Embed Size (px)

Citation preview

FOXCONN TECHNOLOGY CO., LTD. AND COSOLIDATED SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS AND

REVIEW REPORT OF INDEPENDENT

ACCOUNTANTS

FOR THE SIX-MONTH PERIOD ENDED

JUNE 30, 2005

This English financial statements, expressed in thousands of New Taiwan dollars, were translated from the financial statements originally prepared in Chinese language.

----------------------------------------------------------------------------------------------------------------------------------------------------

The accompanying consolidated financial statements are not intended to present the financial position and results of operations and cash flows in accordance with accounting principles and practices generally accepted in countries and jurisdictions other than the Republic of China. The standards, procedures and practices utilized in the Republic of China to audit such consolidated financial statements may differ from those generally accepted in countries and jurisdictions other than the Republic of China. Accordingly, the accompanying consolidated financial statements and report of the independent accountants are not intended for use by those who are not informed about the accounting principles or auditing standards generally accepted in the Republic of China, and their applications in practice.

~1~

REVIEW REPORT OF INDEPENDENT ACCOUNTANTS

To The Board of Directors and Shareholders of Foxconn Technology Co., LTD. :

We have reviewed the accompanying consolidated balance sheets of Foxconn Technology Co., LTD. (the “Company”) and its subsidiaries as of June 30, 2005, and the related consolidated statements of income, of shareholders’ equity and of cash flows for the six-month period then ended. These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our review.

We conducted our review in accordance with the Statement of Auditing Standard No.36 “Review of Financial Statements” in the Republic of China on the consolidated financial statements of the company and its subsidiaries as of and for the six-month period ended June 30, 2005. A review consists principally of inquiries of company personnel comparing and analytical procedures applied to financial data. It is substantially less in scope than an audit conducted accordance with generally accepted auditing standards in the Republic of China, the objective of which is the expression of an opinion regarding the consolidated financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the consolidated financial statements in order for them to be in conformity with the “Rules Governing the Preparation of Financial Statements of Securities Issuers” and generally accepted accounting principles in the Republic of China.

August 29, 2005 Taipei, Taiwan Republic of China

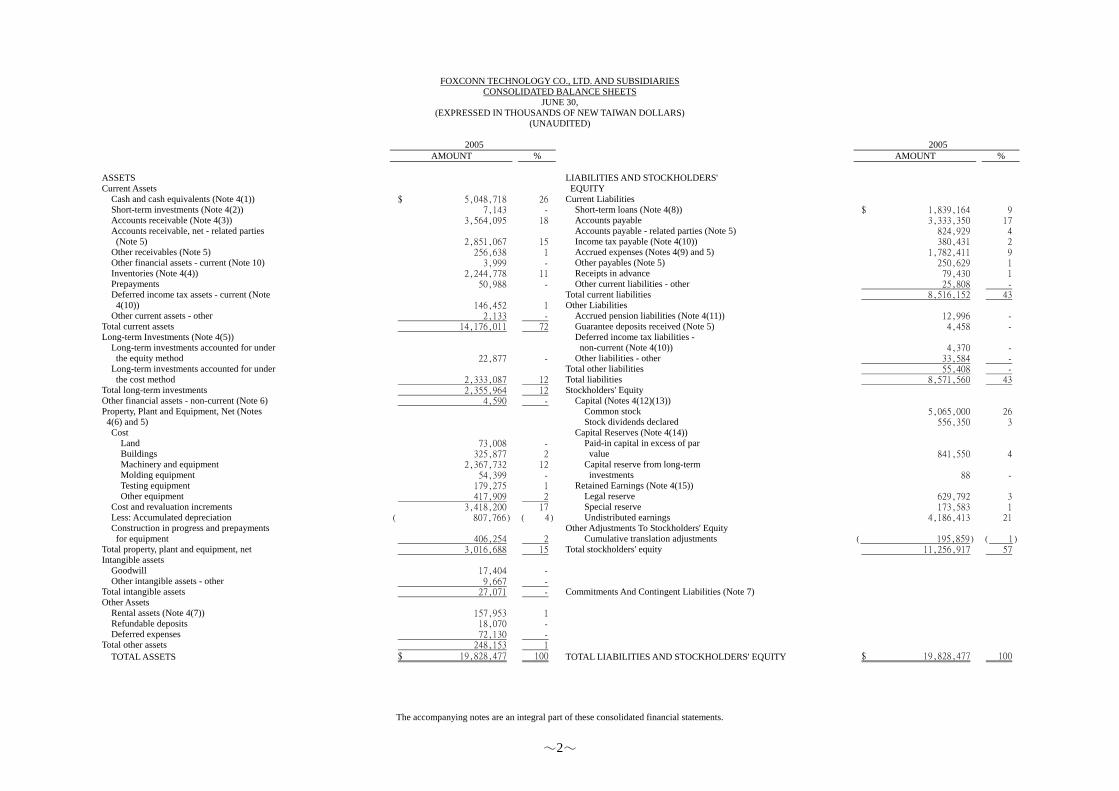

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS

JUNE 30, (EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS)

(UNAUDITED)

2005 2005 AMOUNT % AMOUNT %

The accompanying notes are an integral part of these consolidated financial statements.

2

ASSETS LIABILITIES AND STOCKHOLDERS' Current Assets EQUITY Cash and cash equivalents (Note 4(1)) $ 5,048,718 26 Current Liabilities Short-term investments (Note 4(2)) 7,143 - Short-term loans (Note 4(8)) $ 1,839,164 9 Accounts receivable (Note 4(3)) 3,564,095 18 Accounts payable 3,333,350 17 Accounts receivable, net - related parties Accounts payable - related parties (Note 5) 824,929 4 (Note 5) 2,851,067 15 Income tax payable (Note 4(10)) 380,431 2 Other receivables (Note 5) 256,638 1 Accrued expenses (Notes 4(9) and 5) 1,782,411 9 Other financial assets - current (Note 10) 3,999 - Other payables (Note 5) 250,629 1 Inventories (Note 4(4)) 2,244,778 11 Receipts in advance 79,430 1 Prepayments 50,988 - Other current liabilities - other 25,808 - Deferred income tax assets - current (Note Total current liabilities 8,516,152 43 4(10)) 146,452 1 Other Liabilities Other current assets - other 2,133 - Accrued pension liabilities (Note 4(11)) 12,996 - Total current assets 14,176,011 72 Guarantee deposits received (Note 5) 4,458 - Long-term Investments (Note 4(5)) Deferred income tax liabilities - Long-term investments accounted for under non-current (Note 4(10)) 4,370 - the equity method 22,877 - Other liabilities - other 33,584 - Long-term investments accounted for under Total other liabilities 55,408 - the cost method 2,333,087 12 Total liabilities 8,571,560 43 Total long-term investments 2,355,964 12 Stockholders' Equity Other financial assets - non-current (Note 6) 4,590 - Capital (Notes 4(12)(13)) Property, Plant and Equipment, Net (Notes Common stock 5,065,000 26 4(6) and 5) Stock dividends declared 556,350 3 Cost Capital Reserves (Note 4(14)) Land 73,008 - Paid-in capital in excess of par Buildings 325,877 2 value 841,550 4 Machinery and equipment 2,367,732 12 Capital reserve from long-term Molding equipment 54,399 - investments 88 - Testing equipment 179,275 1 Retained Earnings (Note 4(15)) Other equipment 417,909 2 Legal reserve 629,792 3 Cost and revaluation increments 3,418,200 17 Special reserve 173,583 1 Less: Accumulated depreciation ( 807,766) ( 4) Undistributed earnings 4,186,413 21 Construction in progress and prepayments Other Adjustments To Stockholders' Equity for equipment 406,254 2 Cumulative translation adjustments ( 195,859) ( 1) Total property, plant and equipment, net 3,016,688 15 Total stockholders' equity 11,256,917 57 Intangible assets Goodwill 17,404 - Other intangible assets - other 9,667 - Total intangible assets 27,071 - Commitments And Contingent Liabilities (Note 7) Other Assets Rental assets (Note 4(7)) 157,953 1 Refundable deposits 18,070 - Deferred expenses 72,130 - Total other assets 248,153 1

TOTAL ASSETS $ 19,828,477 100 TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY $ 19,828,477 100

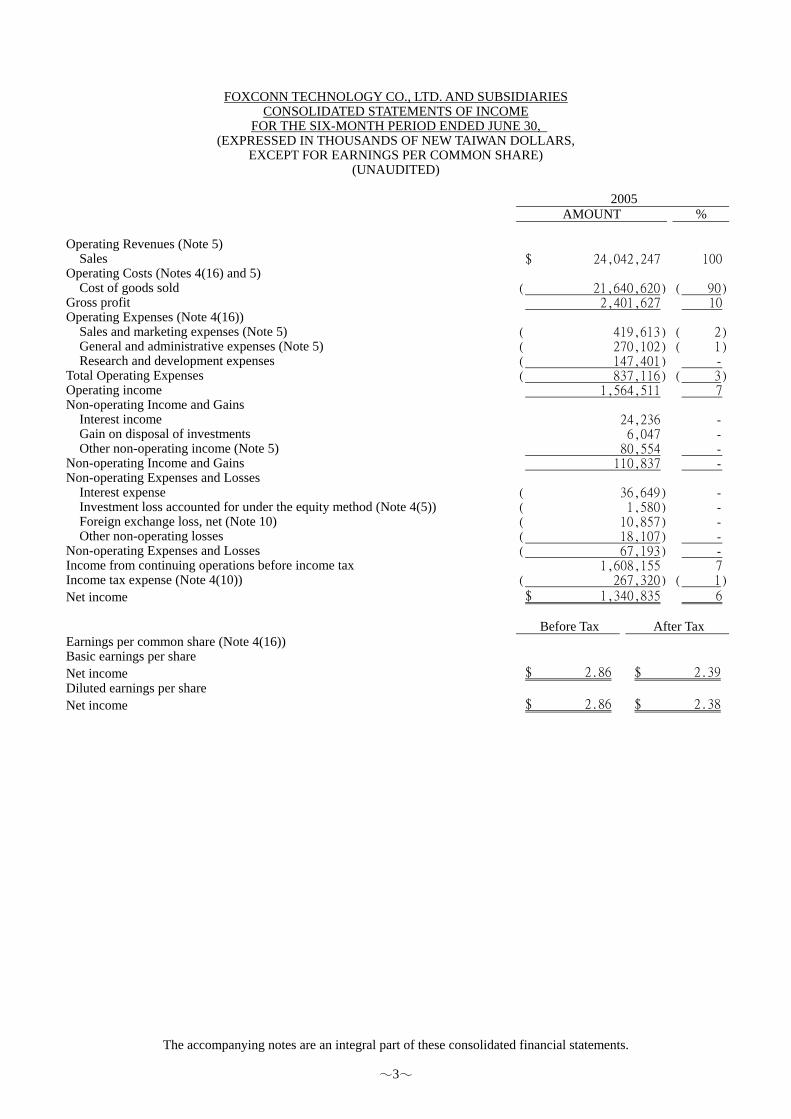

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME FOR THE SIX-MONTH PERIOD ENDED JUNE 30,

(EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS, EXCEPT FOR EARNINGS PER COMMON SHARE)

(UNAUDITED)

2005 AMOUNT %

The accompanying notes are an integral part of these consolidated financial statements.

3

Operating Revenues (Note 5) Sales $ 24,042,247 100Operating Costs (Notes 4(16) and 5) Cost of goods sold ( 21,640,620) ( 90)Gross profit 2,401,627 10Operating Expenses (Note 4(16)) Sales and marketing expenses (Note 5) ( 419,613) ( 2) General and administrative expenses (Note 5) ( 270,102) ( 1) Research and development expenses ( 147,401) -Total Operating Expenses ( 837,116) ( 3)Operating income 1,564,511 7Non-operating Income and Gains Interest income 24,236 - Gain on disposal of investments 6,047 - Other non-operating income (Note 5) 80,554 -Non-operating Income and Gains 110,837 -Non-operating Expenses and Losses Interest expense ( 36,649) - Investment loss accounted for under the equity method (Note 4(5)) ( 1,580) - Foreign exchange loss, net (Note 10) ( 10,857) - Other non-operating losses ( 18,107) -Non-operating Expenses and Losses ( 67,193) -Income from continuing operations before income tax 1,608,155 7Income tax expense (Note 4(10)) ( 267,320) ( 1)

Net income $ 1,340,835 6 Before Tax After Tax Earnings per common share (Note 4(16)) Basic earnings per share

Net income $ 2.86 $ 2.39Diluted earnings per share

Net income $ 2.86 $ 2.38

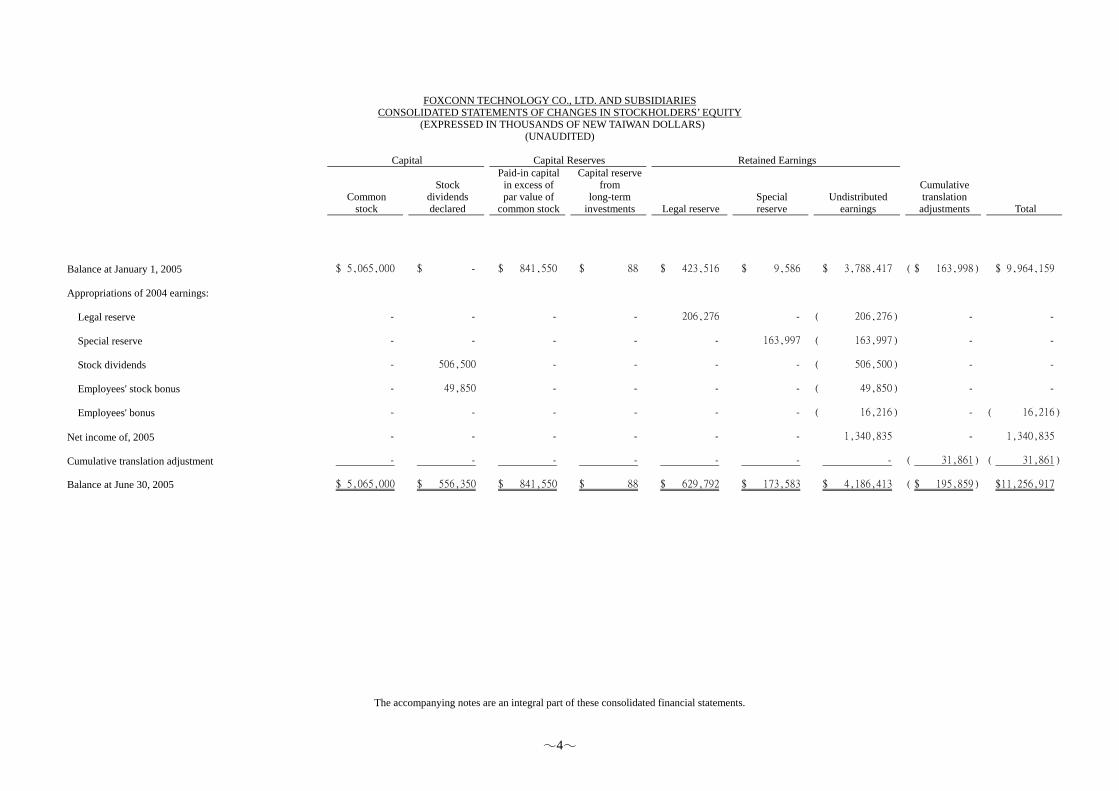

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS) (UNAUDITED)

Capital Capital Reserves Retained Earnings

Common stock

Stock dividends declared

Paid-in capital in excess of par value of

common stock

Capital reserve from

long-term investments

Legal reserveSpecial reserve

Undistributed earnings

Cumulative translation

adjustments

Total

The accompanying notes are an integral part of these consolidated financial statements.

4

Balance at January 1, 2005 $ 5,065,000 $ - $ 841,550 $ 88 $ 423,516 $ 9,586 $ 3,788,417 ( $ 163,998) $ 9,964,159

Appropriations of 2004 earnings:

Legal reserve - - - - 206,276 - ( 206,276) - -

Special reserve - - - - - 163,997 ( 163,997) - -

Stock dividends - 506,500 - - - - ( 506,500) - -

Employees' stock bonus - 49,850 - - - - ( 49,850) - -

Employees' bonus - - - - - - ( 16,216) - ( 16,216)

Net income of, 2005 - - - - - - 1,340,835 - 1,340,835

Cumulative translation adjustment - - - - - - - ( 31,861) ( 31,861)

Balance at June 30, 2005 $ 5,065,000 $ 556,350 $ 841,550 $ 88 $ 629,792 $ 173,583 $ 4,186,413 ( $ 195,859) $ 11,256,917

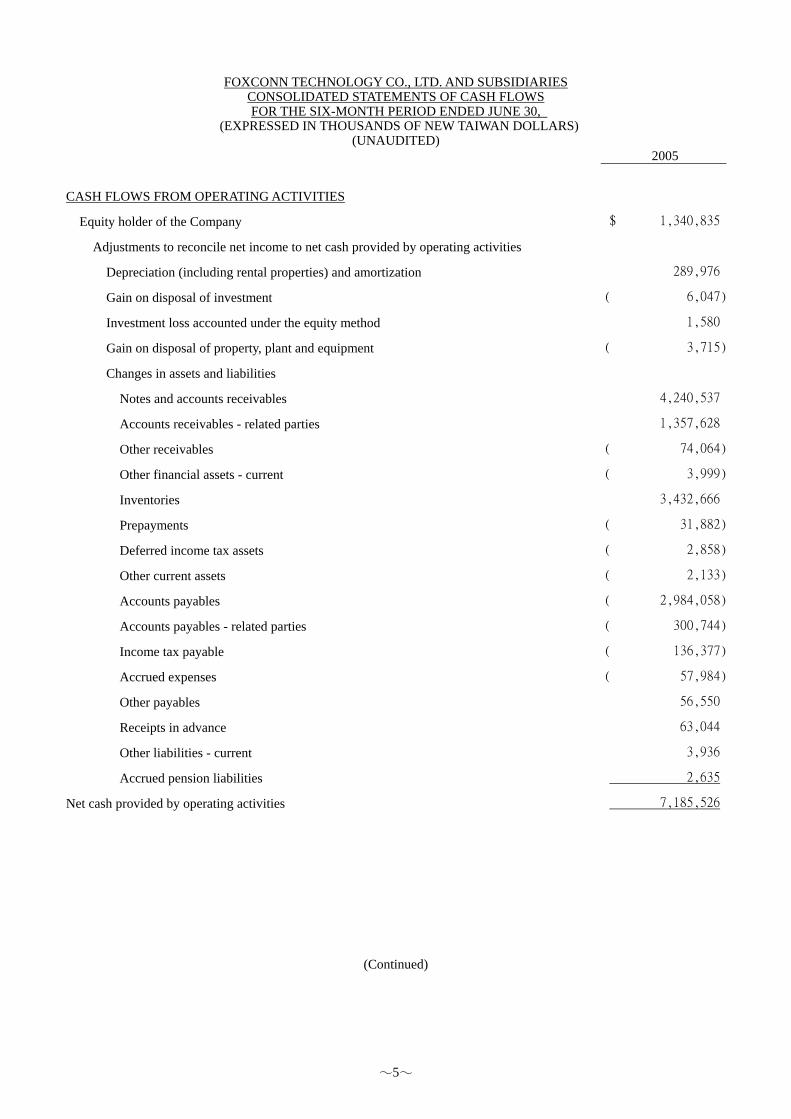

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS FOR THE SIX-MONTH PERIOD ENDED JUNE 30,

(EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS) (UNAUDITED)

2005

5

CASH FLOWS FROM OPERATING ACTIVITIES

Equity holder of the Company $ 1,340,835

Adjustments to reconcile net income to net cash provided by operating activities

Depreciation (including rental properties) and amortization 289,976

Gain on disposal of investment ( 6,047)

Investment loss accounted under the equity method 1,580

Gain on disposal of property, plant and equipment ( 3,715)

Changes in assets and liabilities

Notes and accounts receivables 4,240,537

Accounts receivables - related parties 1,357,628

Other receivables ( 74,064)

Other financial assets - current ( 3,999)

Inventories 3,432,666

Prepayments ( 31,882)

Deferred income tax assets ( 2,858)

Other current assets ( 2,133)

Accounts payables ( 2,984,058)

Accounts payables - related parties ( 300,744)

Income tax payable ( 136,377)

Accrued expenses ( 57,984)

Other payables 56,550

Receipts in advance 63,044

Other liabilities - current 3,936

Accrued pension liabilities 2,635

Net cash provided by operating activities 7,185,526

(Continued)

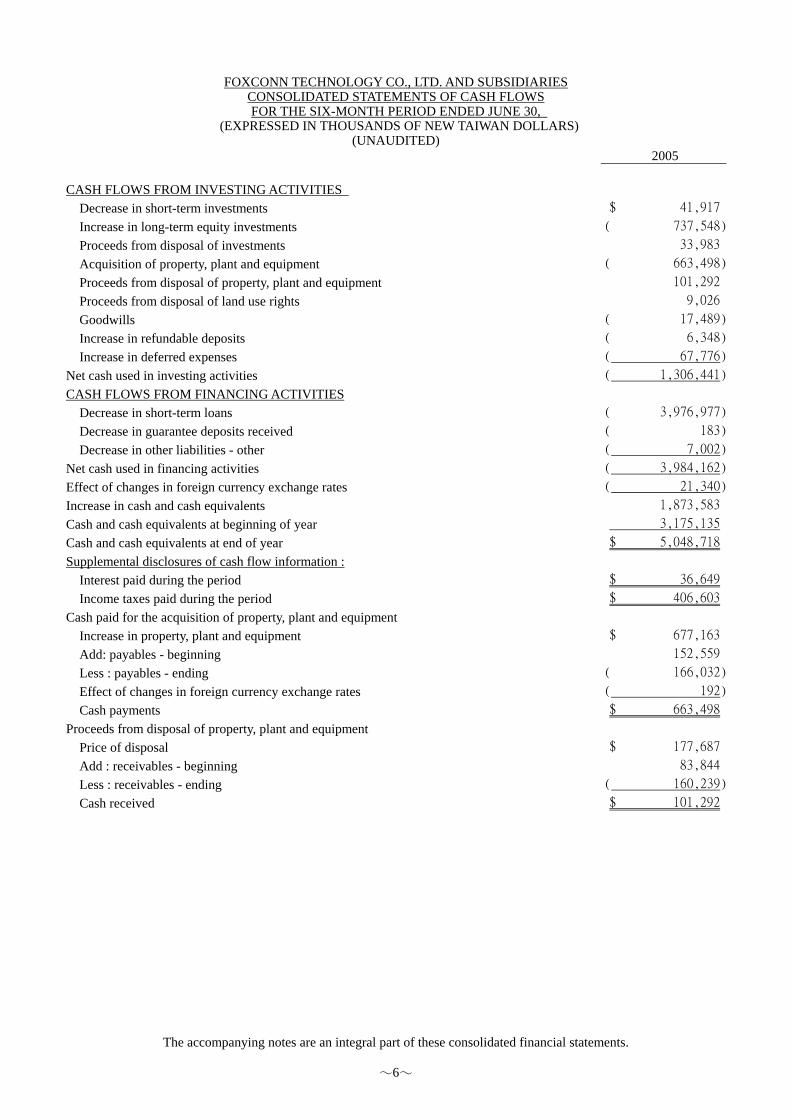

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS FOR THE SIX-MONTH PERIOD ENDED JUNE 30,

(EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS) (UNAUDITED)

2005

The accompanying notes are an integral part of these consolidated financial statements.

6

CASH FLOWS FROM INVESTING ACTIVITIES

Decrease in short-term investments $ 41,917

Increase in long-term equity investments ( 737,548)

Proceeds from disposal of investments 33,983

Acquisition of property, plant and equipment ( 663,498)

Proceeds from disposal of property, plant and equipment 101,292

Proceeds from disposal of land use rights 9,026

Goodwills ( 17,489)

Increase in refundable deposits ( 6,348)

Increase in deferred expenses ( 67,776)

Net cash used in investing activities ( 1,306,441)

CASH FLOWS FROM FINANCING ACTIVITIES

Decrease in short-term loans ( 3,976,977)

Decrease in guarantee deposits received ( 183)

Decrease in other liabilities - other ( 7,002)

Net cash used in financing activities ( 3,984,162)

Effect of changes in foreign currency exchange rates ( 21,340)

Increase in cash and cash equivalents 1,873,583

Cash and cash equivalents at beginning of year 3,175,135

Cash and cash equivalents at end of year $ 5,048,718

Supplemental disclosures of cash flow information :

Interest paid during the period $ 36,649

Income taxes paid during the period $ 406,603

Cash paid for the acquisition of property, plant and equipment

Increase in property, plant and equipment $ 677,163

Add: payables - beginning 152,559

Less : payables - ending ( 166,032)

Effect of changes in foreign currency exchange rates ( 192)

Cash payments $ 663,498

Proceeds from disposal of property, plant and equipment

Price of disposal $ 177,687

Add : receivables - beginning 83,844

Less : receivables - ending ( 160,239)

Cash received $ 101,292

7

FOXCONN TECHNOLOGY CO., LTD. AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2005 (EXPRESSED IN THOUSANDS OF NEW TAIWAN DOLLARS,

EXCEPT AS OTHERWISE INDICATED) (UNAUDITED)

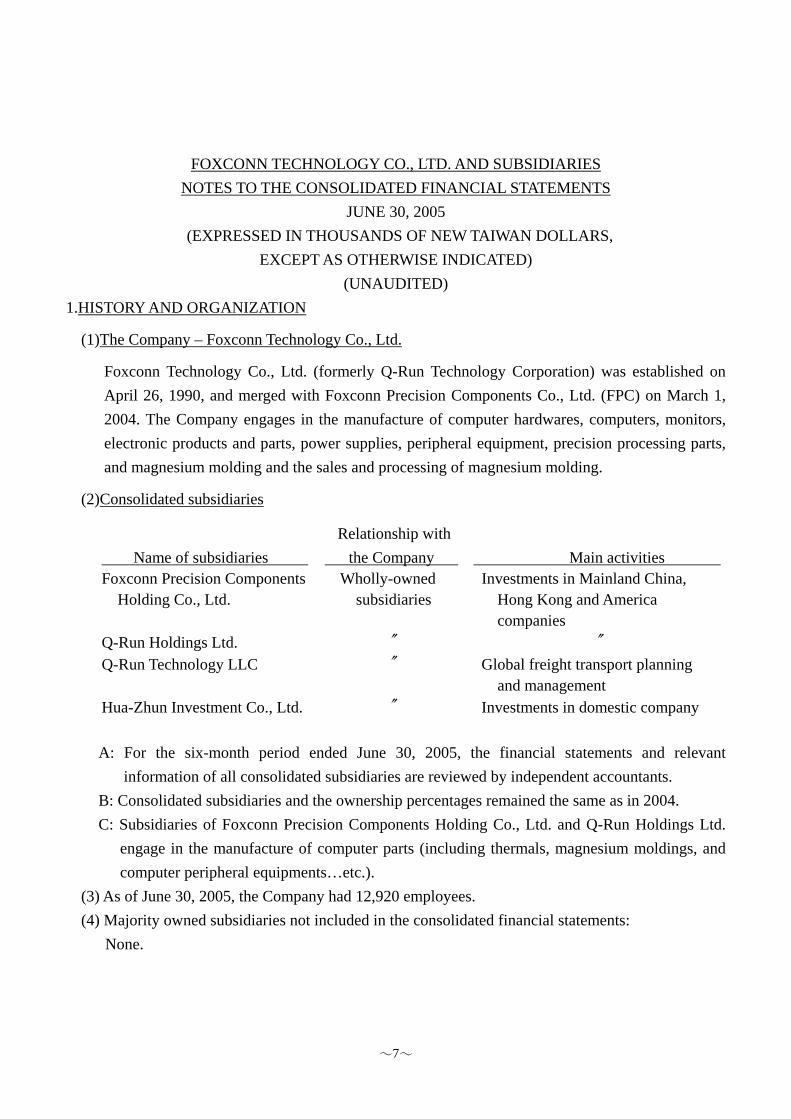

1.HISTORY AND ORGANIZATION

(1)The Company – Foxconn Technology Co., Ltd.

Foxconn Technology Co., Ltd. (formerly Q-Run Technology Corporation) was established on April 26, 1990, and merged with Foxconn Precision Components Co., Ltd. (FPC) on March 1, 2004. The Company engages in the manufacture of computer hardwares, computers, monitors, electronic products and parts, power supplies, peripheral equipment, precision processing parts, and magnesium molding and the sales and processing of magnesium molding.

(2)Consolidated subsidiaries

Relationship with Name of subsidiaries the Company Main activities

Foxconn Precision Components Wholly-owned Investments in Mainland China, Holding Co., Ltd. subsidiaries Hong Kong and America companies Q-Run Holdings Ltd. Q-Run Technology LLC Global freight transport planning and management Hua-Zhun Investment Co., Ltd. Investments in domestic company

A: For the six-month period ended June 30, 2005, the financial statements and relevant

information of all consolidated subsidiaries are reviewed by independent accountants. B: Consolidated subsidiaries and the ownership percentages remained the same as in 2004. C: Subsidiaries of Foxconn Precision Components Holding Co., Ltd. and Q-Run Holdings Ltd.

engage in the manufacture of computer parts (including thermals, magnesium moldings, and computer peripheral equipments…etc.).

(3) As of June 30, 2005, the Company had 12,920 employees. (4) Majority owned subsidiaries not included in the consolidated financial statements:

None.

8

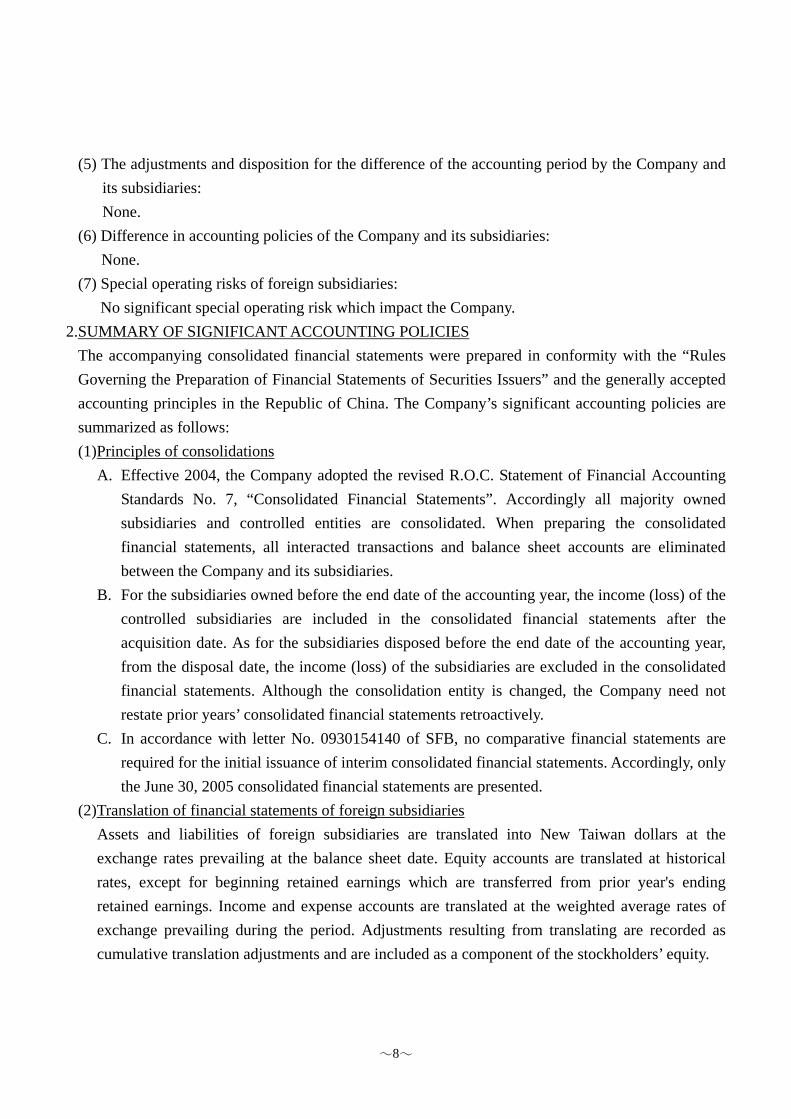

(5) The adjustments and disposition for the difference of the accounting period by the Company and its subsidiaries: None.

(6) Difference in accounting policies of the Company and its subsidiaries: None.

(7) Special operating risks of foreign subsidiaries: No significant special operating risk which impact the Company.

2.SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The accompanying consolidated financial statements were prepared in conformity with the “Rules Governing the Preparation of Financial Statements of Securities Issuers” and the generally accepted accounting principles in the Republic of China. The Company’s significant accounting policies are summarized as follows: (1)Principles of consolidations

A. Effective 2004, the Company adopted the revised R.O.C. Statement of Financial Accounting Standards No. 7, “Consolidated Financial Statements”. Accordingly all majority owned subsidiaries and controlled entities are consolidated. When preparing the consolidated financial statements, all interacted transactions and balance sheet accounts are eliminated between the Company and its subsidiaries.

B. For the subsidiaries owned before the end date of the accounting year, the income (loss) of the controlled subsidiaries are included in the consolidated financial statements after the acquisition date. As for the subsidiaries disposed before the end date of the accounting year, from the disposal date, the income (loss) of the subsidiaries are excluded in the consolidated financial statements. Although the consolidation entity is changed, the Company need not restate prior years’ consolidated financial statements retroactively.

C. In accordance with letter No. 0930154140 of SFB, no comparative financial statements are required for the initial issuance of interim consolidated financial statements. Accordingly, only the June 30, 2005 consolidated financial statements are presented.

(2)Translation of financial statements of foreign subsidiaries Assets and liabilities of foreign subsidiaries are translated into New Taiwan dollars at the exchange rates prevailing at the balance sheet date. Equity accounts are translated at historical rates, except for beginning retained earnings which are transferred from prior year's ending retained earnings. Income and expense accounts are translated at the weighted average rates of exchange prevailing during the period. Adjustments resulting from translating are recorded as cumulative translation adjustments and are included as a component of the stockholders’ equity.

9

(3) Criteria for classifying assets and liabilities A. Assets that meet one of the following criteria are classified as current assets; otherwise they

are classified as non-current assets: (1) Assets consisting of unrestricted cash or cash equivalents. (2) Assets held for trading purpose, or held for a short-term period and expected to be

realized within 12 months from the balance sheet date. (3) Assets expected to be realized available for sale or consume in normal operate process

of enterprises operate cycle. B. Liabilities that meet one of the following criteria are classified as current liability; otherwise

they are classified as non-current liabilities: (1) Liabilities to be paid within 12 months from the balance sheet date. (2) Liabilities incurred in operating activities and expected to be paid during the normal

course of business. (4)Use of estimates

The preparation of consolidated financial statements in conformity with R.O.C. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities as at the date of the financial statements and the amounts of revenues and expenses reported during the period. Actual results could differ from those assumptions and estimates.

(5)Translation of foreign currency transactions The Company maintains its accounting records in New Taiwan dollars. Transactions arising in foreign currencies are measured at the exchange rates prevailing at the transaction dates. Receivables, other monetary assets and liabilities denominated in foreign currencies are translated at the exchange rate prevailing at the balance sheet date. Foreign exchange gains or losses are included in current year’s net income.

(6)Cash equivalents Cash equivalents represent short-term, highly liquid investments that are readily convertible to known amounts of cash and with maturity periods of less than three months that do not present significant risk of change in value because of change in interest rates. The Company’s consolidated statement of cash flow was prepared on the base of cash and cash equivalents.

(7)Derivative financial instruments Forward exchange contracts entered into for hedging purposes are recorded using the spot rate on the contract date. Gains or losses determined by the difference between the spot rate on the contract date and the specified rate on the forward exchange contract are amortized over the period of the contract. Discounts or premiums on forward contracts are amortized over the periods

10

of the contract. The receivables and payables on forward contracts are adjusted using the exchange rate prevailing at the balance sheet date and any losses are recognized in current operation.

(8)Short-term investments Short-term investments are stated at the lower of cost or market value. Cost is calculated by the weighted-average method. Exess of aggregate cost over the market value is included in current operation. Subsequent recoveries in market value are recovered to the extent of original cost of the investment. The market values of listed securities are determined based on the average closing prices of the last month of the period. The market value of open-end fund is the net asset value at the balance sheet date.

(9)Allowance for doubtful accounts Allowance for doubtful accounts is provided based on past experience and the evaluation of the collectibility of accounts and notes receivables, and other receivables taking into account the aging analysis of receivables.

(10)Inventories Inventories are stated at the lower of cost or market value. Inventory cost is determined using the weighted average cost method. Allowance is provided for decline in market value and obsolescence. The aggregate value method is used to determine the lower of cost or market value. The market value for raw materials is determined based on current replacement cost while work in process and finished goods inventories are determined based on net realizable values. Provision for obsolescence is based on the specific identification method.

(11)Long-term equity investments A. Long-term investments in which the Company owns less than 20% of the investee company's

voting rights and has no significant influence on the investee company’s opeprational decisions are accounted for at (a) cost, if the investee company is not listed or (b) the lower of cost or market value, if the investee company is listed. Valuation allowance for unrealized loss under the lower of cost or market value method is shown under stockholders’ equity. When it becomes evidently clear that there has been a permanent impairment in value and the chance of recovery is minimal, loss is recognized in the current year's net income.

B. Long-term investment in which the Company owns at least 20% of the investee company’s voting rights or has significant influence on are accounted for under the equity method. The excess of acquisition cost over the investee company’s net assets value is capitalized and amortized over 5~20 years using the straight-line method.

C. For investee company accounted for under the equity method, if the Company has significant influence but does not have control power over the investee company, the use of the equity method is discontinued if losses on investment reduce the balance of the investment to zero,

11

unless the Company has a commitment to provide financial support to the investee company or acts as guarantor for loans made to the investee company. If the Company has control power over the investee company, losses of the investee company should be fully recognized, unless other stockholders of the investee company have duty and able to provide additional capital to assume the loss. If the investee company profits subsequently, the profit should belong to the Company first until the loss which recognized by the Company is recovered.

D. The Company's proportionate share of the investee company's cumulative translation adjustment is recognized by the Company and included in the stockholders' equity account as "Cumulative Translation Adjustment."

(12)Property, plant and equipment A. Fixed assets are stated at cost. Significant renewals or betterments are capitalized.

Maintenance and repairs are charged to expense as incurred. B. Depreciation of major assets is provided on the straight-line method using estimated service

lives of the assets plus one year as salvage value. Depreciation of leasehold improvements is provided on the straight-line method, but using the shorter of estimated economical lives or leasehold period. Fully depreciation assets still in use are depreciated based on the residual values over the remaining useful lives. The estimated useful lives are 50 to 55 years for buildings and 2 to 10 years for other fixed assets.

C. Assets not for operational purpose are classified under other assets at the lower of the net realizable values or book values; and the depreciation expense is included in non-operating expense.

(13)Other intangible asstes A. Goodwill is the difference of investment cost over the equity in net assets of the investee

companies and is amortized over 5~20 years. B. Other intangible assets, land use rights, are stated at cost and amortized over 50 years , under

the straight-line method. (14)Deferred expenses

The costs of computer software, molding equipments, tooling equipments and pipelined installation charges are stated at cost and are amortized over their estimated economic lives between 1~3 years, under the straight-line basis.

(15)Retirement plan and pension cost A. The Company has a non-contributory and funded defined benefit retirement plan (the Plan)

covering all regular employees. In accordance with the Labor Standards Law of the R.O.C., the Company contributes monthly an amount equal to 2% of total monthly salaries and wages to an independent retirement trust fund, with the Central Trust of China, the trustee. The trust fund assets are not reflected in the Company’s consolidated financial statements.

12

B. The Company recognizes net periodic pension cost, which includes service cost, interest cost, expected return on plan assets, amortization of unrecognized transition obligation and prior service cost, and pension gains/losses, based on an actuarial valuation. The unrecognized net asset obligation at transition is amortized equally over 15 years.

C. The overseas subsidiaries have defined contribution pension plans in accordance with the local regulations.

D. In preparing interim financial statements, the minimum pension liability is adjusted by subsequent pension cost and funded amount.

(16)Income tax A. Income Tax expense is provided based on accounting income after adjusting for permanent

differences. The provision for income tax includes deferred income tax for the expected future tax consequences of events that have been included in different periods for financial or tax reporting purposes. Deferred income tax assets and liabilities are determined using enacted tax rates in effect for the year(s) in which the differences are expected to reverse. Valuation allowance for deferred income tax assets is recognized to the extent that it is more likely than not that the income tax benefit will not be realized.

B. Over or under provision of income tax from the previous years is recorded as adjustment to the current years' income tax expense.

C. According to the Taiwan imputation tax system, undistributed current earnings, of a company derived on or after January 1, 1998 are subject to an additional 10% corporate income tax if the earnings are not distributed in the following year. This 10% additional corporate income tax on undistributed earnings is recorded as income tax expense in the year when the stockholders approve a resolution to retain the earnings.

D. Income tax credits are provided for in accordance with R.O.C. SFAS No.12, " Income Tax Credit Accounting Principle". Income tax credits arising from the purchase of equipment or technology, expenditures for research and development, employee training and development and investment in qualified stocks are charged to deferred income tax assets and credited to income tax expense in the period the tax credits arise.

(17)Earnings per share A. Basic earnings per share is calculated by dividing net income by the weighted average

number of shares outstanding during the period. Diluted earnings per share is calculated by taking into account the potentially dilutive securities assumed to be converted to common stock at the beginning of the period and net income is adjusted by the amount associated with conversion.

B. The potentially dilutive securities of the Company consist of employee stock options. The

13

employee stock options are counted on diluted earnings per share by treasury stock method. (18)Revenue and expenses

Revenue is recognized when the earning process is completed and realized or realizable. Relevant costs and expenses are recorded as incurred accordance with the occurrence of revenue.

(19)Impairment loss Effective the fourth quarter of 2004, the Company adopted SFAS No. 35 ”Accounting for Assets Impairments.” When there exits an indication that the recoverable amount of the Company’s assets is lower than the carrying amount, an impairment loss is recognized. Recoverable amount is referred to the greater of the fair value less costs to sell or the value in use. Fair value less costs to sell is referred to the net disposal amount received of an asset under a fair transaction. Value in use is referred to the discounted value of estimate future cash flow for the useful lives of an asset. When the indication of prior years’ impairment no longer exists, the impairment loss recognized in prior year may be recovered. Recovery of impairment loss on goodwill is not allowed.

3.CHANGES IN ACCOUNTING PRINCIPLES Effective the fourth quarter of 2004, the Company adopted SFAS No. 35 ”Accounting for Assets Impairments” and recorded impairment loss of $22,463 for the year ended December 31, 2004. As a result of the adoption of the new accounting principle, total consolidated assets and total stockholders’ equity were decreased by $22,463 at June 30, 2005.

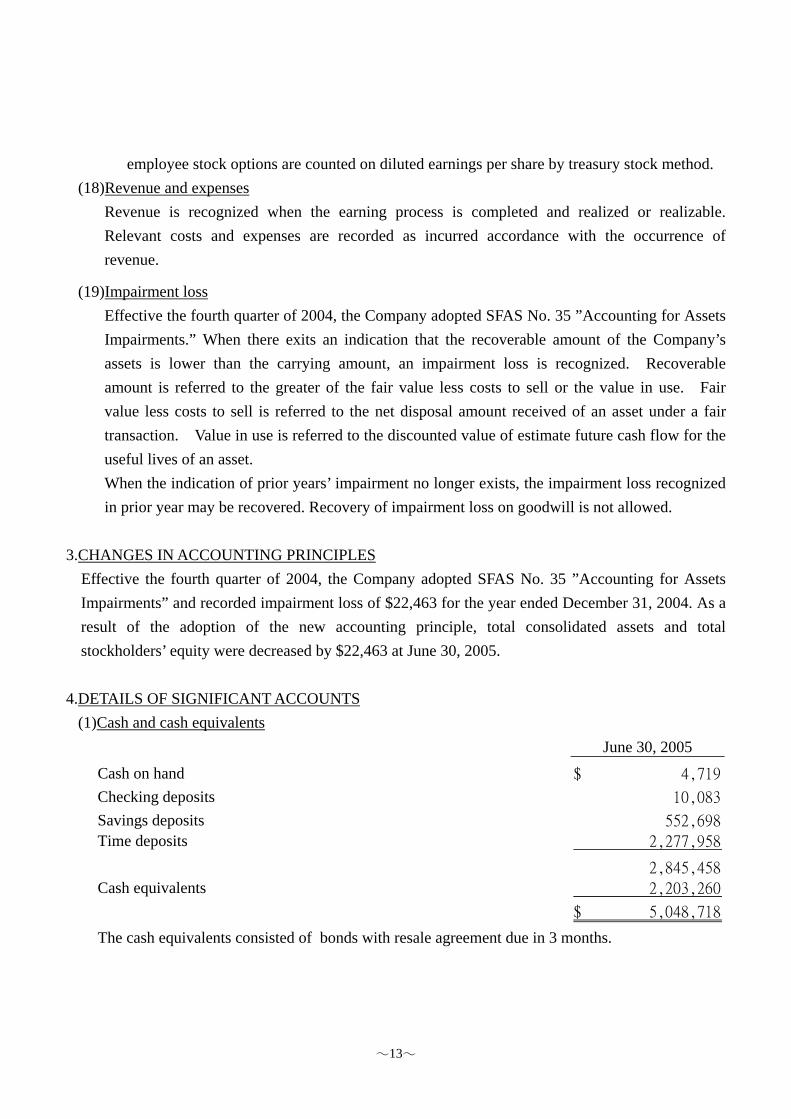

4.DETAILS OF SIGNIFICANT ACCOUNTS (1)Cash and cash equivalents

June 30, 2005

Cash on hand 4,719$

Checking deposits 10,083

Savings deposits 552,698

Time deposits 2,277,958

2,845,458

Cash equivalents 2,203,260

5,048,718$

The cash equivalents consisted of bonds with resale agreement due in 3 months.

14

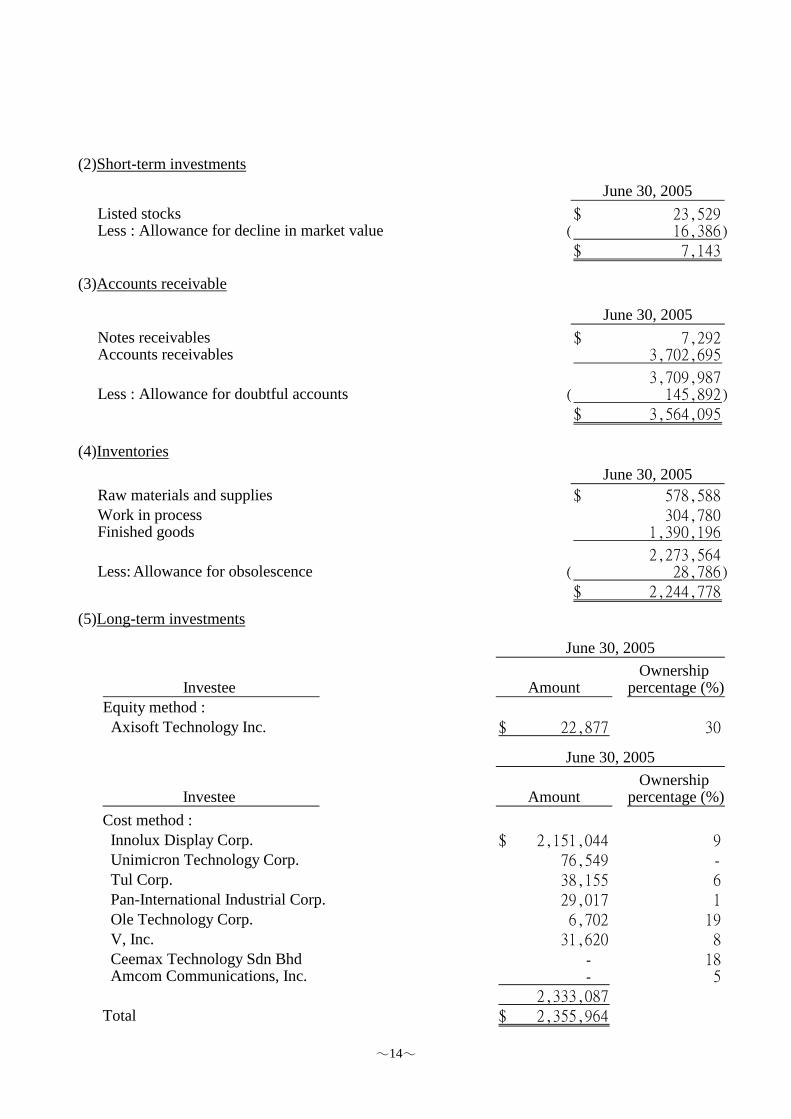

(2)Short-term investments

June 30, 2005Listed stocks 23,529$ Less : Allowance for decline in market value 16,386)(

7,143$ (3)Accounts receivable

June 30, 2005Notes receivables 7,292$ Accounts receivables 3,702,695

3,709,987 Less : Allowance for doubtful accounts 145,892)(

3,564,095$

(4)Inventories June 30, 2005

Raw materials and supplies 578,588$ Work in process 304,780 Finished goods 1,390,196

2,273,564 Less: Allowance for obsolescence 28,786)(

2,244,778$ (5)Long-term investments

Ownership Investee Amount percentage (%)

Equity method : Axisoft Technology Inc. 22,877$ 30

June 30, 2005

Ownership

Investee Amount percentage (%)

June 30, 2005

Cost method : Innolux Display Corp. 2,151,044$ 9 Unimicron Technology Corp. 76,549 - Tul Corp. 38,155 6 Pan-International Industrial Corp. 29,017 1 Ole Technology Corp. 6,702 19 V, Inc. 31,620 8 Ceemax Technology Sdn Bhd - 18 Amcom Communications, Inc. - 5

2,333,087 Total 2,355,964$

15

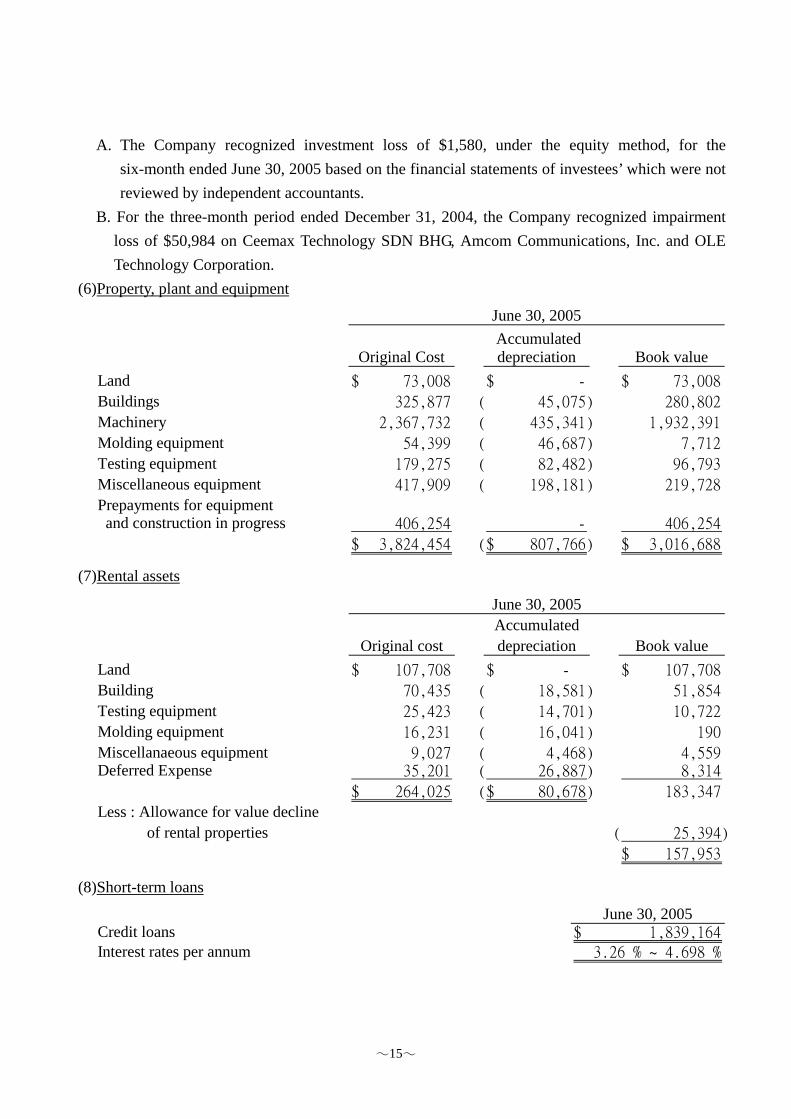

A. The Company recognized investment loss of $1,580, under the equity method, for the six-month ended June 30, 2005 based on the financial statements of investees’ which were not reviewed by independent accountants.

B. For the three-month period ended December 31, 2004, the Company recognized impairment loss of $50,984 on Ceemax Technology SDN BHG, Amcom Communications, Inc. and OLE Technology Corporation.

(6)Property, plant and equipment

AccumulatedOriginal Cost depreciation Book value

Land 73,008$ -$ 73,008$

Buildings 325,877 45,075)( 280,802

Machinery 2,367,732 435,341)( 1,932,391

Molding equipment 54,399 46,687)( 7,712

Testing equipment 179,275 82,482)( 96,793

Miscellaneous equipment 417,909 198,181)( 219,728

Prepayments for equipment and construction in progress 406,254 - 406,254

3,824,454$ 807,766)($ 3,016,688$

June 30, 2005

(7)Rental assets

AccumulatedOriginal cost depreciation Book value

Land 107,708$ -$ 107,708$

Building 70,435 18,581)( 51,854

Testing equipment 25,423 14,701)( 10,722

Molding equipment 16,231 16,041)( 190

Miscellanaeous equipment 9,027 4,468)( 4,559 Deferred Expense 35,201 26,887)( 8,314

264,025$ 80,678)($ 183,347

Less : Allowance for value decline of rental properties 25,394)(

157,953$

June 30, 2005

(8)Short-term loans

June 30, 2005Credit loans 1,839,164$ Interest rates per annum 3.26 % ~ 4.698 %

16

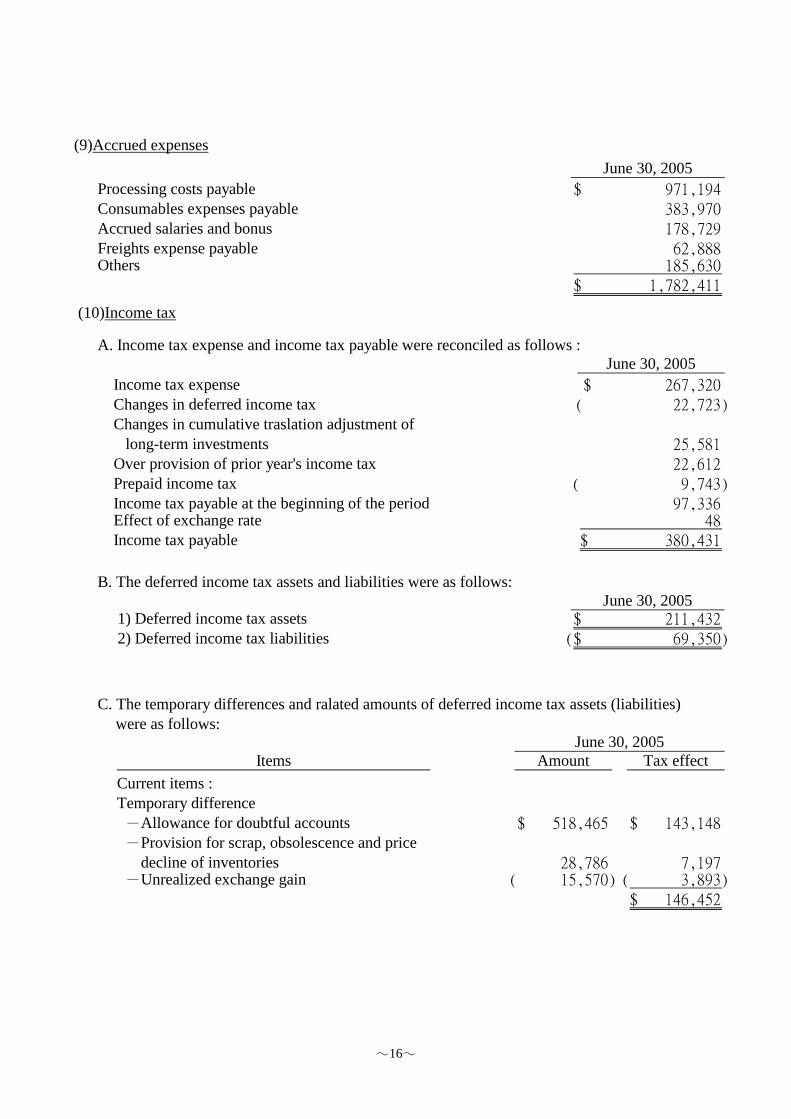

(9)Accrued expenses June 30, 2005

Processing costs payable 971,194$ Consumables expenses payable 383,970 Accrued salaries and bonus 178,729 Freights expense payable 62,888 Others 185,630

1,782,411$ (10)Income tax

A. Income tax expense and income tax payable were reconciled as follows :June 30, 2005

Income tax expense 267,320$ Changes in deferred income tax 22,723)(

Changes in cumulative traslation adjustment of long-term investments 25,581 Over provision of prior year's income tax 22,612 Prepaid income tax 9,743)( Income tax payable at the beginning of the period 97,336 Effect of exchange rate 48 Income tax payable 380,431$

B. The deferred income tax assets and liabilities were as follows:June 30, 2005

1) Deferred income tax assets 211,432$ 2) Deferred income tax liabilities 69,350)($

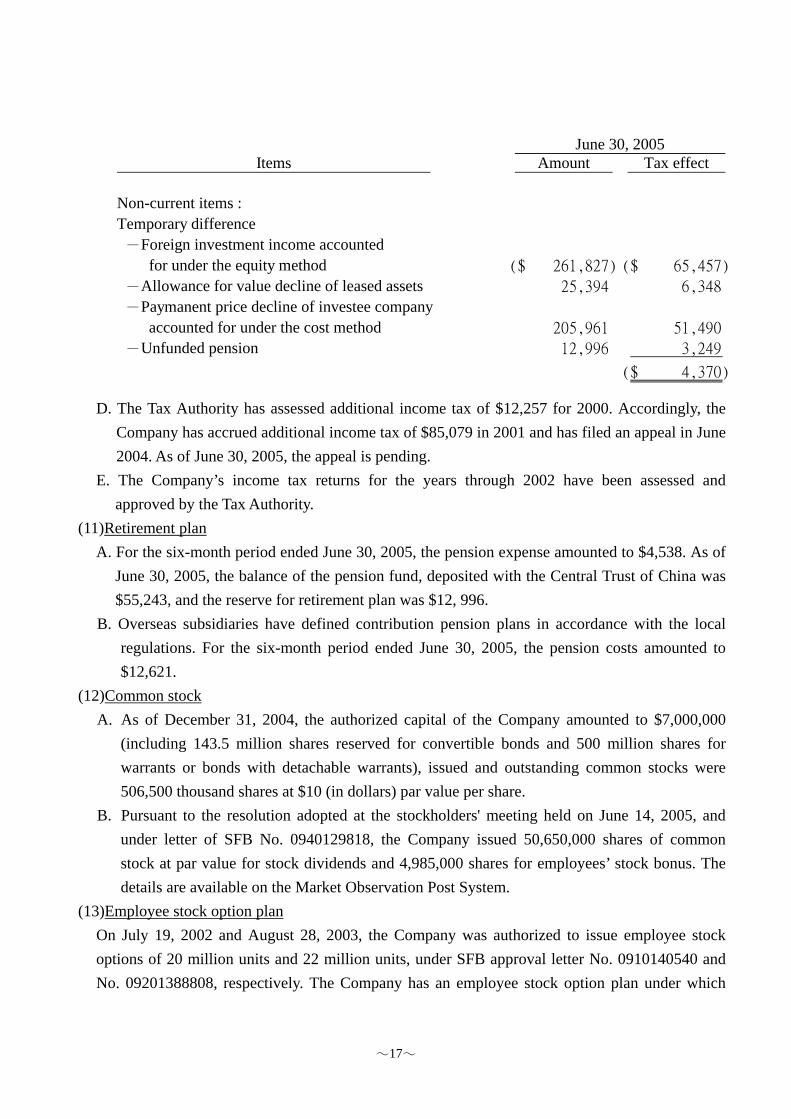

C. The temporary differences and ralated amounts of deferred income tax assets (liabilities) were as follows:

Items Amount Tax effectCurrent items :Temporary difference -Allowance for doubtful accounts 518,465$ 143,148$ -Provision for scrap, obsolescence and price decline of inventories 28,786 7,197 -Unrealized exchange gain 15,570)( 3,893)(

146,452$

June 30, 2005

17

Items Amount Tax effectJune 30, 2005

Non-current items :Temporary difference -Foreign investment income accounted for under the equity method 261,827)($ 65,457)($

-Allowance for value decline of leased assets 25,394 6,348

-Paymanent price decline of investee company accounted for under the cost method 205,961 51,490

-Unfunded pension 12,996 3,249

4,370)($

D. The Tax Authority has assessed additional income tax of $12,257 for 2000. Accordingly, the Company has accrued additional income tax of $85,079 in 2001 and has filed an appeal in June 2004. As of June 30, 2005, the appeal is pending.

E. The Company’s income tax returns for the years through 2002 have been assessed and approved by the Tax Authority.

(11)Retirement plan A. For the six-month period ended June 30, 2005, the pension expense amounted to $4,538. As of

June 30, 2005, the balance of the pension fund, deposited with the Central Trust of China was $55,243, and the reserve for retirement plan was $12, 996.

B. Overseas subsidiaries have defined contribution pension plans in accordance with the local regulations. For the six-month period ended June 30, 2005, the pension costs amounted to $12,621.

(12)Common stock A. As of December 31, 2004, the authorized capital of the Company amounted to $7,000,000

(including 143.5 million shares reserved for convertible bonds and 500 million shares for warrants or bonds with detachable warrants), issued and outstanding common stocks were 506,500 thousand shares at $10 (in dollars) par value per share.

B. Pursuant to the resolution adopted at the stockholders' meeting held on June 14, 2005, and under letter of SFB No. 0940129818, the Company issued 50,650,000 shares of common stock at par value for stock dividends and 4,985,000 shares for employees’ stock bonus. The details are available on the Market Observation Post System.

(13)Employee stock option plan On July 19, 2002 and August 28, 2003, the Company was authorized to issue employee stock options of 20 million units and 22 million units, under SFB approval letter No. 0910140540 and No. 09201388808, respectively. The Company has an employee stock option plan under which

18

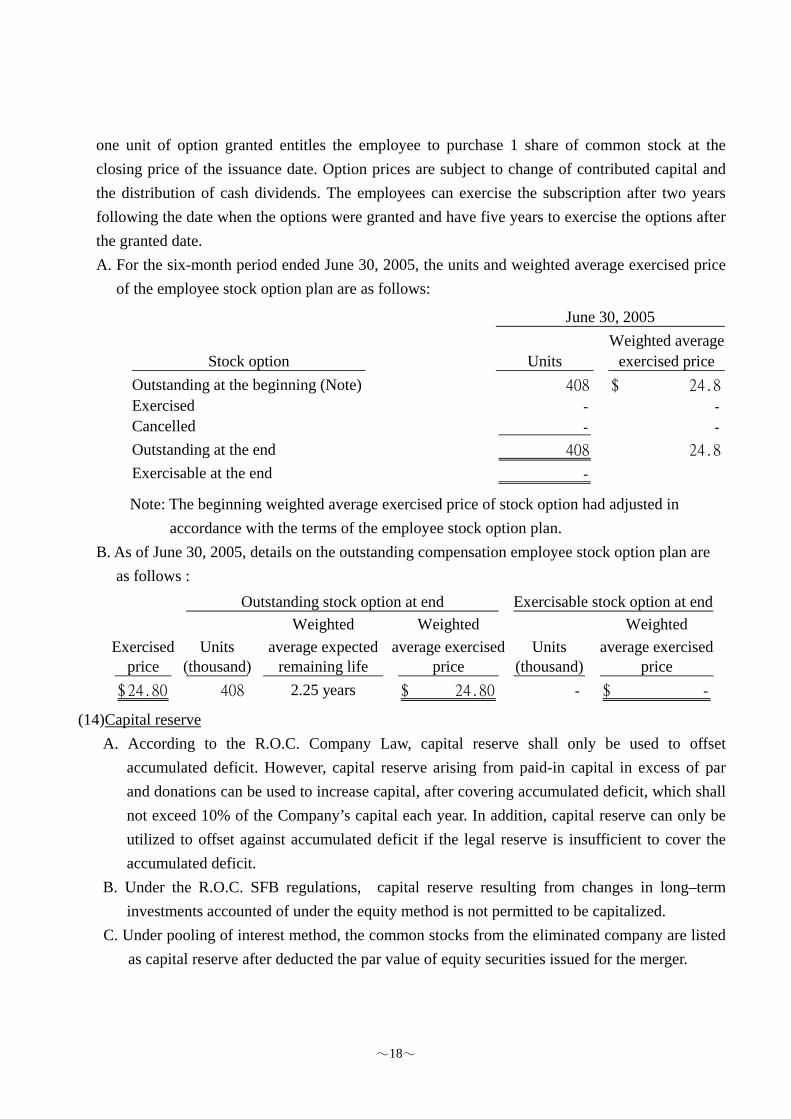

one unit of option granted entitles the employee to purchase 1 share of common stock at the closing price of the issuance date. Option prices are subject to change of contributed capital and the distribution of cash dividends. The employees can exercise the subscription after two years following the date when the options were granted and have five years to exercise the options after the granted date. A. For the six-month period ended June 30, 2005, the units and weighted average exercised price

of the employee stock option plan are as follows:

Weighted averageStock option Units exercised price

Outstanding at the beginning (Note) 408 24.8$

Exercised - -

Cancelled - -

Outstanding at the end 408 24.8

Exercisable at the end -

June 30, 2005

Note: The beginning weighted average exercised price of stock option had adjusted in

accordance with the terms of the employee stock option plan. B. As of June 30, 2005, details on the outstanding compensation employee stock option plan are

as follows :

Weighted Weighted WeightedExercised Units average expected average exercised Units average exercised

price (thousand) remaining life price (thousand) price24.80$ 408 2.25 years 24.80$ - -$

Outstanding stock option at end Exercisable stock option at end

(14)Capital reserve

A. According to the R.O.C. Company Law, capital reserve shall only be used to offset accumulated deficit. However, capital reserve arising from paid-in capital in excess of par and donations can be used to increase capital, after covering accumulated deficit, which shall not exceed 10% of the Company’s capital each year. In addition, capital reserve can only be utilized to offset against accumulated deficit if the legal reserve is insufficient to cover the accumulated deficit.

B. Under the R.O.C. SFB regulations, capital reserve resulting from changes in long–term investments accounted of under the equity method is not permitted to be capitalized.

C. Under pooling of interest method, the common stocks from the eliminated company are listed as capital reserve after deducted the par value of equity securities issued for the merger.

19

(15)Retained earnings

A. Based on the Company’s Articles of Incorporation, the annual net income shall be distributed as follows:

1) Cover any accumulated losses of previous years; 2) 10% of the balance of annual net income after covering accumulated losses should be set

aside as legal reserve; 3) Based on R.O.C. Securities Exchange Law, a special reserve should be set aside, if

necessary; and The residual earnings are to be distributed according to the board of directors’ resolution as approved by the shareholders’ which shall include 8% of employees’ bonuses and the rest of supervisors’ remuneration.

B. Under the R.O.C. regulation, the legal reserve should not exceed 100% of contributed capital after covering any accumulated losses of previous years and distributing 10% of annual net income as legal reserve. Accordingly, the legal reserve can only be used for covering accumulated losses of previous years and capitalizing. When legal reserve is capitalized, the amount of the legal reserve shall aggregate up to 50% of the paid-in capital, and only one half of the amount of such legal reserve can by capitalized.

C. Under the R.O.C. SFC regulation, the Company has appropriated special reserve to cover the balance of the cumulative translation adjustment as of December 31, 2004.

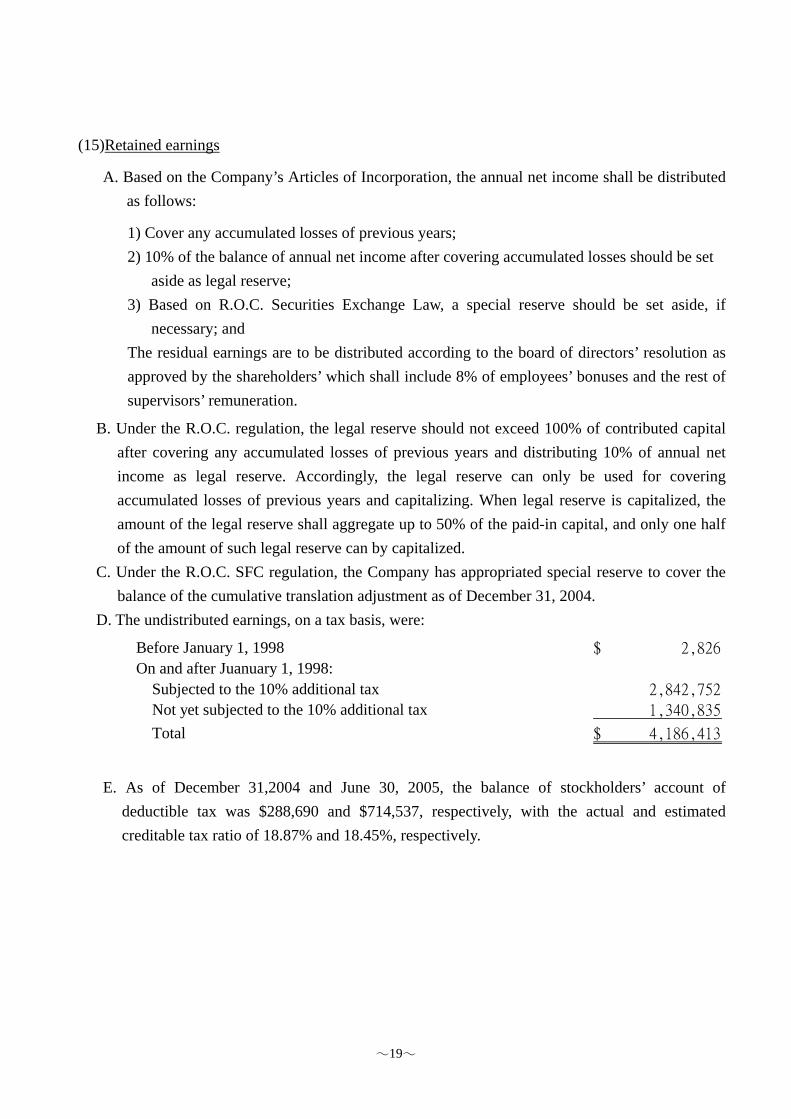

D. The undistributed earnings, on a tax basis, were:

Before January 1, 1998 2,826$

On and after Juanuary 1, 1998:Subjected to the 10% additional tax 2,842,752

Not yet subjected to the 10% additional tax 1,340,835

Total 4,186,413$

E. As of December 31,2004 and June 30, 2005, the balance of stockholders’ account of deductible tax was $288,690 and $714,537, respectively, with the actual and estimated creditable tax ratio of 18.87% and 18.45%, respectively.

20

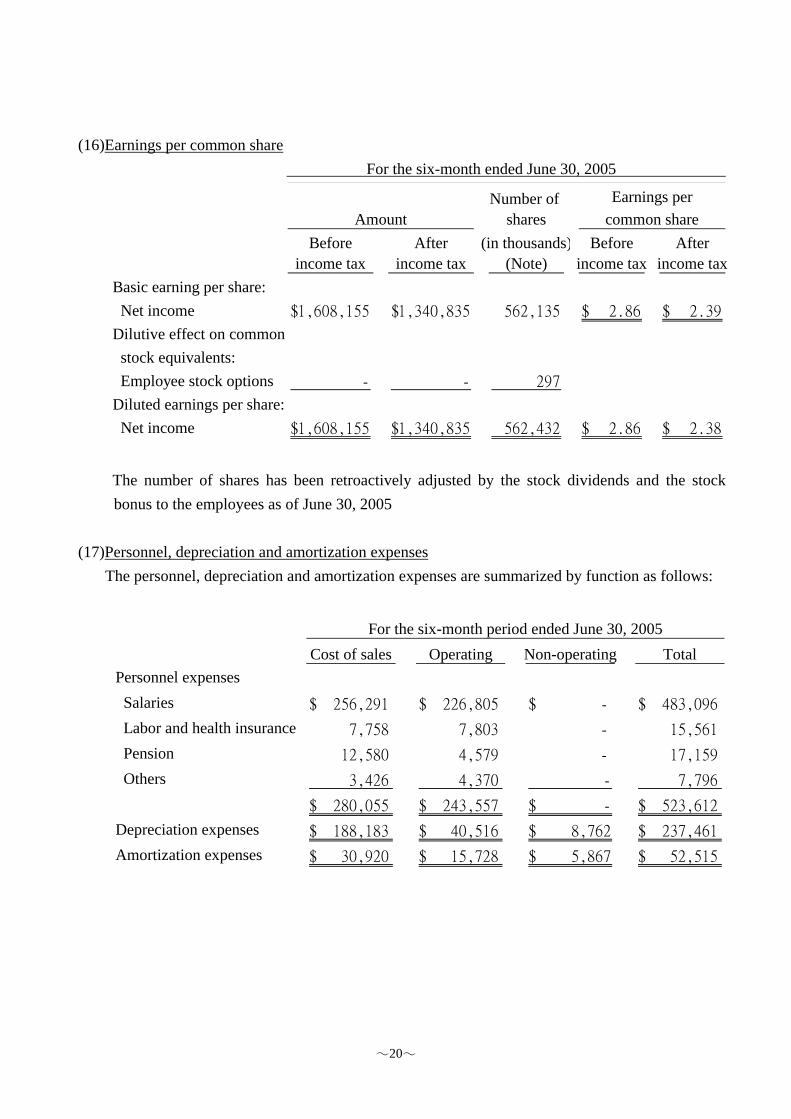

(16)Earnings per common share For the six-month ended June 30, 2005

Number of shares

Before After (in thousands) Before Afterincome tax income tax (Note) income tax income tax

Basic earning per share: Net income 1,608,155$ 1,340,835$ 562,135 2.86$ 2.39$

Dilutive effect on common stock equivalents:

Employee stock options - - 297

Diluted earnings per share: Net income 1,608,155$ 1,340,835$ 562,432 2.86$ 2.38$

Amount common shareEarnings per

The number of shares has been retroactively adjusted by the stock dividends and the stock bonus to the employees as of June 30, 2005

(17)Personnel, depreciation and amortization expenses The personnel, depreciation and amortization expenses are summarized by function as follows:

Cost of sales Operating Non-operating Total

Personnel expenses Salaries $ 256,291 $ 226,805 $ - $ 483,096

Labor and health insurance 7,758 7,803 - 15,561

Pension 12,580 4,579 - 17,159

Others 3,426 4,370 - 7,796

$ 280,055 $ 243,557 -$ $ 523,612

Depreciation expenses $ 188,183 $ 40,516 8,762$ $ 237,461

Amortization expenses $ 30,920 $ 15,728 5,867$ $ 52,515

For the six-month period ended June 30, 2005

21

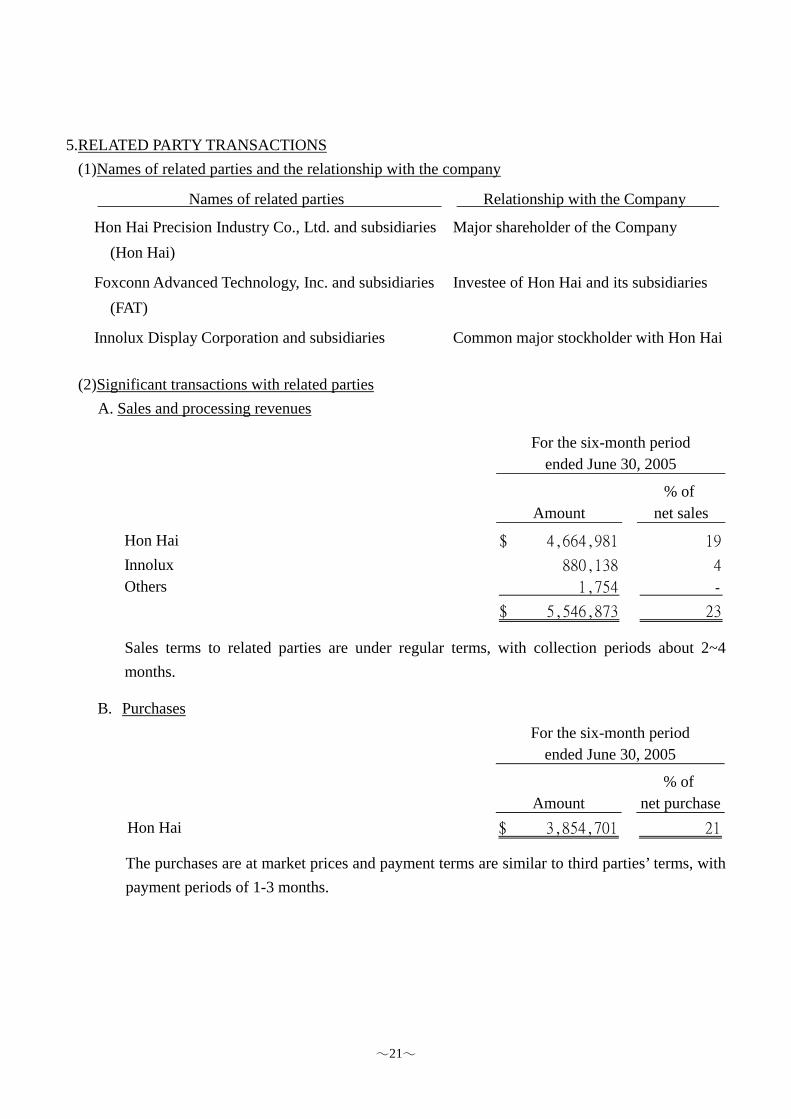

5.RELATED PARTY TRANSACTIONS (1)Names of related parties and the relationship with the company Names of related parties Relationship with the Company

Hon Hai Precision Industry Co., Ltd. and subsidiaries Major shareholder of the Company (Hon Hai)

Foxconn Advanced Technology, Inc. and subsidiaries Investee of Hon Hai and its subsidiaries (FAT)

Innolux Display Corporation and subsidiaries Common major stockholder with Hon Hai

(2)Significant transactions with related parties A. Sales and processing revenues

% of Amount net sales

Hon Hai 4,664,981$ 19

Innolux 880,138 4

Others 1,754 -

5,546,873$ 23

ended June 30, 2005For the six-month period

Sales terms to related parties are under regular terms, with collection periods about 2~4 months.

B. Purchases

% of Amount net purchase

Hon Hai 3,854,701$ 21

ended June 30, 2005For the six-month period

The purchases are at market prices and payment terms are similar to third parties’ terms, with payment periods of 1-3 months.

22

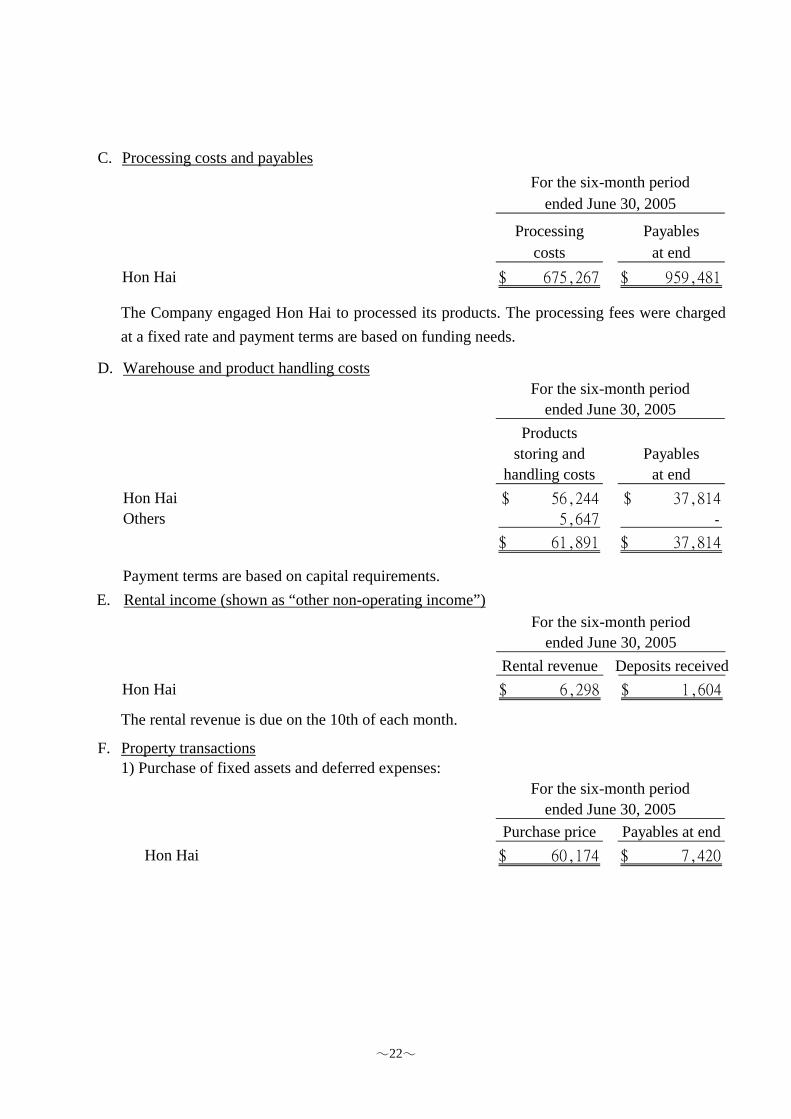

C. Processing costs and payables

Processing Payablescosts at end

Hon Hai 675,267$ 959,481$

ended June 30, 2005For the six-month period

The Company engaged Hon Hai to processed its products. The processing fees were charged at a fixed rate and payment terms are based on funding needs.

D. Warehouse and product handling costs

Productsstoring and Payables

handling costs at endHon Hai 56,244$ 37,814$

Others 5,647 -

61,891$ 37,814$

ended June 30, 2005For the six-month period

Payment terms are based on capital requirements.

E. Rental income (shown as “other non-operating income”)

Rental revenue Deposits receivedHon Hai 6,298$ 1,604$

ended June 30, 2005For the six-month period

The rental revenue is due on the 10th of each month.

F. Property transactions1) Purchase of fixed assets and deferred expenses:

Purchase price Payables at endHon Hai 60,174$ 7,420$

ended June 30, 2005For the six-month period

23

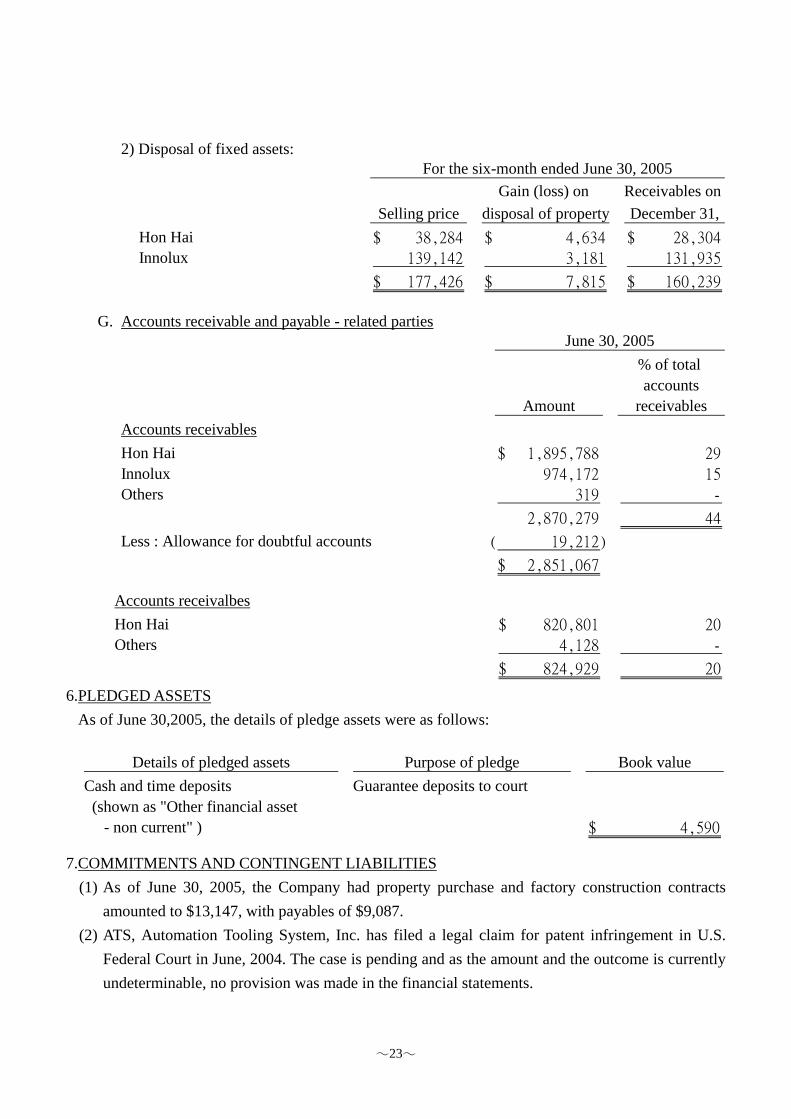

2) Disposal of fixed assets:

Gain (loss) on Receivables on Selling price disposal of property December 31,

Hon Hai 38,284$ 4,634$ 28,304$

Innolux 139,142 3,181 131,935

177,426$ 7,815$ 160,239$

For the six-month ended June 30, 2005

G. Accounts receivable and payable - related parties

% of total accounts

Amount receivablesAccounts receivablesHon Hai 1,895,788$ 29

Innolux 974,172 15

Others 319 -

2,870,279 44

Less : Allowance for doubtful accounts 19,212)(

2,851,067$

June 30, 2005

Accounts receivalbesHon Hai 820,801$ 20

Others 4,128 -

824,929$ 20 6.PLEDGED ASSETS

As of June 30,2005, the details of pledge assets were as follows:

Details of pledged assets Purpose of pledge Book valueCash and time deposits Guarantee deposits to court (shown as "Other financial asset - non current" ) 4,590$

7.COMMITMENTS AND CONTINGENT LIABILITIES (1) As of June 30, 2005, the Company had property purchase and factory construction contracts

amounted to $13,147, with payables of $9,087. (2) ATS, Automation Tooling System, Inc. has filed a legal claim for patent infringement in U.S.

Federal Court in June, 2004. The case is pending and as the amount and the outcome is currently undeterminable, no provision was made in the financial statements.

24

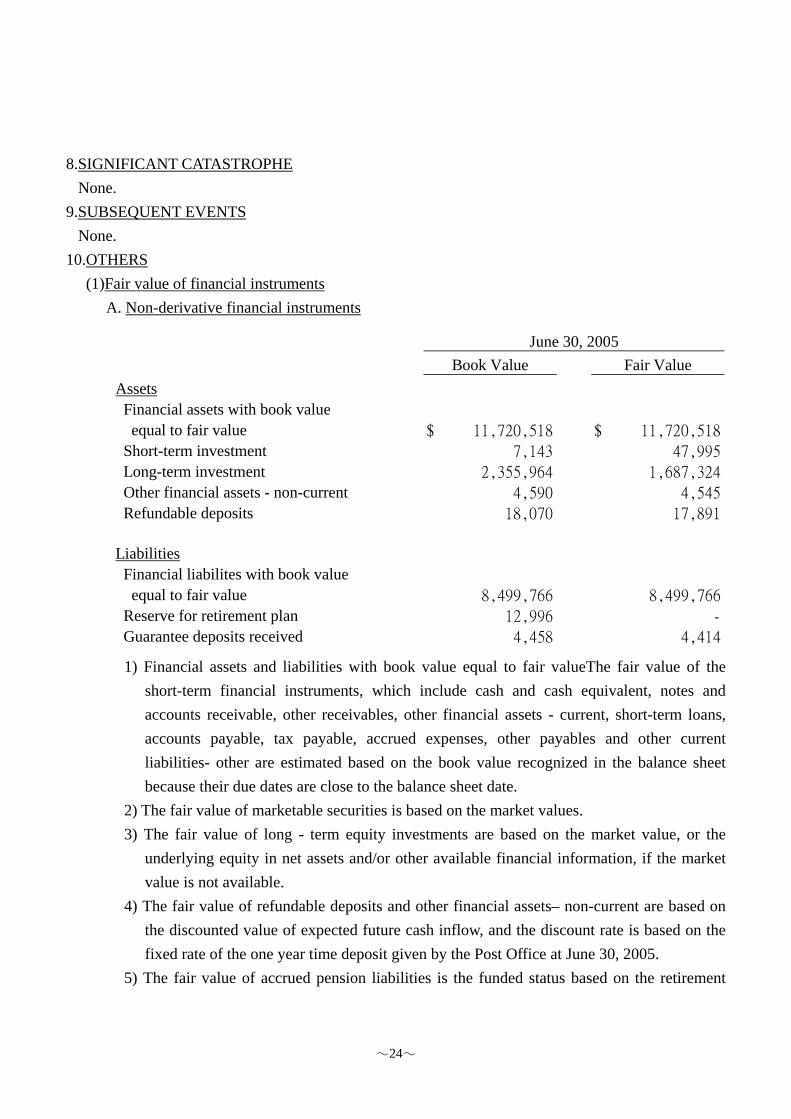

8.SIGNIFICANT CATASTROPHE None.

9.SUBSEQUENT EVENTS None.

10.OTHERS (1)Fair value of financial instruments

A. Non-derivative financial instruments

Book Value Fair ValueAssets

Financial assets with book value equal to fair value 11,720,518$ 11,720,518$

Short-term investment 7,143 47,995

Long-term investment 2,355,964 1,687,324

Other financial assets - non-current 4,590 4,545

Refundable deposits 18,070 17,891

June 30, 2005

Liabilities Financial liabilites with book value equal to fair value 8,499,766 8,499,766

Reserve for retirement plan 12,996 -

Guarantee deposits received 4,458 4,414 1) Financial assets and liabilities with book value equal to fair valueThe fair value of the

short-term financial instruments, which include cash and cash equivalent, notes and accounts receivable, other receivables, other financial assets - current, short-term loans, accounts payable, tax payable, accrued expenses, other payables and other current liabilities- other are estimated based on the book value recognized in the balance sheet because their due dates are close to the balance sheet date.

2) The fair value of marketable securities is based on the market values. 3) The fair value of long - term equity investments are based on the market value, or the

underlying equity in net assets and/or other available financial information, if the market value is not available.

4) The fair value of refundable deposits and other financial assets– non-current are based on the discounted value of expected future cash inflow, and the discount rate is based on the fixed rate of the one year time deposit given by the Post Office at June 30, 2005.

5) The fair value of accrued pension liabilities is the funded status based on the retirement

25

actuarial report as of December 31, 2004, adjusted by the pension costs recognized and contributions to pension fund for the six-month periods ended June 30, 2005.

B. Derivative financial instruments

1) The Company entered into forward exchange contracts with banks to hedge the effect of exchange rate fluctuations on monetary assets or liabilities denominated in foreign currencies. Due to the nature of the hedge, the hedged items offset the gains and losses resulting from fluctuation in exchange rate, therefore, no material market risk is anticipated.

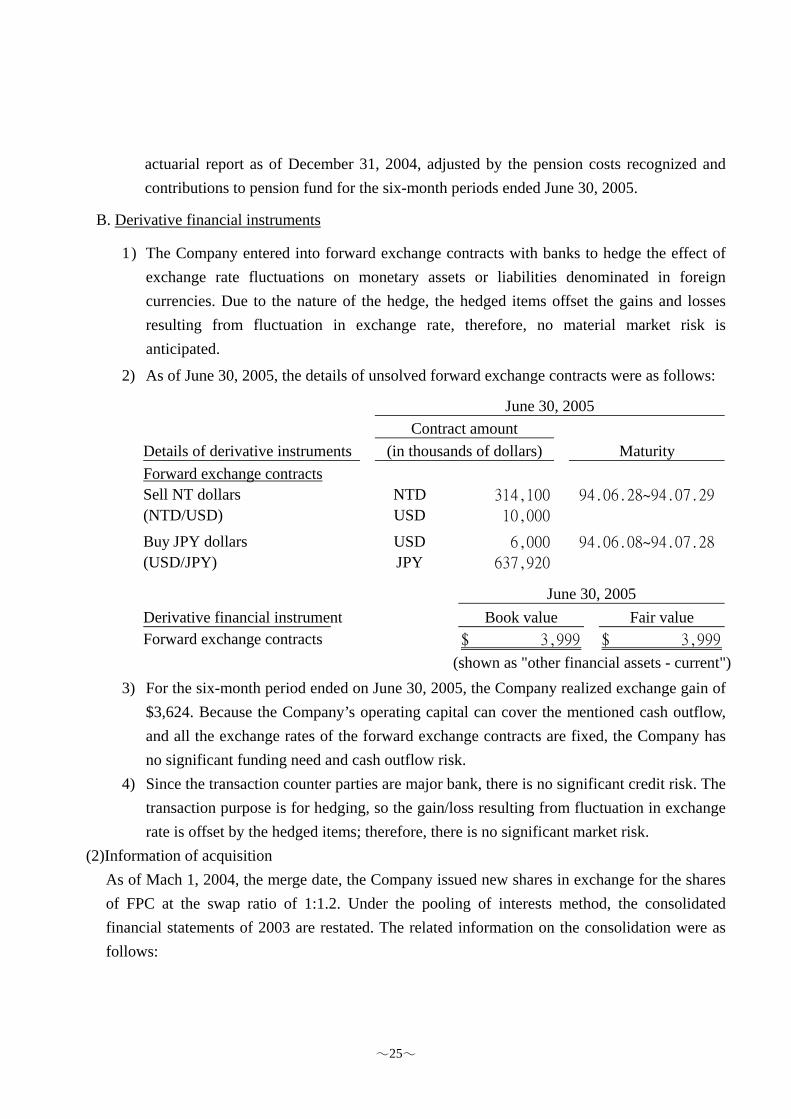

2) As of June 30, 2005, the details of unsolved forward exchange contracts were as follows:

Details of derivative instruments Maturity Forward exchange contracts

Sell NT dollars NTD 314,100 94.06.28~94.07.29

(NTD/USD) USD 10,000

Buy JPY dollars USD 6,000 94.06.08~94.07.28

(USD/JPY) JPY 637,920

June 30, 2005

(in thousands of dollars)Contract amount

Derivative financial instrument Book value Fair value

Forward exchange contracts 3,999$ 3,999$

(shown as "other financial assets - current")

June 30, 2005

3) For the six-month period ended on June 30, 2005, the Company realized exchange gain of

$3,624. Because the Company’s operating capital can cover the mentioned cash outflow, and all the exchange rates of the forward exchange contracts are fixed, the Company has no significant funding need and cash outflow risk.

4) Since the transaction counter parties are major bank, there is no significant credit risk. The transaction purpose is for hedging, so the gain/loss resulting from fluctuation in exchange rate is offset by the hedged items; therefore, there is no significant market risk.

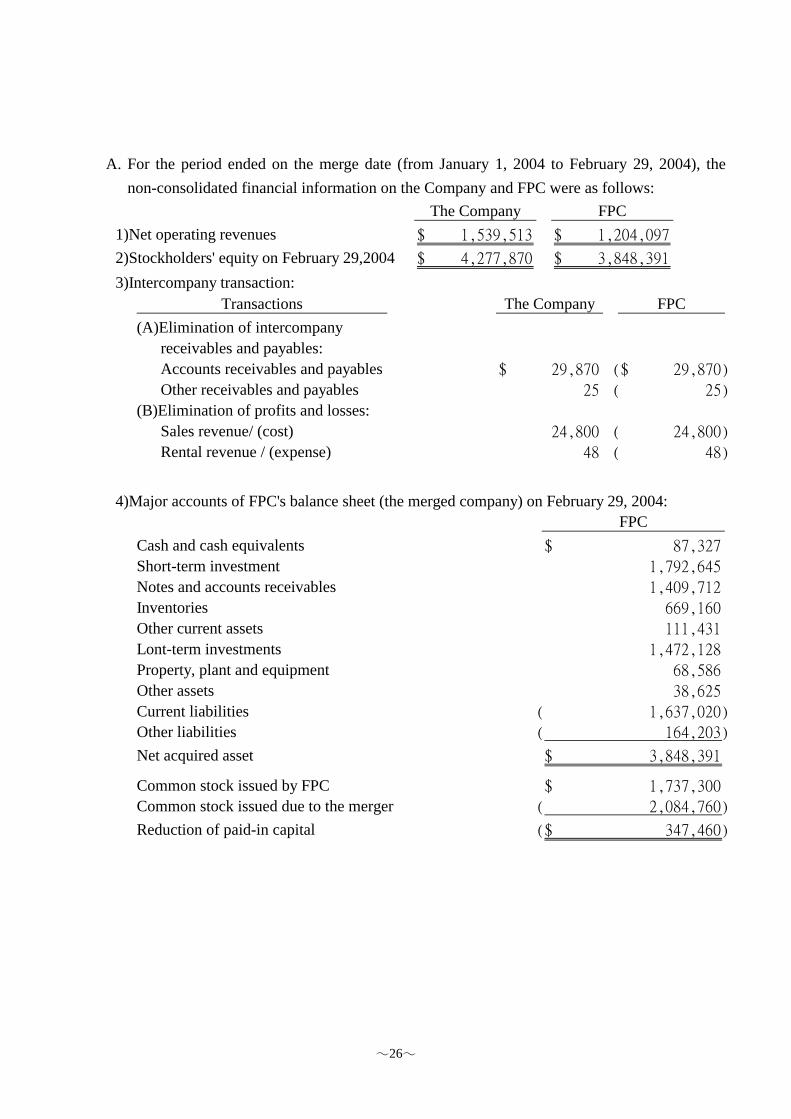

(2)Information of acquisition As of Mach 1, 2004, the merge date, the Company issued new shares in exchange for the shares of FPC at the swap ratio of 1:1.2. Under the pooling of interests method, the consolidated financial statements of 2003 are restated. The related information on the consolidation were as follows:

26

A. For the period ended on the merge date (from January 1, 2004 to February 29, 2004), the non-consolidated financial information on the Company and FPC were as follows:

The Company FPC 1)Net operating revenues 1,539,513$ 1,204,097$

2)Stockholders' equity on February 29,2004 4,277,870$ 3,848,391$ 3)Intercompany transaction:

Transactions The Company FPC(A)Elimination of intercompany receivables and payables: Accounts receivables and payables 29,870$ 29,870)($

Other receivables and payables 25 25)(

(B)Elimination of profits and losses: Sales revenue/ (cost) 24,800 24,800)(

Rental revenue / (expense) 48 48)(

4)Major accounts of FPC's balance sheet (the merged company) on February 29, 2004: FPC

Cash and cash equivalents 87,327$

Short-term investment 1,792,645

Notes and accounts receivables 1,409,712

Inventories 669,160

Other current assets 111,431

Lont-term investments 1,472,128

Property, plant and equipment 68,586

Other assets 38,625

Current liabilities 1,637,020)(

Other liabilities 164,203)(

Net acquired asset 3,848,391$

Common stock issued by FPC 1,737,300$

Common stock issued due to the merger 2,084,760)(

Reduction of paid-in capital 347,460)($

27

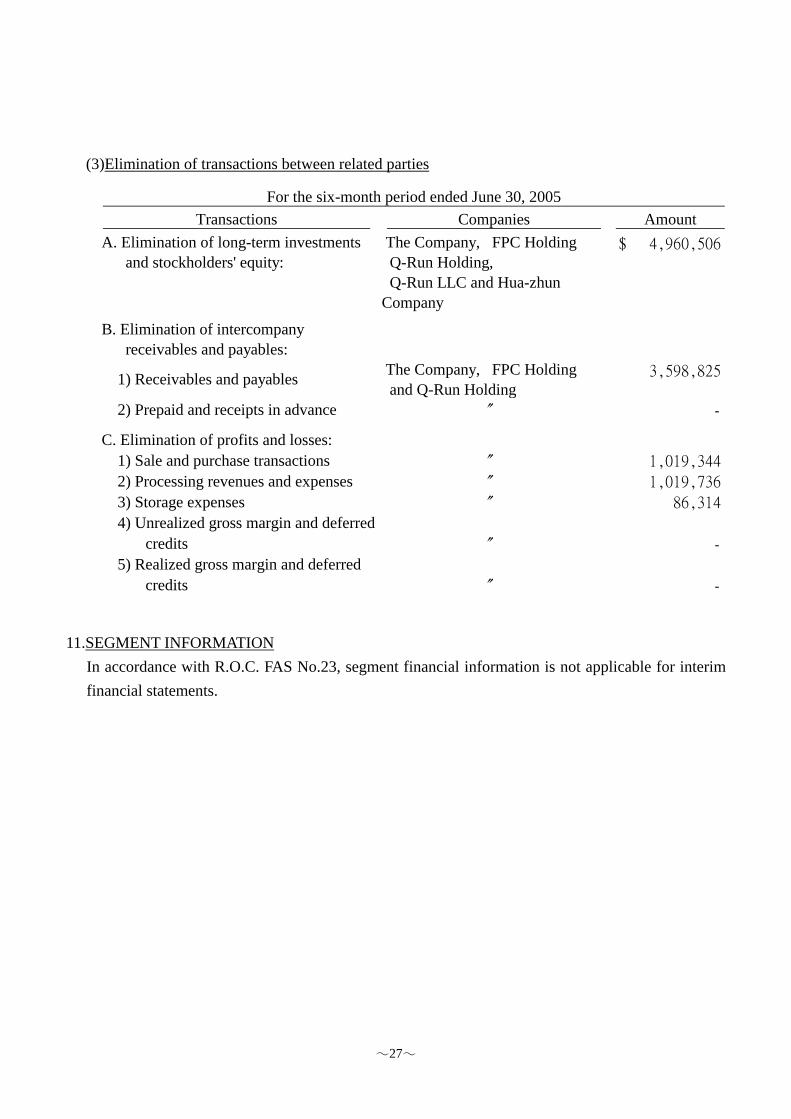

(3)Elimination of transactions between related parties

Transactions Companies Amount A. Elimination of long-term investments and stockholders' equity:

The Company, FPC Holding Q-Run Holding, Q-Run LLC and Hua-zhunCompany

4,960,506$

B. Elimination of intercompany receivables and payables:

1) Receivables and payables The Company, FPC Holding and Q-Run Holding

3,598,825

2) Prepaid and receipts in advance -

C. Elimination of profits and losses: 1) Sale and purchase transactions 1,019,344

2) Processing revenues and expenses 1,019,736

3) Storage expenses 86,314

4) Unrealized gross margin and deferred credits -

5) Realized gross margin and deferred credits -

For the six-month period ended June 30, 2005

11.SEGMENT INFORMATION

In accordance with R.O.C. FAS No.23, segment financial information is not applicable for interim financial statements.

![Alphabetical Cosolidated List of Unapproved Institutions- Final 16[1].07](https://img.pdfslide.us/doc/110x75/553ede73550346bb798b4643/alphabetical-cosolidated-list-of-unapproved-institutions-final-16107.jpg)