Embed Size (px)

Citation preview

industry/Business

For plasticizers an unfulfilled promise Overcapacity, eroding prices, and disappearing profit margins mar performance of a dream business

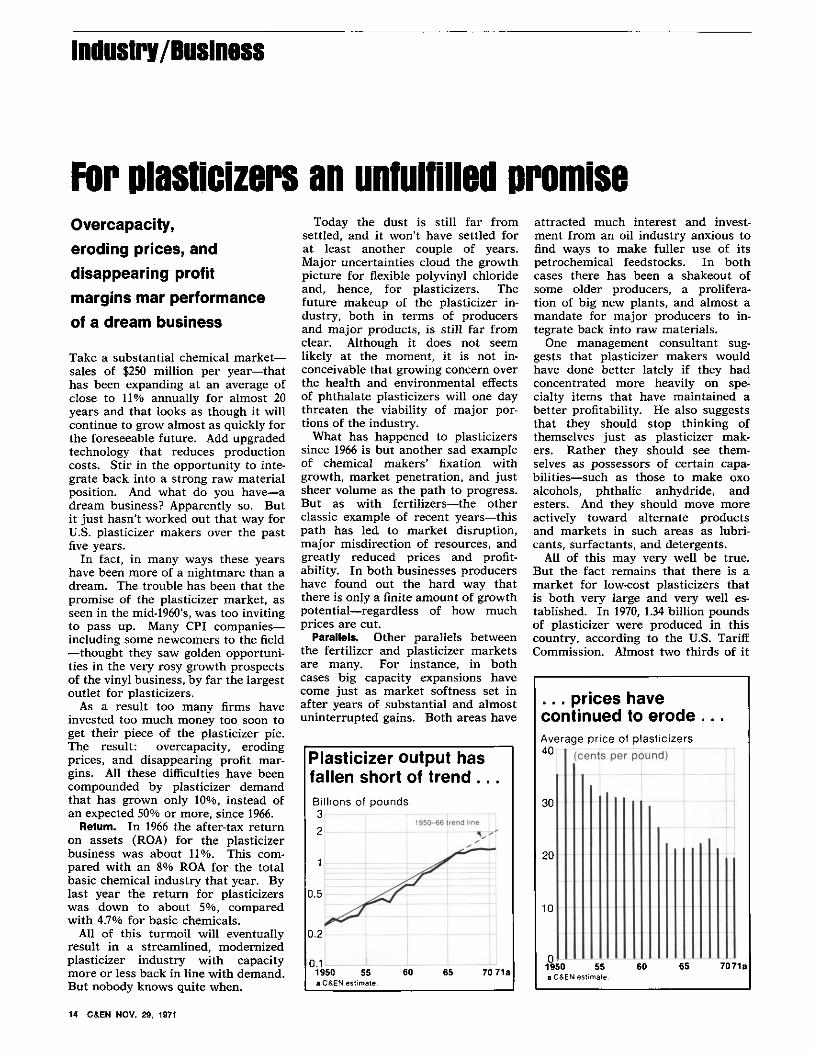

Take a substantial chemical market— sales of $250 million per year—that has been expanding at an average of close to 11% annually for almost 20 years and that looks as though it will continue to grow almost as quickly for the foreseeable future. Add upgraded technology that reduces production costs. Stir in the opportunity to integrate back into a strong raw material position. And what do you have—a dream business? Apparently so. But it just hasn't worked out that way for U.S. plasticizer makers over the past five years.

In fact, in many ways these years have been more of a nightmare than a dream. The trouble has been that the promise of the plasticizer market, as seen in the mid-1960's, was too inviting to pass up. Many CPI companies— including some newcomers to the field —thought they saw golden opportunities in the very rosy growth prospects of the vinyl business, by far the largest outlet for plasticizers.

As a result too many firms have invested too much money too soon to get their piece of the plasticizer pie. The result: overcapacity, eroding prices, and disappearing profit margins. All these difficulties have been compounded by plasticizer demand that has grown only 10%, instead of an expected 50% or more, since 1966.

Return. In 1966 the after-tax return on assets (ROA) for the plasticizer business was about 11%. This compared with an 8% ROA for the total basic chemical industry that year. By last year the return for plasticizers was down to about 5%, compared with 4.7% for basic chemicals.

All of this turmoil will eventually result in a streamlined, modernized plasticizer industry with capacity more or less back in line with demand. But nobody knows quite when.

Today the dust is still far from settled, and it won't have settled for at least another couple of years. Major uncertainties cloud the growth picture for flexible polyvinyl chloride and, hence, for plasticizers. The future makeup of the plasticizer industry, both in terms of producers and major products, is still far from clear. Although it does not seem likely at the moment, it is not inconceivable that growing concern over the health and environmental effects of phthalate plasticizers will one day threaten the viability of major portions of the industry.

What has happened to plasticizers since 1966 is but another sad example of chemical makers ' fixation with growth, market penetration, and just sheer volume as the path to progress. But as with fertilizers—the other classic example of recent years—this path has led to market disruption, major misdirection of resources, and greatly reduced prices and profitability. In both businesses producers have found out the hard way that there is only a finite amount of growth potential—regardless of how much prices are cut.

Parallels. Other parallels between the fertilizer and plasticizer markets are many. For instance, in both cases big capacity expansions have come just as market softness set in after years of substantial and almost uninterrupted gains. Both areas have

Plasticizer output has fallen short of trend . . Billions of pounds 3

1950-66 trend line

0.1 1950 55 a C&EN estimate.

60 65 70 71a

attracted much interest and investment from an oil industry anxious to find ways to make fuller use of its petrochemical feedstocks. In both cases there has been a shakeout of some older producers, a proliferation of big new plants, and almost a mandate for major producers to integrate back into raw materials.

One management consultant suggests that plasticizer makers would have done better lately if they had concentrated more heavily on specialty items that have maintained a better profitability. He also suggests that they should stop thinking of themselves just as plasticizer makers. Rather they should see themselves as possessors of certain capabilities—such as those to make oxo alcohols, phthalic anhydride, and esters. And they should move more actively toward alternate products and markets in such areas as lubricants, surfactants, and detergents.

All of this may very well be true. But the fact remains that there is a market for low-cost plasticizers that is both very large and very well established. In 1970, 1.34 billion pounds of plasticizer were produced in this country, according to the U.S. Tariff Commission. Almost two thirds of it

. . . prices have continued to erode Average price of plasticizers 40 ι

1 (cents per pound)

30

20

10

0 1950 55 a C&EN estimate.

60 65 7071a

14 C&EN NOV. 29, 1971

was priced at less than 20 cents per pound. Almost half of it was at less than 15 cents.

Vinyl. The near sixfold increase in plasticizer production in this country over the past 20 years has very largely been generated by the expansion of the vinyl industry. About 75% of plasticizers end up in vinyl products. Today, PVC resin production is running at slightly more than 3 billion pounds per year, compared with 325 million in 1950. (Another 15% of plasticizers goes into synthetic rubber, cellulosic resins, and other plastics. The remaining 10% ends up in nonplasticizer uses such as gasoline additives, synthetic lubricants, and functional fluids.)

External plasticizers, the type discussed in this article, soften a resin without reacting chemically with it. They reduce the forces, other than primary chemical bonds, that exist between polymer chains. Internal plasticizers do the same thing, but do so by reacting chemically with a resin monomer and becoming part of the polymer chain.

The possible use of internally plasti-cized vinyl resins offers a constant potential threat to the entire plasticizer industry as it is known today. But no large-scale and economically feasible way has yet been found to internally plasticize PVC—and none is expected.

External plasticizers have to have other properties in addition to the ability to impart flexibility to a resin. Depending on the end use of the product, they may, for instance, be required to resist extraction by soapy water or solvents, to add good low-temperature properties, or to reduce flammability.

Di-2-ethylhexyl phthalate (DOP), di-isooctyl phthalate (DIOP), and diiso-decyl phthalate (DIDP) all impart a good overall balance of properties at

L.. and dollar sales volume has dipped Plasticizer sales

3 ($100 million) ^ * 2 jT

1 r - ^

0.5

0.2

0.1 1950 55 60 65 a C&EN estimate. Source: U.S. Tariff Comnr

70 71a ission

low cost. DOP, in particular, has long been the industry standard for general-purpose uses.

But these general-purpose plasticizers are not ideal for all applications. Hence the need for other phthalate esters and for adipate esters, phosphate esters, expoxidized esters, trimellitate esters, and a host of other specialty plasticizers. - These higher cost products are used where their special properties are required, often in conjunction with general-purpose plasticizers.

Advantage. New and modified plasticizers are constantly being introduced as producers jostle for market advantage. Currently, diisononyl phthalate and phthalates of various linear alcohols are making big plays for major penetration. But in spite of such activity, the breakdown of the plasticizer market has remained fairly constant for 20 years. General-purpose plasticizers have shown great resilience to constant attempts to whittle away at their dominant volume position. In fact, they have actually gained a market share in recent years.

Last year, DOP production was 350 million pounds; DIDP output was 123 million pounds; 85 million pounds of DIOP brought the general-purpose total to 559 million pounds. This represents 42% of the 1970 industry total of 1.34 billion pounds. Other phthalates added another 296 million pounds, or 22%. These include 59 million pounds of N-octyl iV-decyl, 23 million pounds of dibutyl, and 21 million pounds of diethyl. Other cyclic plasticizers, including about 70 million pounds of phosphate esters, added another 143 million pounds, or 11%. Acyclic plasticizers accounted for the remaining 338 million pounds, or 25%. The major members of this acyclic group include 95 million pounds of epoxidized esters, 54 million pounds of adipates, and 47 million pounds of polyesters and other polymeries.

Pattern. This pattern is not radically different from what it was 10 years earlier. In 1960, DOP production of 123 million pounds represented 20% of the total, compared with 26% last year. DIOP and DIDP brought the 1960 general-purpose total to 34%, compared with 42% last year. Other phthalates accounted for 23% in 1960 and 22% in 1970 while the percentage of other cyclics dropped from 17% to 11% over the 10-year span. The percentage of acyclics remained almost constant: 26% in 1960, 25% last year.

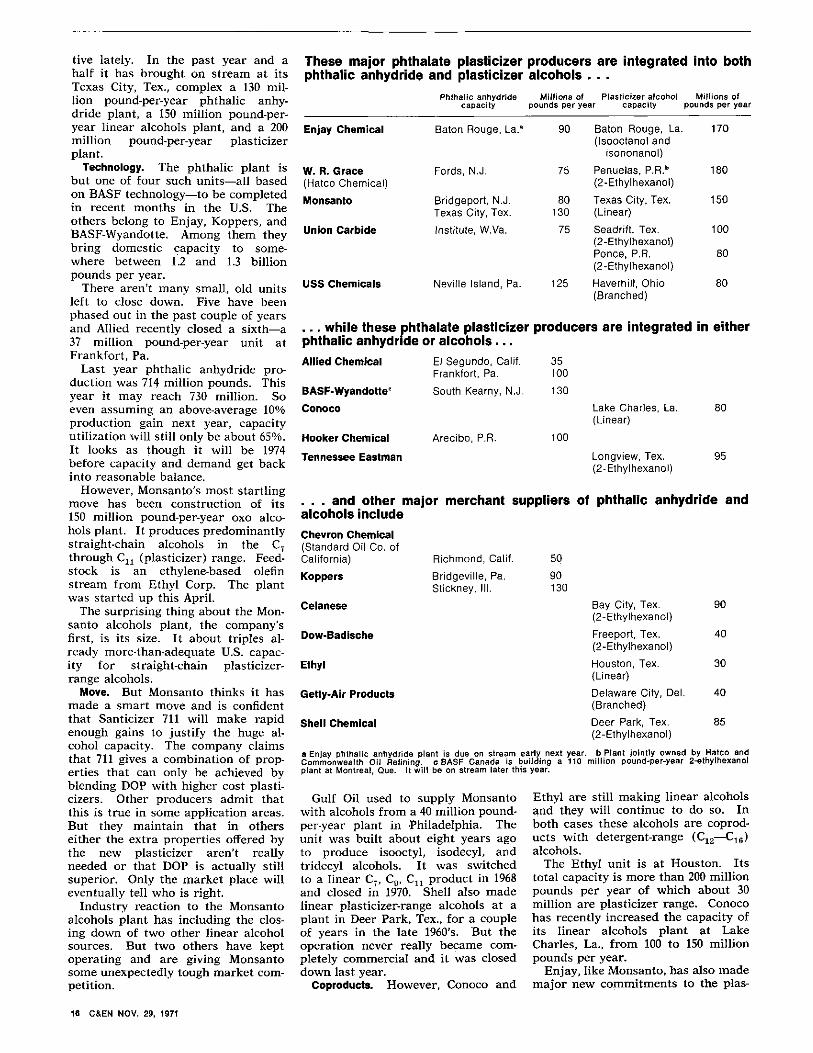

Today, all producers of big-volume plasticizers are either fully integrated

into both phthalic anhydride and alcohols or at least partially integrated into one or other of these raw materials. It is not too hard to fathom why. As one producer puts it, there is really only one profit to have from making plasticizer-range alcohols, phthalic, and plasticizers themselves. Hence to be in the big-volume, low profit margin end of the plasticizer business a company almost has to make all three if it hopes to survive.

This need to integrate is intensified by the fact that the actual making of plasticizers is the small end of the business from a capital investment point of view. Capital investment in a typical oxo alcohols plant amounts to about $15 million per 100 million pounds per year of capacity. For a phthalic plant it is about $12 million per 100 million pounds. But a 100 million pound-per-year esterification plant can be built for about $3 million.

Producers. There are five fully integrated domestic plasticizer producers —En jay Chemical, Hatco chemical division of W. R. Grace, Monsanto, Union Carbide, and USS Chemicals. These companies probably account for about 75% of the U.S. plasticizer business. They have taken three distinct routes to the market in recent years. Monsanto and En jay have actively developed and promoted new products to compete directly with general-purpose plasticizers. Hatco has gone ahead to establish itself very firmly in DOP and Union Carbide and USS Chemicals have kept relatively low profiles trying to maintain traditionally strong positions in the market without investing too much more money.

Monsanto has been particularly ac-

NOV. 29, 1971 C&EN 15

Stable market over past 20 years Per cent of total plasticizer production

These major phthalate plasticizer producers are integrated into both phthalic anhydride and plasticizer alcohols . . .

Phthalic anhydride Millions of Plasticizer alcohol Millions of capacity pounds per year capacity pounds per year

Enjay Chemical

W. R. Grace (Hatco Chemical)

Monsanto

Union Carbide

USS Chemicals

Baton Rouge, La.a

Fords, N.J.

Bridgeport, N.J. Texas City, Tex.

Institute, W.Va.

Neville Island, Pa.

90

75

80 130

75

125

Baton Rouge, La. (Isooctanol and

isononanol)

Penuelas, P.R.b

(2-Ethylhexanol)

Texas City, Tex. (Linear)

Seadrift, Tex. (2-Ethylhexanol) Ponce, P.R. (2-Ethylhexanol)

Haverhill, Ohio (Branched)

170

180

150

100

80

80

tive lately. In the past year and a half it has brought on stream at its Texas City, Tex., complex a 130 million pound-per-year phthalic anhydride plant, a 150 million pound-per-year linear alcohols plant, and a 200 million pound-per-year plasticizer plant.

Technology. The phthalic plant is but one of four such units—all based on BASF technology—to be completed in recent months in the U.S. The others belong to Enjay, Koppers, and BASF-Wyandotte. Among them they bring domestic capacity to somewhere between 1.2 and 1.3 billion pounds per year.

There aren't many small, old units left to close down. Five have been phased out in the past couple of years and Allied recently closed a sixth—a 37 million pound-per-year unit at Frankfort, Pa.

Last year phthalic anhydride production was 714 million pounds. This year it may reach 730 million. So even assuming an above-average 10% production gain next year, capacity utilization will still only be about 65%. It looks as though it will be 1974 before capacity and demand get back into reasonable balance.

However, Monsanto's most startling move has been construction of its 150 million pound-per-year oxo alcohols plant. It produces predominantly straight-chain alcohols in the C7

through C n (plasticizer) range. Feedstock is an ethylene-based olefin stream from Ethyl Corp. The plant was started up this April.

The surprising thing about the Monsanto alcohols plant, the company's first, is its size. It about triples already more-than-adequate U.S. capacity for straight-chain plasticizer-range alcohols.

Move. But Monsanto thinks it has made a smart move and is confident that Santicizer 711 will make rapid enough gains to justify the huge alcohol capacity. The company claims that 711 gives a combination of properties that can only be achieved by blending DOP with higher cost plasti-cizers. Other producers admit that this is true in some application areas. But they maintain that in others either the extra properties offered by the new plasticizer aren't really needed or that DOP is actually still superior. Only the market place will eventually tell who is right.

Industry reaction to the Monsanto alcohols plant has including the closing down of two other linear alcohol sources. But two others have kept operating and are giving Monsanto some unexpectedly tough market competition.

. . . while these phthalate plasticizer phthalic anhydride or alcohols... Allied Chemical El Segundo, Calif.

Frankfort, Pa.

BASF-Wyandotte South Kearny, N.J.

Conoco

Hooker Chemical Arecibo, P.R.

Tennessee Eastman

Gulf Oil used to supply Monsanto with alcohols from a 40 million pound-per-year plant in Philadelphia. The unit was built about eight years ago to produce isooctyl, isodecyl, and tridecyl alcohols. It was switched to a linear C7, C9, C n product in 1968 and closed in 1970. Shell also made linear plasticizer-range alcohols at a plant in Deer Park, Tex., for a couple of years in the late 1960's. But the operation never really became completely commercial and it was closed down last year.

Coproducts. However, Conoco and

producers are integrated in either

35 100

130

Lake Charles, La. 80 (Linear)

100

Longview, Tex. 95 (2-Ethylhexanol)

Ethyl are still making linear alcohols and they will continue to do so. In both cases these alcohols are coproducts with detergent-range (C12—C16) alcohols.

The Ethyl unit is at Houston. Its total capacity is more than 200 million pounds per year of which about 30 million are plasticizer range. Conoco has recently increased the capacity of its linear alcohols plant at Lake Charles, La., from 100 to 150 million pounds per year.

Enjay, like Monsanto, has also made major new commitments to the plas-

. . . and other major merchant suppliers of phthalic anhydride and alcohols include

Chevron Chemical (Standard Oil Co. of California)

Koppers

Celanese

Dow-Badische

Ethyl

Getty-Air Products

Shell Chemical

Richmond,

Bridgeville, Stickney, II

Calif.

Pa. 1.

50

90 130

Bay City, Tex. (2-Ethylhexanol)

Freeport, Tex. (2-Ethylhexanol)

Houston, Tex. (Linear)

Delaware City, Del. (Branched)

Deer Park, Tex. (2-Ethylhexanol)

90

40

30

40

85

a Enjay phthalic anhydride plant is due on stream early next year, b Plant jointly owned by Hatco and Commonwealth Oil Refining, c BASF Canada is building a 110 million pound-per-year 2-ethylhexanol plant at Montreal, Que. It will be on stream later this year.

16 C&EN NOV. 29, 1971

ticizer business lately. Apart from the new phthalic anhydride plant, the company has alcohol and plasticizer units at Baton Rouge, La. En jay has a flexible operation and produces a wide range of plasticizers. But it is making a very big play for its di-isononyl phthalate. This product sells at the same price as DOP—12 cents per pound—and is claimed to have major advantages, such as lower volatility and extraction. The company hopes that DINP sales will reach 100 million pounds by 1975.

Standby. Unlike Monsanto and Enjay—that are promoting products to challenge DOP—Hatco has put most of its future marbles on the solid old industry standby. The company has just completed its big alcohols plant in Puerto Rico. It has a capacity of about 180 million pounds per year of 2-ethylhexyl alcohol—the parent alcohol for DOP. The plant has a strong feedstock situation. It is half-owned by Commonwealth Oil Refining —a big olefin producer.

USS Chemicals has a solid position in plasticizers with a smoothly running phthalic anhydride plant at Neville Island, Pa., and a big new plasticizer unit at the same site. It is not overly strong in alcohols. Its plant in Haverhill, Ohio, is not new and the company has to buy feedstocks.

Union Carbide is also fairly well situated. But in this case its phthalic anhydride position is a little weak. Carbide has one aging plant at Institute, VY.Va. This summer the company stopped further construction work on a 130 million pound-per-year plasticizer unit at Ponce,. P.R., that is considerably more than half finished.

BASF-Wyandotte is making a determined and aggressive bid to become a major factor in the U.S. plasticizer business. The parent company is probably the largest plasticizer producer worldwide. And in this country BASF-Wyandotte is just bringing on stream at Kearny, N.J., both a 130 million pound-per-year phthalic anhydride plant and a 66 million pound-per-year plasticizer unit.

BASF does not make plasticizer alcohols in the U.S. But BASF Canada is just completing a 110 million pound-per-year oxo alcohol plant near Montreal. It will supply the Canadian market with a surplus for export.

Of course, phthalates are not the entire plasticizer ball game—just almost all the low-cost section of it. But many of the higher cost, specialty products have also been quite stagnant on the market place recently.

For instance, production of epoxi-dized esters has been at about 100 million pounds per year for the past four

years. Adipic acid ester production actually fell last year to 54 million pounds from 65 million pounds the year before.

Phosphoric acid ester plasticizers are attracting considerable attention —even if they are not currently showing strong growth. The interest stems from their ability to lessen the flam-mability of vinyl when used as about a 25% replacement for DOP.

Current use of phosphate plasticizers is running at about 50 million pounds per year. It has been growing about 3 to 5% annually for the past several years. About a third of it is tricresyl phosphate. Other triaryl phosphates add another 30%. Alkyl-aryl phosphates, mostly made by Monsanto, contribute another 22% and tri-alkyl phosphates make up the remaining 15%.

Flammability. This market is particularly difficult to predict because of the large number of actual and pending government flammability regulations on a host of products. For instance, new federal flammability standards for automobiles become effective next September. Federal standards for carpets are already operative and there are many building codes covering a myriad of construction materials.

The big unknown is how manufacturers will move to meet these new specifications as they apply to vinyl products. Phosphate esters are not the only products that will reduce the flammability of vinyls.

Investment. However, in spite of these uncertainties, phosphate plasticizers are attracting investment and enthusiasm. Monsanto has expanded capacity by 50 million pounds per year. FMC has introduced a new triaryl phosphate based on a mixed isopro-pylphenol intermediate that it is making in its complex at Nitro, W.Va. Stauffer, too, is very bullish, predicting something like a tripling in phosphate plasticizer use in vinyls by about 1975.

There are a couple of clouds overhanging the further growth for vinyl plasticizers. One concerns the environmental problems of disposing of PVC—particularly in packaging materials—and the other concerns the health and environmental implications of phthalate plasticizers.

Critics claim that the hydrogen chloride generated when PVC is incinerated is a serious pollutant. They also claim that it corrodes incinerators. A study also points out that PVC can even improve the efficiency of an incinerator. The study was sponsored by the Society of the Plastics Industry.

The scare over plasticizers was trig-

ι gered by a report late last year by Dr. Robert Rubin of Johns Hopkins University that phthalate plasticizers used in PVC bags for human blood storage leach out of the plastic into the blood. The effect of such plasticizers on the human system is still unknown. Dr. Rubin is now looking into the distribution and metabolism of such phthalates when they are fed, injected into, or inhaled by test animals. He stresses that it is still far too early for anybody to get alarmed and certainly too early for any products to be pulled off the market.

But, as Dr. Rubin acknowledges, such health scares often seem to have a life of their own and to develop political and commercial implications that are way ahead of supporting scientific data. Reports of DOP and other phthalates in the ecosystem are already proliferating. For instance, they have been reported in heart muscles, in fish, and as water pollutants. Some very preliminary work at the National Institutes of Health in Bethesda, Md., indicates that they may be present in concentrations of 20 p.p.m. and higher in blood taken from human patients.

Disruptions. Both these scares are certainly causing concern in the plasticizer industry. However, the betting today is that neither will cause any major market disruptions. The pressure on PVC packaging materials seems to have lessened slightly in recent months and so far nobody is actively making a political issue out of the phthalate question.

The typical short-term outlook for the plasticizer business calls for a modest 2 or 3% production increase to bring output back about to the 1969 level. There is talk—and maybe a little genuine hope—of modest price improvement for the big-volume products. The list price for DOP was boosted from 11 to 12 cents per pound this spring. On paper, it has held.

The consensus for the five-year outlook calls for about a 6 to 8% annual production increase—down from the traditional 11% but enough to mop up a lot of today's overcapacity by 1974.

So it all looks as though the industry's growing pains will last for a total of five years—from 1969 to 1973. Before those pains started it was a highly diversified industry characterized by many producers with a host of small and widely scattered production units. But by 1974 it will be a fairly highly concentrated industry, dominated by a relatively few producers with large centralized plants and an integrated raw material position.

NOV. 29, 1971 C&EN 17

![EGFR as a Target for Glioblastoma Treatment: An Unfulfilled Promise … · 2017. 8. 28. · which there is only preclinical promise [34]. Brain pene-trance is difficult to measure](https://img.pdfslide.us/doc/110x75/60589686b1bd3b19386788e4/egfr-as-a-target-for-glioblastoma-treatment-an-unfulfilled-promise-2017-8-28.jpg)