Embed Size (px)

Citation preview

Appendix 1: Materials used by Mr. Kos

November 1, 2005 103 of 114

3.00

3.50

4.00

4.50

5.00

6/1 7/1 8/1 9/1 10/13.00

3.50

4.00

4.50

5.009/20 FOMC +25bps

10/24 Bernanke Nomination

8/29 Hurricane Katrina

6/30 FOMC+25bps

8/9 FOMC+25bps

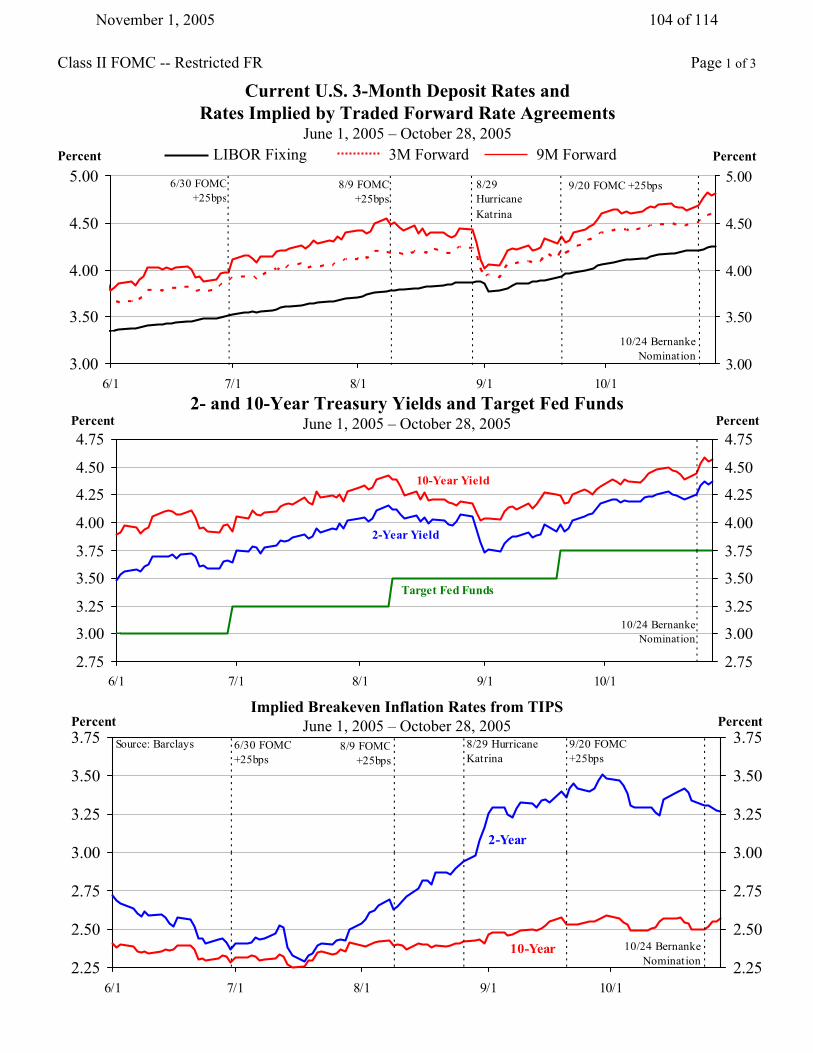

Current U.S. 3-Month Deposit Rates and Rates Implied by Traded Forward Rate Agreements

June 1, 2005 – October 28, 2005LIBOR Fixing 3M Forward 9M Forward PercentPercent

Page 1 of 3

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

6/1 7/1 8/1 9/1 10/1

Percent

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75Percent

2-Year Yield

10-Year Yield

Target Fed Funds

10/24 Bernanke Nomination

2- and 10-Year Treasury Yields and Target Fed FundsJune 1, 2005 – October 28, 2005

Class II FOMC -- Restricted FR

Implied Breakeven Inflation Rates from TIPSJune 1, 2005 – October 28, 2005

2.25

2.50

2.75

3.00

3.25

3.50

3.75

6/1 7/1 8/1 9/1 10/1

Percent

2.25

2.50

2.75

3.00

3.25

3.50

3.75Percent

2-Year

10-Year

8/29 Hurricane Katrina

Source: Barclays 9/20 FOMC +25bps

8/9 FOMC+25bps

6/30 FOMC+25bps

10/24 Bernanke Nomination

November 1, 2005 104 of 114

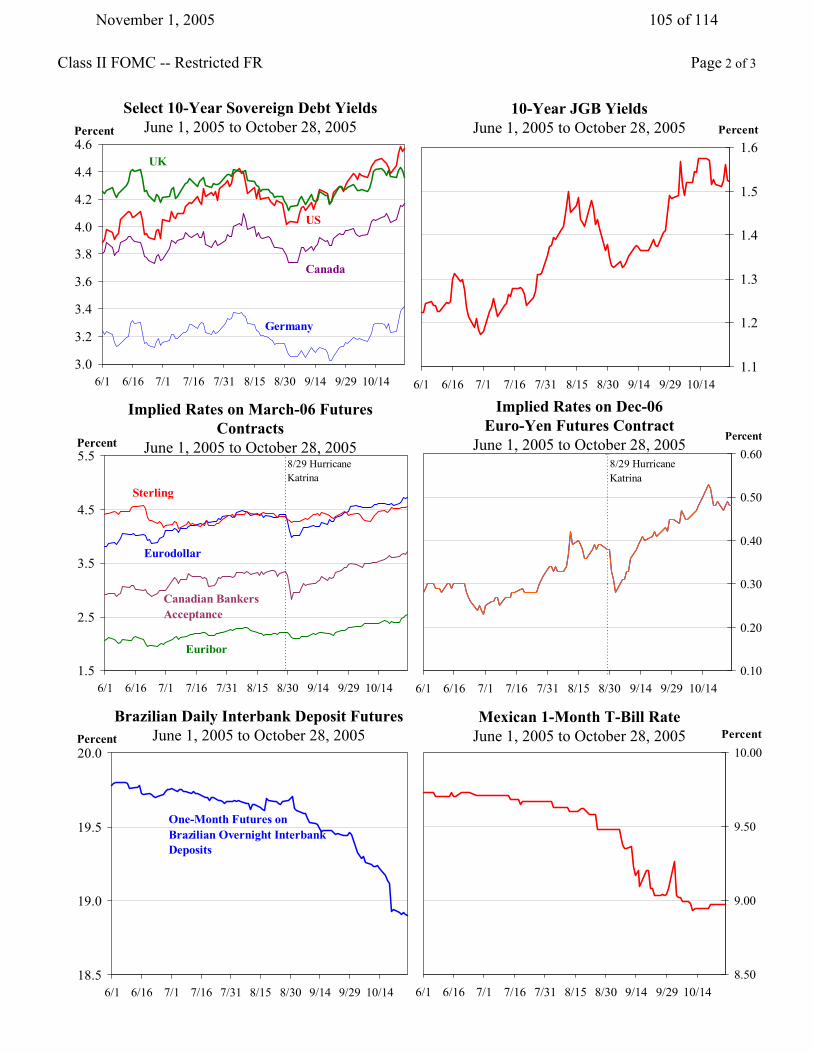

Select 10-Year Sovereign Debt Yields June 1, 2005 to October 28, 2005

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14

Percent

Germany

Canada

US

UK

10-Year JGB Yields June 1, 2005 to October 28, 2005

Page 2 of 3Class II FOMC -- Restricted FR

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/141.1

1.2

1.3

1.4

1.5

1.6Percent

Implied Rates on March-06 Futures Contracts

June 1, 2005 to October 28, 2005

1.5

2.5

3.5

4.5

5.5

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14

Percent

Sterling

Canadian Bankers Acceptance

Eurodollar

Euribor

8/29 Hurricane Katrina

Implied Rates on Dec-06 Euro-Yen Futures Contract

June 1, 2005 to October 28, 2005

Brazilian Daily Interbank Deposit FuturesJune 1, 2005 to October 28, 2005

18.5

19.0

19.5

20.0

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14

Percent

One-Month Futures on Brazilian Overnight Interbank Deposits

Mexican 1-Month T-Bill RateJune 1, 2005 to October 28, 2005

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/140.10

0.20

0.30

0.40

0.50

0.60Percent

8/29 Hurricane Katrina

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/148.50

9.00

9.50

10.00Percent

November 1, 2005 105 of 114

Page 3 of 3Class II FOMC -- Restricted FR

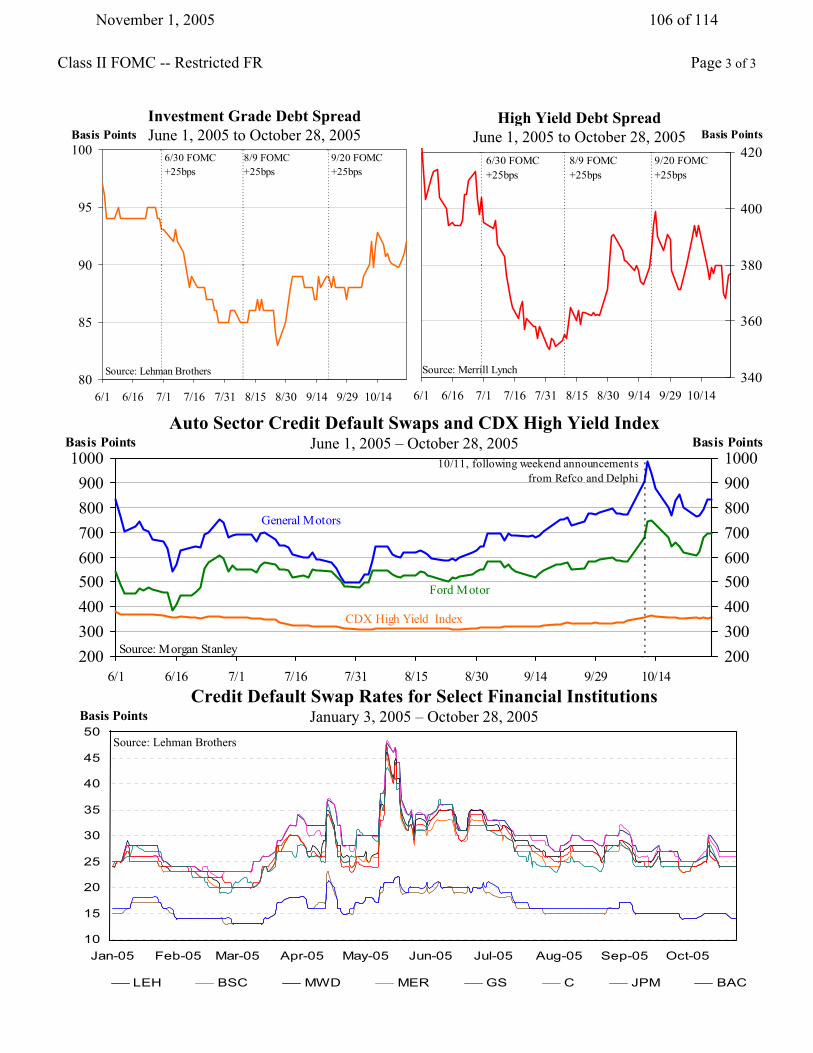

Banks/Brokerage 5 Year CDS

10

15

20

25

30

35

40

45

50

Jan-05 Feb-05 Mar-05 Apr-05 May-05 Jun-05 Jul-05 Aug-05 Sep-05 Oct-05

LEH BSC MWD MER GS C JPM BAC

Credit Default Swap Rates for Select Financial Institutions January 3, 2005 – October 28, 2005Basis Points

Auto Sector Credit Default Swaps and CDX High Yield IndexJune 1, 2005 – October 28, 2005

Source: Lehman Brothers

200300400500600700800900

1000

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14

Basis Points

2003004005006007008009001000

Basis Points

Source: Morgan Stanley

General Motors

CDX High Yield Index

Ford Motor

10/11, following weekend announcements from Refco and Delphi

Investment Grade Debt Spread June 1, 2005 to October 28, 2005

80

85

90

95

100

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14

Basis Points

6/30 FOMC +25bps

8/9 FOMC +25bps

9/20 FOMC +25bps

Source: Lehman Brothers

High Yield Debt Spread June 1, 2005 to October 28, 2005

6/1 6/16 7/1 7/16 7/31 8/15 8/30 9/14 9/29 10/14340

360

380

400

420Basis Points

6/30 FOMC +25bps

8/9 FOMC +25bps

9/20 FOMC +25bps

Source: Merrill Lynch

November 1, 2005 106 of 114

Appendix 2: Materials used by Mr. Reinhart

November 1, 2005 107 of 114

Class I FOMC - Restricted Controlled FR

SIateria/lfor

FOMC Briefing on Monetary Policy Alternatives

Vincent R. Reinhart

November 1, 2005

November 1, 2005 108 of 114

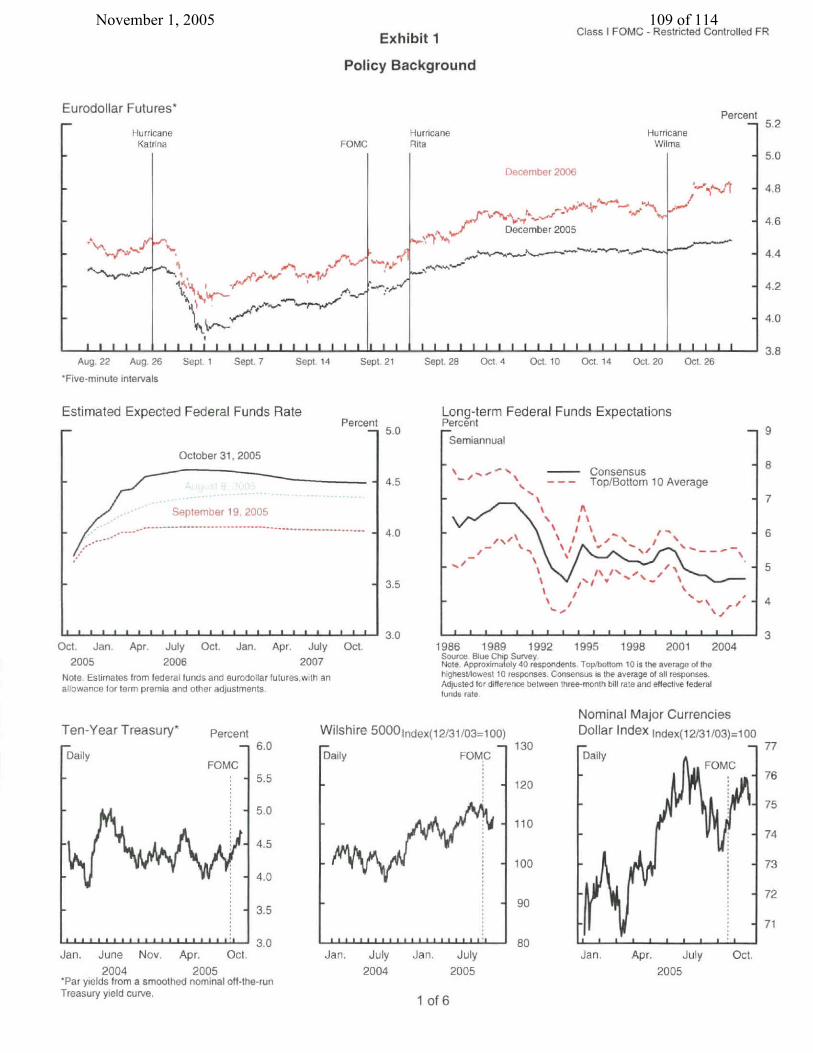

Exhibit 1

Policy Background

Class i FOMC - Restricted Controlled FR

Eurodollar Futures*

Hurricane Katrina

I I 1

- , I "It*'

I I 1 1 1 i 1

Aug, 22 Aug. 26 Sept 1 Sept 7

'Five-minute intervalsSept 14

December 2005

II 1 1Sept 21

Estimated Expected Federal Funds RatePercent

-1 5.0

October 31, 2005

Seteber 19 2005

Oct. Jan. Apr. July Oct. Jan. Apr. July Oct. 2005 2006 2007

Note. Estimates from federal lunds and eurodollar futures.with an allowance for term premia and other adjustments.

Long-term Federal Funds Expectations Percent

FIsemiannual

1986 1989 1992 1995 1998 2001 2004 Source Blue Chip Survey Note Approximately 40 respondents Toptbottom 10 is the average of the highestlowest 10 responses. Consensus is the average of all responses. Adjusled for difference between three-month bill rate and effective federal funds rate

Ten-Year Treasury* Percent6.0

Daily FOMC

5.5

5.0

4.5

4.0

3.5

3.0 Jan. June Nov. Apr. Oct.

2004 2005 Par yields from a smoothed nominal off-the-run

Treasury yield curve.

Wilshire 5 0 0 0 ndex(12/31/03=100)

Daily FOMC]

Jan. July Jan. July 2004 2005

Nominal Major Currencies Dollar Index lndex(12/31/03)=100

130 Daily A ~^_ ̂̂

Jan. Apr. July 2005

1 of 6

FOMCHurricane Rita

Hurricane Wilma

Percent -i 5.2

11 1 I I I li 1Ii 11 I1 1 1 I1 1 11 1 1

Sept. 28 Oct. 4 Oct. 10 Oct. 14 Oct, 20 Oct. 26

-1 9

November 1, 2005 109 of 114

Class I FOMC - Restricted Controlled FR

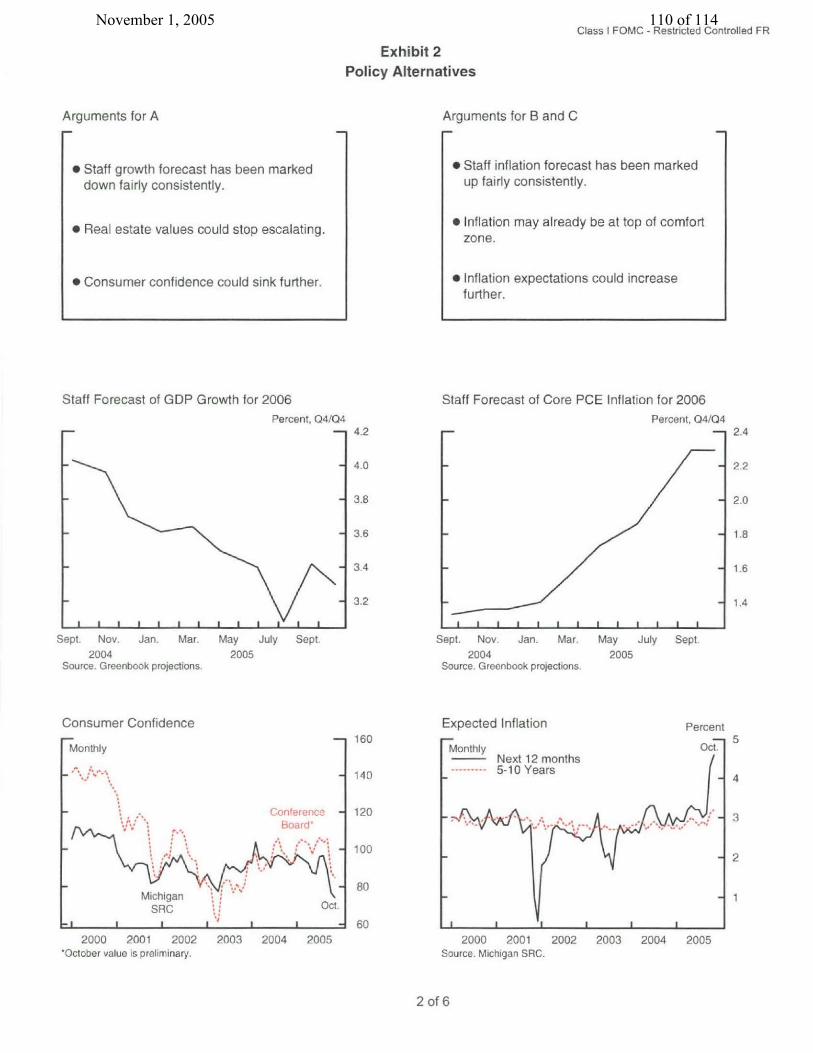

Exhibit 2 Policy Alternatives

Arguments for B and C

" Staff growth forecast has been marked down fairly consistently.

" Real estate values could stop escalating.

" Consumer confidence could sink further.

" Staff inflation forecast has been marked up fairly consistently.

" Inflation may already be at top of comfort zone.

" Inflation expectations could increase further.

Staff Forecast of GDP Growth for 2006 Percent, Q4/Q4

Staff Forecast of Core PCE Inflation for 2006 Percent, 04/04

May July Sept. 2005

Sept. Nov. Jan. Mar. 2004

Source. Greenbook projections.

Consumer Confidence

Monthly

Conference Board'

Michigan SRC

-I 1 1

Oct. 1 I

Sept. Nov. Jan. Mar. 2004

Source. Greenbook projections.

Expected Inflation

Monthly Next 12 months

-. 5-10 Years

I I

2000 2001 2002 2003 2004 2005 Source. Michigan SRC,

2 of 6

Arguments for A

i I I I I I I I _ I I I I

May July

2005Sept.

Percent

2000 2001 2002 2003 2004 2005 'October value is preliminary.

I I I

November 1, 2005 110 of 114

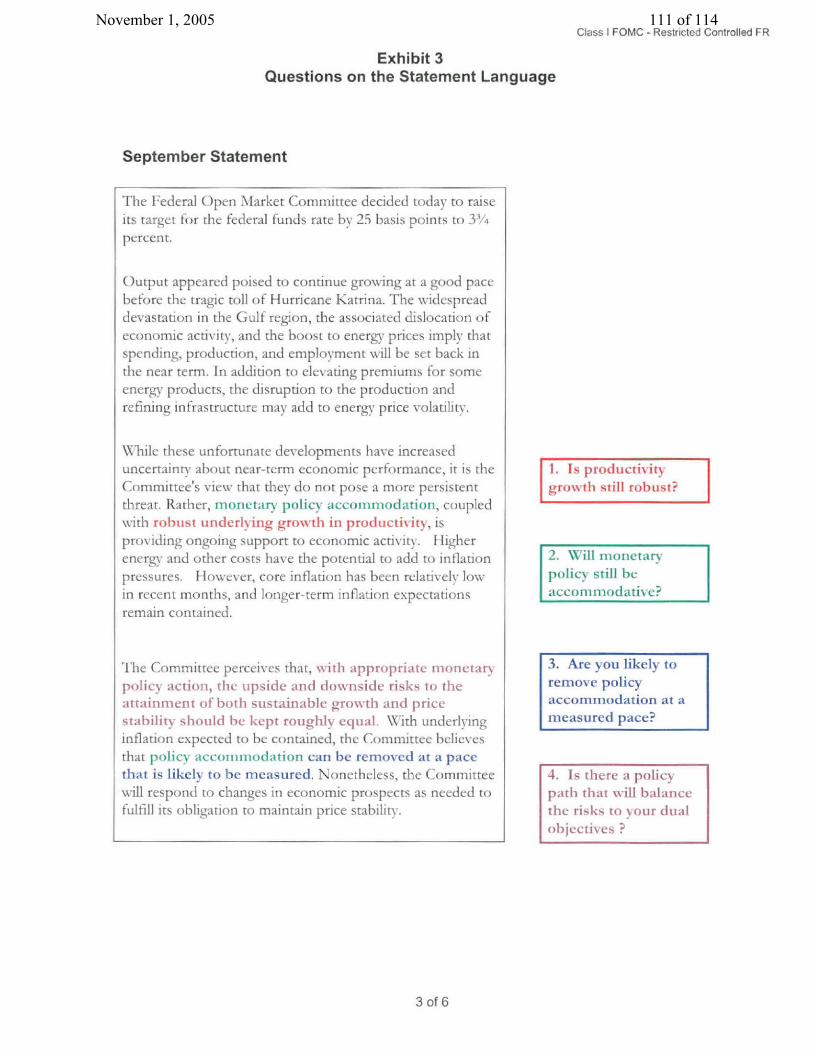

Exhibit 3 Questions on the Statement Language

September Statement

Class I FOMC - Restricted Controlled FR

The Federal Open Market Committee decided today to raise its target for the federal funds rate by 25 basis points to 3%f percent.

Output appeared poised to continue growing at a good pace before the tragic toll of Hurricane Katrina. The widespread devastation in the Gulf region, the associated dislocation of economic activiry, and the boost to energy prices imply that spending, production, and employment will be set back in the near term. In addition to elevating premiums for some energy products, the disruption to the production and refining infrastructure may add to energy price volatility.

\While these unfortunate developments have increased uncertainty about near-term economic performance, it is the Committee's view that they do not pose a more persistent threat. Rather, monetary policy accommodation, coupled with robust underlying growth in productivity, is providing ongoing support to economic activity. igher energy and other costs have the potential to add to inflation pressures. However, core inflation has been relatively low in recent months, and longer-term inflation expectations remain contained.

The Committee perceives that, w ith appropriate monetary policy action, the upside and downside risks to the attainment of both sustainable grow th and price stability should he kept roughly equal \With underlying inflation expected to be contained, the Committee believes that policy accommodation can be removed at a pace that is likely to be measured. Nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability.

3. Are you likely to remove policy accommodation at a

measured pace?

4. Is there a policy path that will balance the risks to your dual objectives ?

3 of 6

1. Is productivity

growth still robust?

2. Will monetary policy still be accommnodative?

November 1, 2005 111 of 114

Class I FOMC - Restricted Controlled FR

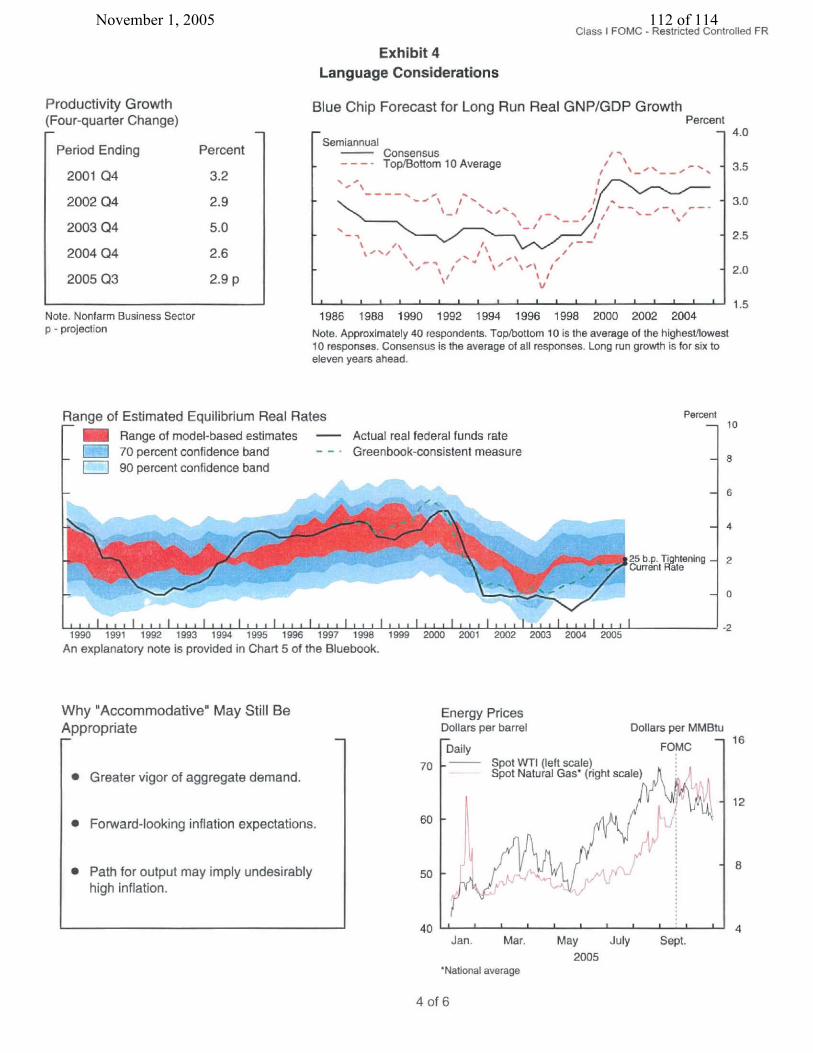

Exhibit 4 Language Considerations

Productivity Growth (Four-quarter Change)

Period Ending

2001 Q4

2002 Q4

2003 04

2004 04

2005 Q3

Note. Nonfarm Business Sector p - projection

Blue Chip Forecast for Long Run Real GNP/GDP Growth Percent

Percent

3.2

2.9

5.0

2.6

2.9 p

Range of Estimated Equilibrium Real Rat Range of model-based estimates

[II0 70 percent confidence band [I ]90 percent confidence band

Semiannual Consensus

- - - Top/Bottom 10 AverageIr

a / /

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 Note. Approximately 40 respondents. Top/bottom 10 is the average of the highest/lowest 10 responses. Consensus is the average of all responses. Long run growth is for six to eleven years ahead.

Percent

Actual real federal funds rate - - Greenbook-consistent measure

p T ening -

L I I ~I ~.l * *~l 111111111111111111111 *I *~~l ~ ~ liii II I ~I t~1 I I I~ I1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

An explanatory note is provided in Chart 5 of the Bluebook.

Why "Accommodative" May Still Be Appropriate

" Greater vigor of aggregate demand.

" Forward-looking inflation expectations.

" Path for output may imply undesirably high inflation.

Energy Prices Dollars per barrel

Daily

Dollars per MMBtu

Spot WTI (left scale) Spot Natural Gas* (right scale)

FOMC

A '

60 -

Jan. Mar.

'National average

May July Sept. 2005

4 of 6

,I

November 1, 2005 112 of 114

Class I FOMC - Restricted Controlled FR

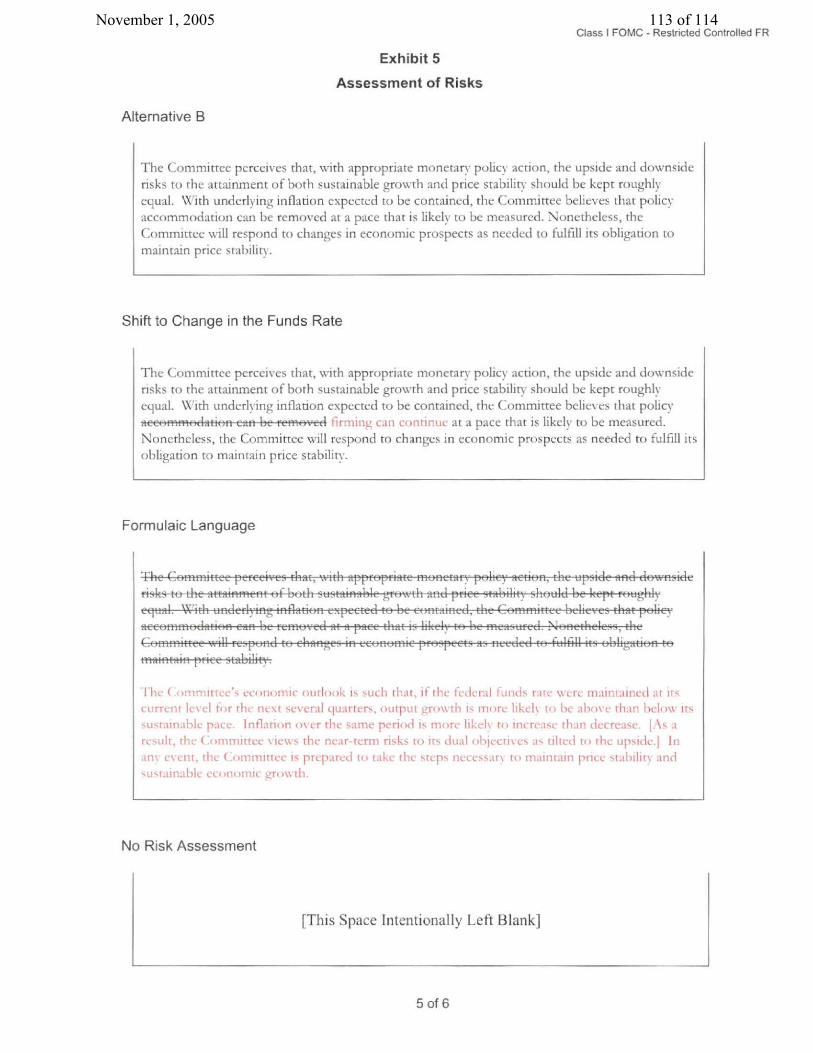

Exhibit 5

Assessment of Risks

Alternative B

The Committee perceives that, with appropriate monetary pohcy action, the upside and downside risks to the attainment of both sustainable growth and price stability should be kept roughly equal. \With underlying inflation expected to be contained, the Committee believes that policy accommodation can be removed at a pace that is likely to be measured. Nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stabilit.

Shift to Change in the Funds Rate

The Committee perceives that, with appropriate monetary policy action, the upside and downside risks to the attainment of both sustainable growth and price stabilit should be kept roughly equal. \With underlying inflation expected to be contained, the Committee believes that policy aceome-ioda ioan be removd tirnu"ngO ca ca.IntIna at a pace that is likely to be measured. Nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability.

Formulaic Language

Thne ( tmminee preonomi turlo, wit apuchptat ite, federal fun , tw wer m ununed o~~ fis

rsksrn tL etieirrent of both rt rttpu gro wth ani priem hktabilie shold bea kept roughly

a be rt e inf lan+n te r the e peri to d io re h t m I e1 i thatrI pI~"a reeouh 0,Lth I om ir e e ien ie near term risks t o it, u.a i i. ettes as tihe-d II the u Id the.|

m em, r m prep.tc a red t, rak e Ilhe pr st e - .need to uatn price .tir. and 4uanabl ec onmic wt

No Risk Assessment

[This Space Intentionally Left Blank]

5 of 6

November 1, 2005 113 of 114

Class I FOMC - Restricted Controlled FR

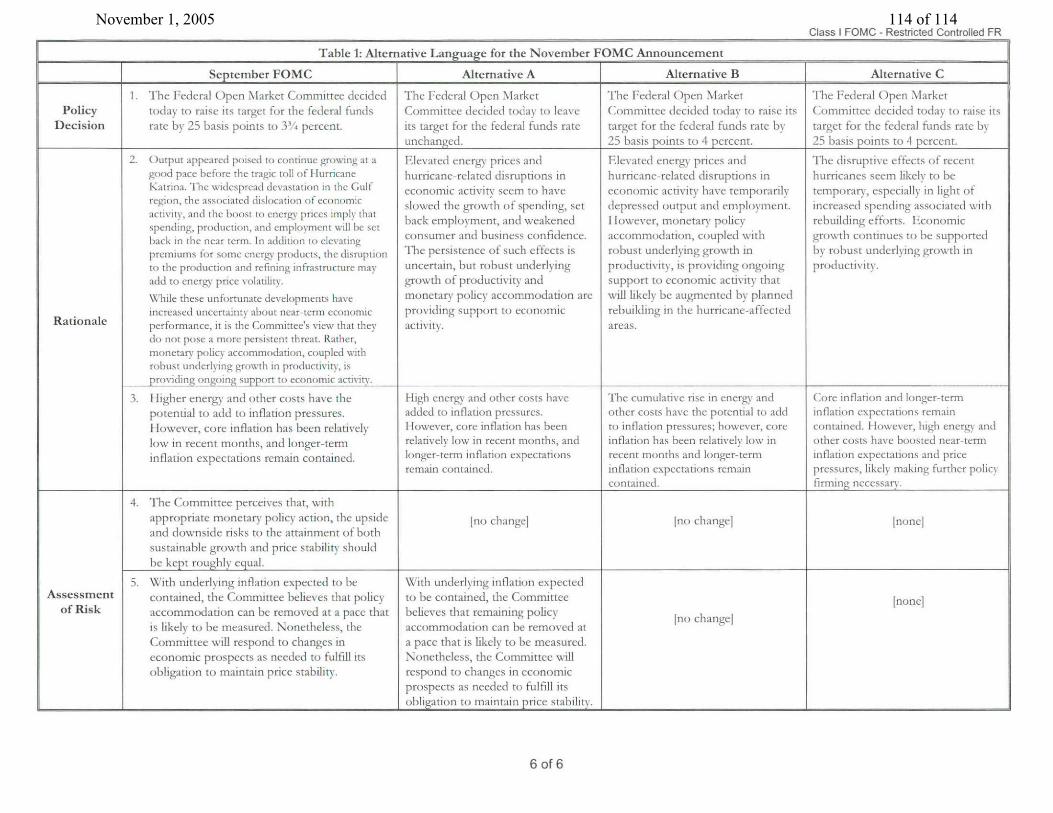

Table 1: Alternative Language for the November FOMC Announcement

September FOMC Alternative A Alternative B Alternative C 1. The Federal Open Market Committee decided The Federal Open Market The Federal Open Market The Federal Open Market

Policy today to raise its target for the federal funds Committee decided today to leave Committee decided today to raise its Committee decided today to raise its Decision rate by 25 basis points to 3% percent. its target for the federal funds rate target for the federal funds rate by target for the federal finds rate by

unchanged. 25 basis points to 4 percent. 25 basis points to 4 percent.

2. Output appeared poised to continue growing at a Elevated energ prices and Elevated energy prices and The disruptive effects of recent good pace before the tragic toll of Hurricane hurricane-related disruptions in hurneane-related disruptions in hurricanes seem likely to he Katrina. The widespread devastation in the Gulf economic acity seem to have economic activity have temporarily temporary, especiall in light of region, the associated dislocation of economic slowed the growth of spending, set depressed output and employment increased spending associated with activity, and the boost to energy prices imply that hack employment, and weakened lowever, monetary policy rebuilding efforts. Economic spending, production, and employment will be set back in the near term. In addition to elevating consumer and husiness confidence, accommodation, coupled with grosth continues to be supported premiums for some energy products, the disruption The persistence of such effects is robust underlying grosth in by robust undeiIing growth in to the production and refining infrastructure may uncertain, but robist underlying productivity, is providing ongoing productivity. add to energy price volatility. growth of productivity and support to economic activits that

While these unfortunate developments have monetary policy accommodation arc will likely be augmented by planned increased uncertainty about near-term economic providing support to economic rebuilding in the hurricane-affected

Rationale performance, it is the Committee's view that they activity, areas. do not pose a more persistent threat. Rather, monetary policy accommodation, coupled with robust underlying growth in productivity, is pros iding ongoing support to economic actnitv

3. Higher energy and other costs have the High energy and other costs have The cumulatixe rise in energy and Core inflation and longer-term

potential to add to inflation pressures. added to inflation pressures. other costs have the potential to add inflation expectations remain However, core inflation has been relativel Iowever, core inflation has been to inflation pressures; hover, core contained. aoteler, high enrgs and

low in recent months, and longer-term relatively low in recent months, and inflation has been relanxvel lox in tther costs have boosted near-term inflation expectations remain contained, longerterm inflation expectations recent months and longerterm inflation expectatins ant price

remain contained inflation expectations remain pressures, likely making further polic tcontained firming necessar.

4. sdwe Commiktew perceives that, with

appropriate monetary' policy action, the upside [no change] [no change] [none] and cdocnside risks to the attainment of both

sustainable grossth and price stability should

be kept roughly equal.

5. With underlying inflanion expected to be With underlying inflation expected Assessment contained, the Committee believes that policy to be contained, the C ommittee [none]

of Risk accommodation can be removed at a pace that beliesves that remaining policy[ochne

growth~[n ofhroucivtyan

is likely to be measurcm. Nonetheless, the accommodation can be removed at

(Committee wsill respond to changes in a pace that is likely to be measured. economic prospects as needed to fulfill its Nonetheless, the Committee will

obligation to maintain price stability. respond to changes in economic prospects as needed to fulfill its

support toon econo c a i rice stability.

6 of 6

November 1, 2005 114 of 114