Embed Size (px)

DESCRIPTION

Foreign Exchange Markets. Dr Bryan Mills. Based on http://faculty.washington.edu/karpoff/FIN%20509/FIN509_session7.ppt. Outline of these slides. The foreign exchange (FX) market Basic questions and definitions Four theories Purchasing Power Parity Interest Rate Parity - PowerPoint PPT Presentation

Citation preview

Foreign Exchange Markets

Dr Bryan Mills

Based on http://faculty.washington.edu/karpoff/FIN%20509/FIN509_session7.ppt

Outline of these slides

• The foreign exchange (FX) market

• Basic questions and definitions

• Four theories

– Purchasing Power Parity

– Interest Rate Parity

– Fisher condition for capital market equilibrium

– Expectations theory of forward rates

2

1. The Foreign Exchange Market

3

Currency Last Day High Day Low % Change Bid Ask

Euro/US $ 1.3489 1.3489 1.3489 +0.01% 1.3489 1.3494

UK £/US $ 1.5338 1.5339 1.5338 +0.01% 1.5338 1.5342

US $/¥en 92.450 92.460 92.420 +0.06% 92.450 92.5

US $/SFranc 1.0625 1.0632 1.0628 -0.03% 1.0625 1.0631

US $/Can $ 1.0144 1.0152 1.0146 +0.02% 1.0144 1.0149

Aust $/US $ 0.92400 0.92410 0.92370 +0.03% 0.92400 0.92440

Reuters 19/4/2010 Sell buy

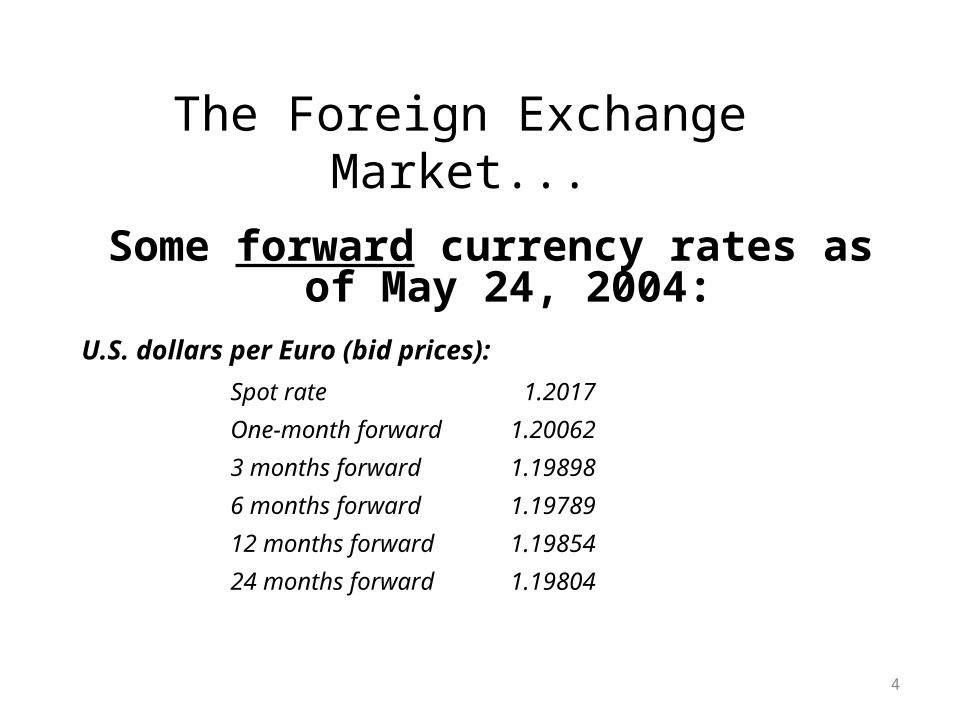

The Foreign Exchange Market...

Some forward currency rates as of May 24, 2004:

U.S. dollars per Euro (bid prices):

Spot rate 1.2017

One-month forward 1.20062

3 months forward 1.19898

6 months forward 1.19789

12 months forward 1.19854

24 months forward 1.19804

4

2. Some basic questions• Why aren’t FX rates all equal to one?

• Why do FX rates change over time?

• Why don’t all FX rates change in the same direction?

• What drives forward rates – the rates at which you can trade currencies at some future date?

5

Definitions

• r$ : dollar rate of interest (r¥, rHK$,…)

• i$ : expected dollar inflation rate

• f€/$ : forward rate of exchange

• s€/$ : spot rate of exchange

– “Indirect quote”: s€/$ = 0.83215 1 $ buys 0.83215 €– “Direct quote”: s$/€ = 1.2017 1 € buys $1.2017

6

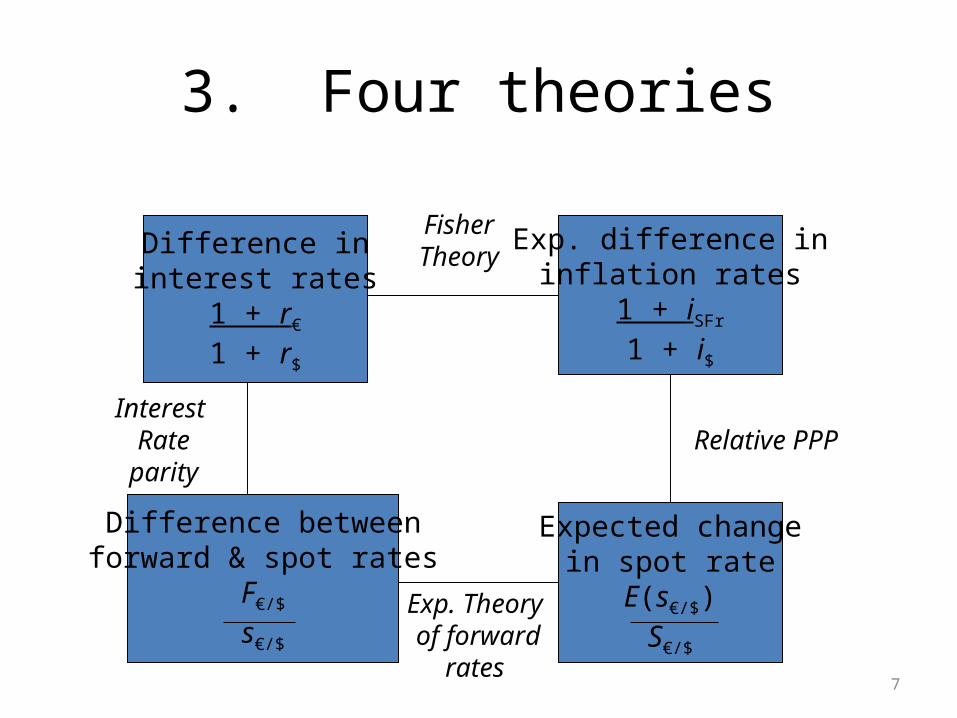

3. Four theories

.

7

Difference ininterest rates

1 + r€

1 + r$

Exp. difference ininflation rates

1 + iSFr

1 + i$

Difference betweenforward & spot rates

F€/$

s€/$

Expected changein spot rate

E(s€/$)S€/$

FisherTheory

Relative PPPInterest

Rateparity

Exp. Theory of forward

rates

Theory #1: Purchasing power parity

8

Versions ofPURCHASING

POWERPARITY

Versions ofPURCHASING

POWERPARITY

Law of One Price

Absolute PPP

Relative PPP

The Law of One Price

• A commodity will have the same price in terms of common currency in every country– In the absence of frictions (e.g. shipping costs,

tariffs,..)

– ExamplePrice of wheat in France (per bushel): P€

Price of wheat in U.S. (per bushel): P$

S€/$ = spot exchange rate9

P€ = s€/$ P$

The Law of One Price, continued

• Example: Price of wheat in France per bushel (p€) = 3.45 €

Price of wheat in U.S. per bushel (p$) = $4.15

S€/$ = 0.83215 (s$/€ = 1.2017)

Dollar equivalent priceof wheat in France = s$/€ x p€

= 1.2017 $/€ x 3.45 € = $4.15

When law of one price does not hold, supply and demand forces help restore the equality

10

Absolute PPP• Extension of law of one price to a basket of goods

• Absolute PPP examines price levels– Apply the law of one price to a basket of goods with

price P€ and PUS (use upper-case P for the price of the basket):

where P€ = i (wFR,i p€,i )PUS = i (wUS,i pUS,i )

11

S€/$ = P€ / PUS

Absolute PPP

• If the price of the basket in the U.S. rises relative to the price in Euros, the U.S. dollar depreciates:

May 21 : s€/$ = P€ / PUS

= 1235.75 € / $1482.07 = 0.8338 €/$

May 24: s€/$ = 1235.75 € / $1485.01 = 0.83215 €/$

12

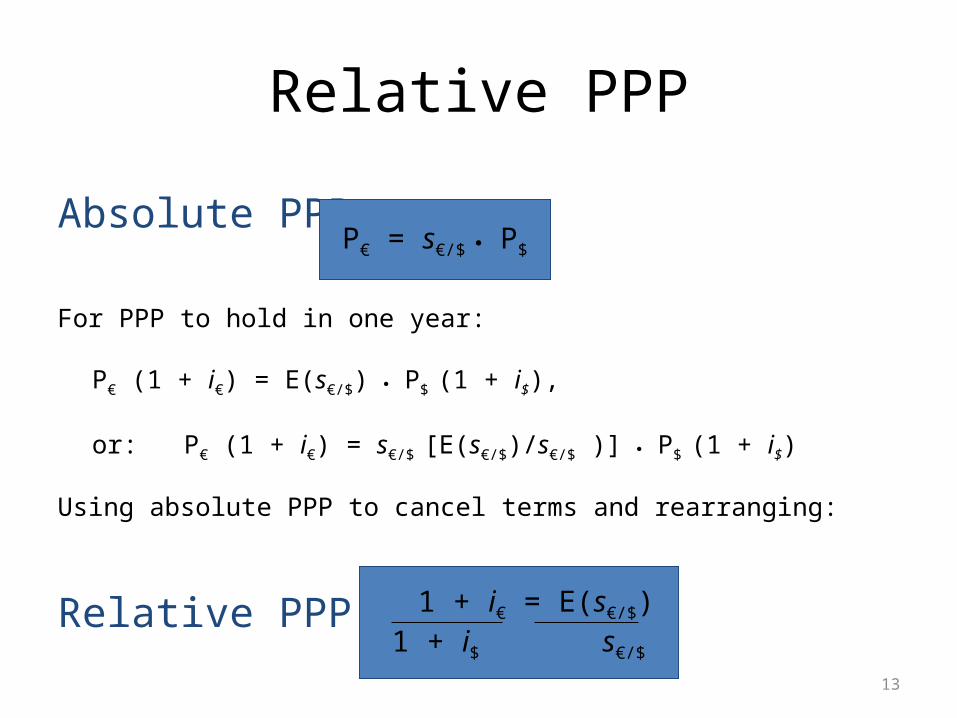

Relative PPP

Absolute PPP:

For PPP to hold in one year:

P€ (1 + i€) = E(s€/$) P$ (1 + i$),

or: P€ (1 + i€) = s€/$ [E(s€/$)/s€/$ )] P$ (1 + i$)

Using absolute PPP to cancel terms and rearranging:

Relative PPP:13

P€ = s€/$ P$

1 + i€ = E(s€/$)1 + i$ s€/$

Relative PPP

• Main idea – The difference between (expected) inflation rates equals the (expected) rate of change in exchange rates:

14

1 + i€ = E(s€/$)1 + i$ s€/$

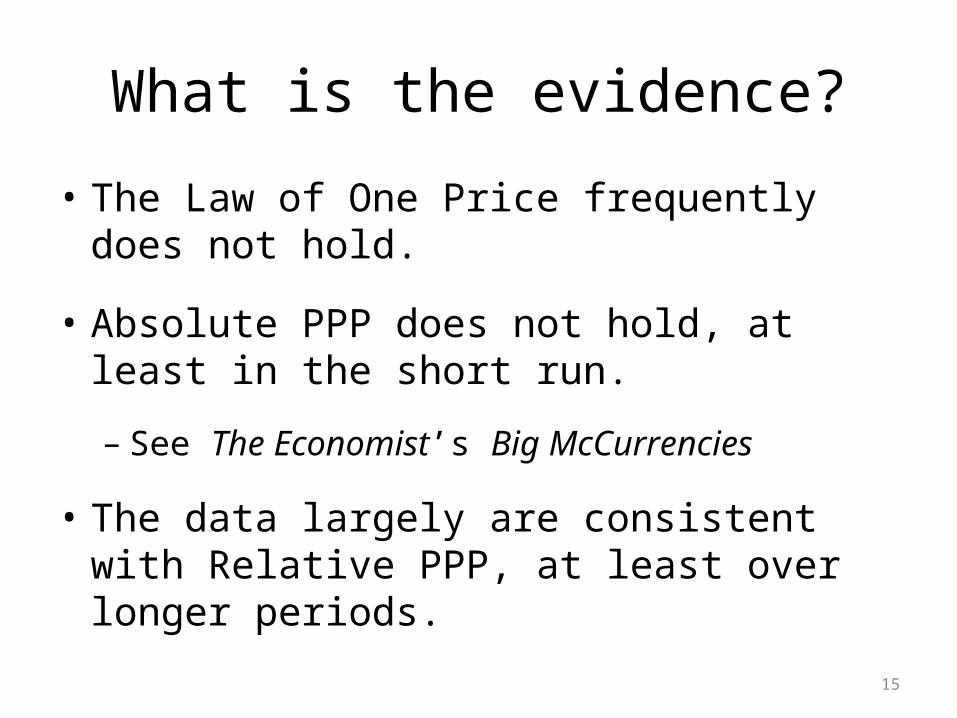

What is the evidence?

• The Law of One Price frequently does not hold.

• Absolute PPP does not hold, at least in the short run.

– See The Economist’s Big McCurrencies

• The data largely are consistent with Relative PPP, at least over longer periods.

15

Deviations from PPP

16

Why doesPPPnot

hold?

Why doesPPPnot

hold?

Simplistic model

Imperfect Markets

Statistical difficulties

Deviations from PPP

17

Simplistic model

Imperfect Markets

Statistical difficulties

Transportation costsTariffs and taxesConsumption patterns differNon-traded goods & services

Sticky pricesMarkets don’t work well

Construction of price indexes- Different goods- Goods of different qualities

Summary of theory #1:

.

18

Exp. difference ininflation rates

1 + i€

1 + i$

Expected changein spot rate

E(s€/$)S€/$

Relative PPP

Theory #2: Interest rate parity• Main idea: There is no fundamental advantage

to borrowing or lending in one currency over another

• This establishes a relation between interest rates, spot exchange rates, and forward exchange rates

– Forward market: Transaction occurs at some point in future– BUY: Agree to purchase the underlying currency at a predetermined

exchange rate at a specific time in the future– SELL: Agree to deliver the underlying currency at a predetermined

exchange rate at a specific time in the future

19

Example of a forward market transaction

• Suppose you will need 100,000€ in one year

• Through a forward contract, you can commit to lock in the exchange rate

• f$/€ : forward rate of exchangeCurrently, f$/€ = 1.19854 1 € buys $1.19854

1 $ buys 0.83435 €

• At this forward rate, you need to provide $119,854 in 12 months.

20

Interest Rate ParitySTART (today) END (in one year)

21

$117,228 $117,228 1.0224 = $119,854

r$=2.24%

$117,228 0.83215 = 97,551€

s€/$=0.83215

r€=2.51%

97,551€ 1.0251 = 100,000€

f€/$=0.83435One year

(Invest in $)

(Invest in €)

Interest rate parity

• Main idea: Either strategy gets you the 100,000€ when you need it.

• This implies that the difference in interest rates must reflect the difference between forward and spot exchange rates

Interest Rate Parity:

22

1 + r€ = f€/$

1 + r$ s€/$

Interest rate parity example

• Suppose the following were true:

– Does interest rate parity hold?– Which way will funds flow?– How will this affect exchange rates?

23

U.S Dollar Euro

12 month interest rate

2.24% 2.70%

Spot rate 1.2017 € / $

Forward rate 1.19854 € / $

Evidence on interest rate parity• Generally, it holds

• Why would interest rate parity hold better than PPP?

– Lower transactions costs in moving currencies than real goods

– Financial markets are more efficient that real goods markets

24

Summary of theories #1 and #2:

.

25

Difference ininterest rates

1 + r€

1 + r$

Exp. difference ininflation rates

1 + i€

1 + i$

Difference betweenforward & spot rates

f€r/$

s€/$

Expected changein spot rate

E(s€/$)s€/$

Relative PPPInterest

Rateparity

Theory #3: The Fisher condition• Main idea: Market forces tend to allocate

resources to their most productive uses

• So all countries should have equal real rates of interest

• Relation between real and nominal interest rates:

(1 + rNominal) = (1 + rReal)(1 + i )

(1 + rReal) = (1 + rNominal) / (1 + i )

26

Example of capital market equilibrium

• Fisher condition in U.S. and France:(1 + r$(Real)) = (1 + r$) / (1 + i$)(1 + r€(Real)) = (1 + r€) / (1 + i€)

• If real rates are equal, then the Fisher condition implies:

• The difference in interest rates is equal to the expected difference in inflation rates

27

1 + r€ = 1 + i€1 + r$ 1 + i$

Summary of theories 1-3:

.

28

Difference ininterest rates

1 + r€

1 + r$

Exp. difference ininflation rates

1 + i€

1 + i$

Difference betweenforward & spot rates

f€/$

s€/$

Expected changein spot rate

E(s€/$)s€/$

FisherTheory

Relative PPPInterest

Rateparity

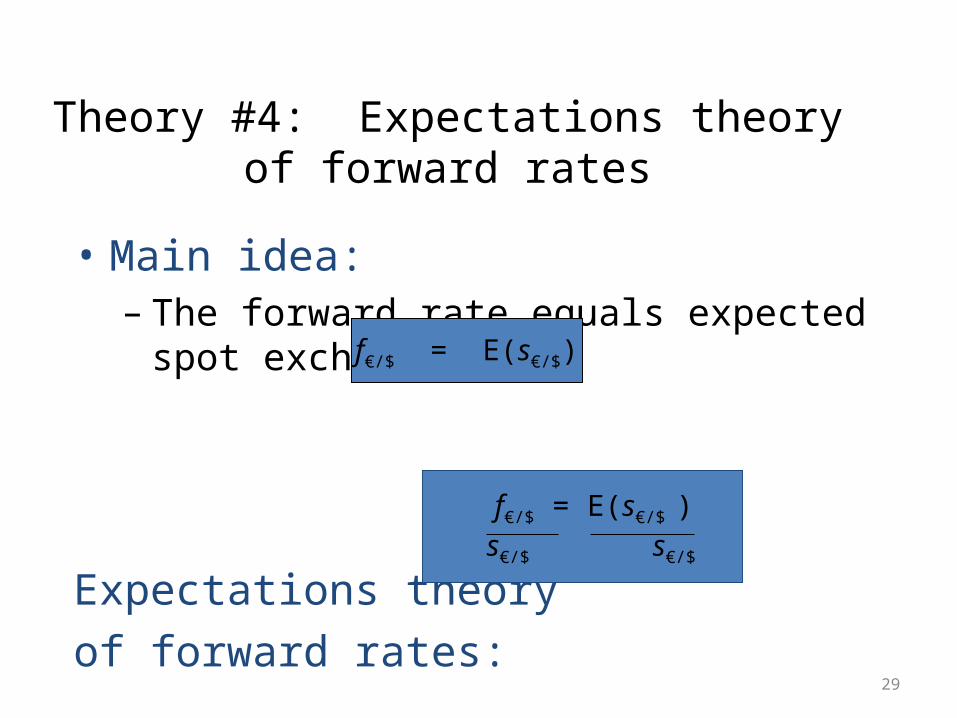

Theory #4: Expectations theory of forward rates

• Main idea:– The forward rate equals expected spot exchange

rate

Expectations theory of forward rates:

29

f€/$ = E(s€/$)

f€/$ = E(s€/$ ) s€/$ s€/$

Expectations theory of forward rates• With risk, the forward rate may not equal the spot rate

• If Group 1 predominates, then E(s€/$) < f€/$ • If Group 2 predominates, then E(s€/$) > f€/$ 30

Group 1: Receive € in six months, want $

• Wait six months and convert € to $

or• Sell € forward

Group 1: Receive € in six months, want $

• Wait six months and convert € to $

or• Sell € forward

Group 2: Contracted to pay out € in six months

• Wait six months and convert $ to €

or• Buy € forward

Group 2: Contracted to pay out € in six months

• Wait six months and convert $ to €

or• Buy € forward

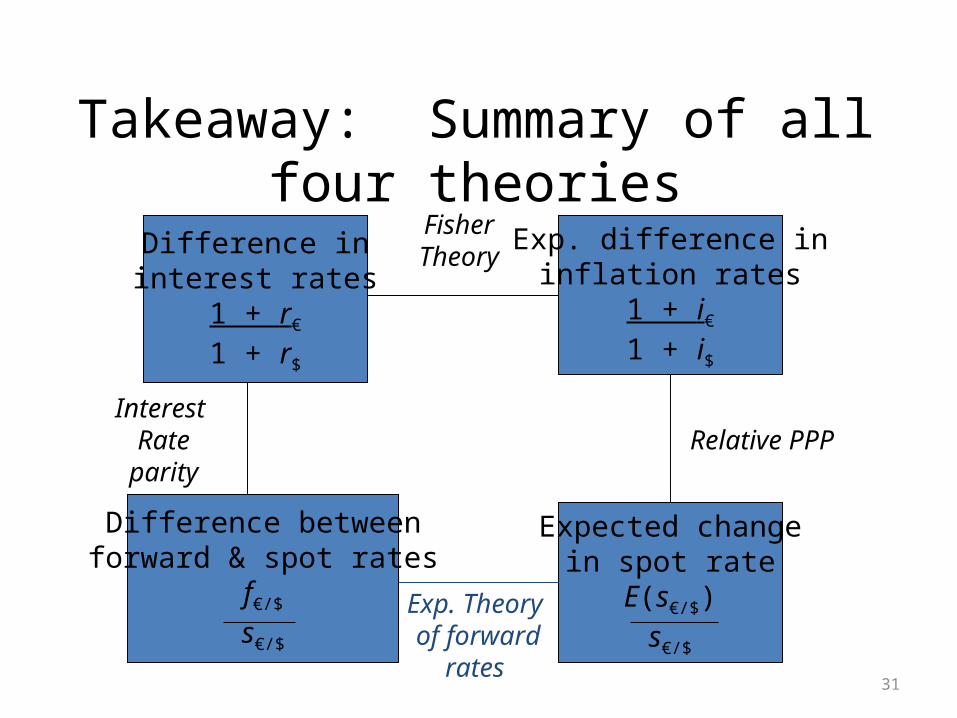

Takeaway: Summary of all four theories.

31

Difference ininterest rates

1 + r€

1 + r$

Exp. difference ininflation rates

1 + i€

1 + i$

Difference betweenforward & spot rates

f€/$

s€/$

Expected changein spot rate

E(s€/$)s€/$

FisherTheory

Relative PPPInterest

Rateparity

Exp. Theory of forward

rates