Embed Size (px)

Citation preview

Fourth Quarter

2012

Grupo Aeroportuario del Centro Norte

Business and Strategy Overview

Our Location

13 airports and 1 hotel in 10 states in

the central-north of Mexico

* Based on 4Q12 passenger traffic

Pax: 12.6 million in 2012 (+7.0%)

Hotel NH T2

REX MTY

TAM

SLP

DGO

TRC

CUU

CJS

CUL

ZCL

ACA

ZIH

MZT

OMA holds 50-year

concessions to operate 13

airports; the concessions’

term started in 1998.

2

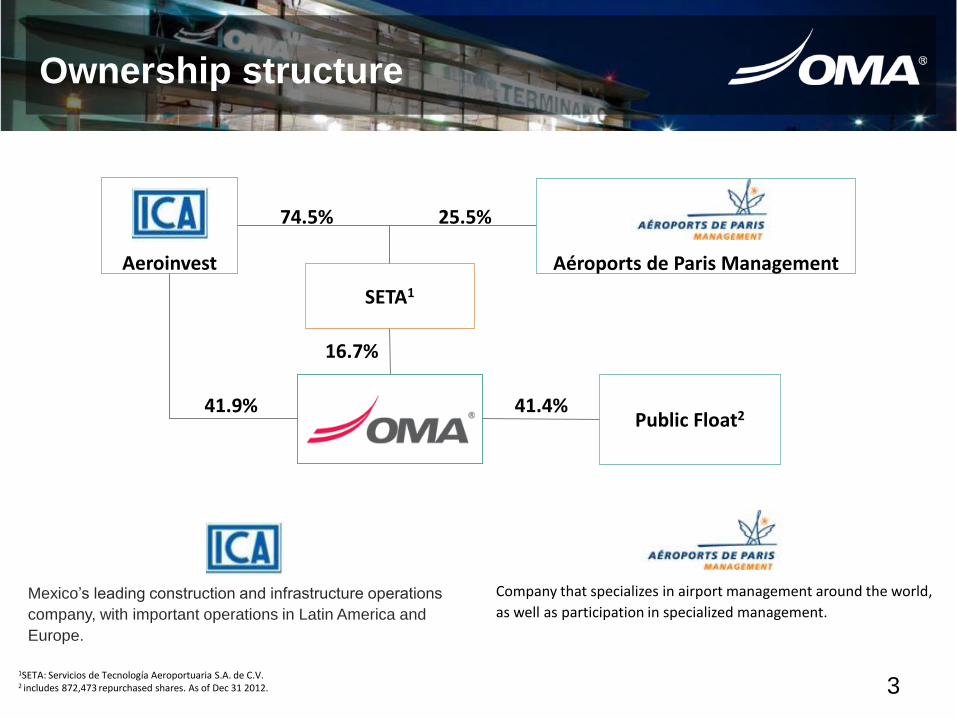

Mexico’s leading construction and infrastructure operations

company, with important operations in Latin America and

Europe.

Ownership structure

1SETA: Servicios de Tecnología Aeroportuaria S.A. de C.V. 2 includes 872,473 repurchased shares. As of Dec 31 2012.

Company that specializes in airport management around the world,

as well as participation in specialized management.

Aeroinvest

SETA1

Aéroports de Paris Management

25.5% 74.5%

16.7%

41.9%

Public Float2 41.4%

3

Main strategic actions

Increase aeronautical revenues

Air traffic

development

and

connectivity

Increase non-aeronautical revenues

Improve

passenger

experience

Diversification

Su

sta

ina

ble

co

mp

an

y

Op

era

tio

nal, s

ecu

rity

, an

d

eff

icie

nc

y le

ad

ers

hip

Current

Industry

outlook

Passenger traffic evolution

16 months of consecutive growth

+5.9% +1.6% +0.6% -18.1%

10.6

11.8

14.2 14.1

11.5 11.6 11.812.5

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012 (udm nov-dic '11)

mil

lon

es

de

pa

xM

illio

n p

asse

nge

rs

12.6

7.0% growth from

2011 to 2012.

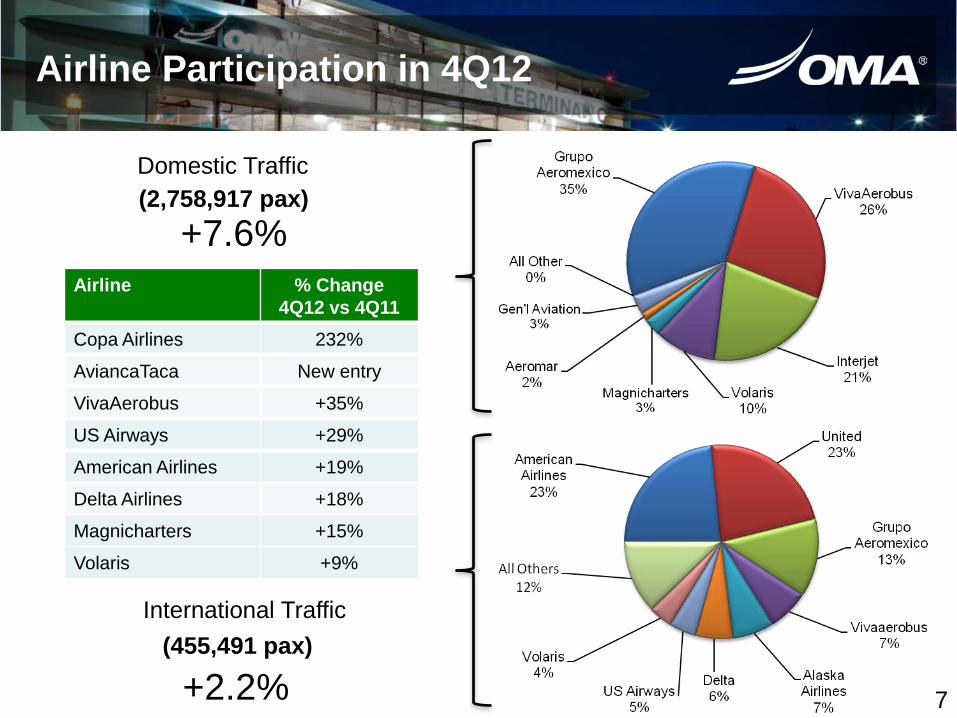

Airline % Change

4Q12 vs 4Q11

Copa Airlines 232%

AviancaTaca New entry

VivaAerobus +35%

US Airways +29%

American Airlines +19%

Delta Airlines +18%

Magnicharters +15%

Volaris +9%

Airline Participation in 4Q12

(2,758,917 pax)

(455,491 pax)

Domestic Traffic

International Traffic

+7.6%

+2.2% 7

Aircrafts available

-200

-160

-120

-80

-40

0

40

80

0

50

100

150

200

250

300

350 Avio

nes Perd

ido

s vs. Gan

ado

sA

vio

nes

Dis

po

nib

les

Aviones disponibles

Aviones perdidos - Aerolineas que dejaron de operar

Aviones nuevos - Aerolíneas existentes

(155)

80307

232

Jun ’08 Aug ’12

There is still a 75 aircraft deficit compared to June 2008.

Airline Average age

(years)

Total number

of aircrafts

Aeroméxico 9.1 113

Interjet 6.6 37

Vivaaerobus 21.8 18

Volaris 4.6 36

Aeromar 16.2 18

Magnicharters 26.6 12

jun-08 ago-12Aviones

Nuevosjun-08 ago-12

INTERJET 11 36 25 MEXICANA 78 0VOLARIS 17 37 20 ALMA 15 0

AEROMEXICO 94 114 20 AEROCALIFORNIA 22 0

VIVAAEROBUS 7 18 11 AVOLAR 8 0AEROMAR 14 16 2 ALADIA 3 0MAGNICHARTERS 5 9 4 AVIACSA 26 0

GLOBAL AIR 4 2 (2) NOVA AIR 3 0

Subtotal 152 232 80 Subtotal 155 0

Aerolíneas Existentes Aviones PerdidosExisting airlines Lost Aircrafts

Industry outlook

Fleet expansion plans of major mexican carriers Source: airlines

Airline Fleet Expansion plans

Aeroméxico • B737, B767, B777

• E145, E190

114 Has received 10 E190 planes in 2012, of an order of 20 placed in 2011. Will receive 1 additional B737-8 for 4Q12, out of an order of 10. It recently confirmed an order to buy 90 Boeing 737-8 and 10 787-9 planes.

Interjet • A320 36 In March it will start operations with Sukhoi regional jet. In 2013 it will receive 9 regional aircrafts and 6 more A320. Recently announced an order of 40 A320Neo aircrafts.

VivaAerobus • B737-300 18 In negotiation with Boing to make a fleet renovation in upcoming years with completely new aircrafts. Expected increase in fleet of 2 or 3 aircrafts in 2013.

Volaris • A319, A320 37 Plans to receive 6 A320 in 2012. For the next 15 years it will receive 44 A320 Neo Aircrafts.

Aeromar • ATR42-300 • ATR42-500

18 Added 2 planes in 2012. In 2013 it will increase its fleet with ATR aircrafts of more capacity.

Maximum Rates –

Formula Per Airport

n

nnn

n

nr

OWLMRTVNPV

)1(

)(15

1

NPV: Net Present Value, reference value of airport.

MR: Maximum Rate used to cap revenues from aeronautical services per

workload unit.

WL: Number of workload units forecasted per year (explicit forecast) in

the Master Development Plan.

O: Total outcome per year:

a. OPEX Operational costs anda expenditures (before depreciation and

amortization)

b. CAPEX Capital expeditures.

r: Discount rate.

n: Time period, every year included in the explicit forecast.

TV: Terminal Value, discounted value of all future cash flows beyond the

15th year.

Air traffic

Development

strategy

Four main actions to develop air traffic

1.- Develop a HUB in Monterrey airport

2.- Enhance the number of low cost passengers

3.- More aggressive incentive policy for new flights

4.- Increase the number of international flights

Four main actions to develop air traffic

1.- Develop a HUB in Monterrey Airport Current route network in Monterrey airport.

Chicago Tijuana

Cd. Juárez

Culiacán

Las Vegas

Atlanta

Guadalajara

Cancún

Hermosillo

Villahermosa

Dallas

Veracruz Bajío

Acapulco

Houston

Toluca

Mazatlán

Mérida

Querétaro

México

Tampico

Chihuahua

Detroit

Los Cabos

Oaxaca

Brownsville

San

Antonio

Tuxtla Gutiérrez

Panamá

Orlando

Costa Rica

La Habana

Monterrey

Puerto Vallarta

Conectivity in Monterrey increased to Cuba, Panama and Costa Rica. Potential for NY and Miami.

Four main actions to develop air traffic

1.- Develop a HUB in Monterrey Airport

Monterrey

Detroit

Toluca

El Paso

Laredo

New routes (january 2013)

New routes (april 2013)

Morelia

Chicago

Bajío

Routes that started in 2012

OMA proposed 35 potential routes to Aeroméxico, out of which 7 have started or will start in 2013.

E170 and E190 favor conectivity for regional routes.

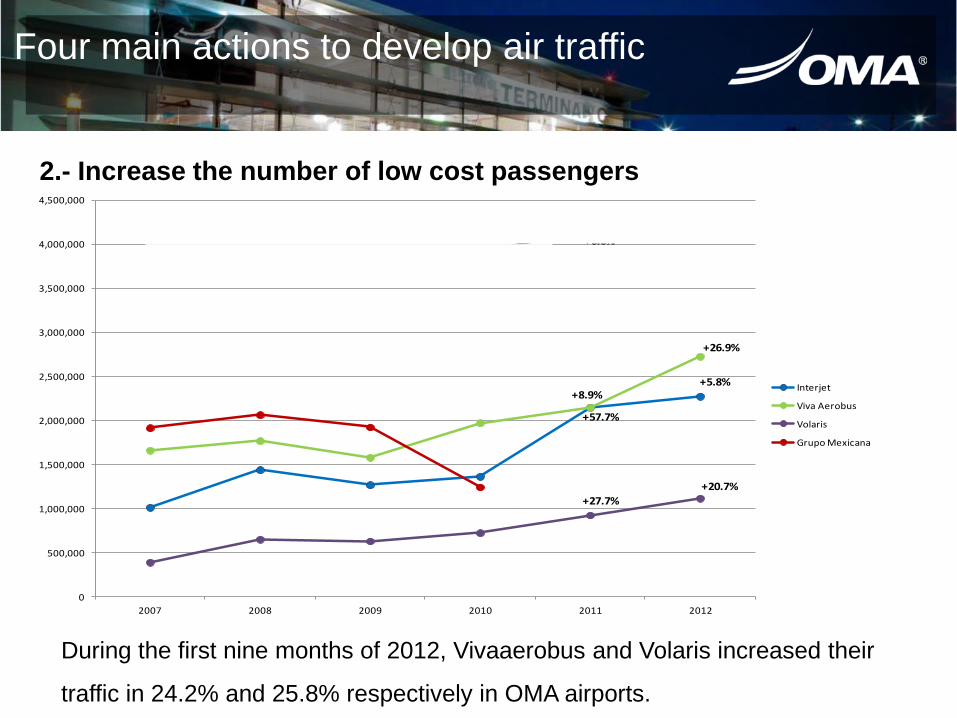

Four main actions to develop air traffic

2.- Increase the number of low cost passengers

During the first nine months of 2012, Vivaaerobus and Volaris increased their

traffic in 24.2% and 25.8% respectively in OMA airports.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2007 2008 2009 2010 2011 2012

Grupo Aeroméxico

Interjet

Viva Aerobus

Volaris

Grupo Mexicana

+6.6%

+57.7%

+8.9%

+27.7%

-0.5%

+5.8%

+26.9%

+20.7%

Var% 11/10 Var% 12/11

Four main actions to develop air traffic

Three main ways to increase low cost passengers:

1.- Global incentives offer

2.- Incentives policy with CANAERO

3.- Constant and direct promotion with airlines to promote new routes.

2.- Increase the number of low cost passengers

Four main actions to develop air traffic

3.- More aggressive incentive policy

A) New routes: 50% discount on landing fees, platform and jet bridges for the first 6

months of operation.

B) New frequencies: 50% discount on landing fees, platform and jet bridges for the first 6

months of operation depending on the non-peak hours of the airport for domestic

flights and 80% discount for international flights. From 50%, since November of 2011.

C) Marketing: one billboard at the airport and a promotional video of the new route in the

monitors that are inside the terminal building. Each marketing campaign has a 2

month period.

Four main actions to develop air traffic

3.- More aggressive incentive policy

Grant a 30% discount on TUA for national routes and 40% discount

on international routes that start in 2012.

Grant an incentive on incremental traffic volume: A) Turistic Airports

Year Airports % Growth Incentive

2012 ACA,MZT,ZIH, ZCL At least 5% 17%

At least 10% 20%

At least 15% 23%

At least 20% 26%

B) Regional, Border and Metropolitan Airports

Year Airports % Growth Incentive

2012 CJS,CUU,CUL,DGO,MTY,REX,SLP,TAM,TRC At least 5% 12%

At least 10% 15%

At least 15% 18%

At least 20% 21%

Four main actions to develop air traffic

Chicago Los Angeles

Phoenix

Culiacán

Las Vegas

Atlanta Dallas

Zihuatanejo

Houston

Mazatlán

Chihuahua

Detroit

Brownsville

San Antonio

Panamá

Orlando

Costa Rica

La Habana Monterrey

4.- Increase the number of international routes

Durango

Vancouver

Calgary Edmonton

San Luis Potosí

Tampico

Torreón

Zacatecas

Acapulco

OMA currently has 35 internacional routes.

Four main actions to develop air traffic

4.- Increase the number of international routes

Mazatlán

Los Angeles

Oakland Denver

San Antonio

Houston

New routes 2012

For the winter season of 2013,

Caljet, an airline charter based in

San Diego, will operate 5

destinations, 4 of them new from

Mazatlan.

Caljet operates 8 B737-400 for

150 passengers in a 2 type

configuration.

Current routes

Commercial

Strategy

Business Strategy Commercial activity development

Air traffic – Non Aeronautical Revenue (relation)

110 125 165

219 261

298 342

371 369

492

589

726

8.8 8.3 8.6 9.5

10.3 11.5

13.9 13.7

11.5 11.6 11.8 12.6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 UDM 2012

INA (MDP)

PAX (M)

NAR (Ps.M)

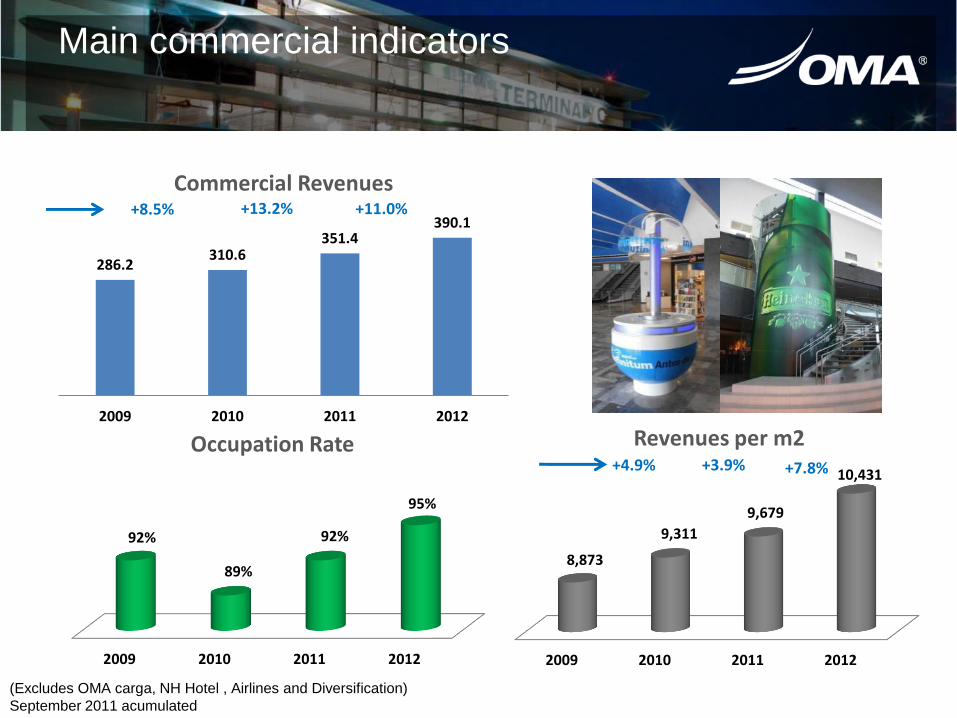

Commercial results

Commercial revenues are consistently growing in the last years:

Increasing by +11% and +Ps.38.6 million in 2012 Vs 2011.

The commercial revenue lines that have contributed the most to the variation, given its growth are the following:

Parking +10% ó +Ps. 10.9 million. Advertising +9% ó +Ps. 7.1 million. Passenger Service +205% ó +Ps. 6.1 million. Restaurants +14% ó +Ps. 5.2 million.

Average annual commercial spaces occupation from 89% in 2010 to 95% in December 2012

286.2 310.6

351.4 390.1

11.5 11.6

11.8

12.6

0

50

100

150

200

250

300

350

400

450

2009 2010 2011 2012

Commercial Income Pax

Note: Full year comparisons.

2009 2010 2011 2012

8,873

9,311

9,679

10,431

Revenues per m2

Main commercial indicators

+3.9% +4.9% +7.8%

(Excludes OMA carga, NH Hotel , Airlines and Diversification)

September 2011 acumulated

+13.2% +8.5% +11.0%

286.2 310.6

351.4 390.1

2009 2010 2011 2012

Commercial Revenues

2009 2010 2011 2012

92%

89%

92%

95%

Occupation Rate

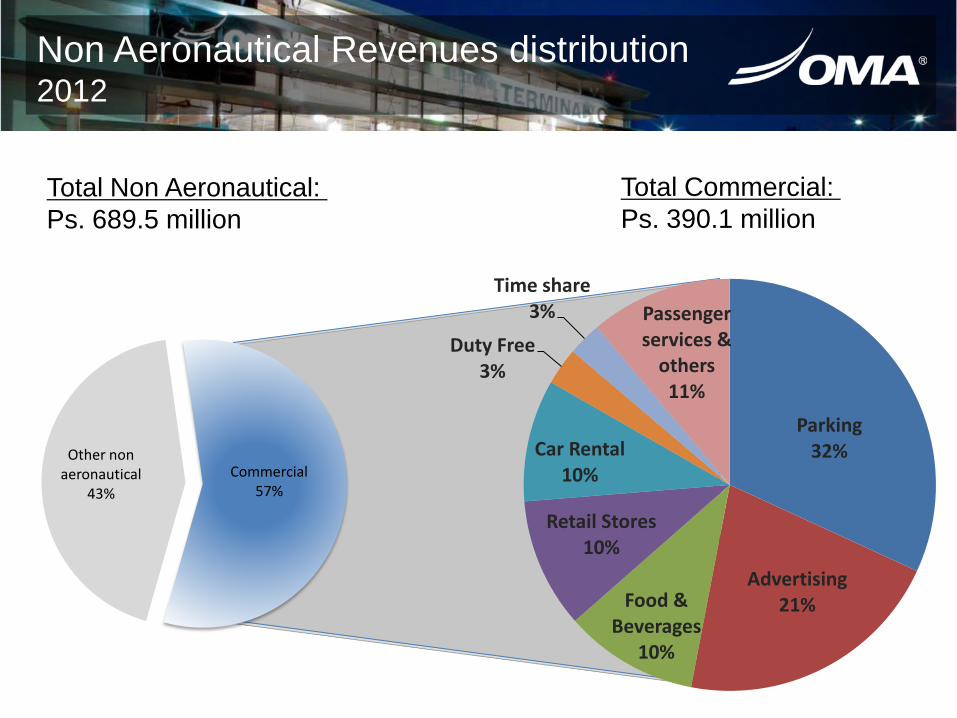

Non Aeronautical Revenues distribution 2012

Commercial 57%

Other non aeronautical

43%

Total Non Aeronautical:

Ps. 689.5 million

Total Commercial:

Ps. 390.1 million

Parking 32%

Advertising 21% Food &

Beverages 10%

Retail Stores 10%

Car Rental 10%

Duty Free 3%

Time share 3% Passenger

services & others

11%

Business Strategy Commercial activity development

Commercial strategic focus

‒ Diferentiation

‒ Global and local recognized brands

‒ Marketing campaigns

‒ Space optimization

‒ Premium product introduction

‒ Alternative advertizing innovation

Innovative Concepts

Alternative Advertising +9% 2012 vs. 2011 Accounted for 19% of commercial revenue in 2012

Retail Stores, Restaurants and Duty Free

24% of total commercial

revenue

Commercial spaces occupation 11,783 sq.

meters in 2009 to 15,216 sq. meters in 2012.

+29% commercial space

+5% revenues 2012 vs 2011

95% occupation

Parking

32% of commercial revenues

+10% 2012 Vs 2011.

Premium – Short and Long Stay– New Low Cost –

Airport Community New strategy of sales.

Commercial passenger services

Enhance passenger

experience

+205% 2012 vs 2011

Diversification

Strategy

Business Strategy New businesses and diversification

Diversification: Take advantage of land reserve

Diversification

Offices

Commercial and retail

Industrial and Logistics

Hotels

Intermodal center

Service stations

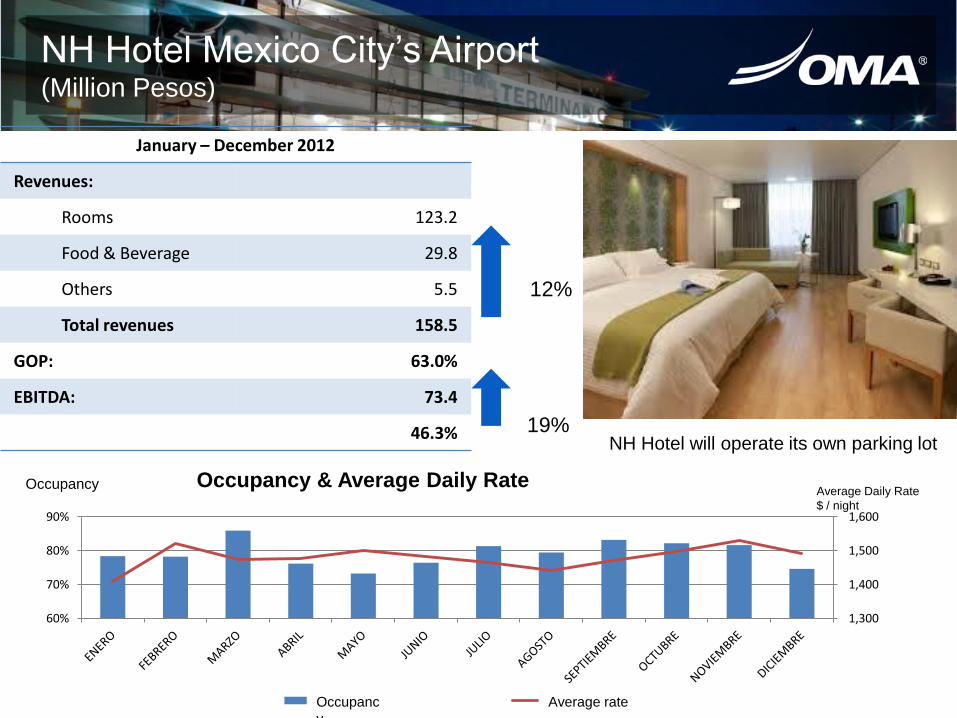

NH Hotel Mexico City’s Airport (Million Pesos)

Occupancy

January – December 2012

Revenues:

Rooms 123.2

Food & Beverage 29.8

Others 5.5

Total revenues 158.5

GOP: 63.0%

EBITDA: 73.4

46.3%

12%

19% NH Hotel will operate its own parking lot

Average Daily Rate

$ / night

Occupancy & Average Daily Rate

1,300

1,400

1,500

1,600

60%

70%

80%

90%

OCUPACION TARIFA PROMEDIO Occupanc

y

Average rate

OMA Carga - Key Highlights

0 2,000 4,000 6,000 8,000

10,000

1Q 2Q 3Q 4Q

'00

0 P

eso

s

2012 2011

OMA Carga • Revenue increased:

• 4Q-12 vs 4Q-11 – 21% • 4Q-12 vs 4Q-10 – 52%

Land

23%

Land

46%

Air77%

Air

54%

2011 2012

Volume Distribution

1. Abril 2012: New initiatives (FFCC, Customer Service)

2. Revenues per kilo Increasing

Main Drivers:

Imports, Security and Ground business conectivity

Business covered

Maneuvers (Load & Unload shipments)

Warehousing

X Ray screening

Cross dock and temporary warehousing

Import – Export Process

Secure & Control – Bonded Area

Driving growth

• MULTIMODAL: driving the "next gen"

performance

• "Clustering" for competitive advantage: AIR-

GROUND-FFCC

• Diversification: Logistics hub, Free Trade

Zones, Industrial Parks

Monterrey airport Hotel

Hotel business in other airports

‒ Monterrey airports. Complete studies, looking for partners

‒ Culiacán airport. Studies in process

Terminal B

Terminal A

Hotel

MTY Hotel – Feasibility studies complete 120-140 rooms

Monterrey Hotel negociation highlights: • Interested investor groups • Investment structure in process • Investment analysis

Marketing and financial studies complete

Cargo City Monterrey

Cargo City MTY – Only terminal in Mexico for logistic services

Development of a planned logistics

terminal integrating all the stakeholders of

the logistic supply chain: customs,

customs agents, transports, etc.

1,045 sq. m offices 95% occupation

Cargo City – Lower and higher levels

Current situation :

• Allocated 61% of the Ground Level spaces.

Strategy:

• Replicar el éxito de cargo city ofreciendo espacios en renta acondicionados

• Brokers participation – New brands in target.

• Target: International companies looking for corporate offices in Apodaca

• Satisfy existing demand at competitive prices

• Conditioning works in Mar-13 on a pre-lease base

Projects in progress – Strip Mall Monterrey Airport

On Going Projects - Monterrey’s Airport

Real Estate Master Plan

Urban design will cover

• Total area: 66 has

• 42 has:

• Retail

• Industrial park

• Near to terminal zone

On Going Projects - Gas Station Monterrey Gas Station Construction Works

Opening date: December 24, 2012

First rent payment: December 2012

Project Render

Gas Station and Convenience Stores Other Developments

Tampico:

Local gas and tire merchant signed a contract:

• 3,200 sqm of land in lease

• Two phases:

• Convenience store and gas

station

• Commercial spaces to car related

business.

Monterrey – Convenience store at gas station:

• Contract in process

• 725 sqm land in lease.

• Term: 15 years

Project Portfolio

Industrial & Logistic

• Chihuahua – Industrial park

• Mazatlan- Multimodal logistic and cargo park

• Durango, San Luis Potosí, Zacatecas- Industrial parks, warehouses & Free Trade Zones.

• Reynosa- Fiscal maneuvers park adjacent to bonded area. Retail developments

• Culiacan, Ciudad Juarez, Tampico & Torreon – Hotel & Commercial area

• Convention and meeting room facilities in NH Hotel T2 Mexico City Airport

• Retail & office developments in Monterrey

Possible future proyects

4. Sustainability and

Human Capital

‒Quality: ISO 9001

‒Environment: ISO 14001

‒Environment : Environmental quality PROFEPA

‒Occupational health and security: OHSAS 18001

‒Occupational health and security : Automanagement programSTPS

‒Sustainability: Part of Sustainability Index by the Mexican Stock Exchange

‒Sustainability: Socially responsible company, by CEMEFI and AliaRSE

‒ Corporate Sustainability: Corporate transparency Index

‒Great Place to Work Mexico: Ranked top 100 by the GPTW Institute.

‒Passenger satisfaction: Mazatlán airport qualified by Airports Council

International as the best in its category for Latinamerica

Sustainability and Human Capital

Our certifications

Results and guidance

Consistent Revenue and EBITDA Growth

48

Revenues (Excluding construction revenues, Ps. Million)

1,4

62

1,3

60

1,4

40

1,5

96

1,7

70

2,0

18

2,2

69

2,2

32

2,0

55

2,1

44

2,4

59

2,8

19

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EBITDA (Adjusted EBITDA for years 2010, 2011 and 2012, Ps. Million)

53

7

52

5

60

9

75

2

87

7

1,0

98

1,2

73

1,1

83

1,0

53

87

0

1,0

84

1,5

11

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Strategy Execution

Strategy execution in all lines of action

+7.0% traffic increase 2012 vs 2011

International traffic recovery

MTY Connectivity

Non Aeronautical Revenues maximization (3Q12):

95% occupancy in commercial spaces

19 quarters with NAR / PAX growth

+9% Non Aeronautical Revenues / PAX (w/o NH)

+47% commercial area since 2005

Diversification: 29% of Non Aeronautical Revenues

+24% OMA Carga Revenues

+12% NH Hotel Revenues

* Acummulated 9M2012

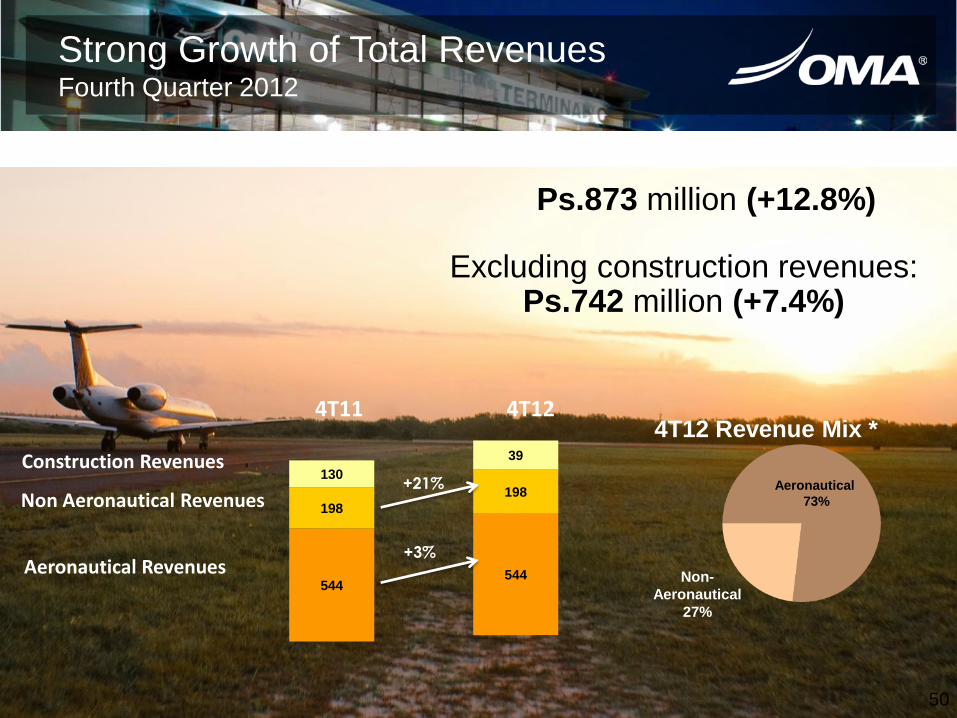

Strong Growth of Total Revenues Fourth Quarter 2012

50

Non-

Aeronautical

27%

Aeronautical

73%

Ps.873 million (+12.8%)

4T12 Revenue Mix *

544

198

39

Excluding construction revenues: Ps.742 million (+7.4%)

544

198

130

4T11 4T12

+3%

+21%

Construction Revenues

Non Aeronautical Revenues

Aeronautical Revenues

4Q12

Ps.544 M

4Q11

Ps.527 M

51

Maximizing Regulated Revenues

18%

65%

17% 17%

18%

65%

Aeronautical Revenue / Pax increased reached 169.3 MXN in 4Q12

Aeronautical Revenues:

+3.3% in 4Q12

Total traffic increased +6.8%

Full year incentives payment

Airport services, leases and access rights

Domestic Passenger Charge

International Passenger Charge

Non Aeronautical Revenues increased 21% to Ps.198 million in 4Q12

Better occupancy rate at parking lots (+7%) NH T2 Hotel maturity (+10%) Growth of OMA Carga (+21%)

In 4Q12 49 new commercial spaces, advertizing, communication, passenger

services and other 52

Improving the Passenger Experience Expansion of Commercial Activities

NAR Composition

Non Aeronautical Revenues / PAX increased 13.0% to 61.6 MXN in 4Q12.

NH Hotel 23%

Parking 19%

Advertising 12%

Airline Leasing 8%

Restaurants 6%

Cost recoveries

6%

Space Leasing 6%

Car Rental 5%

OMA Carga 5%

Baggage Screening

4%

Other 6%

* Retail, Duty Free, and other leases such as VIP lounges

53

Operating Costs and Expenses

Million pesos 4Q11 4Q12 %

Change

Total operating costs and

expenses

516 580 12.2

Cost of services 160 181 13.9

Maintenance provision 41 41 (0.9)

G & A 141 127 (9.5)

Construction cost 82 130 58

Concession tax 33 37 12

Technical Assistance

Fee

16 17 5

Depreciation &

Amortization

44 49 12

Factors:

Start of operations of baggage

screening services.

Security services contract increase.

Concession tax and technical

assistance increased due to higher

revenues.

Cost

control

initiatives

► Increase efficiency in

conjunction with

suppliers

► Strengthen audit and

cost control system

► Develop a savings

culture program

► Encourage and

implement employee

recommendations

301 341

4T11 4T12

EBITDA Adjusted EBITDA

342 382

4T11 4T12

54

Growth in Cash Flow Generation

39.1% 49.5% 38.8% 51.5%

OMA achieved 51.5% in Adjusted EBITDA Margin, an important increase in

cash flow generation.

OMA calculates Adjusted EBITDA, which further adjusts EBITDA for the

maintenance provision, construction revenue, and construction expense.

The Adjusted EBITDA margin is calculated against the sum of aeronautical

and non-aeronautical revenues.

• Data in million pesos

55

Return on Equity

Important improvement in recent years

11% 10%

13%

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012

ROE (bajo IFRS desde 2010)

(Bajo IFRS desde 2010)

Visibility Capex, Dividends

and guidance

2012

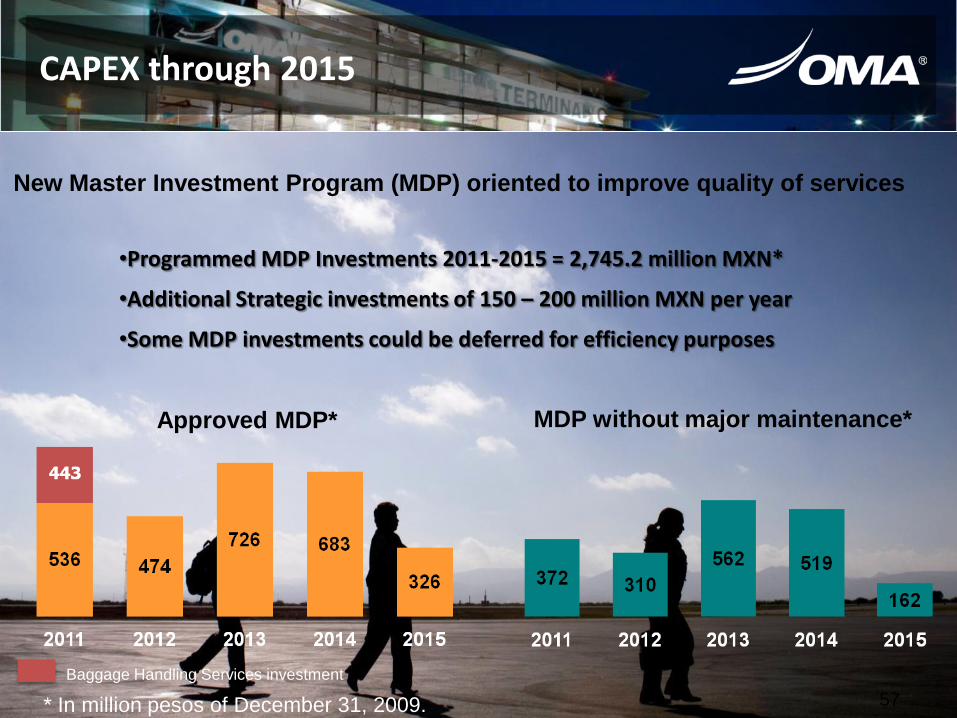

CAPEX through 2015

•Programmed MDP Investments 2011-2015 = 2,745.2 million MXN*

•Additional Strategic investments of 150 – 200 million MXN per year

•Some MDP investments could be deferred for efficiency purposes

57

New Master Investment Program (MDP) oriented to improve quality of services

Approved MDP* MDP without major maintenance*

* In million pesos of December 31, 2009.

Baggage Handling Services investment

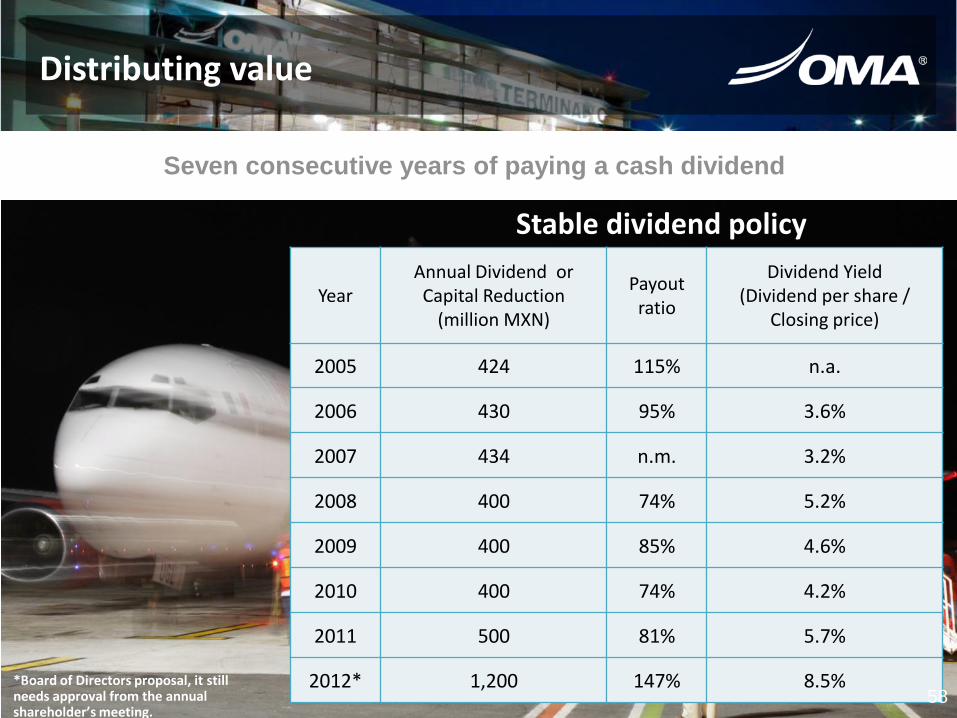

Year Annual Dividend or Capital Reduction

(million MXN)

Payout ratio

Dividend Yield (Dividend per share /

Closing price)

2005 424 115% n.a.

2006 430 95% 3.6%

2007 434 n.m. 3.2%

2008 400 74% 5.2%

2009 400 85% 4.6%

2010 400 74% 4.2%

2011 500 81% 5.7%

2012* 1,200 147% 8.5%

Seven consecutive years of paying a cash dividend

Stable dividend policy

58

Distributing value

*Board of Directors proposal, it still needs approval from the annual shareholder’s meeting.

Leverage

1.0%

99.0%

USD

MXN

60

Financial Ratios (million MXN)

Fuente: OMA UAFIDA Ajustada excluye provisión de mantenimiento, ingreso y costo de construcción. Deuda a corto plazo= prestamos a corto plazo + porción circulante del pasivo a largo plazo Deuda a largo plazo = deuda a largo plazo Deuda total = deuda a largo plazo + deuda a corto plazo Deuda neta = deuda total – efectivo y equivalentes de efectivo

Fuente: OMA

Debt Composition 2012

2011 2012

Cash and cash equivalents 524 1,152

Short term debt 29 584

Long term debt 1,535 1,510

Total debt / Adjusted EBITDA 1.3x 1.38x

Net debt / Adjusted EBITDA 0.83x 0.62x

Adjusted EBITDA/ Interest 12.7x 14.6x

Total debt/ Total assets 17% 21%

Sound Balance Sheet

Fuente: OMA Nota: nivel de caja mínimo MXN$150mm Deuda total incluye deuda de corto plazo e interés devengados no pagados

2012 debt break-down (mdp) Net debt / Adjusted EBITDA

Fuente: OMA

-1.8 -1.7

-0.1

0.4 0.8 0.8 0.6

2006 2007 2008 2009 2010 2011 2012

2,095 1,152

942

Total Debt Cash Net Debt

61

Debt /EBITDA Comparables

Debt /EBITDA Comparables

Fuente: Últimos reportes Financieros de cada compaña, calculados en moneda local OMA UAFIDA Ajustada.

-0.03 -0.55

1.33 2.04 2.14 2.33 3.69 3.34 4.97

2.24 4.13

3.09

7.00 7.33

14.37 Net debt /EBITDA Average 3.07x

GAP aquired additional debt of 287.8 million pesos in december 2012 that is not considered for being 3Q 2012 numbers.

Possilbe additional debt for ASUR of 410 mdd.

AENA’s ratio is GROSS DEBT/EBITDA. It’s shown as a reference and is not included in the average.

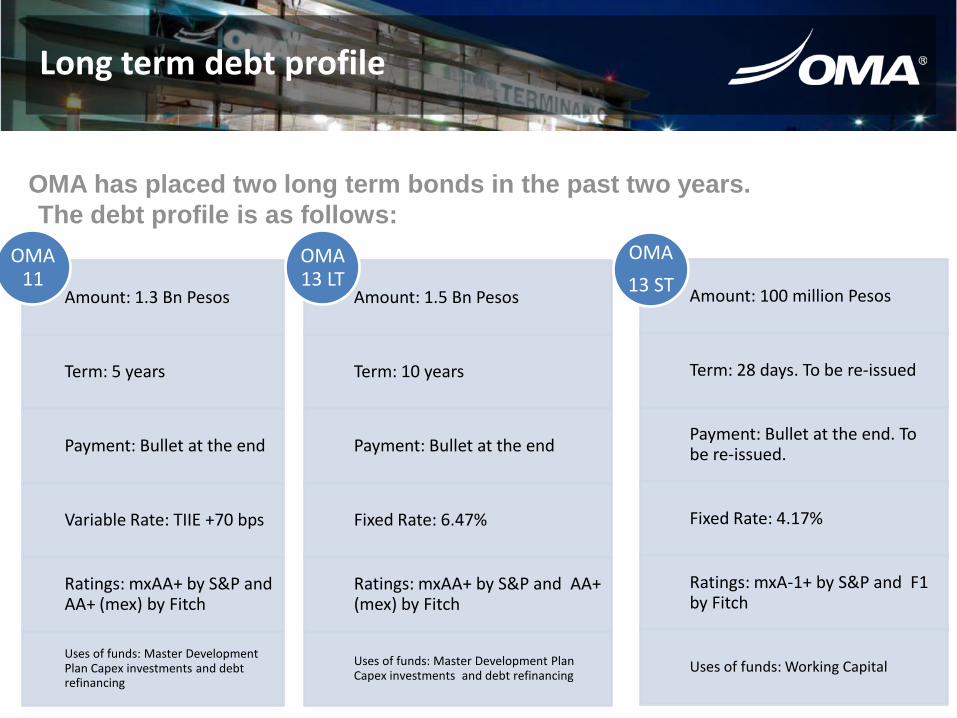

Long term debt profile

Amount: 1.3 Bn Pesos

Term: 5 years

Payment: Bullet at the end

Variable Rate: TIIE +70 bps

Ratings: mxAA+ by S&P and AA+ (mex) by Fitch

Uses of funds: Master Development Plan Capex investments and debt refinancing

OMA11

Amount: 1.5 Bn Pesos

Term: 10 years

Payment: Bullet at the end

Fixed Rate: 6.47%

Ratings: mxAA+ by S&P and AA+ (mex) by Fitch

Uses of funds: Master Development Plan Capex investments and debt refinancing

OMA13 LT

Amount: 100 million Pesos

Term: 28 days. To be re-issued

Payment: Bullet at the end. To be re-issued.

Fixed Rate: 4.17%

Ratings: mxA-1+ by S&P and F1 by Fitch

Uses of funds: Working Capital

OMA

13 ST

OMA has placed two long term bonds in the past two years.

The debt profile is as follows:

Macroeconomic Factors to take into

account

Bullish Mexican Outlook on Internal & External Factors

64

2

Factores Internos Positivos Factores Externos Positivos

1

3

4

5

6

1

2

3

Low Debt Leverage and Low Fiscal Deficit

Healthy Banking System

Trade Openness

Population Demographics

Economic and Employment Growth-Oriented Government

Macroeconomic Stability

Global Economic Recovery Increases Mexican Exports

Higher Remittances due to an Expected US Housing Recovery

Growing amount of Foreign Direct Investment (“FDI”) as Mexico increases even more its importance as North America’s key manufacture hub

65

Young Population with an Average of 27 years.

Demographic bonus

US$ per Hour ULC (1Q 2006=100, US$, 5QMA)

Favorable macroeconomic and demographic factors

0.0

0.5

1.0

1.5

2.0

2.5

2003 2004 2005 2006 2007 2008 2009 2010 2011

Mexico China

____________________

Source: BofAML Research, Bloomberg, INEGI and Banxico.

Ag

e

The gap in unit labor costs between Mexico and China

has been closing. Mexico consolidates as manufacturing

HUB

66

Growth potential in the sector

Source: Secretaria de Comunicaciones y Transportes

Source: Economist Intelligence Unit Source: Airbus (Market Analysis)

Source: Airbus Market analysis, CIA World Factbook y World Economic Forum Global Competitiveness Report

Source: Airbus Market analysis, CIA World Factbook y World Economic Forum Global Competitiveness Report

Bus - Economy 59.0%

Air 1.6%

Bus – Luxury and first class

20.6%

Train traffic 0.9%

Sea traffic 0.4%

Bus - Tourist 17.5%

Anual expected Population Growth (%) Compound Anual Growth Rate for Domestic traffic ,

2012-2031

Flights per Capita (Anual Average)

Available Seats per Km per Capita

Traffic in Mexico by travel type

Annex

Proposed new routes

Monterrey

Zacatecas

Puebla

Durango

Chicago

Morelia San Luis Potosí

Torreón Miami

Los Angeles

Cancún

Veracruz

Proposed routes for Aeromexico 8 routes proposed for 2013

Current propose routes

New routes 2012

New frequencies 2012

Proposed new routes

Proposed routes for

Vivaaerobus 7 routes proposed for 2013

Torreón

Reynosa

Tampico

México

Guadalajara

Chihuahua

Ciudad Juárez

Monterrey

Cuernavaca

Mazatlán

Bajío

Tuxtla Gutierrez

Tijuana

Cancún

Zacatecas

Acapulco

Culiacán

Mexicali

Demand elasticity continues to be strong in the air transport industry, we are seeking to grow in markets like CUL-MXL, MEX-ZCL, TAM-CUN.

Current propose routes

New routes 2012

New frequencies 2012

Proposed routes for Interjet 25 routes proposed for 2013

Monterrey

México

Tijuana

Cancún

Cd. Juárez

Torreón

Chihuahua

Mazatlán

San Luis Potosí

Zacatecas

Zihuatanejo

Guadalajara

Los Angeles

Mexicali

Culiacán Miami

San Antonio

Mérida

Villahermosa

Huatulco

Los Cabos

La Habana

Proposed new routes

Sukoi Superjet 100 permits to operate an important combination of regional routes.

Current proposed routes

New routes 2012

Proposed new routes

Guadalajara

Culiacán

Los Ángeles

Mexicali

Cancún

Tijuana

Chihuahua

Ciudad Juárez

Durango Mazatlán

México

Torreón Monterrey

Hermosillo

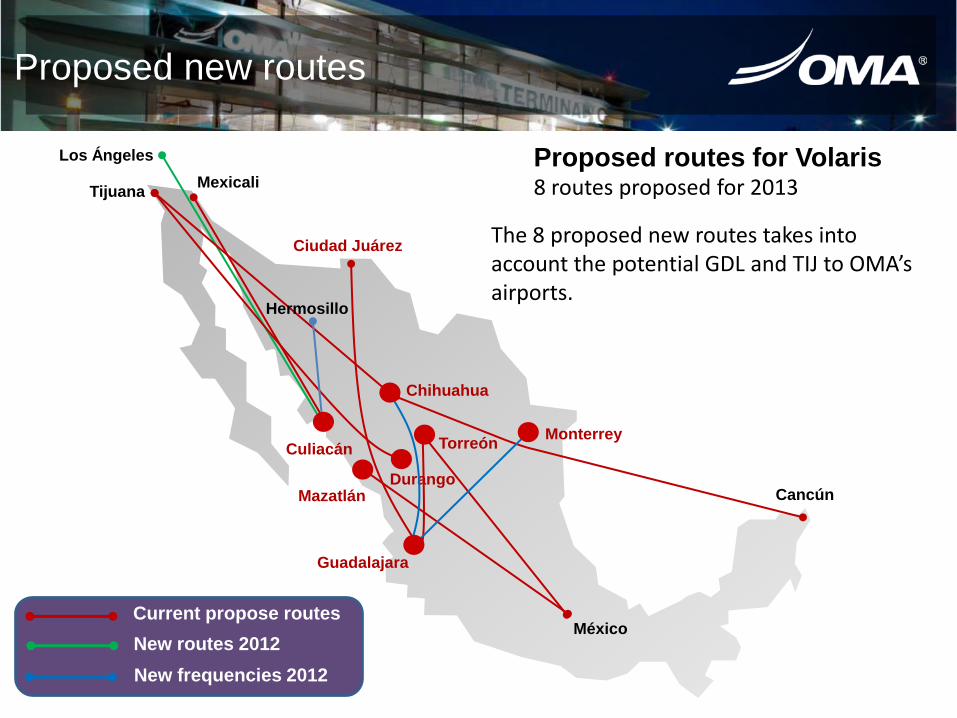

Proposed routes for Volaris 8 routes proposed for 2013

The 8 proposed new routes takes into account the potential GDL and TIJ to OMA’s airports.

Current propose routes

New routes 2012

New frequencies 2012

Proposed new routes

Torreón

Reynosa

Tampico

San Luis Potosí

Cd. Victoria

Harlingen

Guadalajara

Chihuahua

Ciudad Juárez

Zihuatanejo

Proposed routes for Aeromar 6 routes proposed for 2013

ATR42 planes allow to work with a limited market like the routes TAM-REX, REX-CVM o SLP-CUU-CJS.

Current proposed routes

New routes 2012