Embed Size (px)

Citation preview

Foodservice Trade Investment 2020-What it will look like

and how we’ll get there

Speakers: Jim Klass Managing Partner MarketIntelligence

Bill Mason Managing Director The Hale Group

Page 2

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with:• Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with:• Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Agenda

Page 3

Trade Investment: “Above the Line”

We have worked to define trade investment with a group of foodservice manufacturers.

Comprised of various types of spending that can be considered a “reduction in revenue” according to the Financial Accounting Standard Board’s interpretation, defined after the Sarbanes-Oxley Act of 2002.

Included monies paid by the manufacturer to a distributor, wholesaler, GPO, customer or operator as payment for consideration of various promotional, merchandising and/or product, brand or category-building activities for the manufacturer.

• Bids

• Rebates

• Off-Invoice

• Price Allowances

• Market Pricing

Trade Investment: “Above the Line”

We have worked to define trade investment with a group of foodservice manufacturers.

Comprised of various types of spending that can be considered a “reduction in revenue” according to the Financial Accounting Standard Board’s interpretation, defined after the Sarbanes-Oxley Act of 2002.

Included monies paid by the manufacturer to a distributor, wholesaler, GPO, customer or operator as payment for consideration of various promotional, merchandising and/or product, brand or category-building activities for the manufacturer.

• Bids

• Rebates

• Off-Invoice

• Price Allowances

• Market Pricing

First let’s define trade…..

• Deviated Pricing

• Distributor Food Shows

• Earned Income / Shelter

• Corporate Growth Programs

• Local Growth Programs

• Deviated Pricing

• Distributor Food Shows

• Earned Income / Shelter

• Corporate Growth Programs

• Local Growth Programs

• Corporate Marketing Programs

• Local Marketing Programs

• Distributor Sales Spiffs

• Local Blanket Bids

• Conversion Fees

• Corporate Marketing Programs

• Local Marketing Programs

• Distributor Sales Spiffs

• Local Blanket Bids

• Conversion Fees

Page 4

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Agenda

Page 5

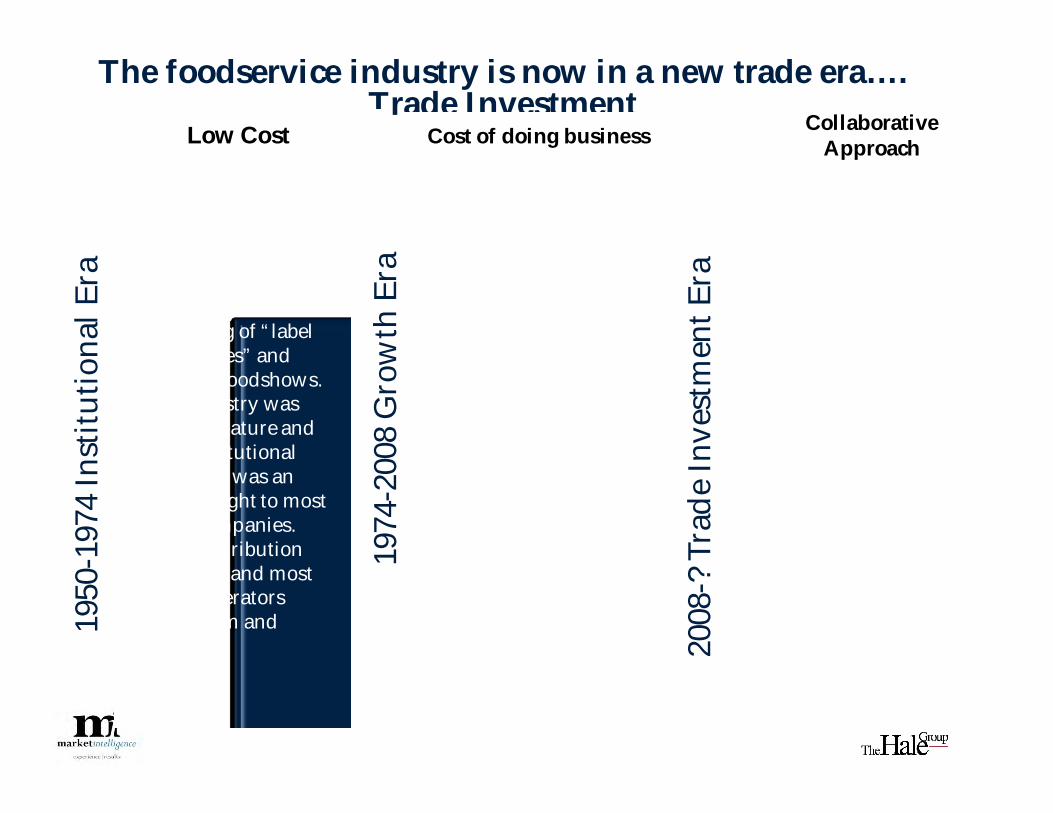

1950

-197

4 In

stitu

tiona

l Era •Simple programs

directed exclusively by the Manufacturer consisting of “label allowances” and selected foodshows. The industry was very immature and the “Institutional "business was an afterthought to most retail companies. Most Distribution was local and most of the operators were mom and pops.

1974

-200

8 G

row

th E

ra

•Power shifted to the distributor after the Imposition of wage and price controls in 1971. Manufacturers were able to build in margin through the introduction of new products .Foodservice was in a tremendous growth cycle and they offered programs “Earned Income” and Shelter to distributors and rebate and deviated pricing to National accounts and LLOs to drive sales. The industry evolved as National distributors and chains began to dominate. Trade Spend was a cost of doing business and until later in the 2000s was manageable 20

08-?

Tra

de In

vest

men

t Era

•The financial collapse in late 2008 destroyed the myth that foodservice was recession proof. The industry declined yet distributors and operators continued to look to the manufacturer as a funding source. Contracted business and GPOs captured a larger portion of the higher margin street sales, commodities fluctuated and inflation was held in check. The game has changed to market share and the vehicle to capture it is prudent trade investment. Manufacturers will need to utilize their trade dollars more efficiently and effectively. The opportunity to “cut” trade is long past.

The foodservice industry is now in a new trade era…. Trade Investment

Low Cost Cost of doing business Collaborative Approach

Page 6

This is the second survey of what we call Trade Investment, the era of trade spend is over. Foodservice is not the growth industry of the 1974-2008 era but a

battle, as in retail, for market share Participants There was abroad spectrum of participants representing all major

foodservice categories Protein Frozen Refrigerated Dry Non Foods

Firms were both branded and distributor label manufactures and the majority were part of a larger CPG company

This is the second survey of what we call Trade Investment, the era of trade spend is over. Foodservice is not the growth industry of the 1974-2008 era but a

battle, as in retail, for market share Participants There was abroad spectrum of participants representing all major

foodservice categories Protein Frozen Refrigerated Dry Non Foods

Firms were both branded and distributor label manufactures and the majority were part of a larger CPG company

Survey Background

Page 6

The environment today …..

Foodservice has shrunk-

7% since 2005

The street is using

alternative distribution 10% to Club

Stores

“Contracted” Operator now over 60% of

Manufactures Sales

At Distributor 3-4% of SKUs generate over 80% of True

Profit

Distributors are looking at “Cost to Serve”

• How will manufactures manage conflicts with distributor brands?

Operators have more visibility to pricing

• How will manufacturers manage the Club/ Cash& Carry conflict?

Page 8

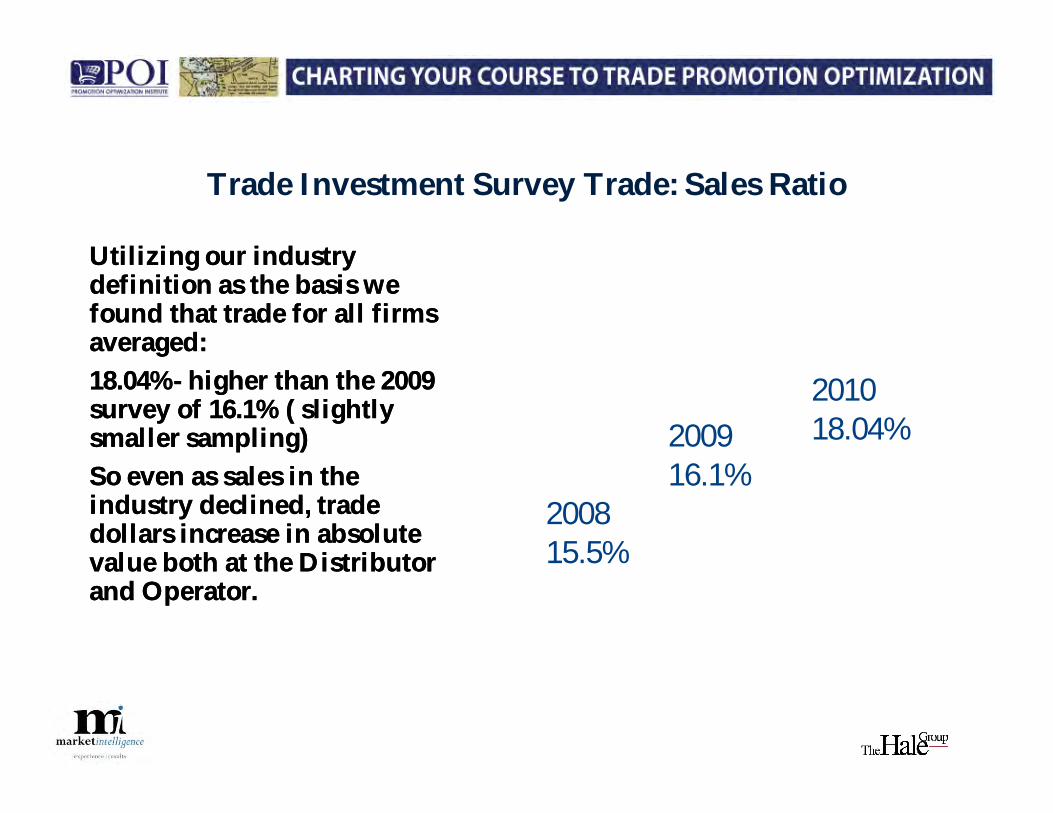

Utilizing our industry definition as the basis we found that trade for all firms averaged:18.04%- higher than the 2009 survey of 16.1% ( slightly smaller sampling)So even as sales in the industry declined, trade dollars increase in absolute value both at the Distributor and Operator.

Utilizing our industry definition as the basis we found that trade for all firms averaged:18.04%- higher than the 2009 survey of 16.1% ( slightly smaller sampling)So even as sales in the industry declined, trade dollars increase in absolute value both at the Distributor and Operator.

Trade Investment Survey Trade: Sales Ratio

Page 8

2008 15.5%

2009 16.1%

2010 18.04%

Page 9

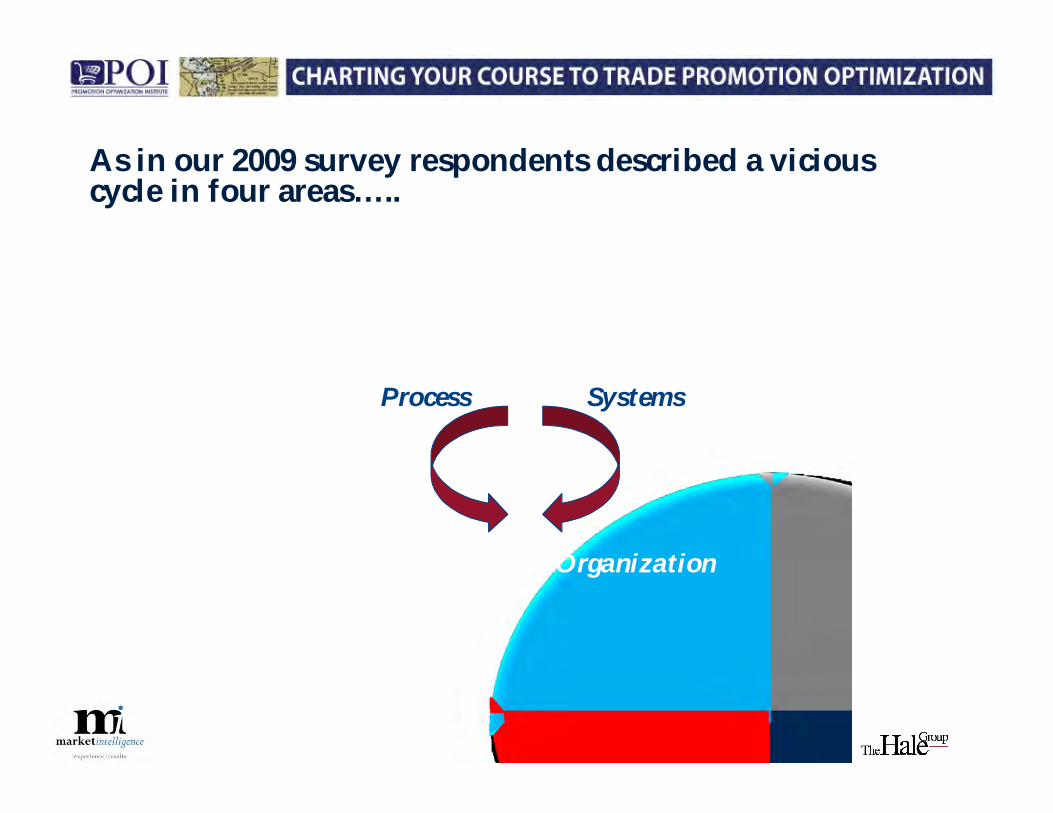

As in our 2009 survey respondents described a vicious cycle in four areas…..

Process Systems

OrganizationAnalytics & Data

Vicious Cycle

Page 10

Process

Lack of standard processes

Inefficiency (high level of manual work and re-work required)

Lack of timely (& accurate) information sharing between

stakeholders

Very Manual Settlement Process

Different planning time horizon

Organization

Sales group’s incentives are not tied to customer profitability…

…they align to increasing sales, not profit

No dedicated trade team with complete oversight

Unable to provide insights to effectiveness of programs to field

sales

Confusion over who “owns” trade

Analysis

Lack of clarity on return of customer investments

No standard analytics used company wide

Limited availability of unit level information

Unable to measure impact at operator over time

No post Promotional analysis

Systems

Low level of automation compared to other industries

No standard system for tracking and control

Lack of visibility and accountability, e.g., contract

execution

Lack of Useable electronic PoP

data

No leading provider of trade

solutions

Observation for each of the key areas

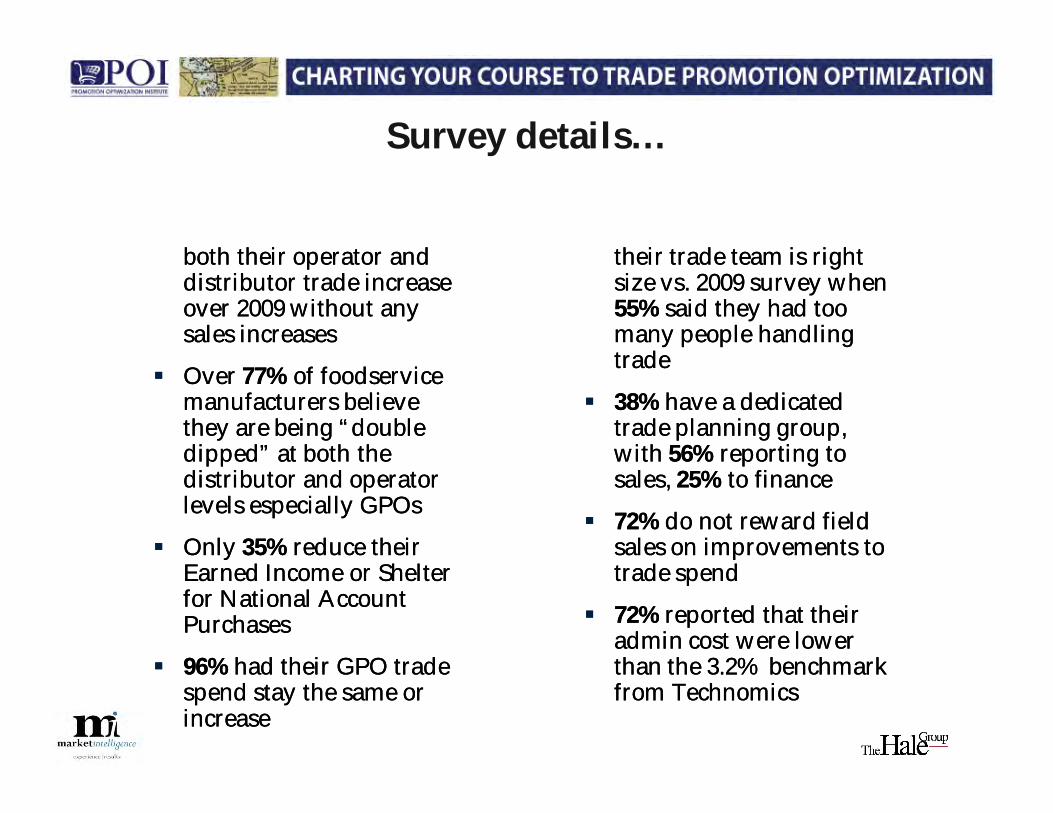

Survey details…

85% of respondents said both their operator and distributor trade increase over 2009 without any sales increases

Over 77% of foodservice manufacturers believe they are being “double dipped” at both the distributor and operator levels especially GPOs

Only 35% reduce their Earned Income or Shelter for National Account Purchases

96% had their GPO trade spend stay the same or increase

85% of respondents said both their operator and distributor trade increase over 2009 without any sales increases

Over 77% of foodservice manufacturers believe they are being “double dipped” at both the distributor and operator levels especially GPOs

Only 35% reduce their Earned Income or Shelter for National Account Purchases

96% had their GPO trade spend stay the same or increase

58% of manufacturer said their trade team is right size vs. 2009 survey when 55% said they had too many people handling trade

38% have a dedicated trade planning group, with 56% reporting to sales, 25% to finance

72% do not reward field sales on improvements to trade spend

72% reported that their admin cost were lower than the 3.2% benchmark from Technomics

58% of manufacturer said their trade team is right size vs. 2009 survey when 55% said they had too many people handling trade

38% have a dedicated trade planning group, with 56% reporting to sales, 25% to finance

72% do not reward field sales on improvements to trade spend

72% reported that their admin cost were lower than the 3.2% benchmark from Technomics

Process Organization

Survey details continued…..

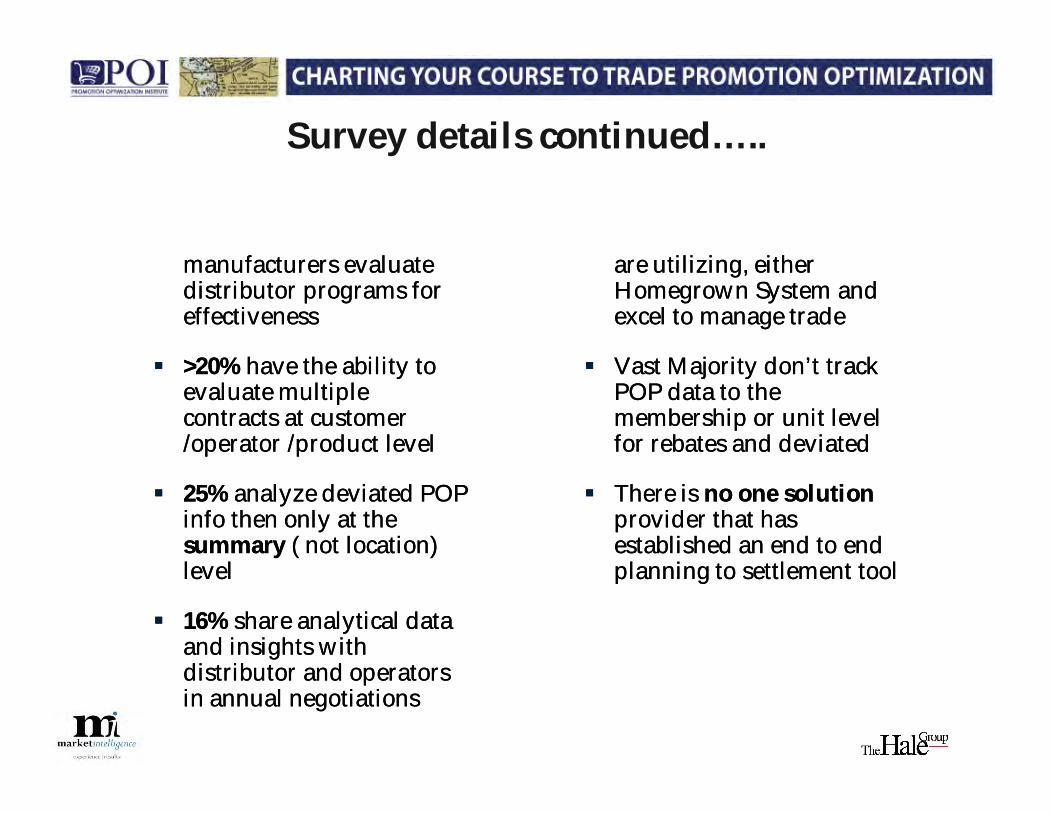

Only 35% of manufacturers evaluate distributor programs for effectiveness

>20% have the ability to evaluate multiple contracts at customer /operator /product level

25% analyze deviated POP info then only at the summary ( not location) level

16% share analytical data and insights with distributor and operators in annual negotiations

Only 35% of manufacturers evaluate distributor programs for effectiveness

>20% have the ability to evaluate multiple contracts at customer /operator /product level

25% analyze deviated POP info then only at the summary ( not location) level

16% share analytical data and insights with distributor and operators in annual negotiations

Majority of Manufacturers are utilizing, either Homegrown System and excel to manage trade

Vast Majority don’t track POP data to the membership or unit level for rebates and deviated

There is no one solution provider that has established an end to end planning to settlement tool

Majority of Manufacturers are utilizing, either Homegrown System and excel to manage trade

Vast Majority don’t track POP data to the membership or unit level for rebates and deviated

There is no one solution provider that has established an end to end planning to settlement tool

Analysis Systems

Page 13

Trade Investment• Outpacing net

sales growth• Declining

product contribution

• Costly to administer

• Difficult to gauge effectiveness

Customer Strategy

•Unable to execute customer strategy due to lack of internal streamlined processes that are:•Fact-based /

analytical•Performance driven•Lots of data- little

useable information

As a result “trade is a strategy of tactics not a tactic of a well thought out strategy”*

* Jim Klass

Page 14

Process•Manufacturers should

revisit their budgeting process

•Opportunity to reduce “double dipping “

Organization•Consider a Trade

Investment Group -trade is the second largest expense after COGS

•Involve Field sales (& brokers) in trade

Analysis•Develop an analytics

group within the Trade Organization

•Develop analytics beyond summary data-drive to unit level

Systems•Review systems

capabilities to support ,planning ,settlement and analytics

•Require EDI PoP to enable analytics

Survey Take aways…..

Page 15

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Agenda

Page 16

Contracted Operators

• 80% of all foodservice operators will be engaged in a contract

Growth

• Continued slow growth battle is now for market share

Information

• Ability to share information and insights cement relationships and drives partnerships

So where are we heading . . . Based on The Hale Group Foodservice 2020 Whitepaper

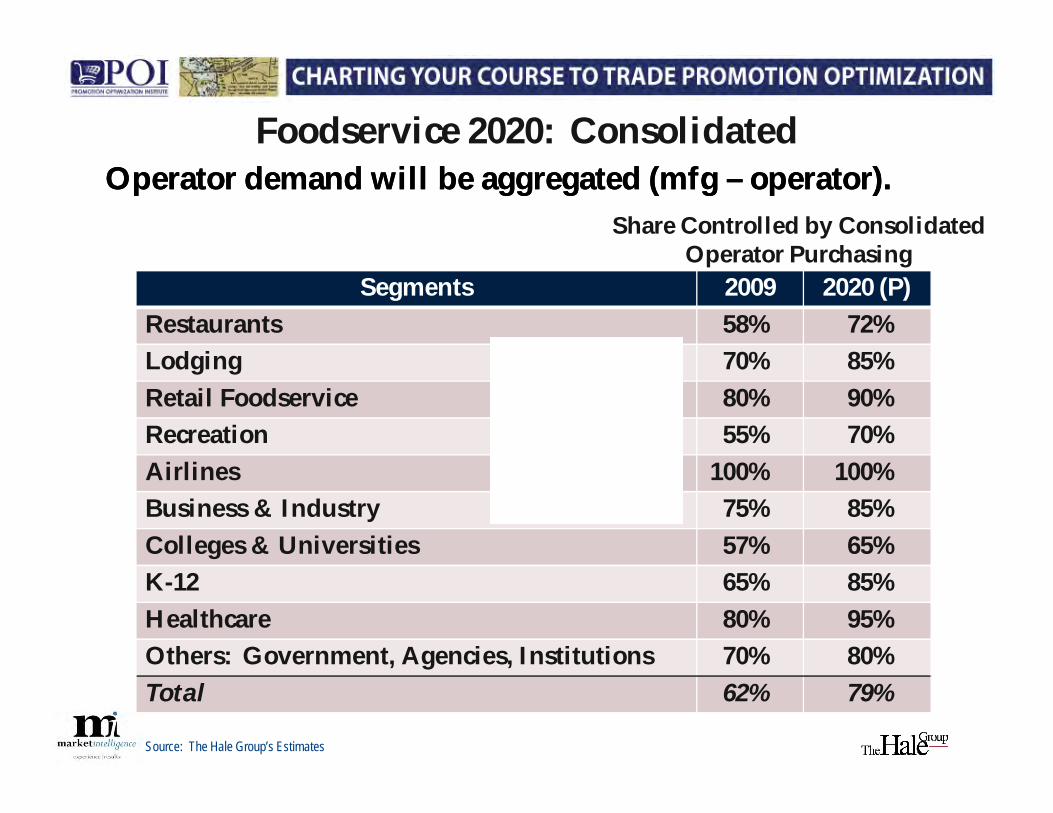

Operator demand will be aggregated (mfg – operator).Operator demand will be aggregated (mfg – operator).Share Controlled by Consolidated

Operator Purchasing

Source: The Hale Group’s Estimates

Segments 2009 2020 (P)Restaurants 58% 72%Lodging 70% 85%Retail Foodservice 80% 90%Recreation 55% 70%Airlines 100% 100%Business & Industry 75% 85%Colleges & Universities 57% 65%K-12 65% 85%Healthcare 80% 95%Others: Government, Agencies, Institutions 70% 80%Total 62% 79%

Foodservice 2020: Consolidated

Fewer but

bigger buyers

Page 18

Therefore by 2020, operator purchases will be: Conducted under structured agreements Negotiated between operator organizations (individual

or managed) and:• Manufacturers, and/or• Distributors

Compliance and consumption building responsibility at a local level

Therefore by 2020, operator purchases will be: Conducted under structured agreements Negotiated between operator organizations (individual

or managed) and:• Manufacturers, and/or• Distributors

Compliance and consumption building responsibility at a local level

Sales processes move up to strategic level – represents millions and 10’s of millions.

Foodservice 2020: Structured

Page 19

Contract terms to build around: Product spec’s Quantities to be purchased Pricing formulas Risk mitigation mechanisms Performance metrics – both parties Rewards and penalties

Therefore,

Contract terms to build around: Product spec’s Quantities to be purchased Pricing formulas Risk mitigation mechanisms Performance metrics – both parties Rewards and penalties

Therefore,

Greater analysis to assure financial and fulfillment conditions are acceptable and viable.

Foodservice 2020: Structured

Page 20

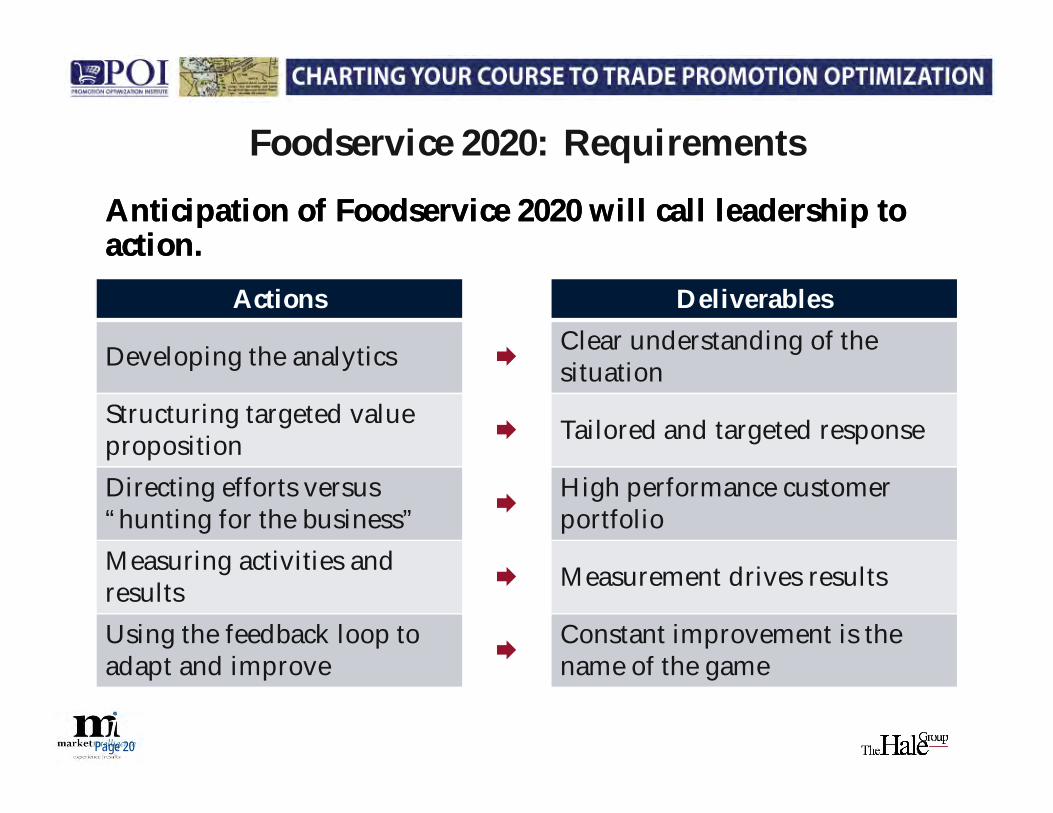

Anticipation of Foodservice 2020 will call leadership to action.Anticipation of Foodservice 2020 will call leadership to action.

Page 20

Actions Deliverables

Developing the analytics Clear understanding of the situation

Structuring targeted value proposition Tailored and targeted response

Directing efforts versus “hunting for the business”

High performance customer portfolio

Measuring activities and results Measurement drives results

Using the feedback loop to adapt and improve

Constant improvement is the name of the game

Foodservice 2020: Requirements

Implications…

More transparency through out the supply chain

Drive to promote at the consumer level

Reallocation of trade funds to reflect ROI potential

Stricter enforcement of program requirement at both the distributor and operator levels

Trade dollars will shift from the distributor to the operator and consumer

More transparency through out the supply chain

Drive to promote at the consumer level

Reallocation of trade funds to reflect ROI potential

Stricter enforcement of program requirement at both the distributor and operator levels

Trade dollars will shift from the distributor to the operator and consumer

Trade will become a strategic part of the organization

Trade will develop as a separate and distinct group with Director/VP level responsibilities

Field Sales will be measured on their trade results

Brokers and Field sales will have compliance and ROI responsibilities as part of their compensation

Trade will become a strategic part of the organization

Trade will develop as a separate and distinct group with Director/VP level responsibilities

Field Sales will be measured on their trade results

Brokers and Field sales will have compliance and ROI responsibilities as part of their compensation

Process Organization

Implications…..

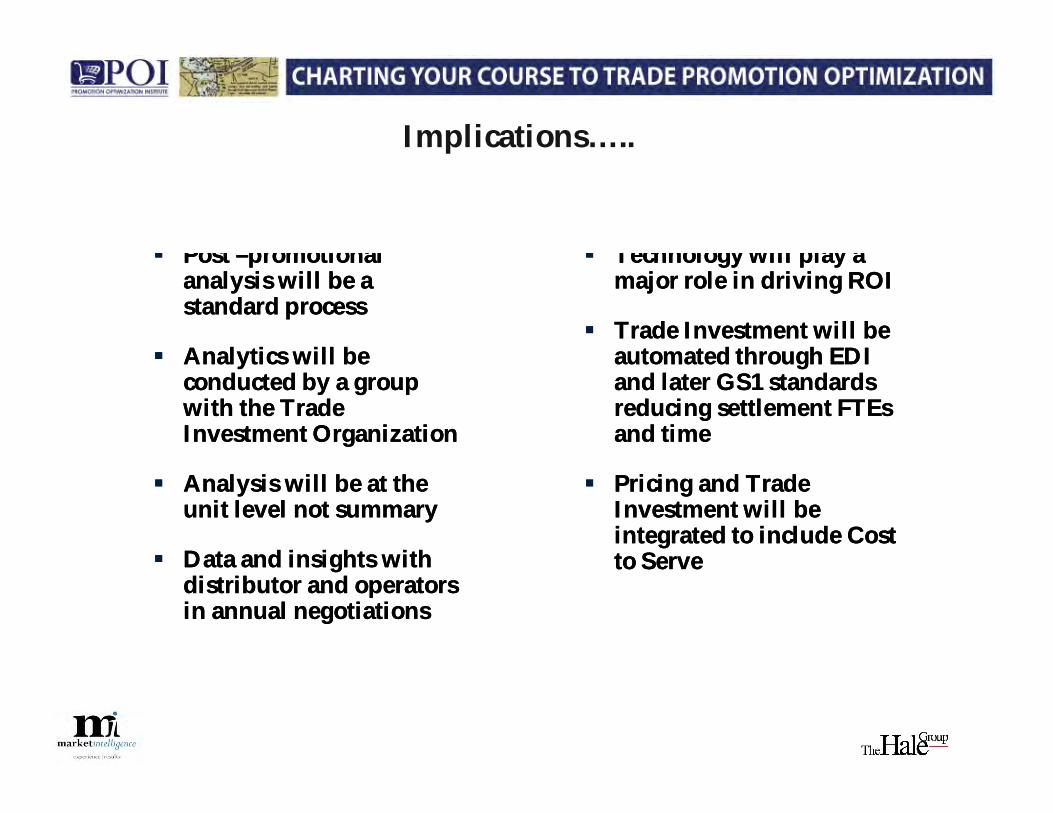

Post –promotional analysis will be a standard process

Analytics will be conducted by a group with the Trade Investment Organization

Analysis will be at the unit level not summary

Data and insights with distributor and operators in annual negotiations

Post –promotional analysis will be a standard process

Analytics will be conducted by a group with the Trade Investment Organization

Analysis will be at the unit level not summary

Data and insights with distributor and operators in annual negotiations

Technology will play a major role in driving ROI

Trade Investment will be automated through EDI and later GS1 standards reducing settlement FTEs and time

Pricing and Trade Investment will be integrated to include Cost to Serve

Technology will play a major role in driving ROI

Trade Investment will be automated through EDI and later GS1 standards reducing settlement FTEs and time

Pricing and Trade Investment will be integrated to include Cost to Serve

Analysis Systems

Page 23

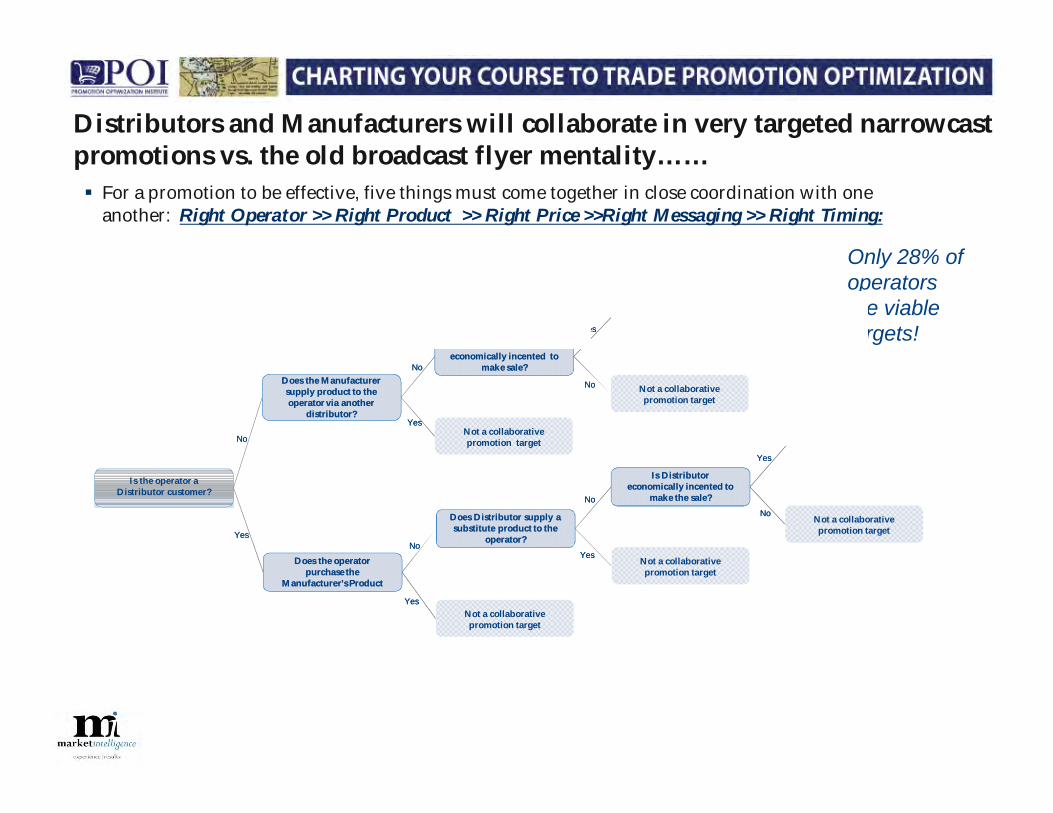

Does the operator purchase the

Manufacturer’s Product

Does the operator purchase the

Manufacturer’s Product

Does the Manufacturer supply product to the operator via another

distributor?

Does the Manufacturer supply product to the operator via another

distributor?

Is Distributor economically incented to

make the sale?

Is Distributor economically incented to

make the sale?

Is the operator a Distributor customer?

Not a collaborative promotion target

Not a collaborative promotion target

Not a collaborative promotion target

Not a collaborative promotion target

Does Distributor supply a substitute product to the

operator?

Does Distributor supply a substitute product to the

operator?

Collaborative Promotion target identified

Is the Distributor economically incented to

make sale?

Is the Distributor economically incented to

make sale?

Collaborative Promotion target identified

Not a collaborative promotion target

YesYes

NoNo

YesYes

NoNo

NoNo

YesYes

YesYes

NoNoYesYes

NoNoNoNo

YesYes

Scientifically Targeted Approach

The infrastructure and analytical capabilities now available make the odds of trade investments being squandered obsolete and enable a new era of collaborative

promotion with trading partners.

Distributors and Manufacturers will collaborate in very targeted narrowcast promotions vs. the old broadcast flyer mentality…… For a promotion to be effective, five things must come together in close coordination with one

another: Right Operator >> Right Product >> Right Price >>Right Messaging >> Right Timing:

Only 28% of operators are viable targets!

Page 24

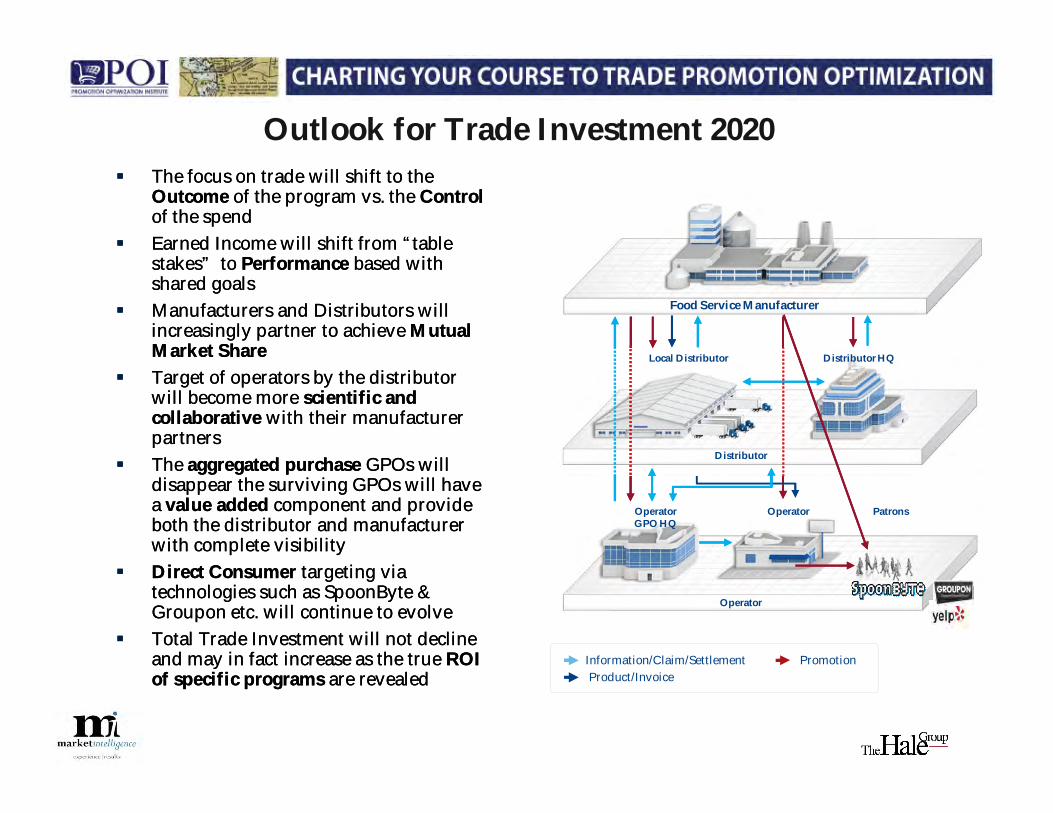

The focus on trade will shift to the Outcome of the program vs. the Controlof the spend

Earned Income will shift from “table stakes” to Performance based with shared goals

Manufacturers and Distributors will increasingly partner to achieve Mutual Market Share

Target of operators by the distributor will become more scientific and collaborative with their manufacturer partners

The aggregated purchase GPOs will disappear the surviving GPOs will have a value added component and provide both the distributor and manufacturer with complete visibility

Direct Consumer targeting via technologies such as SpoonByte & Groupon etc. will continue to evolve

Total Trade Investment will not decline and may in fact increase as the true ROI of specific programs are revealed

The focus on trade will shift to the Outcome of the program vs. the Controlof the spend

Earned Income will shift from “table stakes” to Performance based with shared goals

Manufacturers and Distributors will increasingly partner to achieve Mutual Market Share

Target of operators by the distributor will become more scientific and collaborative with their manufacturer partners

The aggregated purchase GPOs will disappear the surviving GPOs will have a value added component and provide both the distributor and manufacturer with complete visibility

Direct Consumer targeting via technologies such as SpoonByte & Groupon etc. will continue to evolve

Total Trade Investment will not decline and may in fact increase as the true ROI of specific programs are revealed

Outlook for Trade Investment 2020

OperatorOperator GPO HQ

Food Service Manufacturer

Local Distributor

Distributor

Distributor HQ

Operator

Patrons

PromotionInformation/Claim/SettlementProduct/Invoice

Page 25

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Quick Intros Definition of Trade Investment Review of where we are… 2010 Foodservice Trade Survey Point of View -Where we are heading…. MarketIntelligence/ Hale

Group 2020 Panel Discussion with • Dror Karidi, Senior Director Operational Strategy- US

Foodservice • Scott Modica Vice President Smithfield Packing

Q&A

Agenda

Page 26

Where do you see the industry going? What are the significant factors that would change?

How is distribution and B2B different than B2C and are there any analogies to be made?

How do you see collaboration between Manufacturers, Distributors and Operators changing over time?

Where do you see the industry going? What are the significant factors that would change?

How is distribution and B2B different than B2C and are there any analogies to be made?

How do you see collaboration between Manufacturers, Distributors and Operators changing over time?

Page 26

Questions for Dror and Scott:

Page 27

Thank You!Thank You!

Page 27

![The role of trade and investment liberalization in the sugar … · 2018-05-31 · major consumer foodservice chains [23]. In 2013, sales of Coca-Cola and PepsiCo alone accounted](https://img.pdfslide.us/doc/110x75/5f0889467e708231d4227eec/the-role-of-trade-and-investment-liberalization-in-the-sugar-2018-05-31-major.jpg)