Embed Size (px)

Citation preview

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code. You will have to write down

only the final verification code on the attestation form, which will be emailed to registered attendees.

• To earn full credit, you must remain connected for the entire program.

Income in Respect of a Decedent: Mastering Sec. 691 IRD

Calculations, Reporting and Planning Strategies Preserving Deductions and Minimizing the Tax Impact of IRD Through Transfers and Conversions

WEDNESDAY, AUGUST 31, 2016, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

Aug. 31, 2016

Income in Respect of a Decedent

Monica Haven, E.A., J.D., LLM, Founder

Los Angeles

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Income in Respect of a Decedent: Mastering §691 IRD Calculations, Reporting & Planning Strategies

Monica Haven, EA, JD, LLM

© 2016

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

What is IRD?

6

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Answer…

IRD = Income-in-Respect-of-Decedent

7

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Not defined in IRC Treas. Reg. 1.691(a)-1(b)

“those amounts to which a decedent was

entitled as gross income but which were not

properly includible in computing his taxable

income for the taxable year ending with the

date of his death or for a previous taxable

year under the method of accounting

employed by the decedent”

8

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Example Facts

• Bob worked for XYZ & received pay check each Monday

morning for work performed the previous week

• Bob worked last week & then died over the weekend

• Bob’s executor will collect the final pay check on Bob’s behalf

Where should income be reported?

o Form 1040

o Form 1041

o Form 706

o Widow’s Form 1040

9

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Method of Accounting • Cash – report income upon constructive receipt;

claim deductions when paid

• Accrual – report income as it is earned; report

expenses when incurred

• Individuals are generally cash-basis & do not

include accrued income

Decedent cannot include wages earned but not

yet paid before DoD (This is IRD!)

10

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

IRD is taxable • To recipient when received

• Who is recipient?

o Decedent's personal representative (if paid to estate) Form 1041

o Decedent’s beneficiary (if paid to individual)

Form 1040

11

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Transfer of Right to IRD

• Transfer –by gift or sale – is taxable to transferor

• Transfer – by inheritance or bequest – is taxable to

transferee

TAX TIP: Transfer IRD to beneficiary in lower tax

bracket; defer income recognition until beneficiary

actually receives income

12

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

History • IRD was initially deemed to be an asset

o Includible in decedent’s net worth on estate return

o Received stepped-up basis

o Theory: Income becomes corpus on DoD

• Tax Code change in 1934

o Accrued income (IRD) is taxable as income on final 1040

o Treated cash-basis taxpayers as accrual-basis

o Forced early recognition & bunching of income

o Ignored basic principal that taxpayers must have money

with which to pay taxes

13

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Asset or Income? • It’s BOTH!

• IRD is includible as asset on Form 706 and as income

on Form 1041 (or beneficiary’s 1040)

• To mitigate double taxation –

fiduciary (beneficiary) receives

income tax deduction for estate

tax paid

14

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Double Taxation Facts

• Wages of $10K had been earned but not yet paid to employee

before death

• Decedent’s estate is in 40% estate tax bracket & 35% income tax

bracket

Therefore, total estate ($4K) & income taxes ($3.5K) that would be

owed = $7,500

BUT estate may claim deduction on Form 1041 for estate tax paid:

• Taxable income = $10K - $4K estate tax deduction = $6,000

• Income tax = $6K X 35% tax rate = $2,100

• Total estate ($4K) & income taxes ($2.1K) actually due = $6,100

15

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

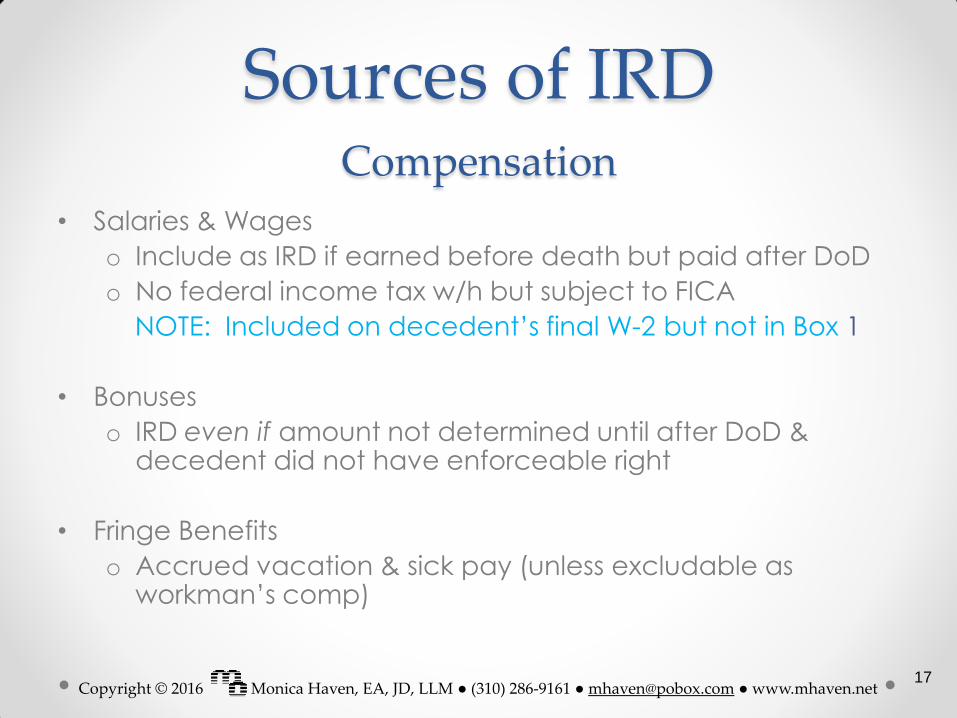

Sources of IRD Compensation

• Salaries & Wages

o Include as IRD if earned before death but paid after DoD

o No federal income tax w/h but subject to FICA

NOTE: Included on decedent’s final W-2 but not in Box 1

• Bonuses

o IRD even if amount not determined until after DoD & decedent did not have enforceable right

• Fringe Benefits

o Accrued vacation & sick pay (unless excludable as workman’s comp)

17

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Compensation - Post-death Payments

Contractual

Employment contract guaranteed payment of $10,000/month

for services rendered & that salary would be paid to employee’s

estate for 1 year after death.

Report as IRD income on Form 1041

Report as IRD asset on Form 706

[b/c employee had rights]

Voluntary

Employer voluntarily issued monthly checks to deceased

employee’s spouse for 1 year after death.

Report on Form 1041 [b/c attributable to employee’s services]

Do NOT report on Form 706

18

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

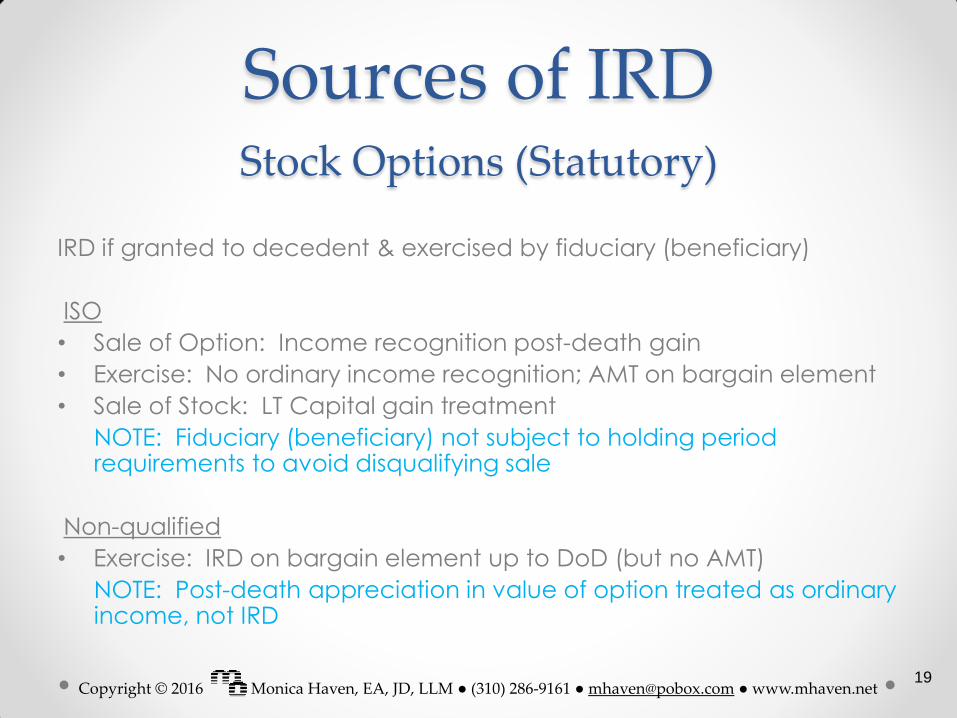

Sources of IRD Stock Options (Statutory)

IRD if granted to decedent & exercised by fiduciary (beneficiary)

ISO

• Sale of Option: Income recognition post-death gain

• Exercise: No ordinary income recognition; AMT on bargain element

• Sale of Stock: LT Capital gain treatment

NOTE: Fiduciary (beneficiary) not subject to holding period requirements to avoid disqualifying sale

Non-qualified

• Exercise: IRD on bargain element up to DoD (but no AMT)

NOTE: Post-death appreciation in value of option treated as ordinary income, not IRD

19

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

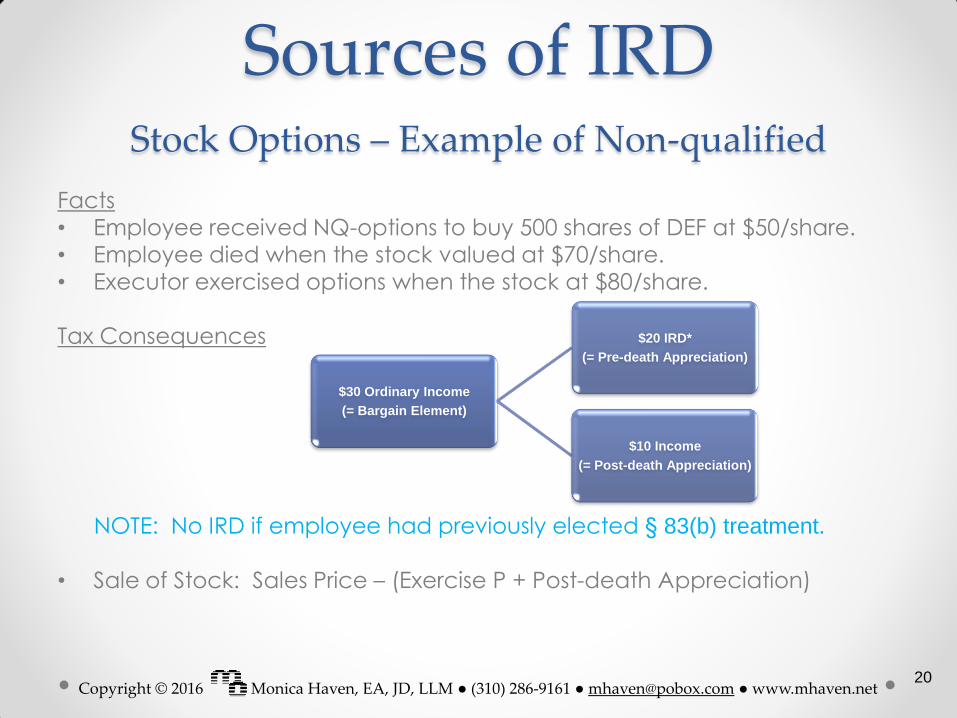

Sources of IRD Stock Options – Example of Non-qualified

Facts

• Employee received NQ-options to buy 500 shares of DEF at $50/share. • Employee died when the stock valued at $70/share. • Executor exercised options when the stock at $80/share. Tax Consequences

NOTE: No IRD if employee had previously elected § 83(b) treatment.

• Sale of Stock: Sales Price – (Exercise P + Post-death Appreciation)

$30 Ordinary Income

(= Bargain Element)

$20 IRD*

(= Pre-death Appreciation)

$10 Income

(= Post-death Appreciation)

20

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Employee Stock Purchase Plans

Basics

• Must be non-discriminatory

• Must be exercised w/i 5 years after grant if strike ≥ 85% of stock price

• Non-transferrable during life; but can be bequeathed

Tax Treatment

• Exercise: No ordinary income recognition (& no AMT)

• Sale of Stock: LT Capital gain treatment if stock held ≥ 1 year after exercise and ≥ 2 years after grant

NOTE: If holding period not met by estate, ordinary income recognized is treated as IRD.

21

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Deferred Compensation

Employer-Employee Agreement

• Allows employee to defer recognition of income until later (retirement?)

• IRD if post-death payments are made to estate (beneficiary)

Tax Treatment

• Agreement to forfeit all payments during life in exchange for employer’s promise to pay at death

• IRD when accumulated deferral is paid out

NOTE: Although decedent did not have right to income, post-death income classified as IRD if only to prevent tax loophole

22

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Retirement: IRAs

• Lump-sum distributions: FMVDOD less Decedent’s

Basis taxed as IRD in year of payment

NOTE: Had decedent lived & taken withdrawals, he

would have been taxed on all income & growth in

excess of basis

• No IRD if spouse makes

rollover to Spousal IRA

23

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Traditional IRA

Pre-tax Contributions Only

• FULL balance on DoD is IRD

• Beneficiary must include as income but may claim deduction

for estate tax attributable to the IRD

• Post-death appreciation is not IRD (but is income, of course)

Some Non-deductible Contributions

• IRD = Payout amount – Decedent’s Non-deductible

Contributions – Post-death Appreciation

24

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

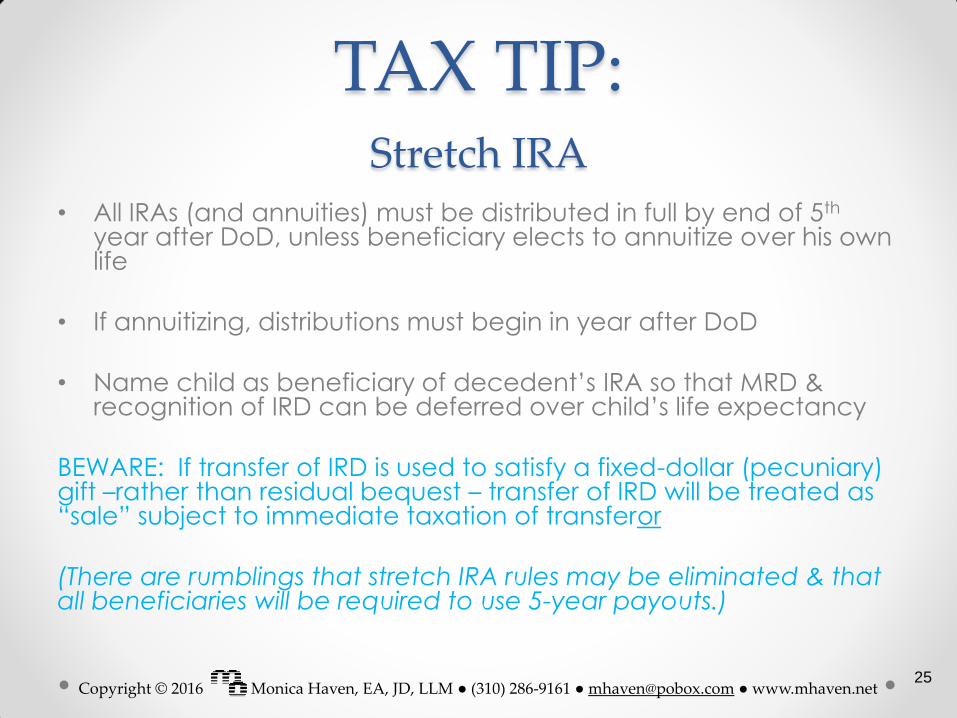

• All IRAs (and annuities) must be distributed in full by end of 5th year after DoD, unless beneficiary elects to annuitize over his own life

• If annuitizing, distributions must begin in year after DoD

• Name child as beneficiary of decedent’s IRA so that MRD & recognition of IRD can be deferred over child’s life expectancy

BEWARE: If transfer of IRD is used to satisfy a fixed-dollar (pecuniary) gift –rather than residual bequest – transfer of IRD will be treated as “sale” subject to immediate taxation of transferor

(There are rumblings that stretch IRA rules may be eliminated & that all beneficiaries will be required to use 5-year payouts.)

TAX TIP: Stretch IRA

25

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

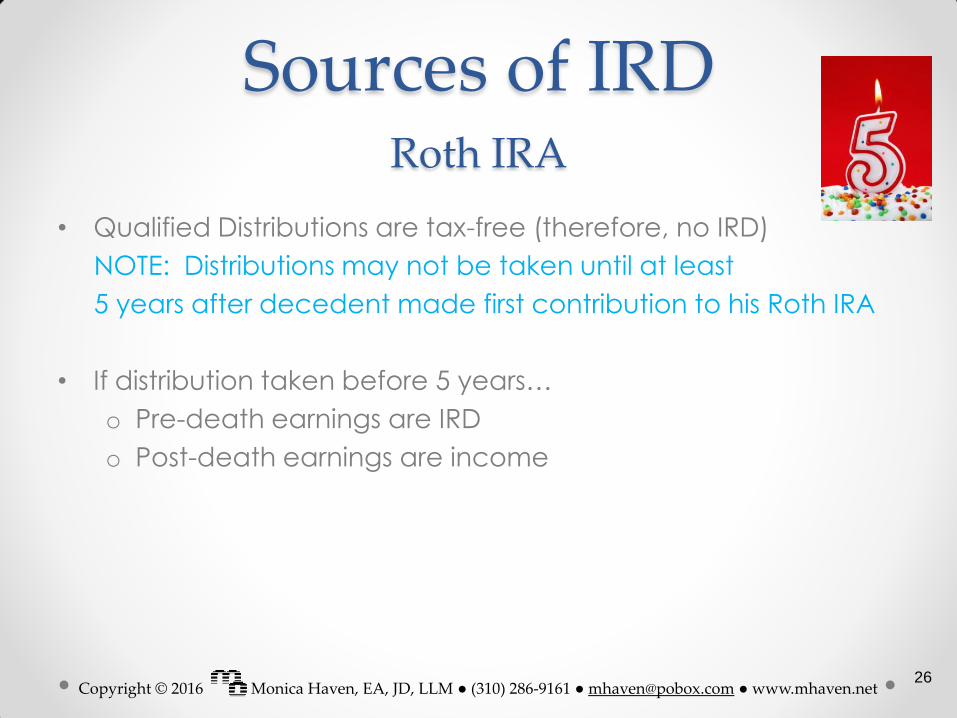

Sources of IRD Roth IRA

• Qualified Distributions are tax-free (therefore, no IRD)

NOTE: Distributions may not be taken until at least

5 years after decedent made first contribution to his Roth IRA

• If distribution taken before 5 years…

o Pre-death earnings are IRD

o Post-death earnings are income

26

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

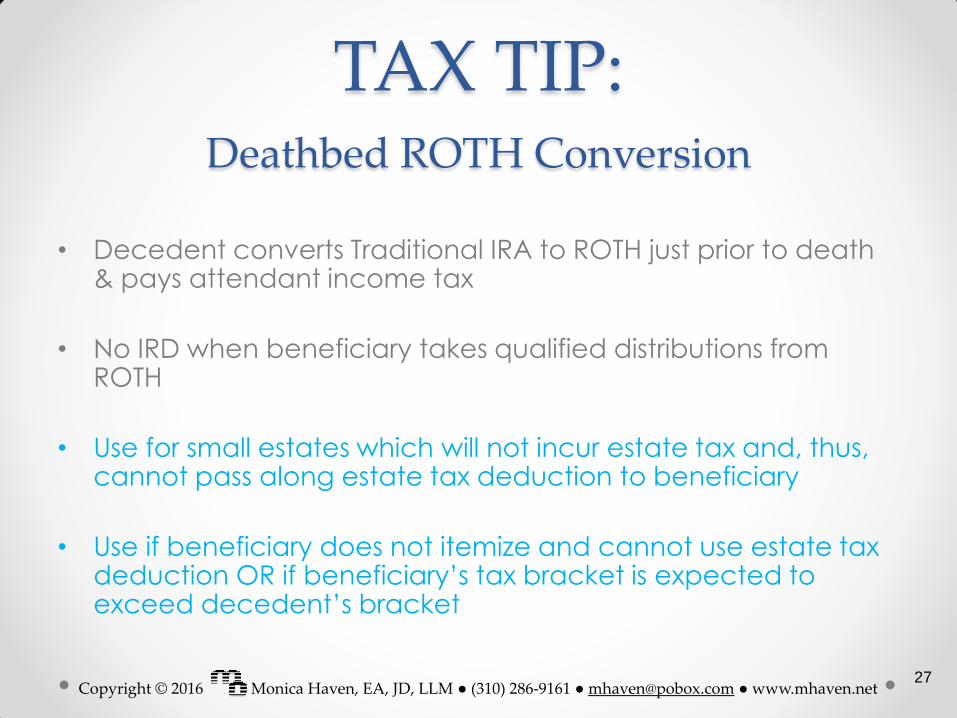

• Decedent converts Traditional IRA to ROTH just prior to death & pays attendant income tax

• No IRD when beneficiary takes qualified distributions from ROTH

• Use for small estates which will not incur estate tax and, thus, cannot pass along estate tax deduction to beneficiary

• Use if beneficiary does not itemize and cannot use estate tax deduction OR if beneficiary’s tax bracket is expected to exceed decedent’s bracket

TAX TIP: Deathbed ROTH Conversion

27

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

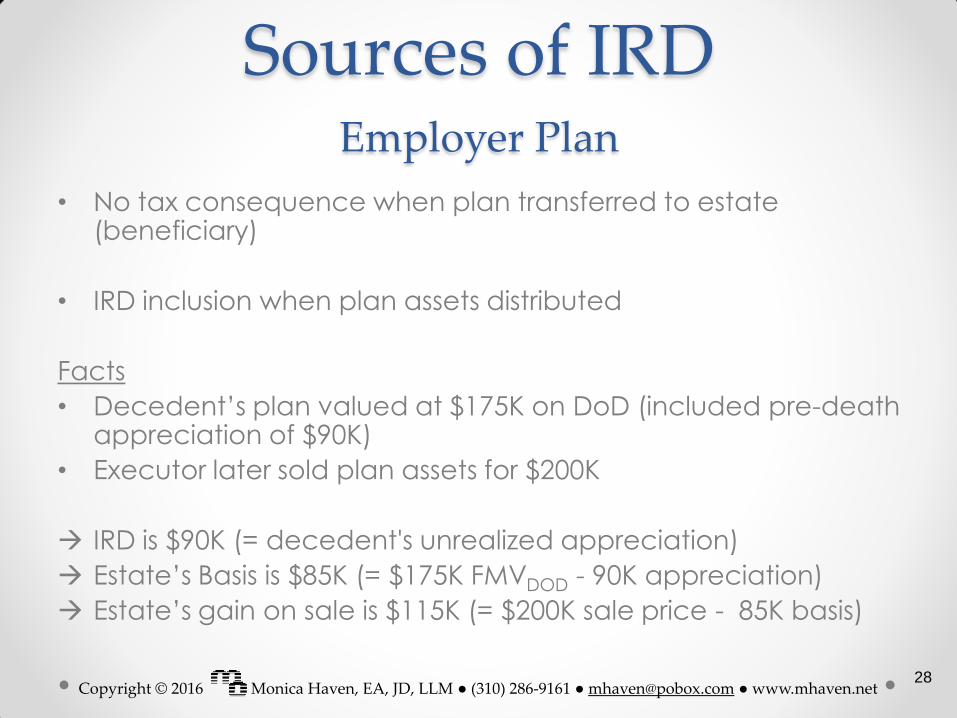

Sources of IRD Employer Plan

• No tax consequence when plan transferred to estate (beneficiary)

• IRD inclusion when plan assets distributed

Facts

• Decedent’s plan valued at $175K on DoD (included pre-death appreciation of $90K)

• Executor later sold plan assets for $200K

IRD is $90K (= decedent's unrealized appreciation)

Estate’s Basis is $85K (= $175K FMVDOD - 90K appreciation)

Estate’s gain on sale is $115K (= $200K sale price - 85K basis)

28

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Self-employment Income

• Sales Revenues – uncollected income at death (even if decedent was cash-basis taxpayer)

• Receivables

o Insurance Commissions – trailing sales commissions paid to estate (beneficiary)

o Royalties – pre-death earnings (post-death royalties on decedent’s invention or writing ≠ IRD)

• Contracts – post-death income received from agreements made before death

29

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Crops & Livestock

• Assets owned at death are reported on Form 706

• IRD only if farmer had sold or pledged harvest or livestock pre-

death

Facts

• Farmer delivered 5,000 crates of oranges but did not collect

payment

• Farmer tried but did not complete sale of another 4,000 crates

• Executor collects payment for 5,000 crates & arranges sale of

remainder

Gain on sale of 5,000 crates = IRD

Gain on sale of 4,000 ≠ IRD

30

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Interest: US Savings Bonds

• EE & I-bonds are issued at discount & mature at full face value

Difference between maturity value and purchase price is deemed “interest”

• Taxpayer – while alive – may elect to…

1. Report interest at maturity

If taxpayer dies pre-maturely, executor may:

- Include decedent’s accrued interest on final 1040 beneficiary liable only for post-death accruals, or

- Allocate decedent's interest to beneficiary who may then elect to include interest at maturity or accrue annually

2. Report accrued interest annually

If taxpayer dies pre-maturely, interest btw. year-start and DoD = IRD

31

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD US Savings Bonds Examples

Fiduciary does not include accrued interest on final 1040

• Decedent bought $1000 Series EE bond for $500

• $94 interest accrued pre-death (not included on decedent’s final 1040)

Beneficiary may elect to include accrued interest on his own 1040 or report full $500 at maturity

If 706 filed, Beneficiary may claim deduction for estate tax attributable to interest accrual

Fiduciary elects to include accrued interest on 1040

• Instead, Executor includes $94 on final 1040

Beneficiary liable for only $406 of interest (= $500 – $94)

No IRD since interest represents post-death accrual

32

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Interest: Treasury & Muni Bonds

• Treasuries

o Pre-death interest accrual = IRD

o Post-death accruals = income to estate (beneficiary)

• Munis

o Only taxable interest generates IRD tax-free interest ≠ IRD

NOTE: Interest on private-activity bonds subject to AMT! Estate (beneficiary) cannot use estate tax deduction to offset AMT liability since no IRD inclusion

NOTE: Value of muni + accrued interest = asset on Form 706

Text Page 13

33

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Interest: CDs & Bank Accounts

• Pre-death interest on CD paid at maturity = IRD

• Pre-death interest on savings account paid at end of

month after death = IRD

NOTE: Unless notified of new EIN assigned to decedent’s

estate, bank will likely issue only one 1099 attributing all interest

to decedent's SSN --> Fiduciary must allocate pre- and post-

death interest

• Pre-death interest actually received by decedent must be

reported on Form 1040

• Pre-death interest accrued but not received by decedent

must be reported as IRD on From 1041 and Form 706

• Post-death interest must be reported on Form 1041

34

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

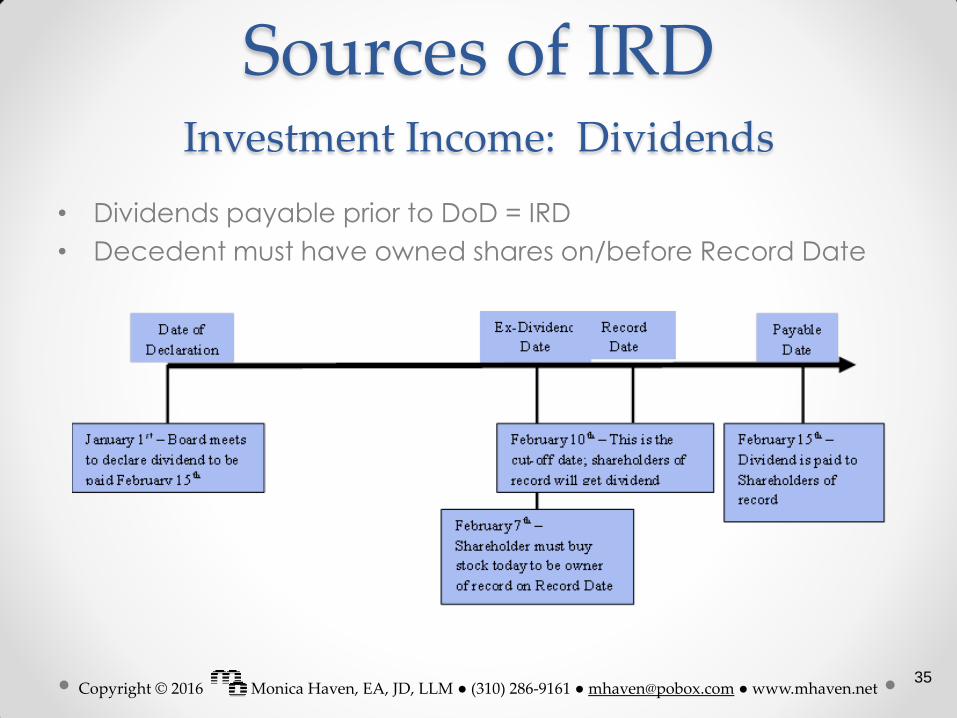

Sources of IRD Investment Income: Dividends

• Dividends payable prior to DoD = IRD

• Decedent must have owned shares on/before Record Date

35

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Investment Income: Annuities

Contractual agreements which provide tax-deferred growth during Accumulation Phase & guaranteed payments during Pay-out Phase

Annuitant dies after payments have begun o Continuing payments to estate (beneficiary) = IRD

Annuitant dies before payments have begun

o Eventual payments to estate (beneficiary) in excess of decedent’s basis = IRD

Facts

Owner selected 10-yr term certain; policy will pay owner (then bene) for 10 years

Owner’s pre-determined exclusion ratio is 40%; portion of owner’s investment is allocated to each payment until recovered

Owner (then bene) will include 60% of each payment as taxable income (IRD)

36

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Investment Income: Capital Gains

• If decedent entitled to sales proceeds, then IRD

o e.g., property (inventory) sold pre-death but

proceeds collected post-death by estate

(beneficiary)

Facts

• Seller contracts to sell home pending Buyer’s loan approval w/i 60 days

• Seller dies before Buyer receives timely loan approval

Gain on sale = IRD

If Buyer had not qualified until Day 65; gain ≠ IRD

• Capital assets (inventory) includible in estate ≠ IRD

o Receive basis step-up instead

37

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Installment Sales

• Estate (beneficiary) has to use same Gross Profit Percentage as decedent

• If self-canceling at death of lender, treat as taxable transfer include as-yet unrecognized income as IRD

to estate (beneficiary)

TIP: Bequeath sufficient cash to beneficiary which he may

then use to pay off note [make sure terms of loan allow for

penalty-free pre-payment]

• If note sold at discount by executor, then IRD can be

reduced by amount of discount

38

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Rental & Royalty Income

• Rents

o Accrued rents paid after DoD = IRD

o Advance rents are liabilities (not IRD)

• Crop Shares

o Crops or livestock are used to pay rent = IRD

• Oil & Gas Royalties

o Income for production before DoD = IRD

NOTE: Royalties are often paid in arrears – contact payer to determine amounts “suspensed” (earned previously but paid later)

39

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Flow-Through Entities: Partnerships

• Income prior to DoD reported on decedent’s K-1 (& final 1040)

• Income after DoD reported on estate’s K-1 (& 1041) no IRD

• IRD if:

o Estate (beneficiary) receives decedent’s guaranteed payments

o Estate (beneficiary) receives payments attributable to unrealized receivables (if decedent was general partner in service)

o Insurance proceeds from buy-sell agreement which represent payments for decedent’s work-in-progress = IRD

o Estate (beneficiary) receives payments for liquidation of partner’s interest

40

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Flow-Through Entities: S-Corps

• Entity may perform an interim closing of the books with shareholder consent to properly allocate pre- & post-

death income

• Income attributable to unrealized receivables = IRD

can be used to reduce basis of inherited (acquired)

stock

41

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Litigation Proceeds

IRD if settlement was related to services provided by decedent

Facts

• Plaintiff sued for fraud arising from sale of business to Defendant

• After Plaintiff's death, court awards estate $50K

No IRD; instead report gross proceeds on estate’s Schedule D & offset

entire amount by stepped-up basis on DoD

42

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Life Insurance

• IRD if policy sold prior to decedent’s death

• IRD if decedent owns policy on 3rd party insured (cash value of

policy includible in decedent’s estate)

Facts

• Taxpayer bought life insurance on niece for $10K + $1K/year

• Taxpayer died after 10 years when cash value was $80K

• Executor paid another $1K; niece dies while estate was being administered

• Estate, as beneficiary, received policy value of $300K

Taxable income of $288K (= Proceeds – Decedent’s Basis– Estate’s Basis);

includes IRD of $68K (= Cash ValueDoD – Taxpayer’s Basis)

43

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Sources of IRD Miscellaneous

Alimony

• Spousal support collected by

estate (beneficiary) = IRD

Medical Reimbursements

• IRD if associated expense previously deducted on

decedent’s 1040

44

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

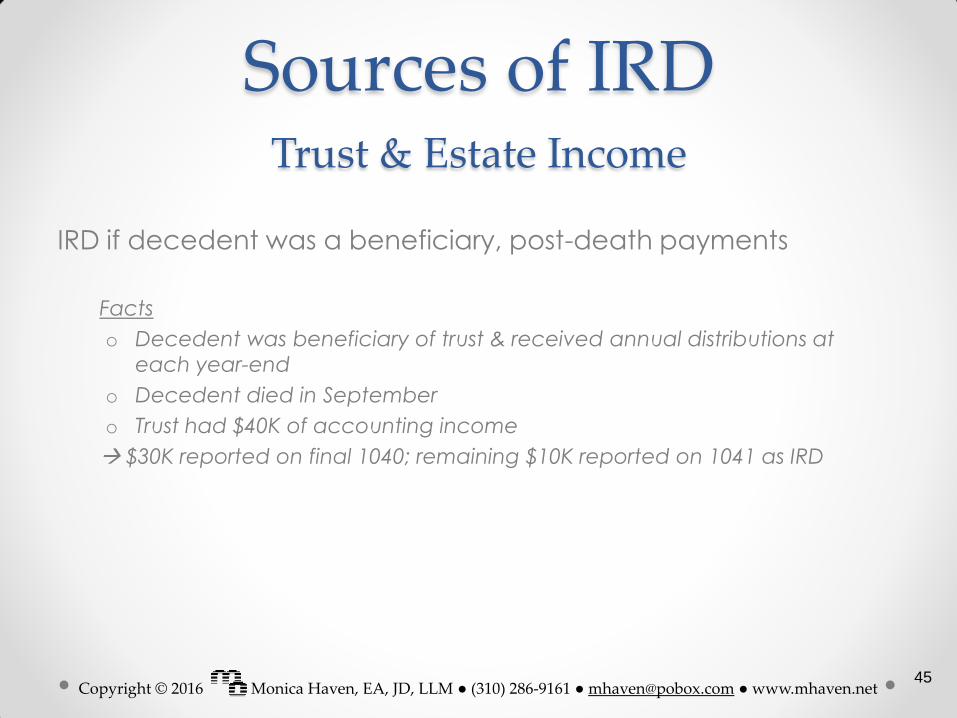

Sources of IRD Trust & Estate Income

IRD if decedent was a beneficiary, post-death payments

Facts

o Decedent was beneficiary of trust & received annual distributions at

each year-end

o Decedent died in September

o Trust had $40K of accounting income

$30K reported on final 1040; remaining $10K reported on 1041 as IRD

45

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

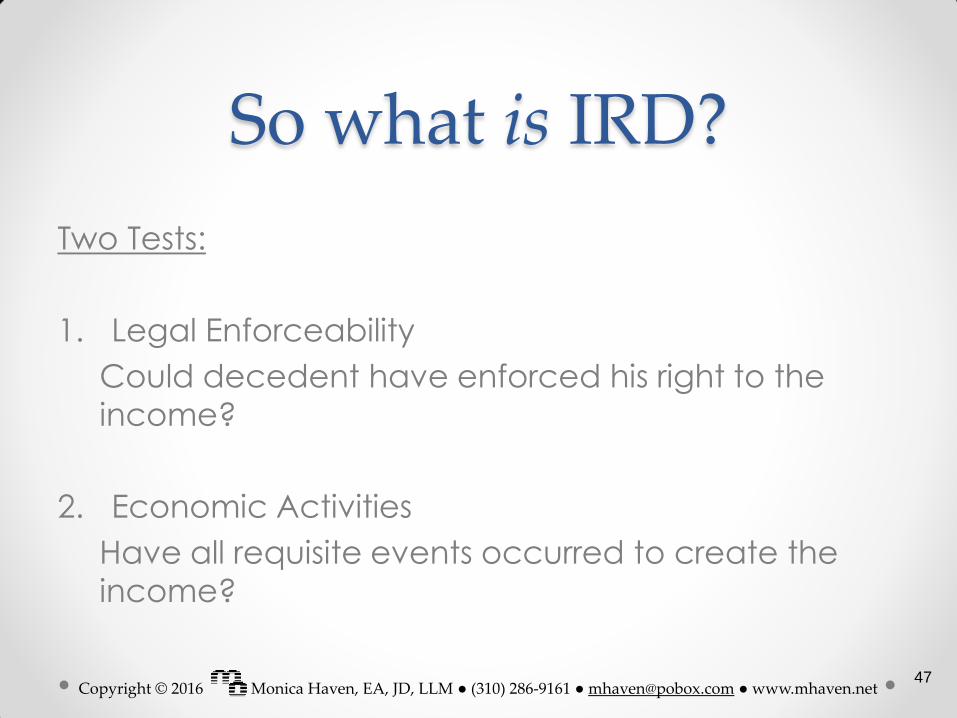

So what is IRD?

Two Tests:

1. Legal Enforceability

Could decedent have enforced his right to the

income?

2. Economic Activities

Have all requisite events occurred to create the

income?

47

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

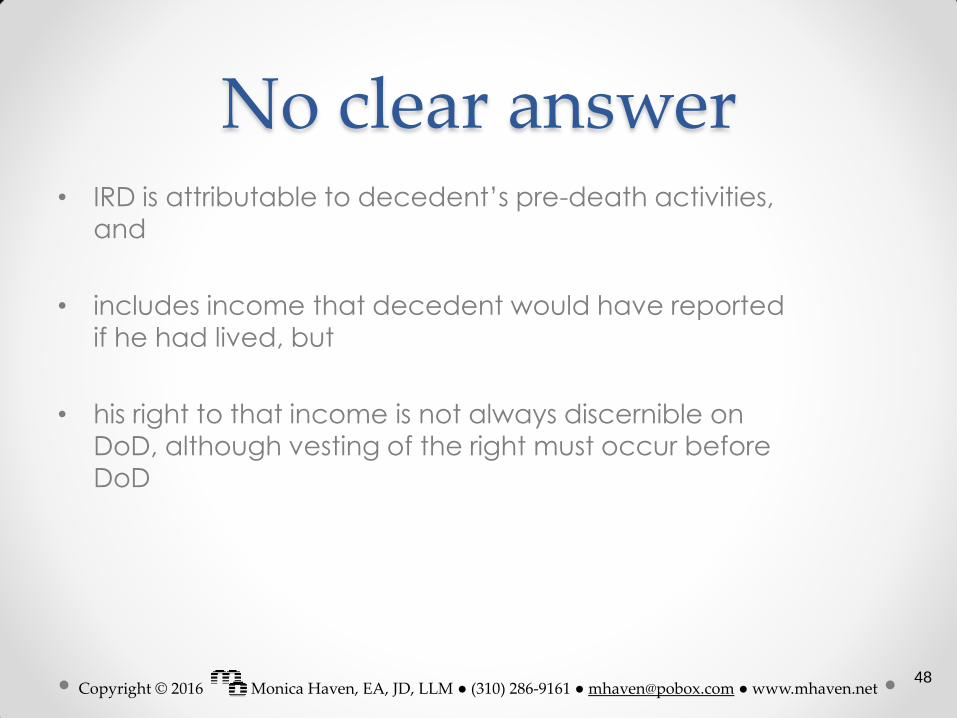

No clear answer • IRD is attributable to decedent’s pre-death activities,

and

• includes income that decedent would have reported

if he had lived, but

• his right to that income is not always discernible on

DoD, although vesting of the right must occur before

DoD

48

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

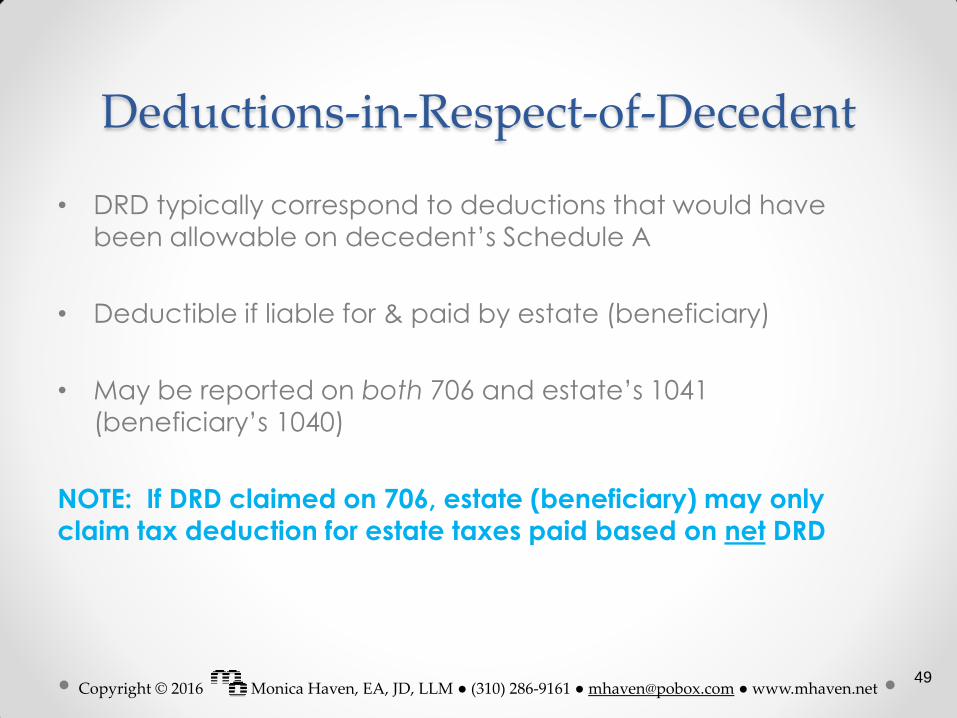

Deductions-in-Respect-of-Decedent

• DRD typically correspond to deductions that would have

been allowable on decedent’s Schedule A

• Deductible if liable for & paid by estate (beneficiary)

• May be reported on both 706 and estate’s 1041 (beneficiary’s 1040)

NOTE: If DRD claimed on 706, estate (beneficiary) may only

claim tax deduction for estate taxes paid based on net DRD

49

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

DRD Expenses Allowable:

• Business expenses

• Interest

• State, local & property taxes

• Depletion – only if percentage method used

• Foreign Tax Credit

Not Allowed:

• Credit card charges (considered paid when charged)

• Pre-death checks if decedent had sufficient funds

• Decedent's alimony payments

• Depreciation (attendant asset gets stepped-up basis instead)

• Loss carry-forwards (capital, passive & NOL) – amounts not used on final 1040 are forfeited

50

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Reporting IRD

• Must be reported by whoever receives it (estate or beneficiary)

• Retain character as if reported by decedent

REMEMBER: IRD is “income” and also an “asset”

therefore, report on estate’s 1041 (beneficiary’s 1040)

and 706 (if required to be filed)

51

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Estate Tax Deduction ETD = Estate Tax paid on net IRD

• Can be used by estate (beneficiary) to reduce taxable IRD income on 1041 (1040)

• Deductible only if estate tax was paid by estate (beneficiary)

• Must be claimed in same year that IRD is included in income

No ETD if:

Form 706 not required No estate tax due

No DRD on Form 706 DRD exceeds IRD

53

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

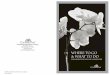

How to Calculate ETD Re-compute Estate Tax (Form 706)…

Step 1

Adjusted Gross Estate on Form 706 (Page 1, Line 5) – Net IRD =

Recomputed Estate Tax

Step 2

Actual Estate Tax Due – Recomputed Estate Tax = Estate Tax Deduction

Step 3

Allocate ETD to fiduciary (beneficiary)

54

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

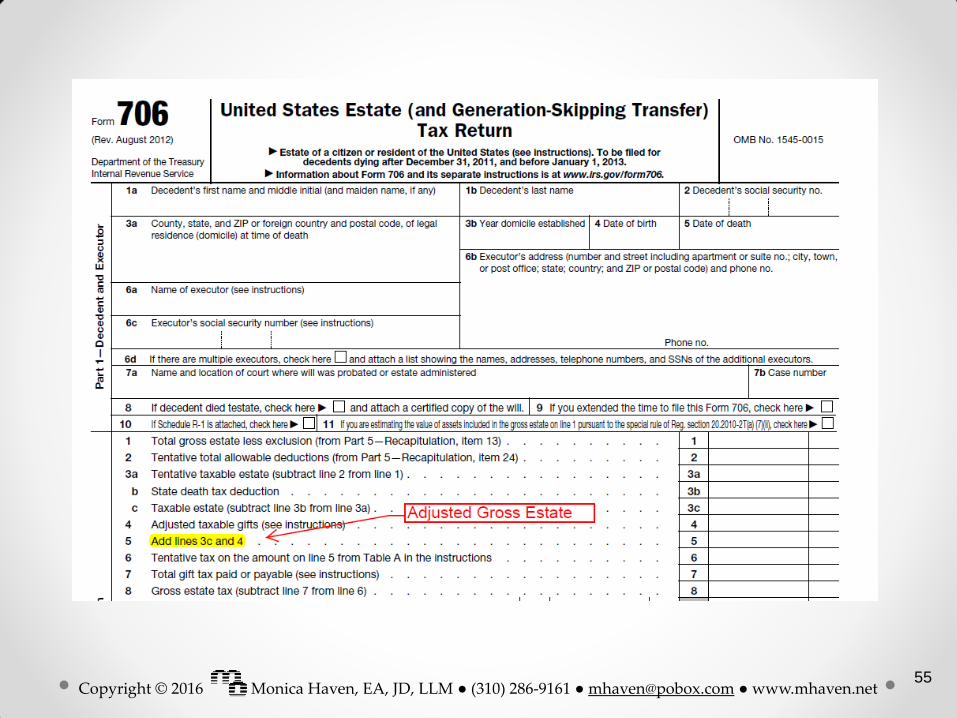

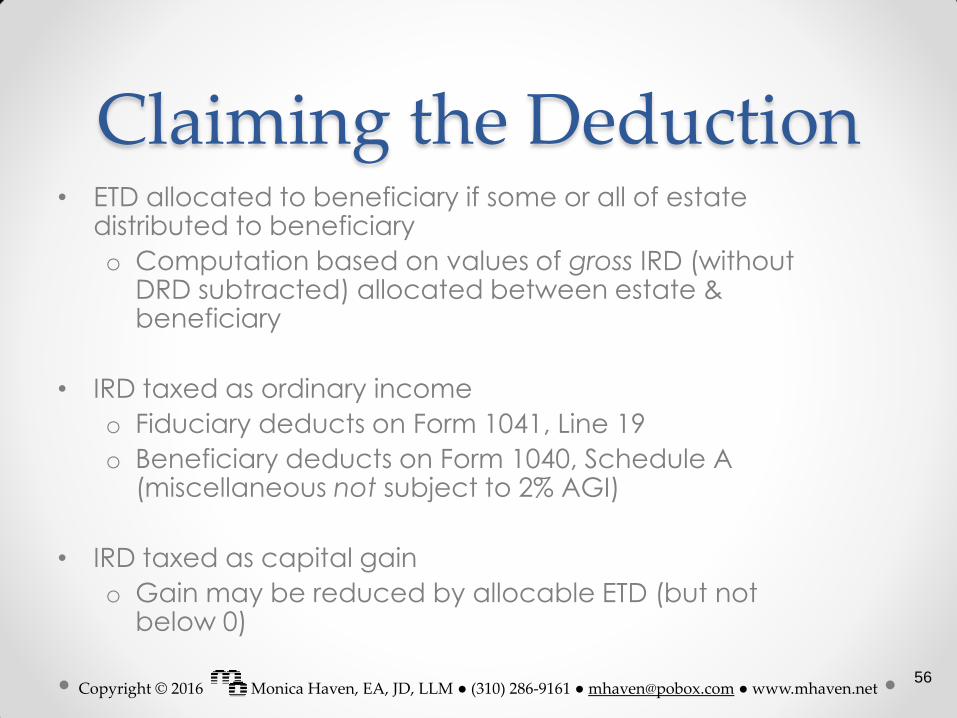

Claiming the Deduction

• ETD allocated to beneficiary if some or all of estate distributed to beneficiary

o Computation based on values of gross IRD (without DRD subtracted) allocated between estate & beneficiary

• IRD taxed as ordinary income

o Fiduciary deducts on Form 1041, Line 19

o Beneficiary deducts on Form 1040, Schedule A (miscellaneous not subject to 2% AGI)

• IRD taxed as capital gain

o Gain may be reduced by allocable ETD (but not below 0)

56

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

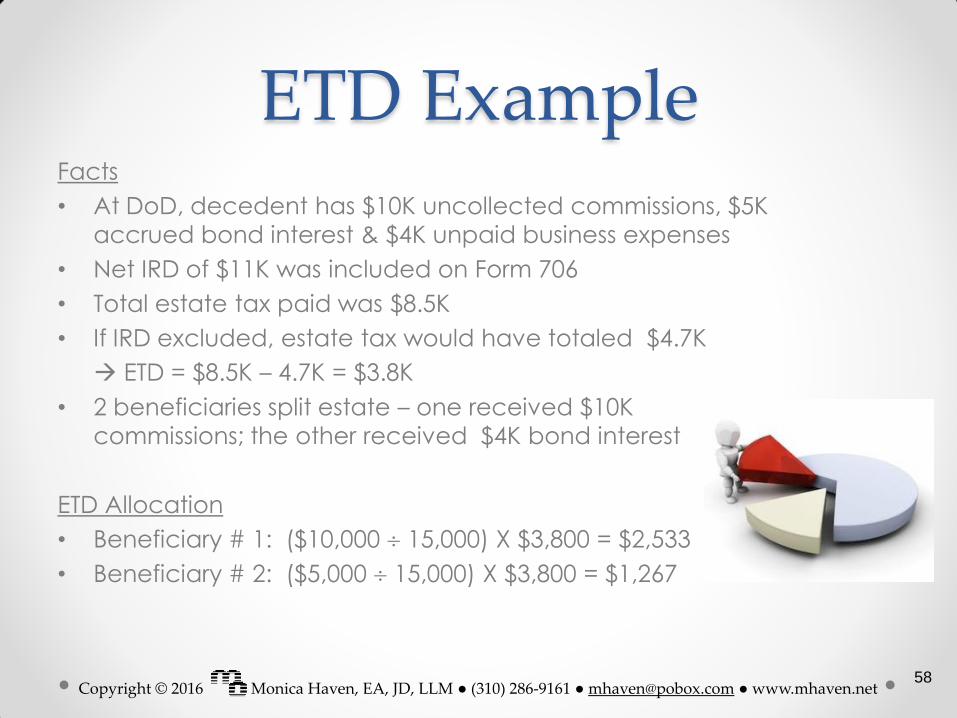

ETD Example Facts

• At DoD, decedent has $10K uncollected commissions, $5K

accrued bond interest & $4K unpaid business expenses

• Net IRD of $11K was included on Form 706

• Total estate tax paid was $8.5K

• If IRD excluded, estate tax would have totaled $4.7K

ETD = $8.5K – 4.7K = $3.8K

• 2 beneficiaries split estate – one received $10K

commissions; the other received $4K bond interest

ETD Allocation

• Beneficiary # 1: ($10,000 15,000) X $3,800 = $2,533

• Beneficiary # 2: ($5,000 15,000) X $3,800 = $1,267

58

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

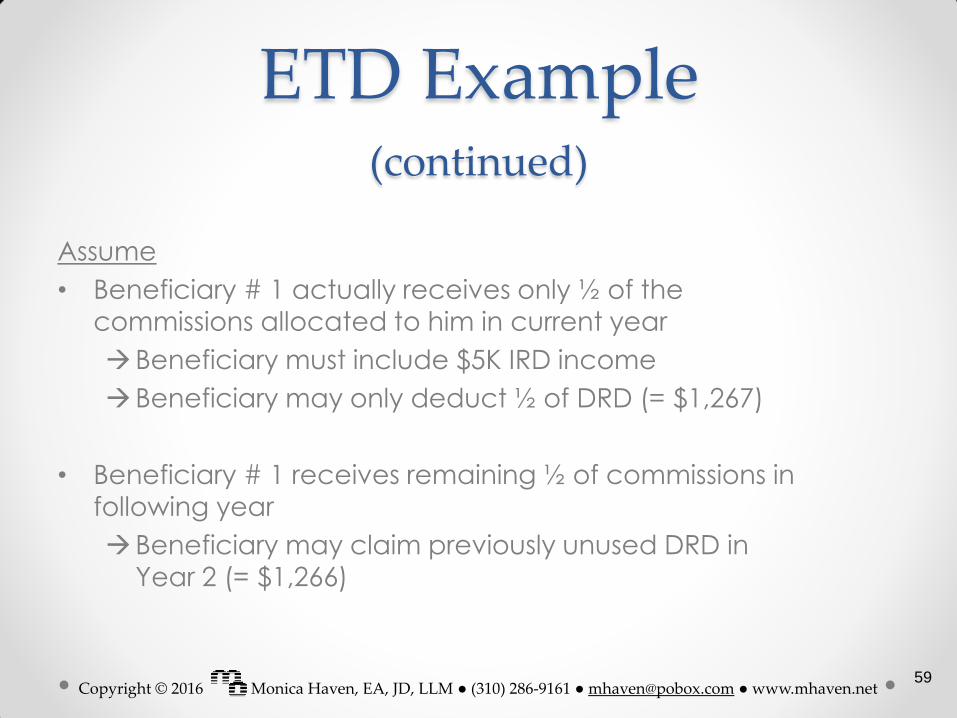

ETD Example (continued)

Assume

• Beneficiary # 1 actually receives only ½ of the

commissions allocated to him in current year

Beneficiary must include $5K IRD income

Beneficiary may only deduct ½ of DRD (= $1,267)

• Beneficiary # 1 receives remaining ½ of commissions in

following year

Beneficiary may claim previously unused DRD in Year 2 (= $1,266)

59

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

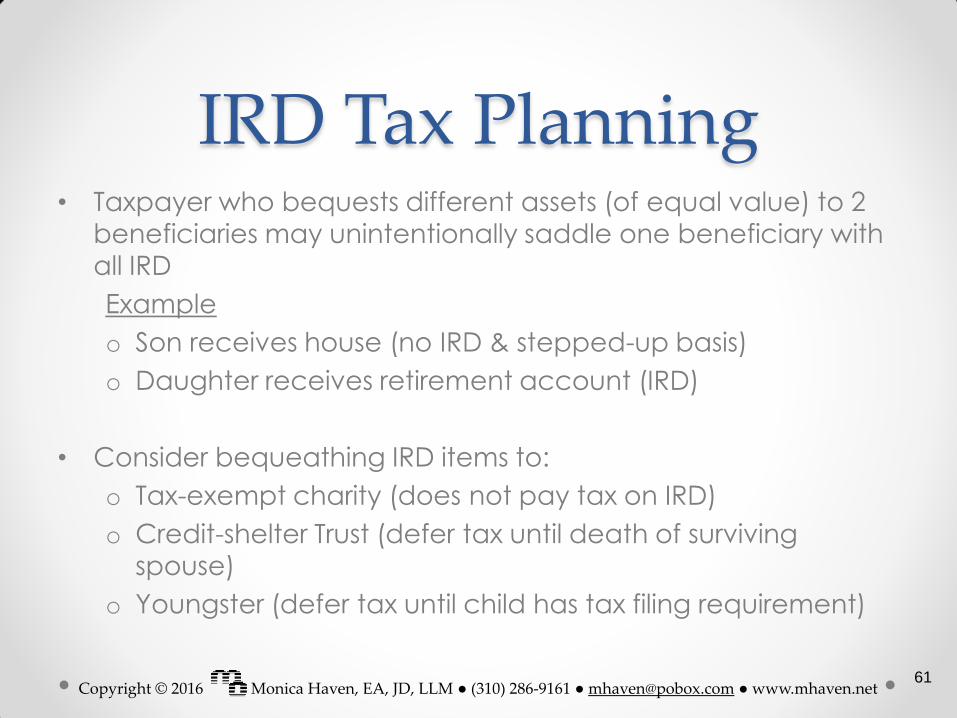

IRD Tax Planning • Taxpayer who bequests different assets (of equal value) to 2

beneficiaries may unintentionally saddle one beneficiary with all IRD

Example

o Son receives house (no IRD & stepped-up basis)

o Daughter receives retirement account (IRD)

• Consider bequeathing IRD items to:

o Tax-exempt charity (does not pay tax on IRD)

o Credit-shelter Trust (defer tax until death of surviving

spouse)

o Youngster (defer tax until child has tax filing requirement)

61

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Minimizing IRD

• Accelerate recognition of income; report on decedent’s final

1040 (e.g., report accrued savings bond interest or elect out of

installment sales)

• Elect fiscal filing year for estate’s 1041 to gain time to

accumulate DRD

• Close estate prior to receipt of taxable IRD (shift burden to

beneficiary in lower marginal bracket)

62

Copyright © 2016 Monica Haven, EA, JD, LLM ● (310) 286-9161 ● [email protected] ● www.mhaven.net

Monica Haven, E.A., J.D.

(310) 286-9161 PHONE

(310) 557-1626 FAX

WEBSITE: www.mhaven.net

The information contained herein is for educational use only and should not be

construed as tax, financial, or legal advice. Each individual’s situation is unique

and may require specialized treatment. It is, therefore, imperative that you consult

with tax and legal professionals prior to implementation of any strategies discussed.

63