Embed Size (px)

Citation preview

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Tony Surtees

Founding VP and GM, Yahoo! Commerce Group

CEO, Santa Clara Group

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Shoot your Marketing Manager…Shoot your Marketing Manager…

RMIT BUSINESS DEAN’S LECTURE SERIESJune 17 2003

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Lessons from

• User experience drives everything

• Technology creates new opportunities

• Led by the market

• Human face to technology

• Power of a global brand & local relevance

• eBay!

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market changed forever

Brands win, Experience Delivers, Ads?

Networks are everywhere

Marketing led by CFO, CIO & CEO

Marketing+Finance+Technology

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Coca ColaCoca Cola

“Here at Coca-Cola we're thinking about marketing in a radically different way”

Steven J. Heyer COO, Coca Cola Co.

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“While we recognize great advertising and great marketing,this year one of the biggest awards we gave out was for marketing ROI…”

“We are going to learn how to leverage more knowledge, scale and drive the efficiency and the effectiveness of our marketing investment.”

P&G CEO A.G.P&G CEO A.G. LafeyLafey

June 17, 2003 ©Santa Clara Group Pty Ltd scg

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Trends

• Fragmentation & proliferation of media

• Erosion of mass markets

• Global market for talent, capital

• Next leap in productivity?

• Marketing is the target!

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market changed forever

Brands win, Experience Delivers, Ads?

Networks are everywhere

Marketing led by CFO, CIO & CEO

Marketing+Finance+Technology

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“CFOs used to see the brand as ‘soft’… Du Pont is turning the softness of brand valuations into hard numbers.”

Carol Gee, Du Pont Global Director of Brands for Apparel and Textile SciencesCFO Magazine, November 2001, p99

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“The common ground around companies that have built great brands

is not performance. They recognize that consumers live in an emotional

world. Emotions drive most, if not all, our decisions”

Scott Bedbury, Starbucks

Brand leaders deliver experiences

These companies have outperformed the stock market for the last fifteen years and secured the greatest share of wallet

Citibank-Interbrand study 1998

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“This is the end of the pure product era. We are a platform for delivering services that drive the customer experience.”

Carly Fiorina, CEO - HP

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“What British Airways does is to go beyond the function and compete

on the basis of providing an experience.”

Sir Colin Marshall, British AirwaysSir Colin Marshall, British Airways

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Expectations affects experienceExpectations affects experience

June 17, 2003 ©Santa Clara Group Pty Ltd scg

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Effectiveness of advertisingEffectiveness of advertising

• 30% of media had major positive effects

• 20% of media had minor positive effects

• 50% of media had NO positive effects

Marder, Eric. “The Laws of Choice: Predicting Customer Behavior.” ( in Professional Investor, Feb. 2003, p25)

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Intel had better than an 80% market share in microprocessors …

…before it ran its first "Intel Inside" ad

June 17, 2003 ©Santa Clara Group Pty Ltd scg

What ad agencies & marketers think about each other?

June 17, 2003 ©Santa Clara Group Pty Ltd scg

“rests on the assumption that a repeated message can change people’s opinions and behavior and that it can keep them coming back as long as they hear or see the message often enough”

“Bob Coen’s Insiders Report”Universal McCann, McCann Erickson

June 17, 2003 ©Santa Clara Group Pty Ltd scg

• ANA• American Express • BBDO • Bayer • Beringer-Blass • Bristol-Myers

Squibb • British Airways • Brown-Forman • Campbell Soup • Carat • Citigroup • Coca-Cola • Compaq • DAS • DDB • DaimlerChrysler • D’Arcy

• Johnson & Johnson

• KFC• Kellogg • Leo Burnett • Levi Strauss • McCann-Erickson • Mars • Merrill Lynch • Microsoft • Mindshare • M-real • Nestle • Ogilvy & Mather • Omnicom • Orange • Pfizer • Procter & Gamble

• Dell • Diageo • Dow • DuPont • Eli Lilly • Ernst & Young • ExxonMobil • FutureBrand • FCB • FedEx • General Motors • Grey • Hakuhodo • Hewlett Packard • H&R Block • IBM • J Walter

Thomson

• Reckitt Benckiser • Saatchi & Saatchi • Sonera • Sony • Springpoint • TBWA • Unilever • Universal McCann • UPS • USPostal Service • United Airlines• Verizon • Volkswagen

survey by: –Nick Bishop & The O Partnership (Paris)

–Through The Loop (London)

–Bellwether Leadership Research (Detroit).

New research New research

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Agencies said …Agencies said …

• Clients provoke dislocation through a lack of clarity on what constitutes success

• No integration between clients & agencies

• Clients not (technically) structured to handle integration

• No real negotiation on remuneration

• Downward pressure on agency margins has a significant effect on client/agency relationships

• Challenged by increasingly limited talent pool

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Marketers saidMarketers said

• 70% agencies fired by new managers first 12 months

• Agencies just mirroring (their) marketing problems

• Agencies need a better understanding of client needs

• Lost the strategic partner role through cost-cutting

• Big agency groups mean big inefficiencies for clients

• Distance between expectation and delivery in the area of brand communications integration is significant

• Lack of quality resources on the agency side

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market changed forever

Brands win, Experience Delivers, Ads?

Networks are everywhere

Marketing led by CFO, CIO & CEO

Marketing+Finance+Technology

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Networks are everywhereNetworks are everywhereTalking to individual customers

Mass customization (My Yahoo!, Amazon)PersonalizationCustomer care

Talking to each otherMarket networked (IM, email & SMS)Selling each other (viral marketing, eBay)

Business networks buying groups, user groups, lobby groups, etc.Competitors – Ford & GM co-investing building common car power train

June 17, 2003 ©Santa Clara Group Pty Ltd scg

How networked are we?How networked are we?

• June 6, 2003 - In less than 24 hours, Bugbear.B has infected more computers than anything else.

23% of computers infected in 24 hrs!

June 17, 2003 ©Santa Clara Group Pty Ltd scg

technologytechnologyfinancefinance

marketingmarketing%

ROI

$

ERP CRM

24X7integrationIRR

like wow

tools

more relevant & accountable practice…

…the new CMO…

June 17, 2003 ©Santa Clara Group Pty Ltd scg

New CMONew CMO

• Owns the customer experience

• No longer “best creative marketer”

• Critical support to CEO

• Driver of shareholder value, ROIC

• Realities of market & capabilities of new tools

• Product management skills

• Performance culture with process & metrics

June 17, 2003 ©Santa Clara Group Pty Ltd scg

SuccessfulSuccessfulMarketersMarketers

AreAreBehaviouralBehavioural

PsychologistsPsychologists

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market changed forever

Brands win, Experience Delivers, Ads?

Networks are everywhere

Marketing led by CFO, CIO & CEO

Marketing+Finance+Technology

June 17, 2003 ©Santa Clara Group Pty Ltd scg

MF Culture ClashMF Culture Clash

• Marketing is optimism, fun & event driven

• Financial analysis is hard• Same terms to mean

different things• Boards controlled by

accounting/finance• Justify relevant financial

returns

June 17, 2003 ©Santa Clara Group Pty Ltd scg

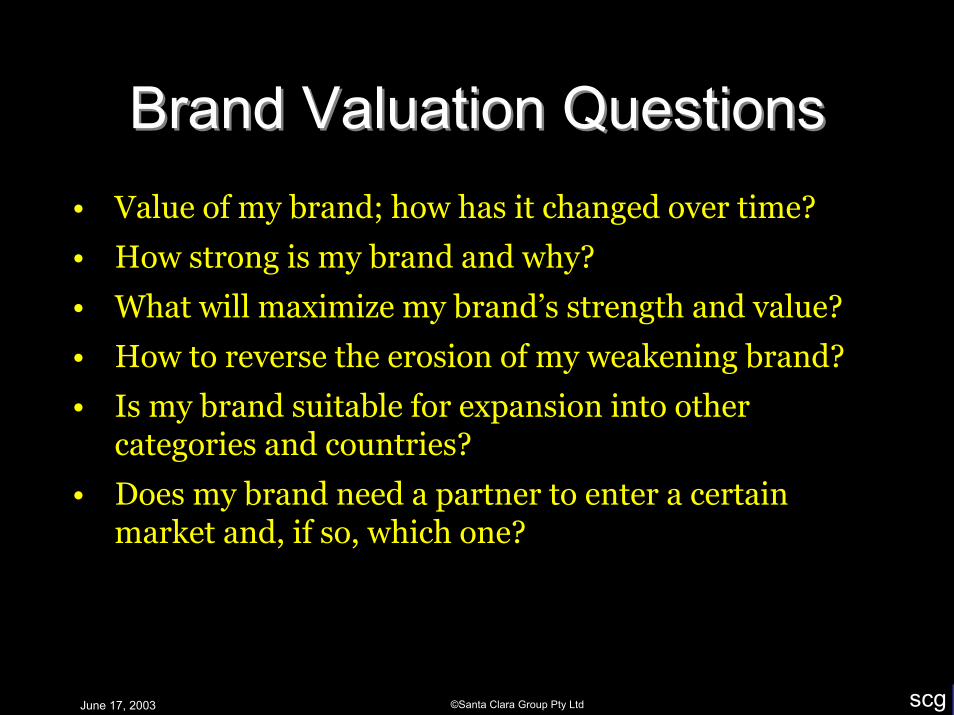

Brand Valuation QuestionsBrand Valuation Questions• Value of my brand; how has it changed over time?

• How strong is my brand and why?

• What will maximize my brand’s strength and value?

• How to reverse the erosion of my weakening brand?

• Is my brand suitable for expansion into other categories and countries?

• Does my brand need a partner to enter a certain market and, if so, which one?

June 17, 2003 ©Santa Clara Group Pty Ltd scg

BrandEconomicsBrandEconomics

• Relative brand strength

• Brand essence & imagery

•EVA® financial management

•Industry economic analysis

•definitive, financially grounded answers to key branding questions

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market Value AddedMarket Value AddedMVA measures how much more a business is worththan the capital invested in it

Net Net Operating Operating Profit After Profit After

TaxTax

Total Total market market valuevalue Charge for Charge for

CapitalCapital

EVA

Equity and Equity and Debt Debt

capitalcapital

MVAShareholderValue Added

Total Shareholder

ValueShareholderInvestment

Gap between intrinsic value and market value is an investor opportunity

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Brand strengthBrand strength

Differentiation + Relevance

Brand statureBrand statureEsteem + Knowledge

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Differentiation (uniqueness)Differentiation (uniqueness)• First stage of brand relationship – leads to trial• More advanced the market, more crucial

Differentiation is• Yahoo & Starbucks ranked high early on• Establishes the price premium

Relevance (size of market)Relevance (size of market)• Intuitively, relevance would seem to come first• Builds the brand relationship & staying power• Fads have low relevance

June 17, 2003 ©Santa Clara Group Pty Ltd scg

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Brand lifecycleBrand lifecycle

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Market changed forever

Brands win, Experience Delivers, Ads?

Networks are everywhere

Marketing led by CFO, CIO & CEO

Marketing+Finance+Technology

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Why is technology relevant?Why is technology relevant?

• Web has 90 million channels

• 40% of US productivity growth in 10 years –largest single private industry contributor & $US373 billion in cost savings by 2005

• OL’s & Network effect

• Expectations changed forever

• Lessons from Intel, Yahoo!, Microsoft

• We’re all in the valley

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Technologies to watchTechnologies to watch

• Database & Analytics

• Addressable Media

• Instant communications

• Collaborative workflow tools

• Integration with ERP, Supply Chain Management, Financial Management, SFA

• Transaction tagging

June 17, 2003 ©Santa Clara Group Pty Ltd scg

The US MarketThe US Market• At least six different markets (north-east, south-east,

mid-west, south-west, California and north-west)

• Able to support many companies competing within each market and across the whole country

• A vast and complex economy

• Supports (demands) a high degree of specialization

• Often highly parochial (ex California & North East)

• The worlds pre-eminent Product Managers

• Success could be measured by achieving market entry in any of the six markets

June 17, 2003 ©Santa Clara Group Pty Ltd scg

ConclusionsConclusions

Market changed forever

Brands win, Experience Delivers

Networks are everywhere

Marketing+Finance+Technology = NM

June 17, 2003 ©Santa Clara Group Pty Ltd scg

Contact Tony SurteesSanta Clara [email protected]: 0410465929o: (02) 9555 4777

www.scgroup.biz

![Hadoop: A View from the Trenches...Founding member of Hadoop team at Yahoo! [2005-2010] ! Contributor to Apache Hadoop since v0.1 ! Built and led Grid Solutions Team at Yahoo! [2007-2010]](https://img.pdfslide.us/doc/110x75/5ec5ee22e9422601c50f805b/hadoop-a-view-from-the-trenches-founding-member-of-hadoop-team-at-yahoo-2005-2010.jpg)