Embed Size (px)

Citation preview

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Self-Employment Tax and NIIT for LLCs and Higher Income

Individuals After Tax Reform

THURSDAY, OCTOBER 18, 2018, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

THURSDAY, OCTOBER 18, 2018

Self-Employment Tax and NIIT for LLCs and Higher Income Individuals After Tax Reform

James R. Browne, Partner

Barnes & Thornburg, Dallas

Cameron L. Hess, Partner

Wagner Kirkman Blaine Klomparens & Youmans, Mather, Calif.

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Self-Employment Tax and NIIT for LLCs and Higher Income Individuals: Navigating the Complex Interplay

Cameron HessWAGNER KIRKMAN BLAINE

KLOMPARENS & YOUMANS LLP

Mather, CA

916.920-5286 x810

James R. Browne

Barnes & Thornburg LLP

Dallas, TX

214.258.4133

December 8, 2015

Agenda

• Introduction

• LLC Members & Self-Employment Tax

• LLC Members & the 3.8% Net Investment Income Tax

• Some Thoughts on Trusts

• Problems & Planning Opportunities

• Proposals and Changes on the Horizon

6

Introduction

7

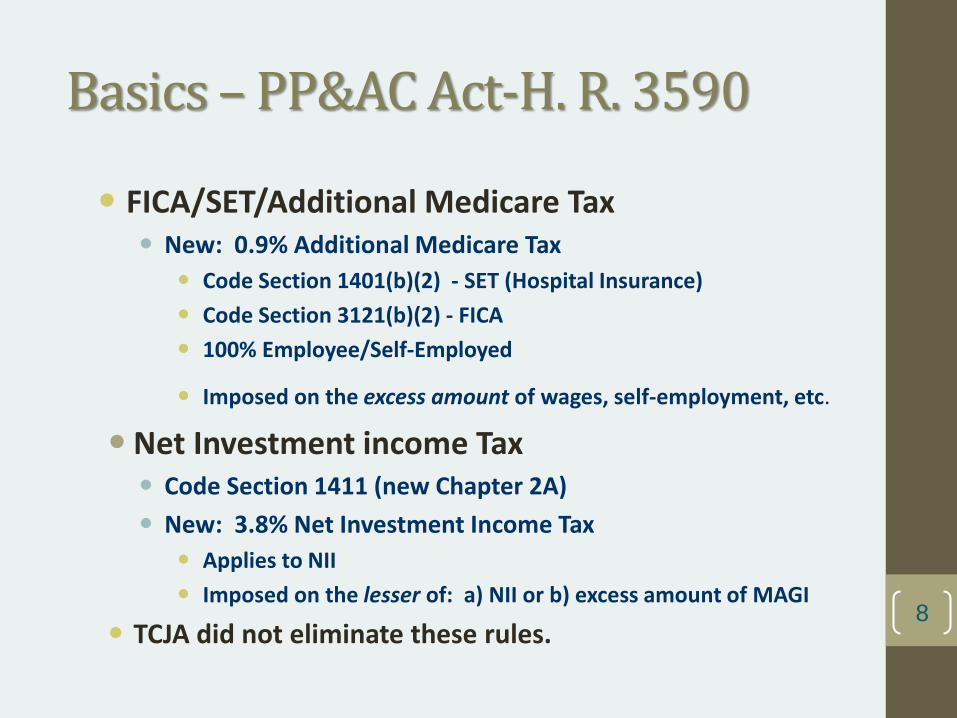

Basics – PP&AC Act-H. R. 3590

FICA/SET/Additional Medicare Tax New: 0.9% Additional Medicare Tax

Code Section 1401(b)(2) - SET (Hospital Insurance)

Code Section 3121(b)(2) - FICA

100% Employee/Self-Employed

Imposed on the excess amount of wages, self-employment, etc.

Net Investment income Tax Code Section 1411 (new Chapter 2A)

New: 3.8% Net Investment Income Tax

Applies to NII

Imposed on the lesser of: a) NII or b) excess amount of MAGI

TCJA did not eliminate these rules.8

Basics – Why do we care?

Planning: higher income individuals (2018-year TCJA Rates).

→ Tax Savings: 20% vs 23.8% Tax Rate; 37%* vs 40.8% Tax Rate

→ Each $250K not s/t 3.8% tax saves $9,750.

*29.8% vs. 33.6- if QBI Deduction Permitted (Section 162 Activity)

One-time events → “high income” for regular folks.

Personal residence or rental sale (e.g., bought 30 years ago)

Big bonus (e.g. for retirement; relocation, incentive)

Nonqualified deferred compensation (“Rabbi Trust”)

Early disposition of stock from ISO

Involuntary conversions (if taxable)

LLC member distributive shares have special planning options9

Basics: 0.9% Additional Medicare Tax

0.9% Additional Medicare Tax – Individuals 0.9% Tax on excess (countable income) > Threshold:

Countable: Total (H+W) - wages, self-employment income.

Threshold - not indexed for inflation

Pay - withhold or estimates (to avoid underpayment penalty)

Why Plan: Avoid 3.8% in Taxes 0.9% Add’l Medicare Tax + 2.9% Medicare Tax*

*SET/FICA – HI portion continues uncapped over $118,500 .

10

Basics: 0.9% Additional Medicare Tax

11

Basics: 3.8% NIIT

3.8% Net Investment Income Tax Individuals, estates and trusts (not entities)

includes Sch K-1 reported income

Tax 3.8% x the lesser of:

(1) Total NII (net investment income), or

(2) Excess MAGI*

*Excess MAGI = MAGI minus Threshold Amount.- (Except US persons overseas, MAGI = AGI – Line 31 Form 1040.)

NII - may deduct related expenses (including alloc. state income taxes) 12

Threshold Amount - Individuals

13

Status

Threshold

Amount

Married, filing jointly $250,000

Married, filing separately $125,000

Single $200,000

Head of household $200,000

Qualifying widow(er) with child $250,000

Threshold Am’t – Estates/Trusts

2018: $12,500 = Threshold

Compare:

12,500 vs 125K/200K/250K

Beneficiary DNI distributions also create deduction for NII to trust/estate

(NII distribution reported to beneficiary) 14

Example 1 – Individual

Big John (unmarried, in US) has $300,000 NII (rental income)

$190,000 AGI (had a business loss)

3.8% NIIT Computation:

NII Tax = $0.

3.8% x lesser of (1) $300K NII or (2) $0.0* *(190K AGI – 200K Threshold)

15

Example 1a – Planning - Irrev. Trust

Big John Irrevocable Trust has

$300K NII; $190K AGI (business loss)

No beneficiary distribution (no DNI Distribution)

3.8% NIIT Computation:

NII Tax = $6,745.00.

3.8% x lesser of (1) $300K NII or (2) $177,500* *(190,000 MAGI – 12,500 Threshold)

But!: If $177,500 DNI distributed, then NII Tax = $0 NII Tax = $0.0 (3.8% x $0 (190K - $177.5K - $12.5K MAGI)) 16

Basics: 3.8% NIIT

• Taxed “Persons”• Individuals

• Trusts (standard trusts)

• Estates

• Exempt “Persons”:• Foreign Persons

• C Corporations

• Foreign Trusts,

• Tax Exempt Trusts (Pensions, CRATs, CRUTS)

• Charitable Trusts

• Partnerships/S corporations

• No SET overlap: • NII excludes income subject to SE tax 17

Basics: 3.8% NIIT

NII = “Gross Investment Income (GII)” less:

“Allowable Deductions”

GII Categories:

1. Portfolio Income § 163 – SAME RULES

2. PAL/PIG § 469 – SOME CHANGES

3. Finance/Commodity traders-SAME RULES

NOT “day traders”.

Reduces value of security/commodity traders tax benefits

4. Net Gain (Dispositions) – LOTS OF

CHANGES 18

TCJA 2018/CPA Rules

• Tax Cuts and Jobs Act does not change the rules.

• Congress could not repeal – too much revenue loss.

• Interesting Interplay – 20% QBI Deduction forsome activities still subject to the 3.8% NIIT.

• 2018-Year Centralized Partnership Audit Regulations

• Do not impact 3.8% NIIT/.9% Medicare Tax

• Still collected at individual level. 19

LLC Members & Self-Employment Tax

20

SET on LLC Members

• Issue:

• Can an LLC member treat any portion of the member’s distributive share of LLC income as exempt from SET under the exception for limited partner distributive share income?

The issue is relevant only for LLC members who materially or substantially participate in the LLC business or can otherwise avoid NIIT on the distributive share income

21

SET on LLC Members

• Historical Context

• All income from a partnership is included in net earnings from self-employment

• Prior to 1977, promoters were marketing passive limited partner investments to persons otherwise ineligible for social security benefits; the partnerships promised to generate a predictable stream of self-employment income eligible for social security

• In 1977, Congress amended the Code to curtail this practice of “buying” social security benefits, by providing that income received as a limited partner is not self-employment income

• After 1977, as taxes on self-employment income increased and social security benefits declined, the limited partner rule lost its anti-abuse purpose and became a benefit to taxpayers

22

SET on LLC Members

• The statutory construct - 1402(a)(13)• In computing net earnings from self-employment:

• Include the “distributive share (whether or not distributed) of income or loss described in section 702(a)(8) from any trade or business carried on by a partnership of which he is a member”

• Exclude (in addition to normal exclusions for rents, dividends, gains, etc.):• “the distributive share of any item of income or loss of a limited partner,

as such,

• other than guaranteed payments described in section 707(c) to that partner for services actually rendered to or on behalf of the partnership to the extent that those payments are established to be in the nature of remuneration for those services”

• Note that the statute expressly contemplates that a limited partner may provide services to the partnership and still have distributive share income excluded from SET 23

SET on LLC Members

• The 1997 proposed regulations

• Context (20 years later):

• Eroding restrictions on limited partner management activities

• Growing use of alternative forms of tax partnerships with full or partial limited liability for managing members (LLCs, LLPs, and LLLPs)

• Increasing SET rate relative to benefits

• General rule: a “limited partner” is any individual unless the individual:

• has personal liability as a partner for the partnership’s debts, or

• has authority (under the law of the jurisdiction in which the partnership is formed) to contract for the partnership, or

• participates in the partnership's business for more than 500 hours during the partnership’s taxable year, or

• is a service partner in a service partnership24

SET on LLC Members

• The 1997 proposed regulations (con’t)• Class of Interest Exceptions

• An individual holding more than one class of interest is a limited partner with respect to a class of interest in which (a) limited partners (as defined above) own a substantial (≥20%), continuing interest and (b) the individual’s rights are identical to such limited partners’ rights

• An individual holding only one class of interest who is not a limited partner solely because he participates in the business for >500 hours is a limited partner with respect to the interest if (a) and (b) above are true with respect to the class of interest

• These exceptions are intended to “exclude from an individual's net earnings from self-employment amounts that are demonstrably returns on capital invested in the partnership”

• Exceptions do not apply to a service partner in a service partnership(i.e., health, law, engineering, architecture, accounting, actuarial science, consulting)

25

SET on LLC Members

• Congress responds

• The 1997 proposed regulations sparked a firestorm of criticism

• Critics claimed that earnings from self-employment must be limited to the fair value of the services actually rendered to the business, and should not sweep in all income derived from the business based on arbitrary factors such as the number or hours worked or the nature of the business

• Congress promptly passed legislation prohibiting finalization of regulations with respect to the definition of limited partner under 1402(a)(13) until July 1, 1998

• The Senate bill expressed the Senate’s view that the proposed regulations should be withdrawn and that “Congress should determine the tax law governing self-employment income”

26

SET on LLC Members

• Case law and rulings

• Renkemeyer, Campbell & Weaver, LLP v. Comm’r, 136 T.C. 137 (2011)

• Irrelevant: Law firm was a general partnership electing LLP status

• Abusive facts: transitory corporate holding company; no partnership agreement; failure to allocate income and distributions according to alleged sharing ratios; low or no compensation for services

• Erroneous and Extraneous Comments:

• Congress “intended” to exclude “earnings that are basically of an investment nature”

• The legislative history “does not support a holding thatCongress contemplated excluding partners who performed services for a partnership in their capacity as partners”

• Because the taxpayers’ distributive share income arose exclusively from legal services performed on behalf of the partnership, and was not “of an investment nature,” the income was subject to SET 27

SET on LLC Members

• Case law and rulings (con’t)

• Riether v. United States, 919 F. Supp. 2d 1140 (D. NM 2012)

• LLC operates a medical diagnostic imaging business; members receive wages and distributive share income from the LLC; no SET on distributive share (<$10,000 tax effect)

• Taxpayers: we can’t be self-employed because we received wages

• No evidence that members lacked management authority, or that wages were reasonable compensation for services

• Held: distributive share income is subject to SET because taxpayers were effectively general partners

• “Plaintiffs are not members of a limited partnership, nor do they resemble limited partners, which are those who ‘lack management powers but enjoy immunity from liability for debts of the partnership.’ [Renkemeyer] Thus, whether Plaintiffs were active or passive in the production of the LLC's earnings, those earnings were self-employment income.” 28

SET on LLC Members

• Case law and rulings (con’t)

• Howell v. Comm’r, T.C. Memo 2012-303

• Medical technology company (LLC) formed by W and B; H (W’s spouse) managed the business with B; LLC paid guaranteed payments to H, B, W and others, leaving only small amounts of distributive share income for W and B; no SET paid on guaranteed payments

• H&W “appear to contend” that W was a limited partner not active in the business and her guaranteed payments were either limited partner distributive share income or not payments for services

• Held:

• Taxpayers are bound by their tax reporting (guaranteed payment)

• W performed some services for the LLC, but failed to prove what portion of the guaranteed payments were for services

• Notably, no SET imposed on distributive share income29

SET on LLC Members

• Case law and rulings (con’t)

• CCA 201436049 (May 20, 2014)

• Investment fund management company organized as an LLC; members were paid a salary, a guaranteed payment for parking and health benefits, and a distributive share; no SET on distributive share

• Members contributed varying amounts of capital to the LLC

• Held: entire distributive share income is subject to SET because the income “is not income which is basically of an investment nature of the sort that Congress sought to exclude from [SET] when it enacted the predecessor to § 1402(a)(13). Accordingly, [the members] are not limited partners within the meaning of § 1402(a)(13).”

• No analysis whether the salary and guaranteed payments represented reasonable compensation for services

• No analysis whether the distributive share income was attributable to invested capital, employee labor, or other non-service factors •30

SET on LLC Members

• Case law and rulings (con’t)

• Sands v. Comm’r, T.C. No. 5650-15 (Petition filed May 18, 2015)

• T owned a limited partnership interest in an investment fund (LP) having 29+ other partners and conducting operations through a subsidiary LLC. T provided services to LLC for which T received $6.5MM in wages. T also allocated $18.5MM of income from LP.

• IRS asserts a deficiency that T concludes must be SET on the distributive share income. T denies liability based on the limited partner exception:

• “Because the Petitioner received significant compensation for his services to [LLC] the additional income passed through to the Petitioner from [LP] satisfies the exclusion permitted under Section 1402(a)(13).”

• IRS answer denies all substantive allegations based on lack of information, and then IRS withdraws the deficiency notice

•31

SET on LLC Members

• Case law and rulings (con’t)

• CCA 201640014 (June 15, 2016)

• T/P = franchisee of restaurants operated through an LLC (partnership) owned by T/P, his wife, and a family trust; T/P was the sole LLC manager

• T/P paid SET on guaranteed payments, but excluded distributive share income under the 1402(a)(13) limited partner exception

• Relying on Renkemeyer and Reither, the IRS concluded that because T/P provided substantial services to the LLC and was not a “mere investor,” T/P’s distributive share income is not exempt from SET, regardless of whether the income is attributable to employee labor or invested capital

• The IRS’s “mere investor” test directly conflicts with the statute

32

SET on LLC Members

• Case law and rulings (con’t)

• Hardy v. Comm’r, T.C. Memo 2017-16 (Jan. 17, 2017)

• Doctor performed surgeries at a surgery center owned and operated by an LLC (MBJ) in which he owned a LLC member interest.

• Held:

• Doctor did not materially participate in MBJ solely by virtue of using the facility, did not otherwise participate in management of MBJ, and did not group MBJ with his medical practice (and could not be forced by the IRS to do so, per TAM 201634022). Therefore, MBJ was a passive activity the income from which could be offset by passive activity losses.

• Doctor’s distributive share income from MBJ is exempt from SET “because he received the income in his capacity as an investor.” He is not involved in the operations of MBJ as a business. Patients separately pay his fees as a surgeon.

33

SET on LLC Members

• Case law and rulings (con’t)

• Castgliola v. Comm’r, T.C. Memo 2017-62 (Apr. 12, 2017)

• Member-managers of a professional LLC (lawyers) were paid reasonable salaries (reported as guaranteed payments) and paid SET on the salaries

• Residual income was reported as exempt from SET

• The PLLC members were formerly general partners in a general partnership, and no evidence that management rights changed upon conversion to a PLLC; the management rights were not equivalent to limited partner rights in a limited partnership

• Held:

• The members’ distributive share income from PLLC is not exempt from SET

34

SET on LLC Members

• Case law and rulings (con’t)

• LBI Compliance Campaign Announcement (March 18, 2018)

• “Some individual partners, including service partners in service partnerships organized as state-law limited liability partnerships, limited partnerships, and limited liability companies, have inappropriately claimed to qualify as “limited partners” not subject to SECA tax.”

• IRS Priority Guidance Plan

• Guidance on the application of §1402(a)(13) to limited liability companies.

35

SET on LLC Members

• Where are we now?

• Reporting position: an LLC member’s distributive share income from a manager-managed LLC is exempt from SET if the member is paid reasonable compensation for services as a manager

• This position is easily reconciled with the statute and legislative history, including the arguments that led to the 1997 Congressional moratorium

• It is consistent with the treatment of S corporations

• It consistent with case law (based on applicable facts and IRS litigating position in Howell and Sands)

• IRS “mere investor” test is plainly contrary to the statute, IRS proposed regulations, and Congressional intent (as expressed in 1997)

• Service partners in service partnerships have more risk 36

LLC Members & 3.8% NIIT

38

LLCs – Passive Activities

NII Includes:

469 PALs/PIGs Some rules changed

Presumed passive:

limited partner

rental real estate

NIIT Rules – to overcome Somewhat Harder to meet than Section 469.

39

LLCs & Real Estate Professionals

Rental Real Estate

To avoid 3.8% NIIT must both:

Be a real estate professional (> 750 hours) Meet one of the 500 hour tests or convince the

Service.

Other material participation tests are rejected (may use for 469 but not NIIT)

40

LLCs & Real Estate Professionals

Rental real estate continued

Most “related activity” safe harbors were rejected.

Rejected:

“Start-up Activities

Pre-Development Activities

Example: Developer leases back to farmer land held for development. While not passive under Section 469, rental income will be deemed NII.

41

LLCs & Real Estate Professional

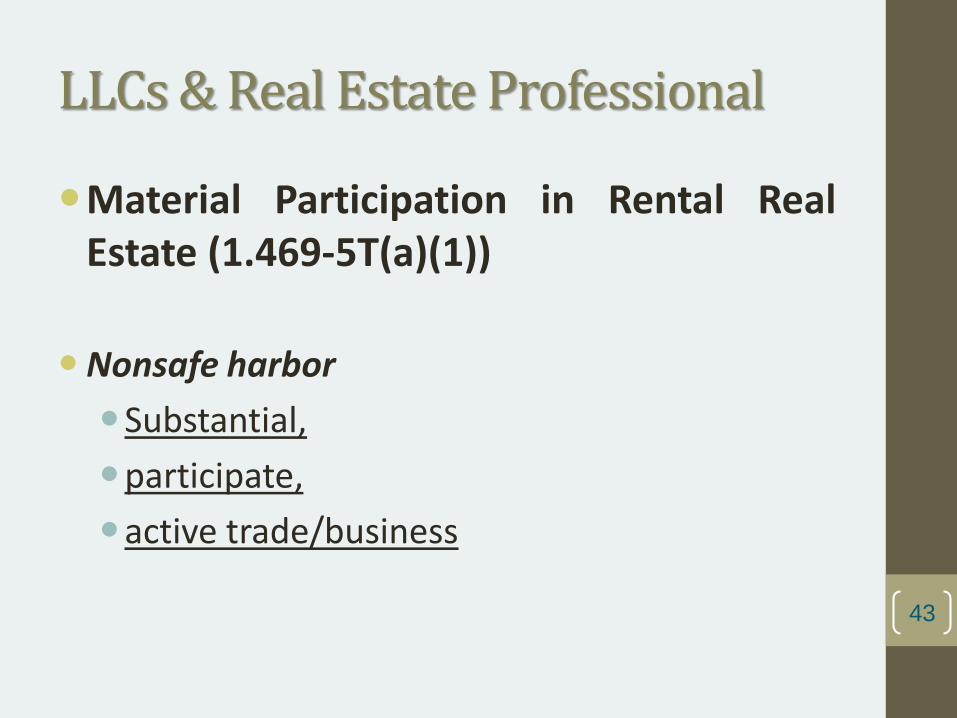

Material Participation in Rental Real Estate(1.469-5T(a)(1))

A. Real estate professional (>750 hrs) +

B. Either

1. participate = > than 500 hours per year,

2. > than 500 hours/year in 5 of 10 prior years

→Active T/B , and thus not subject to §1411.

*Activity Must be Part of That Active Trade or Business42

LLCs & Real Estate Professional

Material Participation in Rental RealEstate (1.469-5T(a)(1))

Nonsafe harbor

Substantial,

participate,

active trade/business

43

LLCs & Limited Partner

3.8% NIIT Regulations: The same Limited Partner rules under Section 469 apply.

Odd Issue – TCJA 20% QBI Deduction:

Can Qualified Business Income Deduction Apply, but 3.8% NIIT is still imposed? Answer: YES!

Situation: Rental activity involves substantial, regular and continuous activity

Will qualify for 20% QBI Deduction (s/t 50% Wage or 2.5% basis/25% Wage Limit)

But, NIIT may still apply if considered a “passive activity” 44

LLCs & Limited Partner

Problem: No statute defines “limited partner”

If Limited Partner, only have 3 tests to prove active.

Affected: LLCs, LPs, LLPs, LLLPs, other entities treated as “partnership”.

45

LLCs & Limited Partner

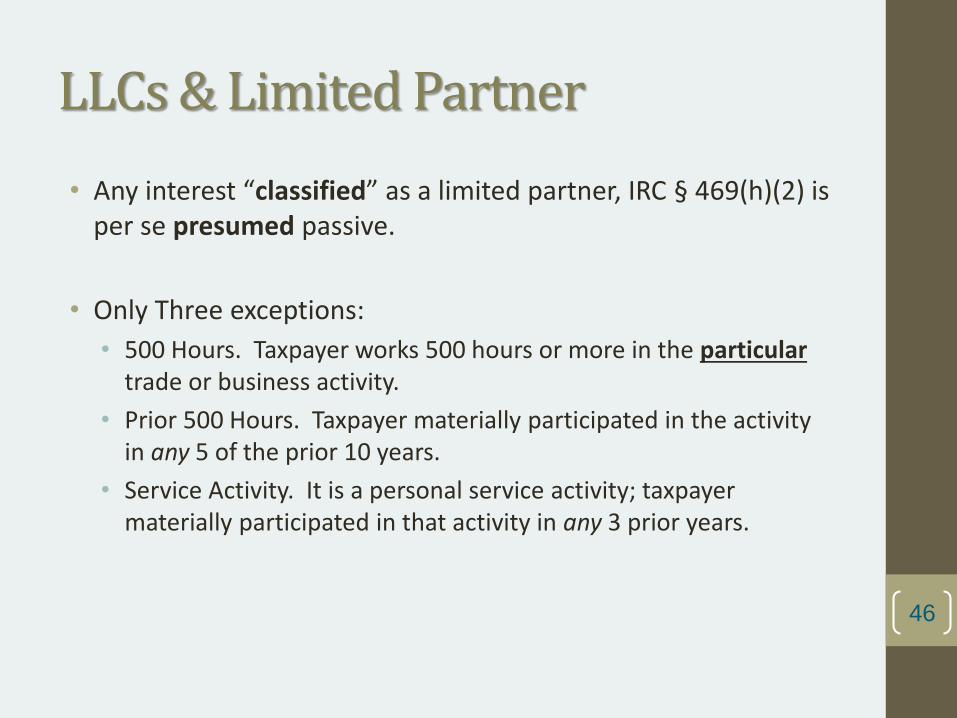

• Any interest “classified” as a limited partner, IRC § 469(h)(2) is per se presumed passive.

• Only Three exceptions:

• 500 Hours. Taxpayer works 500 hours or more in the particulartrade or business activity.

• Prior 500 Hours. Taxpayer materially participated in the activity in any 5 of the prior 10 years.

• Service Activity. It is a personal service activity; taxpayer materially participated in that activity in any 3 prior years.

46

LLCs & Limited Partner

Temp Treas. Reg. 1.469-5T(e)(3)(i)

...interest [is] a limited partnership interest if—

(A) …. designated a limited partnership interest, ….; or

(B) The liability of the holder … is limited, …..

… interest … shall not be treated as a limited partnership interest …. if the individual is a general partner.

47

LLCs & Limited Partner

Good News!: Courts reject LP treatment for LLCs:

Gregg v. U.S., 186 F.Supp.2d 1123 (D. Or. 2000). LLC.

Garnett v. Com’r, 132 T.C. 368 (2009). LLPs and LLCs were not limited partnerships.

Thompson v. U.S., 87 Fed. Cl. 728 (2009). 469(h)(2) requires a partnership. An LLC member is not a limited partner.

Newell v. Com’r, T.C. Memo. 2010-23. 469(h)(2) did not apply to the managing member of an LLC. Member is a general partner under §1.469-5T(e)(3)(ii).

Lamas v. Com’r, T.C. Memo 2015-59. Several LLCs & S Corp. Rejects no material participation. Aggregates S Corps & LLC activities – total hours adequate. 48

LLCs & Limited Partner

IRS Strikes Back: Prop. Treas. Reg. §1.469-5(e)(3)(i) (11/28/11)

...interest [is] a limited partnership interest if—

(A) The entity…is classified as a partnership for Federal income tax purposes under §301.7701-3; and

(B) The holder of such interest does not have rights to manage the entity…..

49

Some Thoughts on Trusts

50

Trusts & 3.8% NIIT

•High income persons do trust planning

• Income shifting

• Asset shifting

•Using both Trusts + LLC is common

• Careful planning on trust distributions is needed.

• Highest Trust tax bracket @ $12,500

• NIIT triggered if Trust AGI > $12,50051

Trust Issue for LLCs & 3.8% NIIT

Scenario: Trust owns % in LLC.

Is Trustee status = limited partner?

Can Trustee materially participate?

IRS Declined to Issue Regulations

52

Trustee Material Participation

▪ IRS: Trustees rarely materially participate – must be directly on

title, and principal person acting1

1Position discussed by IRS in TAM 200733023; PLR 201029014; TAM 201317010.

COURTS REJECT: Carter Trust v. US 256 F. Supp. 2d 536 (N.D. Tex. 2003).

Trustee hired ranch manager. Material participation found through employees and trustee.

Aragona Trust v. Com’r, 142 TC. 9 (3/27/14).

3 of 6 trustees (related) worked FT for R/E management LLC, wholly owned by trust. Trust can materially participate through trustee-employees; R/E professional exception applied.

53

Problems and Planning Opportunities

54

Planning Trap #1

Using an S corporation to avoid SET/NIIT

The properly determined distributive share income of an S corporation engaged in an active non-trading business is unquestionably exempt from both SET and NIIT

In addition, compensation paid to an S corporation shareholder qualifies as W-2 Wages under Section 199A (20% deduction for qualified business income); not so for partner guaranteed payments

BUT

S corporations have significant disadvantages. (e.g., one class of stock, no entity or foreign shareholders, no 754 election, no 721/731 exclusion for gain on property contributions and distributions, no inside basis step-up at death, etc.)

The perceived SET/NIIT benefits may be overstated

A properly structured LLC/LP should achieve similar SET and 199A benefits without the disadvantages of S corporation status

55

Planning Trap #2

• S corporation election for an LLC or LP

• Tax preparers or other tax advisors often elect S corporation status for an LLC or LP solely to obtain SET and NIIT advantages. This is usually bad advice!

• Same considerations as any S corporation (see prior slide)

• Plus additional potential problems if the company agreement is not modified to conform to S corporation requirements; the entity might be classified as a C corporation!

56

Planning Trap #3

• S corporation blocker

• Individuals are employees of LLC or S corp and are paid wages

• Distributive share income flows through S corporations

• NB: Cumbersome and does not eliminate all disadvantages of S corporation ownership 57

Individual A Individual B Individual C

S Corp 1 S Corp 2 S Corp 3

S Corp. S Corp. S Corp.

LLC

Partnership

Planning Opportunities

A properly structured LLC/LP

Individuals perform services for LLC as employees of Manager

Distributive share income received by individuals as an LLC member having no management rights

Manager wage payments should count under Section 199A 59

Individual A Individual B Individual C

Manager

S Corp. (or LLC)

Manager-Managed LLC

Partnership

ManagementFees

Planning Opportunities

• Spousal split ownership of LLC/LP

• T’s activities are imputed to S for passive activity purposes, but are not imputed to S for purposes of SET limited partner proposed regulations

• S’s distributive share income should avoid SET/NIIT60

Taxpayer Spouse

OpCo, LLC

Partnership

Active non-trading, non-

service business

ManagingMember

1%

Member99%

GuaranteedPayment for

Services

Planning Opportunities

• One class of interest exception

• T’s distributive share income is exempt from SET under one class of interest exception, and is exempt from NIIT based on material participation

61

Taxpayer Others

OpCo, LLC

Partnership

Active non-trading, non-

service business

ManagingMember

≤ 80%

Member

≥ 20%GuaranteedPayment for

Services

Planning Opportunities

• Grouping election• Under prior law, it was often advantageous to not group activities

(to accelerate use of suspended losses on activities sold or terminated)

• Under current law, it might be beneficial to group activities so that otherwise passive activities that do not generate self-employment income (but which do generate NII) can become part of a combined Active Non-Trading Business that generates neither NII nor self-employment income

• Appropriate economic unit for grouping: important factors• Similarities or differences in the types of businesses;• Extent of common control;• Extent of common ownership;• Geographical location; and• Interdependence of the activities

• Various limitations apply62

Planning Opportunities

• Self Charged Interest (Loan to related LLC or LLP)

• On self-charged interest from an active (non-passive) business entity, a portion of interest income will be excluded.

• The exclusion amount = the lender’s “share of the nonpassive deduction”. The rule cross-references §1.469–7 for the operative mechanics.

• The limit is inapplicable if the interest deduction is part of a self-employment income computation (subject to tax under section 1401(b)).

63

Planning Opportunities

Self Charged Interest.

Example. Able Designer loans $100,000 @ 10% to an architecture firm in which he owns 15% of the architecture firm located in the same building. Will 100% of the $$ interest paid by the firm be treated as self-charged rent?

No. There is only excluded the income = to the % interest deduction born. Only $1,500 of the $10,000 received will be excluded. $8,500 of the interest will remain NII

64

Planning Opportunities

• “Self-Charged” Rent (Rent property to business)

• Rental income treated as non-passive under §1.469–2(f)(6) (rental income from property used in an activity in which the taxpayer materially participates), including rental property grouped with a non-passive activity, will be deed T/B income.

• Gain/loss from rental property, if sold with active T/B property will also be treated as nonpassive T/B gain

65

Planning Opportunities

• Property s/t “Self-Charged” Rent

• Example. Able Designer owns 100% of a building and 15% of the architecture firm located in the same building. Will 100% of the $$ rent paid by the firm be treated as self-charged rent?

• Yes, under 1.469-2(f)(6), amount of rent paid by the firm will be treated as non-passive. The self-rental regulations do not require “mirror” ownership.

66

Planning Opportunities

• Avoiding 3.8% NIIT through material participation

• Participation by Hours > 500

• Time spent (Self/Spouse)

• Proof of Participation. Appointment book calendar, or narrative summary. To show the services performed & hours.

• Facts & Circumstances Test (difficult)

• Activity regular, continuous, and substantial

• Works at least 100 hours in the activity,

• No one else works more hours

• No one else receives compensation for managing the activity

• AND SERVICE CONVINCED ACTIVE TRADE OR BUSINESS.

67

Planning Opportunities

Counting +500 hours

Per IRS - exclude

Admin Time: Review financials, monitor,

Work normally be assigned to an employee

Travel Time Thomas E. Truskowsky, T.C. Summary Op 2003-130

Per IRS: Few taxpayers can meet the facts and circumstances standard. If there is paid on-site management, the facts and circumstances test cannot be used.

Courts.

Non-trust Decisions. Most are more taxpayer abuse cases.

Some decisions indicate courts will concur that the IRS is over-reaching on its position.

Major problem is burden of proof. 68

Planning Opportunities

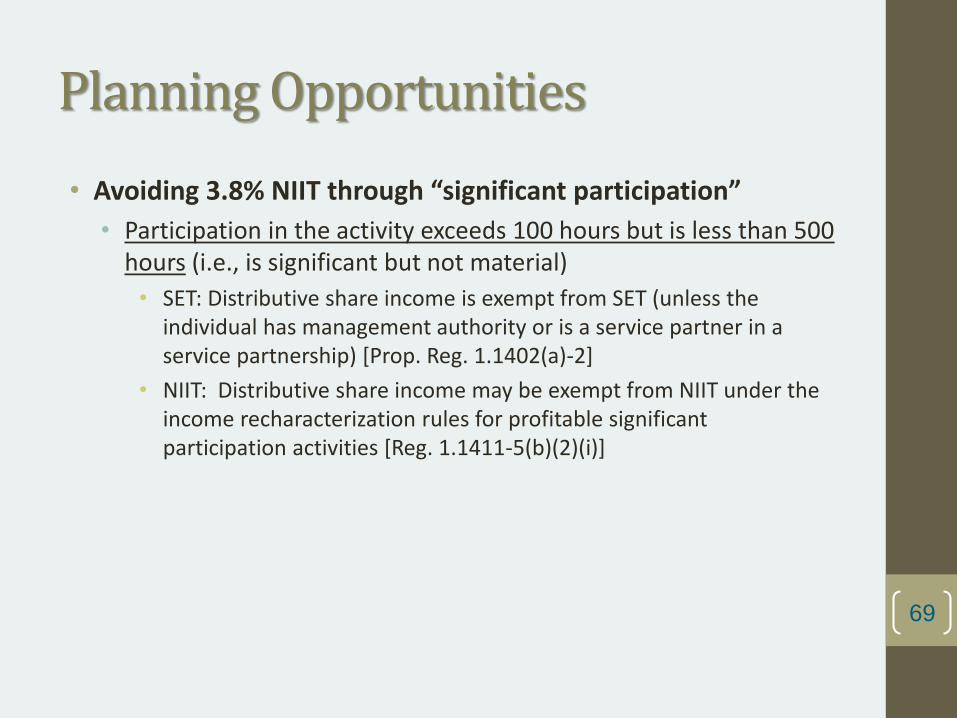

• Avoiding 3.8% NIIT through “significant participation”

• Participation in the activity exceeds 100 hours but is less than 500 hours (i.e., is significant but not material)

• SET: Distributive share income is exempt from SET (unless the individual has management authority or is a service partner in a service partnership) [Prop. Reg. 1.1402(a)-2]

• NIIT: Distributive share income may be exempt from NIIT under the income recharacterization rules for profitable significant participation activities [Reg. 1.1411-5(b)(2)(i)]

69

Planning Opportunities

• Net Gain from Dispositions

• Opportunities to reduce losses by:

• Strategies to reduce NII by Sec.165 losses: abandonment and worthlessness.

• Culling of losses.

• Basic exceptions/limitations/exclusions apply

• Loss limitations (at risk, basis, but capital loss C/F rules are narrower)

• Installment sale rules

• Statutory Exclusions apply – 1031/1033/1038/121(home)

• Look Through Rule:……

70

Planning: Look-Through Rule

• Owner’s “Disposition” of Interest in Pship or S Corp

• 1411(c)(4) & (Prop. Treas. Reg. 1.1411-7).

• Recasts NII gain/loss as business gain/loss.

In the case of a disposition of an interest in a partnership or an S corporation –

(A) gain from such a disposition shall be taken into account…only to the extent of the net gain…if all property of the partnership or S corporation were sold at fair market value immediately before the disposition of such interest, and

(B) a rule similar to the rule of subparagraph (A) shall apply to a loss from such disposition.

71

Planning: Look-Through Rule

• Why. Owner’s pass-through business won’t be treated as an investment. If sell interest – deemed like asset sale.

• How: “look-through”: Had entity its assets (“deemed sale”) at FMV, what portion would be business income? (Prop. Treas. Reg. Section 1.1411-7).

• Trade/business portion is excluded from NII “net gain from disposition”.

• Complicated Computation - difficult to qualify.

• NOTE!: Does not apply to owner of C Corp!

72

Planning: Look Through Rule

• Summary

• T’s gain from sale of interest is bifurcated:

• if part of gain from sale relates to trade/business portion sold, total gain included in NII is reduced (negative adjustment)

• T’s loss bifurcated: if part of loss from sale relates to trade/business sold, total loss is reduced – offset against other disposition gains is less (positive adjustment)

• →“Excess” = deemed investment gain/loss

• Note: Adjustment doesn’t increase total gain or total loss from sale of interest.

73

Planning: Look-Through Steps

• 1. Compute total gain/loss from disposition of interest.

• 2. Compute entity level total gain/loss from deemed FMV sale;

• 3. Compute gain/loss deemed for each separate entity asset (including goodwill);

• 4. Multiply % interest sold x each gain/loss (the look through);

• 5. Sort gain/loss between:

• (i) net investment income and

• (ii) excluded income (e.g., trade or business income.)

74

Planning To Minimize Risks

• SET/469 Cases often have bad LLC documents and records.

• Good Documents.

• Have a “clean” LLC Formation. Articles, Operating Agreement.

• Follow well drafted allocation/distribution provisions

• Guaranteed Payments for “Services” (non-rental LLCs)

• Consider two-class memberships or requiring managers.

• Good Records

• Track hours/activities for “active” trade or business

• Keep good accounting records

• Good Tax Advice

• Identify SET/NIIT issues, advise on risks and set strategies

• Encourage the IRS to challenge someone else. 75

Other LLC/High Income Strategies

▪ Installment Sales

▪ Section 1031 Exchanges

▪ Charitable Donation of Appreciated Property

▪ Distributing investment assets

▪ Successor Trusts (active Trustee) – see above

▪ Spreading Investment Income (Family Limited Partnerships & LLCs)

▪ Suitable Investments

▪ Managing Estate or Trust Distributions

▪ Creating Material Participation in Passive Activities76

Other LLC/High Income Strategies▪ Family Limited Partnerships▪ Purpose: shift income to other family members

▪ How:

▪ Form partnership/LLC

▪ Gift FLP interests – wealth shifting; but retain interest in FLP.

▪ Capital should be material income producing factor

▪ Use trusts for minors

▪ Reverse Family Limited Partnership▪ Purpose: Shift income (same as above) & convert OI into LTCG.

▪ How: Installment sale to 2nd generation to retain some income

▪ 2nd Generation contributes property to partnership/LLC

▪ 1st Generation no longer manages.

▪ Use trusts for minors and to help on down payment77

Other LLC/High Income Strategies

▪ Charitable Remainder Trust▪ Why: Avoid tax on appreciation, still need cash flow

▪ Why: Interest in reducing NIIT

▪ Charitable Intent. Want to make gift during lifetime, but

▪ Willing to accept ordinary income (downside)

▪ NIIT avoided if AGI kept under $250K/year.

▪ Steps: 1. Form Charitable Remainder Trust

▪ 2. Make donation – charitable contribution deduction of

of future interest – AGI limit 5/year carry-forward limit.

▪ Downside – Whether NPV better depends on factors. More effective when CG and OI rates are fairly close. (Ronald Regan era). Other options if not charitably minded. 78

Proposals and Changes on the Horizon

79

Proposals and Changes

• SET on LLC Members, Limited Partners, and S corporation shareholders

• Joint Committee SET proposal (2005)

• Repeal limited partner exception

• Partner that does not materially participate pays SET only on reasonable compensation for services; distributive share income generally subject to NIIT

• Investment income of a service partnership is subject to SET

• S corporation treated same as a partnership for SET purposes

• 2017 Tax Reform Act

• Early version treated 30% of distributive share income and other business income as income from capital exempt from SET, with an option to prove a greater percentage. It was not adopted.

80

Proposals and Changes

• July 31, 2015 IRS 2015-2016 Priority Guidance Plan

• Final Regulations Under Section 469(h)(2) – Ltd P’ships

• Finalize open portions of Section 1411 regulations

• AICPA Proposals to Treasury

• Clarify material participation

• Clean up of regulations/statutory reform

• Buffet Rule (30% min tax on TI > $1 million) – H. Clinton

• Trump – eliminate AMT and the 3.8% NIIT.

81

Proposals and Changes AICPA asked the Treasury to clarify material participation for

trusts and estates: Follow the two court decisions (Carter & Aragona) Count all trustee/executor activities – capacity and personal

ownership is irrelevant; Count the activities of employees and agents employed; Adopt Temp. Reg. § 1.469-5T(a) material participation tests for

trusts/estates; Deem for a statutory period that estate materially participated if the

prior owner materially participated before his or her death; Treat the character of trust/estate’s income and beneficiary’s

distributions the same; Allow beneficiary participation in QSST to determine if QSST gain

from a sale of S Corp. stock is active or passive; Allow both the S portion and the non-S portion of an ESBT to be a

single trust for §469 rules. Allow a trust/estate to be a real estate professional under §469(c)(7)

and state how.82

Proposals and Changes

• AICPA further proposed for individuals:

• Threshold Amounts. Allow an inflation CPI adjustment.

• Simplify Losses. Allow taxpayers to opt to include all gain or excluding all losses under look-through disposition rules for pass-through entities.

• Create Safe Harbor for Tiered. Add a simplified safe harbor for tiered pass-through dispositions

83

Disclaimer

• This document is not intended to provide advice on any specific legal matter or factual situation, and should not be relied upon without consultation with qualified professional advisors.

• Any tax advice contained in this document and any attachments was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties that may be imposed under applicable tax laws, or (ii) promoting, marketing, or recommending to another party any transaction or tax-related matter.

84