Embed Size (px)

Citation preview

Annex 1

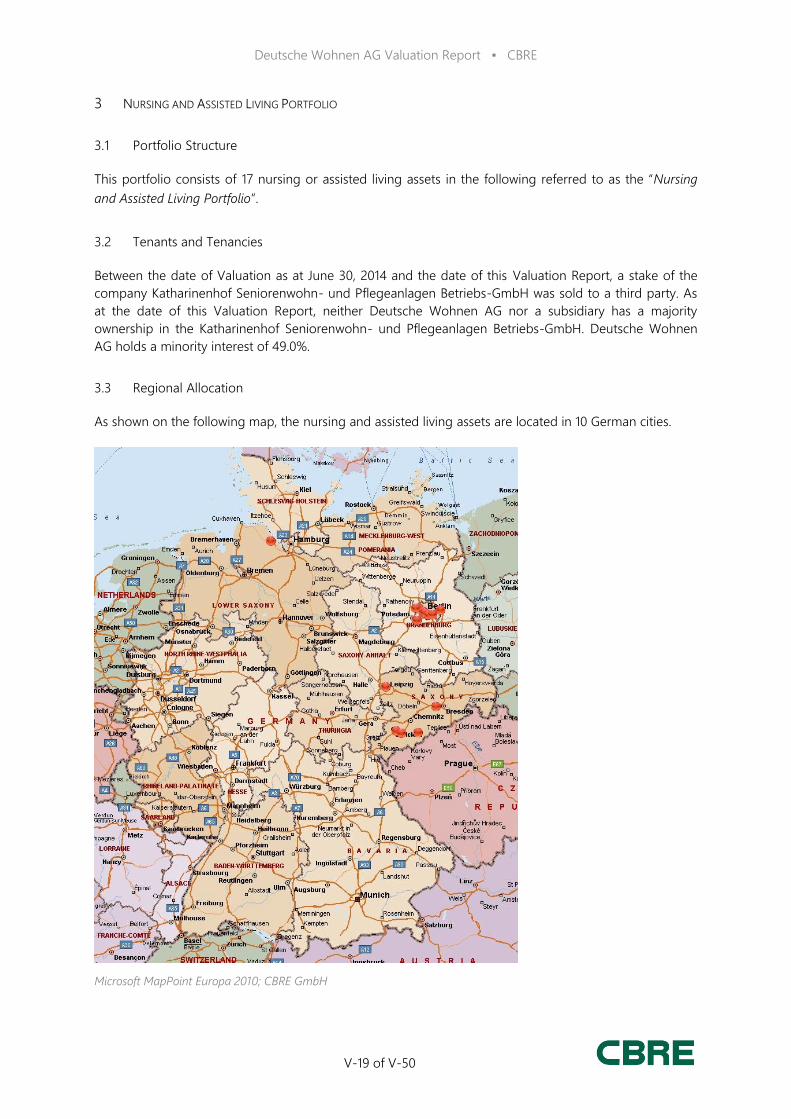

To the Invitation to the Extraordinary General Meeting

on Wednesday, 28 October, 2015 at 10 A.M. (CET)

Deutsche Wohnen AG

Frankfurt am Main, Germany

ISIN DE000A0HN5C6

WKN A0HN5C

Report of the Management Board pursuant to section 186, para. 4, sentence 2 of the German

Stock Corporation Act (“AktG”) on agenda item 1 for the Extraordinary General Meeting to be

held on Wednesday, 28 October 2015 regarding the reason for the exclusion of shareholders’

subscription rights

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 2 -

I.

The management board (the „Management Board“) and the supervisory board (the „Supervisory

Board“) of Deutsche Wohnen AG, with its registered office in Frankfurt am Main, Germany

(“Deutsche Wohnen AG” or the “Company”), propose the following to the general meeting

(“General Meeting”):

Increase of the Company’s Share Capital against Contributions in kind with the

Exclusion of the Shareholders’ Subscription Rights and Authorization for the

Amendment of the Articles of Association

II.

The individual proposed resolution is as follows:

Increase of the Company’s Share Capital against Contributions in kind with the

Exclusion of the Shareholders’ Subscription Rights and Authorization for the

Amendment of the Articles of Association

1. The Company’s current share capital, which is currently registered with the

commercial register (Handelsregister) as EUR 336,426,511.00, divided into

336,426,511 ordinary bearer shares with no par value, each with a notional

value of EUR 1.00, will be increased by up to EUR 213,127,385.00 to up to

EUR 549,553,896.00 through the issuance of up to 213,127,385 ordinary

bearer shares with no par value (Stückaktien), each with a notional value of

EUR 1.00 (the “New Shares”), against contributions in kind.

The issue amount (Ausgabebetrag) of the New Shares is EUR 1.00. The

difference between the issue amount (Ausgabebetrag) of the New Shares and

the contribution value (Einbringungswert) of the contributions in kind shall be

allocated to the capital reserve pursuant to section 272, para. 2, no. 4 of the

German Commercial Code (the “HGB”).

2. The New Shares carry full dividend rights as of 1 January 2015.

3. The subscription rights of the shareholders of Deutsche Wohnen AG are

excluded. The shares resulting from the capital increase against contributions

in kind will be issued in connection with a takeover offer to the shareholders

of LEG Immobilien AG pursuant to sections 29 et seq. of the German

Securities Acquisition and Takeover Act (the “WpÜG”) by way of the

Exchange Offer for the purchase of all shares held by the shareholders of LEG

Immobilien AG at a ratio of 1:3.30. Each shareholder of LEG Immobilien AG

is therefore entitled to receive 3.30 New Shares in exchange for each tendered

LEG Share.

4. UBS Deutschland AG, Opernturm, Bockenheimer Landstraße 2-4, 60306

Frankfurt am Main, Germany, and DZ Bank AG Deutsche Zentral-

Genossenschaftsbank, Frankfurt am Main, Platz der Republik, 60265

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 3 -

Frankfurt am Main, Germany, will, in general, each subscribe for half of the

New Shares in their capacity as Exchange Trustees (Umtauschtreuhänder) for

the shareholders of LEG Immobilien AG that have accepted the Exchange

Offer. Accordingly, the Exchange Trustees are hereby permitted to subscribe

for the New Shares and will contribute the LEG Shares tendered for the

exchange, as far as they are subject to the capital increase against

contributions in kind, as contributor in kind (Sacheinleger) in Deutsche

Wohnen AG.

5. The capital increase against contributions in kind shall only be implemented to

the extent to which the New Shares have been subscribed for by the Exchange

Trustees by the deadline stipulated in no. 9.

6. The Management Board intends to refrain from an appraisal of the

contributions in kind (section 183, para. 3 of the German Stock Corporation

Act (the “AktG”)) pursuant to sections 183a, 33a of the AktG.

7. The Management Board is authorized to determine further details regarding

the implementation of the capital increase against contributions in kind.

8. The Supervisory Board is authorized to amend the articles of association

according to the implementation of the capital increase against contributions in

kind.

9. The resolution concerning the increase of the share capital against

contributions in kind will become null and void if the completion of the capital

increase has not been filed for entry in the commercial register

(Handelsregister) within three months following the entry of this resolution in

the commercial register (Handelsregister), and in any event no later than

16 May 2016. The Management Board and the chairman of the Supervisory

Board are instructed to file for the entry of the resolution concerning the

increase of the share capital against contributions in kind in the commercial

register (Handelsregister) without undue delay once the requirements for its

registration have been met (in particular, in the event of pending rescission

actions (Anfechtungsklagen) upon the conclusion of a release procedure

(Freigabeverfahren) pursuant to section 246a of the AktG).

The Management Board is authorized to file for the entry of the resolution in the

commercial register (Handelsregister) as soon as the conditions of the resolution have

been met.

The base amount (Ausgangsbetrag) for the capital increase which is described in the

proposed resolution is based on the amount of share capital currently registered with the

commercial register (Handelsregister). Since 1 January 2015, additional shares of the

Company from conditional capital have been issued to former shareholders of GSW

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 4 -

Immobilien AG who have exerted their right to compensation based on the domination

agreement concluded between the Company and GSW Immobilien AG. It is possible that

other shareholders of GSW Immobilien AG may exert their right to compensation until the

resolution regarding the capital increase is proposed or the capital increase is implemented.

The corresponding increases out of the conditional capital have not yet been registered with

the commercial register (Handelsregister).

III.

The Management Board of Deutsche Wohnen intends to acquire an interest in LEG by means of an

Exchange Offer and to subsequently integrate LEG into the Deutsche Wohnen Group.

Today, the Management Board has concluded a Business Combination Agreement

(Grundsatzvereinbarung) with LEG with respect to the public takeover offer and the future strategy

and structure of the newly created company group (see III.2.e) below).

In the context of the Exchange Offer, shares of Deutsche Wohnen shall be offered to the shareholders

of LEG. The shares of Deutsche Wohnen shall be issued by means of the proposed capital increase

against contributions in kind and – depending on the number of tendered LEG Shares – possibly also

by means of a capital increase from authorized capital. Because the shares issued by means of the

capital increases shall be offered in exchange for LEG Shares, the subscription rights of the

shareholders of Deutsche Wohnen will be excluded for the proposed capital increase against

contributions in kind.

Hereinafter, the Management Board reports on the reason for the exclusion of subscription rights for

the proposed capital increase against contributions in kind pursuant to section 186, para. 4, sentence 2

of the AktG. This report first describes the background of the planned transaction and the planned

transaction itself in this section III. In particular, this involves the description of Deutsche Wohnen

and LEG, the market environment and the business conditions of the transaction, the expected

synergies resulting from the transaction and an explanation of the valuation of the companies involved

in the transaction.

In section IV., the objective justification for the exclusion of subscription rights in the context of the

capital increase against contributions in kind will be given with regard to the purpose of the capital

measure.

1. Background of the Planned Transaction

a) Deutsche Wohnen

(1) Business activities

Deutsche Wohnen, with its registered office in Frankfurt am Main and its

principal place of business in Berlin, is currently one of the largest publicly

listed real estate stock companies in Germany, based on market capitalization.

The Company is active in residential property management, especially in

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 5 -

letting residential units owned by the Company, management of its residential

portfolio and the sale of select residential properties. Through one of its

participations in another company, it also operates nursing homes and assisted

living facilities. In the context of this business strategy, Deutsche Wohnen

focuses on residential and nursing care real estate properties in high-growth

metropolitan regions in Germany. These include the greater Berlin area, the

Rhine-Main region, Mannheim/Ludwigshafen, the Rhineland and Dresden.

Other important areas include stable urban regions such as Hanover/Brunswick,

Magdeburg, Kiel/Lübeck, Halle/Leipzig and Erfurt. Deutsche Wohnen is listed

in Deutsche Börse’s MDAX Index.

(2) Segments

Deutsche Wohnenʼs business is divided into “Residential Property

Management”, “Sales” and “Nursing and Assisted Living Homes” segments.

The “Residential Property Management” segment is the core and focus of its

business, covering all activities in connection with the management and

administration of residential properties, management of lease contracts and

services for tenants. The “Sales” segment covers all activities relating to the

sale of residential units, buildings and land. Deutsche Wohnen AG’s

residential portfolio earmarked for sale is subdivided into block sales

(institutional sales) and single-unit privatization (residential property

privatization). The residential portfolio for block sales mainly includes

residential units in the so-called non-core regions that are not part of the

business strategy of Deutsche Wohnen as well as opportunistic sales. In

connection with single-unit privatizations, Deutsche Wohnen mainly seeks to

sell residential units to owner-occupants and investors. In its “Nursing and

Assisted Living Homes” segment Deutsche Wohnen predominantly manages

and markets its own nursing and residential properties for senior citizens

through one of ist participations in another company under the brand

KATHARINENHOF®.

(3) Portfolio

As of 30 June 2015, Deutsche Wohnen’s residential property portfolio

comprised 141,943 residential units with a total residential floor space of

approximately 8.6 million square metres, based on the total residential floor

space listed in the rental contracts. As of 30 June 2015, the average monthly

contractual rent, based on Deutsche Wohnen’s total residential portfolio,

amounted to EUR 5.78 per square metre. The vacancy rate as of this date was

roughly 2.10%. In addition to residential properties, as of 30 June 2015,

Deutsche Wohnen’s real estate portfolio included 2,072 commercial property

units with a total floor space of approximately 0.3 million square metres based

on the total commercial area listed in the rental agreements, as well as a total

of 30,502 parking garages, underground garage spaces and parking spaces.

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 6 -

The residential real estate portfolio was evaluated by an external independent

appraiser – CBRE GmbH, Frankfurt (“CBRE”) – as of 30 June 2015 using a

DCF model in accordance with the standards of the Royal Institution of

Chartered Surveyors (RICS) in line with the Red Book, with the exception of

real estate properties for senior citizens used by Katharinenhof, for which the

appraisal as of 30 June 2014 was maintained. According to this appraisal, the

real estate portfolio of Deutsche Wohnen is valued at approximately EUR

10.283 billion (including commercial properties and undeveloped land,

excluding the senior citizen properties used by Katharinenhof) as of 30 June

2015. Deutsche Wohnen’s real estate properties for senior citizens used by

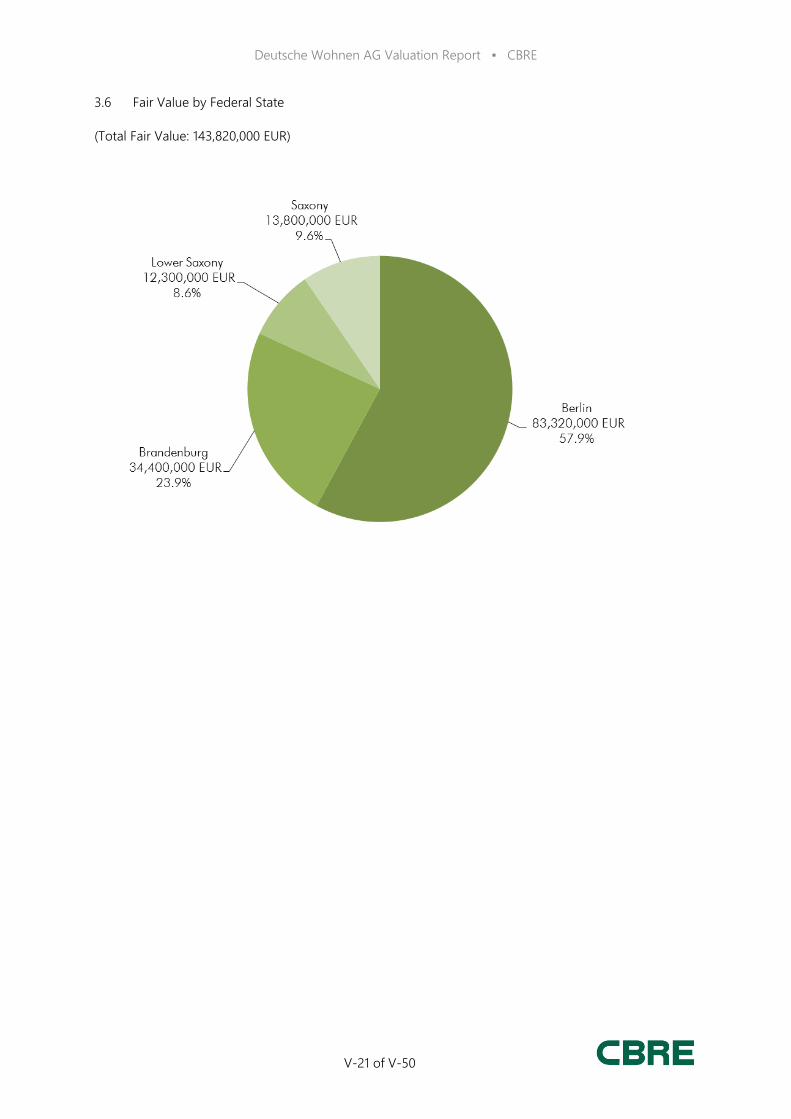

Katharinenhof were valued at EUR 143.8 million by CBRE as of 30 June 2014.

The data calculated by CBRE was updated (fortgeschrieben) by Deutsche

Wohnen in the interim report dated 30 June 2015. According to this report, the

market value as of 30 June 2015 is EUR 143.8 million.

Deutsche Wohnen’s residential real estate portfolio is currently classified into

strategic core- and growth-regions, as well as non-core regions. Within the

strategic core- and growth-regions, Deutsche Wohnen makes a further

distinction between core+-and core-regions.

Core+-regions are dynamic markets in which Deutsche Wohnen sees

considerable potential for rent price increases and a positive market

environment for sales. These markets are characterized by a demand surplus

for residential space. This is the result of a dynamic economic development

and an increase in households, inter alia due to an increase in single-person

households. Deutsche Wohnen’s core+-regions are the metropolitan regions of

(i) greater Berlin, (ii) Rhine-Main, (iii) Mannheim/Ludwigshafen, (iv) the

Rhineland and (v) Dresden. Based on the number of units, approximately 87%

of the units in the residential real estate portfolio were in the core+-regions as

of 30 June 2015.

By contrast, core-regions are regions with a market development that is

expected to be stable. These markets are characterized by a balanced supply

and demand situation, a good economic situation, a stable economic outlook,

average purchasing power and a steady number of households. In particular,

Deutsche Wohnen’s core-regions are (i) Hanover/Brunswick, (ii) Magdeburg,

(iii) Kiel/Lübeck, (iv) Halle/Leipzig, (v) Erfurt and (vi) Other. Based on the

number of units, approximately 11% of the units in the residential real estate

portfolio were in the core-regions as of 30 June 2015.

Non-core-regions are defined as geographic regions where the development is

stagnant and/or there is a negative trend. They include mainly rural areas and

scattered properties. Based on the number of units, approximately 2% of the

units in the residential real estate portfolio were in the non-core-regions as of

30 June 2015.

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 7 -

In the course of the merger of Deutsche Wohnen and LEG, it is intended to

reclassify the residential real estate portfolio, with a focus on distinguishing

among “core+”, “core” and “high-yield-regions”. The reclassification will take

account of the new circumstances of the merged company and the diversified

regional portfolio. The core+-regions will include greater Berlin, the Rhineland,

Münsterland, Rhine-Main, Mannheim/Ludwigshafen and Dresden. The core-

regions will be defined as the geographic regions of Ostwestfalen, the core

cities of the Ruhr region, Hanover/Brunswick, the Lower Rhine, Kiel/Lübeck

and the core cities of the new federal states. The High-Yield regions will

include the rest of the Ruhr region, Bergisches Land/Sauerland, the rest of the

new federal states and all other regions.

(4) Share capital

The Company’s share capital is currently registered with the commercial

register (Handelsregister) as EUR 336,426,511.00, divided into 336,426,511

ordinary bearer shares, each with a notional value of EUR 1.00. Since 1

January 2015, in addition to this amount, shares of the Company from

conditional capital have been issued to former shareholders of GSW

Immobilien AG who have exerted their right to compensation based on the

domination agreement concluded between the Company and GSW Immobilien

AG. It is possible that other shareholders of GSW Immobilien AG may exert

their right to compensation until the resolution regarding the capital increase is

proposed or the capital increase is implemented. The corresponding increases

in conditional capital have not yet been registered with the commercial register

(Handelsregister).

b) LEG

(1) Business activities

LEG is a publicly traded real estate company with its seat of business in

Düsseldorf. The business model of LEG is focused on the letting and

management of residential units with a clear focus on North Rhine-Westphalia.

This business activity is complemented by the sale of residential units via LEG

Consult GmbH, a subsidiary of LEG. Erste WohnServicePlus GmbH,

Düsseldorf, a subsidiary of LEG, offers (in cooperation with Unitymedia

GmbH) multimedia products for LEG’s residential properties, and

EnergieServicePlus GmbH, Düsseldorf, of which LEG holds 51% of the

shares and RWE Vertrieb AG holds 49%, will assume responsibility for the

complete energy and technical management and supply of LEG properties.

(2) Segments

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 8 -

LEG’s business is divided into the “Residential” and “Other” segments. The

“Residential” segment includes all residential and commercial properties, own-

used buildings, property companies (Bestandsgesellschaften) and LEG

Wohnen NRW. Real estate portfolios which have evolved from completed

project developments to long-term leasing and which are solely owned by the

group are also maintained in the “Residential” segment.

The “Other” segment includes development companies as well as the

companies LEG Management GmbH and LCS Consulting und Service GmbH.

Let properties that are available for sale from the development business are

also recognized in the “Other” segment. LEG Management GmbH, which is

included in the “Other” segment, focuses primarily on services in connection

with administrative functions and group management.

(3) Portfolio

By its own account, as of 30 June 2015, LEG’s real estate portfolio comprises

107,347 residential units, 1,059 commercial units and 26,648 parking garages

and parking spaces. The total living space amounts to roughly 6.9 million

square metres and the average rent for residential units of the total portfolio

amounted to EUR 5.16 per square metre as of 30 June 2015. As of this date,

the vacancy rate for residential units was 3.30%.

According to LEG, the portfolio can be classified into Growth Markets

(Wachstumsmärkte), Stable Markets (Stabile Märkte) and Higher-Yielding

Markets (Märkte mit höheren Renditen). According to its 2015 semi-annual

report, 33,574 residential units are situated in Growth Markets, with a vacancy

rate of 1.50% and an average rent of EUR 5.79 per square metre. According to

LEG, this price is below the average rent in the respective markets, meaning

that there is a rental potential of 18.00% here. 42,638 residential units are

situated in the Stable Markets segment, with a vacancy rate of 3.70% and an

average rent of EUR 4.89 per square metre. The rental potential here is

identified as 9.00%. In Higher-Yielding Markets, there are, according to LEG,

29,678 residential units with a vacancy rate of 5.30% and an average rent of

EUR 4.78 per square metre. The rental potential here is identified as 8.00%.

According to information provided by LEG in its report for Q2 2015 dated

14 August 2015, the overall portfolio was worth approximately EUR 6 billion

as of 30 June 2015.

In the course of the merger of Deutsche Wohnen and LEG, it is intended to

reclassify the residential real estate portfolio, with a focus on distinguishing

among “core+”, “core” and “high-yield-regions”. The reclassification will take

account of the new circumstances of the merged company and the diversified

regional portfolio (see section III.1.a)(3) above). It is possible that the future

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 9 -

assessment of the quality of LEG’s markets and sub-portfolios by Deutsche

Wohnen may deviate from the current assessment by LEG as part of this

reclassification of the real estate portfolio.

(4) Share capital

LEG’s current share capital is EUR 58,259,788.00, divided into 58,259,788

registered shares, each with a notional value of EUR 1.00.

LEG has also issued convertible bonds with a nominal value of EUR 300

million (final maturity: 1 July 2021). A complete exercise of the conversion

rights, would, at the current conversion price of EUR 58.4317, lead to the

issuance of approximately 5.13 million shares and thus increase the total

number of shares by about 8.8%.

A change of control as a result of the Exchange Offer would trigger a “Change

of Control” provision under the terms and conditions of the convertible bonds,

according to which the bond holder may, under certain circumstances within

the additional acceptance period pursuant to section 16 of the WpÜG demand,

next to the immediate calling in of the bond its immediate conversion into

LEG Shares at a lower conversion price.

“Change of control” in connection with the Company’s Exchange Offer means

the fulfillment of all offer conditions (including any minimum acceptance

threshold within the offer) that have to occur before the end of the acceptance

period.

In the event of a conversion as a result of a change of control, the conversion

price will be reduced according to the following formula:

Where:

CPa = the adjusted conversion price;

CP = the conversion price on the day directly preceding the day on which the

change of control occurs;

Pr = the initial conversion premium of 30%;

c = the number of days from the day on which the change of control occurs

(inclusive) to the maturity date (exclusive); and

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 10 -

t = the number of days from the day on which the the bonds are issued

(inclusive) to the maturity date (exclusive).

A complete exercise of the conversion rights in the event of an assumed

change of control on 1 December 2015 would result in the issuance of roughly

6,324,268 shares and thus increase the total number of shares by about 10.9%.

c) Competitive advantages and synergies resulting from the acquisition of LEG

With the merger of Deutsche Wohnen and LEG, Deutsche Wohnen is

acquiring a high-quality real estate portfolio that provides additional growth

options with an attractive risk/return profile.

(1) Focused combined real estate portfolio with more than 90% of the market

value based on the market value in core+-and core-regions

The combined company will have a focused residential property portfolio of

roughly 250,000 units. This corresponds to an increase of the current portfolio

of Deutsche Wohnen by approximately 107,000 units, or an increase by

around 75% according to the published figures for Deutsche Wohnen and LEG

for the first half of 2015. Additionally, the strong regional concentration of the

combined portfolio enables a continued high management efficiency (see more

on this below).

The portfolio of LEG is primarily located in dynamic markets with

considerable rent increase potential (about 42% based on the market value

(Fair Value)) as well as markets with stable rents (about 36% based on the

market value). The merger with LEG will thus enable Deutsche Wohnen to

increase the number of residential units in its core+-and core-regions

significantly. These markets will make up more than 90% of the combined

portfolio based on the market value after comnpletion of the transaction.

As a result, the core+-portfolio for the combined company will expand from

roughly 123,000 to roughly 157,000 units, primarily through acquisitions in

the Rhineland and Münsterland, and the core-portfolio will increase from

roughly 16,000 to roughly 58,000 units, primarily through acquisitions in core

cities in the Ruhr region and in Ostwestfalen. Based on the market value, about

73% of the combined portfolio will be in core+-regions and 18% in core-

regions. Berlin’s share of the combined portfolio will be almost 50% in terms

of market value, and, looking forward, it will thus represent a significant

growth driver for Deutsche Wohnen.

In addition, after the transaction about 10% (in terms of market value) of the

units in the combined portfolio will be in regions with above-average returns

(so called high yield Markets), which will contribute to an improvement in the

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 11 -

return profile of Deutsche Wohnen. Significant sell-off portfolios were not

identified by the Management Board on the basis of public information.

The enlarged combined portfolio will enable Deutsche Wohnen to conduct

more active portfolio management through rent management, opportunities for

rounding out the portfolio (Arrondierung) and additional privatization

potential, and thus earn additional increases in revenue and returns. Achieving

critical mass in new core+-and core-regions will also provide additional

opportunities for external growth.

(2) Considerable synergy potential

The merger of the two companies will result in standardized structures and

processes. The Management Board of Deutsche Wohnen believes that,

following the integration, there will be revenue and cost synergies with a

positive effect on the combined FFO (without disposals) of approximately

EUR 35 million per year, before taxes. In addition, the Management Board

expects that the merger will increase the long-term privatization potential by

about 1,500 units, with an additional contribution to earnings

(Ergebnisbeitrag) of about EUR 20 million before taxes each year. Thus, a

total additional contribution to earnings (Ergebnisbeitrag) of about EUR 55

million before taxes per year is expected for the combined FFO (including

disposals).

The Management Board expects that these synergies can be fully realized

within four years after the implementaion of the transaction.

The expected synergy potential mainly arises from the following areas:

Reducing administrative costs (personnel and material costs): The cost ratio

for personnel and material costs, measured on the basis of rental rates, was

about 14.5% at Deutsche Wohnen in the fiscal year 2014. As a result of

scaling effects, the acquisitions carried out in recent years, including GSW

Immobilien AG, were integrated in the Deutsche Wohnen Group with a cost

ratio of about 5 to 10%. For 2015, the Management Board therefore expects

to be able to further reduce Deutsche Wohnen’s cost ratio for personnel and

material costs to about 12% of the rental rates. Based on this experience and

its integration track record, the Management Board expects, as a result of the

merger of Deutsche Wohnen and LEG, to be able to realize considerable cost

reductions through a simplified corporate structure, particularly by unifying

of holding functions, joint contract management and a standardized IT

infrastructure. In the medium term, it targets a cost ratio for personnel and

material costs in the joint company ranging from 11 to 12%.

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 12 -

Consolidation of the West German operating platforms: The West German

portfolio of Deutsche Wohnen and LEG reveals potentials for optimization in

the local management of the holdings. Management costs per residential unit

are typically heavily dependent on the concentration of the holdings.

Concentrated holdings allow for an optimized division of tasks and thus more

efficient management. The overlap of the Deutsche Wohnen and LEG

portfolios in West Germany means that the concentration of holdings will

increase in numerous areas and therefore synergies can be created from the

uniform management of the holdings. The operational management of the

combined companyʼs West German portfolio is to be conducted through the

Dusseldorf office.

Increase in revenue and returns as a result of the merger of central functions

for the management of real estate holdings: Synergies can also be created by

establishing joint central customer services and back office functions. As the

joint service volume of the two companies will increase significantly, this

will enable a much more efficient operational management and thus an

increase in productivity. In particular, this includes centralized management

of the holdings, centralized support of the rental management (service points),

billing of utility costs and claims management. Thanks to greater

standardization and the adjustment of operating processes the rent potential

can be better realized and vacancy-related costs reduced.

Scaling of purchasing: The combined company will, according to the

assessment of the Company, also have more bargaining power for optimising

purchasing. This affects, in particular, contracts with energy suppliers,

insurance companies and system providers, and the procurement of IT

hardware and services. The realization of these potentials is dependent on

current contractual conditions, particularly the contract periods. In addition,

there is potential for a reduction of purchasing positions related to utilities

and common charges, which will initially only have a marginal impact on the

FFO (without disposals), but will lead to higher customer satisfaction in the

medium term due to lower costs for utilities and common charges.

Additional privatization potential: Value-creating and sustainable single-unit

privatizations are a key pillar of Deutsche Wohnen’s business model.

Deutsche Wohnen’s Management Board intends to increase the volume of

privatizations from over 1,500 units on average over the last three years for

the combined company to over 3,000 units per year in order to profit more

from the current attractive market environment. On the basis of the current

market environment and the realizable gross margins from sales, the

Management Board expects a significant additional contribution to earnings

(Ergebnisbeitrag) for the FFO (including disposals). In addition,

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 13 -

privatizations will free up considerable financial resources that can be used

for value-creating investments as well as distributions to shareholders.

Assuming that the revenue and cost synergies can be fully realized within four

years, the capitalized value of the expected revenue and cost synergies of EUR

32 million per year is approximately EUR 990 million after taxes. This figure

is based on a capitalization rate of 4%, based on Deutsche Wohnen’s average

weighted capital costs, a growth factor for perpetuities of 1%, an effective tax

rate of 10% and the assumption of an approximately linear development of the

synergies until 2019.

The synergies are offset by expected expenses. Based on information currently

available, the Management Board estimates these expenses to be

approximately EUR 55 million, after taxes. These are comprised in about

equal proportion of transaction costs and integration costs. Based on the

aforementioned estimates by the Management Board regarding the level of

synergies on the one hand and the expenses required to achieve these synergies

on the other hand, the expected net present value of the synergies amounts to

approximately EUR 935 million after taxes. Taking into account the

privatization potential associated with the increase in the residential real estate

portfolio, which according to the estimate of the Management Board can be

realized within two years, the net value of the synergies is about EUR 1,530

million, after taxes.

(3) Maintaining the conservative capital structure and improving the key

financial indicators

The Management Board expects the acquisition in the form of an exchange of

shares to result in a loan-to-value ratio in the combined company of about 42%.

The average financing costs for the combined company, with an average

residual term on financial liabilities of around 10 years, will only be about 2%.

In addition, assuming that termination rights as a consequence of the

completion of the transaction (change of control provisions) are not exercised,

there will not be any significant maturities up to and including the fiscal year

2019. The conservative capital structure is part of the guidance provided by the

Deutsche Wohnen Management Board and should enable continued growth at

low financing costs and support the current A-/A3 rating of Deutsche Wohnen.

As a result, the combined company will enjoy comparatively attractive

financing conditions within the German exchange-listed real estate sector.

The acquisition together with the aforementioned synergies will lead to an

improvement of key financial indicators and a relative strengthening of

Deutsche Wohnen compared to its competitors. The Management Board

anticipates that the merger will enable efficiency advantages as compared to

publicly traded competitors. The Management Board expects that the FFO

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 14 -

(without disposals) per share, following the full realization of the synergies in

the amount of EUR 35 million (before taxes) per year, will improve in the

lower two digit scale. Taking account of the net present value of the synergies,

the merger will have a broadly neutral impact on the adjusted EPRA NAV

(EPRA NAV minus goodwill plus net present value of the revenue and cost

synergies) per share of Deutsche Wohnen. Thus, taking further account of the

return and risk aspects as well as the growth potential of the combined

company, the merger will clearly create value for Deutsche Wohnen

shareholders (see in detail section III.3.(f)(3) below).

(4) Strengthened capital market profile

Finally, the acquisition strengthens the capital market profile of the combined

company. The expected combined market capitalization (free float) of the

Company and LEG (based on the Xetra closing prices on 18 September 2015

and on the basis of a 100% acceptance rate) in the amount of approximately

EUR 13.4 billion will strengthen the significance and the liquidity of the

Company’s shares and thus its attractiveness for investors. In addition, it is

expected that the solid credit rating of the combined group will allow it to

borrow capital at better conditions in perspective. These factors should also

ensure financing with equity capital and/or debt capital at improved conditions

independently from the market cycle and thus further optimize the capital costs

of the combined company. For example, it is possible that the Exchange Offer

will attract new groups of investors. Furthermore, increased liquidity will also,

in Deutsche Wohnen’s view, open up the possibility of being included in the

DAX 30 in the medium term.

2. Description of the Planned Transaction

Based on the proposed resolution of the Management Board, the acquisition of the shares

of LEG by Deutsche Wohnen is planned as follows:

a) Takeover offer in the form of an Exchange Offer

The Management Board of Deutsche Wohnen resolved to issue a voluntary

takeover offer in the form of an Exchange Offer to all shareholders of LEG

pursuant to sections 29, 31, para. 2, sentence 1, alternative 2 of the WpÜG and

published this decision pursuant to section 10, para. 1, 3, sentence 1 of the

WpÜG. The intention is to offer shares in Deutsche Wohnen to the

shareholders of LEG in exchange for their LEG shares at a ratio of 3.30 shares

of Deutsche Wohnen per share representing a notional amount of EUR 1.00 of

LEG‘s share capital.

The Company plans to make the Exchange Offer subject to the standard

conditions for such takeover offers, particularly a minimum acceptance rate of

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 15 -

50% plus one share, a condition related to a material adverse change of LEG’s

business situation and a condition related to the execution of the proposed

capital increase against contributions in kind.

The Management Board expects that a non-prohibition decision

(Nichtuntersagungsentscheidung) will be issued by the German Federal Cartel

Office before publication of the offer document. If this is not the case by the

time the offer document is published, the approval by the German Federal

Cartel Office will become a further closing condition (Vollzugsbedingung) of

the Exchange Offer.

b) Capital increase against contributions in kind with the exclusion of statutory

subscription rights of shareholders for the purpose of the implementation of the

Exchange Offer

Subject to the limitations described in c) (see below), the shares required for

the implementation of the Exchange Offer will be created by way of a capital

increase against contributions in kind with the exclusion of statutory

subscription rights of the shareholders.

The LEG Shares shall be contributed as contributions in kind, and the LEG

shareholders shall receive the newly created shares of the Company in

exchange for their shares. The Exchange Trustees authorized by the

shareholders of LEG to carry out the Exchange Offer shall be the only persons

admitted for the subscription of the New Shares. The subscription rights of the

shareholders of the Company shall be excluded.

Shareholders of LEG who accept the Exchange Offer will transfer their LEG

Shares to the Exchange Trustees. The Exchange Trustees will then contribute

the LEG Shares that they hold in trust to Deutsche Wohnen as contributions in

kind and subscribe the Company´s shares created as part of the planned capital

increase against contributions in kind. Once the New Shares of Deutsche

Wohnen are created, the Exchange Trustees will transfer the shares, in

accordance with the exchange ratio, via the settlement agent to the respective

shareholders of LEG.

Where shareholders of LEG would be entitled to fractional amounts of

Deutsche Wohnen shares according to the exchange ratio, such fractional

amount shall be sold by the Exchange Trustees. The proceeds from the sale of

the fractional amounts will be credited in cash pro rata to the affected

shareholders of LEG.

The maximum amount of this capital increase against contributions in kind is

such that, based on the number of LEG Shares currently outstanding and likely

to be created through the conversion of outstanding convertible bonds before

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 16 -

the end of the additional acceptance period, and the exchange ratio proposed in

the Exchange Offer, a sufficient number of Deutsche Wohnen shares for all the

tendered LEG Shares may be issued and shall amount to approximately 213.1

million shares (subject to the issuance of shares by means of the capital

increase against cash contributions from authorized capital (as set out inc))).

As the Exchange Trustees do not to bear a differential liability

(Differenzhaftung) under sections 188, para. 2 sentence 1, 36a, para. 2

sentence 3 of the AktG in the amount of the contribution value

(Einbringungswert) of the LEG Shares, the New Shares of Deutsche Wohnen

will be issued at the minimum issue amount (Ausgabebetrag) of EUR 1.00

(sections 8, para. 3, sentence 3, 9, para. 1 of the AktG) and the difference

between the issue amount (Ausgabebetrag) of the New Shares and the

contribution value (Einbringungswert) of the contribution in kind will be

allocated to the capital reserve pursuant to section 272, para. 2 Nr. 4 of the

HGB.

c) Utilization of the existing authorized capital to implement the target tax structure

Pursuant to sections 29, 31, para. 2, sentence 1, alternative 2 and 32 of the

WpÜG, the Exchange Offer must always be directed to all LEG shareholders,

insofar as the Federal Financial Supervisory Authority (“BaFin”) does not

grant an exemption pursuant to section 24 of the WpÜG.

However, for tax purposes Deutsche Wohnen does not intend to acquire more

than 94.9% of the shares of LEG. This is because according to section 1,

para. 3 and para. 3a of the German Real Estate Transfer Tax Act (“GrEStG”),

the acquisition of at least 95% of the shares in a company will lead to a real

estate transfer tax liability for real estate property in Germany belonging to the

Company’s assets, with the applicable tax rate in North-Rhine Westphalia,

LEG’s regional focus, currently being 6.5%. Based on the information

available to it, the Management Board of the Company estimates that the real

estate transfer tax incurred in the case of a full acquisition of LEG would

amount to approximately EUR 390 million.

The tax liability pursuant to section 1, para. 3 and para. 3a of the GrEStG

would arise if the acceptance rate of the Exchange Offer were to be so high

that the Exchange Trustees had to contribute such an amount of LEG shares as

contributions in kind to the Company that Deutsche Wohnen would end up

owning at least 95% of the share capital of LEG.

To the extent that the capital increase against contributions in kind would

result in Deutsche Wohnen owning more than 94.9% of the share capital of

LEG (taking account of any LEG Shares that may already be held by Deutsche

Wohnen that were not acquired as part of the Exchange Offer), Deutsche Bank

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 17 -

AG has agreed to acquire and take over all LEG Shares issued to the Exchange

Trustees above this acceptance rate (i.e. a maximum of 5.1% of the LEG

Shares currently outstanding and anticipated to be created through, inter alia,

the conversion of outstanding convertible bonds before the end of the

additional acceptance period) from the Exchange Trustees instead of Deutsche

Wohnen. The same applies in the event that shareholders of LEG Immobilien

AG are entitled to tender their shares in LEG Immobilien AG after the end of

the acceptance period in accordance with the content of the exchange offer by

analogy to § 39c of the WpÜG, because Deutsche Wohnen AG and Deutsche

Bank AG combined are holding at least 95% of the shares in LEG Immobilien

AG after implementation of the exchange offer.

In order to enable the Exchange Trustees, in accordance with the proposed

Exchange Offer, to provide the LEG shareholders with Deutsche Wohnen

shares even for this excessive number of LEG Shares, the Management Board

and Supervisory Board of the Company have issued corresponding

precautionary resolutions for the utilization of the authorized capital, with the

exclusion of the subscription right, on 21 September 2015. The maximum

amount of this capital increase against cash contributions from authorized

capital is calculated in a way that, based on the number of LEG Shares

currently outstanding and likely to be created through the conversion of

outstanding convertible bonds before the end of the additional acceptance

period and the exchange ratio proposed in the Exchange Offer, a sufficient

number of Deutsche Wohnen shares for 5.1% of the tendered LEG Shares may

be issued and amounts to 10,869,497 shares; in the event that this capital

increase against cash contributions from authorized capital is implemented, the

maximum number of shares issuable in the context of the capital increase

against contributions in kind that is to be resolved will be decreased

correspondingly. Accordingly, from today’s view, the maximum number of

shares to be issued in the context of this capital increase against cash

contributions from authorized capital and the capital increase against

contributions in kind that is to be resolved will not exceed 213,127,385 shares.

Again, only UBS Deutschland AG, Opernturm, Bockenheimer Landstraße 2-4,

60306 Frankfurt am Main and DZ BANK AG Deutsche Zentral-

Genossenschaftsbank, Frankfurt am Main, Platz der Republik, 60265 Frankfurt

am Main as the Exchange Trustees for the LEG shareholders, shall be allowed

to subscribe for the shares issued as part of the capital increase against cash

contributions from authorized capital. The issue amount (Ausgabebetrag) is

EUR 1.00, and the Exchange Trustees have irrevocably undertaken to transfer

the difference between the issue amount (Ausgabebetrag) of EUR 1.00 and the

agreed issue price (vereinbarter Emissionspreis) equal to the closing price on

18 September 2015 in the amount of EUR 24.05 per share to the Company.

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 18 -

Insofar as it is evident at the time of the implementation of the Exchange Offer

that the acquisition of all tendered LEG shares would result in Deutsche

Wohnen owning more than 94.9% of the share capital of LEG, the Exchange

Trustees will subscribe for the number of Deutsche Wohnen shares issued as

part of the capital increase against cash contributions from authorized capital

which is required to exchange the excess tendered LEG Shares. The Exchange

Trustees will make the cash contributions required for the subscription of these

shares with funds made available to them by Deutsche Bank AG in return for

the acquisition of up to 5.1% of LEG Shares. After the implementation of the

capital increase against cash contributions from authorized capital has been

registered with the commercial register (Handelsregister), the Exchange

Trustees will transfer the shares, in accordance with the exchange ratio,

together with the shares created through the capital increase against

contributions in kind, via the settlement agent to the LEG shareholders

accepting the Exchange Offer.

Deutsche Bank AG receives a commission from Deutsche Wohnen in an

amount based, inter alia, on the sum given as a consideration for the

acquisition of the LEG Shares and on the period of time until the resale of

these shares. For two years, Deutsche Wohnen has the opportunity to name a

buyer for the LEG Shares to Deutsche Bank, after this period Deutsche Bank

AG will dispose of the shares at the best possible price. Deutsche Wohnen is

obliged to pay Deutsche Bank AG the difference between the purchase price

paid by the buyer in this process and the amount for which Deutsche Bank AG

acquired the LEG Shares.

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 19 -

d) Simplified Description of the Transaction Structure

e) Next Steps, Conclusion of a Business Combination Agreement

Depending on the acceptance rate in the Exchange Offer, the Management

Board is considering to conclude a domination and/or profit and loss transfer

agreement pursuant to section 291, para. 1, sentence 1 of the AktG following

the implementation of the Exchange Offer between Deutsche Wohnen and

LEG, or to negotiate mutual service agreements with LEG, insofar as this is

expedient for the best possible realization of synergies.

In addition, the Management Board has today concluded a Business

Combination Agreement with LEG with respect to the public takeover offer

and the future strategy and structure. The intention is to subdivide the

company created as a result of the merger into two main regions: Berlin and

North-Rhine Westphalia. The operational management of the combined

companyʼs West German portfolio is to be conducted through the Dusseldorf

office. The new corporate group will continue to pursue the previous growth

strategy, exploiting the expected synergies (see section III.1.c) above) in order

to realize additional added value for the shareholders of the combined

corporate group. The objectives of the future strategy are, in particular, to

maintain a conservative debt ratio, continued growth in the core-regions, the

development of new regions and the expansion of the privatization business in

order to utilize the currently attractive market environment.

Umtausch-

treuhänder Cash

≤ 100% LEG shares

≤ 94.9% LEG shares

+ cash

Deutsche

Wohnen

LEG

shareholders

≤ 100% new

Deutsche

Wohnen shares

≤ 100% new

Deutsche

Wohnen shares

Deutsche Bank

AG

≤ 5.1% LEG

shares

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 20 -

The Offeror will respect the legal rights of employees, works council members

and trade unions of the target company as well as collective bargaining

agreements (kollektivrechtliche Vereinbarungen). The current regulations of

the individual companies based on the social charter or purchase agreements

will remain in place in accordance with their period of validity.

Pursuant to the Business Combination Agreement, two members of the current

LEG Management Board will also become members of the Deutsche Wohnen

Management Board. No changes are planned with respect to the appointment

of the Chairman of the Deutsche Wohnen Management Board. The Chairman

of the LEG Management Board will serve as the Deputy Chairman of the

Deutsche Wohnen Management Board. The supervisory board of Deutsche

Wohnen shall be expanded to nine members, with three current supervisory

board members of LEG to join the Supervisory Board of Deutsche Wohnen.

The members of the LEG Management Board and the shareholder

representative of the LEG Supervisory Board shall be proposed by an

Integration Committee that is to be formed, which shall be comprised of the

respective Chairmen of the Management Boards and Supervisory Boards of

Deutsche Wohnen and LEG.

f) Timetable

The transaction timetable is as follows:

Within the four- to eight-week period beginning tomorrow, the offer

document regarding the Exchange Offer will be communicated to BaFin

(sections 34, 11, 14 para. 1 of the WpÜG).

The offer document will be published without delay pursuant to section 14,

para. 2 and 3 of the WpÜG if BaFin authorizes its publication or if a period

of ten working days (with the possibility of an extension of up to five

working days) has elapsed after BaFin has received the offer document and

BaFin has not prohibited the offer.

During this procedure, the Extraordinary General Meeting will take place on

Wednesday, 28 October 2015 at 10 A.M. (CET) and there will be a vote on

the resolution proposals mentioned under II.

The acceptance period, which is at least four weeks and, as a rule, lasts no

more than ten weeks, commences with the publication of the offer document;

the additional acceptance period of two weeks, which applies to takeover

offers, commences after this period (sections 34, 16, para. 1 and 2, 23, para. 1,

sentence 1, no. 2 of the WpÜG).

If the General Meeting passes the resolution that has been proposed, no

objection has been lodged and no rescission action (Anfechtungsklage) has

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 21 -

been initiated, the resolution regarding the share capital increase will be

registered following the expiration of the addtional acceptance period.

Following this procedure, the Exchange Offer may be implemented if the

other conditions have been met.

If the General Meeting passes the resolution that has been proposed, but a

rescission action (Anfechtungsklage) has been initiated, such resolution shall

be registered following a successful release procedure (Freigabeverfahren)

(section 246a of the AktG). In this case, the resolution may be registered after

the end of the additional acceptance period. In the event the other conditions

are fulfilled, the Exchange Offer will only be implemented at this later point

in time.

3. Explanation and Justification of the Exchange Ratio

a) Preliminary remarks

The determination of the exchange ratio is based on the Management Board’s

valuation of both LEG and Deutsche Wohnen. The same methods and

valuation parameters commonly used in the valuation of real estate companies

were applied in the valuation of both companies involved in the transaction.

In addition, Deutsche Wohnen has commissioned Deutsche Bank AG and

VICTORIAPARTNERS GmbH to examine the appropriateness of the fixed

exchange ratio and to each draft a fairness opinion to such effect. The

examination of the appropriateness of the exchange ratio by the Management

Board as set forth in this section III.3 is supported by the conclusion of these

fairness opinions. The corresponding fairness opinions are attached hereto as

Annex A and Annex B in letter form.

Before publishing the decision to submit this Exchange Offer, there was a

mutual due diligence review; however, pursuant to an agreement, as is

standard when acquiring an exchange-listed company, this review was limited

to the exchange of selected documents and information. In addition, publicly

available information was accessed, and in particular the following documents

were analyzed:

LEG’s listing prospectus dated 18 January 2013

LEG’s annual reports for the fiscal years 2013 and 2014

LEG’s interim reports for the first and second quarters of 2015

Furthermore, the Management Board analyzed analyst reports and other

documents that it believed to be useful with respect to the assessment of the

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 22 -

appropriateness of the exchange ratio and took into consideration the result of

this analysis in its assessment.

b) Valuation approaches and methods

The determination of the exchange ratio is based on the same methods applied

to the valuation of both companies. In particular, the valuation was carried out

on the basis of the following parameters:

Net asset value, measured according to the recommendations of the

European Public Real Estate Association (EPRA NAV). The Management

Board believes that the EPRA NAV is the most commonly used valuation

standard for determining the market value of the net asset value of real estate

companies that keep their property for long-term rental and management. The

properties are to be appraised based on the market value calculated using the

discounted cash flow (“DCF”) method. The EPRA NAV is calculated on the

basis of equity excluding minority interests, adjusted for (i) the exercise of

options, convertible bonds and other equity rights, (ii) the balance of (active

and passive) derivative financial instruments as well as (iii.) certain deferred

taxes. The EPRA NAV is thus derived from the DCF-based values that

account for the intrinsic value (equity) of a real estate company by adjusting

for positions for which it is assumed that there is no influence on long-term

assets held by owners in the regular course of business. For the purpose of the

EPRA NAV for the combined company, any effects arising from the

allocation of the purchase price pursuant to IFRS 3 (e.g. goodwill) in

connection with a potential acquisition of a majority stake in LEG are not

taken into account. Apart from that, the EPRA NAV for the companies

involved was determined both including and excluding goodwill (i.e.

goodwill formed as part of already completed transactions) and on the basis

of undiluted and diluted shares for the purpose of the comparison.

Market capitalization. The market capitalizations of LEG and Deutsche

Wohnen was determined on the basis of the closing prices on Xetra of the

Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) on the last trading

day prior to the publication pursuant to section 10, para. 1, 3, sentence 1 of

the WpÜG, and the sum of the number of shares outstanding as of the

reference date and the number of shares determined on the basis of the

conversion of all outstanding convertible bonds for the respective company at

the respective current conversion price. For the purpose of comparison and to

check for potential reference date-related fluctuations regarding the market

capitalization, the volume-weighted average price (VWAP) for the 3 months

prior to the valuation was also determined and applied to the number of

shares of each company thus obtained (market capitalization on the basis of

the 3-month VWAP). The VWAP was calculated based on the closing prices

and the daily trading volumes on the Xetra trading platform. The comparison

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 23 -

of the market capitalization of each company is, in terms of a value

comparison, meaningful because both companies have a significant amount

of free float, and trading in both companies is considered to be liquid.

The absolute valuation of LEG and Deutsche Wohnen was initially carried out

without considering the related synergies associated with the transaction.

c) Alternative valuation methods

During deliberations, the Management Board considered alternative methods

for valuing the companies involved in the transaction, but these were rejected

as either unsuitable or less suitable.

Income or DCF approach. A valuation of the entire company based on the

income or DCF approach, a method used in some cases for the valuation of

companies in the context of mergers, and in which the determination of the

company’s value is based on projected earnings expectations from the

company’s plans, is a less common method for the valuation of residential

real estate companies. Unlike valuation on the basis of the income approach,

the EPRA NAV-based valuation used here allows for the appraisal of

individual pieces of property, the values of which are in turn based on future

recoverable cash flows from the management of these properties. Because of

the comparatively high visibility of future cash flows from the management

of residential properties, the Management Board is of the opinion that a

valuation on the basis of EPRA NAV leads to a more reliable result

compared to the valuation of a company as a whole based on the income

approach and therefore deems the valuation on the basis of the EPRA NAV

to be superior. In addition, the Management Board would have had no access

to data essential to the valuation of LEG on the basis of the income or DCF

approach, particularly data pursuant to IDW Standard S1. By contrast, LEG

discloses its EPRA NAV in every annual and interim report and has the real

estate valuation based on this key indicator reviewed annually by an

independent external expert in order to prepare its annual financial statements.

Valuation on the basis of liquidation values. A valuation on the basis of

liquidation values was determined to be less suitable, as the intention is for

both companies involved in the transaction to continue operating. In addition,

because of the continuation of the lease contracts in the event of a liquidation,

it is not expected that this valuation method would have led to a substantially

different value ratio compared with a valuation on the basis of the EPRA

NAVs.

Price targets (Kursziele) from analysts’ reports. The Management Board

evaluated available analysts’ reports from major providers for both Deutsche

Wohnen and LEG. The Management Board determined that a valuation based

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 24 -

solely on the price targets (Kursziele) in these reports is less suitable. First,

analysts’ reports are based on different methods for determining the target

price, which is typically issued for a 12-month period. Furthermore, the

valuation methods are not completely transparent and therefore not sufficient

for evaluating their meaningfulness. Both companies were analyzed and

valued by more than 15 analysts at major banks. Within this group, the price

targets (Kursziele) deviate widely from each other, calling into question the

meaningfulness of these price targets (Kursziele). A selection or weighting of

the price targets (Kursziele) would lead to a subjective valuation result.

Although an examination of the arithmetic average as well as the median of

the respective price targets (Kursziele) would mathematically support the

result of the valuation methods used by the Management Board, given the

high variance among such price targets (Kursziele) it, too, seems to be less

suitable.

FFO yields. The Management Board considered a separate valuation of

Deutsche Wohnen and LEG on the basis of their Funds from Operations

(FFO) yields and found it to be less suitable. Because of the limited time

horizon for which the companies involved publish estimates of their future

FFO and because of the different regional focus, the different growth profile

and related lack of comparability of the yields achieved, a comparison on the

basis of the FFO of Deutsche Wohnen and LEG is, in the estimation of the

Management Board, by itself less suitable for reviewing the appropriateness

of the comparative valuation of the two companies. However, for the purpose

of determining the plausibility of its valuation results, the Management Board

compared the FFO profiles of the two companies.

d) Valuation of Deutsche Wohnen

On the basis of the valuation parameters described in section b) Deutsche

Wohnen is valued as follows:

EPRA NAV. On the basis of the EPRA NAV as of 30 June 2015, the

(undiluted) value of Deutsche Wohnen including goodwill is EUR 6,839.3

million, and excluding goodwill is EUR 6,304.2 million. Therefore, the

EPRA NAV per share, based on the number of outstanding shares of

Deutsche Wohnen (337.4 million shares) including good will is EUR 20.27

(excluding goodwill: EUR 18.69).

For the calculation of the EPRA NAV, the underlying valuation of the real

estate held as financial investments (which represents about 99% of the total

real estate holdings of Deutsche Wohnen and about 86% of the assets) is

conducted initially using acquisition and production costs, including ancillary

costs. After the initial valuation, real estate held as financial investments is

measured at its market value (fair value).

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 25 -

The determination of the market value of individual properties was carried out

using the discounted cash flow (DCF) method and was independently

evaluated by CBRE according to the provisions of the Royal Institution of

Chartered Surveyors (RICS) pursuant to the Red Book and pursuant to

international valuation standards (IVS) on the basis of a DCF model. The

valuation by CBRE the real estate assets of Deutsche Wohnen was conducted

as of 30 June 2015, with the exception of senior citizen properties used by

Katharinenhof. The valuation of senior citizen properties used by

Katharinenhof was conducted by CBRE as of 30 June 2014, whereby the

determination of the EPRA NAVs for the purpose of this Management Board

report was based on the updated values of these senior citizen properties from

the interim report as of 30 June 2015.

According to CBRE, the future revenue and expense streams in connection

with the properties that were assessed were forecast along a 10-year detailed

review period, whereby a lease scenario was assumed, without taking account

of the potential privatization of individual residential units. As part of the

valuation, the cash flows were discounted using discount rates of

approximately 5.7% for the residential property portfolio and 7.0% for the

senior citizen property portfolio (weighted average) and capitalization rates of

approximately 4.6% for the residential property portfolio and 7.2% for the

senior citizen property portfolio (weighted average).

The result of the valuation by CBRE does not differ significantly from the

valuation of the real estate determined by the Company and reported in its

financial statements (on the basis of individual properties not more than 10%

or less than EUR 250.000,00 and, based on total holdings valued,

approximately -0.2%). The valuation reports prepared by CBRE for the real

estate assets as of 30 June 2015 (with the exception of the senior citizen

properties used by Katharinenhof) and the valuation reports prepared by

CBRE for the senior citizen properties used by Katharinenhof as of 30 June

2014 updated to 30 June 2015 are attached hereto as Annex C. For the

purpose of this report, the Management Board adopts as its own all of the

information and statements in these reports, and correspondingly includes

them as part of this Management Board report.

EPRA NAV (diluted). In addition to the undiluted EPRA NAV, in its

quarterly report as of 30 June 2015 Deutsche Wohnen also includes a diluted

EPRA NAV including goodwill in the amount of EUR 7,643.4 million. This

corresponds to a diluted EPRA NAV excluding good will of EUR 7,108.3

million.. The diluted EPRA NAV differs from the undiluted EPRA NAV on

the basis of the assumption that the conversion right from the 2013

convertible bond with the amount of EUR 250 million would have been

exercised at a conversion price of EUR 17.7877, and from the 2014

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 26 -

convertible bond with the amount of EUR 400 million at a conversion price

of EUR 21.4120, which would have reduced liabilities by a total of EUR

804.1 million. As a result of the conversion, the number of Deutsche Wohnen

shares existing as of 30 June 2015 would have increased by 32.7 million,

from 337.4 million to 370.1 million and the EPRA NAV per share to

EUR 20.65 (EUR 19.21 excluding goodwill).

The EPRA NAV was derived as follows:

30 June 2015

EUR mn

undiluted diluted

Investment properties .................................. 10,740.3 10,740.3

Other non-current assets ............................. 919.8 919.8

Current assets .............................................. 867.8 867.8

Total assets ................................................. 12,527.8 12,527.8

Non-current liabilities ................................. -5,795.5 -5,795.5

Current liabilities ........................................ -501.1 -501.1

Convertible bonds ....................................... 804.1

Total liabilities ........................................... -6,296.6 -5,492.5

Equity ......................................................... 6,231.2 7,035.3

Minority interests ........................................ -196.4 -196.4

Equity (before minority interests) ........... 6,034.7 6,838.8

Derivative financial instruments ................. 52.4 52.4

Deferred taxes ............................................. 752.2 752.2

EPRA NAV ................................................ 6,839.3 7,643.4

EPRA NAV per share ............................... 20.27 20.65

Goodwill ..................................................... 535.1 535.1

EPRA NAV excluding goodwill ............... 6,304.2 7,108.3

EPRA NAV excluding goodwill per

share ........................................................... 18.69

19.21

Market capitalization. Based on its market capitalization, the value of

Deutsche Wohnen amounts to EUR 8,900.8 million.

This calculation is based on the closing price of Deutsche Wohnen’s shares

on Xetra of the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) on

the last trading day prior to the publication pursuant to section 10, para. 1, 3,

sentence 1 of the WpÜG in the amount of EUR 24.05 multiplied by 370.1

million. 370.1 million is the total of the number of shares outstanding as of 15

September 2015 (337.4 million) and the number of shares that would result if

there were a conversion of all outstanding convertible bonds at the respective

current conversion price (32.7 million).

Based on the volume-weighted average price (VWAP) during the last 3

months up to the last trading day prior to the publication pursuant to

section 10, para. 1, 3 sentence 1 of the WpÜG of EUR 22.84 per share

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 27 -

(according to Bloomberg) and the, with regard to the market capitalization as

of 15 September 2015, relevant number of 370.1 million bearer shares, the

market capitalization would amount to EUR 8,453.3 million.

e) Valuation of LEG

Based on the previously described valuation parameters, LEG is valued as

follows:

EPRA NAV. On the basis of the EPRA NAV as of 30 June 2015, the

(undiluted) value of LEG including goodwill is EUR 2,969.8 million, and

excluding goodwill is EUR 2,943.9 million. Therefore, the EPRA NAV per

share (base around 58.3 million shares) including good will is EUR 50.98

(excluding goodwill: EUR 50.53).

For the 2014 consolidated financial statement, the market values were

determined internally by a subsidiary of LEG (with the exception of a real

estate portfolio which was acquired by Vonovia SE, formerly known as

Deutsche Annington). Parallel to this, the real estate portfolio was assessed by

an independent external appraiser as of 31 December 2014. This appraisal

report was not published. According to the interim report as of 30 June 2015,

the valuation methods used in this report are the same as the ones used in the

2014 consolidated financial statement. LEG Immo as well determined the

market values for real estate held as financial investments or for sale on the

basis of the forecast net cash flows from the management of properties using

the discounted cash flow (DCF) method. As part of the valuation as of 31

December 2014, the cash flows were discounted using discount rates of on

average 5.93% (weighted average) and capitalization rates in perpetuity of on

average 6.50% (weighted average).

EPRA NAV (diluted). In addition to the undiluted EPRA NAV, in its

quarterly report as of 30 June 2015 LEG also reported a diluted EPRA NAV,

including goodwill, in the amount of EUR 3,329.7 million. This corresponds

to a diluted EPRA NAV of EUR 3,303.8 million, excluding goodwill. The

diluted EPRA NAV was calculated on the assumption that the conversion

right for the outstanding convertible bond with the amount of EUR 300

million was exercised at a conversion price of EUR 58.4317, which would

have reduced liabilities by EUR 359.9 million. This would have increased the

number of LEG Shares as of 30 June 2015 by about 5.1 million from at this

point of thime 58.3 million to 63.4 million and the EPRA NAV per share to

EUR 52.52 (EUR 52.12 excluding goodwill).

Pro forma EPRA NAV (diluted). With the end of the acceptance period and

the fulfilment of the closing conditions (Vollzugsbedingungen) of the

Exchange Offer that must be met before the end of the acceptance period, a

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 28 -

“change of control” provision will be triggered, pursuant to which the

bondholders, inter alia, can demand the conversion at an adjusted conversion

price. Depending on the date on which the acceptance period ends, the

conversion price may be reduced; in the event of an assumed change of

control on 1 December 2015 (approximately 5 1/2 years before the final

maturity of the bond) to EUR 47.4363 (see III.1.b)(3) for the rules of the

bond conditions governing this calculation). In this case, the number of LEG

Shares will increase from (currently) about 58.3 million by about 6.3 million

to 64.6 million. Based on the diluted EPRA NAV and taking into

consideration the adjusted conversion price this results in an EPRA NAV on

a pro-forma basis of EUR 51.56 per share including goodwill (EUR 51.16

excluding goodwill) (the “Pro Forma EPRA NAV (diluted)”).

The EPRA NAV for the valuation as of 30 June 2015 was derived as follows:

30 June 2015

EUR mn

undiluted diluted

Pro-forma

diluted

Investment properties ......................... 6,000.9 6,000.9 6,000.9

Other non-current assets .................... 252.7 252.7 252.7

Current assets ..................................... 321.2 321.2 321.2

Assets held for sale ............................ 8.3 8.3 8.3

Total assets ........................................ 6,583.1 6,583.1 6,583.1

Non-current liabilities ........................ -3,245.5 -3,245.5 -3,245.5

Current liabilities ............................... -890.1 -890.1 -890.1

Convertible bonds .............................. 359.9 359.9

Total liabilities .................................. -4,135.6 -3,775.7 -3,775.7

Equity ................................................ 2,447.5 2,807.4 2,807.4

Non-controlling shares ....................... -14.9 -14.9 -14.9

Equity (before minority

interests) ............................................ 2,432.6 2,792.5 2,792.5

Derivative financial instruments ........ 119.3 119.3 119.3

Deferred taxes .................................... 417.9 417.9 417.9

EPRA NAV ....................................... 2,969.8 3,329.7 3,329.7

EPRA NAV per share ...................... 50.98 52.52 51.56

Goodwill ............................................ 25.9 25.9 25.9

EPRA NAV excluding goodwill ...... 2,943.9 3,303.8 3,303.8

EPRA NAV excluding goodwill

per share ........................................... 50.53 52.12 51.16

Market capitalization. Based on its market capitalization, LEG’s value is

EUR 4,454.7 million.

This calculation is based on the closing price of LEG’s shares on Xetra of the

Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) on the last trading

day prior to the publication pursuant to section 10, para. 1, 3, sentence 1 of

Annex 1 – Report of the Management Board purs. to sec. 186, para. 4, sent. 2 AktG

- 29 -

the WpÜG in the amount of EUR 70.27 multiplied by 63.4 million. 63.4

million is the total of the number of shares (58.3 million) outstanding as of

this reference date (Stichtag) and the number of shares that would result if

there were a conversion of all outstanding convertible bonds at the conversion

price as of 18 September 2015 (5.1 million).

Based on the volume-weighted average price (VWAP) during the last 3