Embed Size (px)

Citation preview

Risk. Reinsurance. Human Resources.

Food and Drink InperspectiveIn this issue

Welcome to this Spring 2015 edition of Inperspective; Aon UK’s review of the risk and insurance issues facing the food and drink industry.

As stories about economic recovery continue, we learned recently that UK food and drink manufacturing has stepped up its production. As reported in Food Manufacture magazine, The Confederation of British Industry Industrial Trends Survey found that output in the food and drink sector in the three months to February 2015 was particularly strong. More than half (59%) of manufacturers reported rising output, against 22% who indicated a fall.

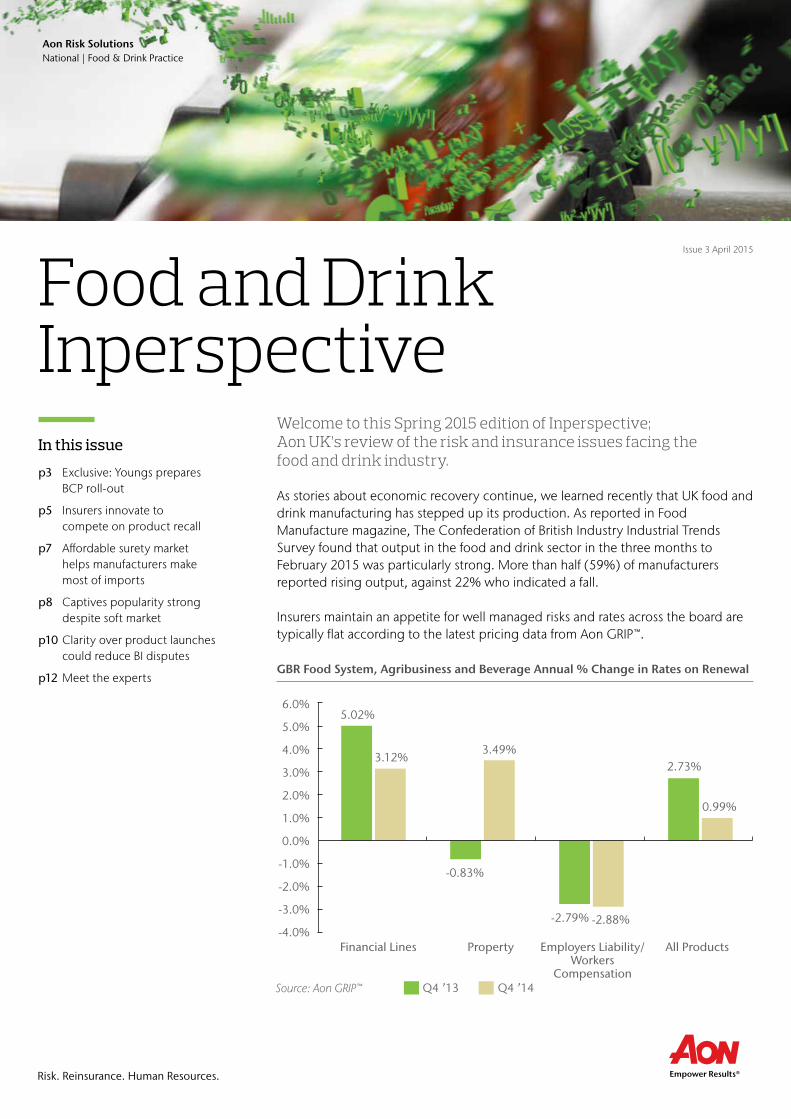

Insurers maintain an appetite for well managed risks and rates across the board are typically flat according to the latest pricing data from Aon GRIP™.

GBR Food System, Agribusiness and Beverage Annual % Change in Rates on Renewal

p3 Exclusive: Youngs prepares BCP roll-out

p5 Insurers innovate to compete on product recall

p7 Affordable surety market helps manufacturers make most of imports

p8 Captives popularity strong despite soft market

p10 Clarity over product launches could reduce BI disputes

p12 Meet the experts

Aon Risk Solutions National | Food & Drink Practice

Issue 3 April 2015

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

-1.0%

-2.0%

-3.0%

-4.0%

5.02%

3.12%3.49%

2.73%

0.99%

-0.83%

Financial Lines

Source: Aon GRIP™ Q4 ’13 Q4 ’14

Property All ProductsEmployers Liability/ Workers

Compensation

-2.79% -2.88%

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 2

In addition to this analysis, Inperspective is packed with content on how the industry is managing risk in a changing environment. In this edition we are delighted to have the insights of Paul Fenner, Director of Health and Safety Environment at Youngs Seafood, who reveals his company’s business continuity strategy and how it drives a flexible insurance programme.

We also have insightful pieces from our own specialist teams. From trade credit, Barrie Watson shows how the food and drink industry is beginning to benefit from an affordable surety market. He explains that cash-intensive duty deferment obligations for manufacturers when they import raw materials are now being managed more effectively with this clever risk transfer option.

Of course, risk transfer can take myriad forms and in this edition we hear from Aon’s captive experts on how the food and drink industry is managing risk in the self-insurance arena. As one of the largest sectors in Aon’s own captive management portfolio, the industry is well represented as a user of captives and David Crofts, Managing Director, ARS UK Global Risk Solutions at Aon, says that continued softening of rates on the traditional insurance market has not dampened enthusiasm.

The final two articles in this edition provide perspectives on business interruption and product recall. Andy King, Head of Claims and Risk Accounting MENA at Aon, observes some interesting trends from a sector known for its reliance on new product development. He says a failure to properly inform underwriters – and a lack of action from insurers themselves – about the potential income new products could generate, has left some manufacturers disappointed when their business interruption claims are calculated.

In the product recall market, Aon Team Leader for Product Recall and Contamination Kary Yates, says a downward push on pricing has encouraged insurers to innovate, with crisis management consulting a helpful option for manufacturers.

We hope you find this edition of Inperspective a useful resource and invite you, as ever, to get in touch with any questions you may have.

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 3

Exclusive: Youngs prepares BCP roll-outChilled and frozen food specialists Young’s Seafood is embarking on a business wide deployment of Aon’s Continuity Complete solution during 2015 after a successful trial. Inperspective talks exclusively to Paul Fenner, Director of Health and Safety Environment at Young’s, about the company’s business continuity strategy and how it drives a flexible insurance programme.

As one of the UK’s best known frozen and chilled food brands, Young’s Seafood has an enviable reputation in the industry. Representing the largest business within the Findus Group, the company’s nine sites and 3500 employees contribute to a business turning over more than £600m a year. In charge of the company’s risk management framework is Paul Fenner, who has continued Young’s relationship with Aon after he joined the business in 2013. “We work very closely with Aon to create plans, processes and coverage that are suitable for our risk profile. We’re prepared to take retain risk using innovative arrangements and deductibles where appropriate. This is enabled by regular benchmarking projects against other organisations in our sector but this year our priority is deploying a new business continuity planning system.”

Paul explains that Young’s previous BCP system had also been developed with Aon’s support, and Continuity Complete has helped the company deploy a newer, more flexible framework. “The existing paper based BCP system was actively managed and delivered a good understanding of our exposures when we carried out scenario tests. However it required considerable resources in order to keep it up to date. As an electronic system, once you’ve input data into Continuity Complete, maintaining its currency is far less labour intensive. Now we can have nine different variations of the system, all hosted securely online.”

Broader view of risk

As Young’s BCP capability has evolved, Paul’s view of risks facing the company has been enhanced. “Our sites are a profit centre in their own right, so they’ve each got a managing director and therefore their own supply chain risks and customers to answer to. Continuity Complete fits in perfectly with this structure, because it can undergo scenario testing at each level of the business.

“It’s highlighted some supply chain risks that we may have been comfortable with before, but now consider key considerations,” Paul adds. “Alongside the obvious raw material supply chain risks, Continuity Complete allows us to integrate things like packaging, film, machine parts, haulage and engineering services. Once you build this satellite view, you very quickly identify other single points of failure that you’d not previously been aware of.”

Paul FennerDirector of Health and Safety Environment Young’s Seafood

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 4

Decentralising BCP

A further benefit, says Paul, is how local managers are now far more able to implement BCP at their own site. “The managers at the individual sites understand and own their own business continuity; it’s not the ones in head office. When an incident occurs they’re already prepared with a framework based on triggers like health and safety, incident value or severity. The site can deal with the incident, manage it, escalate it if necessary and the business can accommodate to make sure that we at least keep customers supplied which is the fundamental goal of the project.”

What’s next?

Young’s Livingston operation has been the first in the network to pilot Continuity Complete and having deployed the software for 12 months the company is now embarking on a roll out across all of its sites by the Autumn of 2015. Paul says his aims do not stop at manufacturing; “We looked at Continuity Complete and have subsequently put together a BCP for the head office. We’re not just looking at production and manufacturing, we’re looking at the support functions, head office, laboratories and all the things that we actually need to keep production going. That’s as a result of the lessons we have learnt in the last two years working with Aon.”

For further information on Business Continuity Management contact Vince West.

Vince West +44 (0)20 7086 [email protected]

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 5

Insurers innovate to compete on product recallA downward push on pricing has encouraged insurers to innovate, with crisis management consulting a helpful option for manufacturers. Aon Team Leader for Product Recall and Contamination, Kary Yates, highlights the latest market trends in food and drink.

Market dynamics shifted again in 2014 toward increased competition and new entrants at Lloyd’s at the beginning of 2015, while global insurers also eyed product recall as a profitable business line leading to flat and in many cases, downward pressure on prices.

Where food and drink company turnovers are increasing, market appetite is strong for the best accounts, while decreased rates of up to 10-20% are being seen on renewals for the most attractive businesses.

Wordings vary widely and clients have to be aware of the advantages and disadvantages of moving from one carrier to another, however terms and conditions have remained quite stable across Aon’s UK food and drink portfolio. This has presented an opportunity for Aon to push for enhancements to market wordings which have included adding sub limits for claims preparation expenses utilising Aon’s complex claims teams and higher sub limits on rehabilitation expenses.

In addition, crisis consultancy is becoming a key aspect of the product recall armoury and with a 5% standard bursary (of net premium) available for clients to spend with their insurer’s crisis consultant, clients can take some comfort by having that expertise available to assist them in the review of their supply chain management, business continuity and recall management plans.

On the claims side there were fewer limit losses than we saw in 2013, but a general increase in the number of recalls and an associated rise in costs is being driven by more regulation, greater media attention and more stringent contractual obligations being passed down the supply chain.

For example, regulators are increasing random testing in an attempt to discover economically motivated adulteration of food and the US regulators have stepped up their inspections of food manufacturing facilities outside of the US in respect of foreign companies exporting into the US.

New in 2014 was the enforcement of criminal prosecutions in the US by the FDA (US Food and Drug Administration) and there are currently some very high profile cases going through court, including the Peanut Corporation of America and Wright Brothers.

These factors obviously put insurers on notice, and they will be observant of manufacturers with regulatory exposures to ensure that have taken all necessary steps to mitigate those risks and ensure a robust supply chain.

Kary YatesTeam Leader | Crisis Management Aon Risk Solutions | Global Broking Centre

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 6

The Elliott Review

The review’s publication in September 2014 was in response to the horsemeat scandal the year before. In response, underwriting appetite has been restricted in instances where a client does not have the proper control procedures in place. Markets tend to avoid writing risks where the client cannot demonstrate that they manage their supply chain well or source ingredients from suppliers and distributors based in unregulated jurisdictions.

For further information on Product Recall contact Kary Yates.

Kary Yates +44 (0)20 7086 [email protected]

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 7

Affordable surety market helps manufacturers make most of importsA competitive market for guarantee insurance products means food and drink companies are enjoying greater flexibility and less pressure on their cash flow. As Barrie Watson, Executive Client Director at Aon Trade Credit, Special Products explains, Surety Bonds and Guarantees can provide a helpful window of opportunity.

It’s arguable that the surety bond marketplace is one of the best kept secrets in the industry’s finance department locker. These unsecured facilities are not insurance per se, but they are issued by insurers as a competitor to bank guarantees with the UK’s food and drink manufacturing sector standing to benefit considerably from their growing availability.

As one of the country’s largest single import markets manufacturers will frequently have a duty deferment account with Her Majesty’s Revenue & Customs (HMRC), in respect of non-EU imports.

Within that account HMRC allows them to defer tax owed to the government for a period of up to 45 days in return for which the retailer or wholesaler may have to provide bank guarantees. This is fine, except for the fact that a bank guarantee will potentially tie up cash and impact the bank credit line which could otherwise be put to work for the business. Having recognised this demand, surety underwriters have increasingly stepped into the breach meaning retailers are able to get products onto their shelves without the stranglehold of cash tied up at the bank to guarantee deferred duty payments.

Similarly, importers of foodstuffs, particularly meats, have legal obligations to provide security under provisions of European Commission (EC) regulation. In a common scenario, a company may have to post tens of millions in guarantees to the Rural Payments Agency, even while the nature of the regulations mean the actual exposure is a mere fraction of this.

As a result of improving conditions in the surety markets, there is aggressive competition for business from surety providers and a consistent reminder that freeing up a credit line enables reinvestment into the business. With that competition comes more products including deferred consideration guarantees for acquisitions, deductible guarantees, as well as a plethora of traditional contractual bonds providing surety in terms of performance, retention, advance payment and other criteria.

This increasing sophistication is also translating into a broader licencing regime and an expansion in the number of global territories where these bonds can be issued.

For further information contact Barrie Watson.

Barrie Watson +44 (0)20 7086 [email protected]

Barrie WatsonExecutive Client DirectorAon Risk Solutions | Trade Credit

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 8

Captives popularity strong despite soft marketFood and drink manufacturing companies represent one of the largest sectors in the Aon Captive portfolio. Inperspective speaks with David Crofts, Managing Director, ARS UK Global Risk Solutions who explains that eight years of softening commercial insurance rates have done nothing to dampen the food and drink sector’s enthusiasm for captive solutions.

With such a unique risk profile where competition, regulation and quality standards are so important, it’s no wonder the UK’s food and drink manufacturing sector is the fourth largest industry group in the Aon Captive management portfolio. 76 captives operate in support of some of the country’s best known brands and are increasingly providing ‘risk incubation’ for the parent company where the commercial insurance market is currently not perceived to have a compelling risk transfer solution.

“The concept of risk incubation for industries like food and drink manufacturing is becoming increasingly well known,” says David Crofts. “Risk incubation is the process of building a company’s knowledge and understanding of an emerging risk in conjunction with the insurance market. Working together, over a period of time, the enhanced understanding of the exposure enables better informed decision making regarding risk financing and risk transfer options.”

As a former risk manager at a global confectionery company and through the risk consulting partnership in place with Aon’s global client base, David is well placed to comment on the client’s approach to captive financing of risk. He observes that the popularity of captives has moved in the opposite direction to many predictions. “There was historically an assumption that with falling insurance prices, captive utilisation would drop as well. But with the backdrop of a soft insurance market for the last eight years, the fact that captives have continued to be utilised and, in many cases, extended, shows that their use as strategic risk management tools is well established and growing.”

Now, the challenge for manufacturers is increasingly around supply chains and the interconnectivity of risks. “In mid-February, we began to see the latest example of the potential problems the industry can face, with the revelations related to the substitution of raw materials,” adds David. “Like the horsemeat crisis, food manufacturers that have a less than robust supply chain may find themselves vulnerable. The story has all the hallmarks of interconnected risk, with regulators across multiple jurisdictions potentially imposing sanctions against companies that are found to have used tainted or counterfeit raw materials. Although this story has yet to fully unfold, the consequences in terms of product recall, liability and reputational risk could be severe.”

David CroftsManaging Director | UKAon Risk Solutions | Global Risk Solutions

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 9

As Aon’s review of commercial product liability markets reveals, many insurers are now looking to support food and drink manufacturers with crisis consulting services to handle situations in which reputations are at risk. “The insurance market hasn’t always been quick to respond to the evolving risk exposures that manufacturers face related to product recall,” David says. “The market has covered certain perils that have the potential to cause illness or bodily injury. In recent years, coverage has been extended to include government mandated recall. But a lot of organisations don’t want to differentiate between those product recalls that the market has been willing to cover and those that fall outside of the scope of the policy coverage because it doesn’t help risk managers to explain the value of the coverage to their internal stakeholders or manage expectations in the event of an actual claim.

“This is an area where we have seen captives looking to provide a solution in order to provide broader coverage and incremental capacity, particularly on global programmes for brands being sold around the world.”

For further information on Captives, contact David Crofts.

David Crofts +44 (0)20 7086 [email protected]

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 10

Clarity over product launches could reduce BI disputes Failures to account for the potential cost of delays to product launches are creating challenges for risk managers in the manufacturing sector. Inperspective talks to Andy King, Head of Claims and Risk Accounting MENA at Aon, who says nowhere is this truer than when companies and their insurers disagree over business interruption losses.

In a highly competitive market where food and drink manufacturers frequently rely on reinvigorating existing product lines or launching entirely new ones, it takes considerable care to build in mitigation strategies should a launch be delayed.

Andy King, Head of Claims and Risk Accounting MENA (Middle East & North Africa) at Aon say’s the challenge is particularly acute for medium sized companies. “Typically, these are the fastest growing manufacturers in the sector, where many are experiencing double digit increases. They often operate from single sites and rely on launching new products or collections outside of typical seasonal cycles to stay competitive.

“Of course it’s true of any business that without careful planning you can be a victim of your own success. But manufacturers that build their business model around being nimble enough to get products to market quickly create an inbuilt business interruption exposure for themselves.”

Andy has worked on a number of BI claims in the past year in which product launches had not been adequately defined in the original underwriting presentation. “You can only imagine what kind of pressure a delayed product launch will cause a manufacturer. Being first to market has never been more important, and if an incident occurs which cannot be quickly rectified, manufacturers have little to fall back on other than their BI cover.”

Supply chain is another area that is becoming more acute for companies. Single supplier agreements indicate serious reliability on key suppliers and these exposures need evaluating carefully. “ A supply chain review is essential and the exposure needs properly monetising”, says Andy. “The good news for clients is that my colleagues and I in the claims and risk accounting practice have experience of handling these claims which we are able to apply when carrying out supply chain reviews. And, as we are fully regulated by the FCA we are the go-to group in Aon in this area as we can advise directly on policy limits and appropriate policy wordings so that the client transfers the risk correctly.”

Triggers for BI losses are extremely varied, and Andy says the prudent measure is to conduct a BI review which accurately costs and monetises the necessary measures. “A forecast should be built into the company’s estimated maximum loss so that when a BI claim is brought there is no doubt as to what you are going to be claiming for and what measures you’re going to be taking in the event of a claim.”

Andy KingHead of Claims and Risk Accounting | MENAAon Risk Solutions | Global Risk Consulting

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 11

Inadequate coverage?

Another concern Andy has with the manufacturing sector has been in the prevalence of 12 month maximum indemnity periods. “Knowing how long it can take to bring a manufacturing facility back on line, it is essential for businesses to give themselves enough slack to cover their lost profits under a BI policy. Lead times for manufacturing equipment which is very often bespoke can be lengthy and a short maximum indemnity period will be inadequate to reinstate equipment and allow the business to recover.”

Meanwhile, in a similar trend to those identified by Aon’s product recall experts, Andy says claims preparation is increasingly on the menu. “Advocacy for clients so that they don’t have to devote management time in the event of a claim is an important consideration for many manufacturers; this is getting headlines in the product recall arena where crisis consulting has become an important addition to many policies. However in more general terms, claims preparation simplifies the process of quantifying and documenting losses; we are able to guide risk managers on what steps they can take to ensure that restoration is achieved and the claim is handled satisfactorily.”

For further information contact Andy King.

Andy King [email protected]

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 12

David CroftsManaging Director | UKAon Risk Solutions | Global Risk Solutions Solutions

Andy KingHead of Claims and Risk Accounting | MENAAon Risk Solutions | Global Risk Consulting

David Crofts is Managing Director of ARS UK Global Risk Solutions with responsibility for bringing our consulting led broking and servicing proposition to ARS major accounts. David joined Aon in December 2010 from Cadbury where he held a number of international roles over 12 years including Group Risk and Property Director based in the UK.

He is based in London focusing on alignment of Aon’s risk consulting proposition with our Global broking and servicing capability in order to deliver a market leading approach towards major clients. David also acts as the Senior Account Manager for a number of clients in the UK.

He is a graduate of Nottingham University and holds an FIA diploma in Actuarial Analysis and Techniques.

Andy King is a Chartered Loss Adjuster with 32 years’ experience at handling major losses both in the UK and abroad. He has been involved in some of the largest losses within the London market. He has also carried out a number of expert witness assignments in respect of both insurance and commercial disputes.

Andy has gained a wide experience of dealing with large and complex insurance claims, particularly in respect of business interruption across a wide range of industries, including power, energy, petrochemical, hospitality and leisure, food and beverage, and metal industries.

In addition Andy has experience in managing and calculating product recall claims and putting together proofs of loss in respect of fraud and misfeasance losses. He has appeared as an expert witness in arbitrations and court proceedings and has been involved in managing difficult and disputed claims, working closely with lawyers and other experts.

Andy has been involved in managing large teams and setting strategic direction and goals. He is involved in mentoring programmes for graduates.

Andy has carried out numerous lectures throughout the UK and abroad on business interruption and major loss topics. He has appeared on BBC Radio 4 commenting on insurance matters.

Meet the experts

aon.co.uk/food-drink

Inperspective | Food and Drink | April 2015 FPNAT.112 13

Barrie WatsonExecutive Client DirectorAon Risk Solutions | Trade Credit

Kary YatesTeam Leader | Crisis Management Aon Risk Solutions | Global Broking Centre

Barrie Watson has over 17 years’ experience working with a number of broking houses including Rattner Mackenzie Ltd and Arthur J Gallagher. Barrie has experience working with international corporations designing and placing trade credit and political risk, including structured trade credit, programmes across Asia, Europe, Latin America and the Middle East. He has also worked on projects with the Export Credit Agency PT ASEI – Indonesian, designing beneficial trade finance facilities for exporters. Barrie also places innovative surety facilities for clients including Deductible Guarantees and Deferred Consideration Bonds. He has a BA (Hons) in Risk Management.

Kary Yates has 29 years’ experience in producing and placing property and casualty business with emphasis on product recall and contamination since 2002. Kary has 14 years’ broking experience in the London market, including Lloyd’s of London and the London company market. Kary has a number of qualifications in food and drink including a Level 2 and 3 in Food Safety Supervision for Manufacturing.

Vince WestHead of Business Continuity PracticeAon Risk Solutions | Global Risk Consulting

Vince West has considerable experience formulating and advising clients on their respective business continuity strategies and has been engaged on business continuity projects with many leading organisations. His extensive experience of business continuity management has been deployed across sectors including Food Manufacturing , Petro- Chemical, Telecommunications, Banking, Finance and Insurance, Defence, IT, Publishing, Retail, Regional Development and other Government Agencies.

Risk. Reinsurance. Human Resources.

About AonAon plc (NYSE:AON) is a leading global provider of risk management, insurance and reinsurance brokerage, and human resources solutions and outsourcing services. Through its more than 66,000 colleagues worldwide, Aon unites to empower results for clients in over 120 countries via innovative and effective risk and people solutions and through industry-leading global resources and technical expertise. Aon has been named repeatedly as the world’s best broker, best insurance intermediary, best reinsurance intermediary, best captives manager, and best employee benefits consulting firm by multiple industry sources. Visit aon.com for more information on Aon and aon.com/manchesterunited to learn about Aon’s global partnership with Manchester United. Aon UK Limited is authorised and regulated by the Financial Conduct Authority. Aon UK Limited Registered Office: 8 Devonshire Square, London EC2M 4PL. Registered No. 210725. VAT Registration No. 480 8401 48. Some links on this website may redirect you to third party sites. Aon is not responsible for this content. Telephone calls are recorded and may be monitored. © 2015 Aon UK Limited. FP number: FPNAT.112

![‘Drink Free Days’ Campaign · • Women “drink and do” – often talking about drink being a companion to an activity, e.g. cooking, socialising • Men “drink and [not]](https://img.pdfslide.us/doc/110x75/5e8c20eff6276811d42dbdd8/adrink-free-daysa-campaign-a-women-aoedrink-and-doa-a-often-talking-about.jpg)