Embed Size (px)

Citation preview

9-1

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Flexible Budgets and Overhead Analysis

Management Accounting Lecture 16 (Chapter 9)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Today’s Agenda

n What is a Flexible Budget n Flexible versus Static Budget

n Shortcomings of Static Budgets

n Advantages of Flexible Budgets

n Building a Flexible Budget

n Variance Analysis

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

AH × SR AH × AR

Spending variance = AH(AR - SR) Efficiency variance = SR(AH - SH)

SH × SR

Spending Variance

Efficiency Variance

Actual Flexible Budget Flexible Budget Variable for Variable for Variable Overhead Overhead at Overhead at Incurred Actual Hours Standard Hours

Variable Overhead Variances

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

3,300 hours 3,200 hours × × $2.00 per hour $2.00 per hour

Variable Overhead Variances – Example

$6,740 $6,600 $6,400

Spending variance $140 unfavorable

Efficiency variance $200 unfavorable

$340 unfavorable flexible budget total variance

Actual Flexible Budget Flexible Budget Variable for Variable for Variable Overhead Overhead at Overhead at Incurred Actual Hours Standard Hours

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Efficiency Variance Controlled by managing the overhead cost

driver.

Variable Overhead Variances – A Closer Look

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

2,050 hours 2,100 hours × × $5 per hour $5 per hour

Quick Check Summary

Actual Flexible Budget Flexible Budget Variable for Variable for Variable Overhead Overhead at Overhead at Incurred Actual Hours Standard Hours

$10,950 $10,250 $10,500

Spending variance $700 unfavorable

Efficiency variance $250 favorable

$450 unfavorable flexible budget total variance

9-2

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Activity-based Costing and the Flexible Budget

It is unlikely that all variable overhead will be driven by a single activity.

Activity-based costing can be used when multiple

activity bases drive variable overhead costs.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Computing Overhead Rates

Overhead from the flexible budget for the

denominator level of activity POHR =

Recall that overhead costs are assigned to products and services using a

predetermined overhead rate (POHR):

Assigned Overhead = POHR × Standard Activity

Denominator level of activity

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

The fixed component is useful

for preparing and analyzing fixed overhead

variances.

The predetermined overhead rate can be broken down into fixed

and variable components.

The variable component is useful

for preparing and analyzing variable overhead

variances.

Computing Overhead Rates

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Normal versus Standard Cost Systems

In a normal cost system, overhead is

applied to work in process based on the actual number of hours worked

in the period.

In a standard cost system, overhead is

applied to work in process based on the standard hours

allowed for the output of the period.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Budget Variance

Volume Variance

FR = Standard Fixed Overhead Rate SH = Standard Hours Allowed DH = Denominator Hours

SH × FR

Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied

DH × FR

The General Model – Fixed Overhead Variances

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Overhead Rates and Overhead Analysis – Example

ColaCo prepared this budget for overhead:

Total Variable Total Fixed Machine Variable Overhead Fixed Overhead

Hours Overhead Rate Overhead Rate 3,000 6,000 $ ? 9,000 $ ? 4,000 8,000 ? 9,000 ?

ColaCo applies overhead based on machine-hour activity.

Let’s calculate overhead rates.

9-3

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Rate = Total Variable Overhead ÷ Machine Hours

This rate is constant at all levels of activity.

Total Variable Total Fixed Machine Variable Overhead Fixed Overhead

Hours Overhead Rate Overhead Rate 3,000 6,000 $ 2.00 $ 9,000 $ ? 4,000 8,000 2.00 9,000 ?

Overhead Rates and Overhead Analysis – Example

ColaCo prepared this budget for overhead:

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Total Variable Total Fixed Machine Variable Overhead Fixed Overhead

Hours Overhead Rate Overhead Rate 3,000 6,000 $ 2.00 $ 9,000 $ 3.00 $ 4,000 8,000 2.00 9,000 2.25

Rate = Total Fixed Overhead ÷ Machine Hours

This rate decreases when activity increases.

Overhead Rates and Overhead Analysis – Example

ColaCo prepared this budget for overhead:

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Total Variable Total Fixed Machine Variable Overhead Fixed Overhead

Hours Overhead Rate Overhead Rate 3,000 6,000 $ 2.00 $ 9,000 $ 3.00 $ 4,000 8,000 2.00 9,000 2.25

The total POHR is the sum of the fixed and variable rates

for a given activity level.

Overhead Rates and Overhead Analysis – Example

ColaCo prepared this budget for overhead:

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

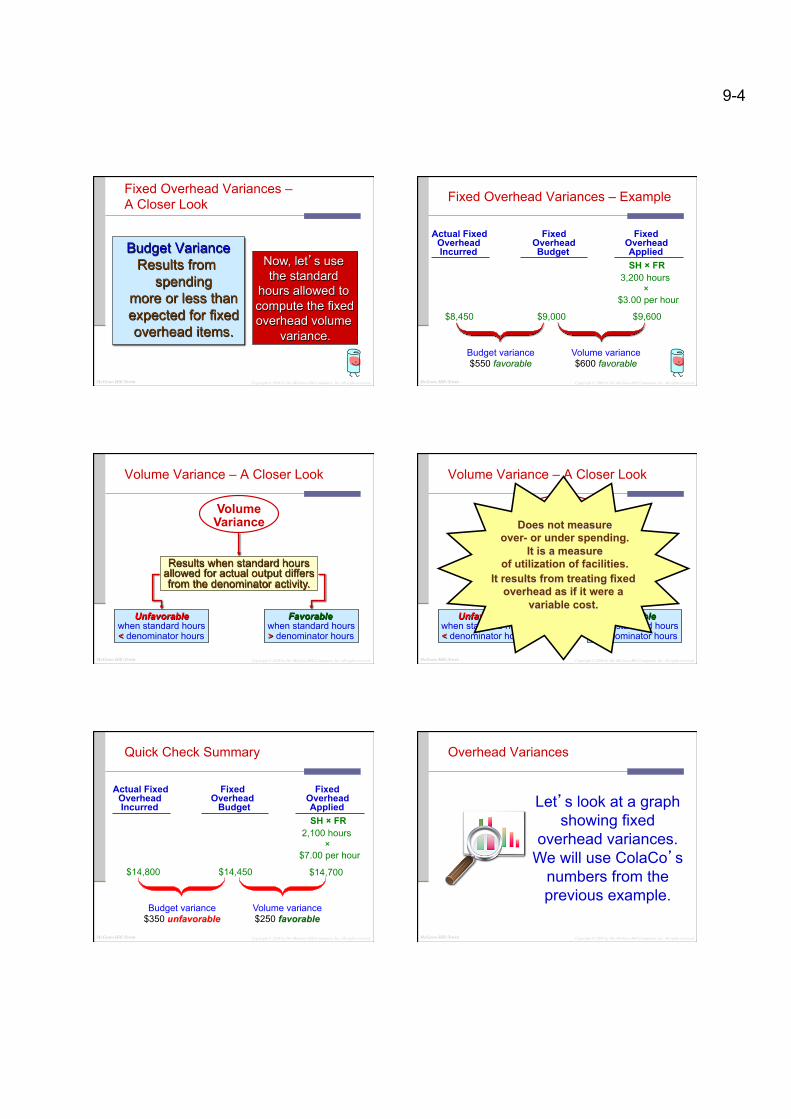

Fixed Overhead Variances – Example

ColaCo’s actual production required 3,200 - standard machine hours.

Actual fixed overhead was $8,450. The predetermined overhead rate is

based on 3,000 machine hours.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Overhead Variances

Now let’s turn our attention to calculating

fixed overhead variances

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Fixed Overhead Variances – Example

Budget variance $550 favorable

$8,450 $9,000

Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied

9-4

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Fixed Overhead Variances – A Closer Look

Budget Variance Results from

spending more or less than expected for fixed overhead items.

Now, let’s use the standard

hours allowed to compute the fixed overhead volume

variance.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

3,200 hours × $3.00 per hour

Budget variance $550 favorable

Fixed Overhead Variances – Example

$8,450 $9,000 $9,600

Volume variance $600 favorable

SH × FR

Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Volume Variance – A Closer Look

Volume Variance

Results when standard hours allowed for actual output differs from the denominator activity.

Unfavorable when standard hours < denominator hours

Favorable when standard hours > denominator hours

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Volume Variance

Results when standard hours allowed for actual output differs from the denominator activity.

Unfavorable when standard hours < denominator hours

Favorable when standard hours > denominator hours

Volume Variance – A Closer Look

Volume Variance

Results when standard hours allowed for actual output differs from the denominator activity.

Does not measure over- or under spending.

It is a measure of utilization of facilities.

It results from treating fixed overhead as if it were a

variable cost.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

2,100 hours × $7.00 per hour

Budget variance $350 unfavorable

$14,800 $14,450 $14,700

Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied

Volume variance $250 favorable

SH × FR

Quick Check Summary

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Overhead Variances

Let’s look at a graph showing fixed

overhead variances. We will use ColaCo’s

numbers from the previous example.

9-5

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Fixed Overhead Variances

Activity

Cost

3,000 Hours Expected Activity

$9,000 budgeted fixed OH

Fixed overhead

applied to products

Note: The slope of the line indicates that fixed overhead is applied at the rate of $3 per machine hour ($9,000/3,000)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Fixed Overhead Variances

$8,450 actual fixed OH

3,000 Hours Expected Activity

$9,000 budgeted fixed OH

$8,450 actual fixed OH $550 Favorable

Budget Variance

{

Activity

Cost

Fixed overhead

applied to products

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

{

Fixed Overhead Variances

$8,450 actual fixed OH

3,200 machine hours × $3.00 fixed overhead rate

$600 Favorable Volume Variance

$9,600 applied fixed OH

3,200 Standard

Hours

3,000 Hours Expected Activity

$9,000 budgeted fixed OH

$550 Favorable

Budget Variance

{ $8,450 actual fixed OH

Activity

Cost

Fixed overhead

applied to products

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Overhead Variances and Under- or Overapplied Overhead Cost

In a standard cost system:

Unfavorable variances are equivalent

to underapplied overhead.

Favorable variances are equivalent to overapplied overhead.

The sum of the overhead variances equals the under- or over applied

overhead cost for a period.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Review

n What is a Flexible Budget n Flexible versus Static Budget

n Shortcomings of Static Budgets

n Advantages of Flexible Budgets

n Building a Flexible Budget

n Variance Analysis

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Tutorial

n Review of today’s lecture

n Questions to be provided n E n F

9-6

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Exercise E (Question) Chapter 009, Flexible Budgets and Overhead Analysis

9-139

158. Holl Corporation has provided the following data for November.

Required: a. Compute the budget variance for November. Show your work! b. Compute the volume variance for November. Show your work!

a. Budget variance = Actual fixed overhead cost - Budgeted fixed overhead cost = $55,860 - $56,640 = $780 F b. Fixed portion of the predetermined overhead rate = $56,640/4,800 machine-hours = $11.80 per machine-hour Volume variance = Fixed portion of the predetermined overhead rate (Denominator hours - Standard hours allowed) = $11.80 (4,800 - 5,100) = $3,540 F

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Learning Objective: 6 Level: Easy

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Exercise F (Question) Chapter 009, Flexible Budgets and Overhead Analysis

9-134

153. Creger Corporation, which makes landing gears, has provided the following data for a recent month:

Required: Determine the total variance, the spending variance, and the efficiency variance for the variable overhead item supplies cost that would appear on the company's variable overhead performance report. Show your work!

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Learning Objective: 4 Level: Easy