Embed Size (px)

Citation preview

Form 1099 – Overview

Robert J. KigginsMay 15, 2013

What We Will Cover

IRS Information Reporting Procedures Purposes of Form 1099 Reporting Due Dates for Form 1099 Series Penalties for Noncompliance

Consequences of Errors with Inaccurate Names and TINS

Reasonable Cause

IRS Information Reporting Procedures

What is an Information Return? An information return is a tax document businesses are

required to file to report certain business transactions to the Internal Revenue Service (IRS).

The requirement to file Information Returns is mandated by the Internal Revenue Service and associated regulations.

Who must file Information Returns? Any person, including a corporation, partnership,

individual, estate, and trust. Who make reportable transactions during the calendar

year Must file information returns to report those transactions

to the IRS.

IRS Information Reporting Procedures (Cont’d)

Persons required to file Information Returns to the IRS must also furnish statements to the recipients (Payees) of the income. In fact the order is

First furnish statements to the recipients. Second file the information reports to the IRS

Filers who have 250 or more returns must file these returns with the IRS electronically.

Purposes of Form 1099 Reporting

IRS Form 1099 has many purposes for reporting income and there is more than one Form 1099. 1099-A is used to report all amounts

owed which are the result of the recovery or abandonment of property that is security for a debt for which you are the creditor.

1099-B is used to report all amounts from brokerage and barter exchange transactions.

Purposes of Form 1099 Reporting – Cont’d

1099-DIV is used to report all dividends and capital gains of $10.00 or more.

1099-G is used for government payments. $10.00 or more for unemployment

compensation and state and local income tax refunds.

$600.00 or more for taxable grants and discharge of indebtedness in bankruptcy.

1099-INT is used for reporting all interest income

in excess of $10.00.

Purposes of Form 1099 Reporting – Cont’d

1099-MISC is used to report miscellaneous income.

Royalty payments exceeding $10.00. Rent, prizes or awards in excess of $600.00. Payments to any non-employee of a business, i.e. contract

labor, subcontractors, directors in excess of $600.00. "Golden Parachute" payments made in excess of $600.00

1099-R is used to report all amounts paid from retirement, profit sharing, IRAs, SEPs or 401(K) and 403(C) programs.

1099-S is used to report all gross receipts from the sale or exchange of real estate

Due Dates (General Rules)

As a General Rule, Form 1099’s must Be Sent to the Payees by January 31 Consult Handout Materials for Specifics

Manually Filed Form 1099’s Must be Sent to the IRS by February 28

Electronically Filed Form 1099’s Must be Transmitted to the IRS by March 31

Penalties - Failure To File Correct Information Returns with the IRS by the Due Date (Section

6721)

If you fail to file a correct information return with the IRS by the due date and you cannot show reasonable cause, you may be subject to a penalty.

The penalty applies if you fail to file timely, you fail to include all information required to be

shown on a return, or you include incorrect information on a

return.

Penalties - Failure To File Correct Information Returns with the IRS by the

Due Date (Section 6721) – Cont’d The penalty also applies if

you file on paper when you were required to file electronically,

you report an incorrect TIN or fail to report a TIN, or

you fail to file paper forms that are machine readable.

The amount of the penalty is based on when you file the correct information return.

Penalties - Failure To File Correct Information Returns with the IRS by the Due Date (Section

6721) - Cont’d The penalty is:

$30 (was $15 before Small Business Jobs Act of 2010) per information return if you correctly file within 30 days (by March 30 if the due date is February 28);

maximum penalty $250,000 per year ($75,000 for small businesses, defined below).

$60 (was $30) per information return if you correctly file more than 30 days after the due date but by August 1;

maximum penalty $500,000 per year ($200,000 for small businesses).

Penalties - Failure To File Correct Information Returns with IRS by the Due Date (Section

6721) - Cont’d $100 (was $50) per information return if you

file after August 1 or you do not file required information returns;

maximum penalty $1,500,000 per year ($500,000 for small businesses).

Small businesses—lower maximum penalties. You are a small business if your average annual gross receipts for the 3 most recent tax years (or for the period you were in existence, if shorter) ending before the calendar year in which the information returns were due are $5 million or less.

This same penalty scheme applies to a failure to report to a payee

Penalties - Failure To File Correct Information Returns with IRS by the Due Date (Section

6721) - Cont’d

Intentional disregard of payee statement requirements. If any failure to provide a correct payee statement is due to intentional disregard of the requirements to furnish a correct payee statement, the penalty is at least $250 (old minimum was $100) per payee statement with no maximum penalty

Penalties - Failure To Furnish Correct Payee Statements (Section 6722)

If you fail to provide correct payee statements and you cannot show reasonable cause, you may be subject to a penalty.

The penalty applies if you fail to provide the statement by

January 31 (February 15 for Forms 1099-B, 1099-S, and 1099-MISC (boxes 8 and 14 only)),

Penalties - Failure To Furnish Correct

Payee Statements (Section 6722) - you fail to include all information required to be shown

on the statement, or you include incorrect information on the statement.

"Payee statement" has the same meaning as "statement to recipient”

The amount of the penalty is based on when you furnish the

correct payee statement.

Penalties - Failure To Furnish Correct Payee Statements (Section 6722)

It is a separate penalty, and is applied in the same manner as the penalty for failure to file correct information returns by the due date (Section 6721)

Penalties - Failure To Furnish Correct Payee Statements (Section 6722)

Exception. An inconsequential error or omission is not considered a failure to include correct information.

An inconsequential error or omission cannot reasonably be expected to prevent or hinder the payee from timely receiving correct information and reporting it on his or her income tax return or from otherwise putting the statement to its intended use.

Penalties - Failure To Furnish Correct Payee Statements (Section 6722)

Errors and omissions that are never inconsequential are those relating to a dollar amount, a significant item in a payee's address, the appropriate form for the information

provided (that is, whether the form is an acceptable substitute for the official IRS form), and

whether the statement was furnished in person or by "statement mailing," when required.

Penalties - Failure To Furnish Correct Payee Statements (Section 6722)

Intentional disregard of payee statement requirements. If any failure to provide a correct payee statement is due to intentional disregard of the requirements to furnish a correct payee statement, the penalty is at least $250 (old minimum was $100) per payee statement with no maximum penalty.

Reasonable Cause Penalties Don’t Apply where Reasonable Cause under Treas. Reg.

§ 301.6724-1 Can Be Shown:

Significant mitigating factors + Filer Acting in a Responsible Manner = Reasonable Cause

Significant Mitigation Factors

(1) The fact that prior to the failure the filer was never required to file the particular type of return or furnish the particular type of statement with respect to which the failure occurred, or

(2) The fact that the filer has an established history of complying with the information reporting requirement with respect to which the failure occurred. In determining whether the filer has such an established history, significant consideration is given to—

(i) Whether the filer has incurred any penalty under in prior years for the failure (or under parallel provisions of prior law), and

(ii) If the filer has incurred any such penalty in prior years, the extent of the filer's success in lessening its error rate from year to year.

A filer may treat as a penalty not incurred any penalty that was self-assessed under section 6724(c)(3) and any penalty under section 6676(b) that was self-assessed under section 6676(d), prior to amendment or repeal by the Omnibus Budget Reconciliation Act of 1989.

Reasonable Cause Responsible manner— Acting in a responsible manner generally means— (i) That the filer exercised reasonable care, which is that standard of care that a

reasonably prudent person would use under the circumstances in the course of its business in determining its filing obligations and in handling account information such as account numbers and balances, and

(ii) That the filer undertook significant steps to avoid or mitigate the failure, including, where applicable—

(A) Requesting appropriate extensions of time to file, when practicable, in order to avoid the failure,

(B) Attempting to prevent an impediment or a failure, if it was foreseeable, (C) Acting to remove an impediment or the cause of a failure, once it occurred,

and (D) Rectifying the failure as promptly as possible once the impediment was

removed or the failure was discovered.

Reasonable Cause Events beyond the filer's control. In order to establish reasonable cause

under this standard, the filer must be meet the Responsible manner test set forth above and must show that the failure was due to events beyond the filer's control.

Events which are generally considered beyond the filer's control include but are not limited to—

(i) The unavailability of the relevant business records fire or other casualty that damages or impairs the filer's relevant business records or the

filer's system for processing and filing such record regulatory change that has a direct impact upon data processing and that is made so

close to the time that the return or payee statement is required that, the change cannot be complied with

unavoidable absence (e.g., due to death or serious illness) of the person with the sole responsibility for filing a return or furnishing a payee statement

(ii) An undue economic hardship relating to filing on magnetic media (as described in paragraph (c)(3) of the Reg),

(iii) Certain actions of the Internal Revenue Service failure was due to the filer's reasonable reliance on erroneous written information from

the Internal Revenue Service. Reasonable reliance means that the filer relied in good faith on the information. The filer shall not be considered to have relied in good faith if the Internal Revenue

Service was not aware of all the facts when it provided the information to the filer. In order to substantiate reasonable cause under this paragraph (c)(4), the filer must

provide a copy of the written information provided by the Internal Revenue Service and, if applicable, the filer's written request for the information.

Reasonable Cause (iv) Certain actions of the filer’s agent

The filer exercised reasonable business judgment in contracting with the agent to file timely correct returns or furnish timely correct payee statements with respect to which the failure occurred.

This includes contracting with the agent and providing the proper information sufficiently in advance of the due date of the return or statement to permit timely filing of correct returns or timely furnishing of correct payee statements; and

The agent satisfied the reasonable cause criteria for mitigating circumstances or one of the reasonable cause criteria

(v) Certain actions of the payee or any other person providing necessary information with respect to the return or payee statement (as described in paragraph (c)(6) of the Reg).

(i) That the failure resulted from the failure of the payee, or any other person required to provide information necessary for the filer to comply with the information reporting requirements (“any other person”), to provide information to the filer, or

(ii) That the failure resulted from incorrect information provided by the payee (or any other person) upon which information the filer relied in good faith.

To substantiate reasonable cause the filer must provide documentary evidence upon request of the Internal Revenue Service showing that the failure was attributable to the payee (or any other person).

There are special rules relating to the availability of a waiver where the filer's failure relates to a taxpayer identification number (TIN), and the failure is attributable to actions of the payee described above

Employee or Independent Contractor?

Robert J. Kiggins

General Test Generally an employee relationship exists when the person for

whom services are performed has the right to control and direct the individual who performs ' the services,

not only as to the result to be accomplished by the Work but also as to the details and means by which that result is accomplished.

That is an employee is subject to the will and control of the employer not only as to what shall be done but how it shall be done.

In this connection, it is not necessary that the employer actually direct or control the manner in which the services are performed; it is sufficient if he has the right to do so.

The right to discharge is also an important factor indicating that the person possessing that right is an employer.

Other factors characteristic of an employer, but not -necessarily present in every case, are

the fur nishing 'Of tools and the furnishing of a place to work to the individual who performs the services.

General Test In general, if an, individual is subject to the control or direc

tion of another merely as to the result to be accomplished by the work and not as to the means and methods for accomplishing the result, he is an independent contractor.

An individual performing services as an independent contractor' is not as to such services an employee under the usual common law rules.

Individuals such as physicians, lawyers, dentists, veterinarians, construction contractors, public stenographers, and auctioneers, engaged in the pursuit of an independent trade, business, or profession, in which they offer their services to the public, are independent Contractors and not employees.

Revenue Ruling 87-41: The Twenty Factors

To help determine whether a worker is an employee under the common law rules, the IRS identified 20 factors that

may indicate whether the employer can exercise enough control to establish an employer-employee relationship.

These factors, set forth in Revenue Ruling 87-41, were based on the circumstances that the courts identified and relied upon to decide whether an employment relationship existed.

Not all the factors must be present to find an employee/employment relationship,

but the factors are guides to use to assess the likelihood as to whether an individual is an employee or

an independent contractor.

(1) Instructions. An employee must comply with instructions about when, where and how to work. The control factor is present if the employer has the right to require compliance with the instructions.

Revenue Ruling 87-41: The Twenty Factors

(2) Training. An employee receives on-going training from, or at the direction of, the employer.

Independent contractors use their own methods and receive no training from the purchasers of their services.

(3) Integration. An employee’s services are integrated into the business

operations because the services are important to the business. This shows that the worker is subject to direction and control of the employer.

(4) Services rendered personally. If the services must be rendered

personally, presumably the employer is interested in the methods used to accomplish the work as well as the end results. An employee often does not have the ability to assign their work to other employees, an independent contractor may assign the work to others.

(5) Hiring, supervising and paying assistants. If an employer hires,

supervises and pays assistants, the worker is generally categorized as an employee. An independent contractor hires, supervises and pays assistants under a contract that requires him or her to provide materials and labor and to be responsible only for the result.

Revenue Ruling 87-41: The Twenty Factors

(6) Continuing relationship. A continuing relationship between the worker and the employer indicates that an employer-employee relationship exists. The IRS has found that a continuing relationship may exist where work is performed at frequently recurring intervals, even if the intervals are irregular.

(7) Set hours of work. A worker who has set hours of work established by an employer is generally an employee.

An independent contractor sets his/her own schedule. (8) Full time required. An employee normally works full time for an

employer.

An independent contractor is free to work when and for whom he or she chooses. (9) Work done on premises. Work performed on the premises of the

employer for whom the services are performed suggests employer control, and therefore, the worker may be an employee.

Independent Contractor may perform the work wherever they desire as long as the contract

requirements are performed. (10) Order or sequence set. A worker who must perform services in the

order or sequence set by an employer is generally an employee. Independent Contractor performs the work in whatever order or sequence they may desire.

Revenue Ruling 87-41: The Twenty Factors

(11) Oral or written reports. A requirement that the worker submit regular or written reports to the employer indicates a degree of control by the employer.

(12) Payments by hour, week or month. Payments by the hour, week or

month generally point to an employer-employee relationship. (13) Payment of expenses. If the employer ordinarily pays the worker’s

business and/or travel expenses, the worker is ordinarily an employee. (14) Furnishing of tools and materials. If the employer furnishes

significant tools, materials and other equipment by an employer, the worker is generally an employee.

(15) Significant investment. If a worker has a significant investment in

the facilities where the worker performs services, the worker may be an independent contractor.

Revenue Ruling 87-41: The Twenty Factors

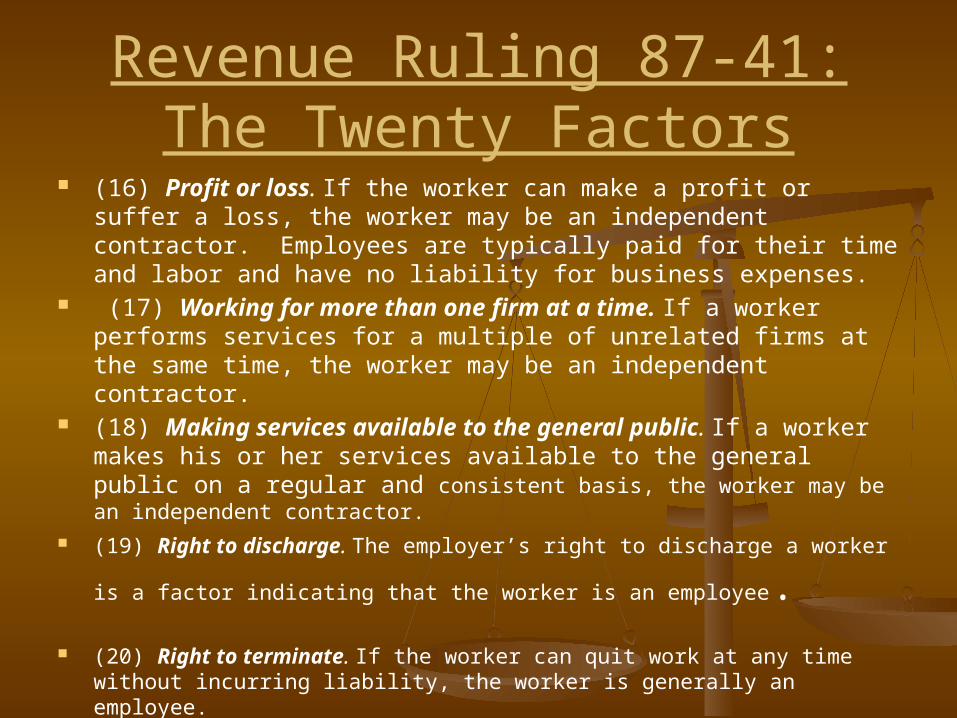

(16) Profit or loss. If the worker can make a profit or suffer a loss, the worker may be an independent contractor. Employees are typically paid for their time and labor and have no liability for business expenses.

(17) Working for more than one firm at a time. If a worker performs services for a multiple of unrelated firms at the same time, the worker may be an independent contractor.

(18) Making services available to the general public. If a worker makes his or her services available to the general public on a regular and consistent basis, the worker may be an independent contractor.

(19) Right to discharge. The employer’s right to discharge a worker is a

factor indicating that the worker is an employee. (20) Right to terminate. If the worker can quit work at any time without

incurring liability, the worker is generally an employee.

Three Categories of Control Factors

Over the years, the Internal Revenue Service recognized changes in business practices and therefore created three categories of factors to assess the degree of control and independence.

These factors are to be used in conjunction with the 20 Factors. (1) Behavioral Control - Includes the type of instructions the business

gives to the worker, such as when and where to do the work, and the training the business provides to the worker. The key consideration is whether the business has retained the right to control the details of

the worker’s performance or has relinquished that right

(2) Financial Control - Address the business’s right to control the business aspects of the worker’s job.

(3) Relationship Of Parties - The nature of the relationship may be evidenced by:

a written contract; the benefits the business provides to an employee, such as paid vacation and health

coverage; the permanency of the position; and the extent to which the services performed are a key aspect of the regular business of the

company.

Indicator Zones

The ultimate test is whether the principal has the “right to direct” and control the individual in question.

Case law tends to look at six indicator zones to answer this test:1. Details of Work Performance2. Expenses of Work Performed3. Compensation for Work4. Duration of Work Performance5. Structure of Work Position6. Location of Work Performance

1. Details of Work Performance Right to Control

Employee – activities and time are surrendered to the control of the employer

Put differently – the employer has the right to say when, where, and how the worker is to work

Independent contractor – agreement to accomplish results or to use skill and care in accomplishing results

Training a Worker Where a worker is required by the person for whom services are

perfomed to be trained or required to work with an experienced worker this is indicative of an employee relationship

Set Hours of Work and Requirement to Work Full Time These are factors indicative of employee status

1. Details of Work Performance Order or Sequence Set – Tends to Show Employee Status

Where the worker is required to follow the established routines and schedules of the person or persons for whom the services are performed – this indicates employee status

The key fact to consider is whether the business retains the right to direct and control the worker, regardless of whether the business actually exercises that right.

Required Written or Oral Reports – Tends to Show Employee Status when the reporting system "measures compliance with

performance standards concerning the details of how the work is performed, the system and its enforcement are evidence of control over the worker's behavior

1. Details of Work Performance Skill

Less skilled more likely to be employees By contrast, highly trained professional

Almost impossible to give such a person detailed instructions

In such a case the key point whether the workers are engaged in the pursuit of an independent' trade, business, or profession in which they offer their services to the public.

If so – they are likely independent contractors If not – they are likely employees

Labels Although the label placed on a relationship is irrelevant if it does not

represent its true substance, it can be helpful in deciphering the parties' intent.

2. Expenses of Work Performance

Payment of business or/or Travel Expenses – indicia of employee status Note: clients of lawyers and accountants pay their travel expenses –

does not maker them employees Unreimbursed expenses – independent contractors more likely to have

these IRS does recognized that both employees and independent contractors

have reimbursed expenses It is more useful to IC status that worker pays fixed on going costs that

are paid regardless of whether work is being performed Furnishing of Tools and Materials to Worker – indicia of employee status

The more valuable the items furnished the more importance that is placed on this factor

Relatively minor items furnished by worker do not typically support independent contractor status

Significant Investment in Business – indicia of IC status E.g. - Maintaining an office – c.f. but a home office would be scrutinized Costly equipment – e.g. computer systems

2. Expenses of Work Performance

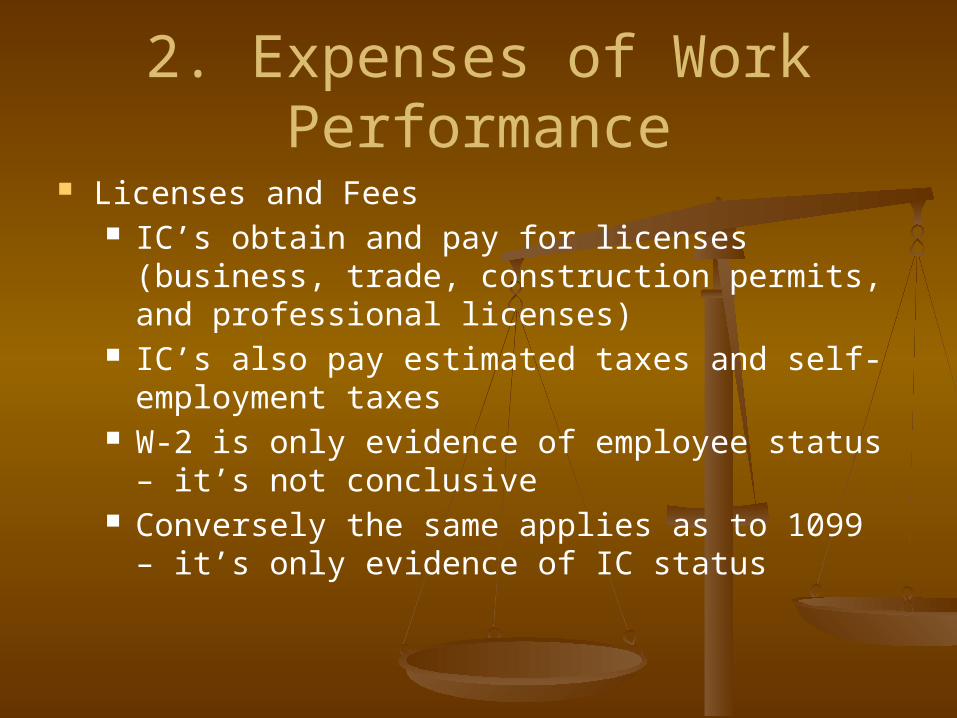

Licenses and Fees IC’s obtain and pay for licenses (business,

trade, construction permits, and professional licenses)

IC’s also pay estimated taxes and self-employment taxes

W-2 is only evidence of employee status – it’s not conclusive

Conversely the same applies as to 1099 – it’s only evidence of IC status

3. Compensation for Work Payment by the hour week or month

Generally indicates EE status C.F. Payment by the job or on a commission generally indicates IC

status A minimum salary or a non-refundable draw is indicative of EE status

Realization of a Profit or a Loss Worker subject to real risk of economic loss due to significant

investments or expense liability – IC Risk of non-payment of earned amounts – IC Is the worker making the decisions that affect the worker’s bottom line

– if so IC Insurance

Worker’s comp, fidelity bond, medical/dental/disability – Employee IC’s provide own insurance in these areas

Benefits Tax qualified plan, annuity or cafeteria plan – can only be provided to

employees Sick pay, paid vacations, bonuses, travel and business expense

reimbursement, advances or drawing account – indicate employee status

4. Duration of Work Performance

Right of Discharge Employee – can be fired IC – generally can’t be fired as long as

performs pursuant to contract Right of Worker to Terminate =

neutral Length of Relationship

In general, the longer the term of the relationship the more likely that employee status will be found

5. Structure of Work Position Integration into the Business

The more the success of the business is dependent upon the success of the worker the more likely that EE status results

However, this is likely not a determinative factor In fact, it is likely less a factor now than in the past

Services rendered personally If worker can’t delegate performance – some evidence that worker is

EE Many courts don’t consider this a helpful factor

Hiring, Supervising and Paying Assistants This is some evidence of IC status Generally won’t be determinative

Working for more than one firm at a Time Some evidence of IC status Not determinative – e.g especially if the firms are somewhat related

5. Structure of Work Position Making service available to General Public

A worker who consistently makes his or her service available to the general public – strong evidence of IC status

This might be done by advertising, use of business cards, a web site, or other materials to make the public aware of availability

Status of Principal If principal is in business – evidence that worker is EE Fits into a consideration under “relationship” of the

parties Intent

Status of worker (IC or EE) intended by parties is a factor

However, just calling a worker an EE or IC is not determinative

5. Structure of Work Position

Industry Custom IE whether workers of the same type are

generally treated as IC’s or EE’s by the industry

This will generally not be afforded much weight by the IRS

However, there is case law that does use industry custom to decide

5. Structure of Work Position

State Law Characterization It is not determinative whether state law

characterizes a worker (e.g. for unemployment or workers comp) as an IC or an EE

In fact, IRS Training Course says state law determinations should be disregarded

Rationale – different standards apply Usually under broader or different definitions

of “employee” than exist under common law

5. Structure of Work Position Incorporation – Worker sets up Corporate Shell

This will do the trick of making the corporation an IC However, the worker in turn will be an employee of his

corporation It also means the workers corporation will have to do

payroll withholding, provide worker’s compensation, provide disability and generally do what a payroll office function has to do

Location of work performance If worker performs on premises furnished by person hiring – some evidence of

EE CF – if worker performs off premises – some evidence of IC These days – remote home office workers are becoming more common – many

are EE’s Probably more the key is if the worker has to work on premises of hirer, at set

hours, and on set dats

Backup Withholding

Robert J. Kiggins

Backup Withholding

What is Backup Withholding? Income tax may have to be withheld at a flat rate

of 28% on the following types of income: Interest, Dividends, Rents Royalties, Commissions and fees paid to independent contractors, Payments from brokers on stock and bond transactions.

Backup Withholding

When does the IRS require Backup Withholding?

The payee fails to furnish his or her taxpayer identification number (TIN) to you.

For interest, dividend, and broker and barter exchange accounts the payee fails to certify, under penalties of perjury, that the TIN provided is correct,

Backup Withholding

When does the IRS require Backup Withholding? - Continued

The IRS notifies you to impose backup withholding because the payee furnished an incorrect TIN,

For interest and dividend accounts or instruments, you are notified that the payee is subject to backup withholding or

For interest and dividend accounts the payee fails to certify to you, under penalties of perjury, that he or she is not subject to backup withholding

Backup WithholdingPenalties

If you do not collect and pay over backup withholding from affected payees as required, you may become liable for any uncollected amount!!!!

When to Apply Backup Withholding

1. Failure to furnish TIN in the manner required.

Withhold on payments made until the TIN is furnished in the manner required.

Special backup withholding rules may apply if the payee has applied for a TIN.

The payee may certify to this on Form W-9 by noting "Applied For" in the TIN block and by signing the form.

This form then becomes an "awaiting-TIN" certificate, and the payee has 60 days to obtain a TIN and furnish it to you.

If you do not receive a TIN from the payee within 60 days and you have not already begun backup withholding, begin backup withholding and continue until the TIN is provided.

When to Apply Backup Withholding

1. Failure to furnish TIN in the manner required – Cont’d.

The 60-day exemption from backup withholding applies only to interest and dividend payments and certain payments made with respect to readily tradable instruments.

Therefore, any other payment, such as nonemployee compensation, is subject to backup withholding even if the payee has applied for and is awaiting a TIN.

When to Apply Backup Withholding

2. Notice from the IRS that payee's TIN is incorrect. You may choose to withhold on any reportable payment

made to the account(s) subject to backup withholding after receipt of a backup withholding notice.

But you must withhold on any reportable payment made to the account more than 30 business days after you received the notice.

This triggers a “B” Notice Requirement – More on this in a bit

Stop withholding within 30 days after you receive a certified Form W-9 (or other form that requires the payee to certify under penalty of perjury).

When to Apply Backup Withholding

3. Notice from the IRS that payee is subject to backup withholding due to notified payee underreporting.

You may choose to withhold on any reportable payment made to the account(s) subject to backup withholding after receipt of the notice,

but you must withhold on any reportable payment made to the account more than 30 business days after you receive the notice.

The IRS will notify you in writing when to stop withholding, or the payee may furnish you a written certification from the IRS stating when the withholding should stop.

In most cases, the stop date will be January 1 of the year following the year of the notice.

When to Apply Backup Withholding

4. Payee failure to certify that he or she is not subject to backup withholding.

Withhold on reportable interest and dividends until the certification has been received.

Backup Withholding – B Notices How do I know if a TIN on my account is incorrect?

The IRS will send you a CP2100 or a CP2100A Notice and a listing of incorrect name/TINs.

This will trigger a Requirement that you send a “B” Notice to the Accounts Involved

A "B" Notice is a backup withholding notice. There are two "B" Notices -- the First "B" Notice and the

Second "B" Notice. You must send the First "B" Notice and a Form W-9 to a

payee after you receive the first CP2100/CP2100A Notice with respect to this account for the purpose of soliciting a correct name/TIN combination.

Backup Withholding – B Notices The text of the Second "B" Notice is different than that

of the First "B" Notice. It tells the payee to contact IRS or SSA to obtain the

correct name/TIN combination. The mailing of the second notice should not include a

Form W-9. You must send the second B Notice after receiving the second CP2100 or CP2100A with respect to this account. The payee must certify the Name/TIN combination after receiving the second "B" Notice.

Generally, you do not have to send a "B" Notice more than two times within three calendar years to the same account.

Backup Withholding

Who's Exempt from Backup Withholding?

US citizens and resident aliens will be exempt from backup withholding if: You properly report your name and Social

Security number to the payer using Form W-9, and that information matches the IRS records,

You have not been notified by the IRS that you are subject to mandatory backup withholding.

Backup Withholding

How do I get the individual's taxpayer ID?

Use Form W-9 to request the identification number of the individual.

What if the individual refuses or neglects to give the taxpayer ID number?

If you do not receive the information, start backup withholding immediately and continue until you receive it.

Backup Withholding

Reporting backup withholding. Report backup withholding on Form

945, Annual Return of Withheld Federal Income Tax

Additional information. For more information about backup withholding, see Pub. 1281.

Backup Withholding

How do I deposit the backup withholding amounts?

Generally the deposit rules for Form 945 are the same as those for Form 941 (payroll taxes).

You are a semiweekly or monthly depositor, depending on the amount deposited.

You may use the IRS e-file (EFTPS) system or make deposits using the deposit coupon.

There are some special rules that relate to depositing backup withholding

Read the Instructions for Form 945 for more information.

Filing with the IRS and Correcting Returns

Robert J. Kiggins

Intro to Filing Caveat: Don’t confuse filing with IRS with sending reports to Payees .

Here we are generally talking about filing with the IRS

When To File File Forms 1099 on paper by February 28, 2012, or April 2, 2012, if filing electronically. Also file Form

1096 with paper forms.

You will meet the requirement to file if the form is properly addressed and mailed on or before the due date. If the regular due date falls on a Saturday, Sunday, or legal holiday, file by the next business day. A business day is any day that is not a Saturday, Sunday, or legal holiday.

Private delivery services. You can use certain private delivery services designated by the IRS to meet the “timely mailing as timely filing” rule for information returns. The list includes only the following.

DHL Express (DHL): DHL Same Day Service.

Federal Express (FedEx): FedEx Priority Overnight, FedEx Standard Overnight, FedEx 2 Day, FedEx International Priority, and FedEx International First.

United Parcel Service (UPS): UPS Next Day Air, UPS Next Day Air Saver, UPS 2nd Day Air, UPS 2nd Day Air A.M., UPS Worldwide Express Plus, and UPS Worldwide Express.

The private delivery service can tell you how to get written proof of the mailing date.

Intro to Filing

Private delivery services cannot deliver items to P.O. boxes. You must use the U.S. Postal Service to mail any item to an IRS P.O. box address

Reporting period. Forms 1099 are used to report amounts paid during the calendar year. Forms 5498, 5498-ESA, and 5498-SA are used to report amounts contributed and the fair market value of an account for the calendar year.

Extension. You can get an automatic 30-day extension of time to file by completing Form 8809, Application for Extension of Time To File Information Returns.

The form may be submitted on paper, or through the FIRE (Filing Information Returns Electronically) system either as a fill-in form or an electronic file. No signature or explanation is required for the extension.

However, you must file Form 8809 by the due date of the returns in order to get the 30-day extension.

Under certain hardship conditions you may apply for an additional 30-day extension. See the instructions for Form 8809 for more information.

How to apply. As soon as you know that a 30-day extension of time to file is needed, file Form 8809.

If you are requesting an extension for 10 or fewer filers, follow the instructions on Form 8809 and mail it to the address listed in the instructions on the form or you can fax it. See the instructions for Form 8809 for more information.

If you are requesting an extension for more than 10 filers, you must submit the extension request online or electronically through the FIRE system.

Intro to Filing Where to File Send all information returns filed on paper to the following: If your principal business, office or agency, or legal residence in the case of an

individual, is located in Alabama, Arizona, Arkansas, Connecticut, Delaware, Florida, Georgia, Kentucky, Louisiana, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, Texas, Vermont, Virginia, West Virginia :

Department of the Treasury Internal Revenue Service Center Austin, TX 73301

If your principal business, office or agency, or legal residence in the case of an individual, is located in Alaska, California, Colorado, District of Columbia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Maryland, Michigan, Minnesota, Missouri, Montana, Nebraska, Nevada, North Dakota, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Utah, Washington, Wisconsin, Wyoming:

Department of the Treasury Internal Revenue Service Center Kansas City, MO 64999

If your legal residence or principal place of business or principal office or agency is outside the United States, file with the Department of the Treasury, Internal Revenue Service Center, Austin, TX 73301.

State and local tax departments. Contact the applicable state and local tax department as necessary for reporting requirements and where to file.

Form 1096 – Paper Form Filers Filing Returns With the IRS The IRS strongly encourages the quality review of data before filing to

prevent erroneous notices from being mailed to payees (or others for whom information is being reported).

If you must file any 1099 with the IRS and you are filing paper forms, you must send a Form 1096 with each type of form as the transmittal document.

You must group the forms by form number and submit each group with a separate Form 1096. For example, if you file Forms 1099-DIV, 1099-INT and 1099-MISC, complete one Form 1096 to

transmit Forms 1099-DIV , another for Forms 1099-INT, and a third for Forms 1099-MISC. Specific instructions for completing Form 1096 are included on the form.

Transmitters, paying agents, etc. A transmitter, service bureau, paying agent, or disbursing agent (hereafter referred to as “agent”) may sign Form 1096 on behalf of any person required to file (hereafter referred to as “payer”) if the conditions in 1 and 2 below are met.

1. The agent has the authority to sign the form under an agency agreement (oral, written, or implied) that is valid under state law and

2. The agent signs the form and adds the caption “For: (Name of payer).” Signing of the form by an authorized agent on behalf of the payer does

not relieve the payer of the liability for penalties for not filing a correct, complete, and timely Form 1096 and accompanying returns.

Filing – Additional General Considerations

Forms 1099 or acceptable substitute statements to recipients issued by a service bureau or agent should show the same payer's name as shown on the information returns filed with the IRS.

For information about the election to report and deposit backup withholding under the agent's TIN and how to prepare forms if the election is made, see Rev. Proc. 84-33, 1984-1 C.B. 502, and the Instructions for Form 945.

Keeping copies. Generally, keep copies of information returns you filed with the IRS or have the ability to reconstruct the data for at least 3 years, 4 years for Form 1099-C, from the due date of the returns. Keep copies of information returns for 4 years if backup withholding was imposed.

Shipping and mailing. Send the forms to the IRS in a flat mailing (not folded). If you are sending many forms, you may send them in conveniently sized packages. On each package, write your name, number the packages consecutively, and place Form 1096 in package number one. Postal regulations require forms and packages to be sent by First-Class Mail.

Paper Filing Paper Document Reporting If you are required to file 250 or more information returns, you must file electronically

Follow these guidelines. If you have a small number of forms, consider contacting an IRS business partner who may be able to

prepare them with little or no cost to you. Type entries using black ink in 12-point Courier font. Copy A is read by machine and must be typed

clearly using no corrections in the data entry fields. Data must be printed in the middle of the blocks, well separated from other printing and guidelines.

Entries completed by hand, or using script, italic, or proportional spaced fonts, or in colors other than black, cannot be read correctly by machine.

Make all dollar entries without the dollar sign, but include the decimal point (00000.00). Show the cents portion of the money amounts. If a box does not apply, leave it blank.

Do not enter 0 (zero) or “None” in money amount boxes when no entry is required. Leave the boxes blank unless the instructions specifically require that you enter a 0 (zero). For example, in some cases, you must enter 0 (zero) to make corrections. See part H on this page.

Do not enter number signs (#) e.g. use RT 2, not Rt. #2. Send the entire page of Copy A of your information returns with Form 1096 to the IRS even if some of

the forms are blank or void Do not use staples on any forms. To locate an IRS business partner who may be able to offer low-cost or even free filing of certain forms,

enter e-file for Business Partners in the Search box on IRS.gov.

Paper Filings Multiple filings. If, after you file Forms 1099 you discover additional

forms that are required to be filed, file these forms with a new Form 1096. Do not include copies or information from previously filed returns.

Required format. Because paper forms are scanned, all Forms 1096 and Copies A of Forms 1099, must be prepared in accordance with the following instructions. If these instructions are not followed, you may be subject to a penalty for each incorrectly filed document.

Do not cut or separate Copies A of the forms that are printed two or three to a sheet (except Forms W-2G and 1098-C).

Generally, Forms 1099 are printed two or three to an 8 x 11 inch sheet. Form 1096 is printed one to an 8 x 11 inch sheet. These forms must be submitted to the IRS on the 8 x 11 inch sheet. If at least one form on the page is correctly completed, you must

submit the entire page Send the forms to the IRS in a flat mailing (not folded).

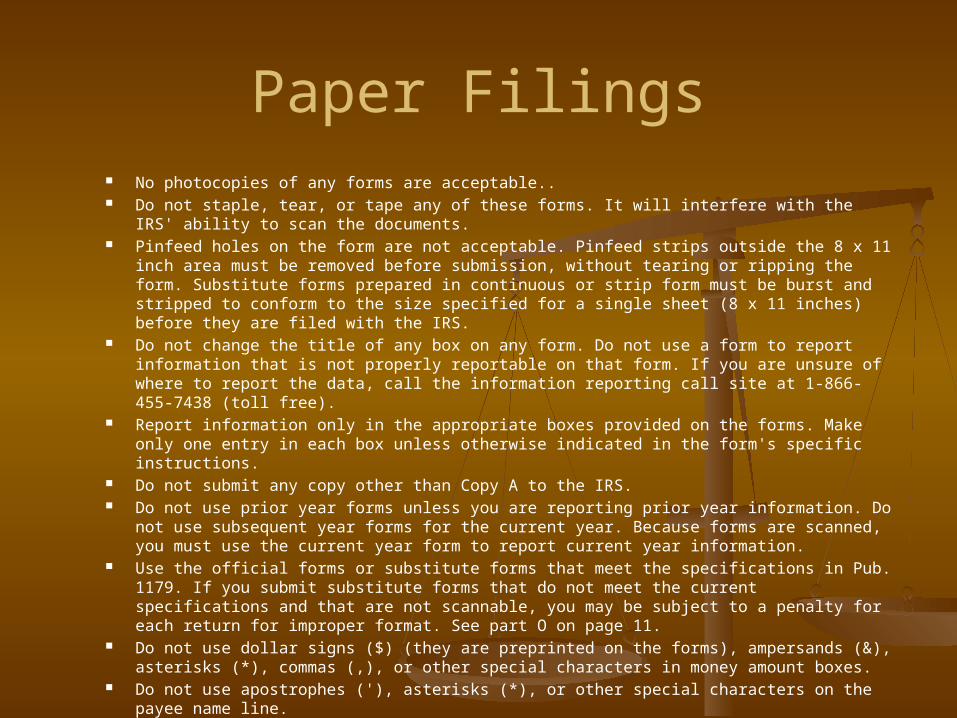

Paper Filings No photocopies of any forms are acceptable.. Do not staple, tear, or tape any of these forms. It will interfere with the IRS' ability to scan the

documents. Pinfeed holes on the form are not acceptable. Pinfeed strips outside the 8 x 11 inch area must

be removed before submission, without tearing or ripping the form. Substitute forms prepared in continuous or strip form must be burst and stripped to conform to the size specified for a single sheet (8 x 11 inches) before they are filed with the IRS.

Do not change the title of any box on any form. Do not use a form to report information that is not properly reportable on that form. If you are unsure of where to report the data, call the information reporting call site at 1-866-455-7438 (toll free).

Report information only in the appropriate boxes provided on the forms. Make only one entry in each box unless otherwise indicated in the form's specific instructions.

Do not submit any copy other than Copy A to the IRS. Do not use prior year forms unless you are reporting prior year information. Do not use

subsequent year forms for the current year. Because forms are scanned, you must use the current year form to report current year information.

Use the official forms or substitute forms that meet the specifications in Pub. 1179. If you submit substitute forms that do not meet the current specifications and that are not scannable, you may be subject to a penalty for each return for improper format. See part O on page 11.

Do not use dollar signs ($) (they are preprinted on the forms), ampersands (&), asterisks (*), commas (,), or other special characters in money amount boxes.

Do not use apostrophes ('), asterisks (*), or other special characters on the payee name line.

Paper Filings - Errors Common errors. Be sure to check your returns to prevent the following common

errors. Duplicate filing. Do not send the same information to the IRS more than once. Also see Multiple filings on this page.

Filer's name, address, and TIN are not the same on Form 1096 and the attached Forms 1099.

Decimal point to show dollars and cents omitted. For example, 1230.00 is correct, not 1230.

Two or more types of returns submitted with one Form 1096 (for example, Forms 1099-INT and 1099-MISC with one Form 1096). You must submit a separate Form 1096 with each type of return.

Correcting Paper Filed Returns If you filed a return with the IRS and later discover you made an error on it, you must:

Correct it as soon as possible and file Copy A and Form 1096 with your Internal Revenue Service Center

Furnish statements to recipients showing the correction. When making a correction, complete all information (see Filing corrected returns on paper

forms below). Do not cut or separate forms that are two or three to a page. Submit the entire page even if

only one of the forms on the page is completed. Do not staple the forms to Form 1096. Do not send corrected returns to the IRS if you are correcting state or local information only.

Contact the state or local tax department for help with this type of correction. To correct payer information, write a letter to the IRS:

1. Name and address of the payer2. Type of error (including the incorrect payer name/TIN that was reported)3. Tax year4. Payer TIN5. Transmitter Control Code (TCC)6. Type of return7. Number of payees8. Filing method (paper or electronic)9. Was federal income tax withheld? Send the letter to Internal Revenue Service, Information Returns Branch, 230 Murall

Drive, Mail Stop 4360, Kearneysville, WV 25430. If a payer realizes duplicate reporting or a large percentage of incorrect information has

been filed, contact the information reporting customer service site at 1-866-455-7438 for further instructions.

Correcting Paper Filed Returns Form 1096.

Use a separate Form 1096 for each type of return you are correcting. For the same type of return, you may use one Form 1096 for both originals and corrections. You do not need to correct a previously filed Form 1096.

CORRECTED checkbox. Enter an “X” in the corrected checkbox only when correcting a form previously filed with the

IRS or furnished to the recipient. Certain errors require two returns to make the correction. See Filing corrected returns on paper forms below to determine when to mark the

“CORRECTED” checkbox. Account number.

If the account number was provided on the original return, the same account number must be included on both the original and corrected returns to properly identify and process the correction

If the account number was not provided on the original return, do not include it on the corrected return. See part L on page 8.

Recipient's statement. You may enter a date next to the “CORRECTED” checkbox. This will help the recipient in the case of multiple corrections.

Filing corrected returns on paper forms. The error charts following give step-by-step instructions for filing corrected returns for the

most frequently made errors. They are grouped under Error Type 1 or 2. Correction of errors may require the submission of more than one return. Be sure to read and

follow the steps given.

Error Type 1 – Form 1099

1. Prepare a new information return.

2. Enter an “X” in the “CORRECTED” box (and date (optional)) at the top of the form.

3. Correct any recipient information such as money amounts and address. Report other information as per

original return.

Incorrect money amount(s), code, or checkbox, or Incorrect address, or Incorrect payee name, or

Error Type 1- Form 1096A return was filed when one should not have been filed. These errors require only one return to make the correction. Caution: If you must correct a TIN and/or a name and address, follow the instructions under Error Type 2.

1. Prepare a new transmittal Form 1096.

2. Provide all requested information on the form as it applies to Part A, 1 and 2.

3. File Form 1096 and Copy A of the return with the appropriate service center.

4. Do not include a copy of the original return that was filed incorrectly

Error Type 2No payee TIN (SSN, EIN, QI-EIN, or ITIN), or Incorrect payee TIN, or Incorrect name and address, or

Step 1. Identify incorrect return submitted.

1. Prepare a new information return.

2. Enter an “X” in the “CORRECTED” box (and date (optional)) at the top of the form

3. Enter the payer, recipient, and account number information exactly as it appeared on the original incorrect return; however, enter 0 (zero) for all money amounts.

Original return filed using wrong type of return (for example, a Form 1099-DIV was filed when a Form 1099-INT should have been filed). Two separate returns are required to make the correction properly. Follow all instructions for both Steps 1 and 2.

Step 2. Report correct information. A. Form 1099 Prepare a new information return.Do not enter an “X” in the “CORRECTED” box at the top of the form. Prepare the new return as though it is an original. Include all the correct information on the form including the correct TIN, name, and address.

B. Form 1096 Prepare a new transmittal Form 1096.Enter the words “Filed To Correct TIN,” “Filed To Correct Name and Address,” or “Filed To Correct Return” in the bottom margin of the form. Provide all requested information on the form as it applies to the returns prepared in Steps 1 and 2.File Form 1096 and Copy A of the return with the appropriate service center.Do not include a copy of the original return that was filed incorrectly.

Void Returns An “X” in the “VOID” box at the top of the form will not correct a

previously filed return. See foregoing for instructions for making corrections.

VOID box. If a completed or partially completed Form 1097, 1098, 1099, 3921, 3922, or 5498 is incorrect and you want to void it before submission to the IRS:

enter an “X” in the “VOID” box at the top of the form. For example, if you make an error while typing or printing a form, you should void it.

The return will then be disregarded during processing by the IRS.

Go to the next form on the page, or to another page, and enter the correct information; but do not mark the “CORRECTED” box

Do not cut or separate the forms that are two or three to a page.

Submit the entire page even if only one of the forms on the page is a good return.

Electronic Reporting

You can file electronically through the Filing Information Returns Electronically System (FIRE System);

however, you must have software that can produce a file in the proper format according to IRS Pub. 1220.

The FIRE System does not provide a fill-in form option for information return reporting. i.e. you need to work with a private vendor

The FIRE System operates 24 hours a day, 7 days a week. You may access the FIRE System via the Internet at fire.irs.gov. See Pub. 1220 for more info

Due dates. File Forms 1099 electronically through the FIRE System by April 2, 2012.

You can request an extension – same rules apply as for paper filing – i.e Form 8809 filed via FIRE

Who must file electronically. If you are required to file 250 or more information returns, you must file electronically. The 250-or-more requirement applies separately to each type of form. For example, if you must file 500 Forms 1098 and 100 Forms 1099-A, you must file Forms 1098 electronically, but you are not required to file Forms 1099-A electronically.

The electronic filing requirement does not apply if you apply for and receive a hardship waiver

Electronic Filing Filing requirement applies separately to originals and corrections. The electronic filing

requirements apply separately to original returns and corrected returns. Originals and corrections are not aggregated to determine whether you are required to file electronically

For example, if you file 400 Forms 1098 electronically and you are making 75 corrections, your corrections can be filed on paper because the number of corrections for Form 1098 is less than the 250 filing requirement. However, if you were filing 250 or more Form 1098

How to get approval to file electronically. File Form 4419, Application for Filing Information Returns Electronically, at least 30 days before the due date of the returns. File Form 4419 for all types of returns that will be filed electronically. See Form 4419 for more information. Once you have received approval, you need not reapply each year. The IRS will provide a written reply to the applicant and further instructions at the time of approval, usually within 30 days.

How to request a waiver from filing electronically. To receive a waiver from the required filing of information returns electronically, submit Form 8508, Request for Waiver From Filing Information Returns Electronically, at least 45 days before the due date of the returns. You cannot apply for a waiver for more than 1 tax year at a time. If you need a waiver for more than 1 tax year, you must reapply at the appropriate time each year.

If a waiver for original returns is approved, any corrections for the same types of returns will be covered under the waiver. However, if you submit original returns electronically but you want to submit your corrections on paper, a waiver must be approved for the corrections if you must file 250 or more corrections.

If you receive an approved waiver, do not send a copy of it to the service center where you file your paper returns. Keep the waiver for your records only.

Penalty. If you are required to file electronically but fail to do so, and you do not have an approved waiver, you may be subject to a penalty of up to $100 per return for failure to file electronically unless you establish reasonable cause. However, you can file up to 250 returns on paper; those returns will not be subject to a penalty for failure to file electronically

corrections, they would have to be filed electronically.

Furnishing Statements to Recipients

If you are required to file Forms 1099you must also furnish statements to recipients containing the information furnished to the IRS and, in some cases, additional information. Be sure that the statements you provide to recipients are clear and legible.

Substitute statements. If you are not using the official IRS form to furnish statements to recipients, see Pub. 1179 for specific rules about providing “substitute” statements to recipients. Generally, a substitute is any statement other than Copy B of the official form. You may develop them yourself or buy them from a private printer. However, the substitutes must comply with the format and content requirements specified in Pub. 1179 that is available on IRS.gov.

Telephone number. You are required to include the telephone number of a person to contact on the following statements to recipients: 1099-A, 1099-B, 1099-C, 1099-CAP, 1099-DIV, 1099-G (excluding state and local income tax refunds), 1099-H, 1099-INT, 1099-K, 1099-LTC, 1099-MISC (excluding fishing boat proceeds), 1099-OID, 1099-PATR, 1099-Q, and 1099-S.

You may include the telephone number in any conspicuous place on the statements.

This number must provide direct access to an individual who can answer questions about the statement. Although not required, if you report on other Forms 1099 and 5498, you are encouraged to furnish telephone numbers.

Rules for furnishing statements. Different rules apply to furnishing statements to recipients depending on the type of payment (or other information) you are reporting and the form you are filing.

Statements to Recipients Dividend, interest, and royalty payments. For payments of dividends reported on Form 1099-DIV, interest including original

issue discount and tax-exempt interest) under section 6049 (reported on Form 1099-INT or 1099-OID), or royalties under section 6050N (reported on Form 1099-MISC or 1099-S)

you are required to furnish an official IRS Form 1099 or an acceptable substitute Form 1099 to a recipient either in person, by First-Class Mail to the recipient's last known address, or electronically (see Electronic recipient statements

below ). Statements may be sent by intraoffice mail if you use intraoffice mail to send account information and other correspondence

to the recipient.

Statement mailing requirements for Forms 1099-DIV, 1099-INT, 1099-OID, and 1099-PATR, and forms reporting royalties only.

The following statement mailing requirements apply only to Forms 1099-DIV (except for section 404(k) dividends), 1099-INT (except for interest reportable in the course of your trade or business under section 6041), 1099-OID, 1099-PATR, and timber royalties reported under section 6050N (on Form 1099-MISC or 1099-S).

The mailing must contain the official IRS Form 1099 or an acceptable substitute and may also contain the following enclosures: (a) Form W-2, applicable Form W-8, Form W-9, or other Forms W-2G, 1097, 1098, 1099, 3921, 3922, and 5498 statements; (b) a check from the account being reported; (c) a letter explaining why no check is enclosed; (d) a statement of the person's account shown on Forms 1097, 1098, 1099, 3921, 3922, or 5498; and (e) a letter explaining the tax consequences of the information shown on the recipient statement.

A statement of the person's account (year-end account summary) that you are permitted to enclose in a statement mailing may include information similar to the following: (a) the part of a mutual fund distribution that is interest on U.S. Treasury obligations; (b) accrued interest expense on the purchase of a debt obligation; and (c) the cost or other basis of securities and the gain/loss on the sale of securities.

No additional enclosures, such as advertising, promotional material, or a quarterly or annual report, are permitted. Even a sentence or two on the year-end statement describing new services offered by the payer is not permitted. Logos are permitted on the envelope and on any nontax enclosures.

A recipient statement may be perforated to a check or to a statement of the recipient's specific account. The check or account statement to which the recipient statement is perforated must contain, in bold and conspicuous type, the legend “Important Tax Return Document Attached.”

The legend “Important Tax Return Document Enclosed” must appear in a bold and conspicuous manner on the outside of the envelope and on each letter explaining why no check is enclosed, or on each check or account statement that is not perforated to the recipient statement. The legend is not required on any tax form, tax statement, or permitted letter of tax consequences included in a statement mailing. Further, you need not pluralize the word “document” in the legend simply because more than one recipient statement is enclosed.

Statements to Recipients Other information. Statements to recipients for Forms 1099-A, 1099-B, 1099-C, 1099-CAP, 1099-G, 1099-

H, 1099-K, 1099-LTC, 1099-MISC, 1099-Q, 1099-R, 1099-SA, 1099-DIV only for section 404(k) dividends reportable under section 6047, 1099-INT only for interest reportable in the course of your trade or business under section 6041, or 1099-S only for royalties

Need not be, but can be, a copy of the official paper form filed with the IRS. If you do not use a copy of the paper form, the form number and title of your substitute must be the same

as the official IRS form. All information required to be reported must be numbered and titled on your substitute in substantially the

same manner as on the official IRS formHowever, if you are reporting a payment as “Other income” in Box 3 of Form 1099-MISC, you may substitute

appropriate explanatory language for the box title. For example, for payments of accrued wages to a beneficiary of a deceased employee required to be reported on Form 1099-MISC, you might change the title of Box 3 to “Beneficiary payments” or something similar.

Appropriate instructions to the recipient, similar to those on the official IRS form, must be provided to aid in the proper reporting of the items on the recipient's income tax return. For payments reported on Form 1099-B, rather than furnish appropriate instructions with each Form 1099-B statement, you may furnish to the recipient one set of instructions for all statements required to be furnished to a recipient in a calendar year.

Except for royalties reported on Form 1099-MISC, the statement mailing requirements explained on page 8 do not apply to statements to recipients for information reported on the forms listed under Other information above. You may combine the statements with other reports or financial or commercial notices, or expand them to include other information of interest to the recipient. Be sure that all copies of the forms are legible. See Pub. 1179 for certain “composite” statements that are permitted.

Statement to Recipients When to furnish forms or statements. Generally, you must furnish

Forms 1099 information by January 31, 2012. Forms 1099-B, 1099-S, and 1099-MISC (only if you are reporting payments in boxes 8 or 14) must be furnished by February 15, 2012. at the time of

You will meet the requirement to furnish the statement if it is properly addressed and mailed, or, with respect to electronic recipient statements, posted to a website, on or before the due date. If the regular due date falls on a Saturday, Sunday, or legal holiday, the due date is the next business day. A business day is any day that is not a Saturday, Sunday, or legal holiday. redemption.

Electronic recipient statements. If you are required to furnish a written statement (Copy B or an acceptable substitute) to a recipient, then you may furnish the statement electronically instead of on paper. This includes furnishing the statement to recipients of, 1099-A, B, C, CAP, DIV, G, H, INT, K, LTC, MISC, OID, PATR, Q, R, S, SA.

Recipient must consent and there are format, posting and notification requirements!!!

THANK YOU!

Robert J. KigginsCounselor-At-Law

McCarthy Fingar LLP11 Martine Avenue

White Plains, NY 10606Tel (914) 946-3700 Ext. 324E-mail: [email protected]

![WELCOME! [saas.convey.com]saas.convey.com/rs/sovos/images/2013.08.20-b-p-notice-webinar.pdf · Form Types Include: 1099-B 1099-Div 1099-Int 1099-Misc 1099-OID W-2G 1099-K CP2100 or](https://img.pdfslide.us/doc/110x75/5b93a81b09d3f2df3f8b4a61/welcome-saas-saas-form-types-include-1099-b-1099-div-1099-int-1099-misc.jpg)