Embed Size (px)

Citation preview

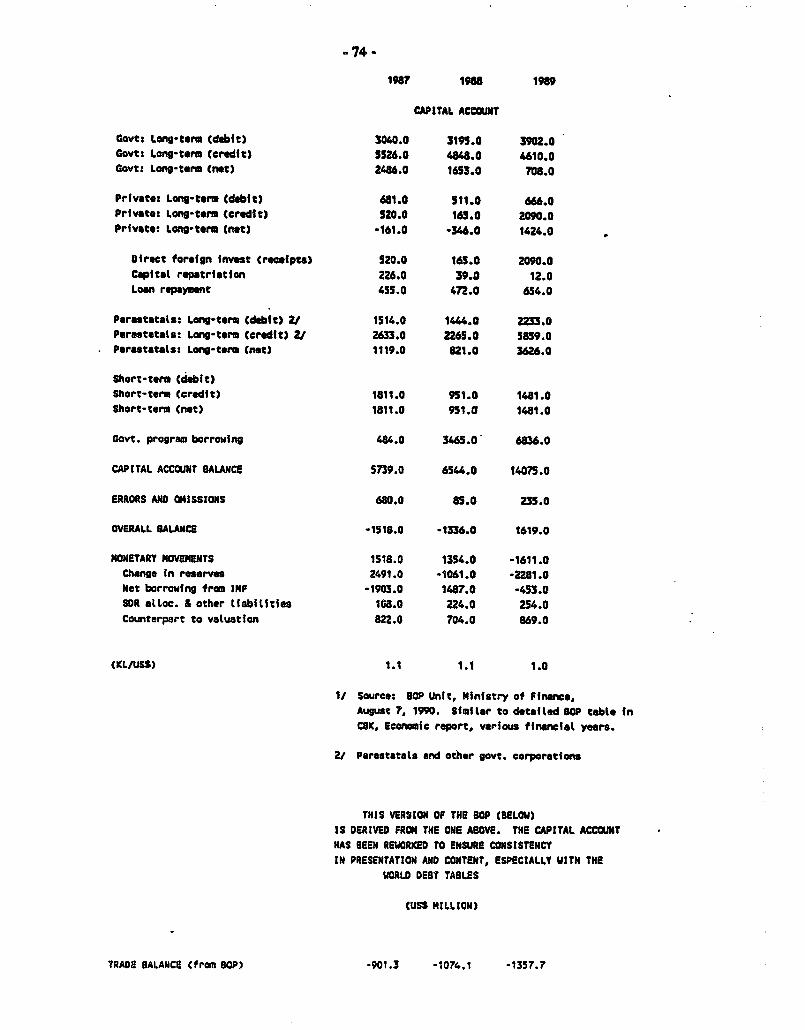

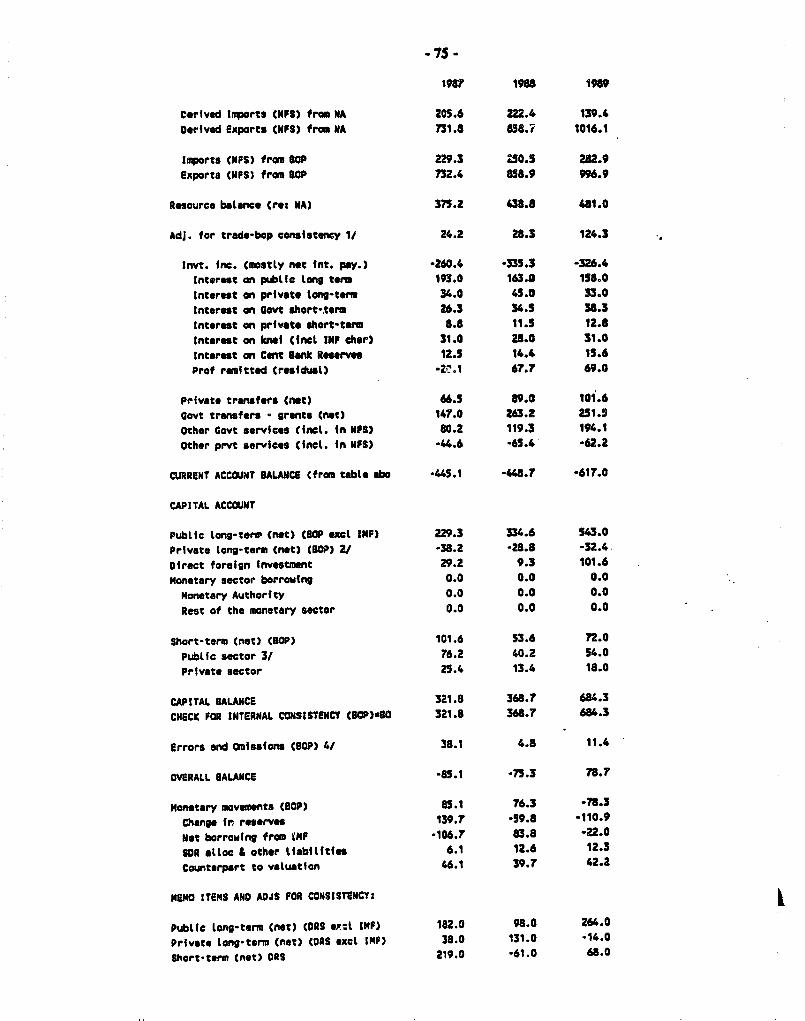

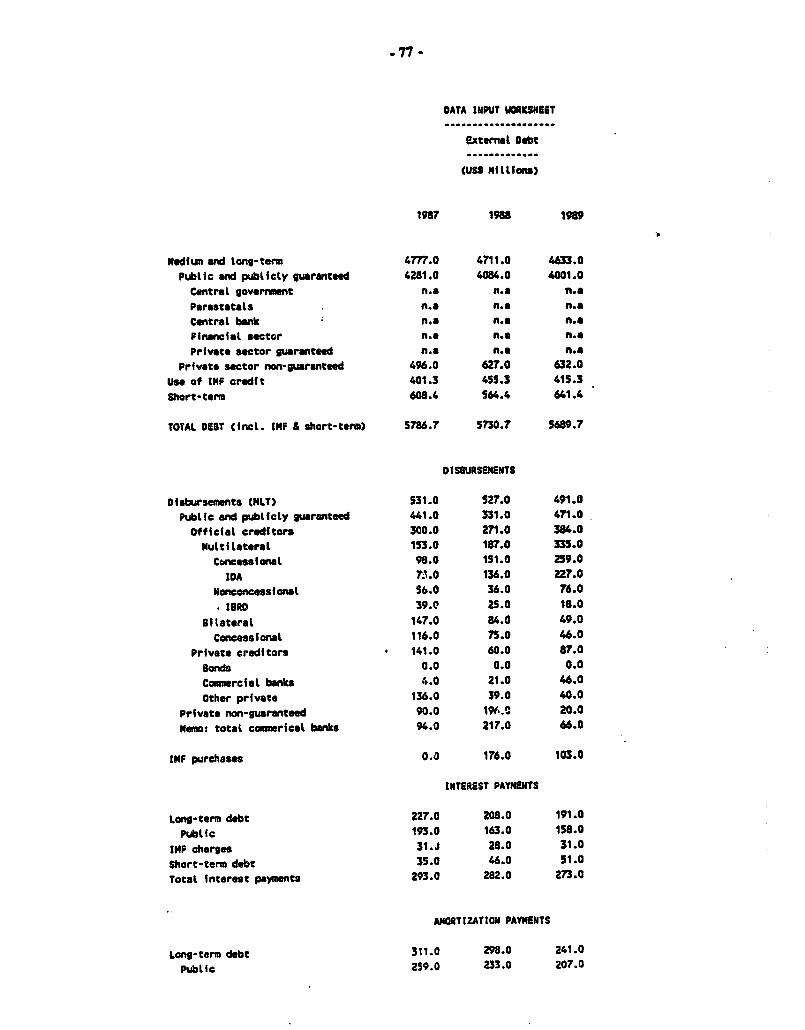

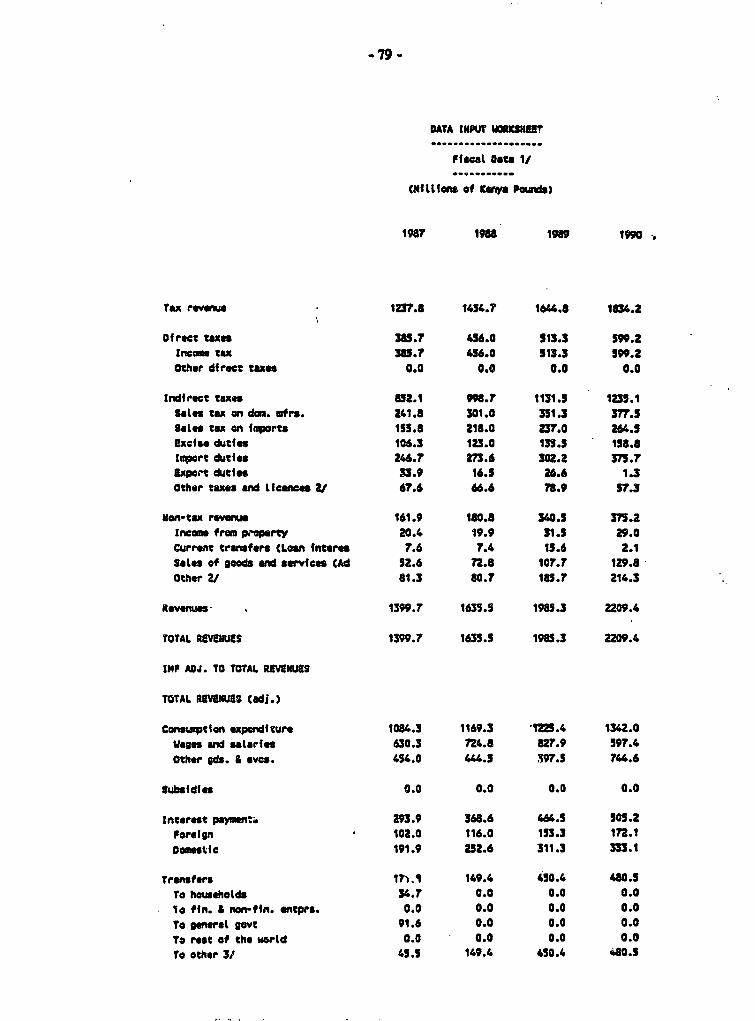

Policy, Research, and External Affairs

WORKING PAPERS

Country Operations

Eastern Africa DepartmentAfrica Regional Office

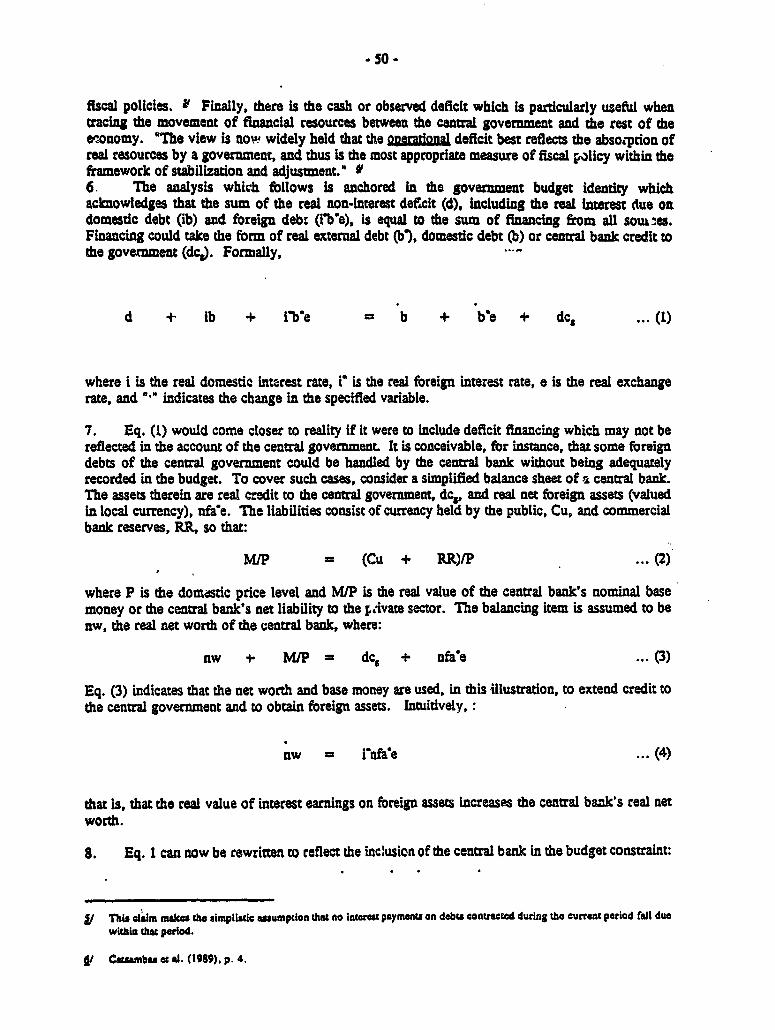

The World BankSeptember 1991

WPS 767

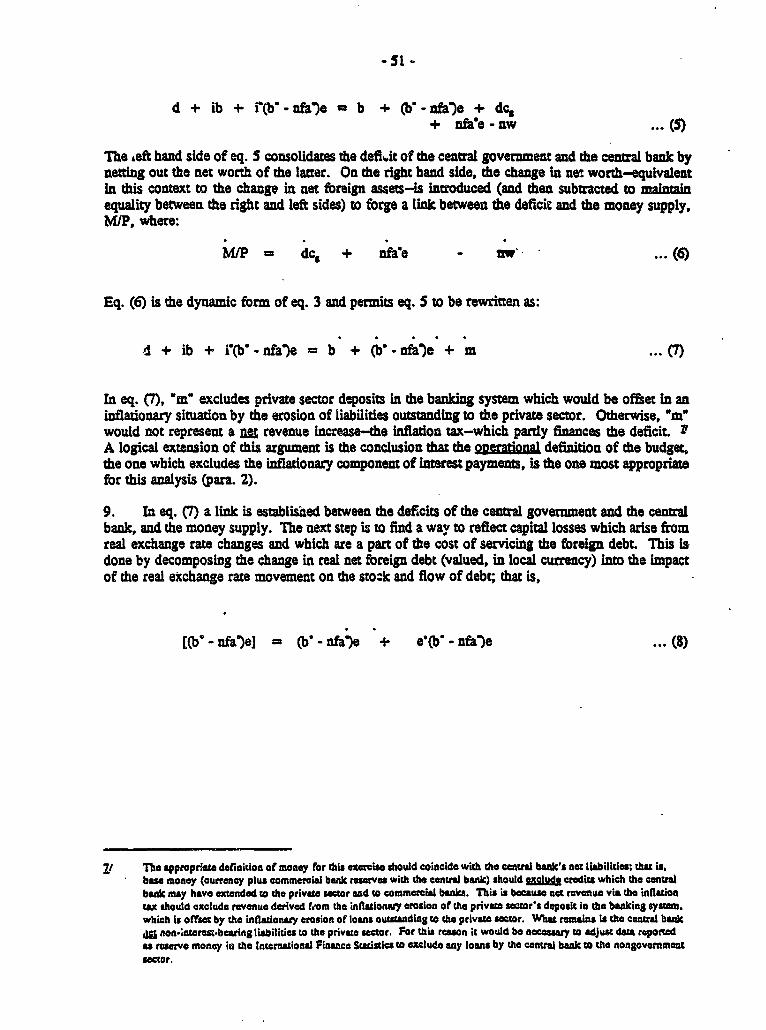

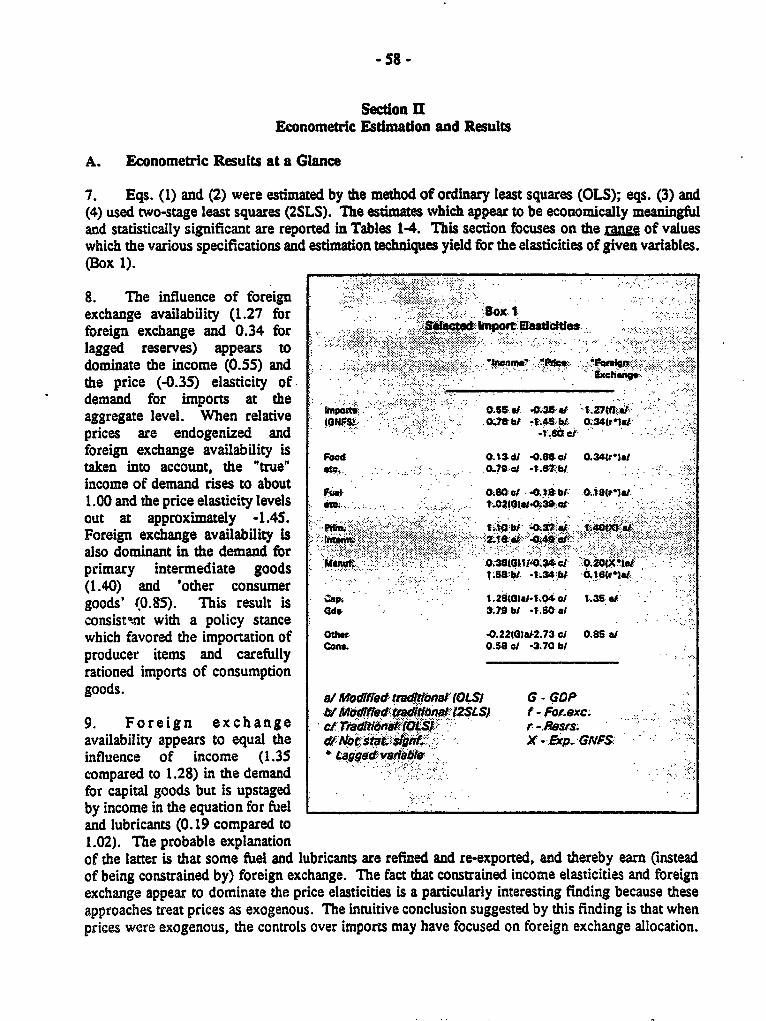

Frameworkfor Macroeconomic

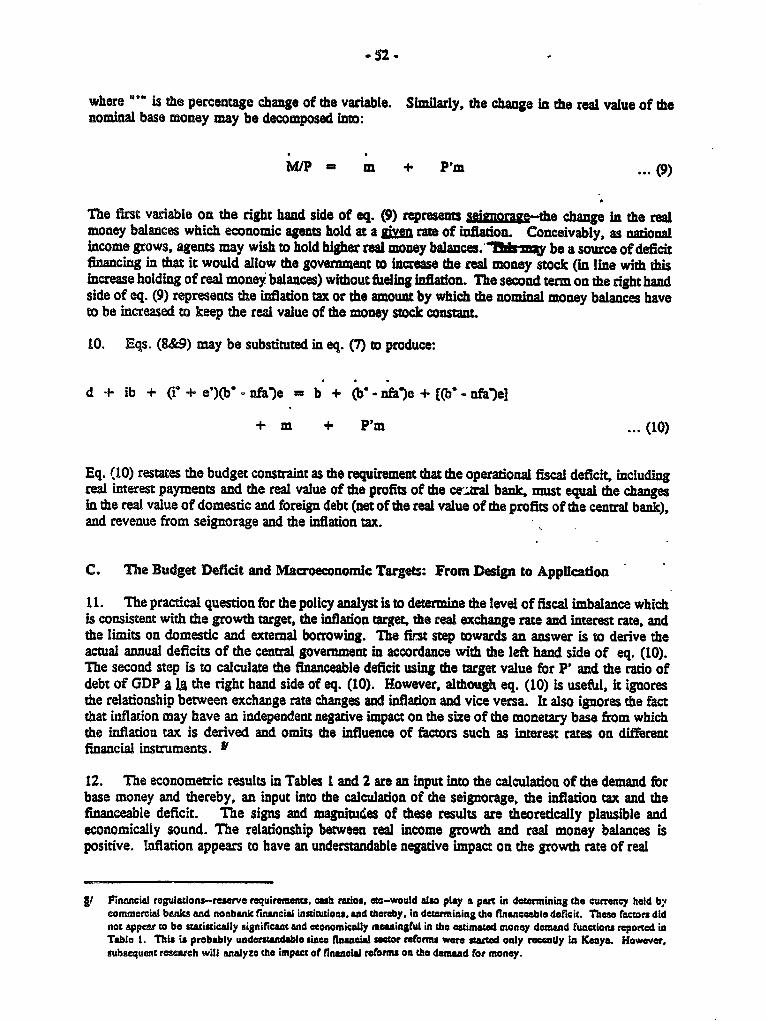

Analysis

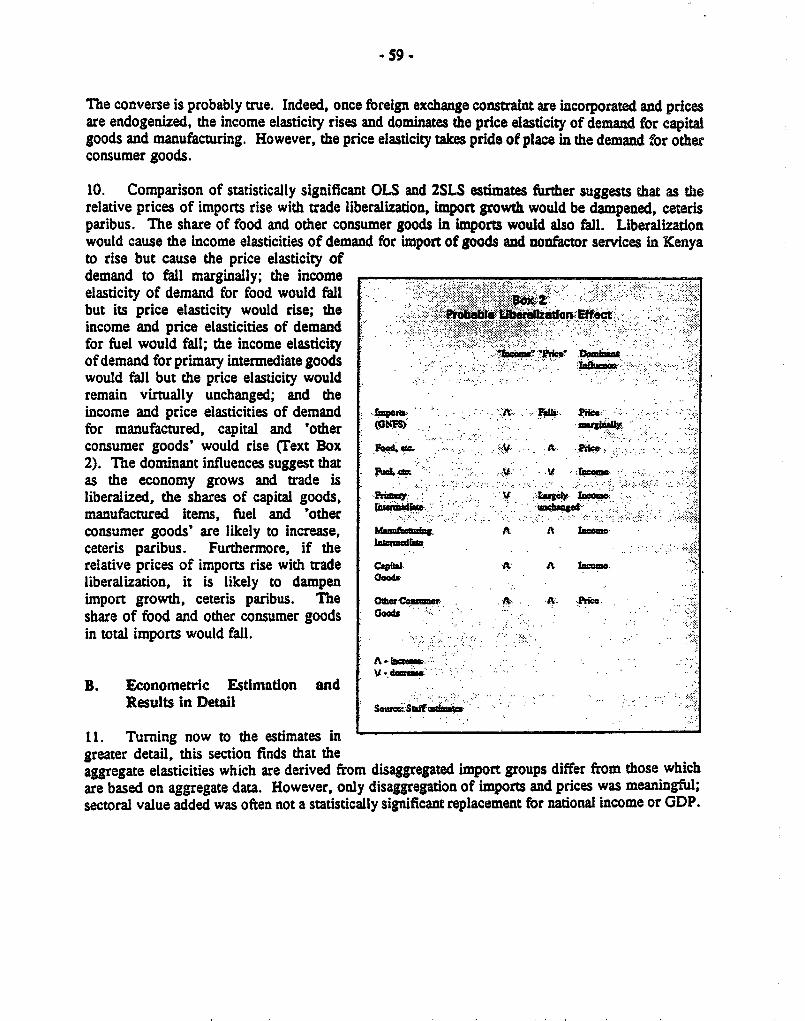

(Applied to Kenya)

Colin A. Bruceand

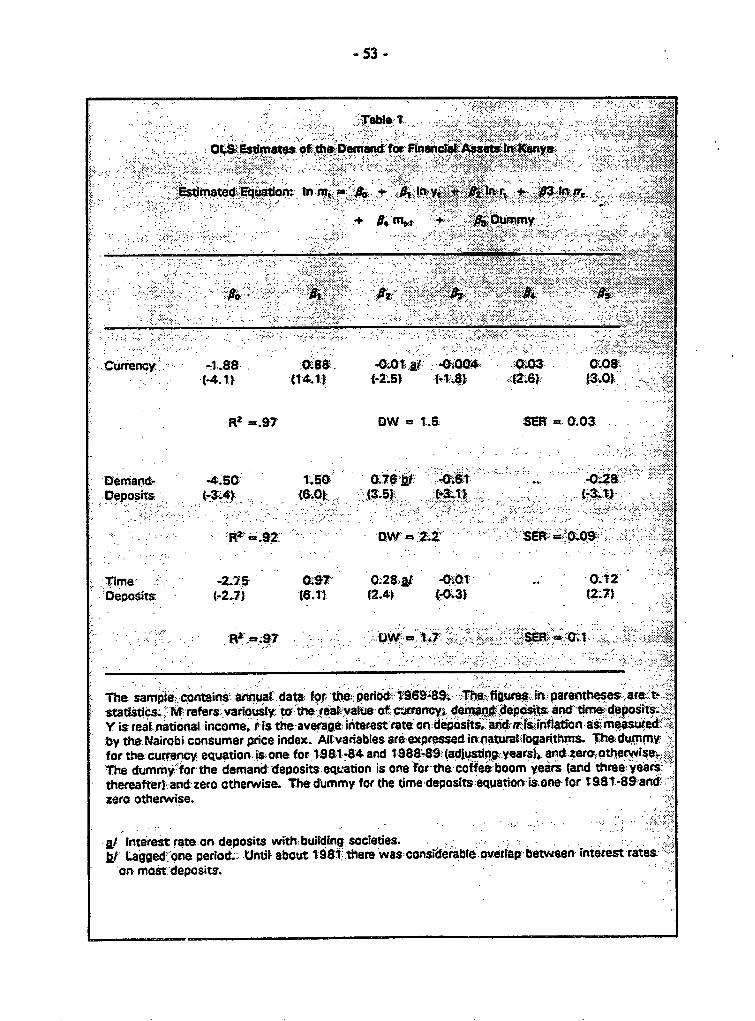

David Ndii

Models of the RMSM-X genre can - while preserving theirlogical structure - incorporate behavioral equations and pro-vide useful insights into policy actions thiat would correctinternal and external macroeconomic imbalances.

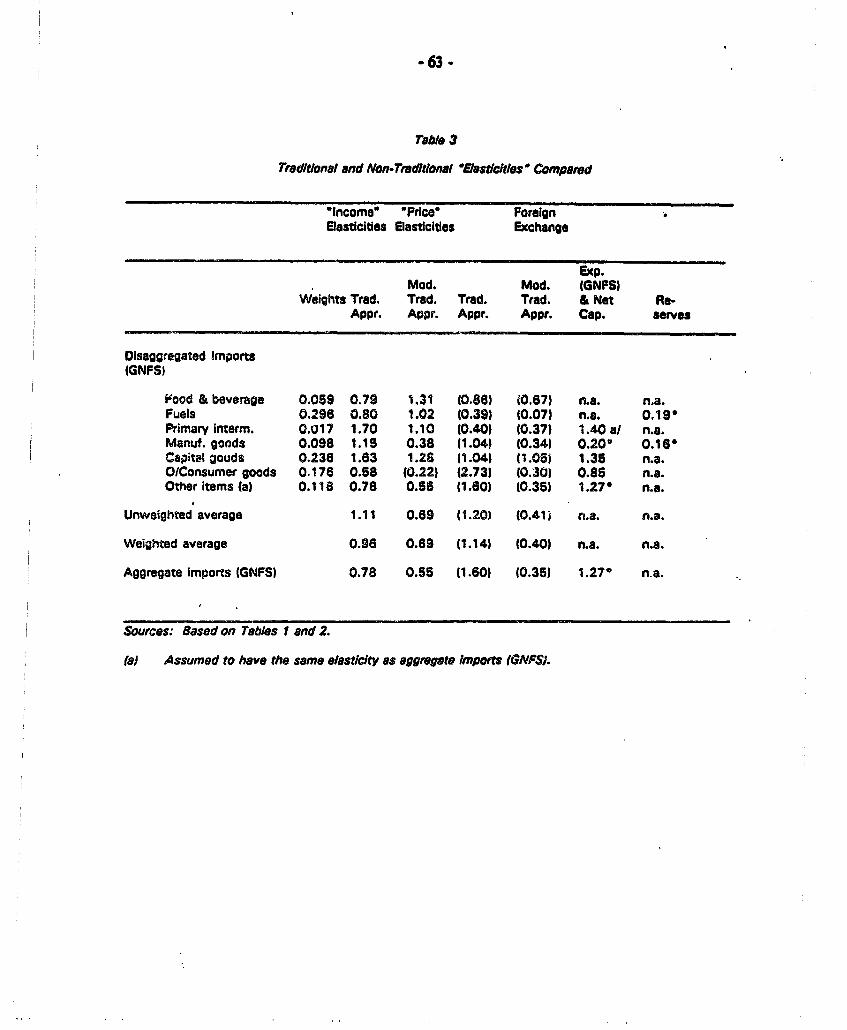

The Policy, Research, and Extemal Affairs Complex distobutes PRE Working Papers to dissemuate the findings of work in progress andto encourage the cxchange of ideas ar-ong Bank staff and all others interested in deselopmnent issues. These papers carry the names ofthe authors, reflect only their views, and should be used and cited accordingly. The findings, unterpretauons, and conclusions are theauthors' own. They should not be attributed to the World Bank, Its Board of Directors, its managcment, or any of its member countries.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Policy, Research, and External Affairs

Country Operations

WPS 767

This paper- a product of the Country Opcrations Division, Eastern Africa Department, Africa RegionalOffice - is part of a larger PRE effort, led by the Macroeconomic Adjustment and Growtlh Division,Country Economics Department, to develop a macroeconomic projection model that will improve andextend the Bank's RMSM model. Copies are available free from the World Bank, 1818 H Street NW,Washingtor DC 20433. Please contact Margaret Lynch, room 110-271, extension 34046 (10(4 pages,including figures and tables).

Bruce anl Ndii develop a macroeconomic model projections. For ease of exposition, these gapsfor Kenya that projects detailed national, fiscal, are assumed to be independent.monetary, and private sector accounts, and thebalance of payments. With no changes in its Next, Bruce and Ndii illustrate the model'slogical structure, the model also calculates the usefulness in calculating the policy adjustmentsmagnitude of policy adjustments that would - exchange rate, interest rate, and monetizationeliminate external and internal imbalances. - that would eliminate intemal and extemal

macroeconomic imbalances. The policy adjust-Their approach emphasizes transparcticy and ments are applied independently and jointly.

user-friendliness, which they achieve in two Predictably, the exchange rate depreciates toways. First, historical data - the basis for eliminate the external financing gap. Similarly,projections - are entered in worksheets that are the real domestic loan interest rate rises, crowdssimilar (in format, coverage, and units of ac- out private investment, and releases financing forcount) to standard tables produced by the data the residual PSBR. The model also calculatesgenerating agencies. Second, key behavioral the level to which domestic inflation would haveassumptions and targets are entered in a clearly to rise to finance the residual PSBR throughi andesignated worksheet. This worksheet contains inflation tax.details such as commodity price projections andthe LIBOR rate that would nornally be provided When activated jointly with exchange rateby the Bank's International Trade Division. This depreciation, a smaller increase in the interestworksheet also accommodates coefficients for rate eliminates the residual PSBR. This isthe import and export price and income elastici- because the exchange rate adjustment improvesties by major commodity groups; the interest and the net foreign assets position and increases theincome elasticities of private investment; and the scope for creating domestic credit. Understand-impact of inflation, income growth, and changes ably, therefore, the increase in interest rate isin interest rates on the demand for currency, even smaller whCIl action in the exchange rate isdemand deposits, and time deposits. The targets combined with partial monetization of the fiscalinclude domestic inflation and sectoral growth deficit.rates.

As an important by-product. these simula-Initially, they use the f'ramework to project tions also illustrate the impact of exchange rate

detailed national and sectoral accounts, including and interest rate adjustments on the fiscal deficit.the financeable fiscal deficit. But they arcespecially interested in the external financing Subsequent versions of the model willgap and the residual public sector borrowing endogeniize growth andi extend coverage to therequirement (PSBR) that emerge in these base consolidated public sector.

The PRE Working Paper Serics disseminates thc findings of work under way in the Bank's l'olicy, Research, and ExtemalAffairsCornplcx. An objectiveofthcseries is to get these finidingsout quickly. even if presentations are less than fully polishedThe findings, interpretations, and conclusions in these papers do not necessarily represent offic ial Bank policy.

ProdUced hy the PRE Dissemination Center

TABLE OF CONTENIS

I. INTRODUCTION ............... I1

U. FRAMEWORK FOR MACROECONOMIC POLICY ANALYSIS. 2

Overview 2..... : 2Behavioral Relationships, Accounting Rules md Flow-of-Funds Consistency 3The Monetary Sector: the demand for fimancial assets. 3Government revenue ............... 5.. ............... SGovernment expenditure ............... 6The balance of payments ............... 6National accounts ............... 7Miscellaneous .............................................. 8Flow of Funds Consistency ................................ 8

III. POLICY SOLUTIONS .10

Introduction .10The Economics of the Exchange Rate Solu.on .10The Econouics of the Interest Rate Solution .13The Economics of Monetizing the Fiscal Defcit .15The Economics of Joint Policy Action. . 16Summary .18

IV. POLICYSIMLATIONS .18

The Base Projections ... . ........................................ 18Exchange Rate Solution ......................................... 22The Interest Rate Solution ..................................... 26Monetization ....... 29loint Exchange Rate and Interest Rate Policy Action.ii*v***@*********** 30Joint Exchange Rate and Interest Rate Policy Action and Monetzati.on .34Summary of Simulation Results. .............. ....... ... 34

V. LIMITATIONS AND FUTURE EXTENSIONS .......... 37

ANNEXES

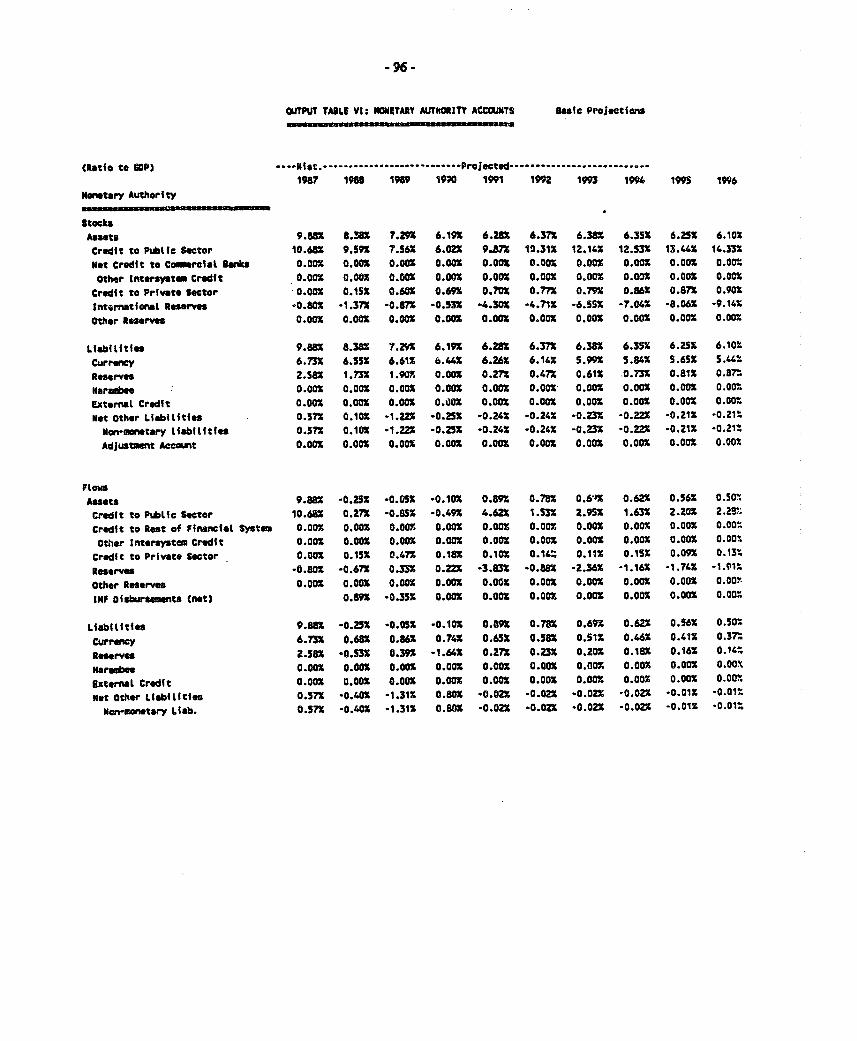

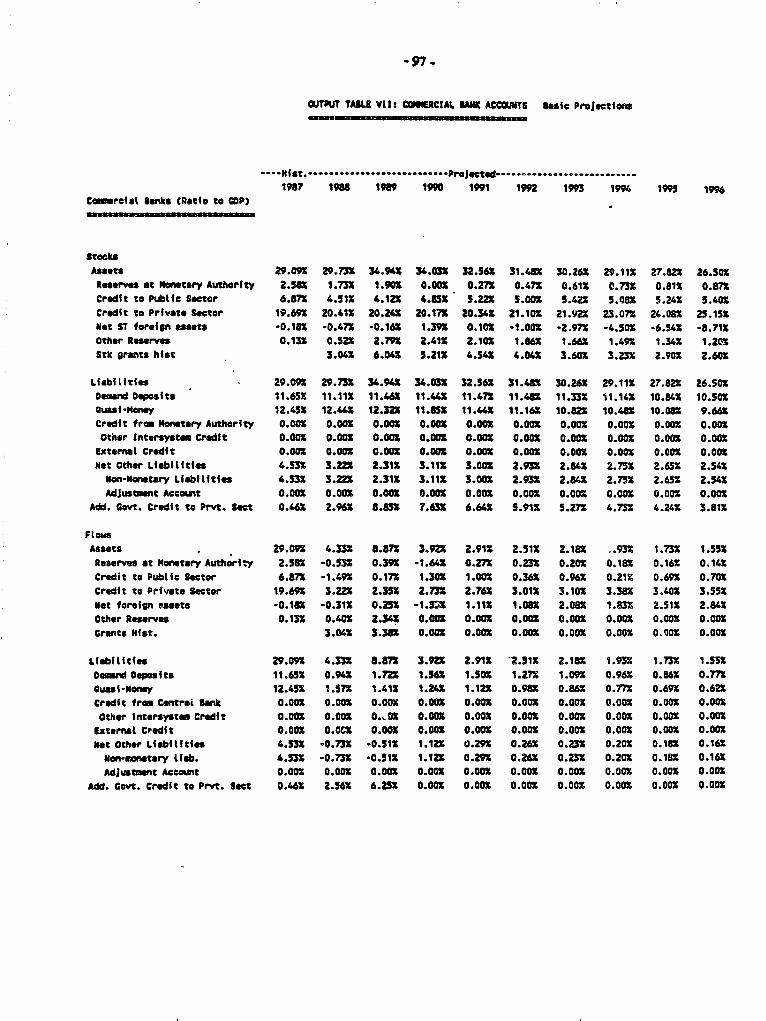

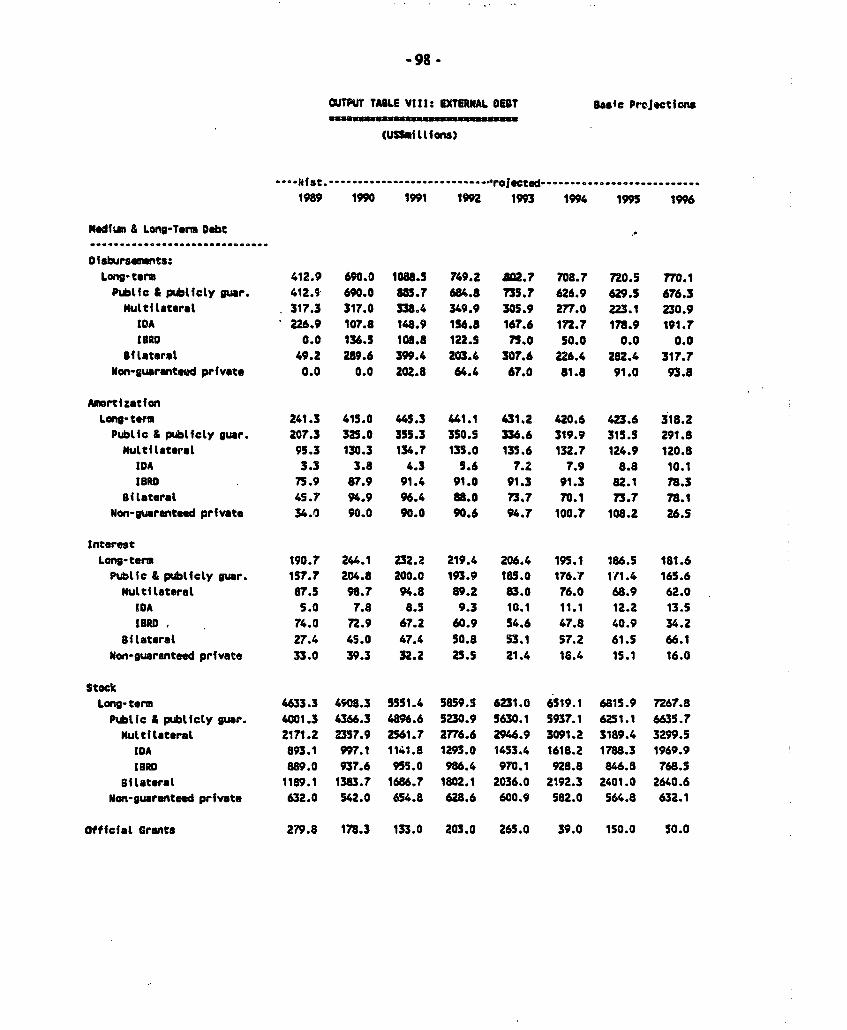

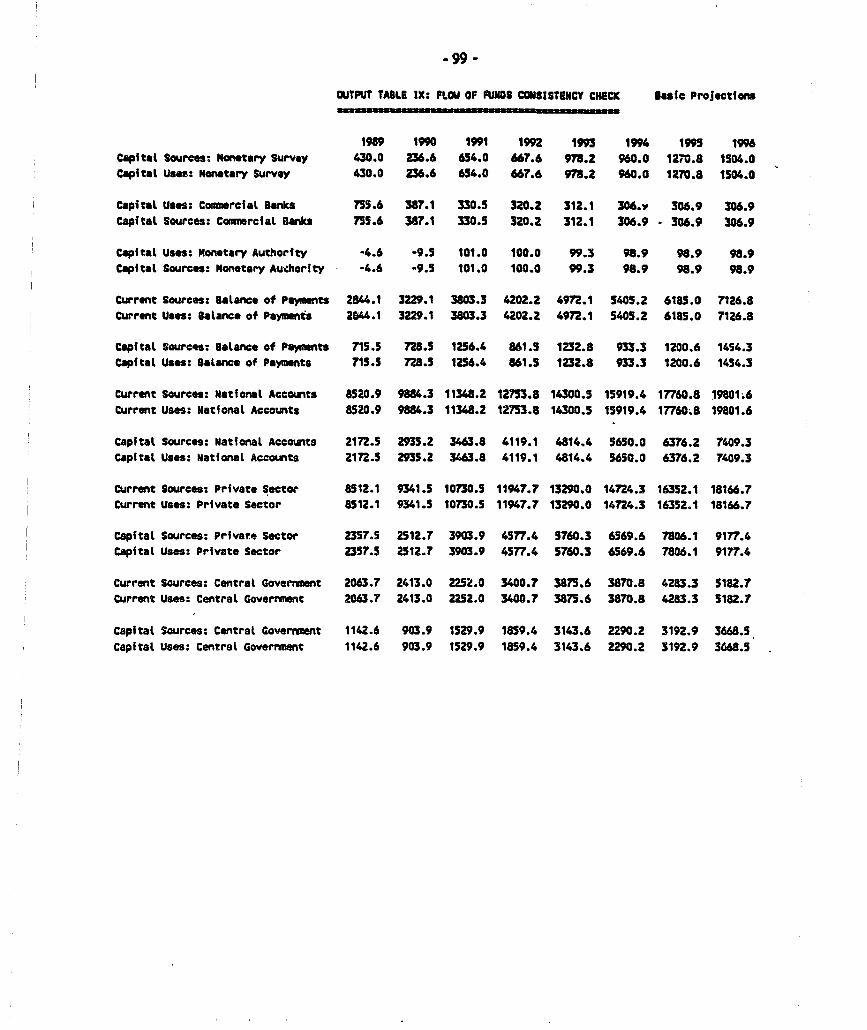

Annex I: Descripdon of Model . ............................. 40Annex 11: Fiscal Deficits and Macroeconomic Consistency .................... 49Annex III: Import Elasdcities in Kenya: 1968 and Beyond 56Annex IV: Key Assumptions and Targets Input Worksheets and Output Tables 66Annex V: Time Bound Formulae ..................... I 100

REEEESNCS .103

TEff TABLES

Table I: Key Indicators: Base Projections .......................... 20Table 11: Key Indicators: ExchageRate Policy ........ ............... 23Table m: Key Indicators: Interest RatePolicy ........................ 27Table TV: Monetzaton of the Residual Pt'blic Sector Borrowing Requirement .... 28Table V: Key Indicators: Joint Exchange/Inters Rate Policy ..... ......... 31Table VI: Exchange, Interest Rate Policy and Monedizatio ................ 35

FIGURES IN TEXT

Figure One: External Gap and Residual Public Sector BorrowingRequirement .......... ......................... 25

Figure Two: Exchange Ra Simulations, Real Loan nterest RateSimuaion, flation Rate Simulaions ........................ 33

We gtezly wknowledge the ugemeand helpful suggestio of John Holem,Pew Miovic and coleague i AF2CO. Katheen B. Jordan provided valuable editonalausitanc whil plyabha Kongsamut wiligly shared her experence with JAVELIN.

Introduction

1.1 This paper presents a transparent, user-friendly framework for analyzing macroeconomic

policy issues in Kenya. It adheres to flow-of-funds consistency, covers the fiscal, monetry,

national and private sector accounts, and balance of payments, and is an analytical tool for

grappling with the economic relationships and institutional realities which ultimately dictate the

design, implementation and effectiveness of macroeconomic policies. The model is programmed

in JAVELIN.

1.2 A recent report concluded that Kenya's "... recovery ... is somewhat fagile as it has

relied on foreign savings, leaving the economy vulnerable to external shocks, and the remaining

domestic macroeconomic imbalances, unless corrected, threaten to undermine recent economic

and stabilization gains." (World Bank, 1990). The model presented in this paper is usefil to the

policy analyst who may wish to project the broad magnitude of these imbalances under different

fiure growth assumptions. With these results in hand, the policy analyst may choose to revise

growth targets in an ad hoc, piecemeal manner until acceptable" imbalances are obtained and

then focus on mobilizing inflows to fill the resource gaps. Alternatively, the policy analyst may

wish to determine what levels of imbalances are sustainable, financeable and consistent with other

development goals. Here judgment about institutional/political feasibility is indispensable. But

so too is a map of inviolable accounting macro-relationships, their evolution under different

behavioral assumptions, and the technical limitations they impose on policy selection and

effectiveness. The model developed in ftis paper is such a map which could also demonstrate

-2-

the usefulness of instruments such as the interest rate, exchange rate and monetary policy in

managing macroeconomic imbalances and steering the economy doser to its development goals.

1.3 The paper is organized as follows. Chapter Two sketches the analytical firamework and

discusses the econemics of its structure. Chapter Three contains the policy solutions (the

technical details are presented in Annex I). Chapter Three illustrates three policy options-

exchange rate adjusunent, interest rate adjustment and monetization-and highlights their

implications when used individually and jointly. Chapter Five identifies the model's limitations

and scope for expansion.

II. Framework for Macroeconomic Policy Analysis

Ovrview

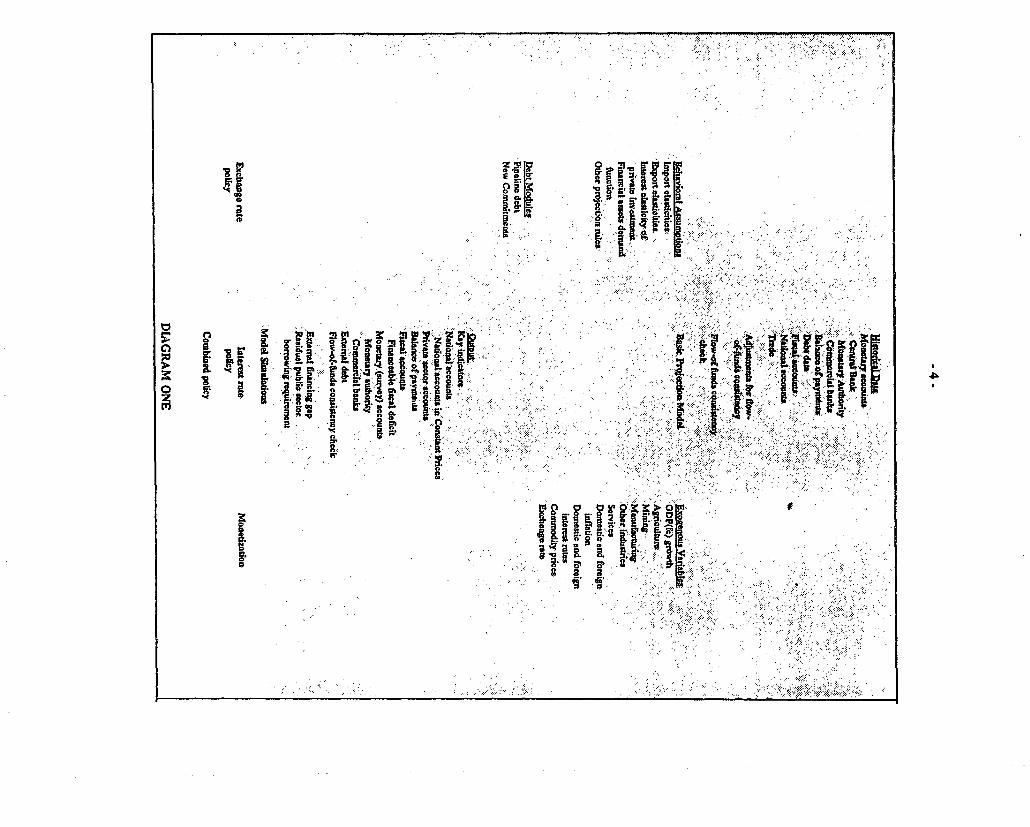

2.1 The model comprises .ix data input worksheets, debt modules for existing and new

external debt, and output tables (Diag:am One). There is also one central worksheet which

contains key behavioral assumptions and macroeconomic targets. The model covers the national

accounts as well as the accounts of the central bank, the monetary authority, the commercial

banks, the central government, the external sector (trade, balance of payments and external debt)

and the non-financial private sector. 11 The projection period is 1990-96.

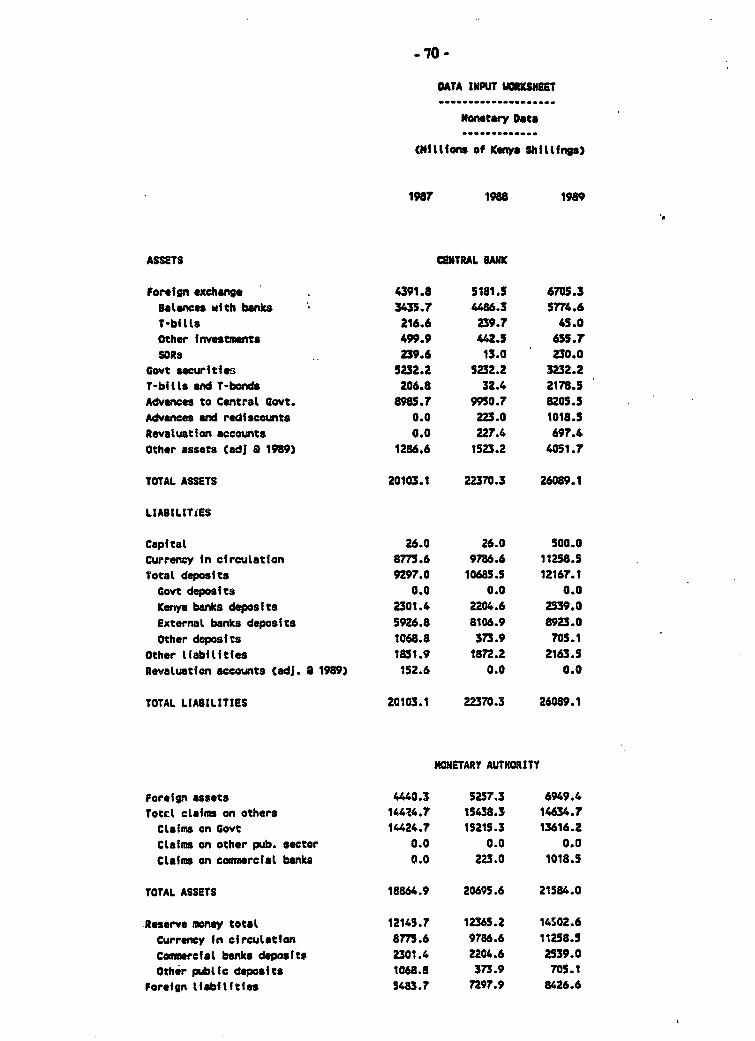

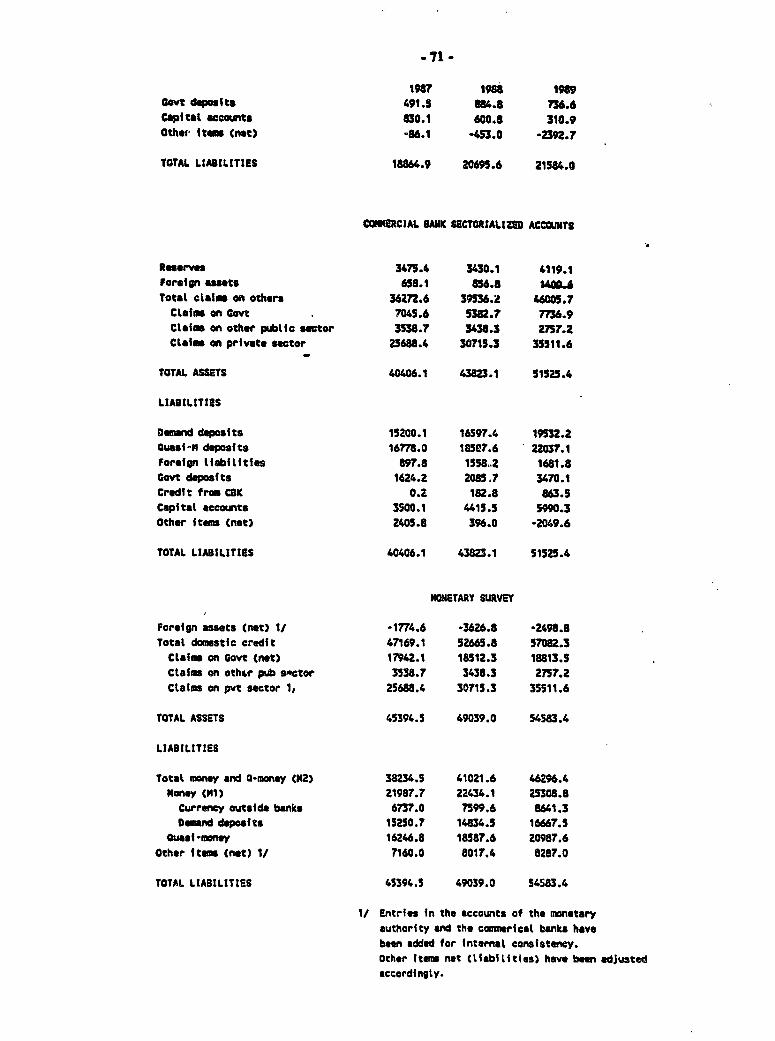

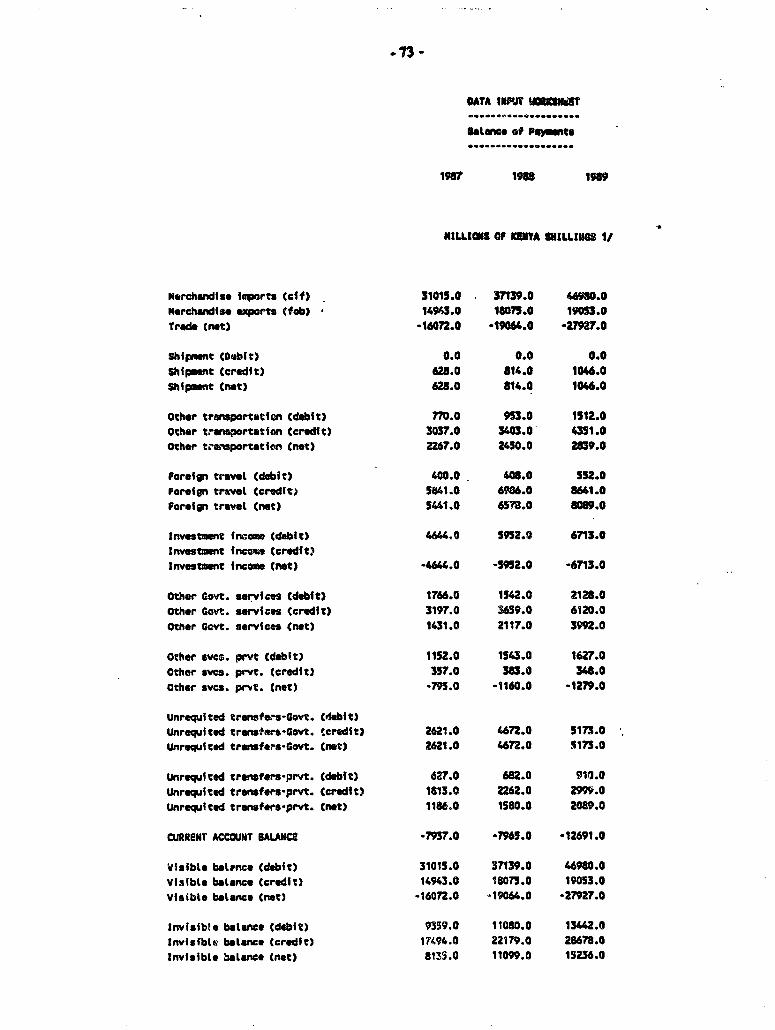

2.2 The data inpit worksheets contain annual historical data for 1987-89. In general the

format, units of account and coverage of these worksheets are similar to standard tables produced

by the data-generating agencies of the GovernAent of Kenya. The exceptions are the worksheets

.L1/. TM accounts of monewy auhority consolidate the accounts of the central bank with the accounts arising frommoncay funiions undertaken by other insitutions or tho cntral govemment.

3 -

for central government finances and exteumal debt which eome from the IM and the World Bank

respectively. Ihese historical data must be consistent within and across sectors, and conform to

standard macroeconomic accounting rules. Both of these requirements obtain in the flow of finds

famework. Accordingly, the model reconciles historical data for flow of fumds consistency and

then uses them as the basis for projections.

Behavioral Relationships, Accoundng Rules and Flow-of-Funds Consistency

2.3 Macroeconomic accounting rules and flow of funds consistency set limits within which

economic behavior takes place in the model. The accounting rules and flow of funds consistency

requirements are the same as those set out in Holsen (1989), Khadr et al. (1989) and Easterly et

al. (1990). The behavioral relationships are the projection rules for variables. Some originate

in econometric analysis that has yielded coefficients linking the variable of interest to its

determinants. Others are constant ratios of other vaiables with which they had, or are exp -- ted

to have, a stable long run relationship. Yet others are projected on the basis of their relationship

to variables whiclt are exogenous to the model.

2.4 To simplify the exposition of the model, this section only specifies and discusses the main

behavioral relationships in the monetary sector, the central government accounts, the external

sector and the national accounts. A more comprehensive notational presentation of the behavioral

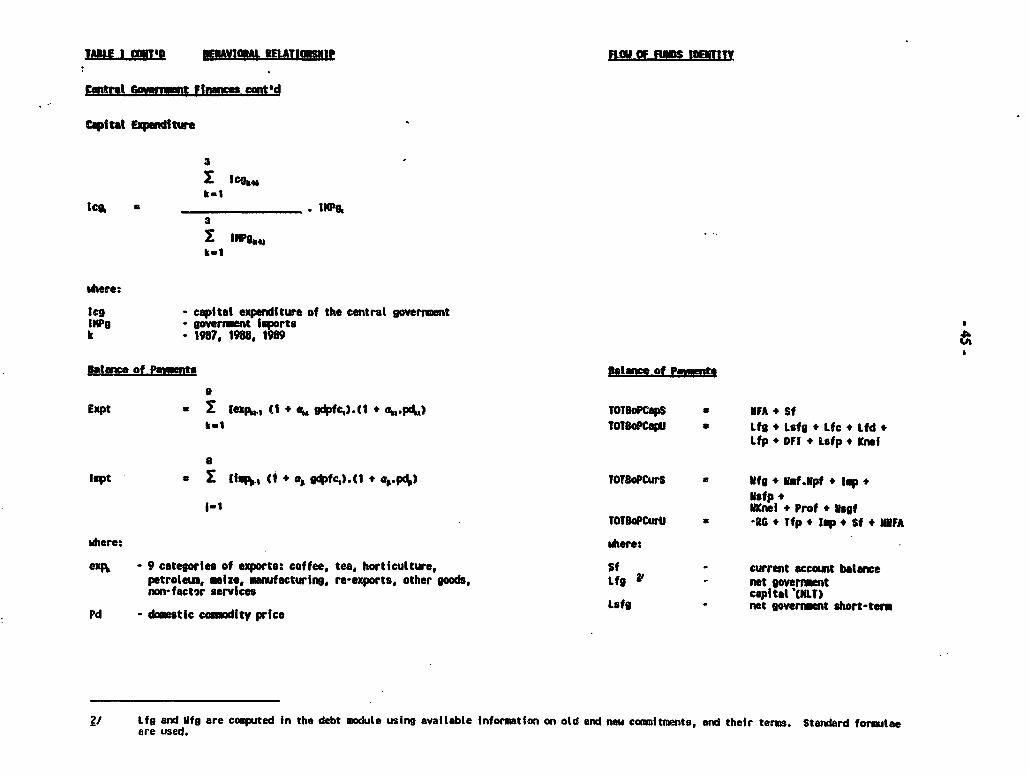

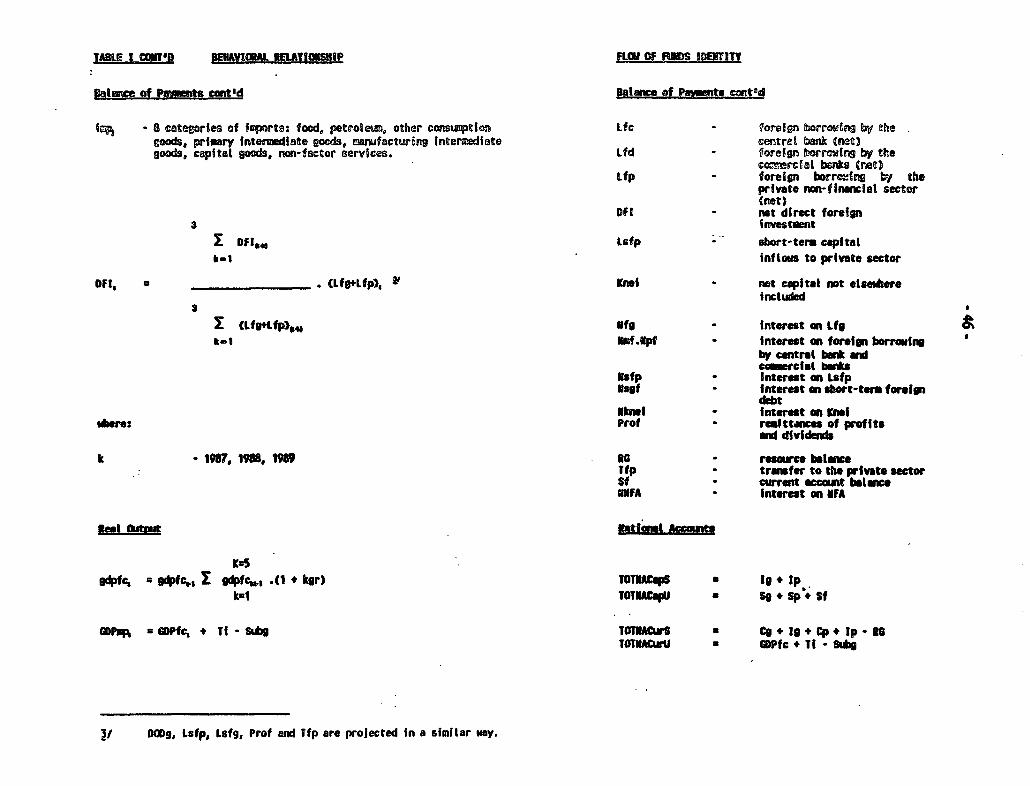

relationships, with their flow-of-fimds accounting identities, is provided in Annex I.

The Monetar Sector: the demand for financial assets

2.5 The model identifies demand functions for three financial assets-currency, demand

deposits and time deposits (quasi-money). The demand for currency is a positive fniction of real

income growth and a negative function of the real deposit interest rate and the rate of inflation.

C ~ ~ ~ ~ ~ ~ ~~ D . , ..l .

t t i , 0 t i | [!|i W. : .

C2 Li~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

. ',' . ' '' 00 'S' ,, z"'V i; ', ''. ii >. "''0 2'.'z,y,'

~~~~~~jj; : ¢.. :"Ij tr ', ,,, '- -i.'

~~~~~~~X:'',.''' .- .. , 4 ,a.:, . .... :,, ., . , :.>; ,ieQ

-5-w

The demand for demand deposits and time deposits is a positive fnction of real income growth,

a negative function of the rate of inflation, and a positive function of the real interest rate on

deposits. In essence, the demand for currency, demand deposits and time deposits increases with

national income but is eroded by inflation. Demand and time deposits, unlike currency, earn

interest and therefore move in the same direction as interest rates. The coefficients entering the

framework are based on econometric estimates discussed in Annex H. The model ensures

consistency between financial stocks and flows by expressing flows as changes in the respective

stocks over the specified period. Where appropriate, stocks are derived by aggregating flows.

Government revenue

2.6 In the model, government revenue falls into two main categories, recurrent revenue and

capital revenue. Recurrent revenue is subdivided into direct taxes, indirect taxes and other

recurrent items. Direct taxes throughout the projection period are assumed to maintain the ratio

of direct taxes to GDP (at factor cost) estimated for the base period, 1987-89. Other recurrent

items obey a similar projection rule. Indirect taxes are disaggregated into sales taxes on domestic

manufactures and imports, duties on imports, and other taxes and licenses. 21 In turn, each of

these revenue categories is projected with respect to the activities which generate them. Sales

taxes on imports (in local currency) are assumed to maintain the ratio of sales taxes to total

imports (in local currency) esimated for the base period, 1987-89. The same relationship is

assumed for sales taxes on exports with respect to exports and for duties on imports with respect

to imports. Other indirect taxes are projected in a similar way but are linked instead to the pool

of tax revenues (net of indirect taxes).

Z/ Duties on exports have been discontinued by the Government of Kenya.

-6-:

Governm t penditure

2.7 Govenment consumpdon expenditr has two main cowponents. The first is wages and

salaries which are determined by an exogenous nominal growth target. The second component

is expenditure on goods and services. Its relationship to government consumpdon expenditue

is assumed to be the same in the future as in 19874B9. Subsidies, trnsfers and other current

expenditures are projected in a similar mner but with respect to GDP. Interest on foreign debt

is calculated by the debt module on the basis of the debt stock. Interest on domestic debt is

calculated in a similar manner.

2.8 External inflows are an important source of funding for and determinant of government

capital expenditure. Often these inflows finance imported investment goods. Accordingly, the

model projects government capital expenditure as a fixod ratio of government imports, based on

the ratio in 1987-89. In turn, govermment imports are linked to long-term capital inflows (as

at 198749) which are computed in the debt module.

The balance of payments

2.9 Exports are disaggregated into commodity groups-coffee, tea, horticulture, petroleum,

maize, manufacatring, re-exports, other goods and non-factor services. The import groups

idendfied are food, petroleum, other consumption goods, primary intermediate goods,

manufacturing intermediate goods, capital goods, leases, government imports, and non-factor

services. With the exception of leases of aircrafts and government imports, these traded goods

are projected solely on the basis of their estimated elasticities with respect to GDP and to their

prices in local currency (Annex o).

2.10 Thrughout the projecon peiod net crret fer, nct direct rbr?ign investment,

offici gram and short-term captal are deemined by their respective ratios to GDP estiated

for 1987-89. Long-term public and publicly guamteed inflows, Don-guaranteed private medium

and long-tem inflows together with their amorzation and interest obligadons are calculated in

the debt module. Short-term public and private debt are assumed to be a fixed ratio of total long-

term inflvuw. Interest on short-term extenal debt and on reserves is determined by applying

the exogenous foreign interest rate to their stocks. Reserve accumlation is derived from the

overall balance of payments or stated as an explicit target.

National accounts

2.11 Several items for the national accounts are determined in the sectoral accounts described

in paras. 2.6 to 2.10. They include indirect taxes, subsidies, the net current transfers in the

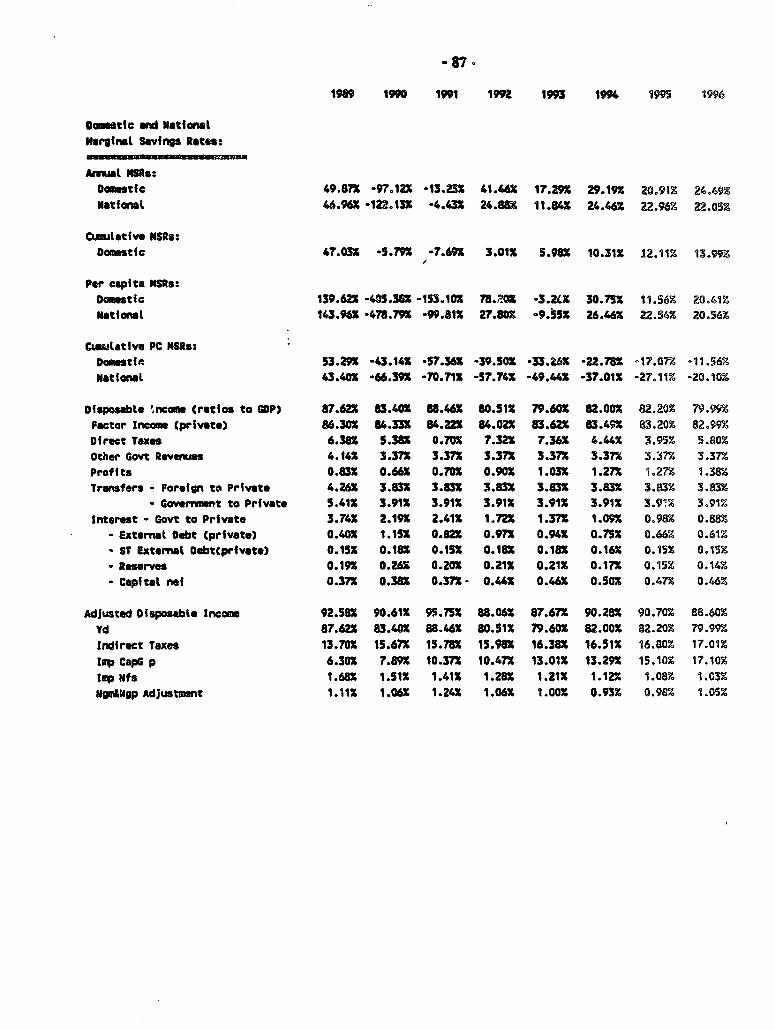

balance of payments, Government consumption and investment. Domestic savings is simply the

difference between total investment and the external resource gap. LikbwiLe, national savings

is the difference between total investment and the current account balance. Private savings is the

residual after public savings-defined as the current balances in the fiscal accounts-is subtracted

from national savings.

2.12 GDP at ftctor cost is broken down into value added in agriculture, mining,

imanufacturing, other industry and services. Growth in each of these sectors is projected

exogenously. GDP at market prices is then determined in conjunction with net direct taxes which

are calculated in the fiscal account.

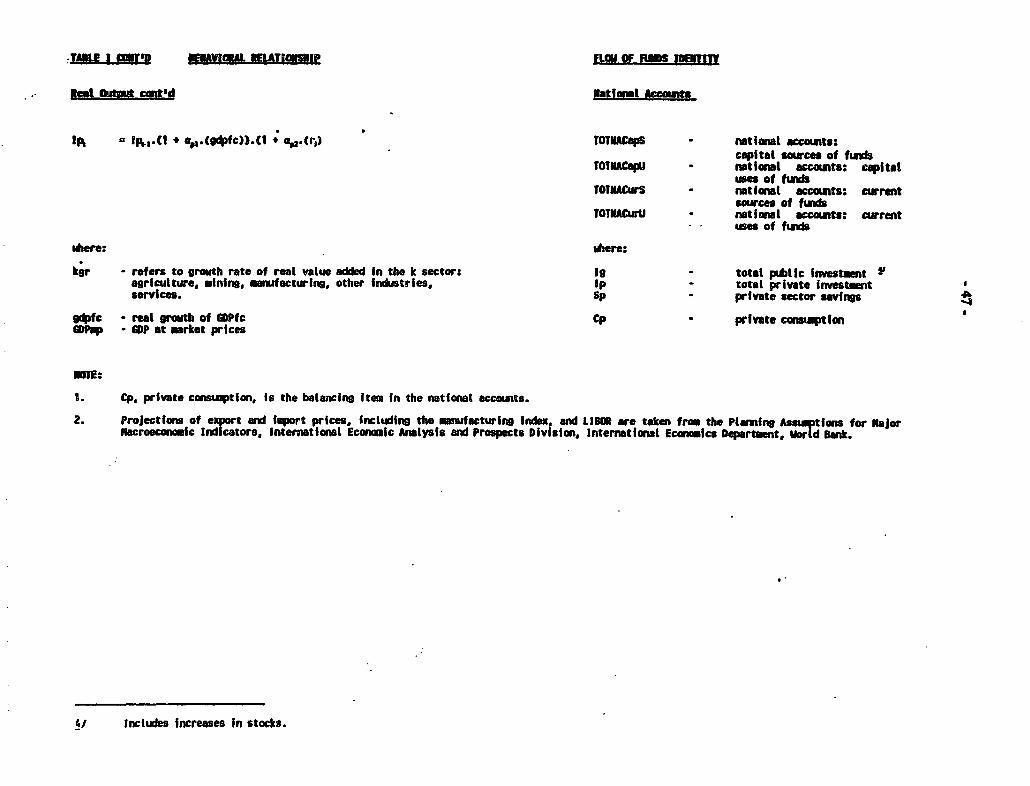

2.13 Public investment and consumption are projected in the public sector accounts. Private

Iinestment is a negative function of the change in the real domestic loan interest rate and a

-8-

positive function of GDP growth. Private consumption is the residual item for balancing GDP

at market prices with gross domestic expenditure

Miscellaneous

2.14 Tle projected population growth rate, dollar prices of Imports and exports including the

manufactuing uiit index, and LIBCOR are external to the model and are obtained from sources

within the World Bank. The commodity prices from these sources serve as inputs into the

exl,ort, import, investment, consumption and GDP deflators. All deflators are weighted by the

shares of commodities whose prices enter their calculation.

Flow of Funds Consistency

2.15 Economic flows generated in one sector may be used within that sector or other sectors

of the economy. This is the fundamental organizing principle of the flow of funds consistency

framework as presented in Holsen (19S9), Khadr et al. (1989) and Easterly et al. (1990). It

classifies each variable as a source of funds or a use of funds. The sources and uses may be

current or capital. Consistency prevails when current sources of funds equal current u;es of

funds within eack. sector and in the overall economy. The same condition holds for capita

sources and uses of finds.

2.16 The flow of funds identities for the nonetary sector, central government finances, the

balance of payments and the national accounts are presented in Annex I. They include the stocks

and flows of the central bank, monetary authority and commercial banks, as well as the non-

financial private sector. The projectigns derived from the behavioral relationships satisfy these

identities at the sectoral and aggregate level. Historical data, however, required several

adjustments to achieve consistency. An adjustment was made for consistency among the capital

-9-

fiows and stocks implied by the debt data, the balance of payments, the fiscal accoun and the

monetary accounts. Similar calculations were done after balance of payments data in the national

accounts were compared with the figures in the balance of paymen. The rule of thvmb was to

identify those adjustments which made the data in each input worksheet internally consistent,

reconciled stocks with flows and achieved intersectoral consistency in relation to the national

accounts.

2.17 Historical net foreign assets of the central bank and monetary authority were also adjusted

for consistency with their capital sourcm. This adjuement became the balancing item in the

capital sources of the balance of payments. An adjustment was also needed to make the capital

uses of government revenue equal to the capital sources. This adjustment balanced the private

sector's sources and uses of funds. Finally, the total historical sources of the capital funds of

the central government were changed by an amount which became the balancing item for the

historical uses of capital funds by the private sector. After reconciliation for flow-of-funds

consistency, the historical data are used by the model as the basis for projections and policy

simulations.

- 10-

HI. POLICY SOLUTIONS

Introduction

3.1 This chapter discusses the economics of using exchange rate policy, interest rate policy

and monetization of the fiscal deficit, independently and jointly, to redress macroeconomic

imbalances. These policy instruments have been selected because of their increasing role in

managing the Kenyan economy. Prior to 1982, Kenya had a fixed exchange rate regime.

Increasingly since 1985, the exchange rate adjustments have been used to ensure Kenya's external

competitiveness, support the import liberalization program, and strengthen the overall

macroeconomic policy environment. The regulation of interest rates in Kenya dates back to

1974 but movement toward market-determined interest rates is expected to be completed by June

1991. Other instruments for managing monetary aggregates are also being strengthened.

The Economics of the Exchange Rate Solution

3.2 The exchange rate policy simulation computes the exchange rate at which the specified

external financing gap would be closed at a given GDP level. ai The solution depends largely

on the negative relationship between import demand and import prices, and the positive

relationship between export supply and export prices. A devaluation of the exchange rate would,

other things being equal, raise the domestic currency prices of traded goods, increase the supply

of exports, decrease the demand for imports and narrow the resource gap. Because the exports

and imports are each subdivided into major commodity groups-each with its own price and

income elasticity-the model can account in a realistic way for differences in response lags. For

/ 'MTho ternal fancing gap is the additional capital inflows-over and above those already accounted *br-whichare required to finance the current account deficit in the balance of payments and to meet the reserveaccumulaton target.

- I1 -

example, in the absence of large stocks, the supply response of coffee exports to coffee price

increases is likely to be slower than manufactured items. Imported food, with its many local

substitutes, is likely to be more sensitive to price changes than imported crude oil which has no

close local substitutes. Similarly, to the extent that government imports are financed by donors,

their demand is expected to be fairly inelastic with respect to prices.

3.3 All other variables in the model which are linked to exports, imports and the exchange

rate are affected by this solution. When the exchange rate is devalued, governnent revenue from

imports falls if there is a reduction in the local currency value of imports. An exchange rate

devaluation would also increase the domestic currency expenditure on foreign debt service and

externally financed activities. In addition, it would increase the domestic currency receipts from

external transfers, loans and grants. The impact of the exchange rate depreciation on the fiscal

deficit therefore would be ambiguous.

3.4 To maintain macroeconomic consistency, domestic investment and/or savings must adjust

when an exchange rate devaluation results in the importation of fewer goods and the export of

more goods. Consider the simple macroeconomic identity:

+ ?-

GDP(fc) + Ti (net) = Cp + Cg + Ip + Ig + X -M (1)

where GDP(fc) is gross domestic product at factor cost, Ti (net) is net indirect taxes, Cp and Cg

are private and public consumption respectively, Ip and Ig are private and public investment

respectively, X is exports and M is imports-all in domestic currency units. Equation (1) equates

the total current sources of fimds with the total current uses of funds in the national accounts. The

12 -

signs above the variables indicaze their possible response ('+' is positive,'-' is negative) to an

exchange rate devaluation. Equation (1) shows that variables on left and right hand sides of

equation (1) may have to adjust to maintain equality.

3.5 GDP at factor cost (measured in domestic prices) is exogenous and therefore does not

change with exchange rate movements in the model. In contrast, indirctames could rise or fall.

Public consumption comprises government consumption and wage targets, and therefore is not

affected in the model by exchange rate changes (paras. 2.7, 2.12). Private investment is

deternined by the real domestic loan interest rate and GDP at factor cost. Neither is affected by

exchange rate movements in the model. By definition, the increase in the resource balance (X-M)

would be greater than any increase in net indirect taxes Ti) (for a given tax rate). Accordingly,

Cp and/or Ig must fall to maintain equality in equaion (1). Ig could only fall on economic

grounds if government imports, including inputs into investment, fall in response to the exchange

rate devaluation. Ultimately, if government investment does not contract sufficiently, the

residual variable-private consumption-must fall. In essence, private domestic savings must rise

to finance the unchanged level of private investment and a largely unchanged or slightly reduced

level of government investment, becuse of the reduction in foreign savings (X-M).

3.6 The exchange rate solution affects monetary aggregates via its impact on the net foreign

exchange assets and the demand for financial assets. Equation (2):

M g+ +* . +4.

M1 (rd,wr,gdpfc) + QM (rd,Tr,gdpfc) + Nol = NFA + Lcg + Ldg + Lmip (2)

- 13 -

represents equilibrium in the monetary sector, where MI is currency (negative function of the

real interest rate) and demand deposits (positive function of the real interest rate), QM is time

deposits (quasi-money), rd is the real domestic loan interest rate, X is the rate of domestic

inflation, NOL is the flow of net other liabilities of the monetary system, NFA is the net foreign

assets, Lcg is the flow of net credit from the central bank to the government, Ldg is the flow of

net lending from the commercial banks to the government and Lmp is the flow of net credit to

the private sector. Equation (2) equates the total capital sources of funds with the total'capital

uses of funds in the monetary survey; that is, equality of the liabilities and assets of the banking

system as a whole. While it is obvious that NFA could be affected by an exchange rate

devaluation, it is also conceivable that only variables on the left hand side of the equation would

change. MI and QM are negatively affected by inflation which could be induced by the exchange

rate policy but they are driven in different directions by real interest rates. The important point

is that equation (2) has economically meaningful behavioral flexibility to achieve overaU balance

after an exchange rate adjustment.

The Economics of the Interest Rate Solution

3.7 The interest rate simulation computes the interest rate at which the residual public sector

borrowing requirement would be met by borrowing from domestic commercial banks, given the

level of GDP and the private sector's demand for credit from these banks. _4/ Because of data

limitations, the 'public sector" is limited to the central government in the model.

3.8 The recent Country Economic Memorandum ascribes three main objectives to interest

rate policy in Kenya. The first is to maintain positive real interest rates in order to encourage

41 The residual public sector borrowing requirement is defined in the model u the additional domestic financing--net of the anticipated current and capital revenues, and domestic and foreign financing-which would covertotal government expenditure.

- 14 -

savings and thereby contribute to the mobilization of financial resources. The second objectve

is to move gradually to market determined interest rates which in turn would encourage a more

efficient allocation of credit across and within sectors. The third goal is to encourage competition

between commercial banks and near-bank financial institutions by reducing the artificial

differentials between their lending rates (World Bank, 1990). Towards this end, restrictions on

commercial bank fees and charges were lifted as of April 1, 1990, providing these institutions

with greater flexibility in determining the cost of borrowing and lending. The Government plans

to adopt a fully liberalized interest rate structure by June 1991.

3.9 In recognition of this policy direction, the model uses the real interest rate to reallocate

domestic credit between the private sector and the public sector, given the pool of credit in the

economy. This means that net credit to the private sector must fall when net credit to the public

sector increases, other things being equal (equation (2)). Accordingly, the private sector's

demand for credit is negatively related to real interest rates, reflecting the negative relationship

between the real interest rate and private investment.

3.10 Research in several countries suggests that the transition from negative to positive

interest rates, rather than the levels themselves, has a more significant impact on the level of

domestic savings. Once the rate becomes positive, further increases appear not to affect savings.

The reasons may be two-fold. First, target savers-persons wishing to reach a certain level of

savings-would not need to increase their savings because of rising interest income from a given

level of savings. This income effect may actually lower savings at higher interest rates. Second,

and in contrast to the first, higher real interest rates raise the opportuniy cost of consumption-

savings and its interest income. Savers may therefore switch from consumption to savings when

real interest rates rise. Because of this indeterminate impact of interest rates and savings in

- 15 -

theory, and indeed in practice, no direct link is forged In the model between domestic savings

and interest rates. Increases in the government's demand for credit would raise the real domestic

loan interest rate and cause private investment (and d.rivatively, private sector credit demand)

to contract. However, aggregate consumpdon need not fall or savings rise if the additional credit

to the govermment is spent on consumption.

3.11 Increases in the real domestic interest rates in the model affect tke demand for currency

negatively, but affect the demand for demand deposits and quasi-money positively (para. 2.5).

In equation (2) therefore, both right and left hand side variables may change. Accordingly, the

policy solution for the residual public sector borrowing requirement of the government which is

fimanced by domestic borrowing would be higher real domestic interest rates, subject to the

indirect changes induced in the assets (currency, deposits, etc) of the monetary system. The

interest rate solution provided by the model also covers any incremental financing which may be

required if higher real, and derivatively nominal, interest rates increase the residual public sector

borrowing requirement. Such increases in the residual public sector requirement are possible

because the debt service obligations of the government would rise as interest rates rise.

The Economics of Monetizing the Fiscal Defcit

3.12 Instead of borrowing domestically to finance the public sector borrowing requirement,

the Government could print money. However, 'excessive' monetary expansion creates inflation.

Loosely speaking, monetary expansion is excessive if it exceeds what individuals would

ordinarily hold at given levels of real income. Annex m shows how the willingness of

individuals to hold mon'v helps to determine the *financeable" fiscal deficit. One of its

conclusions is that the Government mighg be able to monetize a larger fiscal deficit if it is also

willing to tolerate a higher level of domestic inflation.

- 16 *

3.13 Ihe model computes the rate of inflation, measured as the change in the GDP deflator,

which would be required to maintain macroeconomic consistency when given fiscal defichs (or

portions thereof) are monetized at the given level of GDP. Higher inflation raises nominal values

of the domestic interest rates, the exchange rate and GDP growth (at factor cost) but leaves their

real values unchanged. In consequence, real private investment remains unchanged. In contrast,

the demand for currency, demand deposits and quasi-deposits all fail as inflation rises. To

maintain macroeconomic consistency at the fixed level of GDP, the reduction in the demand for

the financial assets-currency, demand deposits and quasi-deposits-must be offset by an increase

in the demand for government debt; that is, the residual public sector borrowing requirement.

In practice, the portfolio reallocation to government debt would be induced by monetary

expansion which raises inflation, reduces real money balances, and yields the government an

inflation tax which eliminates the public sector borrowing requirement.

The Economics of Joint Policy Action

3.14 This solution calculates the exchange rate, interest rate and level of inflation which, if

applied together, would eliminate the residual public sector borrowing requirement and close the

external financing gap. Put differendy, it shows how the same outcome may be obtained by

various combinations of policies. The underlying economies is the same as in the application of

individual policy instruments. But the magnitude of the required adjustment may differ because

of the indirect effects of each policy instrument on the policy target to which it is not directly

assigned. For example, exchange rate depreciation reduces the external financing gap but may

simultaneously worsen govenament revenue (from indirect taxes). It may also worsen the residual

public sector borrowing requirement if the reduction in recurrent revenue is less than the

reduction in govermnent investment expenditure. At the same time however, higher real interest

- 17-

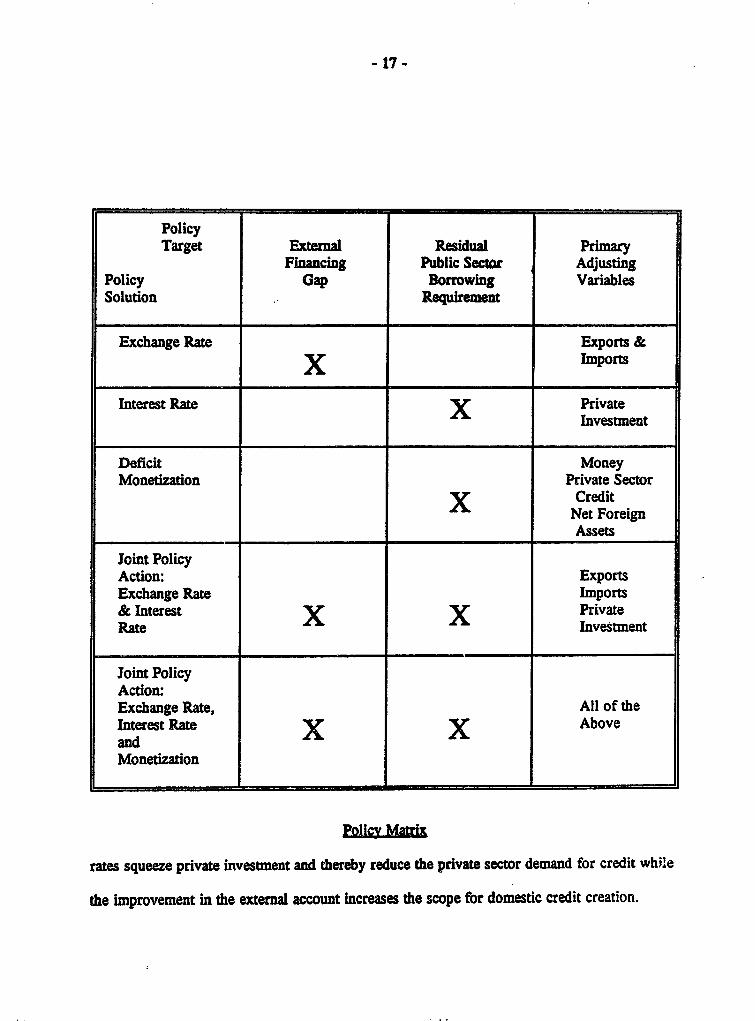

PolicyTarget External Residual Primary

Financing Public Sectr AdjustingPolicy Gap Borrowing VariablesSolution Requirement

Exchange Rate Exports &

X Imports

Interest Rate X PrivateInvestment

Deficit MoneyMonedzation Private Sector

x ~~~~CreditX Net ForeignAssets

Joint PolicyAction: ExportsExchange Rate Imports& Interest X X PrivateRate Investment

Joint PolicyAction:Exchange Rate, All of theInterest Rate X X AboveandMonetization

Poligy Matrix

rates squeeze private investment and thereby reduce the private sector demand for credit while

the improvement in the extemal account increases the scope for domestic credit creation.

- 18 -

Summary

3.1S Ita policy solutions discussed in paras. 3.2 to 3.14 are distlled in the policy matrix

above for easy reference. In brief, the exchange rate solution depends on export expansion and

Import contraction to meet the economy's surplus demand for foreign exchange. The interest rate

solution crowds out private Investment and releases domestic credit to finance the residual public

sector borrowing requirement. Finally, the fiscal deficit could be financed through monetary

expansion which raises inflation and the resulting inflation tax. Our next task is to illustrate these

solutions and thereby demonstrate how the analytical framework presented in this paper could be

helpful in designing macroeconomic policy packages for Kenya.

IV. POLICY SIMULATIONS

4.1 This chapter is illustrative, not predictive or prescriptive. The first and only order of

business is to demonstrate that the tool-the analytical framework sketched in Chapter E-can

calculate policy adjustments which would be required to achieve particular policy targets, given

selected behavioral assumptions and inviolable macroeconomic accounting rules. S/ However,

the leap from illustration to prescription would merely involve agreement on base year data and

behavioral coefficients, most of which are conveniently assembled in one worksheet (Annex IV).

Base Projections

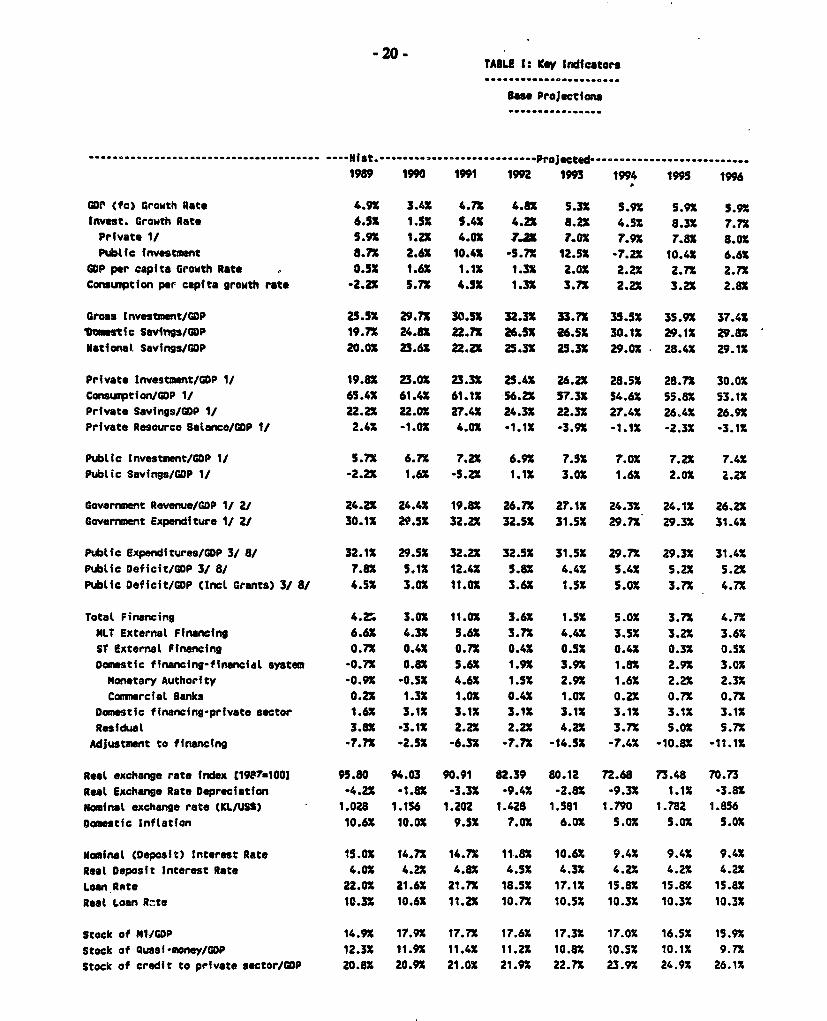

4.2 Table 1 shows key indicators of the Kenyan economy as they would evolve under the

projection rules and assumptions discussed in Chapter 2 and base year data in the input

worksheets in Annex IV. In these base projections, domestic interest rates are based on

I/ . To better demonstmte how the interest rate solution of the modd works, an adjustment factor was used toInflate the residual public sector borrowing requirement (albeit without violating flow of funds consistency).

v 19 -

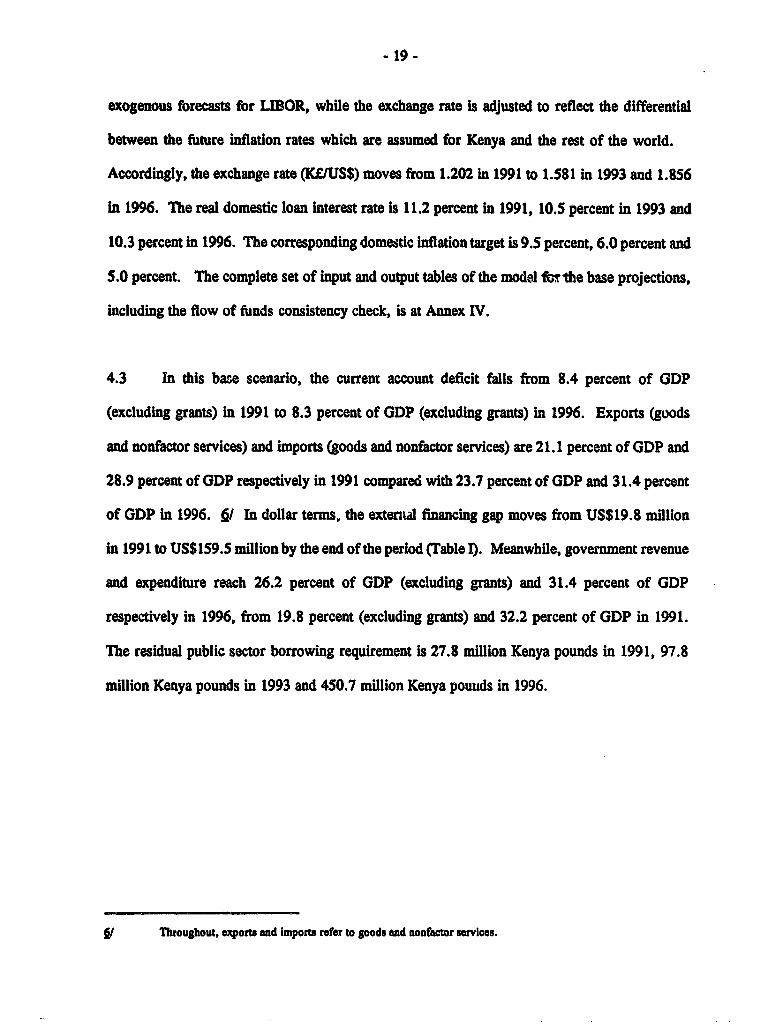

exogenous fbrecasts for LIBOR, while the exchange rate is adjusted to reflect the differential

between the future inflation rates which are assumed for Kenya and the rest of the world.

Accordingly, the exchange rate (K£1US$) moves from 1.202 in 1991 to 1.581 in 1993 and 1.856

in 1996. The real domestic loan interest rate is 11.2 percent in 1991, 10.5 percent in 1993 and

10.3 percent in 1996. The corresponding domestic inflation target is 9.5 percent, 6.0 percent and

S.0 percent. The complete set of input and output tables of the model fori e base projections,

including the flow of funds consistency check, is at Annex IV.

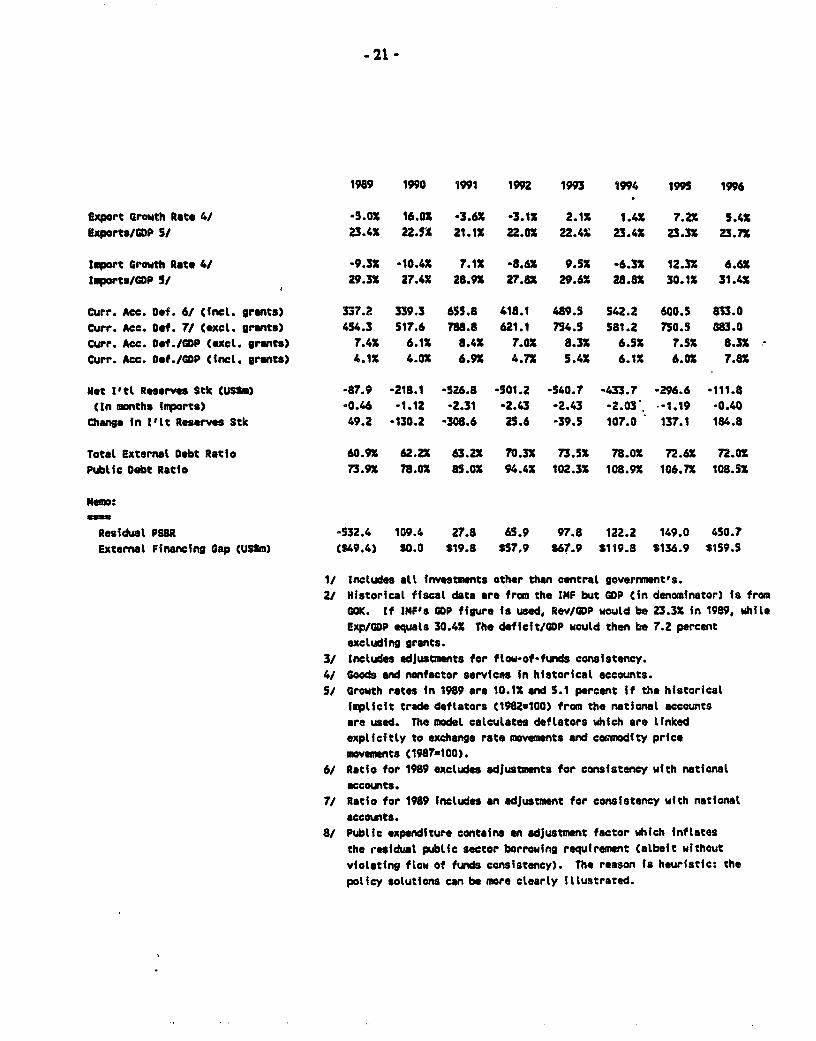

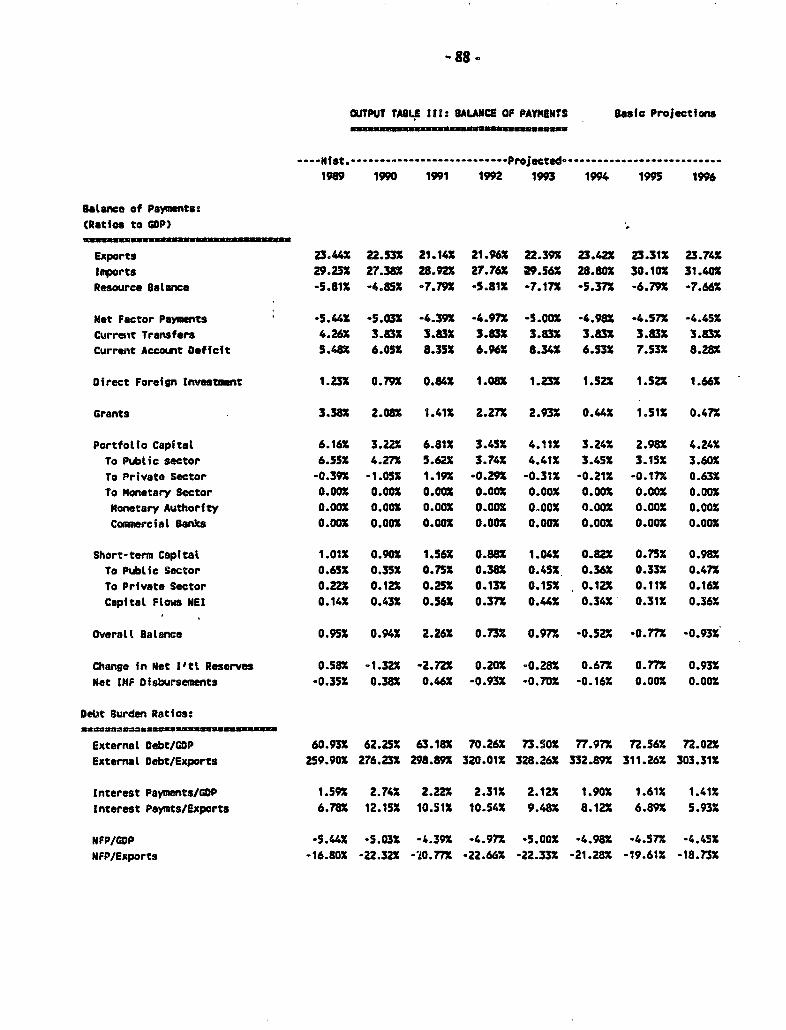

4.3 In this base scenario, the current account deficit falls from 8.4 percent of GDP

(excluding grants) in 1991 to 8.3 percent of GDP (excluding grants) in 1996. Exports (goods

and nonfactor services) and imports (goods and nonfactor services) are 21.1 percent of GDP and

28.9 percent of GDP respectively in 1991 compared with 23.7 percent of GDP and 31.4 percent

of GDP in 1996. 6/ In dollar terms, the external financing gap moves from US$19.8 million

in 1991 to US$159.5 million by the end of the period (Table I). Meanwhile, government revenue

and expenditure reach 26.2 percent of GDP (excluding grants) and 31.4 percent of GDP

respectively in 1996, from 19.8 percent (excluding grants) and 32.2 percent of GDP in 1991.

The residual public sector borrowing requirement is 27.8 million Kenya pounds in 1991, 97.8

million Kenya pounds in 1993 and 450.7 million Kenya pounds in 1996.

f lThroughout, exports and imports refer to goods and nonflactor services.

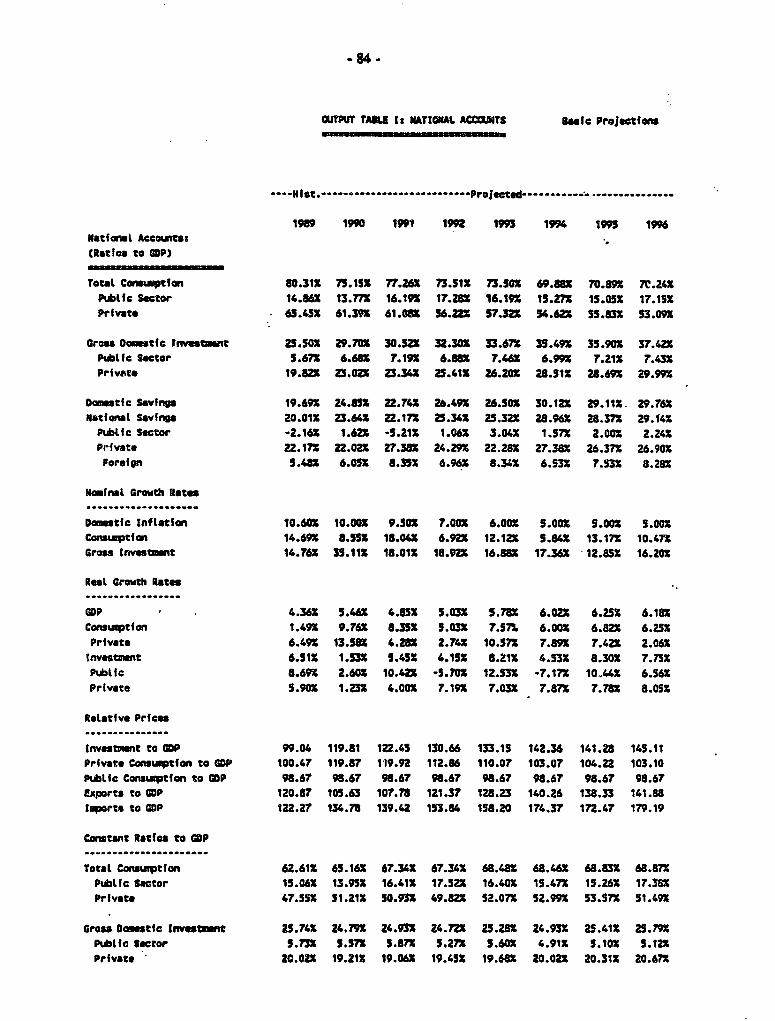

-20 -TABLE I: Key Indfcators..... ......... - - 0,,,

lase Projectlos

. . . . . . .. .Nut......................... Projected. .........................

1989 1990 1991 199Z 1993 1994 195 1996

Gor (fc) Growth Rate 4.9X 3.4X 4.7X 4.82 5.32 5.92 5.92 5.9°tnvest. Growth Rate 6.5X 1.52 5.4X 4.2X 8.22 4.52 8.3X 7.7X

Private 1/ 5.92 1.22 4.02 I?. 7.02 7.9X 7.82 8.02Pubtlic investmnt 8.72 2.6 10.42 5.7X 12.52 -7.2X 10.42 6.6o

GOP per capita Growth Rate 0.32 1.6" 1.1X 1.32 2.02 2.22 2.72 2.72Consumption per capita growth rate -2.2X 5.7X 4.5X 1.32 3.7X 2.2X 3.22 2.82

Gross Investment/GOP 25.52 29.72 30.52 32.3X 33.7S 33.52 35.92 37.42hostic Savings/GOP 19.72 24.82 22.72 26.52 26.52 30.12 29.12 29.82National Savings/GOP 20.0X 23.6S 22.2Z2 25.32 25.3X 29.02 28.42 29.1X

Private Investment/GOP 1/ 19.82 23.02 23.32 25.42 26.2X 28.52 28.72 30.02Consumwtion/GDP 1/ 65.42 61.4X 61.12 56.22 57.3X S4.61 55.8X 53.12Private Savings/GOP 1/ 22.2X 22.02 27.42 24.32 22.32 27.42 26.42 26.92Private Resource Balance/GDP 1/ 2.42 -1.02 4.02 -1.12 -3.9X -1.12 -2.3X -3.12

Public Investment/GOP 1/ 5.7X 6.72 7.22 6.92 7.52 7.02 7.22 7.42Public Savings/GOP 1/ -2.22 1.4X -5.22 1.12 3.02 1.62 2.02 2.22

Governmeent Revenue/GDP 1/ 2/ 24.22 24.42 19.8S 26.72 27.1X 24.32 24.12 26.21Government Expenditure 1/ 2/ 30.12 29.52 32.2X 32.S 31.52 29.72 29.3X 31.42

Public Expenditures/GDP 3/ 8/ 32.12 29.52 32.22 32.52 31.52 29.72 29.3X 31.42PubLic Deficit/GDP 3/ 8/ 7.8% 5.1% 12.42 5.82 4.42 S.42 5.2Z 5.2XPublic Deficit/GDP (Inct Grants) 3/ 8/ 4.52 3.02 11.02 3.61 1.52 5.0X 3.72 4.7X

Total Financing 4.2 3.0X 11.02 3.62 1.52 5.02 3.72 4.7XNLT External Financing 6.62 4.3X 5.6" 3.72 4.42 3.52 3.22 3.6%ST External Financing 0.72 0.42 0.7X 0.42 0.52 0.42 0.32 O.S5Domestic financing-financifL system -0.7X 0.82 5.62 1.9X 3.9X 1.82 2.9X 3.0%

monetary Authority -0.92 -0.52 4.6X 1.52 2.9% 1.62 2.22 2.32CommerciaL Banks 0.2X 1.3X 1.02 0.4X 1.02 0.2% 0.7X 0.72

Domestic financing-private sector 1.6X 3.1X 3.1X 3.1X 3.12 3.12 3.12 3.1%Residual 3.80 -3.1X 2.22 2.22 4.2X 3.7X 5.0X 5.72Adjustment to financing -7.72 -2.52 -6.32 -7.72 -14.5 -.7.4 -10.82 -11.12

Real exchange rate Index C1987s1001 95.80 94.03 90.91 82.39 80.12 72.68 73.48 7o.73Real Exchange Rate Depreciation -4.22 -1.82 -3.3X -9.42 -2.82 -9.3% 1.12 -3.8XNominal exchange rate CKL/USS) 1.028 1.1%6 1.202 1.428 1.581 1.790 1.782 1.856Domestic Inftation 10.62 10.02 9.52 7.02 6.02 5.02 5.02 5.02

omfinal (Deposit) Interest Rate 15.0X 14.72 14.72 11.82 10.62 9.42 9.42 9.42Real Deposit Interest Rate 4.02 4.22 4.8X 4.52 4.3X 4.22 4.22 4.22Loan Rate 22.02 21.62 21.72 18.52 17.12 15.8 15.8 15.82Real Loan Rcte 10.3Z 10.62 11.2X 10.7X 10.5X 10.3% 10.32 10.3X

Stock of Wi/COP 14.92 17.92 17.7X 17.62 17.32 17.0% 16.52 15.9°Stock of auasi-money/GOP 12.32 11.9X 11.42 11.22 10.82 10.5% 10.12 9.7XStock of credit to private sectr/GOP 20.8X 20.9X 21.02 21.9X 22.7X 23.9X 24.92 26.1X

- 21 -

1989 1990 1991 1992 1993 194 1995 1996

Export Growth Rate 4/ 5.0X 16.01 -3.6X 3.11 2.1X 1.4X 7.2X 5.4X

Experts/GDP 5/ 23.46 22.5X 21.1X 22.0X 22.4X 23.41 23.31 23.7X

Import Growth Rate 4/ -9.31 -10.4. T.11 -8.6" 9.5X -6.3X 12.31 6.60

1 arts/GOP 5/ 29.31 27.41 28.91 27.81 29.61 28.81 30.11 31.41

Curr. Ace. Def. 6/ (ineL. grants) 337.2 339.3 655.8 418.1 489.5 542.2 600.5 833.0

Curr. Ace. De.. 7/ (exct. grants) 454.3 517.6 788.8 621.1 754.S 581.2 730.5 883.0

Curr. Acc. Oef./GDP CexcI. grants) 7.41 6.11 8.41 7.01 8.31 6.51 7.51 8.31

Curr. Ace. Oet./GOP (lncl. grants) 4.1X 4.02 6.91 4.71 5.41 6.1X 6.01 7.81

Net I'tl Reserves Stk CUSS.) -87.9 -218.1 *526.8 -501.2 -540.7 -433.7 -296.6 *111.8

Cln months inports) -0.46 -1.12 -2.31 -2.43 -2.43 -2.03 -1.19 -0.40

Change in Ilt% Resrves Stk 49.2 -130.2 -308.6 25.6 -39.5 107.0 137.1 184.8

TotaL ExternaL Debt Ratio 60.91 62.21 63.21 70.31 73.51 78.0x 72.6 72.o0

Pubtic Debt Ratio 73.91 78.01 85.01 94.41 102.31 108.91 106.71 108.51

Memo:

Residual PSIR -532.4 109.4 27.8 65.9 97.8 122.2 149.0 4SO.?

External Financing Gap (USSm) CS49.4) 80.0 819.8 s57.9 S67.9 S119.8 S136.9 S159.5

1/ Includes aLl lnvestmn ts other than central government's.

2/ Historical fiscal data are from the IMF but GOP Cin denomfnator) Is from

GOK. Itf IMFs GDP figure is used, Rev/GDP would be 23.31 in 1989, while

Exp/GOP equals 30.41 The deffcit/GDP would then be 7.2 percent

excluding grants.

3/ Includes adjustments for flow-of-funds consistency.

4/ Goods and nonfactor services in historical accounts.

5/ Growth rates In 1989 are 10.11 and s.1 percent if the historical

implicit trade deflators C1982u1D0) from the national accounts

are used. The model calculates deftlators which are linked

explfcitly to exchange rate movements and comeodity price

movements (198a7100).6/ Ratio for 1989 exeludes adjustments for consistency with national

accounts.7/ Ratio for 1989 fncLudes an adjustment for consistency with national

accounts.8/ Publie expenditure contains an adjustment factor whfch Inftlates

the residual pubife sector borrowing requirement (albeit without

violating flow of funds consistency). The reason Is heuristic: the

policy solutions can be more elearly illustrated.

-22 -

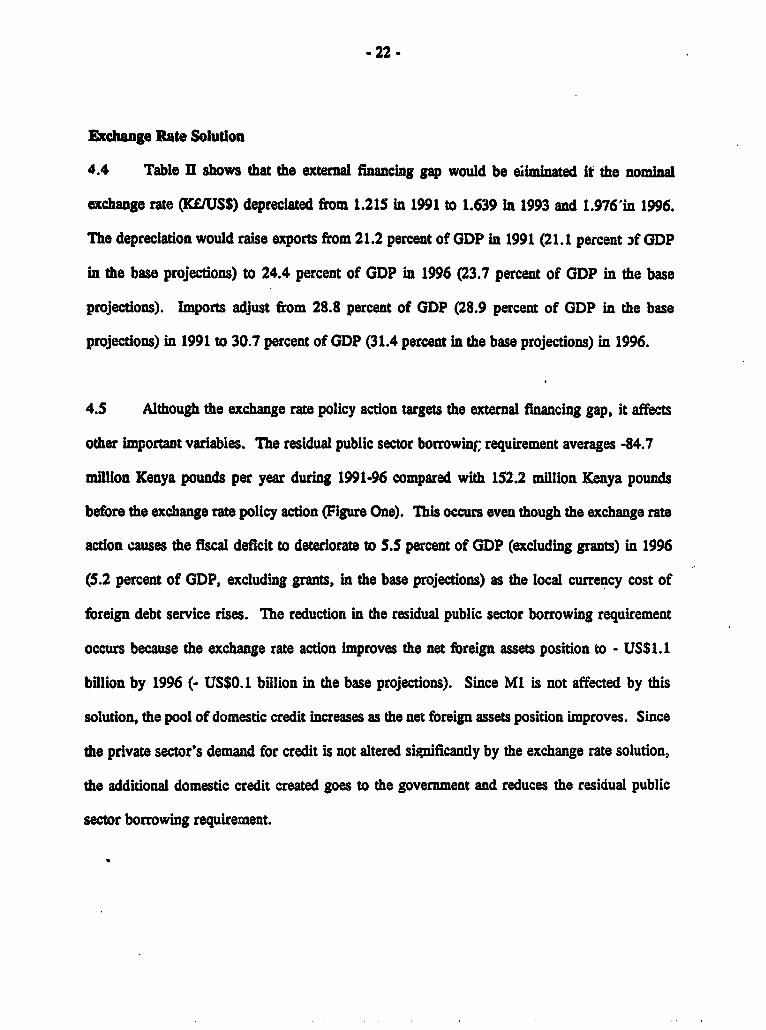

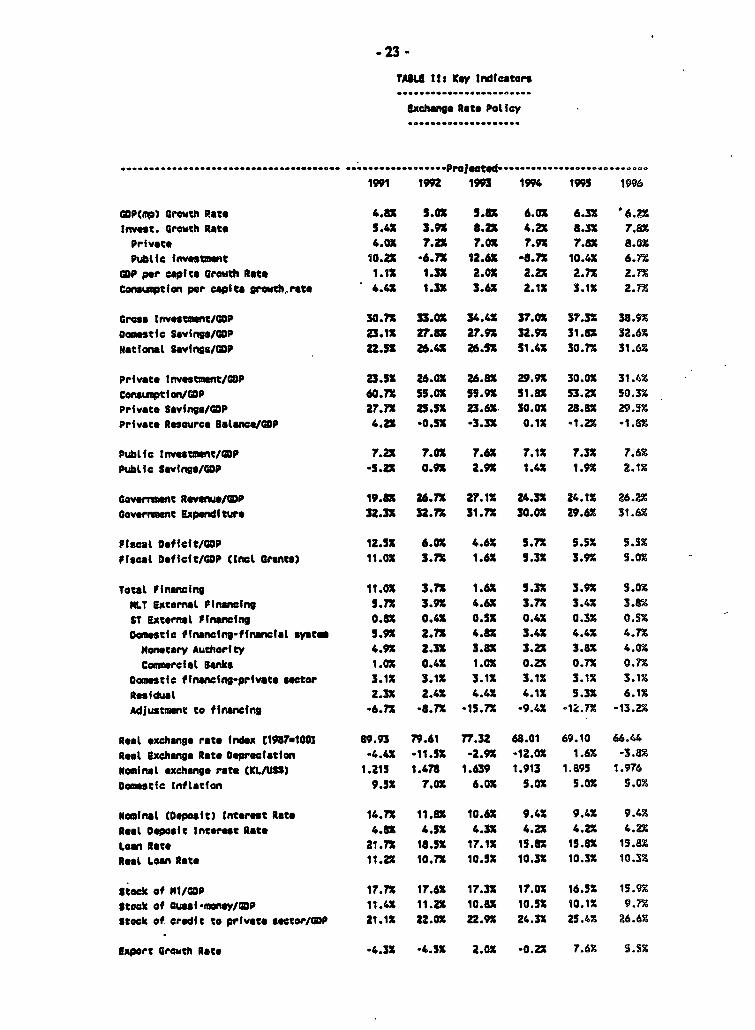

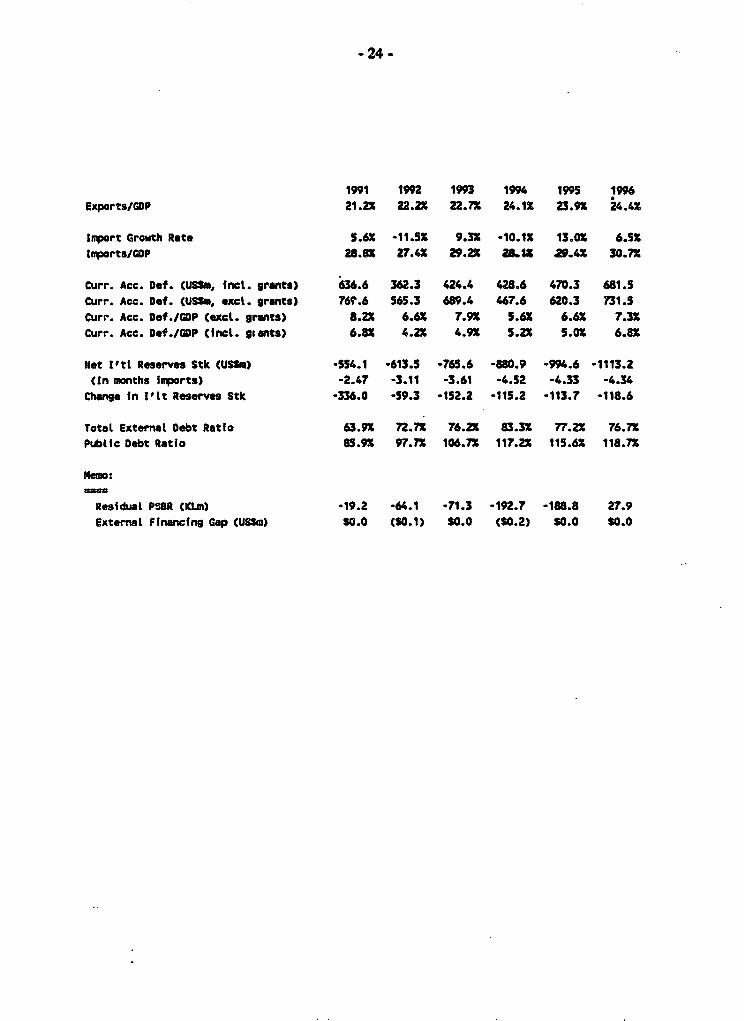

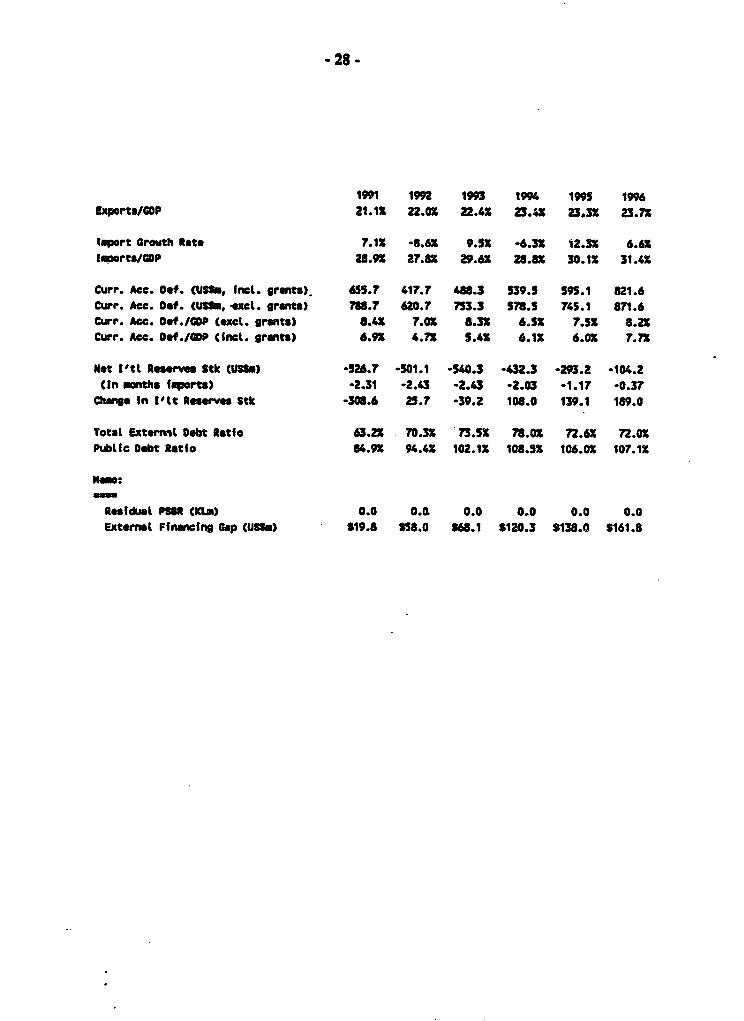

Exchange Rate Solution

4.4 Table II shows that the external financing gap would be eiim;nated It the nominal

exchange rate (K£/USS) depreciated from 1.215 in 1991 to 1.639 in 1993 and 1.976'in 1996.

The depreciation would raise exports from 21.2 percent of GDP in 1991 (21.1 percent 3f GDP

in the base projections) to 24.4 percent of GDP in 1996 (23.7 percent of GDP in the base

projections). Imports adjust from 28.8 percent of GDP (28.9 percent of GDP in the base

projections) in 1991 to 30.7 percent of GDP (31.4 percent in the base projections) in 1996.

4.5 Although the exchange rate policy action targets the external financing gap, it affects

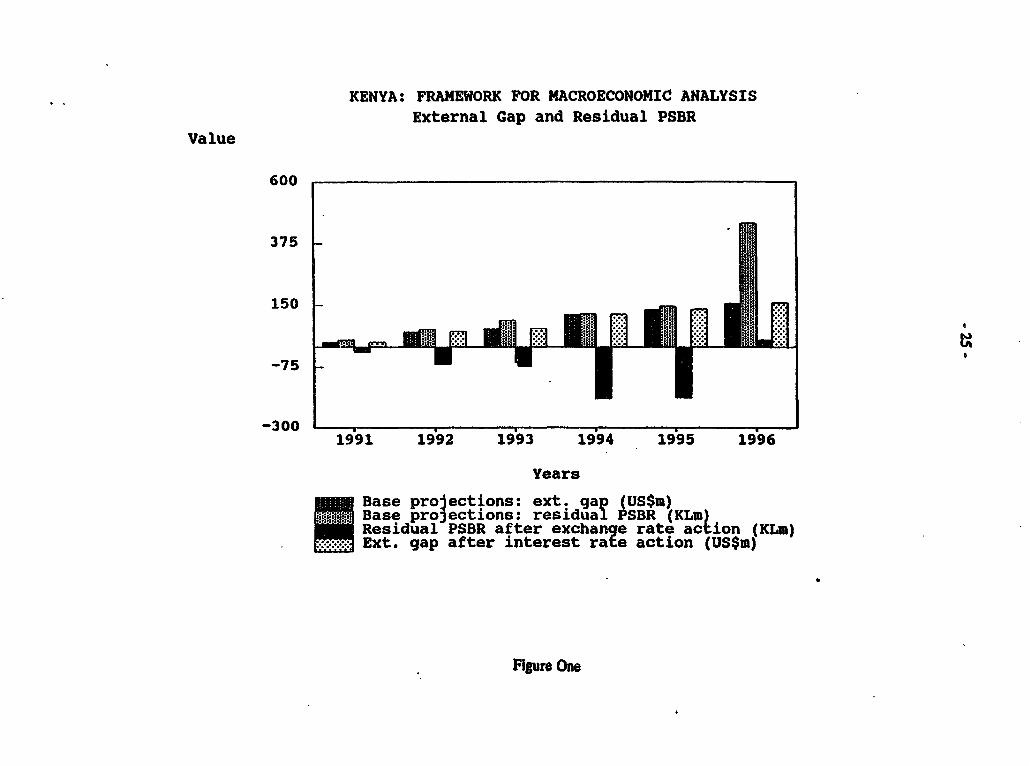

other important variables. The residual public sector borrowing requirement averages -84.7

million Kenya pounds per year during 1991-96 compared with 152.2 million Kenya pounds

before the exchange rate policy action (Figure One). This occurs even though the exchange rate

action causes the fiscal deficit to deteriorate to S.5 percent of GDP (excluding grants) in 1996

(5.2 percent of GDP, excluding grants, in the base projections) as the local currency cost of

foreign debt service rises. The reduction in the residual public sector borrowing requirement

occurs because the exchange rate action improves the net foreign assets position to - US$1.1

billion by 1996 (- US$0.1 billion in the base projections). Since Ml is not affected by this

solution, the pool of domestic credit increases as the net foreign assets position improves. Since

the private sector's demand for credit is not altered significantly by the exchange rate solution,

the additional domestic credit created goes to the government and reduces the residual public

sector borrowing requirement.

-23-

TABU tt: Key tditcartos

xchawge Rate Pot icy....................

,, ,,,,,,,,,,.,,,,,,,,,, ............. Prolected......................

1991 1992 199 1994 1995 1996

UDP(tp) Growth Rate 4.8J 5.03 5.X 6.02 6.3X 6.2Invest. Growth Rate 5.4X 3.9X 8.2X 4.2X 8.32 7.82Private 4.02 7.23 7.ox 7.92 78X 8.0XPubtic investmet 10.2X 6.7X 12.62 -8.72 10.41 6.72

GOP per capita Growth Rate 1.1 1.3X 2.0X 2.2X 2.73 2.72Conswptifn per capita grcosh rat 4.X 1.33 3.62 2.1X 3.1X 2.7X

Gross Investment/UP 30.73 33.0% 34.42 37.02 37.32 38.92Doamestfc Savings/GOP 23.1X 27.8x 27.92 32.9X 31.82 32.62Naltialt Savings/GP 2.5X 26.4X 26.52 31.42 30.7Z 31.62

Private tnvestment/GOP 23.53 26.02 26.82 29.9X 30.02 31.4bConsmptifa/GDP 60.72 55.02 55.92 51.82 53.2% 50.3%Prfvate Savfngs/DP z2.7x 25.52 23.62 30.02 28.82 29.5sPrivate Resource Bata COP 4.2X *0.5X -3.32X O.X -1.2 -1,2X

Pubtfc Investment/COP 7.2x 7.0x 7.6X 7.1X 7.3x 7.62Pubic Savings/GOP -5.ZX 0.9X 2.92 1.42 1.92 2.12

Government Revenue/U0P 19.80 26.72 27.12 24.33 24.1X 26.2%Government Expenditure 32.33 32.7X 31.72 30.02 29.62 31.6X

Fiscalt Defict/UP 12.52X 6.0 4.6X 5.72 5.52 5.35

Ffscal Deficit/GP CInol Grants) 11.0X 3.7X 1.62 5.32 3.9z 5.02

Totat financing l1.OX 3.72 1.62 5.3X 3.9X 5.0XNLT Externml Financing 5.72 3.9X 4.62 3.72 3.42 3.8%

ST External Financfng 0.82 0.42X O.5 0.42 0.33 0.5XDomestec financing-ffnancitl syats 5.92 2.72 4.82 3.42 4.42 4.7Z

Monetary Authority 4.92 2.32 3.82 3.2X 3.82 4.02Commrciat Banks 1.OX 0.4X 1.02 0.2 0.7X 0.7%

Ocm tic fInncing-prfvate setor 3.1X 3.12 3.12 3.12 3.12 3.12Residual 2.3X 2.42 4.42 4.12 5.3X 6.12Adjustment to financing -6.72 -8.7 15.7X -9.42 -12.7% -13.2X

Rest exchange rate index C198741003 89.93 79.61 77.32 68.01 69.10 66.44Rest Exchange Rate Deprecatfon -4.42 -11.32 -2.92 -12.02 1.68 -3.82Nominat exchange rate CKL/U35) 1.215 1.478 1.639 1.913 1 .B9 1.976Domestic Inflatfon 9.53 7.02 6.02 5.0X 5.0X 5.0J

Nominal (Oeposit) Interest Rats 14.72 11.82 10.6X 9.4X 9.42 9.4%

Rest Deposit Interest Rate 4.82 4.52 4.3X 4.2Z 4.22 4.2XLoan Rate 21.72 18.5X 17.1X 19.82 15.82 15.82Reat Loan Rate 11.2X 10.7X 10.52 10.32 10.3X 10.32

Stock of MI/GOP 17.72 17.62 17.32 17.0X 16.52 15.9%Stock of uai-mney/GDP 11.42 11.22 108 10.52 10.12 9.72stock of credit to private setor/UP 21.12 22.0X 22.92 24.32 25.42 26.62

Export Growth Rate .4.32 -4.53 2.02 -0.22 7.62 5.52

-24-

1991 1992 1993 1994 1995 1996Exports/GOP 21.2X 22.2X 22.7X 24.12 23.9X 24.42

Inport Growth Rate S.6 -11.52 9.32 -10.12 13.0X 6.52Imports/GOP 28.82 2.42 29.2 ZaLIX 29.4x 30.7X

Curr. Acc. Oef. CUSS, inct. grants) 636.6 362.3 424.4 428.6 470.3 681.SCurr. Ace. Oef. (USS., exel. grants) 769.6 565.3 689.4 467.6 620.3 731.5Curr. Ace. Oaf .GOP (axeL. grants) 8.22 6.62 7.92 5.62 6.62 7.32Curr. Ace. D*f./GDP Cnet. giants) 6.8X 4.22 4.92 5.22 5.02 6.82

Net I'tl Reserves Stk USSW) -554.1 .613.5 -765.6 -880.9 -994.6 -1113.2(Cn months Imports) -2.47 -3.11 -3.61 -4.52 -4.33 -4.34

Change fn Pllt Reserves Stk -336.0 -59.3 -152.2 -115.2 -113.7 -118.6

TotaL Extemal Debt Ratio 63.9X 72.72 76.22 83.32 77.22 76.72Public Debt Ratio 85.92 97.72 106.72 117.22 115.62 118.72

Memo:

Residual PS5R CKLm) -19.2 -64.1 .71.3 -192.7 -188.8 27.9ExternaL Financig Gap CUSSm) SO.0 CSO.1) 90.0 CS0.2) S0.0 80.0

KENYA: FRAMEWORK FOR MACROECONOMIC ANALYSISExternal Gap and Residual PSBR

Value

600

375-

150

-75-

-300 1991 1992 1993 1994 1995 1996

Years

Base projections: ext. gap (US$m)gRR Base projections: residual PSBR (KLm)

Residual PSBR after exchange rate action (KLm)Ext. gap after interest rate action (US$m)

Figure One

26 -

The Interest Rate Solution

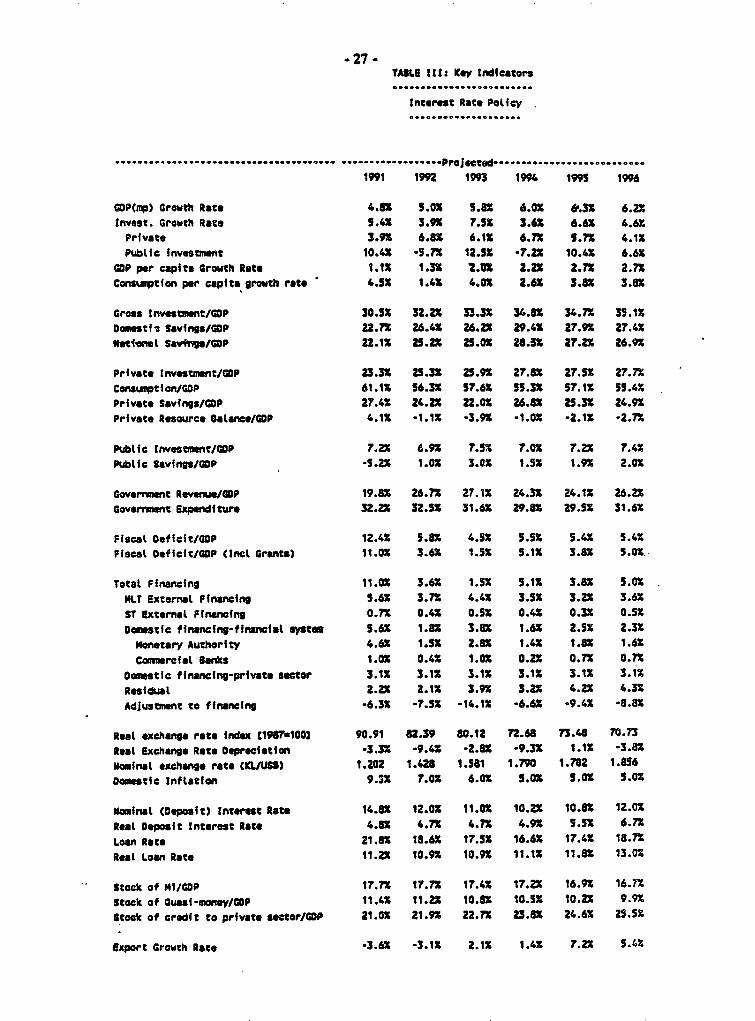

4.6 The results of the interest rate policy action are presented in Table m. The real

domestic loan interest rate which would eliminate the residual public sector borrowing

requirement is 11.2 percent in 1991, 10.9 percent in 1993 and 13.0 percent in 1996. The figures

for the base projections are 11.2 percent, 10.5 percent and 10.3 percent respectively. The kty

adjusting variable is private investment which is 23.3 percent of GDP in 1991, 25.9 percent of

GDP in 1993 and 27.7 percent of GDP in 1996 (Table Im). In comparison, it is 23.3 percent of

GDP in 1991, 26.2 percent of GDP in 1993 and 30.0 percent of GDP in 1996 in the base

projections (Table 1). Similarly, the stock of credit to the private sector in 1996 is 25.5 percent

of GDP after interest rate policy action but is 26.1 percent of GDP in the base projections.

4.7 The interest rate policy action causes government expenditure to reach 31.6 percent of

GDP in 1996 (31.4 percent in the base projections), reflecting higher interest payments and larger

domestic debt. Since loan and deposits interest rates move in the same direction under this

scenario, the policy action also affects the demand for currency, demand deposits and time

deposits. Table m shows a marginal increase in the stock of MI and quasi-money in 1996 to

26.6 percent of GDP relative to 25.6 percent of GDP in the base projections. Since the policy

action leaves domestic credit unchanged, the net foreign assets position worsens slightly from - -

- US$111.8 million in 1996 in the base projections to - US$104.2 million after the interest rate

policy action. In turn, the external financing gap rises marginally to US$161.8 million compared

with US$159.5 million in the base projections (Figure One).

-27 -TA3LB ItSS Key Indicators.......... ................. ,0

Interest Rate Policy....................

--... .-.. .-... .. Projected. ...................

199 1992 199 1994 1995 199

GOP(mp) Growth Rate 4.IIX 5OX 5.83 6.0b 6&.3X 6.23

tnvest. Growth Rate 5.4X 3.93 7.53 3.6X 6.6X 4.61

Private 3.93 6.8 6.1X 6.7 5.73 4.1X

PublIc invesmnt 10.4IX *9.7 12.53 7.21 10.4X 6.6X

GOP per capita Growth Rate 1.1X 1.3X 2LU 2.ZX 2.73 2.73Conswpton per capita growth rate 4.5X 1.4X 4.03 2.61 3.8X 3.81

Gross Investenwt/GOP 30.5X 32.2X 33.3X 34.8X 34.73 35.13

Damestfi Savings/GOP Z.7X 26.4X 26.2 29.4$ 27.93 27.43

9tfiol Sav+in/GDP 22.1Z 25.2 Z5.0X 28.5X 27.21 26.93

Private Investment/GOP 23.3X 25.3X 25.93 27.83 27.5 27.73

Coneusttion/GOP 61.13 56.3X 57.63 55.31 57.13 59.41

Private Savings/COP 27.41 24.2X 22.03 o 26.X 25.33 24.91

Private Resource Balance/GOP 4.13 -1.13 -3.9X -1.01 -2.13 -2.7X

Public Investment/GOP r.2 6.93 7.52 7.03 7.23 7.43

Pubifc Savings/GDP -5.2X 1.03 3.DX 1.5X 1.93 2.01

Government ReveCD/GOP 19.86 26.7X 27.11 24.3X 24.13 26.22

Goverrent Expenditure 32.2X 32.53 31.6 29.8X 29.51 31.6X

Fiscat efficit/GOP 12.4S 5.sx 4.53 5.5X 5.41 5.43

Fiscal Deffcit/GOP (tmc Grants) 11.03 3.61 1.53 5.11 3.8X 5.0S

Total Financing 11.0X 3.6Z 1.53 5.11 3.8x 5.03

NLT External Finncing 5.6X 3.77 4.4X 3.5X 3.23 3.6X

ST External financing 0.73 0.41 0.53 0.43 0.31 0.53

Domestc financing-financial syetem 5.61 1.86 3.Z 1.61 2.53 2.33

ne14tary Authority 4.61 1.51 2.86 1.43 1.83 1.61

Conarcial Banks 1.01 0.43 1.03 0.2X 0.73 0.73

Domestic financing-private seator 3.13 3.11 3.13 3.13 3.13 3.13

Residual Z.2X 2.1X 3.9x 3.21 4.21 4.33

Adjustment to financing -6.35 -7.5X -14.11 -6.61 -9.43 -8.8%

Resl exchange rate index C1981o0o] 90.91 82.39 80.12 72.68 7148 70.73

Real Exchane Rate Depreciation -3.3S -9.41 -2.86 -9.33 1.13 -3.81

Nominal exchange rate CU L/USS) 1.202 1.428 1.581 1.790 1.7a2 1.856

oamstic inflatfon 9.21 7.o0 6.03 5.03 5.0X 5.03

mina l COepasit) Interest Rate 14.6X 12.03 11.01 10.23 10.83 12.03

Real Deposit Interest Rate 4.81 4.73 4.7X 4.9X S.X 6.73

Loan Rate 21.8X 18.63 17.53 16.63 17.43 18a.7Real Loan Rate 11 .ZX l.93 lo.9x 11.11 11.63 13.03

Stock of M1/GOP 17.73 17.73 17.41 17.2X 16.93 16.73

Stock of Guasf-money/GOP 11.43 11.21 10.63 10.53 10.23 9.93

Stock of credit to private sector/GOP 21.03 21.93 22.73 23.8X 24.63 25.5S

Export Growth Rage .3.61 -3.13 2.13 1.41 7.2x 5.46

- 28 -

1991 1992 1993 199 1995 196Exprtas/OP 21.1t 22.02 22.4X 23.X 23.3X 23.7X

taort Grath Rate 7.1X -8.6 9.52 -6.3X 12.3X 6.62Imorts/GOP 28.9X 27.8 29.6X 28.8X 30.12 31.42

Curr. Acc. Def. CMs, Mld. grants). 655.7 417.? 488.3 539.5 595.1 821.6Curr. Ace. Otf. (USM,6 exel. grants) 78.7 620.7 73.3 578.5 745.1 871.6Curr. Ace. D*f./GDP Cexal. gornts) 8.4X 7.0 8.32 6.52 7.5s 8.22Curr. Ace. Def./GOP (Inst. grants) 6.9X 4.72 5.4 6.12 6.0X 7.72

Net I'tt Rserves Stk CIUSM) -S26.7 -501.1 -540.3 -432.3 -293.2 -104.2(in months aports) -2.31 -2.43 -2.43 -2.03 -1.17 -0.37

Change in Iltt Reseves Stk -308.6 25.7 -39.2 108.0 139.1 189.0

Total Extermt Debt Ratfo 63.22 70.3 n73.52 78.02 72.6 72.02Publle Debt Ratfo 84.92 94.42 102.12 108.52 106.02 107.12

Ne:

Residuat PSI CKL.) 0.0 0.A 0.0 0.0 0.0 0.0External Ffnrclng Cap (UP.) 119.8 158.0 S68.1 1120.3 1138.0 1161.8

- 29 -

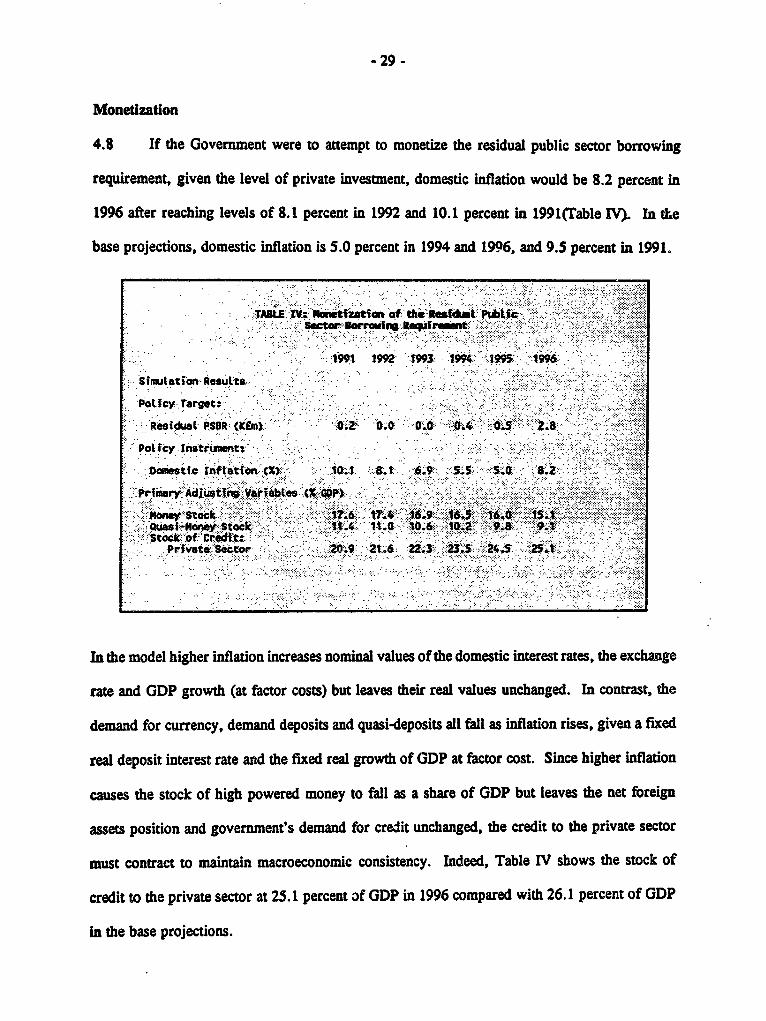

Monetization

4.8 If the Government were to attempt to monetize the residual public sector borrowing

requirement, given the level of private investment, domestic inflation would be 8.2 percent in

1996 after reaching levels of 8.1 percent in 1992 and 10.1 percent in 199 1(Table IV)- In the

base projections, domestic inflation is 5.0 percent in 1994 and 1996, and 9.5 percent in 1991.

.. . ,: NTBe.:.t .,:.:::.:.tiati of.. t,es i .ph .t

sector ' .. Mem -'.f-.:'.-.f ..̀.. ... . .- . ... ..

1991 1992 t993 194 .199 1:996

Simutation ResuLts. ... -

PoQty Target.-

ResidL PSSR (KEin) 0.' O.GX D.0 0 Ov 4. 05....... 2, & :. .. .du: : - O iR- .K M.: . . a

-Pot fcy r nsteument.. : ,

cm: est1.C tInfation (X): - .:11 .-. t .6.9 -5< -5* :S. a iz

. :;mry Adui tJ4 V taestX . .

.Oe .. i Stack 17:< 'F .6 1.4 :~. 1:.'4. 16 0t7 IS{ fi$ 8v.5 ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~..'t o , .". : dX*. ' C<*.......

0uasi-morey S3tockt. A106 0Z 9& 91.::stock". o Cre zt:

Prfvate or 2 2. 9 : . 23.5 2 25A

In the model higher inflation increases nominal values of the domestic interest rates, the exchange

rate and GDP growth (at factor costs) but leaves their real values unchanged. In contrast, the

demand for currency, demand deposits and quasi-deposits all fall as inflation rises, given a fixed

real deposit interest rate and the fixed real growth of GDP at factor cost. Since higher inflation

causes the stock of high powered money to fall as a share of GDP but leaves the net foreign

assets position and government's demand for credit unchanged, the credit to the private sector

must contract to maintain macroeconomic consistency. Indeed, Table IV shows the stock of

credit to the private sector at 25.1 percent of GDP in 1996 compared with 26.1 percent of GDP

in the base projections.

-30 -

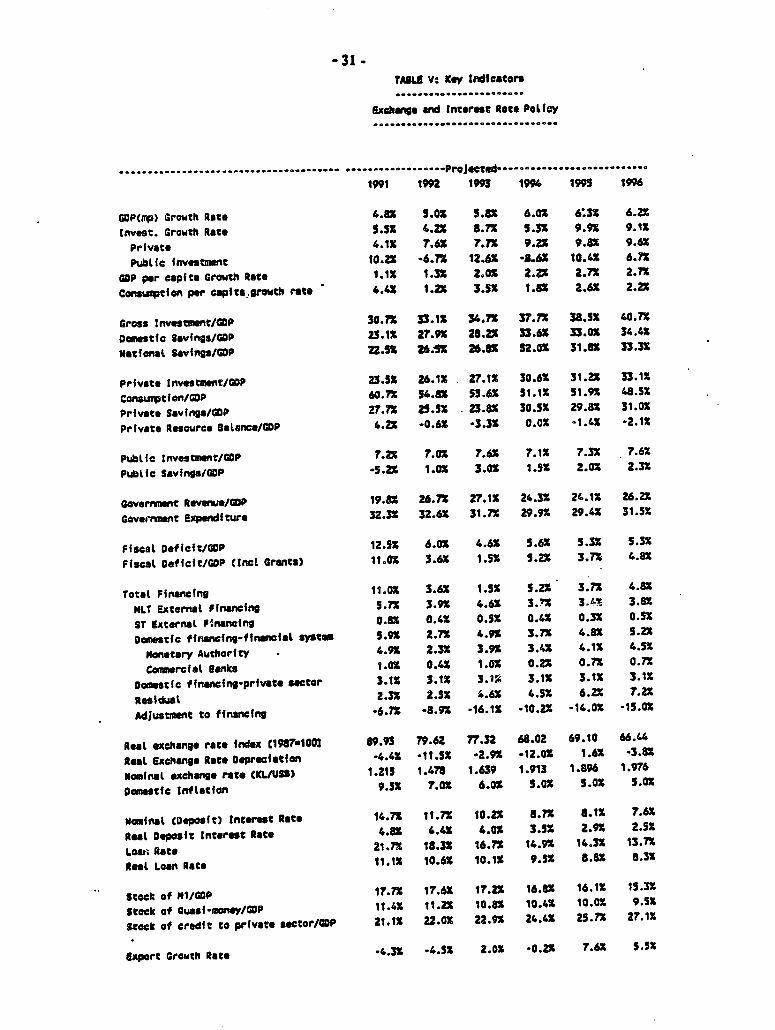

Joint Exchange Rate and Interest Rate PoUcy Action

4.9 Table V presents the key economic indicators when joint exchange rate and interest rate

policy action is taken to eliminate a public sector borrowing requirement which is additional to

an external financing gap. Exchange rate action retuces the residual public sector borrowing

requirement compared to a situation in which no such action is taken (para. 4.5).

In principle, the interest rate policy action also reduces the overall demand for credit in the

economy relative to the base projections. From this perspective therefore, the required exchange

rate adjustment would be expected to approximat that of the independent exchange rate policy

solution while the required interest rate adjustment would be less than in the independent interest

rate policy solution (Figure Two). These expectations are confirmed by the simulation results

presented in Table V.

4.10 The required real domestic loan inerest rate is 11.1 perce' a 1991, 10.1 percent in

1993 and 8.3 percent in 1996. In comparison, it is 11.2 percent in 1991, 10.9 percent in 1993

and 13.0 percent in 1996 when only interest rate policy action is taken. The equilibrating

interest rate is lower because the net foreign assets increase to - US$1119.4 million in i996 aoint

exchange rate and interest rate action) compared with - US$104.2 million (mterest rate action

only). Because the pool of domesdc credit increases when joint exchange rate and interest rate

action are taken, more private investment can be accommodated for a given level of residual

public sector borrowing. Thus, private investment is only 27.7 percent of GDP in 1996 when

interest rate policy action is used (33.1 percent with joint policy action).

-31 -TAILS VS Key tndieators........ .............. .,..,

Ixoange wad Interest Rate PolICy.................................

,, ,,,,,,....- P r d........ ,,,.,,,,,........ - "Prol ed ..........................

191 1992 193 19K 199S 1996

GOP(ap) Growth Rate 4.82 5.0X 5.8X 6.02 6 3X 6.2%Invest. Growth Rate 5.52 4.22 8.72 5.32 9.92 9.12

Private 4.12 7.62 7r.7 9.22 9.82 9.62Public investment 10.22 -6.72 12.62 -8.6X 10.41 6.71

GOP per capita rowth Rate 1.1X 1.32 2.02 2.2X 2.72 2.?XConaurptifn per capita.growth r ate 4.4X 1.2X 3.12 1.82 2.62 2.2X

Gross Investment/GUP 30.7X 33.12 34.?X 37.7X 38.52 40.72Domestic Savings/GUP 23.12 27.92 28.2% 33.6X 33.02 34.42lational SavIngs/GP 22.5 26.51 26.82 52.02 31.82 33.32

Private tnvestment/UP 23.52 26.12 27.12 30.62 31.22 33.12Consuiption/GDP 60.7X 54.82 55.62 51.12 51.92 48.5XPrivste Savings/UOP 27.72 25.52 23.82 30.52 29.82 31.02Private Resource Balanne/CP 4.22 -0.62 -3.32 0.02 -1.42 -2.12

Pubtlc InvestmnUt/GOP 7.Z4 7.0o 7.61 7.12 7.3x 7.62PubLic Savings/GUP -5.22 1.02 3.02 1.52 2.02 2.32

Government Revenue/UP 19.82 26.72 27.12 24.3X 24.12 26.22Govenrant Expendfture 32.32 32.62 31.7% 29.92 29.42 31.5X

Fifscal Deficit/GP 12.52 6.0X 4.6X 5.62 5.32 5.32FIscat Defifit/GDP (Inct Grants) 11.0X 3.62 1.52 1.2% 3.71 4.8%

Total Ffnancfng 11.02 3.6X 1.52 5.22 3.71 4.82NLT External Financfng 1.72 3.92 4.62 3.7X 3.t% 3.82ST External Penancing 0.82 0.42 0.5% 0.41 0.32 O.5Danmestic ffnancing-ff fnaal sstom 5.92 2.72 4.92 3.7X 4.82 5.22

Monetary Authority . 4.92 2.32 3.92 3.42 4.1S 4.5%Conmercfel Banks 1.02 0.42 1.02 0.21 0.71 0.7X

Doamstfc ffnaning-prfvate owstor 3.1X 3.1% 3. W 3.1X 3.12 3.11Residual 2.32 2.52 9.6X 4.52 6.22 7.22Adjustmn t to financing -6.72 -8.92 .16.1X -10.22 -14.02 -15.02

Real exchange rate Index t1987*1003 89.93 79.62 77.32 68.02 69.10 66.44Real Exchange Rate Depreciatfon -4.4Z -11.51 -2.9% -12.02 1.6X -3.82Nominal oxchwne rate CKL/USS) 1.215 1.478 1.639 1.913 1.896 1.976Domestic Inflatfin 9.5X 7.ox 6.02 5.0X 5.0X 5.02

ominafl (Deposit) Internet Rate 14.7X 11.72 10.2% 1.72 8.12 7.62Real Dwosit Interest Rste 6.82 4.42 4.02 3.52 2.9X 2.32Loan Rate 21.72 18.32 16.72 14.92 14.32 13.71Rtes Loan Rate 11.11 10.6X 10.12 9.52 8.82 8.32

Stockz of Mi/UP 17.72 17.62 17.2% 16.82 16.12 15.32Stock of Quas-monay/GDP 11.42 11.2X 10.82 10.42 10.0 9.52Stock of credft to private sector/UDP 21.12 22.02 22.9% 24.42 25.71 27.12

export Growth Rate -4.32 .4.5X 2.02 -0.22 7.62 5.52

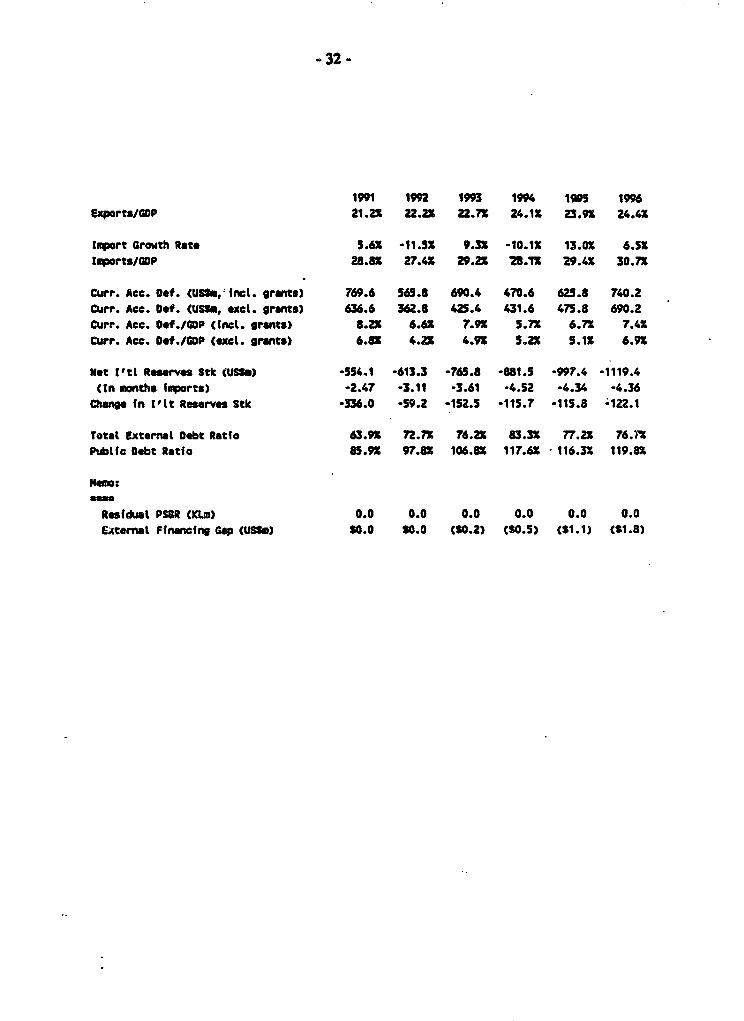

-32 -

1W1 1992 1993 1994 Sws 1996Exports/GOP 21.2X 22.2X 22.7X 24.1X 23.9X 24.4X

lIport Growth Rate 5.6X -11.52 9.32 -10.12 13.02 6.52Imports/GOP 28.82 27.42 29.2X 5.1M 29.42 30.72

Curr. Ace. Daf. CUSS., rct. grants) 769.6 565.8 690.4 470.6 625.8 740.2Curr. Ace. Def. (USSm, exet. grants) 636.6 362.8 425.4 431.6 475.8 690.2COrr. Ace. Oe /ClDP (anct. grants) 8.2X 6.62 7.9X 5.72 6.72 7.4XCurr. Ace. Def./GDP texel. grants) 6.82 4.21 4.9X 5.2X 5.1X 6.92

Net I'tL Reserves Stk (USSW) -554.1 -613.3 -765.8 -881.5 -997.4 -1119.4(In onths faports) -2.47 -3.11 -3.61 -4.52 -4.34 -4.36

Change fn [lOt Reserves Stk -336.0 -59.2 -152.5 -115.7 -115.8 .122.1

Totat External Debt Ratio 63.92 72.7X 76.2X 83.32 77.22 76.i%Pubtic Debt Ratio 8S.92 97.82 106.82 117.oX 116.32 119.82

1e:

Residual PS8R tKLM) 0.0 0.0 0.0 0.0 0.0 0.0EAternat Financing G Up tU) S0.0 0.0 (30.2) (30.5) (31.1) tS1.8)

uue1 iieah - -'USA

.~~~~~~~~~~~~~~~~~

am~~~~~~~~~

T2

142.eiwm,ms m¶a2135

"i mo "Oumi tw9 is"yai

............ . t

9441 1661 91 144 244 leSsn

S.n

.~~~~~~~~~~~~~~~~~,

onWTn Ab t va S.OM WM To".insftwv A" XMAOM & ...

awl~~~~~~~I2

$2.1

; n Iw .lmmmi *33 ESmt £t * 4 t

..................... .....

u..w-- --m- -A°t1 w

63 m ,=.B OMV

9461 4441 9641 1461 3441 164!-- ~ ~ ~ ~ ~ ~ ~ ~ ~~~3

nzs

.* £63.1~~~~~~~~~~~~~~*

uzui. azm i E.U - ' YUUt

-34 -

Joint Exchange Rate and Intereat Rate Policy Actiop and Monetization

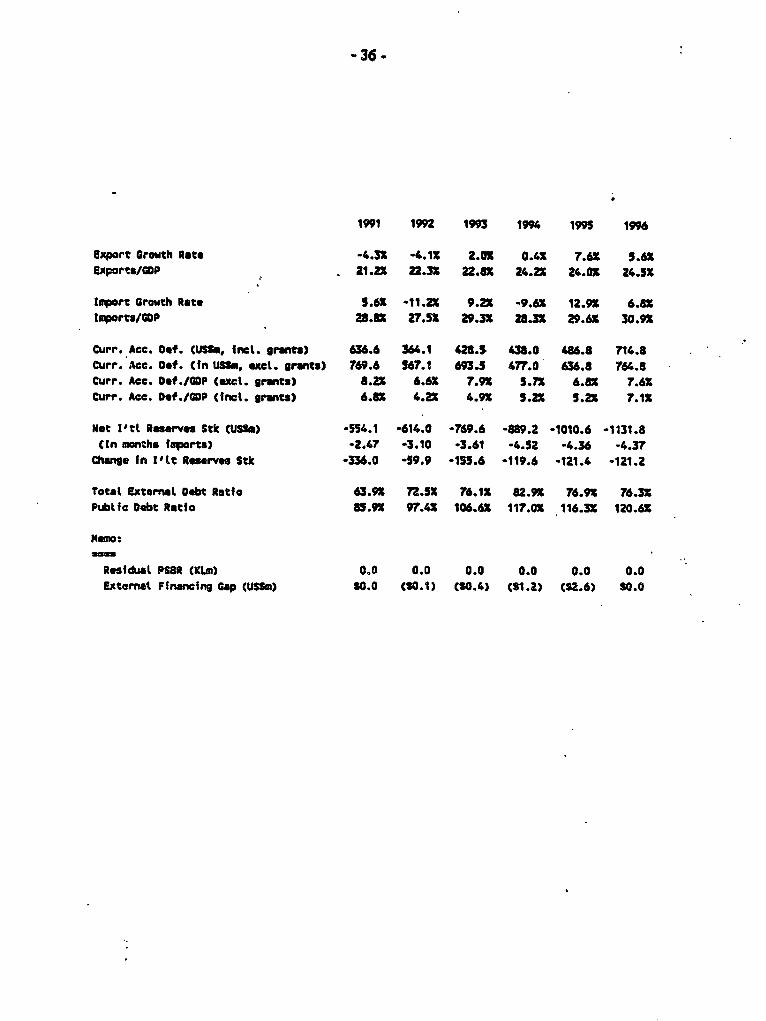

4.11 The simulation results in Table VI are from joint exchange rate and interest rate policy

action and monedzation of the residual public sector borrowing requirement. Viewed

appropriately, this scenario is one of exchange rate and interest rate policy action when the

domestic inflation target is not of primary concern. In &ict, under this scenario infladon is

allowed to reach 8.5 percent in 1992 and 6.5 percent in 1993 compared with 7.0 pecent and 6.0

percent respectively in the base projections. Real domestic interest rates also behave differently:

11.1 percent in 1991, 9.7 percent In 1993 and 5.3 percent in 1996 when the exchange rate,

interest rate and monetization are used; 11.2 percent in 1991, 1O.S percent in 1993 and 10.3

percent in the base projections; 11.2 percent in 1991, 10.9 percent in 1993 and 13.0 percent in

1996 when the interest rate is used alone; and 11.1 percent in 1991, 10.1 percent in 1993 and

8.3 percent in 1996 when joint exchange rate and interest rate policy action is taken (Figure

Two). Clearly, the interest rates are lowest when all three policy options are activated

simultaneously. Then private investment reaches 36.0 percent of GDP in 1996 compared with

27.7 percent of GDP in 1996 when the interest rate policy is used aloae, and 33.1 percent when

interest rate policy is supported by exchange rate policy action. In sum, the economy reaches

a higher equilibrium path but experiences slightly higher inflation than all scenarios except when

the fiscal deficit is monetized.

Summary of Simulation Results

4.12 Para. 1.2 identified domestic macroeconomic imbalances as threats to recent economic

and stabilization gains In Kenya. The prevailing threats arise, in part, from high fiscal deficits,

monetary expansion and external shocks. The gains originated, in part, in adjustment programs

which reduced the fiscal deficit and lowered its domestic financing, maintained positive real

borrowing prudently. Other reforms in key sectors such as agriculture, industry and interest

-35 -

tASLE Vl: Key Indtceton....... ............ , -..

ExchOnge wa Interest Pace Potliy...........................................

eNd MoneStzatan................

..................................... .................. Projected..........................

1991 1992 1993 1994 1995 1996

GOP(wp) Growth Rate 4.81 4.91 5.82 6.01 6.3S 6.ZXInvest. Growth Rats 5.31 4.2X 9.41 5.43 12.01 12.61Private 4.1X 7.81 8.62 10.61 12.41 13.91Pubtic Investment 10.21 -7.31 12.31 -9.1X 10.2S 6.91

GOP per capita Growth Rate 1.1X 1.2X 2.11 2.21 2.7X 2.71Consumpcian per coplu growth rate 4.4X 1.0X 3.31 1.3X 1.81 0.8X

Grosa Investment/COP 30.71 33.0X 34.9X 38.82 39.8S 43.4aOomestic savings/COP 23.1X 27.81 28.41 34.11 34.31 37.01National S5vings/cOP 22.51 26.31 27.0S 32.31 33.11 35.81

Private Investm nt/GOP 23.51 26.11 27.4X 31.21 32.61 36.01Consumption/GDP 60.71 55.11 55.71 51.01 51.11 46.31Prfvate Savings/GOP 27.7X 25.63 23.81 30.61 30.4X 32.81Private Reource Baltae*/GOP 4.21 -0.61 -3.61 -0.61 -2.2% -3.21

Pubtic tnvestment/GOP 7.21 6.91 7.51 7.01 7.21 7.41Pubtle Savings/GOP -5.21 0.91 3.2t 1.81 2.61 3.0X

Gcvernment Revenue/COP 19.8X 26.53 27.01 24.2X 24.11 26.11Govenernt Expenditure 32.31 32.51 31.31 29.41 28.71 30.61

Fiscat OeffcVt/GDP 12.5 6.0X 4.31 5.2Z 4.6o 4.46Fiscal Deicit/GOP trtnt Grants) 11.01 3.71 1.31 4.71 3.01 3.91

TotaL Ffinacing 11.01 3.71 1.31 4.7T 3.01 3.91

MLT Extemnal Financing 5.72 3.9' 4.61 3.71 3.31 3.81

ST ExternaL Financing 0.81 0.4X 0 .S 0.41 0.31 0.51

Domestic tfnancing-financiat ysctm 5.91 2.8t 5.11 3.91 5.31 6.1X

Monetary Authority 4.91 2.4X 4.11 3.71 4.61 5.41

Cemerciat Banks 1.01 0.41 1.01 0.21 0.72 0.71Oemstfic *inacing-prvatce sector 3.11 3.11 3.11 3.1X 3.11 3.11Residual 2.31 2.61 4.9X 5.21 7.82 9.3%Adjustmen'. to financfng -6.71 -9.11 -16.8S -11.51 -16.31 -18.91

Rest exchange rate fndex n1987r1002 89.93 79.97 77.41 68..1 69.40 66.80Real Exchange Rate Depreciation -4.41 -I1.11 -3.2X -11.61 1.bX -3.7?

Nominel exchange rate CtL/U5 ) 1.215 1.492 1.668 1.956 1.941 2.021Domestic Inftacion 9.51 8.51 6.31 6.01 5.01 5.01

Noaminat (Deposft) Interest Rate 14.71 13.11 10.41 8.91 6.51 4.7X

Reat Oeposit Interest Rate 4.81 4.3X 3.61 2.71 1.41 -0.31Loan Rate 21.71 19.91 16.81 15.2X 12.51 10.51

Resl Loan Rate 11.11 10.5X 9.71 8.61 7.11 5.32

SCock .a* MI/GOP 17.7X 17.3X 16.81 16.1X 15.21 14.0XStock of auwsl-morteyC/OP 11.4X 11.01 10.61 10.11 9.51 8.81Stock of credft to prfvate sectoe/GDP 21.11 21.81 22.71 24.11 25.61 27.41

-36-

1991 1992 1993 1994 1995 1996

Export Growth Rate -4.31 -4.1X 2.0Z 0.4% 7.6X 5.61Exparras/P . 21.21 22.3X 22.81 24.21 24.01 24.5X

lRport Growth Rate 5.61 -11.2X 9.2 -9.6X 12.9X 6.81eportas/GDP 2Z.8X 27.5X 29.31 23.31 29.6X 30.91

Curr. Ace. Ocf. CUSS. lncl. grants) 636.6 364.1 423.s 438.0 486.8 714.8Curr. Ace. Oot. Cln USS, cxcl. grants) 769.6 567.1 693. 47r.o 436.8 764.8Curr. Ace. Dcf./GDP (out. grants) 8.21 6.61 7.91 5.71 6.81 7.61Curr. Ace. D*t./GDP (tntl. grans) 6.81 4.21 4.91 5.2X 5.21 7.11

Net l'tl Reseves Stk (USS.) -554.1 .614.0 -769.6 -889.2 -1010.6 -1131.8(in months fwports) -2.47 -3.10 *3.61 -4.52 -4.36 *4.37

Change fn I1t1 Reserves Stk -336.0 -59.9 -155.6 -119.6 -121.4 -121.2

Total External Debt Ratfo 63.9X 72.51 76.11 82.91 76.91 76.31Piubtl Debt Ratio 85.9X 97.4X 106.6X 117.0X 116.3X 120.6X

Memo:

Residual PS8R (M) 0.0 0.0 0.0 0.0 0.0 0.0Externat Finamcing Cap CUSS.) 30.0 (SO.1) CSO.4) CS1.2) (M2.6) 30.0

- 37.-

interest rates, adopted an appropriate exchange rate policy, and generally managed exenal

finance have begun to remove structural constaints and to foster an eninm ent which Is more

conducive to efficient resource use.

4.13 Ihe simulations discussed in paras. 4.24.12 suggest that exchange rate, interest rate and

fiscal policy have an important role to play in managing future macroeconomic imbalances in

Kenya. A 5 percent devaluation of the real exchange rate appears to reduce the current deficit

by about one percent of GDP. However, it also appears to have a negative impact on the fiscal

deficit Likewise, in a constrained credit envivonment, every one percentage point (of GDP)

increase in domestic borrowing to finance the iscal deficit appears to increase the real domestic

loan rate by around 0.5 percentage points. However, the required increase in the real domestic

interest rate falls as domestic inflation rises.

4.14 In summary, the simulations suggest the need for joint exchange rate and interest rate

flexibility in managing the macroeconomic imbalances in Kenya. More important perhaps,

aggressive exchange rate action is necessary if the economy is o reduce its dependence on

foreign savings. On the fiscal front, greater discipline is warranted since it would reduce the

public sector borrowing requirement, lower the equilibrium real interest rate and accommodate

a higher level of investment in the private secmr.

V. Limitations and Future Extensions

5.1 The model is only as useful as the accuracy of the response functions. The coefficients

used in the simulations reported in Chapter IV are based on our econometric analysis using

Kenyan data (import elasticities, the demand for financial assets), the econometric studies of other

-38 -

researchers on Kenya and comparable economies, and judgment based on casual empiricism

(export elasticities, private investment elasticities). But the most sophisticated quantiative

techniques are still guty of projecdng the future on the basis of past behavior. nhis approach

is particularly uncomfortable because current adjustment policies in Kenya are changing,.however

slowly, the macroeconomic Incentives and the scope for responding to them. Estimates of import

eldasticities deal with these changing circumstances explicitly. As observation points become

available, this would need to be done especially for exports and private investment.

S.2 The interest rate and exchange rate adjustments required for solving the model are

cumulative. That is, the adjustment required in any given year is based on the interest rate and

exchange rate level in the previous year and not to some fixed point in the past. In contrast, the

gaps are dealt with annually, not cumulatively. As a result, the adjustments in the policy

variables could be large fxom year to year if the gaps exhibit large annual fluctuations. For

example, to finance a large public sector borrowing requirement in a given year, the model may

produce a large increase in the real domestic loan interest rate. Because interest rate adjustments

are cumulative, the real interest rate may actually fall or even become negadve in the next year

If the public sector borrowing requirement is small. The economic logic of this solution is that

the previous year's high real interest rate must fall if private sector investment is to absorb the

additional domestic credit which is no longer required to finance the public sector. Similar

results obtain for the exchange rate when there are large fluctuations in the external gap. Such

drastic adjustments in policy variables from year to year are not likely to occur in practice. Still,

this is not a problem for the model to deal with as much as a signal about how to frame the

policy questions and interpret the policy solutions. When the gaps fluctuate widely from year to

year, it may be appropriate to ask the model to solve for the average annual gap over the period.

Another approach would be to treat the solution for the largest annual gap as an indication of the

upper limit of the policy adjustnents needed during the projection period.

-39 -

5.3 Ihe model treats the residual public sector borrowing requirement and the external

fundlg gap as mutually exclusive and independen. This simplifies the exposition of the model.

However, the residual public sector borrowing requirement may be a component of the external

financing requirement. Under this scenario, closure of the exteral gap would amount to

elimination of the public sector borrowing requirement. Reality is somewhere between the two

extremes, one in which the extenal gap includes the residual public sector borrowing requirement

and the other in which they are completely independent. To capture this reality, a simple

specification would be required to indicate the relationship between the public sector borrowing

requirement and the external financing gap. The model could then solve for the interest rate

and/or the exchange rate which closes the net gap.

5.4 Recent economic work on Kenya recognizes the need for data on the consolidated public

sector but this information is only just being gathered and coUated by the Central Government

In time, this data should be used to extend the coverage of the public sector accounts in the

model. Parastatal imports also need to be disaggregated from private imports and a more reliable

series on government imports obtained. As progress is made in public sector investment

programming, the recurrent expenditure implications of capital outlays should also be captured

explicitly.

5.5 With relatively few modifications, the model could endogenize economic growth (at

factor cost). At this stage however, it may be more rewarding to concentrate on refining the

response functions and to widening the coverage of the public sector finances. Econometric

work should also be done on the income and price elasticities of exports, the interest elasticity

of private investment and the behavior of private consumpdon.

-40-

ANNEX I

DESCRIPTION OF MODEL

Overview

1. The model comprises six data input worksheets, a debt module for pipeline and new externaldebt, and output tables. There is also one central worksheet wh contains key behavioralassumptions and macroeconomic targets.

7782. The data input worksheets are similar in fornat, units of account and coverage to standardtables produced by the Government. These input worksheets are:

(a) Original Data: CB (GOK)(b) Original Data: BOP (GOK)(c) Original Data: Fiscal Data (FY) (GOK & IM)(d) Original Data: DRS (World Bank)(e) Original Data: National Accounts (GOK)(t) Original Data: Trade (GOK)