Embed Size (px)

Citation preview

Federal Reserve Bank of St. Louis REVIEW January/February 2013 51

Four Stories of Quantitative Easing

Brett W. Fawley and Christopher J. Neely

C entral banks typically conduct monetary policy through control of short-term nominalinterest rates that can potentially affect the economy through a variety of channels.Because inflation expectations do not immediately react one for one to changes in nomi-

nal interest rates, central banks can also control real interest rates, at least over the short tomedium term. The typical assumption is that monetary policy changes real (inflation-adjusted)short-term rates to influence economic decisions through their effect on other asset prices.That is, real interest rates will change asset prices in such a way as to change the willingness ofbanks to lend, firms to invest, or individuals to consume or invest in housing. Thus, a changein short-term real interest rates potentially influences the level of output and employment.

Because people can always hold currency instead of depositing it in a bank, short-termnominal interest rates cannot go (much) below zero, which limits the effectiveness of conven-tional monetary policy.1 Concerns about the consequences of the zero bound for interest ratesdate at least to Keynes (1936), and many observers have believed that central banks are helplesswhen short-term rates are near the zero bound. Many others, however, have argued that centralbanks can influence prices and output even when short-term rates are near their zero floor byincreasing liquidity, particularly by purchasing long-term assets. For example, Mishkin (1996)

This article describes the circumstances of and motivations for the quantitative easing programs of theFederal Reserve, Bank of England, European Central Bank, and Bank of Japan during the recent financialcrisis and recovery. The programs initially attempted to alleviate financial market distress, but this pur-pose soon broadened to include achieving inflation targets, stimulating the real economy, and contain-ing the European sovereign debt crisis. The European Central Bank and Bank of Japan focused theirprograms on direct lending to banks—reflecting the bank-centric structure of their financial systems—while the Federal Reserve and the Bank of England expanded their respective monetary bases by pur-chasing bonds. (JEL E51, E58, E61, G12)

Federal Reserve Bank of St. Louis Review, January/February 2013, 95(1), pp. 51-88.

Brett W. Fawley is a senior research associate and Christopher J. Neely is an assistant vice president and economist at the Federal Reserve Bankof St. Louis.

© 2013, The Federal Reserve Bank of St. Louis. The views expressed in this article are those of the author(s) and do not necessarily reflect theviews of the Federal Reserve System, the Board of Governors, or the regional Federal Reserve Banks. Articles may be reprinted, reproduced,published, distributed, displayed, and transmitted in their entirety if copyright notice, author name(s), and full citation are included. Abstracts,synopses, and other derivative works may be made only with prior written permission of the Federal Reserve Bank of St. Louis.

characterizes the view that monetary policy can do nothing to stimulate the economy onceshort-term nominal interest rates approach zero as “demonstrably false.”

Recent events have twice tested this claim: first in the early 2000s in Japan and then afterthe 2007-09 financial crisis in the United States, United Kingdom, Japan, and the euro area. Withshort rates approaching the zero lower bound in late 2008/early 2009, the Federal Reserve, theBank of Japan (BOJ), the Bank of England (BOE), and the European Central Bank (ECB) beganto pursue less conventional monetary policies—including forms of quantitative easing (QE)—to stimulate economic growth. QE policies are those that unusually increase the monetary base,including asset purchases and lending programs. Programs designed to improve credit condi-tions—that is, credit easing—are a special case of QE if they also increase the monetary base.

Academics have already conducted substantial research on recent QE programs. Stroebeland Taylor (2009), Kohn (2009), Meyer and Bomfim (2010), and Gagnon et al. (2011a,b), forexample, study the Fed’s 2008-09 QE programs. Gagnon et al.’s (2011a,b) announcement studyfinds that large-scale asset purchase (LSAP) announcements reduced U.S. long-term yields.Joyce et al. (2011) find that the BOE’s QE program had bond yield effects quantitatively similarto those reported by Gagnon et al. (2011a,b) for the U.S. program. Hamilton and Wu (2011)indirectly calculate the effects of the Fed’s 2008-09 QE programs with a term structure model.Neely (2012) evaluates the effect of the Fed’s 2008-09 QE on international long bond yields andexchange rates, showing that the effects are consistent with a simple portfolio balance modeland long-run purchasing power parity.

Despite this profusion of research on asset purchase programs and QE more generally, therehas been little attempt to describe and compare QE programs across central banks.2 This articlefills that gap by describing and comparing the QE and related maturity extension programs ofthe BOJ, the BOE, the Fed, and the ECB. We emphasize, however, that although we draw somelimited conclusions about the immediate effects of the programs on financial markets, we donot evaluate the efficacy of the QE programs on the broader economies, as that would requirecounterfactual models and empirical work well beyond the scope of this article.

The details of the QE programs varied across central banks and depended on the particularstructures of their respective economies and the specific motivations for each of the QE actions.For example, this article details the circumstances under which the ECB and BOJ generouslylent money to banks to inject reserves into their bank-centric economies, but the Fed and BOEinjected reserves into the U.S. and U.K. economies by purchasing bonds. One topic on whichthis article does not shed light is the extent to which the QE and related programs might havebeen coordinated; there is no significant public information on the extent of international coor-dination, if any.

The QE programs in response to the financial crisis differ radically from temporary increasesin the monetary base that are occasionally used to provide liquidity for short periods, such ascentral banks did for Y2K or short-term emergency last-resort lending. Instead, this article dis-cusses the recent episodes in which central banks used QE to stimulate the economy, perhapsby facilitating the functioning of particular financial markets.

The next section discusses potential monetary transmission mechanisms at the zero lowerbound, how the mechanisms provide a role for QE, and how they explain the choices involved

Fawley and Neely

52 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

in QE programs. We then discuss the relationship between QE and credit easing and describethe Fed, BOJ, BOE, and ECB motivations and programs in the context of a timeline. This is fol-lowed by summaries of the amounts and types of asset purchases and our conclusion.

MONETARY TRANSMISSION MECHANISMS AT THE ZERO LOWERBOUND

Central banks ordinarily conduct monetary policy by buying and selling short-term debtsecurities to target short-term nominal interest rates. These purchases and sales of assets changeboth short-term interest rates and the monetary base (the quantity of currency and bank reservesin the economy). For example, a central bank can expand the monetary base in two essentiallyequivalent ways: by buying bonds from the public or by lending money to the public. Buyingbonds reduces the public’s bond holdings and increases the amount of currency and bankreserves in the economy. This conventional monetary policy can potentially stimulate the econ-omy through two types of channels: asset price channels (including interest rates) and creditchannels.

By purchasing short-term securities, expanding the monetary base, and lowering short-termreal interest rates, central banks can affect a variety of asset prices, including exchange rates andstock prices. The changes in asset prices can affect economic decisions. Higher stock prices candirectly stimulate consumption and business investment by increasing consumer wealth andmaking the issuance of new stock more lucrative. A lower foreign exchange value of the domesticcurrency makes domestic goods more competitive with foreign goods. Lower interest ratesencourage borrowing for consumption and investment.

Credit channels require asset price changes to work but they also exploit the fact that easiermonetary policy can reduce the effect of certain financial frictions—adverse selection and moralhazard—that hinder borrowing.3 These problems are especially pervasive during difficult eco-nomic times. One example of how economic conditions influence lending through these frictionsis that expectations of low profitability can discourage potentially creditworthy borrowers fromseeking to borrow at all, but they will not discourage fraudulent borrowers who have no intentionof repaying the loan. Thus, the pool of firms and individuals seeking loans will become heavilyweighted toward fraudulent borrowers and banks—knowing this—will become increasinglyreluctant to make loans. By lowering interest rates and raising stock prices, expansionary mone-tary policy can improve the balance sheets of firms and consumers, reducing problems of adverseselection and moral hazard.

However, purchasing short-term securities cannot lower interest rates when they are at zero;therefore, increasing the monetary base is not—by itself—considered an effective stimulus.Because money and bonds become close substitutes, the public can simply choose to hold cen-tral bank injections of money as currency “under the mattress,” which prevents the additionalmoney from stimulating economic activity. Such a situation is called a liquidity trap and canmotivate central banks to focus on specific markets and/or interest rates rather than simplyexpanding the quantity of money.4

In the face of near-zero short-term rates, central banks have recently turned to unconven-tional policies, which often dramatically increase their monetary bases, to alleviate financial

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 53

distress or stimulate their economies. Some of these unconventional policies involve direct lend-ing to specific, distressed short-term credit markets, whereas others involve purchases of long-term assets that are intended to reduce real, long-term interest rates.

To understand how monetary policy can potentially affect long-term interest rates, it is usefulto decompose the n-year real yield on a bond as follows:

where yt,t+n is the expected real yield at time t on an n-year bond, y–t,t+n is the average expectedovernight rate over the next n years at time t, TPt,n is the term premium on an n-year bond attime t, and Etpn is the expected average rate of inflation over the next n years at time t. Long-termreal yields can decline in any of three ways: (i) Expected inflation can increase, (ii) the expectedpolicy rate path can fall, and (iii) the term premium can fall.

What sort of monetary policy would change expected inflation, the expected path of shortrates, and/or the term premium? First, a central bank can commit to zero interest rates beyondthe period that their reaction function would normally call for, what Eggertsson (2006) refers toas “committing to be irresponsible.”5 Such a strategy—often termed “signaling”—is time incon-sistent, however: The central bank will want to renege on its commitment and return to its nor-mal policy when conditions improve. The second and third methods—outright asset purchasesand bank lending (QE)—can help resolve the apparent time inconsistency of a commitment toan announced policy rate path by changing the central bank’s incentives through its balancesheet. A central bank that purchases a sizable quantity of long bonds when long rates are lowwill see the value of its bond portfolio decline if long rates rise.6 Similarly, the value of long-termloans will decline as long-term rates rise.

Despite concerns about time consistency, recent policy has incorporated strategies thatattempt to commit to a path: The Fed, for example, used five variations of “extended period”language to restrain expectations of policy rate hikes, eventually suggesting that it would main-tain its low policy rate until at least mid-2015. On December 12, 2012, the FOMC linked therate hikes to economic conditions rather than a fixed date. Specifically, the FOMC announcedthat it expected low rates to be appropriate as long as the unemployment rate was above 6.5 per-cent, medium-term inflation forecasts stayed below 2.5 percent, and long-run inflation expec-tations remained anchored.7

Central banks can also lower long-term real rates by reducing term premia through assetpurchases. This method relies on the portfolio balance channel, which assumes frictions—typi-cally preferred habitat/market segmentation—that (i) preclude perfect arbitrage between longand expected short rates and (ii) permit changes in the maturity composition of nominal govern-ment debt to affect asset prices. That is, a central bank’s purchase of a quantity of a certain typeof risk (i.e., duration) will cause investors to demand less compensation to hold the remainingamount of that type of risk and term premia will fall. Thus, signaling and portfolio balancechannels allow asset purchases to lower long real rates and thereby stimulate the economythrough the aforementioned asset price and credit channels (Mishkin, 1996).

yt ,t+n = yt ,t+n +TPt ,n !Et!n ,

Fawley and Neely

54 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

QUANTITATIVE EASING VERSUS CREDIT EASING This section differentiates credit easing from pure QE. Credit easing policies are intended

to reduce specific interest rates/restore market function, while QE describes any policy thatunusually increases the magnitude of central bank liabilities—currency and bank reserves—particularly at the zero bound. Credit easing can entail QE but it specifically targets certainmarkets and/or interest rates. Federal Reserve Chairman Ben Bernanke termed the Fed’s LSAPs“credit easing” because the Fed sought to improve the functioning of long-term bond marketsand decrease long-term interest rates rather than simply increase the monetary base. In the samespeech, the Chairman stated that “in a pure QE regime, the focus of policy is the quantity of bankreserves, which are liabilities of the central bank; the composition of loans and securities on theasset side of the central bank’s balance sheet is incidental” (Bernanke, 2009). ECB executiveboard member Lorenzo Bini Smaghi describes QE similarly: “When the central bank decides toexpand the size of its balance sheet, it has to choose which assets to buy. In theory, it could pur-chase any asset from anybody” (Bini Smaghi, 2009).

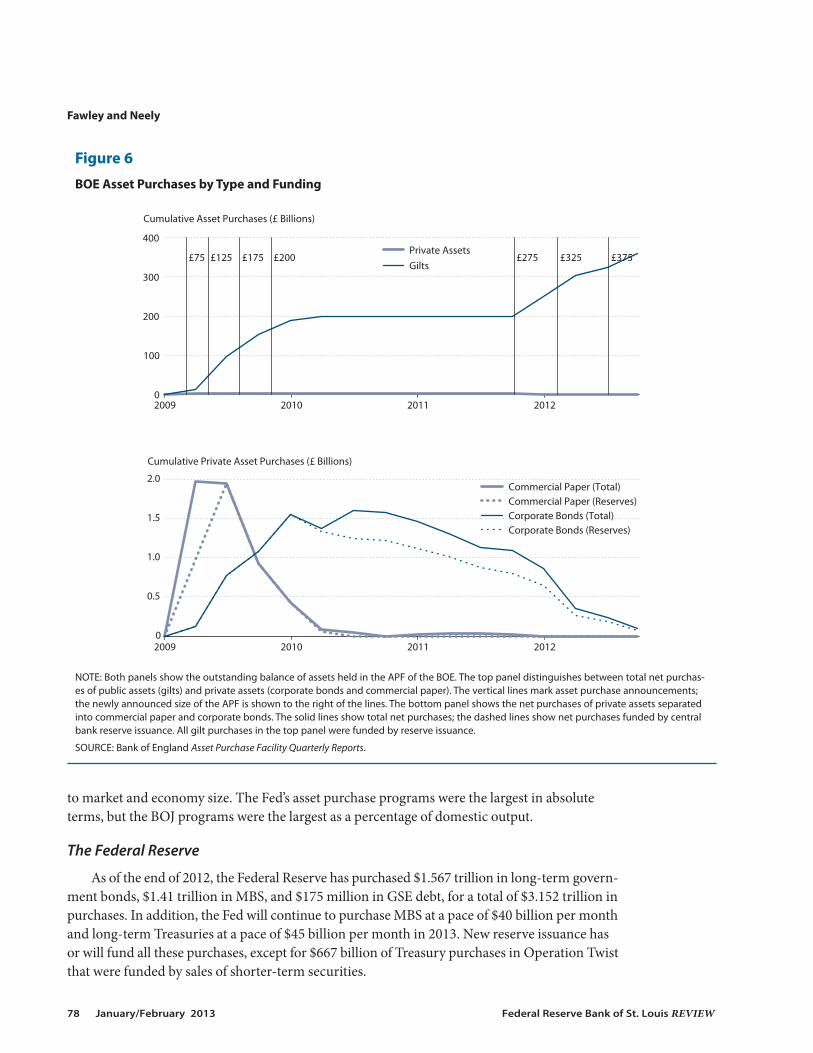

Both the BOJ in the early 2000s and the BOE in the recent episode explicitly described theirobjectives as expanding bank reserves—that is, QE—rather than easing credit market conditions.The BOE described its policy in this manner even though its purchases of medium- and long-term gilts would tend to reduce the corresponding interest rates.8 The ECB and BOJ have recentlyinitiated lending programs that could also be considered “pure” QE in the sense that they targetedreserves and typically accepted a wide range of assets as collateral.

PROGRAM DESCRIPTIONS AND MOTIVATIONSThis article focuses on the QE programs in response to the subprime crisis, but the BOJ

created a precursor to such programs in 2001 in response to an extended period of very sluggisheconomic conditions. On March 19, 2001, the BOJ changed its main operating target from theuncollateralized overnight call rate to the outstanding balance of “current accounts” (i.e., thequantity of bank reserves). The BOJ announced that it was increasing the target for bank reservesfrom ¥4 trillion to ¥5 trillion, which was expected to drive the overnight call rate from 0.15 per-cent to zero.

By 2004, the BOJ had incrementally increased the target for bank reserves to ¥30 trillion to¥35 trillion while simultaneously purchasing public and private debt and communicating theconditions necessary for exiting the zero interest rate policy (ZIRP). On March 9, 2006, the BOJended its official QE regime when it reinstated the uncollateralized overnight call rate as themain policy instrument (setting the target at 0 percent).

The Japanese experience provides few firm conclusions as to the potential for QE as a policyinstrument. Ito and Mishkin (2006) argue that the BOJ managed market expectations very poorlyfrom 1998 to 2003, compromising any potential for success. Central banks would soon haveanother opportunity to employ QE to battle very difficult economic conditions.

Initial Post-Lehman Brothers Responses (September 2008–November 2009)

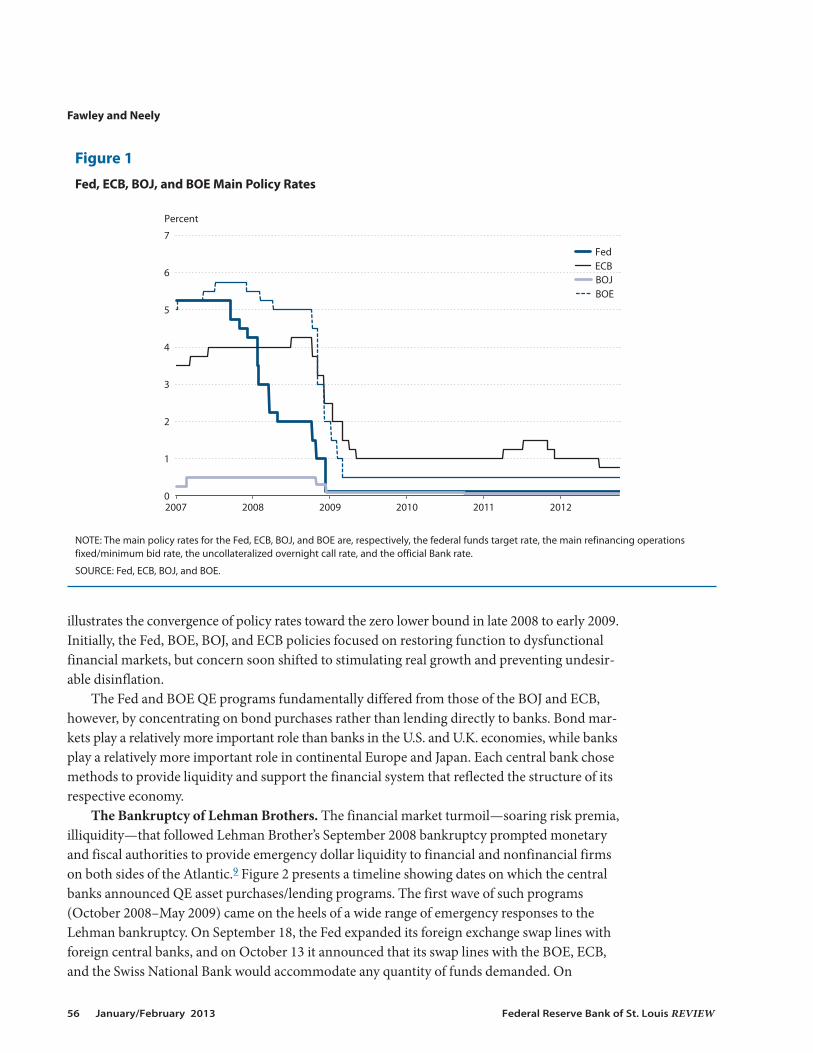

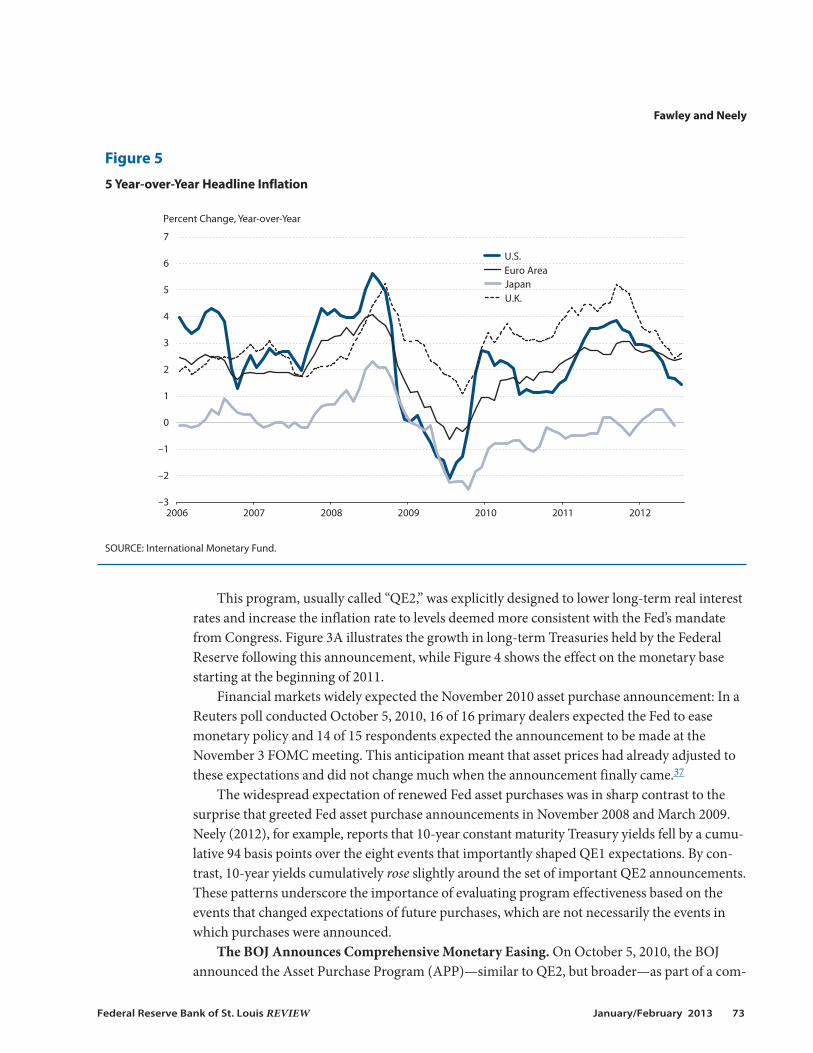

By late 2008, the delayed indirect effects of the housing price bubble collapse of 2006 hadleft financial markets dysfunctional, output falling, and short-term rates close to zero. Figure 1

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 55

illustrates the convergence of policy rates toward the zero lower bound in late 2008 to early 2009.Initially, the Fed, BOE, BOJ, and ECB policies focused on restoring function to dysfunctionalfinancial markets, but concern soon shifted to stimulating real growth and preventing undesir-able disinflation.

The Fed and BOE QE programs fundamentally differed from those of the BOJ and ECB,however, by concentrating on bond purchases rather than lending directly to banks. Bond mar-kets play a relatively more important role than banks in the U.S. and U.K. economies, while banksplay a relatively more important role in continental Europe and Japan. Each central bank chosemethods to provide liquidity and support the financial system that reflected the structure of itsrespective economy.

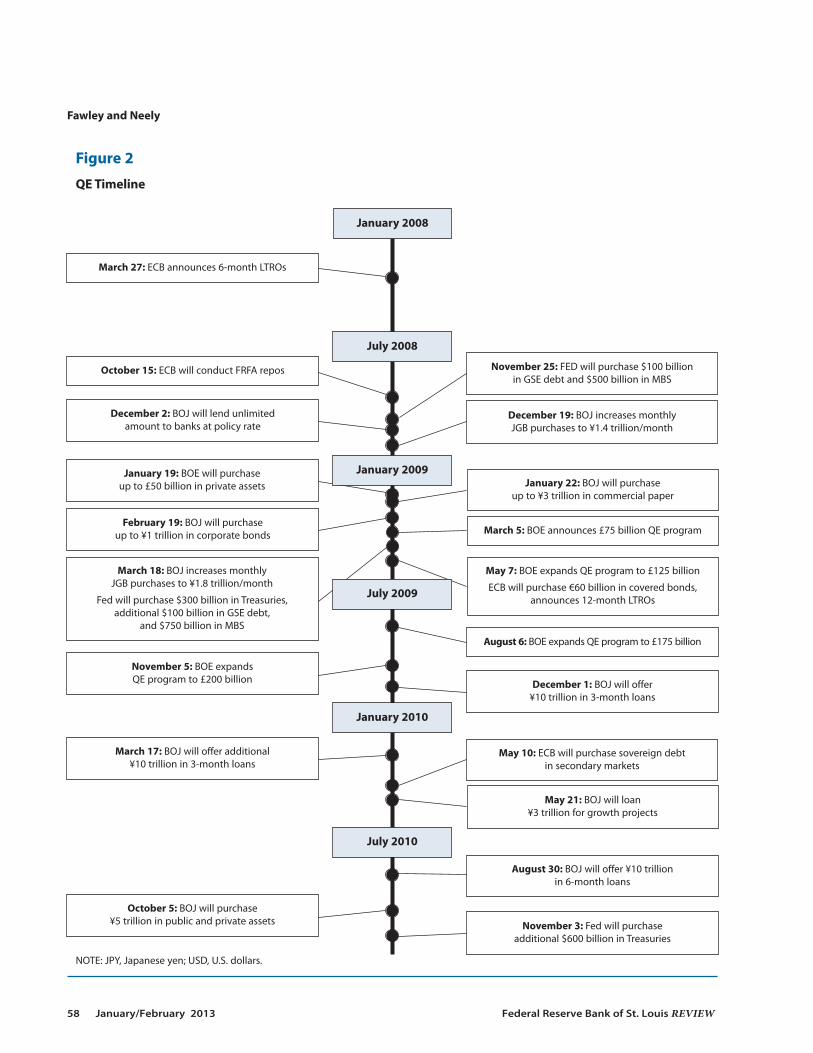

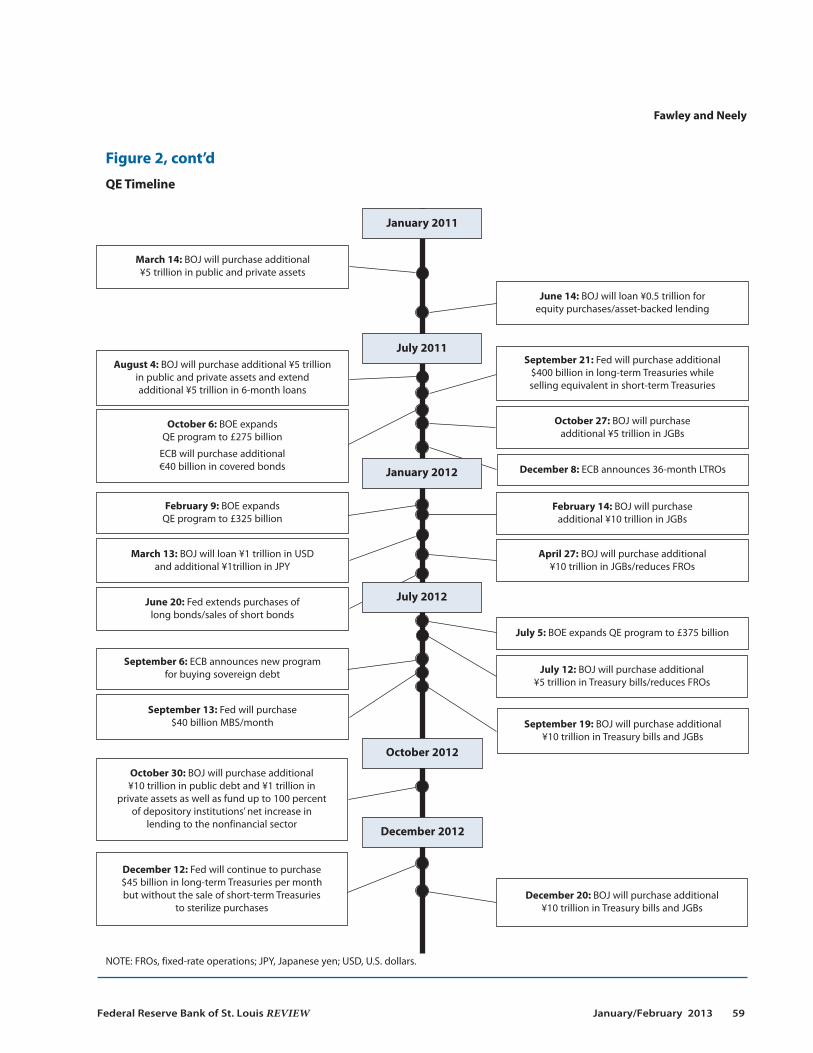

The Bankruptcy of Lehman Brothers. The financial market turmoil—soaring risk premia,illiquidity—that followed Lehman Brother’s September 2008 bankruptcy prompted monetaryand fiscal authorities to provide emergency dollar liquidity to financial and nonfinancial firmson both sides of the Atlantic.9 Figure 2 presents a timeline showing dates on which the centralbanks announced QE asset purchases/lending programs. The first wave of such programs(October 2008–May 2009) came on the heels of a wide range of emergency responses to theLehman bankruptcy. On September 18, the Fed expanded its foreign exchange swap lines withforeign central banks, and on October 13 it announced that its swap lines with the BOE, ECB,and the Swiss National Bank would accommodate any quantity of funds demanded. On

Fawley and Neely

56 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012

Fed ECB BOJ BOE

Percent

Figure 1

Fed, ECB, BOJ, and BOE Main Policy Rates

NOTE: The main policy rates for the Fed, ECB, BOJ, and BOE are, respectively, the federal funds target rate, the main refinancing operationsfixed/minimum bid rate, the uncollateralized overnight call rate, and the official Bank rate.

SOURCE: Fed, ECB, BOJ, and BOE.

September 19, the U.S. Treasury guaranteed money market mutual fund (MMMF) deposits andthe Fed created the Asset-Backed Commercial Paper (ABCP) Money Market Mutual FundLiquidity Facility, which lent money to banks for the purpose of purchasing high-quality ABCP.10

On October 7, the Fed created the Commercial Paper Funding Facility (CPFF) to directly pur-chase high-quality commercial paper. The ECB announced on September 29, 2008, that on thatday it would begin a 1-month “special term refinancing operation…to improve the overall liq-uidity position of the euro area banking system.” Although the Fed previously had responded tothe financial crisis (e.g., implementing the Term Auction Facility), these actions were the firstunsterilized policy actions—that is, the first Fed actions that were allowed to unusually expandthe monetary base (see the boxed insert).

The ECB’s Fixed-Rate Tender, Full-Allotment Programs. The 3-month Euribor/overnightindexed swap (OIS) spread widened as financial conditions deteriorated. On October 10, 2008,the spread hit an all-time high of 198 basis points, which reflected the sharp rise in perceivedcounterparty risk.11 The ECB responded to these widening spreads on October 15, 2008, withits first measure of QE: The ECB announced it would lend as much as banks wanted at a fixed-rate tender—provided the banks had collateral—while also expanding the list of eligible collateral.These fixed-rate tender, full-allotment (FRFA) operations reversed the ECB’s conventional policyof offering a fixed allotment of funds at rates determined by the bidding process.12

The ECB implemented the FRFA liquidity provision through its usual lending procedures.In normal times, the ECB’s primary policy instrument is refinancing operations, direct lendingto banks against eligible collateral at two maturities. Main refinancing operations (MROs) havea period of two weeks and longer-term refinancing operations (LTROs) have a period of threemonths.13 In the usual MROs and LTROs, the ECB predetermines the amount of funding avail-able and auctions those funds by price. Under the new policy, the ECB filled all MRO and LTRO

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 57

Abbreviations Used

ABCP Asset-Backed Commercial Paper GSFF Growth-Supporting Funding Facility

APF Asset Purchase Facility JGBs Japanese government bonds

APP Asset Purchase Program J-REITs Japanese real estate investment trusts

BOE Bank of England LSAP large-scale asset purchase

BOJ Bank of Japan LTROs longer-term refinancing operations

CBPP covered bond purchase program MBS mortgage-backed securities

CFI corporate finance instruments MMMF money market mutual fund

CPFF Commercial Paper Funding Facility MROs main refinancing operations

ECB European Central Bank OIS overnight indexed swap

ETFs exchange-traded funds OMTs outright monetary transactions

FOMC Federal Open Market Committee QE quantitative easing

FRFA fixed-rate, full-allotment SBLF Stimulating Bank Lending Facility

FROs fixed-rate operations SFSOs special-funds-supplying operations

GDP gross domestic product SMP Securities Markets Programme

GSE government-sponsored enterprise ZIRP zero interest rate policy

Fawley and Neely

58 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

Figure 2

QE Timeline

NOTE: JPY, Japanese yen; USD, U.S. dollars.

March 27: ECB announces 6-month LTROs

October 15: ECB will conduct FRFA repos November 25: FED will purchase $100 billion in GSE debt and $500 billion in MBS

December 2: BOJ will lend unlimited amount to banks at policy rate

December 19: BOJ increases monthly JGB purchases to ¥1.4 trillion/month

January 19: BOE will purchase up to £50 billion in private assets

December 1: BOJ will offer ¥10 trillion in 3-month loans

August 6: BOE expands QE program to £175 billion

November 5: BOE expands QE program to £200 billion

May 7: BOE expands QE program to £125 billion

ECB will purchase €60 billion in covered bonds,announces 12-month LTROs

March 18: BOJ increases monthly JGB purchases to ¥1.8 trillion/month

Fed will purchase $300 billion in Treasuries, additional $100 billion in GSE debt,

and $750 billion in MBS

March 5: BOE announces £75 billion QE program

January 22: BOJ will purchase up to ¥3 trillion in commercial paper

February 19: BOJ will purchase up to ¥1 trillion in corporate bonds

October 5: BOJ will purchase ¥5 trillion in public and private assets

May 21: BOJ will loan ¥3 trillion for growth projects

March 17: BOJ will offer additional ¥10 trillion in 3-month loans

November 3: Fed will purchase additional $600 billion in Treasuries

August 30: BOJ will offer ¥10 trillion in 6-month loans

May 10: ECB will purchase sovereign debt in secondary markets

January 2008

July 2008

January 2010

July 2010

January 2009

July 2009

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 59

Figure 2, cont’d

QE Timeline

NOTE: FROs, fixed-rate operations; JPY, Japanese yen; USD, U.S. dollars.

March 14: BOJ will purchase additional ¥5 trillion in public and private assets

June 14: BOJ will loan ¥0.5 trillion for equity purchases/asset-backed lending

August 4: BOJ will purchase additional ¥5 trillionin public and private assets and extend additional ¥5 trillion in 6-month loans

September 21: Fed will purchase additional$400 billion in long-term Treasuries while selling equivalent in short-term Treasuries

October 6: BOE expands QE program to £275 billion

ECB will purchase additional €40 billion in covered bonds

October 27: BOJ will purchase additional ¥5 trillion in JGBs

July 5: BOE expands QE program to £375 billion

April 27: BOJ will purchase additional ¥10 trillion in JGBs/reduces FROs

June 20: Fed extends purchases of long bonds/sales of short bonds

March 13: BOJ will loan ¥1 trillion in USD and additional ¥1trillion in JPY

February 14: BOJ will purchase additional ¥10 trillion in JGBs

February 9: BOE expands QE program to £325 billion

December 8: ECB announces 36-month LTROs

September 13: Fed will purchase $40 billion MBS/month

July 12: BOJ will purchase additional ¥5 trillion in Treasury bills/reduces FROs

September 19: BOJ will purchase additional ¥10 trillion in Treasury bills and JGBs

September 6: ECB announces new program for buying sovereign debt

January 2011

July 2011

July 2012

January 2012

October 2012

December 2012

October 30: BOJ will purchase additional ¥10 trillion in public debt and ¥1 trillion in

private assets as well as fund up to 100 percentof depository institutions’ net increase in

lending to the nonfinancial sector

December 12: Fed will continue to purchase $45 billion in long-term Treasuries per month but without the sale of short-term Treasuries

to sterilize purchasesDecember 20: BOJ will purchase additional

¥10 trillion in Treasury bills and JGBs

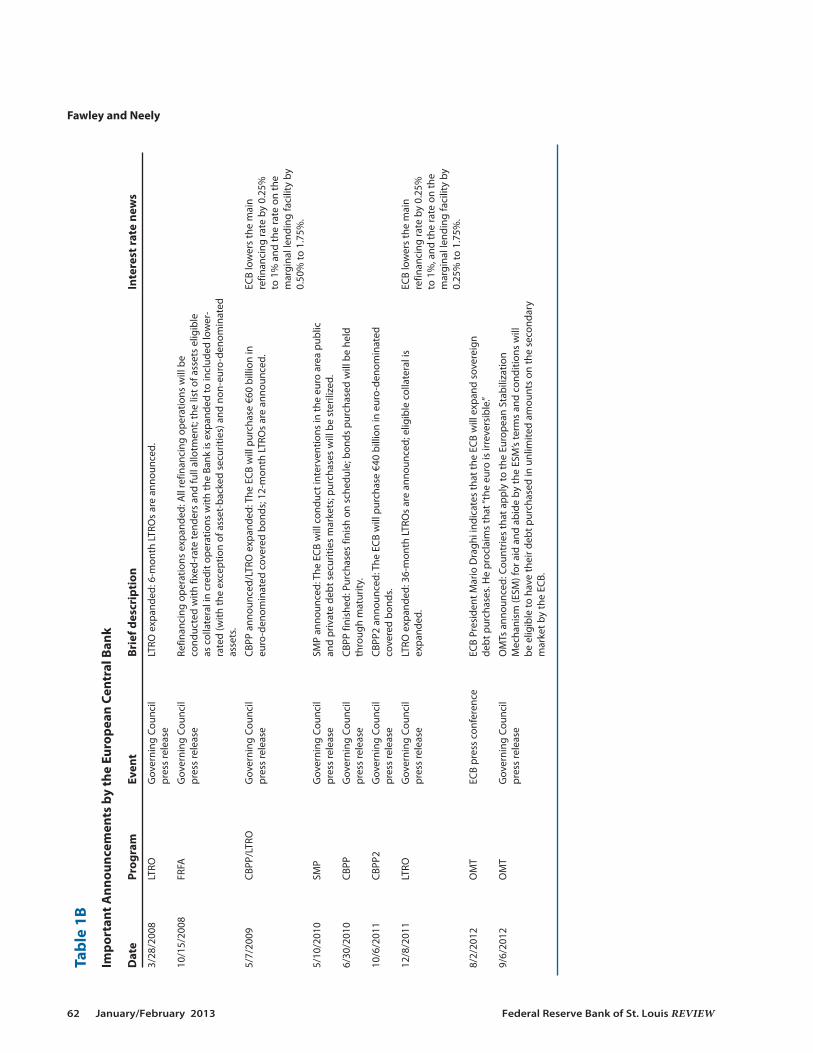

loan requests at the ECB’s primary policy rate, the main refinancing rate. From October 2008 toMay 2009, the ECB cut this rate from 4.25 percent to 1 percent.14

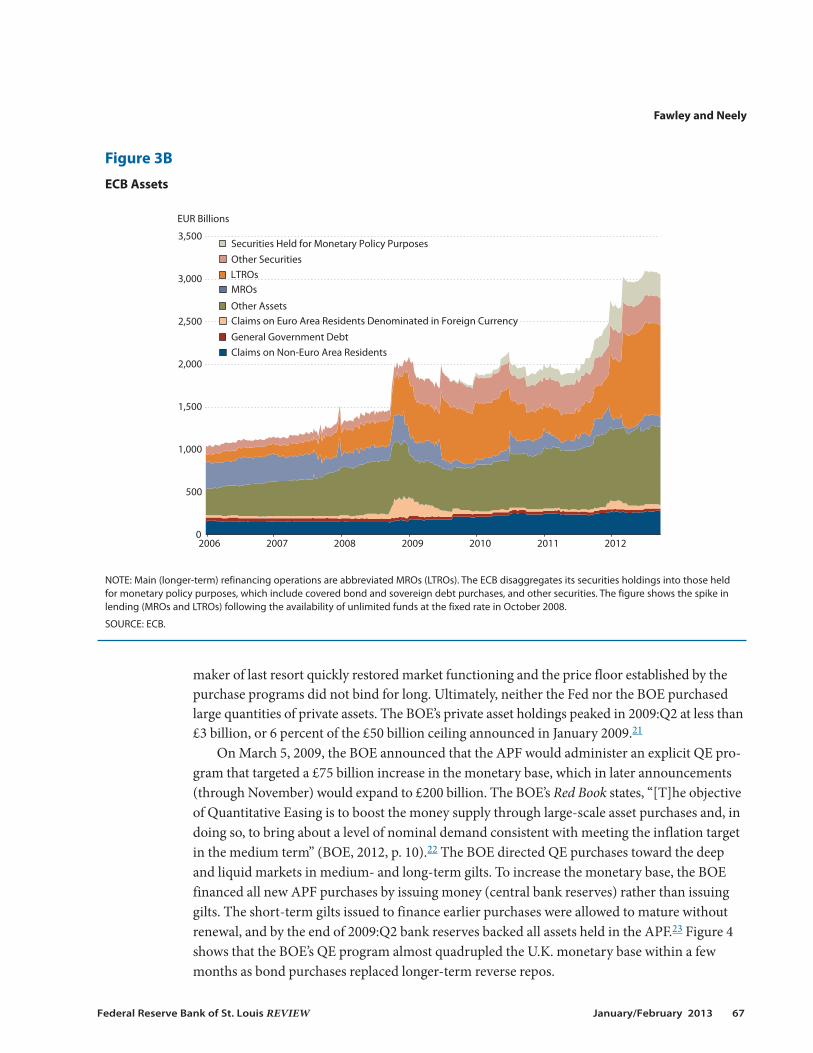

Bini Smaghi (2009) calls the FRFA liquidity policy “endogenous credit easing” becausebanks’ demand for liquidity at the fixed-rate tender determines liquidity. Figure 3B shows thespike in lending under MROs and LTROs following the availability of unlimited funds at thefixed rate in October 2008.

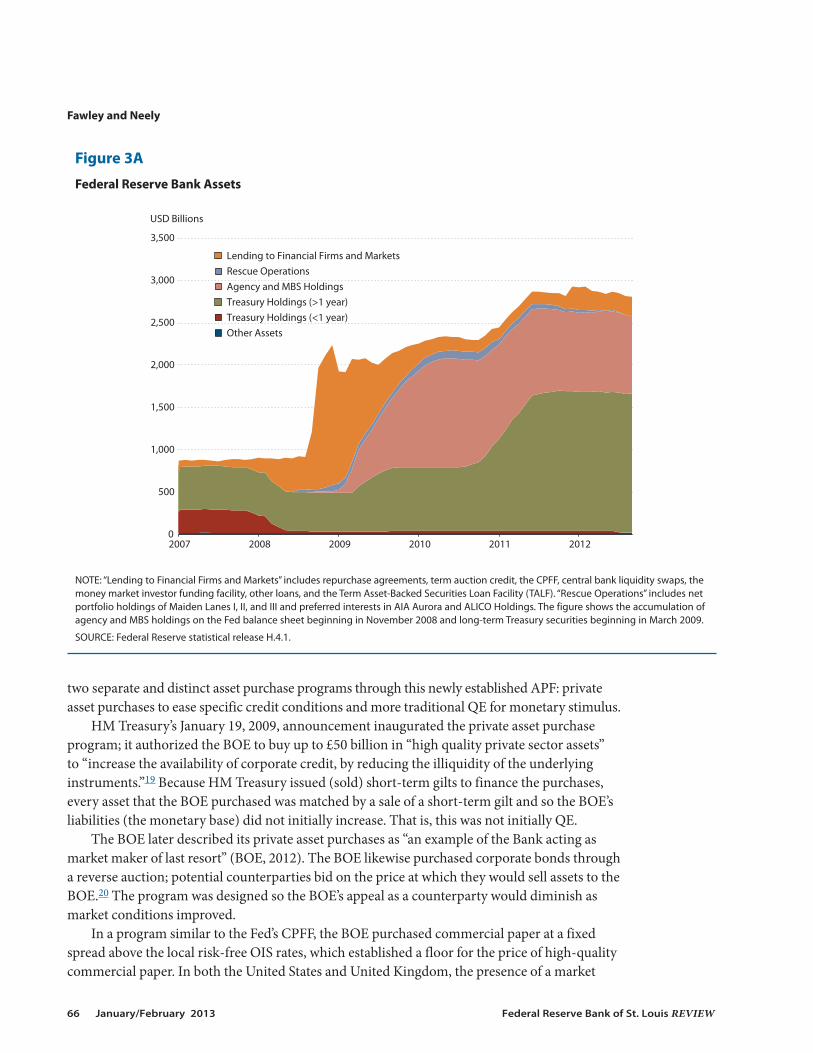

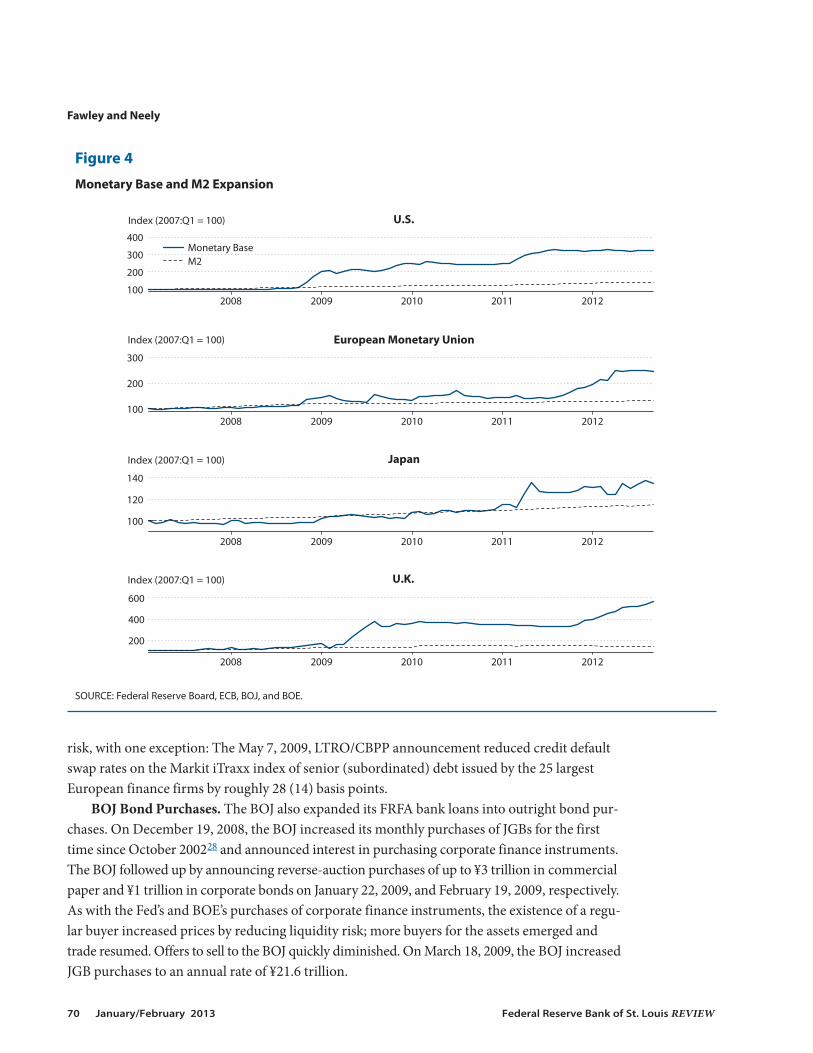

The Fed’s QE1 Programs. While the ECB expanded bank lending operations, the FederalReserve pursued outright asset purchases. On November 25, 2008, the Federal Reserve announcedplans to purchase $100 billion in government-sponsored enterprise (GSE) debt and $500 billionin mortgage-backed securities (MBS) issued by those GSEs (Table 1A).15 On March 18, 2009,the Fed announced additional purchases of $100 billion in GSE debt, $750 billion in MBS, and$300 billion in long-term Treasury securities. Figure 3A illustrates the accumulation of agencyand MBS holdings on the Fed balance sheet beginning in November 2008 and long-termTreasuries beginning in March 2009. Figure 4 reveals that these purchases roughly doubled thesize of the U.S. monetary base.

The Fed’s November 2008 and March 2009 asset purchase programs—commonly called“QE1”—were designed to support the entire economy but they naturally prioritized housingcredit markets, which had been especially hard hit by the 2006-08 fall in U.S. real estate prices,sales, and construction. Housing GSE debt and MBS accounted for more than 80 percent of theassets purchased by the Federal Reserve in its first round of QE, or LSAPs; these assets weredirectly linked to housing market credit.16 The Federal Open Market Committee (FOMC) statedthat the goal of the initial LSAPs was to “reduce the cost and increase the availability of creditfor the purchase of houses, which in turn should support housing markets and foster improvedconditions in financial markets more generally.”17 Gagnon et al. (2011a) report that the November2008 and March 2009 purchases lowered long-term real U.S. interest rates through their effecton term premia. These purchases substantially increased excess bank reserves.

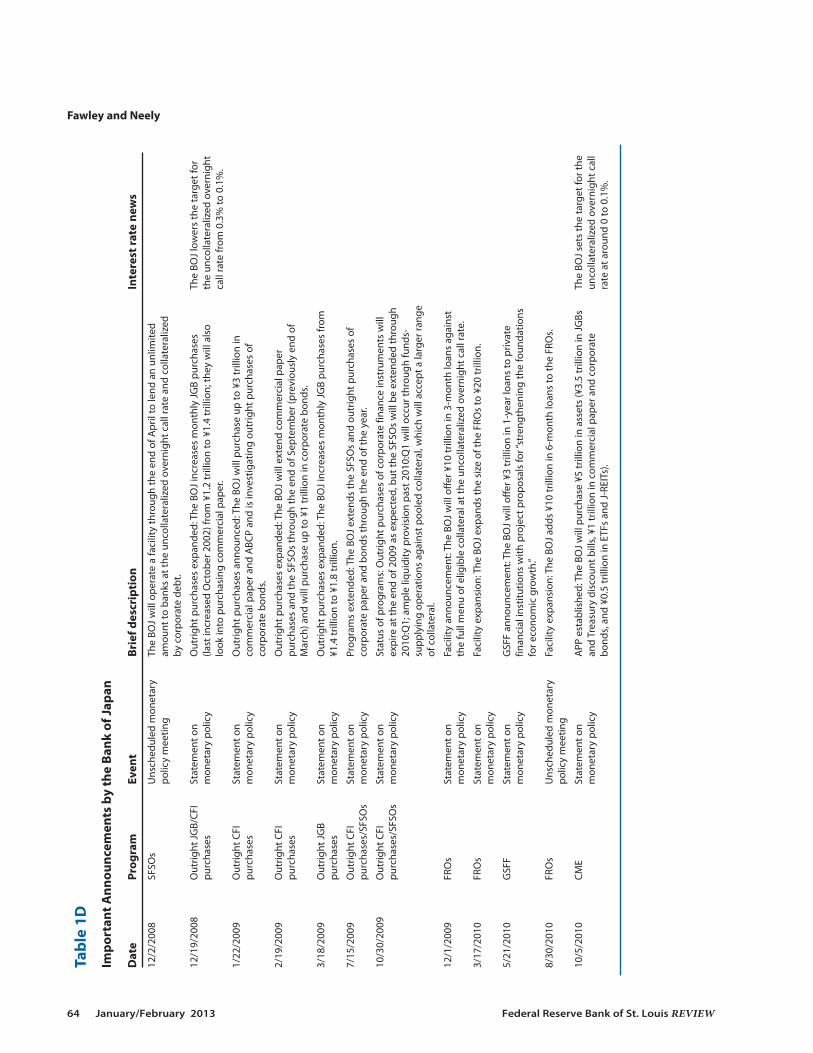

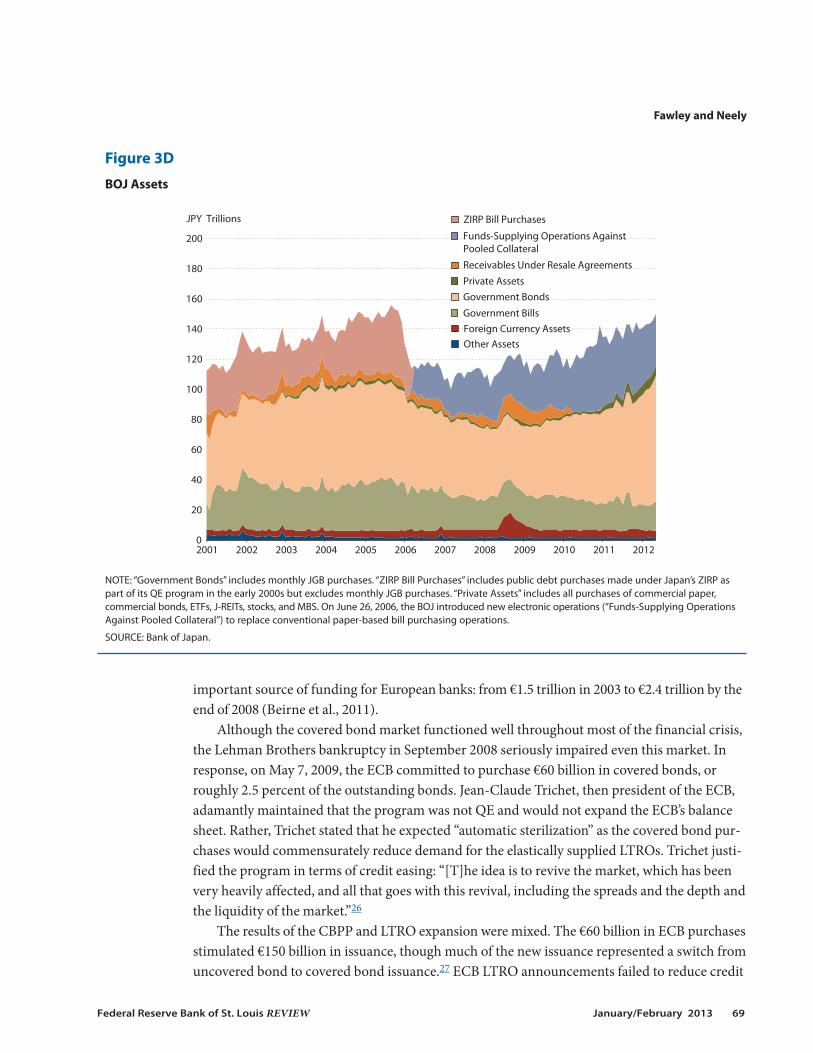

The Bank of Japan’s Special-Funds-Supplying Operations. Following closely on the heelsof the Fed’s November 25 asset purchase release, the BOJ announced on December 2, 2008, thatit would lend unlimited amounts to banks at near-zero rates through special-funds-supplyingoperations (SFSOs), which were much like the ECB’s lending operations. The SFSOs offered3-month loans to banks at the uncollateralized overnight call rate, which was then at 0.3 percent.The only limit on the size of the loans from the BOJ to banks was the amount of available collat-eral (commercial paper and corporate debt). The SFSOs, like the ECB’s FRFA repurchase agree-ment (repo) auctions, constituted QE because they increased the monetary base. On December19, 2008, the BOJ followed this action by lowering the overnight call rate to 0.1 percent andannouncing an increase in outright purchases of Japanese government bonds (JGBs) and a newprogram to purchase corporate financial instruments.18 BOJ assets did not increase sharply inDecember 2008 (see Figure 3D), though the BOJ’s balance sheet did begin to expand after thispoint.

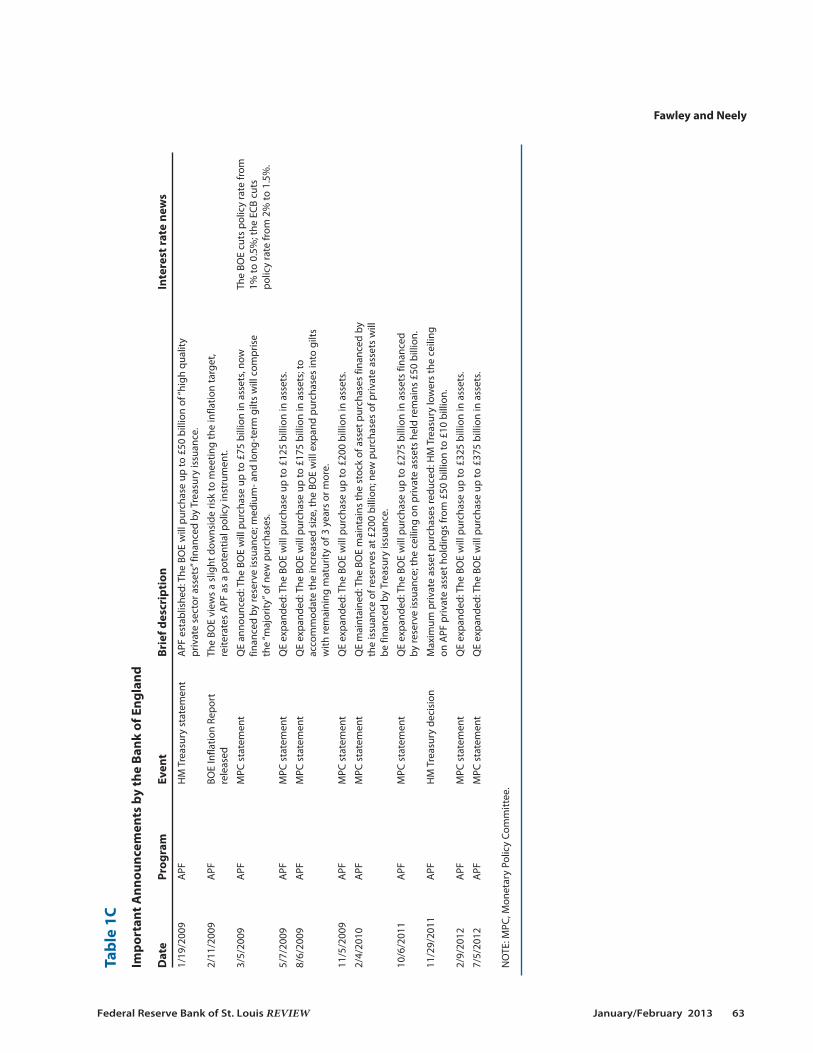

The Bank of England’s Programs. After some initial reluctance to engage in credit easingor QE, U.K. authorities announced plans to purchase assets for these purposes in January andMarch 2009. On January 19, 2009, Her Majesty’s (HM) Treasury announced the establishmentof the Asset Purchase Facility (APF), which was to be operated by the BOE. The BOE conducted

Fawley and Neely

60 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 61

Table 1A

Important Announcem

ents by the Federal Reserve

Date

Program

Event

Brief description

Interest rate news

11/2

5/20

08Q

E1FO

MC

stat

emen

tLS

APs

ann

ounc

ed: F

ed w

ill p

urch

ase

$100

bill

ion

in G

SE d

ebt a

nd $

500

billi

on

in M

BS.

12/1

/200

8Q

E1Be

rnan

ke s

peec

hFi

rst s

ugge

stio

n of

ext

endi

ng Q

E to

Tre

asur

ies.

12/1

6/20

08Q

E1FO

MC

stat

emen

tFi

rst s

ugge

stio

n of

ext

endi

ng Q

E to

Tre

asur

ies

by F

OM

C.Th

e Fe

d cu

ts th

e fe

dera

l fun

ds

rate

from

1%

to 0

.00-

0.25

%;

expe

cts

low

rate

s “fo

r som

e tim

e.”1/

28/2

009

QE1

FOM

C st

atem

ent

Fed

stan

ds re

ady

to e

xpan

d Q

E an

d bu

y Tr

easu

ries.

3/18

/200

9Q

E1FO

MC

stat

emen

tLS

APs

exp

ande

d: F

ed w

ill p

urch

ase

$300

bill

ion

in lo

ng-t

erm

Tre

asur

ies

and

Fed

expe

cts

low

rate

s fo

r an

add

ition

al $

750

and

$100

bill

ion

in M

BS a

nd G

SE d

ebt,

resp

ectiv

ely.

“an

exte

nded

per

iod.

”8/

12/2

009

QE1

FOM

C st

atem

ent

LSA

Ps s

low

ed: A

ll pu

rcha

ses

will

fini

sh b

y th

e en

d of

Oct

ober

, not

mid

-Sep

tem

ber.

9/23

/200

9Q

E1FO

MC

stat

emen

tLS

APs

slo

wed

: Age

ncy

debt

and

MBS

pur

chas

es w

ill fi

nish

at t

he e

nd o

f 201

0:Q

1.11

/4/2

009

QE1

FOM

C st

atem

ent

LSA

Ps d

owns

ized

: Age

ncy

debt

pur

chas

es w

ill fi

nish

at $

175

billi

on.

8/10

/201

0Q

E1FO

MC

stat

emen

tBa

lanc

e sh

eet m

aint

aine

d: T

he F

ed w

ill re

inve

st p

rinci

pal p

aym

ents

from

LSA

Ps

in T

reas

urie

s.8/

27/2

010

QE2

Bern

anke

spe

ech

Bern

anke

sug

gest

s ro

le fo

r add

ition

al Q

E “s

houl

d fu

rthe

r act

ion

prov

e ne

cess

ary.”

9/21

/201

0Q

E2FO

MC

stat

emen

tFO

MC

emph

asiz

es lo

w in

flatio

n, w

hich

“is

likel

y to

rem

ain

subd

ued

for s

ome

time

befo

re ri

sing

to le

vels

the

Com

mitt

ee c

onsi

ders

con

sist

ent w

ith it

s m

anda

te.”

10/1

2/20

10Q

E2FO

MC

min

utes

rele

ased

FOM

C m

embe

rs’ “s

ense

” is

that

“[ad

ditio

nal]

acco

mm

odat

ion

may

be

appr

opria

te

befo

re lo

ng.”

10/1

5/20

10Q

E2Be

rnan

ke s

peec

hBe

rnan

ke re

itera

tes

that

Fed

sta

nds

read

y to

furt

her e

ase

polic

y.11

/3/2

010

QE2

FOM

C st

atem

ent

QE2

ann

ounc

ed: F

ed w

ill p

urch

ase

$600

bill

ion

in T

reas

urie

s.6/

22/2

011

QE2

FOM

C st

atem

ent

QE2

fini

shes

: Tre

asur

y pu

rcha

ses

will

wra

p up

at t

he e

nd o

f mon

th, a

s sc

hedu

led;

pr

inci

pal p

aym

ents

will

con

tinue

to b

e re

inve

sted

.9/

21/2

011

Mat

urity

Ext

ensi

on

FOM

C st

atem

ent

Mat

urity

Ext

ensi

on P

rogr

am (“

Ope

ratio

n Tw

ist”

) ann

ounc

ed: T

he F

ed w

ill p

urch

ase

Prog

ram

$400

bill

ion

of T

reas

urie

s w

ith re

mai

ning

mat

uriti

es o

f 6 to

30

year

s an

d se

ll an

eq

ual a

mou

nt w

ith re

mai

ning

mat

uriti

es o

f 3 y

ears

or l

ess;

MBS

and

age

ncy

debt

pr

inci

pal p

aym

ents

will

no

long

er b

e re

inve

sted

in T

reas

urie

s, bu

t ins

tead

in M

BS.

6/20

/201

2M

atur

ity E

xten

sion

FO

MC

stat

emen

tM

atur

ity E

xten

sion

Pro

gram

ext

ende

d: T

he F

ed w

ill c

ontin

ue to

pur

chas

e lo

ng-t

erm

Pr

ogra

mse

curit

ies

and

sell

shor

t-te

rm s

ecur

ities

thro

ugh

the

end

of 2

012.

Pur

chas

es/s

ales

w

ill c

ontin

ue a

t the

cur

rent

pac

e, a

bout

$45

bill

ion/

mon

th.

8/22

/201

2Q

E3FO

MC

min

utes

rele

ased

FOM

C m

embe

rs “j

udge

d th

at a

dditi

onal

mon

etar

y ac

com

mod

atio

n w

ould

like

ly

be w

arra

nted

fairl

y so

on…

”9/

13/2

012

QE3

FOM

C st

atem

ent

QE3

ann

ounc

ed: T

he F

ed w

ill p

urch

ase

$40

billi

on o

f MBS

per

mon

th a

s lo

ng

Fed

expe

cts

low

rate

s “at

as “t

he o

utlo

ok fo

r the

labo

r mar

ket d

oes

not i

mpr

ove

subs

tant

ially

…in

the

leas

t thr

ough

mid

-201

5.”

cont

ext o

f pric

e st

abili

ty.”

12/1

2/20

12Q

E3FO

MC

stat

emen

tQ

E3 e

xpan

ded:

The

Fed

will

con

tinue

to p

urch

ase

$45

billi

on o

f lon

g-te

rm

The

Fed

expe

cts

low

rate

s to

Trea

surie

s pe

r mon

th b

ut w

ill n

o lo

nger

ste

riliz

e pu

rcha

ses

thro

ugh

the

sale

be a

ppro

pria

te w

hile

une

m-

of s

hort

-ter

m T

reas

urie

s.pl

oym

ent i

s ab

ove

6.5

perc

ent

and

infla

tion

is fo

reca

sted

be

low

2.5

per

cent

.

NO

TE: T

he a

ppen

dix

prov

ides

URL

s fo

r the

offi

cial

pol

icy

stat

emen

ts in

clud

ed in

Tab

les

1A-1

D a

nd th

ose

disc

usse

d in

the

text

.

Fawley and Neely

62 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

Table 1B

Important Announcem

ents by the European Central Bank

Date

Program

Event

Brief description

Interest rate news

3/28

/200

8LT

ROG

over

ning

Cou

ncil

LTRO

exp

ande

d: 6

-mon

th L

TRO

s ar

e an

noun

ced.

pres

s re

leas

e

10/1

5/20

08FR

FAG

over

ning

Cou

ncil

Refin

anci

ng o

pera

tions

exp

ande

d: A

ll re

finan

cing

ope

ratio

ns w

ill b

e pr

ess

rele

ase

cond

ucte

d w

ith fi

xed-

rate

tend

ers

and

full

allo

tmen

t; th

e lis

t of a

sset

s el

igib

le

as c

olla

tera

l in

cred

it op

erat

ions

with

the

Bank

is e

xpan

ded

to in

clud

ed lo

wer

-ra

ted

(with

the

exce

ptio

n of

ass

et-b

acke

d se

curit

ies)

and

non

-eur

o-de

nom

inat

edas

sets

.

5/7/

2009

CBPP

/LTR

OG

over

ning

Cou

ncil

CBPP

ann

ounc

ed/L

TRO

exp

ande

d: T

he E

CB w

ill p

urch

ase

€60

billi

on in

EC

B lo

wer

s th

e m

ain

pres

s re

leas

eeu

ro-d

enom

inat

ed c

over

ed b

onds

; 12-

mon

th L

TRO

s ar

e an

noun

ced.

re

finan

cing

rate

by

0.25

%

to 1

% a

nd th

e ra

te o

n th

e m

argi

nal l

endi

ng fa

cilit

y by

0.

50%

to 1

.75%

.

5/10

/201

0SM

PG

over

ning

Cou

ncil

SMP

anno

unce

d: T

he E

CB w

ill c

ondu

ct in

terv

entio

ns in

the

euro

are

a pu

blic

pr

ess

rele

ase

and

priv

ate

debt

sec

uriti

es m

arke

ts; p

urch

ases

will

be

ster

ilize

d.

6/30

/201

0CB

PPG

over

ning

Cou

ncil

CBPP

fini

shed

: Pur

chas

es fi

nish

on

sche

dule

; bon

ds p

urch

ased

will

be

held

pr

ess

rele

ase

thro

ugh

mat

urity

.

10/6

/201

1CB

PP2

Gov

erni

ng C

ounc

il CB

PP2

anno

unce

d: T

he E

CB w

ill p

urch

ase

€40

billi

on in

eur

o-de

nom

inat

ed

pres

s re

leas

eco

vere

d bo

nds.

12/8

/201

1LT

ROG

over

ning

Cou

ncil

LTRO

exp

ande

d: 3

6-m

onth

LTR

Os

are

anno

unce

d; e

ligib

le c

olla

tera

l is

ECB

low

ers

the

mai

n pr

ess

rele

ase

expa

nded

.re

finan

cing

rate

by

0.25

%

to 1

%, a

nd th

e ra

te o

n th

e m

argi

nal l

endi

ng fa

cilit

y by

0.

25%

to 1

.75%

.

8/2/

2012

OM

TEC

B pr

ess

conf

eren

ceEC

B Pr

esid

ent M

ario

Dra

ghi i

ndic

ates

that

the

ECB

will

exp

and

sove

reig

n de

bt p

urch

ases

. He

proc

laim

s th

at “t

he e

uro

is ir

reve

rsib

le.”

9/6/

2012

OM

TG

over

ning

Cou

ncil

OM

Ts a

nnou

nced

: Cou

ntrie

s th

at a

pply

to th

e Eu

rope

an S

tabi

lizat

ion

pres

s re

leas

eM

echa

nism

(ESM

) for

aid

and

abi

de b

y th

e ES

M’s

term

s an

d co

nditi

ons

will

be

elig

ible

to h

ave

thei

r deb

t pur

chas

ed in

unl

imite

d am

ount

s on

the

seco

ndar

y m

arke

t by

the

ECB.

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 63

Table 1C

Important Announcem

ents by the Bank of England

Date

Program

Event

Brief description

Interest rate news

1/19

/200

9A

PFH

M T

reas

ury

stat

emen

tA

PF e

stab

lishe

d: T

he B

OE

will

pur

chas

e up

to £

50 b

illio

n of

“hig

h qu

ality

pr

ivat

e se

ctor

ass

ets”

fina

nced

by

Trea

sury

issu

ance

.

2/11

/200

9A

PFBO

E In

flatio

n Re

port

Th

e BO

E vi

ews

a sl

ight

dow

nsid

e ris

k to

mee

ting

the

infla

tion

targ

et,

rele

ased

reite

rate

s A

PF a

s a

pote

ntia

l pol

icy

inst

rum

ent.

3/5/

2009

APF

MPC

sta

tem

ent

QE

anno

unce

d: T

he B

OE

will

pur

chas

e up

to £

75 b

illio

n in

ass

ets,

now

Th

e BO

E cu

ts p

olic

y ra

te fr

om

finan

ced

by re

serv

e is

suan

ce; m

ediu

m- a

nd lo

ng-t

erm

gilt

s w

ill c

ompr

ise

1% to

0.5

%; t

he E

CB c

uts

the

“maj

ority

” of n

ew p

urch

ases

.po

licy

rate

from

2%

to 1

.5%

.

5/7/

2009

APF

MPC

sta

tem

ent

QE

expa

nded

: The

BO

E w

ill p

urch

ase

up to

£12

5 bi

llion

in a

sset

s.

8/6/

2009

APF

MPC

sta

tem

ent

QE

expa

nded

: The

BO

E w

ill p

urch

ase

up to

£17

5 bi

llion

in a

sset

s; to

ac

com

mod

ate

the

incr

ease

d si

ze, t

he B

OE

will

exp

and

purc

hase

s in

to g

ilts

with

rem

aini

ng m

atur

ity o

f 3 y

ears

or m

ore.

11/5

/200

9A

PFM

PC s

tate

men

tQ

E ex

pand

ed: T

he B

OE

will

pur

chas

e up

to £

200

billi

on in

ass

ets.

2/4/

2010

APF

MPC

sta

tem

ent

QE

mai

ntai

ned:

The

BO

E m

aint

ains

the

stoc

k of

ass

et p

urch

ases

fina

nced

by

the

issu

ance

of r

eser

ves

at £

200

billi

on; n

ew p

urch

ases

of p

rivat

e as

sets

will

be

fina

nced

by

Trea

sury

issu

ance

.

10/6

/201

1A

PFM

PC s

tate

men

tQ

E ex

pand

ed: T

he B

OE

will

pur

chas

e up

to £

275

billi

on in

ass

ets

finan

ced

by re

serv

e is

suan

ce; t

he c

eilin

g on

priv

ate

asse

ts h

eld

rem

ains

£50

bill

ion.

11/2

9/20

11A

PFH

M T

reas

ury

deci

sion

Max

imum

priv

ate

asse

t pur

chas

es re

duce

d: H

M T

reas

ury

low

ers

the

ceili

ngon

APF

priv

ate

asse

t hol

ding

s fr

om £

50 b

illio

n to

£10

bill

ion.

2/9/

2012

APF

MPC

sta

tem

ent

QE

expa

nded

: The

BO

E w

ill p

urch

ase

up to

£32

5 bi

llion

in a

sset

s.

7/5/

2012

APF

MPC

sta

tem

ent

QE

expa

nded

: The

BO

E w

ill p

urch

ase

up to

£37

5 bi

llion

in a

sset

s.

NO

TE: M

PC, M

onet

ary

Polic

y Co

mm

ittee

.

Fawley and Neely

64 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

Table 1D

Important Announcem

ents by the Bank of Japan

Date

Program

Event

Brief description

Interest rate news

12/2

/200

8SF

SOs

Uns

ched

uled

mon

etar

y Th

e BO

J w

ill o

pera

te a

faci

lity

thro

ugh

the

end

of A

pril

to le

nd a

n un

limite

d po

licy

mee

ting

amou

nt to

ban

ks a

t the

unc

olla

tera

lized

ove

rnig

ht c

all r

ate

and

colla

tera

lized

by

cor

pora

te d

ebt.

12/1

9/20

08O

utrig

ht J

GB/

CFI

Stat

emen

t on

Out

right

pur

chas

es e

xpan

ded:

The

BO

J in

crea

ses

mon

thly

JG

B pu

rcha

ses

The

BOJ

low

ers

the

targ

et fo

r pu

rcha

ses

mon

etar

y po

licy

(last

incr

ease

d O

ctob

er 2

002)

from

¥1.

2 tr

illio

n to

¥1.

4 tr

illio

n; th

ey w

ill a

lso

the

unco

llate

raliz

ed o

vern

ight

lo

ok in

to p

urch

asin

g co

mm

erci

al p

aper

.ca

ll ra

te fr

om 0

.3%

to 0

.1%

.

1/22

/200

9O

utrig

ht C

FI

Stat

emen

t on

Out

right

pur

chas

es a

nnou

nced

: The

BO

J w

ill p

urch

ase

up to

¥3

trill

ion

in

purc

hase

sm

onet

ary

polic

yco

mm

erci

al p

aper

and

ABC

P an

d is

inve

stig

atin

g ou

trig

ht p

urch

ases

of

corp

orat

e bo

nds.

2/19

/200

9O

utrig

ht C

FI

Stat

emen

t on

Out

right

pur

chas

es e

xpan

ded:

The

BO

J w

ill e

xten

d co

mm

erci

al p

aper

purc

hase

sm

onet

ary

polic

ypu

rcha

ses

and

the

SFSO

s th

roug

h th

e en

d of

Sep

tem

ber (

prev

ious

ly e

nd o

f M

arch

) and

will

pur

chas

e up

to ¥

1 tr

illio

n in

cor

pora

te b

onds

.

3/18

/200

9O

utrig

ht J

GB

Stat

emen

t on

Out

right

pur

chas

es e

xpan

ded:

The

BO

J in

crea

ses

mon

thly

JG

B pu

rcha

ses

from

pu

rcha

ses

mon

etar

y po

licy

¥1.4

trill

ion

to ¥

1.8

trill

ion.

7/15

/200

9O

utrig

ht C

FI

Stat

emen

t on

Prog

ram

s ex

tend

ed: T

he B

OJ

exte

nds

the

SFSO

s an

d ou

trig

ht p

urch

ases

of

purc

hase

s/SF

SOs

mon

etar

y po

licy

corp

orat

e pa

per a

nd b

onds

thro

ugh

the

end

of th

e ye

ar.

10/3

0/20

09O

utrig

ht C

FI

Stat

emen

t on

Stat

us o

f pro

gram

s: O

utrig

ht p

urch

ases

of c

orpo

rate

fina

nce

inst

rum

ents

will

pu

rcha

ses/

SFSO

sm

onet

ary

polic

yex

pire

at t

he e

nd o

f 200

9 as

exp

ecte

d, b

ut th

e SF

SOs

will

be

exte

nded

thro

ugh

2010

:Q1;

am

ple

liqui

dity

pro

visi

on p

ast 2

010:

Q1

will

occ

ur th

roug

h fu

nds-

supp

lyin

g op

erat

ions

aga

inst

poo

led

colla

tera

l, w

hich

will

acc

ept a

larg

er ra

nge

of c

olla

tera

l.

12/1

/200

9FR

Os

Stat

emen

t on

Faci

lity

anno

unce

men

t: Th

e BO

J w

ill o

ffer ¥

10 tr

illio

n in

3-m

onth

loan

s ag

ains

t m

onet

ary

polic

yth

e fu

ll m

enu

of e

ligib

le c

olla

tera

l at t

he u

ncol

late

raliz

ed o

vern

ight

cal

l rat

e.

3/17

/201

0FR

Os

Stat

emen

t on

Faci

lity

expa

nsio

n: T

he B

OJ

expa

nds

the

size

of t

he F

ROs

to ¥

20 tr

illio

n.m

onet

ary

polic

y

5/21

/201

0G

SFF

Stat

emen

t on

GSF

F an

noun

cem

ent:

The

BOJ

will

offe

r ¥3

trill

ion

in 1

-yea

r loa

ns to

priv

ate

mon

etar

y po

licy

finan

cial

inst

itutio

ns w

ith p

roje

ct p

ropo

sals

for “

stre

ngth

enin

g th

e fo

unda

tions

fo

r eco

nom

ic g

row

th.”

8/30

/201

0FR

Os

Uns

ched

uled

mon

etar

y Fa

cilit

y ex

pans

ion:

The

BO

J ad

ds ¥

10 tr

illio

n in

6-m

onth

loan

s to

the

FRO

s.po

licy

mee

ting

10/5

/201

0CM

ESt

atem

ent o

n A

PP e

stab

lishe

d: T

he B

OJ

will

pur

chas

e ¥5

trill

ion

in a

sset

s (¥

3.5

trill

ion

in J

GBs

Th

e BO

J se

ts th

e ta

rget

for t

he

mon

etar

y po

licy

and

Trea

sury

dis

coun

t bill

s, ¥1

trill

ion

in c

omm

erci

al p

aper

and

cor

pora

te

unco

llate

raliz

ed o

vern

ight

cal

l bo

nds,

and

¥0.5

trill

ion

in E

TFs

and

J-RE

ITs)

. ra

te a

t aro

und

0 to

0.1

%.

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 65

Table 1D, cont’d

Important Announcem

ents by the Bank of Japan

Date

Program

Event

Brief description

Interest rate news

3/14

/201

1CM

ESt

atem

ent o

n A

PP e

xpan

ded:

The

BO

J w

ill p

urch

ase

an a

dditi

onal

¥5

trill

ion

in a

sset

s m

onet

ary

polic

y(¥

0.5

trill

ion

in J

GBs

, ¥1

trill

ion

in T

reas

ury

disc

ount

bill

s, ¥1

.5 tr

illio

n in

co

mm

erci

al p

aper

, ¥1.

5 tr

illio

n in

cor

pora

te b

onds

, ¥0.

45 tr

illio

n in

ETF

s, an

d ¥0

.05

trill

ion

in J

-REI

Ts).

6/14

/201

1G

SFF

Stat

emen

t on

GSF

F ex

pand

ed: T

he B

OJ

mak

es a

vaila

ble

anot

her ¥

0.5

trill

ion

in lo

ans

to

mon

etar

y po

licy

priv

ate

finan

cial

inst

itutio

ns fo

r the

pur

pose

of i

nves

ting

in e

quity

and

ex

tend

ing

asse

t-ba

sed

loan

s.

8/4/

2011

CME

Stat

emen

t on

APP

/FRO

s ex

pand

ed: T

he B

OJ

will

pur

chas

e an

add

ition

al ¥

5 tr

illio

n in

ass

ets

mon

etar

y po

licy

(¥2

trill

ion

in J

GBs

, ¥1.

5 tr

illio

n in

Tre

asur

y di

scou

nt b

ills,

¥0.1

trill

ion

in

com

mer

cial

pap

er, ¥

0.9

trill

ion

in c

orpo

rate

bon

ds, ¥

0.5

trill

ion

in E

TFs,

and

¥0.0

1 tr

illio

n in

J-R

EITs

); 6-

mon

th c

olla

tera

lized

loan

s th

roug

h th

e FR

Os

are

expa

nded

by

¥5 tr

illio

n.

10/2

7/20

11CM

ESt

atem

ent o

n A

PP e

xpan

ded:

The

BO

J w

ill p

urch

ase

an a

dditi

onal

¥5

trill

ion

in J

GBs

.m

onet

ary

polic

y

2/14

/201

2CM

ESt

atem

ent o

n A

PP e

xpan

ded:

The

BO

J w

ill p

urch

ase

an a

dditi

onal

¥10

trill

ion

in J

GBs

.m

onet

ary

polic

y

3/13

/201

2G

SFF

Stat

emen

t on

GSF

F ex

pand

ed: T

he B

OJ

mak

es a

vaila

ble

anot

her ¥

2 tr

illio

n in

loan

s to

priv

ate

mon

etar

y po

licy

finan

cial

inst

itutio

ns, i

nclu

ding

¥1

trill

ion

in U

.S.-d

olla

r-de

nom

inat

ed lo

ans

and

¥0.5

trill

ion

in s

mal

ler-

size

d (¥

1 m

illio

n-¥1

0 m

illio

n) lo

ans.

4/27

/201

2CM

ESt

atem

ent o

n A

PP e

xpan

ded/

FRO

s re

duce

d: T

he B

OJ

will

pur

chas

e an

add

ition

al ¥

10 tr

illio

n m

onet

ary

polic

yin

JG

Bs, ¥

0.2

trill

ion

in E

TFs,

and

¥0.0

1 in

J-R

EITs

. The

BoJ

als

o re

duce

s th

e av

aila

bilit

y of

6-m

onth

FRO

loan

s by

¥5

trill

ion.

7/12

/201

2CM

ESt

atem

ent o

n A

PP e

xpan

ded/

FRO

s re

duce

d: T

he B

OJ

will

pur

chas

e an

add

ition

al ¥

5 tr

illio

n in

m

onet

ary

polic

yTr

easu

ry d

isco

unt b

ills

and

redu

ces

the

avai

labi

lity

of F

RO lo

ans

by ¥

5 tr

illio

n.

9/19

/201

2CM

ESt

atem

ent o

n A

PP e

xpan

ded:

The

BO

J w

ill p

urch

ase

an a

dditi

onal

¥5

trill

ion

in J

GBs

and

m

onet

ary

polic

y¥5

trill

ion

in T

reas

ury

disc

ount

bill

s.

10/3

0/20

12CM

E/SB

LFSt

atem

ent o

nA

PP e

xpan

ded/

SBLF

ann

ounc

ed: T

he B

OJ

will

pur

chas

e an

add

ition

al ¥

5 tr

illio

n m

onet

ary

polic

yin

JG

Bs, ¥

5 tr

illio

n in

Tre

asur

y di

scou

nt b

ills,

¥0.1

trill

ion

in c

omm

erci

al p

aper

, ¥0

.3 tr

illio

n in

cor

pora

te b

onds

, ¥0.

5 tr

illio

n in

ETF

s, an

d ¥0

.01

trill

ion

in J

-REI

Ts.

Thro

ugh

the

SBLF

it w

ill fu

nd u

p to

100

per

cent

of d

epos

itory

inst

itutio

ns’ n

et

incr

ease

in le

ndin

g to

the

nonf

inan

cial

sec

tor.

12/2

0/20

12CM

ESt

atem

ent o

nA

PP e

xpan

ded:

The

BO

J w

ill p

urch

ase

an a

dditi

onal

¥5

trill

ion

JGBs

and

¥5

trill

ion

mon

etar

y po

licy

in T

reas

ury

disc

ount

bill

s.

NO

TE: C

FI, c

orpo

rate

fina

nce

inst

rum

ents

(cor

pora

te b

onds

plu

s co

mm

erci

al p

aper

); CM

E, c

ompr

ehen

sive

mon

etar

y ea

sing

.

two separate and distinct asset purchase programs through this newly established APF: privateasset purchases to ease specific credit conditions and more traditional QE for monetary stimulus.

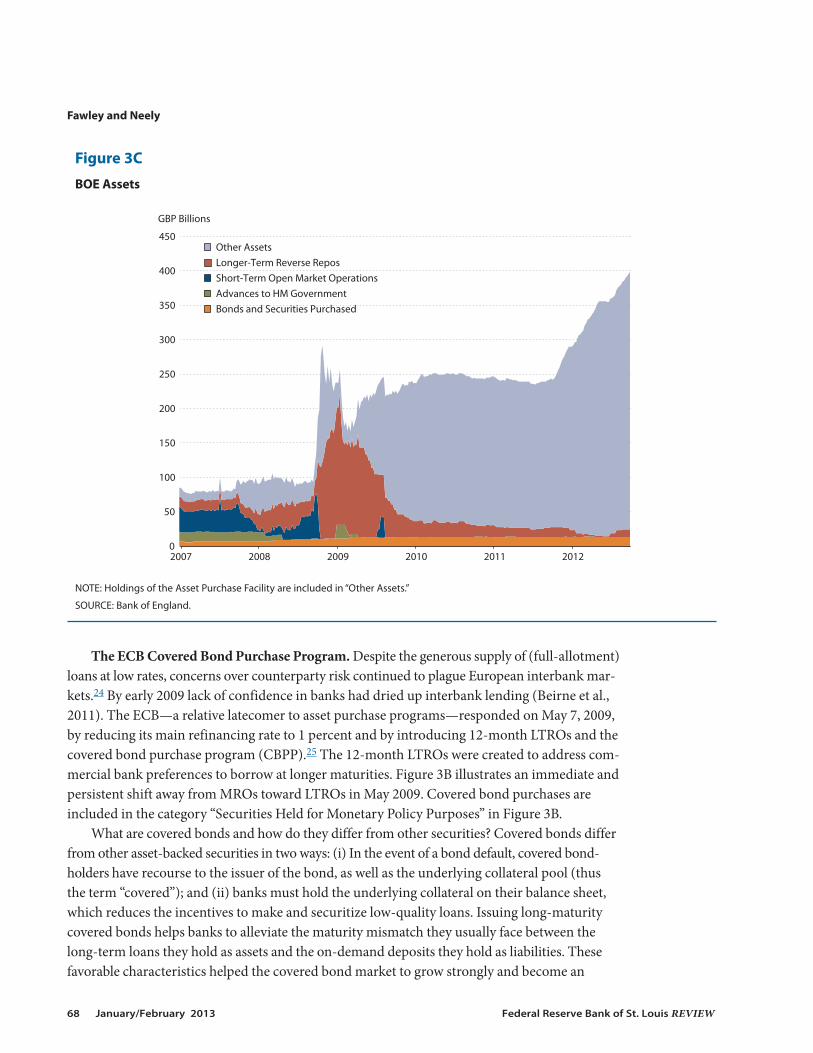

HM Treasury’s January 19, 2009, announcement inaugurated the private asset purchaseprogram; it authorized the BOE to buy up to £50 billion in “high quality private sector assets” to “increase the availability of corporate credit, by reducing the illiquidity of the underlyinginstruments.”19 Because HM Treasury issued (sold) short-term gilts to finance the purchases,every asset that the BOE purchased was matched by a sale of a short-term gilt and so the BOE’sliabilities (the monetary base) did not initially increase. That is, this was not initially QE.

The BOE later described its private asset purchases as “an example of the Bank acting asmarket maker of last resort” (BOE, 2012). The BOE likewise purchased corporate bonds througha reverse auction; potential counterparties bid on the price at which they would sell assets to theBOE.20 The program was designed so the BOE’s appeal as a counterparty would diminish asmarket conditions improved.

In a program similar to the Fed’s CPFF, the BOE purchased commercial paper at a fixedspread above the local risk-free OIS rates, which established a floor for the price of high-qualitycommercial paper. In both the United States and United Kingdom, the presence of a market

Fawley and Neely

66 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011 2012

USD Billions

Lending to Financial Firms and Markets Rescue Operations Agency and MBS Holdings Treasury Holdings (>1 year) Treasury Holdings (<1 year) Other Assets

Figure 3A

Federal Reserve Bank Assets

NOTE: “Lending to Financial Firms and Markets” includes repurchase agreements, term auction credit, the CPFF, central bank liquidity swaps, themoney market investor funding facility, other loans, and the Term Asset-Backed Securities Loan Facility (TALF). “Rescue Operations” includes netportfolio holdings of Maiden Lanes I, II, and III and preferred interests in AIA Aurora and ALICO Holdings. The figure shows the accumulation ofagency and MBS holdings on the Fed balance sheet beginning in November 2008 and long-term Treasury securities beginning in March 2009.

SOURCE: Federal Reserve statistical release H.4.1.

maker of last resort quickly restored market functioning and the price floor established by thepurchase programs did not bind for long. Ultimately, neither the Fed nor the BOE purchasedlarge quantities of private assets. The BOE’s private asset holdings peaked in 2009:Q2 at less than£3 billion, or 6 percent of the £50 billion ceiling announced in January 2009.21

On March 5, 2009, the BOE announced that the APF would administer an explicit QE pro-gram that targeted a £75 billion increase in the monetary base, which in later announcements(through November) would expand to £200 billion. The BOE’s Red Book states, “[T]he objectiveof Quantitative Easing is to boost the money supply through large-scale asset purchases and, indoing so, to bring about a level of nominal demand consistent with meeting the inflation targetin the medium term” (BOE, 2012, p. 10).22 The BOE directed QE purchases toward the deepand liquid markets in medium- and long-term gilts. To increase the monetary base, the BOEfinanced all new APF purchases by issuing money (central bank reserves) rather than issuinggilts. The short-term gilts issued to finance earlier purchases were allowed to mature withoutrenewal, and by the end of 2009:Q2 bank reserves backed all assets held in the APF.23 Figure 4shows that the BOE’s QE program almost quadrupled the U.K. monetary base within a fewmonths as bond purchases replaced longer-term reverse repos.

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 67

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2006 2007 2008 2009 2010 2011 2012

EUR Billions

Securities Held for Monetary Policy Purposes

LTROs

Other Assets

General Government Debt

Other Securities

MROs

Claims on Euro Area Residents Denominated in Foreign Currency

Claims on Non-Euro Area Residents

Figure 3B

ECB Assets

NOTE: Main (longer-term) refinancing operations are abbreviated MROs (LTROs). The ECB disaggregates its securities holdings into those heldfor monetary policy purposes, which include covered bond and sovereign debt purchases, and other securities. The figure shows the spike inlending (MROs and LTROs) following the availability of unlimited funds at the fixed rate in October 2008.

SOURCE: ECB.

The ECB Covered Bond Purchase Program. Despite the generous supply of (full-allotment)loans at low rates, concerns over counterparty risk continued to plague European interbank mar-kets.24 By early 2009 lack of confidence in banks had dried up interbank lending (Beirne et al.,2011). The ECB—a relative latecomer to asset purchase programs—responded on May 7, 2009,by reducing its main refinancing rate to 1 percent and by introducing 12-month LTROs and thecovered bond purchase program (CBPP).25 The 12-month LTROs were created to address com-mercial bank preferences to borrow at longer maturities. Figure 3B illustrates an immediate andpersistent shift away from MROs toward LTROs in May 2009. Covered bond purchases areincluded in the category “Securities Held for Monetary Policy Purposes” in Figure 3B.

What are covered bonds and how do they differ from other securities? Covered bonds differfrom other asset-backed securities in two ways: (i) In the event of a bond default, covered bond-holders have recourse to the issuer of the bond, as well as the underlying collateral pool (thusthe term “covered”); and (ii) banks must hold the underlying collateral on their balance sheet,which reduces the incentives to make and securitize low-quality loans. Issuing long-maturitycovered bonds helps banks to alleviate the maturity mismatch they usually face between thelong-term loans they hold as assets and the on-demand deposits they hold as liabilities. Thesefavorable characteristics helped the covered bond market to grow strongly and become an

Fawley and Neely

68 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012

GBP Billions

Other AssetsLonger-Term Reverse ReposShort-Term Open Market OperationsAdvances to HM GovernmentBonds and Securities Purchased

Figure 3C

BOE Assets

NOTE: Holdings of the Asset Purchase Facility are included in “Other Assets.”

SOURCE: Bank of England.

important source of funding for European banks: from €1.5 trillion in 2003 to €2.4 trillion by theend of 2008 (Beirne et al., 2011).

Although the covered bond market functioned well throughout most of the financial crisis,the Lehman Brothers bankruptcy in September 2008 seriously impaired even this market. Inresponse, on May 7, 2009, the ECB committed to purchase €60 billion in covered bonds, orroughly 2.5 percent of the outstanding bonds. Jean-Claude Trichet, then president of the ECB,adamantly maintained that the program was not QE and would not expand the ECB’s balancesheet. Rather, Trichet stated that he expected “automatic sterilization” as the covered bond pur-chases would commensurately reduce demand for the elastically supplied LTROs. Trichet justi-fied the program in terms of credit easing: “[T]he idea is to revive the market, which has beenvery heavily affected, and all that goes with this revival, including the spreads and the depth andthe liquidity of the market.”26

The results of the CBPP and LTRO expansion were mixed. The €60 billion in ECB purchasesstimulated €150 billion in issuance, though much of the new issuance represented a switch fromuncovered bond to covered bond issuance.27 ECB LTRO announcements failed to reduce credit

Fawley and Neely

Federal Reserve Bank of St. Louis REVIEW January/February 2013 69

0

20

40

60

80

100

120

140

160

180

200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

JPY Trillions ZIRP Bill Purchases

Receivables Under Resale Agreements

Government Bonds

Foreign Currency Assets

Funds-Supplying Operations Against Pooled Collateral

Private Assets

Government Bills

Other Assets

Figure 3D

BOJ Assets

NOTE: “Government Bonds” includes monthly JGB purchases. “ZIRP Bill Purchases” includes public debt purchases made under Japan’s ZIRP aspart of its QE program in the early 2000s but excludes monthly JGB purchases. “Private Assets” includes all purchases of commercial paper,commercial bonds, ETFs, J-REITs, stocks, and MBS. On June 26, 2006, the BOJ introduced new electronic operations (“Funds-Supplying OperationsAgainst Pooled Collateral”) to replace conventional paper-based bill purchasing operations.

SOURCE: Bank of Japan.

risk, with one exception: The May 7, 2009, LTRO/CBPP announcement reduced credit defaultswap rates on the Markit iTraxx index of senior (subordinated) debt issued by the 25 largestEuropean finance firms by roughly 28 (14) basis points.

BOJ Bond Purchases. The BOJ also expanded its FRFA bank loans into outright bond pur-chases. On December 19, 2008, the BOJ increased its monthly purchases of JGBs for the firsttime since October 200228 and announced interest in purchasing corporate finance instruments.The BOJ followed up by announcing reverse-auction purchases of up to ¥3 trillion in commercialpaper and ¥1 trillion in corporate bonds on January 22, 2009, and February 19, 2009, respectively.As with the Fed’s and BOE’s purchases of corporate finance instruments, the existence of a regu-lar buyer increased prices by reducing liquidity risk; more buyers for the assets emerged andtrade resumed. Offers to sell to the BOJ quickly diminished. On March 18, 2009, the BOJ increasedJGB purchases to an annual rate of ¥21.6 trillion.

Fawley and Neely

70 January/February 2013 Federal Reserve Bank of St. Louis REVIEW

2008 2009 2010 2011 2012100

200

300

400

Index (2007:Q1 = 100) U.S.

Monetary BaseM2

2008 2009 2010 2011 2012100

200

300

Index (2007:Q1 = 100) European Monetary Union

2008 2009 2010 2011 2012

100

120

140

Index (2007:Q1 = 100) Japan

2008 2009 2010 2011 2012

200

400

600

Index (2007:Q1 = 100) U.K.

Figure 4

Monetary Base and M2 Expansion

SOURCE: Federal Reserve Board, ECB, BOJ, and BOE.

Summary. Although all four central banks announced outright asset purchases from thefall of 2008 through the spring of 2009, the Fed and BOE targeted large amounts of assets topurchase, but the ECB and BOJ chose to ease their monetary policy stance primarily by elasti-cally supplying loans. Their outright asset purchases were generally small and targeted specificassets. The ECB’s and BOJ’s use of bank loans, rather than bond purchases, to expand the mone-tary base reflects both the desire to specifically support their banking sectors, hit hard by thefinancial crisis, and the relatively greater importance of banks, as opposed to bond markets, inEurope and Japan. At the end of 2007, the U.S. (European) stock of outstanding bank loans tothe private sector totaled 63 percent (145 percent) of gross domestic product (GDP). By contrast,outstanding debt securities in the United States (Europe) accounted for 168 percent (81 percent)of GDP (Bini Smaghi, 2009).