Embed Size (px)

Citation preview

Automotive Holdings Group Limited 21 Old Aberdeen Place

West Perth, WA 6005 www.ahgir.com.au

ABN 35 111 470 038

AHG PRESENTATION 22 October 2014 Automotive Holdings Group Limited (ASX: AHE) is today presenting the attached material to a Credit Suisse institutional investor conference in Sydney. ENDS About AHG Automotive Holdings Group Limited (ASX: AHE) is a diversified automotive retailing and logistics group with operations in every Australian mainland state and in New Zealand. The Company is Australia's largest automotive retailer, with operations in Western Australia, New South Wales, Queensland and Victoria. AHG’s logistics businesses operate throughout Australia via subsidiaries Rand Transport, Harris Refrigerated Transport, Scott’s Refrigerated Freightways and JAT Refrigerated Road Services (transport and cold storage), AMCAP and Covs (motor parts and industrial supplies distribution), VSE (vehicle storage and engineering), Genuine Truck Bodies (body building services to the truck industry), and KTM Sportmotorcycles and HQVA (KTM and Husqvarna motorcycle importation and distribution in Australia and New Zealand). Corporate: Media: David Rowland David Christison Company Secretary Group Executive Corporate Communications Mobile: 0421 661 613 Mobile: 0418 959 817 Email: [email protected] Email: [email protected]

For

per

sona

l use

onl

y

C dit S i A t ti P t tiCredit Suisse Automotive PresentationBronte Howson, AHG Managing Director22 October 2014F

or p

erso

nal u

se o

nly

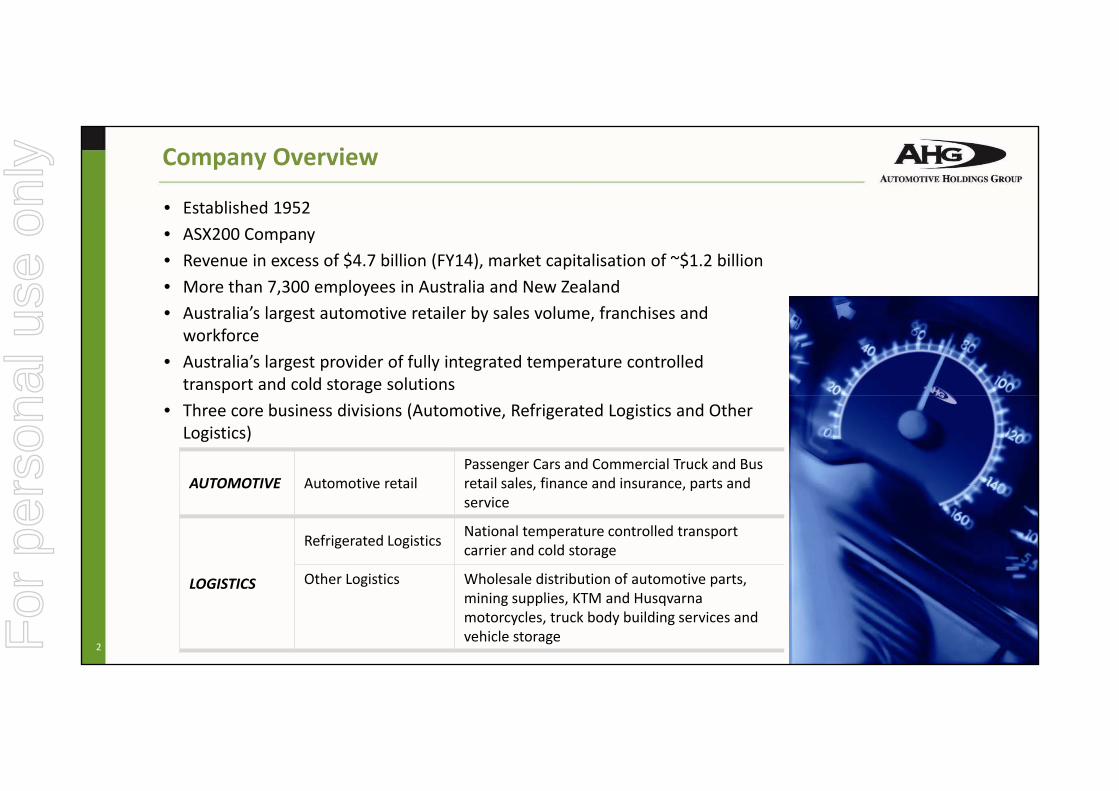

Company Overview

• Established 1952• ASX200 Company • Revenue in excess of $4.7 billion (FY14), market capitalisation of ~$1.2 billion• More than 7,300 employees in Australia and New Zealand• Australia’s largest automotive retailer by sales volume, franchises and

workforce• Australia’s largest provider of fully integrated temperature controlled

transport and cold storage solutions• Three core business divisions (Automotive, Refrigerated Logistics and Other

Logistics)

AUTOMOTIVE Automotive retailPassenger Cars and Commercial Truck and Bus retail sales finance and insurance parts andAUTOMOTIVE Automotive retail retail sales, finance and insurance, parts and service

Refrigerated Logistics National temperature controlled transport carrier and cold storage

Oth L i ti Wh l l di t ib ti f t ti tLOGISTICS Other Logistics Wholesale distribution of automotive parts, mining supplies, KTM and Husqvarna motorcycles, truck body building services and vehicle storage

2For

per

sona

l use

onl

y

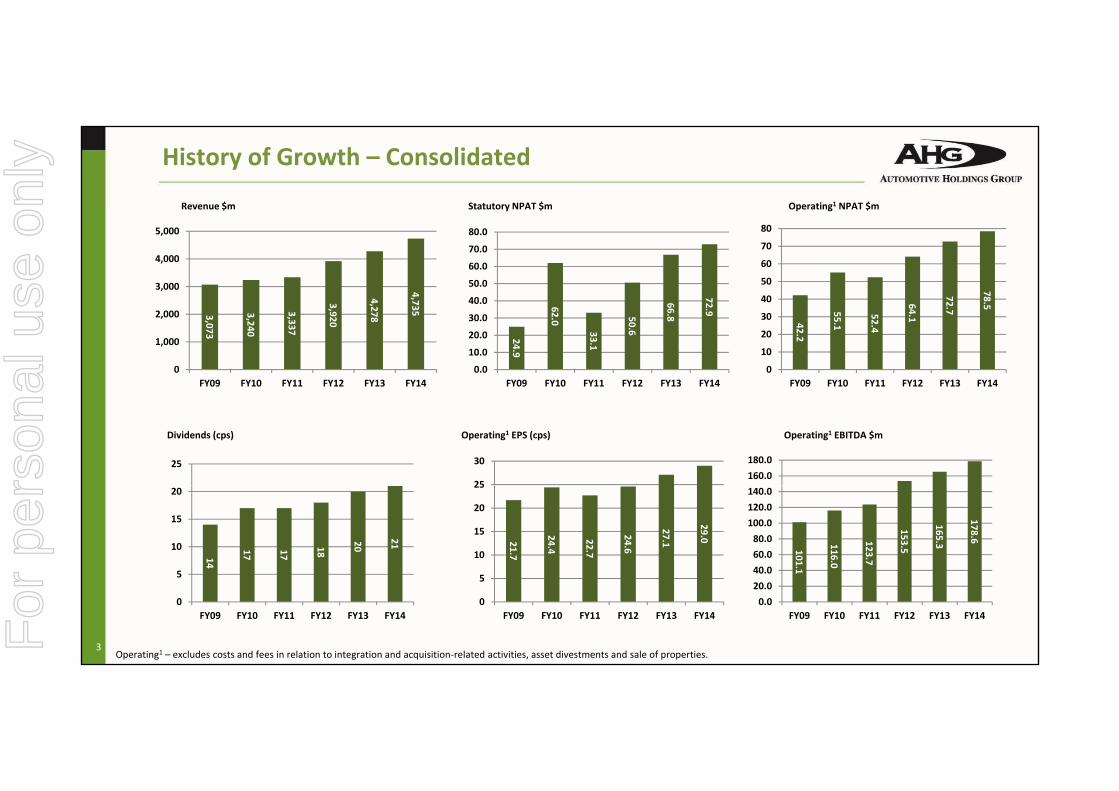

Revenue $m Operating1 NPAT $mStatutory NPAT $m

History of Growth – Consolidated

6

72

78.540

50

60

70

80

3 4,

4,7

3,000

4,000

5,000

6 7240.0

50.0

60.0

70.0

80.0

42.2

55.1

52.4

64.1

2.7 5

0

10

20

30

FY09 FY10 FY11 FY12 FY13 FY14

3,073

3,240

3,337

3,920

,278

35

0

1,000

2,000

FY09 FY10 FY11 FY12 FY13 FY14

24.9

62.0

33.1

50.6

66.8

2.9

0.0

10.0

20.0

30.0

FY09 FY10 FY11 FY12 FY13 FY14

Operating1 EBITDA $mOperating1 EPS (cps)Dividends (cps)

25160.0180.0

25

30

14

17 17

18

20

21

5

10

15

20

101.1

116.0

123.7

153.5

165.3

178.6

40.060.080.0

100.0120.0140.0

21.7

24.4

22.7

24.6

27.1

29.0

5

10

15

20

25

0

5

FY09 FY10 FY11 FY12 FY13 FY140.020.0

FY09 FY10 FY11 FY12 FY13 FY140

5

FY09 FY10 FY11 FY12 FY13 FY14

Operating1 – excludes costs and fees in relation to integration and acquisition‐related activities, asset divestments and sale of properties.3F

or p

erso

nal u

se o

nly

Australia – New Vehicle Sales (VFACTS)

• Record new vehicle sales in CY 2013

1,200,000

3.01% CAGR

800,000

1,000,000

8

909

955,2

988,2

962,6

1,049,98

1,012,1

937,

1,035,5

1,008,4

1,112,032

1,136,227

1,100,000

600,000

772,681

824,309

9,811

229

269

666

82 165

,328

74

437

2 0

200,000

400,000

02001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

VFACTSForecast4F

or p

erso

nal u

se o

nly

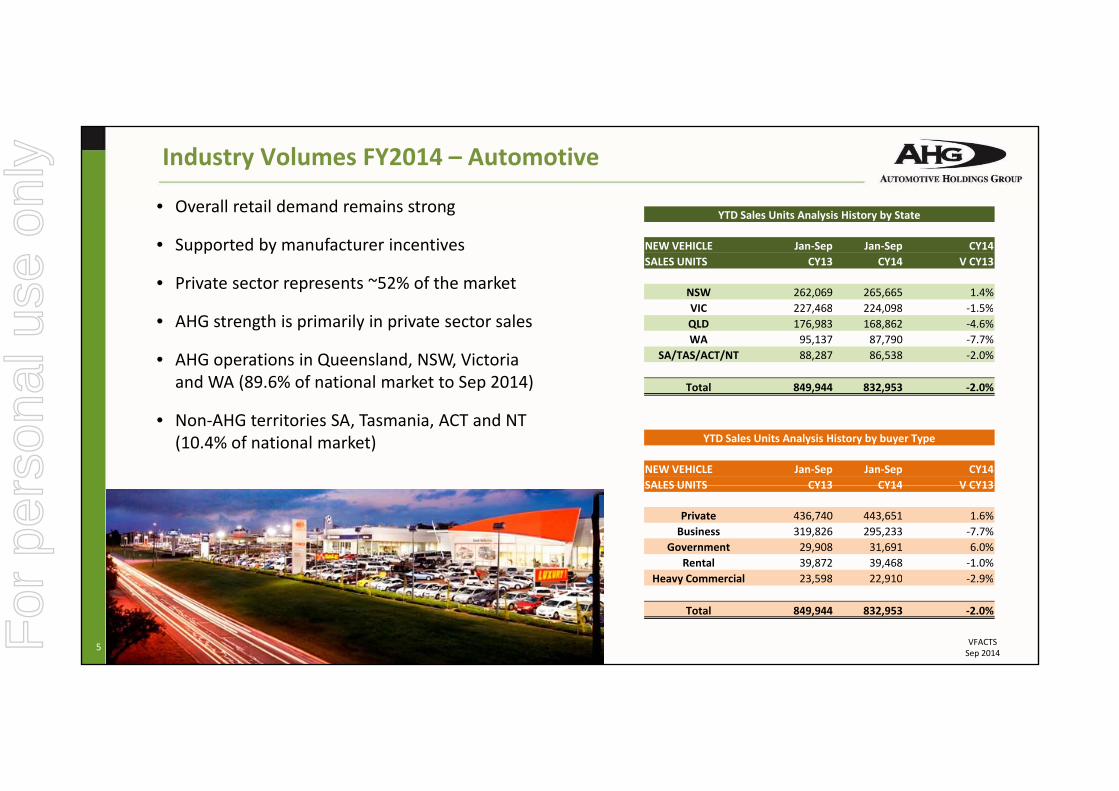

Industry Volumes FY2014 – Automotive

• Overall retail demand remains strong YTD Sales Units Analysis History by State

• Supported by manufacturer incentives

• Private sector represents ~52% of the market

YTD Sales Units Analysis History by State

NEW VEHICLE Jan‐Sep Jan‐Sep CY14SALES UNITS CY13 CY14 V CY13

NSW 262,069 265,665 1.4%VIC 227 468 224 098 1 5%

• AHG strength is primarily in private sector sales

• AHG operations in Queensland, NSW, Victoria and WA (89.6% of national market to Sep 2014)

VIC 227,468 224,098 ‐1.5%QLD 176,983 168,862 ‐4.6%WA 95,137 87,790 ‐7.7%

SA/TAS/ACT/NT 88,287 86,538 ‐2.0%

Total 849,944 832,953 ‐2.0%

• Non‐AHG territories SA, Tasmania, ACT and NT (10.4% of national market) YTD Sales Units Analysis History by buyer Type

NEW VEHICLE Jan‐Sep Jan‐Sep CY14SALES UNITS CY13 CY14 V CY13SALES UNITS CY13 CY14 V CY13

Private 436,740 443,651 1.6%Business 319,826 295,233 ‐7.7%

Government 29,908 31,691 6.0%Rental 39,872 39,468 ‐1.0%

H C i l 23 598 22 910 2 9%Heavy Commercial 23,598 22,910 ‐2.9%

Total 849,944 832,953 ‐2.0%

5 VFACTSSep 2014F

or p

erso

nal u

se o

nly

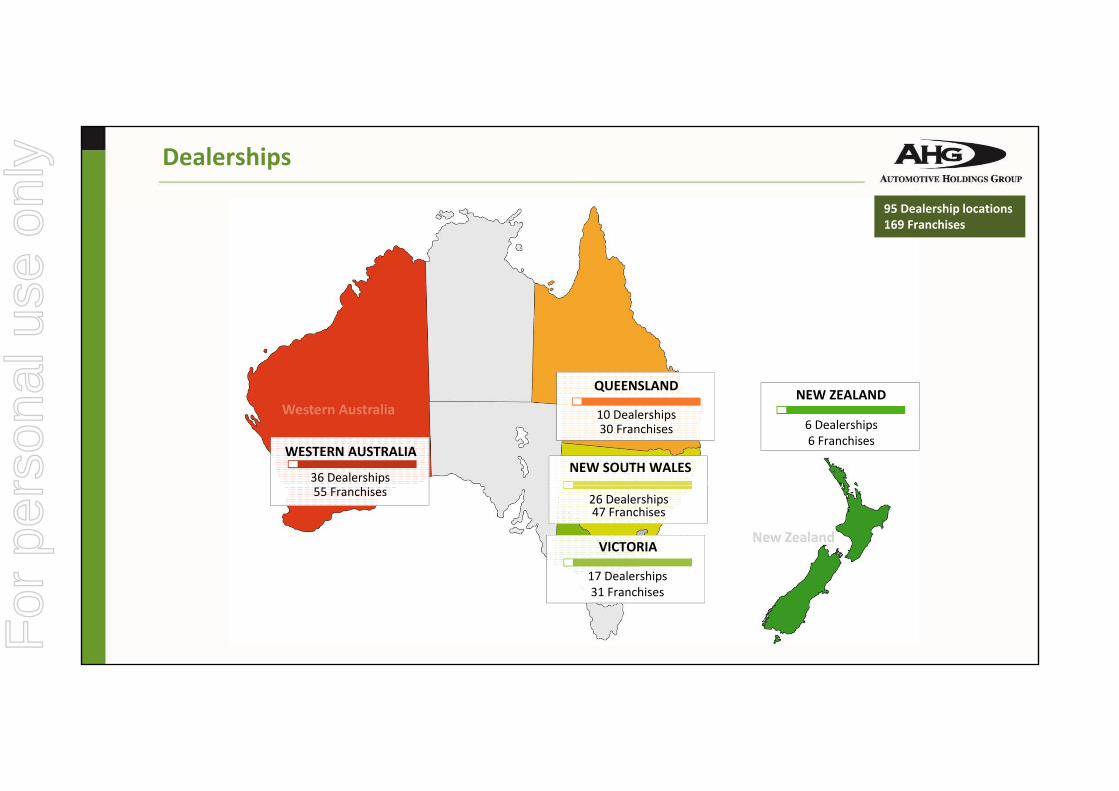

95 Dealership locations

Dealerships

169 Franchises

QUEENSLANDNEW ZEALAND

36 Dealerships

10 Dealerships30 Franchises

NEW SOUTH WALES

6 Dealerships6 Franchises

NEW ZEALAND

WESTERN AUSTRALIA

55 Franchises 26 Dealerships47 Franchises

17 Dealerships

VICTORIA

17 Dealerships31 Franchises

For

per

sona

l use

onl

y

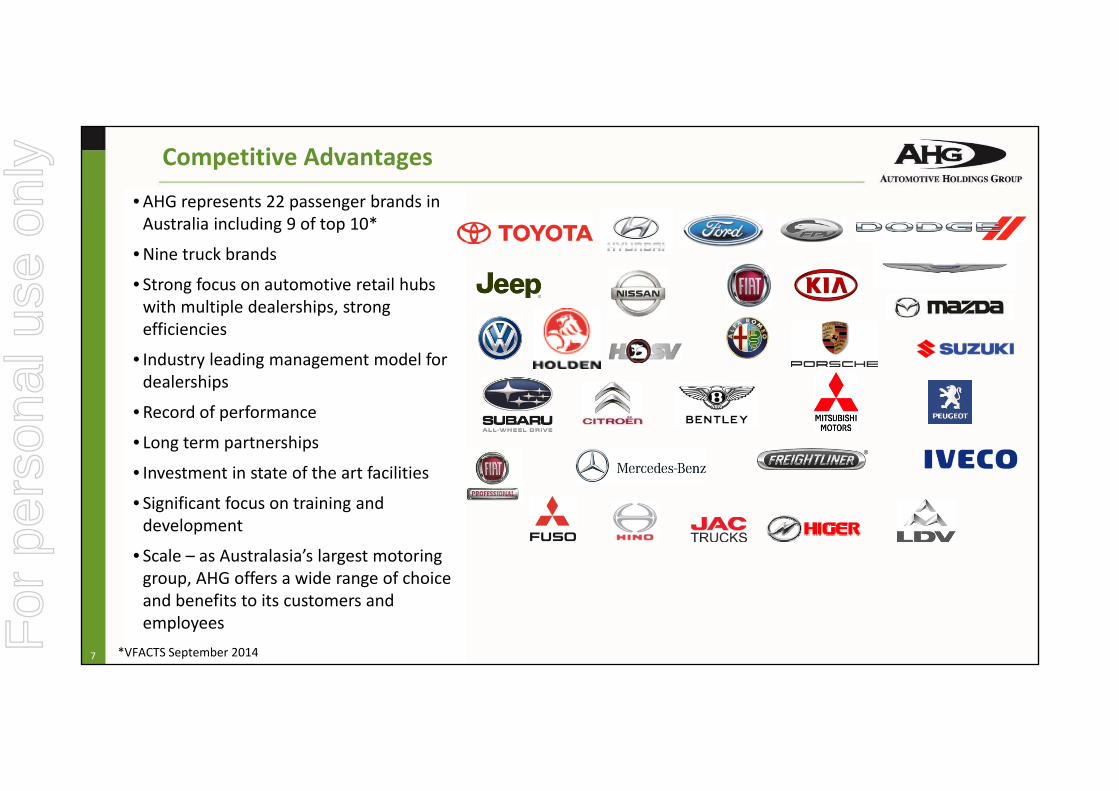

Competitive Advantages

•AHG represents 22 passenger brands in Australia including 9 of top 10*

•Nine truck brands• Strong focus on automotive retail hubs with multiple dealerships strongwith multiple dealerships, strong efficiencies

• Industry leading management model for dealerships

• Record of performance

• Long term partnerships

• Investment in state of the art facilities

• Significant focus on training and development

• Scale – as Australasia’s largest motoring gro p AHG offers a ide range of choicegroup, AHG offers a wide range of choice and benefits to its customers and employees

*VFACTS September 20147

For

per

sona

l use

onl

y

Dealership Revenue Streams

• Strict measurement and reporting processesNew Cars

Strict measurement and reporting processes

• Industry benchmarking across departments

• High penetration rates across Finance & Insurance (F&I)

• Strong CRM programs drive service retentionUsed CarsService

Strong CRM programs drive service retention

• Service department revenue opportunities

PartsFinance & IInsurance

8For

per

sona

l use

onl

y

Automotive highlights of the last 12 months

• Strong revenue and profit growth through successful integration of new acquisitions in WA, VIC and NZ aided by growing success of marketing campaigns

• Increased new vehicle sales complemented by multiple revenue streams of strong used vehicle sales, F&I, service, and parts

• Maturing Greenfield sites including commencement of trading in Castle Hill Nissan (NSW) and Manukau Nissan (NZ)

• Melbourne City Holden/HSV, Melbourne City Hyundai and Clarkson Nissan opened

• Bradstreet acquisition completed – 13 franchises at seven dealerships – increased vehicle and parts sales

9For

per

sona

l use

onl

y

WHERE TO FROM HERE?

For

per

sona

l use

onl

y

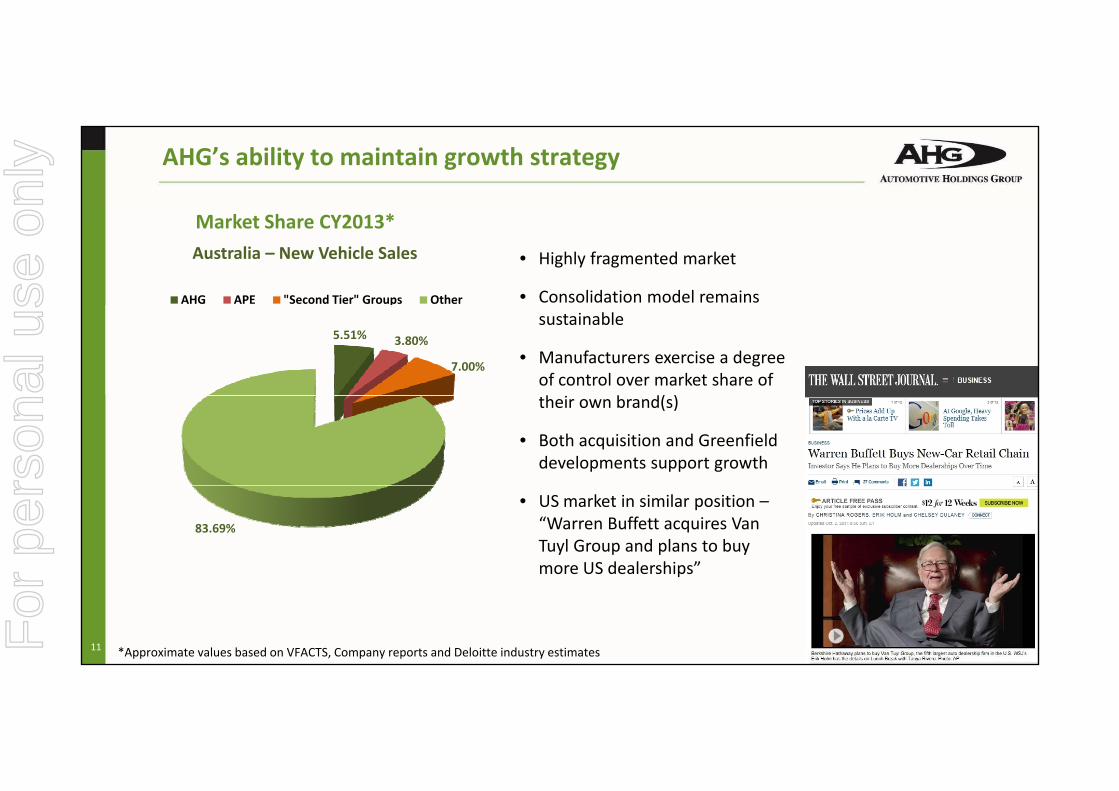

AHG’s ability to maintain growth strategy

M k t Sh CY2013*

• Highly fragmented market

• Consolidation model remains AHG APE "Second Tier" Groups Other

Australia – New Vehicle Sales

Market Share CY2013*

sustainable

• Manufacturers exercise a degree of control over market share of h b d( )

5.51% 3.80%

7.00%

p

their own brand(s)

• Both acquisition and Greenfield developments support growth

• US market in similar position –“Warren Buffett acquires Van Tuyl Group and plans to buy more US dealerships”

83.69%

p

*Approximate values based on VFACTS, Company reports and Deloitte industry estimates11For

per

sona

l use

onl

y

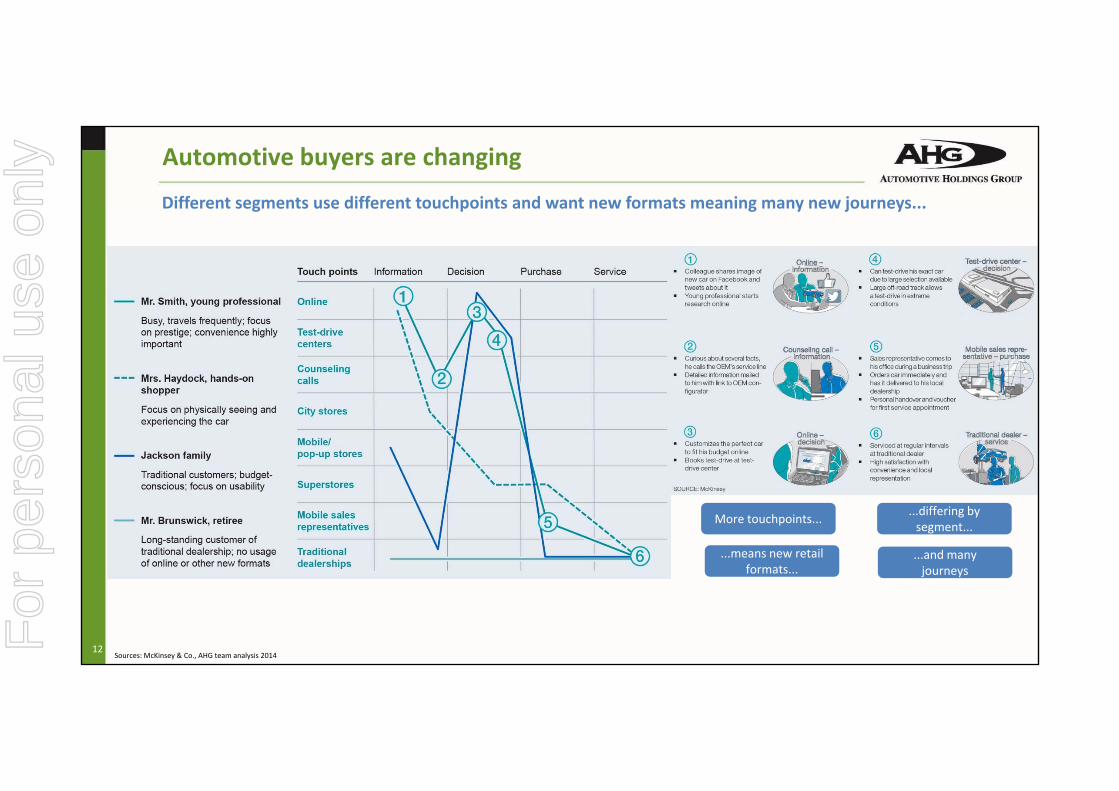

Automotive buyers are changing

Different segments use different touchpoints and want new formats meaning many new journeys...

More touchpoints... ...differing by segment...

...means new retail formats...

...and many journeys

12

j y

Sources: McKinsey & Co., AHG team analysis 2014

For

per

sona

l use

onl

y

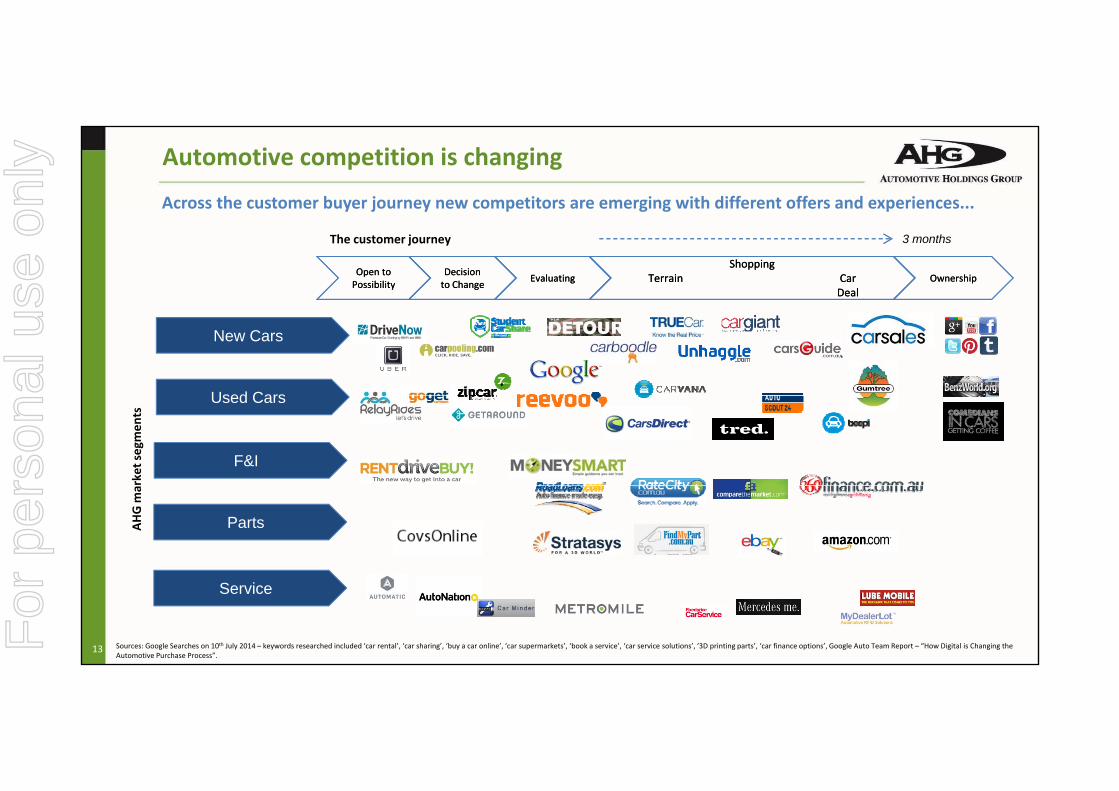

Automotive competition is changing

Across the customer buyer journey new competitors are emerging with different offers and experiences...

The customer journey

Open to PossibilityOpen to Possibility

Decision to ChangeDecision to Change EvaluatingEvaluating

ShoppingTerrain Car

Deal

ShoppingTerrain Car

DealOwnershipOwnership

3 months

New Cars

Used CarsUsed Cars

F&I

rket se

gmen

ts

PartsAHG m

a

13 Sources: Google Searches on 10th July 2014 – keywords researched included ‘car rental’, ‘car sharing’, ‘buy a car online’, ‘car supermarkets’, ‘book a service’, ‘car service solutions’, ‘3D printing parts’, ‘car finance options’, Google Auto Team Report – “How Digital is Changing the Automotive Purchase Process”.

Service

For

per

sona

l use

onl

y

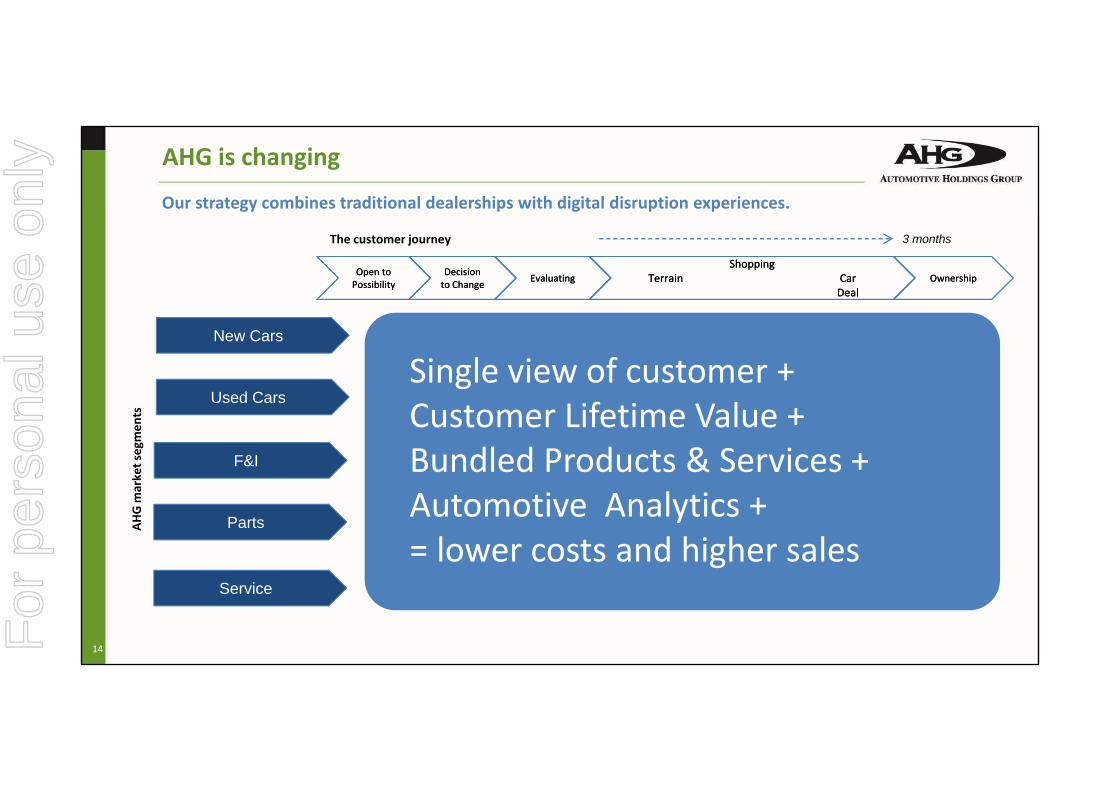

AHG is changing

Our strategy combines traditional dealerships with digital disruption experiences.

The customer journey

Open to PossibilityOpen to Possibility

Decision to ChangeDecision to Change EvaluatingEvaluating

ShoppingTerrain Car

Deal

ShoppingTerrain Car

DealOwnershipOwnership

3 months

New Cars

Used CarsSingle view of customer +

Used Cars

F&I

rket se

gmen

ts Customer Lifetime Value +Bundled Products & Services +

PartsAHG m

a

Automotive Analytics += lower costs and higher sales

14

Service

For

per

sona

l use

onl

y

Addressing the changing market

• Work with manufacturers to deliver best customer experience

• Traditional commerce and e‐commerce converging

• Target omni‐channel prospects in dealership, on‐line, tablet, mobile

• Optimise lead generation (Gumtree, Carsales/Stratton, Carsguide, etc.)

• Maximise database and analytics

• Leverage AHG’s Logistics relationships

• Create future digital offers across all revenue streams

• The result will be lower costs, increased sales and greater customer satisfaction

15For

per

sona

l use

onl

y

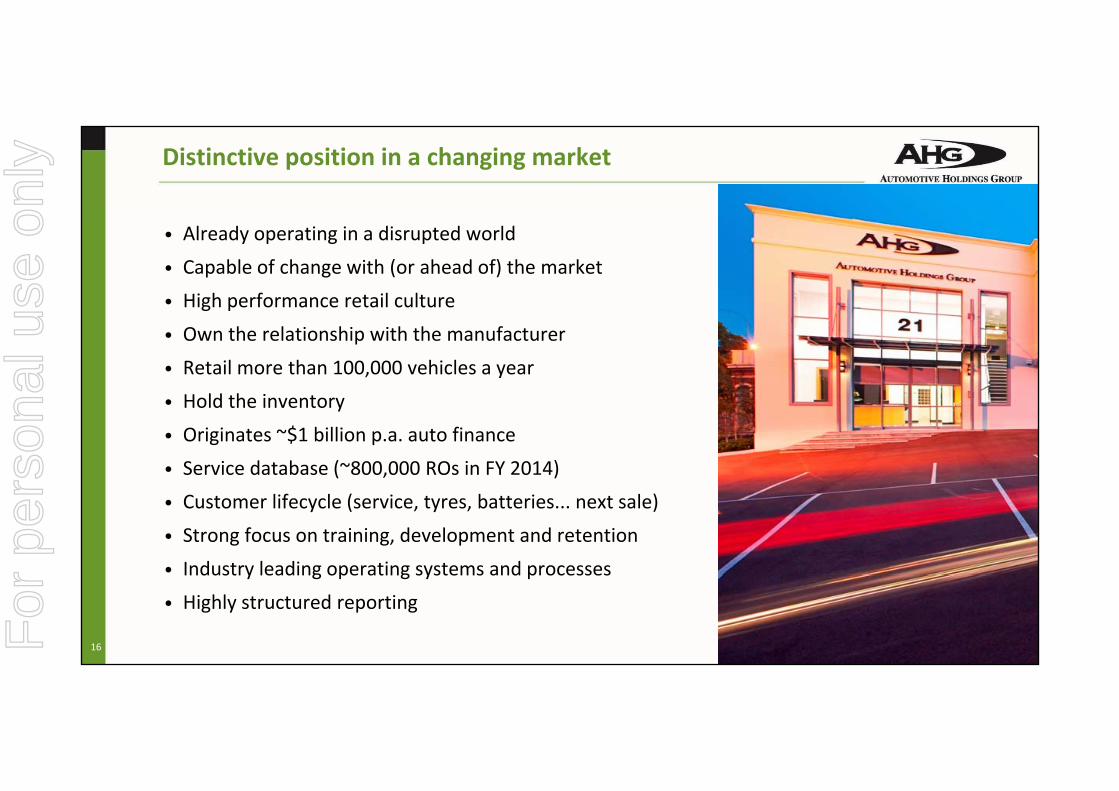

Distinctive position in a changing market

• Already operating in a disrupted world

• Capable of change with (or ahead of) the market

• High performance retail cultureHigh performance retail culture

• Own the relationship with the manufacturer

• Retail more than 100,000 vehicles a year

H ld th i t• Hold the inventory

• Originates ~$1 billion p.a. auto finance

• Service database (~800,000 ROs in FY 2014)

• Customer lifecycle (service, tyres, batteries... next sale)

• Strong focus on training, development and retention

• Industry leading operating systems and processes

16

Industry leading operating systems and processes

• Highly structured reporting

For

per

sona

l use

onl

y

For

per

sona

l use

onl

y