Embed Size (px)

Citation preview

Press Conference 2011

Frankfurt am Main, 29.03.2011

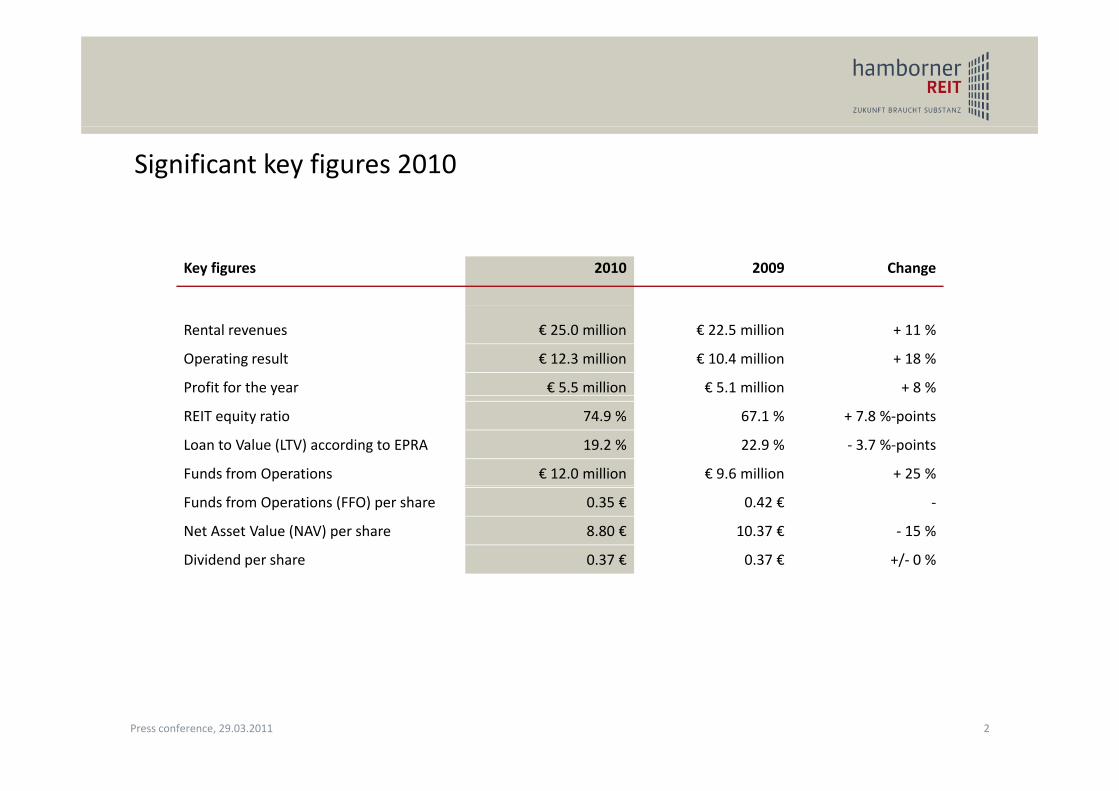

Significant key figures 2010

Key figures 2010 2009 Change

Rental revenues € 25.0 million € 22.5 million + 11 %

Operating result € 12.3 million € 10.4 million + 18 %

Profit for the year € 5.5 million € 5.1 million + 8 %

REIT equity ratio 74.9 % 67.1 % + 7.8 %‐points

Loan to Value (LTV) according to EPRA 19.2 % 22.9 % ‐ 3.7 %‐points

Funds from Operations € 12.0 million € 9.6 million + 25 %

Funds from Operations (FFO) per share 0.35 € 0.42 € ‐

Net Asset Value (NAV) per share 8.80 € 10.37 € ‐ 15 %

Dividend per share 0.37 € 0.37 € +/‐ 0 %

2Press conference, 29.03.2011

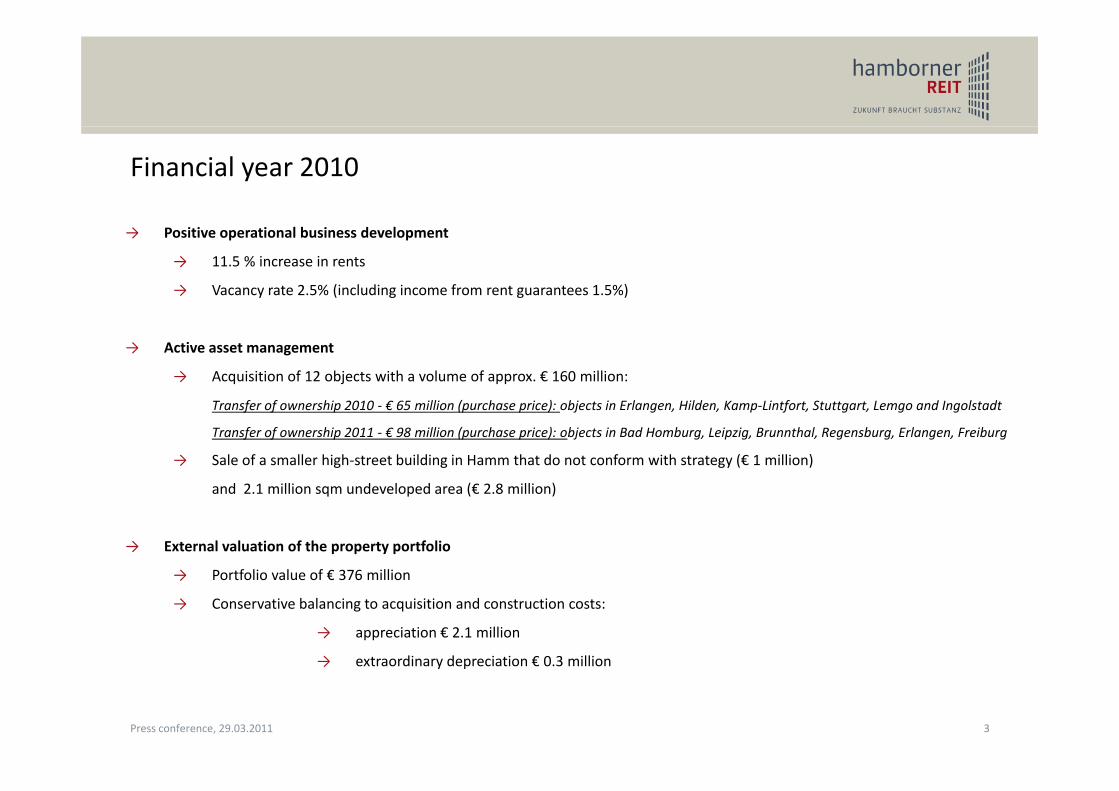

Financial year 2010

→ Positive operational business development

→ 11.5 % increase in rents

→ Vacancy rate 2.5% (including income from rent guarantees 1.5%)

→ Active asset management

→ Acquisition of 12 objects with a volume of approx. € 160 million:

Transfer of ownership 2010 ‐ € 65 million (purchase price): objects in Erlangen, Hilden, Kamp‐Lintfort, Stuttgart, Lemgo and Ingolstadt

Transfer of ownership 2011 ‐ € 98 million (purchase price): objects in Bad Homburg, Leipzig, Brunnthal, Regensburg, Erlangen, Freiburg

→ Sale of a smaller high‐street building in Hamm that do not conform with strategy (€ 1 million)

d 2 1 illi d l d (€ 2 8 illi )and 2.1 million sqm undeveloped area (€ 2.8 million)

→ External valuation of the property portfolio

→ Portfolio value of € 376 million→ Portfolio value of € 376 million

→ Conservative balancing to acquisition and construction costs:

→ appreciation € 2.1 million

→ extraordinary depreciation € 0.3 million→ extraordinary depreciation € 0.3 million

3Press conference, 29.03.2011

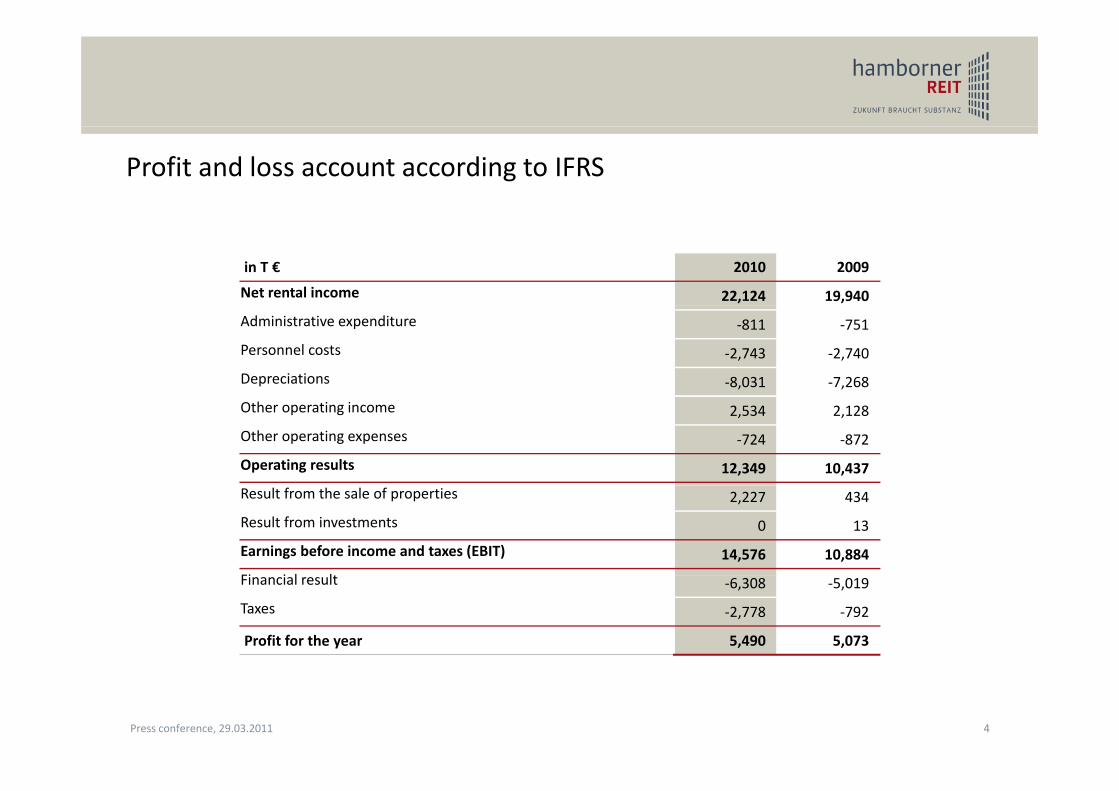

Profit and loss account according to IFRS

in T € 2010 2009

Net rental income 22,124 19,940

Administrative expenditure ‐811 ‐751

Personnel costs ‐2,743 ‐2,740

Depreciations ‐8,031 ‐7,268

Other operating income 2,534 2,128

Other operating expenses ‐724 ‐872

Operating results 12,349 10,437

Result from the sale of properties 2,227 434

Result from investments 0 13

Earnings before income and taxes (EBIT) 14,576 10,884

Fi i l lFinancial result ‐6,308 ‐5,019

Taxes ‐2,778 ‐792

Profit for the year 5,490 5,073

4Press conference, 29.03.2011

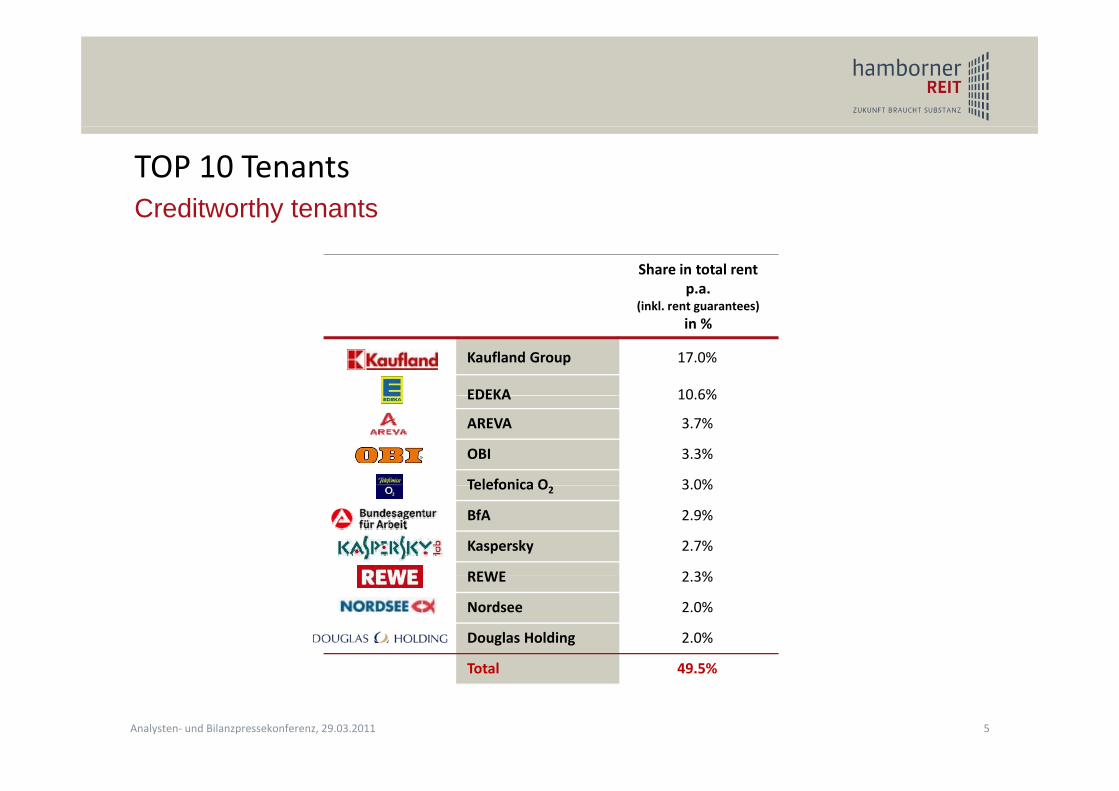

TOP 10 TenantsCreditworthy tenants

Share in total rent p.a.

(inkl rent guarantees)

Creditworthy tenants

(inkl. rent guarantees) in %

Kaufland Group 17.0%

EDEKA 10 6%EDEKA 10.6%

AREVA 3.7%

OBI 3.3%

Telefonica O 3 0%Telefonica O2 3.0%

BfA 2.9%

Kaspersky 2.7%

REWE 2 3%REWE 2.3%

Nordsee 2.0%

Douglas Holding 2.0%

T t l 49 5%

5Analysten‐ und Bilanzpressekonferenz, 29.03.2011

Total 49.5%

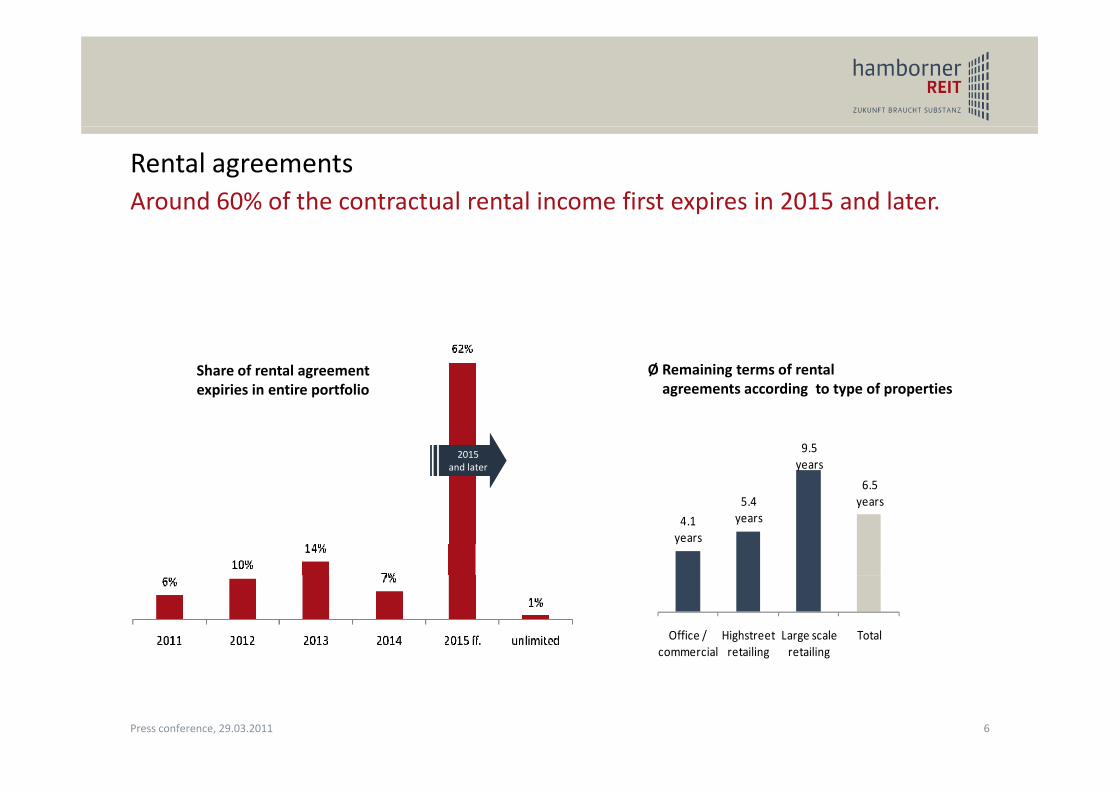

Rental agreementsAround 60% of the contractual rental income first expires in 2015 and later.

Share of rental agreement expiries in entire portfolio

Ø Remaining terms of rental agreements according to type of properties

9.5years

6 5

p p

2015 and later

g g yp p p

4.1years

5.4years

6.5years

Office / commercial

Highstreet retailing

Large scale retailing

Total

6Press conference, 29.03.2011

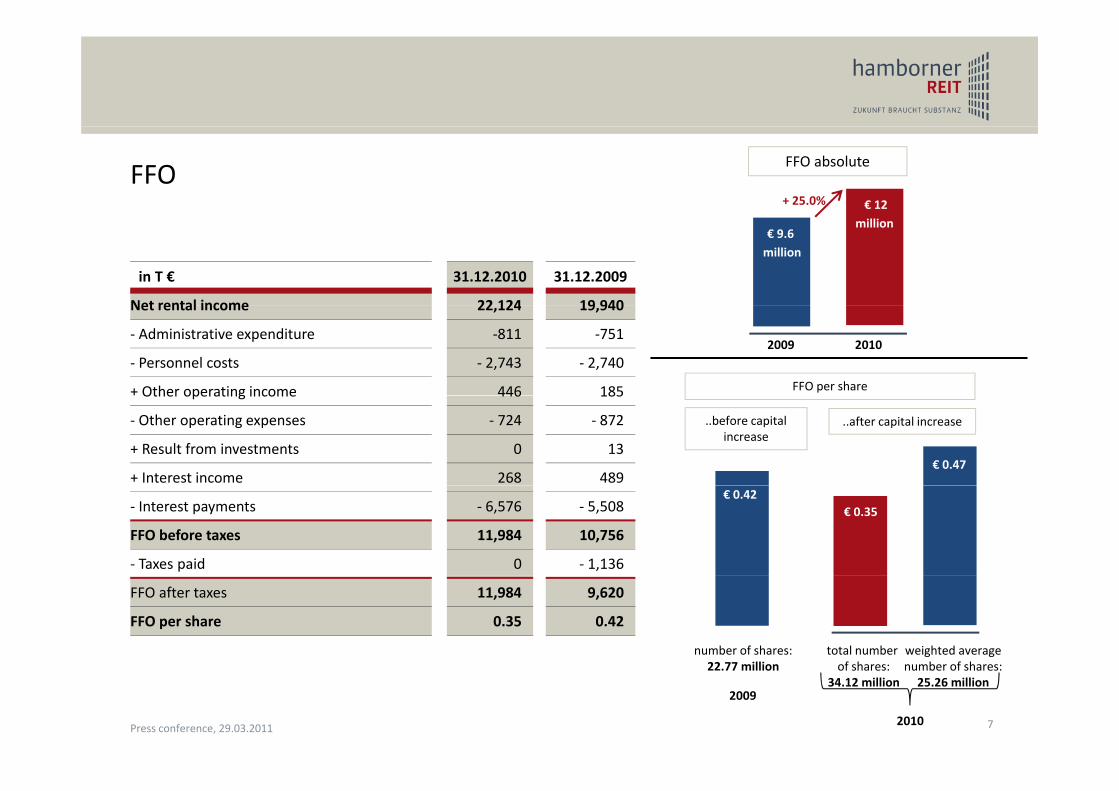

FFO€ 12+ 25.0%

FFO absolute

in T € 31.12.2010 31.12.2009

Net rental income 22 124 19 940

million€ 9.6 million

Net rental income 22,124 19,940

‐ Administrative expenditure ‐811 ‐751

‐ Personnel costs ‐ 2,743 ‐ 2,740

+ Other operating income 446 185

20102009

FFO per share Other operating income 446 185

‐ Other operating expenses ‐ 724 ‐ 872

+ Result from investments 0 13

+ Interest income 268 489€ 0.47

..after capital increase..before capital increase

‐ Interest payments ‐ 6,576 ‐ 5,508

FFO before taxes 11,984 10,756

‐ Taxes paid 0 ‐ 1,136

€ 0.35€ 0.42

FFO after taxes 11,984 9,620

FFO per share 0.35 0.42

total number of shares:

weighted averagenumber of shares:

number of shares:22 77 million

72010

of shares:34.12 million

number of shares:25.26 million

2009

22.77 million

Press conference, 29.03.2011

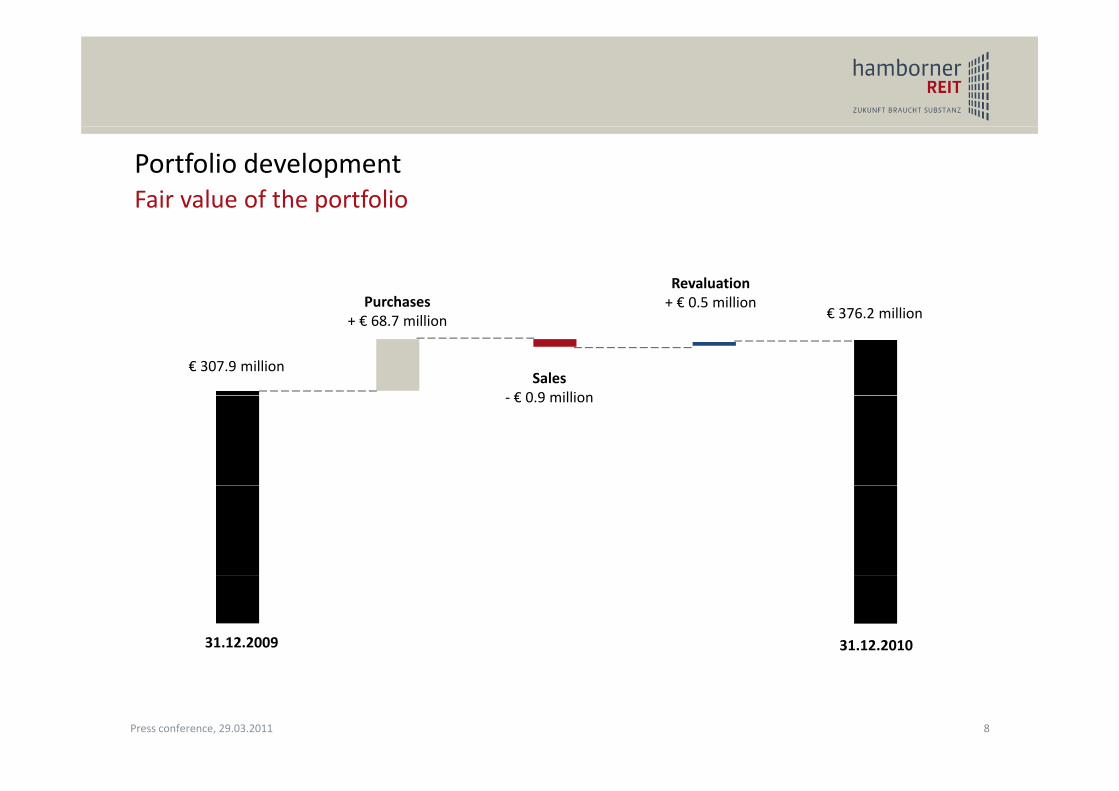

Portfolio developmentFair value of the portfolio

PurchasesRevaluation + € 0.5 million

€ 307.9 million

€ 376.2 millionPurchases

+ € 68.7 million

Sales€ 0 9 million

+ € 0.5 million

‐ € 0.9 million

31.12.2009 31.12.2010

8Press conference, 29.03.2011

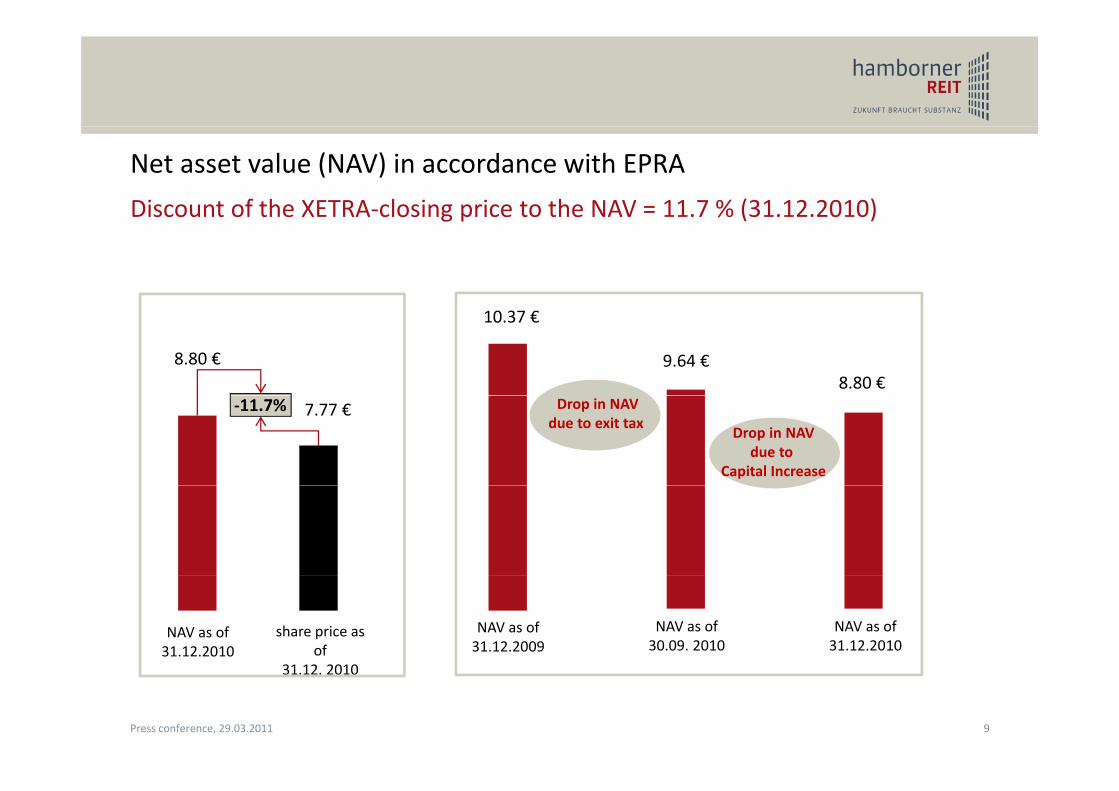

Net asset value (NAV) in accordance with EPRA

Discount of the XETRA‐closing price to the NAV = 11.7 % (31.12.2010)Discount of the XETRA closing price to the NAV 11.7 % (31.12.2010)

8.80 €8.80 €

10.37 €

9.64 €

7.77 €‐11.7% Drop in NAVdue to exit tax

Drop in NAVdue to

Capital Increase

NAV as of 31.12.2010

share price as of

31 12 2010

NAV as of 31.12.2009

NAV as of 31.12.2010

NAV as of 30.09. 2010

31.12. 2010

9Press conference, 29.03.2011

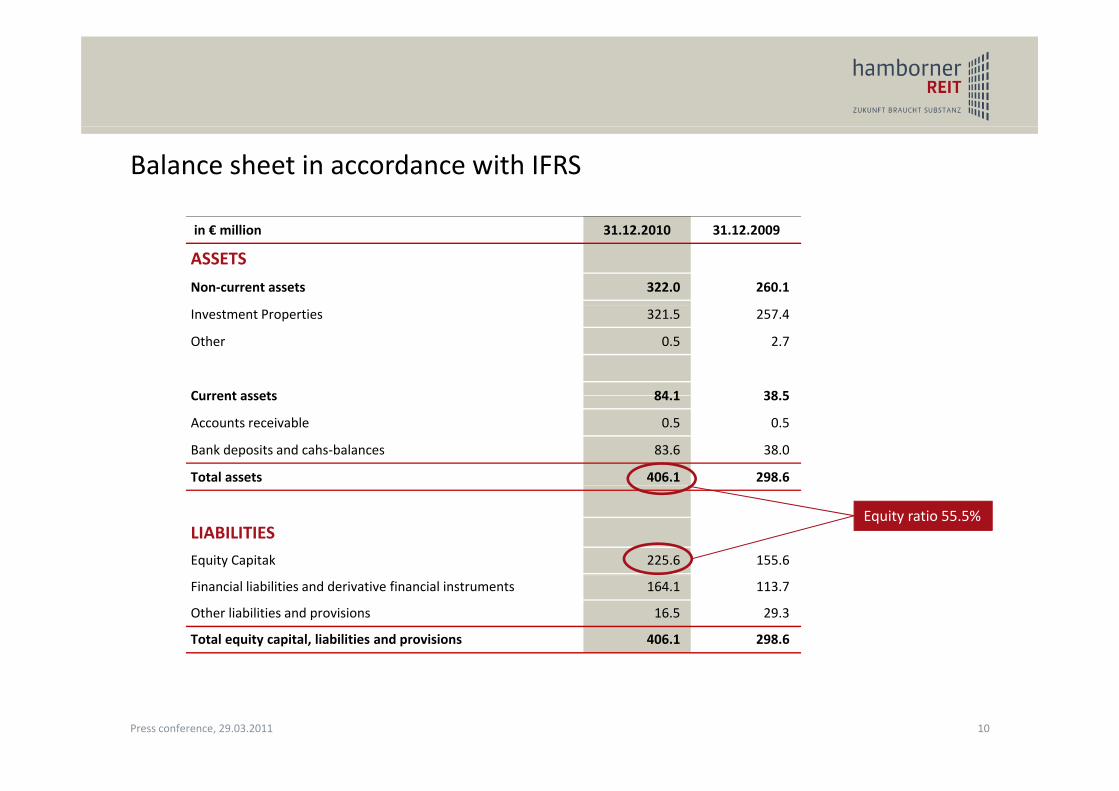

Balance sheet in accordance with IFRS

in € million 31.12.2010 31.12.2009

ASSETS

Non‐current assets 322.0 260.1

Investment Properties 321.5 257.4

Other 0.5 2.7

Current assets 84 1 38 5Current assets 84.1 38.5

Accounts receivable 0.5 0.5

Bank deposits and cahs‐balances 83.6 38.0

Total assets 406.1 298.6

LIABILITIESEquity Capitak 225.6 155.6

Equity ratio 55.5%

Financial liabilities and derivative financial instruments 164.1 113.7

Other liabilities and provisions 16.5 29.3

Total equity capital, liabilities and provisions 406.1 298.6

10Press conference, 29.03.2011

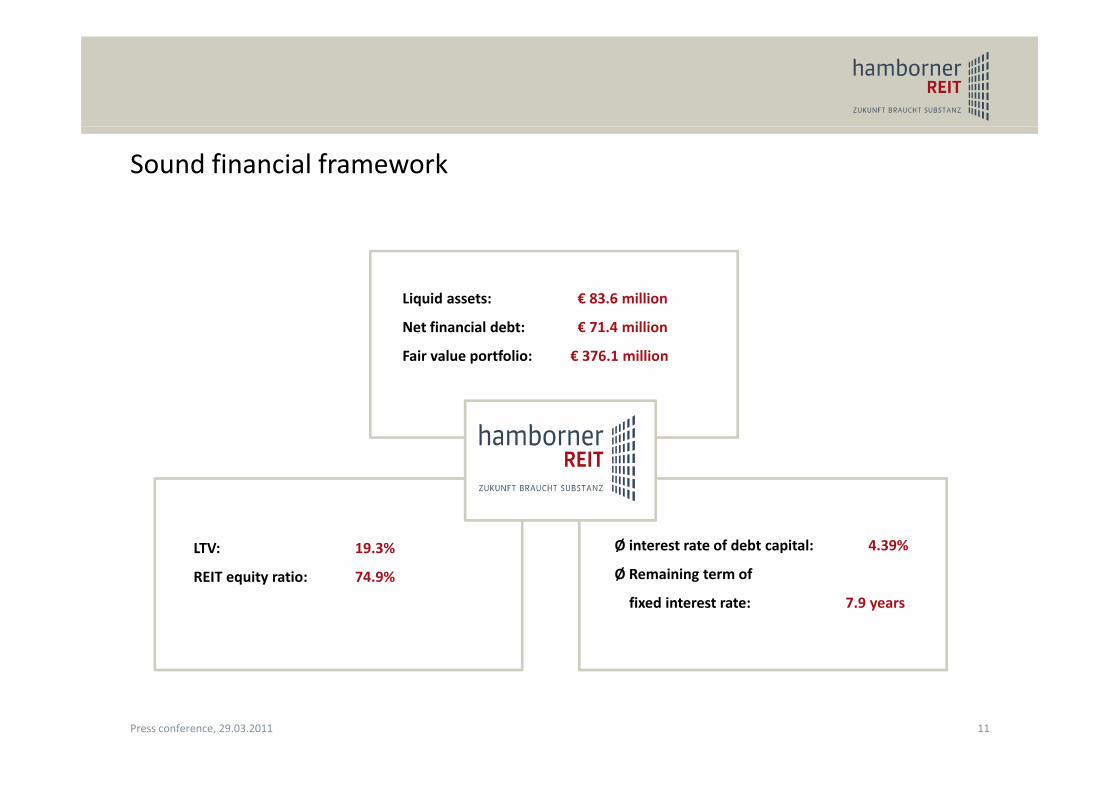

Sound financial framework

Liquid assets: € 83.6 millionq

Net financial debt: € 71.4 million

Fair value portfolio: € 376.1 million

LTV: 19.3%

REIT equity ratio: 74 9%

Ø interest rate of debt capital: 4.39%

Ø Remaining term ofREIT equity ratio: 74.9% Ø Remaining term of

fixed interest rate: 7.9 years

11Press conference, 29.03.2011

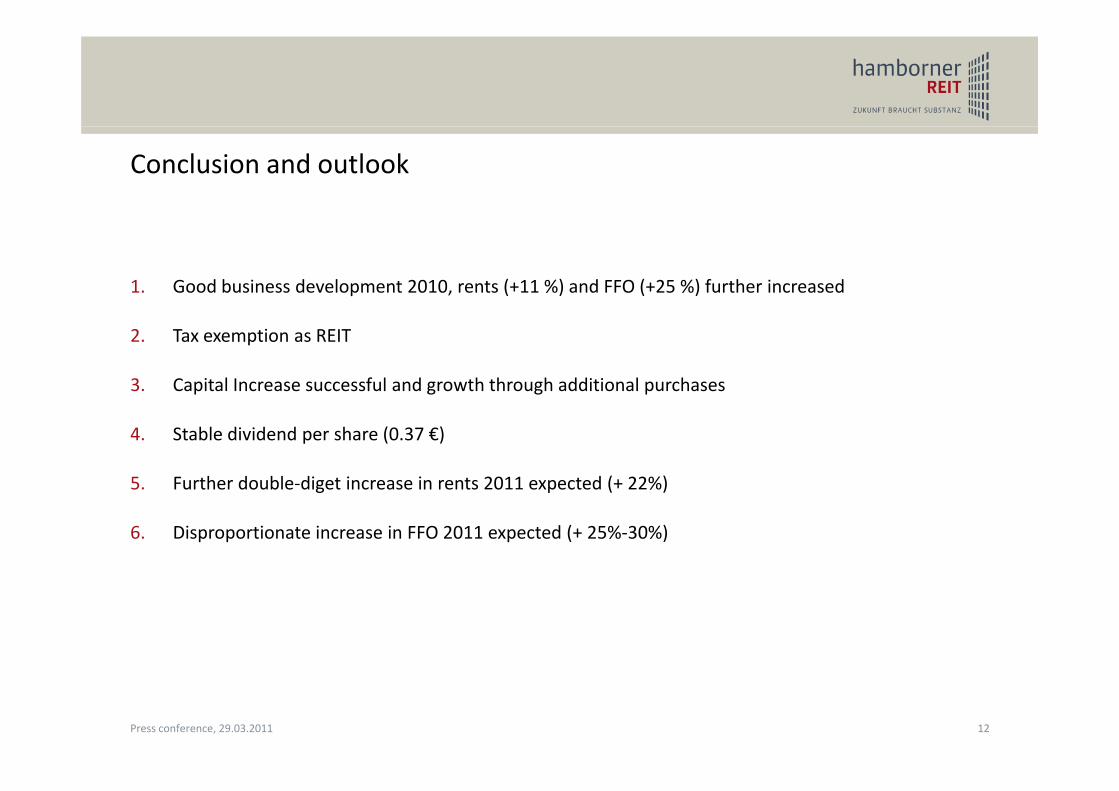

Conclusion and outlook

1. Good business development 2010, rents (+11 %) and FFO (+25 %) further increased

2. Tax exemption as REIT

3. Capital Increase successful and growth through additional purchases

4. Stable dividend per share (0.37 €)

5 Further double‐diget increase in rents 2011 expected (+ 22%)5. Further double diget increase in rents 2011 expected (+ 22%)

6. Disproportionate increase in FFO 2011 expected (+ 25%‐30%)

12Press conference, 29.03.2011

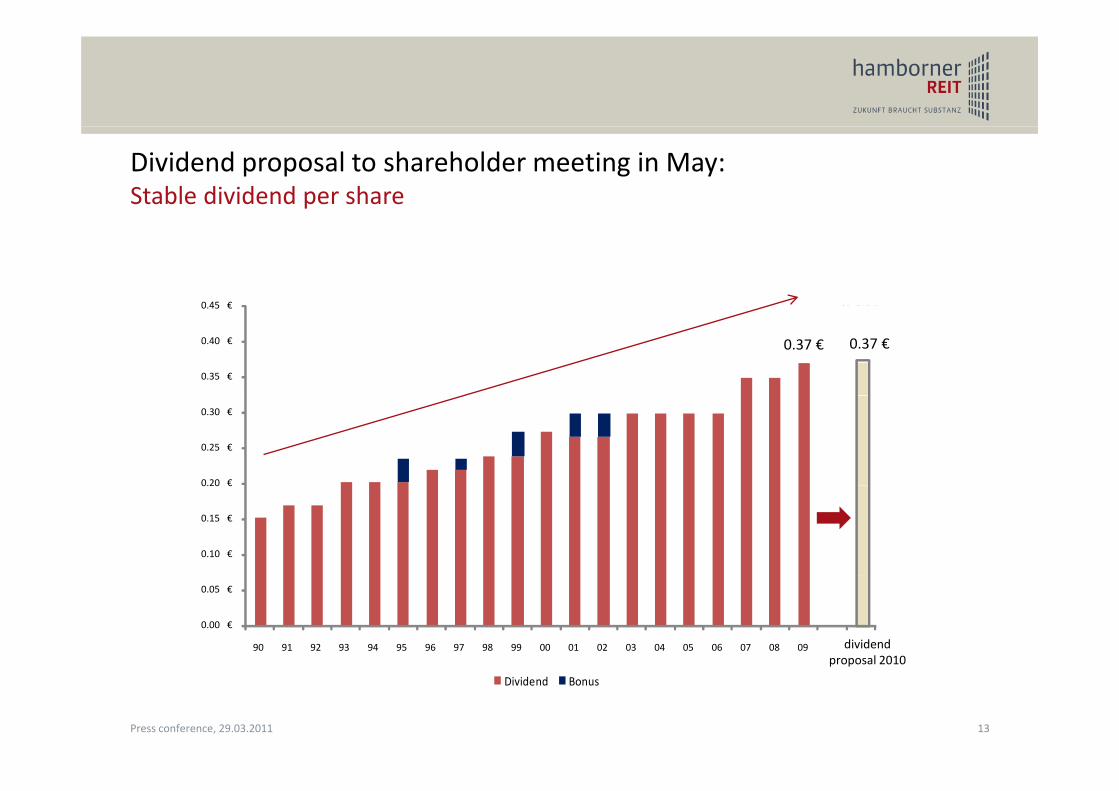

Dividend proposal to shareholder meeting in May: Stable dividend per share

0 42 €0 45 €

0.37 €

0.42 €

0.35 €

0.40 €

0.45 €

0.37 €

0.20 €

0.25 €

0.30 €

0.10 €

0.15 €

0.20 €

0.00 €

0.05 €

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 FFO* 2010

dividendproposal 2010

Dividend Bonus

p p

13Press conference, 29.03.2011

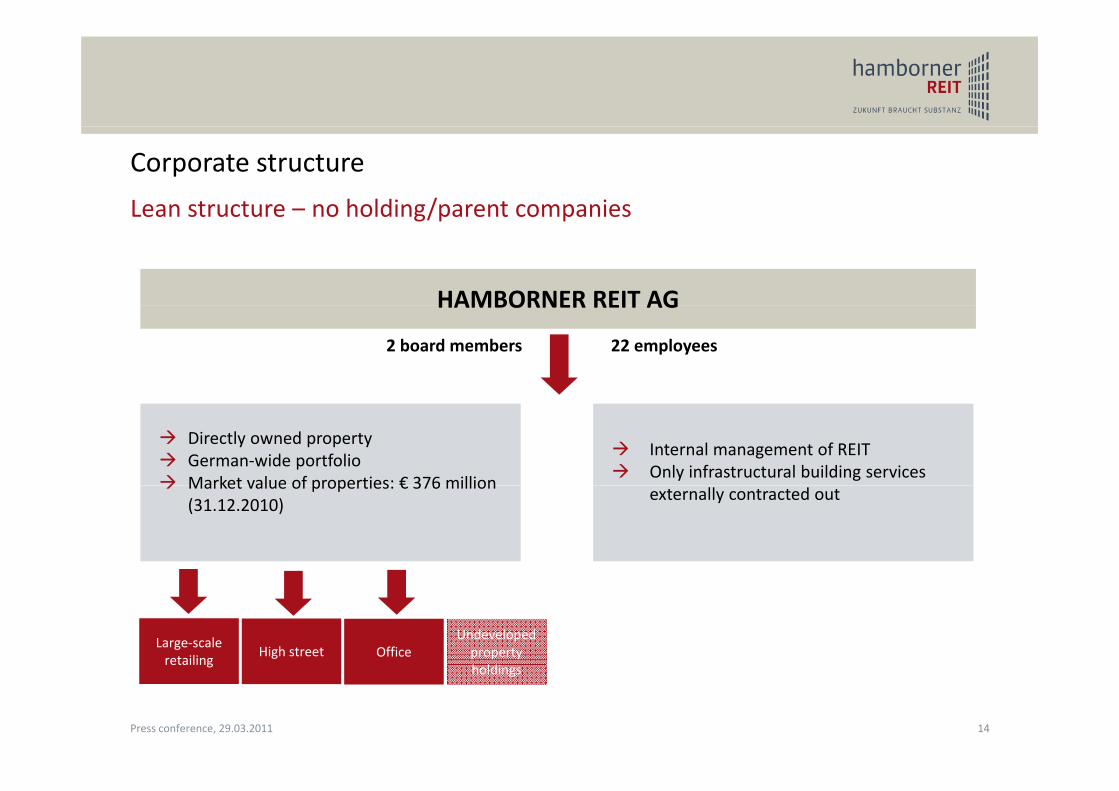

Corporate structure

Lean structure – no holding/parent companiesLean structure no holding/parent companies

HAMBORNER REIT AGHAMBORNER REIT AG

22 employees2 board members

Directly owned propertyGerman‐wide portfolioMarket value of properties: € 376 million

Internal management of REITOnly infrastructural building services

Market value of properties: € 376 million(31.12.2010)

externally contracted out

High street OfficeLarge‐scale retailing

Undeveloped property h ldi

gholdings

14Press conference, 29.03.2011

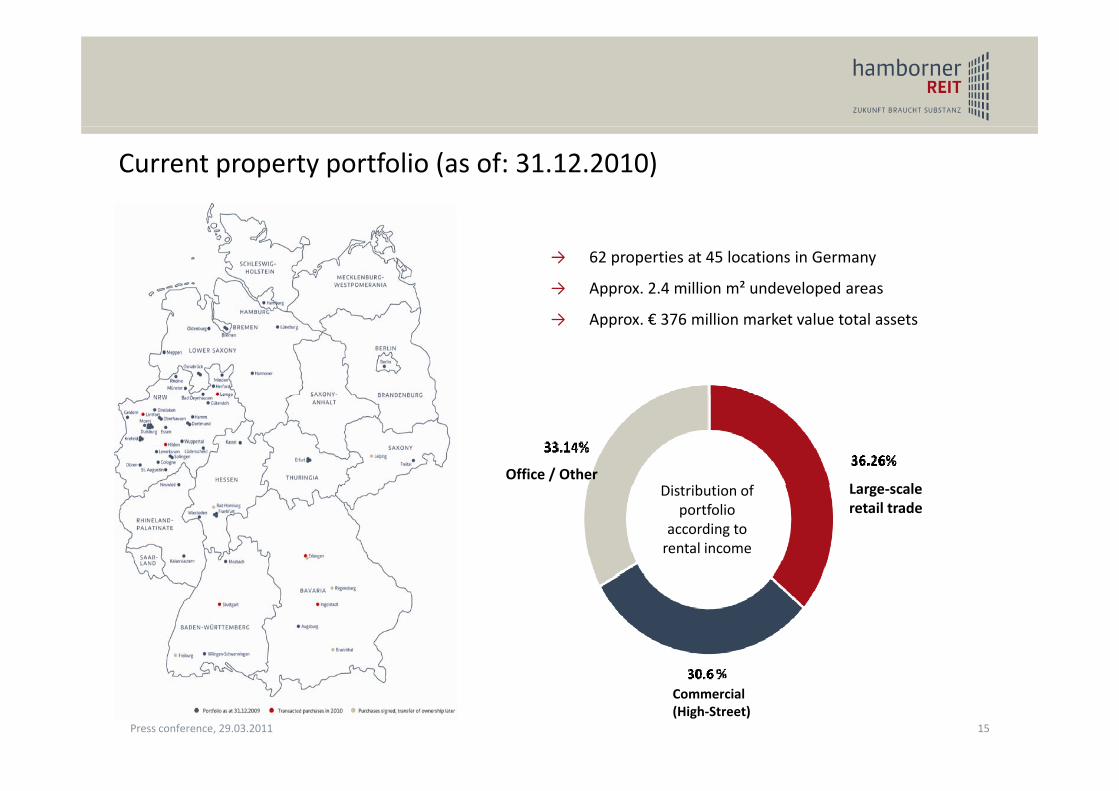

Current property portfolio (as of: 31.12.2010)

→ 62 properties at 45 locations in Germany

→ Approx. 2.4 million m² undeveloped areas

→ Approx. € 376 million market value total assets

i ib i fOffice / Other

L lDistribution of portfolio

according to rental income

Large‐scaleretail trade

Ingolstadt

Commercial (High‐Street)

15Press conference, 29.03.2011

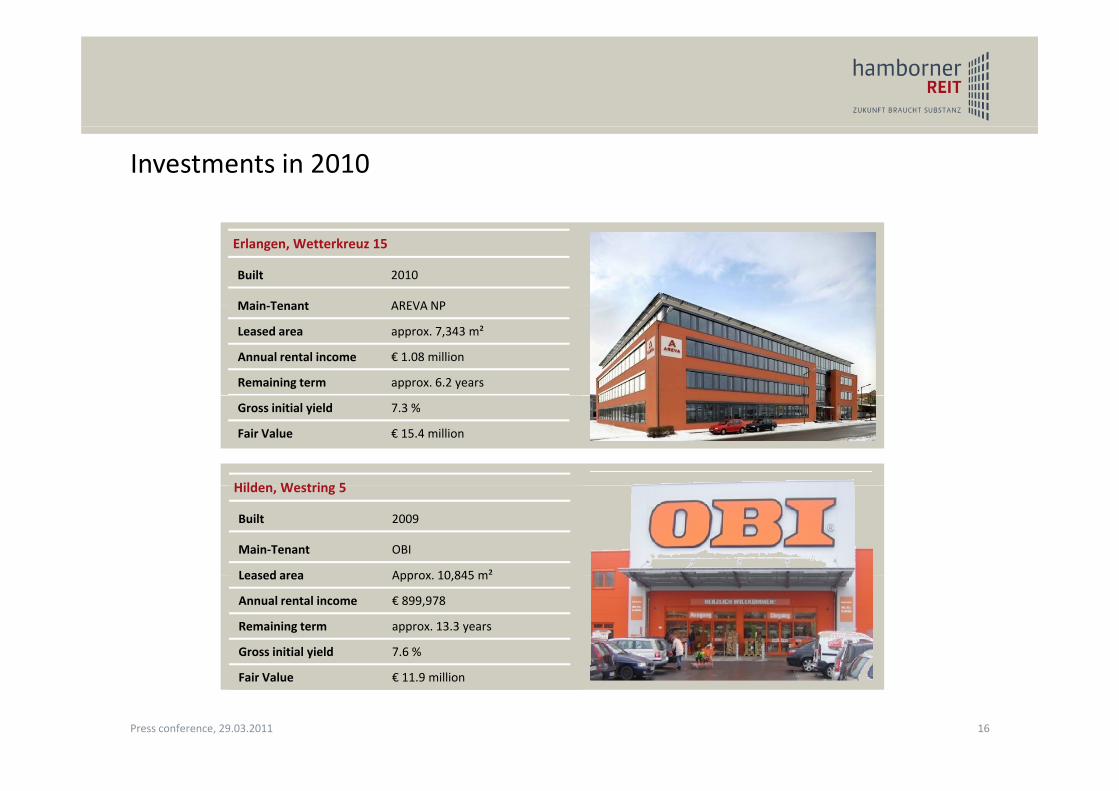

Investments in 2010

Erlangen, Wetterkreuz 15

Built 2010

Main Tenant AREVA NPMain‐Tenant AREVA NP

Leased area approx. 7,343 m²

Annual rental income € 1.08 million

Remaining term approx. 6.2 years

Gross initial yield 7.3 %

Fair Value € 15.4 million

Hilden Westring 5Hilden, Westring 5

Built 2009

Main‐Tenant OBI

Leased area Approx 10 845 m²Leased area Approx. 10,845 m

Annual rental income € 899,978

Remaining term approx. 13.3 years

Gross initial yield 7.6 %

Fair Value € 11.9 million

16Press conference, 29.03.2011

Investments in 2010

Kamp‐Lintfort, Moerser Str. 247

Built 2008

Main‐Tenant C&A dmMain‐Tenant C&A, dm

Leased area approx. 2,093 m²

Annual rental income € 250,397

Remaining term approx. 8.8 years

Gross initial yield 7.7 %

Fair Value € 3.4 million

Stuttgart Stammheimer Str 10Stuttgart, Stammheimer Str. 10

Built 2010

Main‐Tenant EDEKA

Leased area approx 6 395 m²Leased area approx. 6,395 m

Annual rental income € 1.2 million

Remaining term approx. 17.5 years

Gross initial yield 7.1 %

Fair Value € 16.8 million

17Press conference, 29.03.2011

Investments in 2010

Ingolstadt, Despagstraße 3

Built 2008

Main‐Tenant Kaspersky and otherMain‐Tenant Kaspersky and other

Leased area approx. 5,623 m²

Annual rental income € 868,951

Remaining term approx. 9.3 years

Gross initial yield 7.8 %

Fair Value € 12.9 million

Lemgo Mittelstraße 24 28Lemgo, Mittelstraße 24‐28

Built 1970, rebuilt in 2010

Main‐Tenant C&A, H&M

Leased area approx 4 600 m²Leased area approx. 4,600 m

Annual rental income € 479,040

Remaining term approx. 9.8 years

Gross initial yield 7.0 %

Fair Value € 8.2 million

18Press conference, 29.03.2011

Investments in 2010, transfer of ownership in 2011

Brunnthal, Eugen‐Sänger‐Ring 7

Built 2010

Main‐Tenant SFC Energy AGMain‐Tenant SFC Energy AG

Leased area approx. 6,700 m²

Annual rental income approx. € 912,490

Remaining term approx. 9.3 years

Gross initial yield 7.6 %

Purchase price € 12 million

Bad Homburg Louisenstr 55 57Bad Homburg, Louisenstr. 55‐57

Built 1985

Main‐Tenant Naspa, Hussel, Hof Apotheke,…

Leased area approx 3 200m²Leased area approx. 3,200m

Annual rental income € 832,117

Remaining term approx. 3.7 years

Gross initial yield 6.1 %

19

Purchase price € 13.7 million

Press conference, 29.03.2011

Investments in 2010, transfer of ownership in 2011

Leipzig, Brandenburger Str. 21

Built 2010

Main‐Tenant OBIMain‐Tenant OBI

Leased area approx. 11,000 m²

Annual rental income approx. € 889,527

Remaining term approx. 13.8 years

Gross initial yield 7.6 %

Purchase price € 11.6 million

Regensburg Hildegard von Bingen Str 1Regensburg, Hildegard‐von‐Bingen‐Str. 1

Built 2007

Main‐Tenant different medical practices

Leased area approx 8 800 m²Leased area approx. 8,800 m

Annual rental income approx. € 1.432 million

Remaining term approx. 7.3 years

Gross initial yield 6.8 %

20

Purchase price € 21.0 million

Press conference, 29.03.2011

l ll ö h lh i k

Investments in 2010, transfer of ownership in 2011

Erlangen, Allee am Röthelheimpark 11‐15

Built 2010/2011

Main‐Tenant Konsum, dm, Pfrimmer and other

L d 11 600 ²Leased area approx. 11,600 m²

Annual rental income approx. € 1.917 million

Remaining term approx. 9.9 years

Gross initial yield 6.9 %

Purchase price € 27.8 million

Investments in 2010, transfer of ownership in 2012

Freiburg, E‐Center

Built 2011/2012

Main‐Tenant EDEKA

Leased area approx. 4,000 m²

Annual rental income € 860,000

Remaining term 18 years

Gross initial yield 7.5 %

Purchase price € 12 million

21Press conference, 29.03.2011

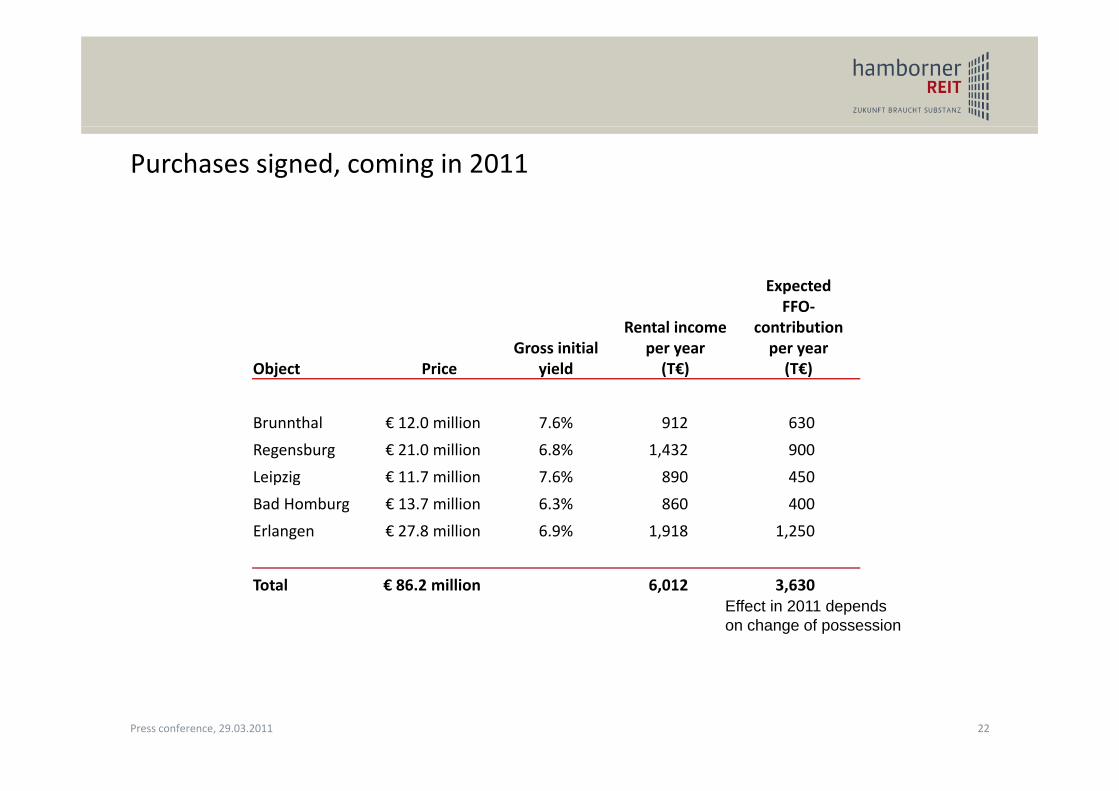

Purchases signed, coming in 2011

ExpectedFFO

Object PriceGross initial

yield

Rental incomeper year(T€)

FFO‐contributionper year(T€)

Brunnthal € 12.0 million 7.6% 912 630

Regensburg € 21.0 million 6.8% 1,432 900

Leipzig € 11.7 million 7.6% 890 450

Bad Homburg € 13.7 million 6.3% 860 400

Erlangen € 27.8 million 6.9% 1,918 1,250

Total € 86.2 million 6,012 3,630Effect in 2011 depends on change of possession

22Press conference, 29.03.2011

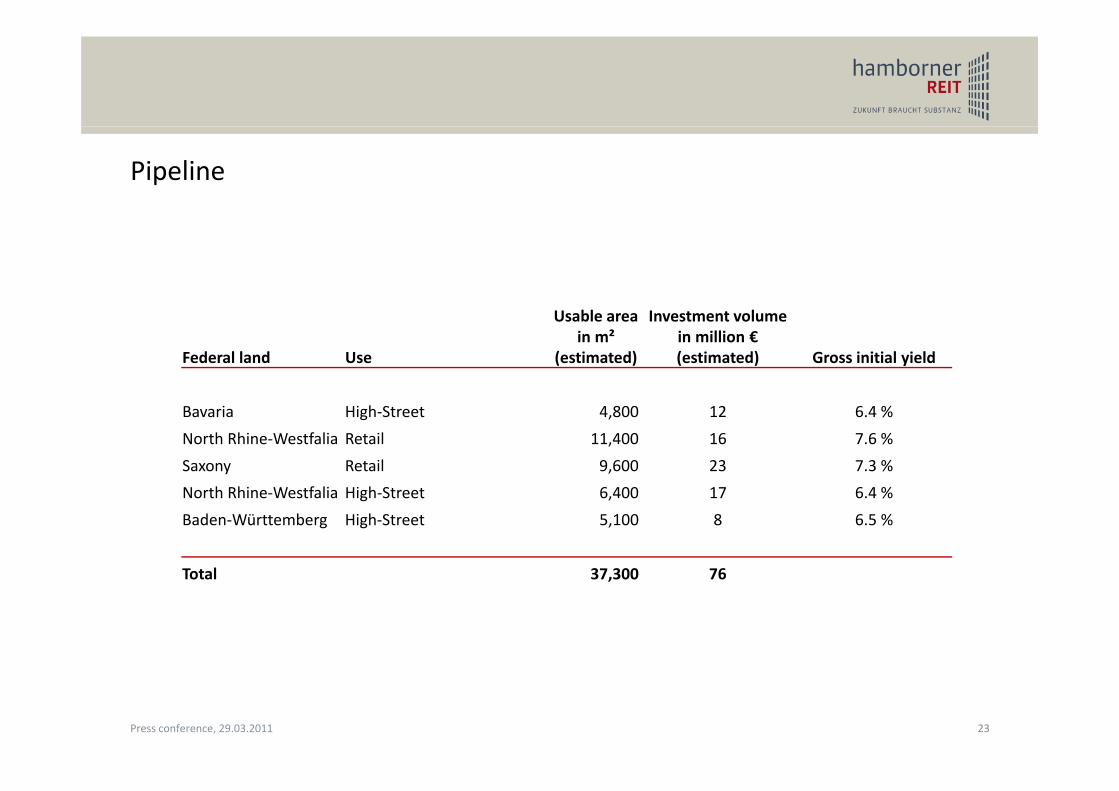

Pipeline

Federal land Use

Usable areain m²

(estimated)

Investment volumein million €(estimated) Gross initial yield

Bavaria High‐Street 4,800 12 6.4 %

North Rhine‐Westfalia Retail 11,400 16 7.6 %

Saxony Retail 9,600 23 7.3 %

North Rhine‐Westfalia High‐Street 6,400 17 6.4 %

Baden‐Württemberg High‐Street 5,100 8 6.5 %

Total 37 300 76Total 37,300 76

23Press conference, 29.03.2011

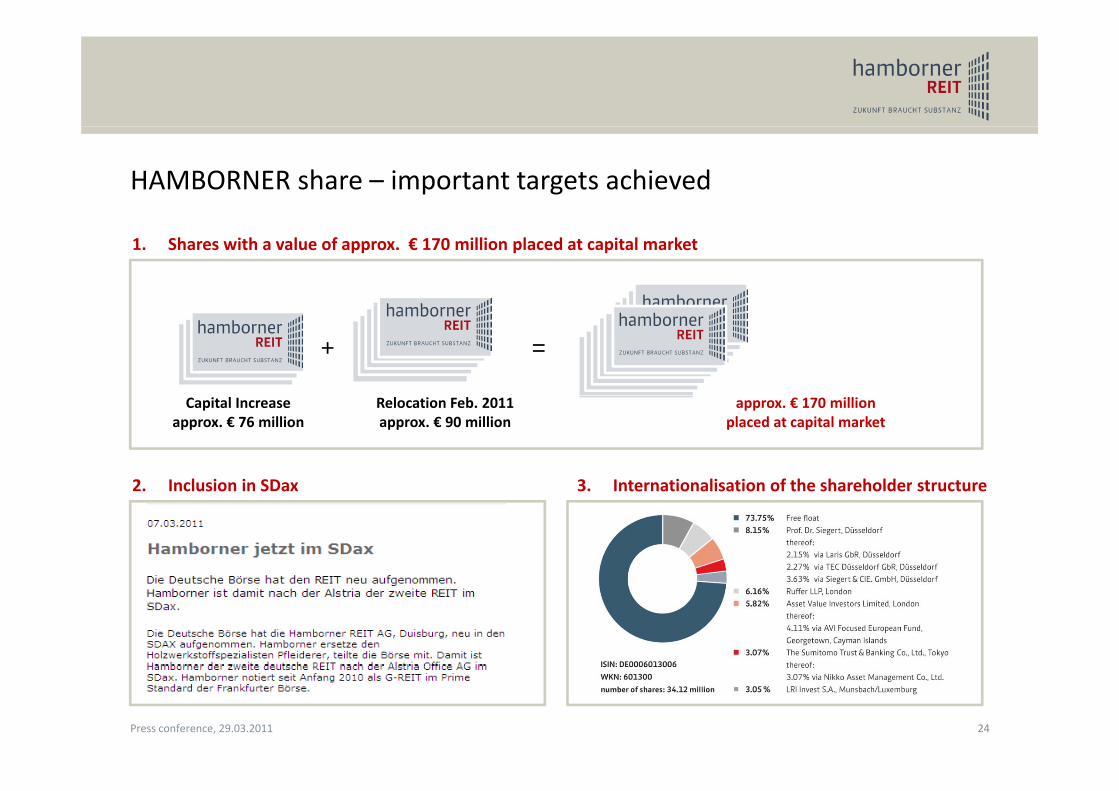

HAMBORNER share – important targets achieved

1. Shares with a value of approx. € 170 million placed at capital market

+ =

Capital Increaseapprox. € 76 million

Relocation Feb. 2011approx. € 90 million

approx. € 170 millionplaced at capital market

2 Inclusion in SDax 3 Internationalisation of the shareholder structure2. Inclusion in SDax 3. Internationalisation of the shareholder structure

24Press conference, 29.03.2011

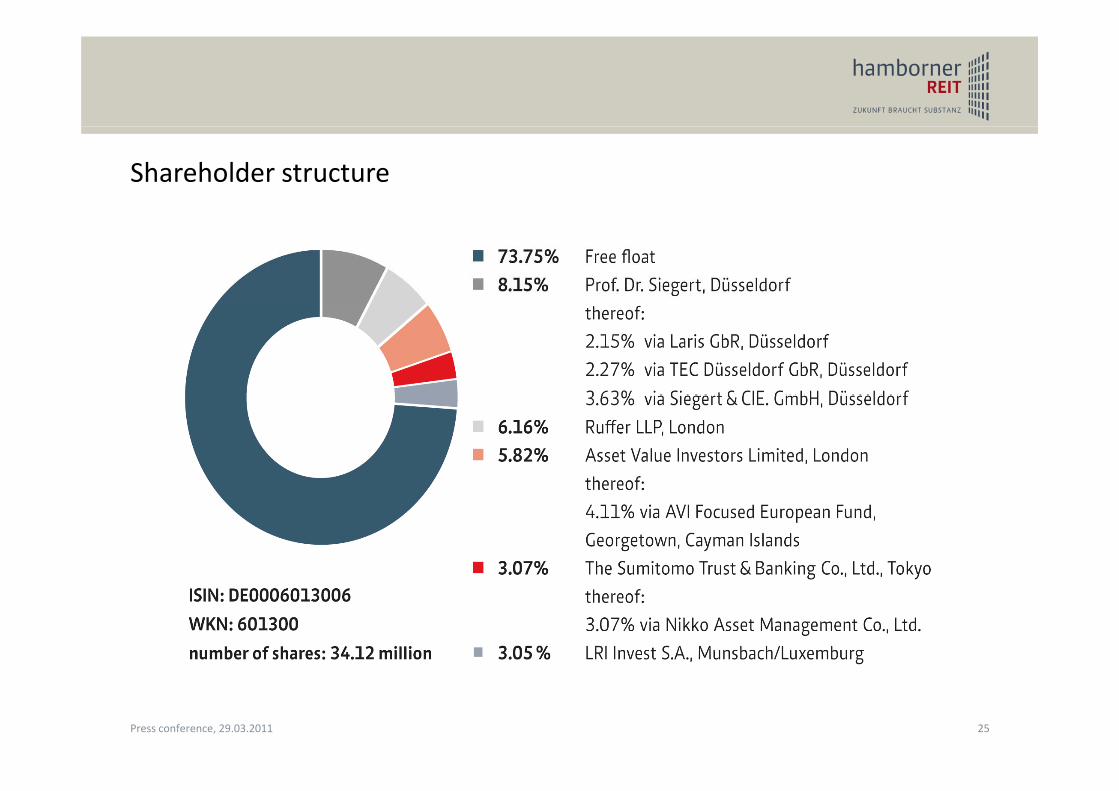

Shareholder structure

25Press conference, 29.03.2011

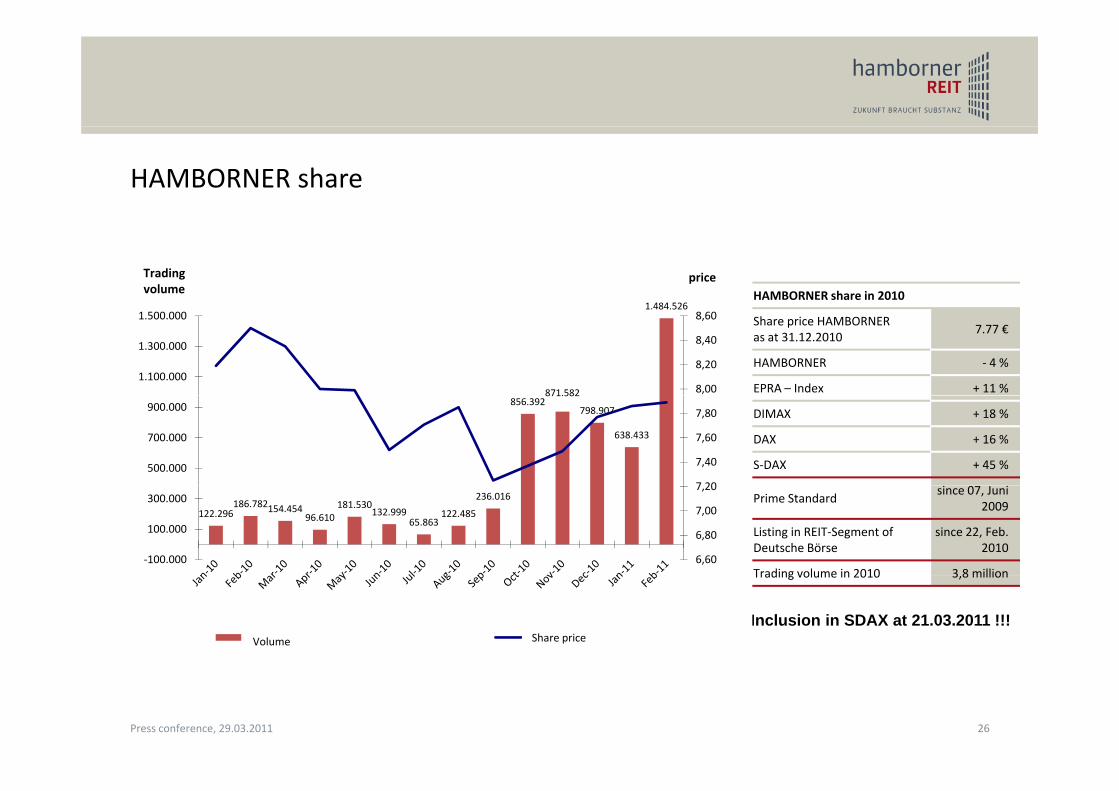

HAMBORNER share

HAMBORNER share in 2010Kurs1 484 526

Trading volume

price

Share price HAMBORNER as at 31.12.2010

7.77 €

HAMBORNER ‐ 4 %

EPRA – Index + 11 %871.582

1.484.526

8,00

8,20

8,40

8,60

1.100.000

1.300.000

1.500.000

DIMAX + 18 %

DAX + 16 %

S‐DAX + 45 %

856.392871.582

798.907

638.433

7 20

7,40

7,60

7,80

500.000

700.000

900.000

Prime Standardsince 07, Juni

2009

Listing in REIT‐Segment of Deutsche Börse

since 22, Feb.2010

Trading volume in 2010 3 8 million

122.296186.782154.454

96.610181.530

132.99965.863

122.485

236.016

6,60

6,80

7,00

7,20

‐100.000

100.000

300.000

Trading volume in 2010 3,8 million

Inclusion in SDAX at 21.03.2011 !!!Volumen in Stück Aktien (alle Börsen) Schlusskurs (alle Börsen)Volume Share price

26Press conference, 29.03.2011

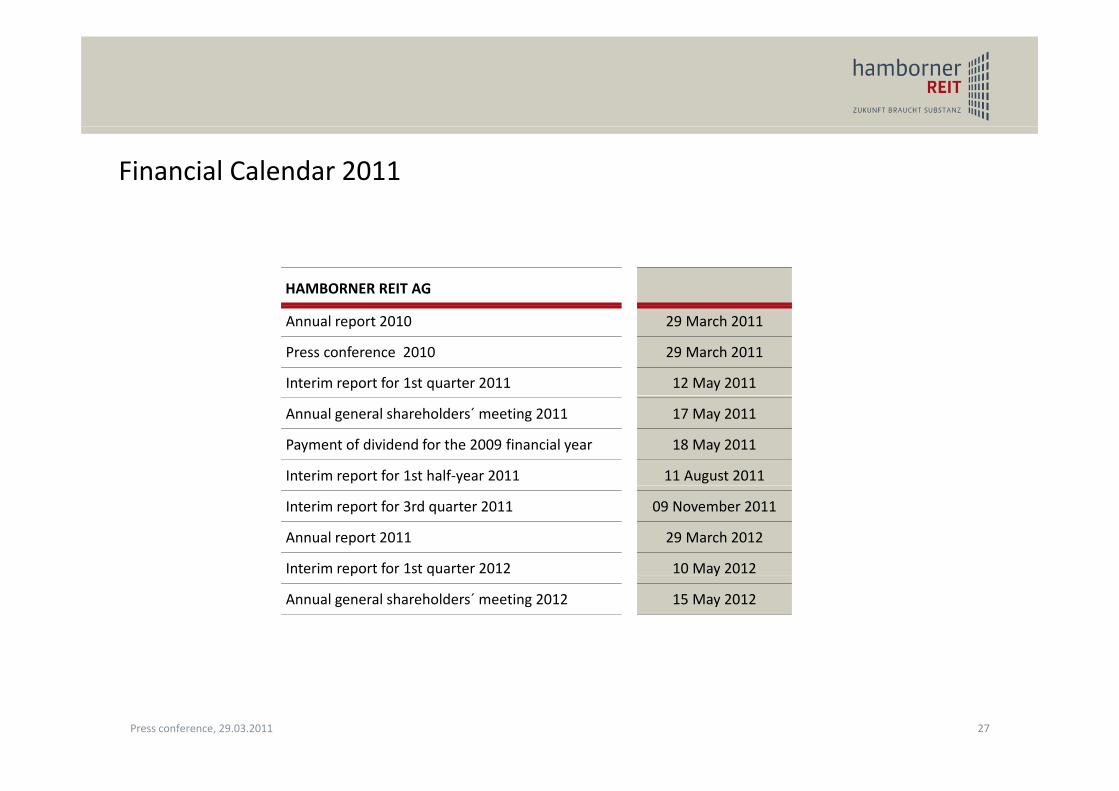

Financial Calendar 2011

HAMBORNER REIT AG

Annual report 2010 29 March 2011

Press conference 2010 29 March 2011

Interim report for 1st quarter 2011 12 May 2011

Annual general shareholders´ meeting 2011 17 May 2011

Payment of dividend for the 2009 financial year 18 May 2011

Interim report for 1st half‐year 2011 11 August 2011

Interim report for 3rd quarter 2011 09 November 2011

Annual report 2011 29 March 2012

Interim report for 1st quarter 2012 10 May 2012p q y

Annual general shareholders´ meeting 2012 15 May 2012

27Press conference, 29.03.2011

Contact

Dr. Rüdiger Mrotzek – Managing Board

P +49 (0)203 / 54405-55

Hans Richard Schmitz – Managing Board

P +49 (0)203 / 54405-21

M h h it @h b dM [email protected]

Sybille Albeser – Investor Relations

P +49 (0)203 / 54405-32

28Press conference, 29.03.2011