Embed Size (px)

Citation preview

1H15 Results Presentation

September 2015

For

per

sona

l use

onl

y

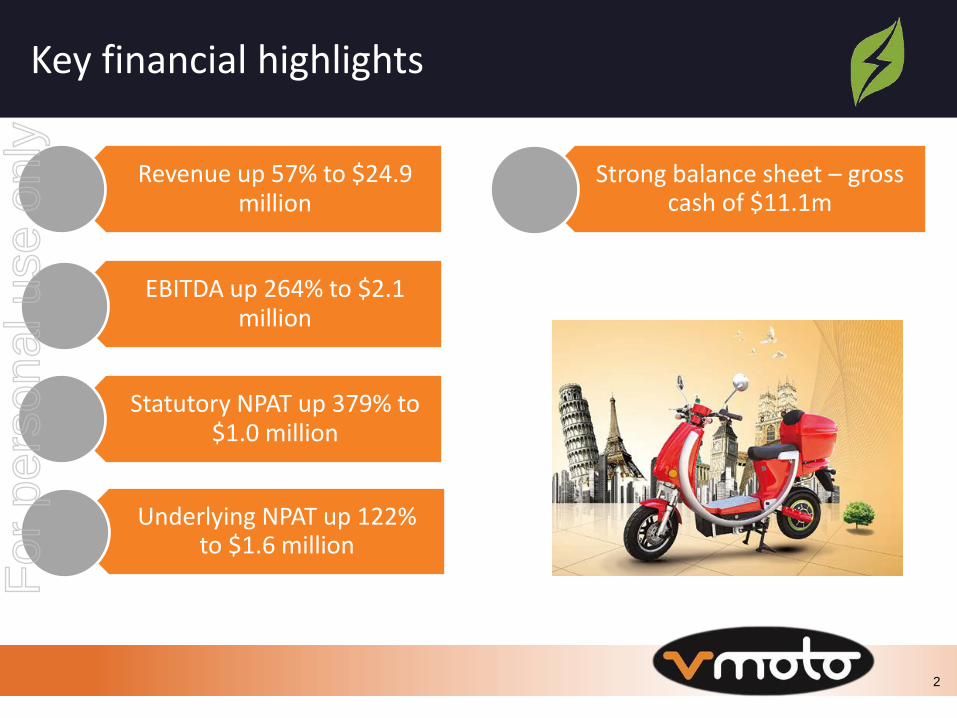

Key financial highlights

Revenue up 57% to $24.9 million

EBITDA up 264% to $2.1 million

Statutory NPAT up 379% to $1.0 million

Strong balance sheet – gross cash of $11.1m

Underlying NPAT up 122% to $1.6 million

2

For

per

sona

l use

onl

y

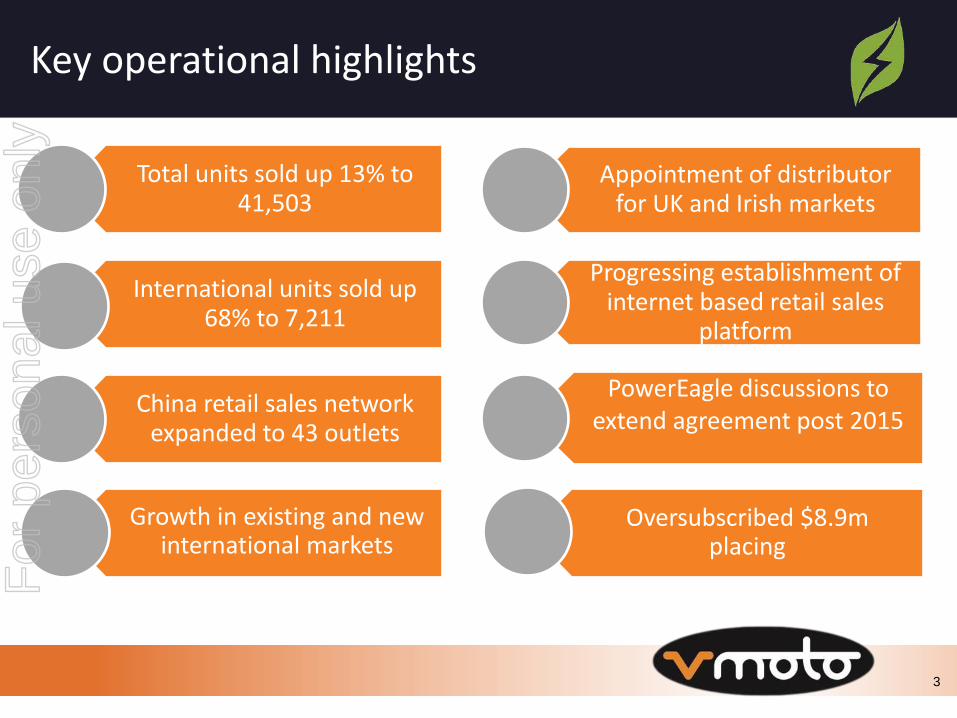

Key operational highlights

Total units sold up 13% to 41,503

International units sold up 68% to 7,211

China retail sales network expanded to 43 outlets

Appointment of distributor for UK and Irish markets

Progressing establishment of internet based retail sales

platform

PowerEagle discussions to extend agreement post 2015

Oversubscribed $8.9m placing

Growth in existing and new international markets

3

For

per

sona

l use

onl

y

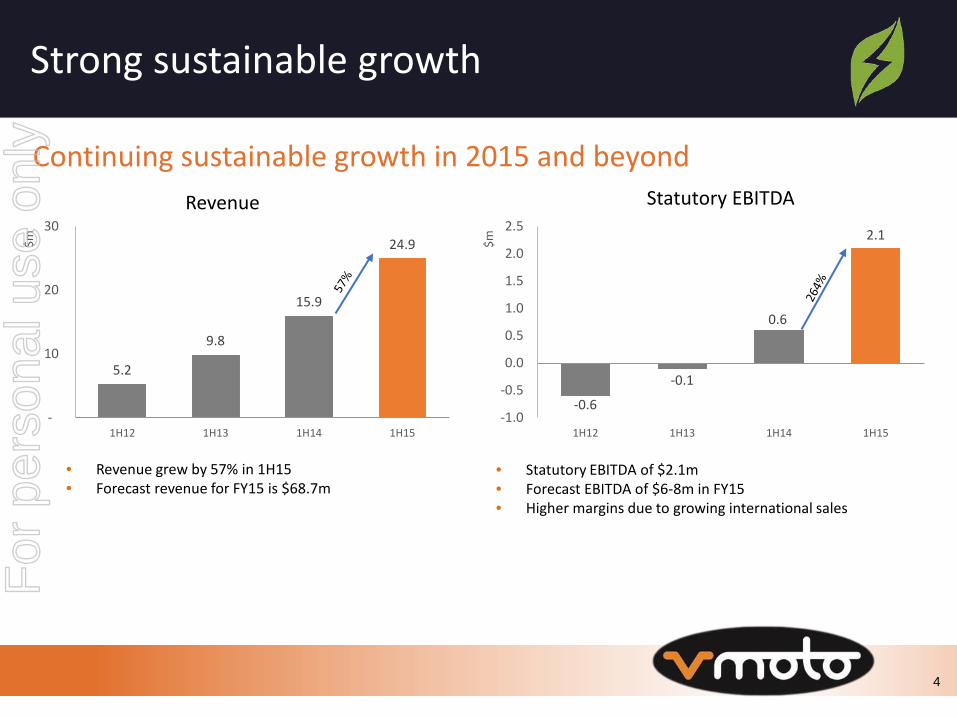

Strong sustainable growth

Continuing sustainable growth in 2015 and beyond

• Revenue grew by 57% in 1H15 • Forecast revenue for FY15 is $68.7m

Revenue Statutory EBITDA

• Statutory EBITDA of $2.1m • Forecast EBITDA of $6-8m in FY15 • Higher margins due to growing international sales

4

5.2

9.8

15.9

24.9

-

10

20

30

1H12 1H13 1H14 1H15

$m

-0.6

-0.1

0.6

2.1

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1H12 1H13 1H14 1H15

$m

For

per

sona

l use

onl

y

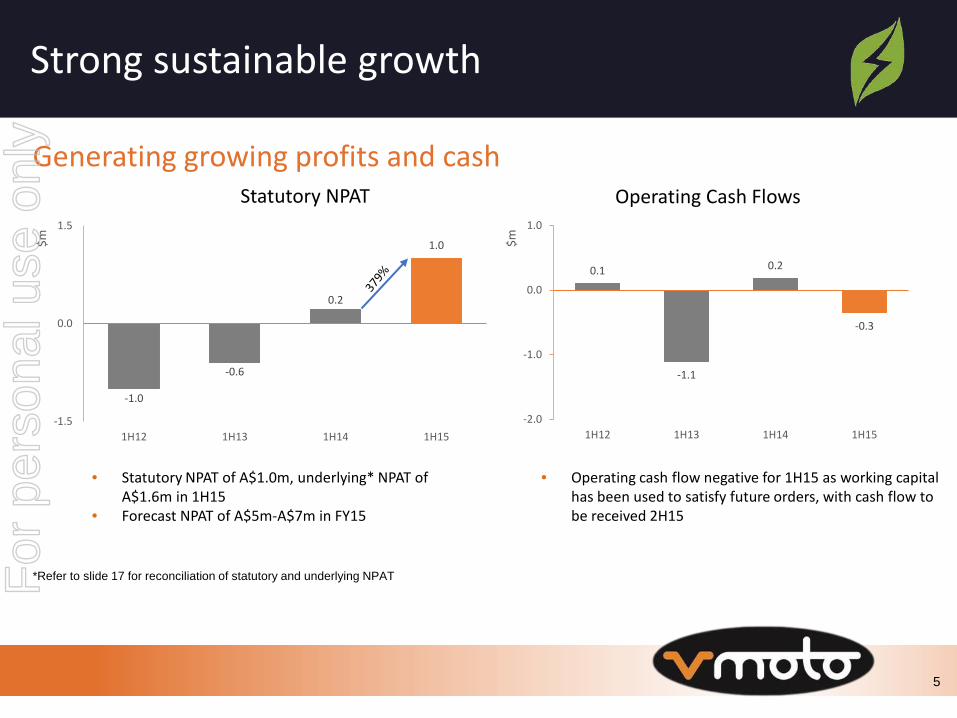

Strong sustainable growth

Generating growing profits and cash

• Operating cash flow negative for 1H15 as working capital has been used to satisfy future orders, with cash flow to be received 2H15

Operating Cash Flows

5

• Statutory NPAT of A$1.0m, underlying* NPAT of A$1.6m in 1H15

• Forecast NPAT of A$5m-A$7m in FY15

Statutory NPAT

*Refer to slide 17 for reconciliation of statutory and underlying NPAT

-1.0

-0.6

0.2

1.0

-1.5

0.0

1.5

1H12 1H13 1H14 1H15

$m

0.1

-1.1

0.2

-0.3

-2.0

-1.0

0.0

1.0

1H12 1H13 1H14 1H15

$m

For

per

sona

l use

onl

y

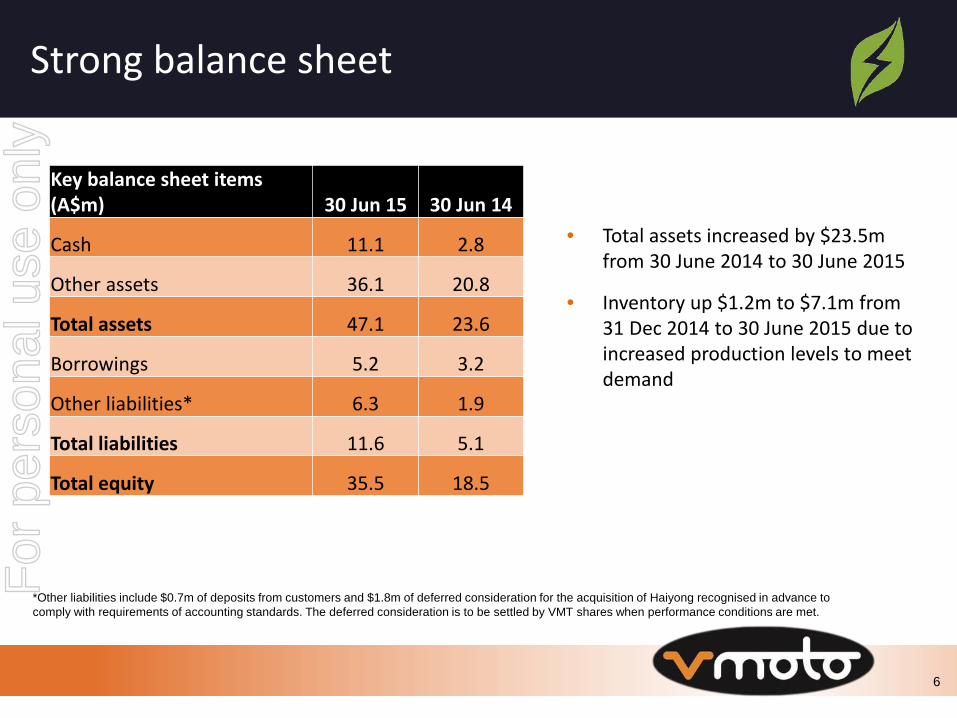

Strong balance sheet

• Total assets increased by $23.5m from 30 June 2014 to 30 June 2015

• Inventory up $1.2m to $7.1m from 31 Dec 2014 to 30 June 2015 due to increased production levels to meet demand

Key balance sheet items (A$m) 30 Jun 15 30 Jun 14

Cash 11.1 2.8

Other assets 36.1 20.8

Total assets 47.1 23.6

Borrowings 5.2 3.2

Other liabilities* 6.3 1.9

Total liabilities 11.6 5.1

Total equity 35.5 18.5

*Other liabilities include $0.7m of deposits from customers and $1.8m of deferred consideration for the acquisition of Haiyong recognised in advance to comply with requirements of accounting standards. The deferred consideration is to be settled by VMT shares when performance conditions are met.

6

For

per

sona

l use

onl

y

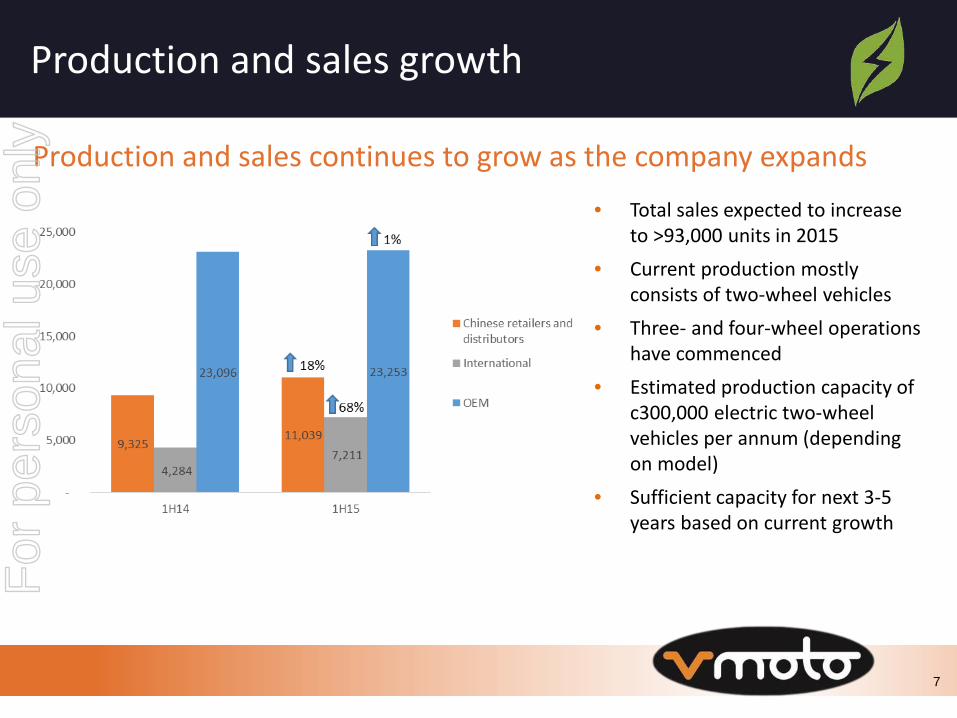

Production and sales growth

Production and sales continues to grow as the company expands • Total sales expected to increase

to >93,000 units in 2015 • Current production mostly

consists of two-wheel vehicles • Three- and four-wheel operations

have commenced • Estimated production capacity of

c300,000 electric two-wheel vehicles per annum (depending on model)

• Sufficient capacity for next 3-5 years based on current growth

7

For

per

sona

l use

onl

y

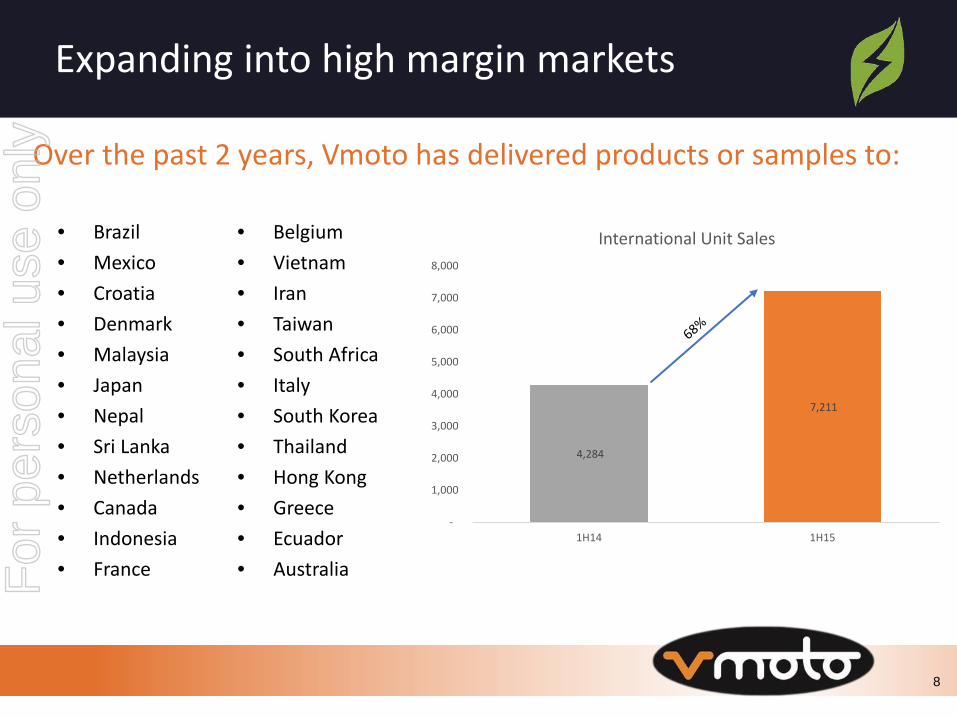

Expanding into high margin markets

• Belgium • Vietnam • Iran • Taiwan • South Africa • Italy • South Korea • Thailand • Hong Kong • Greece • Ecuador • Australia

Over the past 2 years, Vmoto has delivered products or samples to:

• Brazil • Mexico • Croatia • Denmark • Malaysia • Japan • Nepal • Sri Lanka • Netherlands • Canada • Indonesia • France

8

4,284

7,211

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1H14 1H15

International Unit Sales

For

per

sona

l use

onl

y

Other facets to the Company

• 3/4 wheel JV (Vmoto 20% equity interest) established and operational at factory

– design, manufacture and distribution of electric three- and four-wheel vehicles for Chinese domestic and international markets

– Capitalises on demand for electric vehicles generated by political, environmental and business considerations

– Product development and sales commenced

• Agreement signed with the third largest handle bar manufacturer in China - Changzhou Dusheng Electrical Equipment Co.

– Dusheng will pay a royalty to Vmoto based on the sales volume of handle bars that use Vmoto’s patented technology in EV handle bar to control the entire EV

– The agreement is expected to fast-track the penetration of Vmoto’s technology to the market through spare parts manufacturers’ sales channels

– Royalties expected to contribute to revenue in FY16

Complimentary opportunities in the burgeoning electric vehicle market

9

For

per

sona

l use

onl

y

Well positioned to ramp up over the next three to five years

• 30,000sqm state of the art manufacturing facility in Nanjing, China - wholly owned, fully paid for, equipped plant in key industrial zone - currently running at less than 30% utilisation - no short term infrastructure requirements

• Operates under Chinese manufacturing license - Significant intangible value - Expected to open up further opportunities for consolidation within China

• Three and four-wheel electric vehicles operations have commenced

Production facility has capacity to handle increased demand

10

For

per

sona

l use

onl

y

Growth strategy - China

B2C market

• Expansion in China – targeting 300 outlets by 2017

• Plan to launch online sales platform and offline logistics and service from 2016

• Plans to launch e-motorcycle racing brand in China

• Plan to undertake e-motorcycle racing campaign and partner with racing circuit nearby Vmoto Nanjing manufacturing facilities

• Launch international delivery electric scooter from 2016

• Target large and famous B2B customers in China and internationally

• Providing complete and customisable electric vehicle solutions to all B2B customers for their fleet requirements

• Aiming to be number 1 in China by the end of 2019 in terms of brand, profitability and volume in e-scooter segment

11

B2B market

For

per

sona

l use

onl

y

Growth strategy - International

12

B2C markets

• Asia – Increase unit sales to existing distributors and identify new distributors, strategic partners and importers

• Europe – Increasing unit sales to Europe, benefiting from government policies including subsidies for buying electric vehicles and bans on petrol two-wheel vehicles more than 50cc on the road

B2B market • Expand existing and target new B2B customers that have needs to replace petrol fleet with electric fleet e.g.

KFC, McDonalds, DHL, TNT, Dominos Pizza

• Partner with B2B customers for innovative services including e-scooter sharing and battery exchange stations, leveraging Vmoto’s network and technical expertise

For

per

sona

l use

onl

y

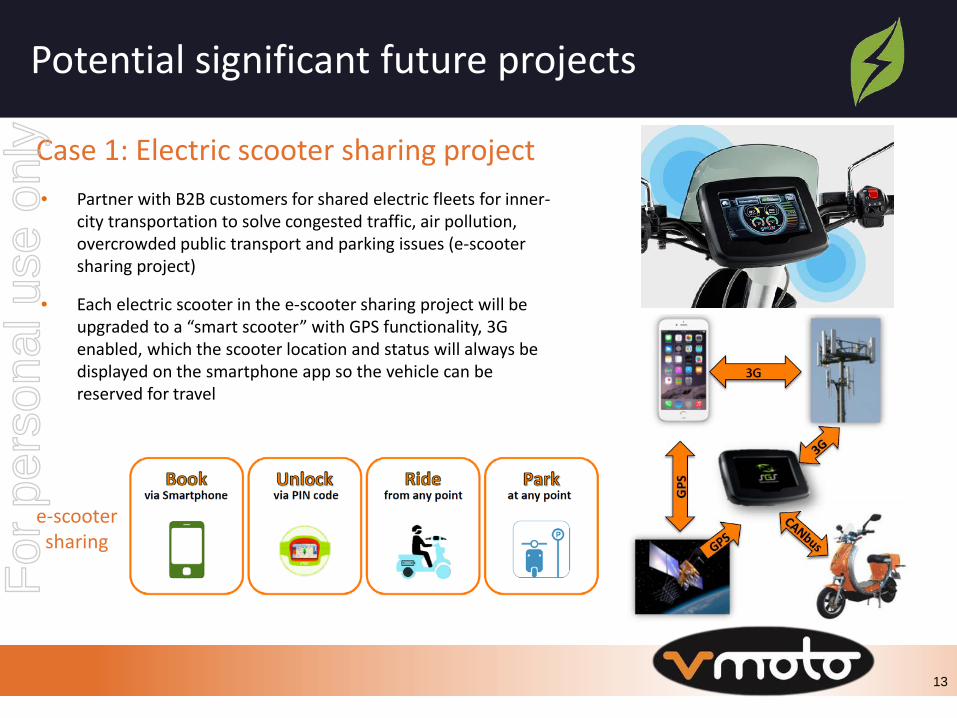

Potential significant future projects

e-scooter sharing

13

Case 1: Electric scooter sharing project • Partner with B2B customers for shared electric fleets for inner-

city transportation to solve congested traffic, air pollution, overcrowded public transport and parking issues (e-scooter sharing project)

• Each electric scooter in the e-scooter sharing project will be upgraded to a “smart scooter” with GPS functionality, 3G enabled, which the scooter location and status will always be displayed on the smartphone app so the vehicle can be reserved for travel

For

per

sona

l use

onl

y

Potential significant future projects

14

Case 2: Battery Exchange Station Project • Partner with B2B customers for battery exchange station project to overcome

long battery charging time and limited travel distance range for electric vehicle users

• Cooperate with battery exchange station operator that have successful track record and battery suppliers that have reliable battery products

• Additional source of income from supplying Vmoto’s electric two-wheel vehicle products to the battery exchange station project and also revenue from operating the battery exchange stations

For

per

sona

l use

onl

y

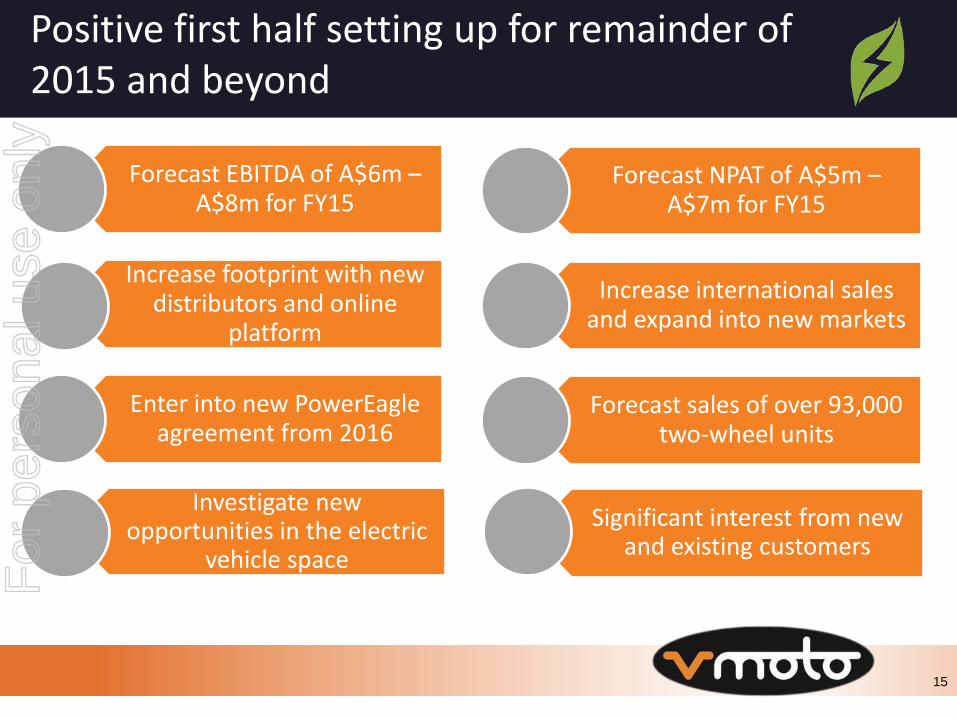

Positive first half setting up for remainder of 2015 and beyond

Forecast EBITDA of A$6m – A$8m for FY15

Increase footprint with new distributors and online

platform

Enter into new PowerEagle agreement from 2016

Forecast NPAT of A$5m – A$7m for FY15

Increase international sales and expand into new markets

Forecast sales of over 93,000 two-wheel units

Significant interest from new and existing customers

Investigate new opportunities in the electric

vehicle space

15

For

per

sona

l use

onl

y

Contact

• Charles Chen, Managing Director – +61 (8) 9226 3865 – [email protected]

• Olly Cairns, Executive Director – +61 (8) 9226 3865 – [email protected]

16

For

per

sona

l use

onl

y

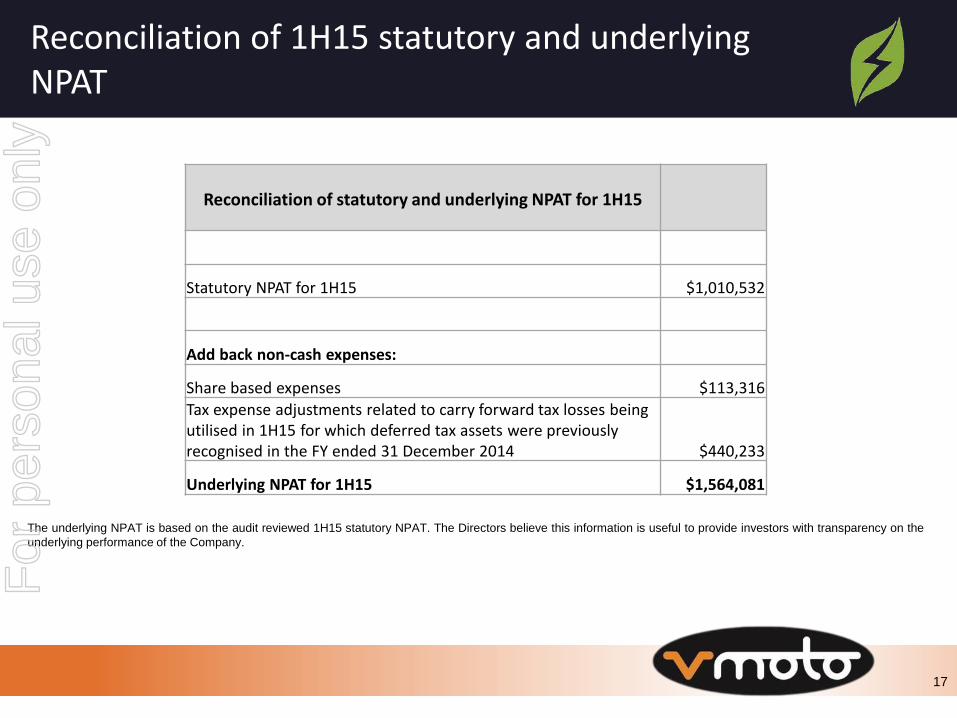

Reconciliation of 1H15 statutory and underlying NPAT

17

The underlying NPAT is based on the audit reviewed 1H15 statutory NPAT. The Directors believe this information is useful to provide investors with transparency on the underlying performance of the Company.

Reconciliation of statutory and underlying NPAT for 1H15

Statutory NPAT for 1H15 $1,010,532

Add back non-cash expenses:

Share based expenses $113,316 Tax expense adjustments related to carry forward tax losses being utilised in 1H15 for which deferred tax assets were previously recognised in the FY ended 31 December 2014 $440,233

Underlying NPAT for 1H15 $1,564,081

For

per

sona

l use

onl

y

Vmoto’s product offering

A wide variety of models with a new model coming in 2015 • Two-wheel electric vehicles priced between A$700 and A$3,500 • Vehicles come with either a lead acid battery or a lithium battery, depending on model

18

For

per

sona

l use

onl

y

Vmoto

19

For

per

sona

l use

onl

y

Vmoto

20

For

per

sona

l use

onl

y

Disclaimer

IMPORTANT NOTICE

The information contained in this presentation is current as at 4 September 2015 and is provided by Vmoto Limited (ABN 36 098 455 460) (“Vmoto”) as a summary document for information purposes only.

Any forward looking statements included in this presentation involve subjective judgment and analysis and are subject to uncertainties risks and contingencies, many of which are outside the control of and may be unknown to Vmoto at the time of preparing this presentation. Actual future events may vary materially from the forward looking statements and the assumptions on which these statements are based. Recipients of this information are cautioned not to place undue reliance on such forward looking statements. The information contained in this presentation is provided in good faith, however, Vmoto makes no representation or warranty as to the accuracy, reliability or completeness of the information. To the extent permitted by law, Vmoto and its officers, employees, related bodies corporate and agents, disclaim all liability, whether direct, indirect or consequential, and whether or not arising out of the negligence, default or lack of care of Vmoto and/or any of its agents, for any loss or damage suffered by a recipient or any other persons, arising out of or in connection with any use or reliance on this presentation or information.

21

For

per

sona

l use

onl

y