Embed Size (px)

Citation preview

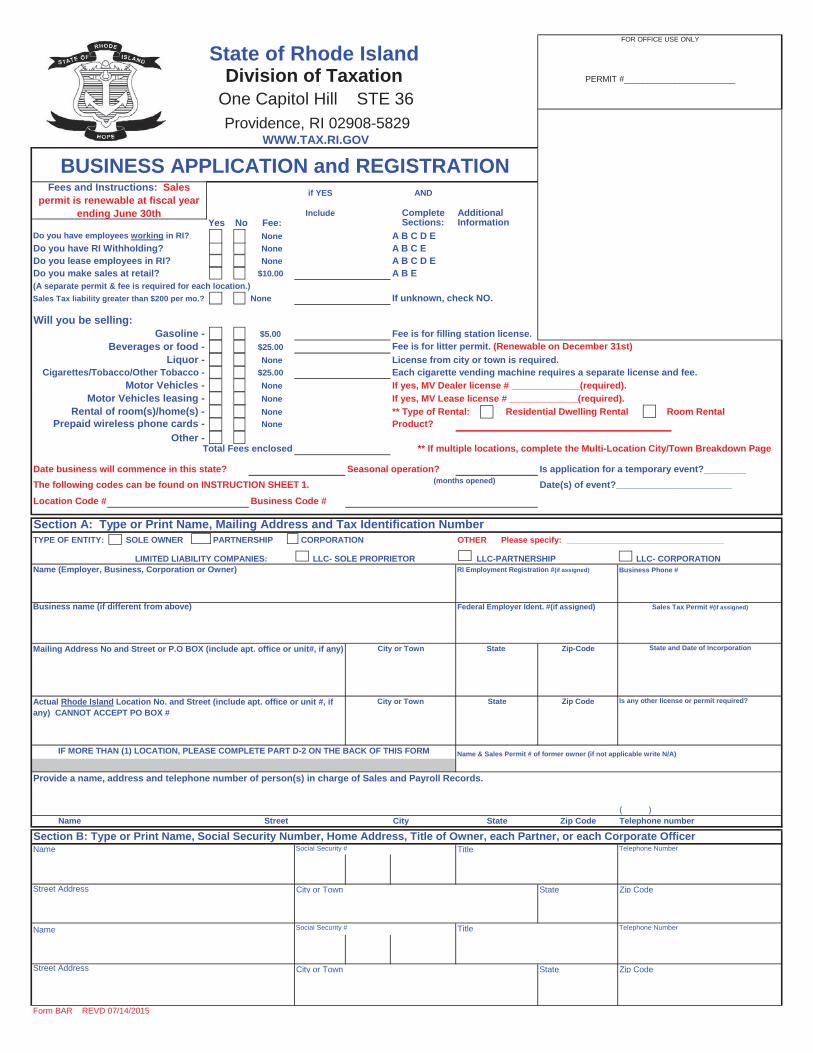

FOR OFFICE USE ONLY

PERMIT #________________________

BUSINESS APPLICATION and REGISTRATION if YES AND

Include Complete AdditionalYes No Fee: Sections: Information

Do you have employees working in RI? None A B C D EDo you have RI Withholding? None A B C EDo you lease employees in RI? None A B C D EDo you make sales at retail? $10.00 A B E (A separate permit & fee is required for each location.)Sales Tax liability greater than $200 per mo.? None If unknown, check NO.

Gasoline - $5.00 Fee is for filling station license.Beverages or food - $25.00 Fee is for litter permit. (Renewable on December 31st)

Liquor - None License from city or town is required.$25.00 Each cigarette vending machine requires a separate license and fee.

Motor Vehicles - None If yes, MV Dealer license # _____________(required).Motor Vehicles leasing - None If yes, MV Lease license # _____________(required).

Rental of room(s)/home(s) - None ** Type of Rental: Residential Dwelling Rental Room RentalPrepaid wireless phone cards - None Product?

Other -Total Fees enclosed ** If multiple locations, complete the Multi-Location City/Town Breakdown Page

Date business will commence in this state? Seasonal operation? Is application for a temporary event?________The following codes can be found on INSTRUCTION SHEET 1. (months opened) Date(s) of event?______________________Location Code # Business Code #

Section A: Type or Print Name, Mailing Address and Tax Identification NumberTYPE OF ENTITY: SOLE OWNER PARTNERSHIP CORPORATION OTHER Please specify: __________________________________

LLC- SOLE PROPRIETORName (Employer, Business, Corporation or Owner) RI Employment Registration #(if assigned) Business Phone #

Business name (if different from above) Federal Employer Ident. #(if assigned)

State Zip-Code

State Zip Code Is any other license or permit required?

Name & Sales Permit # of former owner (if not applicable write N/A)

Provide a name, address and telephone number of person(s) in charge of Sales and Payroll Records.

( )Name State Zip Code Telephone number

Section B: Type or Print Name, Social Security Number, Home Address, Title of Owner, each Partner, or each Corporate OfficerName Social Security # Title Telephone Number

Street Address City or Town State Zip Code

Name Social Security # Title Telephone Number

Street Address City or Town State Zip Code

Form BAR REVD 07/14/2015

LLC- CORPORATION

City or Town

State and Date of Incorporation

Sales Tax Permit #(if assigned)

IF MORE THAN (1) LOCATION, PLEASE COMPLETE PART D-2 ON THE BACK OF THIS FORM

Street

State of Rhode Island Division of Taxation

One Capitol Hill STE 36 Providence, RI 02908-5829

City

Cigarettes/Tobacco/Other Tobacco -

LIMITED LIABILITY COMPANIES:

Actual Rhode Island Location No. and Street (include apt. office or unit #, if any) CANNOT ACCEPT PO BOX #

Mailing Address No and Street or P.O BOX (include apt. office or unit#, if any)

WWW.TAX.RI.GOV

City or Town

Will you be selling:

LLC-PARTNERSHIP

Fees and Instructions: Sales permit is renewable at fiscal year

ending June 30th

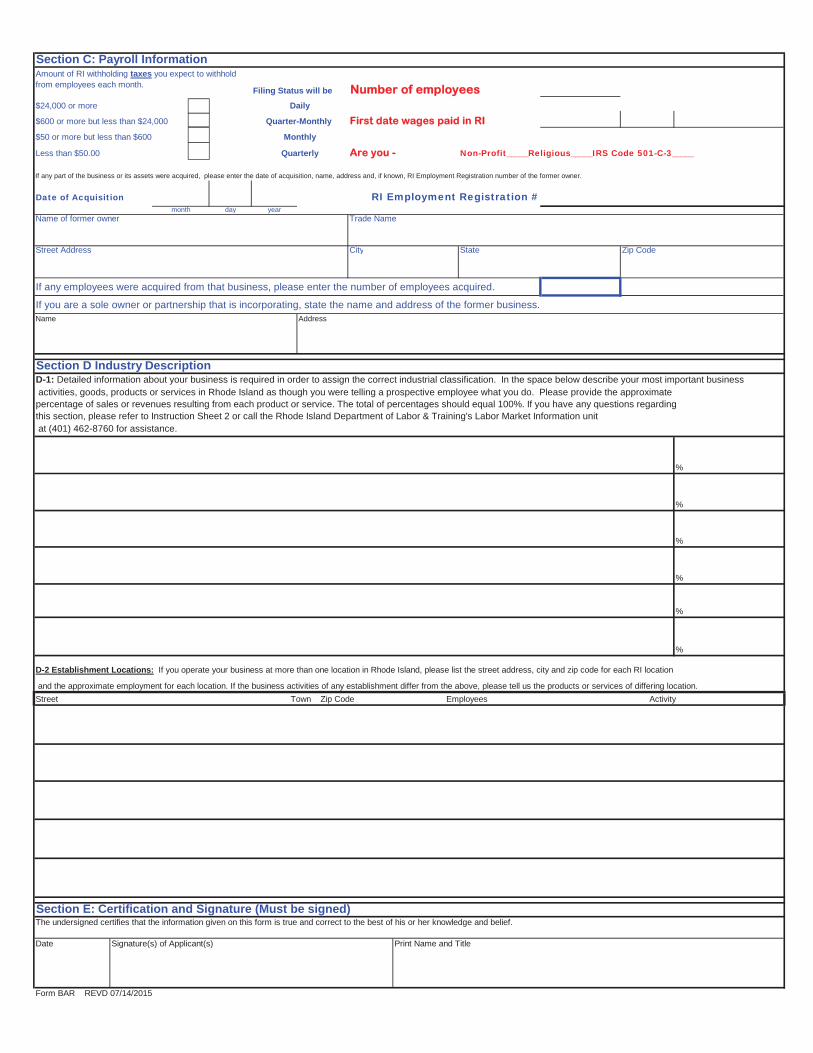

Section C: Payroll InformationAmount of RI withholding taxes you expect to withhold from employees each month.

Filing Status will be Number of employees$24,000 or more Daily

$600 or more but less than $24,000 Quarter-Monthly First date wages paid in RI $50 or more but less than $600 Monthly

Less than $50.00 Quarterly Are you - Non-Profit_____Religious_____IRS Code 501-C-3_____

If any part of the business or its assets were acquired, please enter the date of acquisition, name, address and, if known, RI Employment Registration number of the former owner.

Date of Acquisition month day year

Name of former owner Trade Name

Street Address City State Zip Code

If any employees were acquired from that business, please enter the number of employees acquired.

If you are a sole owner or partnership that is incorporating, state the name and address of the former business. Name Address

Section D Industry Description

%

%

%

%

%

%

D-2 Establishment Locations: If you operate your business at more than one location in Rhode Island, please list the street address, city and zip code for each RI location

and the approximate employment for each location. If the business activities of any establishment differ from the above, please tell us the products or services of differing location.

Section E: Certification and Signature (Must be signed)The undersigned certifies that the information given on this form is true and correct to the best of his or her knowledge and belief.

Date Signature(s) of Applicant(s) Print Name and Title

Form BAR REVD 07/14/2015

RI Employment Registration #

D-1: Detailed information about your business is required in order to assign the correct industrial classification. In the space below describe your most important business activities, goods, products or services in Rhode Island as though you were telling a prospective employee what you do. Please provide the approximate percentage of sales or revenues resulting from each product or service. The total of percentages should equal 100%. If you have any questions regarding

Street ActivityEmployeesTown Zip Code

this section, please refer to Instruction Sheet 2 or call the Rhode Island Department of Labor & Training's Labor Market Information unit at (401) 462-8760 for assistance.

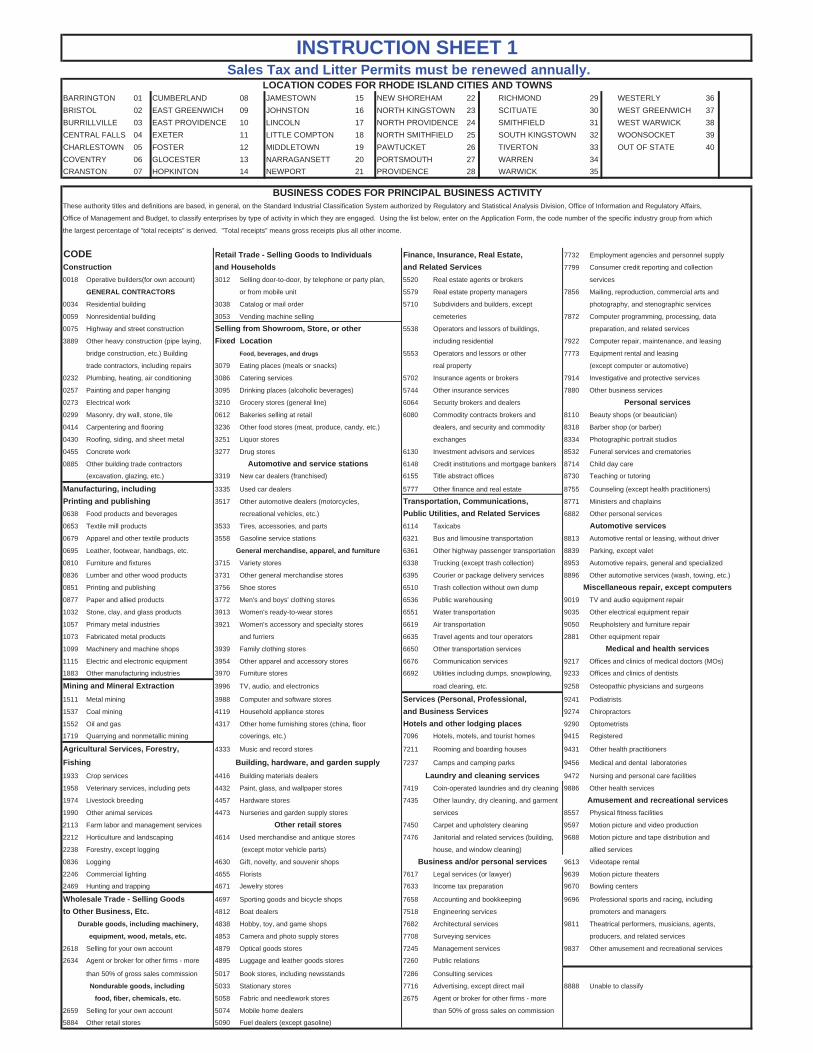

Sales Tax and Litter Permits must be renewed annually.LOCATION CODES FOR RHODE ISLAND CITIES AND TOWNS

BARRINGTON 01 CUMBERLAND 08 JAMESTOWN 15 NEW SHOREHAM 22 RICHMOND 29 WESTERLY 36BRISTOL 02 EAST GREENWICH 09 JOHNSTON 16 NORTH KINGSTOWN 23 SCITUATE 30 WEST GREENWICH 37BURRILLVILLE 03 EAST PROVIDENCE 10 LINCOLN 17 NORTH PROVIDENCE 24 SMITHFIELD 31 WEST WARWICK 38CENTRAL FALLS 04 EXETER 11 LITTLE COMPTON 18 NORTH SMITHFIELD 25 SOUTH KINGSTOWN 32 WOONSOCKET 39CHARLESTOWN 05 FOSTER 12 MIDDLETOWN 19 PAWTUCKET 26 TIVERTON 33 OUT OF STATE 40COVENTRY 06 GLOCESTER 13 NARRAGANSETT 20 PORTSMOUTH 27 WARREN 34CRANSTON 07 HOPKINTON 14 NEWPORT 21 PROVIDENCE 28 WARWICK 35

BUSINESS CODES FOR PRINCIPAL BUSINESS ACTIVITYThese authority titles and definitions are based, in general, on the Standard Industrial Classification System authorized by Regulatory and Statistical Analysis Division, Office of Information and Regulatory Affairs,

Office of Management and Budget, to classify enterprises by type of activity in which they are engaged. Using the list below, enter on the Application Form, the code number of the specific industry group from which

the largest percentage of "total receipts" is derived. "Total receipts" means gross receipts plus all other income.

Retail Trade - Selling Goods to Individuals Finance, Insurance, Real Estate, 7732 Employment agencies and personnel supply

Construction and Households and Related Services 7799 Consumer credit reporting and collection

0018 Operative builders(for own account) 3012 Selling door-to-door, by telephone or party plan, 5520 Real estate agents or brokers services

GENERAL CONTRACTORS or from mobile unit 5579 Real estate property managers 7856 Mailing, reproduction, commercial arts and

0034 Residential building 3038 Catalog or mail order 5710 Subdividers and builders, except photography, and stenographic services

0059 Nonresidential building 3053 Vending machine selling cemeteries 7872 Computer programming, processing, data

0075 Highway and street construction Selling from Showroom, Store, or other 5538 Operators and lessors of buildings, preparation, and related services

3889 Other heavy construction (pipe laying, Fixed Location including residential 7922 Computer repair, maintenance, and leasing

bridge construction, etc.) Building Food, beverages, and drugs 5553 Operators and lessors or other 7773 Equipment rental and leasing

trade contractors, including repairs 3079 Eating places (meals or snacks) real property (except computer or automotive)

0232 Plumbing, heating, air conditioning 3086 Catering services 5702 Insurance agents or brokers 7914 Investigative and protective services

0257 Painting and paper hanging 3095 Drinking places (alcoholic beverages) 5744 Other insurance services 7880 Other business services

0273 Electrical work 3210 Grocery stores (general line) 6064 Security brokers and dealers

0299 Masonry, dry wall, stone, tile 0612 Bakeries selling at retail 6080 Commodity contracts brokers and 8110 Beauty shops (or beautician)

0414 Carpentering and flooring 3236 Other food stores (meat, produce, candy, etc.) dealers, and security and commodity 8318 Barber shop (or barber)

0430 Roofing, siding, and sheet metal 3251 Liquor stores exchanges 8334 Photographic portrait studios

0455 Concrete work 3277 Drug stores 6130 Investment advisors and services 8532 Funeral services and crematories

0885 Other building trade contractors 6148 Credit institutions and mortgage bankers 8714 Child day care

(excavation, glazing, etc.) 3319 New car dealers (franchised) 6155 Title abstract offices 8730 Teaching or tutoring

Manufacturing, including 3335 Used car dealers 5777 Other finance and real estate 8755 Counseling (except health practitioners)

Printing and publishing 3517 Other automotive dealers (motorcycles, Transportation, Communications, 8771 Ministers and chaplains

0638 Food products and beverages recreational vehicles, etc.) Public Utilities, and Related Services 6882 Other personal services

0653 Textile mill products 3533 Tires, accessories, and parts 6114 Taxicabs Automotive services0679 Apparel and other textile products 3558 Gasoline service stations 6321 Bus and limousine transportation 8813 Automotive rental or leasing, without driver

0695 Leather, footwear, handbags, etc. 6361 Other highway passenger transportation 8839 Parking, except valet

0810 Furniture and fixtures 3715 Variety stores 6338 Trucking (except trash collection) 8953 Automotive repairs, general and specialized

0836 Lumber and other wood products 3731 Other general merchandise stores 6395 Courier or package delivery services 8896 Other automotive services (wash, towing, etc.)

0851 Printing and publishing 3756 Shoe stores 6510 Trash collection without own dump

0877 Paper and allied products 3772 Men's and boys' clothing stores 6536 Public warehousing 9019 TV and audio equipment repair

1032 Stone, clay, and glass products 3913 Women's ready-to-wear stores 6551 Water transportation 9035 Other electrical equipment repair

1057 Primary metal industries 3921 Women's accessory and specialty stores 6619 Air transportation 9050 Reupholstery and furniture repair

1073 Fabricated metal products and furriers 6635 Travel agents and tour operators 2881 Other equipment repair

1099 Machinery and machine shops 3939 Family clothing stores 6650 Other transportation services

1115 Electric and electronic equipment 3954 Other apparel and accessory stores 6676 Communication services 9217 Offices and clinics of medical doctors (MOs)

1883 Other manufacturing industries 3970 Furniture stores 6692 Utilities including dumps, snowplowing, 9233 Offices and clinics of dentists

Mining and Mineral Extraction 3996 TV, audio, and electronics road clearing, etc. 9258 Osteopathic physicians and surgeons

1511 Metal mining 3988 Computer and software stores Services (Personal, Professional, 9241 Podiatrists

1537 Coal mining 4119 Household appliance stores and Business Services 9274 Chiropractors

1552 Oil and gas 4317 Other home furnishing stores (china, floor 9290 Optometrists

1719 Quarrying and nonmetallic mining coverings, etc.) 7096 Hotels, motels, and tourist homes 9415 Registered

Agricultural Services, Forestry, 4333 Music and record stores 7211 Rooming and boarding houses 9431 Other health practitioners

Fishing 7237 Camps and camping parks 9456 Medical and dental laboratories

1933 Crop services 4416 Building materials dealers 9472 Nursing and personal care facilities

1958 Veterinary services, including pets 4432 Paint, glass, and wallpaper stores 7419 Coin-operated laundries and dry cleaning 9886 Other health services

1974 Livestock breeding 4457 Hardware stores 7435 Other laundry, dry cleaning, and garment

1990 Other animal services 4473 Nurseries and garden supply stores services 8557 Physical fitness facilities

2113 Farm labor and management services 7450 Carpet and upholstery cleaning 9597 Motion picture and video production

2212 Horticulture and landscaping 4614 Used merchandise and antique stores 7476 Janitorial and related services (building, 9688 Motion picture and tape distribution and

2238 Forestry, except logging (except motor vehicle parts) house, and window cleaning) allied services

0836 Logging 4630 Gift, novelty, and souvenir shops 9613 Videotape rental

2246 Commercial lighting 4655 Florists 7617 Legal services (or lawyer) 9639 Motion picture theaters

2469 Hunting and trapping 4671 Jewelry stores 7633 Income tax preparation 9670 Bowling centers

Wholesale Trade - Selling Goods 4697 Sporting goods and bicycle shops 7658 Accounting and bookkeeping 9696 Professional sports and racing, including

to Other Business, Etc. 4812 Boat dealers 7518 Engineering services promoters and managers

4838 Hobby, toy, and game shops 7682 Architectural services 9811 Theatrical performers, musicians, agents,

4853 Camera and photo supply stores 7708 Surveying services producers, and related services

2618 Selling for your own account 4879 Optical goods stores 7245 Management services 9837 Other amusement and recreational services

2634 Agent or broker for other firms - more 4895 Luggage and leather goods stores 7260 Public relations

than 50% of gross sales commission 5017 Book stores, including newsstands 7286 Consulting services

5033 Stationary stores 7716 Advertising, except direct mail 8888 Unable to classify

5058 Fabric and needlework stores 2675 Agent or broker for other firms - more

2659 Selling for your own account 5074 Mobile home dealers than 50% of gross sales on commission

5884 Other retail stores 5090 Fuel dealers (except gasoline)

INSTRUCTION SHEET 1

CODE

Personal services

Automotive and service stations

Amusement and recreational services

Other retail stores

General merchandise, apparel, and furniture

Miscellaneous repair, except computers

Medical and health services

Hotels and other lodging places

food, fiber, chemicals, etc.

Business and/or personal services

Durable goods, including machinery,

equipment, wood, metals, etc.

Nondurable goods, including

Building, hardware, and garden supplyLaundry and cleaning services

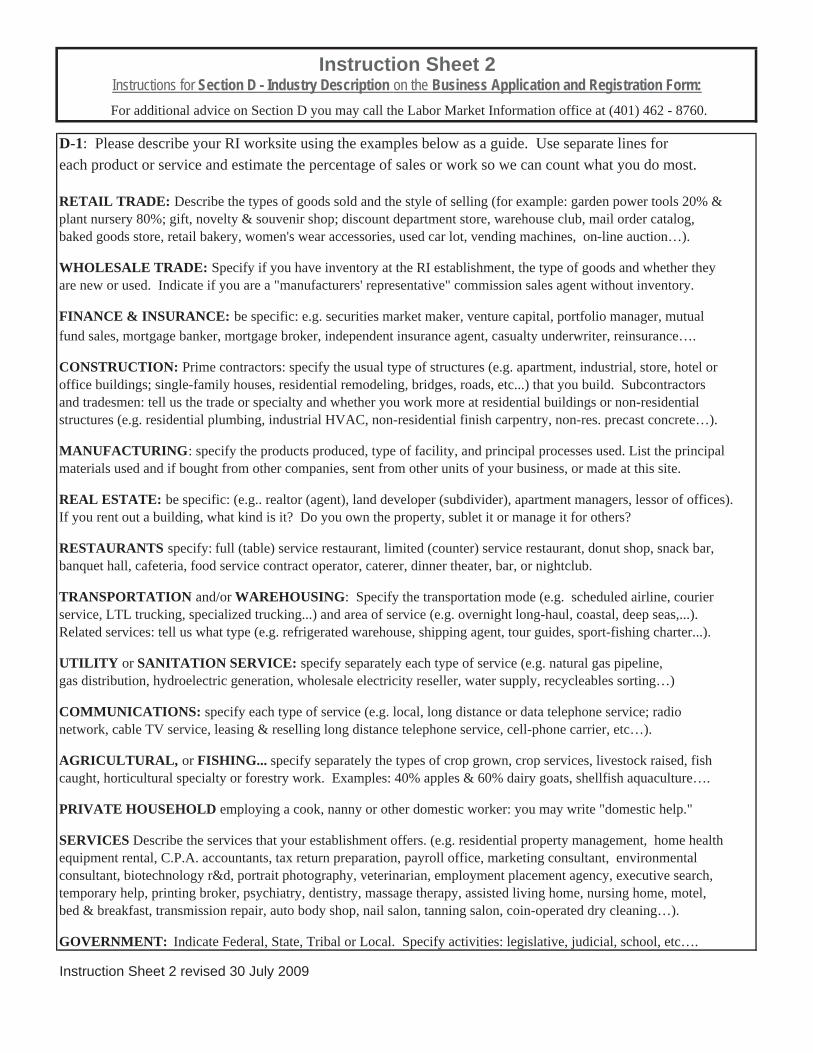

Instruction Sheet 2Instructions for Section D - Industry Description on the Business Application and Registration Form:For additional advice on Section D you may call the Labor Market Information office at (401) 462 - 8760.

D-1: Please describe your RI worksite using the examples below as a guide. Use separate lines foreach product or service and estimate the percentage of sales or work so we can count what you do most.

RETAIL TRADE: Describe the types of goods sold and the style of selling (for example: garden power tools 20% &plant nursery 80%; gift, novelty & souvenir shop; discount department store, warehouse club, mail order catalog,baked goods store, retail bakery, women's wear accessories, used car lot, vending machines, on-line auction…).

WHOLESALE TRADE: Specify if you have inventory at the RI establishment, the type of goods and whether theyare new or used. Indicate if you are a "manufacturers' representative" commission sales agent without inventory.

FINANCE & INSURANCE: be specific: e.g. securities market maker, venture capital, portfolio manager, mutualfund sales, mortgage banker, mortgage broker, independent insurance agent, casualty underwriter, reinsurance….

CONSTRUCTION: Prime contractors: specify the usual type of structures (e.g. apartment, industrial, store, hotel oroffice buildings; single-family houses, residential remodeling, bridges, roads, etc...) that you build. Subcontractorsand tradesmen: tell us the trade or specialty and whether you work more at residential buildings or non-residentialstructures (e.g. residential plumbing, industrial HVAC, non-residential finish carpentry, non-res. precast concrete…).

MANUFACTURING: specify the products produced, type of facility, and principal processes used. List the principalmaterials used and if bought from other companies, sent from other units of your business, or made at this site.

REAL ESTATE: be specific: (e.g.. realtor (agent), land developer (subdivider), apartment managers, lessor of offices).If you rent out a building, what kind is it? Do you own the property, sublet it or manage it for others?

RESTAURANTS specify: full (table) service restaurant, limited (counter) service restaurant, donut shop, snack bar, banquet hall, cafeteria, food service contract operator, caterer, dinner theater, bar, or nightclub.

TRANSPORTATION and/or WAREHOUSING: Specify the transportation mode (e.g. scheduled airline, courierservice, LTL trucking, specialized trucking...) and area of service (e.g. overnight long-haul, coastal, deep seas,...).Related services: tell us what type (e.g. refrigerated warehouse, shipping agent, tour guides, sport-fishing charter...).

UTILITY or SANITATION SERVICE: specify separately each type of service (e.g. natural gas pipeline, gas distribution, hydroelectric generation, wholesale electricity reseller, water supply, recycleables sorting…)

COMMUNICATIONS: specify each type of service (e.g. local, long distance or data telephone service; radio network, cable TV service, leasing & reselling long distance telephone service, cell-phone carrier, etc…).

AGRICULTURAL, or FISHING... specify separately the types of crop grown, crop services, livestock raised, fish caught, horticultural specialty or forestry work. Examples: 40% apples & 60% dairy goats, shellfish aquaculture….

PRIVATE HOUSEHOLD employing a cook, nanny or other domestic worker: you may write "domestic help."

SERVICES Describe the services that your establishment offers. (e.g. residential property management, home healthequipment rental, C.P.A. accountants, tax return preparation, payroll office, marketing consultant, environmental consultant, biotechnology r&d, portrait photography, veterinarian, employment placement agency, executive search,temporary help, printing broker, psychiatry, dentistry, massage therapy, assisted living home, nursing home, motel,bed & breakfast, transmission repair, auto body shop, nail salon, tanning salon, coin-operated dry cleaning…).

GOVERNMENT: Indicate Federal, State, Tribal or Local. Specify activities: legislative, judicial, school, etc….

Instruction Sheet 2 revised 30 July 2009

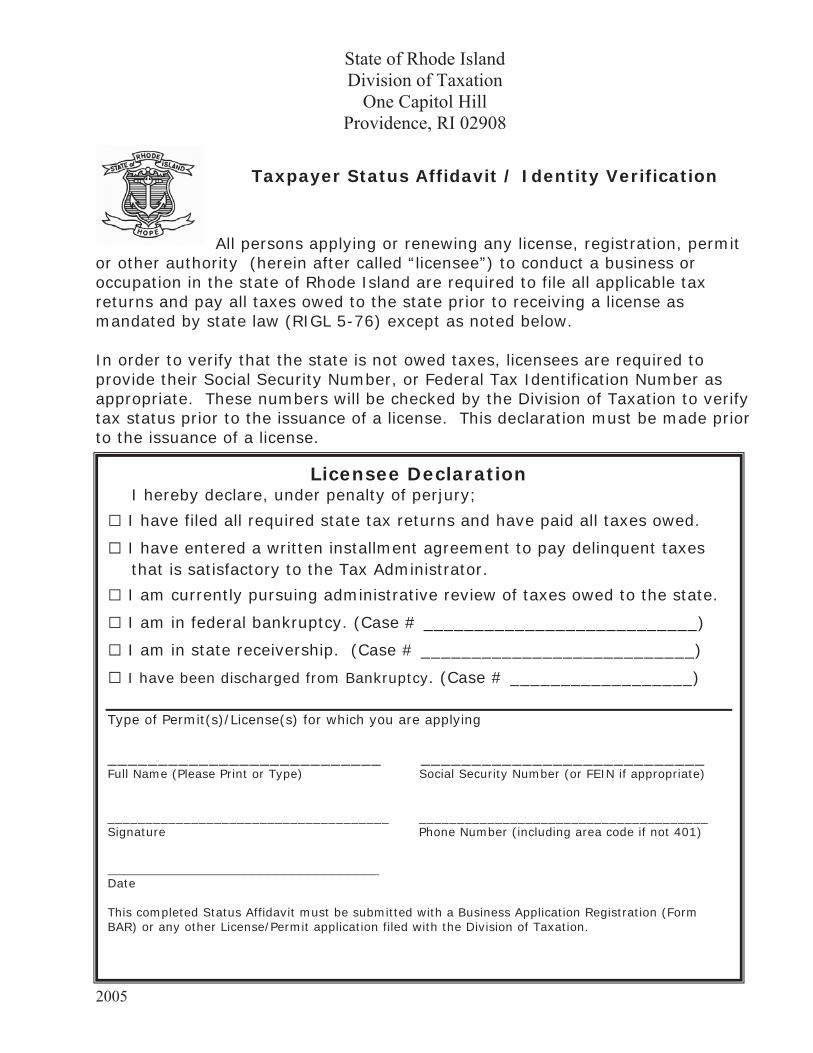

State of Rhode Island Division of Taxation

One Capitol Hill Providence, RI 02908

2005

Taxpayer Status Affidavit / Identity Verification

All persons applying or renewing any license, registration, permit or other authority (herein after called “licensee”) to conduct a business or occupation in the state of Rhode Island are required to file all applicable tax returns and pay all taxes owed to the state prior to receiving a license as mandated by state law (RIGL 5-76) except as noted below. In order to verify that the state is not owed taxes, licensees are required to provide their Social Security Number, or Federal Tax Identification Number as appropriate. These numbers will be checked by the Division of Taxation to verify tax status prior to the issuance of a license. This declaration must be made prior to the issuance of a license. Licensee Declaration

I hereby declare, under penalty of perjury;

I have filed all required state tax returns and have paid all taxes owed.

I have entered a written installment agreement to pay delinquent taxes that is satisfactory to the Tax Administrator.

I am currently pursuing administrative review of taxes owed to the state.

I am in federal bankruptcy. (Case # ___________________________)

I am in state receivership. (Case # ___________________________)

I have been discharged from Bankruptcy. (Case # __________________) Type of Permit(s)/License(s) for which you are applying ___________________________ ____________________________ Full Name (Please Print or Type) Social Security Number (or FEIN if appropriate) _____________________________________ ______________________________________ Signature Phone Number (including area code if not 401) __________________________________ Date This completed Status Affidavit must be submitted with a Business Application Registration (Form BAR) or any other License/Permit application filed with the Division of Taxation.

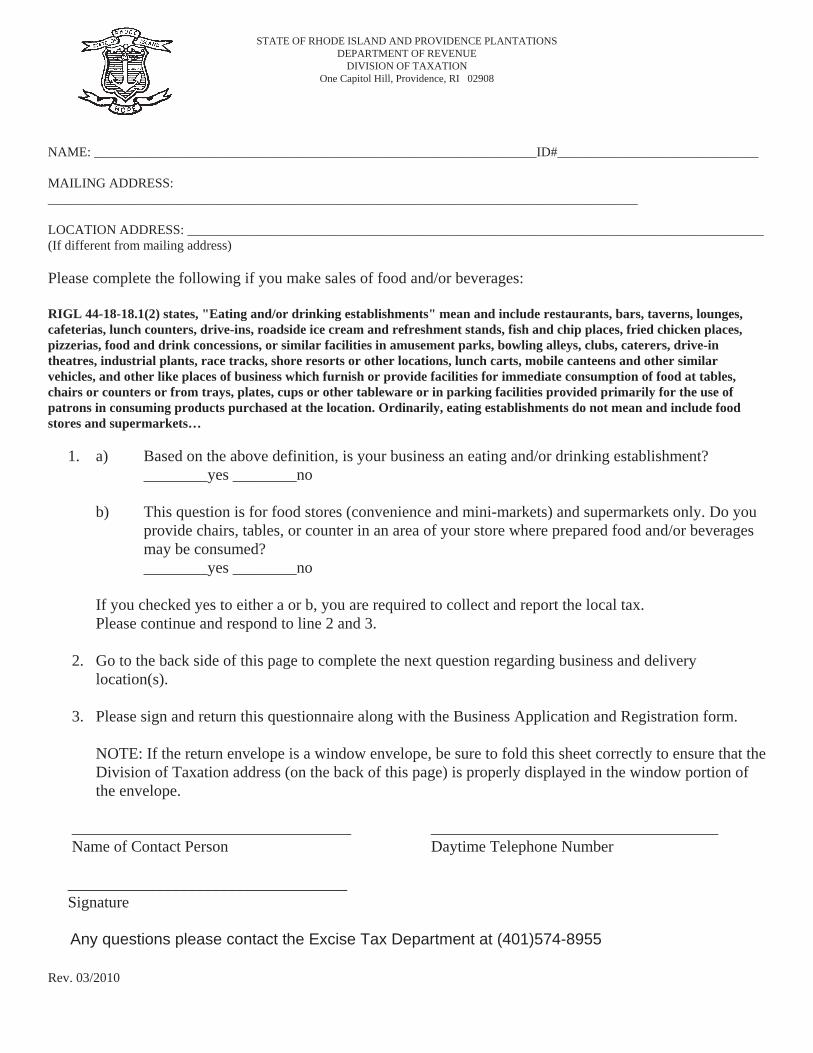

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS DEPARTMENT OF REVENUE

DIVISION OF TAXATION One Capitol Hill, Providence, RI 02908

Rev. 03/2010

NAME: __________________________________________________________________ID#______________________________

MAILING ADDRESS: ________________________________________________________________________________________

LOCATION ADDRESS: ______________________________________________________________________________________ (If different from mailing address)

Please complete the following if you make sales of food and/or beverages:

RIGL 44-18-18.1(2) states, "Eating and/or drinking establishments" mean and include restaurants, bars, taverns, lounges, cafeterias, lunch counters, drive-ins, roadside ice cream and refreshment stands, fish and chip places, fried chicken places, pizzerias, food and drink concessions, or similar facilities in amusement parks, bowling alleys, clubs, caterers, drive-in theatres, industrial plants, race tracks, shore resorts or other locations, lunch carts, mobile canteens and other similar vehicles, and other like places of business which furnish or provide facilities for immediate consumption of food at tables, chairs or counters or from trays, plates, cups or other tableware or in parking facilities provided primarily for the use of patrons in consuming products purchased at the location. Ordinarily, eating establishments do not mean and include food stores and supermarkets…

1. a) Based on the above definition, is your business an eating and/or drinking establishment? ________yes ________no

b) This question is for food stores (convenience and mini-markets) and supermarkets only. Do you provide chairs, tables, or counter in an area of your store where prepared food and/or beverages may be consumed? ________yes ________no

If you checked yes to either a or b, you are required to collect and report the local tax. Please continue and respond to line 2 and 3.

2. Go to the back side of this page to complete the next question regarding business and delivery location(s).

3. Please sign and return this questionnaire along with the Business Application and Registration form.

NOTE: If the return envelope is a window envelope, be sure to fold this sheet correctly to ensure that the Division of Taxation address (on the back of this page) is properly displayed in the window portion of the envelope.

___________________________________ ____________________________________ Name of Contact Person Daytime Telephone Number

___________________________________ Signature

Any questions please contact the Excise Tax Department at (401)574-8955

ID:

Name:

LOCATION CITY/TOWN:

Place a check mark next to the city or town where your eating and/or drinking establishment

is located. Also, if applicable, check the other cities or towns in this state where you deliver meals

and/or beverages.

01 BARRINGTON

04 CENTRAL FALLS

03 BURRILLVILLE

02 BRISTOL

05 CHARLESTOWN

08 CUMBERLAND

07 CRANSTON

06 COVENTRY

09 EAST GREENWICH

12 FOSTER

11 EXETER

10 EAST PROVIDENCE

13 GLOCESTER

16 JOHNSTON

15 JAMESTOWN

14 HOPKINTON

17 LINCOLN

20 NARRAGANSETT

19 MIDDLETOWN

18 LITTLE COMPTON

21 NEWPORT

24 NORTH PROVIDENCE

23 NORTH KINGSTOWN

22 NEW SHOREHAM

25 NORTH SMITHFIELD

28 PROVIDENCE

27 PORTSMOUTH

26 PAWTUCKET

29 RICHMOND

32 SOUTH KINGSTOWN

31 SMITHFIELD

30 SCITUATE

33 TIVERTON

36 WESTERLY

35 WARWICK

34 WARREN

37 WEST GREENWICH

39 WOONSOCKET

38 WEST WARWICK

RHODE ISLAND DIVISION OF TAXATION

ONE CAPITOL HILL

PROVIDENCE, RI 02908

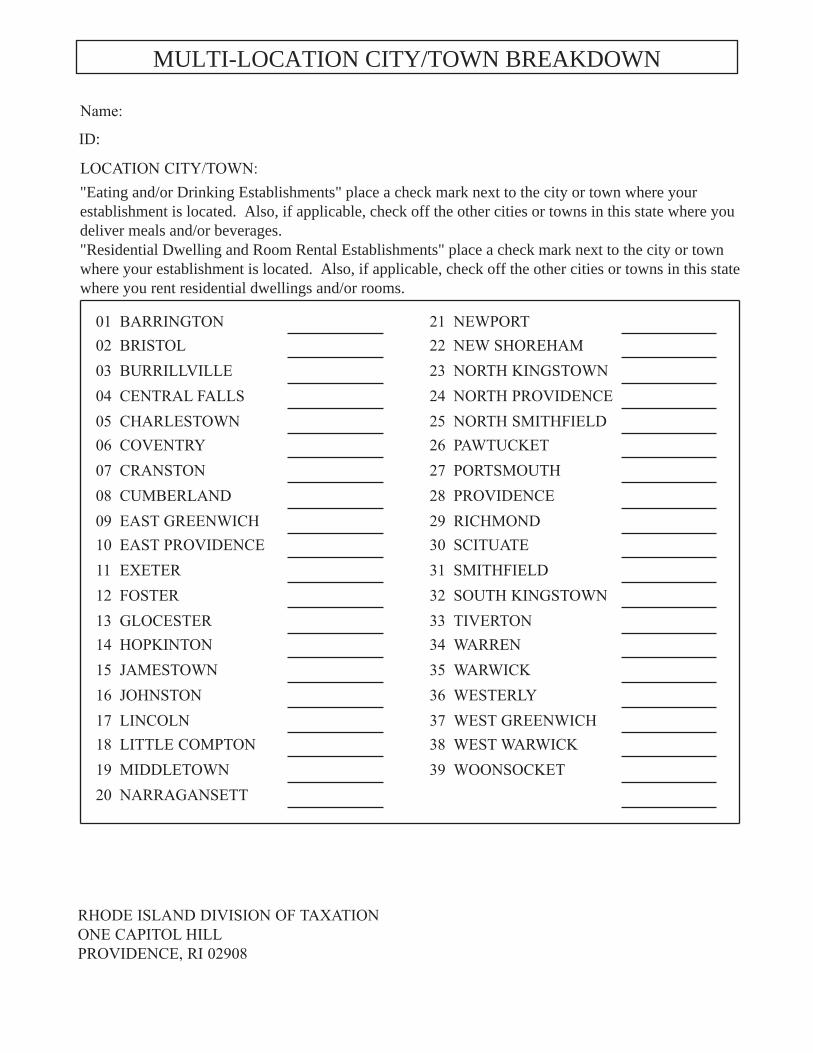

MULTI-LOCATION CITY/TOWN BREAKDOWN

ID:

"Eating and/or Drinking Establishments" place a check mark next to the city or town where yourestablishment is located. Also, if applicable, check off the other cities or towns in this state where youdeliver meals and/or beverages."Residential Dwelling and Room Rental Establishments" place a check mark next to the city or townwhere your establishment is located. Also, if applicable, check off the other cities or towns in this statewhere you rent residential dwellings and/or rooms.

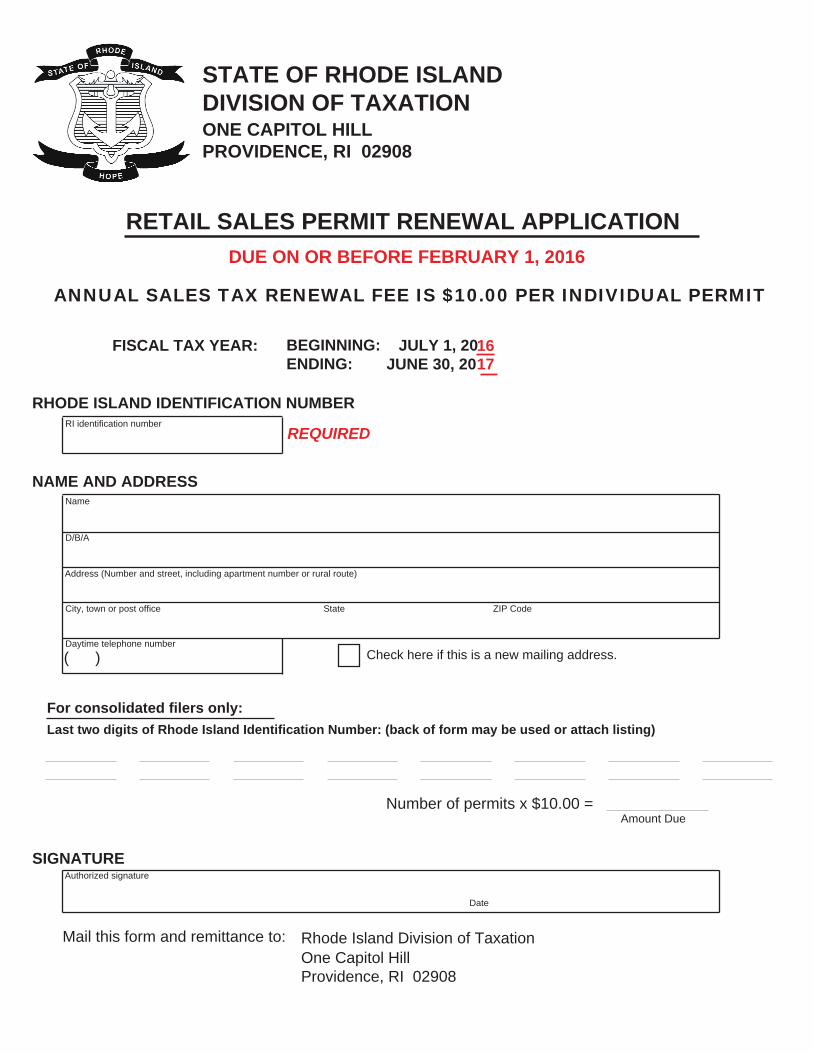

STATE OF RHODE ISLANDDIVISION OF TAXATIONONE CAPITOL HILLPROVIDENCE, RI 02908

RETAIL SALES PERMIT RENEWAL APPLICATIONDUE ON OR BEFORE FEBRUARY 1, 2016

ANNUAL SALES TAX RENEWAL FEE IS $10.00 PER INDIVIDUAL PERMIT

NAME AND ADDRESS

D/B/A

Address (Number and street, including apartment number or rural route)

City, town or post office State ZIP Code

Daytime telephone number

( ) Check here if this is a new mailing address.

SIGNATUREAuthorized signature

Date

Mail this form and remittance to: Rhode Island Division of TaxationOne Capitol HillProvidence, RI 02908

RHODE ISLAND IDENTIFICATION NUMBERRI identification number

BEGINNING:ENDING:

REQUIRED

FISCAL TAX YEAR: JULY 1, 2016JUNE 30, 2017

Name

For consolidated filers only:Last two digits of Rhode Island Identification Number: (back of form may be used or attach listing)

Number of permits x $10.00 =Amount Due

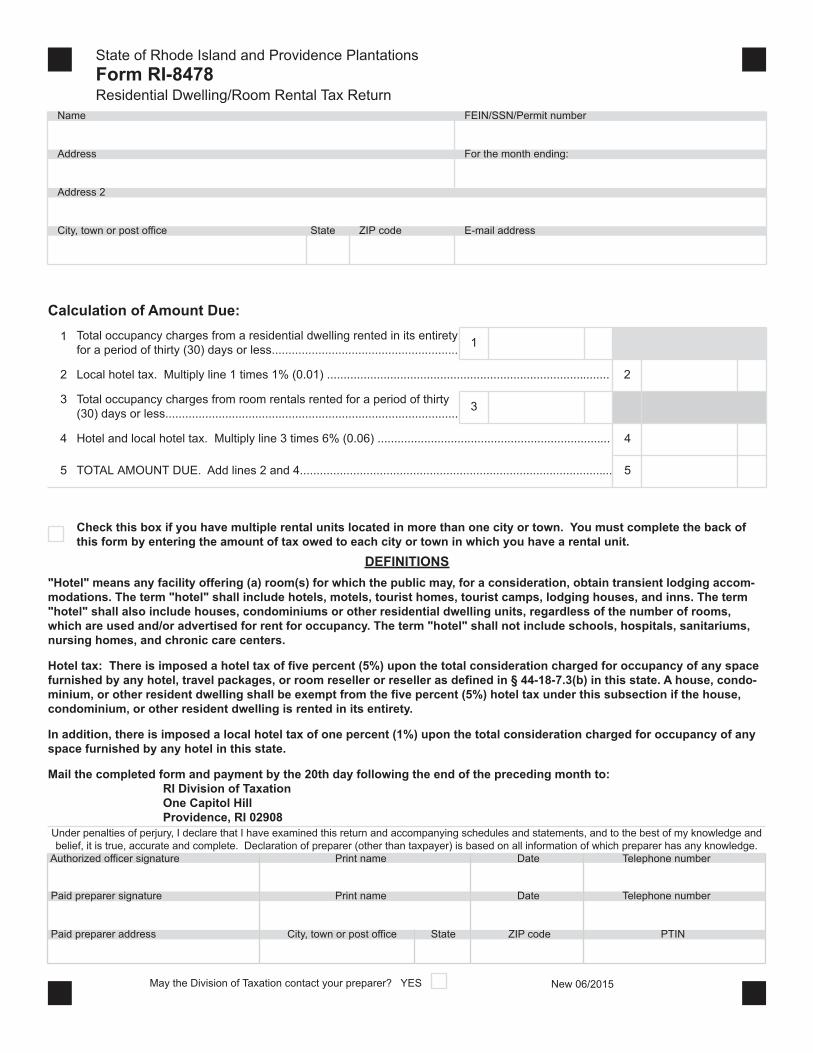

Calculation of Amount Due:

Total occupancy charges from a residential dwelling rented in its entirety

for a period of thirty (30) days or less........................................................1

1

22 Local hotel tax. Multiply line 1 times 1% (0.01) .....................................................................................

Total occupancy charges from room rentals rented for a period of thirty

(30) days or less........................................................................................

3

5

4

TOTAL AMOUNT DUE. Add lines 2 and 4..............................................................................................5

4

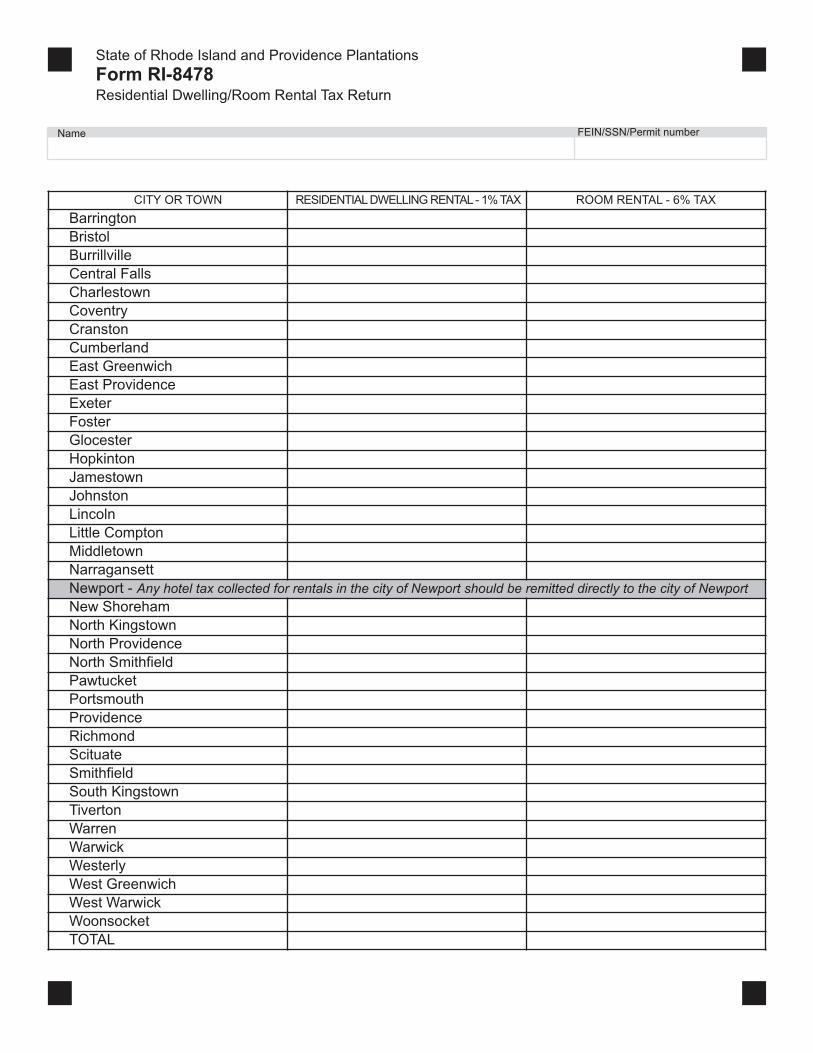

Check this box if you have multiple rental units located in more than one city or town. You must complete the back of

this form by entering the amount of tax owed to each city or town in which you have a rental unit.

"Hotel" means any facility offering (a) room(s) for which the public may, for a consideration, obtain transient lodging accom-

modations. The term "hotel" shall include hotels, motels, tourist homes, tourist camps, lodging houses, and inns. The term

"hotel" shall also include houses, condominiums or other residential dwelling units, regardless of the number of rooms,

which are used and/or advertised for rent for occupancy. The term "hotel" shall not include schools, hospitals, sanitariums,

nursing homes, and chronic care centers.

Hotel tax: There is imposed a hotel tax of five percent (5%) upon the total consideration charged for occupancy of any space

furnished by any hotel, travel packages, or room reseller or reseller as defined in § 44-18-7.3(b) in this state. A house, condo-

minium, or other resident dwelling shall be exempt from the five percent (5%) hotel tax under this subsection if the house,

condominium, or other resident dwelling is rented in its entirety.

In addition, there is imposed a local hotel tax of one percent (1%) upon the total consideration charged for occupancy of any

space furnished by any hotel in this state.

Mail the completed form and payment by the 20th day following the end of the preceding month to:

RI Division of Taxation

One Capitol Hill

Providence, RI 02908

3

Hotel and local hotel tax. Multiply line 3 times 6% (0.06) ......................................................................

State of Rhode Island and Providence Plantations

Form RI-8478Residential Dwelling/Room Rental Tax Return

Name

City, town or post office State ZIP code

FEIN/SSN/Permit number

E-mail address

Address

Address 2

For the month ending:

Authorized officer signature Print name Date Telephone number

Paid preparer address City, town or post office State ZIP code PTIN

Paid preparer signature Print name Date Telephone number

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and

belief, it is true, accurate and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

May the Division of Taxation contact your preparer? YES New 06/2015

DEFINITIONS

CITY OR TOWN RESIDENTIAL DWELLING RENTAL - 1% TAX ROOM RENTAL - 6% TAX

Barrington

Bristol

Burrillville

Central Falls

Charlestown

Coventry

Cranston

Cumberland

East Greenwich

East Providence

Exeter

Foster

Glocester

Hopkinton

Jamestown

Johnston

Lincoln

Little Compton

Middletown

Narragansett

Newport - Any hotel tax collected for rentals in the city of Newport should be remitted directly to the city of NewportNew Shoreham

North Kingstown

North Providence

North Smithfield

Pawtucket

Portsmouth

Providence

Richmond

Scituate

Smithfield

South Kingstown

Tiverton

Warren

Warwick

Westerly

West Greenwich

West Warwick

Woonsocket

TOTAL

State of Rhode Island and Providence Plantations

Form RI-8478Residential Dwelling/Room Rental Tax Return

Name FEIN/SSN/Permit number

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONSDIVISION OF TAXATION - DEPT#300 - PO BOX 9706 - PROVIDENCE, RI 02940-9706

SALES & USE TAX RETURN

MONTHLY

I HEREBY CERTIFY THAT THIS RETURN, TO THE BEST OF MY KNOWLEDGE ANDBELIEF, IS A TRUE, CORRECT AND COMPLETE RETURN.SIGNATURE OF OWNER, PARTNER OR AUTHORIZED AGENT

TITLE DATE

RETURN FOR MONTH ENDINGFEDERAL IDENTIFICATION NUMBER NET SALES AND USETAX DUE AND PAID

$

FO

RM

T-2

04M

RE

VD

7/2

011

STM

NAME

ADDRESS

CITY, STATE & ZIP CODE

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONSDIVISION OF TAXATION - DEPT#300 - PO BOX 9706 - PROVIDENCE, RI 02940-9706

SALES & USE TAX RETURN

MONTHLY

I HEREBY CERTIFY THAT THIS RETURN, TO THE BEST OF MY KNOWLEDGE ANDBELIEF, IS A TRUE, CORRECT AND COMPLETE RETURN.SIGNATURE OF OWNER, PARTNER OR AUTHORIZED AGENT

TITLE DATE

RETURN FOR MONTH ENDINGFEDERAL IDENTIFICATION NUMBER NET SALES AND USETAX DUE AND PAID

$

FO

RM

T-2

04M

RE

VD

7/2

011

STM

NAME

ADDRESS

CITY, STATE & ZIP CODE

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONSDIVISION OF TAXATION - DEPT#300 - PO BOX 9706 - PROVIDENCE, RI 02940-9706

SALES & USE TAX RETURN

MONTHLY

I HEREBY CERTIFY THAT THIS RETURN, TO THE BEST OF MY KNOWLEDGE ANDBELIEF, IS A TRUE, CORRECT AND COMPLETE RETURN.SIGNATURE OF OWNER, PARTNER OR AUTHORIZED AGENT

TITLE DATE

RETURN FOR MONTH ENDINGFEDERAL IDENTIFICATION NUMBER NET SALES AND USETAX DUE AND PAID

$

FO

RM

T-2

04M

RE

VD

7/2

011

STM

NAME

ADDRESS

CITY, STATE & ZIP CODE

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

DEPARTMENT OF REVENUE

DIVISION OF TAXATION

THESE RETURNS ARE TO BE USED BY SELLERS OF TANGIBLE PERSONAL PROPERTY.

CONSUMERS WHO ARE NOT RETAILERS SHOULD USE FORM T-205 FOR REPORTING USE TAX.

ELECTRONIC FUNDS TRANSFER (EFT) IS MANDATED FOR SOME TAXPAYERS. BOTH ACH CREDIT AND ACH DEBIT

METHODS ARE AVAILABLE. FOR INFORMATION CONTACT THE DIVISION’S EFT SECTION AT (401) 574-8484.

INSTRUCTIONS FOR PREPARING MONTHLY SALES & USE TAX RETURN

To report sales and use tax for each month, locate the return for the month you need to report and enter the amount of sales and use tax due for that month. Ifyou have no tax due for the month, enter “- 0 - “. No other sales or deduction information is reported on these returns. The tax reported should include all salestax due, as well as any use tax that is due for the month.

Monthly sales & use tax returns are due on or before the 20th of each month for the previous calendar month.

A return must be filed for each quarter even if no tax is due.

YOUR RETAIL SALES PERMIT MUST BE RENEWED BY FEBRUARY 1, 2012.

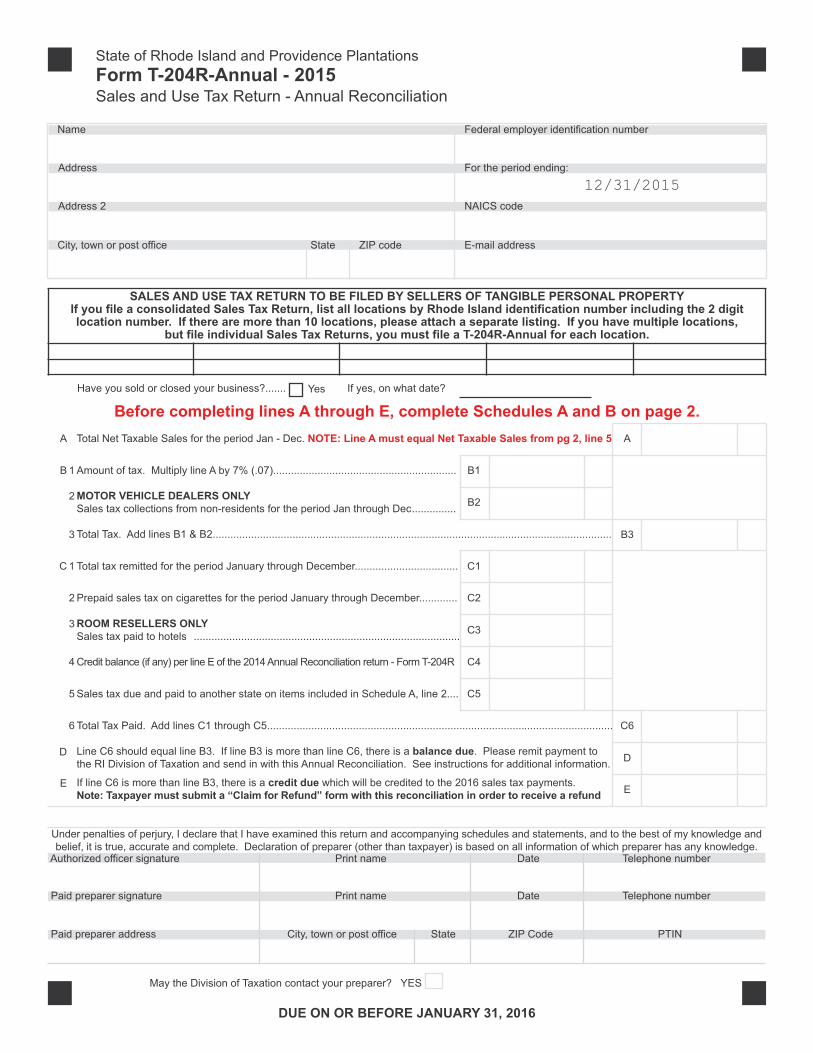

Have you sold or closed your business?....... Yes If yes, on what date?

Before completing lines A through E, complete Schedules A and B on page 2.

SALES AND USE TAX RETURN TO BE FILED BY SELLERS OF TANGIBLE PERSONAL PROPERTYIf you file a consolidated Sales Tax Return, list all locations by Rhode Island identification number including the 2 digit location number. If there are more than 10 locations, please attach a separate listing. If you have multiple locations,

but file individual Sales Tax Returns, you must file a T-204R-Annual for each location.

State of Rhode Island and Providence Plantations

Form T-204R-Annual - 2015Sales and Use Tax Return - Annual Reconciliation

ATotal Net Taxable Sales for the period Jan - Dec. NOTE: Line A must equal Net Taxable Sales from pg 2, line 5

B1

A

Amount of tax. Multiply line A by 7% (.07)..............................................................

B2

B

MOTOR VEHICLE DEALERS ONLY

Sales tax collections from non-residents for the period Jan through Dec...............

B3Total Tax. Add lines B1 & B2.......................................................................................................................................

C1Total tax remitted for the period January through December...................................

C2

C

Prepaid sales tax on cigarettes for the period January through December.............

ROOM RESELLERS ONLY

Sales tax paid to hotels ..........................................................................................C3

Credit balance (if any) per line E of the 2014 Annual Reconciliation return - Form T-204R C4

Sales tax due and paid to another state on items included in Schedule A, line 2.... C5

C6Total Tax Paid. Add lines C1 through C5.....................................................................................................................

DLine C6 should equal line B3. If line B3 is more than line C6, there is a balance due. Please remit payment tothe RI Division of Taxation and send in with this Annual Reconciliation. See instructions for additional information.

E

D

If line C6 is more than line B3, there is a credit due which will be credited to the 2016 sales tax payments. Note: Taxpayer must submit a “Claim for Refund” form with this reconciliation in order to receive a refund

E

1

2

3

1

2

3

4

5

6

Name

Address

Address 2

Federal employer identification number

For the period ending:

NAICS code

City, town or post office State ZIP code E-mail address

DUE ON OR BEFORE JANUARY 31, 2016

12/31/2015

Authorized officer signature Print name Date Telephone number

Paid preparer address City, town or post office State ZIP Code PTIN

Paid preparer signature Print name Date Telephone number

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge andbelief, it is true, accurate and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

May the Division of Taxation contact your preparer? YES

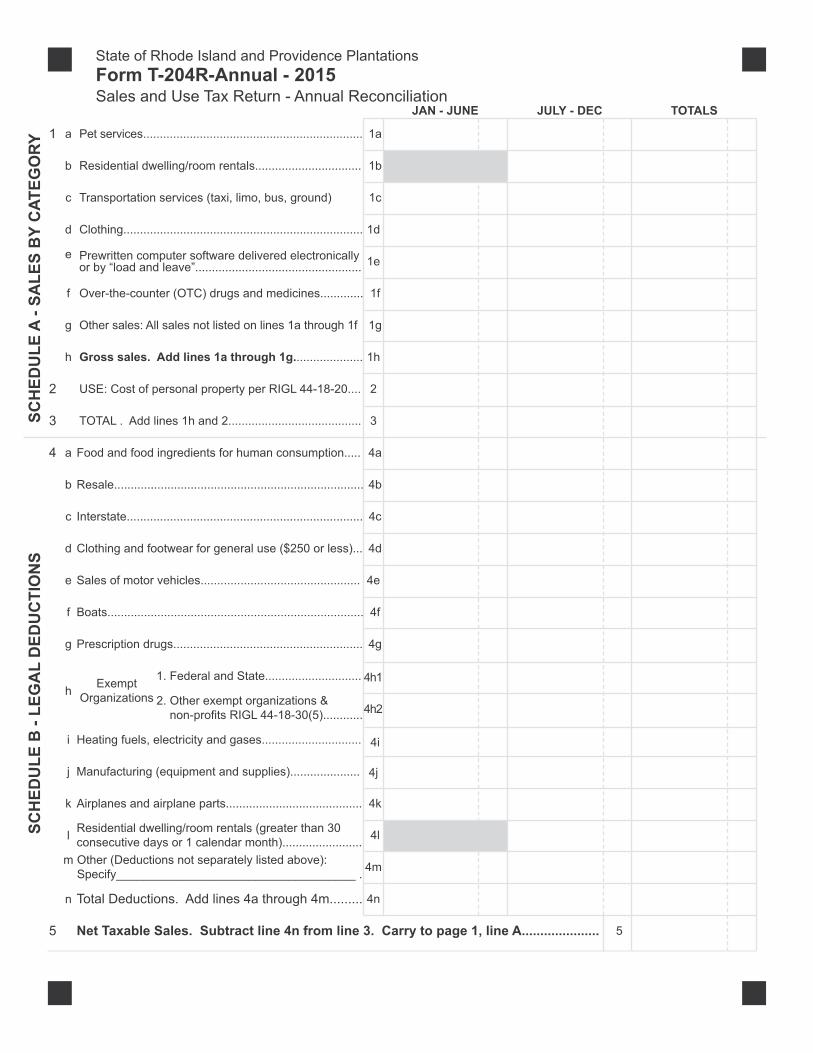

JULY - DEC

Pet services..................................................................

Transportation services (taxi, limo, bus, ground)

Clothing........................................................................

SC

HE

DU

LE

B -

LE

GA

L D

ED

UC

TIO

NS

Food and food ingredients for human consumption.....

Resale...........................................................................

Interstate.......................................................................

Sales of motor vehicles................................................

Clothing and footwear for general use ($250 or less)...

Boats.............................................................................

Prescription drugs.........................................................

1. Federal and State.............................

Heating fuels, electricity and gases..............................

2. Other exempt organizations & non-profits RIGL 44-18-30(5)............

Manufacturing (equipment and supplies).....................

Airplanes and airplane parts.........................................

Exempt Organizations

Residential dwelling/room rentals (greater than 30consecutive days or 1 calendar month)........................

Net Taxable Sales. Subtract line 4n from line 3. Carry to page 1, line A.....................

Total Deductions. Add lines 4a through 4m.........

4

1a

1c

1d

4a

4b

4f

4c

4d

4e

4g

4h1

4h2

4j

4k

4l

4i

4m

4n

5

TOTALS

Prewritten computer software delivered electronicallyor by “load and leave”..................................................

Over-the-counter (OTC) drugs and medicines.............

USE: Cost of personal property per RIGL 44-18-20....

TOTAL . Add lines 1h and 2........................................

1e

1f

1g

1h

1

Other sales: All sales not listed on lines 1a through 1f

Gross sales. Add lines 1a through 1g.....................

2

3

a

c

d

e

f

g

h

Residential dwelling/room rentals................................ 1bb

Other (Deductions not separately listed above):Specify____________________________________ .

5

JAN - JUNE

SC

HE

DU

LE

A -

SA

LE

S B

Y C

AT

EG

OR

Y

a

c

d

e

f

g

b

m

2

3

h

j

k

l

n

i

State of Rhode Island and Providence Plantations

Form T-204R-Annual - 2015Sales and Use Tax Return - Annual Reconciliation

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

DEPARTMENT OF REVENUE

DIVISION OF TAXATION

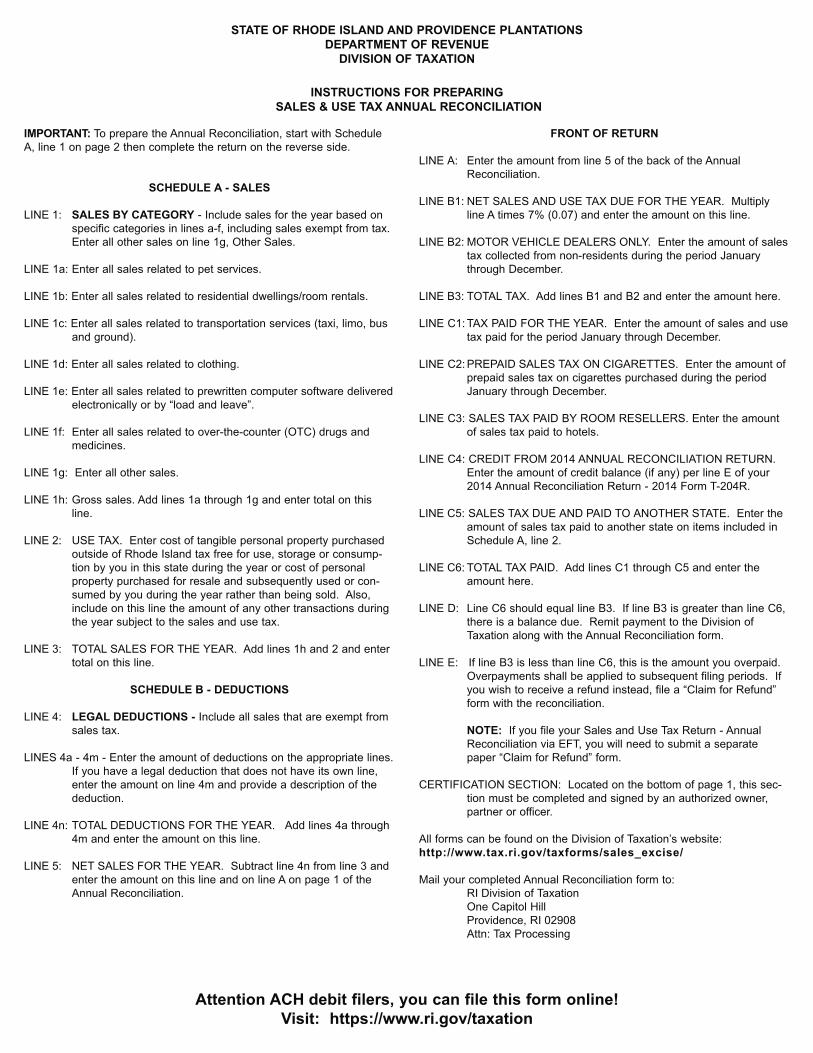

INSTRUCTIONS FOR PREPARING

SALES & USE TAX ANNUAL RECONCILIATION

IMPORTANT: To prepare the Annual Reconciliation, start with ScheduleA, line 1 on page 2 then complete the return on the reverse side.

SCHEDULE A - SALES

LINE 1: SALES BY CATEGORY - Include sales for the year based onspecific categories in lines a-f, including sales exempt from tax.Enter all other sales on line 1g, Other Sales.

LINE 1a: Enter all sales related to pet services.

LINE 1b: Enter all sales related to residential dwellings/room rentals.

LINE 1c: Enter all sales related to transportation services (taxi, limo, busand ground).

LINE 1d: Enter all sales related to clothing.

LINE 1e: Enter all sales related to prewritten computer software delivered electronically or by “load and leave”.

LINE 1f: Enter all sales related to over-the-counter (OTC) drugs andmedicines.

LINE 1g: Enter all other sales.

LINE 1h: Gross sales. Add lines 1a through 1g and enter total on thisline.

LINE 2: USE TAX. Enter cost of tangible personal property purchasedoutside of Rhode Island tax free for use, storage or consump-tion by you in this state during the year or cost of personalproperty purchased for resale and subsequently used or con-sumed by you during the year rather than being sold. Also,include on this line the amount of any other transactions duringthe year subject to the sales and use tax.

LINE 3: TOTAL SALES FOR THE YEAR. Add lines 1h and 2 and entertotal on this line.

SCHEDULE B - DEDUCTIONS

LINE 4: LEGAL DEDUCTIONS - Include all sales that are exempt fromsales tax.

LINES 4a - 4m - Enter the amount of deductions on the appropriate lines.If you have a legal deduction that does not have its own line,enter the amount on line 4m and provide a description of thededuction.

LINE 4n: TOTAL DEDUCTIONS FOR THE YEAR. Add lines 4a through4m and enter the amount on this line.

LINE 5: NET SALES FOR THE YEAR. Subtract line 4n from line 3 and enter the amount on this line and on line A on page 1 of theAnnual Reconciliation.

FRONT OF RETURN

LINE A: Enter the amount from line 5 of the back of the AnnualReconciliation.

LINE B1: NET SALES AND USE TAX DUE FOR THE YEAR. Multiplyline A times 7% (0.07) and enter the amount on this line.

LINE B2: MOTOR VEHICLE DEALERS ONLY. Enter the amount of salestax collected from non-residents during the period Januarythrough December.

LINE B3: TOTAL TAX. Add lines B1 and B2 and enter the amount here.

LINE C1: TAX PAID FOR THE YEAR. Enter the amount of sales and usetax paid for the period January through December.

LINE C2: PREPAID SALES TAX ON CIGARETTES. Enter the amount of prepaid sales tax on cigarettes purchased during the periodJanuary through December.

LINE C3: SALES TAX PAID BY ROOM RESELLERS. Enter the amountof sales tax paid to hotels.

LINE C4: CREDIT FROM 2014 ANNUAL RECONCILIATION RETURN.Enter the amount of credit balance (if any) per line E of your2014 Annual Reconciliation Return - 2014 Form T-204R.

LINE C5: SALES TAX DUE AND PAID TO ANOTHER STATE. Enter theamount of sales tax paid to another state on items included inSchedule A, line 2.

LINE C6: TOTAL TAX PAID. Add lines C1 through C5 and enter theamount here.

LINE D: Line C6 should equal line B3. If line B3 is greater than line C6,there is a balance due. Remit payment to the Division ofTaxation along with the Annual Reconciliation form.

LINE E: If line B3 is less than line C6, this is the amount you overpaid.Overpayments shall be applied to subsequent filing periods. Ifyou wish to receive a refund instead, file a “Claim for Refund”form with the reconciliation.

NOTE: If you file your Sales and Use Tax Return - AnnualReconciliation via EFT, you will need to submit a separatepaper “Claim for Refund” form.

CERTIFICATION SECTION: Located on the bottom of page 1, this sec-tion must be completed and signed by an authorized owner,partner or officer.

All forms can be found on the Division of Taxation’s website:http://www.tax.ri.gov/taxforms/sales_excise/

Mail your completed Annual Reconciliation form to:RI Division of TaxationOne Capitol HillProvidence, RI 02908Attn: Tax Processing

Attention ACH debit filers, you can file this form online!

Visit: https://www.ri.gov/taxation

Page 1 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Rhode Island Department of Revenue Division of Taxation

July 15, 2015 Revised July 24, 2015

Notice 2015-11

Sales and hotel taxes on

short-term residential rentals: FAQs

Legislation approved by the Rhode Island General Assembly and signed into law by Rhode Island Governor Gina M. Raimondo on June 30, 2015, expanded the sales and hotel taxes to include short-term rentals of residential property, including the rental of vacation homes and beach cottages. As an aid to homeowners, practitioners, and others, the Rhode Island Division of Taxation has drafted the following answers to frequently asked questions (FAQs). This document is for general information purposes only and is not a substitute for Rhode Island General Laws or for Division of Taxation regulations or declaratory rulings. Q: I own a vacation home in Narragansett that I rent out a week at a time every summer. Am I subject to this tax?

A: Yes. The tax provisions of the law apply if you are renting out a location in Rhode Island where living quarters or sleeping or housekeeping accommodations are provided to transient guests in exchange for payment. Such accommodations include, but are not limited to, the following:

An apartment. A beach house or cottage. A condominium. A house. A mobile home.

The provisions apply regardless of whether you, the owner of the dwelling, are a Rhode Island resident or nonresident, and regardless of whether the tenant is a Rhode Island resident or nonresident. Following are examples of those to whom the tax provisions of the law apply:

Someone who owns a beach cottage in Sand Hill Cove that is rented out for a week or two at a time every summer.

Someone whose principal residence is in the Barrington area and who rents it out to golfers or golfing fans for one or two weeks each June.

Page 2 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Someone who owns a two-family house in Providence and who, during college graduation season each year, rents out the upstairs apartment to visiting relatives of graduates for a few days or for a week or two.

Q: What does “short-term rental” mean?

A: A rental period of 30 days or less. Q: What about a long-term rental?

A: Any occupancy which is done through a documented arrangement, such as a written lease, for a rental period of more than 30 consecutive days, or for one calendar month, is excluded from the requirement to register with the Division of Taxation and collect taxes. Following are examples of those who would not be required to register and collect the taxes:

Someone who owns a beach cottage in Sand Hill Cove that is rented out to a single customer under a written lease for the entire summer.

Someone whose principal residence is in the Barrington area and who rents it out to golfers or golfing fans, under a written lease, for the entire calendar month of June.

Someone who owns a two-family house in Providence and who, during college graduation season each year, rents out the upstairs apartment to visiting relatives of graduates, under a written lease, for 31 consecutive days.

Q: If the new law does apply to me, what must I do?

A: You must:

Register with the Rhode Island Division of Taxation; Pay the annual $10 sales tax permit fee; and Collect and remit the sales tax and the hotel tax.

Q: How do I register?

A: Fill out the registration form, available on the Division of Taxation’s website. It is called the “Business Application and Registration” form and is sometimes referred to as the “BAR.” To view the latest version of the form, please use the following link: http://www.tax.ri.gov/forms/2015/Excise/Sales/TX_BAR_07202015.pdf It is a multi-page form, but you only need to fill out certain parts of it. The Division of Taxation has posted a sample BAR on its website that shows, in yellow highlight, which parts of the form you must review and/or complete. Please use the following link: http://www.tax.ri.gov/Tax%20Website/TAX/notice/Revised%20sample%20BAR%2007-23-15.pdf When filling out the first page of the BAR form, please keep the following points in mind:

On the “Do you make sales at retail?” line, check “yes”. Under the “Will you be selling” section, check the “yes” box next to “Rental of

room(s)/home(s).” If you are renting out only seasonally, be sure to fill in the “Seasonal Operation” line,

including the months during which rentals will be made. On the “Business Code #” line, enter 5538.

Page 3 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Send the Division of Taxation the completed BAR form with a check for $10 for your sales permit. Completing and submitting the BAR will set you up to collect and remit Rhode Island sales tax and hotel tax. Please note that for purposes of short-term vacation rentals, the BAR can only be filed on paper at this time. The new law took effect July 1, 2015, and the sales permit is good for a year (July 1 through June 30) before it must be renewed. Q: How much must I collect and remit in sales tax and hotel tax? And how is the tax calculated?

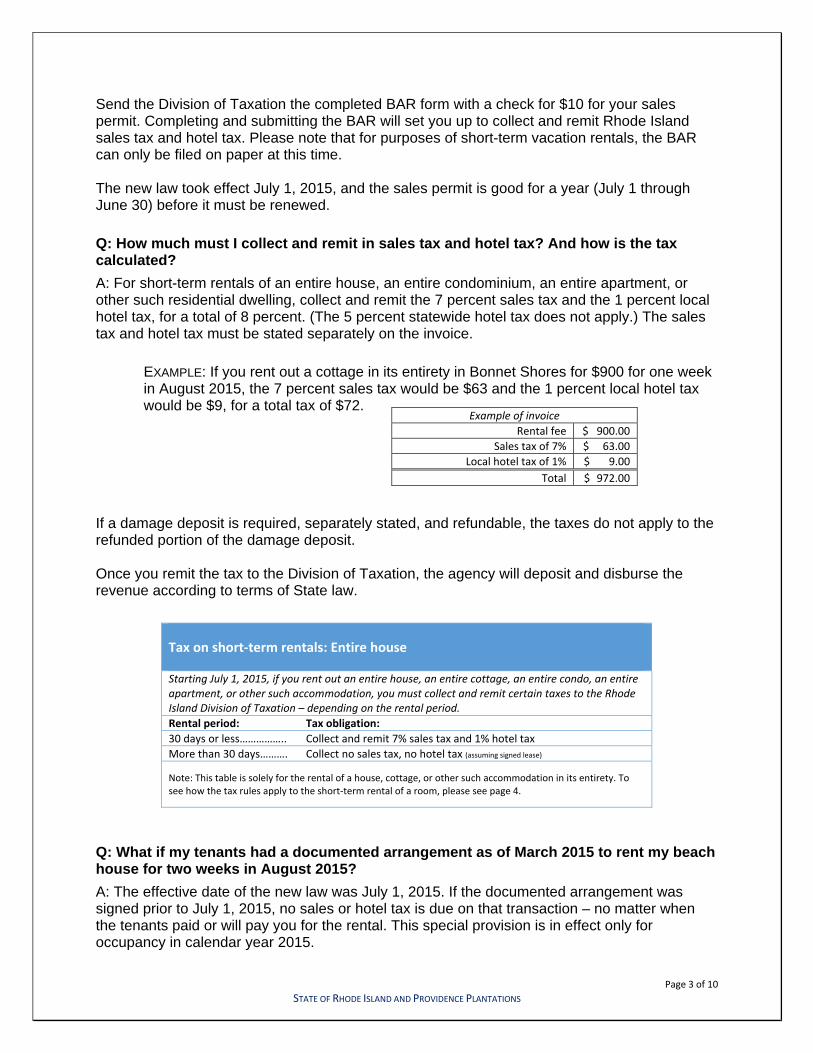

A: For short-term rentals of an entire house, an entire condominium, an entire apartment, or other such residential dwelling, collect and remit the 7 percent sales tax and the 1 percent local hotel tax, for a total of 8 percent. (The 5 percent statewide hotel tax does not apply.) The sales tax and hotel tax must be stated separately on the invoice.

EXAMPLE: If you rent out a cottage in its entirety in Bonnet Shores for $900 for one week in August 2015, the 7 percent sales tax would be $63 and the 1 percent local hotel tax would be $9, for a total tax of $72.

If a damage deposit is required, separately stated, and refundable, the taxes do not apply to the refunded portion of the damage deposit. Once you remit the tax to the Division of Taxation, the agency will deposit and disburse the revenue according to terms of State law. Q: What if my tenants had a documented arrangement as of March 2015 to rent my beach house for two weeks in August 2015?

A: The effective date of the new law was July 1, 2015. If the documented arrangement was signed prior to July 1, 2015, no sales or hotel tax is due on that transaction – no matter when the tenants paid or will pay you for the rental. This special provision is in effect only for occupancy in calendar year 2015.

Example of invoice

Rental fee $ 900.00

Sales tax of 7% $ 63.00

Local hotel tax of 1% $ 9.00

Total $ 972.00

Tax on short‐term rentals: Entire house

Starting July 1, 2015, if you rent out an entire house, an entire cottage, an entire condo, an entire apartment, or other such accommodation, you must collect and remit certain taxes to the Rhode Island Division of Taxation – depending on the rental period.

Rental period: Tax obligation:

30 days or less…………….. Collect and remit 7% sales tax and 1% hotel tax

More than 30 days………. Collect no sales tax, no hotel tax (assuming signed lease)

Note: This table is solely for the rental of a house, cottage, or other such accommodation in its entirety. To see how the tax rules apply to the short‐term rental of a room, please see page 4.

Page 4 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Q: What constitutes a documented arrangement for purposes of this special provision?

A: A written lease or other formal written contract would suffice. So, too, would other types of records, such as e-mails and sales invoices. Even checks with rental dates written on them will be acceptable for this purpose.

EXAMPLE: Maria rents out her cottage near Scarborough Beach for $1,500 a week each August. In October 2014, Tabatha signed a lease to rent the house for two weeks in August 2015 and paid Maria a 50% deposit, agreeing to pay the remaining 50% at move-in. For that transaction, no tax applies because the documented arrangement was entered into prior to the effective date of the law, and occupancy was in 2015.

Q: What if I rent out my summer cottage by the week during the summer, then rent it out to University of Rhode Island students from September through May of the school year?

A: Register with the Division of Taxation and collect and remit the 7 percent sales and 1 percent local hotel tax for the weekly rental periods in the summer. But there is no tax due for the rental during the school year (assuming that the school year rental is done through a written arrangement). Q: I have a cottage in South Kingstown that I do not rent out in the summer; I stay there all summer with my family. But I do rent it out each year to URI students under a lease that covers each September through May. Must I register and collect and remit the taxes?

A: No. Q: Are the rules that govern the short-term rental of an entire home, an entire cottage, an entire condo, or an entire apartment different than the rules for renting out a room?

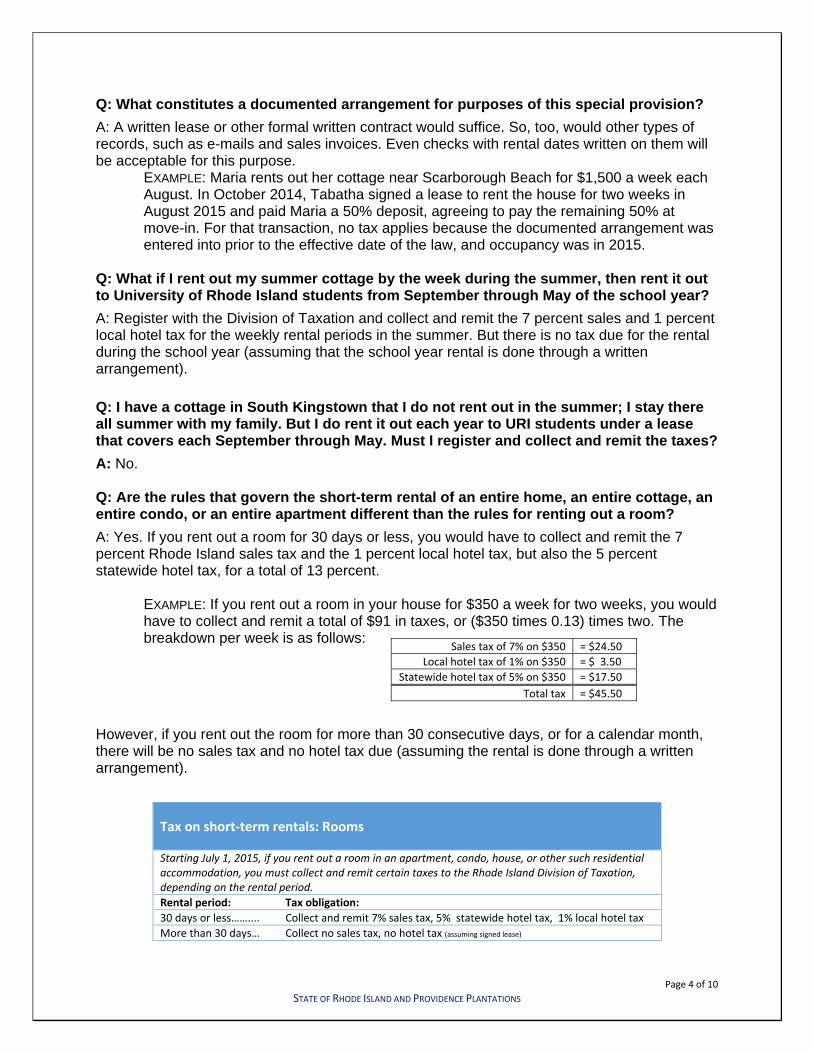

A: Yes. If you rent out a room for 30 days or less, you would have to collect and remit the 7 percent Rhode Island sales tax and the 1 percent local hotel tax, but also the 5 percent statewide hotel tax, for a total of 13 percent.

EXAMPLE: If you rent out a room in your house for $350 a week for two weeks, you would have to collect and remit a total of $91 in taxes, or ($350 times 0.13) times two. The breakdown per week is as follows:

However, if you rent out the room for more than 30 consecutive days, or for a calendar month, there will be no sales tax and no hotel tax due (assuming the rental is done through a written arrangement).

Tax on short‐term rentals: Rooms

Starting July 1, 2015, if you rent out a room in an apartment, condo, house, or other such residential accommodation, you must collect and remit certain taxes to the Rhode Island Division of Taxation, depending on the rental period.

Rental period: Tax obligation:

30 days or less…….... Collect and remit 7% sales tax, 5% statewide hotel tax, 1% local hotel tax

More than 30 days… Collect no sales tax, no hotel tax (assuming signed lease)

Sales tax of 7% on $350 = $24.50

Local hotel tax of 1% on $350 = $ 3.50

Statewide hotel tax of 5% on $350 = $17.50

Total tax = $45.50

Page 5 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Q: What if my tenants signed a lease in March 2015 to rent a room for two weeks in August 2015?

A: The effective date of the new provisions is July 1, 2015. If the lease was signed prior to July 1, 2015, no sales tax and no hotel tax is due on that transaction for occupancy in 2015 – no matter when the tenants paid or will pay you for the rental. This special provision is in effect only for occupancy in calendar year 2015.

Q: How do I remit the tax to the Division of Taxation, and how often must I do it?

A: Sales taxes and hotel taxes are “trust fund taxes.” That means, in effect, that you are serving as the conduit for the tax; the tax is being paid by the tenant and collected by you on behalf of the State of Rhode Island. The taxes are not yours to keep and are not for personal use; they must be remitted – in other words, turned over to – the State of Rhode Island. If you provide short-term residential rentals throughout the year, you must file a monthly sales tax return and a monthly hotel tax return. If you rent out only seasonally, you must file a monthly sales tax return and a monthly hotel tax return only for the months during which you rent.

EXAMPLE: Tammy rents out her beach cottage in Charlestown for a few weeks each July and a few weeks each August. For the remainder of the year, the cottage is not rented out. In this example, Tammy would file a monthly sales tax return and a monthly hotel tax return for the months of July and August. She would not file a sales tax return or a hotel tax return for any other month. She would still have to file the annual reconciliation return in January, covering the previous calendar year. EXAMPLE: Tony rents out a room in his house in East Providence for a few weeks every June. For the remainder of the year, the room is not rented out. In this example, Tony would file a monthly sales tax return and a monthly hotel tax return only for June. He would not file a sales tax return or a hotel tax return for any other month. He would still have to file the annual reconciliation return in January, covering the previous calendar year.

Sales tax payments and hotel tax payments are made in arrears: Monthly sales and use tax returns and payments, and monthly hotel tax returns and payments, are due on or before the 20th day of the following month.

EXAMPLE: Sal registers with the Division of Taxation in July 2015. He rents out his beach cottage on Aquidneck Island for a few weeks in July. In that case, Sal must file a sales and use tax return, and a separate hotel tax return, for the month of July. Each return, along with a separate check for each return, would be due on or before August 20, 2015.

For those who make short-term residential rentals – such as a vacation house, beach cottage, or a room in an apartment or a room in a house – the Division of Taxation has created a new form for remitting the hotel tax. It is Form RI-8478, "Residential Dwelling/Room Rental Tax Return" and it should be completed and mailed in along with a check for payment of the tax. The new form is available at the following link: http://www.tax.ri.gov/forms/2015/Excise/Sales/Vacation%20Rentals%2007202015.pdf

Page 6 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

For purposes of short-term residential rentals, the BAR form, sales tax returns, and the new Form RI-8478 for remitting hotel tax cannot be filed electronically at this time. They must be made on paper. Also, payments related to such filings must be by check. Q: When it comes to short-term residential rentals, is there a rule of thumb for determining who is responsible for registering with the Division of Taxation, charging and collecting the tax, and remitting the tax?

A: Yes. The person or entity collecting the money for a rental is responsible for registering, filing, and remitting the applicable taxes. Q: How would a real estate professional be affected by the new provisions?

If a real estate professional lists a rental on behalf of the property’s owners, and collects the rental amount, the real estate professional must register with the Division of Taxation, collect sales tax and hotel tax from the occupants of the rental, and remit those taxes to the Division of Taxation. The taxes apply to the gross receipts of the transaction – including any commissions or fees, such as cleaning fees and booking fees. However, if a damage deposit is required, separately stated, and refundable, the taxes do not apply to the refunded portion of the damage deposit. (The portion of the damage deposit that is not refunded is taxed.) Q: On behalf of a beach cottage owner, a real estate professional lists the cottage as a short-term residential rental. The cottage is listed for $2,000 for one week in August 2016, under a written agreement executed in August 2016. The price includes $1,600 for the rental fee and $400 for the real estate professional’s commission. The real estate professional asks the tenant to make a check for $1,600 payable to the cottage owner and to make a separate check for $400 payable to the real estate professional. Neither the cottage owner nor the real estate professional is involved in any other rental in 2016. Who must register with the Division of Taxation and collect and remit the tax?

A: Because the real estate professional is initiating the lease agreement and communicating with the tenant, the real estate professional must register with the Division of Taxation, charge and collect the sales tax and hotel tax, and remit the taxes to the Division of Taxation. In this example, the 7 percent sales tax would total $140, and the 1 percent local hotel tax would total $20, for a total of $160. Each of the taxes would have to be separately stated on the invoice. Q: What if a real estate agent initiates the lease agreement and communicates with the tenant for purposes of a short-term residential rental, but the agent works at a real estate agency?

A: In that case, the agency must register with the Division of Taxation, charge the sales and hotel tax on the short-term residential rental transaction, collect the taxes and remit them to the Division of Taxation – regardless of whether the agent is employed by the agency or treated as an independent contractor for the agency. Q: Suppose the owner of a vacation home advertises it as a short-term rental through a real estate agency. The owner is charged an up-front fee for the advertising. Once the prospective tenant finds the advertisement, he or she deals directly with the vacation home owner.

Page 7 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

A: In that case, the vacation home owner must register with the Division of Taxation, charge the sales and hotel tax on the short-term residential rental transaction, collect the taxes and remit them to the Division of Taxation. Q: If I am subject to the requirements of Rhode Island’s tax on short-term residential rentals, what filings must I make?

A: As noted earlier, your very first step is to register for a sales tax permit with the Rhode Island Division of Taxation. Use the “Business Application and Registration” form, or BAR. (It is sometimes called the “Sales and Withholding Tax Registration Form.”) It is available on the sales tax section of the Division of Taxation website through the following link: http://www.tax.ri.gov/forms/2015/Excise/Sales/TX_BAR_07202015.pdf Or call the Division of Taxation’s Forms desk, (401) 574-8970, to have a copy mailed to you. Send the completed form with a check for $10 to the Division of Taxation (using the address listed on the form). Once you complete and submit the BAR form along with a check for $10 made out to the Rhode Island Division of Taxation, and the agency processes your application and payment, you will receive a sales permit in the mail along with some forms for remitting the sales tax and the hotel tax.

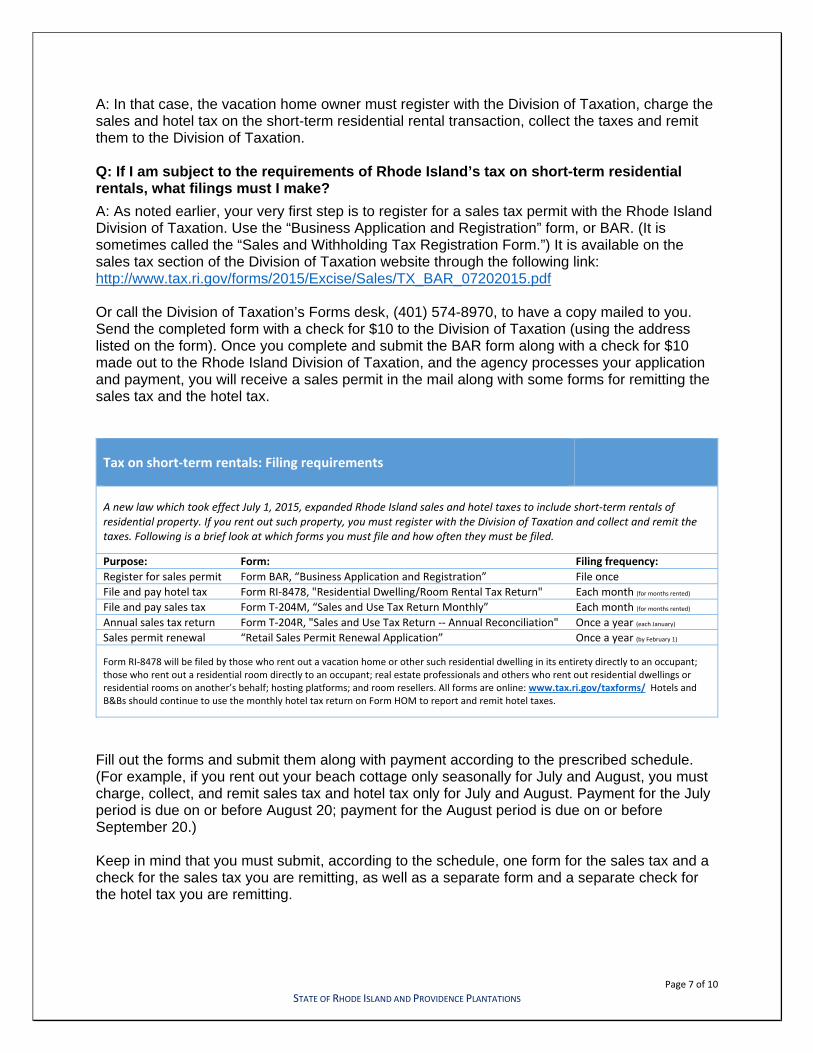

Tax on short‐term rentals: Filing requirements

A new law which took effect July 1, 2015, expanded Rhode Island sales and hotel taxes to include short‐term rentals of residential property. If you rent out such property, you must register with the Division of Taxation and collect and remit the taxes. Following is a brief look at which forms you must file and how often they must be filed.

Purpose: Form: Filing frequency:

Register for sales permit Form BAR, “Business Application and Registration” File once

File and pay hotel tax Form RI‐8478, "Residential Dwelling/Room Rental Tax Return" Each month (for months rented)

File and pay sales tax Form T‐204M, “Sales and Use Tax Return Monthly” Each month (for months rented)

Annual sales tax return Form T‐204R, "Sales and Use Tax Return ‐‐ Annual Reconciliation" Once a year (each January)

Sales permit renewal “Retail Sales Permit Renewal Application” Once a year (by February 1)

Form RI‐8478 will be filed by those who rent out a vacation home or other such residential dwelling in its entirety directly to an occupant; those who rent out a residential room directly to an occupant; real estate professionals and others who rent out residential dwellings or residential rooms on another’s behalf; hosting platforms; and room resellers. All forms are online: www.tax.ri.gov/taxforms/ Hotels and B&Bs should continue to use the monthly hotel tax return on Form HOM to report and remit hotel taxes.

Fill out the forms and submit them along with payment according to the prescribed schedule. (For example, if you rent out your beach cottage only seasonally for July and August, you must charge, collect, and remit sales tax and hotel tax only for July and August. Payment for the July period is due on or before August 20; payment for the August period is due on or before September 20.) Keep in mind that you must submit, according to the schedule, one form for the sales tax and a check for the sales tax you are remitting, as well as a separate form and a separate check for the hotel tax you are remitting.

Page 8 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

At this time, the BAR, the annual renewal form, payments, the sales tax coupons, and the new Form RI-8478 for remitting hotel tax can only be submitted on paper for purposes of short-term residential rentals. (The Division of Taxation is working on allowing an online option.) Looking ahead:

You will receive in the mail each January a renewal notice for your sales permit. You must send back the completed renewal, along with a check for $10 to cover processing of the annual permit, by early February. Sometime in June, you will receive by mail your annual sales permit along with coupons for remitting sales tax and hotel tax.

On or before January 31 of each year, submit the annual sales and use tax reconciliation form. (It is, in essence, an annual tax return focusing solely on the sales and use tax; there is no annual reconciliation return for the hotel tax.) The form is in the process of being revised. To see what annual reconciliation forms look like, see the Division’s sales and use tax forms section: http://www.tax.ri.gov/taxforms/sales_excise/sales_use.php

If you decide someday to stop renting out your vacation house or other such property, notify the Division of Taxation by submitting an account cancellation form (an earlier version is called the final return form). Use the following link: http://www.tax.ri.gov/taxforms/sales_excise/sales_use.php

Q: What other points are there to keep in mind about the new law?

Once you have a sales tax permit, remember that it must be renewed each year. The renewal application and $10 renewal fee are due on or before February 1 of each year.

If you are a seasonal filer, you need only file a sales tax return and a hotel tax return for the months in operation; you are not required to file returns for other months. (Use the new Form RI-8478 for remitting hotel tax for short-term residential rentals.)

All filers must file an annual return, known as an annual reconciliation. It is due on or before January 31 of each year, covering the prior calendar year. For someone who registers in 2015, the first annual reconciliation return will be due on or before February 1, 2016 (January 31, 2016, falls on a Sunday).

The Division of Taxation will not seek criminal penalties or prosecution for anyone who fails to comply with the provisions of this law during the first fiscal year the tax is in effect. But those who fail to comply will still be subject to normal interest and penalty charges.

Q: Do any other states charge such taxes on short-term residential rentals?

Yes, approximately 40 states. They include Maine, New Hampshire, Vermont, Florida, Maryland, Virginia, North Carolina, and South Carolina, to name a few. Depending on the state, short-term residential rentals, including vacation homes, are subject to state, county, and/or local taxes. Depending on the jurisdiction, such taxes may be called lodging taxes, hotel/room taxes, sales taxes, transient accommodation tax, or general excise taxes.

Page 9 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

Q: I sometimes go online to rent out my house, or just a room in my house, for a week at a time. Everything is handled through the website – and the website takes care of collecting the money. Must I register with the Rhode Island Division of Taxation and collect and remit sales and hotel tax, or is that the responsibility of the website?

A: The website you’re talking about is actually a business. Such a business is sometimes referred to as a “hosting platform.” The new Rhode Island law says that the hosting platform is required to register with the Division of Taxation, charge and collect the tax, and remit the tax to the Division of Taxation. In particular, the new Rhode Island law makes the following points about hosting platforms:

No city or town in Rhode Island can prohibit you from offering your room, house, or other such residential unit through a hosting platform.

No city or town in Rhode Island can prohibit a hosting platform from providing a person or entity the means to rent, pay for or otherwise reserve a residential unit.

All hosting platforms are required to collect and remit the tax. Q: I sometimes go online to rent out my house, or just a room in my house, for a week at a time. I use the website to advertise the rentals. I pay the website a fee – it may be a subscription, a fee per booking, or some variation. The tenant who eventually ends up renting the house or room from me deals directly with me and pays me directly for the rental. Must I register with the Rhode Island Division of Taxation and collect and remit sales and hotel tax, or is that the responsibility of the website?

A: You must register with the Division of Taxation, collect the tax, and remit the tax to the Division of Taxation. Q: I sometimes go online to rent out my house, or just a room in my house, for a week at a time. The website gives me a choice: 1.) Let the website handle everything, including collecting the rental fee from the tenant, or 2.) Use the website only for advertising purposes and I collect the rental fee directly from the tenant. What are the registration and tax responsibilities?

A: If the website collects the rental fee directly from the tenant, the website is responsible for registering with the Division of Taxation, charging and collecting the tax, and remitting the tax to the Division of Taxation. If you use the website only for advertising purposes and you collect the rental fee directly from the tenant, you are responsible for registering with the Division of Taxation, charging and collecting the tax, and remitting the tax to the Division of Taxation. Q: Whom shall I call for additional information about the new tax?

A: For questions about sales and use taxes or hotel taxes, or about how to complete the BAR form for purposes of short-term residential rentals, please call the Division of Taxation’s Excise Tax section at (401) 574-8955 from 8:30 a.m. to 3:30 p.m. business days. Q: The term “room reseller” is used in the new law. What is a “room reseller”, and how does it differ from a “hosting platform”?

A: A hosting platform is described above. It typically is a means by which you can rent out a room in your home – or your entire home.

Page 10 of 10

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

By contrast, a room reseller buys rooms from hotels at a discount and resells them to customers at a markup. Under the new law, a room reseller must register with the Division of Taxation and charge the occupant of the room Rhode Island’s 7 percent sales tax, 5 percent statewide hotel tax, and 1 percent local hotel tax, for a total of 13 percent, on the entire sale. The room reseller must remit the tax to the Division of Taxation. However, the room reseller may, in effect, claim a credit for the amount it was originally charged by the hotel in Rhode Island for the 7 percent sales tax, 5 percent statewide hotel tax, and 1 percent local hotel tax. (Room resellers are sometimes called room remarketers or travel websites.) This document contains an informal, plain-language summary of certain provisions of recently enacted legislation, H 5900Aaa. These FAQs are not a substitute for Rhode Island General Laws or for Rhode Island Division of Taxation regulations or rulings. Nothing contained in these FAQs in any way alters or otherwise changes any provisions of Rhode Island statutes, regulations, or formal rulings.

![Bach Concerto Pour Clavecin Bwv 1057 [ Violon 1]](https://img.pdfslide.us/doc/110x75/55cf87fb55034664618c20bd/bach-concerto-pour-clavecin-bwv-1057-violon-1.jpg)

![Bach Concerto Pour Clavecin Bwv 1057 [ Alto ]](https://img.pdfslide.us/doc/110x75/55cf87fb55034664618c20b6/bach-concerto-pour-clavecin-bwv-1057-alto-.jpg)

![Bach Concerto Pour Clavecin Bwv 1057 [ Conducteur ]](https://img.pdfslide.us/doc/110x75/55cf87fb55034664618c20dc/bach-concerto-pour-clavecin-bwv-1057-conducteur-.jpg)