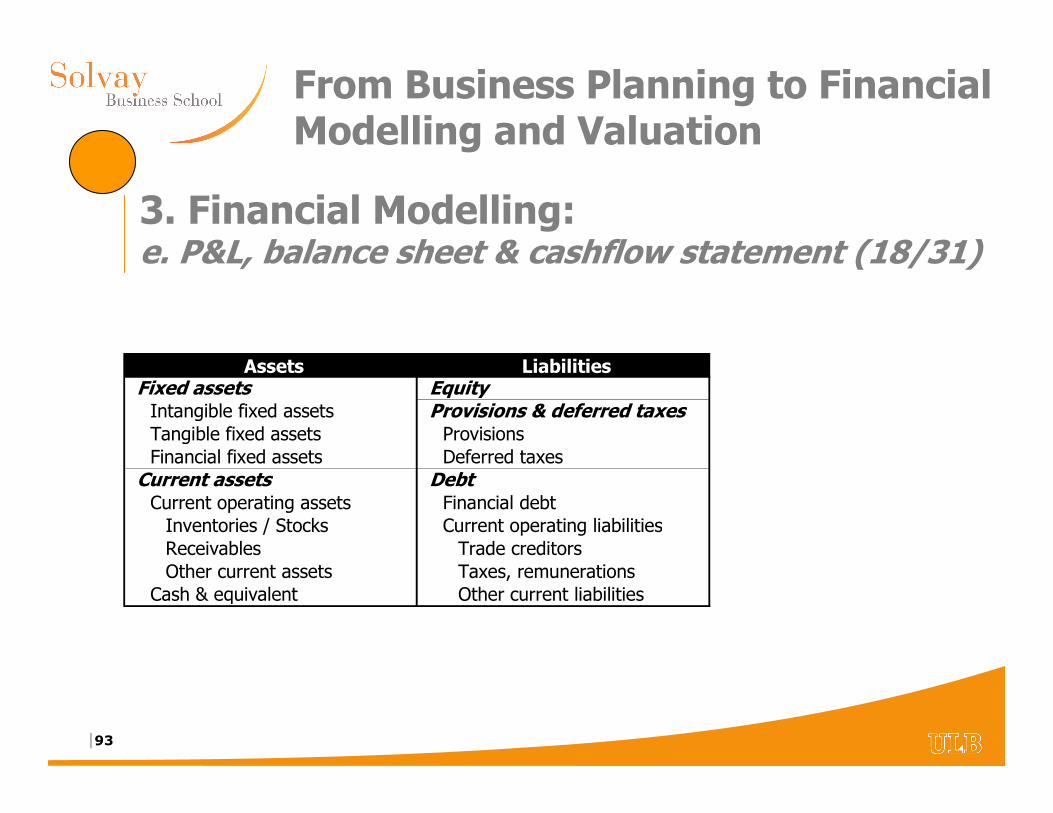

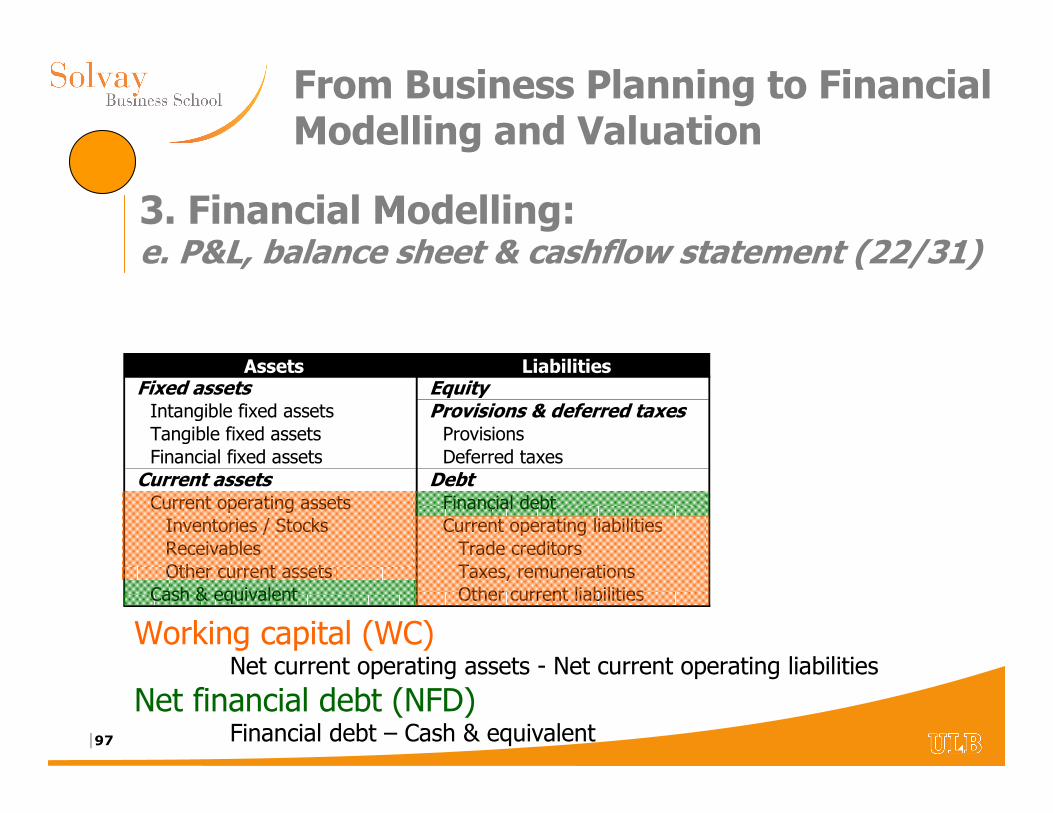

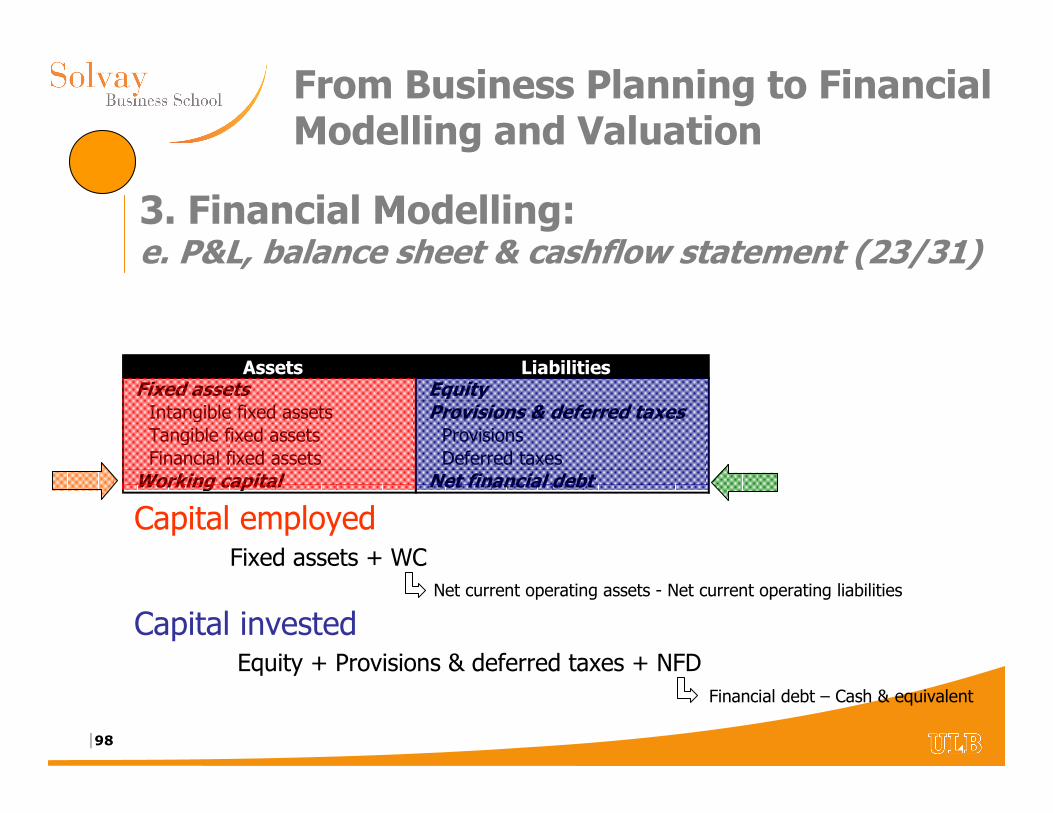

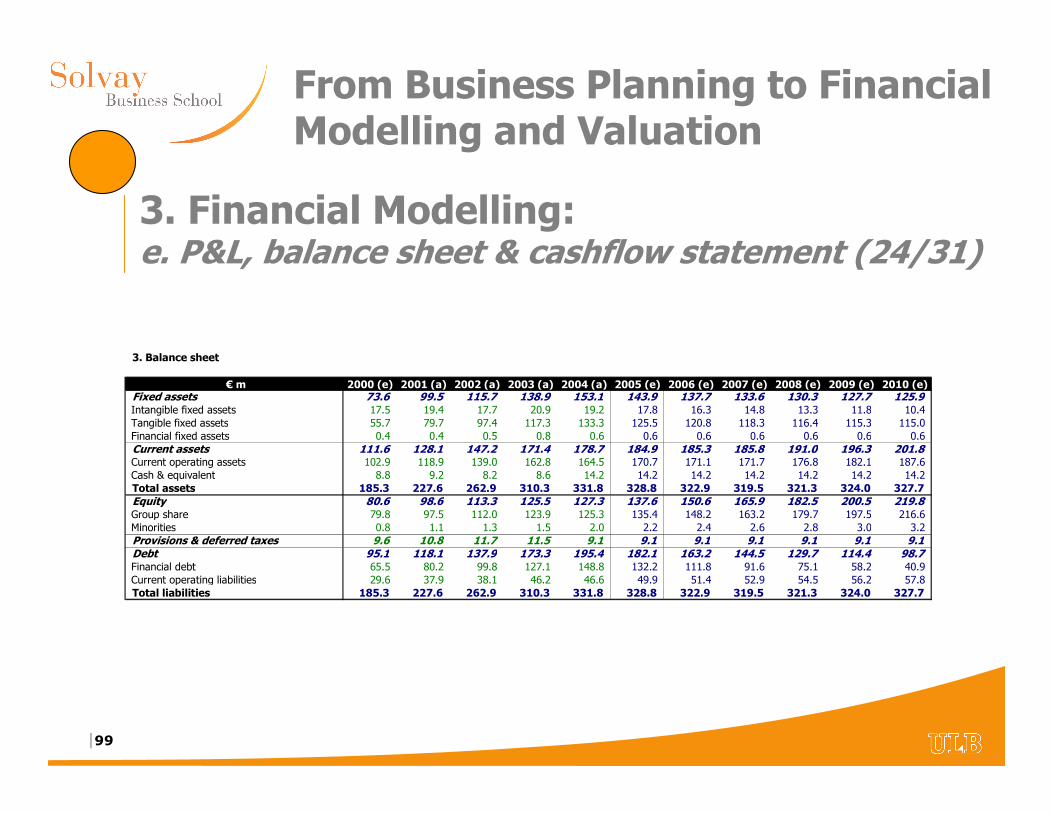

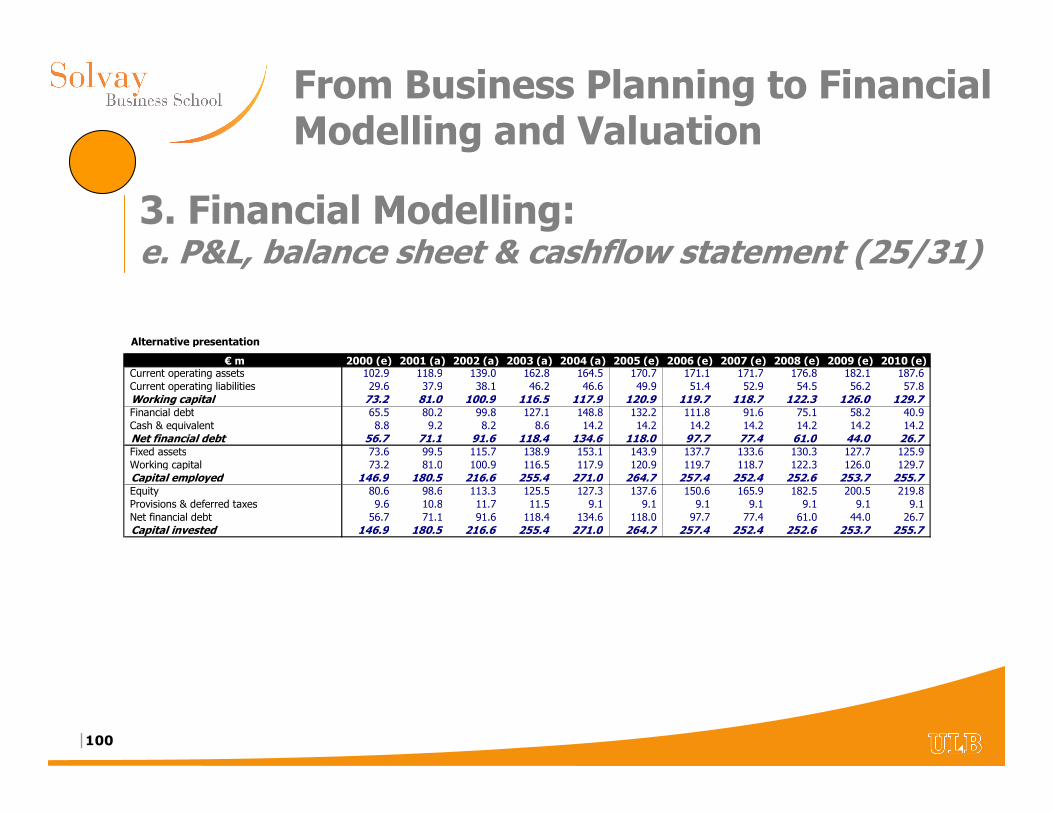

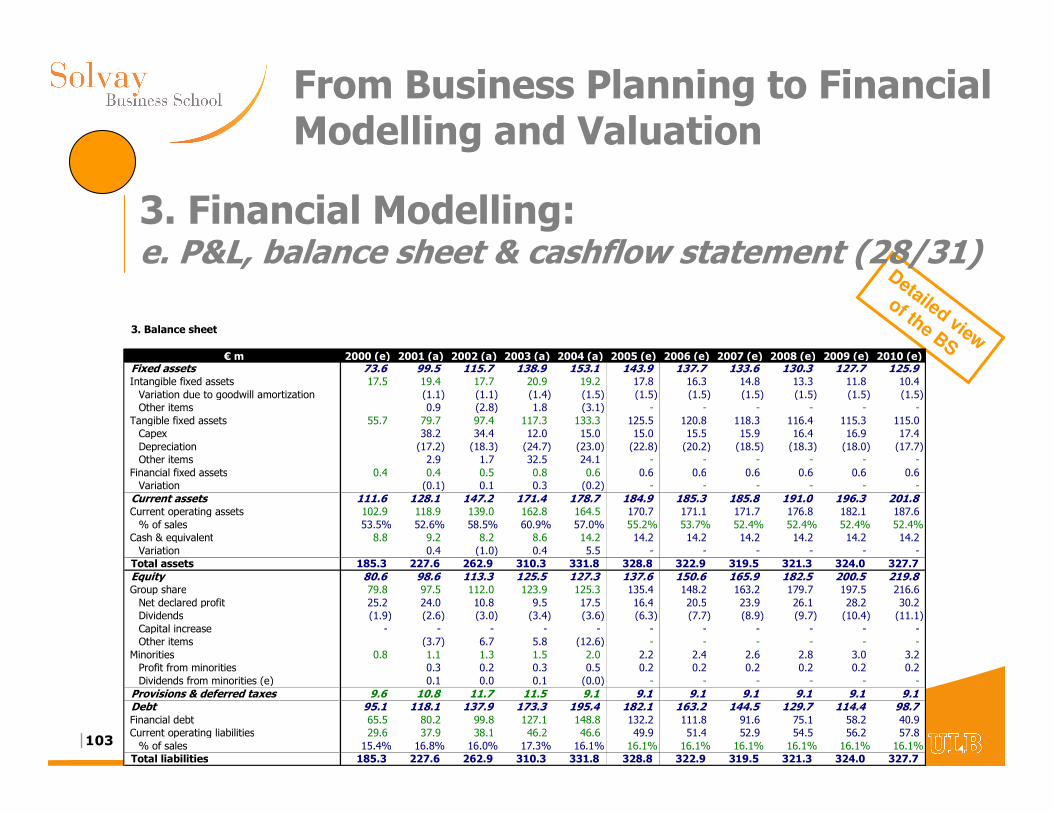

Assets Liabilities Fixed assets EquityIntangible fixed assets Provisions & deferred taxesTangible fixed assets ProvisionsFinancial fixed assets Deferred taxes

Current assets DebtCurrent operating assets Financial debtInventories / Stocks Current operating liabilitiesReceivables Trade creditorsOther current assets Taxes, remunerations

Cash & equivalent Other current liabilities

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (18/31)

|94

From Business Planning to Financial Modelling and Valuation

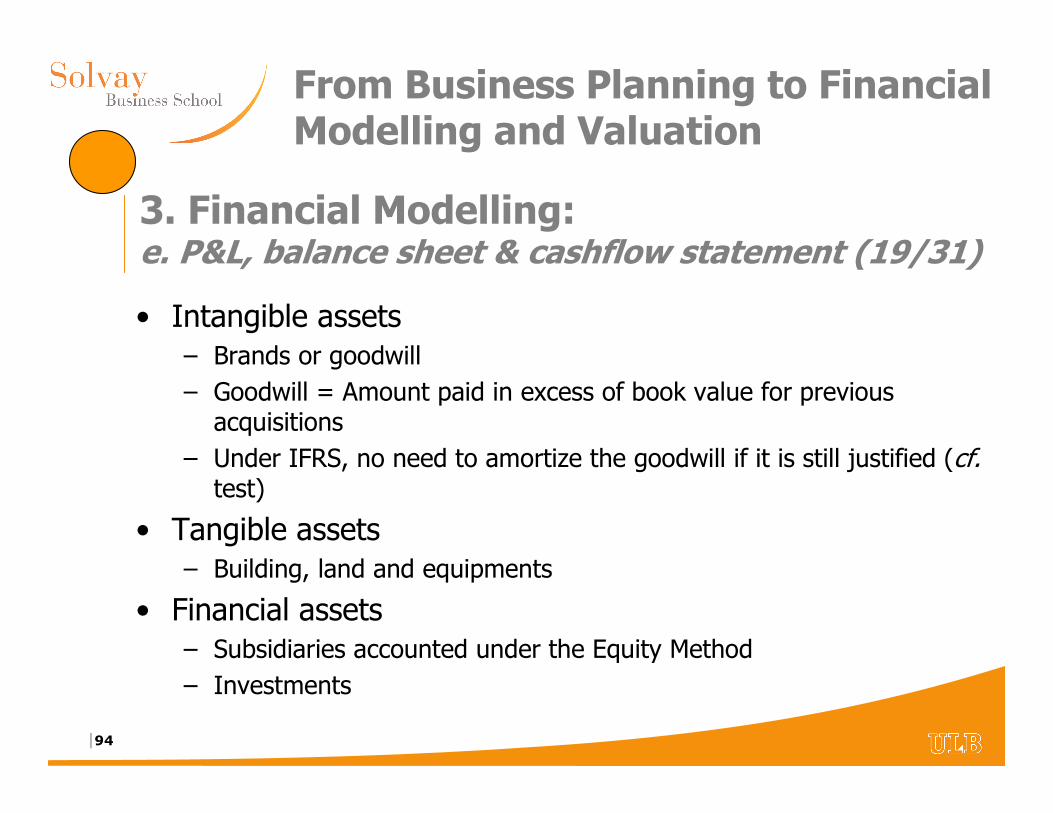

• Intangible assets– Brands or goodwill

– Goodwill = Amount paid in excess of book value for previous acquisitions

– Under IFRS, no need to amortize the goodwill if it is still justified (cf.test)

• Tangible assets– Building, land and equipments

• Financial assets– Subsidiaries accounted under the Equity Method

– Investments

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (19/31)

|95

From Business Planning to Financial Modelling and Valuation

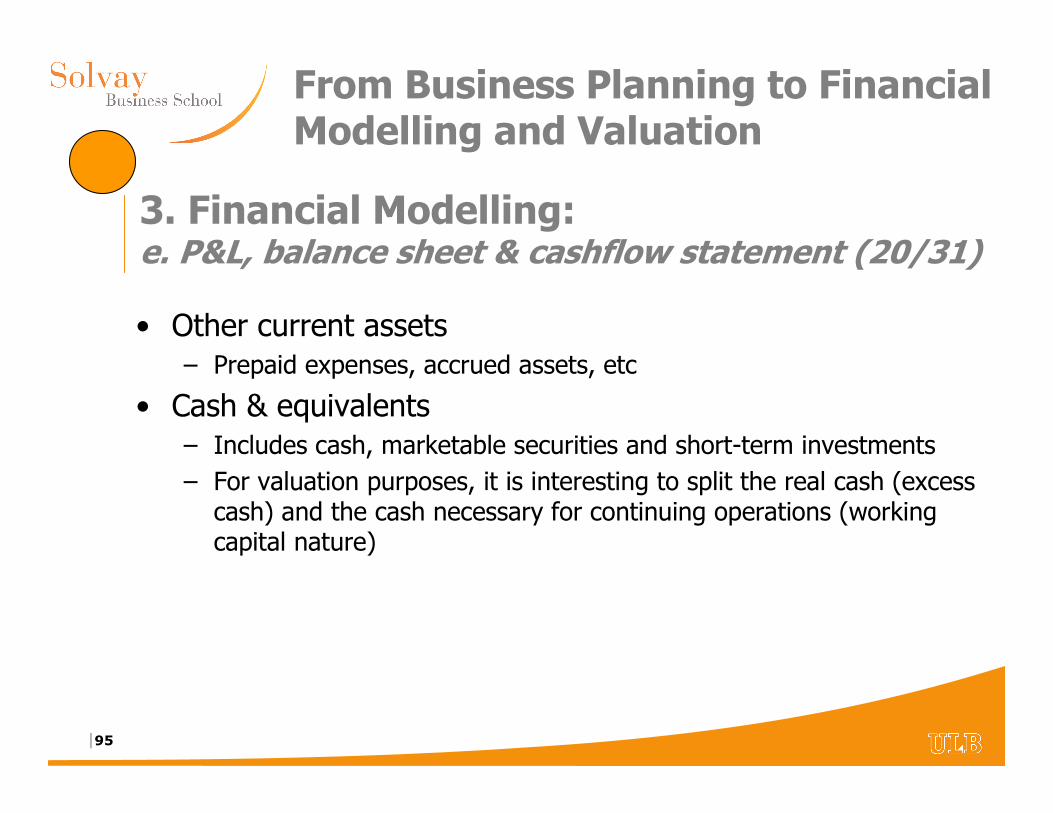

• Other current assets– Prepaid expenses, accrued assets, etc

• Cash & equivalents– Includes cash, marketable securities and short-term investments

– For valuation purposes, it is interesting to split the real cash (excess cash) and the cash necessary for continuing operations (working capital nature)

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (20/31)

|96

From Business Planning to Financial Modelling and Valuation

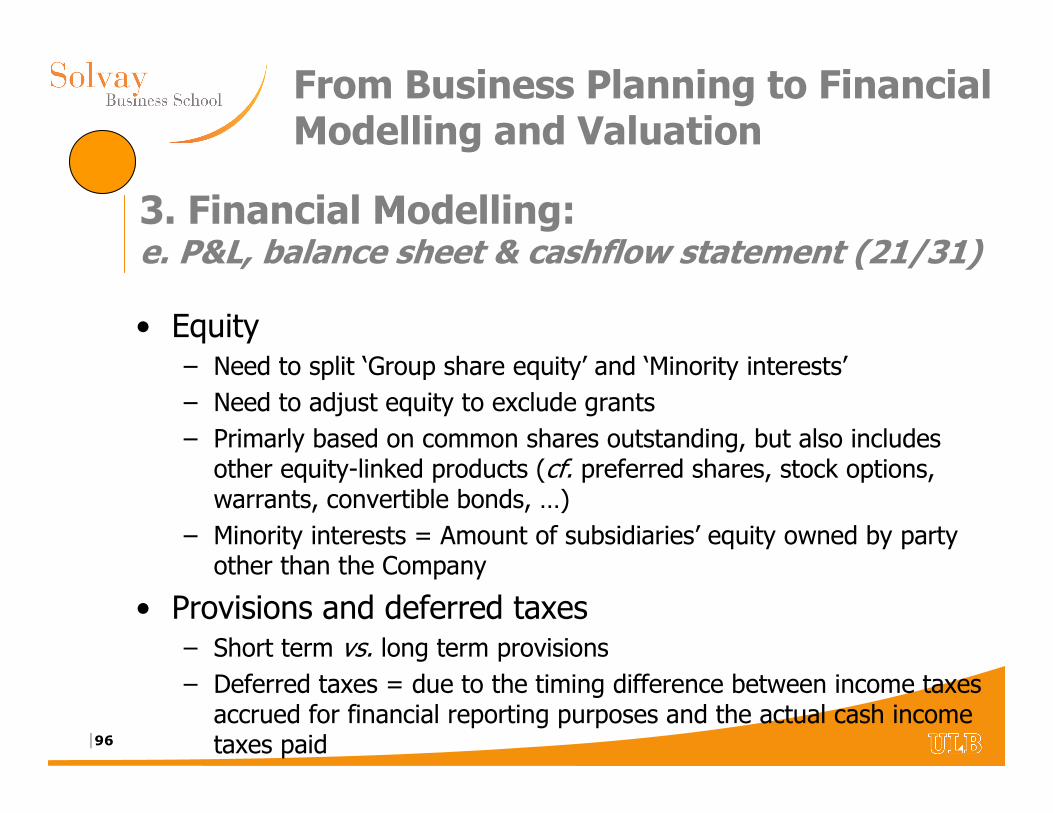

• Equity– Need to split ‘Group share equity’ and ‘Minority interests’

– Need to adjust equity to exclude grants

– Primarly based on common shares outstanding, but also includes other equity-linked products (cf. preferred shares, stock options, warrants, convertible bonds, …)

– Minority interests = Amount of subsidiaries’ equity owned by party other than the Company

• Provisions and deferred taxes– Short term vs. long term provisions

– Deferred taxes = due to the timing difference between income taxes accrued for financial reporting purposes and the actual cash income taxes paid

3. Financial Modelling:e. P&L, balance sheet & cashflow statement (21/31)

|97