Embed Size (px)

Citation preview

Investorium SeminarInvestorium SeminarThe Basement ‐ Sydney

4 February 2013ASX Code: BUY

CEO

Philip F Kelso

For

per

sona

l use

onl

y

Bounty Oil & Gas NL – Major Growth Projects with Production Base

Oil f h lf $1 03 illi (H lf 2011 $1 29 illi ) ith• Oil revenue for half year $1.03 million (Half 2011: $1.29 million) with 2013 increases from SW Queensland expected

• Current assets at December 2012 exceed $6 million

• Oil Business strategy on track to provide further growth:‐– Bounty extends term for 100% owned AC/P32, Timor Sea with potential

20 80 illi bbl il t t t Wi t i W t– 20 – 80 million bbl oil target at Wisteria West

– Development drilling about to commence to test potential 1.8million bblsl(gross) at Utopia, Queensland

• Gas/Condensate Business:‐– Bounty completes acquisition of Key Petroleum’s 5% equity in the Kiliwani

North Development Block, Tanzaniap ,

– Conventional gas upside in Surat Basin

2

For

per

sona

l use

onl

y

Issued Equity and Capital Summary

As at 4-Feb-13

52 Week Price Range $0 016 to $0 04352 Week Price Range $0.016 to $0.043

Shares Quoted 838,400,982

Unlisted Options @ $0.024 20,000,000

Fully Diluted 858,400,982

ASX Closing Price $0.02

M k t C it li ti $16 7 illiMarket Capitalisation $16.7 million

3

For

per

sona

l use

onl

y

BUY –Reserve and Resource Summary

B t Oil & GBounty Oil & GasPetroleum Reserves/Resources

MMbo Gas BCF MMboeProducing Fields (Technically Recoverable 2P) 1.12 1.12Contingent Resources (Pmean) 0.17 2.25 0.58Contingent Resources (Pmean) 0.17 2.25 0.58Prospective Resources (Possible Extent of Known Oil) 4.79 4.79

Prospective Resources (Pmean) UndiscoveredNyuni Tanzania 238 43AC/P 32 Timor Sea 76 76PEP 11 132 24

Total Undiscovered 76 370 143

4

For

per

sona

l use

onl

y

Year on Year Comparison

30

35

Financial

2.50

Shares

25

30

2.00

20

$ Millions

2012

1.50

Cents 2012

2011

10

15 A$ 2012

2011

1.00

5

0.50

‐

Total Assets Net Assets Current Assets

Petroleum Sales

Cashflow

‐

Share price Earnings per Share

5

For

per

sona

l use

onl

y

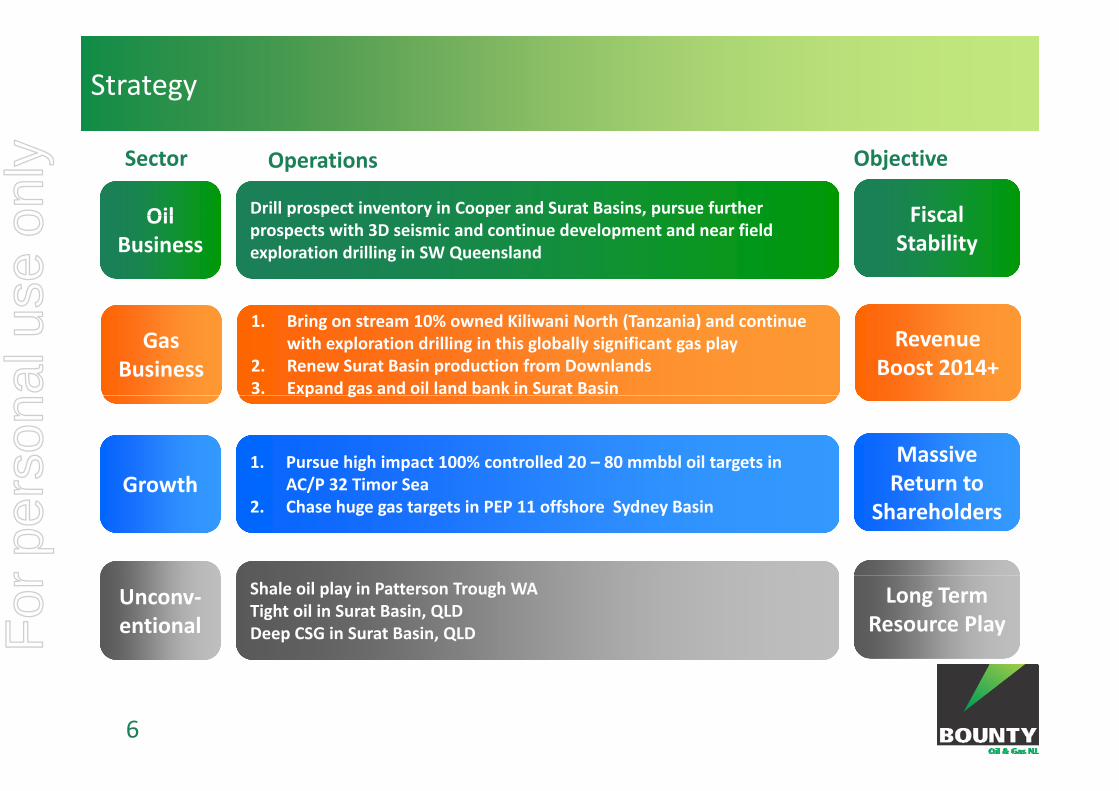

Strategy

Oil Drill prospect inventory in Cooper and Surat Basins, pursue further Fiscal

Sector Operations Objective

OilBusiness

p p y p , pprospects with 3D seismic and continue development and near field exploration drilling in SW Queensland

Fiscal Stability

GasBusiness

1. Bring on stream 10% owned Kiliwani North (Tanzania) and continue with exploration drilling in this globally significant gas play

2. Renew Surat Basin production from Downlands 3. Expand gas and oil land bank in Surat Basin

Revenue Boost 2014+

p g

Growth1. Pursue high impact 100% controlled 20 – 80 mmbbl oil targets in

AC/P 32 Timor Sea

Massive Return toGrowth AC/P 32 Timor Sea

2. Chase huge gas targets in PEP 11 offshore Sydney Basin Return to

Shareholders

Unconv‐entional

Shale oil play in Patterson Trough WATight oil in Surat Basin, QLDDeep CSG in Surat Basin, QLD

Long Term Resource Play

6

For

per

sona

l use

onl

y

Oil Production SW Queensland

Utopia Field

Cooper/Eromanga Basin Projects

/ • Production kept steady by new discoveries Irtalie East and Watson South coming on stream strongly at Naccowlah

• Successful appraisal well Irtalie East 3 60.00

70.00

80.00Naccowlah bopd Utopia bopd

Production FY 2011/12

returned 10 metres of pay in Hutton and oil in the Westbourne

• 3D seismic at Utopia has outlined pools with potential for 8 MMbo

• Drilling about to commence at Utopia20.00

30.00

40.00

50.00

7

• Drilling about to commence at Utopia

• Anticipate 3 – 5 development/appraisal wells in 2013 to continue production

0.00

10.00

Jul‐1

1

Aug

‐11

Sep‐11

Oct‐11

Nov‐11

Dec‐11

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

Jul‐1

2

Aug

‐12

For

per

sona

l use

onl

y

Utopia Current Drilling

8

For

per

sona

l use

onl

y

Surat Basin SW QLD Exploration and Production

Farawell 3D

Downlands Gas Plant

Targets

Prospective Recoverable MMboP10 P50 P90 Mean

Mardi Boxvale 0 42 0 21 0 08 0 24Mardi Boxvale 0.42 0.21 0.08 0.24Eluanbrook Showgrounds

0.28 0.19 0.12 0.2

Total 0.7 0.4 0.2 0.44

9Targeting Oil along the SW margin fairway

For

per

sona

l use

onl

y

Nyuni Block Tanzania ‐ Nyuni 2 Well Site

10

For

per

sona

l use

onl

y

Kiliwani North Gas Commercialisation – BUY 10%

• Tanzanian Government approved construction of new pipeline and gas plant to Songo Songo Island financed by Chinese LoanSongo Songo Island financed by Chinese Loan

• Government plans involve production from Kiliwani North at a rate of 20 million cubic feet per day in early 2014 (2 MMcfg/d or 364 boepd net to BUY)

• Structural prospects targeting same top Neocomian Play total 1.8 Tcf gas Pmean

11

For

per

sona

l use

onl

y

Nyuni Block Stratigraphic Gas Leads – BUY 5%

Lead 3 Seismic Amplitude Anomaly and Flat Spot

BCF GasP90 P50 P10 Pmean

Lead 3 Pande 220 792 2840 1303

Stratigraphic Targets

• Recent Exploration by ENI, Anadarko, BG and others has discovered over 100 Tcf of gas in structural/stratigraphic

Nyuni Seismic Stratigraphic Leads East220 792 2840 1303

Other Leads 1054 1375 1495 1317

Total 1274 2167 4335 2620

12

p y , , g / g ptraps in deep water turbidite sands, sourced from adjacent river deltas

• Bounty has several significant leads in the same units within the Nyuni PSA which are marked by strong seismic amplitude anomalies and other direct indicators of hydrocarbons with targets of 2.6 TCF gas.

For

per

sona

l use

onl

y

AC/P 32 High Impact Oil Exploration – BUY 100%

East Swan Acoustic Impedance Anomalies

Azalea Sand Probability – Sand body with y yAnomalous Amplitudes

Targets:East Swan 16 – 40 MMboAzalea 20 – 80 MmboOthers 20 – 30 MMbo

• Bounty is targeting large stratigraphic prospects with anomalous seismic amplitudes especially in the Puffin Sand up dip from the Puffin Field and the Birch 1 oil accumulation

• Contract signed ‐ work has commenced on seismic reprocessing and detailed study of

13

seismic and amplitude v offset characteristics to predict fluid content

• Once substantially derisked farmin partners will be sought to drill a wellTuronian Channels

For

per

sona

l use

onl

y

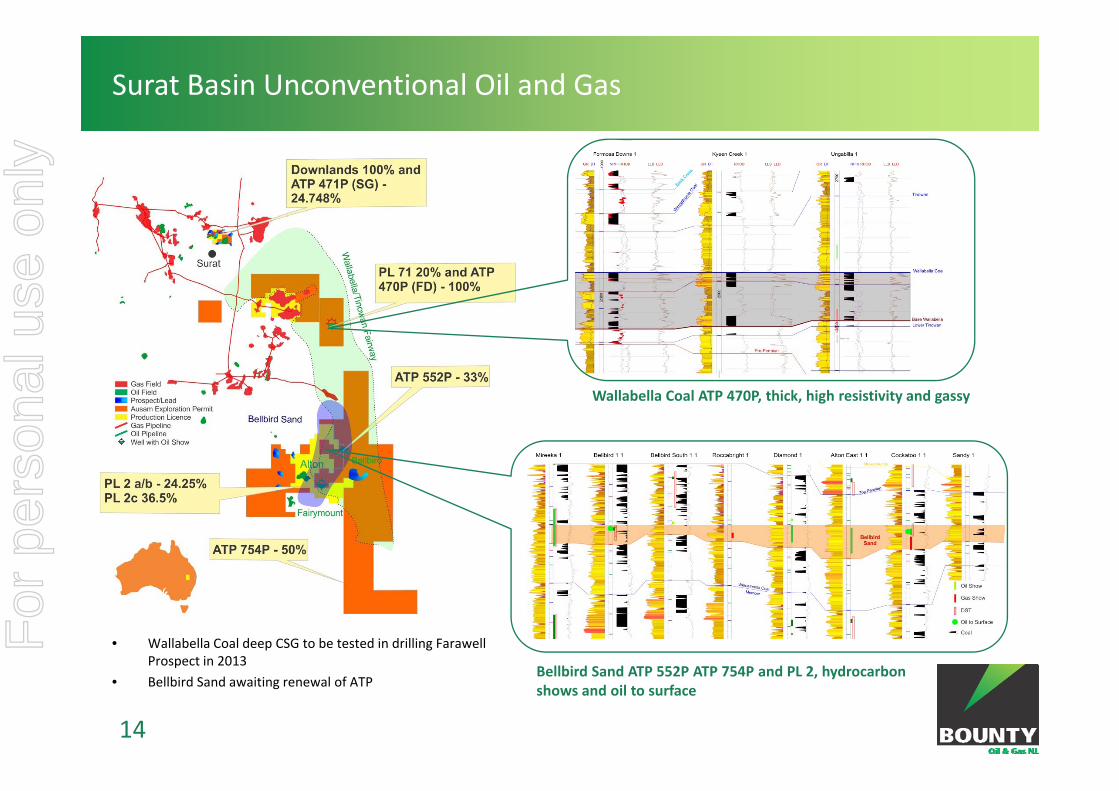

Surat Basin Unconventional Oil and Gas

Wallabella Coal ATP 470P thick high resistivity and gassyWallabella Coal ATP 470P, thick, high resistivity and gassy

• Wallabella Coal deep CSG to be tested in drilling FarawellProspect in 2013

14

Prospect in 2013

• Bellbird Sand awaiting renewal of ATPBellbird Sand ATP 552P ATP 754P and PL 2, hydrocarbon shows and oil to surface

For

per

sona

l use

onl

y

Unconventional Shale Oil Paterson Trough Carnarvon Basin WA

• Drilling into the Paterson TroughDrilling into the Paterson Trough returned oil cut from shales in the Dingo Claystone

• Source rocks TOC in the range 1 ‐ 2.5%

• Dingo Claystone in the Trough is in the oil generation window

• US company farmed into to drill unconventional well at Paterson East

• And drill 5MMbo Bee Eater 1 exploration well

15

For

per

sona

l use

onl

y

Disclaimer

This presentation contains forward looking statements that are subject to risk factors associatedThis presentation contains forward looking statements that are subject to risk factors associatedwith the oil and gas industry. It is believed that the expectations reflected in these statementsare reasonable but they may be affected by a range of variables which could cause actual resultsor trends to differ materially, including but not limited to: product price fluctuations, actuald d fl i h i l f d illi d d i l il ddemand, currency fluctuations, geotechnical factors, drilling and production results, oil and gascommercialisation, development progress, operating results, engineering estimates, reserveestimates, loss of market, industry competition, environmental risks, physical risks, legislative,fiscal and regulatory developments, economic and financial markets conditions in variouscountries, approvals and cost estimates.

All references to dollars, cents or $ in this document are Australian currency, unless otherwiset t dstated

16

For

per

sona

l use

onl

y