Embed Size (px)

Citation preview

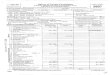

Form 990-PF Return of Private Foundation•, or Section 4947(a)(1) Nonexempt Charitable Trust

Departmentpfthe Treasury Treated as a Private FoundationInternal Revenue service (77) Note The foundation may be able to use a copy of this return to satisfy state report)

OMB No 154 5-0052

2007

cr

r

For calendar year 2007, or tax year beginning JUN 6, 2007 , and ending MAR 31 , 2008G Check all that annly n Initial return F7 Final return n Amenrlerl return n Arlrlracs rhanne n Name rhanna

Use the IRS Name of foundation A Employer identification number

labelOtherwise , PETER G PETERSON FOUNDATION 26-0316905

print Number and street (or P 0 box number if mail is not delivered to street address ) Roorrvsulte B Telephone numberortype 712 FIFTH AVENUE, 47TH FL 212-542-9240

See SpecificInstructions

City or town , state , and ZIP code C If exemption application is pending , check here

NEW YORK, NY 10 019 D 1 Foreign organizations , check here ►H Check typ e of org anization Section 501 ( c )( 3 ) exempt private foundation 2 Foreign organizations meeting tire 85% test,

check here and attach computation

0 Section 4947 ( a )( 1 ) nonexem p t charitable trust = Other taxable p rivate foundation E If t f d tI Fair market value of all assets at end of year J Accounting method 0 Cash Accrual

priva e oun a ion status was terminatedunder section 507(b)(1)(A), check here

(from Part 11, co! (c), line 16) = Other ( specify ) F If the foundation is in a 60-month termination► $ 116 7 80 , 194 . (Part 1, column (d) must be on cash basis.) under section 507(b ) (1 )( B ) , check here ►part I Analysis of Revenue and Expenses ( a) Revenue and (b ) Net investment ( c) Adjusted net ( d) Disbursements

(rhe total o f amounts in columns ( b), (c), and (d) may notnecessanly equal the amounts in column (a)) expenses per books income income for chantable purposes

(cash basis only)

1 Contributions , gifts, grants , etc , received 116,000,000 . N/A2 Check ►= II the foundation is not required to attach Sch B

3Interest

nvestmentssand temporary

1, 036,849. 1,036,849. STATEMENT 14 Dividends and interest from securities

5a Gross rents

b Net rental income or (loss)

W 6a Net gain or (loss ) from sale of assets not on Ilne 107 Gross sales price for all

b assets on line 6a

d 7 Capital gain net income ( from Part IV, use 2) 0 .

8 Net short -term capital gain

9 Income modificationsGross sales less returns

10a and allowances

b Less Cost of goods sold

c Gross profit or (loss)

11 Other income

12 Total Add lines 1 throuoh 11 U17,036,849. 1,036,849.13 Compensation of officers , directors , trustees , etc 0. 0. 0.

14 Other employee salaries and wages

15 Pension plans, employee benefits

16a Legal fees STMT 2 97,005. 0. 97,005.at b Accounting fees

w c Other professional fees STMT 3 97,000. 0. 97,000.4' 17 Interest

18 Taxes STMT 4 20,767. 0. 0.19 Depreciation and depletion

9 E 20 Occupancy

a 21 Travel , conferences , and meetings

C 22 Printing and publications

m 23 Other expenses STMT 5 62,650. 0. 62,650.: 24 Total operating and administrative

0at expenses Add lines 13 throu g h 23 2 7 7, 4 22. 0. 256 , 655.0 25 ContriRE VE®ald

26 T i

lines 24and25 277,422. 0. 256,655.27 trac^ JI 6 1051

a oEx ess o f revenuetn

N

rsements 116 , 7 5 9 , 4 2 7 .tive , enNet i o

UTDer -0- ) 1, 036,849.

^ Ive , en er -o-) N/A

723501LHA For Privacy Act and Paperwork Reduction Act Notice , see the instructions . Form 990-PF (2007)

02-20-08

12040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

1

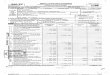

Form 990-PF ( 2007 ) PETER G PETERSON FOUNDATION 26-0 31 6905 Pane2

Balance Sheets Attachedschedules and amounts in the description

P rBeginning of year End of year

a t column should be lerend- ol-yearameuns only (a) Book Value (b) Book Value (c) Fair Market Value

1 Cash - non-interest-bearing

2 Savings and temporary cash investments 116,780,194. 116,780,194.3 Accounts receivable ►

Less allowance for doubtful accounts ►4 Pledges receivable ►

Less allowance for doubtful accounts ►5 Grants receivable

6 Receivables due from officers, directors, trustees, and other

disqualified persons

7 Other noes and loans receivable ►

Less allowance for doubtful accounts ►8 Inventories for sale or use

9 Prepaid expenses and deferred charges

10a Investments - U S and state government obligations

b Investments - corporate stock

c Investments - corporate bonds

11 Investments - land, buildings , and equipment basis ►

Less accumulated depreciason ►

12 Investments - mortgage loans

13 Investments - other

14 Land, buildings, and equipment basis ►Less accumulated depreciation

15 Other assets (describe ► )

16 Total assets ( to be com p leted by all filers) 0. 116 7 8 0 , 19 4 . 116 , 7 8 0 , 19 417 Accounts payable and accrued expenses 20,767.

18 Grants payable

19 Deferred revenue

20 Loans from officers, directors, trustees , and other disqualified persons

r^o 21 Mortgages and other notes payable

J 22 Other liabilities (describe ►

23 Total liabilities (add lines 17 through 22 ) 0. 1 20,767.

Foundations that follow SFAS 117, check here ► OX

and complete lines 24 through 26 and lines 30 and 31

24 Unrestricted 116,759,427.25 Temporarily restricted

CO 26 Permanently restricted

Foundations that do not follow SFAS 117, check here ► 0LL and complete lines 27 through 31

0 27 Capital stock, trust principal, or current funds

too) 28 Paid-in or capital surplus, or land, bldg , and equipment fundN

< 29 Retained earnings, accumulated income, endowment, or other funds

Z 30 Total net assets or fund balances 0. 116,759,427_.

31 Total liabilities and net assets /fund balances 0. 116 7 80 , 19 4 .

part inn Analysis of Changes in Net Assets or Fund Balances

1 Total net assets or fund balances at beginning of year - Part II, column (a), line 30

(must agree with end-of-year figure reported on prior year's return)

2 Enter amount from Part I, line 27a

3 Other increases not included in line 2 (itemize) ►4 Add lines 1, 2, and 3

5 Decreases not included in line 2 (itemize) ►6 Total net asse ts or fund balances at end of year (line 4 minus line 5) - Part II, column (b), line 30

72351102-20-08

0.116,759,427.

0.116,759,427.

0.116,759,427.

Form 990-PF (2007)

212040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

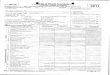

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 3

Part IV Capital Gains and Losses for Tax on Investment Income

(a) List and describe the kind(s) of property sold (e g , real estate,2-story brick warehouse, or common stock, 200 shs MLC Co )

(b How acquired0 - sD -

DDononateationn

(C) Date acquired(mo , day, yr)

(d) Date sold(mo , day, yr )

1a

b NONE

Cd

e

(e) Gross sales price (f) Depreciation allowed(or allowable)

(g) Cost or other basisplus expense of sale

(h) Gain or (loss)(e) plus (f) minus (g)

a

b

c

d

eComplete only for assets showing gain in column (h) and owned by the foundation on 12/31/69 (I) Gains (Col (h) gain minus

(i) F M V as of 12/31/69(1) Adjusted basisas of 12/31/69

(k) Excess of col (i)over col (j), if any

c ol (k), but not less than -0-) orLosses (from col (h))

a

b

c

de

2 Capital ain net income or net capital lossIf gain, also enter in Part I, line 7

g ( ) If (loss) enter -0- in Part I line 7 2

3

, ,

Net short-term capital gain or (loss) as defined in sections 1222(5) and (6)If gain, also enter in Part I, line 8, column (c)If (loss), enter -0- in Part I, line 8 3

Kart V Qualification Under Section 4940 (e) for Reduced Tax on Net Investment Income(For optional use by domestic private foundations subject to the section 4940(a) tax on net investment income ) N/A

If section 4940(d)(2) applies, leave this part blank

Was the foundation liable for the section 4942 tax on the distributable amount of any year in the base penod2 = Yes 0 No

If "Yes," the foundation does not qualify under section 4940(e) Do not complete this part

1 Enter the appropriate amount in each column for each year, see instructions before making any entries

Base period yearsCalendar ear or tax year be g innin g in ) Adjusted qqualifying distributions Net value of noncharitable-use assets

Distribution co(col (b)) divided byy col (c))

2006

2005

2004

2003

2002

2 Total of line 1, column (d) 2

3 Average distribution ratio for the 5-year base period - divide the total on line 2 by 5, or by the number of years

the foundation has been in existence if less than 5 years 3

4 Enter the net value of nonchantable-use assets for 2007 from Part X, line 5 4

5 Multiply line 4 by line 3 5

5 Enter 1% of net investment income (1% of Part I, line 27b) 6

7 Add lines 5 and 6 7

8 Enter qualifying distributions from Part XII, line 4 8

If line 8 is equal to or greater than line 7, check the box in Part VI, line 1b, and complete that part using a 1 % tax rateSee the Part VI instructions

723521/02-20-08 Form 990-PF (2007)

312040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

I

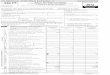

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 4Part - VI Excise Tax Based on Investment Income (Section 4940 (a), 4940 (b), 4940(e), or 4948 - see instructions)1 a Exempt operating foundations described in section 4940(d)(2), check here ►0 and enter "N/A" on line 1

Date of ruling letter (attach copy of ruling letter it necessary-see instructions)

b Domestic foundations that meet the section 4940(e) requirements in Part V, check here ►0 and enter 1 % 1 20,737.

of Part I, line 27b

c All other domestic foundations enter 2% of line 27b Exempt foreign organizations enter 4% of Part I, line 12, col (b)

2 Tax under section 511 (domestic section 4947(a)(1) trusts and taxable foundations only Others enter -0-) 2 0.

3 Add lines 1 and 2 3 20,737.

4 Subtitle A (income) tax (domestic section 4947(a)(1) trusts and taxable foundations only Others enter -0-) 4 0.

5 Tax based on investment income Subtract line 4 from line 3 If zero or less, enter -0- 5 20,737.

6 Credits/Payments

a 2007 estimated tax payments and 2006 overpayment credited to 2007 6a

b Exempt foreign organizations - tax withheld at source 5b

c Tax paid with application for extension of time to file (Form 8868) 6c

d Backup withholding erroneously withheld 6d

7 Total credits and payments Add lines 6a through 6d 7 0.

8 Enter any penalty for underpayment of estimated tax Check here EXI if Form 2220 is attached 8 30.

9 Tax due If the total of lines 5 and 8 is more than line 7, enter amount owed ► g 20,767.

10 Overpayment If line 7 is more than the total of lines 5 and 8, enter the amount overpaid ► 1011 Enter the amount of line 10 to be Credited to 2008 estimated tax ► Refunded ► 11

Part VU-A Statements Regarding Activities1 a During the tax year, did the foundation attempt to influence any national, state, or local legislation or did it participate or intervene in Yes No

any political campaigns 1a X

b Did it spend more than $100 during the year (either directly or indirectly) for political purposes (see instructions for definition) lb X

If the answer is "Yes" to 1 a or 1 b, attach a detailed description of the activities and copies of any materials published or

distributed by the foundation in connection with the activities.

c Did the foundation file Form 1120-POL for this year? 1c X

d Enter the amount (if any) of tax on political expenditures (section 4955) imposed during the year

(1) On the foundation ► $ 0. (2) On foundation managers ► $ 0.

e Enter the reimbursement (if any) paid by the foundation during the year for political expenditure tax imposed on foundation

managers ► $ 0.

2 Has the foundation engaged in any activities that have not previously been reported to the IRS' 2 X

If "Yes, " attach a detailed description of the activities

3 Has the foundation made any changes, not previously reported to the IRS, in its governing instrument, articles of incorporation, or

bylaws, or other similar instruments' If "Yes, " attach a conformed copy of the changes 3 X

4a Did the foundation have unrelated business gross income of $1,000 or more during the year9 4a X

b If "Yes," has it filed a tax return on Form 990 -T for this year? N/A 4b

5 Was there a liquidation, termination, dissolution, or substantial contraction during the year? 5 X

If "Yes, " attach the statement required by General Instruction T

6 Are the requirements of section 508(e) (relating to sections 4941 through 4945) satisfied either

• By language in the governing instrument, or

• By state legislation that effectively amends the governing instrument so that no mandatory directions that conflict with the state law

remain in the governing instrument? 6 X

7 Did the foundation have at least $5,000 in assets at any time during the year' 7 X

If "Yes, " complete Part Il, col (c), and Part XV.

Ba Enter the states to which the foundation reports or with which it is registered (see instructions) ► FFNYb If the answer is "Yes" to line 7, has the foundation furnished a copy of Form 990-PF to the Attorney General (or designate)

of each state as required by General Instniction G? If "No," attach explanation 8b X

9 Is the foundation claiming status as a private operating foundation within the meaning of section 4942(j)(3) or 4942(j)(5) for calendar

year 2007 or the taxable year beginning in 2007 (see instructions for Part XIV)' If "Yes," complete Part XIV 9 X

0 Did any persons become substantial contributors during the tax year' If *Yes ' attach a schedule listing their names and addresses STMT 6 10 X

Form 990-PF (2007)

72353102-20-08

412040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

1 , ,

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316 905 Page 5

Part VU-A Statements Regarding Activities (continued)

11a At any time during the year, did the foundation, directly or indirectly , own a controlled entity within the meaning of section 512(b)(13)'

If "Yes," attach schedule ( see instructions) 11a X

b If "Yes," did the foundation have a binding written contract in effect on August 17, 2006 , covering the interest , rents , royalties, and

annuities described in the attachment for line 1la? N/A 11b

12 Did the foundation acquire a direct or indirect interest in any applicable insurance contract? 12 X

13 Did the foundation comply with the public inspection requirements for its annual returns and exemption application? 13 X

Website address ► WWW . PGPF . ORG

14 The books are in care of ► PAUL L . NEWMAN Telephone no ► 212 -5 4 2 -9 2 4 0

Locatedat ► 712 FIFTH AVENUE, 47TH FL, NEW YORK, NY ZIP+4 ►1001915 Section 4947( a)(1) nonexempt charitable trusts filing Form 990 - PF in lieu of Form 1041 - Check here ►0

and enter the amount of tax-exem p t interest received or accrued durin g the year ► 15 N/A

part VWB Statements Regarding Activities for Which Form 4720 May Be RequiredFile Form 4720 if any item is checked in the " Yes" column , unless an exception applies . Yes No

1 a During the year did the foundation (either directly or indirectly)

(1) Engage in the sale or exchange, or leasing of property with a disqualified person' Yes No

(2) Borrow money from, lend money to, or otherwise extend credit to (or accept it from)

a disqualified persons Yes No

(3) Furnish goods, services, or facilities to (or accept them from) a disqualified person? Yes No

(4) Pay compensation to, or pay or reimburse the expenses of, a disqualified person' Yes No

(5) Transfer any income or assets to a disqualified person (or make any of either available

for the benefit or use of a disqualified person)? Yes No

(6) Agree to pay money or property to a government official? ( Exception . Check "No"

if the foundation agreed to make a grant to or to employ the official for a period after

termination of government service, if terminating within 90 days ) Yes EX7 No

b If any answer is "Yes" to la(1)-(6), did any of the acts fail to qualify under the exceptions described in Regulations

section 53 4941(d)-3 or in a current notice regarding disaster assistance (see page 22 of the instructions)? lb X

Organizations relying on a current notice regarding disaster assistance check here ► I^c Did the foundation engage in a prior year in any of the acts described in 1a, other than excepted acts, that were not corrected

before the first day of the tax year beginning in 20079 1 c X

2 Taxes on failure to distribute income (section 4942) (does not apply for years the foundation was a private operating foundation

defined in section 4942(j)(3) or 4942(j)(5))

a At the end of tax year 2007, did the foundation have any undistributed income (lines 6d and 6e, Part XIII) for tax year(s) beginning

before 20072 Yes No

If "Yes," list the years ►b Are there any years listed in 2a for which the foundation is not applying the provisions of section 4942(a)(2) (relating to incorrect

valuation of assets) to the year's undistributed income? (If applying section 4942(a)(2) to all years listed, answer "No" and attach

statement - see instructions ) N/A 2b

c If the provisions of section 4942(a)(2) are being applied to any of the years listed in 2a, list the years here

3a Did the foundation hold more than a 2% direct or indirect interest in any business enterprise at any time

during the year? Yes 0 No

b If "Yes," did it have excess business holdings in 2007 as a result of (1) any purchase by the foundation or disqualified persons after

May 26, 1969, (2) the lapse of the 5-year period (or longer period approved by the Commissioner under section 4943(c)(7)) to dispose

of holdings acquired by gift or bequest, or (3) the lapse of the 10-, 15-, or 20-year first phase holding period? (Use Schedule C,

Form 4720, to determine if the foundation had excess business holdings in 2007.) N/A 3b

4a Did the foundation invest during the year any amount in a manner that would jeopardize its charitable purposes 4a X

b Did the foundation make any investment in a prior year (but after December 31, 1969) that could jeopardize its charitable purpose that

had not been removed from leopardv before the first day of the tax year begimmna in 20077 4b X

72354102-20-07

Form 990-PF (2007)

512040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

PETER G PETERSON FOUNDATION 26-0316905 Pa g e 6Part VU-B Statements Regarding Activities for Which Form 4720 May Be Required (continued)

5a During the year did the foundation pay or incur any amount to

(1) Carry on propaganda, or otherwise attempt to influence legislation (section 4945(e))7 Yes MX No

(2) Influence the outcome of any specific public election (see section 4955), or to carry on, directly or indirectly,

any voter registration drive9 Yes EXI No

(3) Provide a grant to an individual for travel, study, or other similar purposes' Yes EX No

(4) Provide a grant to an organization other than a charitable, etc , organization described in section

509(a)(1), (2), or (3), or section 4940(d)(2)7 Yes No

(5) Provide for any purpose other than religious, charitable, scientific, literary, or educational purposes, or for

the prevention of cruelty to children or animals' Yes 0 No

b If any answer is "Yes" to 5a(1)-(5), did any of the transactions fail to qualify under the exceptions described in Regulations

section 53 4945 or in a current notice regarding disaster assistance (see instructions)' N/A 5b

Organizations relying on a current notice regarding disaster assistance check here ►0c If the answer is "Yes" to question 5a(4), does the foundation claim exemption from the tax because it maintained

expenditure responsibility forthe grant? N/A Yes No

If "Yes, " attach the statement required by Regulations section 53.4945-5(d).

6a Did the foundation, during the year, receive any funds, directly or indirectly, to pay premiums on

a personal benefit contract' Yes EXI No

b Did the foundation, during the year, pay premiums, directly or indirectly, on a personal benefit contract' 6b X

If you answered "Yes" to 6b, also file Form 8870

7a At any time during the tax year, was the foundation a party to a prohibited tax shelter transaction' Yes No

b If y es , did the foundation receive an y p roceeds or have an y net income attributable to the transaction? N/A 7b

part 'V111Information About Officers, Directors , Trustees, Foundation Managers , HighlyPaid Employees , and Contractors

1 List all officers, directors, trustees, foundation managers and their compensation.

(a) Name and address(b) Title, and average

hours per week devotedto position

(c) Compensation( If not paid ,enter -0 -)

(d)Contributors toempia tlebenerefitplans

compensation

(e) Expenseaccount, otherallowances

PETER G. PETERSON DIRECTOR & CHAIRMAN712 5TH AVE 47TH FLNEW YORK, NY 10019 20.00 0. 0. 0.JOAN GANZ COONEY DIRECTOR712 5TH AVE, 47TH FLNEW YORK, NY 10019 3.00 0. 0. 0.MICHAEL A. PETERSON DIRECTOR, V. CHAIRMAN712 5TH AVE, 47TH FL

NEW YORK, NY 10019 10.00 0. 0. 0.DAVID M. WALKER RESIDENT & C EO712 5TH AVE, 47TH FLNEW YORK, NY 10019 60.00 0. 0. 0.2 Comoensatron of five hiahest-paid emolovees (other than those included on line 11. It none . enter "NONE."

(a) Name and address of each employee paid more than $50,000(b) Title and average

hours p er weekdevoted to position

(c) Compensation( d)Contributions toemplaanddelerrred ans

compensatiodn

(e) Exp enseaccount, otherallowances

NONE

Total number of other employees paid over $50.000 ► 1 U

Form 990-PF (2007)

72355102-20-08

6

12040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 7

Part VIIIInformation About Officers, Directors , Trustees, Foundation Managers , HighlyPaid Employees , and Contractors (continued)

3 Five highest-paid independent contractors for professional services. If none, enter "NONE."

(a) Name and address of each person paid more than $50,000 (b) Type of service (c) Compensation

SIMPSON THACHER & BARTLETT LLP

425 LEXINGTON AVENUE, NEW YORK, NY 10017-3954 LEGAL 97,005.MOXIE FIRECRACKER FILMS

39 LINCOLN PLACE, BROOKLYN, NY 11217 CONSULTANT 62,500.RUBINSTEIN COMMUNICATION1345 AVENUE OF THE AMERICAS, NEW YORK, NY 1010 CONSULTANT 70,000.

Total number of others receivin g over $50 , 000 for p rofessional services 0

L Part IX-A. 1 Summary of Direct Charitable Activities

List the foundation ' s four largest direct charitable activities during the tax year Include relevant statistical information such as thenumber of organizations and other beneficiaries served , conferences convened, research papers produced, etc Expenses

1DURING THE PERIOD THE FOUNDATION WAS IN ITS START-UP ANDPLANNING PHASE AND HAD NOT YET COMMENCED DIRECT CHARITABLEACTIVITIES

2

3

4

[ Part IX-B I Summary of Program - Related InvestmentsDescribe the two largest program - related investments made by the foundation during the tax year on lines 1 and 2 Amou nt

1 N/A

2

All other program - related investments See instructions

3

Total . Add lines 1 throu g h 3 0.

Form 990-PF (2007)

72356102-20-08

712040730 737294 26 -0316905 2007 . 06000 PETER G PETERSON FOUNDATION 26-03161

1 1

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 8

Part X Minimum Investment Return (All domestic foundations must complete this part Foreign foundations , see instructions)

1 Fair market value of assets not used ( or held for use) directly in carrying out charitable , etc , purposes

a Average monthly fair market value of securities 1 a

b Average of monthly cash balances 1 b 46,644,987.c Fair market value of all other assets 1 c

d Total (add lines 1 a, b, and c ) 1 d 46,644,987 .e Reduction claimed for blockage or other factors reported on lines la and

1c (attach detailed explanation) le 0.

2 Acquisition indebtedness applicable to line 1 assets 2 0 .

3 Subtract line 2 from line l d 3 46,644,987 .4 Cash deemed held for charitable activities Enter 1 1/2% of line 3 ( for greater amount, see instructions ) 4 6 9 9 , 6 7 5 .5 Net value of noncharitable - use assets Subtract line 4 from line 3 Enter here and on Part V , line 4 5 45, 9 4 5 , 312 .6 Minimum investment return Enter 5% of line 5 ADJUSTED FOR SHORT TAX PERIOD 6 1,883 , 023.

Part XIDistributable Amount (see instructions ) ( Section 4942 ( l)(3) and ( j)(5) private operating foundations and certainforeign organizations check here ► = and do not complete this part

1 Minimum investment return from Part X , line 6 1 1,883,023 .

2a Tax on investment income for 2007 from Part VI, line 5 2a 20, 737.

b Income tax for 2007 ( This does not include the tax from Part VI) 2b

c Add lines 2a and 2b 2c 2 0 , 7 3 7 .

3 Distributable amount before adjustments Subtract line 2c from line 1 3 1,862,286 .

4 Recoveries of amounts treated as qualifying distributions 4 0 .

5 Add lines 3 and 4 5 1,862,286 .6 Deduction from distributable amount ( see instructions) 5 0 .

7 Distributable amount as adjusted Subtract line 6 from line 5 Enter here and on Part XIII, line 1 7 1,862,286 .

Part X11 Qualifying Distributions (see instructions)

1 Amounts paid ( including administrative expenses) to accomplish charitable , etc , purposes

a Expenses , contributions, gifts, etc - total from Part I, column (d), line 26 1 a 256,655.h Program - related investments - total from Part IX-B 1 b 0.

2 Amounts paid to acquire assets used ( or held for use) directly in carrying out charitable, etc , purposes 2

3 Amounts set aside for specific charitable projects that satisfy the

a Suitability test (prior IRS approval required) 3a

b Cash distribution test (attach the required schedule) 3b

4 Qualifying distributions. Add lines la through 3b Enter here and on Part V, line 8 , and Part XIII , line 4 4 256,655.5 Foundations that qualify under section 4940 ( e) for the reduced rate of tax on net investment

income Enter 1% of Part I , line 27b 5 0.

6 Adjusted qualifying distributions Subtract line 5 from line 4 6 256,655.Note. The amount on line 6 will be used in Part V, column (b), in subsequent years when calculating whether the foundation qualifies for the section

4940(e) reduction of tax in those years

Form 990-PF (2007)

72357102-20-08

812040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 9

P2trt• XIII Undistributed Income (see instructions)

1 Distributable amount for 2007 from Part Xl,

line 7

2 Undistributed income , If any, as of the end of 2006

a Enter amount for 2006 only

b Total for prior years

3 Excess distributions carryover, if any, to 2007

a From 2002

b From 2003

c From 2004

d From 2005

e From 2006

t Total of lines 3a through e

4 Qualifying distributions for 2007 from

Part Xll, line 4 256,655.

a Applied to 2006 , but not more than line 2a

b Applied to undistributed income of prior

years ( Election required - see instructions)

c Treated as distributions out of corpus

(Election required - see instructions)

d Applied to 2007 distributable amount

e Remaining amount distributed out of corpus

5 Excess distributions carryover applied to 2007(If an amount appears in column (d), the same amount

must be shown in column (a) )

6 Enter the net total of each column asindicated below

a Corpus Add lines 3f, 4c , and 4e Subtract line 5

b Prior years ' undistributed income Subtract

line 4b from line 2b

c Enter the amount of prior years'undistributed income for which a notice ofdeficiency has been issued , or on whichthe section 4942(a) tax has been previouslyassessed

d Subtract line 6c from line 6b Taxable

amount - see instructions

e Undistributed income for 2006 Subtract line

4a from line 2a Taxable amount - see fnstr

f Undistributed income for 2007 Subtract

lines 4d and 5 from line 1 This amount must

be distributed in 2008

7 Amounts treated as distributions out of

corpus to satisfy requirements imposed by

section 170 ( b)(1)(F) or 4942(g)(3)

8 Excess distributions carryover from 2002

not applied on line 5 or line 7

9 Excess distributions carryover to 2008

Subtract lines 7 and 8 from line 6a

10 Analysis of line 9

a Excess from 2003

b Excess from 2004

c Excess from 2005

d Excess from 2006

e Excess from 2007

72358102-20-08

(a) (b) (c)Corpus Years prior to 2006 2006

(d)2007

1,862,286.

0.

0.

0.

0.

0.

0.

256,655.0.0. 0.

0.

0.

0.

0.

0.

0.

0.

0.

1,605,631.

Form 990-PF (2007)

912040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Form 990-PF ( 2007 ) PETER G PETERSON FOUNDATION 26-0316905 Page10Part XIV I Private Operating Foundations (see instructions and Part VII-A, question 9) N/A

1 a If the foundation has received a ruling or determination letter that it is a private operating

foundation , and the ruling is effective for 2007, enter the date of the ruling ^Tb Check box to indicate whether the foundation is a p rivate o eratin foundation described in section 4942 (j)( 3 ) or = 4942(j)(5)

2 a Enter the lesser of the adjusted net

income from Part I or the minimum

investment return from Part X for

each year listed

b 85% of line 2a

c Qualifying distributions from Part XII,

line 4 for each year listed

d Amounts included in line 2c not

used directly for active conduct of

exempt activities

e Qualifying distributions made directly

for active conduct of exempt activities

Subtract line 2d from line 2c3 Complete 3a, b, or c for the

alternative test relied upona "Assets" alternative test - enter

(1) Value of all assets

(2) Value of assets qualifyingunder section 4942(I)(3)(B)(i)

b "Endowment" alternative test - enter2/3 of minimum investment returnshown in Part X, line 6 for each yearlisted

c "Support" alternative test - enter

(1) Total support other than grossinvestment income (interest,dividends, rents, payments onsecurities loans (section51 2(a)(5)), or royalties)

(2) Support from general publicand 5 or more exemptorganizations as provided insection 4942(I)(3)(B)(ni)

(3) Largest amount of support from

an exempt organization

( 4 ) Gross investment income

Tax year Prior 3 years

(a) 2007 (b) 2006 (c) 2005 (d) 2004 ( e) Total

Part XV Supplementary Information (Complete this part only if the foundation had $5 , 000 or more in assetsat any time during the year-see the instructions.)

1 Information Regarding Foundation Managers:

a List any managers of the foundation who have contributed more than 2% of the total contributions received by the foundation before the close of any taxyear ( but only if they have contributed more than $5 , 000) (See section 507(d)(2) )

PETER G. PETERSONb List any managers of the foundation who own 10% or more of the stock of a corporation ( or an equally large portion of the ownership of a partnership or

other entity ) of which the foundation has a 10% or greater interest

NONE2 Information Regarding Contribution , Grant , Gift, Loan , Scholarship , etc., Programs:

Check here 01 0 if the foundation only makes contributions to preselected charitable organizations and does not accept unsolicited requests for funds Ifthe foundation makes gifts, grants, etc (see instructions) to individuals or organizations under other conditions, complete items 2a, b, c, and d

a The name, address, and telephone number of the person to whom applications should be addressed

h The form in which applications should be submitted and information and materials they should include

c Any submission deadlines

d Any restrictions or limitations on awards, such as by geographical areas, charitable fields, kinds of institutions, or other factors

723601/02-20-08 Form 990-PF (2007)10

12040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page11Pa[ rt XV Supplementary Information (continued)

S Grants and GontrIbutionS I'amtl Uurnn the Year or Approved Tor ruture a ment

Recipient If recipient is an individual,show any relationship to Foundation Purpose of grant or

Name and address (home or business) any foundation manager status of contribution Amountor substantial contributor recipient

a Paid dung the year

NONE

Total 1110- 3a 0.

b Approved for future payment

NONE

Total 1111- 3b 1 0 .723611 /02-20 -OS Form 990-PF (2007)

11

12040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

1 .^ I

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Page12

Part Xdl -A . Analysis of Income - Producing Activities

Enter)

1 Pro

a

b

c

d

e

92 Me

3 Int

inv

4 Div

5 Net

a

b

6 Ne t

pro

7 Ot

8 Ga

tha

9 Net

10 Gr

11 Ot

a

b

d

e

12 Su

Irons amounts unless otherwise indicated Unrelate d business income Exc l u ded b section 512 , 513 , or 514 (e)

gram service revenue

(a)Businesscode

(b)Amount

Exc?„_^tle

(d )Amount

Related or exemptfunction income

Fees and contracts from government agencies

mbership dues and assessments

Brest on savings and temporary cash

estments 14 1,036,849.idends and interest from securities

rental income or (loss ) from real estate

Debt-financed property

Not debt-financed property

rental income or (loss) from personal

perty

er investment income

n or (loss ) from sales of assets other

n inventory

income or ( loss) from special events

oss profit or ( loss) from sales of inventory

er revenue

btotal Add columns ( b), (d), and (e) 0. 1 1 , 036,849.

t

t

o

h

i

t

h

1 0.

13 Total Add line 12, columns ( b), (d), and (e) 13 1, 036 , 849.

(See worksheet in line 13 instructions to verity calculations

Part XVI-B Relationship of Activities to the Accomplishment of Exempt Purposes

1212040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

02-20oa Form 990-PF (2007)

Form 990-PF (2007) PETER G PETERSON FOUNDATION 26-0316905 Pag e 13Part XVtU Information Regarding Transfers To and Transactions and Relationships With Noncharitable

Exempt Organizations1 Did the organization directly or indirectly engage in any of the following with any other organization described in section 501(c) of Yes No

the Code (other than section 501(c)(3) organizations) or in section 527, relating to political organizations9

a Transfers from the reporting foundation to a nonchantable exempt organization of

(1) Cash la ( l ) X

(2) Other assets 1a 2 X

b Other transactions

(1) Sales of assets to a nonchantable exempt organization 1 b 1 X

(2) Purchases of assets from a noncharitable exempt organization 1b(2)1 X

(3) Rental of facilities, equipment, or other assets 1 b ( 3 ) X

(4) Reimbursement arrangements lb 4 X

(5) Loans or loan guarantees lb 5 X

(6) Performance of services or membership or fundraising solicitations 1b 6 X

c Sharing of facilities, equipment, mailing lists, other assets, or paid employees 1 c X

d If the answer to any of the above is 'Yes,' complete the following schedule Column (b) should always show the fair market value of the goods, ot

or services given by the reporting foundation If the foundation received less than fair market value in any transaction or sharing arrangement, sh

her ass

ow in

ets,

(a) Name of organization ( b) Type of organization ( c) Description of relationship

N/A

Under pens(1es perjury , I declare that I have examined this return , including accompanying schedules and statements , and to the best of my knowledge and belief , it is true, correct,

and comple I rail of prep er (other than taxpayer or fiduciary) is based on all inform ati on of which preparer has any knowledge

4)

0 Signature of officer or trustee

C Preparer'ssignature

Oa o ,, Firm ' s name ( oryours BARRY M RAUSS C .aj itself-employed ). ' 307 FIFTH AVENUE, 8TH

address , andZiPcode NEW YORK, NY 10016-6517

72362202-20-08

12040730 737294 26-0316905 2007.0600

2a is the foundation directly or indirectly affiliated with, or related to, one or more tax-exempt organizations described

in section 501 ( c) of the Code ( other than section 501 (c)(3 )) or in section 5279 Yes ® No

h If "Vac " rmmnlotp the fnilnwlnn crharlnlp

t

Schedule B(Form 990, 990-EZ,or 990-PF)Department of the TreasuryInternal Revenue Service

Name of organization

Schedule of Contributors

Supplementary Information for

line 1 of Form 990, 990-EZ, and 990-PF (see instructions)

OMB No 1545-0047

2007

PETER G PETERSON FOUNDATION

Employer identification number

26-0316905Organization type (check one)

Filers of: Section:

Form 990 or 990•EZ E] 501 (c)( ) (enter number) organization

4947(a)(1) nonexempt charitable trust not treated as a private foundation

0 527 political organization

Form 990-PF XD 501 (c)(3) exempt private foundation

0 4947(a)(1) nonexempt charitable trust treated as a private foundation

LI 501(c)(3) taxable private foundation

Check if your organization is covered by the General Rule or a Special Rule. (Note : Only a section 501(c)(7), (8), or (10) organization can check boxesfor both the General Rule and a Special Rule-see instructions)

General Rule-

M For organizations filing Form 990, 990•EZ , or 990-PF that received, during the year, $5,000 or more (in money or property) from any one

contributor . ( Complete Parts I and II.)

Special Rules-

For a section 501(c)(3) organization filing Form 990, or Form 990•EZ , that met the 33 1/3% support test of the regulations under

sections 509 (a)(1)/170 (b)(1)(A)(vl), and received from any one contributor, during the year , a contribution of the greater of $5,000 or 2%

of the amount on line 1 of these forms. (Complete Parts I and II )

0 For a section 501 (c)( 7), (8), or ( 10) organization filing Form 990, or Form 990•EZ, that received from any one contributor , during the year,

aggregate contributions or bequests of more than $1 ,000 for use exclusively for religious , charitable, scientific, literary, or educational

purposes , or the prevention of cruelty to children or animals. (Complete Parts I, II, and III )

For a section 501(c )(7), (8), or ( 10) organization filing Form 990 , or Form 990 • EZ, that received from any one contributor , during the year,

some contributions for use exclusively for religious , charitable , etc , purposes , but these contributions did not aggregate to more than

$1,000. ( If this box is checked , enter here the total contributions that were received during the year for an exclusively religious,

charitable , etc., purpose . Do not complete any of the Parts unless the General Rule applies to this organization because it received

nonexclusively religious, charitable , etc., contributions of $5,000 or more during the year.) ► $

Caution : Organizations that are not covered by the General Rule and/or the Special Rules do not file Schedule B (Form 990, 990-EZ, or 990-PF), butthey must check the box in the heading of their Form 990, Form 990-EZ, or on line 2 of their Form 990-PF, to certify that they do not meet the filingrequirements of Schedule B (Form 990, 990-EZ, or 990-PF)

LHA For Paperwork Reduction Act Notice , see the Instructions Schedule B (Form 990 , 990-EZ , or 990-PF ) ( 2007)for Form 990 , Form 990-EZ , and Form 990-PF.

723451 12-27-07

1412040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Schedule B (Form 990 , 990-EZ , or 990-PF) (2007) Page 1 of 1 of Part

Name of organization Employer identification number

I

PETER G PETERSON FOUNDATION 26-0316905

Part I Contributors (See Specific Instructions)

( a)

No.

(b)

Name , address , and ZIP + 4

(c)

Aggregate contributions(d)

Type of contribution

1 PETER G PETERSON Person FX

$ 116,000,000.Payroll

Noncash

(Complete Part II if thereis a noncash contribution.)

(a)

No.

(b)

Name , address , and ZIP + 4

(c)

Aggregate contributions

(d)

Type of contribution

Person 0

$

Payroll

Noncash

(Complete Part II if thereis a noncash contribution )

(a)

No.

(b)

Name , address , and ZIP + 4

(c)

Aggregate contributions

(d)

Type of contribution

Person

$

Payroll

Noncash

(Complete Part II if thereis a noncash contribution)

(a)

No.

(b)

Name , address, and ZIP + 4

(c)

Aggregate contributions

(d)

Type of contribution

Person

$

Payroll

Noncash

(Complete Part II if thereis a noncash contribution.)

(a)

No.

(b)

Name , address , and ZIP + 4

(c)

Aggregate contributions

(d)

Type of contribution

Person

$

Payroll

Noncash

(Complete Part II if thereis a noncash contribution

(a)

No.(b)

Name , address , and ZIP + 4(c)

Aggregate contributions(d)

Type of contribution

Person

$

Payroll

Noncash

(Complete Part II if thereis a noncash contribution )

723452 12-27- 07

15Schedule 0 (Form 990 , 990-EZ , or 990 - PF) (2007)

512040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

PETER G'PETERSON FOUNDATION

LEGAL FEES

FORM 990-PF INTEREST ON SAVINGS AND TEMPORARY CASH INVESTMENTS STATEMENT 1

SOURCE AMOUNT

JP MORGAN CHASE BANK 1,036,849.

TOTAL TO FORM 990-PF, PART I, LINE 3, COLUMN A 1,036,849.

FORM 990-PF STATEMENT 2

DESCRIPTION

SIMPSON THACHER & BARTLETTLLP

TO FM 990-PF, PG 1, LN 16A

(A) (B) (C)EXPENSES NET INVEST- ADJUSTEDPER BOOKS MENT INCOME NET INCOME

97,005.

97,005. 97,005.

FORM 990-PF OTHER PROFESSIONAL FEES STATEMENT 3

DESCRIPTION

ROCKEFELLER PHILANTROPHY -CONSULTANT

RUBINSTEIN COMMUNICATION -CONSULTANT

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLEPER BOOKS MENT INCOME NET INCOME PURPOSES

27,000. 0. 27,000.

70,000. 0. 70,000.

TO FORM 990-PF, PG 1, LN 16C 97,000. 0. 97,000.

FORM 990-PF TAXES STATEMENT 4

DESCRIPTION

US EXCISE TAX

TO FORM 990-PF, PG 1, LN 18

(A) (B) (C)EXPENSES NET INVEST- ADJUSTEDPER BOOKS MENT INCOME NET INCOME

20,767.

0.

26-0316905

(D)

CHARITABLE

PURPOSES

97,005.

0.

0.

20,767. 0.

(D)CHARITABLEPURPOSES

0.

0.

16 STATEMENT(S) 1, 2, 3, 412040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

PETER G'PETERSON FOUNDATION 26-0316905

FORM 990-PF' OTHER EXPENSES STATEMENT 5

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLE

DESCRIPTION PER BOOKS MENT INCOME NET INCOME PURPOSES

MOXIE FIRECRACKER FILMS -CONSULTANT 62,500. 0. 62,500.JP MORGAN CHASE BANK - BANKFEE 150. 0. 150.

TO FORM 990-PF, PG 1, LN 23 62,650. 0. 62,650.

FORM 990-PF

NAME OF CONTRIBUTOR

PETER G PETERSON

LIST OF SUBSTANTIAL CONTRIBUTORS STATEMENT 6PART VII-A, LINE 10

ADDRESS

712 FIFTH AVENUE, NEW YORK, NY 10019

17 STATEMENT(S) 5, 612040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

Form 2220Departmbnt of the TreasuryInternal Revenue Service

Name

Underpayment of Estimated Tax by CorporationsOMB No 1545-0142

► See separate instructions 2007► Attach to the corporation ' s tax return FORM 990 -PF

PETER G PETERSON FOUNDATIONEmployer identification number

26-03 16905

Note Generally, the corporation is not required to file Form 2220 (see Part II below for exceptions) because the IRS will figure any penalty owed and bill thecorporation However, the corporation may still use Form 2220 to figure the penalty If so, enter the amount from page 2, line 34 on the estimated taxpenalty line of the corporation's income tax return, but do not attach Form 2220

UI

1 Total tax ( see instructions)

2 a Personal holding company tax (Schedule PH (Form 1120), line 26) included on line 1

b Look-back interest included on line 1 under section 460(b)(2) for completed long-term

contracts or section 167(g) for depreciation under the income forecast method

c Credit for Federal tax paid on fuels (see instructions) 2c

d Total Add lines 2a through 2c

3 Subtract line 2d from line 1 If the result is less than $500, do not complete or file this form The corporation

does not owe the penalty

4 Enter the tax shown on the corporation's 2006 income tax return (see instructions) Caution : If the tax is zero

or the tax year was for less than 12 months , skip this line and enter the amount from line 3 on line 5

20,737.

20,737.

5 Required annual payment Enter the smaller of line 3 or line 4 If the corporation is required to skip line 4,

enter the amount from line 3 5 20 , 73-7,Part II Reasons for Filing - Check the boxes below that apply If any boxes are checked, the corporation must file Form 2220

even if it does not owe a penalty (see instructions)

6 = The corporation is using the adjusted seasonal installment method

7 FX The corporation is using the annualized income installment method

8 0 The corp oration is a "larg e corp oration" figuringits first re q uired installment based on the p rior year's taxPart III Fiaurina the Undernnvment

( a ) ( b ) c d9 Installment due dates . Enter in columns (a) through

(d) the 15th day of the 4th ( Form 990 - PF filersUse 5th month), 6th, 9th, and 12th months of thecorporation's tax year 9 10/15/07 11/15/07 03/15/08

10 Required installments If the box on line 6 and/or line 7

above is checked, enter the amounts from Sch A, line 38 If

the box on line 8 (but not 6 or 7) is checked, see instructions

for the amounts to enter If none of these boxes are checked,

enter 25% of line 5 above in each column 10 1,197.11 Estimated tax paid or credited for each period (see

instructions) For column (a) only, enter the amount

from line 11 on line 15 11

Complete lines 12 through 18 of one column before

going to the next column.

12 Enter amount, if any, from line 18 of the preceding column 12

13 Add lines 11 and 12 13

14 Add amounts on lines 16 and 17 of the preceding column 14

15 Subtract line 14 from line 13 If zero or less, enter -0- 15 0.16 If the amount on line 15 is zero, subtract line 13 from line

14 Otherwise, enter -0- 16

17 Underpayment . If line 15 is less than or equal to line 10,

subtract line 15 from line 10 Then go to line 12 of the next

column Otherwise, go to line 18 17 1,197.18 Overpayment If line 10 is less than line 15, subtract line 10

from line 15 Then g o to line 12 of the next column 18

Go to Part IV on page 2 to figure the penalty Do not go to Part IV if there are no entries on line 17 - no penalty is owedJWA For Paperwork Reduction Act Notice, see separate instructions Form 2220 (2007)

71280102-13-08

1812040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

FO:2M 990-PFForm 2220 (2007) PETER G PETERSON FOUNDATION 26-0316905 Page 2

Part IV Figuring the Penalty

( a ) ( b ) c d

19 Enter the date of payment or the 15th day of the 3rd month

after the close of the tax year , whichever is earlier (see

instructions ) ( Form 990 - PF and Form 990-T filers Use 5th

month instead of 3rd month ) 9

20 Number of days from due date of installment on line 9 to the

date shown on line 19 20

21 Number of days on line 20 after 4 /152007 and before 1 /1/2008 21

22 Underpayment on line 17 x Number of days on line 21 x 8% 22 $365

23 Number of days on line 20 after 1 2/31 2 007 and before 4 /1/2008 23

24 Underpayment on line 17 x Number of days on line 23 x 7% 24 $ $ $ $

366

25 Number of days on line 20 after 3 /312008 and before 7 /1/2008 25

26 Underpayment on line 17 x Number of days on line 25 X' % 26 $ $ $ $

366

27 Number of days on line 20 after 6/302008 and before 10 /12008 27 SEE ATTACHED RKSHEET

28 Underpayment on line 17 x Number of days on line 27 x'% 2B $366

29 Number of days on line 20 after 9/30/2008 and before 1 /12009 29

30 Underpayment on line 17 x Number of days on line 29 x'% 30 $ $ $ $

366

31 Number of days on line 20 after 12 /3112008 and before 2 /16/2009 31

32 Underpayment on line 17 x Number of days on line 31 x'% 32 $ $ $ $

365

33 Add lines 22, 24, 26 , 28, 30, and 32 33 $ $ S $

34 Penalty . Add columns ( a) through ( d) of line 33 Enter the to

or the comp arable line for other income tax returns

tal h ere and on Form 1120, lin e 33,

34 $ 30.

* For underpayments paid after March 31, 2008 For lines 26, 28, 30, and 32, use the penalty interest rate for each calendar quarter, which the IRSwill determine during the first month in the preceding quarter These rates are published quarterly in an IRS News Release and in a revenue ruling inthe Internal Revenue Bulletin To obtain this information on the Internet, access the IRS website at www.irs .gov You can also call 1-800-829-4933to get interest rate information

JWA Form 2220 (2007)

71280202-13-08

1912040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

PETER G PETERSON FOUNDATION 26-0316905Form 2220 ( 2007 ) FORM 9 9 0 -PF Pace 3

Schedule A Adjusted Seasonal Installment Method and Annualized Income Installment Method (see instructions)

Form 11 Z OS tilers For lines 1, 2, 3, and 21, below, taxable income" refers to excess net passive income or the amount on which taxisimposed under section 1374(a), whichever applies

Part I - Adjusted Seasonal Installment Method (Caution : Use this method only if the base oenod percentage foran y 6 consecutive months is at least 70% See instructions ( a ) b c ( d )

1 Enter taxable income for the following periods

First 3

months

First 5

months

First 8

months

First 11

months

a Tax year beginning 2004 1a

b Tax year be g innin g in 2005 1b

c Tax year be inning in 2006 1 c

2 Enter taxable income for each period for the tax year beginning in

2007 (see instructions for the treatment of extraordina ry items 2

3 Enter taxable income for the following periods

First 4

months

First 6

months

First 9

monthsEntire year

a Tax y ear be g innin g in 2004 3a

b Tax year be g innin g in 2005 3b

c Tax year be g innin g in 2006 3c

4 Divide the amount in each column on line la by the

amount in column ( d ) on line 3a 4

5 Divide the amount in each column on line 1 b by the

amount in column ( d ) on line 3b 5

6 Divide the amount in each column on line 1c by the

amount in column ( d ) on line 3c 6

7 Add lines 4 through 6 7

8 Divide line 7 b y 3 0 8

9a Divide line 2 b y line 8 9a

b Extraordina ry items ( see instructions ) 9h

c Add lines 9a and 9b 9c

10 Figure the tax on the amt on In 9c using the instr for Form

1120 , Sch J , In 2 ( or comp arable In of corp 's return ) 10

11 a Divide the amount in columns (a) through (c) on line 3a

b y the amount in column ( d ) on line 3a 11a

b Divide the amount in columns (a) through (c) on line 3b

by the amount in column ( d ) on line 3b 11b

c Divide the amount in columns (a) through (c) on line 3c

by the amount in column ( d ) on line 3c 11c

12 Add lines 1la thou h 11c 12

13 Divide line 12 by 3 0 13

14 Multiply the amount in columns (a) through (c) of line 10

by columns (a) through (c) of line 13 In column (d), enter

the amount from line 10 , column ( d ) 14

15 Enter any alternative minimum tax for each payment

p eriod ( see instructions ) 15

16 Enter an y other taxes for each p a y ment period ( see instr ) 16

17 Add lines 14 throu g h 16 17

18 For each period, enter the same type of credits as allowed

on Form 2220 , lines 1 and 2c see instructions 18

19 Total tax after credits Subtract line 18 from line 17 If

zero or less , enter -0- 19

0zi308 JWA Form 2220 (2007)

2012040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

PETER G PETERSON FOUNDATION 26-0316905

Form 2220 (2007) FORM 990 -PF Pane 4

Part 11 - Annua)k?:ed Income Installment Method

(a) (b) (c) (d)

First 2 First 3 First 6 First 920 Annualization p eriods ( see instructions ) 20 months months months months

21 Enter taxable income for each annualization period (see

instructions for the treatment of extraordina ry items ) 21 44,887.

22 Annualization amounts ( see instructions ) 22 6.000000 4.000000 1 2.000000 1 1. 3 3 3 3 3 3

23a Annualized taxable income Multi p l y line 21 b y line 22 23a 59,849.b Extraordina ry items ( see instructions ) 23b

c Add lines 23a and 23b 23c 59,849.24 Figure the tax on the amount on line 23c using the

instructions for Form 1120, Schedule J, line 2

( or com parable line of cor p oration ' s return ) 24 1, 197

25 Enter any alternative minimum tax for each payment

p eriod ( see instructions ) 25

26 Enter an y other taxes for each p ay ment p eriod ( see instr ) 26

27 Total tax Add lines 24 throu g h 26 27 1,197.

28 For each period, enter the same type of credits as allowed

on Form 2220 , lines 1 and 2c ( see instructions ) 28

29 Total tax after credits Subtract line 28 from line 27 If

zero or less , enter -0- 29 1, 197

30 App licable p ercenta g e 30 25 % 50% 75% 100%

31 Multi p l y line 29 by line 30 31 1,197.

Part III - Required Installments

Note Complete lines 32 through 38 of one column before 1st 2nd 3rd 4th

completing the next column installment installment installment installment

32 If only Part I or Part II is completed, enter the amount in

each column from line 19 or line 31 If both parts are

completed, enter the smaller of the amounts in each

column from line 19 or line 31 32 0. 0. 0. 1,197.33 Add the amounts in all preceding columns of line 38

( see instructions ) 33

34 Adjusted seasonal or annualized income installments

Subtract line 33 from line 32 If zero or less , enter -0- 34 1,197.

35 Enter 25% of line 5 on page 1 of Form 2220 in each

column Note "Large corporations ," see the instructions

for line 10 for the amounts to enter 35 5,184. 5,185. 5,184. 5,184.36 Subtract line 38 of the preceding column from line 37 of

the p recedin g column 36 5, 184. 10,369. 15,553.

37 Add lines 35 and 36 37 5,184. 10,369. 1 15,553. 20,737.38 Required installments . Enter the smaller of line 34 or

line 37 here and on page 1 of Form 2220, line 10

( see instructions ) 38 0 . 0 . 0. 1 , 197.

Form 2220 (2007)** ANNUALIZED INCOME INSTALLMENT METHOD USING STANDARD OPTION

JWA71282205-13-08

2112040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

FORM 990-PFUNDERPAYMENT OF ESTIMATED TAX WORKSHEET

Name ( s)

PETER G PETERSON FOUNDATION

Identifying Number

26-0316905

(A) (B)

Amount

(C)

AdjustedBalance Due

(D)

Number DaysBalance Due

(E)

DailyPenalty Rate

(F)

Penalty

-0-

03/15/08 1,197. 1,197. 16 .000191257 4.

03/31/08 0. 1,197. 91 .000163934 18.

06/30/08 0. 1,197. 46 .000136612 8.

Penalty Due ( Sum of Column F) 30.

Date of estimated tax payment, withholdingcredit date or installment due date

71251104-27-07

2212040730 737294 26-0316905 2007.06000 PETER G PETERSON FOUNDATION 26-03161

AMENDED AND RESTATED

BY-LAWS

OF

PETER G . PETERSON FOUNDATION

(a Delaware corporation not for profitand without capital stock)

ARTICLE I

OFFICES

The principal office of the PETER G. PETERSON FOUNDATION (the"Corporation") will be-located at a place within or without the State ofDelaware as the Board of

Directors (referred to in these By-Laws as the "Board ofDirectors ''! or the "Board") may from

time to time determine . The Corporation may also have other offices at other places both within

and without the State of Delaware as the Board ofDirectors may from time to'fime determine or

the business of the Corporation may require. ,

ARTICLE II

MEMBERS -

Section 1, Membership . The Corporation has one class of members who will be

the persons who are elected or appointed from time to time as directors of the Corporation andwho will be considered to be the members ofthe Corporation for the purposes of any statutory

provision or rule of law relating to members of a non-stock not-for-profit corporation.

Sectioh 2., Meetings . A meeting of the membership will be held annually foii the

election of directors and the transaction of any'other business as may properly come before therliembership. Unless otherwise fixed by the Board ofDirectors,,the annual meeting of the

membership will take place immediately preceding the annual meeting of the Board of Directors.At any time in the interval between annual meetings, a special meeting of the members may becalled by the Chairman, by a majority of the Board of Directors or by a majority of the members

by vote at ,a meeting or in, writing (addressed to the Secretary of the Corporation).

Section 3. Notice . In accordance with Section 222 of the Delaware General

Corporation Law, written notice which states the place, if any, date and hour of the meeting, and

the means ofremote commur}ications, if any, by which members may be deemed to be present inperson and vote at a meeting, will be made by first class mail, electronic mail, facsimiletransmission, courier service or hand delivery and will be, given not less than ten nor more than

sixty days before the date of tlie.meeting, , Notice of special meetings will indicate the purpose

for which they are called. Notice of meetings need not be given to any member who submits a

019629-0002-11640-NYO1.2651107.11

Lei

2

signed waiver of notice whether before or after the meeting, or who attends the meeting withoutprotesting, prior to the meeting or at its commencement, the lack of notice to him or her.

Section 4. Quorum, Adjournment ofMeetings . At all rmeet :igs of the members,one-third of all the members will be present in person to constitute 'a quorum for the transactionof business, provided, however, that for so long as the Founding Chairman is serving asChairman, the Founding Chairman must be present in person for a quorum to exist.' At anyadjourned meeting for which a quorum was present at the original meeting, any business may betransacted which might have been transacted at the original meeting. If the adjournment is formore than thirty days, notice of the adjourned meeting will be givens -

Section 5 , Orrganization. For so long as the Founding Chairman is serving asChairman, the Founding Chairman will preside at all meetings of the members . After theFounding Chairman ceases to act as Chairman, the Chairman will preside at all meetings of themembers or, in the absence of the Chairman, an acting Chairman will be chosen by the members.The Secretary, of the Corporation will act as secretary at all meetings of the members, but in theabsence of the Secretary, the presiding officer may appoint any person to act as secretary of themeeting.

Section 6. Voting. At any meeting of the members, each member present inperson will be entitled to one vote.

Section 7. Proxies . In accordance with Section 215 of the Delaware GeneralCorporation Law, voting by proxy will be permitted.

Section 8 . Action by the Members . As authorized under Section 215(c) of theDelaware General Corporation Law, and except as otherwise provided by law or by these By-Laws, any corporate action authorized by a majority of the votes cast at a meeting of themembers will be an act of the members. As authorized under Section 228 (b) of the DelawareGeneral Corporation Law, action may be taken without a meeting on written consent, settingforth the action so taken, signed by the-members having not less than •the minimum number ofvotes that would be required to authorize or take that action at a meeting at which all membersentitled to vote were present in person.

Section 9. Meeting by Conference Telephone or Similar Communication Means .

In accordance with Section 211 ofthe Delaware General Corporation Law, any one or more

members may participate, be deemed present in person , andlor vote at any meeting of the

membership by means of a,conference telephone or similar communications equipment allowing

all persons participating in the meeting to hear each other at the same time . Participation by

these means will constitute presence in person at a meeting. Subject to the requirements of

Section 211 of the Delaware General Corporation Law, the Board ofDirectors may, in its sole

discretion, adopt additional guidelines and procedures to allow members to participate, be

deemed present in person, and vote at any meeting of the members.

019629-0002-! 1640-NY 01.2651107.11

ARTICLE III

BOARD OF DIRECTORS

Section 1. Powers and Number. The business and affairs of the Corporation willbe managed by or under the direction of the Board of Directors in accordance with the purposesand limitations set forth in the Certificate of Incorporation. The number of directors that willconstitute the Board will be not less than one nor more than seven. Within the specified limits,the-number of directors will-be determined by resolution of the Board of Directors.

Section 2 . Election and Term. The directors will be elected for a term of one

year at the annual meeting of the members by a majority of the'-votes cast at the meeting, and

each will hold office until the election or appointment and qualification of the director's

successor or until the director 's earlier death, incapacity, resigna'bon, or removal . For the

purposes of these By-Laws the term "incapacity'' will refer to an individual with respect to

whom any member of the Board of Directors comes into possession of (i) a court order'holding

the individual to be legally incapacitated to act on the individual ' s own behalf or (ii) certificates

of two licensed physicians certifying that the individual is unable to act rationally and prudently

in the conduct ofthe individual ' s.affairs.'

Section 3. Vacancies and Newly Created Directorships . Newly created

directorships resulting from an increase in the authorized number of directors and vacancies

bccurring in the Board of Directors for any cause, including by reason of the removal of any

director from office with cause,'may be filled by the vote of a majority ofthe directors then in

office, although less than a quorum, or by a sole remaining director. Each director so elected

will serve until the next annual meeting and until the director 's successor is elected onappointed

and qualified or until the director ' s earlier death, incapacity , resignation, or removal . If at any

time tlfere are no directors then qualified and serving, whether due to their death, incapacity,

removal , resignation or for any other reason, the persons then serving as members of the

Advisory Board will become all of the directors of the Corporation and will serve as the

members of the Corporation as is set forth in Article 11, Section 1.1 "1

Section 4. Removal . any director may be removed with cause by the vote of a

majority of the members entitled to vote at an election of directors. Provided there is a quorum

of not less than a majority of directors then in office present in person, a director may be --

removed with cause by the vote of a majority of the Board of'Directors present in person at the

meeting at which such action is taken. For the purposes of this section, cause-will mean

fraudulent or dishonest conduct, or gross abuse of authority or discretion, with respectto the

Corporation. Removal of a director with cause requires that the individual be provided with: (i)

a list enumerating the charges for removal; (ii) adequate notice; and (iii) a full opportunity to

respond to the charges.

019629-0002-1 1640-NY01.2651107.11

4

I-'Section 5., Resignations . Any director may resign at any time by giving written

notice to the Chairman or Secretary. The resignation will take effect at the time specified in thenotice, and, unless otherwise specified in the notice; the acceptance ofthe resignation will not be

necessary to make it effective.

Section 6. Meetings . Regular or annual meetings of the Board of Directors willbe held at the times and places fixed by-the Board ofDirectors or specified in a notice of

meeting. Special ' meetings of the Board of Directors maybe held at any time upon the call of the

Chairman or any two directors . Unless otherwise fixed by the Board of Directors , the annual

J meeting of the Board will be the first regular meeting following the beginning of the

Corporation ' s fiscal year.

Section 7, Notice of Meetings . Notice need not be given of regular meetings ofthe Board if the time and place of those meetings are fixed by the Board of Directors . Notice ofeach special meeting of the Board of Directors must be given to each director not less than twodays before the meeting . Notice may be.in writing and sent by mail, addressed to each directorat the director's address as it appears 'on the records of the Corporation . Notice will be deemedto have been given when it is deposited in the United States mail. Notice may also be bytelephone or\sent by facsimile transmission, telegraph, telex, courier service, electronic mail orhand delivery. Notice of a meeting ofthe Board need not be given to a director who submits asigned waiver of notice before or after the meeting, or who attends • the meeting withoutprotesting, prior to the meeting or at its commencement, the lack of notice to him or her.

I Section 8. Place and Time of Meetings . Meetings of the Board of Directors will

be held at the location; within or without the State of Delaware, which is fixed by the Board of

Directors or, in the case of a special meeting, by the person or persons calling the special

meeting. I ( ^'

Section 9. Quorum, At each meeting of the Board one-third of the total number

of directors then in office will constitute a quorum for the transactionof business, provided,

however, that for so long as the Founding Chairman is serving as,Chairman, the Founding

Chairman must be present in person for a quorum to, exist. If a quorum is not present at any

meeting of the Board ofDirectors, a'majority ofthe directors present in person may adjourn the

meeting, from time to time, without notice other than announcement at the meeting, until a

quorum is present. - '

Section 10. Manner of Acting. Except as otherwise provided in these By-Laws

or requited by applicable law, the vote of a majority of the directors present in person at any

meeting at which there is a quorum will be the act of the Board of Directors.

Section 11. ConflictsTolicy. Any potential conflict of interest which could result

in a direct or indirect financial or personal benefit to a director, officer or staff member must be

disclosed in good faith or known to the Board ofDirectors or committee authorizing a contract or

other transaction. The interested individual'may participate in the information-gathering stage of

the Board of Directors', or committee's, discussion but will retire from the room in which the

Board of Directors or committee is meeting and will not participate in the final deliberation or

n19629-OOO2-1 16,40-NYO 1.2651 107.11

decision regarding the contract of other transaction. The interested individual may not vote onthe contract or other transaction.

Common or interested directors maybe counted in determining the presence of aquorum at the meeting of the Board or of a committee which authorizes the contracts or othertransaction. I i

The minutes' ofthe meeting of the Board ofDirectors or committee of the Boardwill reflect (a) that the conflict of interest was disclosed, (b) that the interested director, officer orstaff member was not present in person during the final discussion or vote of the Board ofDirectors or committee and (c) that the interested individual abstained from voting.

All questions as to whether a conflict of interest exists will be resolved by a voteof the Board of Directors in which the interested individual may not vote. `

A conflict of interest disclosure statement will be furnished annually to the Boardby each director, officer and staff member. The disclosure statements will be reviewed annuallyby the"-Board of Directors or by a committee of the Board: Jitaddition,, each director, officer and .staff membermust reportpromptly to the Corporation any potential conflict of interest as andwhen it^arises.

In determining whether to approve a contract or transaction involving an actual orpotential conflict of interest, disinterested directors will take into account the restrictionsregarding self-dealing under Section 4941 of the Internal Revenue Code of 1986, as amended.

Section 12. Committees of Directors . The Board of Directors may designate one

or more committees , including without limitation an executive committee, tohave and exercise

the power and authority specified by the Board ofDirectors and permitted by law. Each

committee willconsist of one or more directors . In the absence or disqualiication of a member

of a committee, the member or members of the committee present in person at any meeting and

not disqualified from voting-, whether or not that person or persons constitute a quorum, may

unanimously appoint another director to act at the meeting in place of any absent or disgpalified

member. At each meeting of a committee , a majority of the members of the committee will be

present in person to constitute a quorum . The vote of a majority of the members of a committee

present in person at any meeting at which there is a quorum will be the act of the committee.1r

Section 13. Meeting by Conference Telephone or Similar Communications

Equipment . Any one or more members of the Board of Directors or any committee of the Board

may participate in a meeting of the Board of Directors or the committee by means of a

conference telephone or similar communications equipment-allowing all persons participating in

the meeting to hear each other at the same time . Participation by those means will constitute

presence in person at a meeting. -

Section 14. Action Without a Meeting. Any action required or permitted to betaken by the Board of Directors or any committee of the Board may be taken without a meetingif all members of the Board of Directors or the committee consent in writing to the adoption of a

j

o1s629-0ooza 3 64o-NYO1.26S 11 ma 1

6

resolution authorizing the action. The resolution and the.written consents by the members of theBoard of Directors-or the committee will be filed with the minutes' of the proceedings of theBoard of Directors or the committee. -

Section 15. Compensation of Directors . The 'Corporation will not pay anycompensation to directors for services rendered to the Corporation, except that directors may bereimbursed for reasonable expenses incurred in the performance of their duties to theCorporation.

ARTICLE IV

ADVISORY BOARD

The Board, by resolution adopted by a majority of the entire Board, maydesignate an Advisory Board. The Advisory Board will consist of persons who are interested inthe purposes and principles of the Corporation. The Advisory Board and each member of theAdvisory Board will serve at the pleasure of the Board of Directors. Any vacancy in theAdvisory Board may be filled and any member of the Advisory Board may be removed, eitherwith or without cause, by the Board ofDirectors. The Advisory Board will advise the Board ofDirectors as to any matters that are put before it by the Board of Directors concerning theCorporation. The Advisory Board will not have or purport to exercise any powers ofthe Boardof Directors nor will it have the power to bind the Corporation contractually or to authorize theseal of the Corporation to be affixed to any papers that may require it.

ARTICLE V

OFFICERS

Section 1. Officers . The officers.of the Corporation may consist of a Chairman,a Secretary, a Treasurer, a President and Chief Executive Officer and such other officers withsuch titles as the Board ofDirectors will determine, all ofwhom will be chosen by and will serveat the pleasure of the Board of Directors.

Section 2. Election, Term of Office, and Qualifications . The officers of theCorporation will be elected annually by the Board of Directors at the annual meeting of theBoard ofDirectors, and each officer will hold office until the officer's successor is elected andqualified or until the officer's earlier death, incapacity, resignation, or removal. Except as mayotherwise be provided in the resolution ofthe Board ofDirectors choosing an officer, no officerneed be a director. One person may hold, and perform the duties of, more than one office. Allofficers will be subject to the supervision and direction of the Board of Directors.

Section 3. Removal . Any officer elected or appointed by the Board of Directors.may be removed by the vote of a majority of the Board of Directors, either with or without cause,at any meeting of the Board at which a majority of the directors is present in person.

019629-0002-11640•NYOI 1651107.11

7

l^Section 4 . Resi >~nations . Any officer may resign at any time by giving written

notice to the Chairman. The resignation will take effect at the time specified in the notice, and,

unless otherwise specified in,the'notice, the acceptance of the resignation will not be necessary to

make it effectjve.l J

Section 5 . Vacancies . A vacancy in any office arising from any cause will befilled for the -unexpired portion of the term in the manner prescribed in these By-Laws for regular-appointment to that office.

Section 6 . Chairman. The Chairman will preside at all meetings of the Board of

Directors . In the Chairmen ' s absence, a person chosen by the directors present in person will

preside . The Chairman will have and exercise general charge and supervision of the affairs of the

Corporation and will do and perform any other duties that the Board of Directors assigns to the

Chairman. Until the earliest of Peter G. Peterson ' s death, incapacity or resignation, Mr. Peterson

will serve as the initial Chairman (the "Founding Chairman")- -

Section 7. Secre . The Secretarywill act as secretary of each meeting of theBoard of Directors . In the absence of the- Secretary, the presiding officer of the meeting willappoint a Secretary of the meeting. In addition, the Secretary will:

(a) record and keep the minutesof all meetings of the Board of Directors in

books to be kept for that purpose;

(b) see that all notices and reports are given or filed in accordance with these By-

Laws or as required by law;

(c) be custodian of the records (other than financial) and have charge'of the seal

of the Corporation and see that it is used upon all papers or documents whose execution

on behalf of the Corporation under its seall is required by law or authorized in accordance

with these By7Laws; and

(d) in general, perform all duties incident to,the office of Secretary and any otherduties as the Chairman or the Board of Directors may from time to time assign to theSecretary. _

,Section 8, Treasurer . The Treasurer will: - - c