Embed Size (px)

Citation preview

FRENCH COMMERCIAL REAL ESTATE CURRENT MARKET AND OUTLOOK

22TH APRIL 2015

1. OFFICE MARKETS IN ILE DE FRANCE

3

STOCK: ZOOM ON PARIS ET INNER SUBURDS

Paris Centre West 8.6 M sq m

Rest of Paris 8.1 M sq m

Total Paris 16.7 M sq m

La Défense 3.3 M sq m

Western Crescent 8.7 M sq m

Inner Rim 6.4 M sq m

Total Paris + Inner Rim

+ Western Crescent

+ La Défense

35.2 M sq m

Total Ile-de-France 55.5 M sq m

Source : ORIE / CBRE

4

OFFICE MARKET DYNAMICS IN PARIS REGION

5

TAKE UP Q1 2015 – PARIS REGION

,500,000 sq m

1,000,000 sq m

1,500,000 sq m

2,000,000 sq m

2,500,000 sq m

3,000,000 sq m

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Q1 Q2 Q3 Q4

Q1 2014 : 508,900 sq m - 662 deals

Q1 2015 : 372,500 sq m - 665 deals

Source : CBRE / Immostat / ORIE

6

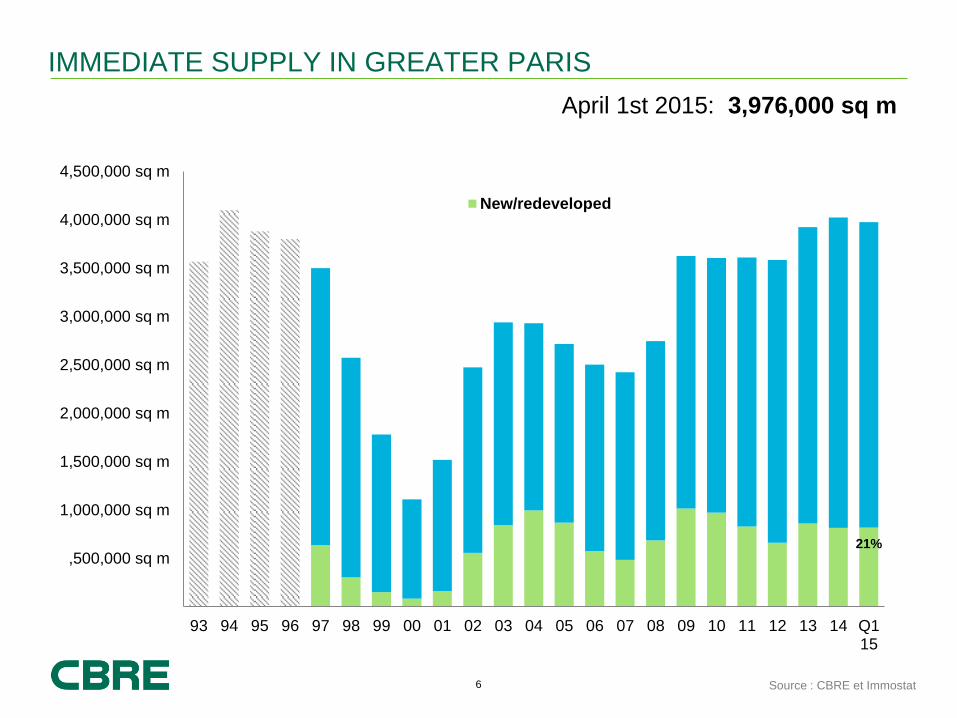

IMMEDIATE SUPPLY IN GREATER PARIS

21% ,500,000 sq m

1,000,000 sq m

1,500,000 sq m

2,000,000 sq m

2,500,000 sq m

3,000,000 sq m

3,500,000 sq m

4,000,000 sq m

4,500,000 sq m

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 Q115

New/redeveloped

April 1st 2015: 3,976,000 sq m

Source : CBRE et Immostat

7

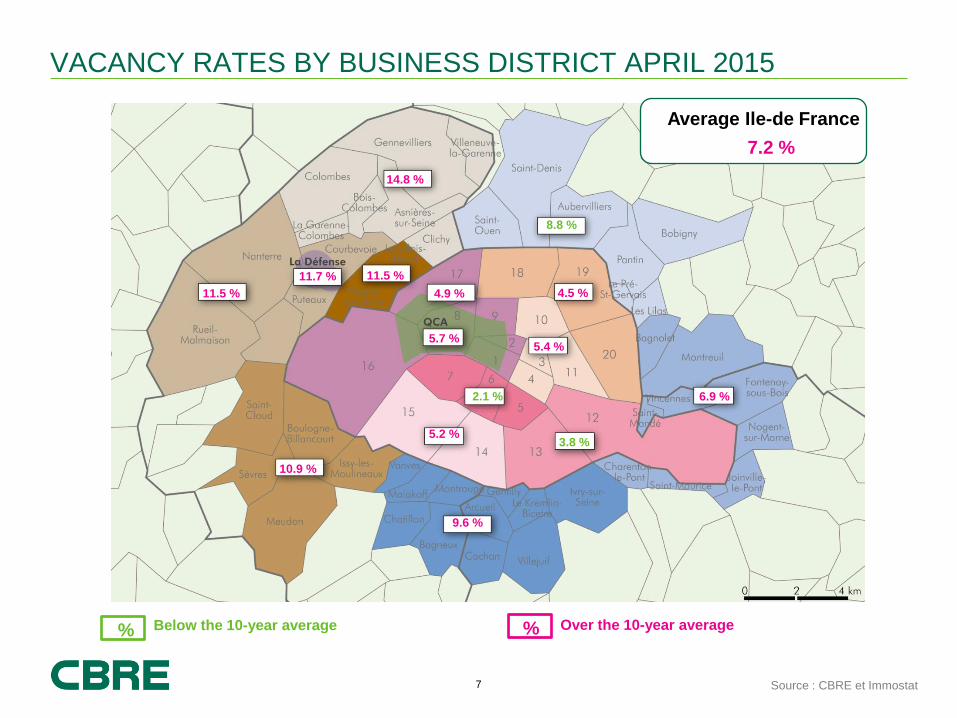

5.2 %

5.7 %

9.6 %

10.9 %

11.5 %

11.7 %

14.8 %

3.8 %

% Below the 10-year average Over the 10-year average

%

Average Ile-de France

7.2 %

8.8 %

4.5 %

5.4 %

6.9 % 2.1 %

4.9 %

11.5 %

VACANCY RATES BY BUSINESS DISTRICT APRIL 2015

Source : CBRE et Immostat

8

TRENDS IN AVERAGE PRIME RENTS

549 503

762

691

625

698 750

716

664

734 771 707

687

695

305

432

455 486

478

401

502

441 442

498 495

351

457

610

497

430 456

422

462

430 438

459 456

248

239

360

297 300

316

298 301

297 296 297

0

100

200

300

400

500

600

700

800

900

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 Q115

Paris CBD La Défense

Western Crescent Average weighted Ile-de-France

Methodological note: before 2001, average prime rents correspond to the highest transaction value registered on top-of-the-range buildings, except atypical transaction.

Since 2001, prime rents correspond to the weighted average of the 10 highest transactions in terms of rental values, registered during the 6 preceding months and concerning surfaces

over or equal to 500 sq m

HEADLINE RENTAL VALUES IN CURRENT € NET/SQ. M PA, AT PERIOD END

Source : CBRE

2. INVESTMENT MARKET

10

€0 bn

€5 bn

€10 bn

€15 bn

€20 bn

€25 bn

€30 bn

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Q1 Q2

FRANCE - COMMERCIAL REAL ESTATE VOLUMES INVESTED

Ma

rch

é d

e l’In

ve

stisse

me

nt e

n F

ran

ce

Sources : CBRE et Immostat

2014: €24.1 B

Q1 2014: €4.0 B / Q1 2015: €4.3 B

+10% YoY

11

DEAL SIZE

Q1 2014

Sources : CBRE et Immostat

38 opérations

18 opérations

21 opérations

250 opérations

Q1 2015

Average deal size Q1 2014: €230.3 M / Nb of transactions: 131 Average deal size Q1 2015: €53.1 M / Nb of transactions : 82

+10% in volume/ - 37 % in nb of transactions YoY

€100 -200 M€

96 deals 15.6%

21 deals 17.1%

6 deals 10.7%

6 deals 18.8%

2 deals 37.8%

> €200 M

46 deals 8.4%

14 deals 9.8%

9 deals 16.2%

5 deals 15.7%

8 deals 49.9%

€25–50 M €50-100 M < €25 M

12

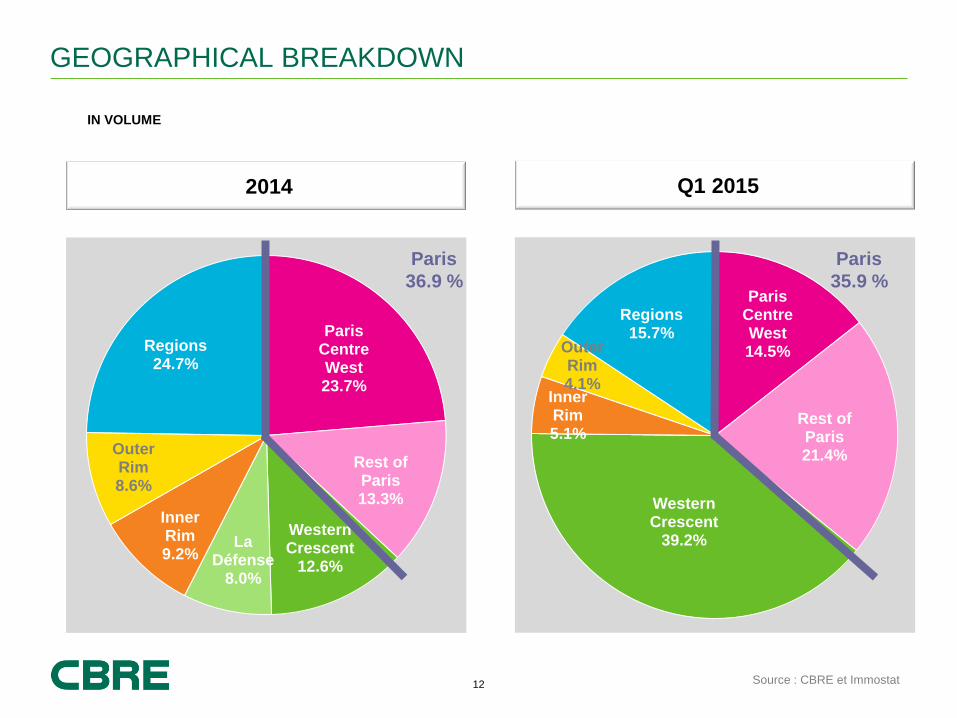

GEOGRAPHICAL BREAKDOWN

Paris Centre West 23.7%

Rest of Paris 13.3%

Western Crescent

12.6%

La Défense

8.0%

Inner Rim 9.2%

Outer Rim 8.6%

Regions 24.7%

Source : CBRE et Immostat

Q1 2015 2014

Paris

36.9 % Paris

Centre West 14.5%

Rest of Paris 21.4%

Western Crescent

39.2%

Inner Rim 5.1%

Outer Rim 4.1%

Regions 15.7%

Paris

35.9 %

IN VOLUME

13

TYPE OF PRODUCTS

Q1 2015 2014

Source: CBRE et Immostat

76.6%

2.9%

20.5%

65.6% 7.6%

26.8%

VOLUME (EXCLUDING MULTI-PURPOSE AND MULTI-ASSET PORTFOLIOS)

Industrial / logistics Retail Offices

14

2,000 sq m

4,000 sq m

6,000 sq m

8,000 sq m

10,000 sq m

12,000 sq m

14,000 sq m

16,000 sq m

18,000 sq m

20,000 sq m

22,000 sq m

05 06 07 08 09 10 11 12 13 14 Q1 2015

Av. des Champs Elysées Avenue Montaigne

Rue St Honoré Rue de Rennes/bd St Germain (Rive Gauche)

Rue des Francs Bourgeois (Le Marais)

TREND IN PRIME RENTS ON THE MAIN SHOPPING STREETS IN PARIS

+ 130%

+ 275%

+ 78%

+ 140%

Change 2005-Q1 2015

+ 203%

(ITZA IN € NET/SQ M PA)

15

RETAIL INVESTMENT VOLUMES

0%

5%

10%

15%

20%

25%

30%

€0 bn

€1 bn

€2 bn

€3 bn

€4 bn

€5 bn

€6 bn

€7 bn

03 04 05 06 07 08 09 10 11 12 13 14 Q1 15

French Investment

Foreign investment

Share of retail in Frenchdirect RE investments

Sources : CBRE et Immostat

16

FRANCE LOGISTIC TAKE UP ET RENTAL VALUES

,500,000 sq m

1,000,000 sq m

1,500,000 sq m

2,000,000 sq m

2,500,000 sq m

3,000,000 sq m

08 09 10 11 12 13 14 15

Q1 Q2 Q3 Q4

Annual average:

2,526,900 sq m

* Nord-Pas de Calais, Ile-de-France, Rhône-Alpes, PACA regions

Sources: CBRE et Immostat

714,400 sq m

+44%

1Q1 2015: 714,400 sq m

81% located on the North-South route*

Headline rents A Class

€30 / €60 net/sq m pa

17

Sources : CBRE et Immostat

LOGISTICS/INDUSTRIAL INVESTMENT VOLUMES

€0 bn

€1 bn

€2 bn

€3 bn

€4 bn

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1T 2015

Industrial spaces Logistics

18

BREAKDOWN BY STRATEGY

TRANSACTIONS > €50 M, IN VOLUME

Source : CBRE et Immostat

Q1 2015 2014

66.6%

26.2%

7.2%

67.8%

16.3%

15.9%

« Core + » « Value added / opportunistic» « Core »

19

BREAKDOWN BY NATIONALITY

0%

10%

20%

30%

40%

50%

60%

70%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q12015

Source : CBRE

IN VOLUME

French 44,3%

Middle East 11.3%

German 7.4%

North-American 18.4%

British 4.0 % Asian 5.4%

20

COMPARED CHANGE IN YIELDS

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 Q115

Prime office yields* Paris CBD

OAT TEC 10

Euribor 3 months

3,75 %

0,02%

0,46 %

Negative real risk premium

Explosion of financing costs

Real estate risk

premium above

Floor to financing costs

Sources : CBRE, Banque de France - Comité de normalisation

obligataire

• Well located, leased in line with general market practice

As references do not systematically exist for each category, some

values are estimates provided by market specialists

(Capital Markets, Valuation, Research)

21

PRIME* YIELDS

Q1 2014 Q1 2015 Outlook

PARIS CBD Offices 4.15 % - 4.75 % 3.75 % - 4.25 %

La Defense Offices 5.90 % - 7.00 % 5.25 % - 6.50 %

Regions Offices 5.70 % - 8.00 % 5.40 % - 8.00 %

Logistics classe A 7.00 % - 8.00 % 6.75 % - 8.00 %

Light industrial 8.25 % - 12.00 % 8.00 % - 12.00 % =

Industrial Parks 8.00 % - 10.00 % 7.50 % - 10.00 % =

Regional Shopping

Centres 4.50 % - 7.75 % 4.00 % - 6.25 % =

City centre retail – top

locations 3.90 % - 6.75 % 3.00 % - 6.00%

Retail Parks 5.50 % - 9.50 % 5.25 % - 9.25 % =

* Well located, leased in line with general market practice

As references do not systematically exist for each category, some values are estimates

provided by market specialists (Capital Markets, Valuation, Research)

Source : CBRE

22

€,0 M

€,200 M

€,400 M

€,600 M

€,800 M

€1,000 M

€1,200 M

€1,400 M

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Marseille Toulouse Lille Lyon

REGIONS – OFFICE INVESTMENT VOLUMES

Ma

rch

é d

e l’In

ve

stisse

me

nt e

n F

ran

ce

Sources : CBRE et Immostat

23

100,000 sq m

200,000 sq m

300,000 sq m

400,000 sq m

500,000 sq m

600,000 sq m

700,000 sq m

800,000 sq m

900,000 sq m

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Marseille Toulouse Lille Lyon

REGIONS – OFFICE TAKE UP

Ma

rch

é d

e l’In

ve

stisse

me

nt e

n F

ran

ce

Sources : CBRE et Immostat

24

5.50%

5.40%

5.75%

6.00%

4%

5%

6%

7%

8%

9%

10%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q12015

Lyon Lille Marseille Toulouse

PRIME* OFFICE YIELDS IN REGIONS

Sources: CBRE, Banque de France - Comité de

normalisation obligataire

AT PERIOD END

* Well located, leased in line with general market practice

As references do not systematically exist for each category, some

values are estimates provided by market specialists (Capital Markets,

Valuation, Research)

T +33 (0)1 53 64 34 88

F +33 (0)1 53 64 40 00

For more information regarding this presentation please contact: AURELIE LEMOINE

Head of Research

www.cbre.fr

@CBREFrance