Embed Size (px)

Citation preview

Flexible Plug and Play

Smart Solutions for connecting Distributed Generation

Sotiris Georgiopoulos

2011. UK Power Networks. All rights reserved

• Introduction to Flexible Plug and Play

• Trial location

• Case studies

• Overall project plan

• Commercial arrangements workstream

• Concepts to keep in mind throughout the day

2

Contents

2011. UK Power Networks. All rights reserved

Objective: Cheaper and faster connection of DG to constrained parts of the network by

trialing smart grid technologies and smart commercial agreements

Duration: 3 years: January 2012 - December 2014

Project Value: £9.7 million (6.7m funding from LCNF Tier 2)

Partners:

Flexible Plug and Play

2011. UK Power Networks. All rights reserved

Connected Wind Farms

Consented Wind Farms

Received Applications Wind Farms

Scoping Sites Wind Farms

Grid Substation

Primary Substation

33 kV 132 kV 400 kV

Location: Cambridgeshire

Surface: ~ 700km²

Network: 33kV and 11kV Network (2 Grid, 10 Primary substation sites)

Connected Wind Generation: 120MW

Planning & Delivery Stage: approx 270MW

Flexible Plug and Play:

Trial location

2011. UK Power Networks. All rights reserved Classification: Restricted 5

The challenge – March Grid (case study)

In the context of the heat map

Constraints

(focus on 33 and 11kV)

• Reverse power flow

limitations

• Thermal line limits

2011. UK Power Networks. All rights reserved Classification: Restricted 6

The challenge – March Grid (case study)

Constraints

• Reverse power flow limitation (N-

1) due to protection – set at a max

of 75% rating of the transformer

• Constraint occurs at min Load

max Gen situations

Consequences

• Substation considered full

• Very expensive quotes for

connections to projects in the

vicinity (Distance or increased

voltage level)

G L Generator Load Circuit

breaker

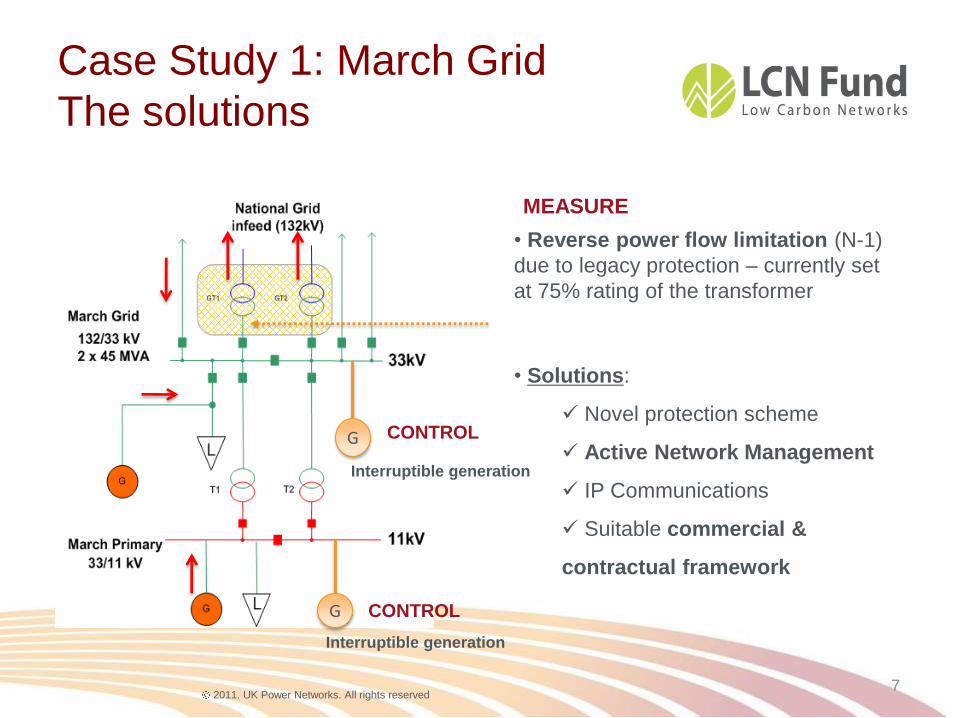

Case Study 1: March Grid

The challenge

2011. UK Power Networks. All rights reserved

• Reverse power flow limitation (N-1)

due to legacy protection – currently set

at 75% rating of the transformer

• Solutions:

Novel protection scheme

Active Network Management

IP Communications

Suitable commercial &

contractual framework

7

G

Interruptible generation

Interruptible generation

MEASURE

CONTROL

CONTROL

G

Case Study 1: March Grid

The solutions

2011. UK Power Networks. All rights reserved

Local Substation thermal constraint

Proposed New Generation Project

ANM

WAN / RF Mesh

Proposed New

Generation Project

New 33kV

underground cable

Closest point of

connection

Case Study 2: Single Wind Farm Dynamic Line Rating

DLR

Business as Usual:

• Higher costs

• Longer lead times

Local Substation thermal constraint

Smart Solution: Smart Device – Dynamic Line Rating (DLR)

Active Network Management (ANM) System

Smart Commercial Arrangements

2011. UK Power Networks. All rights reserved 9

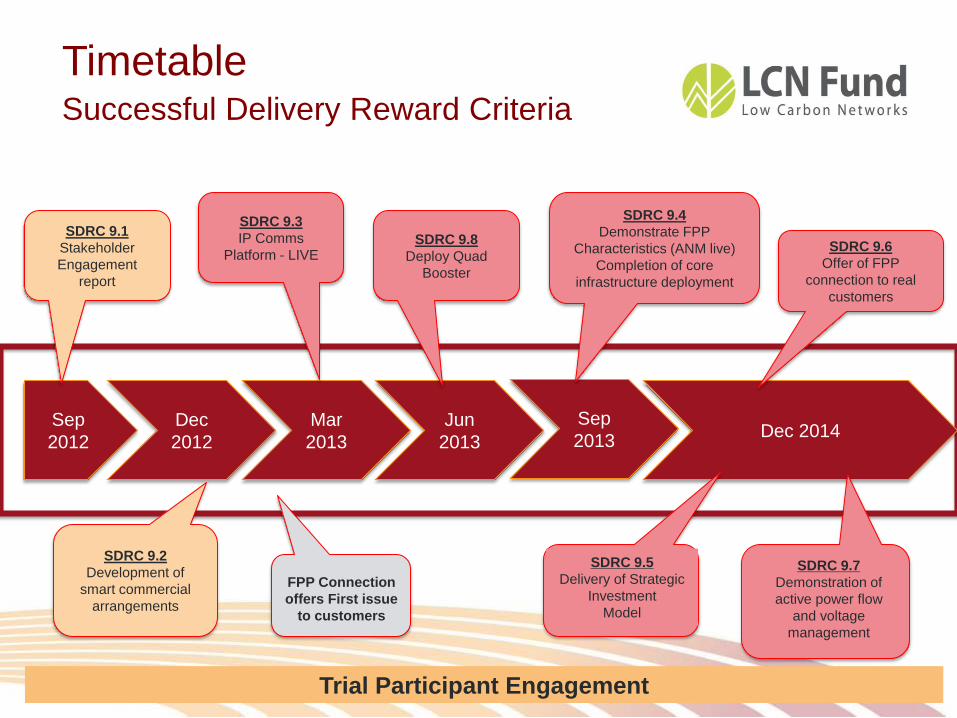

Sep

2012

Dec

2012

Mar

2013

Jun

2013 Dec 2014

SDRC 9.1

Stakeholder

Engagement

report

SDRC 9.3

IP Comms

Platform - LIVE SDRC 9.8

Deploy Quad

Booster

Sep

2013

SDRC 9.4

Demonstrate FPP

Characteristics (ANM live)

Completion of core

infrastructure deployment

SDRC 9.6

Offer of FPP

connection to real

customers

SDRC 9.7

Demonstration of

active power flow

and voltage

management

SDRC 9.5

Delivery of Strategic

Investment

Model

Trial Participant Engagement

SDRC 9.2

Development of

smart commercial

arrangements

FPP Connection

offers First issue

to customers

Timetable Successful Delivery Reward Criteria - SDRC

2011. UK Power Networks. All rights reserved

Customer engagement

Seven projects seeking connection in the trial area were identified and six of them

(26.2MW) have received FPP offers on1 March 2013

The FPP “Opt-in” offer introduced a standstill period and a commitment to UK Power

Networks to provide an alternative by 01/03

Customers received a “Briefing Document” which is an FPP information pack

Applications were consolidated in the FPP area to ensure all customers are treated

equally

1 March 2013

Enquiry and

application

Accept s16

Offer & opt

into FPP

FPP

investigation

period

S16 offer with

FPP Opt in

option

Receive s16

variation

including FPP

alternative

Accept FPP

variation

Proceed with

s16 Offer

Walk away 1st

stage

payme

nt

2011. UK Power Networks. All rights reserved

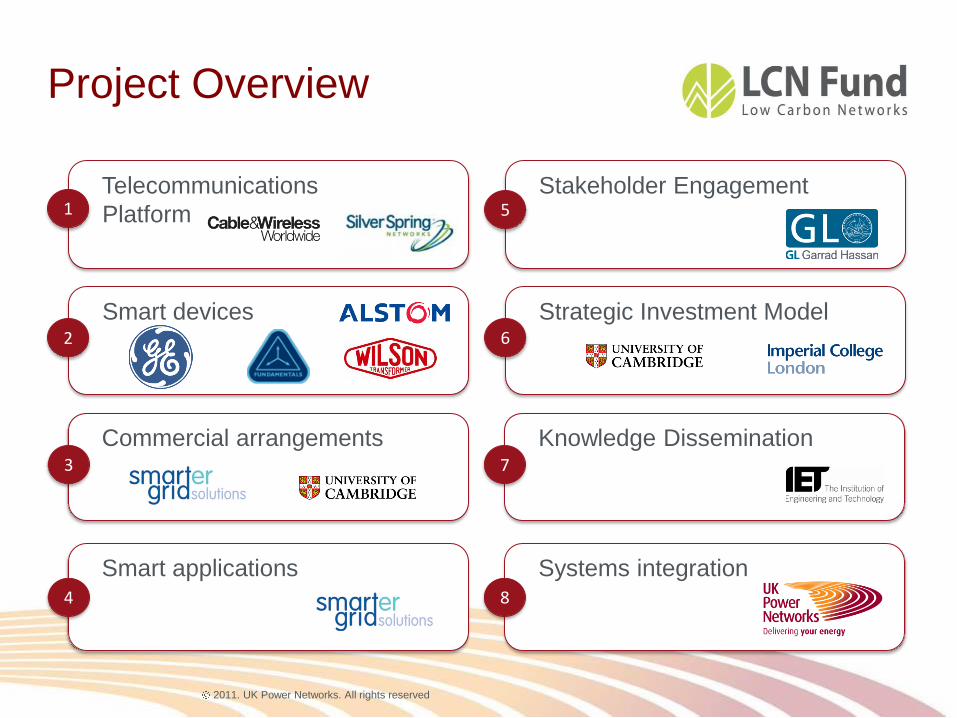

Systems integration

Smart applications

Knowledge Dissemination

Commercial arrangements

Strategic Investment Model

Smart devices

Telecommunications

Platform

Stakeholder Engagement 1 5

2 6

3 7

4 8

Project Overview

2011. UK Power Networks. All rights reserved

Commercial Arrangements

University of Cambridge Report:

Four case studies to understand how these issues are addressed elsewhere

Principles of Access Report:

In collaboration with Baringa Partners and Smarter Grid Solutions

Understand commercial alternatives for immediate implementation

Connection Agreement Template

Incorporate interruptibility to existing template

Case Study Principles of Access Pay compensation

Orkney, SSE LIFO NO

Connect and Manage Market Based approach YES

Ireland Pro-Rata YES

California Pro-Rata YES

2011. UK Power Networks. All rights reserved

Concepts to keep in mind

• Constraints

• Curtailment

• Interruptible connections

• Active Network Management

• Distributed Generation

Flexible Plug and Play Smart Commercial Arrangements

Adriana Laguna-Estopier - Low Carbon Project Manager

2011. UK Power Networks. All rights reserved

Contents

• Customer Recruitment

• Understanding Curtailment

• Principles of Access

• Commercial Packages

• Capacity Quota

• Commercial Framework for Flexible Plug and Play

• Challenges and Next Steps

2011. UK Power Networks. All rights reserved 16

Customers seeking connection in the trial area

Be proactive through stakeholder engagement

Recruiting within the existing connections process

Demonstrating a clear business case and benefits to customers

Customer recruitment

Wind Farm 33 kV 11 kV BAU offer Point of Connection

A 0.5 £1.9 m 11kV feeder - 10.5km

B 2.5 £1.9 m 11kV feeder - 12.75km

C 1 £2.0 m 11kV feeder - 9.5km

D 7.2 £3.5 m 33kV feeder - 13.5km

E 10 £4.8 m 132/33kV site

F 5 £1.2 m 132/33kV site

2011. UK Power Networks. All rights reserved 17

Understanding Curtailment

Network topology can

change through time, both

for maintenance and network

efficiency

Local demand can off set

generation output that exceeds

the capacity limit of the constraint

The level of the thermal

constraints can vary with

temperature / weather

Level of generation behind a

constraint relative to the capacity

of the constraint is a key driver of

curtailment

When we have multiple generators, how do we decide when to curtail each

one and how much do we curtail them?

2011. UK Power Networks. All rights reserved

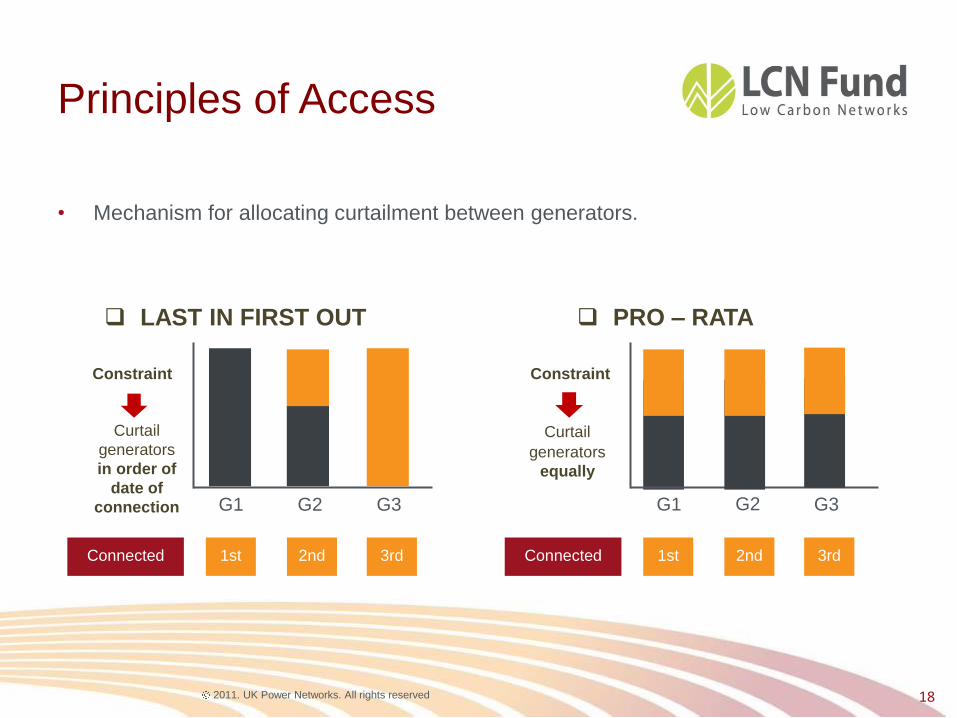

• Mechanism for allocating curtailment between generators.

LAST IN FIRST OUT PRO – RATA

G1 G2 G3

Curtail

generators

in order of

date of

connection

Constraint

G1 G2 G3

Curtail generators

equally

Constraint

Connected 1st

18

2nd 3rd Connected 1st 2nd 3rd

Principles of Access

2011. UK Power Networks. All rights reserved

19

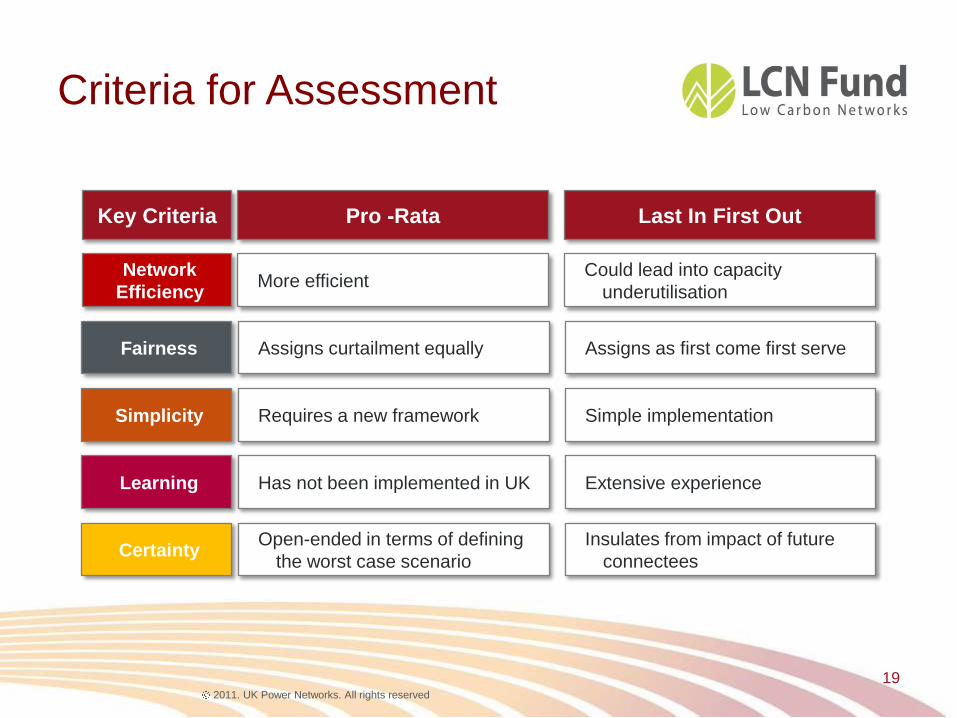

More efficient

Pro -Rata

Network

Efficiency

Certainty

Fairness

Simplicity

Learning

Criteria of Assessment: What are we optimising? Criteria for Assessment

Could lead into capacity

underutilisation

Key Criteria Last In First Out

Open-ended in terms of defining

the worst case scenario

Insulates from impact of future

connectees

Assigns curtailment equally Assigns as first come first serve

Requires a new framework Simple implementation

Has not been implemented in UK Extensive experience

2011. UK Power Networks. All rights reserved

Commercial Packages

• Time Vintaging

• Capacity Auction

• Capacity Quota:

– Based on defining a specific level of curtailment

– Based on comparing the cost of curtailment to the cost

of reinforcement

2011. UK Power Networks. All rights reserved

Capacity Quota

• Curtailment levels (MWh/yr) will increase as more capacity connects, increasing

generators’ lost revenues

• We plan to set the quota at the level where the cost of curtailment is equal or

exceeds the cost of reinforcement

2011. UK Power Networks. All rights reserved

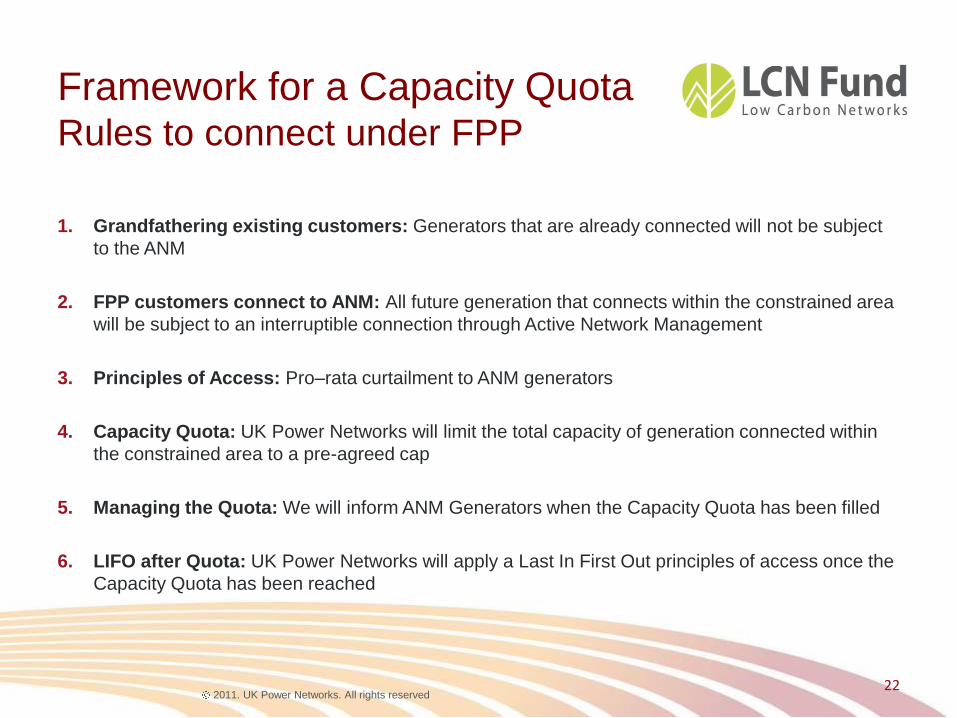

Framework for a Capacity Quota Rules to connect under FPP

1. Grandfathering existing customers: Generators that are already connected will not be subject

to the ANM

2. FPP customers connect to ANM: All future generation that connects within the constrained area

will be subject to an interruptible connection through Active Network Management

3. Principles of Access: Pro–rata curtailment to ANM generators

4. Capacity Quota: UK Power Networks will limit the total capacity of generation connected within

the constrained area to a pre-agreed cap

5. Managing the Quota: We will inform ANM Generators when the Capacity Quota has been filled

6. LIFO after Quota: UK Power Networks will apply a Last In First Out principles of access once the

Capacity Quota has been reached

22

2011. UK Power Networks. All rights reserved

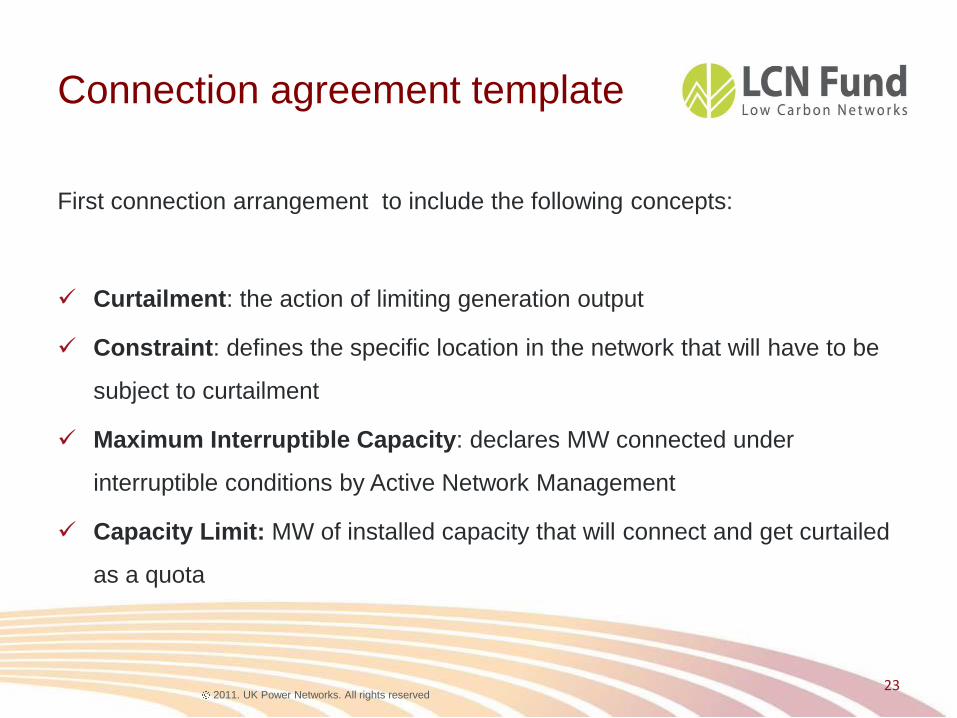

Connection agreement template

First connection arrangement to include the following concepts:

Curtailment: the action of limiting generation output

Constraint: defines the specific location in the network that will have to be

subject to curtailment

Maximum Interruptible Capacity: declares MW connected under

interruptible conditions by Active Network Management

Capacity Limit: MW of installed capacity that will connect and get curtailed

as a quota

23

2011. UK Power Networks. All rights reserved

Reinforcement Triggers

G

G G L

G G G

Reinforce transformer

G

G G

G

Reinforce transformer

L

2. Generation triggered 1. Demand (load) triggered

2011. UK Power Networks. All rights reserved

Challenges and Next Steps

Challenges

Evaluate the possible alternatives while developing a solution for immediate trial

implementation with real customers

Address internal and external stakeholders’ concerns

Next Steps

Understand optimal cost allocation

Further sensitivity analysis

Continue customer engagement, understand client’s perception of our methodology

and findings

Signup customers and deliver connections under the FPP framework

25

2011. UK Power Networks. All rights reserved

Boardinghouse Wind Farm

UK Power Networks – Flexible Plug & Play

18 March 2013

www.ecogen.co.uk

2011. UK Power Networks. All rights reserved

About EcoGen

• Established renewable energy specialist

• Over 20 years experience in the design, build and operation of projects

• Capital financing expertise

• Significant practical experience of grid issues

2011. UK Power Networks. All rights reserved

About EcoGen

Development and Consenting

Commercialisation and Contract Procurement

Financial Structuring

Construction Management

Operational Management

Lifecycle Planning

EcoGen’s offering covers the entire range of services required to successfully manage a renewable

energy project

from initial site feasibility assessment to end of its operational life

2011. UK Power Networks. All rights reserved

About Boardinghouse Wind Farm

• 5 turbine project – 5km south west of March

• Submitted for planning in September 2009

• Consented on appeal in July 2011

• Subject to MoD Radar constraint – removed in August 2012

• Unable to accept a grid offer whilst significant project uncertainty existed

• Applied to UKPN in September 2012

• BAU offer accepted late 2012

2011. UK Power Networks. All rights reserved

Challenges Ahead

• Understanding the implications of the FPP offer Construction

Operational

Financial

• Undertaking suitable due diligence on the constraint modelling Identifying and appointing suitable consultants

Translating the constraint effect in to the energy yield forecast

Deciding on a suitable range of sensitivities

Presenting it to financiers

• Assessing the connection agreement documentation

• Within the next 90 days

2011. UK Power Networks. All rights reserved

Challenges Ahead

• Managing all of this through the contractual, technical and financial due diligence process

• Identifying a funding structure which does not unduly discount the value of the project as the result of perceived uncertainty

• Staying clear of Government intervention in the Renewables Obligation

2011. UK Power Networks. All rights reserved

Contact Details

• Steve Read +44 (0)1354 699026

+44 (0)7876 252 154

• Tim Kirby +44 (0)8453 457731

+44 (0)7774 606646

• Main Office Ecogen Limited

PO Box 49

Chacewater

Truro

TR4 8WZ

• www.ecogen.co.uk

2011. UK Power Networks. All rights reserved

Flexible Plug and Play

Understanding best practice regarding interruptible

connections for wind generation: lessons from national and

international experience

Michael G. Pollitt, Karim L. Anaya

EPRG-University of Cambridge 18 March 2013

33

2011. UK Power Networks. All rights reserved

Contents

• This Report

• About Curtailment

• Selection of Case Studies

• Case Studies

• Conclusions

• Next Steps

34

2011. UK Power Networks. All rights reserved

This report

• The Electricity Policy Research Group (EPRG) from

University of Cambridge is the project partner responsible

for exploring and analysing different case studies of

commercial arrangements that involve the allocation of

curtailment (‘Principle’ of Access) in response to network

constraints.

• The report is part of the SDRC 9.2 (submitted by UK Power

Networks in December 2012).

35

2011. UK Power Networks. All rights reserved

About Curtailment

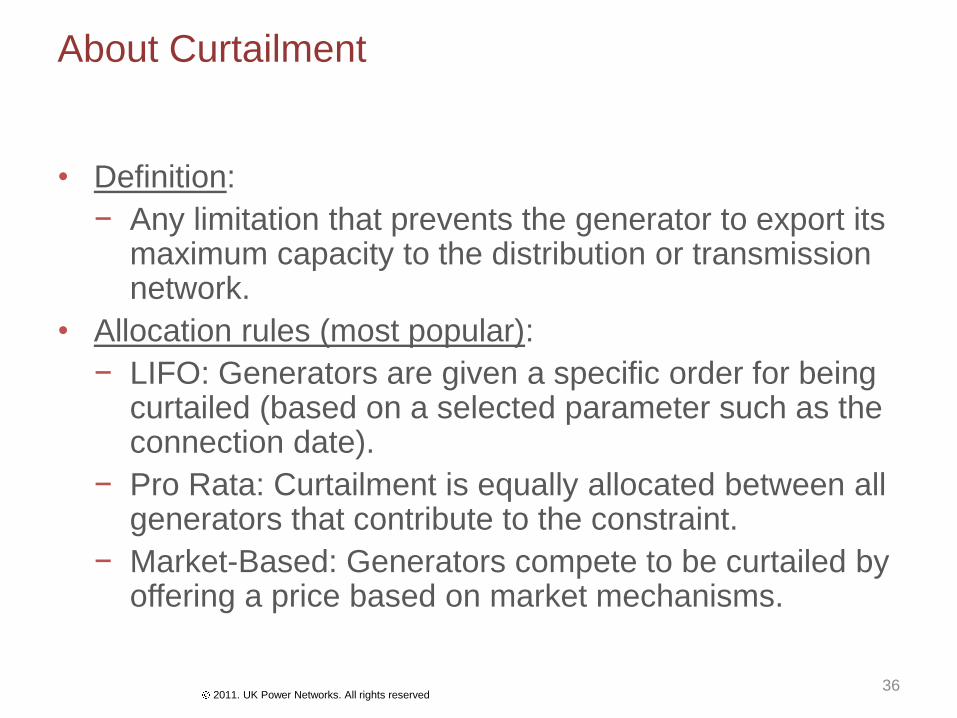

• Definition:

− Any limitation that prevents the generator to export its maximum capacity to the distribution or transmission network.

• Allocation rules (most popular):

− LIFO: Generators are given a specific order for being curtailed (based on a selected parameter such as the connection date).

− Pro Rata: Curtailment is equally allocated between all generators that contribute to the constraint.

− Market-Based: Generators compete to be curtailed by offering a price based on market mechanisms.

36

2011. UK Power Networks. All rights reserved

About Curtailment

37

Figure 1: Example of Risk Allocation

2011. UK Power Networks. All rights reserved

About Curtailment • Social optimality:

− LIFO: reflects the social optimum (each generator is exposed to their marginal connection/curtailment cost, MCC) to the system) . MCC should be = Marginal Benefit (MB).

− Pro Rata: does not reflect the social optimum (generator faces the average connection/curtailment costs, ACC). ACC=MB. Social loss = shaded area (figure 2).

− Shaded area: those incremental system costs above the system benefit (produced by each additional MW of wind generation beyond the point where MCC=MB).

− It has been assumed that the MB to the system of each additional unit capacity is constant (same subsidy and technology).

38

2011. UK Power Networks. All rights reserved

About Curtailment

39

Where M C C : M arginal connection cost, A C C : Average connectio cost, M B : M arginal benefits,

Q M F C : M ax firm connection, Q* M L : M ax LIFO, Q M P R : M ax Pro Rata. Own elaboration.

Cost

s (£)

MW connectedQMFC Q*ML QMPR

MCC

ACC

MB

Social loss under Max Pro Rata

Figure 2: Optimal connection (MW) with fixed constraint (ignoring risk)

2011. UK Power Networks. All rights reserved

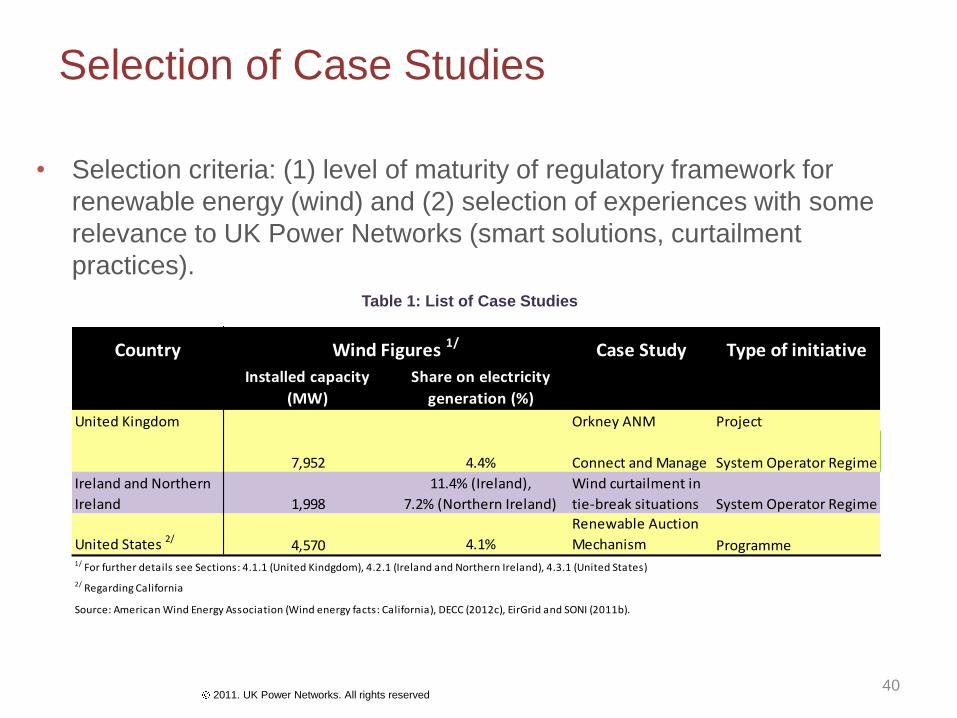

Selection of Case Studies

• Selection criteria: (1) level of maturity of regulatory framework for

renewable energy (wind) and (2) selection of experiences with some

relevance to UK Power Networks (smart solutions, curtailment

practices).

40

Country Case Study Type of initiative

Installed capacity

(MW)

Share on electricity

generation (%)

United Kingdom Orkney ANM Project

7,952 4.4% Connect and Manage System Operator Regime

Ireland and Northern

Ireland 1,998

11.4% (Ireland),

7.2% (Northern Ireland)

Wind curtailment in

tie-break situations System Operator Regime

United States 2/4,570 4.1%

Renewable Auction

Mechanism Programme1/ For further details see Sections: 4.1.1 (United Kindgdom), 4.2.1 (Ireland and Northern Ireland), 4.3.1 (United States)

2/ Regarding California

Source: American Wind Energy Association (Wind energy facts: California), DECC (2012c), EirGrid and SONI (2011b).

Wind Figures 1/

Table 1: List of Case Studies

2011. UK Power Networks. All rights reserved

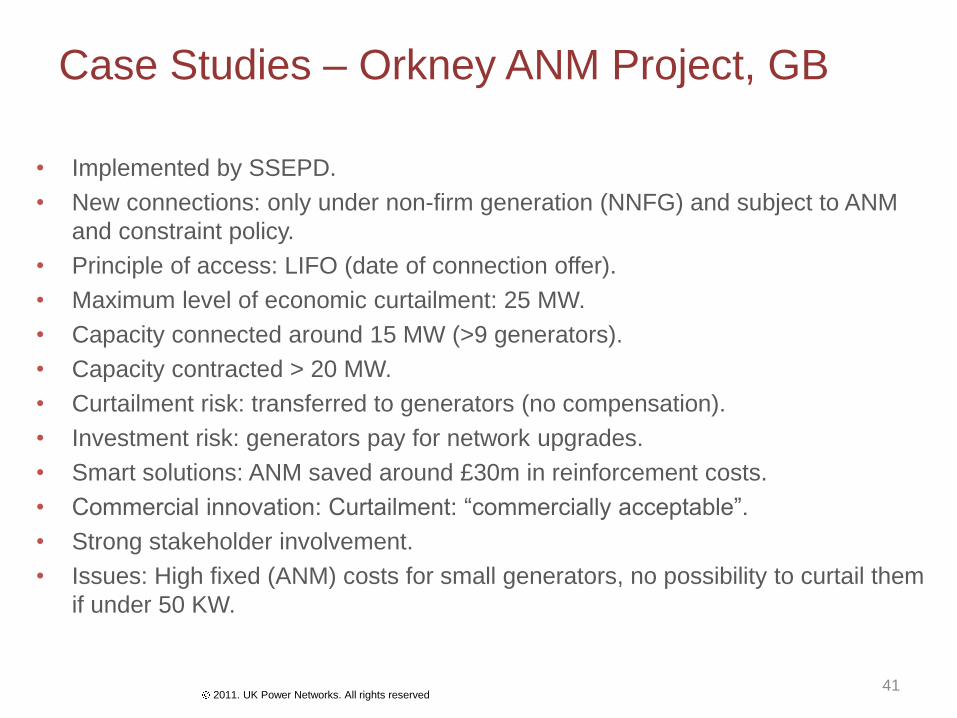

Case Studies – Orkney ANM Project, GB

• Implemented by SSEPD.

• New connections: only under non-firm generation (NNFG) and subject to ANM

and constraint policy.

• Principle of access: LIFO (date of connection offer).

• Maximum level of economic curtailment: 25 MW.

• Capacity connected around 15 MW (>9 generators).

• Capacity contracted > 20 MW.

• Curtailment risk: transferred to generators (no compensation).

• Investment risk: generators pay for network upgrades.

• Smart solutions: ANM saved around £30m in reinforcement costs.

• Commercial innovation: Curtailment: “commercially acceptable”.

• Strong stakeholder involvement.

• Issues: High fixed (ANM) costs for small generators, no possibility to curtail them

if under 50 KW.

41

2011. UK Power Networks. All rights reserved

Case Studies – Connect and Manage, GB

• Implemented by National Grid, replaced Invest and Connect (IC) and Interim Connect and Manage (ICM). The aim is to accelerate the number of generators connected.

• New connections: firm access (full access).

• Principle of Access: market-based. High price payments to wind generators under local constraints/low competition.

• Type of generators: renewable and non-renewables, including large and small embedded generation.

• Types of reinforcement works: (1) enabling works, (2) wider works. Enabling works allow early connections. The two-stage approach contribute to mitigating stranding risk for consumers. 805 MW connected by 31 December 2012.

• Curtailment risk: socialisation of all constraint costs (BSUoS).

• Investment risk: transferred to SO users (TNUoS).

• Issues: increase on network congestion, payments to generators (wind generators) do not reflect subsidies, difficult to apply to DNOs.

42

2011. UK Power Networks. All rights reserved

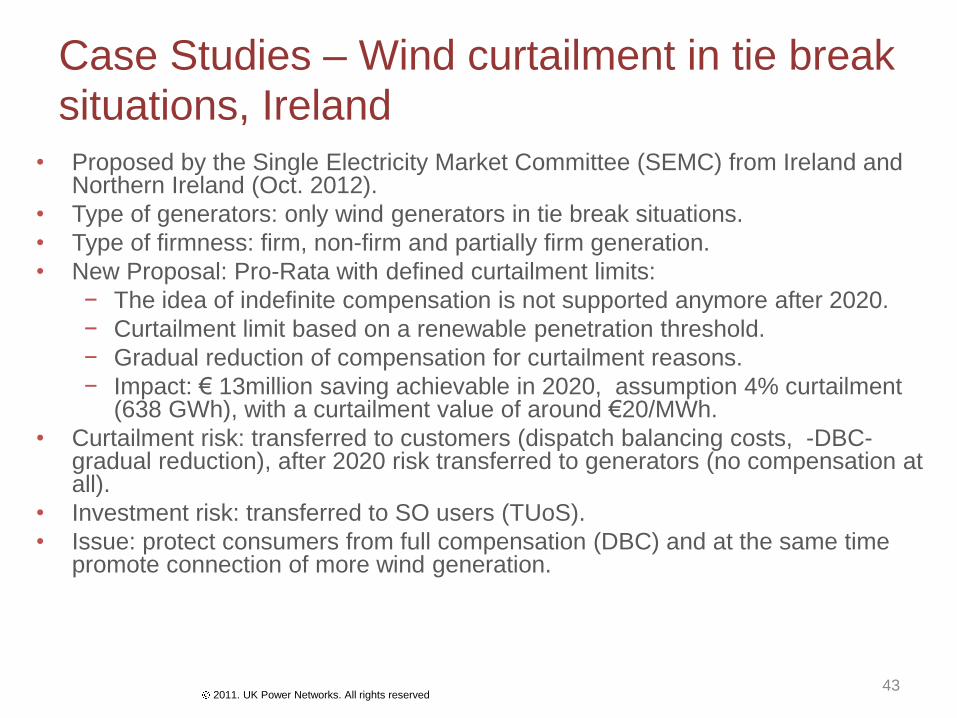

Case Studies – Wind curtailment in tie break

situations, Ireland • Proposed by the Single Electricity Market Committee (SEMC) from Ireland and

Northern Ireland (Oct. 2012).

• Type of generators: only wind generators in tie break situations.

• Type of firmness: firm, non-firm and partially firm generation.

• New Proposal: Pro-Rata with defined curtailment limits:

− The idea of indefinite compensation is not supported anymore after 2020.

− Curtailment limit based on a renewable penetration threshold.

− Gradual reduction of compensation for curtailment reasons.

− Impact: € 13million saving achievable in 2020, assumption 4% curtailment (638 GWh), with a curtailment value of around €20/MWh.

• Curtailment risk: transferred to customers (dispatch balancing costs, -DBC- gradual reduction), after 2020 risk transferred to generators (no compensation at all).

• Investment risk: transferred to SO users (TUoS).

• Issue: protect consumers from full compensation (DBC) and at the same time promote connection of more wind generation.

43

2011. UK Power Networks. All rights reserved

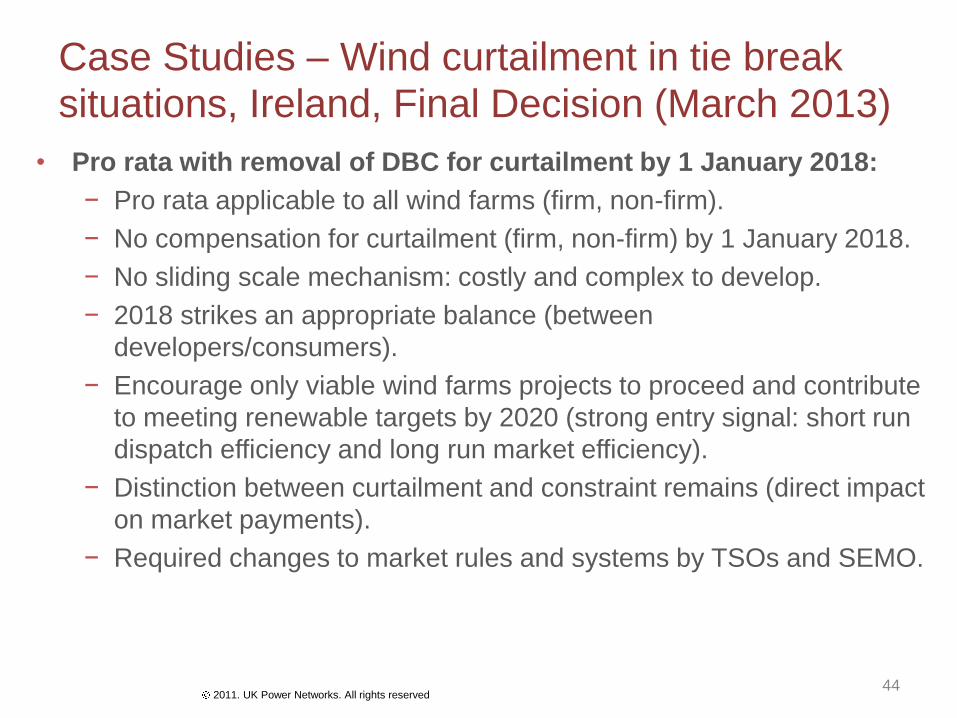

Case Studies – Wind curtailment in tie break

situations, Ireland, Final Decision (March 2013)

• Pro rata with removal of DBC for curtailment by 1 January 2018:

− Pro rata applicable to all wind farms (firm, non-firm).

− No compensation for curtailment (firm, non-firm) by 1 January 2018.

− No sliding scale mechanism: costly and complex to develop.

− 2018 strikes an appropriate balance (between

developers/consumers).

− Encourage only viable wind farms projects to proceed and contribute

to meeting renewable targets by 2020 (strong entry signal: short run

dispatch efficiency and long run market efficiency).

− Distinction between curtailment and constraint remains (direct impact

on market payments).

− Required changes to market rules and systems by TSOs and SEMO.

44

2011. UK Power Networks. All rights reserved

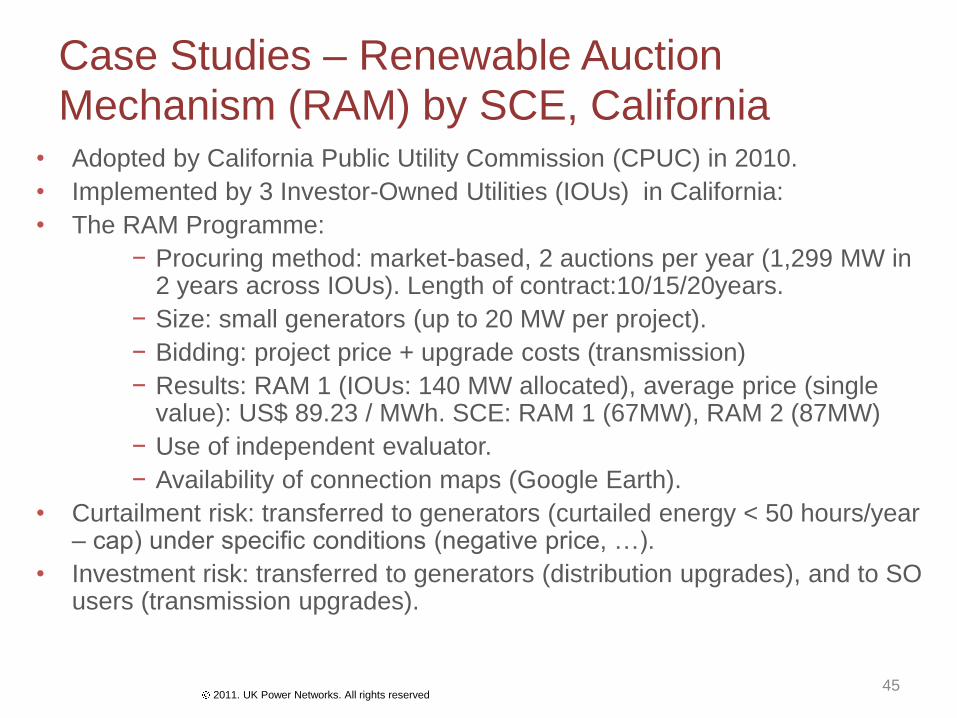

Case Studies – Renewable Auction

Mechanism (RAM) by SCE, California • Adopted by California Public Utility Commission (CPUC) in 2010.

• Implemented by 3 Investor-Owned Utilities (IOUs) in California:

• The RAM Programme:

− Procuring method: market-based, 2 auctions per year (1,299 MW in 2 years across IOUs). Length of contract:10/15/20years.

− Size: small generators (up to 20 MW per project).

− Bidding: project price + upgrade costs (transmission)

− Results: RAM 1 (IOUs: 140 MW allocated), average price (single value): US$ 89.23 / MWh. SCE: RAM 1 (67MW), RAM 2 (87MW)

− Use of independent evaluator.

− Availability of connection maps (Google Earth).

• Curtailment risk: transferred to generators (curtailed energy < 50 hours/year – cap) under specific conditions (negative price, …).

• Investment risk: transferred to generators (distribution upgrades), and to SO users (transmission upgrades).

45

2011. UK Power Networks. All rights reserved

Conclusions

• Principle of Access: LIFO, Pro Rata and market-based

represent different alternatives of how the DNOs could

address the need for connection of more wind to the existing

distribution system.

− LIFO: makes economically efficient use of the available

capacity in the short run, but transfers increasing risk to

the last in generator connected. May compromise

dynamic efficiency by making it more difficult to get

agreement to increase network capacity when this

becomes socially valuable.

46

2011. UK Power Networks. All rights reserved

Conclusions

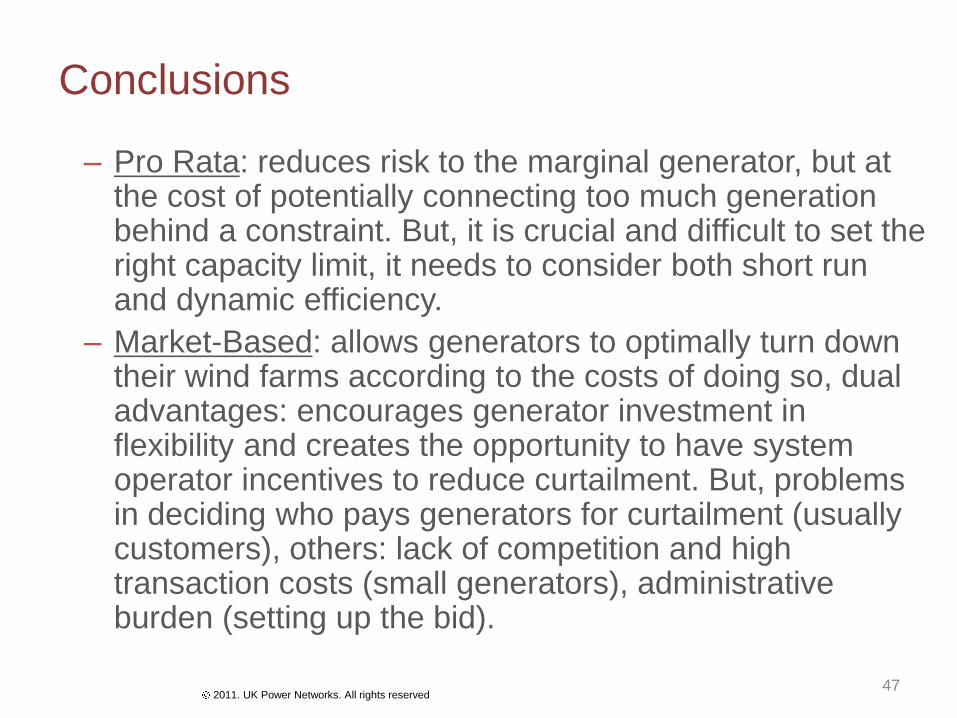

– Pro Rata: reduces risk to the marginal generator, but at the cost of potentially connecting too much generation behind a constraint. But, it is crucial and difficult to set the right capacity limit, it needs to consider both short run and dynamic efficiency.

– Market-Based: allows generators to optimally turn down their wind farms according to the costs of doing so, dual advantages: encourages generator investment in flexibility and creates the opportunity to have system operator incentives to reduce curtailment. But, problems in deciding who pays generators for curtailment (usually customers), others: lack of competition and high transaction costs (small generators), administrative burden (setting up the bid).

47

2011. UK Power Networks. All rights reserved

Conclusions

• Allocation of risks among the parties:

– Curtailment risk:

System operators usually transfer the risk of transmission

connected generation being curtailed to final customers (i.e.

through DBC-Ireland/NI, BSUoS-UK). However for

distribution connected generation, the rules are less

homogeneous (SEEPD does not compensate, SCE

compensates based on a cap curtailment: 50 hours/year).

48

2011. UK Power Networks. All rights reserved

Conclusions

• Allocation of risks among the parties

– Investment risk:

Generally transferred to the generators when an upgrade to

the distribution network is required. When a transmission

network upgrade is necessary the investment risk is

transferred to the users. Thus, regulation allows the

socialisation of transmission upgrades but not the

socialisation of distribution upgrades.

49

2011. UK Power Networks. All rights reserved

Conclusions

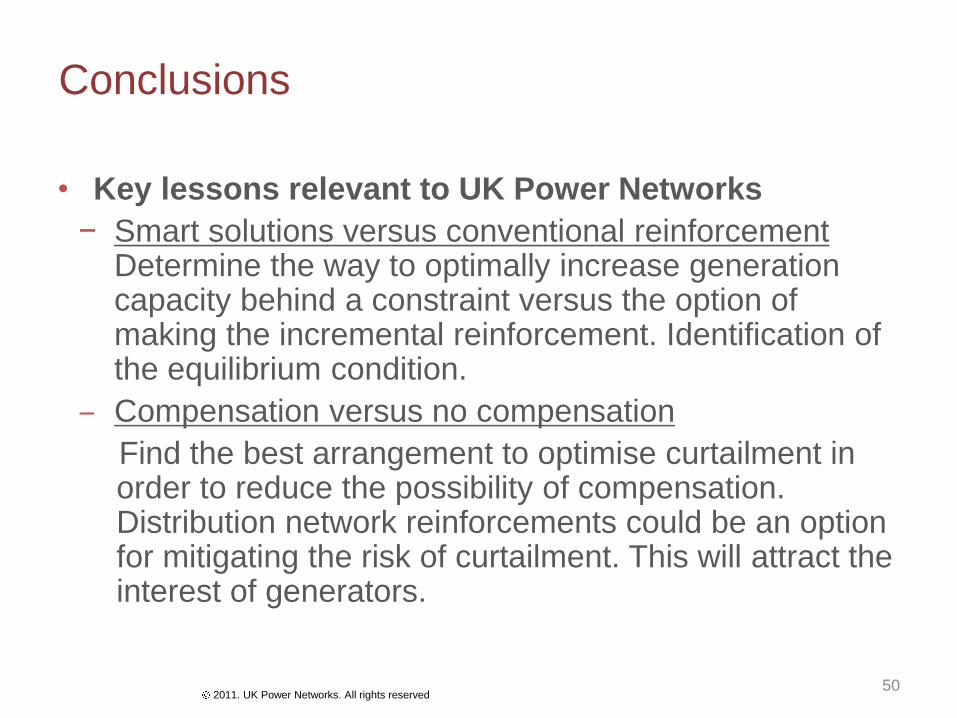

• Key lessons relevant to UK Power Networks

− Smart solutions versus conventional reinforcement Determine the way to optimally increase generation capacity behind a constraint versus the option of making the incremental reinforcement. Identification of the equilibrium condition.

‒ Compensation versus no compensation

Find the best arrangement to optimise curtailment in order to reduce the possibility of compensation. Distribution network reinforcements could be an option for mitigating the risk of curtailment. This will attract the interest of generators.

50

2011. UK Power Networks. All rights reserved

Conclusions

‒ Publishing interconnection/connection maps as a way

for encouraging connections to less congested points:

Provides more transparency on the status of the

network (valuable information for generators for the

selection of the most convenient connection points)

and accelerates the evaluation process conducted by

the DNOs.

‒ Stakeholder engagement matters:

Promote stakeholder engagement by encouraging

active participation of key parties in the development

and implementation of the Flexible Plug and Play trial.

51

2011. UK Power Networks. All rights reserved

Conclusions

‒ Auction mechanism is an alternative way for

procurement of renewables with focus on small

generators in which price and connection costs are bid:

Applied by SCE (4.9 million customers). A regional

auction mechanism for procurement of small scale

renewables can be seen as a potential option to

accelerate the connection of the most cost-efficient

projects. This option may add more complexity to the

energy procurement process in terms of

implementation when there is not enough demand.

52

2011. UK Power Networks. All rights reserved

Next steps

• Publish the report as working paper (EPRG), academic

journals (shorter versions): IEEE Transactions on Power

Systems, Energy Policy.

• Writing new report examining the costs and benefits of

different options for connecting non-firm generation to

the DNO networks, while taking decisions on when to

reinforce into account.

53

Flexible Plug and Play Connection Offer and Next Steps

2011. UK Power Networks. All rights reserved

Flexible Plug and Play Offer

• On 1 March, FPP customers received:

Cost of FPP connection

Interruptible Connection Agreement template

Briefing Document explaining the rules of FPP and Calculation of

the Quota

Curtailment estimates for now and worst case scenario

2011. UK Power Networks. All rights reserved

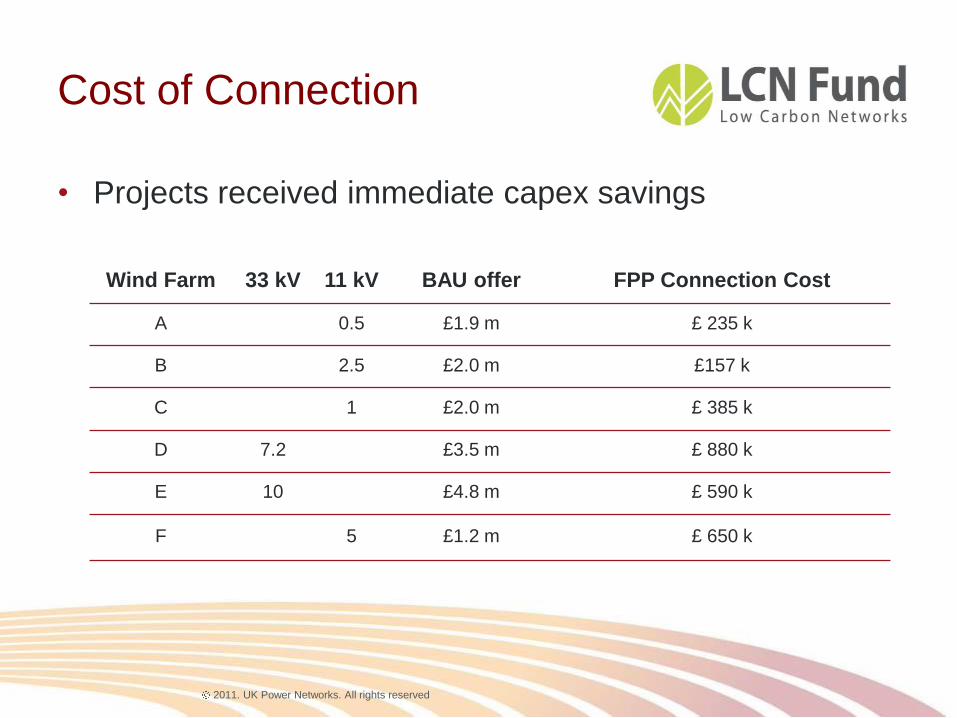

Cost of Connection

• Projects received immediate capex savings

Wind Farm 33 kV 11 kV BAU offer FPP Connection Cost

A 0.5 £1.9 m £ 235 k

B 2.5 £2.0 m £157 k

C 1 £2.0 m £ 385 k

D 7.2 £3.5 m £ 880 k

E 10 £4.8 m £ 590 k

F 5 £1.2 m £ 650 k

2011. UK Power Networks. All rights reserved

Capacity quota Methodology

57

1. Calculate the reinforcement cost (£4.1m)

2. Curtailment modeling results (MWh curtailed / MW connected behind the constraint)

3. Generator revenue loss assumptions (determine £/MW of curtailed output)

March Grid calculations indicate a quota of 33.5 MW

2011. UK Power Networks. All rights reserved

Curtailment Estimates

58

The Flexible Plug and Play connection offer includes:

Curtailment estimates, considering the worst case scenario of when

the “Quota” is full.

2011. UK Power Networks. All rights reserved

Curtailment Estimates

59

Scenario 3, full quota, 5-year power output

2011. UK Power Networks. All rights reserved

Next Steps

• Facilitate due diligence on offers and respond to questions

• Support the customers as required to acceptance of their connection offers

and discussions with financing bodies

• Define how the capacity quota will be managed

• Continue to identify potential customers in the FPP trial area and offer the FPP

solution

• Continue discussions around cost allocation, reinforcement guarantees and

potential commercial solutions

• Learning and dissemination / Stakeholder engagement

• Assessment for BAU implementation