Embed Size (px)

Citation preview

Fourth Quarter & FY 2017Earnings ReviewTodd Stevens | President & CEO | Los Angeles, CA | February 26, 2018

Mark Smith | Sr. EVP & CFO

4Q & YE 2017 Earnings | 2

Forward Looking / Cautionary Statements

This presentation contains forward-looking statements that involve risks and uncertainties that could materially affect our expected results of operations, liquidity, cash flows and

business prospects. Such statements include those regarding our expectations as to our future:

Actual results may differ from anticipated results, sometimes materially, and reported results should not be considered an indication of future performance. While we believe

assumptions or bases underlying our expectations are reasonable and make them in good faith, they almost always vary from actual results, sometimes materially. We also believe third-

party statements we cite are accurate but have not independently verified them and do not warrant their accuracy or completeness. Factors (but not necessarily all the factors) that

could cause results to differ include:

Words such as "anticipate," "believe," "continue," "could," "estimate," "expect," "goal," "intend," "likely," "may," "might," "plan," "potential," "project," "seek," "should," "target, "will" or "would"

and similar words that reflect the prospective nature of events or outcomes typically identify forward-looking statements. Any forward-looking statement speaks only as of the date on

which such statement is made and we undertake no obligation to correct or update any forward-looking statement, whether as a result of new information, future events or otherwise,

except as required by applicable law.

See www.crc.com Investor Relations for important information about 3P reserves and other hydrocarbon resource quantities, finding and development costs, recycle ratio calculations,

and drilling locations.

• financial position, liquidity, cash flows and results of operations

• business prospects

• transactions and projects

• operating costs

• Value Creation Index (VCI) metrics are based on certain estimates

including future production rates, costs and commodity prices

• operations and operational results including production, hedging and capital

investment

• budgets and maintenance capital requirements

• reserves

• type curves

• commodity price changes

• debt limitations on our financial flexibility

• insufficient cash flow to fund planned investment

• inability to enter desirable transactions including asset sales and joint

ventures

• legislative or regulatory changes, including those related to drilling,

completion, well stimulation, operation, maintenance or abandonment of

wells or facilities, managing energy, water, land, greenhouse gases or

other emissions, protection of health, safety and the environment, or

transportation, marketing and sale of our products

• unexpected geologic conditions

• changes in business strategy

• inability to replace reserves

• insufficient capital, including as a result of lender restrictions, unavailability

of capital markets or inability to attract potential investors

• inability to enter efficient hedges

• equipment, service or labor price inflation or unavailability

• availability or timing of, or conditions imposed on, permits and approvals

• lower-than-expected production, reserves or resources from development

projects or acquisitions or higher-than-expected decline rates

• disruptions due to accidents, mechanical failures, transportation or storage

constraints, natural disasters, labor difficulties, cyber attacks or other

catastrophic events

• factors discussed in “Risk Factors” in our Annual Report on Form 10-K

available on our website at crc.com.

4Q & YE 2017 Earnings | 3

Key Highlights

618 MMboe119% Organic Reserve

Replacement Ratio

$761 Million

$429 Million$96 Million Funded by BSP

$58 Million Funded by MIRA

9 Drilling RigsSustainable Level of Activity

Capital

Adjusted EBITDAX*

ACTIVITY

PRODUCTION & RESERVES

*See www.crc.com, Investor Relations for a reconciliation to the closest GAAP

measure and other important information.

4th Quarter 2017

Program VCI* of 1.7229 Gross Wells Drilled & 460

Capital Workovers

$222 Million

$159 Million$14 Million Funded by BSP

$20 Million Funded by MIRA

1.5%Q-o-Q Production Decline

126 MBoe/d

4Q & YE 2017 Earnings | 4

Drilling

28%

Workover

20%BSP JV

Capital

26%

Exploration

2%

Other1

7%

Development

Facilities

16%

Moved from Defense to Offense – 2017 Review

• CRC 2017 capital plan was directed to oil-weighted projects in our core fields: Elk Hills, Wilmington, Kern Front, Buena Vista, Mt. Poso, Pleito

Ranch, Wheeler Ridge and the delineation of Kettleman North Dome

• JV capital was primarily focused in the San Joaquin Basin

2017 Capital Investment Program Summary

Total: $371 million

1Other includes maintenance and occupational health, safety and environmental projects, seismic and other investments.2Facility Costs and other non-return capital are apportioned to producing wells in the year they are drilled.

2017 Total Capital Invested

1.70

2.00

30%

45%

0%

10%

20%

30%

40%

50%

0.00

0.50

1.00

1.50

2.00

2.50

$55 Brent Flat

$3 NYMEX

$55 Brent 2017, $65 Brent

in 2018+ & $3 NYMEX

IRR

VC

IVCI IRR

Results of Fully-Burdened2

2017 CRC Development Program

Total: ~$240 million

Other1

4Q & YE 2017 Earnings | 5

Drilling

JV - Capital

Workover

Development

Facilities

ExplorationOther1Other1

San

Joaquin

Ventura

Los

Angeles

Production Enhancement Plans for 2018

• CRC 2018 capital plan will be directed to oil-weighted projects in our core fields: Elk Hills,

Wilmington, Kern Front, Huntington Beach, and continued delineation of Kettleman North

Dome and Buena Vista

• JV capital will be focused in the San Joaquin Basin and Huntington Beach

• We have a dynamic plan that can be scaled up or down depending on the price environment

and efficient deployment of joint venture proceeds

Capital Investment Program – Living Within Cash Flow

Approx. $425 to $450 million

1Other includes maintenance and occupational health, safety and

environmental projects, seismic and other investments.

2018E Total Capital Plan 2018E Drilling Capital – By Drive

28%

30%22%

12%

4%4%

10%

10%

Conventional

ExplorationWaterfloods

Steamfloods

Unconventional

42%

6%30%

16%

80%

The JV capital increases

flexibility or provides for

incremental deleveraging

Approx. $250 million Approx. $250 million

6%

2018E Drilling Capital – By Basin

4Q & YE 2017 Earnings | 6

Deep Inventory of Actionable Projects at $65

Portfolio Spectrum

• Growth portfolio focus, fully

burdened

• All projects meet a Value

Creation Index (VCI)1

threshold of 1.3 at $65 Brent

and $3.50 NYMEX, and

deliver robust cash flow

• Portfolio has large

contributions from all

recovery mechanisms and

reserves types

• Many projects take

advantage of existing

infrastructure, while other

new projects may require

infrastructure investment in

facilities and sales points

1VCI is calculated by dividing the net present value of the project’s expected pre-tax cash flow over its life by the net present value of the investments, each using a 10% discount rate.2Full cycle costs = operating costs + development costs + facility costs + field-level G&A + taxes other than on income.3See www.crc.com, Investor Relations for details regarding net resources.

0

2

4

6

8

10

0 100 200 300 400 500 600 700 800Deve

lop

me

nt

Ca

pit

al (B

$)

Net Resources3 (MMBoe)

0

5

10

15

20

25

30

35

40

45

50

0 100 200 300 400 500 600 700 800

Fu

ll C

ycle

Co

st2

($/B

oe

)

Net Resources3 (MMBoe)

4Q & YE 2017 Earnings | 7

70

80

90

100

110

120

130

140

2017 2018E 2019E 2020E 2021E

Oil P

rod

ucti

on

MB

/d

400

800

1,200

1,600

2,000

2017 2018E 2019E 2020E 2021E

EB

ITD

AX

$M

M

Portfolio Flexibility Provides Range of Crude Oil Scenarios

Note: Scenarios assume flat pricing from $55 to $75 Brent and $3.00 to $3.10 NYMEX gas, respectively. Assumes lease operating costs are equal to 2017 levels for the mid-point of the range of planning scenario outcomes. Ranges of portfolio planning scenario outcomes assume development of a variety of combinations of steamflood, waterflood, conventional and unconventional projects in our inventory and reflect estimates of geologic, development and permitting risk. All discretionary cash flow reinvested in business for each scenario. * See www.crc.com Investor Relations for a description of the calculation of debt-adjusted per share and other important information.

Combined with mid-cycle commodity

prices, we are positioned for growth in:

• Cash flow

• Production

• Reserves

on a debt-adjusted per share basis*

Portfolio

Planning

Scenarios

Portfolio

Planning

Scenarios

Capital focused on oil projects that provide

Increasing

Margins

Low

Decline Rates

Compounding

Cash Flow+ =

-

-

Estimated Crude Oil Production Outcomes

Estimated Range of EBITDAX Outcomes

≈

≈

0

300

600

900

1,200

1,500

2017 2018E 2019E 2020E 2021E

Ca

pit

al ($

MM

)

Estimated Ranges of Capital Investments

4Q & YE 2017 Earnings | 8

Resilient Resource Base

0

25

50

75

100

125

150

175

200

0

20

40

60

80

100

120

140

160

180

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 FY

2015

FY

2016

FY

2017

Ca

pit

al ($

MM

)

MB

oe

/d

)

Oil NGL Gas Capital

Production By Stream (Mboe/d)

Note: Capital and production for 2017 include BSP’s investment and exclude MIRA’s investment.

Total Capital: $75MM$401MM $371MM

4Q & YE 2017 Earnings | 9

Nimble Operations Enable Flexibility to Improve Margins

$-

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17 3Q 17 4Q 17

$/B

oe

Operating Cash Margin = Oil and Gas Revenue excluding settled hedges – LOE – Taxes Other than on Income – Operating Overhead.

Margin expansion into

mid-cycle pricing

4Q & YE 2017 Earnings | 10

FY14 FY15 FY16 FY17

0

400

800

1,200

1,600

2,000

2,400

2,800

An

nu

al

($M

M)

Adj. EBITDAX Operating Cash Flow Capital Investment

Living Within Cash Flow

1 See www.crc.com, Investor Relations for a reconciliation to the closest GAAP measure and other important information.2 Does not include JV capital.3 FY17 Capital Investment includes $27mm in Changes in Capital Accruals

1 2

3

4Q & YE 2017 Earnings | 11

$3.26 $3.14 $2.95 $3.00

$2.75 $2.42

$3.09

$2.90

$2.47 $2.56 $2.77 $2.66

$2.28 $2.67

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1Q 2017 2Q 2017 3Q 2017 4Q 2017 2015 2016 2017

$/

Mc

f

NYMEX Realizations

CRC – Price Realizations

66% 62%

72%79%

40%

52%

70%

63%59%

66%

72%

37%

50%

65%

0%

20%

40%

60%

80%

100%

1Q 2017 2Q 2017 3Q 2017 4Q 2017 2015 2016 2017

% o

f W

TI

& B

ren

t

WTI Brent

$51.91

$48.29

$48.21

$55.40

$48.80 $43.32

$50.95

$50.24 $47.98

$50.02

$56.92

$49.19

$42.01

$51.24

$54.66 $50.92

$52.18

$61.54

$53.64

$45.04

$54.82

30

40

50

60

70

1Q 2017 2Q 2017 3Q 2017 4Q 2017 2015 2016 2017

$/B

bl

WTI Realizations Brent

Realization %

of WTI97% 99% 104% 103% 101% 99% 101%

Realization %

of NYMEX89 % 79% 87% 92% 97% 94% 86%

Oil Price Realization (with Hedges) Gas Price Realization

NGL Price Realization - % of WTI & Brent

CRC believes near-term

differentials will remain strong

• California refinery demand for native crude continues to be strong

and reduction in heavy waterborne crude has positively

influenced differentials.

• NGL prices have been supported by lower inventories and export

markets.

-≈

4Q & YE 2017 Earnings | 12

CRC Benefitted from Price and Managed Controllables in Q4

130

248

-100

-50

0

50

100

150

200

250

300

350

400

4Q16 Volume Price Costs Interest

Working

Capital and

Other 4Q17($

MM

)

Op

era

tin

g C

ash

Flo

w

4Q & YE 2017 Earnings | 13

$100

$100

$193

$2,250

$1,000

$1,300

$0$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun

-18

Se

p-1

8

De

c-1

8

Ma

r-1

9

Jun

-19

Se

p-1

9

De

c-1

9

Ma

r-2

0

Jun

-20

Se

p-2

0

De

c-2

0

Ma

r-2

1

Jun

-21

Se

p-2

1

De

c-2

1

Ma

r-2

2

Jun

-22

Se

p-2

2

De

c-2

2

Ma

r-2

3

Jun

-23

Se

p-2

3

De

c-2

3

Ma

r-2

4

Jun

-24

Se

p-2

4

De

c-2

4

2014 RCF

2017 Term Loan

2016 Term Loan

2nd Lien Notes

Unsecured Notes

Strengthening the Balance Sheet - Improved Creditworthiness and Liquidity

• Pro forma net results from the Ares transactions which closed on February 7, 2018:

• The RCF was paid in full

• CRC received $797 million in net proceeds, $8mm of which is restricted cash

• The RCF has approximately $850 million of available borrowing capacity, excluding

$150 million minimum liquidity

• The recent amendment extends the maturity of the RCF to June 2021 and relaxes

financial covenants

1st Lien 2014 Revolving Credit Facility (RCF) -

1st Lien 2017 Term Loan 1,300

1st Lien 2016 Term Loan 1,000

2nd Lien Notes 2,250

Senior Unsecured Notes 393

Total Debt 4,943

Less cash2

(441)

Total Net Debt 4,502

Equity3

(764)

Total Net Capitalization 3,738

Total Net Debt / Total Net Capitalization 120%

Total Net Debt / LTM Adjusted EBITDAX4

5.9x

LTM Adjusted EBITDAX4

/ LTM Interest Expense 2.2x

PV-105 / Total Net Debt 1.0x

Total Net Debt / Proved Reserves ($/Boe) $7.28

Total Net Debt / Proved Developed Reserves ($/Boe) $10.23

Total Net Debt / 2017 Production ($/Boepd) $34,899

Pro-Forma1 Capitalization ($MM)

Pro-Forma1 Debt Maturities ($MM)*

1 Pro-forma capitalization table and debt maturities graph reflect the payoff of the 12/31/17 outstanding balance

of $363 million on our RCF after the completion of the Ares JV and $50 million private placement. 2 The $441 million of available cash includes (1) $15 million unrestricted cash as of 12/31/17 and (2) $426

million of available cash after the Ares transaction and proforma repayment of the RCF.3 Excludes noncontrolling interest at 12/31/17 and includes $50 million of equity from the Ares private placement.4 See www.crc.com, Investor Relations for a reconciliation to the closest GAAP measure and other important

information.5 PV-10 as of 12/31/17, see Attachment 2 of CRC’s Fourth Quarter Earnings Release from February 26, 2018 for

details on this calculation.

* Previously, the RCF, the 2017 Term Loan and the 2016 Term Loan were subject to springing maturities related to the 2020

and 2021 Notes. During the fourth quarter of 2017, CRC repurchased $65 million in principal amount of the 2020 Notes and

$35 million in principal amount of the 2021 Notes, which eliminated the springing maturity feature. The 2017 Term Loan also

has a springing maturity related to the 2016 Term Loan.

Undrawn RCF

4Q & YE 2017 Earnings | 14

PDP Value

Proved Value

Unproved4

$0

$4

$8

$12

$16

$20

$24

$55 Brent $65 Brent $75 Brent

($B

illio

n)

2017 Reserves Value1 In Excess EV

Current EV

of $6.4 Bn5

Infrastructure2

Surface & Minerals3

1-5 See endnotes in the Appendix.

See www.crc.com Investor Relations for important information about 3P reserves and other hydrocarbon quantities.

4Q & YE 2017 Earnings | 15

Strategy at a Glance

Value Directed Investments

Targeting Balance Sheet Leverage 2x-3x (mid-cycle)

Value

Focus

Live within

Cash Flow

Smart Growth

(per share)

PV10 pre-tax cash flows

PV10 of investmentsVCI =

Value Creation Index (VCI)

Enhance Production

Deliver Margin Expansion

Live within Cash Flow

Long-TermShort-Term

4Q & YE 2017 Earnings | 16

Diverse Assets with Flexible Development Opportunities

BasinNet Proved Reserves

(MMBOE)Avg. Net

Production (MBOE/d)

% Oil Production

Net Mineral Acreage

(million acres)

Identified GrossDrilling Locations2

Drive Mechanisms Competitive Advantage

618 129 64 ~2.3 33,870 Portfolio Flexibility

San Joaquin 419 90 58 1.5 25,190Big fields get bigger,

substantial infrastructure in place

Los Angeles 145 27 100 <0.1 1,950World class waterfloods,

cash flow positive

Ventura 40 6 67 0.2 4,310Upside from the

application of technology

Sacramento 14 6 0 0.5 2,420 Large, scalable

• World-class resource base that is positioned to grow

• Utilizing current costs, the SEC 2017 price deck1, PV-10 of proved reserves of $4.5 BN or $8.9 BN for proved, probable and possible reserves2

• Achieved 2017 organic recycle ratio2 of 2.1x

Drive Mechanisms: Conventional Unconventional Steamflood Waterflood Gas

1 Assumes a flat $54.98 Brent crude price deck and $2.98/MMBTU NYMEX natural gas and utilizes current costs.2 See www.crc.com Investor Relations for important information about 3P reserves and other hydrocarbon quantities. Drilling locations exclude

6,400 gross exploration locations related to unconventional reservoirs.

Figures shown are for full-year 2017, unless otherwise noted.

4Q & YE 2017 Earnings | 17

Life of Field Plans – Growing Inventory

• Comprehensive technical review of 40% of CRC’s fields

• Updated Geologic models, OOIP

• Teams shared analog experience across CRC

• Cataloged opportunities consistent with our proven reserves methodology

• Rolled into our portfolio ranking process

• Over 95% of our total proved reserves have been audited by Ryder Scott in the last three years

3P Reserves Growth

58 109 156

768 644 568618

222 251202

321

340

826

1,129

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

Spin-off 2015 2016 2017

MM

Bo

e

Cummulative Production Proven

Revisions Due to Price Since 2014 Unproven

>350%

Growth

See www.crc.com Investor Relations for important information about 3P reserves and other hydrocarbon quantities.

4Q & YE 2017 Earnings | 18

2017 Proved Reserves Increased with Minimal Investments

568618

300

350

400

450

500

550

600

650

Balance

as of

12/31/16

Production Performance

Related

Revisions

Extensions

and

Discoveries

Sales of

Proved Reserves

Price Related

Revisions

Balance

as of

12/31/17

Pro

ved

Re

se

rve

s (

MM

BO

E)

-≈

4Q & YE 2017 Earnings | 19

Margin Expansion Driven by Liquid-Rich Resource Base

• As we develop our reserves we anticipate the oil weight of production to trend from 64% produced in 2017 toward the 72% reflected in our 2017 Proved Reserves

• The 2017 average blended realized price of $41 per BOE was 75% of the average Brent Crude index

0%

25%

50%

75%

FY 2015 FY 2016 FY 2017 2017

Reserves

% O

il M

ix

Oil NGL Gas Blended

Realized Price*

2017 Production Mix 64% 12% 24% $41.09

2017 Proved Reserves

Mix72% 9% 19%

*Includes effects of settled hedges

4Q & YE 2017 Earnings | 20

CRC Midstream JV Structure with Ares

California Resources Elk

Hills, LLC

Elk Hills Power, LLC

Contributed

Assets

$750 MM gross proceeds

Class A (50%) and

Class C (95.25%)

Common Interests

Power and

Gas Processing

Services

Commercial Agreement

Capacity Charges

Ares Management, L.P. $750 MM gross

proceeds

Class B Preferred Interests, Class A and Class C

Common Interests

Benefits• Strategic alignment with Ares

• Provides CRC paths for opportunistic deleveraging through cash flow growth or debt reduction

• Greatly enhances liquidity

• Retain ownership and operational control

• Defined exit criteria

4Q & YE 2017 Earnings | 21

Strategic Partner Alignment

Summary of Deal

Partner ▪ Affiliate of Ares Management (Ares)

Contributed

Assets▪ Elk Hills power plant, gas processing assets and related non-borrowing base

infrastructure currently owned by CRC

Midstream JV

Capitalization

▪ Class A common interests (voting) owned 50% by Ares and 50% by California

Resources Elk Hills (CREH)

▪ Class B preferred interests (“Preferred”) owned 100% by Ares

▪ Class C common interests (distributing) owned 95.25% by CREH and 4.75% by Ares

Distribution to

Partners

▪ Preferred interests to receive distributions of 13.5% per annum on the $750 MM

contributed amount

▪ 9.5% cash pay and 4.0% PIK to be deferred for the first three years

▪ Deferred distributions are interest bearing and repaid over two years following the

deferral period

▪ Remaining cash after preferred distributions to be distributed pro rata to Class C

interests

Exit Provisions

▪ Prior to end of 5 or 7.5 years, CRC may redeem Preferred at variable amounts that

include make whole premiums

▪ At end of 5 years, CRC may elect to either redeem or extend to 7.5 years

▪ At 7.5 years, if not redeemed by CRC, Preferred can monetize the JV

Board▪ Board of Managers to consist of three CRC representatives and three

representatives from Ares

4Q & YE 2017 Earnings | 22

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

0% 10% 20% 30% 40% 50%

PR

OJE

CT V

CI

DISCOUNT ON SECOND LIEN NOTES

PROJECT VS. SECOND LIEN (2L) NOTE REPURCHASE*

INVEST If the VCI of an investment opportunity falls above the indifference

curve, investing in the new project could be a better option

PURCHASE DEBTIf the VCI of an investment opportunity falls below the indifference curve, repurchasing 2L notes could be a better option

Example of Investment Alternatives for Asset Sale Proceeds

Per the terms of the 2014 credit agreement on

asset sales, 2L notes must be repurchased at a

minimum 20% discount to par

Indifference Curve

*CRC will continue to review all opportunistic debt reduction transactions. We utilize our Value Creation Index (“VCI”) to guide management in allocating capital and prioritizing investments.

4Q & YE 2017 Earnings | 23

1Q 2018 2Q 2018 3Q 2018 4Q 2018 1Q 2019

Sold Calls Barrels per Day 9,000 6,200 16,100 16,100 1,100

Weighted Average Ceiling

Price per Barrel$59.58 $60.24 $58.91 $58.91 $60.00

Purchased Calls Barrels per Day - - - - 2,000

Weighted Average Ceiling

Price per Barrel- - - - $71.00

Purchased Puts Barrels per Day 1,200 1,200 6,100 1,100 14,100

Weighted Average

Floor Price per Barrel$45.82 $45.83 $61.48 $45.85 $58.93

Sold Puts Barrels per Day 29,000 29,000 24,000 19,000 10,000

Weighted Average

Floor Price per Barrel$45.00 $45.00 $46.04 $45.00 $47.50

Swaps Barrels per Day 38,300 34,000 19,000 19,000 7,000

Weighted Average

Price per Barrel$60.03 $60.00 $60.13 $60.13 $67.71

Percentage of 4Q 2017

Oil Production Hedged*49% 44% 31% 25% 26%

Opportunistically Built Oil Hedge Portfolio

Certain of our counterparties have options to increase swap volumes at weighted average costs between $60 and

$70 Brent.. For potential volume changes and further details please see Attachment 10 of our Earnings Release.

* Assumes counterparty options are not exercised.

We target hedges

on 50% of crude

oil production

Strategy Protect cash flow for capital investments and covenant compliance

4Q & YE 2017 Earnings | 24

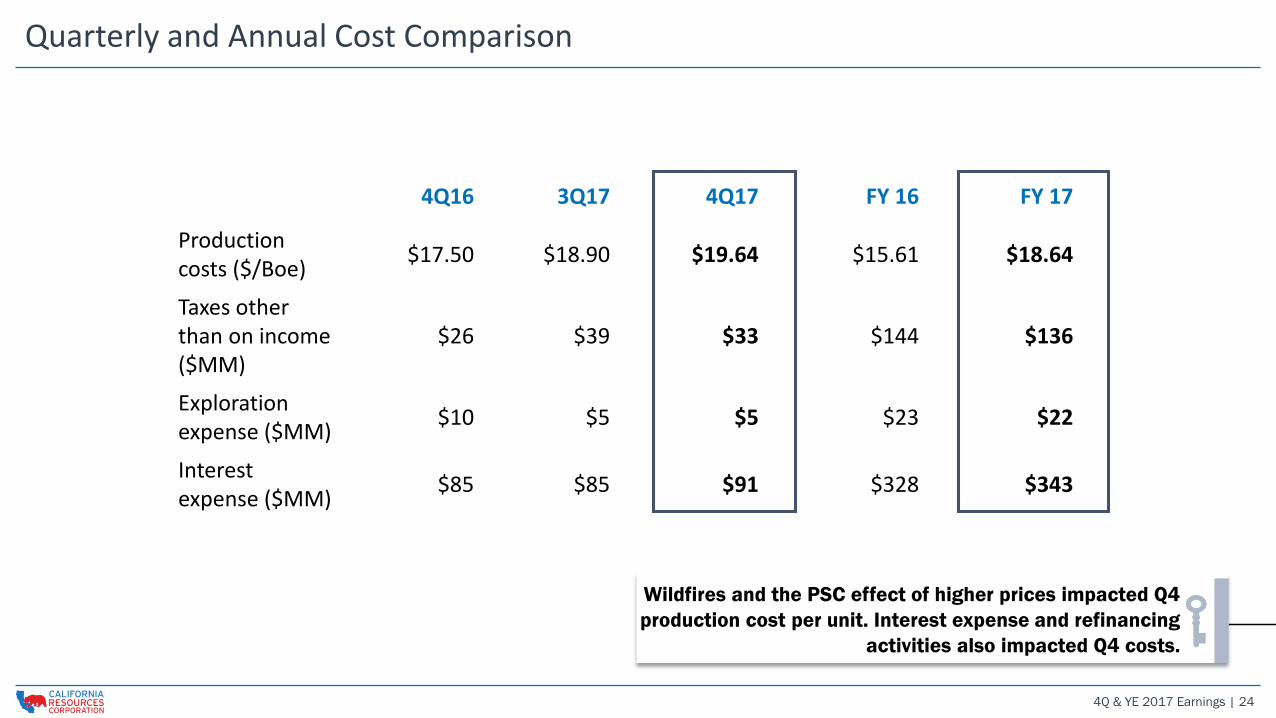

Quarterly and Annual Cost Comparison

4Q16 3Q17 4Q17 FY 16 FY 17

Productioncosts ($/Boe)

$17.50 $18.90 $19.64 $15.61 $18.64

Taxes other than on income ($MM)

$26 $39 $33 $144 $136

Exploration expense ($MM)

$10 $5 $5 $23 $22

Interest expense ($MM)

$85 $85 $91 $328 $343

Wildfires and the PSC effect of higher prices impacted Q4

production cost per unit. Interest expense and refinancing

activities also impacted Q4 costs.

4Q & YE 2017 Earnings | 25

4Q17 Results Summary

4Q16 3Q17 4Q17

Net Loss Attributable to Common Stock Per Share

($1.83) ($3.11) ($3.23)

Adjusted Net Loss Per Share* ($1.76) ($1.22) ($0.33)

Oil Production 87 MBbl/d 82 MBbl/d 80 MBbl/d

Total Production 135 MBoe/d 128 MBoe/d 126 MBoe/d

Realized Oil Price w/ Hedge ($/Bbl) $45.48 $50.02 $56.92

Realized NGL Price ($/Bbl) $28.99 $34.63 $44.03

Realized Natural Gas Price ($/Mcf) $2.79 $2.56 $2.77

Net Loss Attributable to Common Stock ($77 mm) ($48 mm) ($138 mm)

Adjusted EBITDAX* $168 mm $181 mm $222 mm

Capital Investments $31 mm $100 mm** $139 mm

Cash Flow from Operating Activities ($15 mm)*** $105 mm $23 mm* See www.crc.com Investor Relations for a reconciliation to the closest GAAP measure and other important information.

** Capital Investments include BSP Capital but exclude MIRA Capital.

*** Operating cash flow includes a semi-annual cash property tax payment.

4Q & YE 2017 Earnings | 26

1Q18 Guidance

Anticipated Realizations Against the Prevailing Index Prices for 1Q18

Oil 92% to 96% of Brent

NGLs 62% to 66% of Brent

Natural Gas 88% to 92% of NYMEX

Production, Capital and Income Statement Guidance

Production 120 to 125 Mboe/d

Capital $115 to $135 million

Production Costs $19.25 to $20.75 per Boe

Adjusted G&A $6.05 to $6.35 per Boe

DD&A $10.50 to $10.80 per Boe

Taxes other than on income $36 to $40 million

Exploration expense $6 to $10 million

Interest expense $89 to $93 million

Cash Interest $58 to $62 million

Income tax expense rate 0%

Cash tax rate 0%

4Q & YE 2017 Earnings | 27

History of Proactive Strategic Decisions

Swift, decisive actions through the commodity downturn have positioned CRC for growth. Proactive discussions with

lenders and solid asset base provide a path to recovery and an actionable inventory.

0

5

10

15

20

25

30

$0

$20

$40

$60

$80

$100

$120

07/06/14 10/06/14 01/06/15 04/06/15 07/06/15 10/06/15 01/06/16 04/06/16 07/06/16 10/06/16 01/06/17 04/06/17 07/06/17 10/06/17 01/06/18

CR

C D

rillin

g R

ig C

ou

nt

Bre

nt

Cru

de

Oil P

rice

($

/B

bl)

*

Oil Price

CRC Rig Count

1. Cut rig count/began hedging 4. Deleveraging Transactions

2. Cut 2015 Capital Budget 5. Increasing activity, invest within Cash Flow

3. Bank Amendments 6. JV Transactions

2

1

5

3Under

OXY

6

SPIN-OFF

3

3

333

44

4

4

6

63

4Q & YE 2017 Earnings | 28

The Case for CRC: Investment Thesis Overview

Grow within

cash flow

Industry leading

decline rate

Integrated and

complementary

infrastructure

Maintain

Production

Production and

Cash Flow Growth

Production Innovation Deep Inventory

Investment Case for CRC

World-class assets

with significant

inventory

Resilient model that

preserves optionality

and protects downside

Focused on value

and poised for

growth

Moved from defense to offense

Why Own CRC Now

Competitive Advantages

Disciplined portfolio management Potential for EBITDAX growth

0

400

800

1,200

1,600

2,000

2,400

2,800

2017 2018E 2019E 2020E 2021E

$M

M

Clear runway and

available cash

-

Appendix

4Q & YE 2017 Earnings | 30

2014 Revolving Credit Facility Capacity -$1 billion

Updated Capital Structure from Recent Transactions – Improved Liquidity

2017 Term Loan - $1.3 billion

2016 Term Loan - $1 billion

2015 Second Lien - $2.25 billion

Unsecured Notes - $0.393 billion

Drawn Revolver

$837

$0

$250

$500

$750

$1,000

3Q17 PF 4Q17*

($M

M)

Revolver

Availability

$431

Revolver

Availability

$850

Cash $11

Cash $441

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

3Q17 PF 4Q17*A

vaila

bilit

y ($

MM

)

Increased Liquidity**

* Pro Forma for the Ares JV and $50mm private placement

** Subject to minimum liquidity requirement under 2014 Revolving Credit Facility. Includes unrestricted cash.

Reduced Revolver Borrowing

Added in NovemberD

eb

t H

iera

rch

y

Undrawn

Revolver

4Q & YE 2017 Earnings | 31

0%

10%

20%

30%

40%

50%

1 Year Decline

Median: 29%

Best In Class Corporate Decline Rates

0%

10%

20%

30%

40%

50%

60%

70%

80%

3 Year Decline

Median: 49%

CRC

CRC

Peers included: CLR, COG, CPE, CXO, DNR, EGN, EOG, EPE, FANG, HK, LPI, MRO, MTDR, MUR, NFX, OAS, PDCE, PE, PXD, QEP,RRC, RSPP, SM, SN, WLL,WPX, and XEC.

Source: Wood Mackenzie - Operated Production Data through 2016, CRC analysis.

FY 2016 Production Percentage Liquids

Less than 55% 55% - 75% Greater than 75%

4Q & YE 2017 Earnings | 32

Significant Reduction in Net Debt from Post-Spin Peak

6,7651

4,502

3,000

4,000

5,000

6,000

7,000

2Q15 Debt Exchange for

2L

Open Market

Repurchases

Equity for Debt

Exchange

Cash Tender

for Unsecureds

Cash Flow Ares Transactions PF 4Q17

Tota

l N

et

De

bt

($ M

M)

2

Cumulative Debt Reduction Total

Total Net Principal Reduction$535

million

$153

million

$102

million

$625

million

$59

million

$789

million$2,263 million

1 Represents mid-second quarter 2015 peak debt.2 Includes operating cash flow, positive working capital and proceeds from asset sales in 1H 2017, net of restricted cash.3 Pro Forma net debt at 4Q17 includes the payoff of the 12/31/2017 outstanding balance of $363 million on our RCF and $441 million of available cash after the completion of the of Ares transactions.

-

Chose options to maximize deleveraging and minimize recurring cost to the income statement on a per share basis.

Continue to seek opportunistic transactions that reduce overall debt.

3

4Q & YE 2017 Earnings | 33

End Notes

1 Current CRC estimate of reserves value as of December 31, 2017. Includes field-level operating expenses and G&A. Assumes

$3.00/MMBTU NYMEX.

2Reflects that the value of facilities and midstream assets at 50% of estimated replacement value. This discount is estimated to

exceed the burden on reserves that would be incurred if assets were monetized. Excludes the value of the assets monetized in the

Ares transaction.

3 Surface & Minerals reflect the estimated value of undeveloped surface and minerals held in fee.

4 Unproved inventory comprises risked probable and possible reserves and contingent and prospective resources. Contingent and

prospective resources consist of volumes identified through life-of-field planning efforts to date.

5 Calculated using December 31, 2017 debt at par and market cap as of February 19, 2018.

Value Creation Index (VCI) Note: VCI is calculated by dividing the net present value of the project’s expected pre-tax cash flow over its

life by the net present value of the investments, each using a 10% discount rate.