Embed Size (px)

Citation preview

[National financial regulations]: 'purchase to pay' process /Health Service Executive

Item type Report

Authors Health Service Executive (HSE)

Rights HSE

Downloaded 17-Jul-2018 11:57:40

Link to item http://hdl.handle.net/10147/44495

Find this and similar works at - http://www.lenus.ie/hse

Foreword The new national financial regulations have been prepared, and must be applied, in the context of the primary objective of the Health Service Executive. This primary objective, as set out in the Health Act 2004, is to use the resources available to it in the most beneficial, effective and efficient manner to improve, promote and protect the health and welfare of the public. The public rightly expect high standards of accountability and probity in all that the HSE does and I know that all of our staff are committed to providing excellent services within this context. I hold strongly the view that if we are to move towards a world class health service then every aspect of what we do, our support processes as well as our direct service provision, must meet the highest standards. I see implementation and compliance with these financial regulations as a positive step forward for the HSE. Managers and staff at all levels and across all disciplines within the HSE are responsible and must take responsibility for the successful implementation of these regulations. My thanks goes to all those stakeholders who contributed to the process of compiling these regulations and in particular I would like to congratulate the National Finance Director and his team for their commitment and effort in bringing this important project successfully to this stage.

Professor Brendan Drumm Chief Executive Officer

Health Service Executive National Financial Regulations

Ver 1.3 Page 1 of 176

‘Purchase to Pay’ Process

Contents

MAIN CHAPTERS

Chapter Description Page No.

Introduction to Financial Regulations ................................................9

1. General Provisions regarding Financial Regulations........................10

2. Purchase to Pay (General) ...............................................................19

3. Purchase To Pay – Tendering Process..............................................46

4. Purchase to Pay – Specific Topics .....................................................56

5. Capital Projects and Property Transactions ......................................62 APPENDICES ………………………………………………(Page 68 to 176)

Additional Information Re; Chapter 1, Appendix ……………………………… on page 74

Chapter 2, Purchase to Pay (PTP) ……………… on page 76 Chapter 3 Tendering ……………………………… on page 95 Chapter 4 Non Order Payments ………………… on page 103 to 119 Chapter 5 Capital Projects & Property………… on page 124

INDEX …………………………………………………………………… on page 171 to 175

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 2 of 176

The essential requirements of the financial regulations are contained within the main chapters listed above. However, these should be read in conjunction with additional information set out in the more detailed elements of the regulations that are contained within the respective appendices (by chapter).

General Provisions

of Financial

Regulations

Chapter 1

Purpose &Objectives

Page 10

Budget Holders-Responsibilties

Page 12

Mgnt. & StaffGeneral

ResponsibiltiesPage 15

Approval & Amendments

to NFRPage 17

Departures from NFR

Page 18

Compliance toNFR

ObjectivesPage 10

NFR identifyMinimum Controls

Primary Responsibility

Appointment Of Budget Holders

P14

Map of Chapter 1

General Provisions

of Financial

Regulations

Chapter 1

Purpose &Objectives

Page 10

Budget Holders-Responsibilties

Page 12

Mgnt. & StaffGeneral

ResponsibiltiesPage 15

Approval & Amendments

to NFRPage 17

Departures from NFR

Page 18

Compliance toNFR

ObjectivesPage 10

NFR identifyMinimum Controls

Primary Responsibility

Appointment Of Budget Holders

P14

Map of Chapter 1

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 3 of 176

Map of Chapter 2

Purchase to PayChapter 2

Scope

Page 19

Objective

Page 20

Minimum Requirements

EstablishedPage 21

Main Requirements

Appendices

Additional Information

Page 68- 157

Mandatory Controls in Purchasing

Mandatory Controls

in Receiving

Identification of Need (P25)

Confirm Availabilityof Funds (P26)

Sourcing of Goods Or Services (P26)

Expenditure Approval& Issue PO (P34)

Segregation of Duties (P23)

Procurement Planning (P24) Segregation

of Duties (P39)

Delivery/ReceiptOf Goods/Services

(P40)

Receiving Procedures

Purchasing

Page 22

Receiving

Page 37

Payment

Page 43

Table 1, p69

Table 2, p70

Table 3, p73

Purchase to PayChapter 2

Scope

Page 19

Objective

Page 20

Minimum Requirements

EstablishedPage 21

Main Requirements

Appendices

Additional Information

Page 68- 157

Mandatory Controls in Purchasing

Mandatory Controls

in Receiving

Identification of Need (P25)

Confirm Availabilityof Funds (P26)

Sourcing of Goods Or Services (P26)

Expenditure Approval& Issue PO (P34)

Segregation of Duties (P23)

Procurement Planning (P24) Segregation

of Duties (P39)

Delivery/ReceiptOf Goods/Services

(P40)

Receiving Procedures

Purchasing

Page 22

Receiving

Page 37

Payment

Page 43

Table 1, p69

Table 2, p70

Table 3, p73

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 4 of 176

Map of Chapter 3

October 2006

Tendering

Chapter Three

General

Page 46

Forms of Tender

Appendices

Additional Information

Page 95

Four Options for

Non EU Tenders EU Tendering Undertaking by

Procurement only

Restricted Tendering

(Non EU) Page 50

Abridged(Selective) Tendering

Page 51

Negotiated Tendering

Page 52

Open TenderingPage 49

Non EU Tenders

Page 48

EU TenderingPage 53

Topic 3General

RequirementsPage 97

Topic 1Public

AdvertisingPage 95

Non EU

Topic 2Aggregation

Page 96

EU Tendering

Thresholds Custody & Opening

TenderEvaluation Tender Award Notification

Documentation

RMM ProcedurePage 96 & 163

Tendering

Chapter Three

General

Page 46

Forms of Tender

Appendices

Additional Information

Page 95

Four Options for

Non EU Tenders EU Tendering Undertaking by

Procurement only

Restricted Tendering

(Non EU) Page 50

Abridged(Selective) Tendering

Page 51

Negotiated Tendering

Page 52

Open TenderingPage 49

Non EU Tenders

Page 48

EU TenderingPage 53

Topic 3General

RequirementsPage 97

Topic 1Public

AdvertisingPage 95

Non EU

Topic 2Aggregation

Page 96

EU Tendering

Thresholds Custody & Opening

TenderEvaluation Tender Award Notification

Documentation

RMM ProcedurePage 96 & 163

Health Service Executive National Financial Regulations

Ver 1.3 Page 5 of 176

October 2006

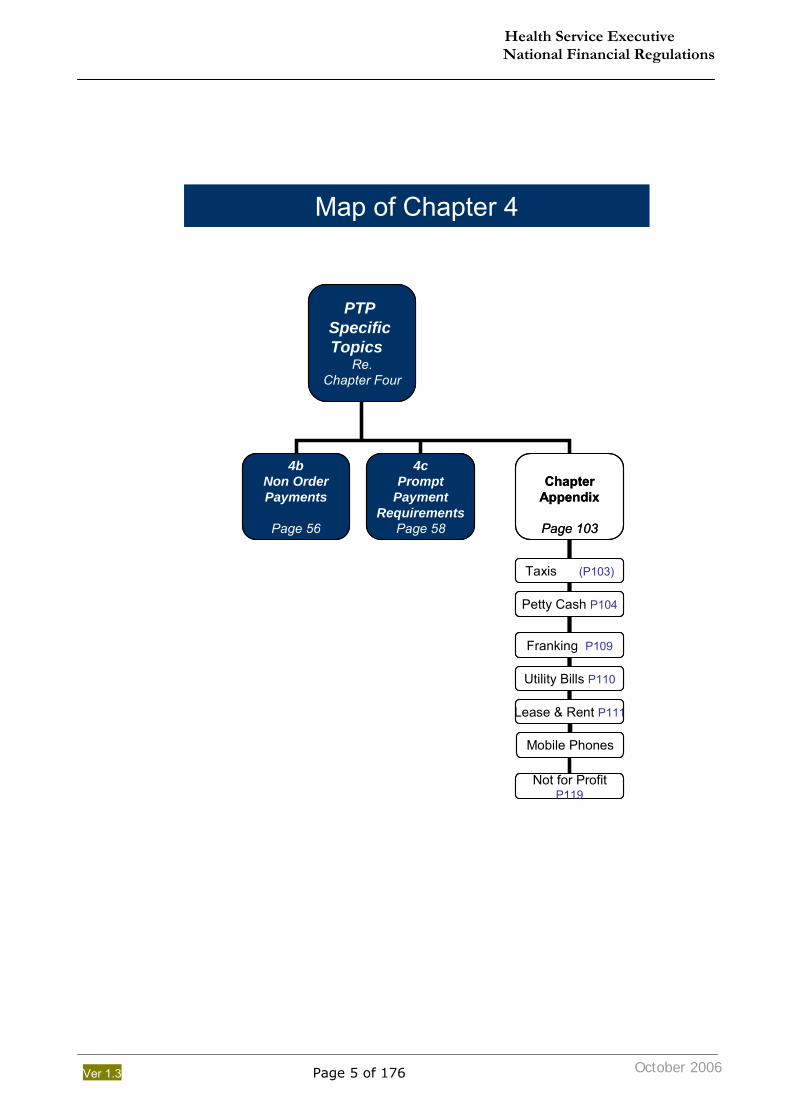

PTP Specific Topics

Re.Chapter Four

4bNon OrderPayments

Page 56

4cPrompt

PaymentRequirements

Page 58

ChapterAppendix

Page 103

Map of Chapter 4

Taxis (P103)

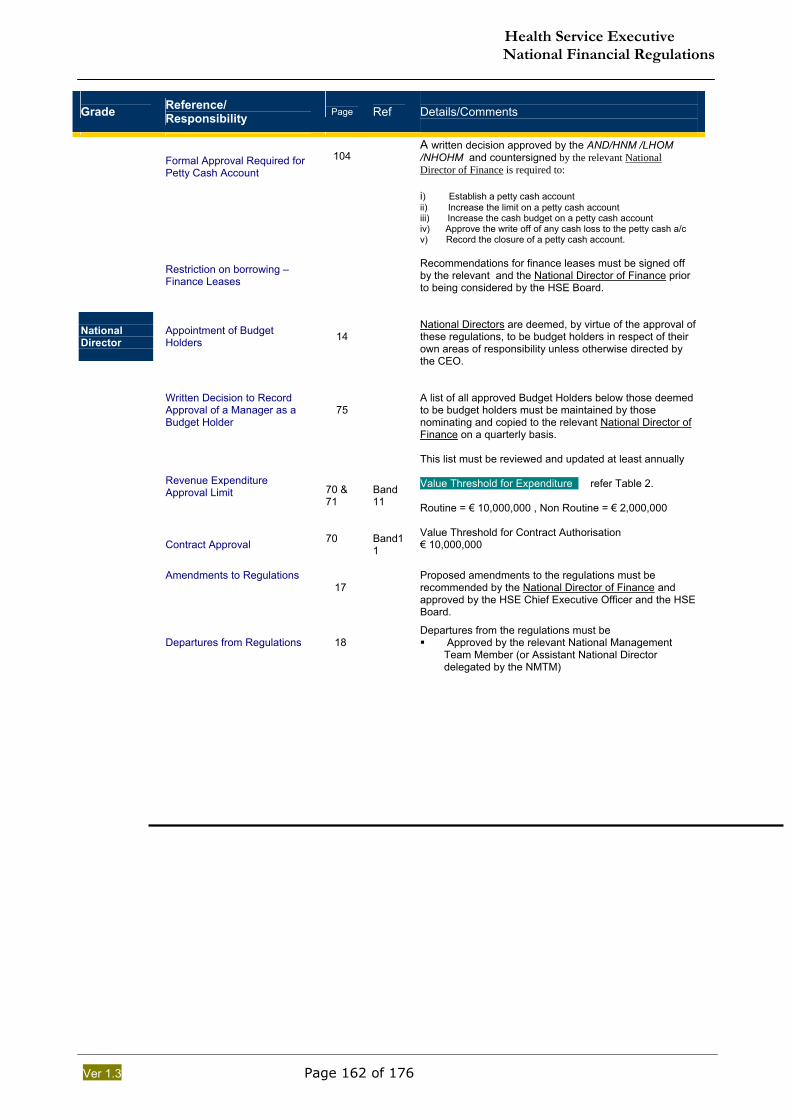

Petty Cash P104

Franking P109

Lease & Rent P111

Utility Bills P110

Mobile Phones

Not for ProfitP119

PTP Specific Topics

Re.Chapter Four

4bNon OrderPayments

Page 56

4cPrompt

PaymentRequirements

Page 58

ChapterAppendix

Page 103

Map of Chapter 4

Taxis (P103)

Petty Cash P104

Franking P109

Lease & Rent P111

Utility Bills P110

Mobile Phones

Not for ProfitP119

Health Service Executive National Financial Regulations

Ver 1.3 Page 6 of 176

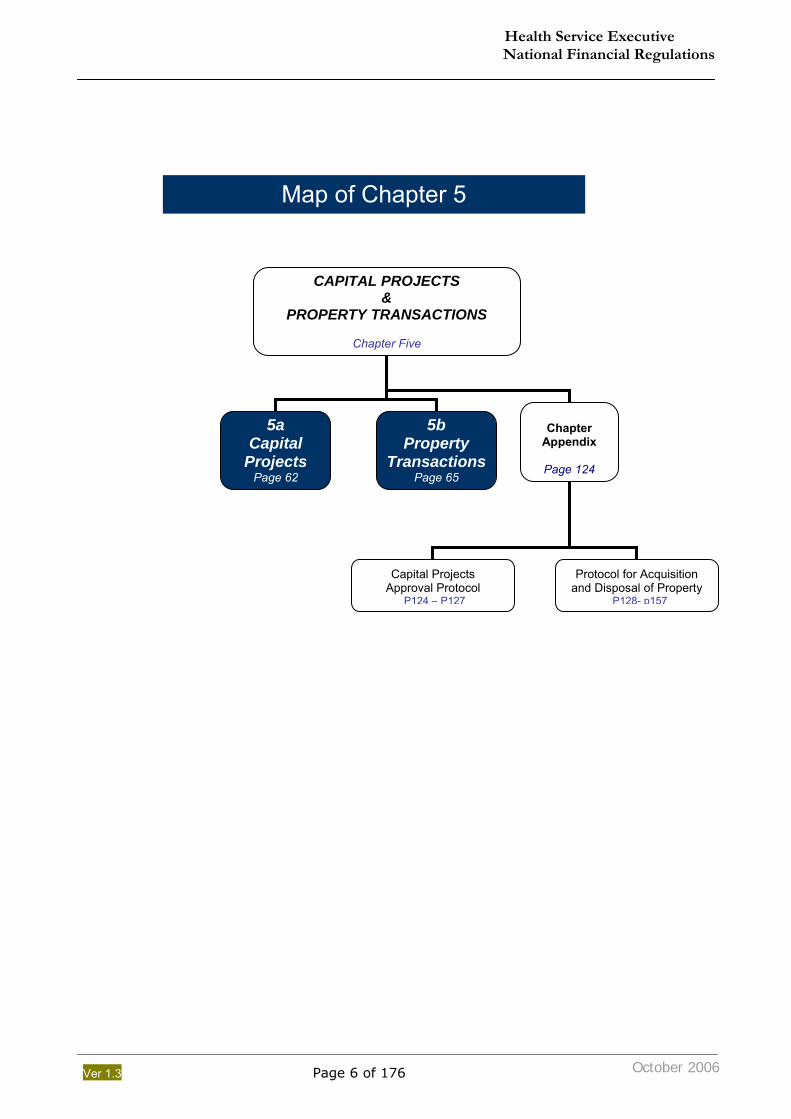

CAPITAL PROJECTS &

PROPERTY TRANSACTIONS

Chapter Five

5a Capital

Projects Page 62

5b Property

TransactionsPage 65

Chapter

Appendix

Page 124

Map of Chapter 5

Capital Projects Approval Protocol

P124 – P127

Protocol for Acquisition and Disposal of Property

P128- p157

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 7 of 176

October 2006

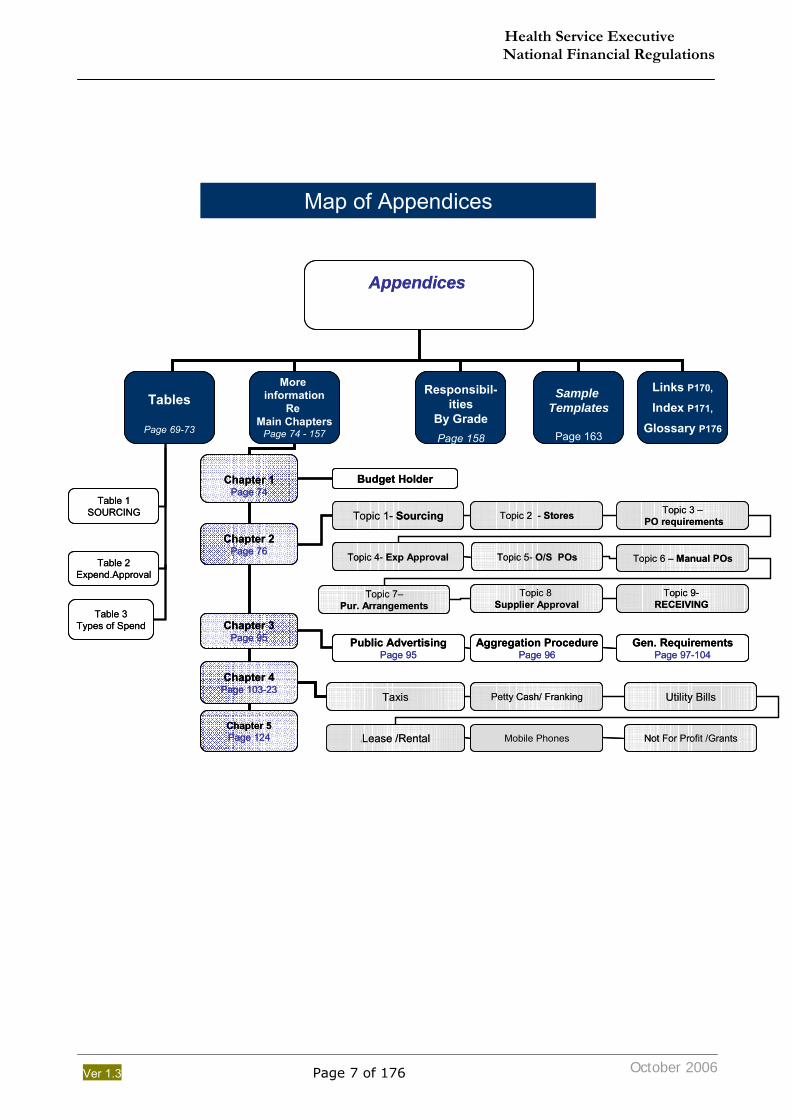

Appendices

Tables

Page 69-73

More information

Re Main Chapters

Page 74 - 157

Responsibil-ities

By GradePage 158

Sample Templates

Page 163

Links P170,

Index P171,

Glossary P176

Table 3Types of Spend

Table 1SOURCING

Table 2Expend.Approval

Chapter 1Page 74

Map of Appendices

Chapter 2Page 76

Chapter 3Page 95

Chapter 4Page 103-23

Budget Holder

Topic 1- Sourcing

Topic 4- Exp Approval

Topic 2 - Stores

Topic 5- O/S POs

Topic 3 –PO requirements

Topic 7–Pur. Arrangements

Topic 6 – Manual POs

Topic 8 Supplier Approval

Topic 9-RECEIVING

Public AdvertisingPage 95

Aggregation ProcedurePage 96

Gen. RequirementsPage 97-104

Taxis Petty Cash/ Franking Utility Bills

LLease /Rental Mobile Phones Not For Profit /GrantsChapter 5Page 124

Appendices

Tables

Page 69-73

More information

Re Main Chapters

Page 74 - 157

Responsibil-ities

By GradePage 158

Sample Templates

Page 163

Links P170,

Index P171,

Glossary P176

Table 3Types of Spend

Table 1SOURCING

Table 2Expend.Approval

Chapter 1Page 74

Map of Appendices

Chapter 2Page 76

Chapter 3Page 95

Chapter 4Page 103-23

Budget Holder

Topic 1- Sourcing

Topic 4- Exp Approval

Topic 2 - Stores

Topic 5- O/S POs

Topic 3 –PO requirements

Topic 7–Pur. Arrangements

Topic 6 – Manual POs

Topic 8 Supplier Approval

Topic 9-RECEIVING

Public AdvertisingPage 95

Aggregation ProcedurePage 96

Gen. RequirementsPage 97-104

Taxis Petty Cash/ Franking Utility Bills

LLease /Rental Mobile Phones Not For Profit /GrantsChapter 5Page 124

Health Service Executive National Financial Regulations

Ver 1.3 Page 8 of 176

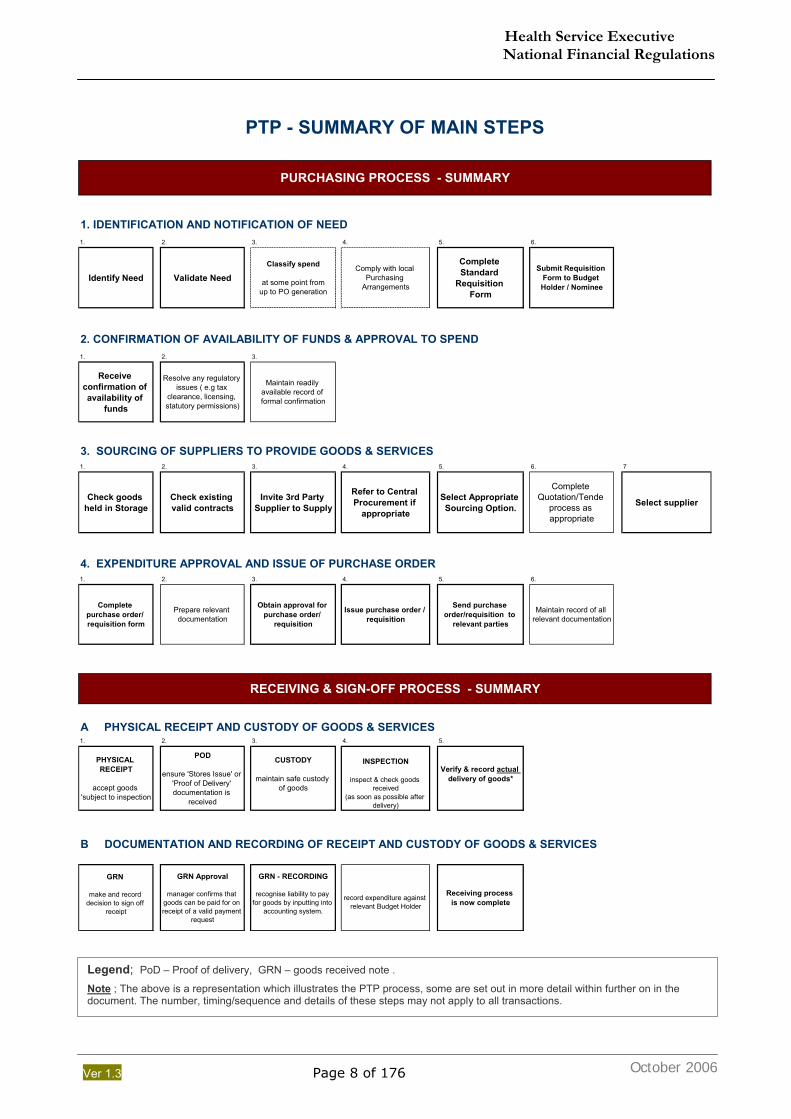

PTP - SUMMARY OF MAIN STEPS

1. 2. 3. 4. 5. 6.

Identify Need Validate NeedClassify spend

at some point fromup to PO generation

Comply with local Purchasing

Arrangements

Complete Standard

Requisition Form

Submit Requisition Form to Budget Holder / Nominee

1. 2. 3.

Receive confirmation of availability of

funds

Resolve any regulatory issues ( e.g tax

clearance, licensing, statutory permissions)

Maintain readily available record of formal confirmation

1. 2. 3. 4. 5. 6. 7

Check goods held in Storage

Check existing valid contracts

Invite 3rd Party Supplier to Supply

Refer to Central Procurement if

appropriate

Select Appropriate Sourcing Option.

Complete Quotation/Tende

process as appropriate

Select supplier

1. 2. 3. 4. 5. 6.

Complete purchase order/ requisition form

Prepare relevant documentation

Obtain approval for purchase order/

requisition

Issue purchase order / requisition

Send purchase order/requisition to

relevant parties

Maintain record of all relevant documentation

1. 2. 3. 4. 5.

PHYSICAL RECEIPT

accept goods 'subject to inspection

POD

ensure 'Stores Issue' or 'Proof of Delivery' documentation is

received

CUSTODY

maintain safe custody of goods

INSPECTION

inspect & check goods received

(as soon as possible after delivery)

Verify & record actual delivery of goods*

GRN

make and record decision to sign off

receipt

GRN Approval

manager confirms that goods can be paid for on receipt of a valid payment

request

GRN - RECORDING

recognise liability to pay for goods by inputting into

accounting system.

record expenditure against relevant Budget Holder

Receiving process is now complete

PURCHASING PROCESS - SUMMARY

3. SOURCING OF SUPPLIERS TO PROVIDE GOODS & SERVICES

2. CONFIRMATION OF AVAILABILITY OF FUNDS & APPROVAL TO SPEND

1. IDENTIFICATION AND NOTIFICATION OF NEED

A PHYSICAL RECEIPT AND CUSTODY OF GOODS & SERVICES

B DOCUMENTATION AND RECORDING OF RECEIPT AND CUSTODY OF GOODS & SERVICES

RECEIVING & SIGN-OFF PROCESS - SUMMARY

4. EXPENDITURE APPROVAL AND ISSUE OF PURCHASE ORDER

Legend; PoD – Proof of delivery, GRN – goods received note .

Note ; The above is a representation which illustrates the PTP process, some are set out in more detail within further on in the document. The number, timing/sequence and details of these steps may not apply to all transactions.

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 9 of 176

0. Introduction to Financial Regulations

0.1. The National Financial Regulations (NFR) contained within this document update and replaces all previous Financial Regulations unless otherwise specified.

0.2. The Financial Regulations form an integral part of the overall system of Financial Corporate

Governance and are intended as the framework underpinning the System of Internal Financial Control.

0.3. The Financial Regulations have been prepared to reflect current best practice generally, as

well as the guiding principles and best practice embedded within the processes under the scope of the Financial Information System Project (FISP).

0.4. Particular attention has been made to ensure that the Financial Regulations, are consistent

with statutory requirements and government guidelines.

0.5. In addition, existing former Health Board and other Financial Regulations already in existence throughout the country and elsewhere have been reviewed, and the best elements have been incorporated as part of the development of these regulations.

0.6. A range of primary reference materials have been used including:

NPPPU Government Procurement Guidelines (2004) Health Service Procurement Policy (updated Jan 2006) Department of Finance Code of Practice for the Governance of State Bodies Prompt payment legislation (1997 Act & SI388 dated 2002) EU tendering legislation FISP design documentation

0.7. The regulations outline responsibilities for all levels of management and staff.

0.8. The importance of managers and staff recognising their personal responsibilities in relation

to the understanding of and compliance with the Financial Regulations is stressed.

0.9. The Financial Regulations and compliance with them will require continuous monitoring by management at all levels to ensure that the level of assurance provided, regarding the effectiveness of our system of internal financial controls, is maximised.

0.10. The initial task for managers in implementing these new Financial Regulations is to identify

any areas where there may be compliance gaps and put in place planned actions to address these gaps.

Nominees of National Management Team Members 0.11. Where these financial regulations reference members of the National Management Team,

such references can be taken to include their formally delegated nominees, unless otherwise expressly provided.

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 10 of 176

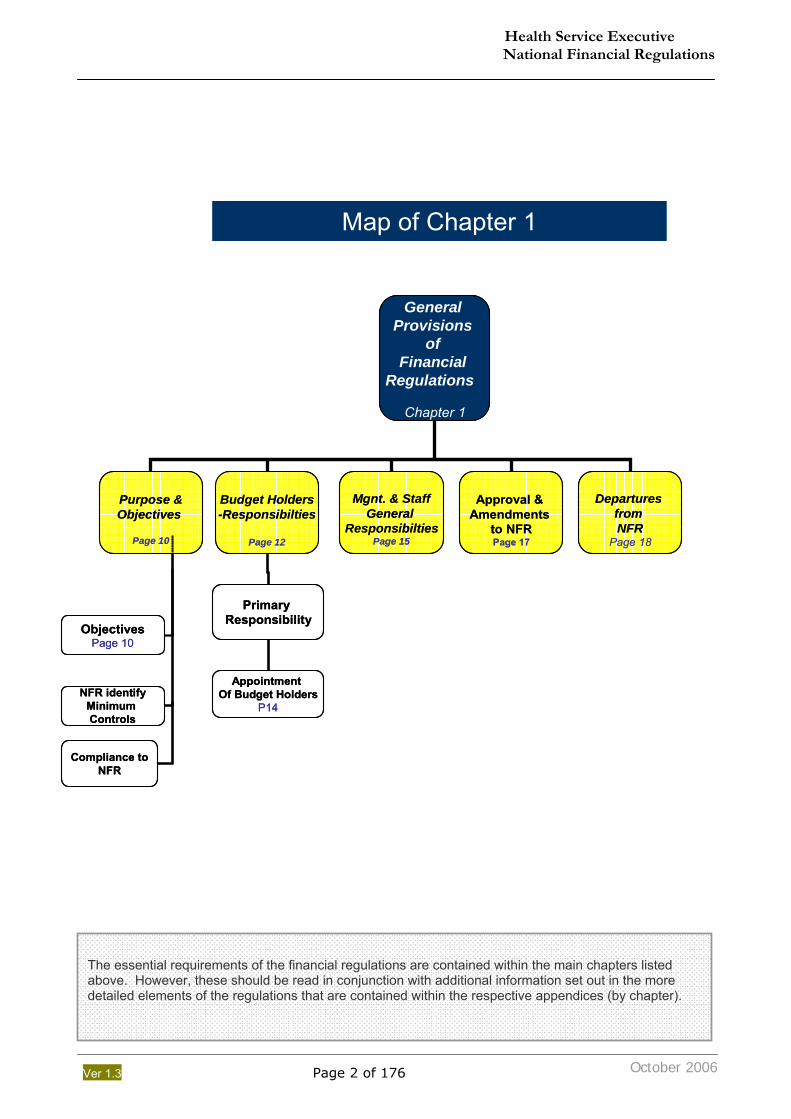

1. General Provisions regarding Financial Regulations

Go to next chapter; on page 19 Go to Appendix ; on page 68

1.a Purpose and Objectives of Financial Regulations Ref; Page 10 1.b Appointment & Responsibilities of Budget Holders Ref; Page 12 1.c General Responsibilities of Management and Staff Ref; Page 15 1.d Approval and Amendment to the Financial Regulations Ref; Page 17 1.e Departures from the Financial Regulations ; Ref; Page 18 Approval, Recording, Annual Review and Reapproval The key requirements of the financial regulations are contained within the main chapters. However, this should be read in conjunction with the ‘additional information’ which sets out in the more detailed elements of the regulations that are contained within the respective appendices (by chapter). 1.a Purpose and Objectives of Financial Regulations

1.1. Introduction 1.1.1. The Financial Regulations are intended to outline the high level framework within

which the internal financial control system of the Health Service Executive (HSE) will operate.

1.1.2. These regulations are not intended as a detailed procedural guide for financial

processes or activity within the HSE as the organisation is too diverse to allow that to be achieved in a practical and accessible document.

1.1.3. This document may be of assistance in providing training to managers and staff as to

what their obligations are around compliance with the Financial Regulations, however, it has not been produced as a training document, again for reasons of practicality.

1.1.4. These regulations have been prepared with the intention of ensuring that the financial

controls in operation within the HSE are consistent with: Irish and EU statutory requirements Achievement of Best Value for Money Department of Health and Children and Government policies and guidelines Presently available best practice appropriately interpreted for the Irish Public

Health Service context.

1.2. Compliance with Financial Regulations

1.2.1. No set of Financial Regulations will be effective unless they are specific, understood and monitored for compliance.

1.2.2. It is the responsibility of all Budget Holders, managers and staff to ensure that

the day-to-day operations and procedures of the organisation comply with the Financial Regulations.

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 11 of 176

1.2.3. Budget Holders must ensure that a record is maintained of the training undertaken by

each employee with regard to Financial Regulations. Certification of users of the Financial Regulations where applicable, together with other relevant training records (e.g. Financial Information System/Accounting training) should be maintained as a record of user knowledge, available skill sets, training history etc.

1.2.4. All Budget Holders and other managers and staff have a direct responsibility to be pro-

active in ensuring that they are aware of, understand and comply with these Financial Regulations.

1.2.5. Persistent and negligent failure to comply with the Financial Regulations is a very

serious matter for any HSE employee and may lead to disciplinary proceedings.

1.3. Objectives 1.3.1. The Financial Regulations and the system of internal financial controls that they

underpin are intended to:

i. Support the achievement of the corporate objectives of the HSE

ii. Ensure the HSE operates within the limits of its notified Budget

iii. Facilitate open and transparent accountability for the financial resources

entrusted to the HSE

iv. Support the efficient and effective use of resources assigned to HSE

v. Ensure the safeguarding of the assets of the HSE

vi. Reduce the likelihood of fraud, theft or error in relation to financial matters

and increase the likelihood of its detection

1.4. Context

1.4.1. These Financial Regulations and compliance with them must be viewed in the context of the role of the HSE which is to improve the health and social well being of the population it serves.

1.4.2. Proper financial controls will assist the Health Service Executive in meeting this

primary objective.

1.5. Financial Regulations identify Minimum Controls 1.5.1. These Financial Regulations set out what are, in effect, minimum standards of

financial controls that are acceptable across this very large and diverse organisation.

1.5.2. It is the responsibility of every Budget Holder and his/her staff to put in place and document the detailed arrangements applicable to their own areas of responsibility.

1.5.3. Budget Holders may decide to apply a higher level of control than the minimum set out in the regulations in order to achieve the objectives of the Financial Regulations. For example, expenditure control could be amended for local use so that the value that each grade has approval authority for could be lower than that allowed by these regulations.

Health Service Executive National Financial Regulations

Ver 1.3 Page 12 of 176

Related Appendix ; on page 74

1.b Responsibilities and Appointment of Budget Holders

Budget Holders & Budget Holding More Information regarding Budget Holders responsibilities, see appendix on page 74.

1.6. Minimum Controls required by these Financial Regulations

These regulations require: 1) That there is clarity as to which managers are budget holders and this is known both to

the budget holders and generally, as required.

2) That each budget holder is clear as to what his or her key responsibilities are, and are complying with same to the greatest extent possible.

3) That formal assignment of budget amounts to budget holders must be notified

N1 by the Finance Directorate on foot of decisions of the Chief Executive, each National Directors and their relevant staff.

1.7. These regulations do not require:

1) The delegation of budget holding responsibility N2 to any particular level or grade within the organisation or

2) Complete uniformity across the HSE as to the level at which, or the grades, by which

budgets are held and managed

1.8. Primary responsibilities of Budget Holders

These are:

1) To operate within the limits of the budgets notified to them subject to the overall direction of the budget holder to whom they report

2) To monitor variances from budget limits on an ongoing basis and initiate corrective

measures in order to bring financial performance in on target, at the latest, by the end of each financial year

3) To co-operate fully with the requirements of the budget holder to whom they report so

that higher level budget holder can meet their primary responsibility as outlined above.

4) To comply with the additional responsibilities placed upon them in relation to the general system of internal financial controls as dictated by these financial regulations (see par1.9 below)

1 Notification via the Finance Directorate is a basic control requirement to ensure there is overall corporate clarity in terms of the total financial resource being managed. Responsibility and Authority for budgets, once notified, rest with each of the HSE National Directors, and their staff. 2 It is expected that, over time, HSE will move towards appropriate national standardisation in relation to a range of matters including budget holding and budget management.

Health Service Executive National Financial Regulations

Ver 1.3 Page 13 of 176

Related Appendix; on page 74 Note:

At its most basic and simplified level, the key objective of budget management is to ensure that the HSE meets its statutory requirement not to spend more money, in total, than it has been given by the Oireachtas. In order to meet this objective the HSE needs to assign budgets to individuals so that they can be managed effectively. In essence the Chief Executive assigns budgets to the National Directors who in turn assign them to Assistant National Directors / Hospital Network Managers etc and so on down to whatever level is considered appropriate and feasible by each manager in the chain.

Accountability is exercised in a top down manner. Each budget holder remains fully responsible and accountable for the budget assigned to them regardless of however many levels of staff below them they may have assigned as budget holders. If a budget holder at a particular level achieves breakeven by year end, it is entirely possible that the budget holders they are managing below them may have achieved a variety of results with some over budget and some under budget. This is a matter in the first instance between the higher level budget holder and those managing budgets below him or her. While it would clearly be preferable for all budget holders at all levels to be assigned budgets that they can realistically manage this, for a variety of reasons this may not always be possible. The key requirement is for the higher level manager and those below them to work effectively together so that overall breakeven is achieved. A local budget holder who overspends their budget is unlikely to be considered to be in breach of these financial regulations provided they, at all times;

Act responsibly and pro-actively in managing their budget Keep their manager fully informed of any emerging and continuing material issues affecting

their capacity to achieve financial breakeven Identify any practical options to address these material issues Take corrective action as early as possible Comply fully with any requests or directions of their manager

1.9. Additional responsibilities of Budget Holders in relation to

1.9.1. Financial Controls generally and

1.9.2. The wider aspects of the Financial Regulations

Budget Holders are seen as key managers of resources and as such it is generally appropriate for them to play a role in relation to aspects of financial control that extend beyond the primary requirement for managing budgets within set limits.

These additional responsibilities are set out in more detail in Appendix “Budget Holders – Additional Information” on page 74 and include requirement to ;

1.9.3. To ensure compliance with these Financial Regulations. (A1.2 below).

1.9.4. To put in place Specific Arrangements. (A1.3 below)

1.9.5. To mitigate control deficits with regard to compliance with

the Financial Regulations. (A1.4 below)

1.9.6. To make efficient use of resources. (A1.5 below)

Health Service Executive National Financial Regulations

Ver 1.3 Page 14 of 176

1.10. Appointment of Budget Holders Related Appendix; page 74

1.10.1. All budget holders must be approved and each must be notified of their assignment as budget holders

1.10.2. Only a budget holder can approve the assignment of another person as a budget

holder

1.10.3. Such assignment can only be in relation to an element of the budget held by the budget holder approving the assignment.

1.10.4. Such assignment can only be to a staff member of the budget holder making the

assignment.

1.10.5. The following are deemed, by virtue of the approval of these regulations, to be budget holders in respect of their own areas of responsibility unless otherwise directed by the CEO or their National Director:

National Directors

Assistant National Directors

Hospital Network Managers

Local Health Managers

NHO Hospital Managers

1.10.6. The approval of the assignment of any budget holders below the levels at 1.10.5

above will only take effect once notified to the relevant Assistant National Director of Finance or their nominee(s)

Health Service Executive National Financial Regulations

Ver 1.3 Page 15 of 176

1.c General Responsibilities of Management and Staff

1.11. Managers / Supervisors – General Responsibility

Not withstanding the primary role of the Budget Holder, every manager and supervisor has responsibility in regard to complying with, and assisting with documenting and periodically updating formal arrangements in respect of all the financial processes delegated to him/her including:

a) Responsibility to ensure regulations are complied with by him/her and by any managers and staff that may be involved in the financial processes.

b) Responsibility to ensure awareness, understanding, knowledge, experience, training and

development of any managers and staff he may involve in the processes.

c) Responsibility to minimise staff resource utilised in the financial processes consistent with achieving value for money and complying with the Financial Regulations.

d) Responsibility to mitigate any compliance or capacity deficits regarding any of the managers and staff she/he may involve in the process and notify same to the Budget Holder

1.12. Staff – General Responsibility

1.12.1. Each member of staff has similar responsibilities to the manager / supervisor in respect of themselves with regard to:

Compliance with the regulations. Being personally proactive about his/her own awareness, understanding,

knowledge, training and development in order to ensure this compliance.

1.13. Responsibilities not reduced due to reliance on Health Service Executive Shared Services (HSE-SS)/ Estates / Procurement.

1.13.1. The fact that Budget Holders and their managers may rely upon the Shared Services Organisation or any other party outside their direct control to support them in terms of financial or purchasing activities does not diminish their personal responsibility to ensure compliance with these regulations.

1.13.2. It is a matter for each Budget Holder to effectively manage their relationships with

HSE-SS or any external provider to provide them with the assurances they need around compliance with these regulations.

1.13.3. In practical terms Budget Holders will exercise this responsibility by ensuring that they

fully engage in a proactive manner with the HSE SS in the ongoing monitoring and review of the services provided on their behalf.

Health Service Executive National Financial Regulations

Ver 1.3 Page 16 of 176

1.14. Audit – A Key element of the System of Financial Corporate Governance.

1.14.1. As stated above the Financial Regulations are intended to provide a framework

underpinning the system of Internal Financial Control.

1.14.2. The Financial Regulations will only be effective if they remain robust in nature and if there is a high level of ongoing compliance with their provisions. The responsibilities of Budget Holders, Management and Staff in this regard have been set out on page 12 and 15 and Appendix on page 68 .

1.14.3. Ongoing independent review and compliance monitoring by both internal audit and

external audit (Comptroller and Auditor General) is a key element of the overall assurance required by the Chief Executive Officer and the Board of HSE in respect of the effectiveness of the System of Internal Financial Control.

1.14.4. Further assurance is provided by the existence of a pro-active and empowered Audit

Committee under the guidance of the main board.

1.15. Audit Trail

Throughout these financial regulations there are direct and indirect references that establish the minimum controls that should operate, including supporting documentation, evidence of supply etc. There is an overall requirement irrespective of the level of automation or complexity of the process that sufficient Audit Trail G1 is maintained.

Within the document you will notice that there are; N1 etc - This refers to notes that will appear at the end of the respective page G1 etc. – This refers to Glossary items which provide an explanation of a term used. These will appear at the end of this document but can be accessed by clicking on the item.

Health Service Executive National Financial Regulations

Ver 1.3 Page 17 of 176

1.d Approval of and Amendment to The Financial Regulations

1.16. These regulations take effect when approved by the HSE Chief Executive Officer and the

HSE Board.

1.17. Proposed amendments to the regulations must be recommended by the National Director of Finance and approved by the HSE Chief Executive Officer and the HSE Board.

1.18. Initial approval and any subsequent amendment to the Financial Regulations must be recorded on a formal written decision.

1.19. Clarifications required in respect of these regulations should be addressed to the relevant

Assistant National Director of Finance in the first instance.

Health Service Executive National Financial Regulations

Ver 1.3 Page 18 of 176

1.e Departures from regulations; Approval, Recording, Annual Review and Reapproval

1.20. Unless otherwise provided for in these Financial Regulations, any departures from the regulations must be:

Approved by the relevant National Management Team Member (or Assistant

National Director delegated by the NMTM) and

Co-signed by the relevant Assistant National Director of Finance.

Explained and recorded by way of formal written decision.

Reviewed formally by the relevant MTM or Assistant National Director delegated at

the end of the financial year.

Approved by the relevant MTM and the National Director of Finance where there are

repeated departures from regulations that span more than one financial year.

1.21. The requirement is that a departure from the Financial Regulations must normally represent an interim measure pending the resolution of the issue giving rise to the need for the departure.

1.22. Actions necessary to address issues giving rise to departures from the Financial

Regulations should be identified and implemented as soon as is practicable.

1.23. The relevant National Management Team Member (or Assistant National Director delegated) must identify any additional measures, for example additional supervision or random checking, necessary to mitigate any control risks associated with a departure from the Financial Regulations.

1.24. Such mitigation measures must be complied with fully by the relevant managers and staff.

1.25. The formal written decision approving or renewing a departure from the Financial

Regulations must record:

Description and explanation of the issues giving rise to the need for an approved departure from the Financial Regulations.

Service Area / Location and Budget Holder (s) covered by the departure

Expected duration of the departure and actions proposed to remove the need for the

departure over the short or medium term.

Any expected control risk associated with the departure from the Regulations and the measures being proposed by the National Management Team Member to mitigate that risk.

Health Service Executive National Financial Regulations

Ver 1.3 Page 19 of 176

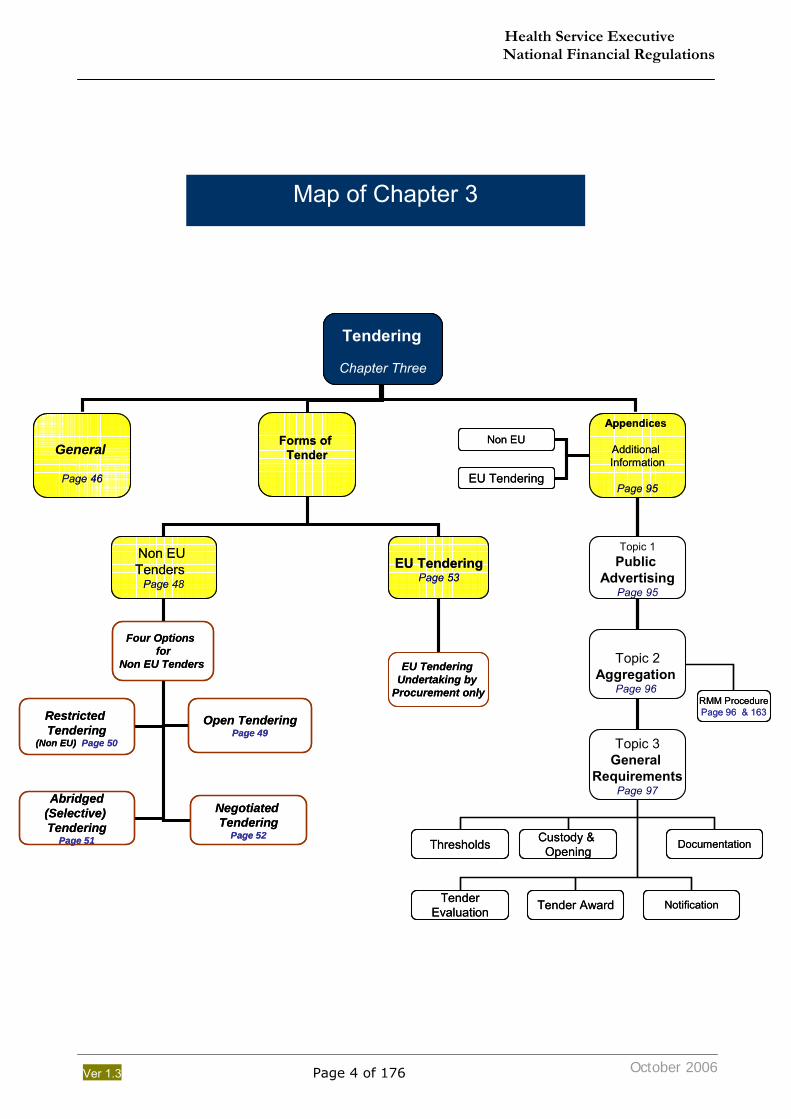

Go to next chapter; on page 46 Go to last chapter; on page 10

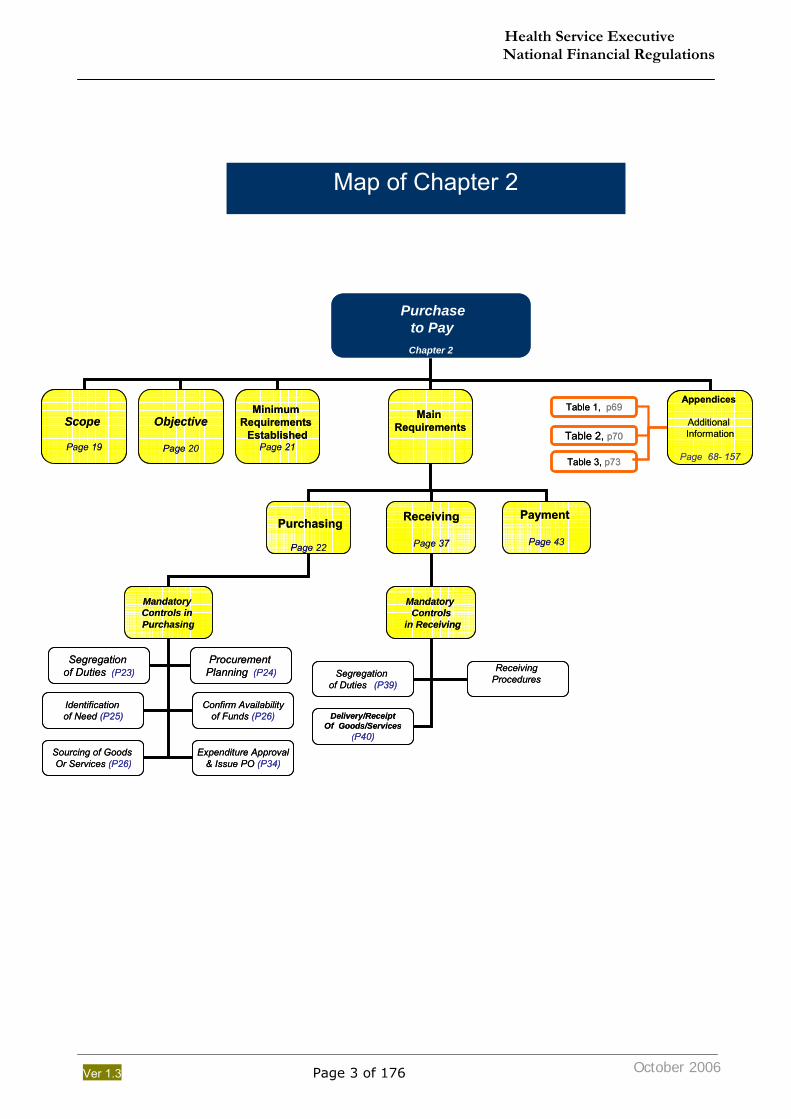

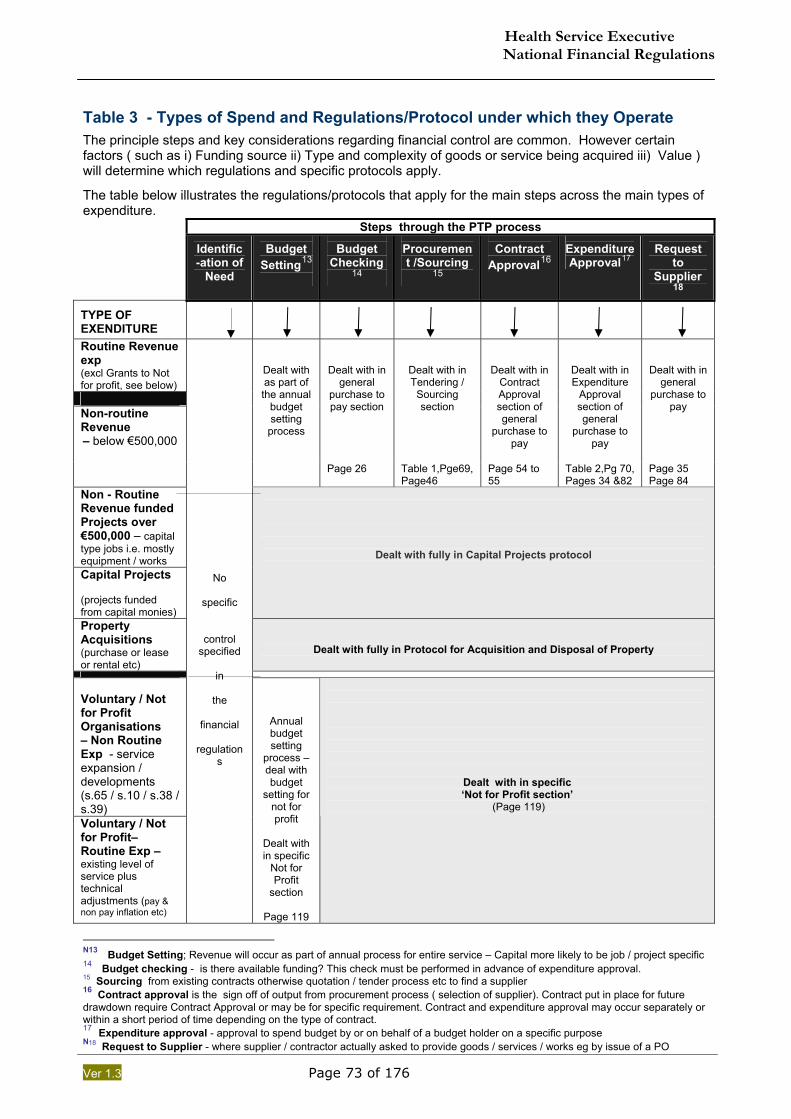

2. Purchase to Pay (General)

The key requirements of the financial regulations are contained within the main chapters. However, this should be read in conjunction with additional information set out in the more detailed elements of the regulations, contained within the respective appendices (by chapter).

2a. Scope 2b. Objective of the Financial Regulations in respect of the ‘Purchase to Pay’ Process. on page 20 2c. Purchase to Pay regulations are Minimum Requirements on page 21 2d. Purchasing Process – Main Requirements on page 22 2e Receiving Process – Main Requirements on page 37 2f Payment Process – Main Requirements on page 43 APPENDIX - More Information re. Chapter 2 Topics on page 76 to 95

2a. Scope

The regulations within this section are intended to set out the Primary Financial Control requirements for all non-pay expenditure (i.e. expenditure not processed through the payroll system).

Summary of Purchase to Pay (PTP) – basic steps / stages

2.1. Section 1.11 above ‘Responsibilities of Management and Staff’ sets out in detail the personal responsibility of Budget Holders, managers and staff in relation to these regulations.

Please ensure that you are familiar with this section before reading this regulation.

Obtaining expenditure approval,

Sourcing of appropriate goods / services from 3rd parties or Stores to meet identified service needs.

Formally requesting the selected 3rd party to provide specified goods or services by issue of PO or contract.

1. PURCHASING

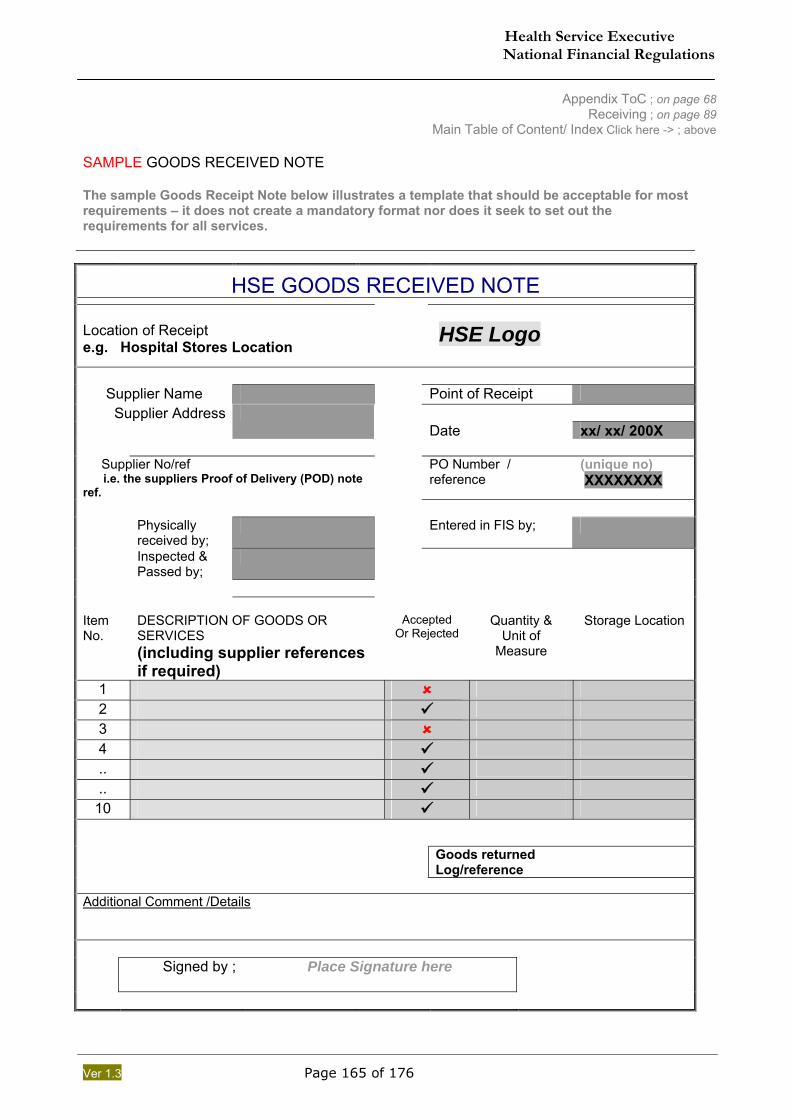

Receipt and checking / inspection of goods and services.

Confirmation that they are fit for purpose, and match what was ordered or contracted for.

Approval that Goods/Service can be paid for upon receipt of an appropriate request for payment

2. RECEIVING ( receipt of goods or services)

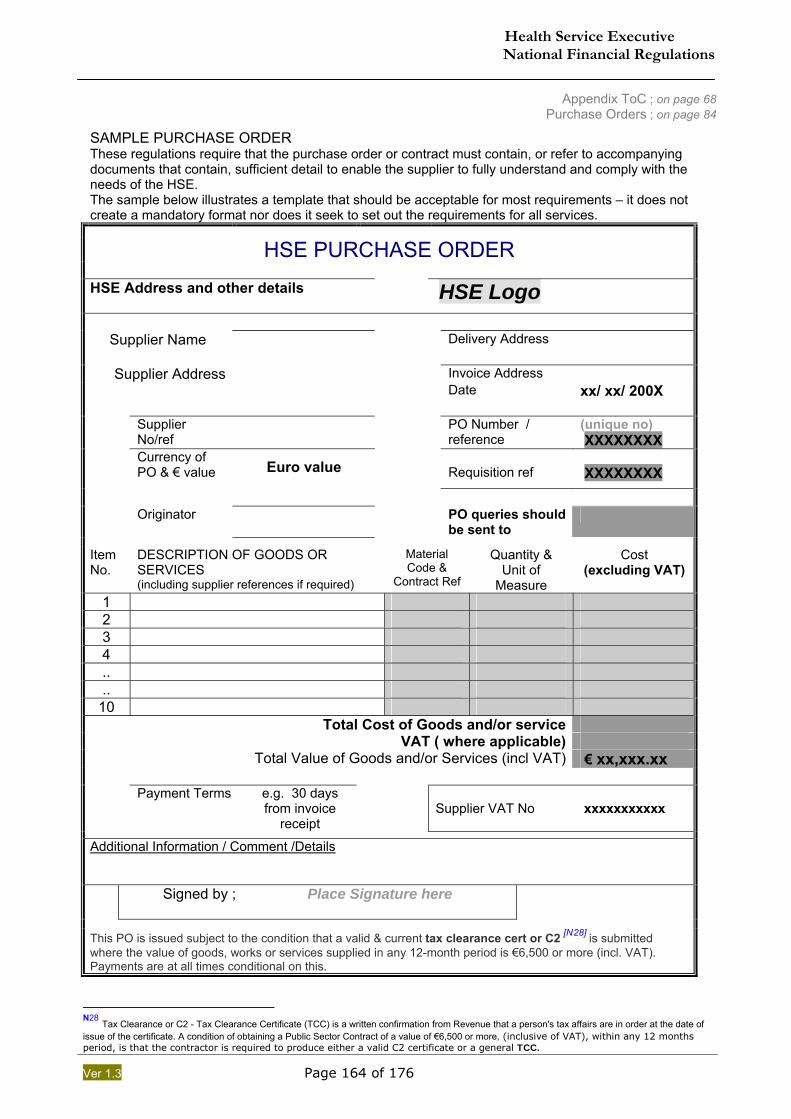

● for goods and services – generally on foot of invoices or other payment requests. ● A Key control within this process is the checking and verification of the invoiced price of good or services to the purchase order price.

3. PAYMENT

October 2006

Health Service Executive National Financial Regulations

Ver 1.3 Page 20 of 176

Go to Start of Chapter ;on page 19

2b. Objective of the Financial Regulations in respect of the ‘Purchase to Pay’ process. The objectives set out below are in addition to those relevant to the entirety of the regulations which are listed in section 1.a Purpose and Objectives of Financial Regulations on page 10.

2.2. The objectives of the Financial Regulations in respect of the Purchase to Pay Process are to ensure the HSE, its Budget Holders, Managers and Staff;

Comply with Government and EU Procurement requirements and ensure that the

procurement process is open and competitive. Properly assess the HSE procurement requirements on a periodic basis to enable

proper procurement planning. Demonstrate full accountability and probity as well as the highest ethical standards in

respect of the public funds expended in the purchasing process. Acquire goods and services that are most appropriate and represent best value for

money for the health service in terms of full life-cycle costs.

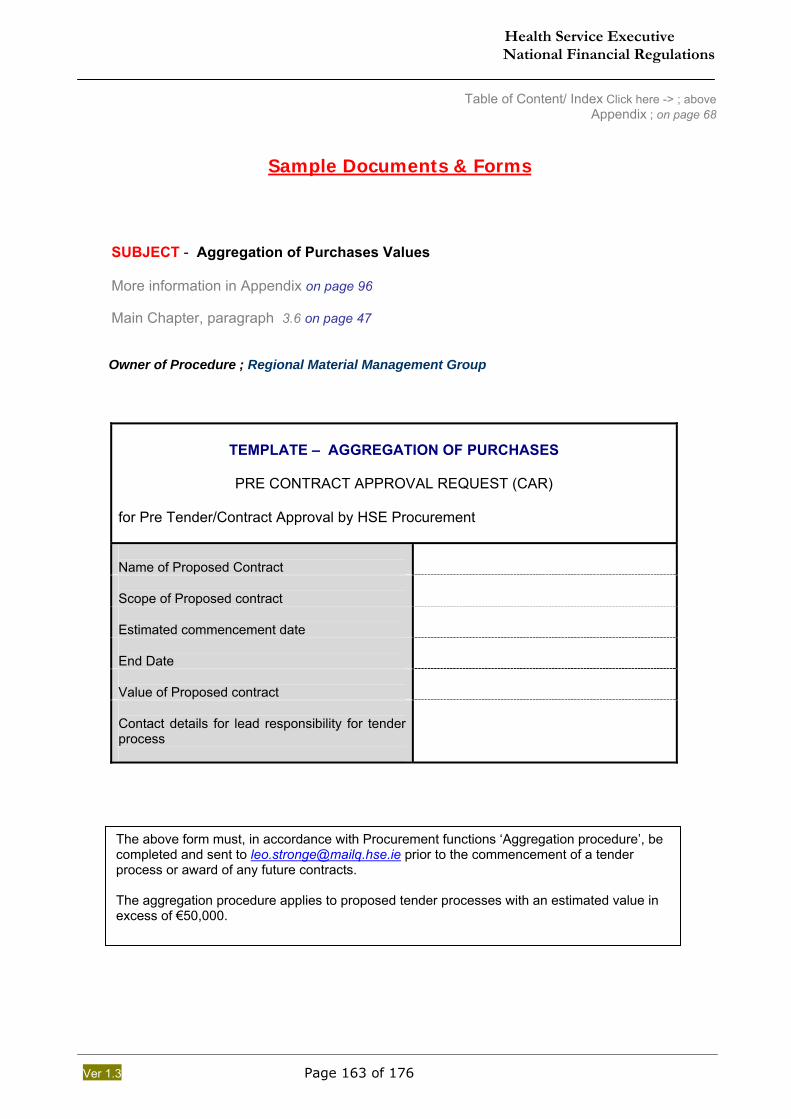

Make best use of the purchasing power of the HSE by entering into contracts including national contracts, wherever appropriate. Aggregate G2 demand to optimise purchasing power (ref to Page 47)

Obtain formal approval from the appropriate Budget Holder or their nominee before requesting the provision of any goods, services or works.

Do not engage in purchasing above the limits of the budget available.

Operate the 'Purchase To Pay' process in an efficient and effective manner that

facilitates the timely production of accurate and comprehensive Annual Financial Statements (AFS).

Properly manage their contacts with suppliers and provide full clarity to suppliers as

regards what is expected of them in relation to all aspects of the process. Consistently apply high standards with respect to evidencing and recording of

‘Receiving’ of Goods/Services and custody of goods.

Health Service Executive National Financial Regulations

Ver 1.3 Page 21 of 176

Go to start of Chapter; on page 19

2c. Purchase to Pay regulations establish PTP Minimum Requirements

2.3. These regulations set out what are minimum requirements around many aspects of the purchase to pay process including:

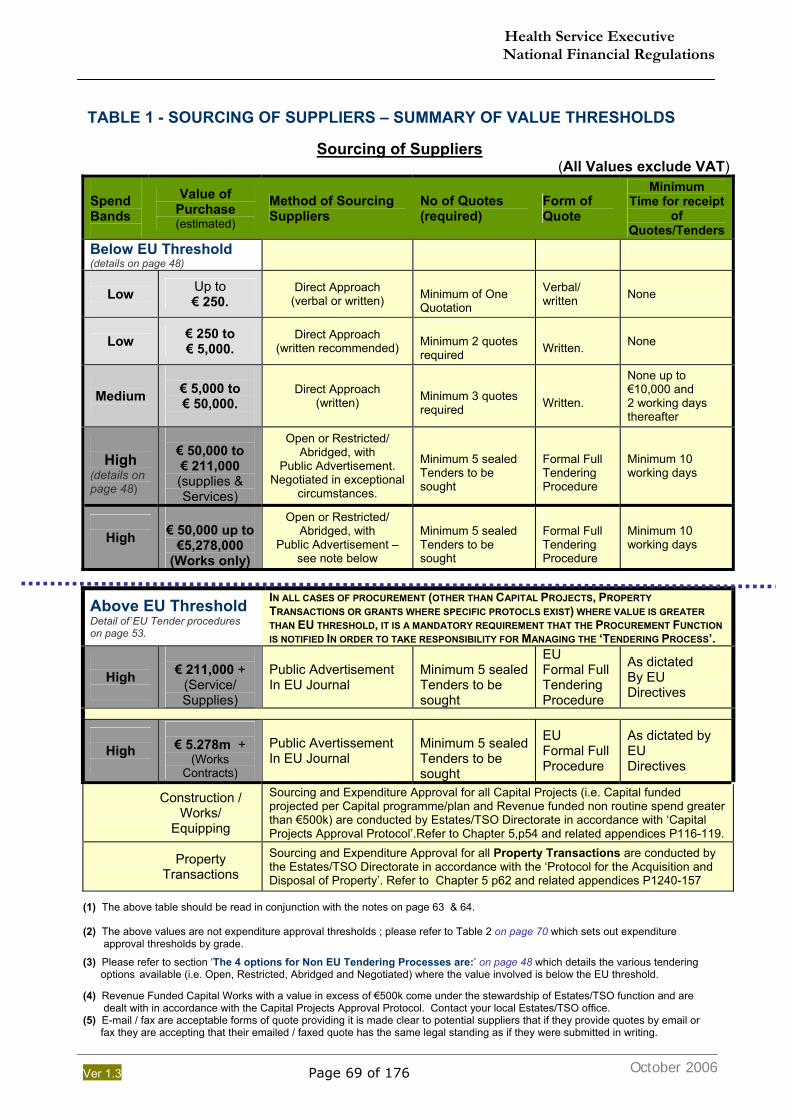

1. Number of quotes / tenders required. (details on page 69) 2. Value thresholds for different sourcing options. (details on page 69) 3. Approval levels. (details on page 70) 4. Time periods for receipt of quotes / tenders.

2.4. The requirements set out in this chapter relate to Non Pay expenditure. In addition, there are other requirements that arise due to the specific nature of expenditure and which are governed by separate protocol. These include;

2.4.1. Capital Projects – Project Approval is governed by Capital Projects Approval

Protocol.

2.4.2. Property Transactions - is governed by the Property Transaction Protocol - ‘Protocol for the Acquisition and disposal of Property’.

2.4.3. Funding of Voluntary Organisations (Not for Profit/Grants).

2.5. It is a requirement that managers operating these regulations will apply higher than the

minimum control level (e.g. next level up authorisation) if this is necessary to ensure the objectives set out above at 2.B. are consistently achieved.

Example: A manager may decide that in the case of purchase of routine medical consumables for one of his/ her hospitals he/she needs to get a Grade Vl to approve any purchase between €5,000 and €10,000 (see Table 2 - normally a Grade V can approve expenditure up to €10,000 for routine expenditure) because of any one or a combination of the following: He needs a tighter level of financial control for the remainder of the financial year in order to clear an overspend earlier in the year He does not have a sufficiently experienced Grade V

He decides that the complexity of the equipment or its purchasing process warrants it.

2.6. The actual steps, the number of steps and the sequencing of steps in the process that is being referred to as “Purchase to Pay” will vary depending on a number of factors including:

Type and complexity of goods or service being acquired. For more complex services, works and equipping, third party sign-off shall be required at each stage of the Purchase to Pay process.

Frequency of purchase of specific goods / services

Value

The source of the goods or services

Specific service unit or area acquiring the goods / services etc

The level of computerisation within the process

but the fundamental process and the required financial controls are common.

Health Service Executive National Financial Regulations

Ver 1.3 Page 22 of 176

Go to Start of Chapter ;on page 19 Receiving Process – Main Requirements on page 37 Payment Process – Main Requirements on page 43

2d. PURCHASING/PROCUREMENT; MAIN REQUIREMENTS

2.7. Definition For the purpose of these regulations purchasing includes all activities up to the point where:

A supplier(s) has been selected The supplier(s) has been formally requested to provide goods /services.

2.8. FOUR KEY ELEMENTS for each Purchasing Transaction It is clear that each and every purchasing transaction will have the following elements:

1 Identification and notification of need. Page 25 2 Confirmation of availability of funds and approval to spend. Page 26 3 Sourcing of supplier(s) to provide goods or services. Page 28 4 Formal request issued to supplier to provide goods/services. Page 34

2.9. General Application of Purchasing Regulations

These regulations cover the entire HSE which is a large and very diverse organisation. It is not practical to cover all potential situations or differences that may exist regarding:

2.9.1. Exactly by whom or in what manner a need for goods or services is identified and communicated.

2.9.2. At what precise stage or by whom the approval to spend available funds is decided.

2.9.3. Exactly how the supplier of goods or services is to be sourced in each specific case. Use of HSE standard procedures should be availed of where appropriate.

2.9.4. The precise manner and by whom the formal request to the supplier to provide the goods or services is made.

2.9.5. Budget Holders must ensure that there are documented Purchasing Arrangements in place for Managers and Users for each respective location /main category of spend. (More Information on page 87 )

2.10. Application of Purchasing Regulations to Bodies funded by the HSE

2.10.1. Where works and related service contracts are being awarded by external

organisations and are funded more than 50% the requirements of these regulations as regards sourcing of suppliers are applicable.

2.10.2. Budget Holders must ensure that relevant voluntary, not for profit or other such

organisations are aware of this requirement and it should be included as part of any service agreement or other contract with such organisations.

2.10.3. Refer to Funding Provided to ‘Not for Profit’ organisations, on page 119.

PURCHASE PROCESS

Health Service Executive National Financial Regulations

Ver 1.3 Page 23 of 176

MANDATORY CONTROLS WITHIN PURCHASING.

These regulations prescribe the following mandatory controls within the Purchasing process:

I. Segregation of Duties within Purchasing Ref # below

II. Procurement Planning Ref on page 24 III. Identification and notification of need Ref on page 25 IV. Confirmation of Availability of Funds and Approval to Spend Ref on page 26 V. Sourcing of Suppliers to Provide Goods and Services Ref on page 28 VI. End of Purchasing Stage; Approval & Issue of Purchase Order Ref pages 34 to 37

( I ) Segregation of Duties within Purchasing Next; ‘Identification of Need’ on page 24

2.11. Appropriate segregation of duties is a key element of any financial control framework. In the context of the purchasing process the following requirements are mandatory;

2.11.1. At some point between initial identification of need and the issue of a purchase order

or contract at least one other staff member in addition to the final decision maker must be involved in the process.

This must be evidenced by signatures appearing on purchasing documents e.g. requisition, purchase orders.

2.11.2. No manager (or staff) should have the final decision regarding the issue of a

purchase order or contract for any goods or service that is for their own day to day use.

2.11.3. There must be a clear separation of tasks between the person raising a Purchase

Order and Recording the ‘Receipt’ of the respective goods/Service.

2.11.4. There is a mandatory requirement to obtain appropriate professional procurement input where the value of purchases exceeds €25,000.

2.11.5. Decisions to authorise expenditure (i.e. to issue purchase order or contract) above

€50,000 must be formally written and recorded.

These decisions must be recommended by a manager at least at Grade V who must not be the same person that has 'signed off' the initial decision.

2.11.6. A minimum of 2 staff, one of whom must be Grade VIII or above must be involved in

both the opening and evaluation of all tenders.

2.11.7. Managers responsible for evaluating tenders (i.e. above €50,000) must not have the final decision as regards selection of the successful tenderer and / or approval to issue the purchase order or contract.

Health Service Executive National Financial Regulations

Ver 1.3 Page 24 of 176

2.11.8. Procurement must be notified of and co-ordinate all tenders above the EU threshold

except those tenders relating to Capital Projects which are the responsibility of the Estates Office.

2.11.9. Procurement is responsible for the ‘Commercial Evaluation’ of all EU Tenders

(other than ‘Works’ agreed specialist supplies). The person responsible for procurement shall co-ordinate procurement process and prepare tender analysis report for purchase approver/budget holder’s evaluation.

2.11.10. The Budget holder/Purchase approver makes the ‘decision’ to proceed /’sign-off’ a

tender based on tender report prepared by Commercial Evaluator.

2.11.11. Budget holders must maintain a list of ‘Commercial evaluators’ N3 for the Tender process

2.12. Segregation of duties (SOD) within purchasing should be read in conjunction with

Segregation of duties within receipt/receiving of Goods and Services on page 39.

( II ) Procurement Planning

Next; ‘Identification of Need’ on page 25

2.13. Budget Holders must, within twelve months of the coming into force of these regulations, ensure that they have reviewed and analysed their likely purchasing requirements over the following 3 years.

2.14. They must put in place a procurement plan, in conjunction with procurement/ Materials

Management/ Estates/ICT as appropriate to address:

2.14.1. Appropriate categorisation and rationalisation of suppliers.

2.14.2. Contracts to be renewed or terminated/allowed to lapse and their timeframes

2.14.3. Additional contracts to be put in place

2.14.4. Main service developments (new services, service expansions, service reductions) likely to impact on procurement over the following 12 months.

2.14.5. Any other relevant matters.

2.15. Procurement plans should be updated annually and replaced every three years.

Given the need for obtaining value for money and making best use of scarce staffing resources there is a requirement to co-ordinate and aggregate procurement plans.

N 3 Commercial Evaluators provide support through the procurement process by (a) Co-ordinating the procurement process (b) provide commercial tender analysis (c) ensure purchase systems and procedures are implemented, (d) procure supplies in line with current purchasing policies and procedures.

Health Service Executive National Financial Regulations

Ver 1.3 Page 25 of 176

2.15.1. Specific Assistant National Director(s) delegated by a National Management Team

Member must take the lead in the procurement planning process with appropriate professional procurement input.

2.15.2. It is a mandatory requirement that procurement plans identify any likely purchases

which will require the use of a tendering process or the EU Procurement Procedure, based on the value thresholds.

2.15.3. Account must be taken of the full likely HSE requirement for the goods or service in

deciding which value threshold and related sourcing option is appropriate.

( III ) Identification and Notification of Need Next; ‘Confirm Available Funds’ on page 26

2.16. Managers and staff who identify and communicate needs for goods and services must satisfy themselves and be in a position to demonstrate that the need:

2.16.1. Is genuine and is appropriate to their service.

2.16.2. Takes account of prevailing policies and constraints (including statutory compliance requirements) together with resource constraints under which their service is operating .

2.16.3. Person Approving expenditure must be aware of cost/value of items/service required and knowledge of budget.

2.16.4. Has been identified following a review of existing goods and services that may

already be available to the service

2.17. There is a requirement to obtain appropriate professional procurement input where the value of purchases exceeds €25,000 (see paragraph 2.11.4 above). i.e. for purchases in excess of €25,000 the procurement function should be contacted and guidance sought.

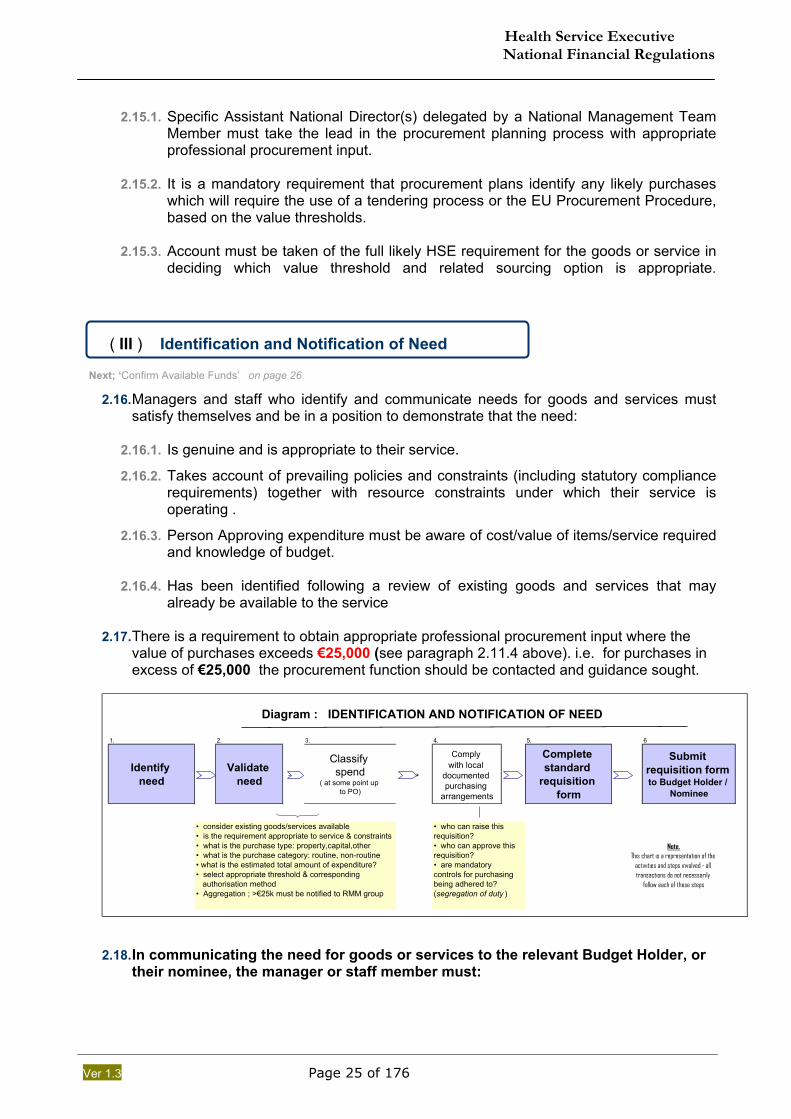

1. 2. 3. 4. 5. 6

Identify need → Validate

need →Classify spend

( at some point up to PO)

→

Comply with local

documented purchasing

arrangements

Complete standard

requisition form

Submit requisition form to Budget Holder /

Nominee

• who can raise this requisition?• who can approve this requisition?• are mandatory controls for purchasing being adhered to? (segregation of duty )

• consider existing goods/services available• is the requirement appropriate to service & constraints• what is the purchase type: property,capital,other• what is the purchase category: routine, non-routine• what is the estimated total amount of expenditure?• select appropriate threshold & corresponding authorisation method• Aggregation ; >€25k must be notified to RMM group

Note.This chart is a representation of the

activities and steps involved - all transactions do not necessarily

follow each of these steps

Diagram : IDENTIFICATION AND NOTIFICATION OF NEED

2.18. In communicating the need for goods or services to the relevant Budget Holder, or

their nominee, the manager or staff member must:

Health Service Executive National Financial Regulations

Ver 1.3 Page 26 of 176

2.18.1. Fully comply with the formal documented purchasing arrangements N4 put in place by or on behalf of the Budget Holder.

2.18.2. Fully comply with any requirement of their own manager 2.18.3. Clearly communicate, in written form, unless otherwise permitted, the following:

Date of Request Specification of goods / services required Name/source of request Purpose for which goods / services required Cost Centre / Internal Order Material Code / GL Preferred delivery address Timescales within which required Likely cost if known & quantity /duration etc

2.18.4. The normal requirement is for requests for the purchase of goods or services to be submitted on a standard pre-formatted sequentially numbered requisition form.

2.18.5. Such standardised requisition forms are particularly important where a purchasing

location receives a high volume of requests from a number of remote locations.

2.18.6. Requisitions must be submitted using the financial information system where required by the relevant Budget Holder.

2.19. Adequately record the request so that it is readily available for future reference or inspection / audit.

( IV ) Confirmation of Availability of Funds and Approval to Spend

Next; ‘Sourcing of Supplier’ on page 28.

2.20. Depending on the specific circumstances of any particular purchasing transaction confirmation of availability of funds may be required:

2.20.1. Before a need is communicated to the manager or staff nominated to source

suppliers and issue purchase orders or contracts to same, or

2.20.2. At the same time and/or by the same manager with authority to issue requests to

suppliers to provide goods or services (i.e. the person who approves purchase orders or contracts)

N4 Budget Holders need to be pragmatic in drawing up the mandatory formal documented purchasing arrangements described at 1.above as regard (a) Value of goods and services and (b) Routine versus non-routine goods and services

Health Service Executive National Financial Regulations

Ver 1.3 Page 27 of 176

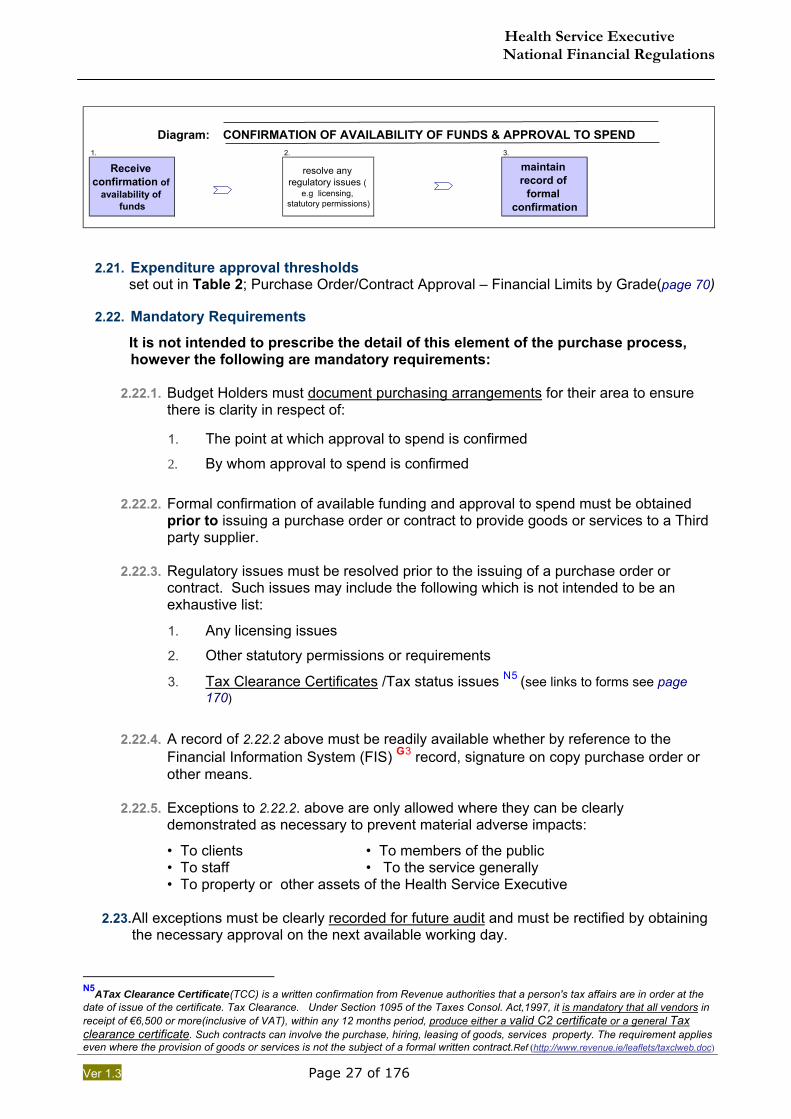

1. 2. 3.

Receive confirmation of

availability of funds

resolve any regulatory issues (

e.g licensing, statutory permissions)

maintain record of

formal confirmation

Diagram: CONFIRMATION OF AVAILABILITY OF FUNDS & APPROVAL TO SPEND

2.21. Expenditure approval thresholds

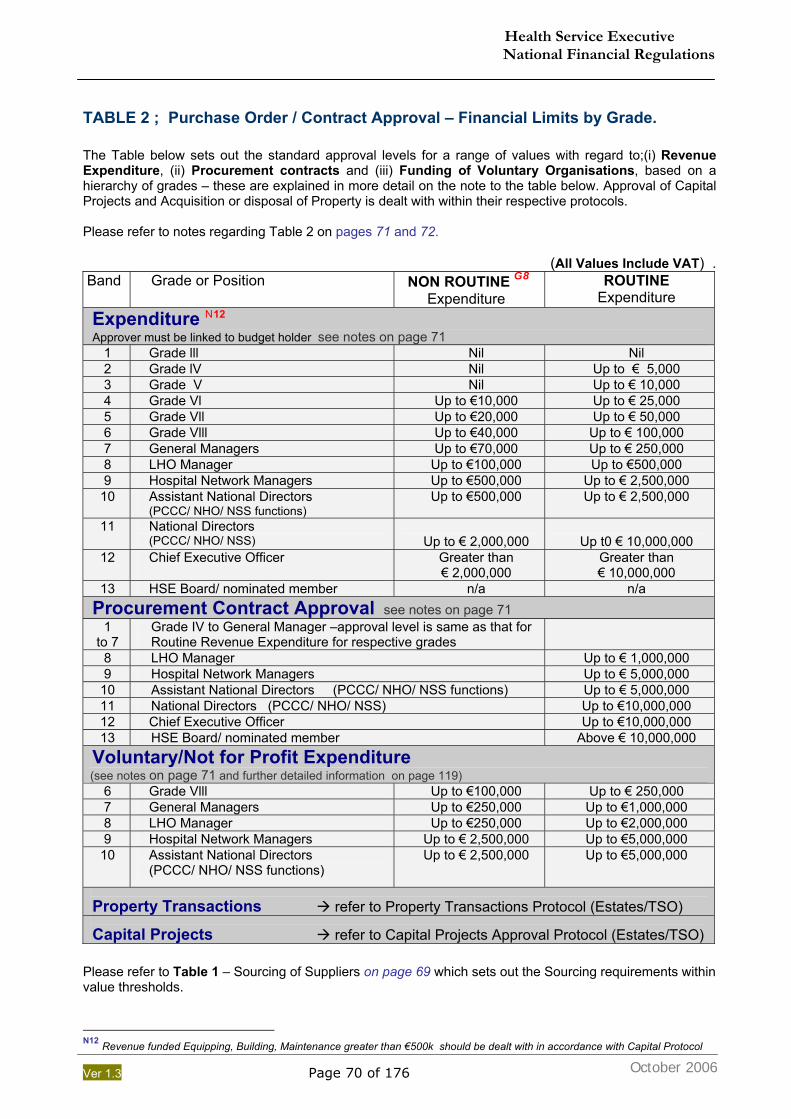

set out in Table 2; Purchase Order/Contract Approval – Financial Limits by Grade(page 70)

2.22. Mandatory Requirements

It is not intended to prescribe the detail of this element of the purchase process, however the following are mandatory requirements:

2.22.1. Budget Holders must document purchasing arrangements for their area to ensure there is clarity in respect of: 1. The point at which approval to spend is confirmed

2. By whom approval to spend is confirmed

2.22.2. Formal confirmation of available funding and approval to spend must be obtained prior to issuing a purchase order or contract to provide goods or services to a Third party supplier.

2.22.3. Regulatory issues must be resolved prior to the issuing of a purchase order or contract. Such issues may include the following which is not intended to be an exhaustive list:

1. Any licensing issues

2. Other statutory permissions or requirements

3. Tax Clearance Certificates /Tax status issues N5 (see links to forms see page 170)

2.22.4. A record of 2.22.2 above must be readily available whether by reference to the Financial Information System (FIS) G3 record, signature on copy purchase order or other means.

2.22.5. Exceptions to 2.22.2. above are only allowed where they can be clearly demonstrated as necessary to prevent material adverse impacts:

• To clients • To members of the public • To staff • To the service generally • To property or other assets of the Health Service Executive

2.23. All exceptions must be clearly recorded for future audit and must be rectified by obtaining

the necessary approval on the next available working day.

N5ATax Clearance Certificate(TCC) is a written confirmation from Revenue authorities that a person's tax affairs are in order at the date of issue of the certificate. Tax Clearance. Under Section 1095 of the Taxes Consol. Act,1997, it is mandatory that all vendors in receipt of €6,500 or more(inclusive of VAT), within any 12 months period, produce either a valid C2 certificate or a general Tax clearance certificate. Such contracts can involve the purchase, hiring, leasing of goods, services property. The requirement applies even where the provision of goods or services is not the subject of a formal written contract.Ref (http://www.revenue.ie/leaflets/taxclweb.doc)

Health Service Executive National Financial Regulations

Ver 1.3 Page 28 of 176

Additional Material; on page 76

( V ) Sourcing of Suppliers to Provide Goods or Services Next; ‘End of Purchasing Stage’ on page 34

2.24. Budget Holders responsibility in relation to Sourcing Budget holders and their nominees must;

2.24.1. Monitor their purchasing activity on an ongoing basis. They must identify opportunities for appropriate extension of centralised contracting. These opportunities should be pursued with Procurement.

2.24.2. Document their sourcing procedures as part of their formal local purchasing

arrangements and all such sourcing procedures must comply with the National Financial Regulations.

2.24.3. Have regard to the need to avoid ordering excess quantities of goods– it is important

to balance the requirement to ensure goods are available when needed against the issues associated with over ordering including:

1. Lack of appropriate storage

2. Excess goods may not last and have to be scrapped

2.25. These requirements should be addressed in the context of meeting the need for

procurement planning as set out on page 24 above. 1st required preference; Source from Stock or Existing Contract

2.26. It is a specific responsibility of each Budget Holder to ensure that:

to the greatest extent practicable and where consistent with achieving value for money

as many purchases of goods and services are from :

(i) “Stock (Stores)” - Goods held and issued from Stores/ storage location on page 78. (ii) Contracts - Acquired by ordering off a pre-existing and still valid contract, or

2.27. Requirement to Utilise Contracts that are in place and still valid.

2.27.1. “ It is incumbent ………… to establish whether an existing contract is already in

place and, if so, to utilise this contract” (Health Service Procurement Policy)

2.27.2. The terms of any given contract must make clear the extent to which the HSE commits to purchasing from the suppliers who have been awarded the contract.

Health Service Executive National Financial Regulations

Ver 1.3 Page 29 of 176

2.27.3. In the negotiation of any contract care must be taken to very clearly state the terms upon which the HSE agrees to any exclusive use of the supplier and their goods or services.

2.27.4. Particular consideration must be given to HSE locations or services that may have

low volume or low value requirements or may be geographically remote.

2.27.5. The following should be the over riding factor in Putting in Place contracts;

1. the achievement of value for money including the use of scarce staff resources (within procurement and service delivery)

2. At all times, one must fully comply with Public procurement requirements.

2.27.6. The non-use of a relevant existing valid contract, other than as clearly provided for the contract, must be approved by the specifically delegated Assistant National Director (delegated by National Management Team Member) or by the Head of Procurement. The Head of Procurement must be notified in all cases.

2.27.7. Where contracts have already been negotiated this simplifies the purchasing

process. It should enable the relevant staff member to focus on selecting the required goods from the contract list or catalogue.

2nd required preference; Invitation to 3rd Party Supplier to supply General

2.28. If goods or services cannot be sourced from stock or by calling off an existing contract then it will be necessary to source a supplier(s) directly.

2.29. It is a mandatory requirement of these regulations that a competitive process should be

used unless there are justifiably exceptional circumstances (see paragraph A2.1 on page 77 which sets out such circumstances).

2.30. Where HSE funds external organisations;

2.30.1. which are awarding works or related services contracts and

2.30.2. HSE is funding these contracts by 50% or more then

2.30.3. these organisations must comply with the sourcing requirements in these

regulations.

2.31. This provision applies to both commercial and voluntary / not for profit organisations

funded by HSE

2.32. Every manager sourcing a supplier has an obligation to ensure that they are in a position to accurately and clearly specify their requirements to potential suppliers, regardless of value threshold.

Health Service Executive National Financial Regulations

Ver 1.3 Page 30 of 176

2.33. Value Thresholds for Sourcing of Suppliers- General (Ref Table 1, on page 69).

2.33.1. The value of the likely purchase is the major factor in choosing the required method

for sourcing the supplier.

2.33.2. All values should be applied excluding VAT unless otherwise stated.

1. Goods – The threshold should be applied in respect of the need for the same or similar goods for the remainder of the current financial year.

2. Services (including construction related services) - The threshold should be applied in respect of the need for the same or similar services for the remainder of the current financial year.

3. Works – The threshold relates to the specific construction works.

Authorisation of Capital Projects, and the related Expenditure Approval and Sourcing of Supplies and Services must be undertaken and managed by Estates Function.

2.33.3. In applying the value thresholds for sourcing managers must take account

requirements for the same or similar goods or services in as wide an area of the overall HSE service as possible.

2.33.4. In practice, managers must, at a minimum, have regard to the likely needs of their

PCCC area ( HSE South, HSE Dublin North, HSE West, HSE Dublin) or Hospital Network in applying the value thresholds to decide on the appropriate method for sourcing potential suppliers. (refer to Aggregation of Tenders on page 47 below).

2.34. Prohibition on “Splitting of Purchases” to avoid value thresholds

“Splitting of Purchases” occurs where a staff member separates what is in effect one requirement into two or more separate lots for the purpose of applying a lower than appropriate value threshold.

This practice represents a very serious breach of the Financial Regulations and is prohibited. (Refer to paragraph 1.2.5 above)

2.35. Value Thresholds for Sourcing represent the minimum acceptable control levels.

A Budget Holder must, if they believe it appropriate, require the use of the more open methods of sourcing suppliers even where the expected value does not make this mandatory.

Such an approach would be required, for example, if they deem it necessary to:

Ensure proper controls are in place Achieve best value for money

Health Service Executive National Financial Regulations

Ver 1.3 Page 31 of 176

2.36. SOURCING OPTIONS THAT COMPLY WITH THIS FINANCIAL REGULATION

2.36.1. Table 1; A summary of main requirements with regard to Sourcing of Suppliers is set

out in Table 1 on page 69. This includes the Methods of Sourcing, Number and form of quotes/tenders and minimum time for receipt of quotes/tenders allowed by these regulations for different bands of spend.

2.36.2. The following options may be utilised in cases where either acquiring from stock or

from an existing contract are not possible:

1. Direct approach to one or more potential suppliers seeking quotes – see variations below but operates within €1 to €50,000 range, excluding VAT.

2. Public Invitation of Tenders (Non EU) – see variations below but operates between € 50,000 to € 211,000, excluding VAT for goods / services € 5,278,000 for works).

3. EU Public Tender – see variations below but operates for anything over the thresholds listed at 2 above.

2.37. If there is any uncertainty as to which value range the required goods / services fall into

then the next highest range should be assumed and the sourcing options required for that value range are to be utilised.

2.38. Budget Holders and their nominees are required to use the sourcing options required by

the higher value ranges where it is probable that this will yield better value for money. They must satisfy themselves that any additional expense and / or additional time involved can be justified.

2.39. Authorisation to seek quotes / tenders N6

2.39.1. Each Budget Holder or their nominee must set out the appropriate authorisation to

be obtained prior to seeking quotes or tenders. This must be covered in the formal documented purchasing arrangements that is required to put in place.

2.39.2. As a minimum the following must be complied with:

1. Grade VI or higher must approve in advance any proposal to seek tenders (above €50k) up to the EU threshold levels

2. Grade VIII or higher must approve in advance any proposal to seek tenders requiring EU tendering procedures.

2.39.3. The ‘General Requirements’ with regard to Tendering are set out on page 54 and include Tender Receipt, Custody and Opening, Tender Evaluation, Tender Award, Notification of Results and Documentation.

2.40. Please refer to section ‘Professional Input to Tendering’ on page 46 which details the requirements to obtain appropriate professional procurement input where the value of purchases exceeds €25,000.

2.41. Issue of Tender Forms / Documentation

A record must be kept of each request for tender documentation detailing when received, when responded to and documentation issue.

N6 Quotations/Quotes (for the purpose of these regulations) refers to values up to €50,000, the term ‘Tender’ or ‘bid’ refers to a more formal submission by a supplier to supply goods or services greater than €50,000.

Health Service Executive National Financial Regulations

Ver 1.3 Page 32 of 176

2.42. Minimum time to be allowed for receipt of quote/tender.

(Refer to Table 1 on page 69) 2.42.1. The times specified are the minimum allowed. Managers are required to allow

additional time where doing so could be considered reasonably necessary.

2.42.2. Additional time should be allowed if it is considered necessary to secure the minimum number of quotes / tenders or to achieve best value for money.

2.42.3. Real time constraints that may exist around meeting service needs must be taken account of when considering allowing additional time.

2.43. Receipt of less than the required number of quotes

(Refer to Table 1 on page 69) Above the €50,000 threshold the receipt of less than the minimum required number of quotes means that there is a requirement for the next level up of authorisation to approve the resulting purchase order or contract.

For example - ordinarily these regulations provide that a Grade V can approve purchase orders up to €10,000 for routine expenditure but in the event that only 2 quotes are obtained for goods costing €9,000 then the approval of a Grade VI is required.

2.44. The relevant manager is required to consider whether the objective of achieving best

value for money would be better served by restarting the quotation process in an effort to achieve the required minimum number of quotes.

2.45. All potential suppliers must have equal access to information

2.45.1. All potential suppliers must be informed in a consistent way as to any criteria that

may be used to evaluate their quotes or tenders. 2.45.2. HSE staff must not give any real or perceived advantage to any potential supplier.

2.45.3. It is essential that any information or clarification provided to one supplier is

provided in the same format and at the same time to all potential suppliers regardless of whether they have requested it or not.

2.50. Evaluation of Quotes and Tenders

The general principles regarding evaluation of tenders set out on page 54 and 98 must be applied to the quotation process. Evaluation of quotes must involve the use of objective and fair criteria that are consistently applied.

2.50.1. The Most Economically Advantageous Tender (MEAT)G4 or Lowest Price

achieved must be accepted. (see paragraph 3.30 below).

2.50.2. As the value threshold for quotes is lower than for tenders (quotes up to €50k, Tenders thereafter) it is expected that the quotation process will be less formal than the tender process and will require less documentation.

2.50.3. A clear record should be kept of the evaluation of all quotes and tenders - in

particular where the lowest priced quote is not accepted the reasons for this must be recorded for future audit.

Health Service Executive National Financial Regulations

Ver 1.3 Page 33 of 176

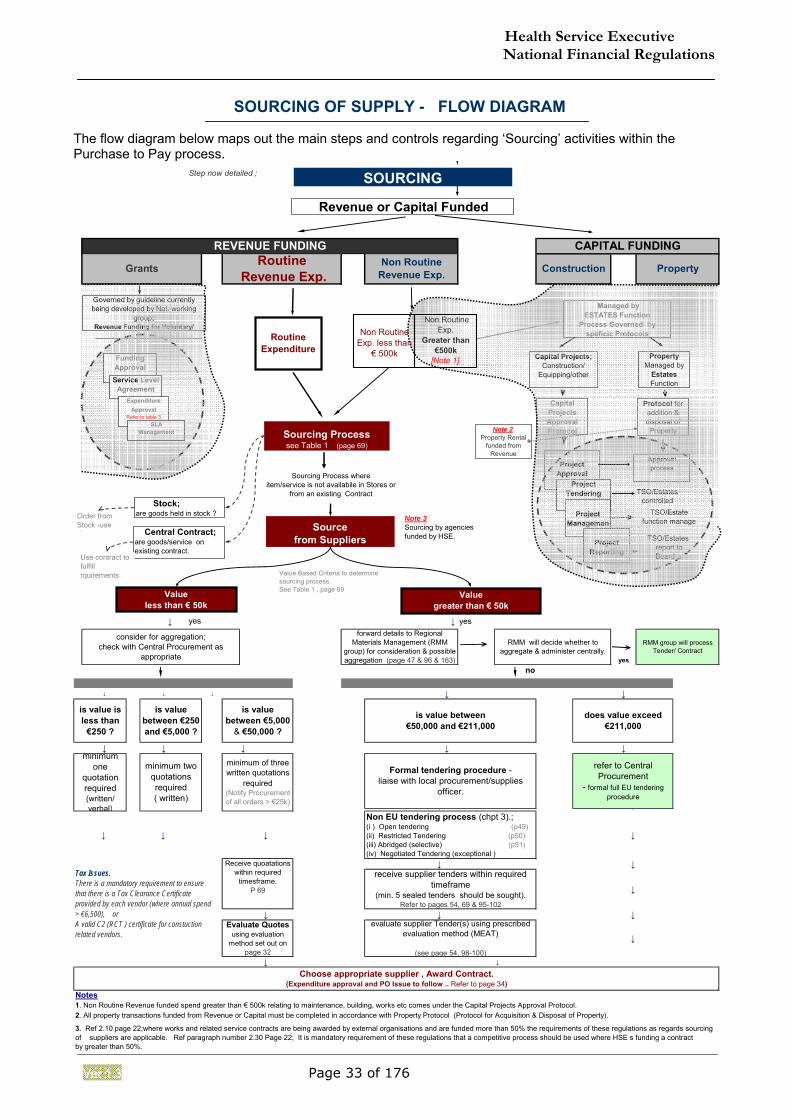

SOURCING OF SUPPLY - FLOW DIAGRAM The flow diagram below maps out the main steps and controls regarding ‘Sourcing’ activities within the Purchase to Pay process. Step now detailed ;

↓ ↓ yes

yesno

↓ ↓ ↓ ↓ ↓

↓ ↓ ↓ ↓ ↓

↓ ↓

↓ ↓ ↓ ↓

↓ ↓

↓

↓ ↓ ↓

↓

↓ ↓

Notes

RMM will decide whether to aggregate & administer centrally.

does value exceed €211,000

refer to Central Procurement

- formal full EU tendering procedure

is value between €50,000 and €211,000

forward details to Regional Materials Management (RMM

group) for consideration & possible aggregation (page 47 & 96 & 163)

RMM group will process Tender/ Contract

Formal tendering procedure - liaise with local procurement/supplies

officer.

1. Non Routine Revenue funded spend greater than € 500k relating to maintenance, building, works etc comes under the Capital Projects Approval Protocol.2. All property transactions funded from Revenue or Capital must be completed in accordance with Property Protocol (Protocol for Acquisition & Disposal of Property).

3. Ref 2.10 page 22;where works and related service contracts are being awarded by external organisations and are funded more than 50% the requirements of these regulations as regards sourcing of suppliers are applicable. Ref paragraph number 2.30 Page 22; It is mandatory requirement of these regulations that a competitive process should be used where HSE s funding a contract by greater than 50%.

Non EU tendering process (chpt 3).;(i ) Open tendering (p49)(ii) Restricted Tendering (p50)(iii) Abridged (selective) (p51)(iv) Negotiated Tendering (exceptional )

receive supplier tenders within required timeframe

(min. 5 sealed tenders should be sought).Refer to pages 54, 69 & 95-102

Choose appropriate supplier , Award Contract. (Expenditure approval and PO Issue to follow .. Refer to page 34)

CAPITAL FUNDINGREVENUE FUNDING

PropertyGrants Non Routine Revenue Exp. ConstructionRoutine

Revenue Exp.

evaluate supplier Tender(s) using prescribed evaluation method (MEAT)

(see page 54, 98-100)

Receive quoatations within required

timesframe.P 69

Evaluate Quotes using evaluation

method set out on page 32

yes

is value is less than

€250 ?

is value between €5,000

& €50,000 ?

is value between €250 and €5,000 ?

minimum of three written quotations

required(Notify Procurement of all orders > €25k)

minimum two quotations required( written)

minimum one

quotation required(written/verbal)

consider for aggregation;check with Central Procurement as

appropriate

Revenue or Capital Funded

Capital ProjectsApproval Protocol

Project Approval

Project Tendering

Property Managed by

Estates Function

Capital Projects;Construction/

Equipping/other

Protocol for addition & disposal of Property

Approval process

TSO/Estates controlled

TSO/Estates report to Board .

Sourcing Processsee Table 1 (page 69)

Sourcing Process whereitem/service is not availabile in Stores or

from an existing Contract Stock;are goods held in stock ?

Central Contract;are goods/service on existing contract.

Source from Suppliers

Value greater than € 50k

Value Based Criteria to determine sourcing process.See Table 1 , page 69

Project Managemen

t

TSO/Estate function manage

Project Reporting

Value less than € 50k

Governed by guideline currently being developed by Nat. working

group; Revenue Funding for Voluntary/

Funding ApprovalService Level

AgreementExpenditure

ApprovalRefer to table 3

SLA Management

Managed by ESTATES Function

Process Governed by speficic Protocols

SOURCING

Order from Stock -use stores

Use contract to fulfill rquirements

Non Routine Exp.

Greater than €500k

[Note 1]

Note 2Property Rental

funded from Revenue

Non Routine Exp. less than

€ 500k

Routine Expenditure

Note 3Sourcing by agencies funded by HSE.

Tax Issues.There is a mandatory requirement to ensure that there is a Tax Clearance Certificate provided by each vendor (where annual spend > €6,500), orA valid C2 (RCT ) certificate for constuction related vendors.

Health Service Executive National Financial Regulations

Ver 1.3 Page 34 of 176

More Information see Appendix ; on page 82

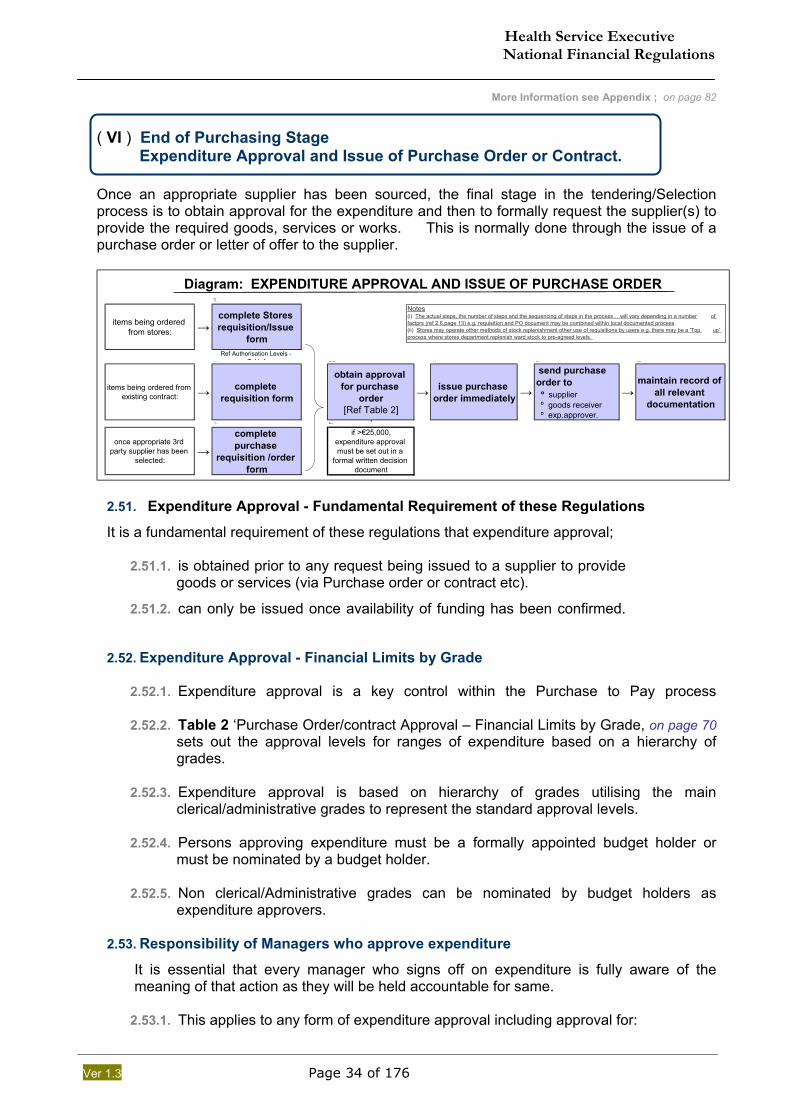

( VI ) End of Purchasing Stage Expenditure Approval and Issue of Purchase Order or Contract. Once an appropriate supplier has been sourced, the final stage in the tendering/Selection process is to obtain approval for the expenditure and then to formally request the supplier(s) to provide the required goods, services or works. This is normally done through the issue of a purchase order or letter of offer to the supplier.

1.

items being ordered from stores: →

complete Stores requisition/Issue

formRef Authorisation Levels -

Table11. 60 4. 5. 6.

items being ordered from existing contract: → complete

requisition form

obtain approval for purchase

order[Ref Table 2]

→ issue purchase order immediately →

send purchase order to º supplier º goods receiver º exp.approver.

→maintain record of

all relevant documentation

↓1. 2.

once appropriate 3rd party supplier has been

selected:→

complete purchase

requisition /order form

if >€25,000,expenditure approval must be set out in a

formal written decision document

Diagram: EXPENDITURE APPROVAL AND ISSUE OF PURCHASE ORDERNotes(i) The actual steps, the number of steps and the sequencing of steps in the process….will vary depending in a number of factprs (ref 2.6,page 13) e.g. requisition and PO document may be combined within local documented process(ii) Stores may operate other methods of stock replenishment other use of requisitions by users e.g. there may be a 'Top up' process where stores department replenish ward stock to pre-agreed levels.

2.51. Expenditure Approval - Fundamental Requirement of these Regulations

It is a fundamental requirement of these regulations that expenditure approval;

2.51.1. is obtained prior to any request being issued to a supplier to provide goods or services (via Purchase order or contract etc).

2.51.2. can only be issued once availability of funding has been confirmed.

2.52. Expenditure Approval - Financial Limits by Grade

2.52.1. Expenditure approval is a key control within the Purchase to Pay process

2.52.2. Table 2 ‘Purchase Order/contract Approval – Financial Limits by Grade, on page 70 sets out the approval levels for ranges of expenditure based on a hierarchy of grades.

2.52.3. Expenditure approval is based on hierarchy of grades utilising the main

clerical/administrative grades to represent the standard approval levels. 2.52.4. Persons approving expenditure must be a formally appointed budget holder or

must be nominated by a budget holder. 2.52.5. Non clerical/Administrative grades can be nominated by budget holders as

expenditure approvers. 2.53. Responsibility of Managers who approve expenditure

It is essential that every manager who signs off on expenditure is fully aware of the meaning of that action as they will be held accountable for same.

2.53.1. This applies to any form of expenditure approval including approval for:

Health Service Executive National Financial Regulations

Ver 1.3 Page 35 of 176

The issue of a purchase order. The issue of a contract. Expenditure by any other means.

2.53.2. In effect the manager is confirming that he has taken all reasonable steps to

assure him/herself that:

1. The expenditure is appropriate to meet the need.

2. Proper procurement has taken place.

3. The expenditure is within the available budget.

4. The Financial Regulations have been complied with.

5. It is in order to request supplier to provide goods/services.

2.53.3. In assessing whether sufficient budget is available to cover any proposed purchase the manager must take account of all expenditure to date including commitments and known additional expenditure to the end of the financial year.

2.54. It is a mandatory requirement that requests to suppliers are in writing in the form of:

System Purchase Orders Manual Purchase Orders Contracts Other written format approved by the relevant Assistant National Director

of Finance

2.55. Purchase orders must actually be sent to suppliers once issued.