Embed Size (px)

Citation preview

A specialist funds manager,

investor and developer providing real estate wealth solutions

Folkestone AGM Presentation 22 October 2013

Welcome & Introduction – Garry Sladden

Welcome & Introduction – Garry Sladden

Ordinary Business and Voting

Item 1: Financial Statements

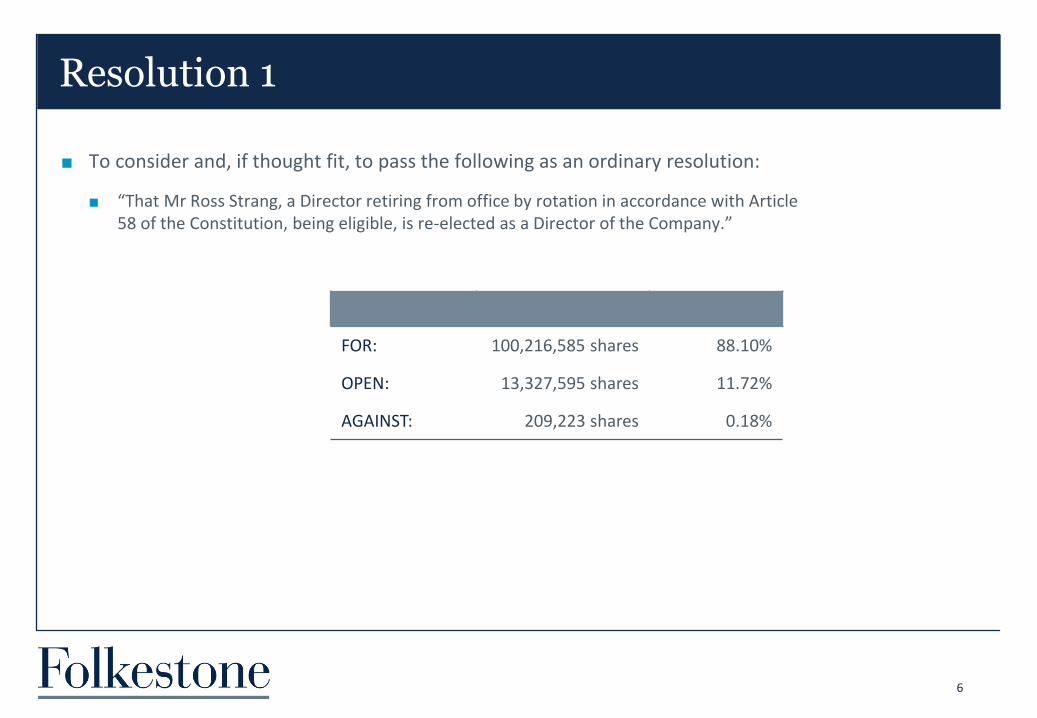

Resolution 1: Re-election of Ross Strang

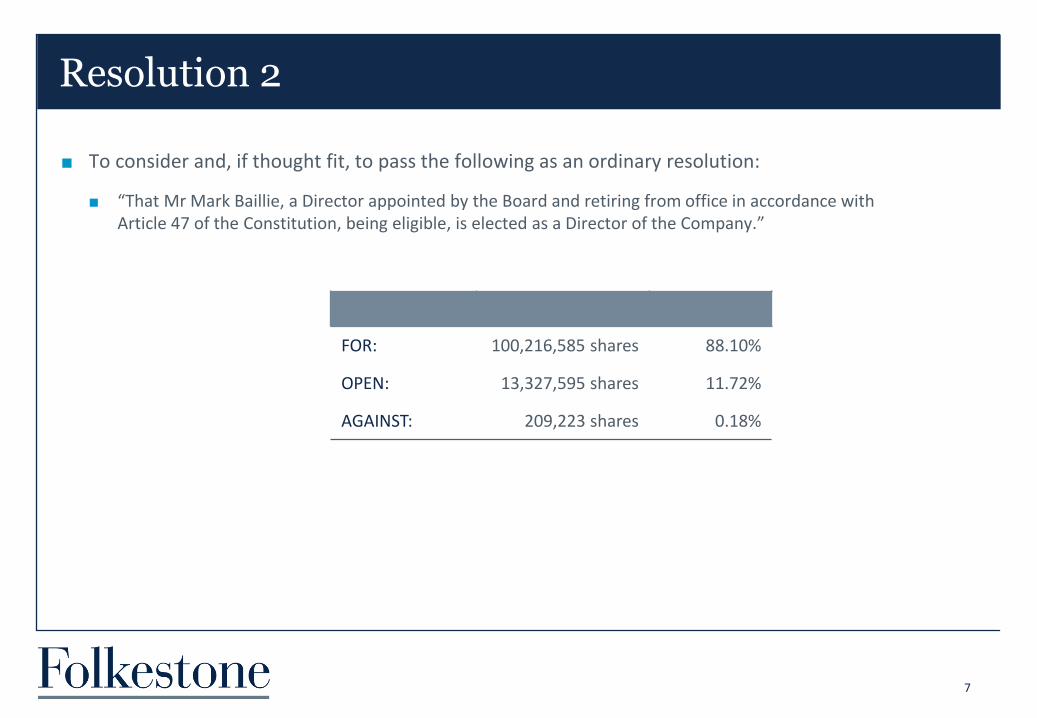

Resolution 2: Election of Mark Baillie

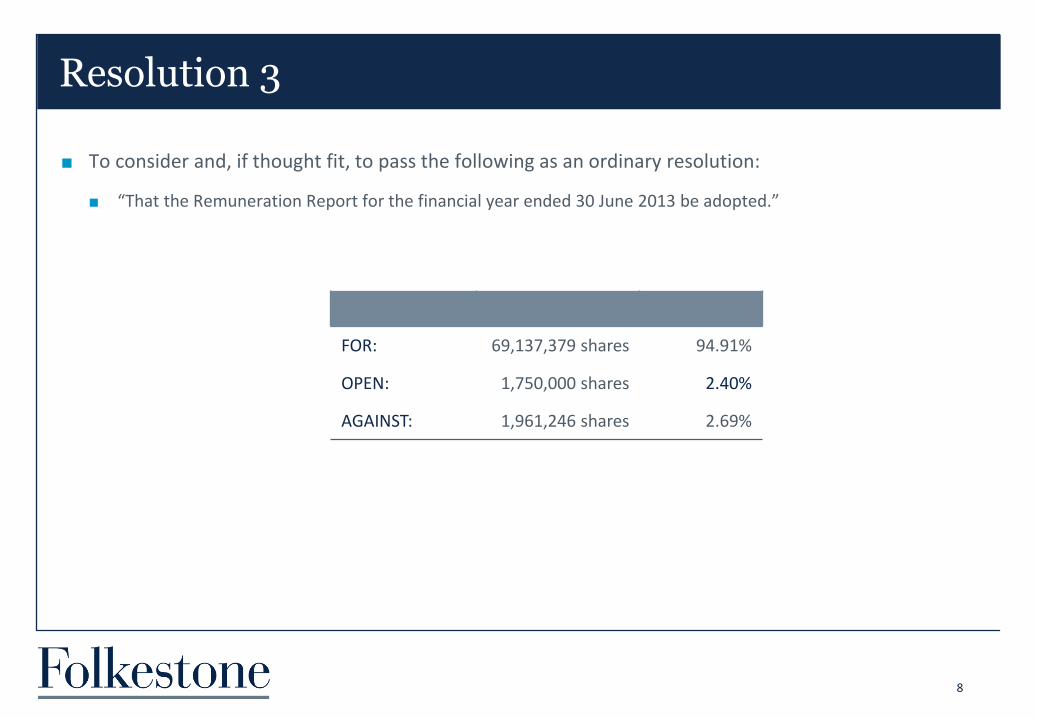

Resolution 3: Adoption of Remuneration Report

Resolution 4: Approval of Executive Incentive Plan and Issue of Shares Thereunder

Folkestone Overview – Greg Paramor

FY13 Results

Folkestone Funds Management

Direct Investments

Market Outlook

Agenda

3

Ordinary Business & Voting

Financial Statements

“To receive and consider the Directors’ Report, Financial Statements and Independent Auditor’s Report for the year ended 30 June 2013.”

Item 1

5

To consider and, if thought fit, to pass the following as an ordinary resolution:

“That Mr Ross Strang, a Director retiring from office by rotation in accordance with Article 58 of the Constitution, being eligible, is re-elected as a Director of the Company.”

Resolution 1

6

FOR: 100,216,585 shares 88.10%

OPEN: 13,327,595 shares 11.72%

AGAINST: 209,223 shares 0.18%

To consider and, if thought fit, to pass the following as an ordinary resolution:

“That Mr Mark Baillie, a Director appointed by the Board and retiring from office in accordance with Article 47 of the Constitution, being eligible, is elected as a Director of the Company.”

Resolution 2

7

FOR: 100,216,585 shares 88.10%

OPEN: 13,327,595 shares 11.72%

AGAINST: 209,223 shares 0.18%

To consider and, if thought fit, to pass the following as an ordinary resolution:

“That the Remuneration Report for the financial year ended 30 June 2013 be adopted.”

Resolution 3

8

FOR: 69,137,379 shares 94.91%

OPEN: 1,750,000 shares 2.40%

AGAINST: 1,961,246 shares 2.69%

To consider and, if thought fit, to pass the following as an ordinary resolution:

“That for purposes of Listing Rule 7.2, exemption 9 and for all other purposes, approval is given:

a. in respect of the Executive Incentive Plan (Amended Plan) for the provision of incentives to officers, employees, executives and senior management whom the Board determines to be eligible to participate in the Amended Plan (Participants); and

b. for the grant of performance rights and/or share appreciation rights to Participants, and the subsequent issue of transfer of Shares to, or in relation to, Participants under the Plan.”

Resolution 4

9

FOR: 59,589,033 shares 77.46%

OPEN: 121,200 shares 0.92%

AGAINST: 4,219,910 shares 5.49%

EXCLUDED: 12,998,666 shares 16.13%

Folkestone Overview – Greg Paramor

First full year net profit since 2008

Significant increase in funds under management to over $630m

Acquisition of Austock property funds management business

Two new unlisted real estate income funds closed oversubscribed

Strong sales at the Officer residential land sub-division

Stage 1a at The Ranges, Karratha opened and 38 lots settled in Stage 1a

Share price increase of 84% in FY13

FY13 Result - Highlights

11

“We have completed the transformation of Folkestone from a pure real estate developer to a real estate fund manager, investor and developer providing real estate wealth solutions to

private clients and select institutions”

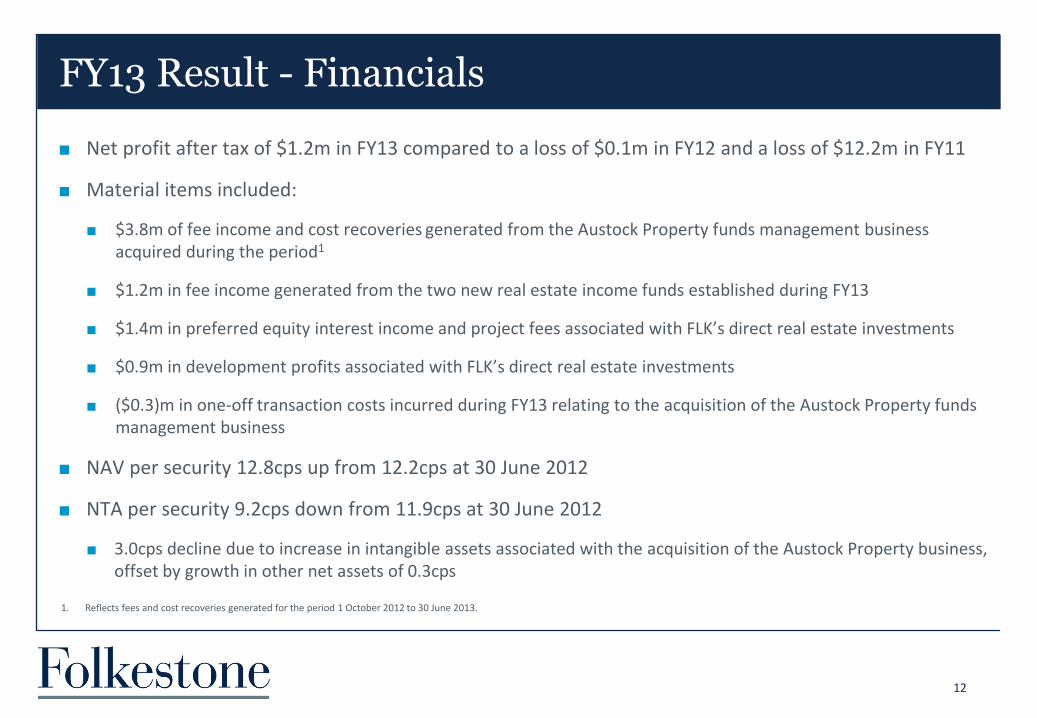

Net profit after tax of $1.2m in FY13 compared to a loss of $0.1m in FY12 and a loss of $12.2m in FY11

Material items included:

$3.8m of fee income and cost recoveries generated from the Austock Property funds management business acquired during the period1

$1.2m in fee income generated from the two new real estate income funds established during FY13

$1.4m in preferred equity interest income and project fees associated with FLK’s direct real estate investments

$0.9m in development profits associated with FLK’s direct real estate investments

($0.3)m in one-off transaction costs incurred during FY13 relating to the acquisition of the Austock Property funds management business

NAV per security 12.8cps up from 12.2cps at 30 June 2012

NTA per security 9.2cps down from 11.9cps at 30 June 2012

3.0cps decline due to increase in intangible assets associated with the acquisition of the Austock Property business, offset by growth in other net assets of 0.3cps

FY13 Result - Financials

12

1. Reflects fees and cost recoveries generated for the period 1 October 2012 to 30 June 2013.

FY13 Result – Financials (continued)

13

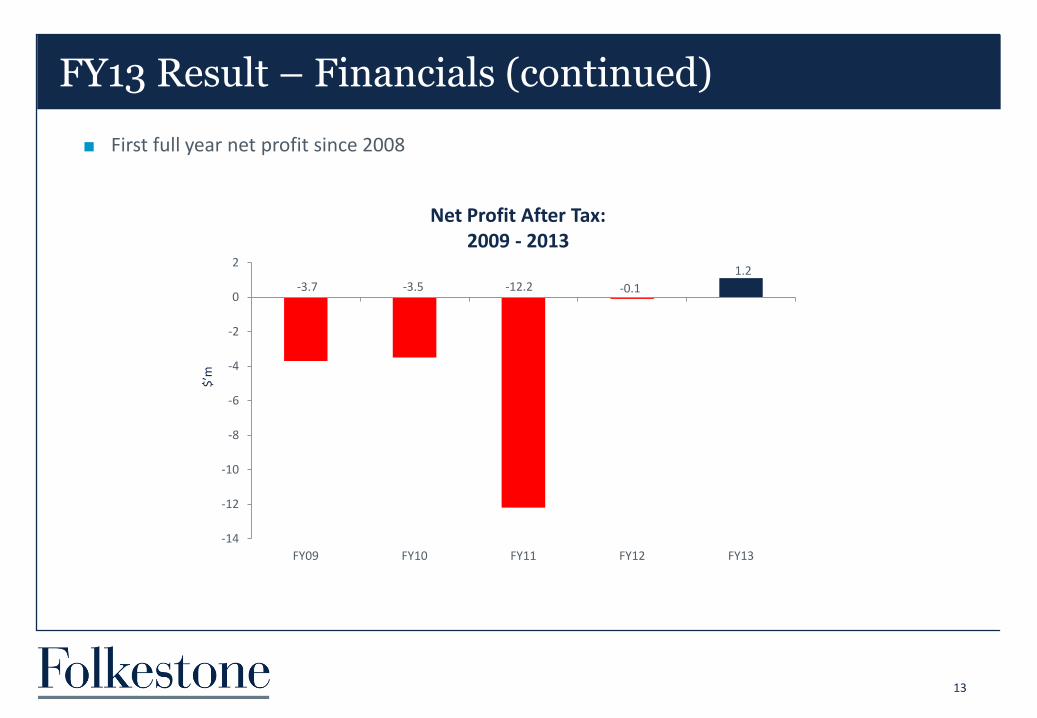

-3.7 -3.5 -12.2 -0.1

1.2

-14

-12

-10

-8

-6

-4

-2

0

2

FY09 FY10 FY11 FY12 FY13

Net Profit After Tax: 2009 - 2013

$’m

First full year net profit since 2008

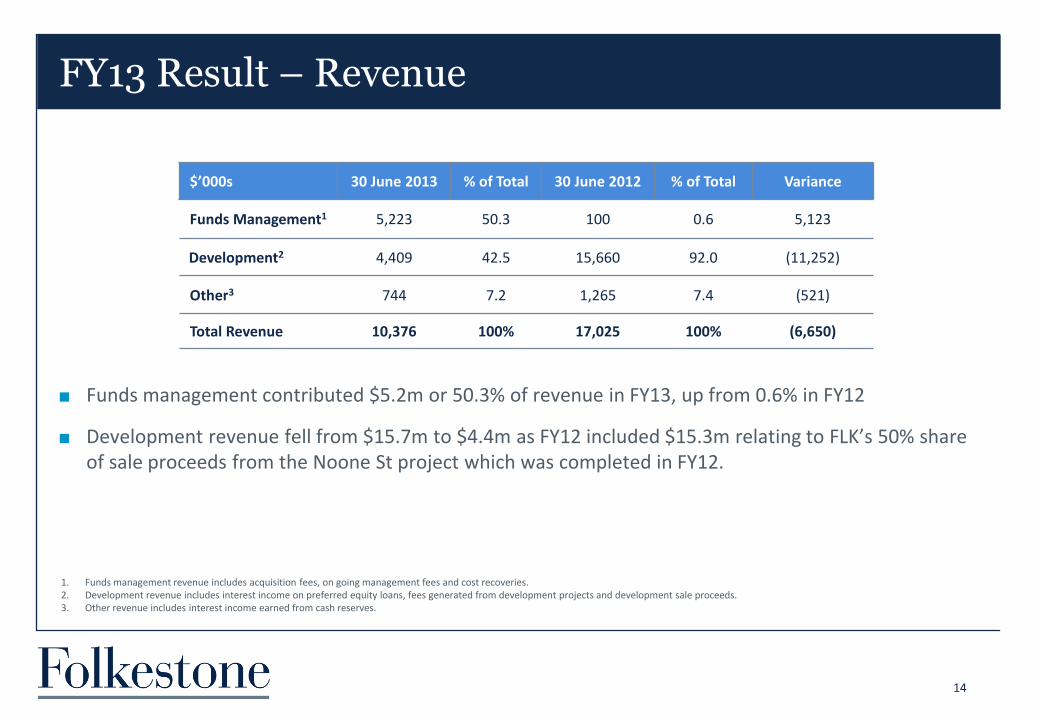

FY13 Result – Revenue

14

$’000s 30 June 2013 % of Total 30 June 2012 % of Total Variance

Funds Management1 5,223 50.3 100 0.6 5,123

Development2 4,409 42.5 15,660 92.0 (11,252)

Other3 744 7.2 1,265 7.4 (521)

Total Revenue 10,376 100% 17,025 100% (6,650)

Funds management contributed $5.2m or 50.3% of revenue in FY13, up from 0.6% in FY12

Development revenue fell from $15.7m to $4.4m as FY12 included $15.3m relating to FLK’s 50% share of sale proceeds from the Noone St project which was completed in FY12.

1. Funds management revenue includes acquisition fees, on going management fees and cost recoveries. 2. Development revenue includes interest income on preferred equity loans, fees generated from development projects and development sale proceeds. 3. Other revenue includes interest income earned from cash reserves.

Funds Management

Balance Sheet

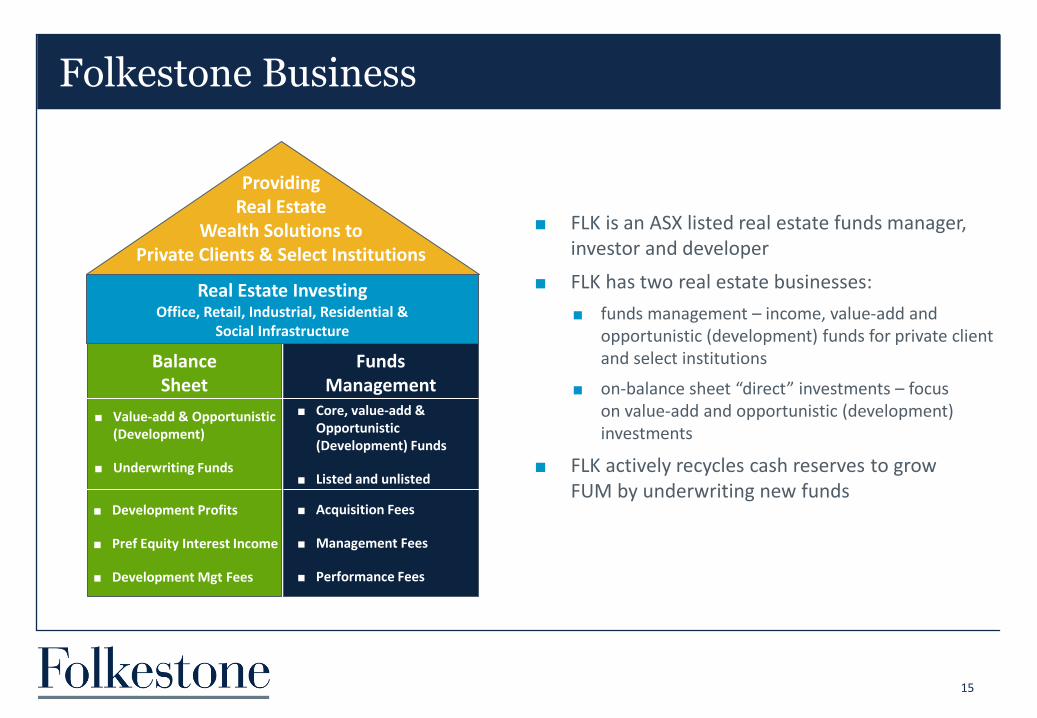

Folkestone Business

15

FLK is an ASX listed real estate funds manager, investor and developer

FLK has two real estate businesses:

funds management – income, value-add and opportunistic (development) funds for private client and select institutions

on-balance sheet “direct” investments – focus on value-add and opportunistic (development) investments

FLK actively recycles cash reserves to grow FUM by underwriting new funds

Real Estate Investing Office, Retail, Industrial, Residential &

Social Infrastructure

Value-add & Opportunistic (Development)

Underwriting Funds

Core, value-add & Opportunistic (Development) Funds

Listed and unlisted

Development Profits

Pref Equity Interest Income

Development Mgt Fees

Acquisition Fees

Management Fees

Performance Fees

Providing Real Estate

Wealth Solutions to Private Clients & Select Institutions

Focus on real estate income funds, social infrastructure funds and development funds

FLK acquired the Austock Property funds management business for $11.5m1 plus $3.0m of regulatory and working capital adjustments

Austock Property:

specialises in social infrastructure assets such as early learning (childcare) centres

four social infrastructure funds (of which two are listed) comprising $570m in funds under management2

provides exposure to growing social infrastructure sector

expands Folkestone’s distribution capability with approximately 5,000 investors

Launched two real estate income funds for private client investors:

Sydney Olympic Park – new 5,918 sqm commercial building, 100% of office space leased to Thales for 10 years

Wollongong – 9,730sqm office building with 79% of income from government tenants

Folkestone Funds Management

16

“Austock Property provides a strong platform to grow Folkestone’s funds management business.”

1. Includes $7.2m initial purchase price for 65% of the business in September 2012 and $4.3m purchase price for remaining 35% of the business in January 2013 2. FUM as at 30 June 2013

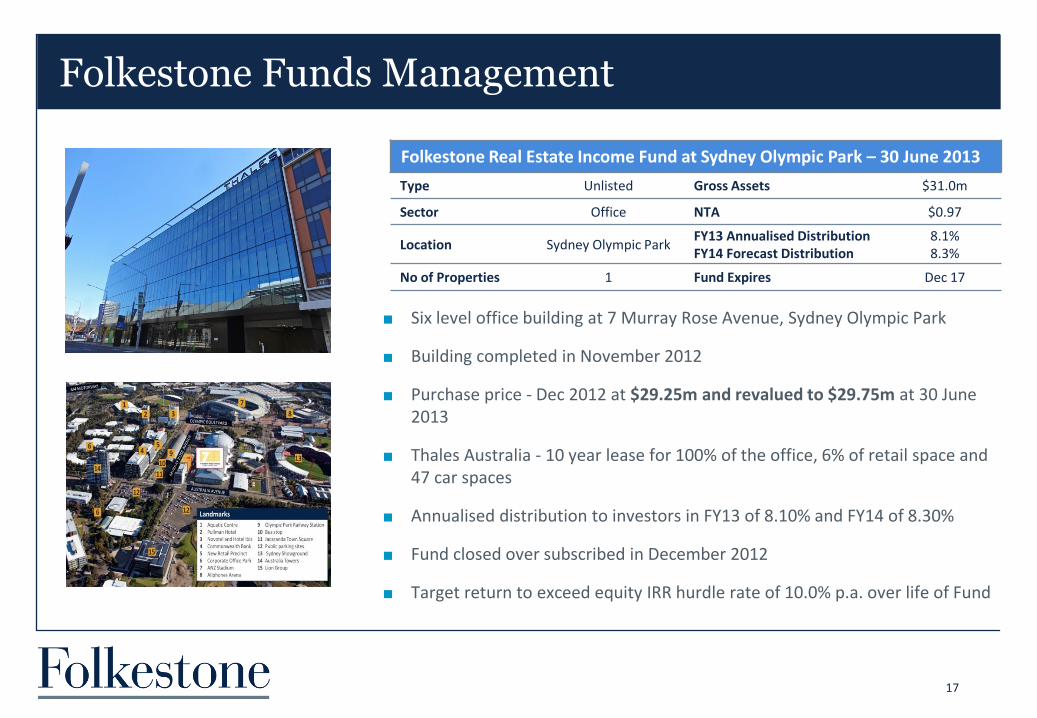

Six level office building at 7 Murray Rose Avenue, Sydney Olympic Park

Building completed in November 2012

Purchase price - Dec 2012 at $29.25m and revalued to $29.75m at 30 June 2013

Thales Australia - 10 year lease for 100% of the office, 6% of retail space and 47 car spaces

Annualised distribution to investors in FY13 of 8.10% and FY14 of 8.30%

Fund closed over subscribed in December 2012

Target return to exceed equity IRR hurdle rate of 10.0% p.a. over life of Fund

Folkestone Funds Management

17

Folkestone Real Estate Income Fund at Sydney Olympic Park – 30 June 2013

Type Unlisted Gross Assets $31.0m

Sector Office NTA $0.97

Location Sydney Olympic Park FY13 Annualised Distribution FY14 Forecast Distribution

8.1% 8.3%

No of Properties 1 Fund Expires Dec 17

A six level commercial office building at 43 Burelli Street and 34 Stewart Street, Wollongong

Acquisition price - $23.27m1 reflecting a 12.00% passing yield and 5.80% discount to independent valuation

High yield – forecast distribution yield of 10.50% in FY14 paid quarterly

Strong lease covenants – approximately 79% of the income is currently sourced from Commonwealth and State Government tenants

Fund closed circa 50% oversubscribed in June 2013

Target return to exceed equity IRR hurdle rate of 12.0% p.a. over life of Fund

Folkestone Funds Management

18

Folkestone Real Estate Income Fund at Wollongong - 30 June 2013

Type Unlisted Gross Assets $26.4m

Sector Office NTA $0.96

Location Wollongong FY13 Annualised Distribution FY14 Forecast Distribution

10.5% 10.5%

No of Properties 1 Fund Expires June 19

1. The Acquisition Price may be reduced to $23.070 million if by 1 July 2014 a new Family Court of Australia (FCA) lease is not executed or FCA vacates the premises.

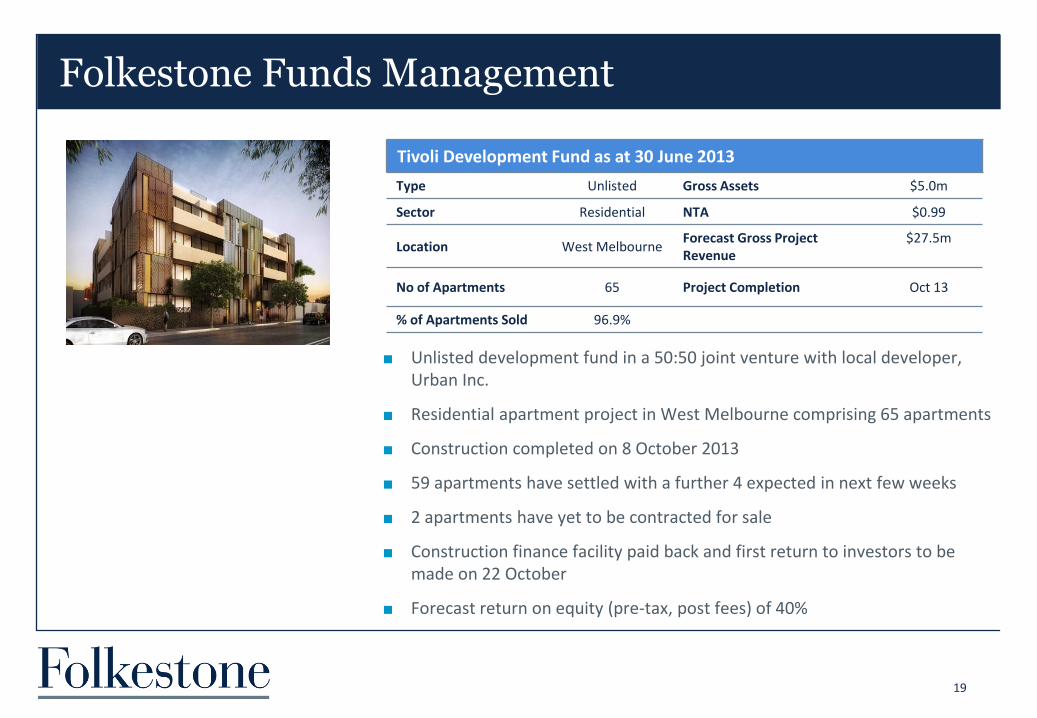

Unlisted development fund in a 50:50 joint venture with local developer, Urban Inc.

Residential apartment project in West Melbourne comprising 65 apartments

Construction completed on 8 October 2013

59 apartments have settled with a further 4 expected in next few weeks

2 apartments have yet to be contracted for sale

Construction finance facility paid back and first return to investors to be made on 22 October

Forecast return on equity (pre-tax, post fees) of 40%

Folkestone Funds Management

19

Tivoli Development Fund as at 30 June 2013

Type Unlisted Gross Assets $5.0m

Sector Residential NTA $0.99

Location West Melbourne Forecast Gross Project Revenue

$27.5m

No of Apartments 65 Project Completion Oct 13

% of Apartments Sold 96.9%

Folkestone Funds Management

20

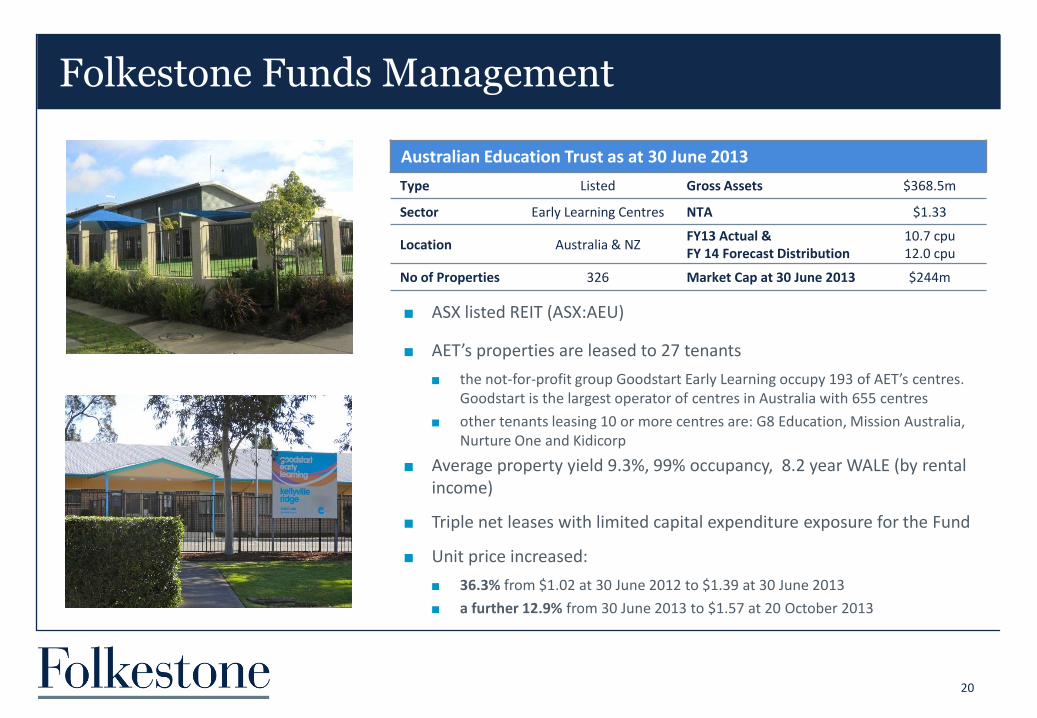

Australian Education Trust as at 30 June 2013

Type Listed Gross Assets $368.5m

Sector Early Learning Centres NTA $1.33

Location Australia & NZ FY13 Actual & FY 14 Forecast Distribution

10.7 cpu 12.0 cpu

No of Properties 326 Market Cap at 30 June 2013 $244m

ASX listed REIT (ASX:AEU)

AET’s properties are leased to 27 tenants

the not-for-profit group Goodstart Early Learning occupy 193 of AET’s centres. Goodstart is the largest operator of centres in Australia with 655 centres

other tenants leasing 10 or more centres are: G8 Education, Mission Australia, Nurture One and Kidicorp

Average property yield 9.3%, 99% occupancy, 8.2 year WALE (by rental income)

Triple net leases with limited capital expenditure exposure for the Fund

Unit price increased:

36.3% from $1.02 at 30 June 2012 to $1.39 at 30 June 2013

a further 12.9% from 30 June 2013 to $1.57 at 20 October 2013

Folkestone Funds Management

21

Australian Social Infrastructure Fund as at 30 June 2013

Type Listed Gross Assets $107.3m

Sector Social Infrastructure NTA $2.48

Location Australia FY13 Actual Distribution FY14 Forecast Distribution

17.6 cpu 19.0 cpu

No of Properties 50 Market Cap at 30 June 2013 $61m

ASX listed REIT (ASX:AZF)

Diversified social infrastructure fund – 48 early learning centres, a self storage facility and a medical centre

Average property yield 9.3%, 98% occupancy and 7.8 year WALE (by rental income)

Triple net leases with limited capital expenditure exposure for the Fund

Portfolio of holdings in four property securities with book value of $19.9m - 19% of ASIF’s total assets

Unit price increased:

19.6% from $1.79 at 30 June 2012 to $2.14 at 30 June 2013

a further 5.0% from 30 June 2013 to $2.25 at 20 October 2013

Folkestone Funds Management

22

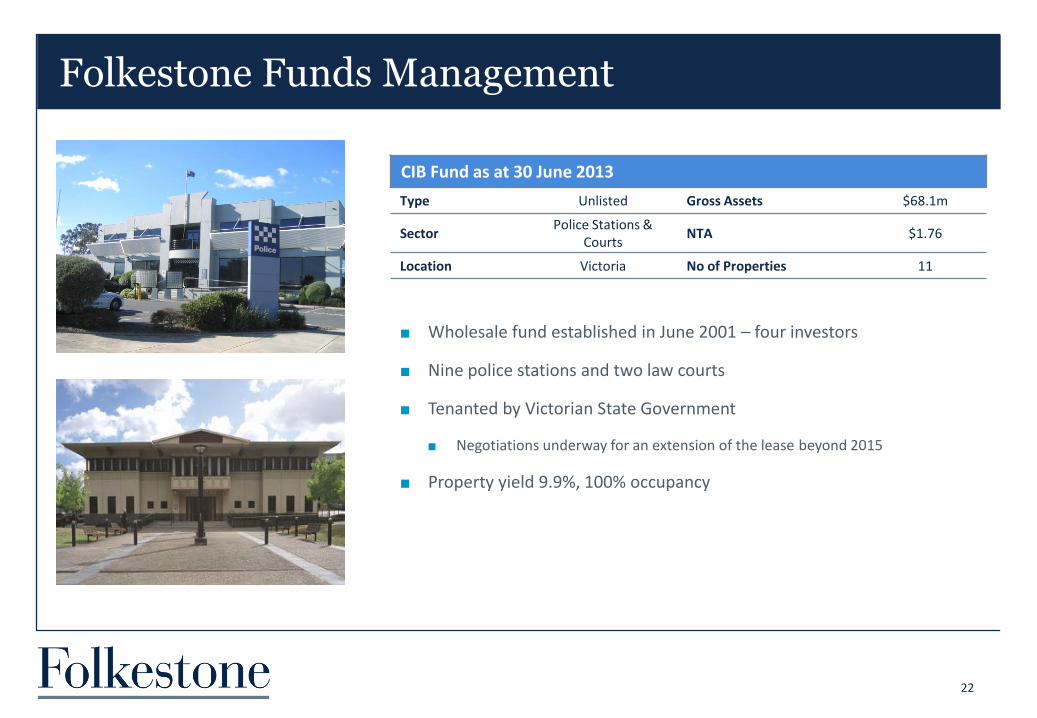

CIB Fund as at 30 June 2013

Type Unlisted Gross Assets $68.1m

Sector Police Stations &

Courts NTA $1.76

Location Victoria No of Properties 11

Wholesale fund established in June 2001 – four investors

Nine police stations and two law courts

Tenanted by Victorian State Government

Negotiations underway for an extension of the lease beyond 2015

Property yield 9.9%, 100% occupancy

Folkestone Funds Management

23

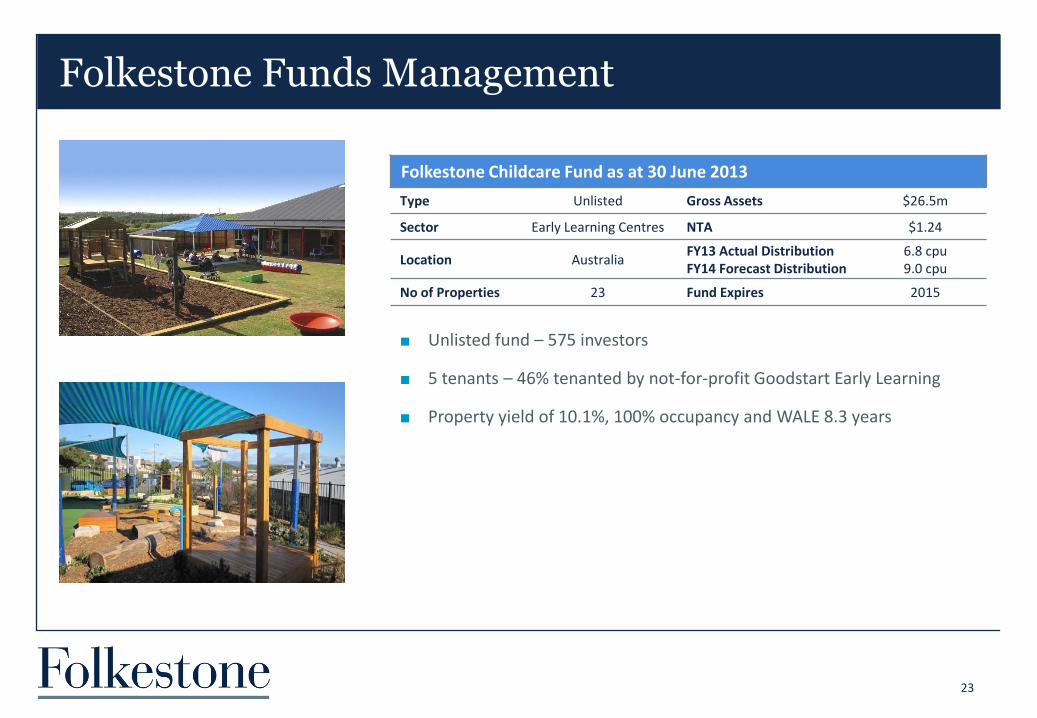

Folkestone Childcare Fund as at 30 June 2013

Type Unlisted Gross Assets $26.5m

Sector Early Learning Centres NTA $1.24

Location Australia FY13 Actual Distribution FY14 Forecast Distribution

6.8 cpu 9.0 cpu

No of Properties 23 Fund Expires 2015

Unlisted fund – 575 investors

5 tenants – 46% tenanted by not-for-profit Goodstart Early Learning

Property yield of 10.1%, 100% occupancy and WALE 8.3 years

Stage 1 (56 lots) started construction in October 2012 and was completed in April 2013

Stage 2 (43 lots) started construction in July 2013 with completion expected early 2014

As at 30 June 2013, 65 lots (53 in Stage 1 and 12 in Stage 2) under contract. Of the Stage 1 lots, 43 were settled by 30 June with a further 10 settled post 30 June (total value of settlements - $9.8m at average price $185,000)

Post 30 June – a further 3 lots in Stage 1, 22 lots in Stage 2 and 3 lots in Stage 3 are now under contract

Forecast FLK equity IRR – 29.0%

Direct Investments

24

Potters Grove, Officer as at 30 June 2013

Sector Residential Ownership Interest 50%

Location Officer, Vic JV Partner ID Land

Area/Size 14.1ha FLK Equity Invested $4.8m

Acquired June 2011 FLK Preferred Equity Invested1 $2.7m

Total Lots 227 Debt Provider Bank of Melbourne

% of Lots Sold 28.6% Debt Amount (FLK Share) $1.6m

Forecast Project Value – Gross Revenue

$44.0m Debt Expiry Post 30 June debt

refinanced to Sept 14

Settlements Started May 2013 FLK Gross Book Value $9.1m

Price Range of Lots $129,000 - $244,000

1. FLK has provided $2.0m in preferred equity to this project. The preferred equity is subject to a fixed rate of interest which is calculated and recognised as income on a monthly basis. The loan balance at 30 June 2013 includes $0.7m of accrued interest.

Providing short and long-term accommodation in Karratha

Stage 1 consists of 108 one bedroom villas:

Stage 1a (41 villas) - 38 sold and settled at 30 June, 1 settled post and 2 are under contract

Stage 1a opened for trade on 3 December 2012

Stage 1b (35 villas) - 16 are under contract with construction to commence early 2014

Adjoining 7.1ha site with potential for circa 261 dwellings settled on 24 January 2013

FLK exposure - $4.8m or 10.0% of FLK net assets and FLK share of project debt on look through basis is $450,000 or 0.95% of FLK net assets

Direct Investments

25

The Ranges, Karratha as at 30 June 2013

Sector Accommodation Ownership Interest1 25%

Location Karratha, WA JV Partner Various Parties

Area/Size Stage 1 - 2.2ha/ Stage 2 - 7.1ha

FLK Equity Invested $1.9m

Acquired Stage 1 - June 2011

Stage 2 – January 2013 FLK Preferred Equity Invested2 $2.9m

Total Villas Stage 1 – 108 FLK Gross Book Value $4.8m

% of Villas Sold Stage 1 – 51% Settlements Start March 2013

Forecast Project Value – Gross Revenue

Stage 1 – $64.4m Price Range of Villas $525,000 to

$565,000

1. FLK’s 25% interest in this project is reflected in the balance sheet as units in associated entities. This project has a debt facility with St George Bank which was drawn to $1.8m as at 30 September 2013. 2. FLK has provided $2.0m in preferred equity to this project. The preferred equity is subject to a fixed rate of interest which is calculated and recognised as income on a monthly basis. The loan balance at 30 June 2013

includes $0.9m of accrued interest.

FLK acquired AMP Capital Investors’ 50% interest in the 13.9ha site in April 2013

Aldi have agreed to acquire 0.8 ha (subject to subdivision) for a circa 1,600 sq.m. supermarket

FLK is developing a 21,500 sqm large format retail centre on Stage 1 land (4.7 ha)

due for completion in late 2014

Negotiations are well advanced with key tenants

FLK will launch a new Real Estate Income Fund to acquire the Stage 1 land, assist in the funding of the development and own the Centre long-term

Direct Investments

26

Millers Rd, Altona North as at 30 June 2013

Sector Large Format Retail FLK Equity Invested $8.5m

Location Altona North, Vic FLK Preferred Equity Invested Nil

Area/Size 13.9ha Debt Provider Bank of Melbourne

Acquired Dec 2007 Debt Amount $8.1m (Post 30 June paid down to $6.0m)

Ownership Interest 100% Debt Expiry Post 30 June debt

refinanced to September 2014

Gross Book Value $16.6m

Well positioned to continue to deliver on the strategy of:

growing its suite of listed and unlisted real estate funds

seeking value-add and opportunistic investments on balance sheet activities

Grow recurring earnings through funds management

actively source product for existing and new income and development funds

take advantage of strong demand from investors for yield based product

opportunity to capitalise on the growing social infrastructure space – social and demographic changes plus government increasingly looking at public-private partnerships

Deliver on existing balance sheet projects - Altona North - Victoria, Officer - Victoria and Karratha - Western Australia

Undertake earnings accretive opportunistic acquisitions

Folkestone Outlook

27

Market Outlook – Greg Paramor

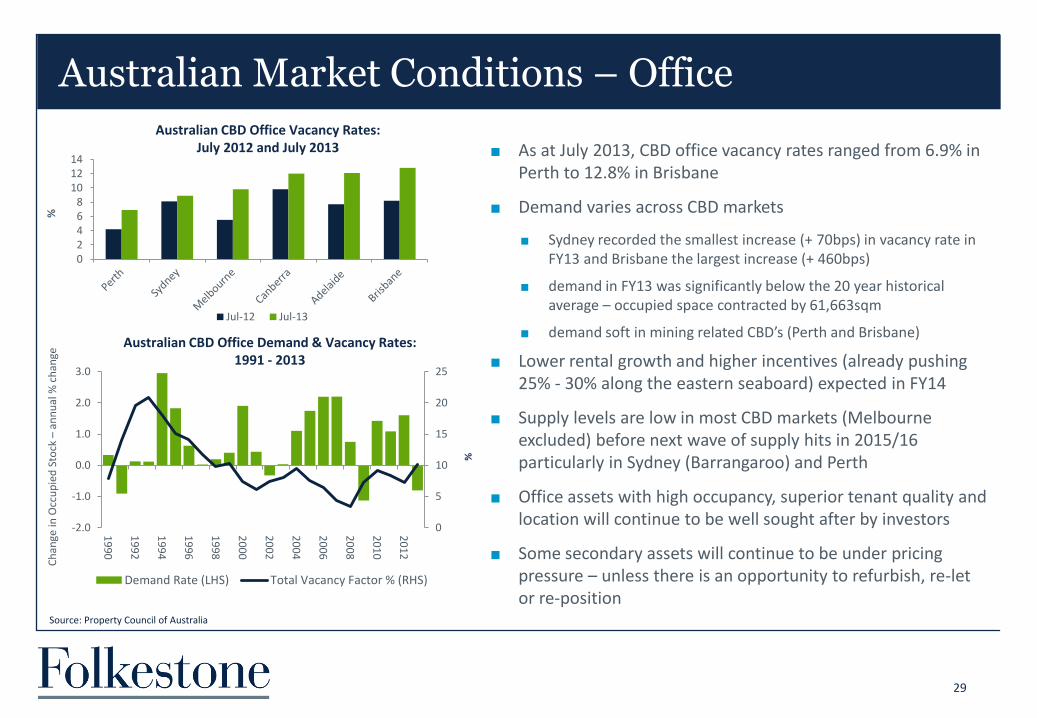

Australian Market Conditions – Office

29

As at July 2013, CBD office vacancy rates ranged from 6.9% in Perth to 12.8% in Brisbane

Demand varies across CBD markets

Sydney recorded the smallest increase (+ 70bps) in vacancy rate in FY13 and Brisbane the largest increase (+ 460bps)

demand in FY13 was significantly below the 20 year historical average – occupied space contracted by 61,663sqm

demand soft in mining related CBD’s (Perth and Brisbane)

Lower rental growth and higher incentives (already pushing 25% - 30% along the eastern seaboard) expected in FY14

Supply levels are low in most CBD markets (Melbourne excluded) before next wave of supply hits in 2015/16 particularly in Sydney (Barrangaroo) and Perth

Office assets with high occupancy, superior tenant quality and location will continue to be well sought after by investors

Some secondary assets will continue to be under pricing pressure – unless there is an opportunity to refurbish, re-let or re-position

Australian CBD Office Vacancy Rates: July 2012 and July 2013

Source: Property Council of Australia

%

Ch

ange

in O

ccu

pie

d S

tock

– a

nn

ual

% c

han

ge

02468

101214

Jul-12 Jul-13

Australian CBD Office Demand & Vacancy Rates: 1991 - 2013

%

0

5

10

15

20

25

-2.0

-1.0

0.0

1.0

2.0

3.0

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Demand Rate (LHS) Total Vacancy Factor % (RHS)

Australian Market Conditions – Retail

30

Retail environment remains challenging

Low consumer confidence keeping retail spending below trend especially in the discretionary retail sector

Cyclical factors (price discounting, low consumer sentiment and continued high savings levels) and structural issues (internet penetration and changing retail formats) continue to impact retailers

Rental growth has slowed, incentives are increasing and vacancy rates are rising especially in secondary centres

Competition between centres will continue to drive defensive investment by owners to improve amenity, maintain occupancy and drive foot traffic

Grocery anchored neighbourhood centres and super regional destination centres should perform better than other types of retail centres

Sub-regional centres and secondary centres in poor locations or with poor tenancy mixes are more likely to be impacted by the cyclical and structural changes impacting the retail sector

Source: Westpac/Melbourne Institute, ABS

Year

ly %

ch

ange

0

2

4

6

8

10

-40

-30

-20

-10

0

10

20

30

40

50

60

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Consumer Confidence (LHS) Retail Spending (RHS)

%

Consumer Sentiment & Retail Trade: 2002 - 2013

Retail Trade: 1994 - 2013

0

2

4

6

8

10

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Retail Sales Avg ('94 - '09) Avg ('09 - '13)

Year

ly %

ch

ange

Australian Market Conditions – Industrial

31

Industrial currently attracting significant investor interest Strong demand from A-REITs (Goodman, Mirvac, GPT, Dexus) and

private investors

Fife Capital industrial REIT IPO well supported

Approximately $1bn worth of investment in H1 2013 with Sydney the focus of buyer activity

Industrial attractive to investors for a number of reasons

yields - prime grade Sydney industrial yields range between 7.75% and 8.25%

typically long term leasing structures with fixed increases

changes to the structure economy (decline of local manufacturing, growing online retailing and improved infrastructure) driving increased demand for distribution and logistic centres

Increasing industrial development activity driving up supply across most markets1

nationally c. 367,000sqm of stock is under construction with 61,000sqm in Sydney – driven by active pre-leasing activity

Melbourne has 122,021sqm under construction with lower pre-commitments putting pressure on rents and incentives (averaging 12%)

Two tier market with prime assets in strong demand whilst secondary assets not as well supported

Sale

s p

er h

alf

$b

n

Capital City Industrial Transaction Volumes: H2 2012 & H1 2013

Sydney Industrial Average Yields: Mar 2005 to Mar 2013

Source: Colliers

10

9

8

7

6

%

1 Colliers, July 2013

0

5

10

15

20

0

100

200

300

400

500

Sydney Brisbane Perth Melbourne Adelaide

H2'12 - Transaction Value (LHS) H1'13 - Transaction Value (LHS)

H2'12 - Transaction Volume (RHS) H1'13 - Transaction Volume (RHS)

Australian Market Conditions – Residential

32

Housing recovery is strong in Sydney and Perth however is patchy across the rest of the capital city markets

Buyer activity varies

first home buyers subdued - 14.7% of the loan market in July 2013 (down from 31.9% in May 2009 and below 20yr average of 19.9%)

investor activity is increasing - loans to investors 36% of total loans in June 2013, above 20 year average of 32%

New home sales up and auction clearance rates improving

sales activity up in four months to June 2013

Sydney and Melbourne averaging above 60% in recent months with Sydney topping 84% on 14 Sep 2013

Rental growth remains strong as vacancies remain low

median Sydney inner ring rents $575/wk up 4.5% year to June 13

national vacancy rate 2.1% and 1.8% in Sydney (as at Aug 2013)

Sydney should lead the recovery given limited price growth over past decade and low levels of construction activity

Medium term outlook positive – high population growth, demographic changes, undersupply of dwellings and growing acceptance of medium density accommodation forcing developers to rethink what consumers want

Major Capital City Dwelling Prices: to Aug 2013

%

Source: RP Data – Rismark Index, HIA New Homes Sales

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2009 2010 2011 2012

Houses Units

Private New Dwelling Sales: 2009 to 2013

Sale

s p

er m

on

th

2013

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Adelaide Brisbane Melbourne Sydney Perth

Month Quarter Year

Early Learning Sector

33

Graph Source: ABS 1 Department of Education, Employment and Workplace Relations – Childcare in Australia - August 2013

The key drivers of the early learning sector:

demand for childcare services remain strong

birth rates has grown steadily - 2012 birth rate at an all time high

increased female participation rate in the labour force, supporting demand for long day care

recognition of social and educational benefits of early learning in children aged 1-5 years

government assisting with access to childcare, largely through Child Care Benefit and Child Care Rebate schemes, with the government forecast to spend $22bn to 2016-171

population of children less than 5 years in the catchment area of a centre drives occupancy and profitability

State of the market:

there are 6,192 long day care centres in Australia, an increase of 1,635 centres or 35.9% since 20041

since 2004, the number of children using long day care centres has increased by 39.5 per cent to 615,630 children1

49.2% of 3 to 5 year olds used childcare in 2012, up from 43.0% in 2006. In the 0-2 years age cohort, 31.4% used childcare compared to 26.9% in 20061

there continues to be unmet demand, as evidenced by healthy waiting lists, in many areas across Australia.

Australian Birth Rates by Year: 2001 - 2012

200,000

220,000

240,000

260,000

280,000

300,000

320,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

40

45

50

55

60

65

70

75

80

85

19

78

19

80

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

04

20

06

20

08

20

10

20

12

20-24 25-34 35-44

Female Participation % by Age-Group: 1978 - 2012

%

34

Market Outlook

Weight of capital to support values

Residential market recovery underway

Mixed fortunes across the non-residential real estate sectors

Office – subdued demand and future supply increases to limit upside

Retail – difficult trading conditions and structural changes to continue

Industrial – currently favourite asset class

Higher global bond yields will provide a challenge across all sectors

Development of niche real estate sectors to continue

Longer term trends supportive of continued investment into real estate from both

domestic and global institutions

private client investors especially SMSF’s

Sources: IbisWorld Industry Report July 2012, DEEWR 2012

A specialist funds manager,

investor and developer providing real estate wealth solutions

Folkestone AGM Presentation 22 October 2013

Disclaimer

This paper has been published for information purposes only. The information contained in this paper is of a general nature only and does not constitute financial product advice. This presentation has been prepared without taking account of any person's objectives, financial situation or needs. Because of that, each person should, before acting on this presentation, consider its appropriateness, having regard to their own objectives, financial situation and needs. You should consult a professional investment adviser before making any decision regarding a financial product.

In preparing this presentation the author has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which has otherwise been reviewed in preparation of the paper. The information contained in this paper is current as at the date of this paper and is subject to change without notice. Past performance is not an indicator of future performance.

Neither Folkestone Limited, nor any of their associates, related entities or directors, give any warranty as to the accuracy, reliability or completeness of the information contained in this paper. Except insofar as liability under any statute cannot be excluded, Folkestone Limited and its associates, related entities, directors, employees and consultants do not accept any liability for any loss or damage (whether direct, indirect, consequential or otherwise) arising from the use of this paper.

If a product managed by Folkestone Limited or its associates is acquired, Folkestone Limited or its associates and related entities may receive fees and other benefits. The author of this paper does not receive commissions or remuneration from transactions involving the financial products mentioned in this paper.

Folkestone Limited Level 10, 60 Carrington Street Level 12, 15 William St

Sydney NSW 2000 Melbourne VIC 3000

T: +612 8667 2800 T: +613 8601 2092

www.folkestone.com.au

36