Embed Size (px)

Citation preview

For A&B Categories

Prepared by

Power & Energy Division

Engineering Staff College of India Autonomous Organ of The Institution of Engineers (India)

An ISO 9001 : 2008 Certified Institution Old Bombay Road, Gachi Bowli, Hyderabad – 500 032

i.exe

Course Book on

Regulatory

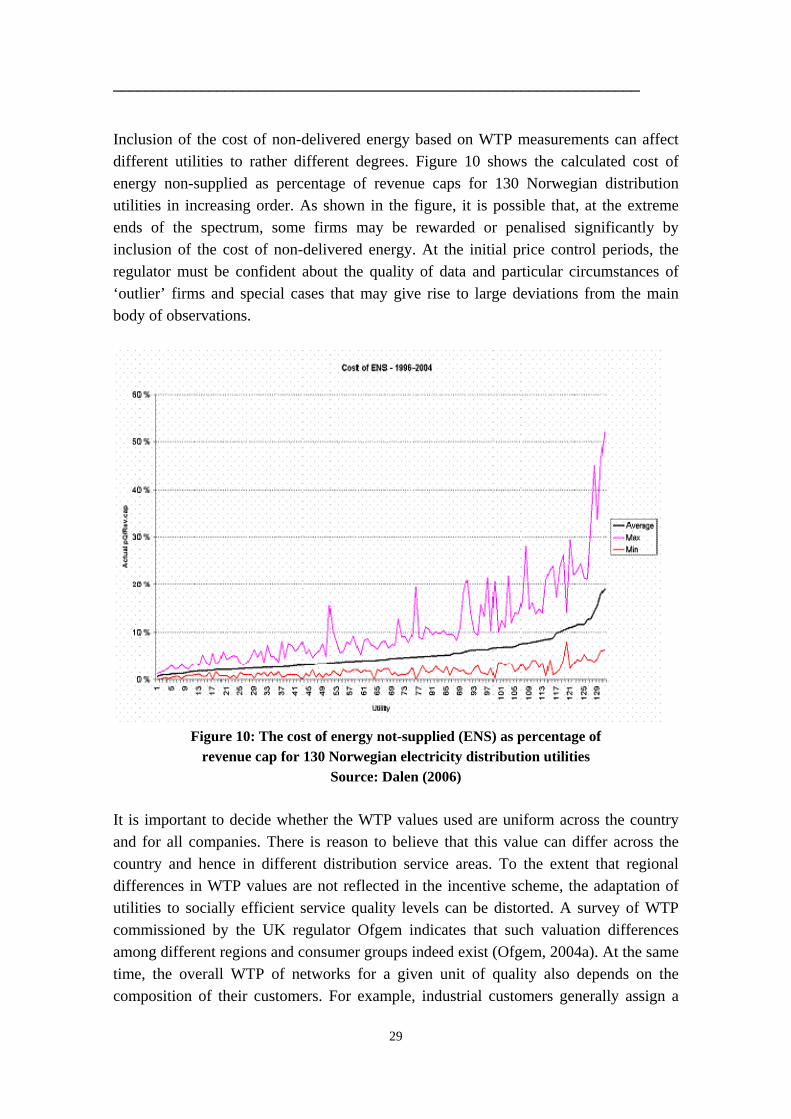

Foreword

ESCI is empanelled as a Resource Institute (RI) for preparation of course book for imparting training to power distribution utility personnel for capacity building under R-APDRP programme of Ministry of Power, Government of India.ESCI is thankful to Power Finance Corporation Limited for giving an opportunity to compile the course content for distribution personnel in Top, Middle and junior management levels

The total material is presented in seven sections.

The first section covers evolution of Regulation of distribution business in India and also global perspectives.

The second section covers natural monopolies, economic, legal and social regulations for electricity distribution. An introduction to regulatory economics is covered.

Third section deals with economic reforms, salient features of Electricity Act 2003, National Tariff policy and trading margins. Additional reading material is provided on emergent regulatory regime in India at annexure

Regulations related to Rate making approach (viz) Rate of Return, based regulation, Price cap regulation, Rate making approaches under National tariff policy are covered under section four. Additional reading material is provided related to these concepts at annexure.

In section five, issues related to Electricity Grid Code, Standards of Performance, Supply code, Terms and conditions of Supply regulations and licensees’ compliance to Distribution Licence conditions are covered.

In section six role of middle management in providing compliance to the directives, Regulatory Information Management System, Cost of Service parameters, guide lines for filling ARR formats, Tariff filing are covered. Implementation of ERP, Accounting Standards and disclosure of information in Annual Reports, XRBL for distribution business is covered.

Conclusions is presented in seventh section. Necessary additional reading material is provided at annexures in form of case studies to get better insight of the concepts.

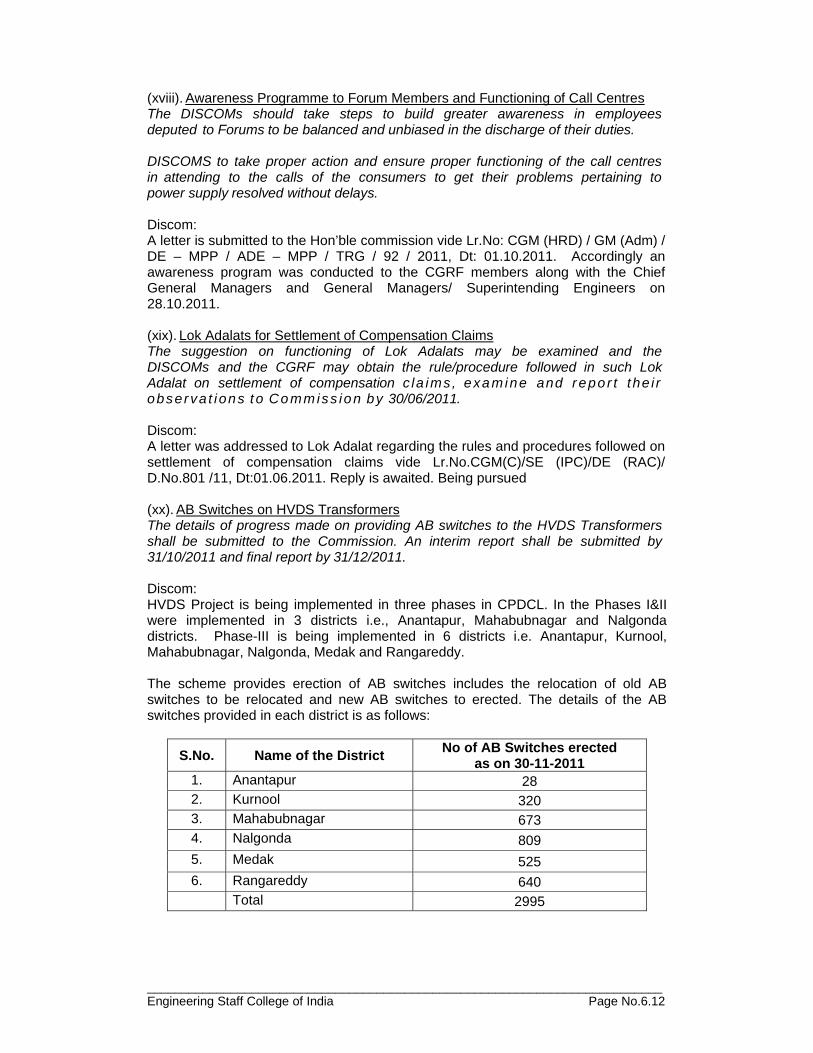

It is earnestly hoped that this book will meet the desired objectives. ESCI welcomes suggestions of the users to improve the content of this book and for enhancing the utility of the book.

_____________________________________________________________________________ Engineering Staff College of India Page No.1.1

Section – 1 Learning Objectives:

a) Uses of electricity b) Basics of electricity distribution c) Need for regulation of electricity distribution d) Evolution of electricity distribution regulation in India e) Regulatory governance of electricity sector – global perspective f) Understanding the concept of national policy on electricity distribution

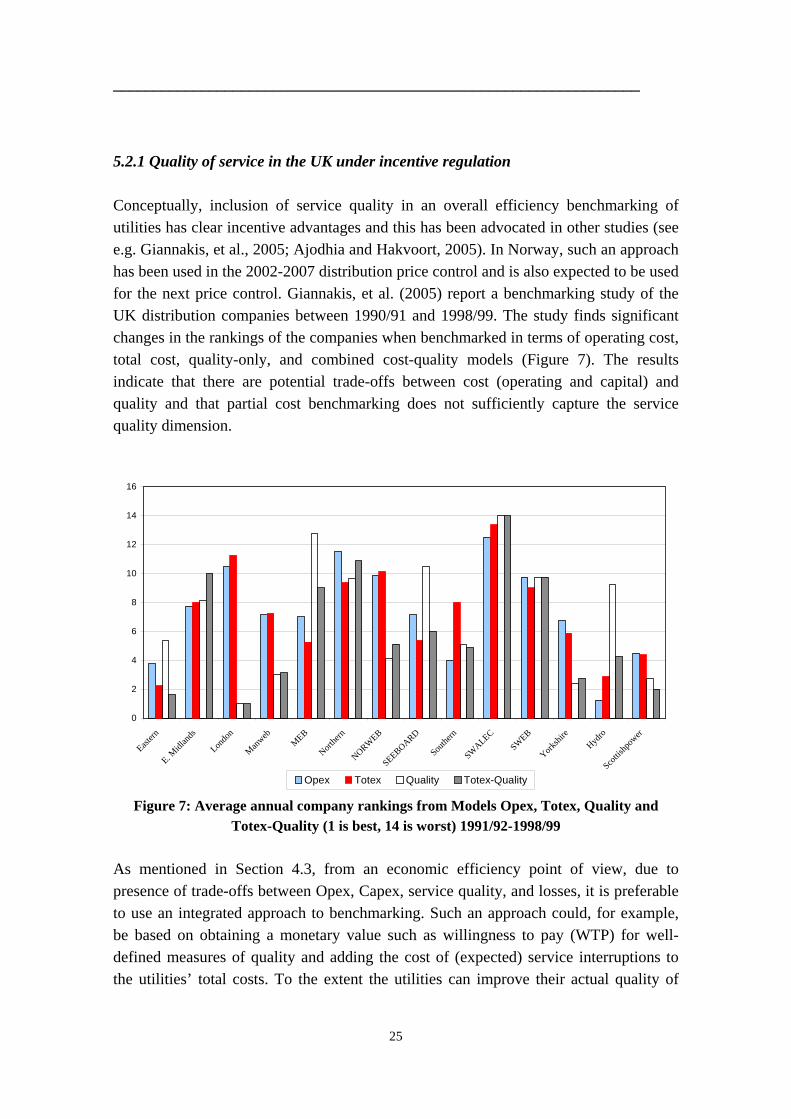

1.0 Introduction 1.0.1 Uses of Electricity We are so much dependent on electric light and other machines and devices which run only with the use of electricity to deliver goods and services essential for our day to day life that we can not think of living a life without electricity even for a day. The social fabric and social security has been dependent on the use of electricity. We may say that electricity has invaded our lives and has become vital in almost all aspects of society today. The list of uses will fill a book but here are a few headings: Transport Trains, buses, trams and cars all use electricity. Many use it as the motive power, meaning that electricity drives the wheels to make the vehicle move. Even gas and diesel powered vehicles use electricity to start the engines, control the engine and power the ancillary devices. Communication as well as providing power for computers, cell phones, fixed phones, electricity is used as the medium for the transmission of signals. Even high speed optical fibers rely on an electrical signal at each end of the line. Without electricity, communication would be reduced to letters, flag waving and lighting fires and shouting at each other. None of the electricity free methods are as flexible as any that we are used to using today. Manufacturing Industry relies on electricity to drive virtually every moving part in a factory. Saws, cutters, conveyor belts, furnaces, chillers - whatever the process, electricity is involved everywhere. Entertainment The MP3 player, the portable battery powered radio, memory stick are all accepted as part of our everyday lives. All rely on electricity to operate. Whether connected to a mains supply or battery, they all use electricity. The list is by no means complete. Take a look around you: if it moves, lights up or makes a noise, it probably uses electricity. Come to think of it, even animals and people use electricity for senses and muscle control, so perhaps the pet dog or cat should be included after all! Can you name all the ways you use electricity at home? We use electricity almost every minute from the time we get up in the morning until we go to bed at night.

_____________________________________________________________________________ Engineering Staff College of India Page No.1.2

Home Heating, lighting, television, radio, computer, telephones all rely on electricity. Even wireless lights such as solar powered lamps will convert sight to electricity. Take a look at all the things we depend on each day that need electricity: In the kitchen: Refrigerators, Dishwashers, Cell phone chargers. In the family room: Video games, Laptops, Lamps and light-bulbs. In the basement or utility room: Washer and dryer, Furnace and water heater. Outdoors: Outdoor lighting, Electric lawn mower, Pool heater. 1.0.2 Electricity Distribution Electricity Distribution and Retail Supply is the third stage of electricity supply chain starting with the Generation of Electricity in a commercial scale. The second stage is the transmission of the electricity i.e. evacuation of the Generated quantum of electricity from the generating stations to the destination of the use or load centres for Distribution and Retail supply to various categories of consumers. In the early days of electricity distribution, direct current (DC) generators were connected to loads at the same voltage. The generation, transmission and loads had to be of the same voltage because there was no way of changing DC voltage levels, other than inefficient motor-generator sets. Low DC voltages were used (on the order of 100 volts) since that was a practical voltage for incandescent lamps, which were the primary electrical load. Low voltage also required less insulation for safe distribution within buildings. The losses in a cable are proportional to the square of the current, the length of the cable, and the resistivity of the material, and are inversely proportional to cross-sectional area. Early transmission networks used copper cable, which is one of the best economically feasible conductors for this application. To reduce the current and copper required for a given quantity of power transmitted would require a higher transmission voltage, but no efficient method existed to change the voltage of DC power circuits. To keep losses to an economically practical level the Edison DC system needed thick cables and local generators. Early DC generating plants needed to be within about 1.5 miles (2.4 km) of the farthest customer to avoid excessively large and expensive conductors. The competition between the direct current (DC) of Thomas Edison and the alternating current (AC) of Nikola Tesla and George Westinghouse was known as the War of Currents. At the conclusion of their campaigning, AC became the dominant form of transmission of power. Power transformers, installed at power stations, could be used to raise the voltage from the generators, and transformers at local substations could reduce voltage to supply loads. Increasing the voltage reduced the current in the transmission and distribution lines and hence the size of conductors and distribution losses. This made it more economical to distribute power over long distances. Generators (such as hydroelectric sites) could be located far from the loads.

_____________________________________________________________________________ Engineering Staff College of India Page No.1.3

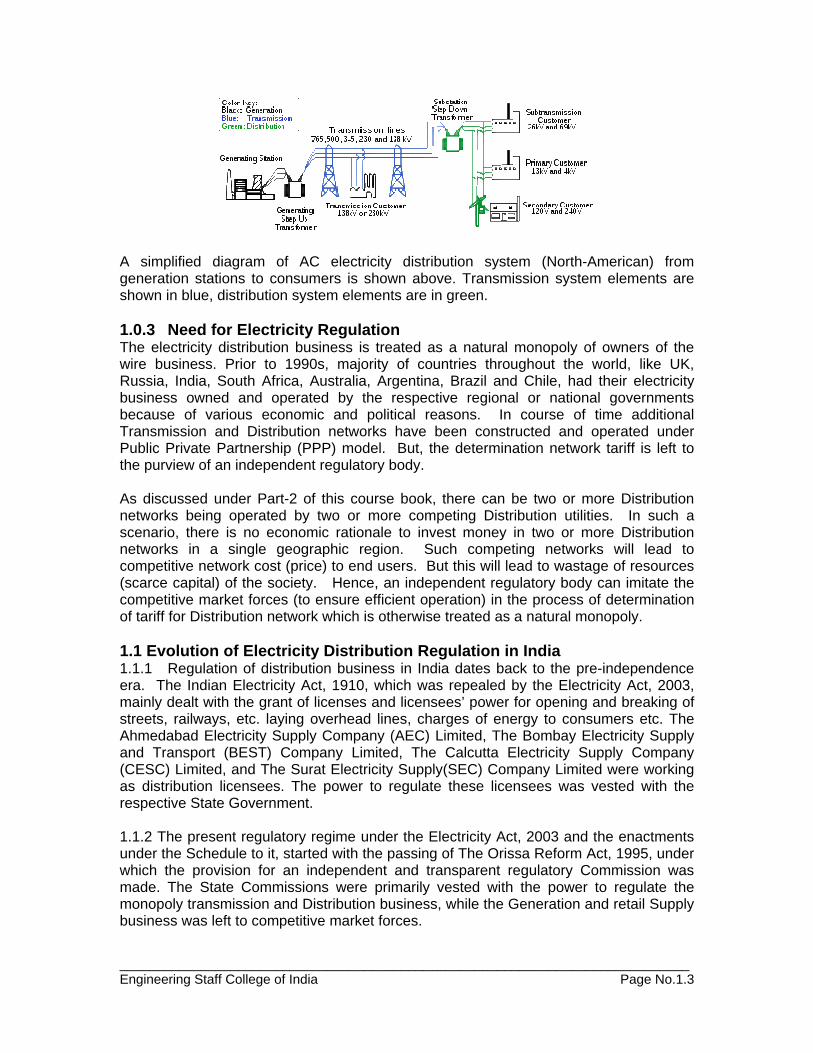

A simplified diagram of AC electricity distribution system (North-American) from generation stations to consumers is shown above. Transmission system elements are shown in blue, distribution system elements are in green. 1.0.3 Need for Electricity Regulation The electricity distribution business is treated as a natural monopoly of owners of the wire business. Prior to 1990s, majority of countries throughout the world, like UK, Russia, India, South Africa, Australia, Argentina, Brazil and Chile, had their electricity business owned and operated by the respective regional or national governments because of various economic and political reasons. In course of time additional Transmission and Distribution networks have been constructed and operated under Public Private Partnership (PPP) model. But, the determination network tariff is left to the purview of an independent regulatory body. As discussed under Part-2 of this course book, there can be two or more Distribution networks being operated by two or more competing Distribution utilities. In such a scenario, there is no economic rationale to invest money in two or more Distribution networks in a single geographic region. Such competing networks will lead to competitive network cost (price) to end users. But this will lead to wastage of resources (scarce capital) of the society. Hence, an independent regulatory body can imitate the competitive market forces (to ensure efficient operation) in the process of determination of tariff for Distribution network which is otherwise treated as a natural monopoly. 1.1 Evolution of Electricity Distribution Regulation in India 1.1.1 Regulation of distribution business in India dates back to the pre-independence era. The Indian Electricity Act, 1910, which was repealed by the Electricity Act, 2003, mainly dealt with the grant of licenses and licensees’ power for opening and breaking of streets, railways, etc. laying overhead lines, charges of energy to consumers etc. The Ahmedabad Electricity Supply Company (AEC) Limited, The Bombay Electricity Supply and Transport (BEST) Company Limited, The Calcutta Electricity Supply Company (CESC) Limited, and The Surat Electricity Supply(SEC) Company Limited were working as distribution licensees. The power to regulate these licensees was vested with the respective State Government.

1.1.2 The present regulatory regime under the Electricity Act, 2003 and the enactments under the Schedule to it, started with the passing of The Orissa Reform Act, 1995, under which the provision for an independent and transparent regulatory Commission was made. The State Commissions were primarily vested with the power to regulate the monopoly transmission and Distribution business, while the Generation and retail Supply business was left to competitive market forces.

_____________________________________________________________________________ Engineering Staff College of India Page No.1.4

1.2 Regulatory Governance of Electricity Sector – Global Perspective 1.2.1 The governance of the monopolistic utility sector was the matter of concern for Managers and Governments across the nations. While the International multilateral agencies wanted the commercial viability of the utilities and sealing the sector from political exploitation, Governments did not show much interest to give up the control over the sector. 1.2.2 World Energy Council (WEC), in its deliberations during the eighties and nineties, tried various reforms and restructuring models for the sector, to introduce efficiency and accountability in to the sector. It is in this context that the South Asian Nations of the WEC had a conference to decide the model of governance for their utilities. 1.2.3 Governments in South Asian countries, at the instance of World Bank, decided to adopt a model where network or wire business like Transmission and Distribution were put under regulatory governance, but Generation and Supply business were put to the competitive market forces. 1.3 National Electricity Policy and Regulation of Distribution Business It is recommended that all participants will go through the entire document of National Electricity Policy, as notified by the Ministry of Power, Government of India, Dated the 12th, February, 2005. The part of the Policy relevant to the distribution business is extracted from the said document, and reproduced in the following paragraphs: 1.3.1 Distribution is the most critical segment of the electricity business chain. The real challenge of reforms in the power sector lies in efficient management of the distribution sector. 1.3.2 The Act provides for a robust regulatory framework for distribution licensees to safeguard consumer interests. It also creates a competitive framework for the distribution business, offering options to consumers, through the concepts of open access and multiple licensees in the same area of supply. 1.3.3 For achieving efficiency gains proper restructuring of distribution utilities is essential. Adequate transition financing support would also be necessary for these utilities. Such support should be arranged linked to attainment of predetermined efficiency improvements and reduction in cash losses and putting in place appropriate governance structure for insulating the service providers from extraneous interference while at the same time ensuring transparency and accountability. For ensuring financial viability and sustainability, State Governments would need to restructure the liabilities of the State Electricity Boards to ensure that the successor companies are not burdened with past liabilities. The Central Government would also assist the States, which develop a clear roadmap for turnaround, in arranging transition financing from various sources which shall be linked to predetermined improvements and efficiency gains aimed at attaining financial viability and also putting in place appropriate governance structures. 1.3.4 Conducive business environment in terms of adequate returns and suitable transitional model with predetermined improvements in efficiency parameters in distribution business would be necessary for facilitating funding and attracting investments in distribution. Multi-Year Tariff (MYT) framework is an important structural incentive to minimize risks for utilities and consumers, promote efficiency and rapid

_____________________________________________________________________________ Engineering Staff College of India Page No.1.5

reduction of system losses. It would serve public interest through economic efficiency and improved service quality. It would also bring greater predictability to consumer tariffs by restricting tariff changes to known indicators such as power purchase prices and inflation indices. Private sector participation in distribution needs to be encouraged for achieving the requisite reduction in distribution losses and improving the quality of service to the consumers. 1.3.5 The Electricity Act 2003 enables competing generating companies and trading licensees, besides the area distribution licensees, to sell electricity to consumers when open access in distribution is introduced by the State Electricity Regulatory Commissions. As required by the Act, the SERCs shall notify regulations by June 2005 that would enable open access to distribution networks in terms of sub-section 2 of section 42 which stipulates that such open access would be allowed, not later than five years from 27th January 2004 to consumers who require a supply of electricity where the maximum power to be made available at any time exceeds one mega watt. Section 49 of the Act provides that such consumers who have been allowed open access under section 42 may enter into agreement with any person for supply of electricity on such terms and conditions, including tariff, as may be agreed upon by them. While making regulations for open access in distribution, the SERCs will also determine wheeling charges and cross-subsidy surcharge as required under section 42 of the Act. 1.3.6 A time-bound programme should be drawn up by the State Electricity Regulatory Commissions (SERC) for segregation of technical and commercial losses through energy audits. Energy accounting and declaration of its results in each defined unit, as determined by SERCs, should be mandatory not later than March 2007. An action plan for reduction of the losses with adequate investments and suitable improvements in governance should be drawn up. Standards for reliability and quality of supply as well as for loss levels shall also be specified, from time to time, so as to bring these in line with international practices by year 2012. 1.3.7 One of the key provisions of the Act on competition in distribution is the concept of multiple licensees in the same area of supply through their independent distribution systems. State Governments have full flexibility in carving out distribution zones while restructuring the Government utilities. For grant of second and subsequent distribution licence within the area of an incumbent distribution licensee, a revenue district, a Municipal Council for a smaller urban area or a Municipal Corporation for a larger urban area as defined in the Article 243(Q) of Constitution of India (74th Amendment) may be considered as the minimum area. The Government of India would notify within three months, the requirements for compliance by applicant for second and subsequent distribution licence as envisaged in Section 14 of the Act. With a view to provide benefits of competition to all section of consumers, the second and subsequent licensee for distribution in the same area shall have obligation to supply to all consumers in accordance with provisions of section 43 of the Electricity Act 2003. The SERCs are required to regulate the tariff including connection charges to be recovered by a distribution licensee under the provisions of the Act. This will ensure that second distribution licensee does not resort to cherry picking by demanding unreasonable connection charges from consumers.

_____________________________________________________________________________ Engineering Staff College of India Page No.1.6

1.3.8 The Act mandates supply of electricity through a correct meter within a stipulated period. The Authority should develop regulations as required under Section 55 of the Act within three months. 1.3.9 The Act requires all consumers to be metered within two years. The SERCs may obtain from the Distribution Licensees their metering plans, approve these, and monitor the same. The SERCs should encourage use of pre-paid meters. In the first instance, TOD meters for large consumers with a minimum load of one MVA are also to be encouraged. The SERCs should also put in place independent third-party meter testing arrangements. 1.3.10 Modern information technology systems may be implemented by the utilities on a priority basis, after considering cost and benefits, to facilitate creation of network information and customer data base which will help in management of load, improvement in quality, detection of theft and tampering, customer information and prompt and correct billing and collection . Special emphasis should be placed on consumer indexing and mapping in a time bound manner. Support is being provided for information technology based systems under the Accelerated Power Development and Reforms Programme (APDRP). 1.3.11 High Voltage Distribution System is an effective method for reduction of technical losses, prevention of theft, improved voltage profile and better consumer service. It should be promoted to reduce LT/HT ratio keeping in view the techno economic considerations. 1.3.12 SCADA and data management systems are useful for efficient working of Distribution Systems. A time bound programme for implementation of SCADA and data management system should be obtained from Distribution Licensees and approved by the SERCs keeping in view the techno economic considerations. Efforts should be made to install substation automation equipment in a phased manner. 1.3.13 The Act has provided for stringent measures against theft of electricity. The States and distribution utilities should ensure effective implementation of these provisions. The State Governments may set up Special Courts as envisaged in Section 153 of the Act. 1.3.14 In the light of above electricity policy, the present regulatory course book will provide the concepts of distribution sector regulations and framework for development of electricity market in India.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.1

Section – 2 Learning Objectives:

a) Economic and social rationale for regulation b) Monopolistic competition c) Legal monopoly d) Understanding marginal cost development

2.0 Economic, Legal and Social Rationale for Electricity Distribution Regulation The Distribution of Electricity or the wire business being a natural monopoly has to be regulated for maximizing the efficiency of operation and economies of scale benefit to the society. The resources of the society can be properly utilized through a legally created regulated entity. Such entity has to be regulated only through an independent regulatory body. This system of regulatory governance of electricity distribution has Economic, Legal and Social Rationale (to be regulated than to be left to competitive market forces) which is being explained in the following paragraphs. Mathematical and other illustrative examples have been quoted from the body of economic literature wherever felt necessary. 2.0.1 The economists have been arguing in favor of regulating the natural monopolies in public utility services. They have established the economic rationale for such regulation in the literature of economics. 2.0.2 The legal and social rationale has also been established by Public Utility (regulatory authorities) Commissions, in almost all States throughout the United States of America, while pricing the various services, such as transmission, distribution, and wheeling of electricity, water, natural gas (including piped gas supply), telecommunications, and transportation services, etc. provided by such monopolist utilities. 2.0.3 The utilities industry is a good example of a natural monopoly. The costs of establishing a means to produce power and supply it, to each household or any other consumer, can be very large. This capital cost is a strong deterrent for possible competitors. Additionally, society can benefit from having natural monopolies because having multiple firms operating in such an industry is economically inefficient. 2.0.4 The regulation of distribution business, of which the main base consisted of threats from the introduction of a regulatory authority and potential competitors, was supported by mandatory information disclosures to identify possible excess profits by lines businesses and thus curbing the monopolistic behavior via self-regulation. Using the data in these information disclosures, it is found that price minus cost margins have increased rather than decreased significantly during the implementation of such regulation. Furthermore, this price minus cost margin can be attributed to the revaluation of fixed assets by network operators. 2.0.5 Throughout the economic literature, the need for regulation of natural monopolies is well documented and well understood. In accordance with the need for regulation, economists have put forward an extensive set of principles for regulating natural

_____________________________________________________________________________ Engineering Staff College of India Page No.2.2

monopoly suppliers. In practice, in many countries around the world, regulatory bodies have come up with different regulatory designs to overcome the problems brought about by the existence of natural monopolies. These regulatory designs can be classified under two main titles. On one side, there is heavy-handed regulation maintaining that the regulatory authority has a strong control over the natural monopoly and proceeds with stronger regulatory surveillance. 2.0.6 Being the traditional stream in economic literature, heavy-handed regulation explores the different ways through which regulatory authorities adopting a hands-on approach intervene in natural monopolies’ industrial operations. On the other side, there is light-handed regulation, which holds that actual regulation is conducted only if the natural monopoly is determined to have exerted its market power or triggered some kind of market failure. Besides, in order to prevent the natural monopoly from abusing its market power, different types of “threat” can be employed in light-handed regulation. Therefore, light-handed regulation is also seen as threat-based regulation. 2.0.7 There is, therefore, a sharp ideological difference between these two schools of thought. On the one hand, heavy-handed regulation implicitly assumes the natural monopoly will not act on socially efficient unless it has been regulated by a regulatory body adopting a hands-on approach. On the other hand, light-handed regulation assumes that through transparency and credible regulatory or other threats, a natural monopoly will behave competitively. 2.1 Economic and Social Rationale for Regulation of Natural Monopoly 2.1.1 The phenomena of natural monopolies and their regulation pose a dilemma that has perplexed and intrigued economists for many years. On the one hand, economic theory teaches that in the industries characterized by intensive economies of scale there should only be one single firm because of efficiency requirements. But on the other side, the uniqueness of the firm gives it power such that it could have an impact on social welfare. The dilemma is intensified by the suggestions of different natural monopoly definitions. 2.1.2 The concept of natural monopoly is generally perceived as a market in which competition is not possible. Alternatively, the term may also refer to the undesirability of competition rather than its possibility. It is crucial to make a distinction between employing natural monopoly in the positive form and employing it in the normative form. In the positive sense, it is predicted that there will only be one single firm in the industry. When employed normatively, a natural monopoly refers to an industry where the average cost of production in the industry is minimized only if there is a single producer. 2.1.3 According to Joskow (2007: 8) a firm producing a single homogeneous product is defined to be a natural monopoly when it is less costly to produce any level of output of this product by a single firm than with two or more firms. A crucial assumption for the validity of this definition is that this “cost dominance” relationship must hold over the full range of market demand for this product Q = D(P), where Q is the quantity produced and D is the demand at price p . 2.1.4 To illustrate this mathematically, consider a market for a homogenous product where each of k firms produces output qi and total output is given by

_____________________________________________________________________________ Engineering Staff College of India Page No.2.3

Each firm has an identical cost function C (qi). According to the technological or cost-based definition of natural monopoly, a natural monopoly will exist when:

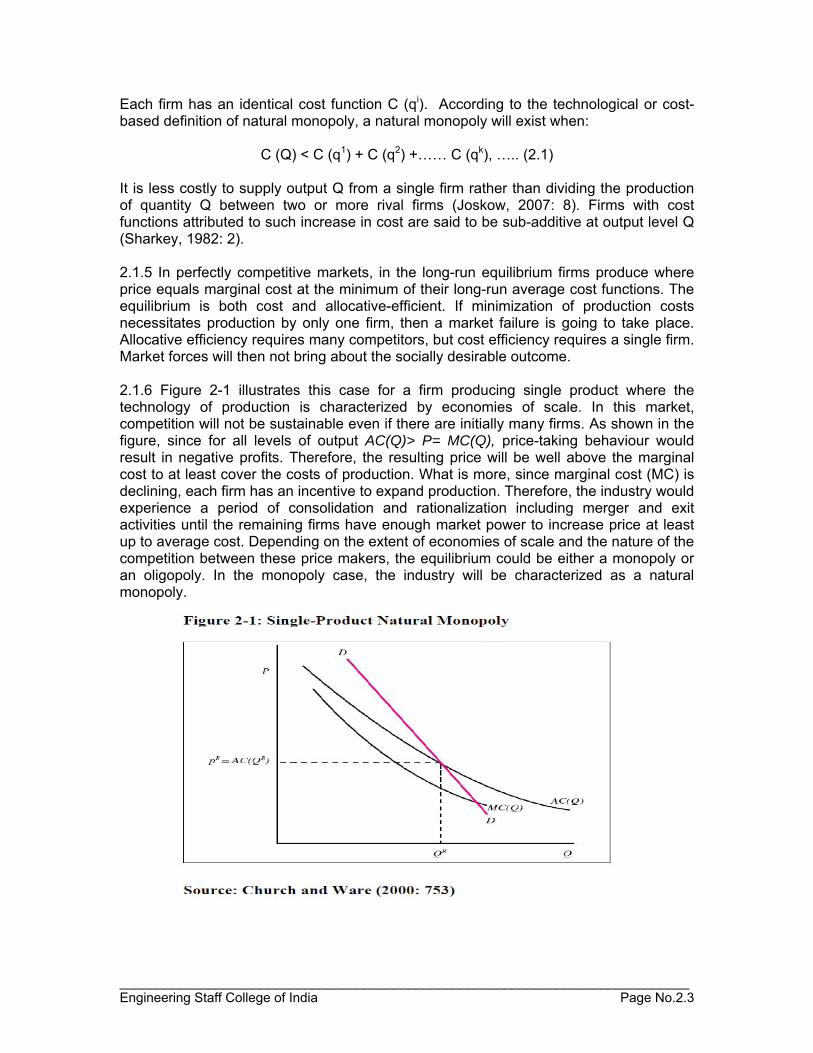

C (Q) < C (q1) + C (q2) +…… C (qk), ….. (2.1) It is less costly to supply output Q from a single firm rather than dividing the production of quantity Q between two or more rival firms (Joskow, 2007: 8). Firms with cost functions attributed to such increase in cost are said to be sub-additive at output level Q (Sharkey, 1982: 2). 2.1.5 In perfectly competitive markets, in the long-run equilibrium firms produce where price equals marginal cost at the minimum of their long-run average cost functions. The equilibrium is both cost and allocative-efficient. If minimization of production costs necessitates production by only one firm, then a market failure is going to take place. Allocative efficiency requires many competitors, but cost efficiency requires a single firm. Market forces will then not bring about the socially desirable outcome. 2.1.6 Figure 2-1 illustrates this case for a firm producing single product where the technology of production is characterized by economies of scale. In this market, competition will not be sustainable even if there are initially many firms. As shown in the figure, since for all levels of output AC(Q)> P= MC(Q), price-taking behaviour would result in negative profits. Therefore, the resulting price will be well above the marginal cost to at least cover the costs of production. What is more, since marginal cost (MC) is declining, each firm has an incentive to expand production. Therefore, the industry would experience a period of consolidation and rationalization including merger and exit activities until the remaining firms have enough market power to increase price at least up to average cost. Depending on the extent of economies of scale and the nature of the competition between these price makers, the equilibrium could be either a monopoly or an oligopoly. In the monopoly case, the industry will be characterized as a natural monopoly.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.4

2.1.7 The determination of whether an industry is a natural monopoly is contingent upon the interaction of technology and demand. If production costs are minimized at all levels of market demand when there is only one firm, then there is justification to regulate with entry controls. Forestalling competitors’ entry to the industry will ensure that industry costs are to be minimized. Therefore, if the industry is a natural monopoly, entry by more than one firm will be inefficient. However, the imposition of entry controls needs to be accompanied by additional regulations since it creates a monopoly. De jure, some sort of regulation is required to avoid the allocative inefficiency associated with monopoly pricing. 2.1.8 Beyond what has been said, there will be a trade-off in the determination of the optimal governance alternative. The unregulated-market outcome will include market power and/or cost inefficiency at the industry level. The regulated-market outcome will be a potential Pareto improvement as long as the assumption of perfect regulation is valid. However, regulation is likely to be imperfect since the regulator will not have perfect information and any regulatory mechanism will not fully align the objectives of the society and firm. Hence the choice of the governance instrument will be between imperfect markets and imperfect regulation (Church and Ware, 2000: 760). 2.1.9 In sum, the need for imposing price and entry regulations in industries where suppliers are thought to have natural monopoly characteristics emerges from the fact that (a) industries having natural monopoly characteristics will perform poorly in a number of economic aspects and, (b) it is feasible in theory and practice for authorities to impose entry and related regulations in such ways that would improve the natural monopoly’s performance compared to the economic performance that would otherwise be associated with the unregulated case (Joskow, 2007: 34). 2.2 Legal and Social Rationale for Distribution Regulation 2.2.1 Definition of 'Monopolist' A person, group or organization with a monopoly. In other words, an individual or company that controls all of the market for a particular good or service. 2.2.2 Investopedia explains 'Monopolist' A monopolist probably also believes in policies that favor monopolies since it gives them greater power. A monopolist has little incentive to improve their product because customers have no alternatives. Instead, their motivation is focused on protecting the monopoly. 2.2.3 Definition of 'Monopolistic Competition' A type of competition within an industry where: 1. All firms produce similar yet not perfectly substitutable products. 2. All firms are able to enter the industry if the profits are attractive. 3. All firms are profit maximizers. 4. All firms have some market power, which means none are price takers. 2.2.4 Investopedia explains 'Monopolistic Competition' Monopolistic competition differs from perfect competition in that production does not take place at the lowest possible cost. Because of this, firms are left with excess production

_____________________________________________________________________________ Engineering Staff College of India Page No.2.5

capacity. This market concept was developed by Chamberlin (USA) and Robinson (Great Britain). 2.2.5 In the case of electricity distribution, if two licensees operate with separate distribution system, overhead lines or cables, with associated transformers and control gears, in the same area of supply, then the average cost per unit of power distributed shall be higher than the case where one distribution company operates and distributes the power with optimum efficiency. Hence, monopolistic competition leads to social dead weight loss of resources. 2.2.6 Definition of 'Legal Monopoly' A company that is operating as a monopoly under a government mandate. A legal monopoly offers a specific product or service at a regulated price and can either be independently run and government regulated, or government run and regulated. Also known as a "statutory monopoly". 2.2.7 Investopedia explains 'Legal Monopoly' A legal monopoly is set up in the beginning as a perceived best option for both government and its citizens. For example, AT&T operated as a legal monopoly until 1982 because it was deemed vital to have cheap and reliable service for everyone. Railroads and airlines have also been operated as legal monopolies at different periods in history. In most cases, capitalism has won out over legal monopolies as technology and the economy have become more advanced. 2.2.8 In most countries of the world, the electricity distribution was working as a government regulated utility till the recent reforms and restructuring of 1990s’ took place at the behest of World Bank. The legal rationale behind distribution regulation was directed towards disciplining the monopolistic network companies under strict enactments of laws, rules and regulations, under which the monopolist behavior of such network companies can be conditioned in such a way that the independent regulator imitates the behavior of market conditions and imposes such conditions so as to achieve results of pricing for consumers, similar to competitive markets without establishing any 'Monopolistic Competition'. 2.3 Introduction to Regulatory Economics and Marginal Cost Development 2.3.1 Regulatory Economics development in theory Two decades ago regulatory economics had just completed some major strides. In part, this had been as a result of a major investment made in economics by the Bell System. Notable in this was the founding in the spring of 1970 of The Bell Journal of Economics and Management Science, which became the Bell Journal of Economics in the spring of 1975 which begat the Rand Journal in the spring of 1984, immediately following the Divestiture. AT&T apparently saw no significant benefit in continuing its major effort in regulatory economics, which had ostensibly been a costly failure memorialized in the Divestiture. The divestiture of the Bell Journal to Rand and the gutting of its premier economics group at Bell Labs might be seen as two casualties in the failure of some outstanding economic brainpower and innovative research to carry the day for Bell. 2.3.2 In many ways the research of the 70s and 80s was inspired in a significant way by the resources ploughed into microeconomics by AT&T. Take the Bell Journal.3 Money appeared to be no object. As two young faculty in the 70s, when young faculty in

_____________________________________________________________________________ Engineering Staff College of India Page No.2.6

business schools were paid significantly less in real terms, we were impressed to receive what appeared to be princely sums for refereeing, not to mention the additional fees paid to us for our 1976 article on peak-load pricing. The Bell Journal had no difficulty attracting extremely talented editors and contributors including already distinguished scholars like William Baumol, Walter Oi, Richard Posner, George Stigler, William Vickrey, Oliver Williamson, and others. Perhaps even more important was that the Bell Journal attracted many young economists, such as Elizabeth Bailey, John Panzar, Robert Willig, and David Sibley, whose work in the 70s and 80s played a major role in the evolution of regulatory economics. Together the visibility of regulated industries and the quality of the researchers involved made regulatory economics the most important subspecialty of industrial organization.

2.3.3 Before the founding of the Bell Journal regulatory economics was extremely undeveloped. There was the seminal work of Averch and Johnson (1962),4 the marginal cost pricing debate for monopolies of the 40s and 50s, which itself became specialized into the peak-load pricing debate through the work of Boiteux (1949), Steiner (1957) and Williamson (1968). These contributions all provided the context for the research that the Bell Journal fostered in the 70s. Peak-load pricing in the early 80s was extremely well developed in theory. Ramsey pricing was given a new lease on life by Baumol and Bradford (1970), the Bell Labs economists, including Rohlfs (1979), and others including Sherman and George (1979), and continues as a source both theoretical and practical inspiration for analyzing and designing regulatory institutions. 2.3.4 All of these developments were outgrowths of already established theory. However, the theory of contestable markets, due primarily to Baumol, Panzar and Willig (1982) and some related development, which began in the 70s, did not have such roots. They were original in a way that the other developments were not. They also lacked the pedigree of the other developments and were for that reason less constrained. Perhaps for this reason the authors of contestability had very high hopes for the impact of their work.5 Despite its detractors, some of whom admit its importance, the work has become one of the landmarks in regulatory economics. Even a leading detractor states: “The major part of the analysis of it is an analysis of multiple products and joint costs, which is already gaining wide acceptance” (Shepherd 1984, p572). Indeed, their analysis of issues of costs, multiproduct pricing and cross subsidy has had and continues to have a major impact on the discipline. As a result of this work cross subsidy is well defined in terms of the burden test – a cross subsidy does not occur if the revenue from a product is between its incremental cost and its stand-alone costs. 2.3.5 Around the mid 80s a change took place in the theoretical regulatory economic and this was the incorporation of the principal-agent theory, mechanism design theory and information economics into regulatory economics. This began with the work of Baron and Myerson (1982). The work was an outgrowth of the work on principal-agent theory in the 1970s (e.g., Ross (1973) and Groves (1973), which, indeed, offered major insights into issue of corporate governance. The problem is, as we noted in Crew and Kleindorfer (1986) that its insights have little to offer when carried over into designing institutions or

3 Henceforth we will not distinguish between the two appellations but will use this term to refer to either The Bell Journal of Economics and Management Science or the Bell Journal of Economics. 4 We intentionally use the word seminal to describe A-J. Although many authors have sought to discredit this paper it is one of the most highly cited and influential papers in regulatory economics.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.7

mechanisms that can be applied to regulatory problems, as they exist in practice. This is not the view of theorists in this area. Indeed, the work of Baron and Myerson spawned a new industry in regulatory economics, the culmination of which can be found in the treatise by Laffont and Tirole (1994). 2.3.6 Theorists employing this “new” approach were highly critical of the earlier work, which they perceived as having little value as it missed the critical problem of incentives. This can be noted in the work of Laffont and Tirole (1993). “In the policy arena discontent was expressed with the price, quality, and cost performance of regulated firms and government contractors…More powerful incentive schemes were proposed and implemented, deregulation was encouraged… [but] regulation theory largely ignored incentive issues.” (Laffont and Tirole 1993, xvi) Previous regulatory theory, they argued, “…did not meet the standards of newly developed principal-agent theory, whose aim is to highlight the information limitations that impair agency relationships. Furthermore the considerably simplified formal models that assumed away imperfect information were less realistic in that they implied policy recommendations that require information not available to regulators in practice.” While we accept that these criticisms certainly have some validity, we argue that the contributions that replaced them were at least as limited in their applicability and fell far short of the expectations created by their authors. Ironically, a principal reason for this is precisely the reason raised above by Laffont and Tirole in ushering in the new theory, namely, a heavy reliance by such schemes on information that is not available to regulators. 2.3.7. Indeed, the entire mechanism design literature, beginning with Baron and Myerson (1981) and strongly promoted by Laffont and Tirole, is based in one way or another on assumptions like common knowledge that endow the regulator with information that he cannot have without a contested discovery process that always leaves him in a state far short of the level of information assumed in these theories. Common knowledge is the Achilles heel of mechanism design theory.6 Why is it that extending the traditional principal-agent theory to regulatory economics is so problematical? When a principal and agent are involved in a private transaction, there is not a fundamental problem with the principal designing incentive systems for the agent based on an assumed “common knowledge” by the principal about the agent’s costs or preferences. In private transactions, the principal bears the costs of any error in his assumptions7 Contrast this with a regulator with responsibility for the price and quality of an essential good. If the regulator is wrong in his common knowledge assumptions about the agent (the regulated firm), it is consumers or the regulated firm that bear the consequences. The anticipation of these consequences will clearly give rise to strategic interactions, both in theory and practice that may have fundamental effects on what common knowledge assumptions are legitimate, and on the ultimate consequences of these for the outcomes of regulation.

5 They were rebuked by Shepherd (1984, p572) “a new theory of industrial organization” which “will transform the field…” (Baumol, Panzar and Willig, 1982, xiii). Shepherd failed to note that these were the words of Elizabeth Bailey in the Foreword

_____________________________________________________________________________ Engineering Staff College of India Page No.2.8

2.3.8 Theories that fail to address these strategic interactions leave a gaping hole in interpreting the results of any such theory. In particular, lifting the common knowledge assumption from a private principal agent framework to the regulatory context leads to major problems because it leaves open how this common knowledge distribution will be determined. Note that in the traditional principal-agent theory the contracting agent is free to take or leave the principal’s offer (which must therefore satisfy an individual rationality constraint), but under regulation this does not apply in the case of the firm which may have considerable sunk costs at risk and cannot simply pull up stakes if the firm does not find the regulator’s assumptions acceptable. 2.3.9 The promise of these mechanism-design-style theories was ostensibly considerable. They promised none other than the holy grail of X-efficiency, something previous regulation had manifestly failed to deliver. X-efficiency, however, was only achieved if two conditions - aside from the basic assumptions criticized above – were met. The first condition was that achievement of the promised X-efficiency required that the regulator concede some information rents to the firm.8 The second condition was what is referred to in mechanism design theory as commitment. This is the notion that the presence of information rents would not present a problem to the regulator and that, as a result, he was committed to his original agreement with the firm. In other words, the ex post appearance of excess profits would not cause the regulator to renege on his commitment to the original incentive scheme. Why this would not be a fatal flaw in the whole scheme was never considered. The new theory promised efficiency as long as the regulator is prepared to allow information rents. Theorists, however, never understood the impossibility of this in practice. No regulator can even admit that it allows the firm to retain information rents let alone commit to such a practice. For the regulator this is a congenital problem of far greater magnitude than has been recognized in economic theory.9,10 How do these rents differ so much from the old style monopoly rents that would make them acceptable to the regulator when it was monopoly rents that were the principal motivation of regulation in the first place? Thus, the promise of X-efficiency was hedged with conditions, which, we argue, make the theory of little significance for real world regulation, as subsequent events have shown.

6 By “common knowledge”, we are referring to the standard assumption of much of the mechanism design literature that the regulated firm actively reveals its type (e.g., its cost or other key parameters), knowing that the regulator will set regulatory parameters (e.g., the allowed rate of return in cost-of-service regulation or the X factor in price-cap regulation) based on the revealed type of the firm. The common knowledge assumption presumes that the regulator and the firm take as incontestable knowledge the probability distribution of possible revealed types, with regulatory design contingent on this common knowledge distribution. We include in our broad criticism of this assumption also weaker forms of this that allow the regulator to simply declare ex ante the distribution of revealed types, whether or not the regulated firm agrees to it. Any such declaration, unless agreed to by the regulated firm, can and would be contested, since different assumptions about this distribution naturally lead to different regulatory incentive systems under the standard Bayesian Incentive Bargaining approaches used in this literature. To put it plainly, the regulated firm definitely cares about what the regulator claims to be the actual distribution of potential types and would attempt to influence the accepted definition of this distribution if it were a central aspect of regulatory design. If such a distribution is a central feature of a design problem, a theory that simply takes it as a given, without modeling the process that would accompany its adversarial determination, is fundamentally flawed. 7 In particular, the models and applications in Laffont and Tirole (1993) that treat private procurement contracts remain significant contributions to the literature of contracting.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.9

2.3.10 Of course, all theory makes simplifying assumptions, which depart from reality in one way or another. The key, at least for normative economic models, is that the assumptions made should not give rise to fundamental infeasibilities when implementing the results of the theory in practice. An apparent case in which this has not been true is the case of regulatory theory derived from the mechanism design literature. In effect, the theory proceeds by ignoring an immutable institutional constraint, namely that neither commitment nor its associated information rents are reasonable assumptions. Other than being a rich source of classroom exercises, this theory seems to have found no takers in practice. A consideration for the reasons underlying this failure may provide useful insights for the future innovations needed in development and application of regulatory theory. While we admire the elegance of the theory of mechanism design applied to regulation, we conclude that it may have led to some misleading policy implications and that overall its contribution is small. In its defense does provide insights into the role of information as a source of monopoly rents, which is a potentially valuable insight. 2.3.11 Another major development in economic theory over the last twenty years has been the progress made in auction and bidding theory and in experimental economics. Auctions and bidding have been applied extensively in regulatory applications as illustrated in the two special issues of JRE in May and July 2000 (see Salant 2000). Although economists now have a much better understanding of auctions and bidding, the applications have not been without their problems as the California electricity generation market illustrates. 2.3.12 However, unlike the mechanism design literature, the bidding, auctions and experimental economics literature offers considerable potential in regulatory economics. These innovations do not mean that franchise bidding along the lines of Demsetz (1968) is going to replace traditional regulation or that bidding will result in radical changes in regulation. They do, however, provided regulatory economists with some powerful tools, which may result in a number of promising applications. 2.3.13 Twenty years ago, concerns over access pricing were a practical issue in telecommunications. With the Divestiture these concerns increased significantly. However, theoretical contributions to address the problem of access pricing came later. 2.3.14 Access to an essential or bottleneck facility is the issue. The problem is compounded when the owner of the essential facility is also selling to final consumers in competition with the other firms. An example would be long distance telephone companies purchasing access from local phone companies to complete their calls. The local companies themselves might be also providing long distance service. This is the case, for example, with British Telecom, and a few jurisdictions for RBOCs. The efficient component pricing rule (ECPR) was one of the first attempts by economists to address

8 These rents arose from the information advantages of the firm relative to the regulator. 9 Loeb and Magat (1979), and Vogelsang and Finsinger (1979) implicitly rely on this same notion of commitment. 10 In Crew and Kleindorfer (2001) we recognize the importance of commitment and its effect on incentives and analyze the constraints on regulatory commitment.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.10

the issue of efficient access pricing. Among the leading exponents of ECPR are Baumol and Sidak (1994).11 The idea of ECPR can be summarized as in Baumol and Sidak (1994, p178): Optimal input price = the input’s direct per-unit incremental cost + the opportunity cost to the input supplied of the sale of a unit of input.

2.3.15 The problem with ECPR arises from the second term on the right-hand side. If this could be determined on the basis of a readily observable price in a competitive market, then ECPR would be an efficient rule. However, it is precisely because of the bottleneck facility that such a competitive price cannot be determined. ECPR then comes down to allowing the bottleneck supplier the monopoly rents that he was earning when he was the only vertical integrated monopolist. As most monopolists are regulated, this presumably comes down to allowing him the regulated return that he would have obtained. The application of ECPR can be illustrated by means of the following simple illustrative example. 2.3.16 If there are two homogeneous products x1 and x2 each having two production stages: - MCij = Marginal Cost of product i in stage j We assume for simplicity that MC11 = MC21 = 8 and MC12 = MC22 =2 and stage 1 is the “access” input for each product. 2.3.17 Ramsey markups of 1.5 and 1.25 are applied to give prices of 15 and 12.5 for product 1 and 2 respectively. If the regulated monopolist has a monopoly in market 1 then ECPR would imply that entrants would be charged 10.5 for the access input. If he has cost lower than 2, he can undercut the monopolist in market 2 and take this market from the monopolist. 2.3.18 Most access pricing problems encountered in the real world are much more complicated than this. For example, products are differentiated and one of the products does not necessarily remain a robust monopoly. Thus, it may be possible to undercut the incumbent in the monopoly market thereby undermining the incumbent’s financial viability. In the area of access pricing it is apparent that significant progress has been made in understanding some of the complexities involved and in developing solutions to the problem. A particularly promising approach seems to be what Laffont and Tirole (1996) have referred to as “global price caps.”12 The idea is intriguingly simple aiming to avoid some of the complexities and information. Access is treated as a final good rather than as an intermediate good and is included in the computation of the price cap. 2.3.19 In addition, “Weights used in the computation of the price cap are exogenously determined and are proportional to the forecast quantities of the associated goods.” (Laffont and Tirole, 1996, p243). Laffont and Tirole explore the possibilities of forming a hybrid of ECPR and global price caps, which may offer benefits in terms of weight setting and protection against anti-competitive practices. Such a hybrid approach may provide a means of achieving a transition to the global price cap, which has considerable advantages summarized by Laffont and Tirole (1996, p254) as “A global price cap

11 The idea seems to have originated over twenty years ago in Willig (1979).

_____________________________________________________________________________ Engineering Staff College of India Page No.2.11

restricts increases in both access prices and final prices and induces the [regulated firm] to price discriminate very much the way an unregulated firm would do, except that the entire price structure is brought down by the cap.” 2.3.20 While significant progress in the theory of access pricing has been made, a considerable amount of further development is required particularly if it is going to contribute to the practical policy debate, which is the subject of the next section. Interest continues in access pricing as illustrated by Armstrong’s (forthcoming) tour de force on access pricing and interconnection. Many problems remain, some of which are addressed by Armstrong, including two way interconnection – an important problem for Internet service providers. Other issues include structural separation of access from the rest of the business and divestiture of access monopolies. Finally, access pricing is part of a much larger problem of the role and obligations of incumbent network industries under deregulation to which we will now turn briefly. 2.3.21 Microeconomic theory over the last twenty years has supported deregulation. However, it has done so in a piecemeal fashion. Consideration of the impact of entry on the obligations of incumbents has left much to be desired. Incumbents have as regulated monopolists faced universal service obligations (USO), default service provider obligations and have been the vehicle for the propagation of many subsidies. While the understanding of the nature of such obligations has been the subject of considerable study, for example, the USO in the postal sector as illustrated in Crew and Kleindorfer (1999,2001a, 2001b), the bigger picture of the impact and nature of deregulation is still undeveloped as will be illustrated in the next section. For example, a major problem exists in linking notions of access pricing to the problem of funding universal or default service obligations. 2.3.22 Addressing the default service obligation is arguably one of the most difficult problems faced in regulatory economics.13 A price cap for a distribution utility with a default service obligation creates a certain dissonance. Is the energy purchased treated as a simple pass through with this component of the bill varying with the purchases in the spot market? Or is the distribution utility required to line up long-term contracts to provide guaranteed prices? In either case the default service provider is on to a losing proposition. If it insists on only making purchases in the spot or short-term market and is allowed a straight pass through the value to consumers of the default service obligation is minimal since they are absorbing all the risks. If the distribution company sets up long term contracts to guarantee prices then if prices fall it loses customers and is stuck with high priced long term contracts, which will prove costly to it under a price cap. 2.3.23 Competition in such markets is very difficult to achieve when distortions like the default service obligation are included. The problem is not well understood and awaits a workable solution. Marginal Cost Development

12 The term is an excellent one. Crew and Kleindorfer (1994) proposed the same basic idea but unfortunately not the term. Laffont and Tirole (1994) first floated the idea. 13 We argue below that this is at the heart of the California electricity crisis. This is a current problem. A long-standing problem of arguably equal importance is the problem of auto insurance in New Jersey, which originated over twenty years ago and shows little sign of being resolved. See Worrall (2001).

_____________________________________________________________________________ Engineering Staff College of India Page No.2.12

2.3.24 Marginal cost is defined as the change in total cost that results from a very small change (increase or decrease) in output. In the standard textbook explanation, marginal cost is the derivative of the total cost curve at a given level of output, or, literally, the change in total cost that results from an infinitely small change in output. As we use the term in the electric utility industry, the concept is more complex than the simple textbook examples. The “output” is a service with many dimensions including time-of-use, voltage level and geographic area. There are also several concepts of the marginal cost of electric service, including short-run (the cost of increasing output with existing capacity), long-term (the pattern of short-run marginal costs, usually averaged over a specified period) and long-run (the cost of increasing output from an optimal system). 2.3.25 This chapter describes the process of developing marginal costs which are considered in setting retail electric rates and making suggestions for improving the efficiency and equity of the marginal cost price signals in the rates charged by electric utilities. Marginal cost study – theory: Marginal Cost Study was first done in USA utilities in a Nation wide survey conducted by NERA Inc., a leading economic research consultants. They adopted the formats of Federal Electricity Regulatory Commission (FERC) of USA for collection of data and other information required for the study to assess the implementation of marginal cost principles by US utilities. The following paragraphs describe in brief the ‘Marginal Cost Theory’ and the process of marginal cost development for utility. Marginal Cost Theory DEFINITION: Marginal Cost = Change in Total Cost from a Small Change in Load Traditional

Arguments for Marginal Cost Pricing

Economic Efficiency Good Business Sense PURPA (USA)

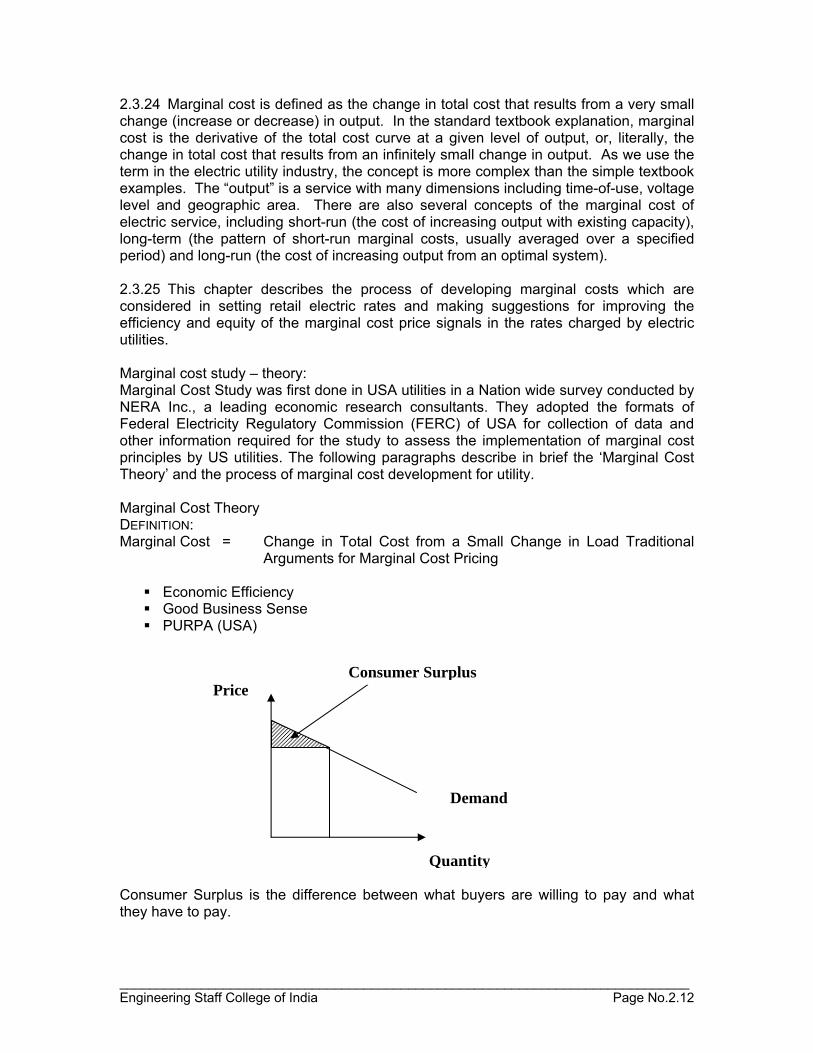

Consumer Surplus is the difference between what buyers are willing to pay and what they have to pay.

Consumer Surplus

Demand

Quantity

Price

_____________________________________________________________________________ Engineering Staff College of India Page No.2.13

Pricing above marginal cost results in a deadweight loss of consumer surplus Pricing below marginal cost results in wasted resources because the cost of producing some units exceeds their value to consumers. CRITICISMS OF MARGINAL COST PRICING

Short-Run or Long-Run Second Best Arguments Income Distribution Revenue Gap

Loss of Consumer Surplus (Deadweight Loss)

Marginal Cost

D

Q1 Quantity

Price and Cost

P1

Loss to Society

Marginal Cost

Demand

Quantity Q2

P2

Price

_____________________________________________________________________________ Engineering Staff College of India Page No.2.14

Judgment Required Equity Revenue Stability

MARGINAL COST COMPONENTS

Marginal Customer “Required Facility” Costs Marginal Energy Costs Marginal Capacity Costs

2.4 Examples to Illustrate the Concept of Economic, Legal and Social Aspects of Electricity Distribution: 2.4.1 Economics of Electricity Access Benefits of Access. It is widely accepted that the provision of electricity enhances the household’s quality of life and stimulates the economy in a broader sense. One immediate benefit is improved lighting. Electrification also improves the quality of health services and spurs income-generating activities by enabling the use of irrigation pumps and other economic activities. That is, rural electrification can generate sufficient benefits for the investment to be warranted from an economic standpoint (IEG 2008). Households’ willingness to pay for electricity is directly associated with the costs that they would avoid from more expensive energy sources (e.g., kerosene, dry cells) and their awareness of potential income gains. There are several illustrations of this willingness to pay: In Bangladesh, where rural residential tariffs start at $0.05/kWh for monthly consumption up to 300 kWh, field research concluded that 49 percent of rural consumers would be willing to pay up to 25 percent more for electricity, and 7.9 percent would pay 10 percent more (Barnes 2007). In Guatemala, monthly consumption of 30 kWh at a social rate of $0.09/kWh would translate to monthly expenditure of $4.00, which represents 8 percent of the average rural household income. Households are ready to pay this price, because the alternative energy cost is approximately $5.75 per month (Mostert 2008). Consequently, consumer payment rates in Guatemala are very high. Surveys of households in Sub-Saharan Africa have shown varying levels of avoided costs and willingness to pay. In Mali, avoided costs from electricity average €16 per month. Surveys held in the country concluded that the willingness to pay for electricity in rural areas averaged €11.1/month, ranging from €8.2 to €16.7 (Mostert 2008). In Senegal, most rural households already spend $2 24 per month on kerosene and dry cell batteries to meet their lighting and small power needs, and hence are likely to be willing and able to pay for electricity use (de Gouvello et al. 2007). In Guinea, rural surveys obtaining data on avoided costs found that the willingness to pay for basic electricity services was about $1.6/month (Mostert 2008), which would cover the cost of 12 kWh per month at the average tariff of the Sub-Saharan region ($0.13/kWh). Productive uses. The promotion of, and capacity building effort to encourage, productive uses of electricity in rural areas have the potential to contribute to increasing the productivity of rural business as well as achieving a more efficient use of the electricity

_____________________________________________________________________________ Engineering Staff College of India Page No.2.15

supply infrastructure and improving the revenues of distribution companies, thereby enhancing the economics of electrification. There are, however, two important barriers to the productive use of electricity: the lack of technical knowledge and skills of potential users and the financial means to acquire relevant equipment (ESMAP 2008). In Bangladesh, the potential for productive uses by cooperatives is a key factor in increasing their revenues and meeting the requirements to qualify for electrification. Cooperatives are therefore encouraged to engage in productive uses and do so particularly in agriculture (e.g., rice mills, tube-wells). In Thailand, the Provincial Electricity Authority (PEA) was successful in promoting replacement of diesel motors with electric motors, mostly for rice mills, in villages with lower-than-expected consumption of electricity. To this end, the PEA facilitated financing for villages to purchase electric motors and other equipment. The importance of incorporating financing for productive uses into the rural electrification program was evident in Chile; absent such a financing mechanism, the economic impact of electrification was sometimes limited (Barnes 2007). Incorporating economic efficiency into the process. There are two ways of incorporating efficiency into the electrification effort: (1) establishing an effective planning process that identifies the country’s needs and electrification opportunities, taking into account the financial viability of investments and their economic impact on the region, and that establishes rational and transparent criteria for the selection and prioritization of projects; and (2) minimizing construction and operating costs. Transparent planning focused on cost-effectiveness. The cost of providing electricity to rural households is usually high, even among the best planned rural electrification programs. A transparent planning process with clear criteria designed to balance cost savings with equity considerations offers two advantages: (1) a cost-effective program and a set of rules for the selection of projects aimed at ensuring the economic and financial viability of electrification effort, and (2) protection from political interference. Failure to adopt such a process may render an electrification program unsustainable, require higher subsidies and, consequently, place undue pressure on public finances. Planning is a public role that should be led by a capable, and usually centralized, government entity. Common features of successful planning of rural electrification include (1) a clearly established system to prioritize the areas to receive electricity and the projects to be selected, (2) a long-term, multi-year vision that coordinates the extension of the grid and off-grid efforts and takes into account the manufacturing capacity of the country, and (3) a broad regional development approach that takes into account other conditions for sustainable rural development (access to education and health services, an adequate transport system, agricultural potential, access to markets). Some examples of useful experience in rural electrification planning and project selection are given below: o Thailand offers a good case of central planning for rural electrification. The PEA prepared a national plan that was sufficiently detailed to serve as a blueprint for the

_____________________________________________________________________________ Engineering Staff College of India Page No.2.16

government, the PEA, and officials responsible. The plan included guidelines and the criteria for the selection of villages to electrify, organizational requirements, etc. Since this plan was incorporated into Thailand’s Five-Year National Economic and Social Development Plan, it protected the PEA from political interference (mainly through objective selection that was formalized in this manner). While regions were selected on the basis of their level of underdevelopment and political instability, villages were selected based on economic criteria. Key factors in village selection were proximity to the grid and roads, the size of the village and the expected number of customers, potential for productive uses, the number of public infrastructure facilities, and the village’s willingness to contribute to construction costs (Barnes 2007). o One of the main characteristics of the success of the rural electrification program in Bangladesh is its centralized planning. From the outset, the REB established a clearly defined master planning process that prioritized system investment according to revenue generation. This model was used universally. The program benefited also from sustained and consistent technical assistance since its beginning and the long-term commitment of the government (Barnes 2007). o In Tunisia, the country’s regional planning processes and successive five-year plans incorporated rural electrification into broader integrated rural development objectives, producing synergistic effects. Indeed, growth in rural electrification and national socioeconomic indicators are strongly correlated. Rural electrification involved rigorous centralized planning with major regional and sub-regional inputs and initiatives. The selection criteria for rural development projects had multiple components, including income levels, unemployment, environmental quality, gender status, expected returns, and costs per job created (Barnes 2007). In practice, these criteria were complemented by incentives provided to the utility Société Tunisienne de l’Electricité et du Gaz (STEG, Tunisian Electricity and Gas Company) to select at an early stage those projects that generated more revenues (through a ceiling on the subsidy level). o The selection criteria for projects in Chile and Peru included minimization of unit costs and subsidies. This mechanism has helped reduce costs and draw contributions from local investors and communities, enabling the central government to reach an additional 30 percent of rural households using the same resources. o Good coordination between grid extension off-grid electrification is essential to avoid duplication or sub-optimal investments. Establishing criteria for comparative assessment should be part of the planning effort. Some countries have chosen practical rules of thumb to do so. For example, in Morocco, the Office National de l’Electricité (National Electricity Office) uses a cut-off cost of €2,500 per (medium- and low-voltage) household connection to choose off-grid in the place of grid extension. In Burkina Faso, the grid is extended to communities located within 50–60 kilometers from the nearest 33-kilovolt line. Ethiopia also uses a similar minimum distance criterion (Mostert 2008). Reducing costs. In many cases, careful attention to system design can enable construction costs to be reduced by up to 20–30 percent (ESMAP 2000), contributing significantly to the pace and scope of electrification programs. If electricity use is likely to be limited—for lights and small appliances, a pattern common in rural areas—there is no justification for applying the same standards as those for high-consumption urban areas. Many countries have been successful in reducing construction costs using technical

_____________________________________________________________________________ Engineering Staff College of India Page No.2.17

standards adapted to rural/low demand patterns, frequently adopting low-cost single-phase distribution systems (typically single-wire earth return, or SWER), centralized procurement processes, and/or incorporating incentives for cost reduction into open and transparent bidding. Three examples are given: o Guinea appears to be the champion of low costs. The country has adopted a radical policy that aims at maximizing the number of connections for a given amount of financial resources (Mostert 2007). Following this policy, they are achieving extremely low costs per connection in mini-grids based on diesel generation: €130 180, including all costs. While this practice implies a very short-term view that appears to be delaying the development of off-grid renewable options (which cost four to five times more per connection) and casts questions on the sustainability of the approach, it is interesting to see how far this cost-reduction strategy will go. The main aspects of the low-cost strategy of the Bureau d’Electrification Rurale Décentralisée (Office of Decentralized Rural Electrification) are (1) meeting basic needs by operating diesel grids only 4 hours a day, although longer hours of operation can be provided if there are customers using electricity for production; (2) always choosing the lowest-cost technical solution, e.g., not including meters or load limiters, cheap wooden poles even if they do not last long; (3) cost-shared training to all actors in the supply chain (consultants, construction companies, project developers); (4) monitoring prices of goods and services; (5) centralized equipment purchase; (6) keeping transaction costs low through built-in coordination of procedures; and (7) monitoring the quality of financed work and equipment. o In Thailand, the PEA followed a comprehensive strategy to reduce costs that included (1) system standardization, including technical, equipment, and other components; (2) standardization of all equipment and components used for construction of distribution systems, including a centralized procurement process and bulk purchases; (3) reliance on locally manufactured materials, which were often cheaper than imported materials; and (4) a strategy to promote electricity use that included credit lines to cover connections and wiring costs and a campaign for productive uses (Barnes 2007). o In Tunisia, STEG has fostered a cost-cutting culture that has been maintained through three decades with innovative technical options. The MALT (mise a la terre, grounding) system, a predecessor of SWER, permitted a cost reduction of 1824 percent. This was not without difficulties because, being a new technology, it faced resistance from engineers more familiar with traditional system designs. The utility monitored the process closely and solved problems as they were encountered. SWER was adopted after a few years, reducing costs even further (Barnes 2007). Another factor that helped reduce costs in Tunisia was the participation of local manufacturing industry that was supported by a specific business development program. 2.4.2 EFFECTS OF TARIFFS IN RURAL AREAS 2.4.2.1 Consumption of electricity in Rural Uganda The study was extended to rural locations with electricity so as to analyze the effects of electricity tariffs on rural areas, and the ability of rural consumers to pay. Although over 80% of the total population of Uganda resides in rural areas, only 2% of rural households have access to electricity. Nationally, less than 4.5% of the population of 24 million is connected to the power grid system.

_____________________________________________________________________________ Engineering Staff College of India Page No.2.18