Embed Size (px)

Citation preview

Annual Report 2012

For

per

sona

l use

onl

y

Contents

ABN 82 062 091 909

Annual Report 2012

Chairman’s review 1

Review of projects 2

Corporate governance statement 12

Directors report 16

Consolidated fi nancial statements 22

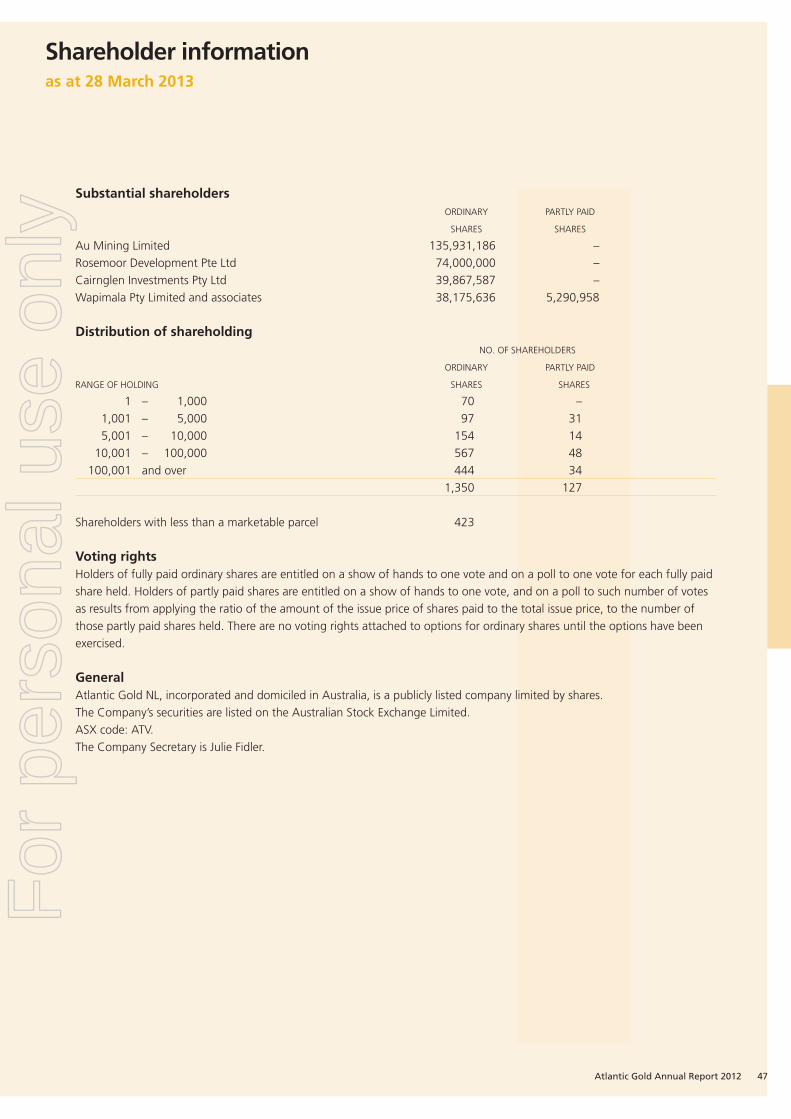

Shareholder information 47

List of mining tenements Inside back cover

Corporate directory Inside back cover

For

per

sona

l use

onl

y

Chairman’s review

Atlantic Gold Annual Report 2012 1

2012 has been a year of solid progress for Atlantic Gold in bringing the Touquoy Gold Project in Nova Scotia, Canada towards production. A vesting order was made by the Minister of Natural Resources for acquisition of the remaining 14 (of 63) surface properties overlying the Touquoy mine site and titles to all of these properties are now held by Atlantic Gold.

Physical possession of the properties – the second step in the acquisition process provided for under the terms of the Expropriation Act – has now been achieved in relation to all but one of the 14 properties. Atlantic Gold is confi dent that possession of the single remaining property will be obtained following an appeal against the Minister’s decision which is to be heard in April 2013.

Concurrently the application for Industrial Approval – the fi nal permit required – has been submitted to Nova Scotia Environment and can be granted once Atlantic Gold is in possession of all surface titles.

Financing discussions are continuing in earnest with detailed proposals being developed with several interested fi nanciers.

During the year the acquisition of 100% of the Cochrane Hill Gold property was completed, enhancing the outcome for shareholders from the conceptual combined Touquoy–Cochrane Hill production plan. In addition the company has continued its methodical assessment of exploration targets in Nova Scotia with similar geological attributes to the Touquoy Gold Deposit.

We welcome new director Rod Hanson to the company. Our personal knowledge of Rod’s technical and managerial expertise and his superior work ethic ensure that his Board membership is a valuable resource for Atlantic Gold.

Once again, we thank our shareholders – including our major shareholder Au Mining Limited and several new large shareholders – for their support in our capital raising initiatives, sharing our aim to bring our projects towards production.

On behalf of the company it is with a refreshed sense of conviction that I convey our gratitude to Wally Bucknell for his expertise and tenacity in realising our objectives in Nova Scotia and to all the employees, consultants and contractors who support us.

We look forward with undiminished enthusiasm not only to commencing development of the Touquoy Gold Mine, but also to beginning signifi cant development of the substantial gold potential that rests in Nova Scotia. Th e company’s persistence will lead to providing employment for the keen local workforce, supporting local businesses and suppliers, and not least to providing a return to our loyal and patient shareholders.

Ronald J HawkesChairman28 March 2013

For

per

sona

l use

onl

y

Review of projects

HALIFAX

Scotia Mine

Lunenberg

Bridgewater

Yarmouth

West Caledonia

Caduesky

West Gore

15 MileBrook

TOUQUOYGOLD DEPOSITS656,000 oz

COCHRANE HILLGOLD DEPOSIT

0

N

30km

Historic gold workings

Atlantic Gold farm-ins

Atlantic Gold 100%

Granite

Goldenville group

Halifax groupMeguma Terrane{

Figure 1: The Touquoy and Cochrane Hill Gold Deposits are located in the northeastern Meguma Terrane of the province of Nova Scotia in the southeast of Canada. Exploration in Nova Scotia is targeted at areas of the Meguma Terrane with characteristics similar to existing deposits at Touquoy and Cochrane Hill

2 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

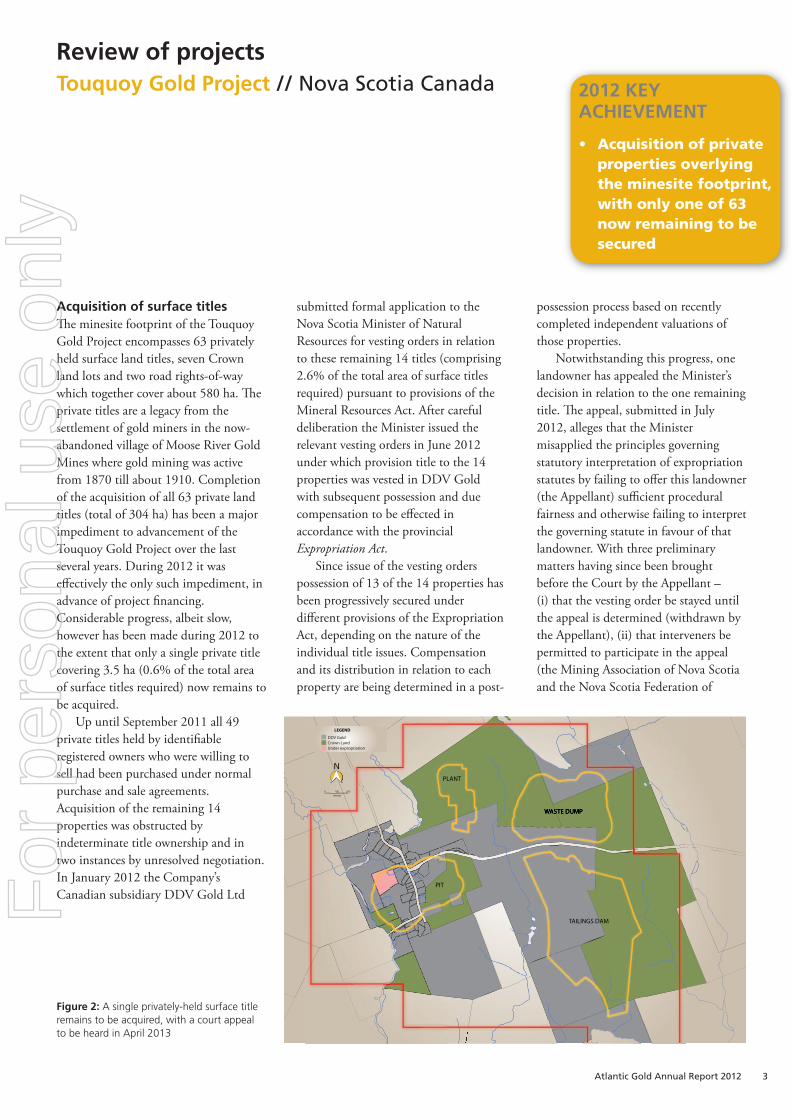

Figure 2: A single privately-held surface title remains to be acquired, with a court appeal to be heard in April 2013

Acquisition of surface titlesTh e minesite footprint of the Touquoy Gold Project encompasses 63 privately held surface land titles, seven Crown land lots and two road rights-of-way which together cover about 580 ha. Th e private titles are a legacy from the settlement of gold miners in the now-abandoned village of Moose River Gold Mines where gold mining was active from 1870 till about 1910. Completion of the acquisition of all 63 private land titles (total of 304 ha) has been a major impediment to advancement of the Touquoy Gold Project over the last several years. During 2012 it was eff ectively the only such impediment, in advance of project fi nancing. Considerable progress, albeit slow, however has been made during 2012 to the extent that only a single private title covering 3.5 ha (0.6% of the total area of surface titles required) now remains to be acquired.

Up until September 2011 all 49 private titles held by identifi able registered owners who were willing to sell had been purchased under normal purchase and sale agreements.Acquisition of the remaining 14 properties was obstructed by indeterminate title ownership and in two instances by unresolved negotiation. In January 2012 the Company’s Canadian subsidiary DDV Gold Ltd

submitted formal application to the Nova Scotia Minister of Natural Resources for vesting orders in relation to these remaining 14 titles (comprising 2.6% of the total area of surface titles required) pursuant to provisions of the Mineral Resources Act. After careful deliberation the Minister issued the relevant vesting orders in June 2012 under which provision title to the 14 properties was vested in DDV Gold with subsequent possession and due compensation to be eff ected in accordance with the provincial Expropriation Act.

Since issue of the vesting orders possession of 13 of the 14 properties has been progressively secured under diff erent provisions of the Expropriation Act, depending on the nature of the individual title issues. Compensation and its distribution in relation to each property are being determined in a post-

possession process based on recently completed independent valuations of those properties.

Notwithstanding this progress, one landowner has appealed the Minister’s decision in relation to the one remaining title. Th e appeal, submitted in July 2012, alleges that the Minister misapplied the principles governing statutory interpretation of expropriation statutes by failing to off er this landowner (the Appellant) suffi cient procedural fairness and otherwise failing to interpret the governing statute in favour of that landowner. With three preliminary matters having since been brought before the Court by the Appellant – (i) that the vesting order be stayed until the appeal is determined (withdrawn by the Appellant), (ii) that interveners be permitted to participate in the appeal (the Mining Association of Nova Scotia and the Nova Scotia Federation of

DDV GoldCrown LandUnder expropriation

LEGEND

N

200100metres

0

WASTE DUMP

TAILINGS DAM

PIT

PLANT

2012 KEY ACHIEVEMENT

Acquisition of private properties overlying the minesite footprint, with only one of 63 now remaining to be secured

•

Review of projectsTouquoy Gold Project // Nova Scotia Canada

Atlantic Gold Annual Report 2012 3

For

per

sona

l use

onl

y

Agriculture so permitted), and (iii) that the appeal be heard as a trial de novo (dismissed by the Court) – the appeal is now set down to be heard on 24–26 and 29 April 2013.

Th e Company fi rmly believes the Minister’s decision was made in accordance with the process set out under Nova Scotia’s Mineral Resources Act after fair, transparent and unhurried consideration of all relevant information received from, and meetings with, the aff ected landowners and Atlantic Gold. Th e Company remains confi dent that this appeal will be dismissed.

It has taken considerable eff ort, diligence, expense, and notably time to reach this critical point in the private surface properties acquisition program. Its conclusion, if successfully achieved as expected, will be a major milestone in the development timeline of the Touquoy Gold Project as the Company prepares to move the Project towards production.

Th e seven Crown land lots, which together comprise 280 ha, are under off er for lease by the Department of Natural Resources (Land Services Branch), subject to appropriate conditions precedent including DDV Gold’s acquisition of all required private properties and receipt of approvals from Nova Scotia Environment (Environmental Assessment Approval (granted) and Industrial Approval). Acquisition of the two public road rights-of-way is subject to DDV Gold’s replacement by alternative routing to the satisfaction of the Nova Scotia Department of Transportation and Infrastructure Renewal.

Final environmental permittingEnvironmental Assessment Approval, the primary and critical environmental permit, has previously been granted for the Touquoy Gold Project and remains in eff ect. In compliance with the terms of this Approval, and in consultation with Nova Scotia Environment and the Department of Natural Resources, a plan to procure appropriate lands near the Project site for the purposes of conservation is being further developed.

Mining Lease ML-11-1, covering 793 ha, was granted by the Department of Natural Resources for a 20 year term in August 2011.

Application for Industrial Approval, the requisite adjunct to Environmental Assessment Approval for the development, operation and reclamation of the Touquoy Gold Project, was submitted to the Minister of Environment pursuant to Part V of the Environment Act of Nova Scotia in November 2012. Th e application is under review and the Company is in ongoing discussion with representatives of Nova Scotia Environment. It is not expected that Industrial Approval will be

granted before acquisition of the last private property is complete. Grant of Industrial Approval will complete the essential licence to develop the Project.

Th e Company looks forward to ongoing cooperation with the Department of Natural Resources and Nova Scotia Environment as it continues to work closely with industry associations from all natural resource sectors, other government departments, First Nations, environmental groups and the local community as it sets the stage for the development of a major and modern gold mining operation long awaited by many in Nova Scotia.

Defi nitive Feasibility StudyTh e Defi nitive Feasibility Study (“DFS”) for the Touquoy Gold Project was originally completed in July 2010 and updated in early 2012 to refl ect costs and revenues where changed from the original DFS. Th e DFS re-affi rms the strong viability of the Touquoy Gold Project as a signifi cant development opportunity. All inputs relating to ore reserves, pit design, mining plan, processing and site infrastructure are unchanged from the original 2010 DFS.

Table 1: Summary results of the Defi nitive Feasibility Study

Ore reserves 9.59 Mt @ 1.49 g/t for 454,000 contained ouncesTotal production 1 422,000 ouncesAnnual production rate (unchanged) 84,000 ouncesPlant All new 2.0 Mtpa conventional gravity/CIL plantMine life 5.0 yearsPre-production capital cost 2 $140 million (nominal). Includes $10 million of working capital and $10 million reclamation bond.Gold price $1600/ozCash operating cost $597/oz. Includes royalty payments of US$37/ozNet cash surplus (pre-tax) $296 millionPayback period 21 months after fi rst gold pourNPV (8%, pre-tax) $178 millionInternal rate of return 47.3%

Note 1: Production excludes 26,000 ounces of in-pit Inferred Resources, and any input from the Touquoy West satellite deposits (previously reported Indicated and Inferred Resources of 2.0 Mt @ 1.5 g/t for 99,000 ounces). DFS remains based on original pit design optimised using a gold price of US$950/oz.Note 2: The DFS is prepared in Canadian dollars. Exchange rates at parity (A$1=C$1=US$1) are used in the Study.

Review of projectsTouquoy Gold Project // Nova Scotia Canada

4 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

HistoryAbout 26,000 ounces of gold were reported to have been recovered from Moose River Gold Mines, site of the Touquoy Project, during the gold rush from 1877 to 1910. Apart from a failed attempt to re-open the mine in 1935-36, the site remained dormant from an exploration, development and production perspective for the next 75 years.Several exploration campaigns, including diamond and percussion drilling and a 57,000 tonne bulk sample, were conducted between 1986 and 2003.

OwnershipAtlantic Gold, through its wholly-owned local subsidiary DDV Gold Limited, entered into an option agreement in May 2003 with the property owners, Moose River Resources Inc (MRRI), a local private company. As the operator and manager of the Touquoy Gold Project DDV Gold sole funds all capital and exploration expenditure. Once gold production at Touquoy has commenced DDV Gold will receive 100% of the Touquoy cashfl ow until all these expenditures plus interest have been recouped. Thereafter DDV Gold will share the pre-tax profi t on a 60:40 basis with the vendor of the Touquoy tenements. A third party holds 3% royalty of which two-thirds can be purchased for $2.5 million. The fi nancial considerations above are net of royalty. Upon DDV Gold’s securing fi nancing for project development its nominal interest in the Exploration Block – defi ned by 77 mineral claims outside the 12-claim Development Block which covers the known resources – increases from 60% to 75%.

GeologyThe Touquoy gold deposit is a shale-hosted, disseminated gold deposit. It is located in the Meguma Group, a belt of sedimentary rocks (Cambro-Ordovician turbidites) extending about 400 km long by 80 km wide through central and southwestern Nova Scotia. Since the fi rst gold discovery in 1861 about sixty underground gold deposits within the Meguma Group have been mined, for a recorded aggregate production of about 1.2 million ounces. The bulk of this production was prior to World War 1. The common geological setting of these many gold deposits is along the crests of anticlinal axes which were mapped over a century ago as extending throughout the length of the Meguma Group.

The Touquoy deposit is similarly located on the crest of an anticlinal axis but is fundamentally different from the many small underground quartz-vein hosted deposits mined historically because the gold mineralisation is disseminated throughout the host sediments. The very wide intersections of relatively even grade gold mineralisation, some in excess of 100 m, and the compact and shallow disposition of the deposit present the Touquoy deposit as a substantial, open-pit, bulk mining proposition with a very favourably low waste:ore ratio.

Th e DFS update was undertaken in association with Merit Engineers Pty Ltd, Ausenco Limited, Australian Mine Design and Development Pty Ltd and Gemell Mining Engineers, all of these parties having been similarly involved with generation of the original DFS.Th e summary in Table 1 refl ects that presented in the Company’s previous Annual Report, though using the current gold price of US$1,600/oz for the revenue returns. Th e capital and operating cost inputs will be next updated once (and assuming) the last private property is eventually acquired, at which time tenders for the mine development and construction of the processing plant and associated infrastructure will be off ered to appropriate parties. Th e project development descriptions following also refl ect those presented in the Company’s previous Annual Report.

As 100% of the Touquoy cashfl ows will be available to service project debt the summary DFS results are reported below on 100% basis (refer to box for ownership details).

Details of the Defi nitive Feasibility Study1. Mining Th e pit is to be developed in two stages with a cutback to the fi nal pit limits in Year 3. Th e fi nal pit will be 760 m long x 400 m wide with a maximum depth of 140 m. Waste-to-ore ratio over life-of-mine is 2.6:1 Mining is planned to be carried out using a leased, owner-operated fl eet of eight 91-tonne payload trucks and two 110-tonne excavators at a projected daily rate of approximately 15,000 tonnes of ore and waste.

2. ProcessingDesign, operation and estimation of capital and operating costs of the Touquoy processing plant have been developed by Ausenco Limited, and

based on comprehensive comminution and metallurgical investigations previously undertaken by Orway Mineral Consultants (WA) Pty Ltd, SGS Lakefi eld Research Limited, Peter Lewis & Associates and Ammtec Limited.

Th e processing plant is designed to treat free milling gold ore at a rate of 2.0 million tonnes per annum using conventional technology. Free gold is recovered using gravity concentration and intensive cyanidation, with the remaining gold recovered by cyanidation in a hybrid carbon-in-leach (CIL) process. Leach residues are detoxifi ed before delivery to the tailings management facility. Th e process plant design is based on a fl ow sheet with unit operations that are well proven in the gold industry.

Th e main areas include:• three-stage crushing of run-of-mine

ore• single-stage ball milling of crushed

ore to a P80 of 150 micron • centrifugal gravity concentration of

gold followed by high intensity cyanidation of the gravity concentrate

• thickening of CIL feed• hybrid leach–CIL using one leach

tank and six adsorption tanks• desorption of precious metals from

carbon using a pressure Zadra elution circuit

• destruction of cyanide in CIL tailings

• pumping of tailings to the tailings management facility for storage.

• Excess site water is treated, for arsenic removal, at a dedicated effl uent treatment plant.

3. InfrastructureTh e mine site is readily accessible by road being located at the former village of Moose River Gold Mines 70 minutes drive along sealed roads from Halifax, the provincial capital. No on-site accommodation will be necessary. During operation the workforce will commute to site from nearby

Atlantic Gold Annual Report 2012 5

For

per

sona

l use

onl

y

communities. Th e site is now serviced by landline telephone, broadband wireless internet and 7.2 kV single phase power.

Maximum power demand is 6 MW, with annual power consumption of 42,000MWh. Connection of 25 kV grid power to site will require construction of 6km of new line and upgrade of 5 km of existing line to site from single phase to three phase power.

A positive water balance prevails at the site. Suffi cient process water is therefore available by recycling from the Tailings Management Facility. Th e minimal fresh and potable water requirement will be sourced locally.

Site facilities will include an administration offi ce, a mobile equipment workshop–warehouse building, reagent storage area, laydown yard, laboratory and miscellaneous process plant buildings.

4. Capital cost estimateTh e capital cost estimate for the project is $140 million:

Table 2: Capital cost estimateITEM $ millionMine 5Process plant 59Tailings management facility 10Site infrastructure 22Other 6EPCM (Engineering, Procurement,Construction Management) 18Sub-total 120Working capital 10Reclamation Bond 10Total 140

The capital cost estimate is based on all new equipment. All Canadian dollars, with currency exchange rate at parity (C$1.00 = US$1.00).All estimates have a base date of Q4 2011.Local labour, services and materials are to be used to the maximum extent feasible.

•

•

••

5. Operating costsTh e total life-of-mine cash operating cost estimate for the Project is $252 million, with unit cash costs of $597/oz.

Table 3: Operating cost estimate TOTAL

LIFE-OF-MINE UNIT COSTS

$ million $/tonne $/oz

Mining 124 12.98 294Processing 88 9.19 209Site administration 22 2.28 52Sub-total 234 24.45 555Off-site costs 2 0.22 5Royalties 16 1.63 37Total 252 26.30 597

6. Implementation ScheduleTh e strategy for project implementation contemplates development under an Engineering, Procurement and Construction Management (“EPCM”) contract. Th e project implementation schedule indicates a duration of 83 weeks from contract award to practical completion. Critical path for the project is delivery of the grinding mill which is presently approximately 50 weeks from placement of order.

Project fi nancingFinancing structures to fund construction of the Touquoy Gold Project continue to be refi ned and evaluated in fi ner detail as the moment of project “de-risking” appears to approach. Indicative responses from a range of major banks confi rm the Company’s view that conventional debt is available to form the major component of the project funding requirement. Th e optimal project funding package will be one which is least dilutive to our existing shareholders.

0 180 360

Metres

N

Existing pit

Proposed pit

Road

Haulroad

Site boundary

Park and museumrelocated

Carpark

Admin

Truck shop

MillROM pad

Crusher

WASTE ROCK PILE

PIT

Ore haulroad

POLISHING POND

Waste haulroad

Square Lake

Scraggy Lake

Fish River

Moose River

TAILINGS POND

Figure 3: The active site, covering a compact area of 265 ha, is located in an area harvested by the forestry industry and directly accessible by sealed public road.

Review of projectsTouquoy Gold Project // Nova Scotia Canada

6 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

OVER 900,000 oz IN-PIT POTENTIALFOR COMBINED NOVA SCOTIA GOLD PROJECTS – TOUQUOY AND COCHRANE HILL

// Nova Scotia Canada

Table 4: Projected conceptual outcomes – 100% BasisTouquoy and Cochrane Hill Gold Projects combined

Th roughput 19.0 Mt @ 1.5 g/t for 970,000 contained ouncesProduction 900,000 ouncesAverage annual production 93,000 ouncesPlant 2 Mtpa Re-located to Cochrane Hill post-TouquoyInitial mine life 9.7 yearsPre-production capital cost $140 millionTotal life-of-mine capital cost $254 millionGold price $1600/ozCash operating cost $646/oz. Includes royalty payments of $37/oz.Net cash surplus (pre-tax) $633 millionPayback period 21 months after fi rst gold pourProject NPV (8%, pre-tax) $320 millionInternal rate of return 48%

Table 5: Nova Scotia Ore Reserves and Mineral Resource inventory

TONNES GRADE CONTAINED GOLD million g/t ounces

ORE RESERVES *

TouquoyProved 2.49 1.48 118,000Probable 7.10 1.47 336,000Total Reserves 9.59 1.48 454,000

MINERAL RESOURCES

TouquoyMeasured resource 2.8 1.5 130,000Indicated resource 7.3 1.5 350,000Inferred resource 1.6 1.5 77,000Total Touquoy 1 11.7 1.5 557,000

Touquoy WestIndicated resource 0.9 1.9 54,000Inferred resource 0.6 2.2 45,000Total Touquoy West 2 1.5 2.0 99,000Total Touquoy Project 13.2 1.5 656,000

Cochrane HillIndicated resource 4.5 1.8 251,000Inferred resource 5.6 1.6 298,000Total Cochrane Hill Project 3 10.1 1.7 549,000TOTAL NOVA SCOTIA 23.3 1.6 1,205,000

* Ore Reserves are included in Mineral Resources, and are not additive. Touquoy Ore Reserves contain no Mineral Resources from Touquoy West. There are an estimated 26,000 additional ounces of gold identifi ed as Inferred Resources within the fi nal pit and which do not form part of the Ore Reserves.Notes 1–3: See page 11.

Review of projects

Th e Touquoy Gold Project represents the fi rst stage of a 10-year production plan of 900,000 ounces for the combined Touquoy and Cochrane Hill Gold Projects. Th is combined production plan involves the re-location of the Touquoy processing plant 80 km to the east to Cochrane Hill upon completion of the Touquoy operation. Cochrane Hill is the Company’s second gold development project in the Nova Scotia goldfi elds.

In addition to the Touquoy DFS this combined production plan considers: (i) production from the Touquoy

Inferred Resources of 26,000 contained ounces located within the designed pit but excluded from the established Ore Reserves and

(ii) recovery of 450,000 ounces gold from Cochrane Hill following completion of the Touquoy operation. It excludes any input from the

satellite resource at Touquoy West (previously reported 2.0 Mt @ 1.5 g/t for 99,000 ounces).

Given the approximation of economic inputs to the development of Cochrane Hill this Extended Case is a study at a conceptual level, and on 100% basis:

Atlantic Gold Annual Report 2012 7

For

per

sona

l use

onl

y

Review of projectsCochrane Hill Gold Project // Nova Scotia Canada

Cochrane Hill is an advanced gold exploration property located 80 km east of Atlantic Gold’s Touquoy Gold Project and where Atlantic Gold has established the following Mineral Resources (as reported to ASX on 18 September 2009, and on 8 March 2011 as Canadian NI43-101 compliant resources):

Table 6: Cochrane Hill Mineral Resources

TONNES GRADE CONTAINED GOLD million g/t ounces

Indicated resource 4.5 1.8 251,000Inferred resource 5.6 1.6 298,000Total Cochrane Hill Project 3 10.1 1.7 549,000

Th is Mineral Resource estimate incorporates results from 39 diamond holes (3,102 m) drilled by Atlantic Gold in 2008 and 2009; 79 holes (11,098 m) drilled during the 1970s and 1980s by previous explorers; and infi ll sampling undertaken by Atlantic Gold on this historic core recovered from storage.

Th e gold mineralisation is developed within a 30 m steeply dipping wide zone of sulphidic and quartz-veined sediments over a length of about 700 m. Coarse (visible) gold is common and the gold is expected to be free-milling on indications from historic testwork and similarities to other gold deposits in this district. Th e mineralised zone plunges gently to the west and it remains open down-plunge in this direction.

Based on this resource inventory and the assumption – to be confi rmed by infi ll drilling yet to be undertaken – that all Inferred Resources can be converted to Measured and Indicated Resources, a conceptual open-pit has been optimised using similar costs and operating plan – 2 Mtpa gravity/CIL – to those presently applicable to the Touquoy Gold Project. For a gold price of US$1050/oz production of 8.9 million tonnes grading 1.7 g/t to recover 450,000 ounces gold (as reported to ASX on 18 September 2009) is indicatively projected:

Following favourable resolution of a third party dispute in relation to the Company’s exercise of its pre-emptive right to purchase 100% interest in the Cochrane Hill gold property, Atlantic Gold completed the purchase mid-year. Th e full purchase price paid to the former owner, Scorpio Gold (Canada) Corporation, was C$1.6 million.

Th e opportunity to acquire 100% interest in the Cochrane Hill Gold Project for what amounts to less than C$3.00 per resource ounce is a very positive step forward in Atlantic Gold’s plan for a minimum one million ounces of gold production from its Nova Scotia properties.

Table 7: Conceptual Cochrane Hill output

GOLD PRICE TONNES GRADE GOLD RECOVERED STRIP RATIO

millions (g/t) ounces

US$875/oz 8.9 1.7 450,000 1:5.8

HistoryGold was fi rst discovered at Cochrane Hill in 1868 with 1354 ounces of gold recovered between 1877 and 1929. Modern exploration commenced in 1974 with 152 diamond core holes and bulk samples.

GeologyAs with the Touquoy Gold Deposit, the Cochrane Hill gold deposit is also developed close to a regional anticlinal axis and in broadly similar fi ne grained sedimentary rocks of the Meguma Group. The 30 m wide mineralised sequence of sulphidic and quartz veined slates which hosts the Cochrane Hill resource is developed within the steeply dipping southern limb of the overturned Cochrane Hill anticline.This mineralised sequence, largely obscured by overburden, has been traced intermittently for 5 km across the property and is identifi ed by several areas of anomalous gold geochemistry. Gold mineralisation that appears to be confi ned to plunging shoots in a similar stratigraphic and structural position to Cochrane Hill has been identifi ed by shallow reconnaissance interface drilling and follow-up diamond drilling by Atlantic Gold between 600 m and 1100 m west of the resource. Further intensive property-wide exploration is yet to be undertaken on this property.

8 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

Review of projectsExploration // Nova Scotia Canada

Th e Nova Scotia goldfi elds, in the so-called Meguma Terrane, are highly prospective for major open-pittable gold reserves similar in style to those at Touquoy and Cochrane Hill. At Touquoy in particular, most of the gold is disseminated throughout dark grey shales devoid of quartz veining. However this unusual style of gold mineralisation in Nova Scotia, now demonstrably commercially viable via open pit mining and conventional gravity/CIL processing, is not widely appreciated. Th erefore, apart from Atlantic Gold’s active, and admittedly insuffi cient, investigations within the Meguma Terrane, regional exploration directed to the discovery of gold reserves of this type has never previously been undertaken.

Furthermore 90% of the Meguma Terrane is estimated to be covered by a veneer of glacial till – on average 5-10 m of unconsolidated sand, clay and boulders transported and dumped during the last ice age. All of the gold deposits known in the Meguma Terrane were found by the “old timers” – and the last gold discovery was reportedly made in the 1890s – only where streams had cut through this overburden and exposed outcropping quartz veins bearing gold. Our careful orientation investigations at Touquoy confi rm that this overburden is geochemically opaque; that is, the geochemical characteristics of soil and plants at surface provide no representation of the bedrock or of the orebody beneath.

Th us in order to effi ciently explore this terrain it is necessary to drill through the overburden and retrieve several metres of bedrock for visual and geochemical analysis. We refer to this as “interface drilling”. In collaboration with a local driller we have developed a reverse circulation drilling rig mounted on a logging transporter, capable of drilling to about 30 m depth and adapted specifi cally for Nova Scotia conditions.

Th e resultant regional exploration land package is a dynamic holding since claims will be dropped and new claims pegged or acquired as results demand. Th e current land position is approximately 400 km2.

Application of this “greenfi elds” work over the last several years has identifi ed a number of (previously described) early stage prospects earmarked for follow-up as exploration funding permits – West Caledonia, Caduesky Lake, East Rawdon, Fifteen Mile Brook and Moses Lake (refer to regional map). Th e Company’s small exploration team based in Moose River undertakes low-cost fi eldwork on these and other gold prospects within the Meguma Terrane, maintains contact with local prospectors and evaluates new opportunities identifi ed through ongoing research.

Directors Wally Bucknell, Ron Hawkes and Rod Hanson inspect core with geologist Caitlin Cameron and visit the Touquoy mini-pit

Atlantic Gold Annual Report 2012 9

For

per

sona

l use

onl

y

In September 2012 Atlantic Gold entered into an option agreement with a private company to earn an interest in the Kemptville gold property located in southwest Nova Scotia (refer to regional map). Atlantic Gold may earn 100% interest in the claims, subject to a 20% carried interest to production in favour of the optionor with aggregate cash payments of $170,000 and expenditure of $1.3 million over 4 years (extendable under defi ned conditions).

Over 3,000 ounces of gold were recovered at Kemptville during 1881–1918 from workings spaced over 600 m. Typically, masking glacial overburden is extensive. Since 1975, 32 diamond core holes have been drilled on the property by previous explorers, with intersections of up to 11.1 m @ 1.9 g/t gold (KV-03-01), 15.1 m @ 0.8 g/t gold (KV-03-02) and 6.3 m @ 5.8 g/t gold (KV-03-03) reported. Of particular signifi cance are two clusters of mineralised boulders from which samples have assayed up to 308 g/t gold (refer to accompanying property plan). Th e previous diamond drilling however does not appear to have intersected the distinctive geochemistry and alteration represented in these mineralised boulders. Th eir source to date remains undiscovered.

A fi rst-pass drilling program of 52 shallow (average 12 m) vertical narrow-diameter reverse circulation (RC) holes on four traverses has now been undertaken over the 1 km-long “main zone” to better defi ne the extent and focus of the known gold mineralisation and to attempt to trace the source of the mineralised boulders.

KEMPTVILLE SH

EAR

272

5m

E

500

mE

272

5m

E

4,881,500 mN

4,882,000 mN

4,881,750 mN

4,881,250 mN

272

00m

E

271

50

mE

271

70

E

20

272

0,0 5

m

, 70

,, ,

KV-03-01KV-03-02

KV-03-03

((

(

(

(

(

(((

(

(

((

(((

(

(((

(( (

((

(

((

(

(

((

(

(

((

(

(

(

((

((

(

((

((

(

(

(

(

(

(

(

N

Historic diamond drill hole

Historic workings

Boulder samples >1 g/t gold

Assay > 0.5 g/t Au

Assay 0.1 - 0.5 g/t Au

All assays < 0.1 g/t Au

Vertical RC hole (DDV Gold drilling)

BED

DIN

G /

FOLI

ATIO

N

MIN

ERA

LISE

DZO

NE

OVERBURDEN

KV-03-

02

(dril

led 20

03)

MRG37

68

MRG37

67

MRG37

66

MRG37

65

MRG37

64

MRG37

63

MRG37

62

MRG37

61

15m15m17m13m

9m6m

16m

114m

6m

1.6m1.2

6.1m1.3

8.0m2.7

-50mRL

0mRL

50mRL

LEGEND

0.1 - 0.5 g/t (RC holes only)

Sampled intervals (DDH hole only)

6.1m1.3

Width (m)Gold (g/t)

0 50m

SENW

BEDDIN

G /

FOLIA

TION

OVERBURDEN

-50mRL

0mRL

50mRL

MRG37

79

MRG37

78

MRG37

77

MRG37

76

MRG37

75

MRG37

74 MRG37

73

MRG37

72

MRG37

71

MRG37

70

MRG37

69

KV-03-

04

(dril

led 20

03)

18m

26m

15m12m9m

9m6m

8m5m

6m9m

93m

2.0m0.7

5.0m1.9

4.0m1.2

2.0m0.6

Single 70cm sampletaken from this

diamond core hole

LEGEND

0.1 - 0.5 g/t (RC holes only)

6.1m1.2 Width (m)

Gold (g/t)

> 0.5 g/t (RC holes only)

0 50m

SENW

Figure 4: Widespread gold geochemical anomalism, as indicated on the plan above and sections below, is being followed up at the Kemptville gold property located in southwest Nova Scotia

Review of projectsExplorationNova Scotia Canada

10 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

Notes to Table 2: Nova Scotia mineral resource inventoryNote 1:Estimation technique: Multiple Indicator Kriging with block variance adjustment applied. Ore selectivity is assumed to be 5 metres (north) by 5 metres (east) by 2.5 metres (elevation) via an open pit mining scenario.Drillholes: 298 NQ diamond core holes for 27,200 m of which Atlantic Gold has drilled 129 holes for 10,480 m.Variable spacing, averages 30 m x 20 m.Assay methodology (all based on ½ NQ core):ATV: Fire assay of pulverised whole-sample (32% of database), with all samples ≥ 0.5 g/t or within ore-grade intervals screen fi re assayed (1825 samples or 6% of database).Historic: Whole-sample fi re assay of +100# gravity concentrate weight–averaged with fi re assay of -100# fraction (28% of database) adjusted in accordance with Atlantic Gold’s trial grade control study, fi re assay of pulverised split from crushed parent (28% of database) and screen fi re assay (6% of database).Bulk density: 2.80 g/cm3. Based on 183 determinations.Lower cut-off grade: 0.5 g/t, to maximum depth of 150 m.Note 2:Estimation technique: Multiple Indicator Kriging with block variance adjustment applied. Ore selectivity is assumed to be 5 metres (north) by 2 metres (east) by 2.5 metres (elevation) via an open pit mining scenario.Assay methodology (all based on ½ NQ core):Fire assays on pulverised split from crushed parent from 116 diamond drill holes.Bulk density: 2.80 g/cm3.Lower cut-off grade: 1.0 g/t.Drillhole spacing: Variable, averages 30 m x 25 m.Note 3:• Estimation technique: Multiple Indicator Kriging with block variance adjustment applied. Data fl agged to mineralised

wireframe. Ore selectivity is assumed to be 4 metres (north) by 8 metres (east) by 2.5 metres (elevation) via an open pit mining scenario.

• Lower cut-off grade 0.5g/t• All Atlantic Gold holes are NQ diameter with half sawn core sampled at 1m intervals and fi re assayed following total

sample pulverisation.• Atlantic Gold’s quality control procedures include routing submission of drill core blanks and accredited standards,

together with selected submission of blank standards immediately following samples containing visible gold. • Bulk density: 2.76g/cm3 (67 mineralised samples).• Resource estimate based on 6,665 sample assays from 39 holes (3,102 m) drilled by Atlantic Gold and 79 holes

(11,098 m) drilled in the 1970s and 1980s. Samples from historic holes fi re assayed, with screened fi re assay on samples bearing visible gold. Results for the 56 underground drillholes (table below) are considered unreliable and have not been used. Seventeen historic surface holes are located beyond the resource limits.

• All samples (six) over 100 g/t cut to 100 g/t.• Hole spacing: Averages 20 m x 20 m in the central portion of the deposit to a depth of 100 m from surface. Outside

this area the drilling sections average 30 metre centres and holes on section are irregularly spaced. • Details of previous diamond drilling campaigns:

Company Year Location No. holes Metres Core size/sampleMassval Mines 1974 Surface 44 4840 A,BQ/splitNorthumberland 1981 Surface 21 3932 A,BQ/splitScominex 1984-87 Surface 31 5107 NQ/sawnScominex 1984-87 Underground* 28 830 NQ/sawnNovagold 1988 Underground* 28 2044 NQ/sawn

152 16753 *Assays from underground drilling have not been used in present resource estimate.

• Bulk sampling: Approximately 14,900 tonnes from 25,000 tonnes development material excavated from surface and underground during 1982-88 were treated by various means:

Company Year Sample type Tonnage Treated Grade (g/t)Northumberland 1982-83 Pit 13,500 13,041 1.6Scominex 1987 Underground 4,443 2.8 1.9Novagold 1988 Underground 7,400 1860 2.1

• Details as to grade control methodology, metallurgical recovery and sample representivity applying at the time are not clear and resultant grades are therefore considered unreliable. These, and the historic tonnage mined (approx 32,000 tonnes in total), have not been deducted from the resource estimate.

The geological information in this report relating to exploration and Mineral Resources has beencomplied by WR Bucknell who is a director of Atlantic Gold NL and a Member of the AustralasianInstitute of Mining and Metallurgy (AusIMM). He has suffi cient experience which is relevant to the styleof mineralisation and type of deposit under consideration to qualify as a Competent Person in respect of the 2004 Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the JORC Code).The resource estimates for Touquoy and Cochrane Hill described in this report were completed by Mr Neil Schofi eld, a principal of Hellman and Schofi eld Pty Ltd. Mr Schofi eld is a Member of AusIMMand qualifi es as a Competent Person in respect of the 2004 JORC Code by virtue of having suffi cientexperience which is relevant to the Touquoy style of mineralisation and deposit type. Mr Schofi eld hasconsented to the inclusion of this information in the form and context in which it appears in this report.The resource estimate for Touquoy West described in this report was completed by Mr Nic Johnson, an employee of Hellman and Schofi eld Pty Ltd. Mr Johnson is a Member of AIG and qualifi es as aCompetent Person in respect of the 2004 JORC Code by virtue of having suffi cient experience which is relevant to the Touquoy West style of mineralisation and deposit type. Mr Johnson has consented to theinclusion of this information in the form and context in which it appears in this report.

Th e best result from this program was 2.7 g/t gold over 8 m1 from 8 m depth (~5 m true width, to end-of-hole) from an apparent 15 m-wide zone partially addressed by old workings. Th e mineralisation is hosted in very strongly sheared greywackes (mylonites) within the so-called Kemptville Shear , and is strengthening towards the northeast. (Refer to accompanying plan and sections).

Re-logging and infi ll sampling of the available diamond drill core is being conducted to further characterise and extend the mineralisation. Only about a quarter of the 4,000 m of core from the 32 diamond holes drilled on this property since 1975 has been sampled, and about 2,900 m of core (from 21 diamond holes) remains intact.

Assay results so far received indicate widespread gold geochemical anomalism with some extended intervals of sub-ore grade (to 0.3 g/t gold over 16 m) and occasional isolated spikes (max 61.2 g/t gold over 1 m) to be generally associated with more intense quartz veining. Th ese investigations are ongoing.

Atlantic Gold has now secured about 20 km strike length elsewhere along the prospective northeast trending Kemptville Shear, through options and pegging in its own right. Th e Kemptville mineralisation was discovered in 1881 by virtue of its exposure as a window of outcrop. Apart from minor outcrop to the southwest, the Kemptville Shear is obscured by glacial overburden, and as such remains eff ectively unexplored. Further work here is planned in 2013.

1 All RC assays are fi re assay of 0.5 kg grab samples of 2 m composites. i.e. not riffl e-split.

Atlantic Gold Annual Report 2012 11

For

per

sona

l use

onl

y

Corporate governance statement

Th e Company’s corporate governance policies have been formulated to ensure that it is a responsible corporate citizen. Th is statement outlines the main corporate governance practices that are in place and which comply with the Australian Stock Exchange Corporate Governance Council recommendations, unless stated otherwise. Th is statement is organised under headings based on the Australian Securities Exchange (ASX) Corporate Governance Council’s Corporate Governance Principles and Recommendations (2nd edition August 2007 with 2010 amendments).

1 Lay solid foundations for management and oversightEstablish and disclose the respective roles and responsibilities of board and management1.1 Establish and disclose the functions reserved to the board and those delegated to senior executives.

Th e directors are responsible to shareholders for the overall corporate governance of the Atlantic Gold Group including its strategic direction, establishing goals for management and monitoring of achievement of these goals. Th e board has also established a framework for the management of the Consolidated Entity including a system of internal control, a business risk management process and the establishment of appropriate ethical standards. Th e board delegates responsibility for day-to-day management of the Company to the Chief Executive Offi cer (CEO). However, the CEO must consult the Board on matters that are sensitive, extraordinary or of a strategic nature.

1.2 Disclose the process for evaluating the performance of senior executives.Th e performance of senior executives is continuously assessed against functions and milestones specifi ed in their contracts of employment, which is considered appropriate for a company of this size.

1.3 Provide the information indicated in the Guide to reporting on Principle 1.Th e Company’s Board Charter is available on the Company’s website.

2 Structure the board to add valueHave a board of an eff ective composition, size and commitment to adequately discharge its responsibilities and duties2.1 A majority of the board should be independent directors.

Th e board consists of non-executive chairman Mr Ronald Hawkes, non-executive directors Mr Robert Symons and Mr Rodney Hanson and executive director and chief executive offi cer Mr Wally Bucknell. Messrs Symons and Hanson are considered independent directors. Mr Hawkes may be considered as not independent as a long-term major shareholder in the Company. On 1 January 2013 the board appointed an additional non-executive director Mr Rod Hanson. Th e size and composition of the Board is considered appropriate to a company of this size. Independent professional advice can be obtained by directors at the Company’s expense on authority of the board or the CEO.

2.2 The chair should be an independent director.Th e Chairman, Mr Ronald Hawkes may be considered as not independent as a long-term major shareholder in the Company. Mr Hawkes brings to the Board extensive experience in the gold mining industry in Australia and Canada. Th e Company considers that Mr Hawkes acts in the best interest of the Company at all times.

2.3 The roles of chair and chief executive offi cer should not be exercised by the same individual.Mr Ronald Hawkes is Chairman and Mr Wally Bucknell is Executive Director and CEO.

2.4 The board should establish a nomination committee.Th is role is performed by the Board which is considered appropriate for a company, and a board of directors, of this size.

2.5 Disclose the process for evaluating the performance of the board, its committees and individual directors.Th e performance of the Board, committees, individual directors and offi cers is continuously assessed which is considered appropriate for a board, and a company, of this size.

2.6 Provide the information indicated in the Guide to reporting on Principle 2.Th e Company is committed to providing a fair and equitable workplace, free from discrimination related to age, gender, ethnic, cultural or other personal factors, in which the exchange of ideas, experiences and perspectives benefi ts all employees and the communities in which we operate.Th e Board Charter is available on the Company’s website. Additional information is provided in the Directors’ Report.

12 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

3 Promote ethical and responsible decision makingActively promote ethical and responsible decision making3.1 Establish and disclose a code of conduct to guide as to:

the practices necessary to maintain confi dence in the company’s integrity; the practices necessary to take into account their legal obligations and the reasonable expectations of their stakeholders; the responsibility and accountability of individuals for reporting and investigating reports of unethical practices.

All directors, offi cers and employees are expected to act with the utmost integrity and objectivity, striving at all times to enhance the reputation and performance of the Company. Th e Code of Conduct is available on the Company’s website.

3.2 Establish a policy concerning diversity including measurable objectives for achieving gender diversity and for the board to assess annually both the objectives and progress in achieving them.

Th e Company has established a Diversity Policy, which includes objectives for achieving gender diversity and for the board to review annually both the policy and progress in achieving the objectives.

3.3 Disclose the measurable objectives for achieving gender diversity and progress towards achieving them.At this time, given the size and composition of the Company’s workforce, the Board has not formalised measurable objectives for achieving gender diversity, however it is committed to providing equal employment opportunity and a fair and equitable workplace, free from discrimination.

3.4 Disclose the proportion of women employees in the whole organisation, women in senior executive positions and women on the board.

Th e proportion of women in the whole organisation, in senior executive positions and on the Board as at the date of this Report are as follows: 2012 2011Whole organisation 3 out of 11 27% 2 out of 7 29%Senior Executive positions 1 out of 3 33% 1 out of 3 33%Board 0 out of 4 0% 0 out of 3 0%In addition to the employees included in the above table, the Company engages contractors from time to time and at all times provides equal employment opportunity to men and women.

3.5 Provide the information indicated in the Guide to reporting on Principle 3.Th e Code of Conduct and the Diversity Policy are available on the Company’s website.

4 Safeguard integrity in fi nancial reportingHave a structure to independently verify and safeguard the integrity of the company’s fi nancial reporting4.1 The board should establish an audit committee.

Th e Board has appointed an Audit Committee. Th e Board has adopted an Audit Committee Charter which is available on the Company’s website.

4.2 Structure the audit committee so that it consists of: only non-executive directors majority of independent directors an independent chairman, who is not chairman of the board at least three members.

Th e members of the Audit Committee are Mr Robert Symons (Chairman), Mr Ronald Hawkes and Mr Rod Hanson. Messrs Symons and Hanson are considered independent directors. Mr Hawkes may be considered as not independent as a long-term major shareholder in the Company. Th e size and structure of the Audit Committee are considered appropriate for a company, and a board of directors, of this size.

4.3 The audit committee should have a formal charter.Th e Audit Committee Charter is available on the Company’s website.

4.4 Provide the information indicated in the Guide to reporting on Principle 4.Further details of members of the Audit Committee are available in the Directors’ Report. Th e Audit Committee Charter is available on the Company’s website. Th e engagement of auditors, including rotation of individuals playing a signifi cant role in the audit, is considered annually.

Atlantic Gold Annual Report 2012 13

For

per

sona

l use

onl

y

5 Make timely and balanced disclosurePromote timely and balanced disclosure of all material matters concerning the company5.1 Establish and disclose written policies and procedures designed to ensure compliance with ASX Listing Rule disclosure

requirements and to ensure accountability at a senior executive level for that compliance.Th e Company provides information on its activities and fi nancial position quarterly, half-yearly and annually. Th e CEO is responsible for overseeing disclosure of Information to the ASX in accordance with continuous disclosure requirements contained in the ASX Listing Rules, and communication of information to the media, analysts, brokers and shareholders. Reports and releases provided to the ASX are available on the Company’s website for shareholders and other interested parties to review. Th e Company’s Continuous Disclosure Policy is available on its website.

5.2 Provide the information indicated in the Guide to reporting on Principle 5.A copy of the Continuous Disclosure Policy is available on the Company’s website.

6 Respect the rights of shareholdersRespect the rights of shareholders and facilitate the eff ective exercise of those rights6.1 Design and disclose a communications policy for promoting effective communication with shareholders and encouraging their

participation at general meetings.Th e board aims to ensure that shareholders are informed of all major developments aff ecting the Company’s state of aff airs. Th e board has adopted the following Communications Strategy: Th e annual report is distributed to all shareholders (unless a shareholder has specifi cally requested not to receive

the document). Th e Board ensures that the annual report includes relevant information about the operations of the Company during the year, changes in the state of aff airs of the Company and details of future developments, in addition to other disclosures required by the Corporations Act 2001.

Th e half yearly report contains summarised fi nancial information and a review of the operations of the Company during the period. Th e report is prepared in accordance with the requirements of Australian Accounting Standards and the Corporations Act 2001. Th e report is sent to any shareholder upon request.

Quarterly Cashfl ow and Activities Report is submitted each quarter to the ASX. Proposed major changes in the Company which may impact on share ownership rights are submitted to a vote of

shareholders.Th e Board encourages full participation of shareholders at the Annual General Meeting to ensure a high level of accountability and identifi cation with the Company’s strategy and goals. Important issues are presented to shareholders as single resolutions.Th e Company’s website provides up to date information to shareholders and other interested parties in relation to the Company’s activities, information on its projects, history of the Company and copies of announcements and reports released to the ASX. In addition, reports and releases are sent by email to shareholders and other interested parties at their request. Emails addresses are verifi ed and kept confi dential in accordance with privacy legislation.

6.2 Provide the information indicated in the Guide to reporting on Principle 6.Th e Communications Strategy is available on the Company’s website.

Corporate governance statement

14 Atlantic Gold Annual Report 2012

For

per

sona

l use

onl

y

7 Recognise and manage riskEstablish a sound system of risk oversight and management and internal control7.1 Establish and disclose policies for the oversight and management of material business risks.

A Risk Management Policy has been adopted which is designed to allow the board to identify and manage the material business risks and statutory fi nancial reporting and continuous disclosure risks associated with the company’s activities. Th e Risk Management Policy is available on the Company’s website.

7.2 Require management to design and implement the risk management and internal control system to manage the company’s material business risks and report to it on whether those risks are being managed effectively.

Th e CEO is responsible for implementing the risk management strategies approved by the board. Material business risks are monitored continuously. A Risk Management Plan, identifying and assessing each risk and proposing an appropriate strategy for its management, has been developed and is reviewed, updated and submitted to the Board at least annually. Th e CEO has reported to the Board on his review of the Risk Management Plan for the current period in accordance with this paragraph.

7.3 Disclose whether the board has received assurance from the CEO and CFO that the declaration in accordance with s.295A of the Corporations Act is founded on a sound system of risk management and internal control and that the system is operating effectively in all material respects in relation to fi nancial reporting risks.

Th e Board has received a statement in writing from the CEO and CFO attesting to the above.7.4 Provide the information indicated in the Guide to reporting on Principle 7.

Th e Risk Management Policy is available on the Company’s website.

8 Remunerate fairly and responsiblyEnsure that the level and composition of remuneration is suffi cient and reasonable and that its relationship to performance is clear8.1 The board should establish a remuneration committee.

Th e Board has appointed a Remuneration Committee. Th e Board has adopted a Remuneration Committee Charter which is available on the Company’s website.

8.2 The remuneration committee should be structured so that it: consists of a majority of independent directors is chaired by an independent director has at least three members.

Th e members of the Remuneration Committee are Mr Robert Symons (Chairman), Mr Ronald Hawkes and Mr Rod Hanson. Messrs Symons and Hanson are considered independent directors. Mr Hawkes may be considered as not independent as a long-term major shareholder in the Company. Th e size and composition of the Remuneration Committee is considered appropriate to a company of this size.

8.3 Clearly distinguish the structure of non-executive directors’ remuneration from that of executive directors and senior executives.

Non-executive directors receive a fi xed fee for their services as directors of the Company. Th e aggregate sum of fees paid to non-executive directors is approved by shareholders. Where shareholders have approved the issue of share options to non-executive directors, such share options are issued at premium to the share price at the time of issue. Any benefi t to directors will only accrue from an increase in share price.

8.4 Provide the information indicated in the Guide to reporting on Principle 8.Th e Remuneration Committee Charter is available on the Company’s website.

Please refer to the Company’s website www.atlanticgold.com.au/corpgov.

Atlantic Gold Annual Report 2012 15

For

per

sona

l use

onl

y

16 Atlantic Gold Annual Report 2012

Directors’ report

The directors present their report together with the fi nancial report of Atlantic Gold NL and the Group, being Atlantic Gold NL (the Company) and its subsidiaries and the Group’s interest in associated and jointly controlled entities, for the fi nancial year ended 31 December 2012, and the Auditor’s Report thereon.

DirectorsThe names of directors in offi ce at any time during or since the end of the fi nancial year are shown below. All directors have been in offi ce since the start of the fi nancial year to the date of this report unless otherwise noted.

Mr Robert H N SymonsBA LLB (Hons)Independent non-executive director

Qualifi cations and experienceBoard member since31 December 2005 Mr Symons is general counsel and practice director and a former senior partner of the law fi rm Norton Rose Australia (formerly Deacons). He has extensive experience in many aspects of corporate and commercial legal practice with particular expertise in resources, energy and infrastructure.He is a member of the Audit Committee and the Remuneration Committee.

Mr Ronald J HawkesBSc, FAusIMM, FGACNon-executive chairman

Qualifi cations and experienceBoard member since18 January 1999Mr Hawkes has 48 years’ experience in the mining industry and was formerly the Managing Director of Plutonic Resources Limited.He is a member of the Audit Committee and the Remuneration Committee.

Mr Wally R BucknellBSc (Hons), FAusIMM, FGAC, MSEGExecutive director

Qualifi cations and experienceBoard member since18 January 1999Mr Bucknell has 44 years’ experience in the mining industry and was formerly the General Manager – Exploration of Plutonic Resources Limited.

Company SecretaryJulie FidlerMs Fidler was appointed to the position of company secretary on 10 December 2003. She assisted with company secretarial functions in the company for 3 years prior to being appointed Company Secretary.

Directors’ report

There are no offi cers of the company during the fi nancial year who were previously partners of the current audit fi rm, KPMG, at a time when KPMG undertook an audit of the company.

Mr Rodney J HansonBe(Min)(Hons), MBA, FAusIMM, MAICDIndependent non-executive director

Qualifi cations and experienceAppointed1 January 2013Mr Hanson has over 40 years’ experience in mine development, operations, project evaluation and corporate management roles, principally in gold but also in base metals and coal. He has managed mines and projects in Australia, the Pacifi c Islands and China. He is currently a non-executive director of ASX-listed Dampier Gold Limited.

For

per

sona

l use

onl

y

Atlantic Gold Annual Report 2012 17

Directors’ meetings heldThe number of directors’ meetings (including meetings of committees of directors) and number of meetings attended by each of the directors of the company during the fi nancial year are: AUDIT REMUNERATION BOARD COMMITTEE COMMITTEE

Meetings held 14 1 1Meetings attended: R J Hawkes 14 1 1 W R Bucknell 14 – – R H N Symons 14 1 1 R J Hanson – – –

Principal activitiesThe principal activity of the Group during the fi nancial year was precious minerals exploration, primarily for gold. There was no change in the nature of the Group’s principal activity during the fi nancial year.

Operating resultsThe consolidated loss of the Group after income tax amounted to $1,783,154 (2011 loss $1,219,668).

Dividends paid or recommendedNo dividends have been paid or declared during the year. The directors do not recommend the payment of a dividend in respect of the year ended 31 December 2012.

State of affairsThe company made the following issue of shares during the year to provide additional working capital:• Issue of 25,000,000 ordinary shares at 3 cents per share pursuant to placement raising $750,000.• Issue of 91,639,916 ordinary shares at 3 cents per share pursuant to rights issue raising $2,749,197.• Issue of 22,735,000 ordinary shares at 3 cents per share pursuant to placement raising $682,050.

Share performance and shareholder wealthThe company’s share price at the beginning of the period was 3.1 cents and 3.4 cents at the end of the period. During the period the share price ranged from a low of 2.6 cents to a high of 4.5 cents. There was no return of capital to shareholders.

Non-audit servicesDuring the year KPMG provided to the Group audit services amounting to $70,000 (2011: $65,400), taxation services amounting to $8,547 (2011: $6,269) and other assurance services amounting to $9,875 (2011: $5,600). The directors are satisfi ed that provision of taxation services or other assurance services does not compromise audit independence.

Events subsequent to balance dateMr Rodney J Hanson was appointed as a director of the Company on 1 January 2013.

The Company issued 74,000,000 shares on 13 March 2013 pursuant to placement at 3.5 cents per share raising $2,590,000.

DDV Gold Limited has signed an extension of the loan agreement with Brianna Holdings Pty Ltd to 31 July 2014. The loan is still able to be paid in advance at any time without penalty.

There has not arisen in the interval between the end of the fi nancial year and the date of this report any other item, transaction or event of a material or unusual nature likely, in the opinion of the directors of the Company, to affect signifi cantly the operations of the Group, the results of those operations, or the state of affairs of the Group, in future fi nancial years.

Likely developmentsThe Group will continue to focus on the further advancement of the Touquoy and Cochrane Hill Gold Projects and gold exploration in Nova Scotia, Canada.

For

per

sona

l use

onl

y

18 Atlantic Gold Annual Report 2012

Remuneration report – auditedThe Remuneration Committee is responsible for making recommendations to the Board on remuneration policies applicable to Board members and senior executives of the Company. The broad remuneration policy is to ensure the remuneration package properly refl ects the person’s duties and responsibilities and that remuneration is competitive in attracting and retaining appropriately qualifi ed and experienced directors and executives.

The terms of employment for senior executives directly employed by the Company are unlimited in term, with statutory notice and termination provisions.

The aggregate sum that may be paid in directors’ fees to non-executive directors is determined by a resolution of shareholders. The aggregate sum may be divided among those directors in such proportion and manner as they agree or in default of agreement equally. Shareholders approved an aggregate remuneration that may be paid to non-executive directors of $200,000 at the Annual General Meeting on 21 May 2004.

Fixed compensation consists of base compensation which is calculated on a total cost basis and includes employer contributions to superannuation funds. Compensation levels are reviewed annually by the Remuneration Committee through a process that considers individual, segment and overall performance of the Group. A senior executive’s compensation is also reviewed on promotion.

The Company to date has not granted other benefi ts.

SHORT TERM POST EMPLOYMENT % OF TOTAL SALARY DIRECTORS’ FEES CONSULTING FEES CASH BONUS % REMUNERATION SUPERANNUATION TOTAL AUD AUD AUD AUD % AUD AUD

2012DirectorsR J Hawkes – 60,000 – – – 8,168 68,168W R Bucknell 268,200 – – 40,000 1 12% 27,855 336,055R H N Symons – 30,000 – – – 2,700 32,700R J Hanson 2 – – – – – – –

There were no termination benefi ts, non-monetary benefi ts or share-based payments relating to options or rights during the year.

2011 - restatedDirectorsR J Hawkes – 60,000 78,000 3 – – 5,400 143,400W R Bucknell 260,400 – – – – 23,436 283,836R H N Symons – 30,000 – – – 2,700 32,700

There were no termination benefi ts, non-monetary benefi ts or share-based payments relating to options or rights during the year.Notes:1 In October 2012 the Remuneration Committee decided to pay a discretionary cash bonus to Mr Bucknell of $40,000 in recognition of his services in

advancing the Touquoy Gold Project through granting of vesting orders by the Province of Nova Scotia, successful completion of the purchase of the Cochrane Hill Gold Project and management of the regional exploration program which continued to identify areas of interest for further more detailed exploration.

2 Mr Hanson was appointed to the Board on 1 January 2013.3 In 2012 Mr Hawkes submitted invoices totalling $198,000 for services rendered in previous years - $120,000 for 2010 and $78,000 for 2011. These were

services rendered in addition to his duties as Chairman of the Company. Directors, Mr Symons and Mr Bucknell, agreed to pay these amounts in recognition of the signifi cant additional services provided by Mr Hawkes during the 2010 and 2011 years, and during previous years for which no such recognition has been sought. These services included attendance at meetings with corporate advisers, investors and potential investors, banks and other fi nancial lenders in Australia, Canada and other jurisdictions, promoting the Company and in particular the Touquoy Gold Project.Mr Hawkes has advised the Company that there will be no charge for any additional services in 2012 and will in future submit timely invoices for any such additional services.

Directors’ reportF

or p

erso

nal u

se o

nly

Atlantic Gold Annual Report 2012 19

Options provided as remunerationThe Company’s approved Employee Share Option Plan has no performance criteria and options over ordinary shares in the Company provided as remuneration to directors and specifi ed executives pursuant to the Employee Share Option Plan have progressive vesting: 20% of the grant is vested on issue, with 30% vested one year later and the balance of 50% vested after 2 years. Unless exercised the options expire 4 years from date of issue. The options cannot be transferred and will not be listed on the Australian Securities Exchange (ASX).

On 29 August 2008 the Company issued 2,000,000 options to Mr Bucknell under the Employee Share Option Plan. These options lapsed on 28 August 2012.

On 9 March 2010 the Company issued 400,000 fully vested options to Mr A A Pilkington pursuant to contract of employment. These options lapsed on 14 October 2012.

Options granted as remuneration NO. OF OPTIONS NO. OF OPTIONS EXERCISE ISSUED DURING LAPSED DURING OUTSTANDING VESTED DURING VESTED PRICE ISSUE DATE EXPIRY DATE THE YEAR THE YEAR AT 31 DEC 2012 THE YEAR AT 31 DEC 2012

$

DirectorsW R Bucknell 0.155 29 Aug 08 28 Aug 12 – 2,000,000 – – –ExecutivesA A Pilkington 0.15 03 Mar 10 14 Oct 12 – 400,000 – – –

Ordinary shares held by directors and executives BALANCE AT GRANTED AS EXERCISE OF PURCHASE BALANCE AT 1 JAN 2012 COMPENSATION OPTIONS OF SHARES 31 DEC 2012

Fully paid ordinary sharesDirectorsR J Hawkes 27,256,561 – – – 27,256,561W R Bucknell 6,289,479 – – 1,126,013 7,415,492R H N Symons 493,500 – – 102,250 595,750R J Hanson 2,608,090 – – 459,487 3,067,577Partly paid ordinary sharesDirectorsR J Hawkes 5,750,000 – – – 5,750,000W R Bucknell 1,036,860 – – – 1,036,860R H N Symons – – – – –R J Hanson 330,732 – – – 330,732

Directors’ interestsThe relevant interest of each Director in the share capital of the companies within the Group as notifi ed by the Directors to the Australian Stock Exchange in accordance with section 205G(1) of the Corporations Act 2001, at the date of this report is as follows: FULLY PAID SHARES PARTLY PAID SHARES OPTIONS

R J Hawkes 27,256,561 5,750,000 –W R Bucknell 7,415,492 1,036,860 –R H N Symons 595,750 – –R J Hanson 3,067,577 330,732 –

[End of Audited Remuneration Report]

For

per

sona

l use

onl

y

20 Atlantic Gold Annual Report 2012

Environmental regulationThe Group’s operations are subject to signifi cant environmental regulation under the laws of both Australia and Canada. The directors are not aware of any breaches of the legislation during the fi nancial year which are material in nature.

Indemnifi cation and insurance of offi cers and auditorsThe Company has entered into an agreement to indemnify the following current directors of the Company, Mr Ronald J Hawkes, Mr Walter R Bucknell, Mr Robert H N Symons and Mr Rodney J Hanson, and the Company Secretary, Ms Julie Fidler, against any liability, including costs and expenses incurred in defending such actions, incurred by that person that may arise from their position as a director or offi cer of the Company and its Controlled Entities, except where the liability arises out of conduct involving a lack of good faith.

During the year to 31 December 2012 the Company has paid insurance premiums in respect of the directors’ and offi cers’ liability and legal expenses insurance contracts for current directors and offi cers of the Company and its Controlled Entities. The insurance policy prohibits disclosure of the amount of the premium and of the nature of the liabilities covered.

Lead Auditor’s Independence Declaration Under Section 307C of the Corporations Act 2001The lead auditor’s independence declaration is set out on page 21 and forms part of the Directors’ Report for the year ended 31 December 2012.

Signed in accordance with a resolution of the Board of Directors.

W R Bucknell, DirectorSydney, 26 March 2013

Directors’ report

Brian Bolton (General Manager Corporate), Wally Bucknell (Executive Director) and John Utley (Senior Geologist) represented Atlantic Gold at Mines & Money 2013 in Hong Kong in March 2013

For

per

sona

l use

onl

y

Atlantic Gold Annual Report 2012 21

Lead auditor’s independence declaration

Lead Auditor’s Independence Declaration under Section 307C of the Corporations Act 2001

To the Directors of Atlantic Gold NL

I declare that, to the best of my knowledge and belief, in relation to the audit for the fi nancial year ended 31 December 2012 there have been:

(i) no contraventions of the auditor independence requirements as set out in the Corporations Act 2001in relation to the audit; and

(ii) no contraventions of any applicable code of professional conduct in relation to the audit.

KPMG

Shane O’ConnorPartner

Sydney26 March 2013

For

per

sona

l use

onl

y

22 Atlantic Gold Annual Report 2012

Consolidated statement of comprehensive incomeFor the year ended 31 December 2012

NOTE CONSOLIDATED

2012 2011

$ $

Continuing operationsOther income 2 – 4,884Impairment of exploration assets 2 (675,257) (615,658)General and administrative expenses 2 (1,072,061) (707,186)Results from operating activities (1,747,318) (1,317,960)

Financial income 31,761 98,307Financial expenses (67,597) (15)Net fi nance income/(expense) (35,836) 98,292

Loss before income tax (1,783,154) (1,219,668)

Income tax expense 4 – –Loss for the year (1,783,154) (1,219,668)

Other comprehensive incomeForeign currency translation differences for foreign operations 50,834 (297,933)Net change in fair value of available for sale assets (34,902) (64,332)Other comprehensive income/(loss) for the yearnet of income tax 15,932 (362,265)

Total comprehensive loss for the year (1,767,222) (1,581,933)

Basic and diluted earnings per share (cents per share) 5 (0.28) (0.25)

The consolidated statement of comprehensive income is to be read in conjunction with the notes to the fi nancial statements set out on pages 26 to 43.

For

per

sona

l use

onl

y

Atlantic Gold Annual Report 2012 23

Consolidated statement of fi nancial positionAs at 31 December 2012

NOTE CONSOLIDATED

2012 2011

$ $

Current assetsCash and cash equivalents 6 1,028,960 1,473,999Trade and other receivables 7 800,801 251,985Prepayments 36,762 13,903Total current assets 1,866,523 1,739,887 Non-current assets Receivables 8 173,297 124,564Other fi nancial assets 9 31,925 70,727Property, plant and equipment 10 3,595,153 3,218,840Exploration and evaluation assets – intangibles 11 20,361,944 18,580,710Total non-current assets 24,162,319 21,994,841Total assets 26,028,842 23,734,728

Current liabilities Trade and other payables 12 249,274 1,266,096Loans and borrowings 13 1,000,000 –Employee benefi ts 232,596 190,000Total current liabilities 1,481,870 1,456,096

Non-current liabilities Employee benefi ts 10,200 7,300Total non-current liabilities 10,200 7,300Total liabilities 1,492,070 1,463,396 NET ASSETS 24,536,772 22,271,332

Share capital 14 50,792,939 46,760,277Reserves (1,175,750) (1,191,682)Accumulated losses (25,080,417) (23,297,263)TOTAL EQUITY 24,536,772 22,271,332

The consolidated statement of fi nancial position is to be read in conjunction with the notes to the fi nancial statements set out on pages 26 to 43.

For

per

sona

l use

onl

y

24 Atlantic Gold Annual Report 2012

FOREIGN

CURRENCY FAIR

SHARE TRANSLATION VALUE OPTIONS RETAINED TOTAL

CAPITAL RESERVE RESERVE RESERVE EARNINGS EQUITY

$ $ $ $ $ $

CONSOLIDATED2011Balance 1 January 2011 43,412,914 (1,272,976) 15,990 427,569 (22,077,595) 20,505,902

Total comprehensive income for the period

Loss for the period – – – – (1,219,668) (1,219,668)

Other comprehensive income

Foreign currency translation differences – (297,933) – – – (297,933)

Net change in fair value of available for sale assets – – (64,332) – – (64,332)

Total other comprehensive income (297,933) (64,332) – (1,219,668) (1,581,933)

Total comprehensive income for the period (297,933) (64,332) – (1,219,668) (1,581,933)

Transactions with owners recorded directly in equity

Contributions by and distributions to owners

Share options exercised 4,247 – – – – 4,247

Placements 1,624,627 – – – – 1,624,627

Proceeds of Share Purchase Plan 1,757,004 – – – – 1,757,004

Costs of issues (38,515) – – – – (38,515)

Total contributions by and distributions to owners 3,347,363 – – – – 3,347,363

Total transactions with owners 3,347,363 – – – – 3,347,363

Balance 31 December 2011 46,760,277 (1,570,909) (48,342) 427,569 (23,297,263) 22,271,332

2012Balance 1 January 2012 46,760,277 (1,570,909) (48,342) 427,569 (23,297,263) 22,271,332

Total comprehensive income for the period

Loss for the period – – – – (1,783,154) (1,783,154)

Other comprehensive income

Foreign currency translation differences – 50,834 – – – 50,834)

Net change in fair value of available for sale assets – – (34,902) – – (34,902)

Total other comprehensive income – 50,834 (34,902) – (1,783,154) (1,767,222)

Total comprehensive income for the period 50,834 (34,902) – (1,783,154) (1,767,222)

Transactions with owners recorded directly in equity

Contributions by and distributions to owners

Placements 1,432,050 – – – – 1,432,050

Rights issue receipts 2,749,197 – – – – 2,749,197

Costs of issues (148,585) – – – – (148,585)

Total contributions by and distributions to owners 4,032,662 – – – – 4,032,662

Total transactions with owners 4,032,662 – – – – 4,032,662

Balance 31 December 2012 50,792,939 (1,520,075) (83,244) 427,569 (25,080,417) 24,536,772

The consolidated statement of changes in equity is to be read in conjunction with the notes to the fi nancial statements set out on pages 26 to 43.

Consolidated statement of changes in equityFor the year ended 31 December 2012

For

per

sona

l use

onl

y

Atlantic Gold Annual Report 2012 25

Statements of cash fl owsFor the year ended 31 December 2012

NOTE CONSOLIDATED

2012 2011

$ $

Cash fl ows from operating activities Payments to suppliers and employees (996,590) (603,662)Interest received 37,796 98,307Interest paid (67,703) (15)Net cash used in operating activities 16(b) (1,026,497) (505,370)