Embed Size (px)

Citation preview

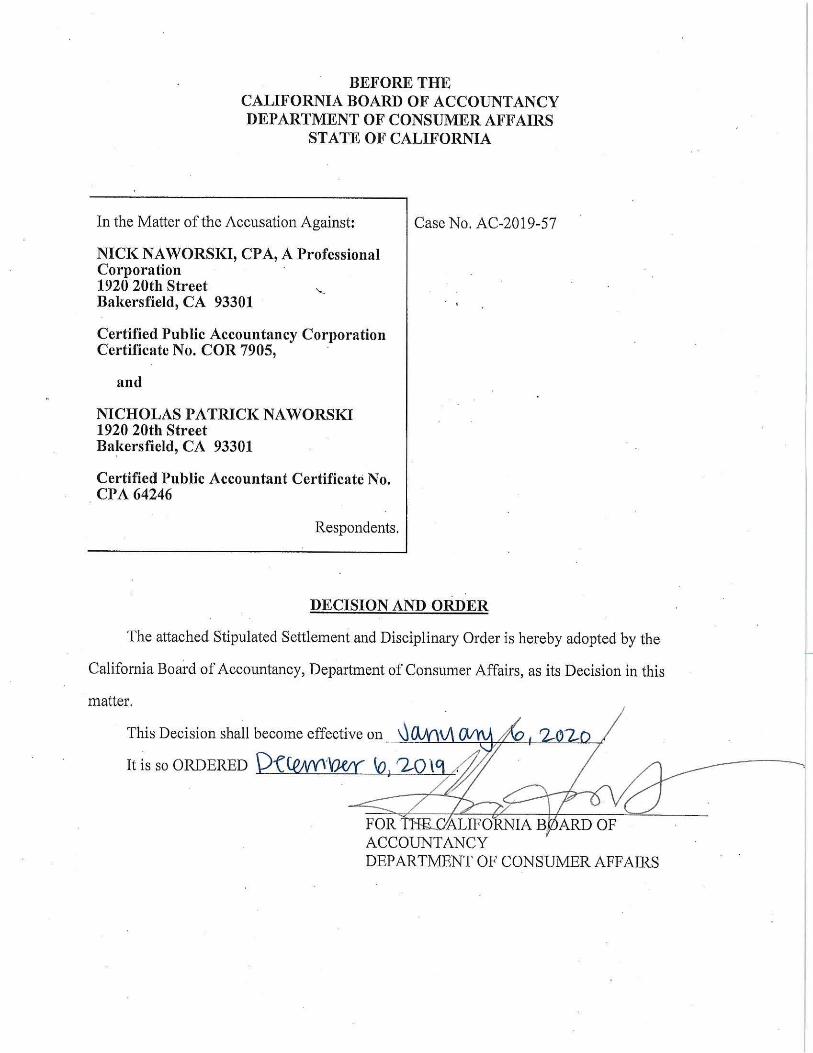

BEFORE THE CALIFORNIA BOARD OF ACCOUNTANCY DEPARTMENT OF CONSUMER AFFAIRS

STATE OF CALIFORNIA

DECISION AND ORDER

The attached Stipulated Settlement and Disciplinary Order is hereby adopted by the

California Board of Accountancy, Department of Consumer Affairs, as its Decision in this

matter.

FOR ·• ~LIFO ACCOUNTANCY DEPARTMENT OF CONSUMER AFFAIRS

In the Matter of the Accusation Against:

NICK NAWORSKI, CPA, A Professional Corporation 1920 20th Street Bakersfield, CA 93301

Certified Public Accountancy Corporation Certificate No. COR 7905,

and

NICHOLAS PATRICK NAWORSKI 1920 20th Street Bakersfield, CA 93301

Certified Public Accountant Certificate No. CPA 64246

Respondents.

Case No. AC-2019-57

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

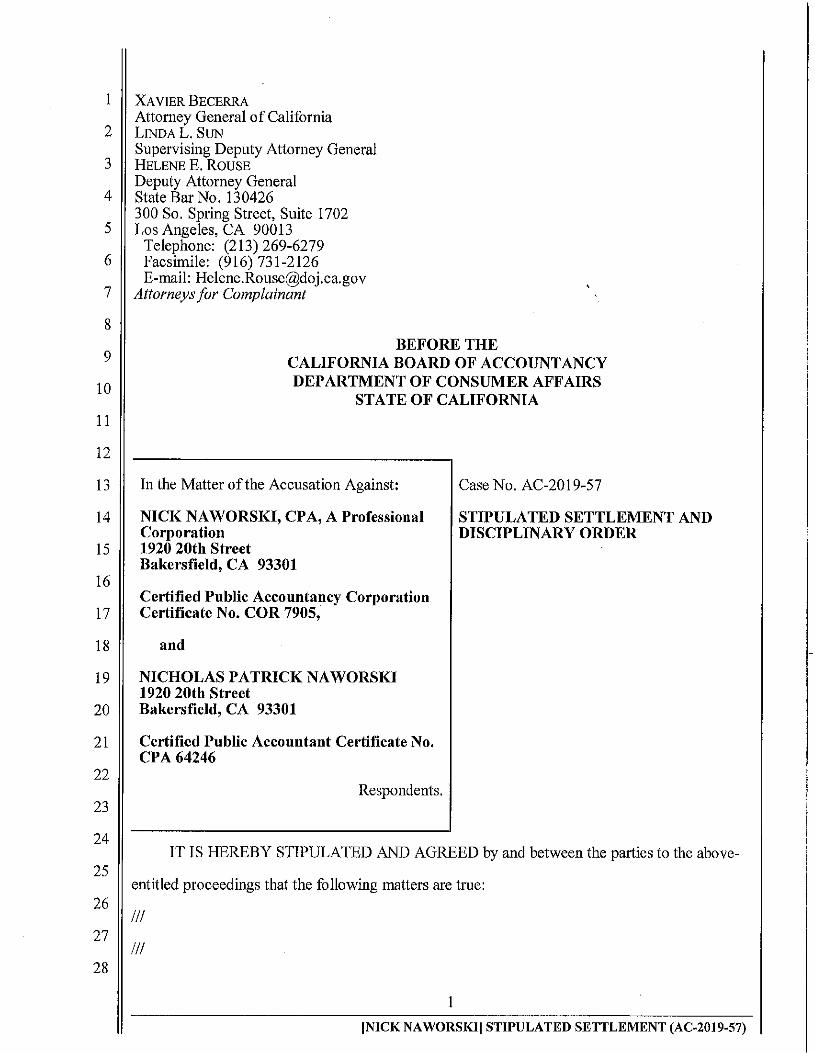

XAVIER BECERRA Attorney General of California LINDAL. SUN Supervising Deputy Attorney General HELENE E. ROUSE Deputy Attorney General State Bar No. 130426 300 So. Spring Street, Suite 1702 Los Angeles, CA 90013

Telephone: (213) 269-6279 Facsimile: (916) 731-2126 E-mail: [email protected]

Attorneys for Complainant

BEFORE THE CALIFORNIA BOARD OF ACCOUNTANCY DEPARTMENT OF CONSUMER AFFAIRS

STATE OF CALIFORNIA

In the Matter of the Accusation Against:

NICK NA WORSKI, CPA, A Professional Corporation 1920 20th Street Bakersfield, CA 93301

Certified Public Accountancy Corporation Certificate No. COR 7905,

and

NICHOLAS PA TRICK NA WORSKI 1920 20th Street Bakersfield, CA 93301

Certified Public Accountant Certificate No. CPA 64246

Respondents.

Case No. AC-2019-57

STIPULATED SETTLEMENT AND DISCIPLINARY ORDER

IT IS HEREBY STIPULATED AND AGREED by and between the parties to the above

entitled proceedings that the following matters are true:

Ill

Ill

1

INICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

•

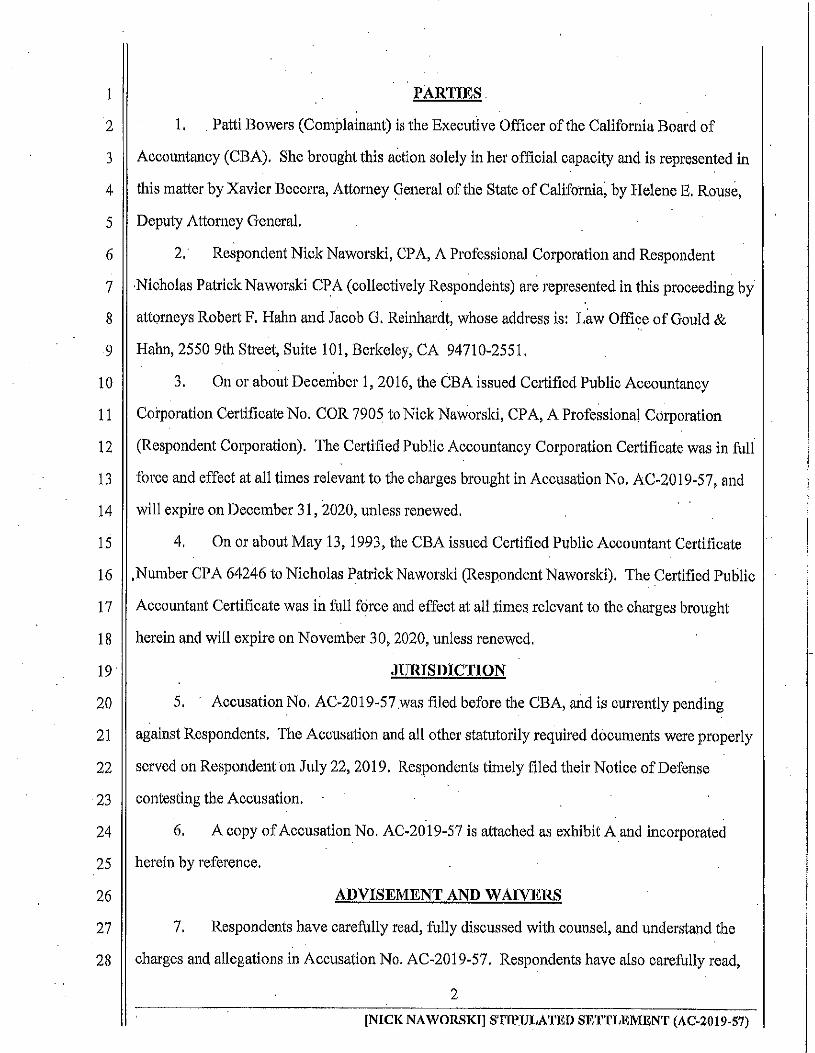

PARTIES.

1. Patti Bowers (Complainant) is the Executive Officer of the California Board of

Accountancy (CBA). She brought this action solely in her official capacity and is represented in

this matter by Xavier Becerra, Attorney General of the State of California, by Helene E. Rouse,

Deputy Attorney General.

2. · Respondent Nick Naworski, CPA, A Professional Corporation and Respondent

-Nicholas Patrick Naworski CPA ( collectively Respondents) are represented in this proceeding by

attorneys Robert F, Hahn and Jacob G, Reinhardt, whose address is: Law Office of Gould &

Hahn, 2550 9th Street, Suite 101, Berkeley, CA 94710-2551.

3. On or about December 1, 2016, the CBA issued Certified Public Accountancy

Corporation Certificate No. COR 7905 to Nick Naworsld, CPA, A Professional Corporation

(Respondent Corporation). The Certified Public Accountancy Corporation Certificate was in full

force and effect at all times relevant to the charges brought in Accusation No, AC-2019-57, and

will expire on December 31, 2020, unless renewed,

4, On or about May 13, 1993, the CBA issued Certified Public Accountant Certificate

,Number CPA 64246 to Nicholas Patrick Naworski (Respondent Naworski). The Certified Public

Accountant Certificate was in full force and effect at all .times relevant to the charges brought

herein and will expire on November 30, 2020, unless renewed.

JURISDICTION

5, Accusation No. AC-2019-57.was filed before the CBA, and is currently pending

against Respondents. The Accusation and all other statutorily required documents were properly

served on Respondent on July 22, 2019. Respondents timely filed their Notice of Defense

contesting the Accusation.

6. A copy of Accusation No, AC-2019-57 is attached as exhibit A and incorporated

herein by reference.

ADVISEMENT AND WAIVERS

7, Respondents have carefully read, fully discussed with counsel, and understand the

charges and allegations in Accusation No. AC-2019-57. Respondents have also carefully read,

2

[NICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

1

2

3

4

5

6

7

8

9

1 O

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25.

26

27

28

fully discussed with counsel, and understand the effects of this Stipulated Settlement and

Disciplinary Order.

8. Respondents are fully aware of their legal rights in this matter, including the right.to a

hearing on the charges and allegations in the Accusation; the right to confront m1d cross-exan1ine

the witnesses against them; the right to present evidence and to testify on their own behalf; the

right to the issuance of subpoenas to compel the attendance of witnesses and the production of

docmnents; the right to reconsideration and co1+rt review of an adverse decision; and all other

rights accorded by the California Administrative Procedure Act and other applicable laws.

9. Respondents voluntarily, knowingly, and intelligently waive and give up each and

every right set forth above.

CULPABILITY

10.. Respondents admit the truth of each and every charge and allegation in Accusation

No. AC-2019-57,

11. Respondents agree that tlleir Certified Public Accountancy Corporation Certificate

and Certified Public Accountant Certificate are subject to discipline Md they agree to be bound

by tlle CBA's probationm-y terms as set forth in tlle Disciplinary Order below,

CONTINGENCY

12. This stipulation shall be subject to approval by the CBA. Respondents understand

and agree that counsel for Complainant and the Staff of the· California Board of Accountancy may

communicate directly with the CBA regarding this stipulation and settlement, without notice to or

participation by Respondents or their counsel. By signing tlle stipulation, Respondents

understand Md agree that they may riot withdraw its agreement or seek. to rescind the stipulation

prior to tlle time the CBA considers and acts upon it. If the CBA fails to adopt tllis stipulation as .

its Decision and Order, tlle Stipulated Settlement Md Disciplinary Order shall be of no force or

effect, except for this paragraph, it shall be inadmissible in any legal action between the parties,

and the CBA shall not be disqualified from further action by having considered this matter,

Ill

Ill

3

[NICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

·

1 .

2

3

4

5

6

7

8

9

10

11

12

·13

14

J5

16

17

J8

19

20

21

22

23

24

25

26

27

28

13. The parties understand and agree that Portable Document Format (PDF) and facsimile

copies of this Stipulated Settlement and Disciplinary Order, including PDF and facsimile

signatures thereto, shall have the same force and effect as the originals.

14. ·This Stipulated Settlement and Disciplinary Order ls intended by the parties to be an

integrated writing representing the complete, final, and exclusive embodiment oftl1eir agreement,

It supersedes any and all prior or contemporaneous agreements, understandings, discussions,

negotiations, and commitments (written or oral). This Stipulated Settlement and Disciplinary

Order may not be altered, amended, modified, supplemented, or otherwise changed except by a

writing executed by an authorized representative of each of the parties.

15. In consideration of the foregoing admissions and stipulations, the parties agree that

the CBA may, without further notice or formal proceeding, issue and enter the following

Disciplinary Order:

DISCIPLINARY ORDER

IT IS HEREBY ORDERED that Certified Public Accountancy Corporation Certificate No.

COR 7905 issued to Respondent Nick Naworski, CPA, A Professional Corporation and Certified

Public Accountant Certificate Number CPA 64246 issued to Nicholas Patrick Naworski are

revoked, However, the revocations are stayed and Respondents are placed on probation for three

(3) years on the following terms and conditions.

1. Obey All Laws

Respondents shall obey all federal, California, other states' and local laws, including those

rules relating to the practice of public accountancy in California.

2. Cost Reimbursement

Respondents shall reimburse the CBA $10,210.13 for its investigation and prosecution

costs, The payment shall be made in quarterly payments ( due with quarterly written reports), with

the final payment being six (6) months before probation is scheduled to terminate.

3. Submit Written Reports

Respondents shall submit, within IO days of completion of the quarter, written reports to

fue CBA on a form obtained fron:i the CBA. Respondents shall submit, under penalty of perjury,

4

[NICK NAWORSKI) STIPULATED SETTLEMENT (AC-2019-57)

5

10

15

20

25

1

2

3

4

6

7

8

9

11.

12

13

14

16

17

18

19

21

22

23

24

26

27

28

such other written reports, declm·ations, and verification of actions as are required. These

declarations shall contain statements relative to Respondents' compliance with all the _terms and

conditions of probation, Respondents shall immediately execute all release of information forms

as niay be required by the CBA or its representatives.

4. Personal Appearances

Respondents shall, during the period of probation, appear in person at interviews/meetings

as directed by the CBA or its designated representatives, provided such notification is

accomplished in a timely manner,

5. Comply With Probation

Respondents shall fully comply with the terms m1d conditions of the probation imposed by

the CBA ru1d shall cooperate fully with representatives of the CBA in its monitoring and

investigation of the Respondents' compliance with probation terms and conditions.

6. Practice Investigation

Respondents shall be subject to, and shall permit, a practice investigation of the

Respondents' professional practice. Such a practice investigation shall be conducted by

.representatives of the CBA, provided notification of such review is accomplished in a timely

manner.

7. Comply With Citations

Respondents shall comply with all final orders resulting from citations issued by the CBA.

8. Tolling of Probation for Out-of-State Residence/Practice

In the event Respondents should leave California to reside or practice outside this state,

Respondents must notify the CBA in ·writing of the dates of departure ru1d return. Periods of non

California residency or practice outside the state shall not apply to reduction of the probationary

period, or of any suspension, No obligation imposed herein, including requirements to file

written reports, reimburse the CBA costs, ru1d make restitution to consumers, shall be suspended

or otherwise affected by such periods of out-of-state residency or practice except at the written

·direction of the CBA.

Ill

5

[NICKNAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

5

10

15

20

25

1

2

3

4

6

7

~

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

9. Violation of Probation

If Respondents violate probation in any respect, the CBA, after giving Respondents notice

and an opportunity to be heard, may revoke probation and carry out the disciplinary order that

was stayed. If an accusation or a petition to revoke probation is filed against Respondent(s)

during probation, the CBA shall have continuing jurisdiction until the matter is final, and the

period of probation shall be extended until the matter is final.

The CBA' s Executive Officer may issue acitation under California Code of Regulations,

Section 95, to a licensee for a violation ofa term or condition contained in an Order placing that

licensee on probation.

10. Completion of Probation·

Upon successful completion of probation, Respondents' licenses will be fully restored,

except as limited by the Restricted Practice Order at the end of this stipulation.

11. Restricted Practice

Respondents shall be prohibited from engaging in or performing audits and reviews.

12. Ethics Continuing Education

Within 180 days of the effective date of this Order, Respondent Naworski shall complete

four hours of continuing education in course subject matter pertaining to the following: a review

of nationally recognized codes of conduct emphasizing how the codes relate to professional

responsibilities; case-based instruction focusing on real-life situati_onal learning; ethical dilemmas

facing the accounting profession; or business ethics, ethical sensitivity, and consumer

expectations. Courses must be a minimum of one hour as described in California Code of

Regulations Section 88.2. This shall be in addition to continuing education requirements for

relicensure.

If Respondent Naworski fails to complete said courses within the time period provided,

Respondent Naworski shall so notify the CBA and shall cease practice until Respondent

Naworski completes sald courses, has submitted proof of same to the CBA, and has been notified

by the CBA that he may resume practice. Failure to complete the required courses within the time

period pro:vided shall constitute a violation of probation.

6

[NICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

1

2

3

4

5

6

7

· 8

9

1O

11

12

13

14

15

16

17

18

. 19

2.0

21

22

23

24

25

26

27

28

13, Continuing Education Courses

. Within 180 days of the effective date of this Order, Respondent Naworski shall complete

and pro:vide proper documentation of 16 hours. of professional education in course subject matter

pertaining to the following: Statements on Standards for Accounting and Review Services, This

shall be iri addition to continuing education requirements for relicensure,

If Respondent Naworski fails to coi:nplete said courses within the time period provided,

Respondent Naworski shall so notify the CBA and shall cease practice until Respondent

N aworski completes said courses, has submitted proof of same to the CBA, and has been notified

by the CBA that he may resume practice, Failure to complete the required courses within the time

period provided shall constitute a violation of probation.

14. Regulatory Review Course

Within 180 days of the effective date of this Order, RespondentNaworski shall complete a

CEA-approved course on the provisions of the CaHfornia Accountancy Act and the CBA

Regulations specific to the practice of public accountancy in California emphasizing the

provisions applicable to current practice, The course also will include an overview of historic and

recent disciplinary actions taken by the CBA, highlighting the misconduct which led to licens.ees

being disciplined, This shall be in addition to continuing education requirements for relicensure,

If Respondent Naworski fails to complete said courses within the time period provided,

Respondent shall so notify the CBA and shall cease practice until Respondent N aworsld

completes said courses, has submitted proof of same to the CBA, and has been notified by the

CBA that he or she may resume practice, Failure to complete the required courses within the time

period provided shall constitute a violation of probation,

15, Peer Review

During the period of probation, all compilation reports and work papers shall be subject to

peer review by a CEA-recognized peer review program provider pur.suant to California Business

and Professions Code Section 5076 and California Code of Regulations, Title 16, Division 1,

Article 6, commencing with section 38, at Respondent's expense, The specific engagements to be

reviewed shall be at the discretion of the peer reviewer. Within 45 days of the peer review report

7

[NICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019-57)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

·

being accepted by a CBA-recognized peer review program provider, Respondents shall submit to

the CBA a copy of the peer review report, including any materials documenting the prescription

of remedial or con·ective actions imposed by the c.BA-recognized peer review program provider.

. Respondents shall also submit, if available, any materials documenting completion of any or all

of the prescribed remedial or corrective actions.

16. · Active License Status

Respondents shall at all times maintain an active license status with the CBA, including

during any period of suspension. If the license(s) is/are expired at the time the CBA's Order

becomes effective, the license(s) must be renewed within 30 days of the effective date of the

Order.

17. Samples - Compilations

During the period ofprobation, if Respondents undertake compilations, Respondents shall

submit to the CBA as an attachment to the required quarterly report a listing of the same. The

CBA or its designee may select one or more from each category and the resulting report and

financial statement and all related working papers must be submitted to the CBA or its designee

upon request.

IT IS HEREBY FURTHER ORDERED that: ·

18. RESTRICTED PRACTICE ORDER, After the completion of probation,

Respondents shall be permanently prohibited from engaging in and performing audits and ·

reviews. This condition shall continue until such time, if ever, Respondents successfully petition

the CBA for the reinstatement of the ability to perform audits and reviews. Respondents

understand and agree that the CBA is under no obligation to reinstate either of Respondents'

ability to perform audits and reviews, that the CBA has made no representations concerning

whether af1y such.reinstatement might occur, and that the decision to reinstate is within the sole

discretion of the CBA.

· 16. Full Compliance. Respondents understand and agree that this Stipulated Settlement

and Disciplinary Order as a resolution to the charges in Accusation attached hereto as exhibit A

and is based upon, inter al/a, Respondents' full compliance with the Restricted Practice Order set

8

[NICK NAWORSKI] STIPULATED SETTLEMENT (AC-2019:57)

7

l

: 2.' 3

4

5

.(i .

8 .

9'

J1 .

J,!.

13

. .14 .

1~

l(?

17

I~

19

20 .

2J

7 ...

123

21 25

26

27

28

forth above,: If Respondents fail to satisfy the Restricted Practice Order, Respondents agree that

the CBA can file an accusation against them for unprofessional conduct ba:sed on the failure to

comply with the Restricted Practice Order as an independent basis for disciplinary action, ' '

pursuant to Businil'ss and Professions C9de section 5100. In addition, Respondents consent that

the CBA may enforce the Restric!ed Practice Ordet ln any court of competent jurisdiction

(including an administrative court) to enjoin them, temporarily and/or permanently, from

violating the Restricted Practice Or(!er, &nd mny seek in such proceeding all other remedies as

allowed by law,

I have carefully read the above Stipulated Settl~ment and Disciplinary Order and have fully

discussed it with my attorney, Jacob G. Reinhardt, l understand the stipulation and the effect it

will have on my Certified Public Accountancy Corporation Certificate·and Certified Public

Accountant Certificate, I enter into this Stipulated Settlement and Disciplinary Order voluntal'ily,

knowingly, and intelligently, and agree to be bound by the Decision and Order ofthe California

Board ofAccountancy.

DATED: I i IIL I!'T I NICK NAWORSKI, CPA A PROFESSIONAL

CORPORATION, AND NICHOLAS PATIUCK NAWORSKI, CPA . Respondents

I have read and fully discussed with Respondents Nick Naworskl, CPA, A Professional .

Corporation and Nicholas Patrick Naworski, .CPA the terms alXL=ditiOJ1s.and other-matters----·----·-·

contained in the above Stipuh1ted Settlement and Disciplinary Order, I ~pprove its form and

content.

DATE!}: ti JA T

A rney for Respondent

9

fNICKNAWP_~~] SIU'.Ul,.ATED SETTLEMENT (AC-2Ql9-57)

................. ,...,,,.,._,___,_,,,,........................... .

5

10

15

20

25

1 ENDORSEMENT

2 The foregoing Stipulated Settlement and Disciplinary Order is hereby respectfully

3 submitted for consideration by the California Board of Accountancy.

4 DATED: November 14, 2019 Respectfully submitted,

XAVIER BECERRA 6 Attorney General of California

LINDAL. SUN 7 Supervising Deputy Attorney General

8

9 HELENE E. ROUSE Deputy Attorney General Attorneys for Complainant

11

12

13

14 LA.2019501162' 53746150.docx

16

17

18

19

--------z1-H---------------~-------------------·-·-- ·-

22

23

24

26

27

28

10

[NICK NAWORSKIJ STIPULATED SETTLEMENT (AC-2019-57)

Exhibit A

Accusation No, AC-2019-57

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

XAVIER BECERRA Attorney General of California LINDAL. SUN Supervising Deputy Attorney General HELENE E. ROUSE Deputy Attorney General _ State Bar No. 130426 300 So. Spring Street, Suite 1702 Los Angeles, CA 90013

Telephone: (213) 269-6279 Facsimile: (213) 897-2804

Attorneys for Complainant

BEFORE THE CALIFORNIA BOARD OF ACCOUNTANCY DEPARTMENT OF CONSUMER AFFAIRS

STATE OF CALIFORNIA

In the Matter of the Accusation Against: Case No. AC-2019-57

NICHOLAS PATRICK NAWORSKI - - -ACCUSATION1--------------+- ---

1920 20th Street Bakersfield, CA 93301

Certified Public Accountant Certificate No, CPA 64246

And

NICK NAWORSKI, CPA, A Professional Corporation 1920 20th Street Bakersfield, CA 93301

Certified Public Accountancy Corporation Certificate No. COR 7905,

Respondent.

PARTIES

1. Patti Bowers (Complainant) brings this Accusation solely in her official capacity as

the Executive Officer of the California Board of Accountancy (CBA), Department of Consumer

Affairs.

///

1 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKJ) ACCUSATION

5

10

15

20

25

1 2, On or about December 1, 2016, the CBA issued Certified Public Accountancy

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

Corporation Certificate Number COR 7905 to Nick Naworski, CPA, A Professional Corporation

(Respondent Corporation), The Certified Public Accountancy Corporation Certificate was in full

force and effect at all times relevant to the charges brought herein and will expire- on December

31, 2020, unless renewed,

3. On or about May 13, 1993, the CBA issued Certified Public Accountant Certificate

Number CPA 64246 to Nicholas Patrick Naworski (Respondent). The Certified Public

Accountant Certificate was in foll force and effect at all times relevant to the charges brought

herein and will expire on November30, 202Q, unless renewed.

JURISDICTION

4, This Accusation is brought before the CBA, under the authority of the following

laws. All section references are to the Business and Professions Code unless othe1wise indicated,

5. Section 5109 states:

The expiration, cancellation, forfeiture, or suspension of a license, practice privilege, or other authority to practice public accountancy by operation of law or by order or decision of the board or a court of law, the placement of a license on a retired status, or the voluntary surrender of a license by a licensee shall not deprive the board of jurisdiction to commence or proceed with any investigation ofor action or disciplinary proceeding against the licensee, or to render a decision suspending or revoking the license.

STATUTES

6, Section 5062 provides that "A licensee shall issue a report which conforms to

professional standards upon completion ofa compilation, review or audit of financial statements."

7, Section 5097 states:

(a) Audit documentation shall be a licensee's records of the procedures applied, the tests performed, the information obtained, and the pertinent conclusions reached in an audit engagement. Audit documentation shall include, but is not limited to, programs, analyses, memoranda, letters of confirmation and representation, copies or abstracts of company documents, and schedules or commentaries prepared or obtained by the licensee.

(b) Audit documentation shall contain sufficient documentation to enable a reviewer with relevant knowledge and experience, having no previous connection with the audit engagement, to understand the nature, timing, extent, and results of the auditing or other procedures performed, evidence obtained, and conclusions reached, and to determine the identity of the persons who performed and reviewed the work,

2

(NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

(c) Failure of the audit documentation to document the procedures applied, tests performed, evidence obtained, and relevant conclusions reached in an engagement shall raise a presumption that the procedures were not applied, tests were not performed, information was not obtained, and relevant conclusions were not reached. This presumption shall be a rebuttable presumption affecting the burden ofproof relative to those portions of the audit that are not documented as required in subdivision (b), The burden may be met by a preponderance of the evidence.

8. Section 5100 states, in pertinent part:

After notice and hearing the board may revoke, suspend, or refuse to renew any permit or certificate granted under Article 4 ( commencing with Section 5070) and Article 5 (commencing with Section 5080), or may censure the holder of that permit or certificate for unprofessional conduct that includes, but is not limited to, one or any combination of the following causes:

(c) Dishonesty, fraud, gross negligence, or repeated negligent acts committed in the same or different engagements, for the same or different clients, or any combination of engagements or clients, each resulting in a violation of applicable professional standards that indicate a lack of competency in the practice ofpublic accountancy or in the performance of the bookkeeping operations described in Section 5052.

(e) Violation of 5097.

(g) Willful violation of this chapter or any rule or regulation promulgated by the board under the authority granted under this chapter,

9, Section 5100.5 provides as follows:

(a) After notice and hearing the board may, for unprofessional conduct, permanently restrict or limit the practice of a licensee or impose a probationary term or condition on a licensee, which prohibits the licensee from performing or engaging in any of the acts or services described in Section 5051.

(b) A licensee may petition the board pursuant to Section 5115 for reduction of penalty or reinstatement of the privilege to engage in the service or act restricted or limited by the board.

(c) The authority or sanctions provided by this section are in addition to any other civil, criminal, or administrative penalties or sanctions provided by law, and do not supplant, but are cumulative to, other disciplinary authority, penalties, or sanctions.

(d) Failure to comply with any restriction or limitation imposed by the board pursuant to this section is grounds for revocation of the license,

3 (NICK NAWORSKI, CPA, A.P,C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

(e) For purposes of this section, both of the following shall apply:

(1) "Unprofessional conduct" includes, but is not limited to, those grounds for discipline or denial listed in Section 5100.

(2) "Permanently restrict or limit the practice of' includes, but is not limited to, the prohibition on engaging in or performing any attestation engagement, audits, or compilations.

ADMINISTRATIVE PENALTY

10. Section 5116 provides, in pertinent part, that the Board may order any licensee to

pay an administrative penalty as part of any disciplinary proceeding. Administrative penalties

shall be in addition to any other penalties or sanctions imposed on the licensee, including, but not

limited to, license revocation and license suspension. Payment of these administrative penalties

may be included as a condition ofprobation when probation is ordered.

COST RECOVERY

11. Section 5107, subdivision (a) states:

The executive officer of the board may request the administrative law judge, as part of the proposed decision in a disciplinary proceeding, to direct any holder ofa permit or certificate found to have committed a violation or violations of this chapter to pay to the board all reasonable costs of investigation and prosecution of the case, including, but not limited to, attorney's fees. The board shall not recover costs incurred at the administrative hearing.

REGULATIONS

12. California Code ofRegulations, title 16, section 58 (Board Rule 58) states:

Licensees engaged in the practice of public accountancy shall comply with all applicable professional standards, including but not limited to generally accepted accounting principles and generally accepted auditing standards.

APPLICABLE PROFESSIONAL STANDARDS

13. Standards ofpractice pertinent to this Accusation and the engagements in issue

include, without limitation:

A. Statements on Standards for Accounting and Review Scrviees. Standards

applicable to the performance of a compilation are discussed in the Statements on Standards for

Accounting Review Services (SSARS) and are codified by the American Institute of Certified

Public Accountants (AICPA). The statements are codified by "AR" or "AR-C" numbers,

depending upon the version applicable. The SSARS relevant to the compilation for the three

4 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSAT[ON

I

2

3

4

5

6

7

8

9

1O

11

12

13

14

15

16

17

19

20

21

22

23

24

25

26

27

28

months ended March 31, 2015, is AR section 80. For the compilations for both the eight months

ended August 31, 2016, and for the ten months ended October 31, 2016, the SSARS relevant are

AR-C sections 60 and 80.

B. Generally Accepted Auditing Standards. Statements on Auditing Standards are

issued by the Auditing Standards Board (ASB), the senior committee of the AICPA designated to

issue pronouncements on auditing matter for nonissuers. The "Compliance with Standards Rule"

of the AICPA Code of Professional Conduct requires an AICPA member who performs an audit

of a nonissuer to comply with standards promulgated by the ASB. The relevant sections to this

Accusation include: AU-C §200 (Overall Objectives); AU-C §210 (Terms of Engagement); AU-

C §220 (Quality Control); AU-C §230 (Audit Documentation); AU-C §240 (Consideration of

Fraud); AU-C §260 (Communication with Those Charged with Governance); AU-C §265

(Communicating Internal Control Matters); AU-C §300 (Planning an Audit); AU-C §315

(Understanding the Entity and Assessing Risks); AU-C §320 (Materiality); AU-C §330

(Procedures in Response to Assessment Risks and Evaluating Audit Evidence); AU-C 501

(Evidence for Specific Items); AU-C §520 (Analytical Procedures); AU-C §550 (Related Parties);

AU-C §560 (Subsequent Events); AU-C §580 (Written Representations); AU-C §700 (Forming

an Opinion and Reporting); and AU-C §705 (Modified Opinions).

C. Department of Labor ERISA Requirements. The Department of Labor (DOL),

through the Employee Retirement Income Security Act (ERISA) of 1974, established auditing

and reporting guidelines for defmed benefit and defined contribution plans with 100 or more

participants. The Auditing Standards Board issues the interpretive AICP A Audit and Accounting

Guide for Employee Benefit Plans to assist management of employee benefit plans in the

preparation of fmancial statements in conformity with the US GAAP and to assist auditors in

auditing and reporting on such financial statements. The guide represents the application of

generally accepted auditing standards and accounting principles to the special circumstances that

are unique to audits of employee benefit plans. Thus, while the interpretive guide is non-

authoritative, the auditor should be prepared to address how the auditor complied with Statements

on Auditing Standards (SAS) provisions addressed by the auditing guidance. This Guide was

5 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

updated January 1, 2014, is codified as "AAG-EBP" number and reference to BRISA Regulations

is included in Appendix A. Among the Guide chapters relevant herein, effective for financial

statements for plan years ending before January 1, 2014, are: Chapter 2-Planning and General

Auditing Considerations; Chapter 4 - Internal Control; Chapter 5 - Defined Contribution

Retirement Plans; and Chapter 10 - Concluding the Audit and Other Considerations.

FACTUAL BACKGROUND

14. The CBA received a copy ofRespondent's documentation ofhis accounting and audit

engagements, as follows:

• S.L. 401(k) Plan, audit for the year ended December 31, 2013. 1

• K.W.K, DDS, Inc., compilation for the year ended December 31, 2013, dated May

15, 2014, and compilation for the eight months ended August 31, 2016 dated September

28, 2016.

• S.H.B., Inc., compilation of consolidated financial statements for the three months

ended March 31, 2015, dated April 20, 2015.

• Dr. C.C., compilation for the ten months ended October 31, 2016, dated December

30, 2016.

15. Respondent received a peer review rating of "fail" on his peer review report dated

September 15, 2014, for a system peer review of the year ended May 31, 2014. Respondent

stopped offering .audit services immediately after receiving the failed peer review. Respondent

received a rating of "fail" on his most recent peer review report, which was an engagement

review for the year ended May 31, 2017, report dated July 26, 2017. After an investigation by the

CBA, the following failures to comply with professional standards were identified:

I. With respect to an BRISA audit engagement for the year ended December 21,,2013,

Respondent was repeatedly negligent for failing to comply with professional standards, including,

but not limited to, the following:

1 The initials of individuals and entities are used to protect their privacy, but their identities will be disclosed in investigation documents, to be provided to Respondent after a timely and proper request for discovery.

6 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

A The engagement Jetter does not state it will be a DOL Limited Scope, and it

incorrectly states that the objective is the expression of an opinion. Consequently, no appropriate

understanding was documented. [AU-C 210.l0(a); AAG-EBP 2.36]

B. Respondent failed to obtain a management representation letter for the audit. [AU-

C 580.10]

C. The auditor's report does not reflect current language and it omits the required

headings. [AU-C 700.26; AU-C 700.29; AU-C 700.34]

D. Respondent's audit documentation lacked evidence to support that the engagement

was properly planned, including:

i. An audit strategy and plan. [AU-C 300.07; AU-C 300.09]

ii. An engagement team meeting, [AU-C 240.43; AU-C 315.33]

iii. Client acceptance procedures. [AU-C 220.25]

iv. Respondent failed to establish materiality, [AU-C 320.11]

v. Respondent did not perform a risk assessment. [AU-C 200.08; AU-C 315.06]

E. There were no communications to either management or those charged with

governance, except the engagement letter. [AU-C 230-11; AU-C 240.17; AU-C 240.45; AU-C

260.05; AU-C 260.12; AU-C 265.12]

F. Inadequate procedures were performed, including the following presumptively

mandatory procedures:

i. Justification ofomitted presumptively mandatory procedures and how

alternative procedures met the objectives. [AU-C 230.13]

ii. Address the presumed risk of management override of controls. [AU-C

240.32.]

iii. Perform procedures for subsequent events. [AU-C 560.09]

iv, Reading minutes. [AAG-EBP 10.14(b)]

v. Obtain a legal representation letter. [AU-C 501.22; AAG-EBP 10.11]

vi. Address the presumed risk of revenue recognition. [AU-C 240.46]

vii. Analytics do not include expectations or acceptable variance. [AU-C

7 (NICK NAWORSKI, CPA, A,P,C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKJ) ACCUSATION

1

2

3

4

5

6

7

8

9

1O

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

520.05(c) & (d)]

viii. Link procedures to the identified risk addressed. [AU-C 330.05; AU-C

330.06; AU-C 330.30]

ix. Consult available interpretative publications. [AU-C 200.27]

G. Respondent failed to follow procedures specific to an employee benefit plan:

i. Respondent did not obtain a SOC (Service Organization Control)

report. [AAG-EBP 4.13; AAG-EBP 4.28; AAG-EBP 10.37]

ii. Respondent did not perform adequate procedures to determine that

allocations were in accordance with the plan instrument, Respondent tested the

employer match, but did not follow stated procedures, The work paper states that

four employees with deferrals on their W-2 will be selected, from employee test,

but only one of the four employees on the work paper had deferrals. [AAG-EBP

5.124]

iii. Respondent did not perform procedures for benefit payments.

Respondent noted in his analytics that the company had laid off approximately 120

employees due to a move to Mexico. The plan had 227 participants at the

beginning of the year, and 123 participants at the end of the year. This indicates a

partial termination of the plan, which increases the need for both participant and

distribution testing. In addition, distributions (benefits paid to participants) for the

year were $1,495,317, which is 23% of beginning net assets available, a very

material amount. However, there was no testing of distributions. [AAG-EBP

5.180 and AAG-EBP 5.203]

H. The documentation of those procedures that were performed do not adequately

describe the objective, what procedures were performed, and they do not identify the preparer or

date, [AU-C 230.08; AU-C 230,09]

I. There is inadequate documentation and insufficient audit evidence to support the

report issued. [AU-C 200.08; AU-C 200.22; AU-C 220.19; AU-C 230.02; AU-C 330.29; AU-C

705.07]

8 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

J. Respondent did not possess the necessal'y skills or experience to conduct an

ERJSA audit in accordance with professional standards. [AU-C 220.03; AU-C 220.16; AAG-

EBP 2.07]

II. Respondent performed multiple compilation engagements which have departures

from professional standards.

A. With respect to the consolidated compilation for the three months ended

March 31, 2015, the engagement letter had the following departures:

i. The compilation is for 2015 annual and month-end financial statements

(statement of assets, liabilities and equity, tax basis, and related statement of revenue,

expense, and retained earnings), but the fmancials do not present a statement of assets,

liabilities and equity.

ii. It does not mention either the consolidation or the single item compilation.

iii. It is dated after the compilation report.

iv. No appropriate understanding with management was obtained for this

engagement by Respondent, who indicated he did not obtain an engagement letter for the

consolidated financials. [AR 80.02]

B. For both a compilation for the eight months ended August 31, 2016, and a

compilation for the ten months ended October 31, 2016:

i. The engagement letters included the following departures:

a. Refers to GAAP instead of the tax basis in the objective

paragraph in the description of management's responsibilities.

b. Omits management's responsibility for the selection of the

financial reporting framework.

c. Omits the description of the income tax basis and the summaries

of significant accounting policies and how it differs from GAAP.

[AR-C 60.26; AR-C 80.08]

ii. The accountant's compilation reports omitted the following:

a.· Management's responsibility for determining that the income

9 (NICK NAWORSKI, CPA, A.P. C, NICHOLAS l'ATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

tax basis is an acceptable financial reporting framework.

h. The statement that the income tax basis of accounting is a basis

ofaccounting other than GAAP. [AR-C 80.20(a); 80.21(c)]

C. For only the compilation for the eight months ended August

31, 2016, the accountant's compilation report refers to

supplemental information, hut there is none presented.

D. For only the compilation for the ten months ended October 31, 2016, the

accountant's compilation report omits the required paragraph stating that management has

elected to omit substantially all of the disclosures ordinarily included in financial

statements prepared in accordance with the tax basis of accounting, and that if the omitted

disclosures were included they might influence the users' conclusions.

FIRST CAUSE FOR DISCIPLINE

(Repeated Acts of Negligence)

16. Respondents' certificates are subject to disciplinary action under section 5100,

subdivision (c), in that they engaged in repeated acts of negligence evidencing a violation of

applicable professional standards and indicating a lack of competency in the practice ofpublic

accountancy, as set forth above in Paragraphs 14-15. ·

SECOND CAUSE FOR DISCIPLINE

(Report Failing to Conform to Professional Standards)

17. Respondents' certificates are subject to disciplinary action under sections 5062 and

5100, subdivision (g), in that Respondents issued an auditor's report and compilation reports

which failed to conform to professional standards, as set forth above in Paragraphs 14-15.

THIRD CAUSE FOR DISCIPLINE

(Failure to Comply with Professional Standards)

18. Respondents' certificates are subject to disciplinary action under section 5100,

subdivision (g) in conjunction with California Code of Regulations, title 16, section 58, in that

Respondents failed to comply with all applicable professional standards, including hut not limited

to SSARS, GAAS, and BRISA requirements, as set forth above in Paragraphs 14-15, inclusive.

10 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATIUCK NAWORSKI and NICHOLAS PATIUCK

NAWORSKI) ACCUSATION

5

10

15

20

25

1

2

3

4

6

7

8

9

11

12

13

14

16

17

18

19

21

22

23

24

26

27

28

FOURTH CAUSE FOR DISCIPLINE

(Failure to Obtain Sufficient Approprinte Audit Evidence)

19. Respondents' certificates are subject to disciplinary action under sections 5100,

subdivision (e) and 5097, in that they failed to obtain sufficient appropriate audit information to

support an ERJSA audit, as set forth above in Paragraphs 14-15.

PRAYER

WHEREFORE, Complainant requests that a hearing be held on the matters herein alleged,

and that following the hearing, the California Board of Accountancy issue a decision:

Revoking or suspending, restricting, limiting or otherwise imposing discipline upon

Certified Public Accountant Certificate Number CPA 64246, issued to Nicholas Patrick

Naworski;

2. Revoking or suspending, restricting, limiting or otherwise imposing discipline upon

Certified Public Accountancy Corporation Certificate Number COR 7905, issued to Nick

Naworsld, CPA, A Professional Corporation, Nicholas Patrick Naworski;

3. Ordering Nicholas Patrick Naworski and Nicholas Patrick Naworski, A Professional

Corporation to pay the California Board of Accountancy an administrative penalty pursuant to

Business and Professions Code section 5116;

4. Ordering Nicholas Patrick Naworski and Nicholas Patrick Naworski, A Professional

Corporation to pay the California Board ofAccountancy the reasonable costs of the investigation

and enforcement of this case, pursuant to Business and Professions Code section 5107; and,

5. Taking such other and further action as deemed necessary and proper.

DATED:~j 9-011 P T fBOWERS Executive Officer California Board of Accountancy Department of Consumer Affairs State of California Complainant

LA2019501162; 53546382.docx

11 (NICK NAWORSKI, CPA, A.P.C, NICHOLAS PATRICK NAWORSKI and NICHOLAS PATRICK

NAWORSKI) ACCUSATION