Embed Size (px)

Citation preview

1

Four Things to Know Before Purchasing Your Next Annuity

Agent Name

Annuity Doctor

State

State License Number

2

Four Important Points

1. Designating contract owner, annuitant and beneficiary

2. Bonus rates, withdrawal charges, insurance company ratings and market value adjustment

3. Annuitization4. Wealth transfer

3

1. Designating Contract Owner, Annuitant and Beneficiary

Rule 1: IRS regulations require that with any annuity, if an owner dies, the value of the contract must be distributed to the primary beneficiary.

Exception to Rule 1: If the sole primary beneficiary of the annuity is the surviving spouse of the deceased owner, then the surviving spouse may assume ownership allowing the contract to continue without interruption.

4

Most Common Designation Structure

Husband = Owner

Husband = Annuitant

Wife = Beneficiary

Children = Contingent Beneficiaries

Note: There is an important distinction between the words contingent and joint. Contingent is an alternate or secondary designation. Joint is a primary designation.

5

Husband = OwnerHusband = AnnuitantWife = BeneficiaryChildren = Contingent Beneficiaries

What happens when…Husband dies:

Wife can:

1. Take a lump sum.

2. Defer distribution for up to five years.

3. Annuitize within one year.

4. Continue contract, becoming the owner and annuitant and must name a new primary beneficiary.

Income Taxes:

If the contract continues, taxes remain deferred. If not continued, the growth portion of the contract proceeds are taxed to the wife based on her ordinary income tax rate.

Wife dies:

The contract remains intact but a new primary beneficiary must be named.

Income Taxes:

Since no distribution, no tax consequences at this point.

6

Husband = OwnerHusband = AnnuitantWife = BeneficiaryChildren = Contingent Beneficiaries

What happens when…Husband and wife die together:

Contract death benefit is divided among the children. Each child can determine if they want to:

1. Take a lump sum.

2. Defer distribution for up to five years.

3. Annuitize within one year.

4. Roll the money to a deferred “stretch annuity.”

Income Taxes: The growth portion of the contract proceeds are taxed at each child’s ordinary income tax rate.

7

Taxation Example:

Assume the beneficiary is in a combined 33% Federal and State tax bracket. The contract “basis” (owners original premium deposit) is $100,000 and the contract at time of death is worth $225,000.

Lump sum tax amount = $41,250. [$125,000 of growth * .33 = $41,250].

Annuitization: Calculate taxation using the exclusion ratio: Premium deposit ($100,000) divided by contract value ($225,000) = 44%. This means 44% of the money is not subject to taxation.

In this example 56% of each monthly annuity payment is assessed ordinary income tax at 33%. [$938 per month annuity payment of which 56% or $525 is subject to 33% tax making the annuity payment = $765 after taxes].

8

2. Bonus Rates, Withdrawal Charges, Company Ratings &

Market Value AdjustmentA better understanding of these features.

9

Bonus Rates

Some fixed-rate annuities offer high first year bonus rates.

High first year rates may come with:

Low renewal rates

Withdrawal charges that are higher or longer than normal. For example, a six year fixed-rate annuity with nine years of withdrawal charges.

The important point is studying all the contract features and determining if the bonus rate works for your particular situation.

10

Contract Example 1

Company A: 9-year fixed-rate annuity First year rate: 1.8% base + 4% bonus = 5.8% Years 2 through 6: 1.8% guaranteed Years 7 through 9: 1% minimum guaranteed Current yield to maturity: 2.24% Withdrawal Charges by year: (1@9%) (2@8%) (3@7%) (4@6%)

(5@5%) (6@4%) (7@3%) (8@2%) (9@1%) $100,000 contract worth $115,671 at 9-year maturity based on

minimum guarantees. $123,794 based on current yield to maturity. S&P company rating: A+

11

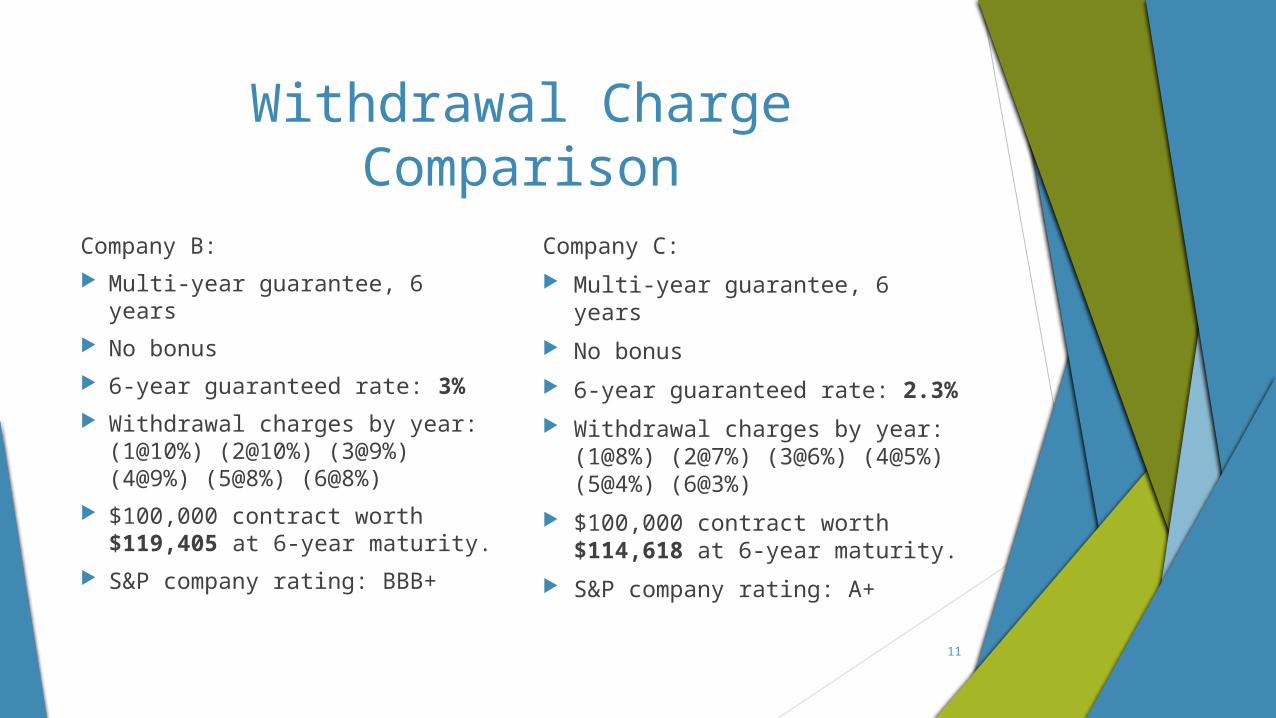

Withdrawal Charge Comparison

Company B: Multi-year guarantee, 6 years No bonus 6-year guaranteed rate: 3% Withdrawal charges by year:

(1@10%) (2@10%) (3@9%) (4@9%) (5@8%) (6@8%)

$100,000 contract worth $119,405 at 6-year maturity.

S&P company rating: BBB+

Company C:

Multi-year guarantee, 6 years

No bonus

6-year guaranteed rate: 2.3%

Withdrawal charges by year: (1@8%) (2@7%) (3@6%) (4@5%) (5@4%) (6@3%)

$100,000 contract worth $114,618 at 6-year maturity.

S&P company rating: A+

12

Insurance Company Ratings

Insurance company ratings are important, especially if you plan to put your money in the company’s hands for a long period of time.

As an independent agent I can provide for you overview reports showing the finances of the insurance companies I represent, and also those I do not represent.

American General Life Ins CoGroup Affiliation:Address:

AIG Life & Retirement GroupP.O. Box 1591Houston TX 77251

713-522-1111

Domicile:NAIC Number: Year Established: Company Type:

Assets & Liabilities

Total Admitted Assets Total Liabilities Separate Accounts Total Surplus & AVRAs % of General Account Assets

TX604881960StockPhone:

Ratings

A.M. Best Company(Best's Rating, 15 ratings)Standard & Poor's(Fin. Strength, 20 ratings) Moody's(Fin. Strength, 21 ratings)Fitch Ratings(Fin. Strength, 21 ratings) Weiss(Safety Rating, 16 ratings)

Comdex Ranking(Percentile in Rated Companies)

Invested Asset Distribution

A (3)A+ (5) A2 (6) A+ (5)C (8)

83

149,627,538138,113,05329,017,66313,923,474

11.5%

5 Year Investment Yields

5 Year AverageTotal Invested Assets 117,255,083 5.93%

Non-Performing Assets

Bonds In or Near DefaultProblem MortgagesReal Estate Acquired by ForeclosureTotal Non-Performing Assets/Surplus & AVR As a Percent of Invested Assets

Bond Quality

1.7%0.7%

1.1%

3.5%0.4%

Income & Earnings

Total IncomeNet Premiums WrittenEarnings Before Dividends and TaxesNet Operating Earnings

14,174,5887,936,9772,527,1942,405,769

A Best's Financial Strength Rating opinion addresses the relative ability of an insurer to meet its ongoing insurance obligations. It is not a warranty of a company's financial strength and ability to meet its obligations to policyholders. View our Important Notice: Best's Credit Ratings for a disclaimer notice and complete details at http://www.ambest.com/ratings/notice.

Data for Year-End 2012 from the life insurance companies' statutory annual statements. All dollar amounts are in thousands. All ratings shown are current as of April 01, 2014.Presented by: Eric Hennum, Berwick Insurance, 2393 Luberon Drive, Henderson, NV 89044 Phone: 702-350-3624 Email: [email protected]

Page 1 of 1 Powered by VitalSales Suite, a product of EbixExchange.

14

Market Value Adjustment

Some annuities include a market value adjustment (MVA) provision.

An MVA allows the insurance company to pass some risk to you.

An MVA may increase or decrease the withdrawal you want to make if your requested withdrawal is larger than the allowed free withdrawal provision listed in the contract.

An MVA is a formula that uses either the Treasury Constant Maturity Series or Barclays U.S. Credit Index as a benchmark.

Rising interest rates work against you, meaning your withdrawal will be less than requested. Falling interest rates work in your favor, meaning your withdrawal will be greater than requested.

If you remain within all the provisions of your contract no MVA will be applied. No MVA is assessed once the contract reaches maturity.

15

3. AnnuitizationCreating a steady stream of income

16

What to know before you annuitize

When annuitizing an existing deferred annuity your insurance company may not be able to give you the best rates available in the market. It is a good idea to shop around and determine the best rate available, with insurance company rating in mind.

Nevada premium tax: Any non-qualified (after-tax) money annuitized in the state of Nevada is subject to a one time 3.5% tax. There is no annuitization (premium) tax for qualified (before-tax) money in Nevada.

Annuitization means fixed payments, like a pension. These fixed payments do not increase with inflation. You can purchase inflation protection for your annuity, however, retirement experts who have examined the cost and benefits closely, believe that purchasing inflation protection is not a good investment. (source: Steven Weisman – elder law attorney).

17

Single Premium Immediate Annuity (SPIA) common payout

options Life Only: Payments are made for the life of the primary annuitant. Payments cease upon death of the primary annuitant. There is no death benefit.

Life with Period Certain: Payments are made for the life of the primary annuitant. If the primary annuitant dies prior to receiving the total number of guaranteed payments (selected at time of purchase), the beneficiary will receive the remainder of those guaranteed payments.

Joint & Survivor (death of primary): Payments are made for the life of the primary annuitant. If upon death of the primary annuitant the contingent annuitant is living, the contingent annuitant will begin to receive payments equal to a percentage (selected at time of purchase) of the original benefit amount. Payments cease upon death of the survivor.

18

4. Wealth TransferOver 90% of annuity owners do not annuitize. Most annuity money today is ear marked for later use or the next generation.

One concept you may not have thought practical at this stage in your life… purchasing life insurance.

19

Wealth Transfer Life Insurance Versus Annuities

Life Insurance Annuity

Free of Probate Yes Yes

Step-up in Basis Yes No

Tax Free to Beneficiary Yes No

20

Wealth Transfer Made Easier

There is at least one Life Insurance product on the market today that is designed to pass an enhanced legacy to loved ones, or your favorite charity, while still allowing you access to your principal and growth in case of emergencies during your life time.

A $54,000 investment buys a $100,000 death benefit. The policy owner has access to 90% of the death benefit in the event of chronic or terminal illness.

The policy underwriting process asks only five yes or no questions.

21

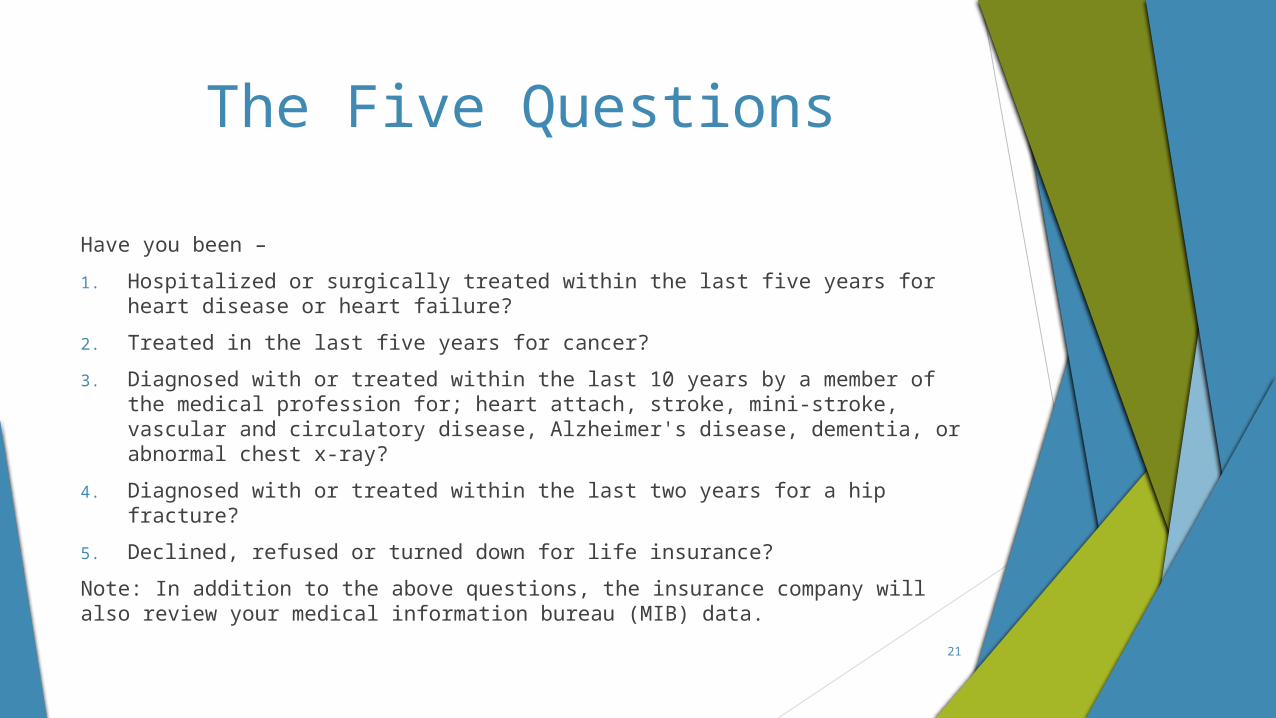

The Five Questions

Have you been –

1. Hospitalized or surgically treated within the last five years for heart disease or heart failure?

2. Treated in the last five years for cancer?

3. Diagnosed with or treated within the last 10 years by a member of the medical profession for; heart attach, stroke, mini-stroke, vascular and circulatory disease, Alzheimer's disease, dementia, or abnormal chest x-ray?

4. Diagnosed with or treated within the last two years for a hip fracture?

5. Declined, refused or turned down for life insurance?

Note: In addition to the above questions, the insurance company will also review your medical information bureau (MIB) data.

22

NameAnnuity Doctor

Phone

Thank you!