Embed Size (px)

Citation preview

356167_WACF_2004-2005.qxd 9/15/04 11:54 AM Page 111

The Boeing Company issues the biennial World Air Cargo Forecast (WACF) to provide a comprehensive, up-to-date overview

of the air cargo industry. The forecast summarizes the world’s major air trade markets, identifies major trends, and presents

forecasts for the future performance and development of markets, as well as for the world freighter airplane fleet.

A strongly resurgent world air cargo industry characterizes the market for the 2004/2005 edition. Traffic has grown nearly

11% during the first half of 2004 relative to 2003, when concern over the Iraq War and the severe acute respiratory

syndrome (SARS) crisis in Asia curbed industry growth. If the current momentum of world air cargo traffic growth is

maintained through the end of 2004, it will mark the first double-digit percentage growth year for the industry since 1997.

In this edition of the WACF, new data sources were used to help model air cargo flows into and out of Europe, which has

improved our understanding of the continent’s air trade patterns. It is hoped that this new data will improve the usefulness

of WACF for all readers.

Data represented as historical in this document were compiled from many sources, including, but not limited to,

Air Cargo Management Group, the Air Transport Association (ATA), the Association of Asia-Pacific Airlines (AAPA),

the Association of European Airlines (AEA), Boeing Foreign Trade Database (TRADE), Global Insight, the International

Air Transport Association (IATA), International Civil Aviation Organization (ICAO), and U.S. Department of Transportation

(DOT) Form 41. Historical information is updated each year as individual sources revise their respective databases.

This document would not be possible without the efforts of several contributors. The Boeing World Air Cargo Forecast

2004/2005 production team included the Creative Services Group design, production, and web teams; the Writing

and Editing Services team; and our colleagues in marketing, John Riley and Lee Hibbets.

Special thanks are extended to Mr. Thomas Klein (www.contrails.de) and Mr. Tom Hoang for their photographic contributions

on the cover of this year’s edition of WACF. Mr. Klein contributed the Cargolux 747-400F photograph that adorns the cover,

and Mr. Hoang is the photographer of the Cathay Pacific 747-400F.

The next update to the WACF will appear fourth quarter 2006. The authors welcome any questions or comments readers

may have. All queries and suggestions should be directed to

The Boeing World Air Cargo Forecast Team

Boeing Commercial Airplanes

P. O. Box 3707, MC 21-33

Seattle, WA 98124-2207 USA

Fax: (206) 766-1030

Web:http://www.boeing.com/commercial/cargo/index.html

World Air Cargo Forecast 2004/200500

Foreword

Tom Crabtree Tom Hoang Jim Edgar

206-766-2576 206-766-2568 206-766-2643

thomas.crabtree thomas.l.hoang james.r.edgar

@boeing.com @boeing.com @boeing.com

Table of Contentse 00

Table of Contents

Executive Summary and Significant Industry Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

World Overview and Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

Latin America and North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

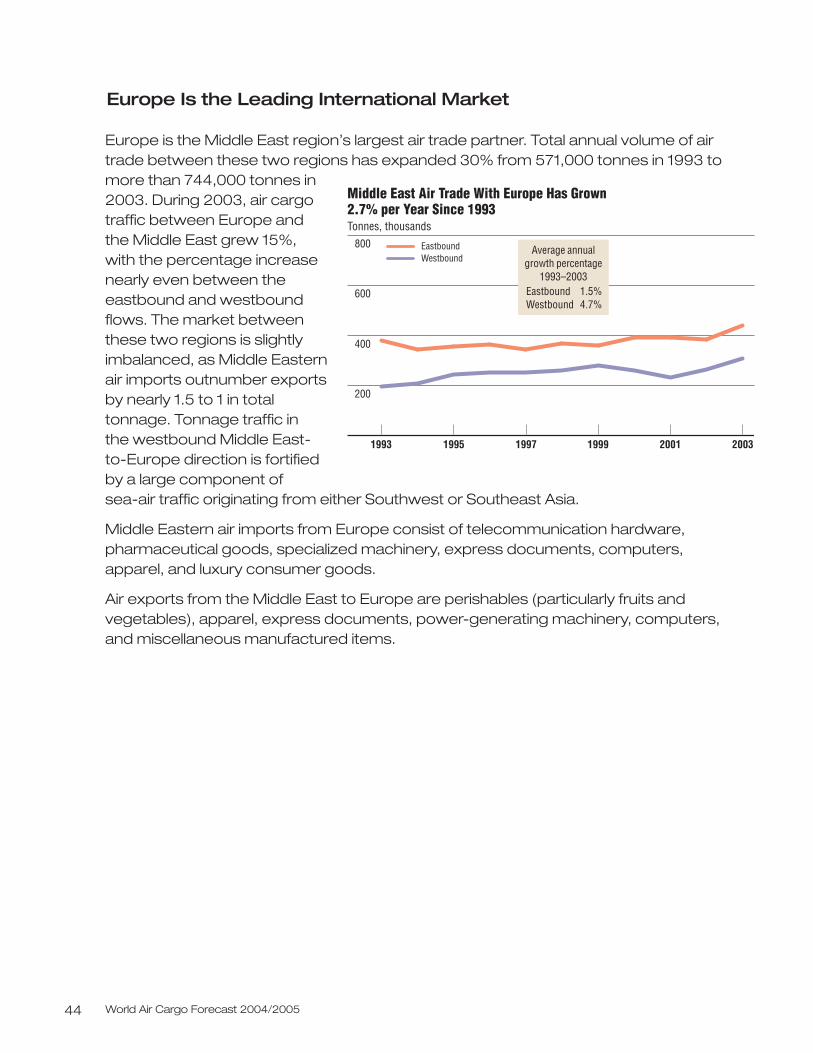

Europe and North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

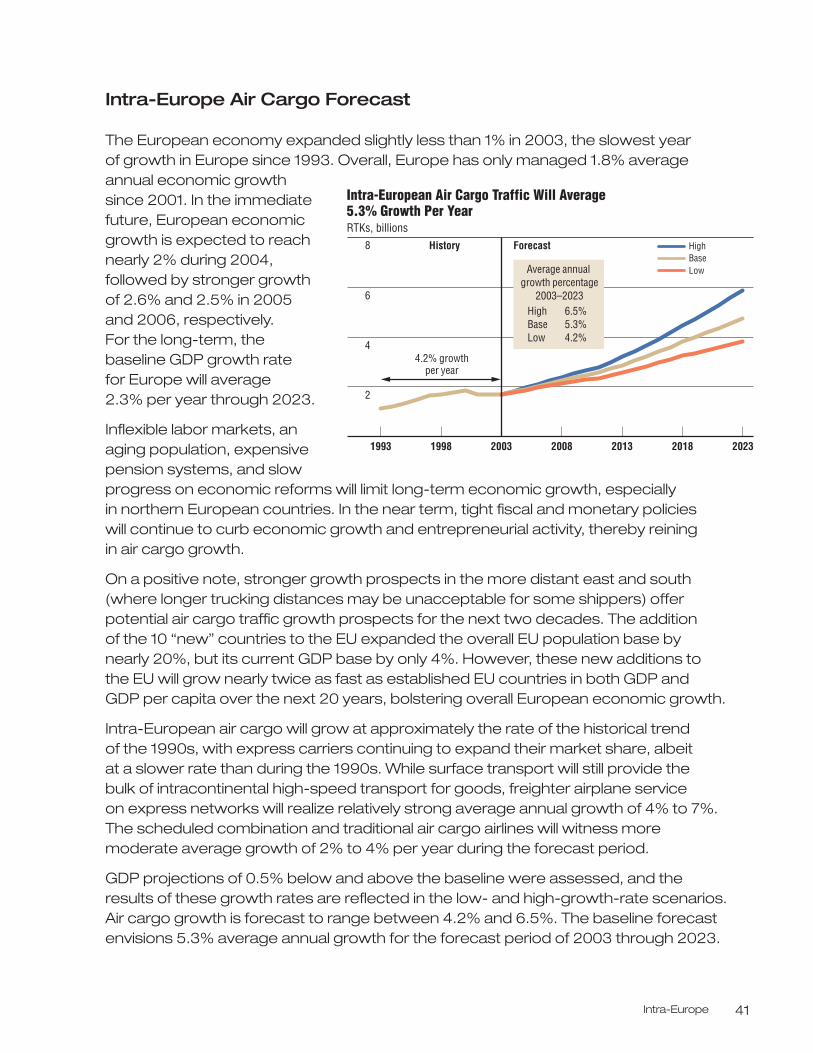

Intra-Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37

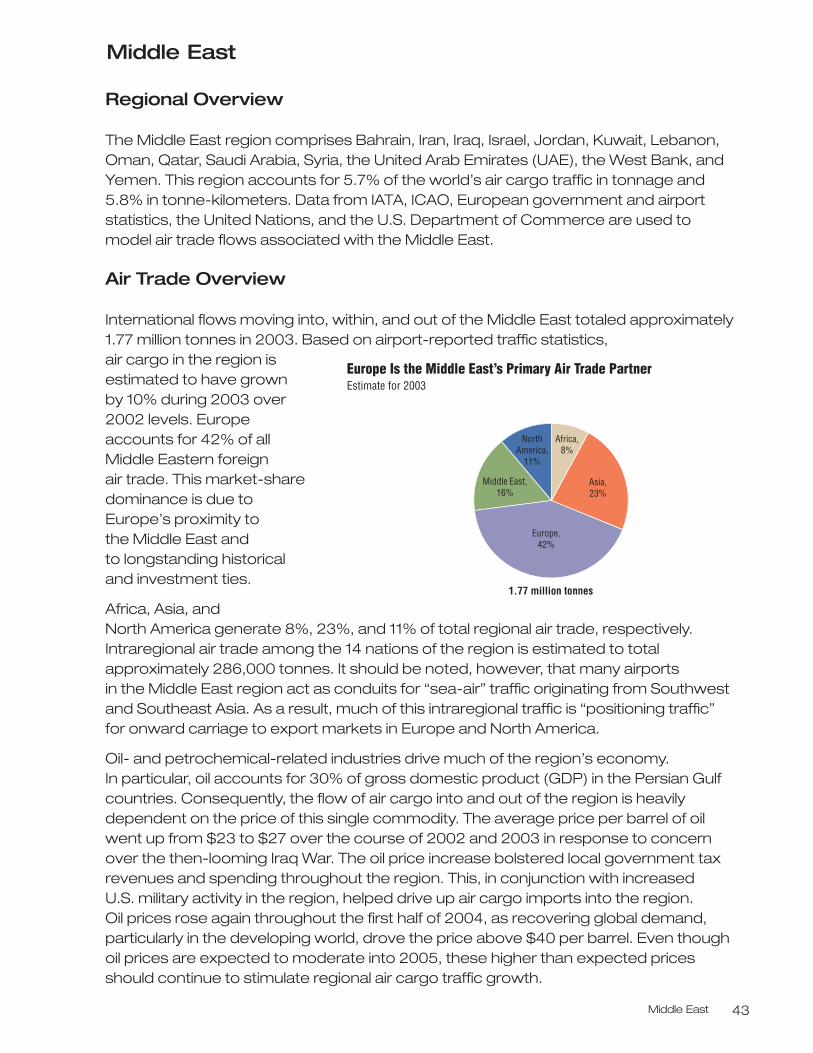

Middle East . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

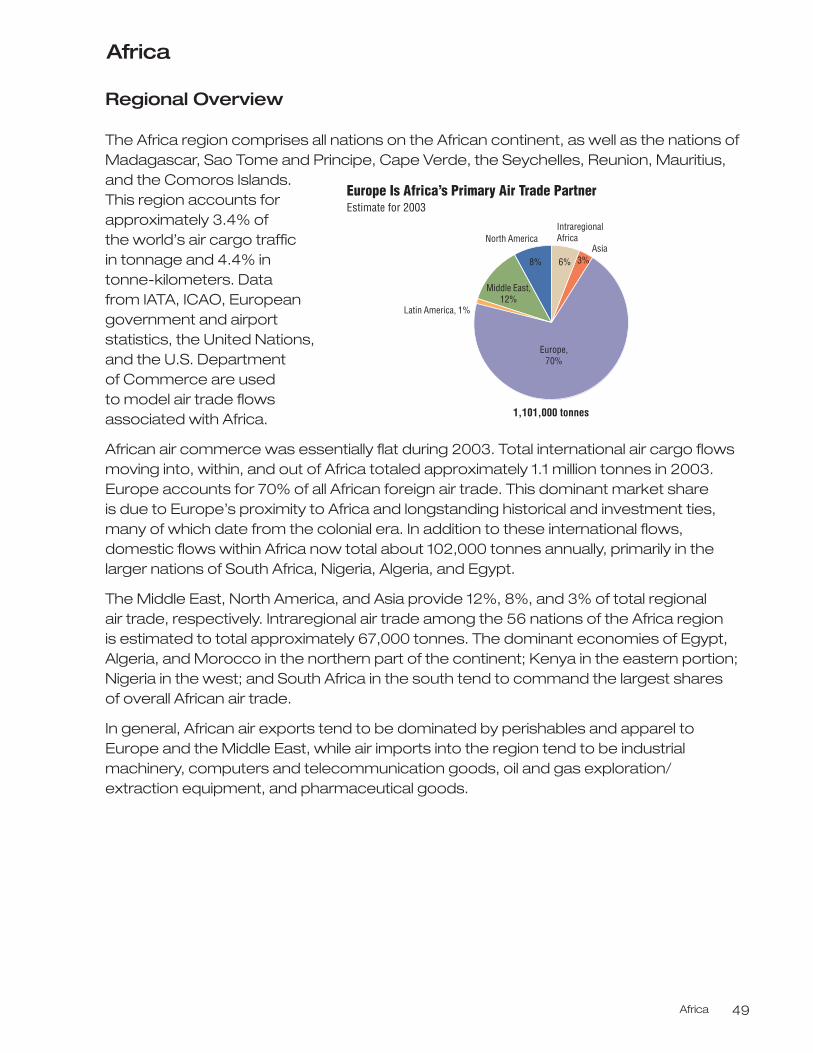

Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49

Asia and North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

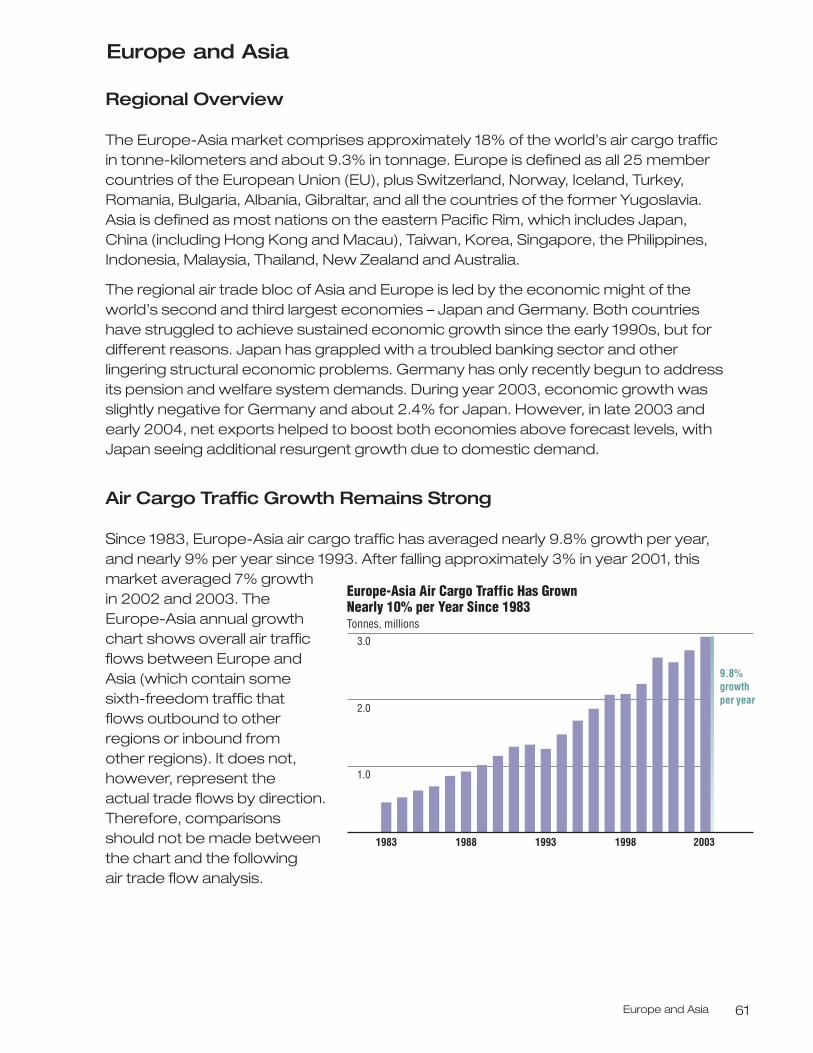

Europe and Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

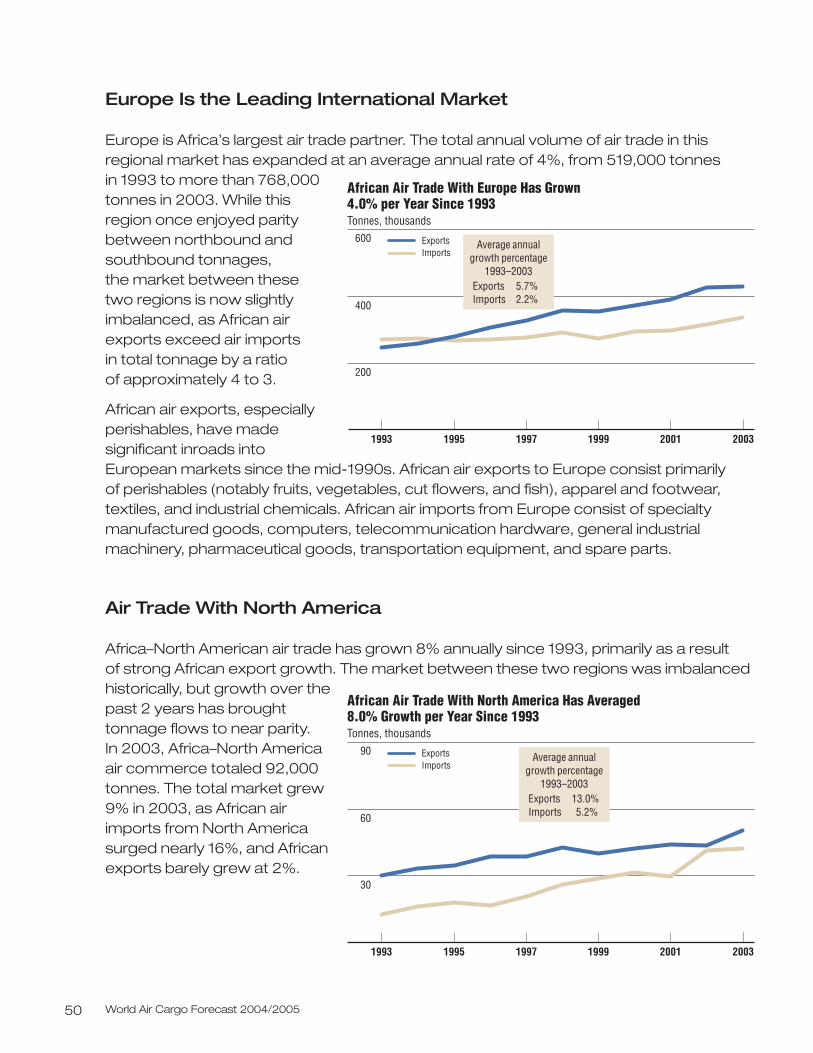

Intra-Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67

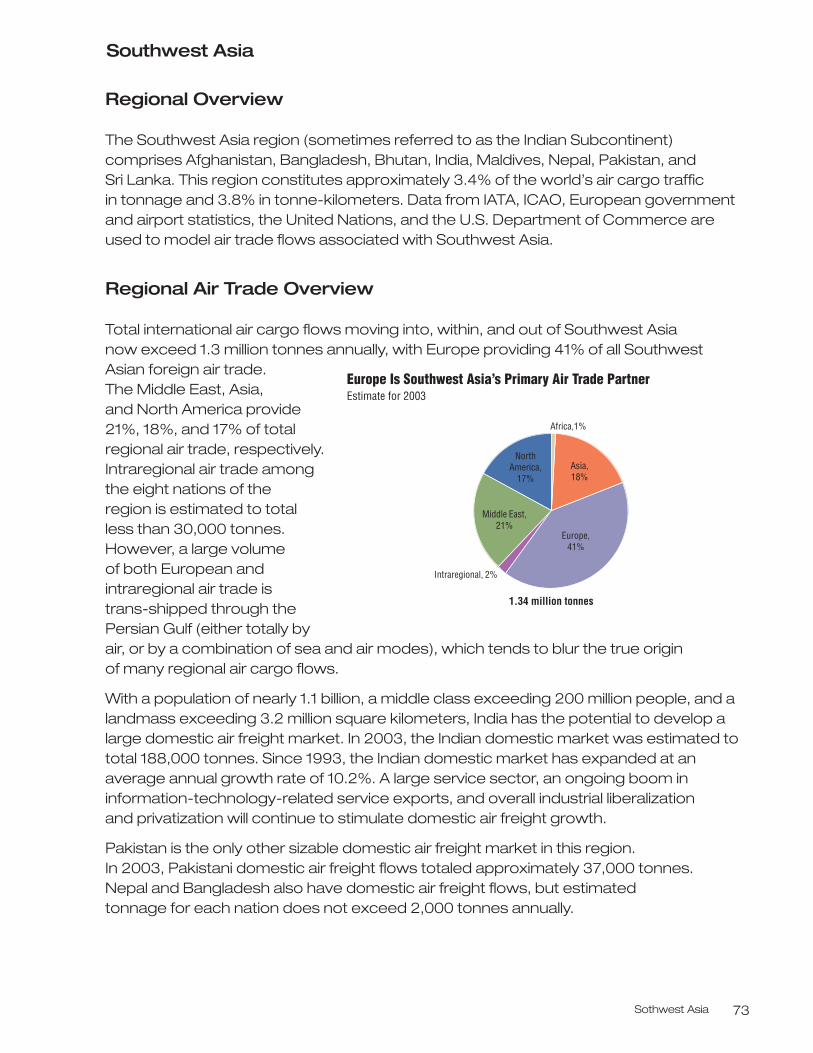

Southwest Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73

Commonwealth of Independent States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

Domestic China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .85

World Freighter Fleet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .99

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .103

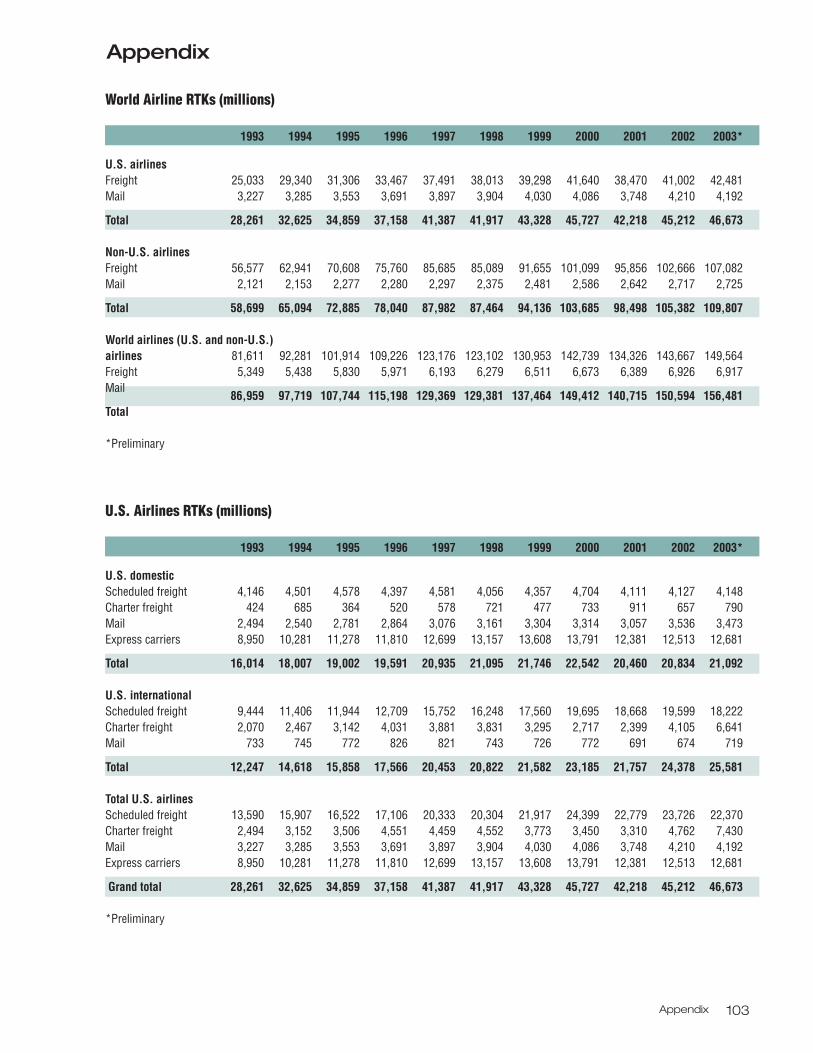

Executive Summary and Significant Industry Trends 1

Summary

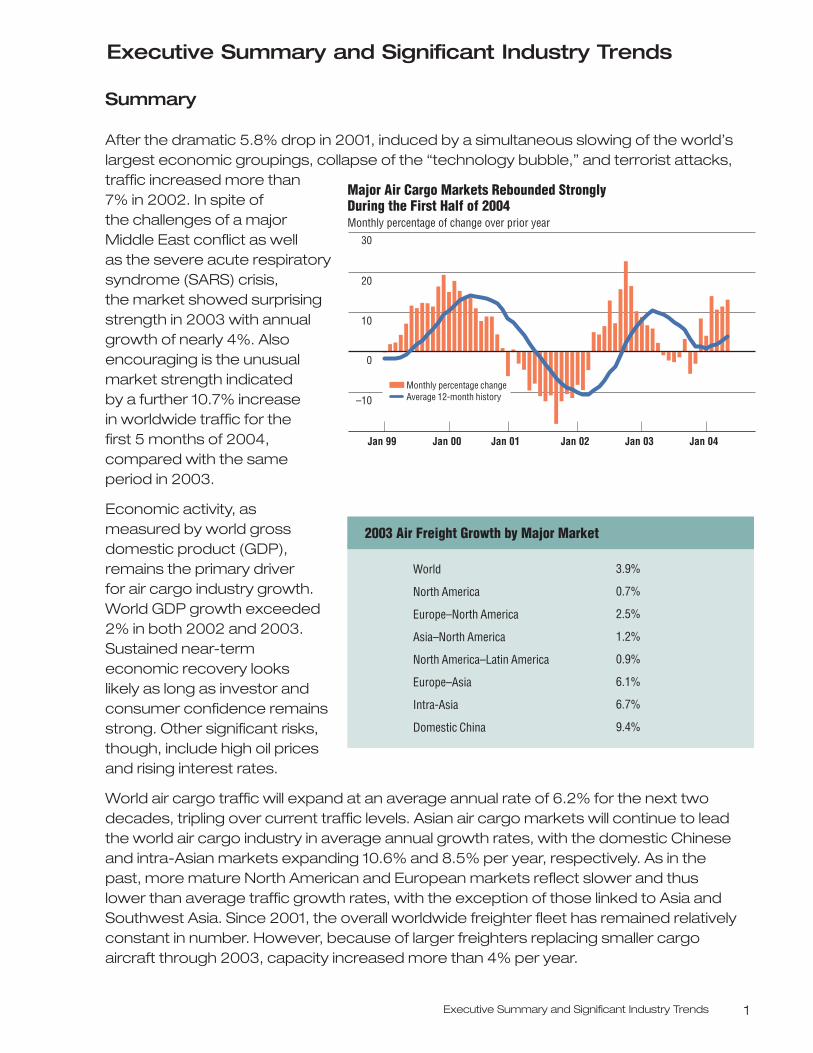

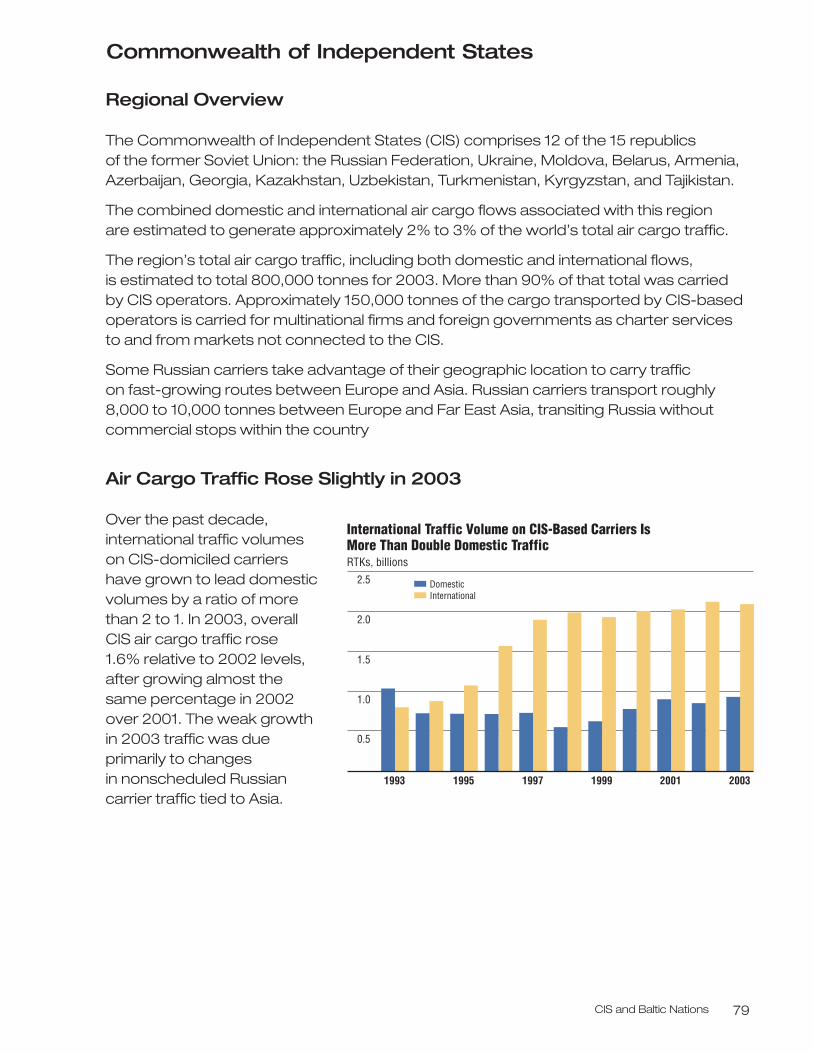

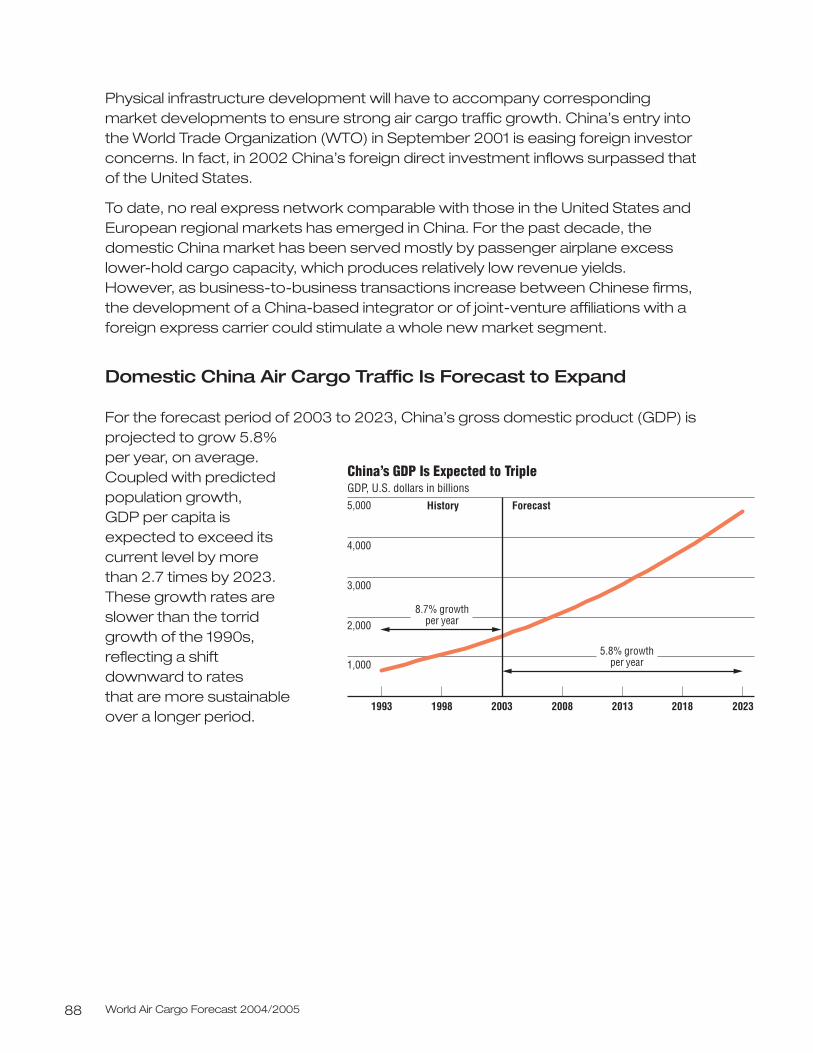

After the dramatic 5.8% drop in 2001, induced by a simultaneous slowing of the world’slargest economic groupings, collapse of the “technology bubble,” and terrorist attacks,traffic increased more than 7% in 2002. In spite of the challenges of a majorMiddle East conflict as well as the severe acute respiratorysyndrome (SARS) crisis, the market showed surprisingstrength in 2003 with annualgrowth of nearly 4%. Alsoencouraging is the unusualmarket strength indicated by a further 10.7% increase in worldwide traffic for the first 5 months of 2004,compared with the same period in 2003.

Economic activity, asmeasured by world grossdomestic product (GDP),remains the primary driver for air cargo industry growth.World GDP growth exceeded2% in both 2002 and 2003.Sustained near-termeconomic recovery looks likely as long as investor andconsumer confidence remainsstrong. Other significant risks,though, include high oil pricesand rising interest rates.

World air cargo traffic will expand at an average annual rate of 6.2% for the next twodecades, tripling over current traffic levels. Asian air cargo markets will continue to leadthe world air cargo industry in average annual growth rates, with the domestic Chineseand intra-Asian markets expanding 10.6% and 8.5% per year, respectively. As in thepast, more mature North American and European markets reflect slower and thuslower than average traffic growth rates, with the exception of those linked to Asia andSouthwest Asia. Since 2001, the overall worldwide freighter fleet has remained relativelyconstant in number. However, because of larger freighters replacing smaller cargoaircraft through 2003, capacity increased more than 4% per year.

–10

0

20

10

30

Major Air Cargo Markets Rebounded Strongly During the First Half of 2004 Monthly percentage of change over prior year

Jan 99 Jan 00 Jan 01 Jan 02 Jan 04Jan 03

Average 12-month historyMonthly percentage change

2003 Air Freight Growth by Major Market

3.9%

0.7%

2.5%

1.2%

0.9%

6.1%

6.7%

9.4%

World

North America

Europe–North America

Asia–North America

North America–Latin America

Europe–Asia

Intra-Asia

Domestic China

Executive Summary and Significant Industry Trends

World Air Cargo Forecast 2004/20052

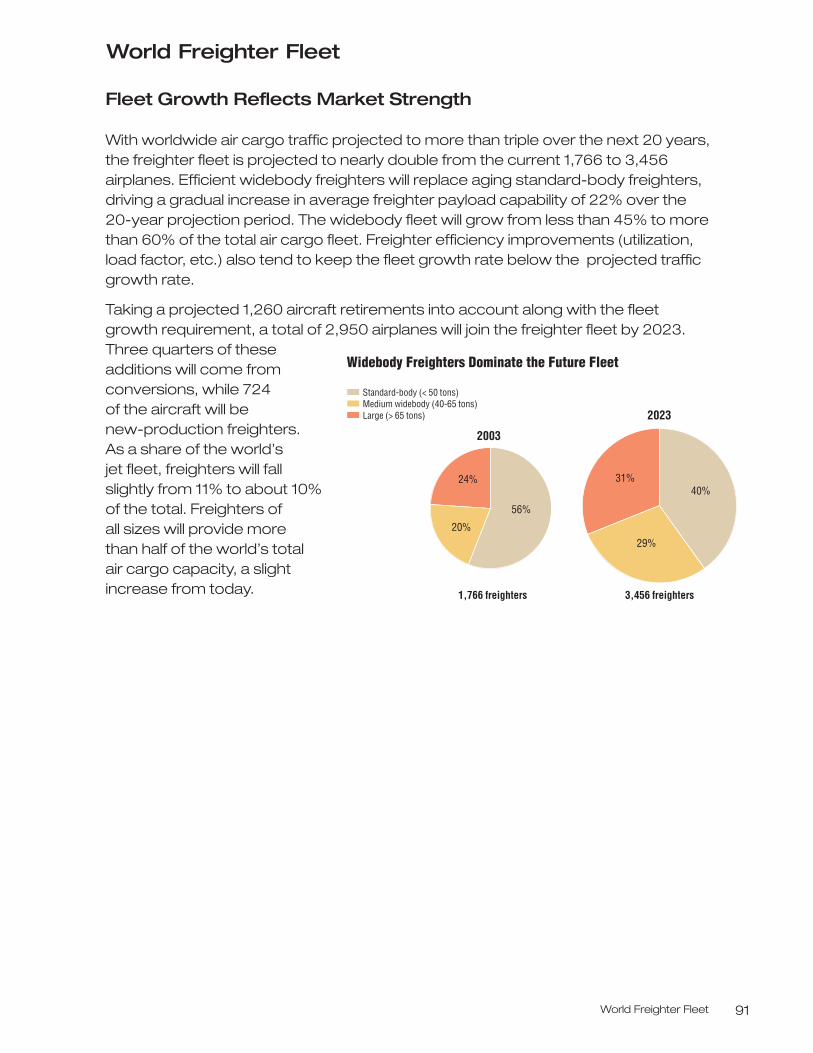

This trend will continue over the next 20 years as well, with capacity increasing parallel to the tripling traffic levels, but with fleet size not quite doubling from 1,766 in 2003 to3,456 in 2023. Medium -widebody and large cargo aircraft will lead fleet additions,growing from an overall share of 44% to 60% as traffic continues to build on long-haul,international trade lanes.

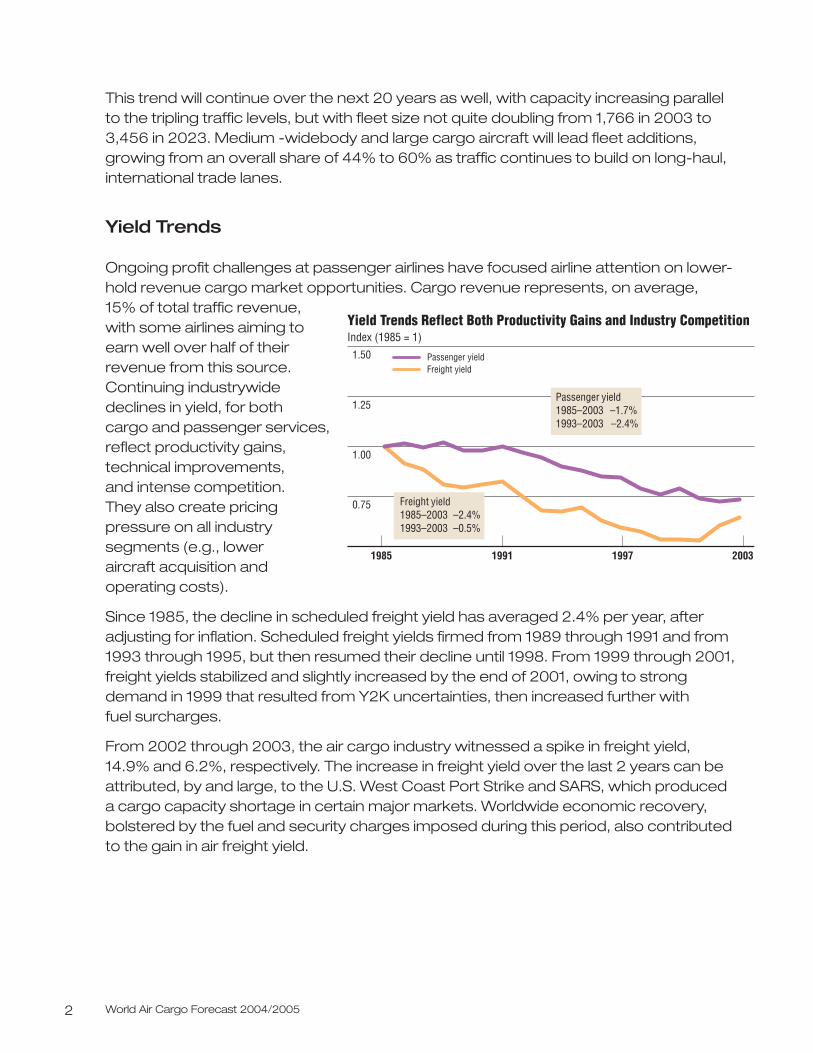

Yield Trends

Ongoing profit challenges at passenger airlines have focused airline attention on lower-hold revenue cargo market opportunities. Cargo revenue represents, on average, 15% of total traffic revenue,with some airlines aiming toearn well over half of theirrevenue from this source.Continuing industrywidedeclines in yield, for both cargo and passenger services,reflect productivity gains,technical improvements, and intense competition. They also create pricingpressure on all industrysegments (e.g., lower aircraft acquisition andoperating costs).

Since 1985, the decline in scheduled freight yield has averaged 2.4% per year, afteradjusting for inflation. Scheduled freight yields firmed from 1989 through 1991 and from1993 through 1995, but then resumed their decline until 1998. From 1999 through 2001,freight yields stabilized and slightly increased by the end of 2001, owing to strongdemand in 1999 that resulted from Y2K uncertainties, then increased further with fuel surcharges.

From 2002 through 2003, the air cargo industry witnessed a spike in freight yield, 14.9% and 6.2%, respectively. The increase in freight yield over the last 2 years can beattributed, by and large, to the U.S. West Coast Port Strike and SARS, which produced a cargo capacity shortage in certain major markets. Worldwide economic recovery,bolstered by the fuel and security charges imposed during this period, also contributedto the gain in air freight yield.

Yield Trends Reflect Both Productivity Gains and Industry Competition Index (1985 = 1)1.50

1.25

1.00

0.75

Passenger yieldFreight yield

1985 1991 1997 2003

Passenger yield 1985–2003 –1.7% 1993–2003 –2.4%

Freight yield 1985–2003 –2.4% 1993–2003 –0.5%

Executive Summary and Significant Industry Trends 3

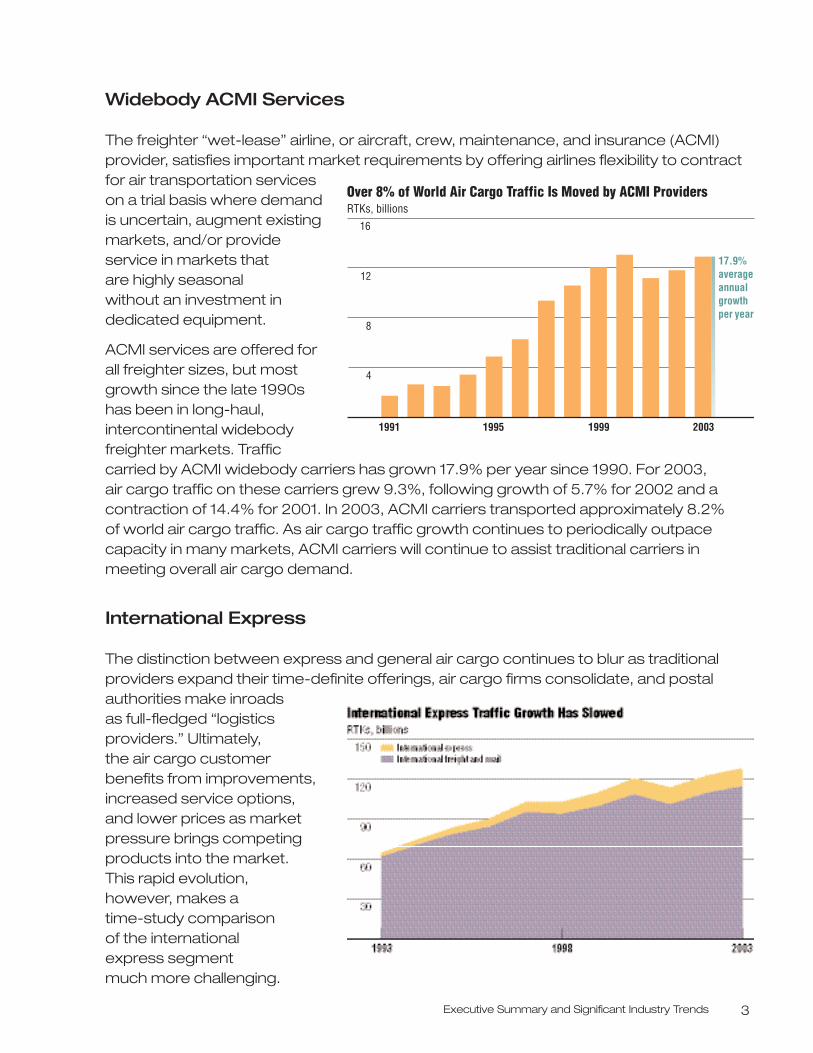

Widebody ACMI Services

The freighter “wet-lease” airline, or aircraft, crew, maintenance, and insurance (ACMI)provider, satisfies important market requirements by offering airlines flexibility to contractfor air transportation serviceson a trial basis where demandis uncertain, augment existingmarkets, and/or provideservice in markets that are highly seasonal without an investment in dedicated equipment.

ACMI services are offered forall freighter sizes, but mostgrowth since the late 1990shas been in long-haul,intercontinental widebodyfreighter markets. Trafficcarried by ACMI widebody carriers has grown 17.9% per year since 1990. For 2003, air cargo traffic on these carriers grew 9.3%, following growth of 5.7% for 2002 and acontraction of 14.4% for 2001. In 2003, ACMI carriers transported approximately 8.2% of world air cargo traffic. As air cargo traffic growth continues to periodically outpacecapacity in many markets, ACMI carriers will continue to assist traditional carriers inmeeting overall air cargo demand.

International Express

The distinction between express and general air cargo continues to blur as traditionalproviders expand their time-definite offerings, air cargo firms consolidate, and postalauthorities make inroads as full-fledged “logisticsproviders.” Ultimately, the air cargo customerbenefits from improvements,increased service options,and lower prices as marketpressure brings competingproducts into the market. This rapid evolution, however, makes a time-study comparison of the international express segment much more challenging.

Over 8% of World Air Cargo Traffic Is Moved by ACMI Providers RTKs, billions

16

12

4

8

1991 1995 20031999

17.9%averageannualgrowthper year

World Air Cargo Forecast 2004/20054

As a result of this provider and service expansion, international express has grown at morethan twice the rate of total worldwide air cargo traffic, averaging 16.4% annually over the last decade (as measured in revenue tonne-kilometers [RTK]). Since 1998, however, while still impressive, annual growth has been a somewhat lower 9.1%. This parallels theexpress industry’s strong double-digit U.S. domestic growth during the 1970s and 1980s,followed later by slower growth.

As a proportion of total international air cargo traffic, international express expanded from4.1% in 1992 to nearly 11% in 2003, a reflection of higher than average annual growth.Average international express shipment size grew from 2.7kg (6.0 lb) in 1992 to 4.0kg (10.7 lb) in 2003, further bolstering the overall express component of international air freighttraffic. As businesses continue to expand beyond domestic or close regional markets, the international express sector will continue to grow, albeit at more sustainable, long-term rates.

Significant Developments

Each of the following issues either currently affects or has the potential to create significant impact on the air cargo industry.

• Security requirements. Of all recent industry developments, government-mandatedsecurity regulations present the highest potential for adverse impact upon the air cargoindustry. They may have debilitating effects on shipment transit time. After disconcertingreactions to 9/11 (many since rescinded or modified), the industry must be diligent inworking with authorities to realize security enhancements that are balanced with a time-sensitive industry’s realities.

• Service fragmentation. The issue of air cargo service “hubbing” versus “point-to-point”often comes up in the context of passenger transport. Compared with the passengerbusiness, air cargo is more concerned with time and efficiency than routing. Hubbing thenbecomes a more acceptable alternative to cargo customers when significant handling,volume, and rate efficiencies can be realized.

• Low-cost carriers. Another passenger business phenomenon that has implications for air cargo is the proliferation of low-cost carriers. The demands of passenger focus andoperational efficiency (e.g., quick airplane turnarounds) reduce the priority of cargo.However, some low-cost carriers realize significant revenues by emphasizing expressshipments and/or by contracting with other airlines to handle their lower-hold space.

World Air Cargo Growth Detail

Over the next 20 years, world air cargo will grow at 6.2% per year. Air freight will grow more rapidly than mail, averaging annual growth of 6.3% through 2023. Mail RTKs will show steady growth of 2.9% during the same period.

Executive Summary and Significant Industry TrendsTitle 5

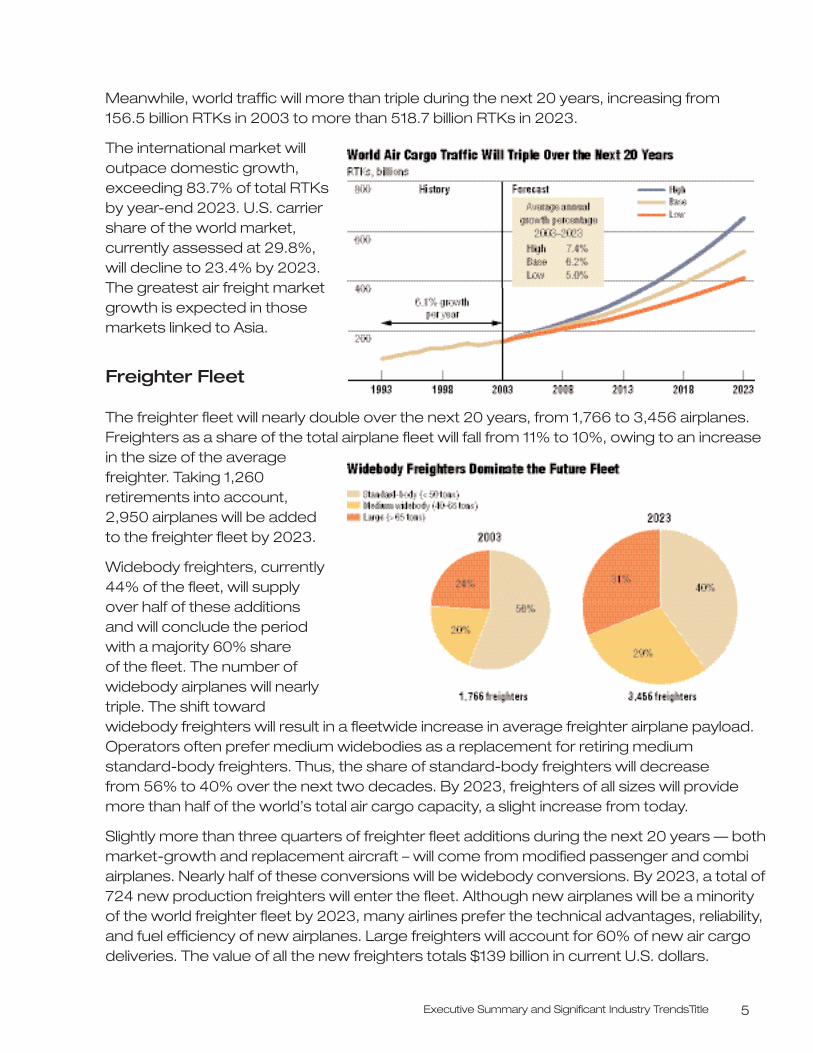

Meanwhile, world traffic will more than triple during the next 20 years, increasing from 156.5 billion RTKs in 2003 to more than 518.7 billion RTKs in 2023.

The international market willoutpace domestic growth,exceeding 83.7% of total RTKsby year-end 2023. U.S. carriershare of the world market,currently assessed at 29.8%,will decline to 23.4% by 2023.The greatest air freight marketgrowth is expected in thosemarkets linked to Asia.

Freighter Fleet

The freighter fleet will nearly double over the next 20 years, from 1,766 to 3,456 airplanes.Freighters as a share of the total airplane fleet will fall from 11% to 10%, owing to an increasein the size of the averagefreighter. Taking 1,260retirements into account,2,950 airplanes will be addedto the freighter fleet by 2023.

Widebody freighters, currently44% of the fleet, will supplyover half of these additions and will conclude the periodwith a majority 60% share of the fleet. The number ofwidebody airplanes will nearlytriple. The shift towardwidebody freighters will result in a fleetwide increase in average freighter airplane payload.Operators often prefer medium widebodies as a replacement for retiring medium standard-body freighters. Thus, the share of standard-body freighters will decrease from 56% to 40% over the next two decades. By 2023, freighters of all sizes will providemore than half of the world’s total air cargo capacity, a slight increase from today.

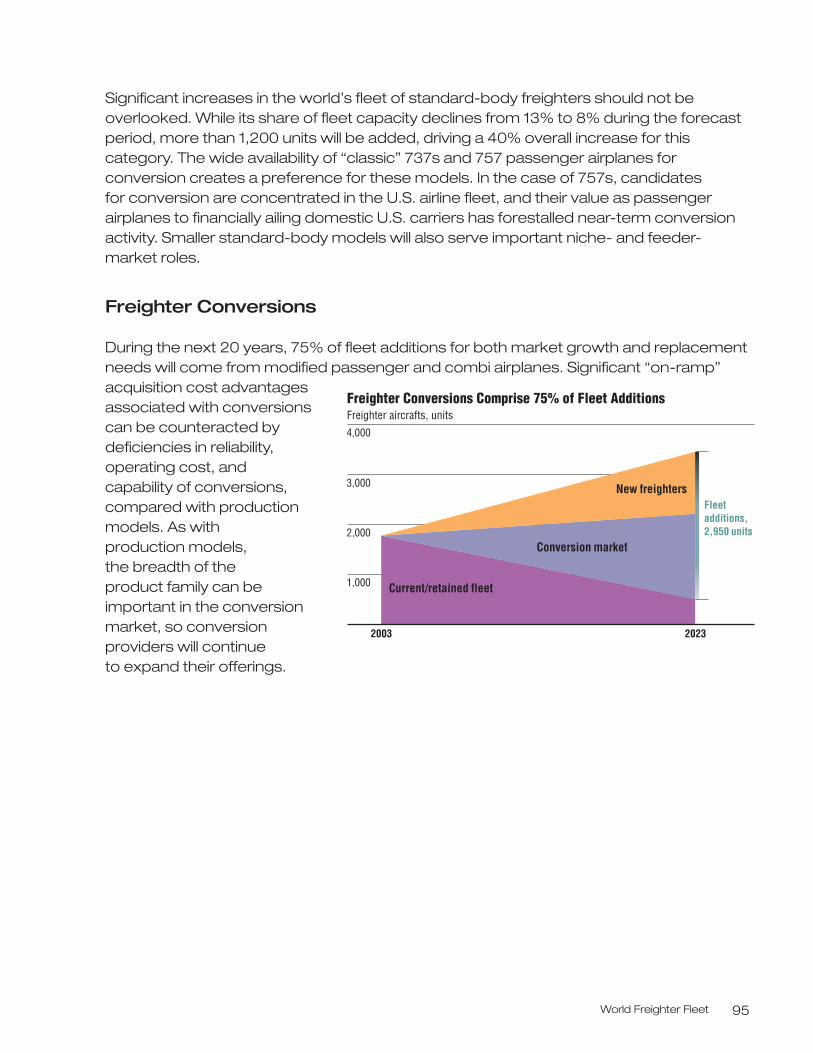

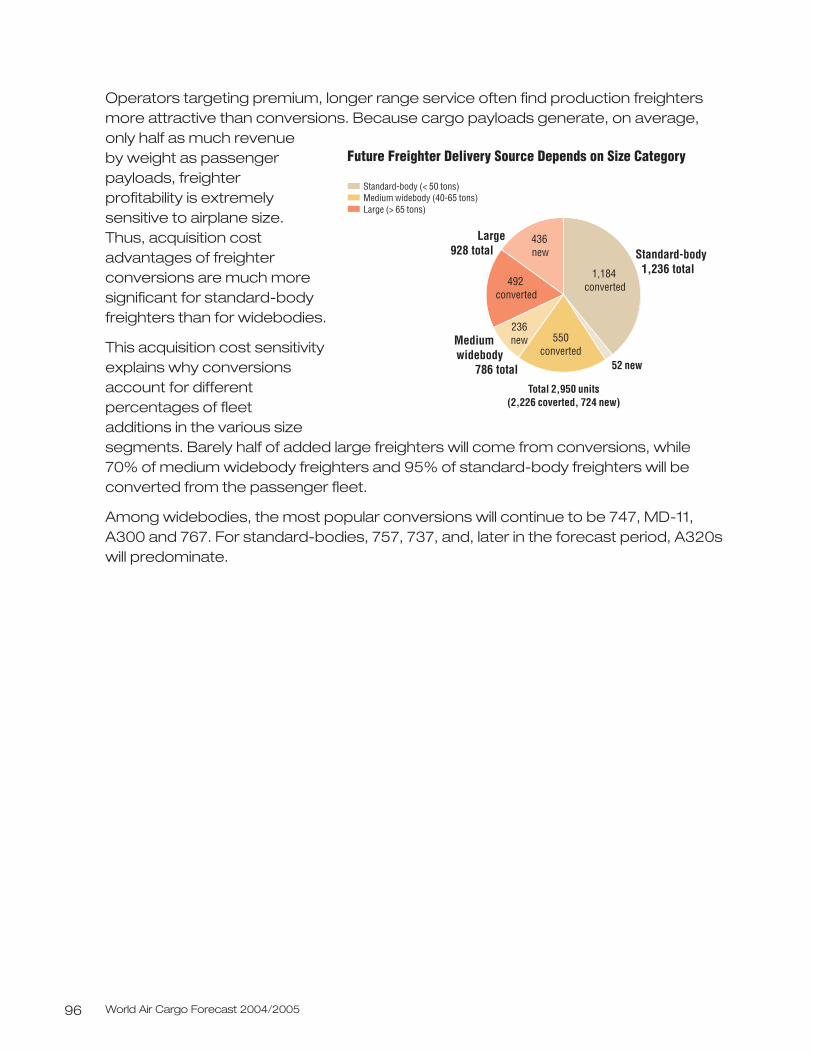

Slightly more than three quarters of freighter fleet additions during the next 20 years — bothmarket-growth and replacement aircraft – will come from modified passenger and combiairplanes. Nearly half of these conversions will be widebody conversions. By 2023, a total of724 new production freighters will enter the fleet. Although new airplanes will be a minorityof the world freighter fleet by 2023, many airlines prefer the technical advantages, reliability,and fuel efficiency of new airplanes. Large freighters will account for 60% of new air cargodeliveries. The value of all the new freighters totals $139 billion in current U.S. dollars.

World Overview and Forecast 7

World Overview and Forecast

World Economic Environment Favors Continued Growth

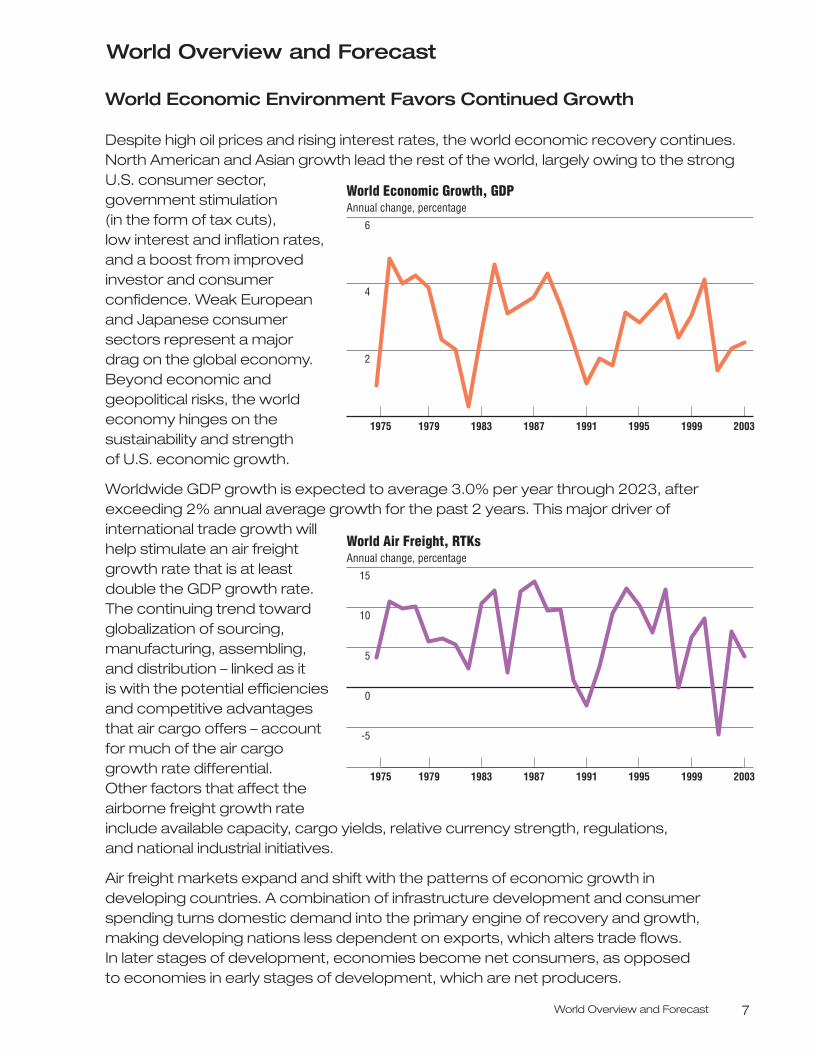

Despite high oil prices and rising interest rates, the world economic recovery continues.North American and Asian growth lead the rest of the world, largely owing to the strongU.S. consumer sector,government stimulation (in the form of tax cuts), low interest and inflation rates,and a boost from improvedinvestor and consumerconfidence. Weak Europeanand Japanese consumersectors represent a majordrag on the global economy.Beyond economic andgeopolitical risks, the worldeconomy hinges on thesustainability and strength of U.S. economic growth.

Worldwide GDP growth is expected to average 3.0% per year through 2023, afterexceeding 2% annual average growth for the past 2 years. This major driver ofinternational trade growth willhelp stimulate an air freightgrowth rate that is at leastdouble the GDP growth rate.The continuing trend towardglobalization of sourcing,manufacturing, assembling,and distribution – linked as it is with the potential efficienciesand competitive advantagesthat air cargo offers – accountfor much of the air cargogrowth rate differential. Other factors that affect theairborne freight growth rateinclude available capacity, cargo yields, relative currency strength, regulations, and national industrial initiatives.

Air freight markets expand and shift with the patterns of economic growth in developing countries. A combination of infrastructure development and consumerspending turns domestic demand into the primary engine of recovery and growth,making developing nations less dependent on exports, which alters trade flows. In later stages of development, economies become net consumers, as opposed to economies in early stages of development, which are net producers.

World Economic Growth, GDPAnnual change, percentage

6

4

2

1975 1979 1983 1991 1995 20031987 1999

World Air Freight, RTKsAnnual change, percentage

15

10

-5

1975 1979 1983 1991 1995 20031987 1999

0

5

World Air Cargo Forecast 2004/20058

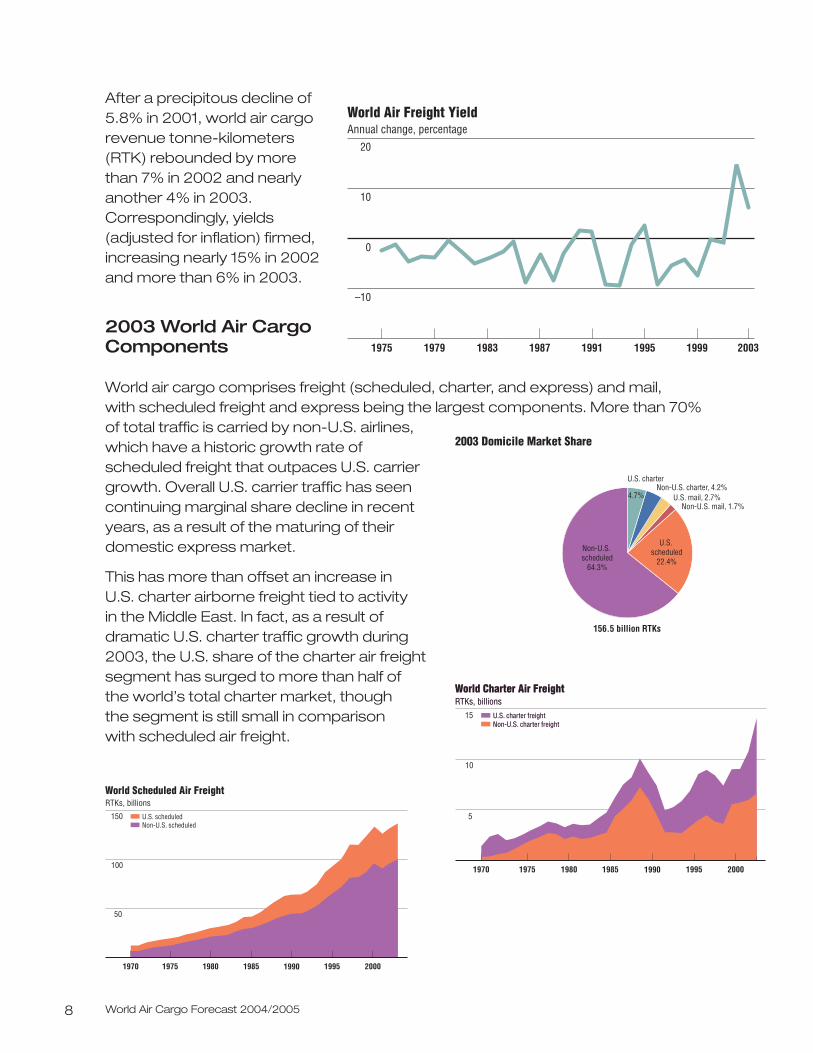

After a precipitous decline of5.8% in 2001, world air cargorevenue tonne-kilometers(RTK) rebounded by more than 7% in 2002 and nearlyanother 4% in 2003.Correspondingly, yields(adjusted for inflation) firmed,increasing nearly 15% in 2002and more than 6% in 2003.

2003 World Air CargoComponents

World air cargo comprises freight (scheduled, charter, and express) and mail, with scheduled freight and express being the largest components. More than 70% of total traffic is carried by non-U.S. airlines,which have a historic growth rate ofscheduled freight that outpaces U.S. carriergrowth. Overall U.S. carrier traffic has seencontinuing marginal share decline in recentyears, as a result of the maturing of theirdomestic express market.

This has more than offset an increase in U.S. charter airborne freight tied to activity in the Middle East. In fact, as a result ofdramatic U.S. charter traffic growth during2003, the U.S. share of the charter air freightsegment has surged to more than half of the world’s total charter market, though the segment is still small in comparison with scheduled air freight.

World Air Freight Yield Annual change, percentage

20

–10

10

0

1975 1979 1983 1991 19951987 20031999

50

100

150

World Scheduled Air FreightRTKs, billions

Non-U.S. scheduledU.S. scheduled

19751970 1980 1985 1995 20001990

World Charter Air FreightRTKs, billionsWorld Charter Air FreightRTKs, billions

Non-U.S. charter freightNon-U.S. charter freightU.S. charter freightU.S. charter freight

5

10

15

19751970 1980 1985 1995 20001990

156.5 billion RTKs

U.S. charter

4.7%Non-U.S. charter, 4.2%

U.S. mail, 2.7%Non-U.S. mail, 1.7%

U.S. scheduled

22.4%

2003 Domicile Market Share

Non-U.S. scheduled

64.3%

World Overview and Forecast 9

Forecasting Methods

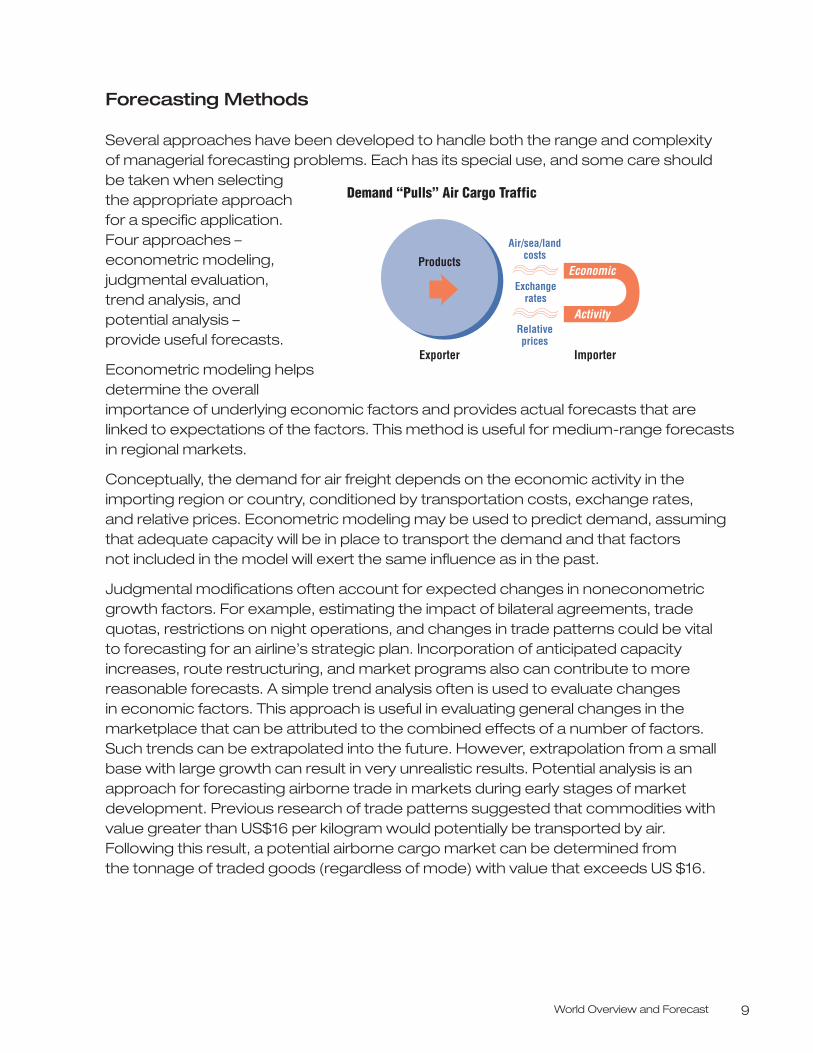

Several approaches have been developed to handle both the range and complexity of managerial forecasting problems. Each has its special use, and some care should be taken when selecting the appropriate approach for a specific application. Four approaches –econometric modeling,judgmental evaluation, trend analysis, and potential analysis – provide useful forecasts.

Econometric modeling helpsdetermine the overallimportance of underlying economic factors and provides actual forecasts that are linked to expectations of the factors. This method is useful for medium-range forecastsin regional markets.

Conceptually, the demand for air freight depends on the economic activity in theimporting region or country, conditioned by transportation costs, exchange rates, and relative prices. Econometric modeling may be used to predict demand, assumingthat adequate capacity will be in place to transport the demand and that factors not included in the model will exert the same influence as in the past.

Judgmental modifications often account for expected changes in noneconometricgrowth factors. For example, estimating the impact of bilateral agreements, tradequotas, restrictions on night operations, and changes in trade patterns could be vital to forecasting for an airline’s strategic plan. Incorporation of anticipated capacityincreases, route restructuring, and market programs also can contribute to morereasonable forecasts. A simple trend analysis often is used to evaluate changes in economic factors. This approach is useful in evaluating general changes in themarketplace that can be attributed to the combined effects of a number of factors. Such trends can be extrapolated into the future. However, extrapolation from a smallbase with large growth can result in very unrealistic results. Potential analysis is anapproach for forecasting airborne trade in markets during early stages of marketdevelopment. Previous research of trade patterns suggested that commodities withvalue greater than US$16 per kilogram would potentially be transported by air. Following this result, a potential airborne cargo market can be determined from the tonnage of traded goods (regardless of mode) with value that exceeds US $16.

Products

Exporter Importer

Exchange rates

Air/sea/land costs

Relative prices

Demand “Pulls” Air Cargo Traffic

Economic

Activity

World Air Cargo Forecast 2004/200510

Market Environment

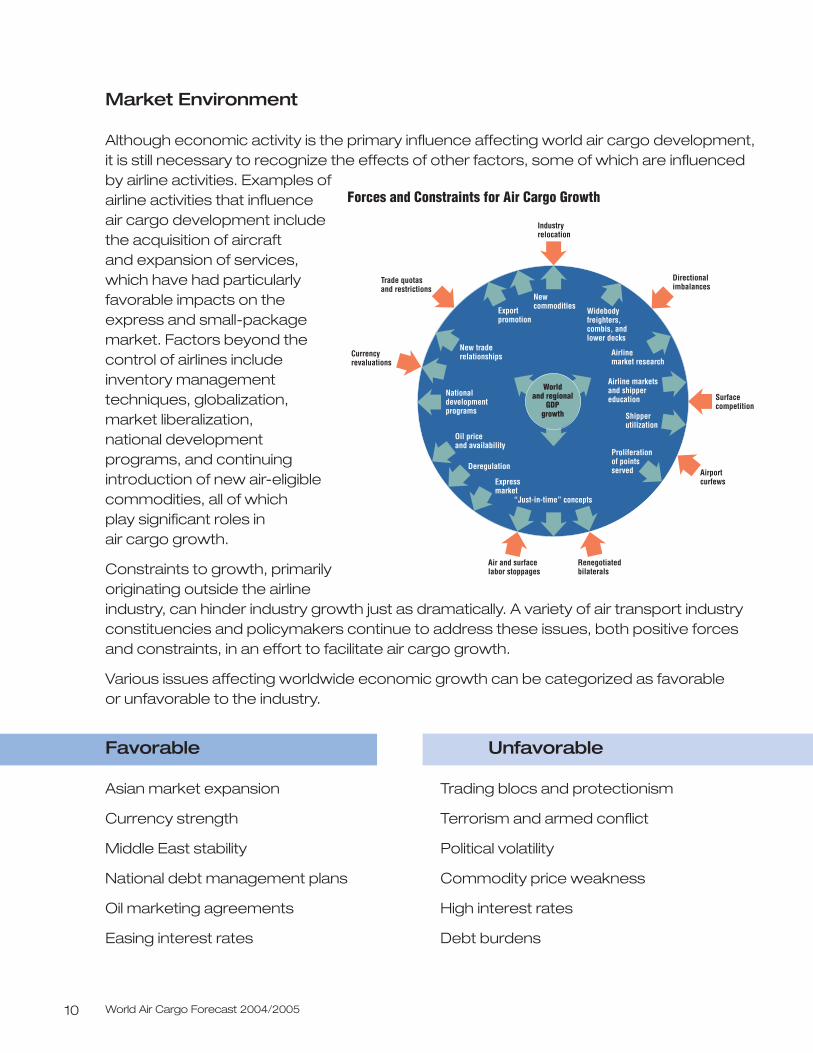

Although economic activity is the primary influence affecting world air cargo development,it is still necessary to recognize the effects of other factors, some of which are influencedby airline activities. Examples ofairline activities that influence air cargo development include the acquisition of aircraft and expansion of services,which have had particularlyfavorable impacts on theexpress and small-packagemarket. Factors beyond thecontrol of airlines includeinventory managementtechniques, globalization,market liberalization, national developmentprograms, and continuingintroduction of new air-eligiblecommodities, all of which play significant roles in air cargo growth.

Constraints to growth, primarilyoriginating outside the airlineindustry, can hinder industry growth just as dramatically. A variety of air transport industryconstituencies and policymakers continue to address these issues, both positive forcesand constraints, in an effort to facilitate air cargo growth.

Various issues affecting worldwide economic growth can be categorized as favorable or unfavorable to the industry.

Favorable Unfavorable

Asian market expansion Trading blocs and protectionism

Currency strength Terrorism and armed conflict

Middle East stability Political volatility

National debt management plans Commodity price weakness

Oil marketing agreements High interest rates

Easing interest rates Debt burdens

Forces and Constraints for Air Cargo Growth

Air and surface labor stoppages

Renegotiated bilaterals

Currency revaluations

National development programs

New trade relationships

Trade quotas and restrictions

Export promotion

New commodities

Industry relocation

Oil price and availability

Deregulation

Express market

“Just-in-time” concepts

Proliferation of points served Airport

curfews

Shipper utilization

Surface competition

Airline marketsand shipper education

Airline market research

Widebody freighters, combis, and lower decks

Directional imbalances

World and regional

GDP growth

World Overview and Forecast 11

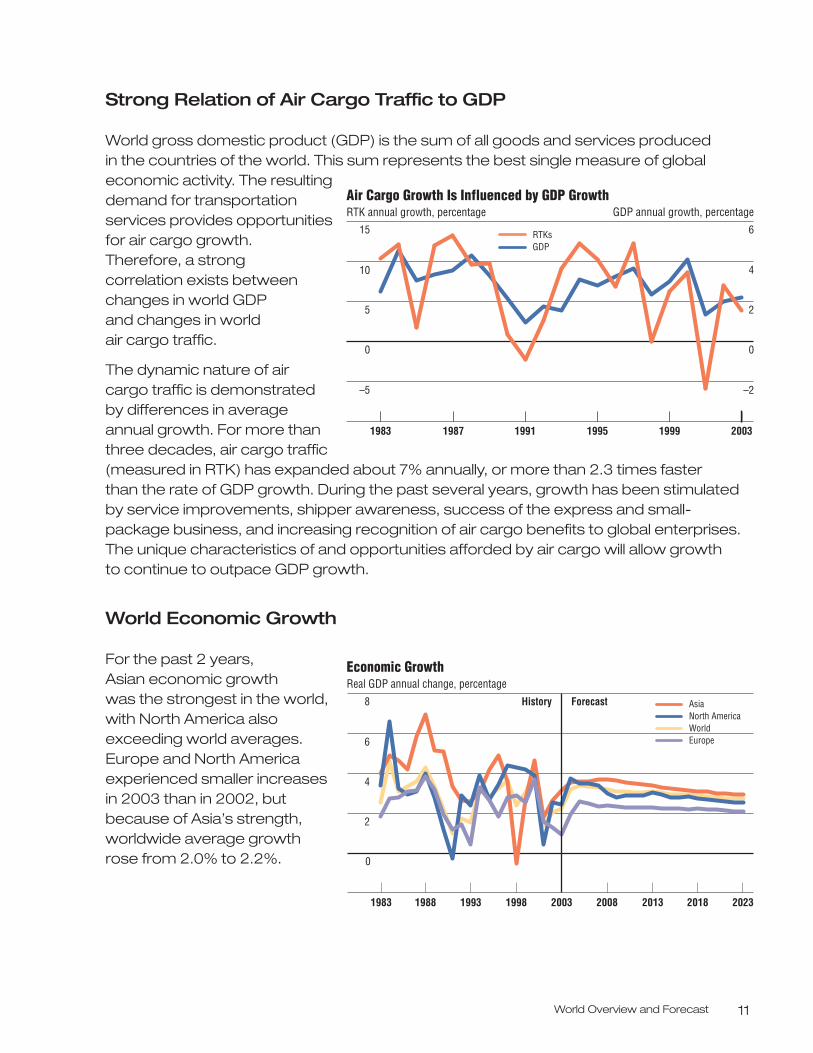

Strong Relation of Air Cargo Traffic to GDP

World gross domestic product (GDP) is the sum of all goods and services produced in the countries of the world. This sum represents the best single measure of globaleconomic activity. The resultingdemand for transportationservices provides opportunitiesfor air cargo growth. Therefore, a strong correlation exists betweenchanges in world GDP and changes in world air cargo traffic.

The dynamic nature of aircargo traffic is demonstratedby differences in averageannual growth. For more thanthree decades, air cargo traffic(measured in RTK) has expanded about 7% annually, or more than 2.3 times faster than the rate of GDP growth. During the past several years, growth has been stimulatedby service improvements, shipper awareness, success of the express and small-package business, and increasing recognition of air cargo benefits to global enterprises.The unique characteristics of and opportunities afforded by air cargo will allow growth to continue to outpace GDP growth.

World Economic Growth

For the past 2 years, Asian economic growth was the strongest in the world, with North America alsoexceeding world averages.Europe and North Americaexperienced smaller increasesin 2003 than in 2002, butbecause of Asia’s strength,worldwide average growthrose from 2.0% to 2.2%.

Air Cargo Growth Is Influenced by GDP Growth RTK annual growth, percentage

15

5

10

0

–5

6

2

4

0

–2

RTKsGDP

GDP annual growth, percentage

19991995199119871983 2003

Economic GrowthReal GDP annual change, percentage

8

4

2

6

0

History Forecast

1983 1993 2003 2008 2013 2018 2023

AsiaNorth AmericaWorldEurope

1988 1998

World Air Cargo Forecast 2004/200512

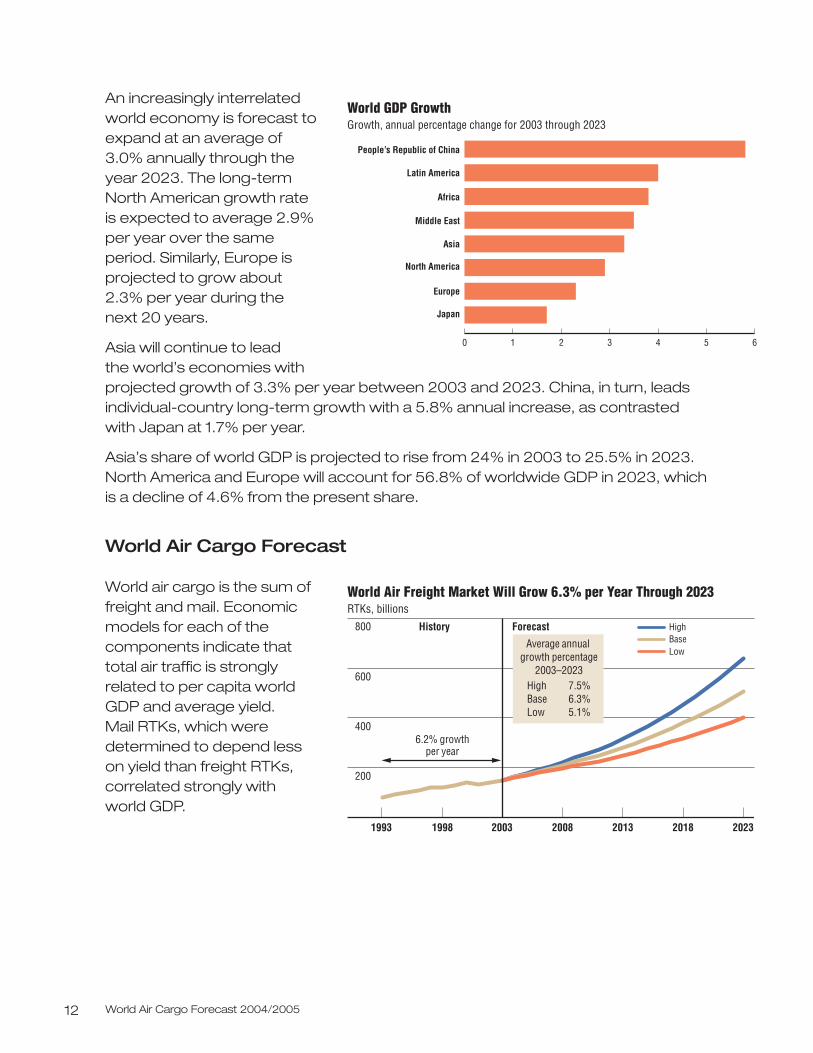

An increasingly interrelatedworld economy is forecast toexpand at an average of 3.0% annually through theyear 2023. The long-termNorth American growth rate is expected to average 2.9%per year over the sameperiod. Similarly, Europe isprojected to grow about 2.3% per year during the next 20 years.

Asia will continue to lead the world’s economies withprojected growth of 3.3% per year between 2003 and 2023. China, in turn, leadsindividual-country long-term growth with a 5.8% annual increase, as contrasted with Japan at 1.7% per year.

Asia’s share of world GDP is projected to rise from 24% in 2003 to 25.5% in 2023.North America and Europe will account for 56.8% of worldwide GDP in 2023, which is a decline of 4.6% from the present share.

World Air Cargo Forecast

World air cargo is the sum offreight and mail. Economicmodels for each of thecomponents indicate that total air traffic is stronglyrelated to per capita worldGDP and average yield. Mail RTKs, which weredetermined to depend less on yield than freight RTKs,correlated strongly with world GDP.

Japan

Europe

North America

Asia

Middle East

Africa

Latin America

People’s Republic of China

0 2 4 6

World GDP GrowthGrowth, annual percentage change for 2003 through 2023

31 5

2013

World Air Freight Market Will Grow 6.3% per Year Through 2023 RTKs, billions

800

600

400

200

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 7.5%Base 6.3%Low 5.1%

6.2% growthper year

1998

World Overview and Forecast 13

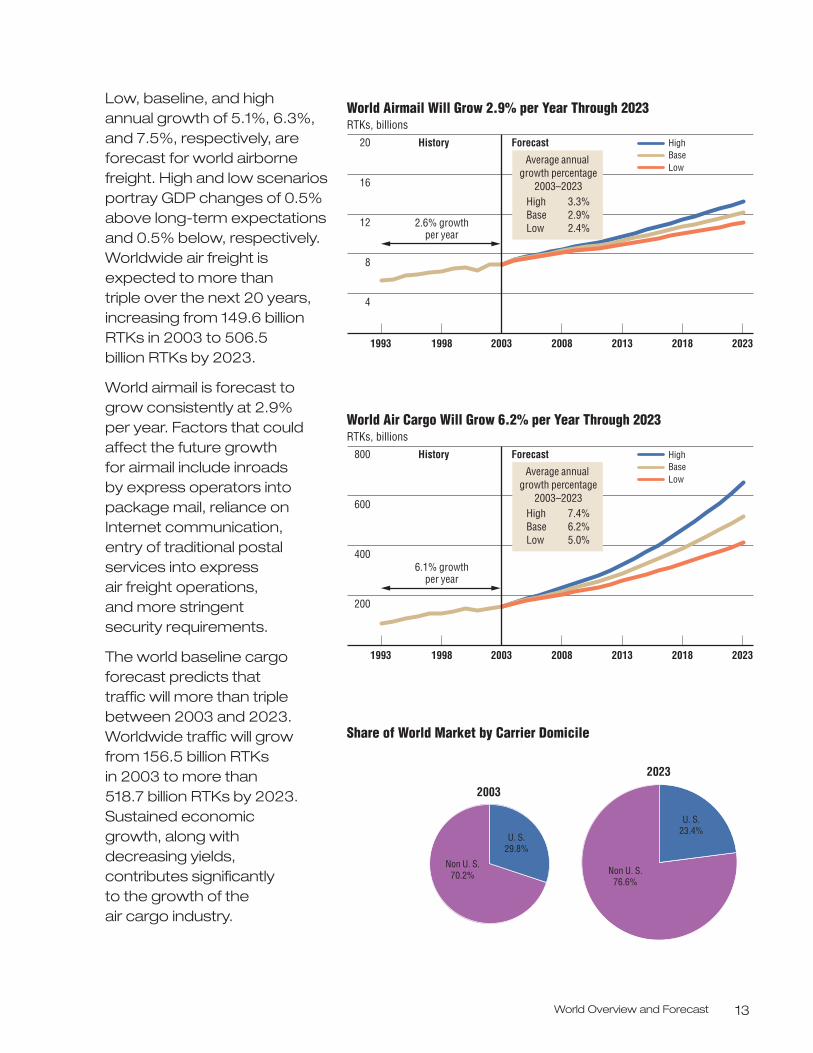

Low, baseline, and high annual growth of 5.1%, 6.3%,and 7.5%, respectively, areforecast for world airbornefreight. High and low scenariosportray GDP changes of 0.5%above long-term expectationsand 0.5% below, respectively.Worldwide air freight isexpected to more than triple over the next 20 years,increasing from 149.6 billionRTKs in 2003 to 506.5 billion RTKs by 2023.

World airmail is forecast to grow consistently at 2.9% per year. Factors that couldaffect the future growth for airmail include inroads by express operators intopackage mail, reliance onInternet communication, entry of traditional postalservices into express air freight operations, and more stringent security requirements.

The world baseline cargoforecast predicts that traffic will more than triplebetween 2003 and 2023.Worldwide traffic will growfrom 156.5 billion RTKsin 2003 to more than 518.7 billion RTKs by 2023.Sustained economic growth, along withdecreasing yields, contributes significantly to the growth of the air cargo industry.

2013

World Airmail Will Grow 2.9% per Year Through 2023 RTKs, billions

20

16

8

12

4

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 3.3%Base 2.9%Low 2.4%2.6% growth

per year

1998

2013

World Air Cargo Will Grow 6.2% per Year Through 2023 RTKs, billions

800

600

400

200

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 7.4%Base 6.2%Low 5.0%

6.1% growthper year

1998

2003

Share of World Market by Carrier Domicile

2023

U. S.23.4%

Non U. S.76.6%

Non U. S.70.2%

U. S.29.8%

World Air Cargo Forecast 2004/200514

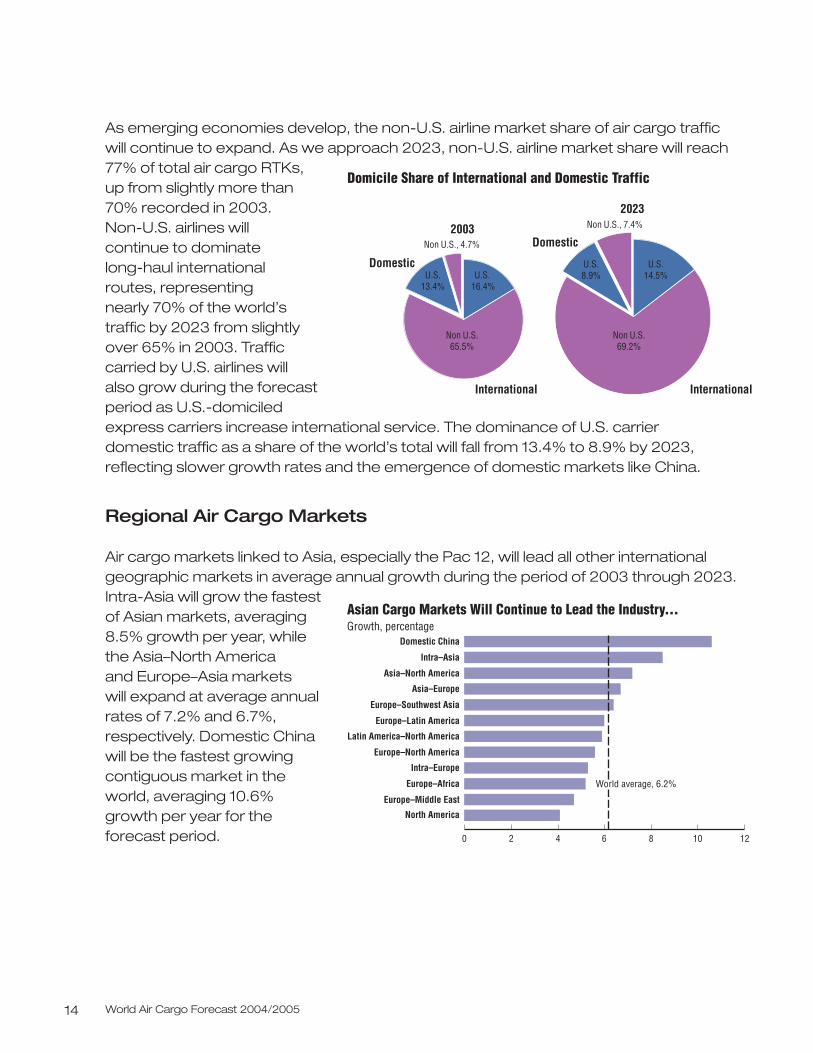

As emerging economies develop, the non-U.S. airline market share of air cargo trafficwill continue to expand. As we approach 2023, non-U.S. airline market share will reach77% of total air cargo RTKs, up from slightly more than 70% recorded in 2003. Non-U.S. airlines will continue to dominate long-haul international routes, representing nearly 70% of the world’s traffic by 2023 from slightlyover 65% in 2003. Trafficcarried by U.S. airlines will also grow during the forecastperiod as U.S.-domiciledexpress carriers increase international service. The dominance of U.S. carrier domestic traffic as a share of the world’s total will fall from 13.4% to 8.9% by 2023,reflecting slower growth rates and the emergence of domestic markets like China.

Regional Air Cargo Markets

Air cargo markets linked to Asia, especially the Pac 12, will lead all other internationalgeographic markets in average annual growth during the period of 2003 through 2023.Intra-Asia will grow the fastestof Asian markets, averaging8.5% growth per year, whilethe Asia–North America and Europe–Asia markets will expand at average annualrates of 7.2% and 6.7%,respectively. Domestic Chinawill be the fastest growingcontiguous market in theworld, averaging 10.6%growth per year for theforecast period.

2003

Domicile Share of International and Domestic Traffic

2023

Domestic

Domestic

InternationalInternational

U.S.8.9%

Non U.S., 7.4%

U.S. 14.5%

Non U.S. 69.2%

U.S.13.4%

Non U.S., 4.7%

U.S. 16.4%

Non U.S. 65.5%

Domestic China

Intra–Asia

Asia–North America

Asia–Europe

Europe–Southwest Asia

Europe–Latin America Latin America–North America

Europe–North America

Intra–Europe

Europe–Africa

Europe–Middle East

North America

0 2 4 6 8 10 12

Asian Cargo Markets Will Continue to Lead the Industry...Growth, percentage

World average, 6.2%

World Overview and Forecast 15

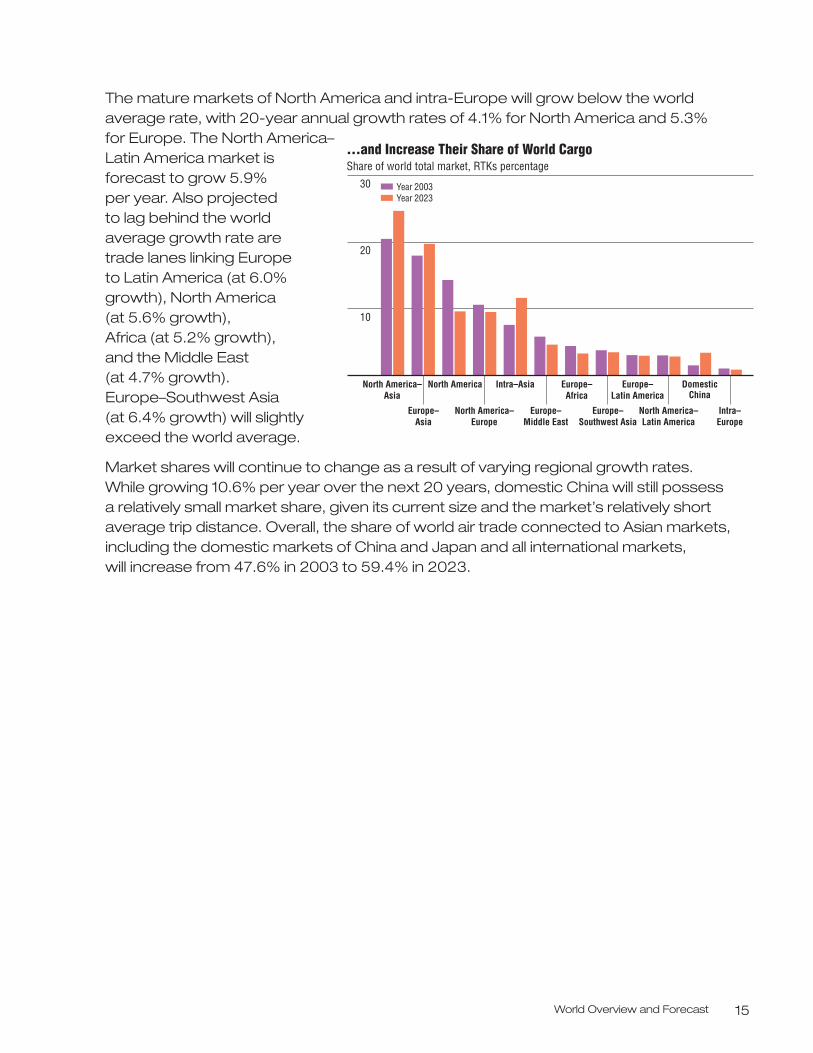

The mature markets of North America and intra-Europe will grow below the worldaverage rate, with 20-year annual growth rates of 4.1% for North America and 5.3% for Europe. The North America–Latin America market isforecast to grow 5.9% per year. Also projected to lag behind the world average growth rate are trade lanes linking Europe to Latin America (at 6.0%growth), North America (at 5.6% growth), Africa (at 5.2% growth), and the Middle East (at 4.7% growth).Europe–Southwest Asia (at 6.4% growth) will slightlyexceed the world average.

Market shares will continue to change as a result of varying regional growth rates. While growing 10.6% per year over the next 20 years, domestic China will still possess a relatively small market share, given its current size and the market’s relatively shortaverage trip distance. Overall, the share of world air trade connected to Asian markets,including the domestic markets of China and Japan and all international markets, will increase from 47.6% in 2003 to 59.4% in 2023.

30

20

10

...and Increase Their Share of World CargoShare of world total market, RTKs percentage

Year 2023Year 2003

North America– Asia

Intra–Asia Europe– Africa

Europe– Latin America

Domestic China

Europe– Asia

North America– Europe

Europe– Southwest Asia

North America– Latin America

Europe–Middle East

Intra– Europe

North America

North America 17

North America

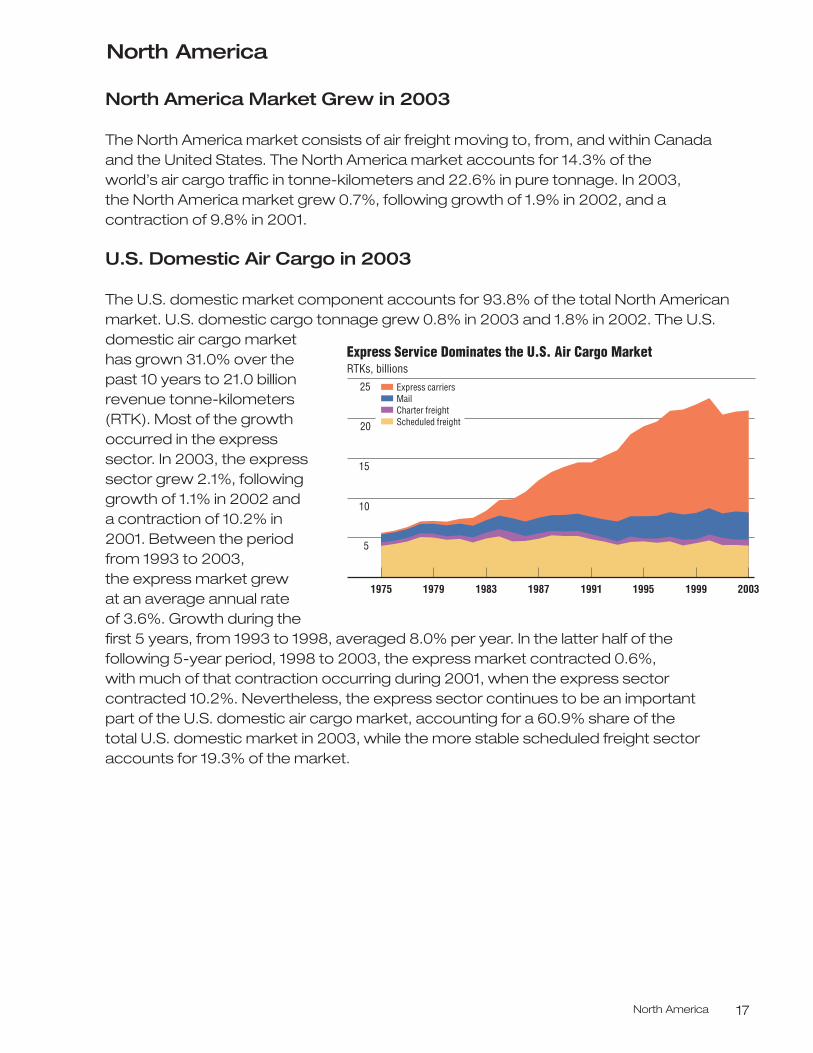

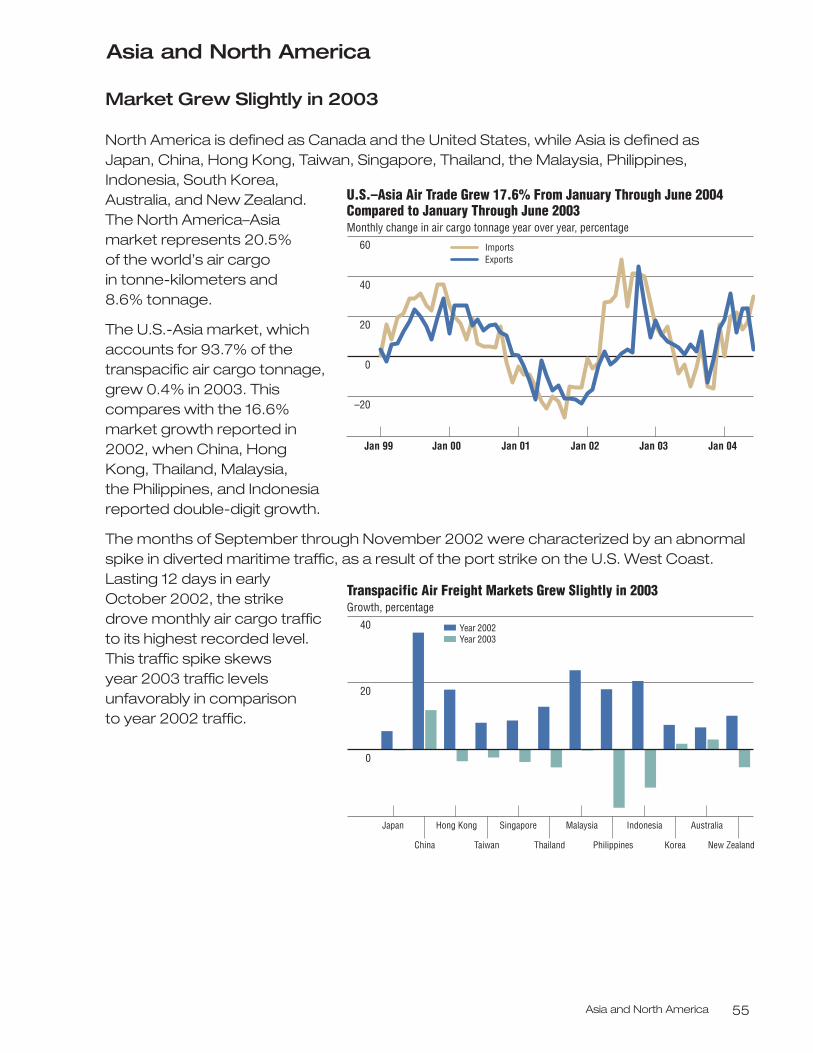

North America Market Grew in 2003

The North America market consists of air freight moving to, from, and within Canada and the United States. The North America market accounts for 14.3% of the world’s air cargo traffic in tonne-kilometers and 22.6% in pure tonnage. In 2003, the North America market grew 0.7%, following growth of 1.9% in 2002, and acontraction of 9.8% in 2001.

U.S. Domestic Air Cargo in 2003

The U.S. domestic market component accounts for 93.8% of the total North Americanmarket. U.S. domestic cargo tonnage grew 0.8% in 2003 and 1.8% in 2002. The U.S.domestic air cargo market has grown 31.0% over thepast 10 years to 21.0 billionrevenue tonne-kilometers(RTK). Most of the growthoccurred in the expresssector. In 2003, the expresssector grew 2.1%, followinggrowth of 1.1% in 2002 and a contraction of 10.2% in2001. Between the periodfrom 1993 to 2003, the express market grew at an average annual rate of 3.6%. Growth during thefirst 5 years, from 1993 to 1998, averaged 8.0% per year. In the latter half of the following 5-year period, 1998 to 2003, the express market contracted 0.6%, with much of that contraction occurring during 2001, when the express sectorcontracted 10.2%. Nevertheless, the express sector continues to be an important part of the U.S. domestic air cargo market, accounting for a 60.9% share of the total U.S. domestic market in 2003, while the more stable scheduled freight sectoraccounts for 19.3% of the market.

1975 1979 1983 1991 1995

5

10

15

20

25

Express Service Dominates the U.S. Air Cargo MarketRTKs, billions

Charter freightMail

Scheduled freight

Express carriers

1987 1999 2003

World Air Cargo Forecast 2004/200518

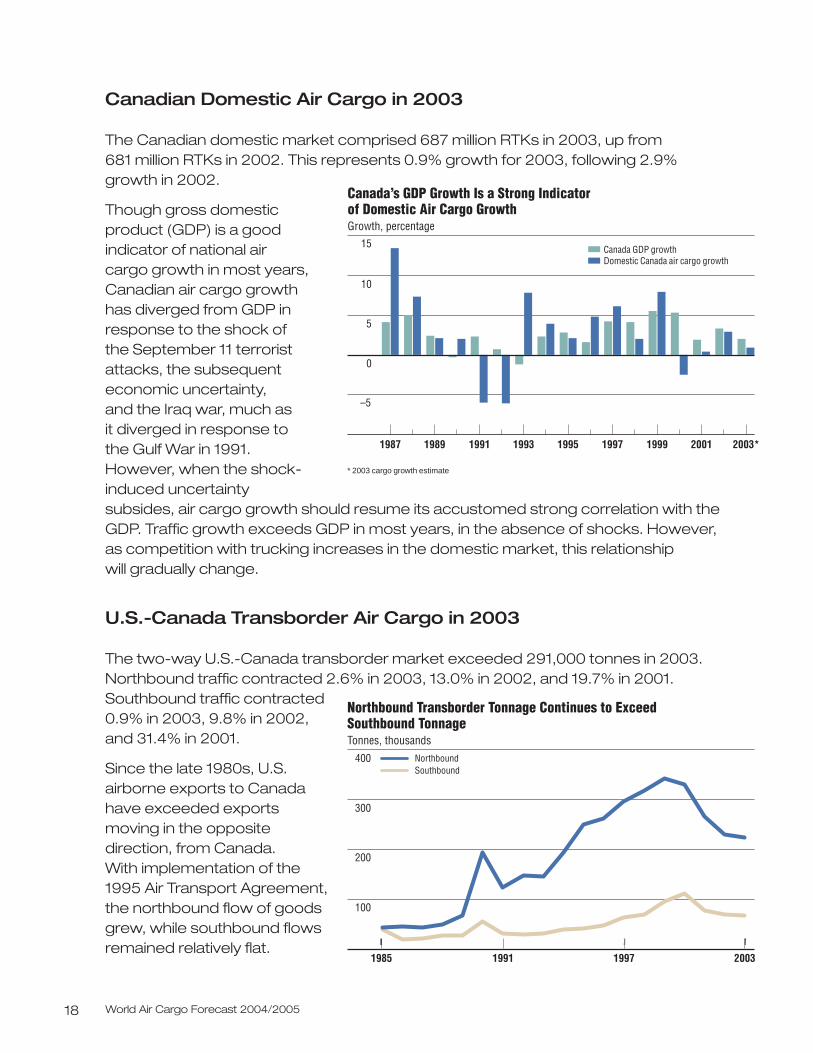

Canadian Domestic Air Cargo in 2003

The Canadian domestic market comprised 687 million RTKs in 2003, up from 681 million RTKs in 2002. This represents 0.9% growth for 2003, following 2.9%growth in 2002.

Though gross domesticproduct (GDP) is a goodindicator of national air cargo growth in most years,Canadian air cargo growth has diverged from GDP inresponse to the shock of the September 11 terroristattacks, the subsequenteconomic uncertainty, and the Iraq war, much asit diverged in response to the Gulf War in 1991.However, when the shock-induced uncertaintysubsides, air cargo growth should resume its accustomed strong correlation with theGDP. Traffic growth exceeds GDP in most years, in the absence of shocks. However, as competition with trucking increases in the domestic market, this relationship will gradually change.

U.S.-Canada Transborder Air Cargo in 2003

The two-way U.S.-Canada transborder market exceeded 291,000 tonnes in 2003.Northbound traffic contracted 2.6% in 2003, 13.0% in 2002, and 19.7% in 2001.Southbound traffic contracted0.9% in 2003, 9.8% in 2002,and 31.4% in 2001.

Since the late 1980s, U.S.airborne exports to Canadahave exceeded exportsmoving in the oppositedirection, from Canada. With implementation of the1995 Air Transport Agreement,the northbound flow of goodsgrew, while southbound flowsremained relatively flat.

–5

0

10

5

15

Canada’s GDP Growth Is a Strong Indicatorof Domestic Air Cargo GrowthGrowth, percentage

Domestic Canada air cargo growthCanada GDP growth

2001 2003*1999199719951993199119891987

* 2003 cargo growth estimate

1985 1991 1997 2003

400

300

200

100

Northbound Transborder Tonnage Continues to Exceed Southbound TonnageTonnes, thousands

NorthboundSouthbound

North America 19

The greatest share of goods moving northbound by air includes computersubassemblies, documents, and motor vehicle parts. Southbound flows are dominated by telecommunication equipment, documents, and crustaceans

Time-Deferred Services

Time-deferred services, which include 2- and 3-day delivery services, include time-definite services beyond those delivery periods. Deferred services, which are lessexpensive than traditional overnight express shipments, appeal to shippers who need to reduce shipping costs but still require time-definite transport. Such lower costofferings often imply lower yields and profits.

The success of air express companies with time-deferred service has attracted othertransportation providers, including combination carriers, combinations of transportationproviders/brokers and less-than-truckload (LTL) shipping companies. Ground-basedlogistics companies offer time-deferred services with similar reliability, yet lower costthan traditional air express carriers

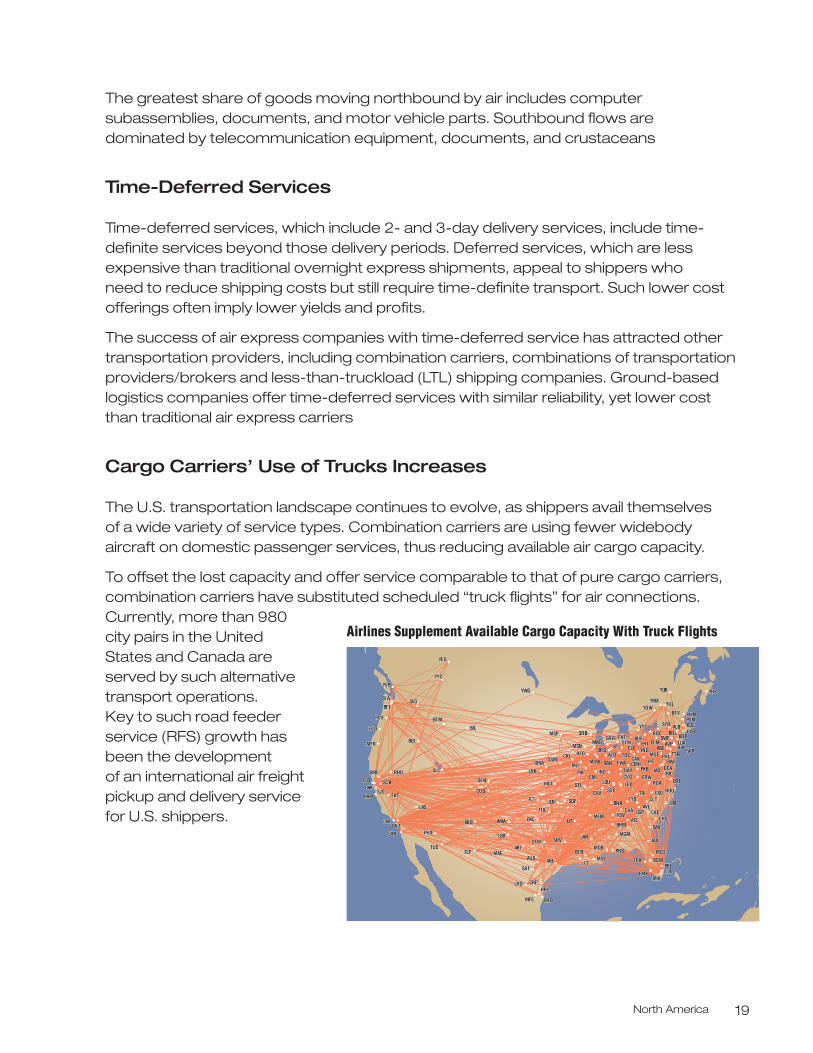

Cargo Carriers’ Use of Trucks Increases

The U.S. transportation landscape continues to evolve, as shippers avail themselves of a wide variety of service types. Combination carriers are using fewer widebodyaircraft on domestic passenger services, thus reducing available air cargo capacity.

To offset the lost capacity and offer service comparable to that of pure cargo carriers,combination carriers have substituted scheduled “truck flights” for air connections.Currently, more than 980city pairs in the UnitedStates and Canada areserved by such alternativetransport operations. Key to such road feederservice (RFS) growth hasbeen the development of an international air freightpickup and delivery servicefor U.S. shippers.

Airlines Supplement Available Cargo Capacity With Truck Flights

ALALBBDBDL BDBDR

BOSBOS

SWSWF

SYSYR

AVAVELELMJFJFKLGALGA

T L

PVPVD

BTBTR

DSDSM

ICTICT

JAJAN

JLJLN

LFLFT

LILIT

LNLNK

MCMCI

MEMEM

MGMGM

MOMOB

MSMSY

OKCOKC

OMOMA

PNPNS

SGFSGF

TULTUL

ABABI

ABABQ AMAMA

AUAUS

BRBRO

COCOS

CRPCRP

DEDEN

DFWDFW

ELPELP

FAFAT

HRLHRL

IAIAH

LASLAS

LAXLAX

LBBLBB

LRLRD

MAMAF

MFMFE

MRMR

OAKOAK

ONONTPHPHX

RNORNO

SASAN

SASAT

SCSCKSFSFO

SHSHV

SJSJC

SLCSLCSMSMF

TUSTUS

ATATL

AVAVL

BHBHM

BNBNA

BOBOW

CACAECHACHA

CHSCHS

CLCLT

FLFLLFMFMY

GSOGSO

GSPGSPHSHSV

ILILM

JAJAX

LELEX

MCOMCO

MIAMIA

PBPBI

RDURDUROROA

SASAV

TPTPA

TRITRITYTYS

ABABEAZAZO

BTBTL

CACAKCIDCIDCLCLE

CMHCMHDADAY

DTWDTW

FWFWAMDMD

MDMDWMLMLI

MSMSN

PIPIA

PIPITPKPKB

RFDRFD

SBSBN

STSTL

TOTOLBWBWI

CMICMI CRWCRWCVCVG

DCADCA

EVEVV

EWEWR

IAIADINDIND

LOULOU ORORF

PHPH

RICRIC

SDSDF

TTTTNYNYNG

P

BTBTV

BUBUFERER

FNTFNTGRGRB

GRGRRMKMKE

MSMSP

PSPSMPWPWM

ROROC

YHYHZ

YMYMXYOYOW

YQBYQB

YUYUL

YYYY

Y

BFBFI

BOBOI

BTBTM

EUEUG

GEGGEG

MFMFR

PDPDX

SESEA

YEYEG

YVYVR

YYYYC

BIBIL

IORORD

YWYWG

Z ALBBDL BDR

BOS

SWF

SYR

AVELMJFKLGA

T L

PVD

BTR

DSM

ICT

JAN

JLN

LFT

LIT

LNK

MCI

MEM

MGM

MOB

MSY

OKC

OMA

PNS

SGF

TUL

ABI

ABQ AMA

AUS

BRO

COS

CRP

DEN

DFW

ELP

FAT

HRL

IAH

LAS

LAX

LBB

LRD

MAF

MFE

MR

OAK

ONTPHX

RNO

SAN

SAT

SCKSFO

SHV

SJC

SLCSMF

TUS

ATL

AVL

BHM

BNA

BOW

CAECHA

CHS

CLT

FLLFMY

GSO

GSPHSV

ILM

JAX

LEX

MCO

MIA

PBI

RDUROA

SAV

TPA

TRITYS

ABEAZO

BTL

CAKCIDCLE

CMHDAY

DTW

FWAMD

MDWMLI

MSN

PIA

PITPKB

RFD

SBN

STL

TOLBWI

CMI CRWCVG

DCA

EVV

EWR

IADIND

LOU ORF

PH

RIC

SDF

TTNYNG

P

BTV

BUFER

FNTGRB

GRRMKE

MSP

PSMPWM

ROC

YHZ

YMXYOW

YQB

YUL

YY

Y

BFI

BOI

BTM

EUG

GEG

MFR

PDX

SEA

YEG

YVR

YYC

BIL

IORD

YWG

Z

World Air Cargo Forecast 2004/200520

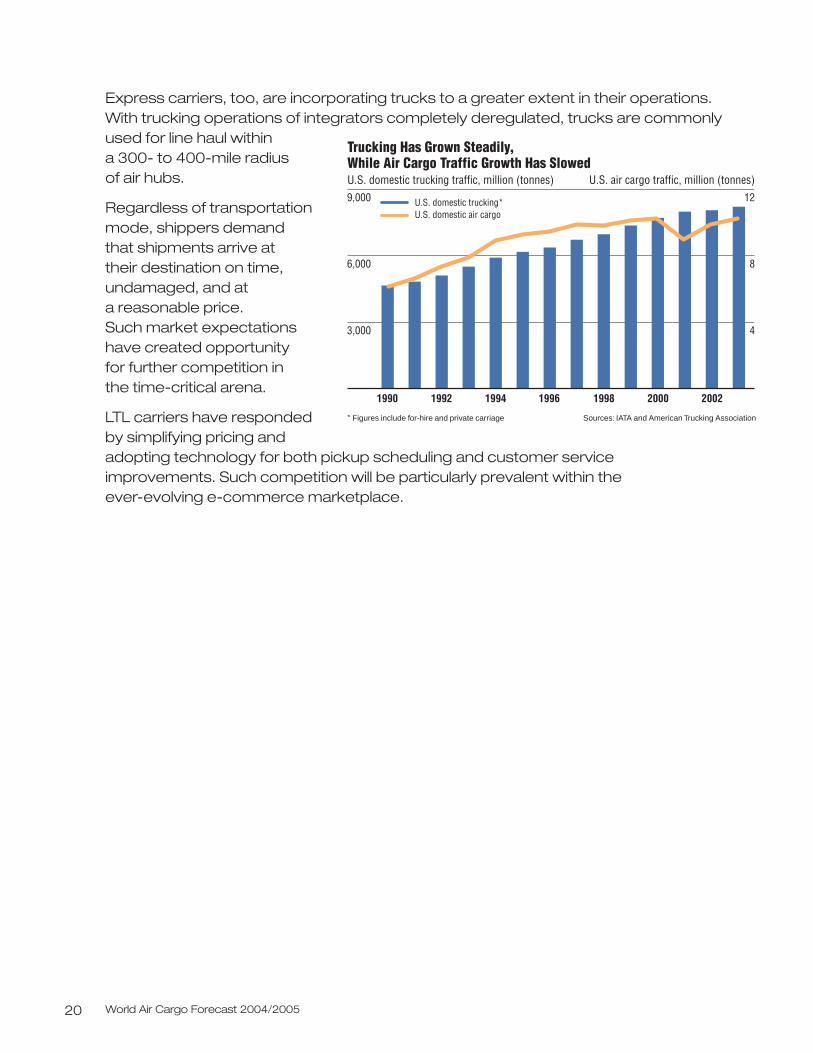

Express carriers, too, are incorporating trucks to a greater extent in their operations.With trucking operations of integrators completely deregulated, trucks are commonly used for line haul within a 300- to 400-mile radius of air hubs.

Regardless of transportationmode, shippers demand that shipments arrive at their destination on time,undamaged, and at a reasonable price. Such market expectationshave created opportunity for further competition in the time-critical arena.

LTL carriers have respondedby simplifying pricing andadopting technology for both pickup scheduling and customer serviceimprovements. Such competition will be particularly prevalent within the ever-evolving e-commerce marketplace.

Trucking Has Grown Steadily, While Air Cargo Traffic Growth Has SlowedU.S. domestic trucking traffic, million (tonnes)9,000

6,000

3,000

12

8

4

1990 1992 1994 1996 1998 2000 2002

U.S. domestic trucking*U.S. domestic air cargo

U.S. air cargo traffic, million (tonnes)

* Figures include for-hire and private carriage Sources: IATA and American Trucking Association

North America 21

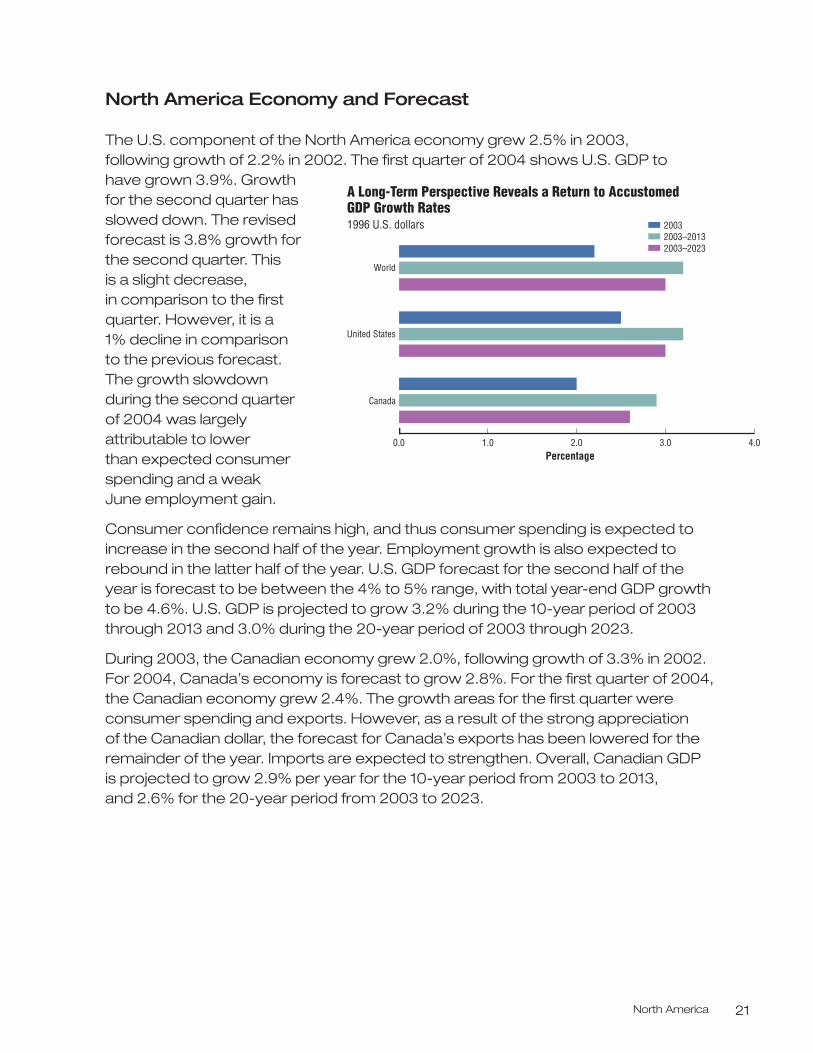

North America Economy and Forecast

The U.S. component of the North America economy grew 2.5% in 2003, following growth of 2.2% in 2002. The first quarter of 2004 shows U.S. GDP to have grown 3.9%. Growth for the second quarter hasslowed down. The revisedforecast is 3.8% growth for the second quarter. This is a slight decrease, in comparison to the firstquarter. However, it is a 1% decline in comparison to the previous forecast. The growth slowdown during the second quarter of 2004 was largelyattributable to lowerthan expected consumerspending and a weak June employment gain.

Consumer confidence remains high, and thus consumer spending is expected toincrease in the second half of the year. Employment growth is also expected to rebound in the latter half of the year. U.S. GDP forecast for the second half of the year is forecast to be between the 4% to 5% range, with total year-end GDP growth to be 4.6%. U.S. GDP is projected to grow 3.2% during the 10-year period of 2003 through 2013 and 3.0% during the 20-year period of 2003 through 2023.

During 2003, the Canadian economy grew 2.0%, following growth of 3.3% in 2002. For 2004, Canada’s economy is forecast to grow 2.8%. For the first quarter of 2004, the Canadian economy grew 2.4%. The growth areas for the first quarter wereconsumer spending and exports. However, as a result of the strong appreciation of the Canadian dollar, the forecast for Canada’s exports has been lowered for theremainder of the year. Imports are expected to strengthen. Overall, Canadian GDP is projected to grow 2.9% per year for the 10-year period from 2003 to 2013,and 2.6% for the 20-year period from 2003 to 2023.

0.0 1.0 2.0 3.0 4.0

Canada

United States

World

A Long-Term Perspective Reveals a Return to Accustomed GDP Growth Rates1996 U.S. dollars

2003–20232003–20132003

Percentage

World Air Cargo Forecast 2004/200522

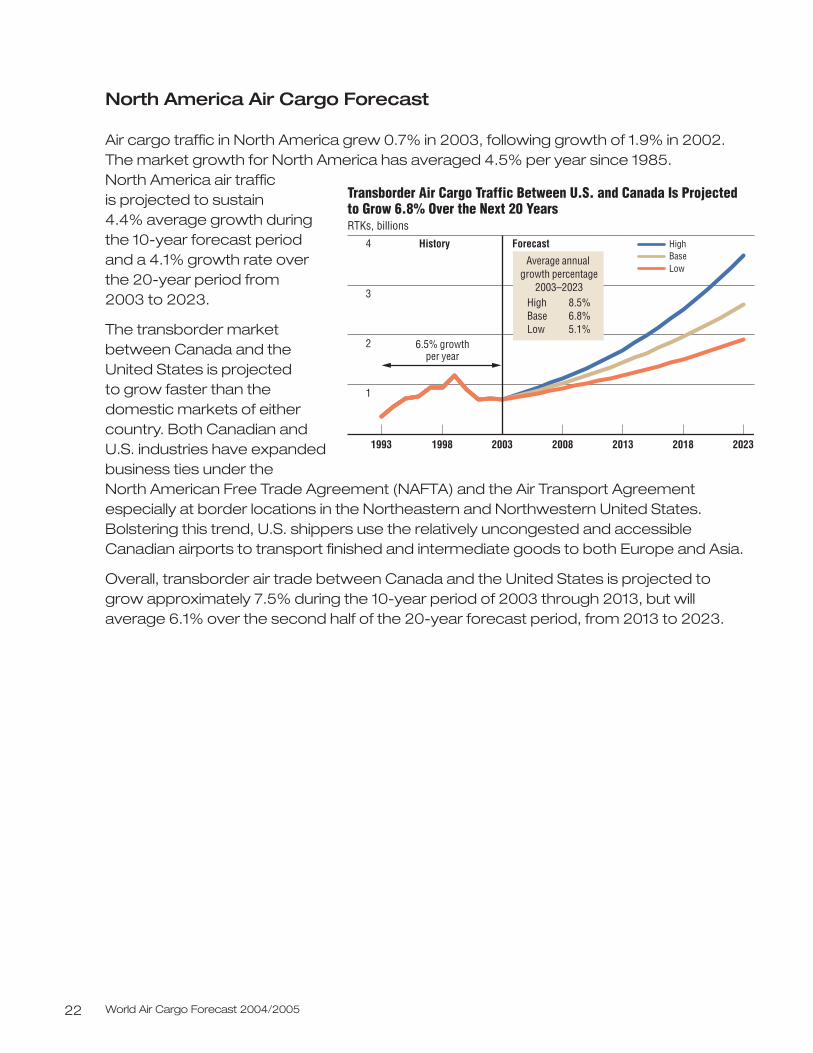

North America Air Cargo Forecast

Air cargo traffic in North America grew 0.7% in 2003, following growth of 1.9% in 2002.The market growth for North America has averaged 4.5% per year since 1985. North America air traffic is projected to sustain 4.4% average growth during the 10-year forecast period and a 4.1% growth rate overthe 20-year period from 2003 to 2023.

The transborder marketbetween Canada and theUnited States is projected to grow faster than thedomestic markets of eithercountry. Both Canadian andU.S. industries have expandedbusiness ties under the North American Free Trade Agreement (NAFTA) and the Air Transport Agreementespecially at border locations in the Northeastern and Northwestern United States.Bolstering this trend, U.S. shippers use the relatively uncongested and accessibleCanadian airports to transport finished and intermediate goods to both Europe and Asia.

Overall, transborder air trade between Canada and the United States is projected togrow approximately 7.5% during the 10-year period of 2003 through 2013, but will average 6.1% over the second half of the 20-year forecast period, from 2013 to 2023.

2013

Transborder Air Cargo Traffic Between U.S. and Canada Is Projected to Grow 6.8% Over the Next 20 YearsRTKs, billions

4

3

2

1

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 8.5%Base 6.8%Low 5.1%

6.5% growthper year

1998

North America 23

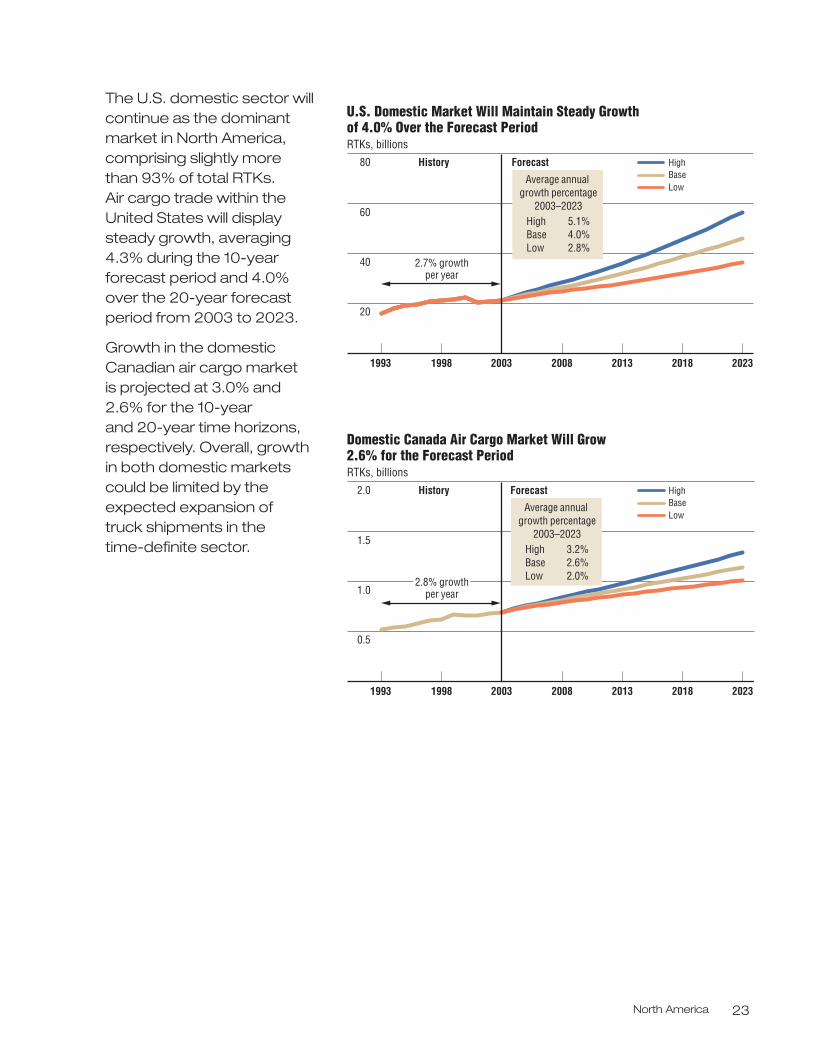

The U.S. domestic sector willcontinue as the dominantmarket in North America,comprising slightly more than 93% of total RTKs. Air cargo trade within theUnited States will displaysteady growth, averaging4.3% during the 10-yearforecast period and 4.0%over the 20-year forecastperiod from 2003 to 2023.

Growth in the domesticCanadian air cargo market is projected at 3.0% and 2.6% for the 10-year and 20-year time horizons,respectively. Overall, growthin both domestic marketscould be limited by theexpected expansion of truck shipments in the time-definite sector.

2013

U.S. Domestic Market Will Maintain Steady Growth of 4.0% Over the Forecast PeriodRTKs, billions

80

60

40

20

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 5.1%Base 4.0%Low 2.8%

2.7% growthper year

1998

2013

Domestic Canada Air Cargo Market Will Grow 2.6% for the Forecast Period RTKs, billions

2.0

1.5

1.0

0.5

20232018200820031993

HighBaseLow

History Forecast

Average annual growth percentage

2003–2023High 3.2%Base 2.6%Low 2.0%2.8% growth

per year

1998

Latin America and North America 25

Latin America and North America

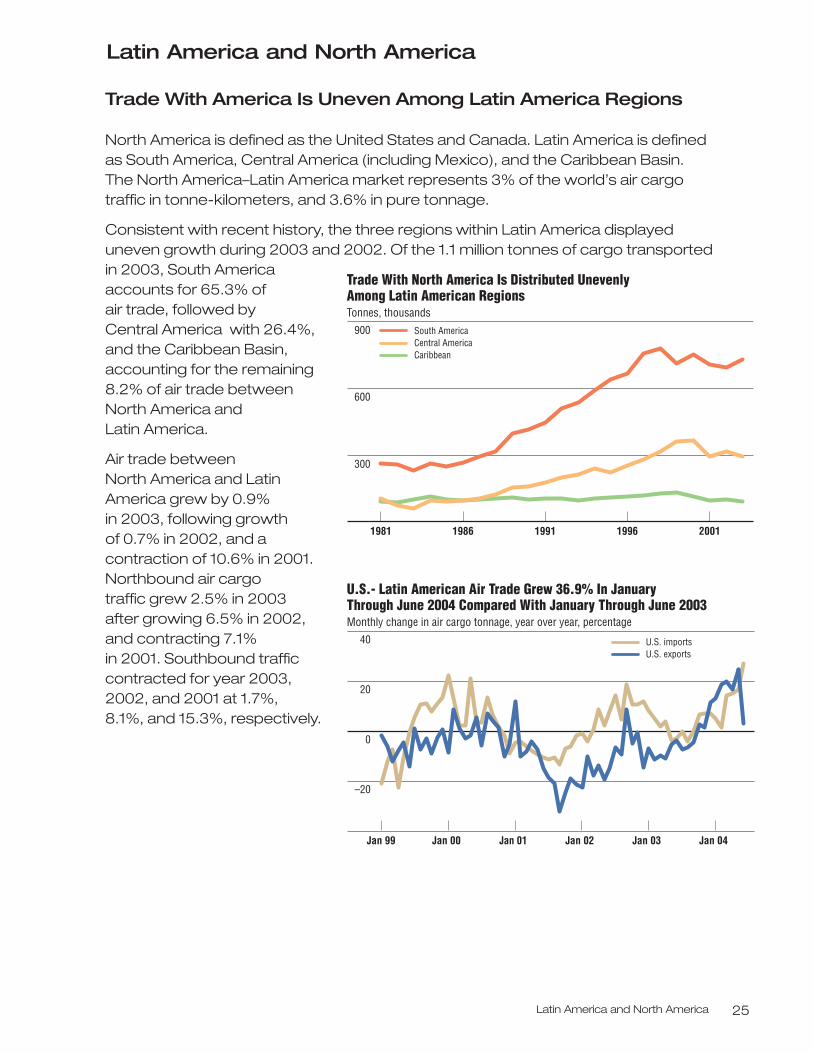

Trade With America Is Uneven Among Latin America Regions

North America is defined as the United States and Canada. Latin America is defined as South America, Central America (including Mexico), and the Caribbean Basin. The North America–Latin America market represents 3% of the world’s air cargotraffic in tonne-kilometers, and 3.6% in pure tonnage.

Consistent with recent history, the three regions within Latin America displayeduneven growth during 2003 and 2002. Of the 1.1 million tonnes of cargo transportedin 2003, South Americaaccounts for 65.3% of air trade, followed by Central America with 26.4%,and the Caribbean Basin, accounting for the remaining8.2% of air trade between North America and Latin America.

Air trade between North America and LatinAmerica grew by 0.9% in 2003, following growth of 0.7% in 2002, and a contraction of 10.6% in 2001.Northbound air cargo traffic grew 2.5% in 2003after growing 6.5% in 2002, and contracting 7.1% in 2001. Southbound trafficcontracted for year 2003,2002, and 2001 at 1.7%, 8.1%, and 15.3%, respectively.

Trade With North America Is Distributed Unevenly Among Latin American RegionsTonnes, thousands

900

600

300

1981 19911986 1996 2001

South AmericaCentral AmericaCaribbean

U.S.- Latin American Air Trade Grew 36.9% In January Through June 2004 Compared With January Through June 2003Monthly change in air cargo tonnage, year over year, percentage

40

20

0

–20

Jan 99 Jan 00 Jan 02 Jan 03

U.S. importsU.S. exports

Jan 01 Jan 04

World Air Cargo Forecast 2004/200526

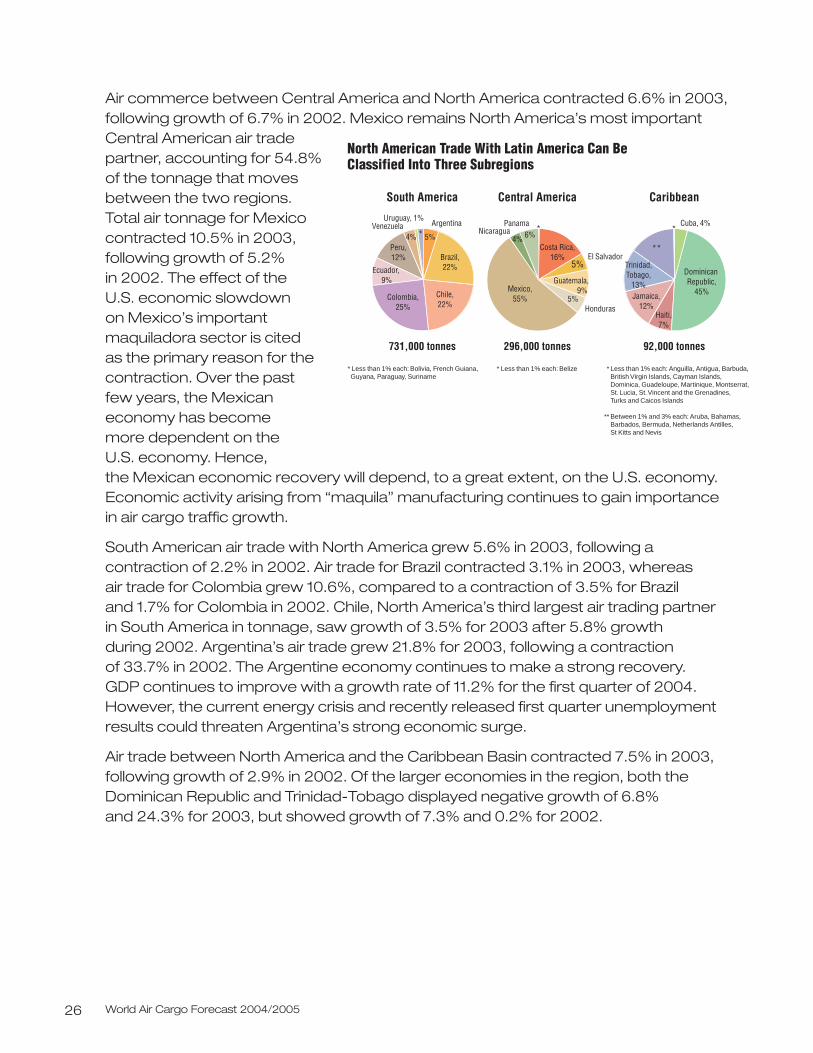

Air commerce between Central America and North America contracted 6.6% in 2003,following growth of 6.7% in 2002. Mexico remains North America’s most importantCentral American air tradepartner, accounting for 54.8%of the tonnage that movesbetween the two regions. Total air tonnage for Mexicocontracted 10.5% in 2003,following growth of 5.2% in 2002. The effect of the U.S. economic slowdown on Mexico’s importantmaquiladora sector is cited as the primary reason for thecontraction. Over the past few years, the Mexicaneconomy has become more dependent on the U.S. economy. Hence, the Mexican economic recovery will depend, to a great extent, on the U.S. economy.Economic activity arising from “maquila” manufacturing continues to gain importancein air cargo traffic growth.

South American air trade with North America grew 5.6% in 2003, following acontraction of 2.2% in 2002. Air trade for Brazil contracted 3.1% in 2003, whereas air trade for Colombia grew 10.6%, compared to a contraction of 3.5% for Brazil and 1.7% for Colombia in 2002. Chile, North America’s third largest air trading partnerin South America in tonnage, saw growth of 3.5% for 2003 after 5.8% growth during 2002. Argentina’s air trade grew 21.8% for 2003, following a contraction of 33.7% in 2002. The Argentine economy continues to make a strong recovery. GDP continues to improve with a growth rate of 11.2% for the first quarter of 2004.However, the current energy crisis and recently released first quarter unemploymentresults could threaten Argentina’s strong economic surge.

Air trade between North America and the Caribbean Basin contracted 7.5% in 2003,following growth of 2.9% in 2002. Of the larger economies in the region, both theDominican Republic and Trinidad-Tobago displayed negative growth of 6.8% and 24.3% for 2003, but showed growth of 7.3% and 0.2% for 2002.

North American Trade With Latin America Can Be Classified Into Three Subregions

92,000 tonnes

Caribbean

296,000 tonnes

Central America

731,000 tonnes

South America

* Less than 1% each: Bolivia, French Guiana, Guyana, Paraguay, Suriname

* Less than 1% each: Belize *

**

Less than 1% each: Anguilla, Antigua, Barbuda, British Virgin Islands, Cayman Islands, Dominica, Guadeloupe, Martinique, Montserrat, St. Lucia, St. Vincent and the Grenadines, Turks and Caicos Islands

Between 1% and 3% each: Aruba, Bahamas, Barbados, Bermuda, Netherlands Antilles, St Kitts and Nevis

Jamaica,12%

Trinidad,Tobago,

13%

ArgentinaUruguay, 1%

Venezuela

Brazil,22%

Chile,22%

Colombia,25%

Ecuador, 9%

Peru,12%

Mexico,55%

El Salvador

Guatemala, 9%

Honduras

NicaraguaPanama

Haiti,7%

*

**

**Cuba, 4%

Dominican Republic,

45%

5%

5%

4% 6%5%4%Costa Rica,

16%

Latin America and North America 27

Air Trade Commodities

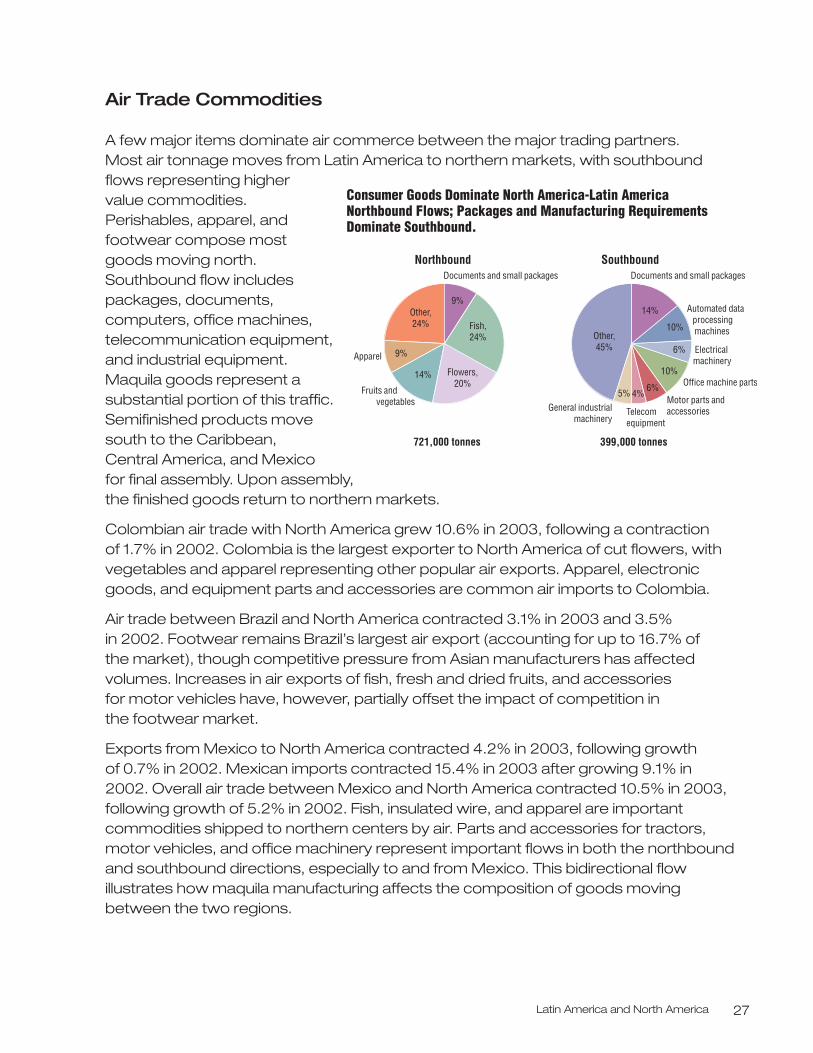

A few major items dominate air commerce between the major trading partners. Most air tonnage moves from Latin America to northern markets, with southboundflows representing higher value commodities.Perishables, apparel, andfootwear compose mostgoods moving north.Southbound flow includespackages, documents,computers, office machines,telecommunication equipment,and industrial equipment.Maquila goods represent asubstantial portion of this traffic.Semifinished products movesouth to the Caribbean, Central America, and Mexicofor final assembly. Upon assembly, the finished goods return to northern markets.

Colombian air trade with North America grew 10.6% in 2003, following a contraction of 1.7% in 2002. Colombia is the largest exporter to North America of cut flowers, withvegetables and apparel representing other popular air exports. Apparel, electronicgoods, and equipment parts and accessories are common air imports to Colombia.

Air trade between Brazil and North America contracted 3.1% in 2003 and 3.5% in 2002. Footwear remains Brazil’s largest air export (accounting for up to 16.7% of the market), though competitive pressure from Asian manufacturers has affectedvolumes. Increases in air exports of fish, fresh and dried fruits, and accessories for motor vehicles have, however, partially offset the impact of competition in the footwear market.

Exports from Mexico to North America contracted 4.2% in 2003, following growth of 0.7% in 2002. Mexican imports contracted 15.4% in 2003 after growing 9.1% in2002. Overall air trade between Mexico and North America contracted 10.5% in 2003,following growth of 5.2% in 2002. Fish, insulated wire, and apparel are importantcommodities shipped to northern centers by air. Parts and accessories for tractors,motor vehicles, and office machinery represent important flows in both the northboundand southbound directions, especially to and from Mexico. This bidirectional flowillustrates how maquila manufacturing affects the composition of goods movingbetween the two regions.

Apparel

Telecomequipment

Automated data processing machines

Electrical machinery

Office machine parts

Motor parts and accessories

Fruits and vegetables

Consumer Goods Dominate North America-Latin America Northbound Flows; Packages and Manufacturing Requirements Dominate Southbound.

Northbound

399,000 tonnes

SouthboundDocuments and small packages Documents and small packages

General industrialmachinery

9%Other,24% Fish,

24%

Flowers,20%

14%

9%

14%

10%

6%

10%

6%4%5%

Other,45%

721,000 tonnes

World Air Cargo Forecast 2004/200528

Air commerce between the Caribbean Basin and North America contracted 7.5% in2003 after growing 2.9% in 2002. Apparel, fresh and dried fruits, and fish are importantcommodities that are transported northbound. Small packages, dairy products, officemachinery, and electrical apparatus represent flows in the southbound direction.

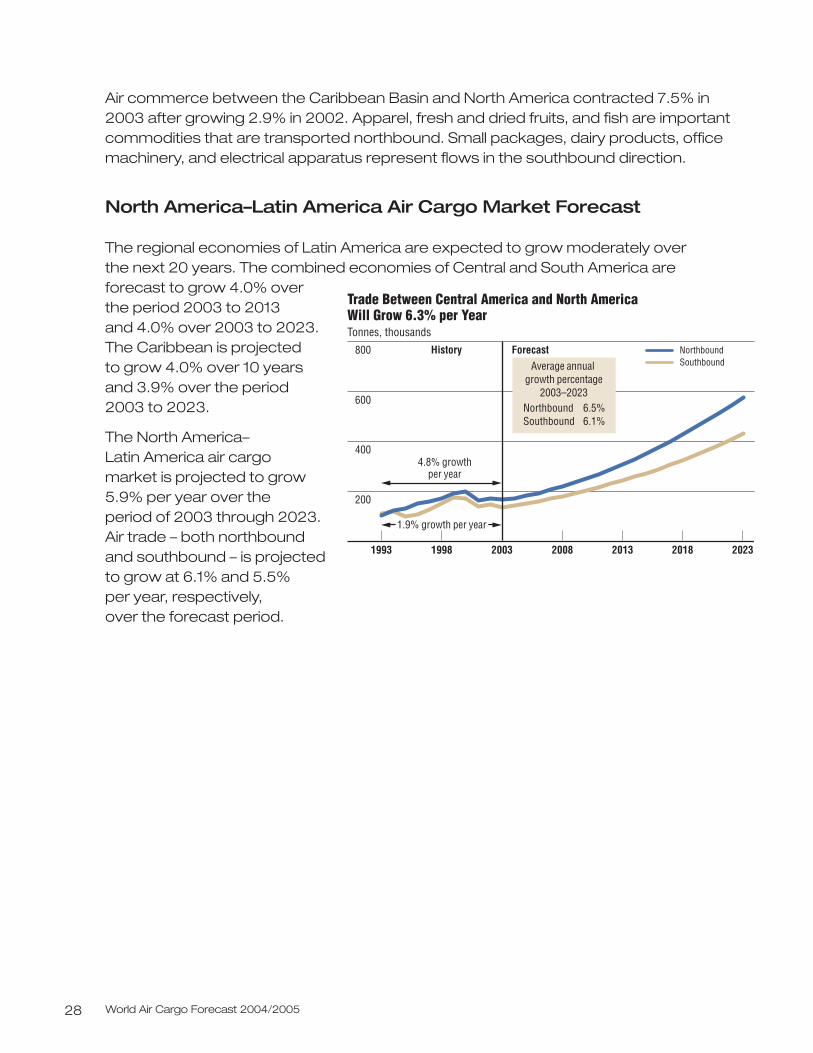

North America–Latin America Air Cargo Market Forecast

The regional economies of Latin America are expected to grow moderately over the next 20 years. The combined economies of Central and South America are forecast to grow 4.0% over the period 2003 to 2013 and 4.0% over 2003 to 2023. The Caribbean is projected to grow 4.0% over 10 yearsand 3.9% over the period 2003 to 2023.

The North America–Latin America air cargo market is projected to grow5.9% per year over the period of 2003 through 2023. Air trade – both northboundand southbound – is projectedto grow at 6.1% and 5.5% per year, respectively, over the forecast period.

1993 1998 2003 2008 2013 2018

800

600

400

200

Trade Between Central America and North AmericaWill Grow 6.3% per YearTonnes, thousands

NorthboundSouthbound

2023

Average annual growth percentage

2003–2023Northbound 6.5%Southbound 6.1%

History Forecast

4.8% growthper year

1.9% growth per year

Latin America and North America 29

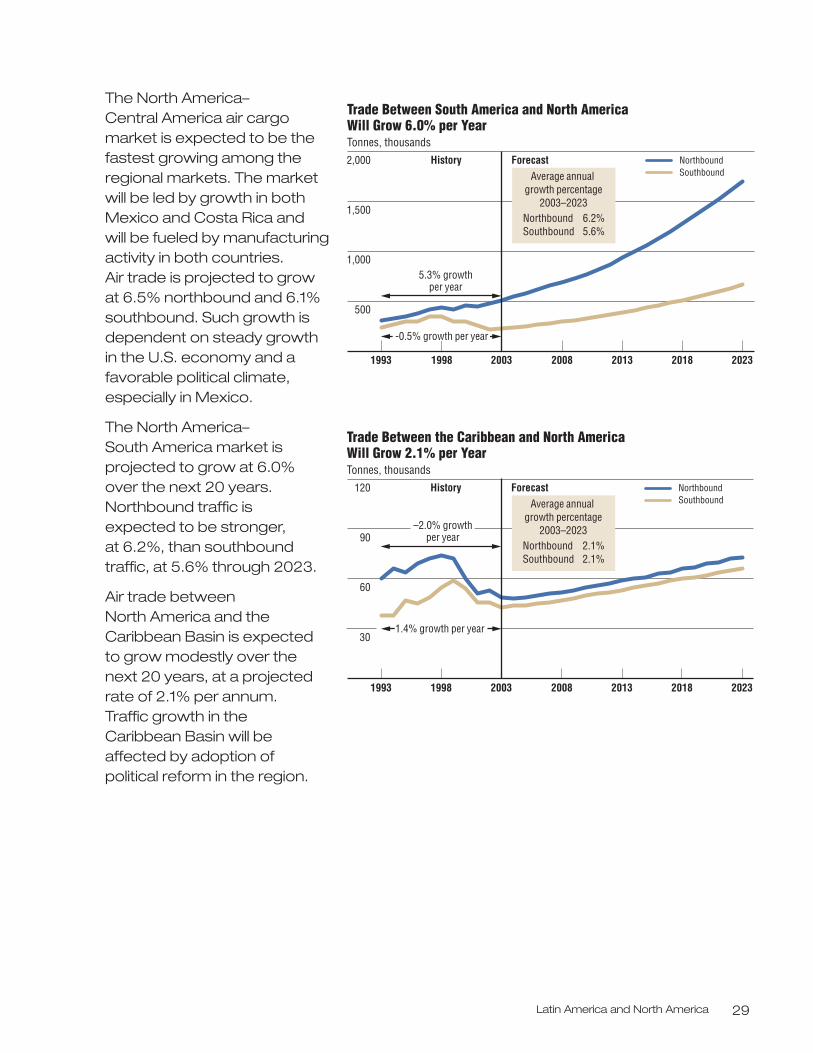

The North America–Central America air cargomarket is expected to be thefastest growing among theregional markets. The marketwill be led by growth in bothMexico and Costa Rica and will be fueled by manufacturingactivity in both countries. Air trade is projected to growat 6.5% northbound and 6.1%southbound. Such growth isdependent on steady growthin the U.S. economy and afavorable political climate,especially in Mexico.

The North America–South America market isprojected to grow at 6.0%over the next 20 years.Northbound traffic is expected to be stronger, at 6.2%, than southboundtraffic, at 5.6% through 2023.

Air trade between North America and theCaribbean Basin is expectedto grow modestly over thenext 20 years, at a projectedrate of 2.1% per annum. Traffic growth in the Caribbean Basin will be affected by adoption of political reform in the region.

1993 1998 2003 2008 2013 2018 2023

2,000

1,500

1,000

500

Trade Between South America and North AmericaWill Grow 6.0% per YearTonnes, thousands

NorthboundSouthboundAverage annual

growth percentage2003–2023

Northbound 6.2%Southbound 5.6%

History Forecast

5.3% growthper year

-0.5% growth per year

1993 1998 2003 2008 2013 2018 2023

120

90

60

30

Trade Between the Caribbean and North AmericaWill Grow 2.1% per YearTonnes, thousands

NorthboundSouthboundAverage annual

growth percentage2003–2023

Northbound 2.1%Southbound 2.1%

History Forecast

–2.0% growthper year

1.4% growth per year

Europe and North America 31

Europe and North America

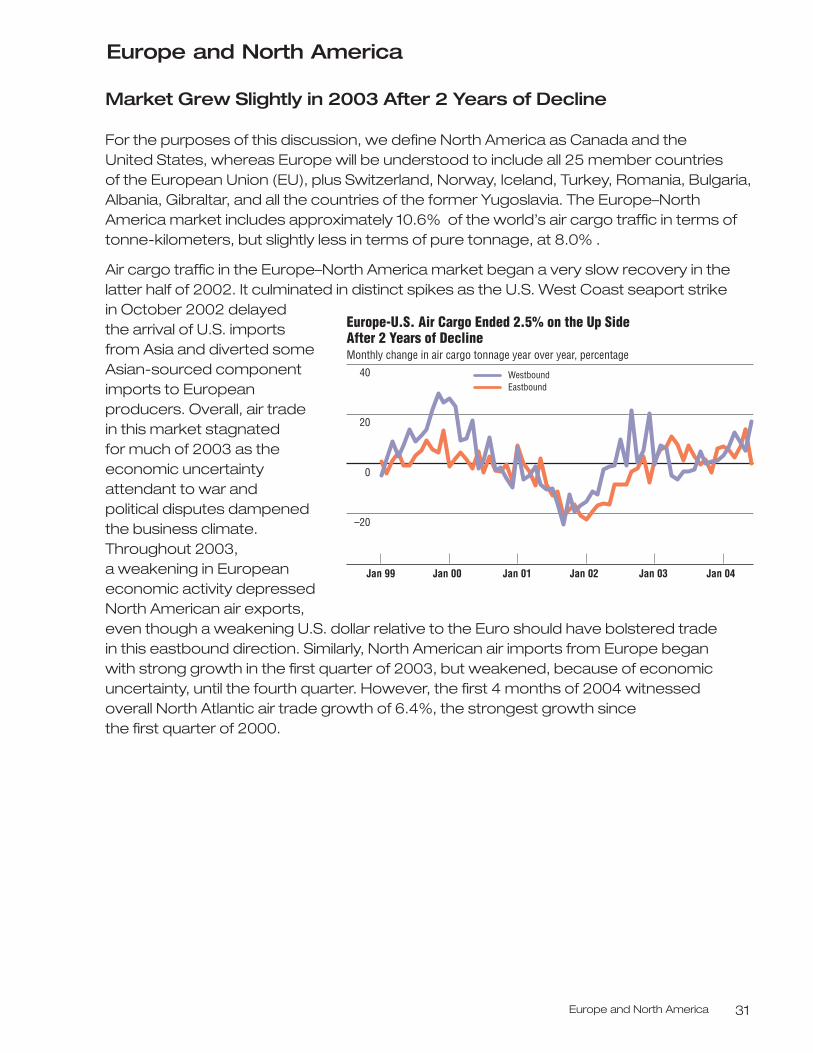

Market Grew Slightly in 2003 After 2 Years of Decline

For the purposes of this discussion, we define North America as Canada and the United States, whereas Europe will be understood to include all 25 member countries of the European Union (EU), plus Switzerland, Norway, Iceland, Turkey, Romania, Bulgaria,Albania, Gibraltar, and all the countries of the former Yugoslavia. The Europe–NorthAmerica market includes approximately 10.6% of the world’s air cargo traffic in terms oftonne-kilometers, but slightly less in terms of pure tonnage, at 8.0% .

Air cargo traffic in the Europe–North America market began a very slow recovery in thelatter half of 2002. It culminated in distinct spikes as the U.S. West Coast seaport strike in October 2002 delayed the arrival of U.S. imports from Asia and diverted some Asian-sourced componentimports to Europeanproducers. Overall, air trade in this market stagnated for much of 2003 as theeconomic uncertaintyattendant to war and political disputes dampenedthe business climate.Throughout 2003, a weakening in Europeaneconomic activity depressedNorth American air exports,even though a weakening U.S. dollar relative to the Euro should have bolstered trade in this eastbound direction. Similarly, North American air imports from Europe began with strong growth in the first quarter of 2003, but weakened, because of economicuncertainty, until the fourth quarter. However, the first 4 months of 2004 witnessed overall North Atlantic air trade growth of 6.4%, the strongest growth since the first quarter of 2000.

Europe-U.S. Air Cargo Ended 2.5% on the Up Side After 2 Years of Decline Monthly change in air cargo tonnage year over year, percentage

40

20

0

–20

WestboundEastbound

Jan 99 Jan 00 Jan 02 Jan 03 Jan 04Jan 01

World Air Cargo Forecast 2004/200532

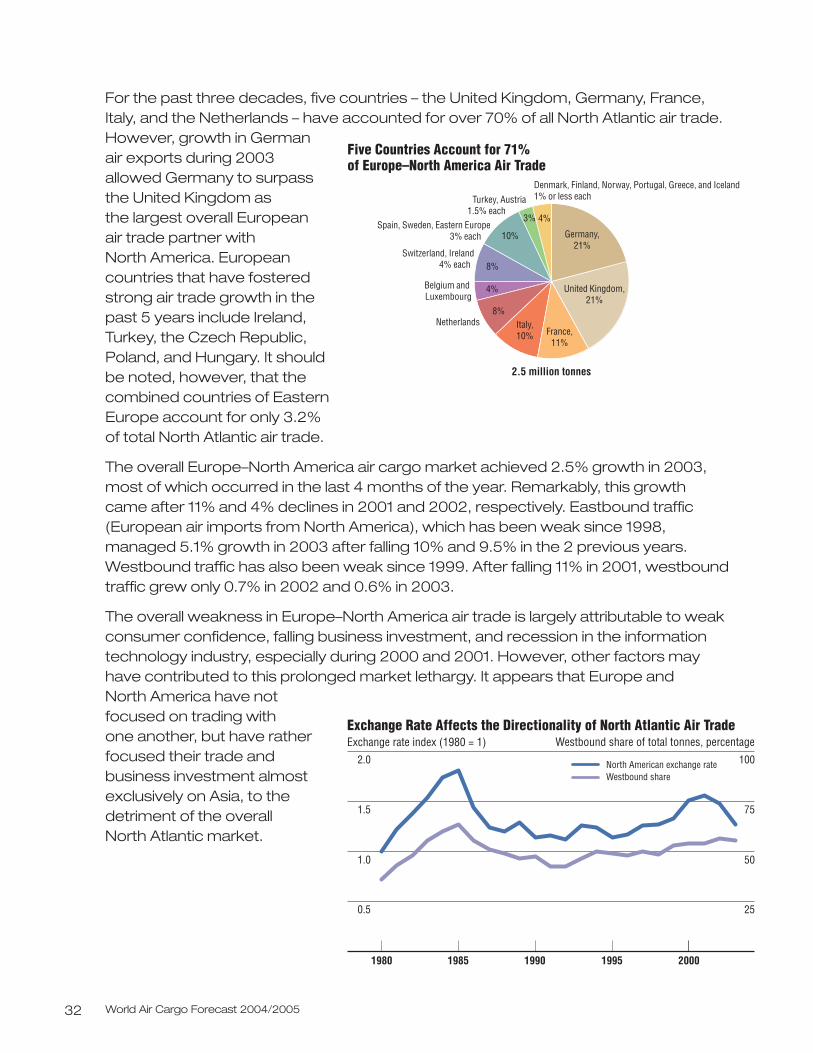

For the past three decades, five countries – the United Kingdom, Germany, France,Italy, and the Netherlands – have accounted for over 70% of all North Atlantic air trade.However, growth in German air exports during 2003allowed Germany to surpassthe United Kingdom as the largest overall European air trade partner with North America. Europeancountries that have fosteredstrong air trade growth in thepast 5 years include Ireland,Turkey, the Czech Republic,Poland, and Hungary. It shouldbe noted, however, that thecombined countries of EasternEurope account for only 3.2% of total North Atlantic air trade.

The overall Europe–North America air cargo market achieved 2.5% growth in 2003,most of which occurred in the last 4 months of the year. Remarkably, this growth came after 11% and 4% declines in 2001 and 2002, respectively. Eastbound traffic (European air imports from North America), which has been weak since 1998,managed 5.1% growth in 2003 after falling 10% and 9.5% in the 2 previous years.Westbound traffic has also been weak since 1999. After falling 11% in 2001, westboundtraffic grew only 0.7% in 2002 and 0.6% in 2003.

The overall weakness in Europe–North America air trade is largely attributable to weakconsumer confidence, falling business investment, and recession in the informationtechnology industry, especially during 2000 and 2001. However, other factors mayhave contributed to this prolonged market lethargy. It appears that Europe and North America have notfocused on trading with one another, but have ratherfocused their trade andbusiness investment almostexclusively on Asia, to thedetriment of the overall North Atlantic market.

2.5 million tonnes

Netherlands

Five Countries Account for 71% of Europe–North America Air Trade

Switzerland, Ireland 4% each

Belgium and Luxembourg

Denmark, Finland, Norway, Portugal, Greece, and Iceland 1% or less eachTurkey, Austria

1.5% each

4%

8%

10%

3% 4%

8%Italy,10% France,

11%

Germany,21%

United Kingdom,21%

Spain, Sweden, Eastern Europe 3% each

Exchange Rate Affects the Directionality of North Atlantic Air TradeExchange rate index (1980 = 1)

2.0

1.5

1.0

0.5

100

75

50

25

1980 2000

North American exchange rateWestbound share

Westbound share of total tonnes, percentage

1990 19951985

Europe and North America 33

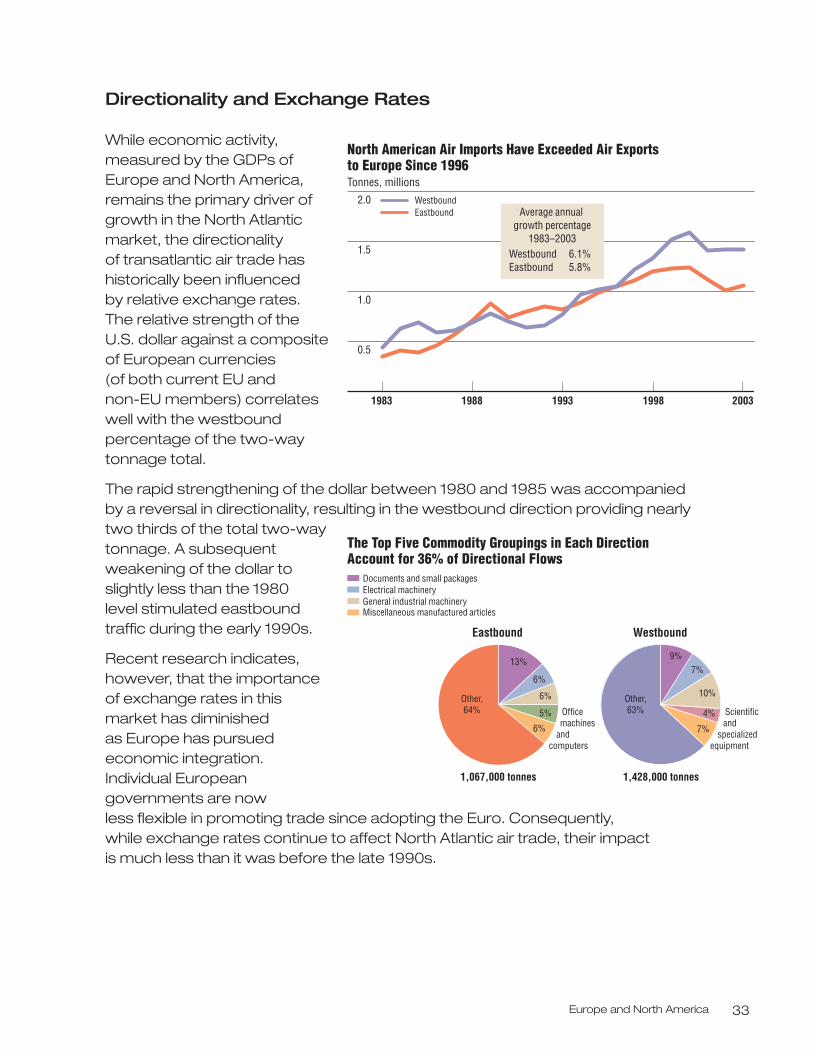

Directionality and Exchange Rates

While economic activity,measured by the GDPs ofEurope and North America,remains the primary driver ofgrowth in the North Atlanticmarket, the directionality of transatlantic air trade hashistorically been influenced by relative exchange rates.The relative strength of theU.S. dollar against a compositeof European currencies (of both current EU and non-EU members) correlateswell with the westboundpercentage of the two-waytonnage total.

The rapid strengthening of the dollar between 1980 and 1985 was accompaniedby a reversal in directionality, resulting in the westbound direction providing nearly two thirds of the total two-waytonnage. A subsequentweakening of the dollar toslightly less than the 1980 level stimulated eastboundtraffic during the early 1990s.

Recent research indicates,however, that the importanceof exchange rates in thismarket has diminished as Europe has pursued economic integration.Individual Europeangovernments are now less flexible in promoting trade since adopting the Euro. Consequently, while exchange rates continue to affect North Atlantic air trade, their impact is much less than it was before the late 1990s.

North American Air Imports Have Exceeded Air Exports to Europe Since 1996Tonnes, millions

2.0

1.5

1.0

0.5

1983 1993 1998 2003

WestboundEastbound

1988

Average annual growth percentage

1983–2003Westbound 6.1%Eastbound 5.8%

1,067,000 tonnes

Scientific and specialized equipment

Office machines and computers

The Top Five Commodity Groupings in Each Direction Account for 36% of Directional Flows

Eastbound

1,428,000 tonnes

Westbound

13%

Other,64%

6%

6%

5%

6%

9%

Other,63%

7%

10%

4%

7%

Miscellaneous manufactured articlesGeneral industrial machineryElectrical machineryDocuments and small packages

World Air Cargo Forecast 2004/200534

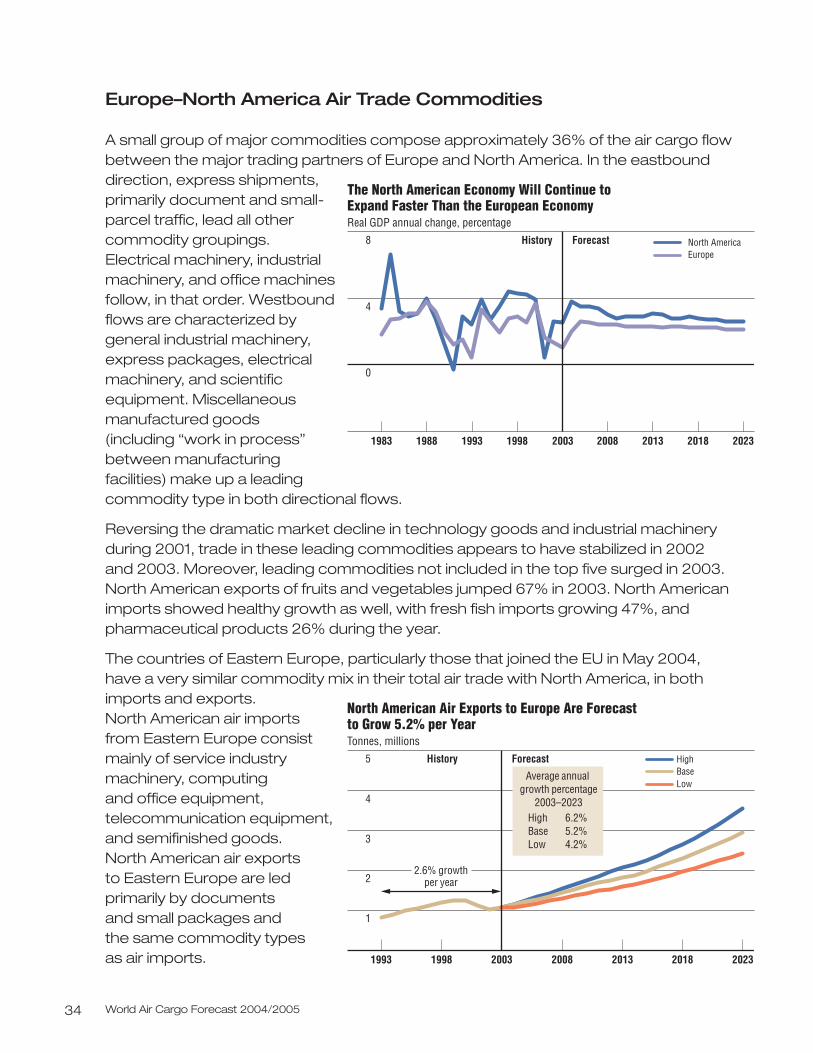

Europe–North America Air Trade Commodities

A small group of major commodities compose approximately 36% of the air cargo flowbetween the major trading partners of Europe and North America. In the eastbounddirection, express shipments, primarily document and small-parcel traffic, lead all othercommodity groupings.Electrical machinery, industrialmachinery, and office machinesfollow, in that order. Westboundflows are characterized bygeneral industrial machinery,express packages, electricalmachinery, and scientificequipment. Miscellaneousmanufactured goods (including “work in process”between manufacturingfacilities) make up a leading commodity type in both directional flows.

Reversing the dramatic market decline in technology goods and industrial machineryduring 2001, trade in these leading commodities appears to have stabilized in 2002and 2003. Moreover, leading commodities not included in the top five surged in 2003.North American exports of fruits and vegetables jumped 67% in 2003. North Americanimports showed healthy growth as well, with fresh fish imports growing 47%, andpharmaceutical products 26% during the year.

The countries of Eastern Europe, particularly those that joined the EU in May 2004,have a very similar commodity mix in their total air trade with North America, in bothimports and exports. North American air importsfrom Eastern Europe consistmainly of service industrymachinery, computing and office equipment,telecommunication equipment,and semifinished goods. North American air exports to Eastern Europe are ledprimarily by documents and small packages and the same commodity types as air imports.

The North American Economy Will Continue to Expand Faster Than the European EconomyReal GDP annual change, percentage

8

4

0

History Forecast

1983 1988 1993 1998 2003 2008 2013 2018 2023

North AmericaEurope

North American Air Exports to Europe Are Forecast to Grow 5.2% per YearTonnes, millions

5

4

3

2

1

HighBaseLow

2.6% growthper year

1993 1998 2003 2008 2013 2018 2023

History Forecast

Average annual growth percentage

2003–2023High 6.2%Base 5.2%Low 4.2%

Europe and North America 35

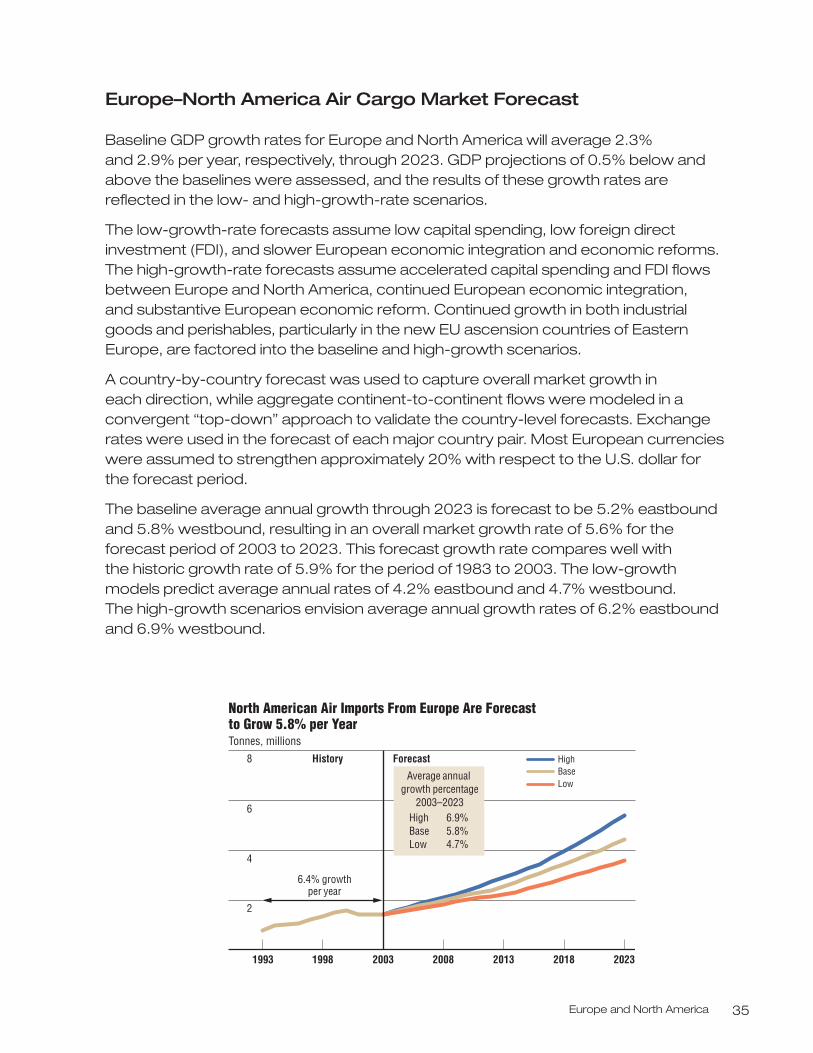

Europe–North America Air Cargo Market Forecast

Baseline GDP growth rates for Europe and North America will average 2.3% and 2.9% per year, respectively, through 2023. GDP projections of 0.5% below andabove the baselines were assessed, and the results of these growth rates arereflected in the low- and high-growth-rate scenarios.

The low-growth-rate forecasts assume low capital spending, low foreign directinvestment (FDI), and slower European economic integration and economic reforms.The high-growth-rate forecasts assume accelerated capital spending and FDI flowsbetween Europe and North America, continued European economic integration, and substantive European economic reform. Continued growth in both industrialgoods and perishables, particularly in the new EU ascension countries of EasternEurope, are factored into the baseline and high-growth scenarios.

A country-by-country forecast was used to capture overall market growth in each direction, while aggregate continent-to-continent flows were modeled in a convergent “top-down” approach to validate the country-level forecasts. Exchangerates were used in the forecast of each major country pair. Most European currencieswere assumed to strengthen approximately 20% with respect to the U.S. dollar for the forecast period.

The baseline average annual growth through 2023 is forecast to be 5.2% eastboundand 5.8% westbound, resulting in an overall market growth rate of 5.6% for theforecast period of 2003 to 2023. This forecast growth rate compares well with the historic growth rate of 5.9% for the period of 1983 to 2003. The low-growthmodels predict average annual rates of 4.2% eastbound and 4.7% westbound. The high-growth scenarios envision average annual growth rates of 6.2% eastboundand 6.9% westbound.

North American Air Imports From Europe Are Forecast to Grow 5.8% per YearTonnes, millions

8

6

4

2

HighBaseLow

6.4% growthper year

1993 1998 2003 2008 2013 2018 2023

History Forecast

Average annual growth percentage

2003–2023High 6.9%Base 5.8%Low 4.7%

Intra-Europe 37

Intra-Europe

Regional Overview

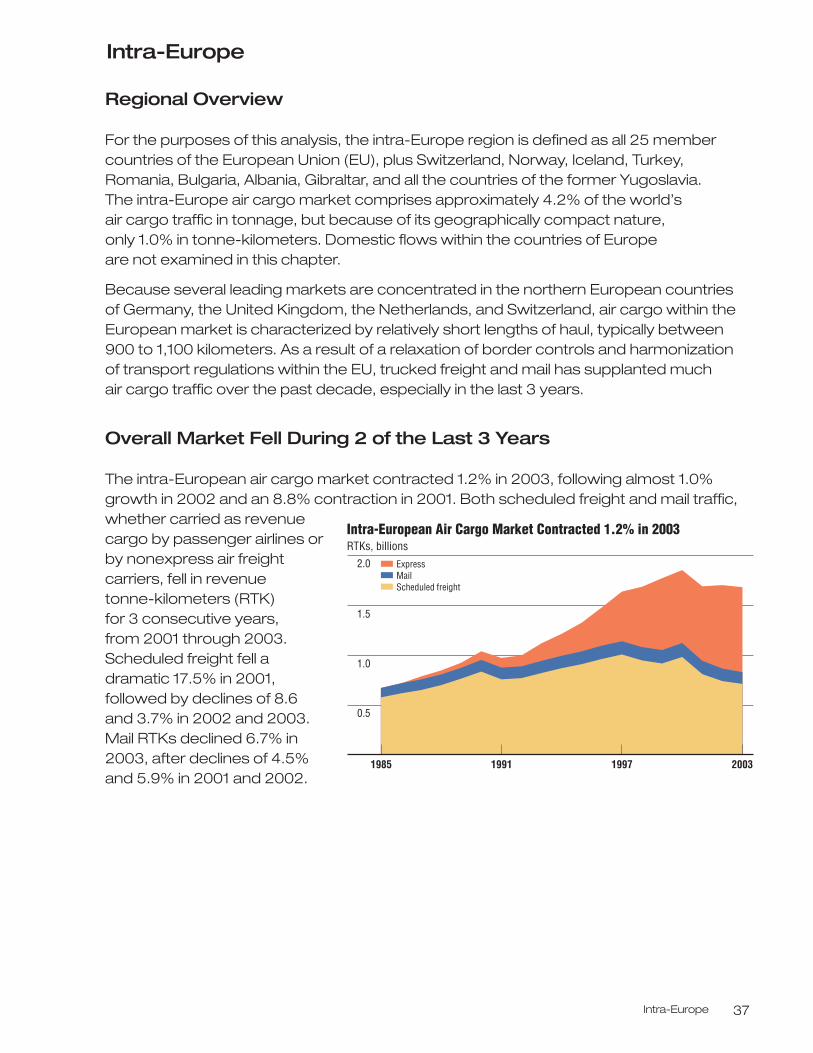

For the purposes of this analysis, the intra-Europe region is defined as all 25 membercountries of the European Union (EU), plus Switzerland, Norway, Iceland, Turkey,Romania, Bulgaria, Albania, Gibraltar, and all the countries of the former Yugoslavia. The intra-Europe air cargo market comprises approximately 4.2% of the world’s air cargo traffic in tonnage, but because of its geographically compact nature, only 1.0% in tonne-kilometers. Domestic flows within the countries of Europe are not examined in this chapter.

Because several leading markets are concentrated in the northern European countriesof Germany, the United Kingdom, the Netherlands, and Switzerland, air cargo within theEuropean market is characterized by relatively short lengths of haul, typically between900 to 1,100 kilometers. As a result of a relaxation of border controls and harmonizationof transport regulations within the EU, trucked freight and mail has supplanted much air cargo traffic over the past decade, especially in the last 3 years.

Overall Market Fell During 2 of the Last 3 Years

The intra-European air cargo market contracted 1.2% in 2003, following almost 1.0%growth in 2002 and an 8.8% contraction in 2001. Both scheduled freight and mail traffic,whether carried as revenuecargo by passenger airlines orby nonexpress air freightcarriers, fell in revenue tonne-kilometers (RTK) for 3 consecutive years, from 2001 through 2003.Scheduled freight fell adramatic 17.5% in 2001,followed by declines of 8.6 and 3.7% in 2002 and 2003.Mail RTKs declined 6.7% in2003, after declines of 4.5%and 5.9% in 2001 and 2002.

Intra-European Air Cargo Market Contracted 1.2% in 2003 RTKs, billions

2.0

1.5

1.0

0.5

1985 1991 1997 2003

Scheduled freightMailExpress

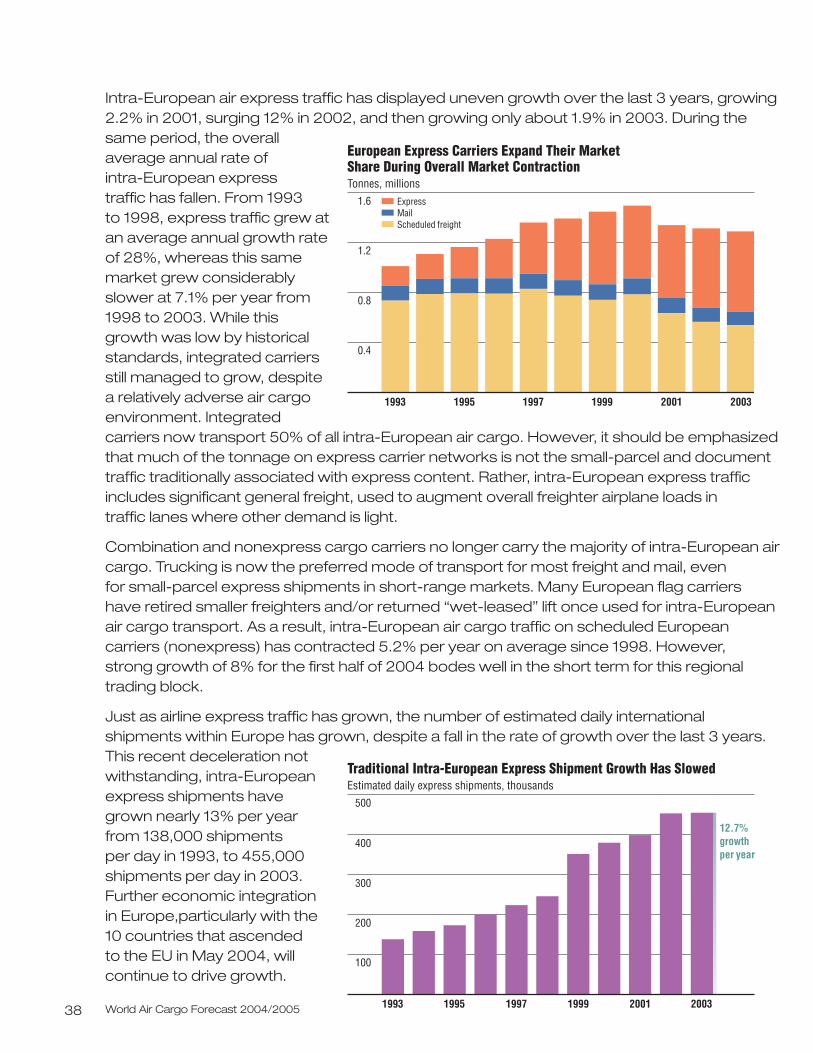

Intra-European air express traffic has displayed uneven growth over the last 3 years, growing2.2% in 2001, surging 12% in 2002, and then growing only about 1.9% in 2003. During thesame period, the overallaverage annual rate of intra-European express traffic has fallen. From 1993 to 1998, express traffic grew atan average annual growth rateof 28%, whereas this samemarket grew considerablyslower at 7.1% per year from1998 to 2003. While thisgrowth was low by historicalstandards, integrated carriersstill managed to grow, despitea relatively adverse air cargoenvironment. Integratedcarriers now transport 50% of all intra-European air cargo. However, it should be emphasizedthat much of the tonnage on express carrier networks is not the small-parcel and documenttraffic traditionally associated with express content. Rather, intra-European express trafficincludes significant general freight, used to augment overall freighter airplane loads in traffic lanes where other demand is light.

Combination and nonexpress cargo carriers no longer carry the majority of intra-European aircargo. Trucking is now the preferred mode of transport for most freight and mail, even for small-parcel express shipments in short-range markets. Many European flag carriers have retired smaller freighters and/or returned “wet-leased” lift once used for intra-European air cargo transport. As a result, intra-European air cargo traffic on scheduled Europeancarriers (nonexpress) has contracted 5.2% per year on average since 1998. However, strong growth of 8% for the first half of 2004 bodes well in the short term for this regionaltrading block.

Just as airline express traffic has grown, the number of estimated daily international shipments within Europe has grown, despite a fall in the rate of growth over the last 3 years.This recent deceleration notwithstanding, intra-Europeanexpress shipments have grown nearly 13% per year from 138,000 shipments per day in 1993, to 455,000shipments per day in 2003.Further economic integration in Europe,particularly with the 10 countries that ascended to the EU in May 2004, willcontinue to drive growth.

World Air Cargo Forecast 2004/200538

European Express Carriers Expand Their MarketShare During Overall Market ContractionTonnes, millions

1.6

1.2

0.8

0.4

200320011999199719951993

Scheduled freightMailExpress

Traditional Intra-European Express Shipment Growth Has SlowedEstimated daily express shipments, thousands

500

400

100

200

300

20031999199719951993 2001

12.7%growthper year

Intra-Europe 39

Contracting Freighter Capacity Helps Drive Up Yields

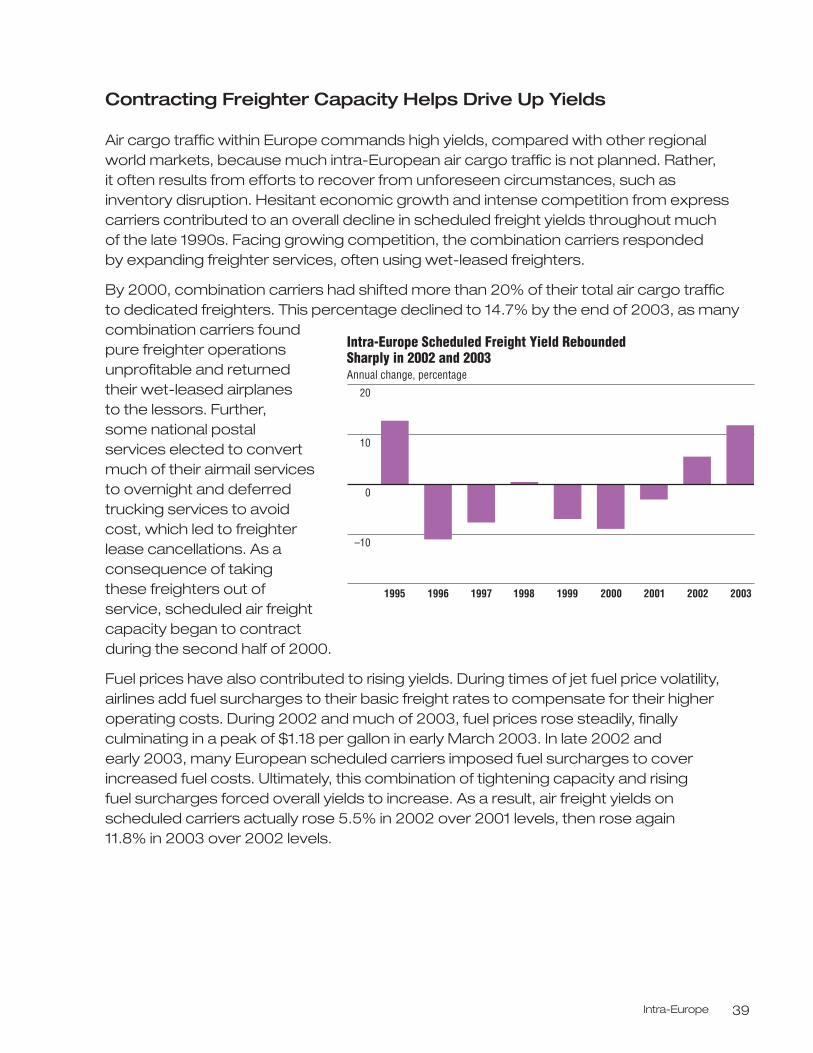

Air cargo traffic within Europe commands high yields, compared with other regionalworld markets, because much intra-European air cargo traffic is not planned. Rather, it often results from efforts to recover from unforeseen circumstances, such asinventory disruption. Hesitant economic growth and intense competition from expresscarriers contributed to an overall decline in scheduled freight yields throughout much of the late 1990s. Facing growing competition, the combination carriers responded by expanding freighter services, often using wet-leased freighters.

By 2000, combination carriers had shifted more than 20% of their total air cargo traffic to dedicated freighters. This percentage declined to 14.7% by the end of 2003, as manycombination carriers foundpure freighter operationsunprofitable and returnedtheir wet-leased airplanes to the lessors. Further, some national postal services elected to convertmuch of their airmail services to overnight and deferredtrucking services to avoidcost, which led to freighterlease cancellations. As aconsequence of taking these freighters out ofservice, scheduled air freightcapacity began to contract during the second half of 2000.

Fuel prices have also contributed to rising yields. During times of jet fuel price volatility,airlines add fuel surcharges to their basic freight rates to compensate for their higheroperating costs. During 2002 and much of 2003, fuel prices rose steadily, finallyculminating in a peak of $1.18 per gallon in early March 2003. In late 2002 and early 2003, many European scheduled carriers imposed fuel surcharges to coverincreased fuel costs. Ultimately, this combination of tightening capacity and rising fuel surcharges forced overall yields to increase. As a result, air freight yields onscheduled carriers actually rose 5.5% in 2002 over 2001 levels, then rose again 11.8% in 2003 over 2002 levels.

Intra-Europe Scheduled Freight Yield Rebounded Sharply in 2002 and 2003 Annual change, percentage

20

10

–10

0

1995 200320012000199919981996 20021997

World Air Cargo Forecast 2004/200540

Trucks Provide Complementary Scheduled Freight Services to Aircraft

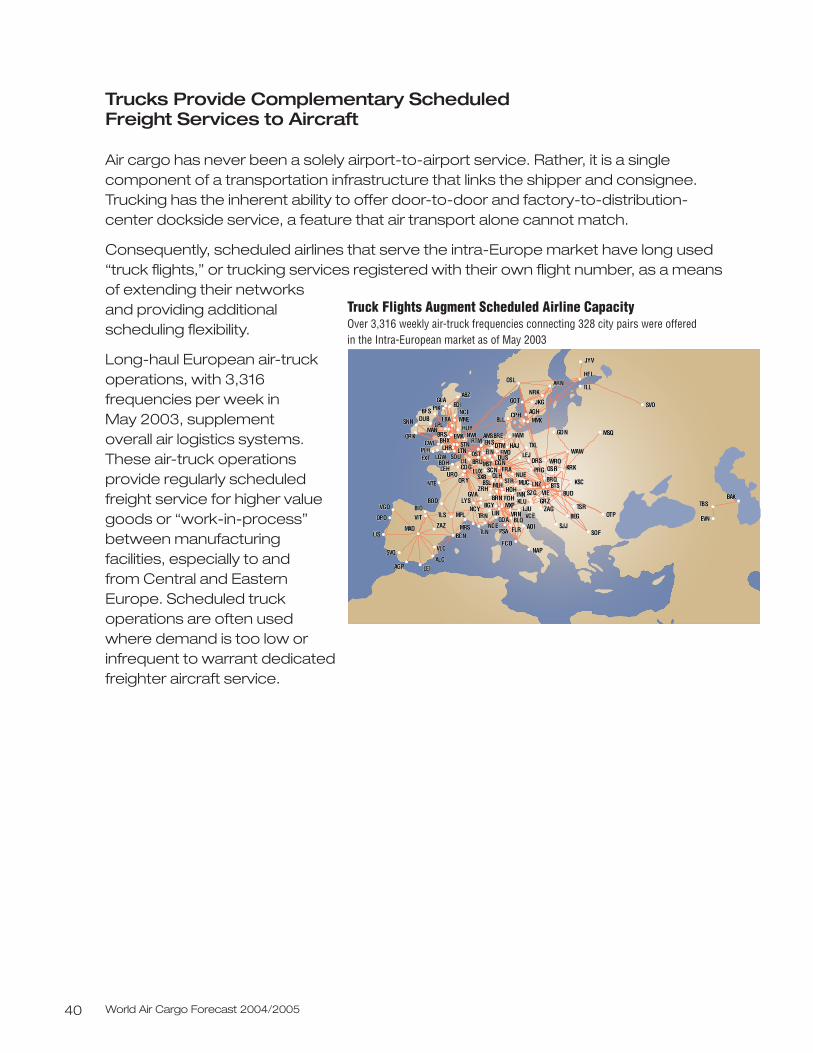

Air cargo has never been a solely airport-to-airport service. Rather, it is a singlecomponent of a transportation infrastructure that links the shipper and consignee.Trucking has the inherent ability to offer door-to-door and factory-to-distribution-center dockside service, a feature that air transport alone cannot match.

Consequently, scheduled airlines that serve the intra-Europe market have long used“truck flights,” or trucking services registered with their own flight number, as a meansof extending their networksand providing additionalscheduling flexibility.

Long-haul European air-truckoperations, with 3,316frequencies per week in May 2003, supplement overall air logistics systems.These air-truck operationsprovide regularly scheduledfreight service for higher valuegoods or “work-in-process”between manufacturingfacilities, especially to andfrom Central and EasternEurope. Scheduled truckoperations are often usedwhere demand is too low orinfrequent to warrant dedicated freighter aircraft service.

Truck Flights Augment Scheduled Airline CapacityOver 3,316 weekly air-truck frequencies connecting 328 city pairs were offered in the Intra-European market as of May 2003

I

FLFL J

S

EIEIN

R

GOGOA

OSOSR

SJSJ

B

BLBLL

HOHOH

KLKLU

AGAGPALALC

AOAOIBCBCN

BIBIO

BLBLQ

BOBOD

FCFCO

LELE

LILIN

LILISMAMAD

MPMPL

MRMRS

NANAP

NCNCE

NCNCY

NTNTE

OPOPO

PSAPSA

SVQSVQ

TLTLN

TLTLS TRTRNVGVGO

VIVIT

VLVLC

ZAZAZ

BAKBAK

BEGBEG

BGBGYBRBRN

EVNEVN

FDFDH GRGRZGVGVA ININN

LJLJULYLYS

MSMSQ

MXMXPOTOTP

SOSOF

SVOSVO

SZSZG

TBTBSTSTSRVCVCE

VIVIE

VRVRN

BOBOH

BSLBSL

CDCDG

CWCWL

EXEXT

LELEH

LGLGW

LULUX

MLMLH

ORORK

ORORY

PLPLH

SXSXURURO

ABZABZ

AGAGH

AMAM

ARARN

BFBFS

BHBHXBRBRE