Embed Size (px)

Citation preview

ACCTG 312Week 15 aChapter 7

Flexible Budgets, Cost Variances

andManagement

Control

1

Learning objectives

At the end of this chapter, you should be able to:

1. Discuss how companies use standard-costing systems to manage costs and describe three ways to set standards.

2. Define and distinguish between perfection and practical standards.

3. Compute and interpret direct-material price and quantity variances, and direct-labour rate, and efficiency variances.

Learning objectives (continued)

4. Determine the significance of cost variances.

5. Discuss the behavioural effects of standard costing and discuss the controllability of variances.

6. Explain how companies use standard costs in product costing.

7. Summarize some advantages attributed to standard costing.

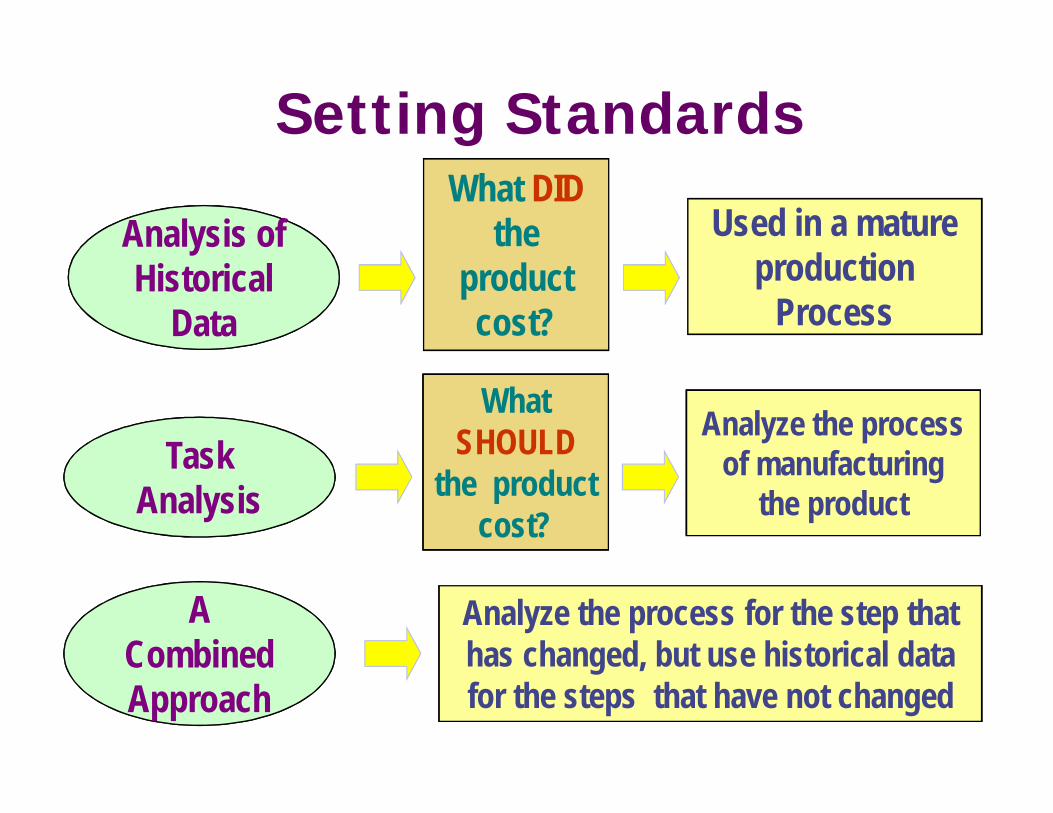

Analysis ofAnalysis ofHistorical

Data

TaskAnalysis

Used in a mature production

Process

Analyze the processof manufacturing

the product

What DIDthe

productcost?

What SHOULD

the product cost?

Approach

A CombinedApproach

Analyze the process for the step thathas changed, but use historical datafor the steps that have not changed

Setting Standards

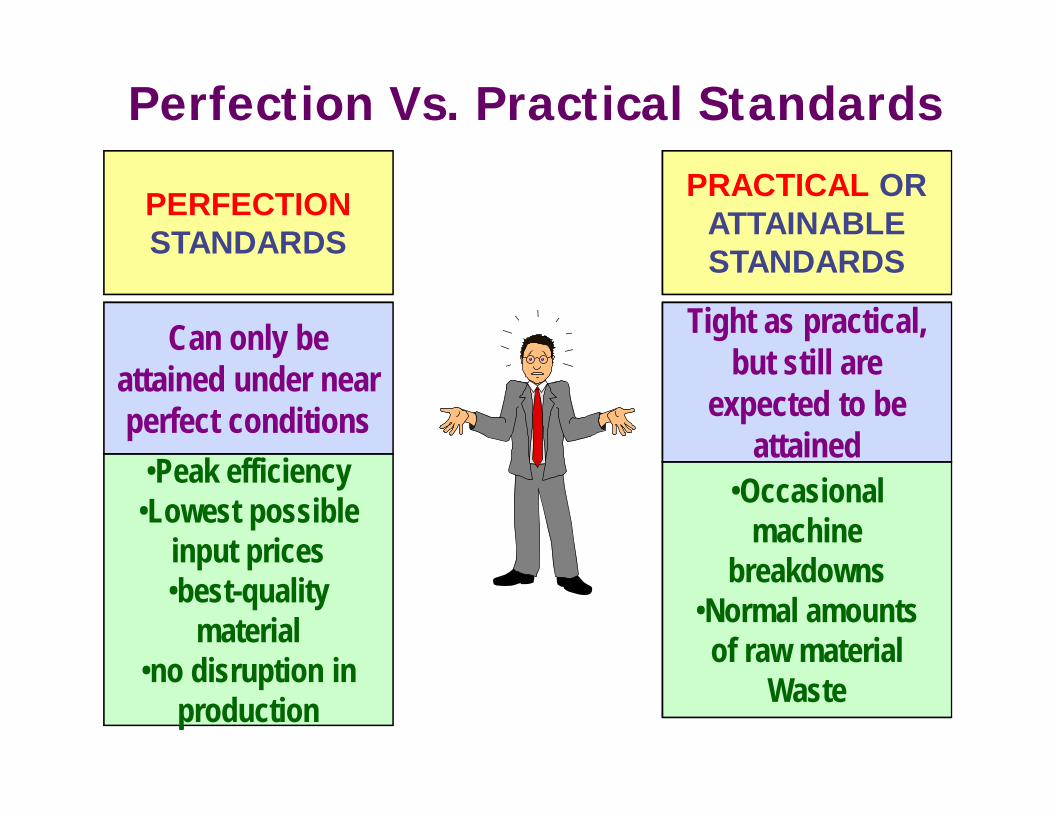

Perfection Vs. Practical Standards

PERFECTIONSTANDARDS

PRACTICAL ORATTAINABLESTANDARDS

Can only be attained under near perfect conditions

Tight as practical,

attained

Tight as practical,but still are

expected to be attained

•Occasional machine

breakdowns•Normal amounts

of raw materialWaste

•Peak efficiency

production

•Peak efficiency•Lowest possible

input prices•best-quality

material•no disruption in

production

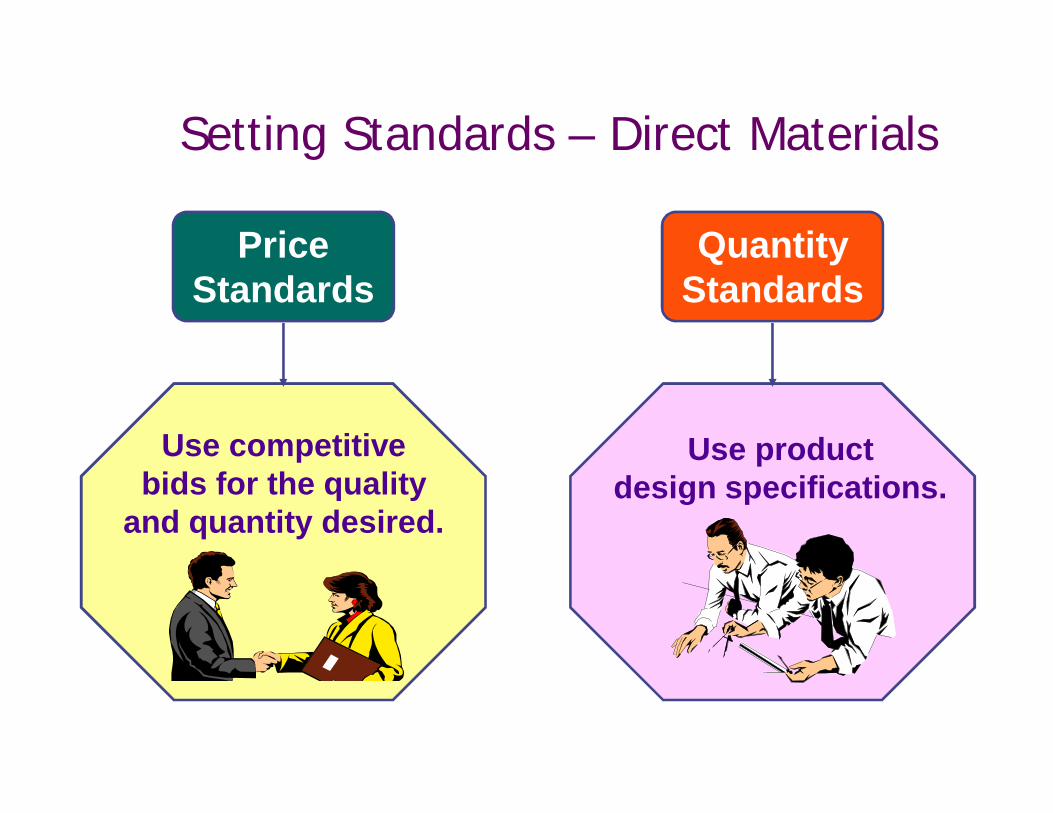

QuantityStandards

PriceStandards

Use product design specifications.

Use competitivebids for the quality

and quantity desired.

Setting Standards – Direct Materials

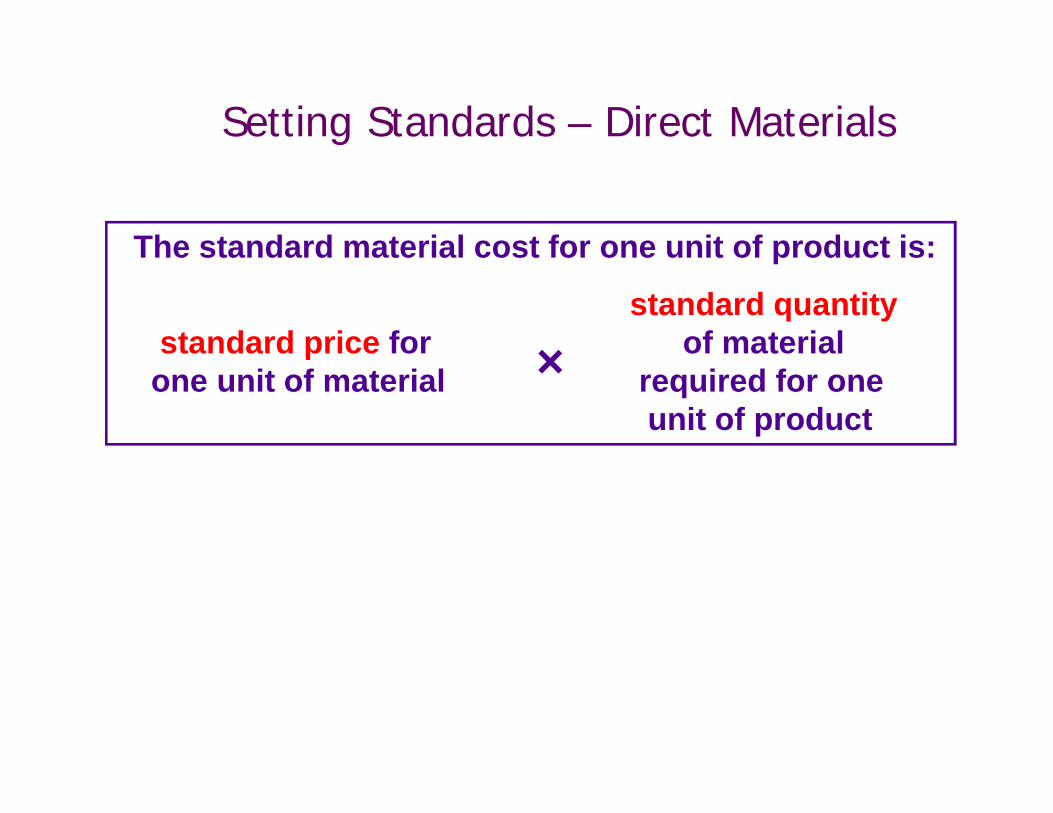

The standard material cost for one unit of product is:

standard quantitystandard price for of material

one unit of material required for one unit of product

×

Setting Standards – Direct Materials

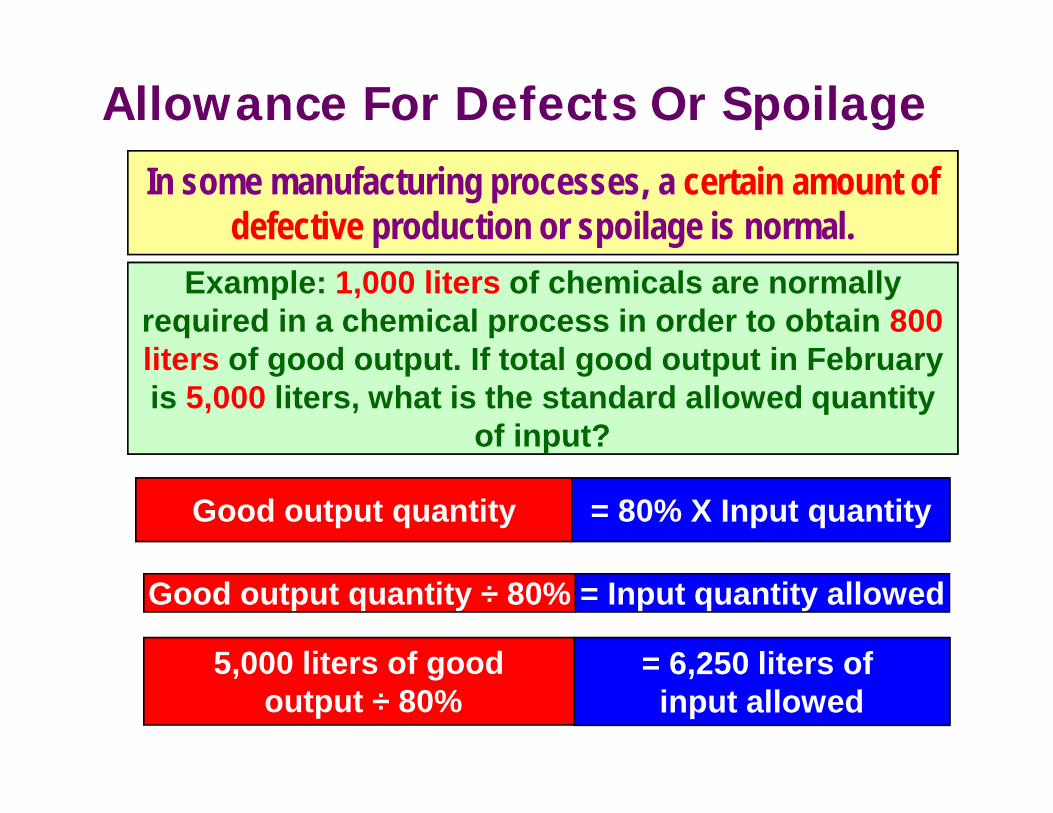

In some manufacturing processes, a certain amount of defective production or spoilage is normal.

Example: 1,000 liters of chemicals are normally required in a chemical process in order to obtain 800 liters of good output. If total good output in February is 5,000 liters, what is the standard allowed quantity

of input?

Good output quantity = 80% X Input quantity

Good output quantity ÷ 80% = Input quantity allowed

5,000 liters of goodoutput ÷ 80%

= 6,250 liters of input allowed

Allowance For Defects Or Spoilage

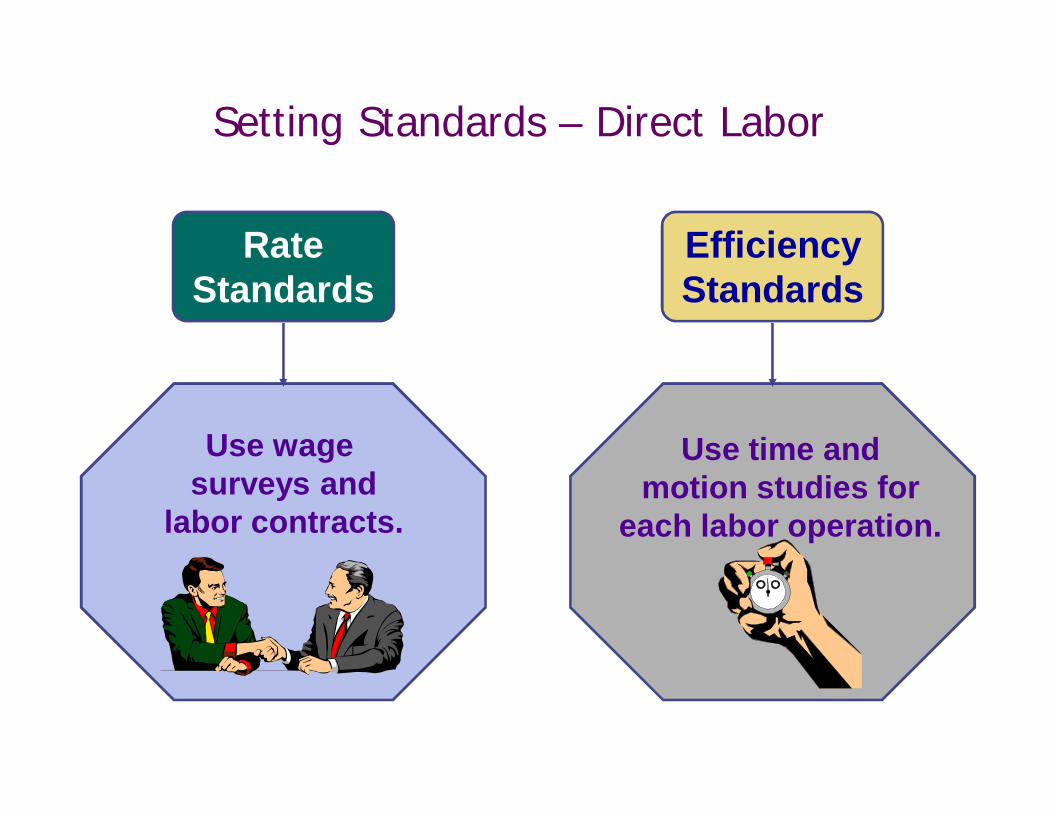

EfficiencyStandards

RateStandards

Use time and motion studies for

each labor operation.

Use wage surveys and

labor contracts.

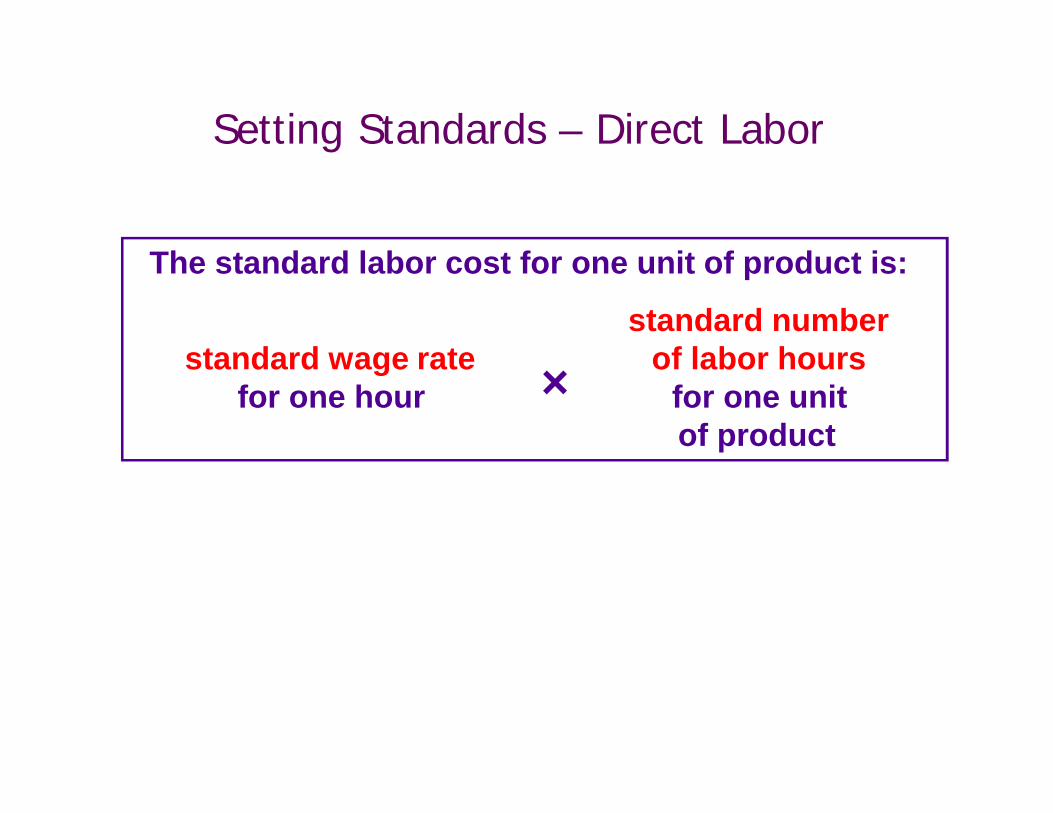

Setting Standards – Direct Labor

The standard labor cost for one unit of product is:

standard numberstandard wage rate of labor hours

for one hour for one unitof product

×

Setting Standards – Direct Labor

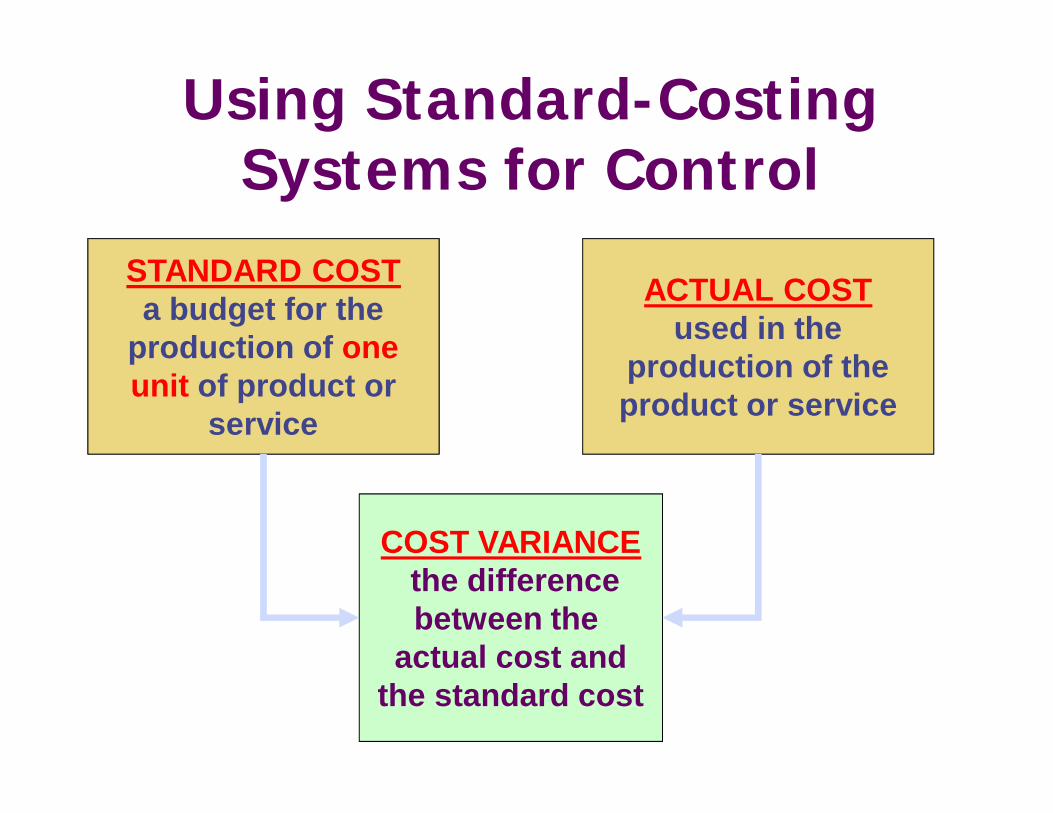

STANDARD COSTa budget for the

production of one unit of product or

service

ACTUAL COSTused in the

production of the product or service

COST VARIANCEthe differencebetween the

actual cost andthe standard cost

Using Standard-Costing Systems for Control

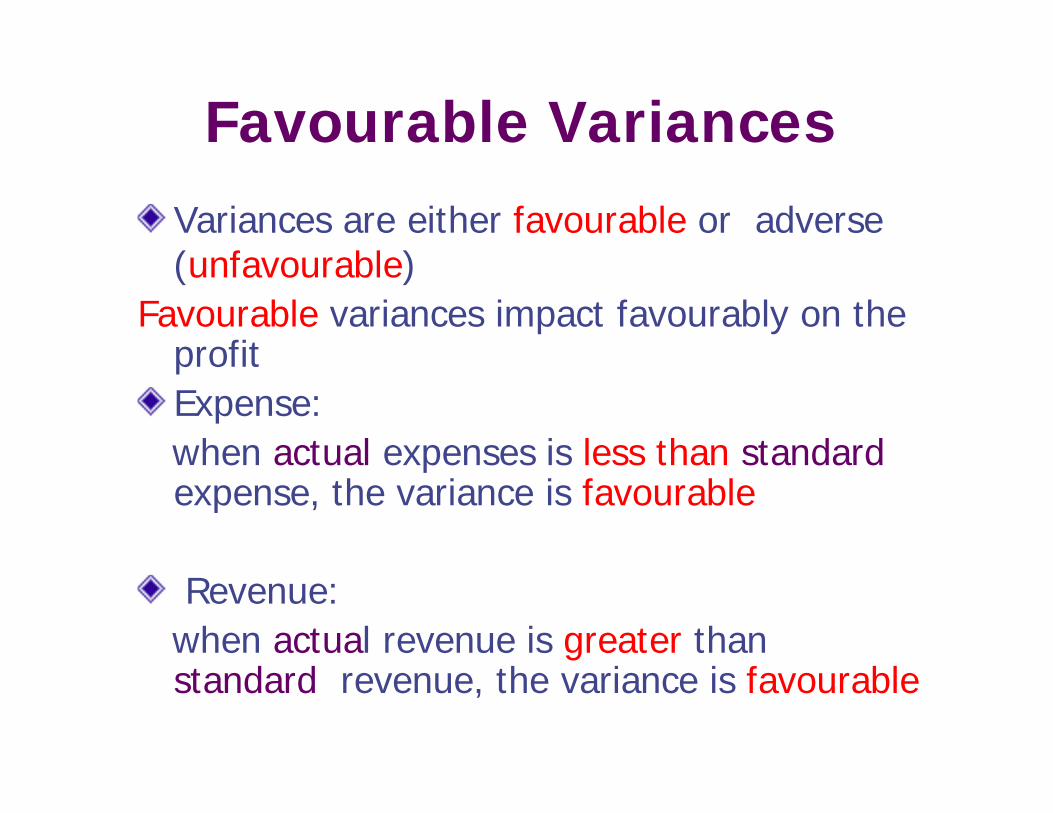

Favourable VariancesVariances are either favourable or adverse (unfavourable)

Favourable variances impact favourably on the profitExpense:when actual expenses is less than standardexpense, the variance is favourable

Revenue:when actual revenue is greater than standard revenue, the variance is favourable

Unfavourable VariancesUnfavourable or adverse variances impact

unfavourably on the profit

Expense:when actual expenses is greater than standardexpense, the variance is unfavourable

Revenue:when actual revenue is less than standardrevenue, the variance is unfavourable

Unfavourable Variances

Unfavourable variances measure a business's failure to meet its plans and large unfavourablevariances represent large failures.

It is worthwhile reporting a variance to a manager only if that manager can exercise some control over the cost (or revenue) being reported.

Broadly controllable costs should be those which the manager is responsible for budgeting.

Control through Management by ExceptionVariance analysis is a tool for alerting management to the fact that there are problems and narrowing down the sources.

It directs the scarce resource of management time to the areas where it is most needed.

The practice of using the variance analysis in this manner is called management by exception (MBE).

MBE refers to the process of delegating all routine functions by means of procedures and focusing management attention on only those items which fall outside those procedures.

Take the time to investigate only Take the time to investigate only significant cost variances

What is significant?

Depends on the Size of theOrganization

Organization

Depends on the Type of the Organization

Depends on Depends on the Production

Process

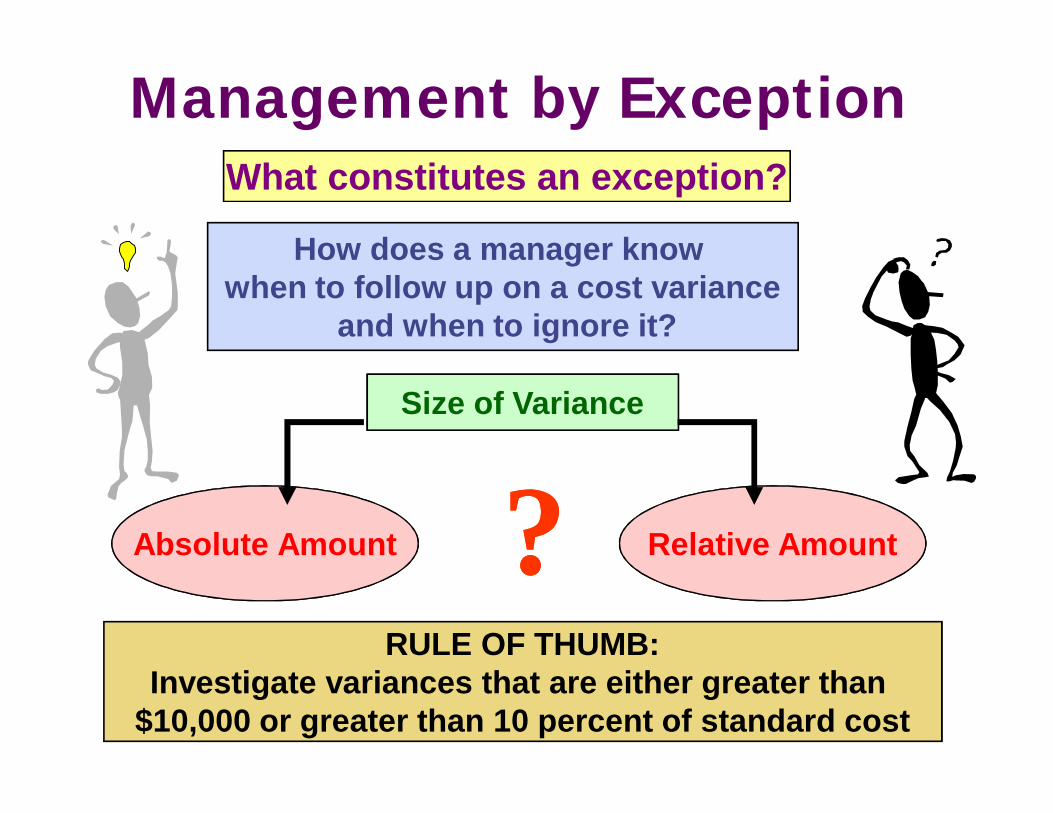

Management by Exception

??

What constitutes an exception?

How does a manager know when to follow up on a cost variance

and when to ignore it?

RULE OF THUMB:Investigate variances that are either greater than

$10,000 or greater than 10 percent of standard cost

Size of Variance

Absolute Amount Relative Amount

Management by Exception

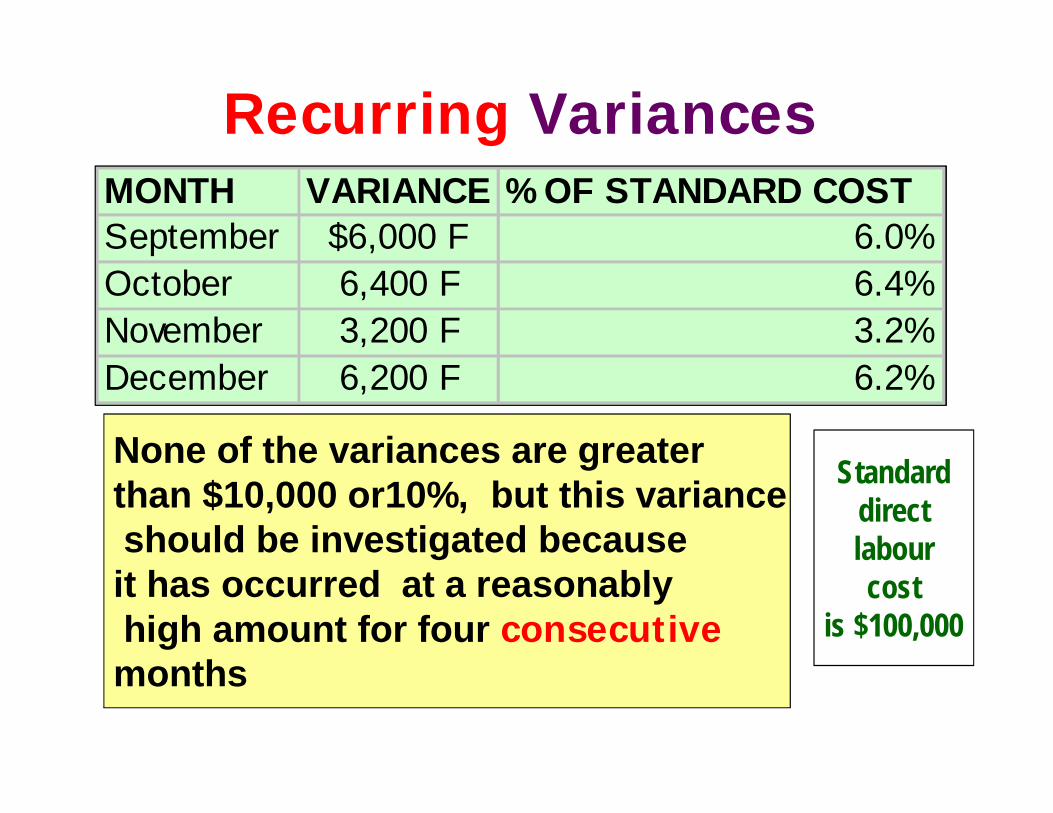

MONTH VARIANCE % OF STANDARD COSTSeptember $6,000 F 6.0%October 6,400 F 6.4%November 3,200 F 3.2%December 6,200 F 6.2%

MONTH VARIANCE % OF STANDARD COSTSeptember $6,000 F 6.0%October 6,400 F 6.4%November 3,200 F 3.2%December 6,200 F 6.2%

None of the variances are greaterthan $10,000 or10%, but this varianceshould be investigated becauseit has occurred at a reasonablyhigh amount for four consecutivemonths

Standarddirect labourcost

is $100,000

Recurring Variances

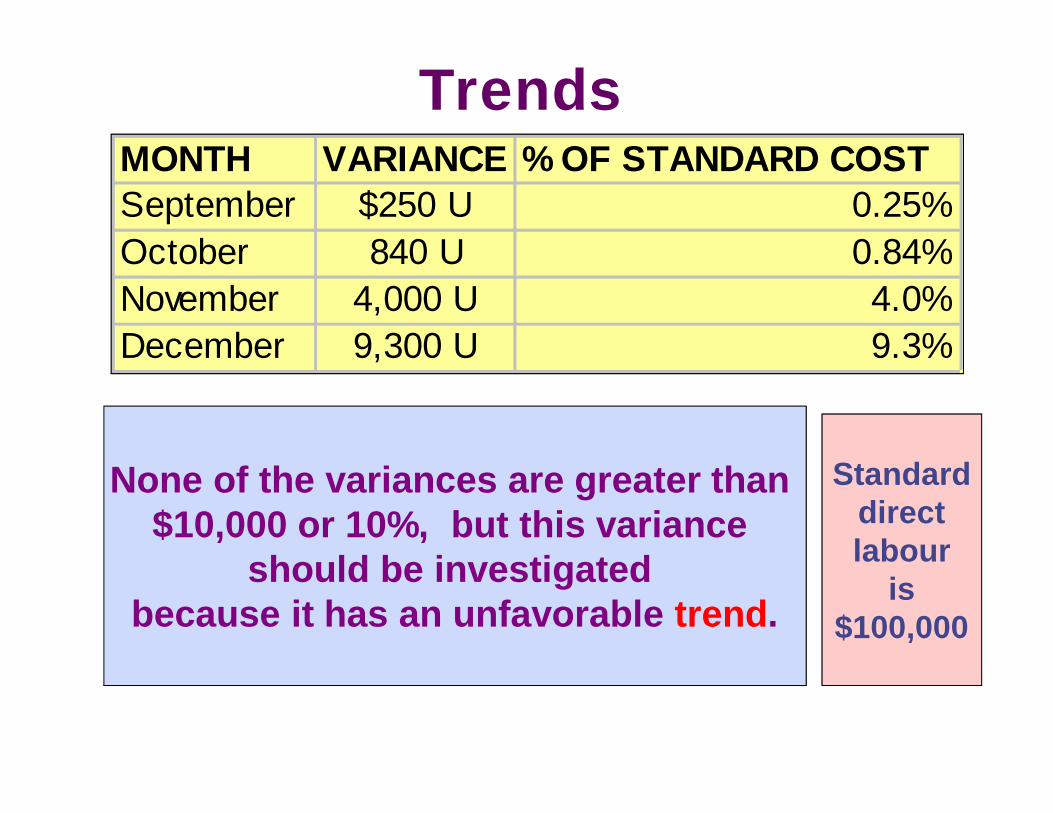

None of the variances are greater than $10,000 or 10%, but this variance

should be investigated because it has an unfavorable trend.

Standarddirect labour

is $100,000

MONTH VARIANCE % OF STANDARD COSTSeptember $250 U 0.25%October 840 U 0.84%November 4,000 U 4.0%December 9,300 U 9.3%

MONTH VARIANCE % OF STANDARD COSTSeptember $250 U 0.25%October 840 U 0.84%November 4,000 U 4.0%December 9,300 U 9.3%

Trends

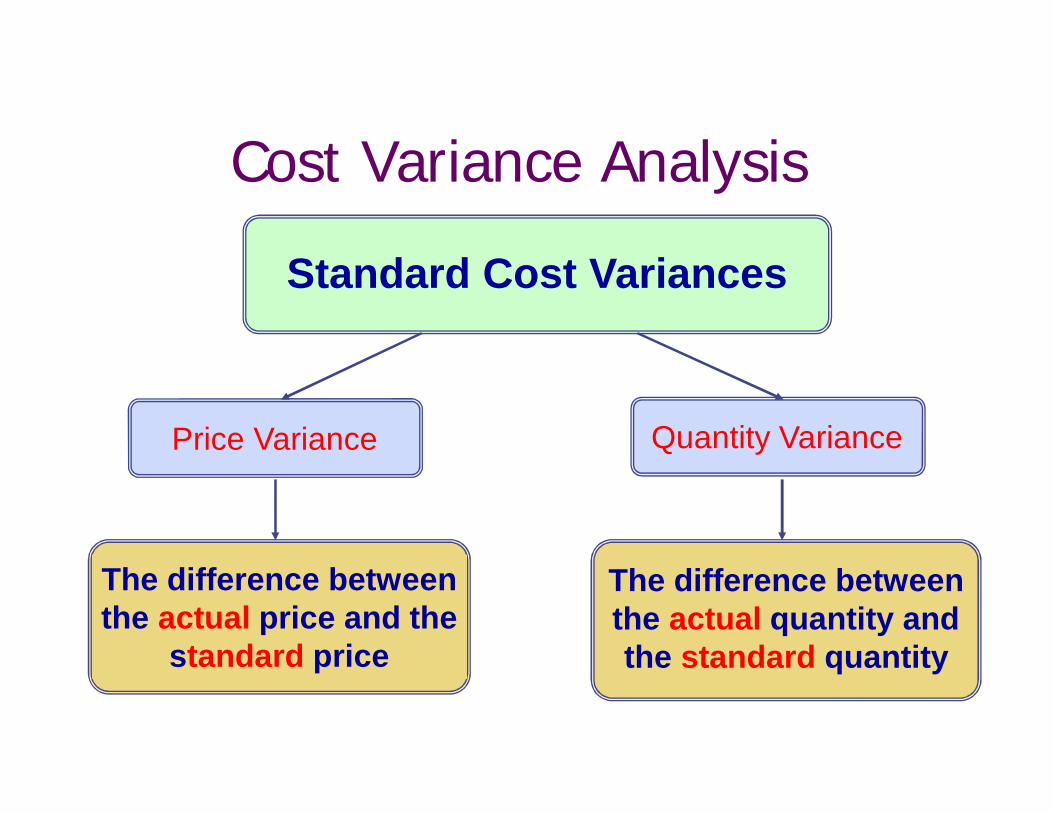

Quantity VariancePrice Variance

The difference betweenthe actual price and the

standard price

The difference betweenthe actual quantity andthe standard quantity

Standard Cost Variances

Cost Variance Analysis

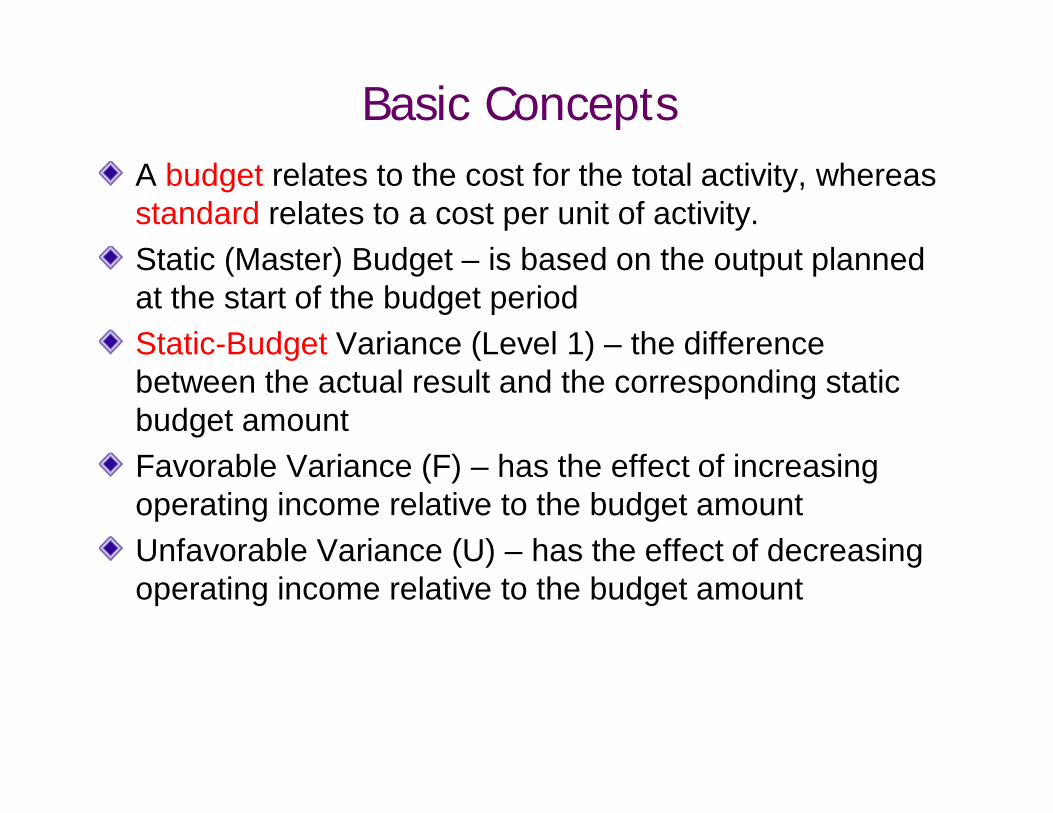

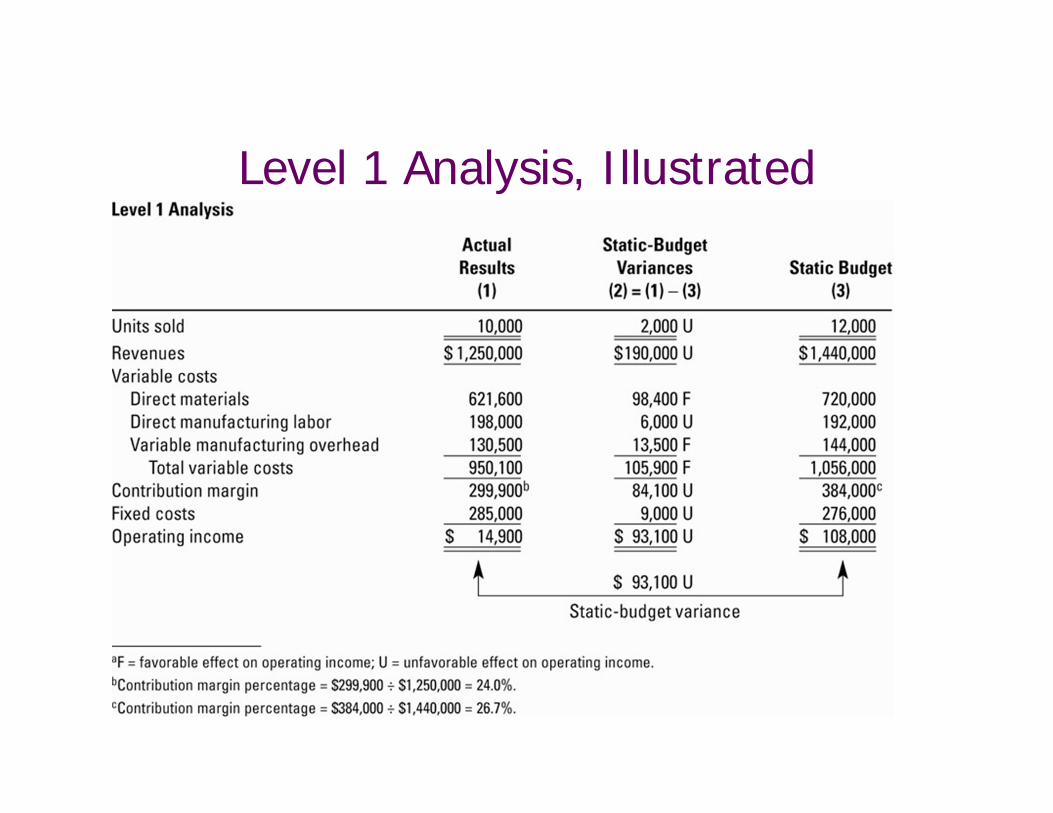

Basic ConceptsA budget relates to the cost for the total activity, whereas standard relates to a cost per unit of activity.Static (Master) Budget – is based on the output planned at the start of the budget periodStatic-Budget Variance (Level 1) – the difference between the actual result and the corresponding static budget amountFavorable Variance (F) – has the effect of increasing operating income relative to the budget amountUnfavorable Variance (U) – has the effect of decreasing operating income relative to the budget amount

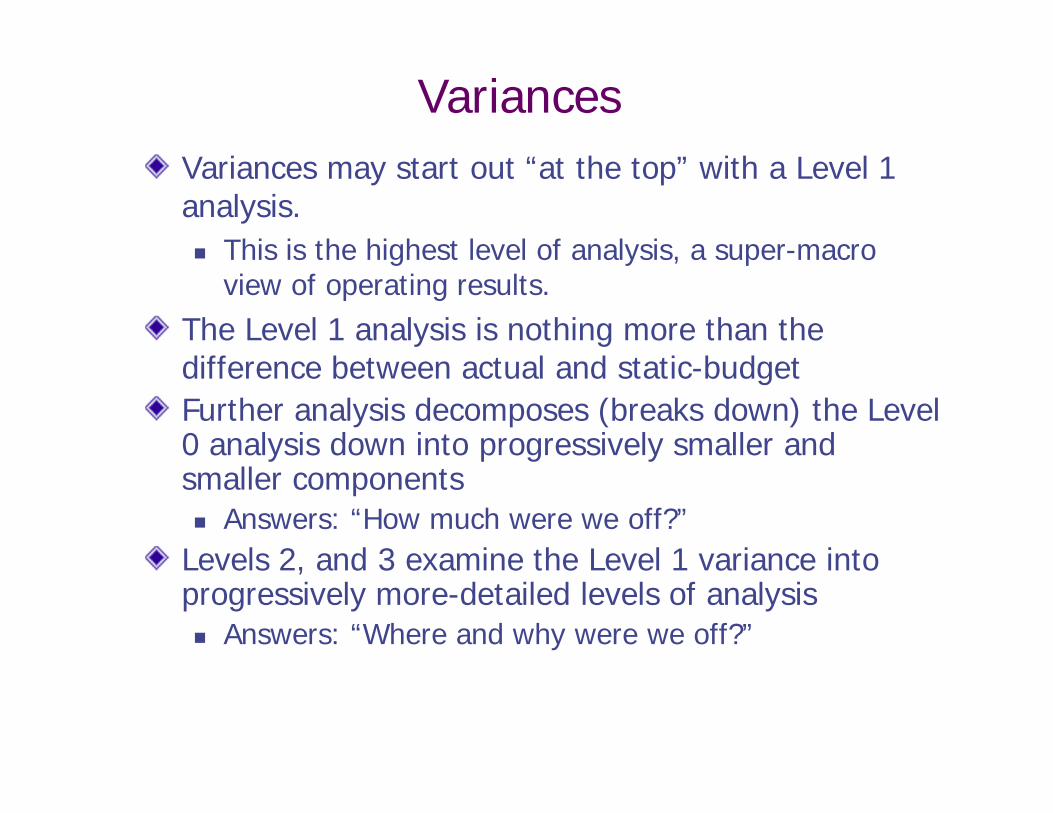

VariancesVariances may start out “at the top” with a Level 1 analysis. This is the highest level of analysis, a super-macro

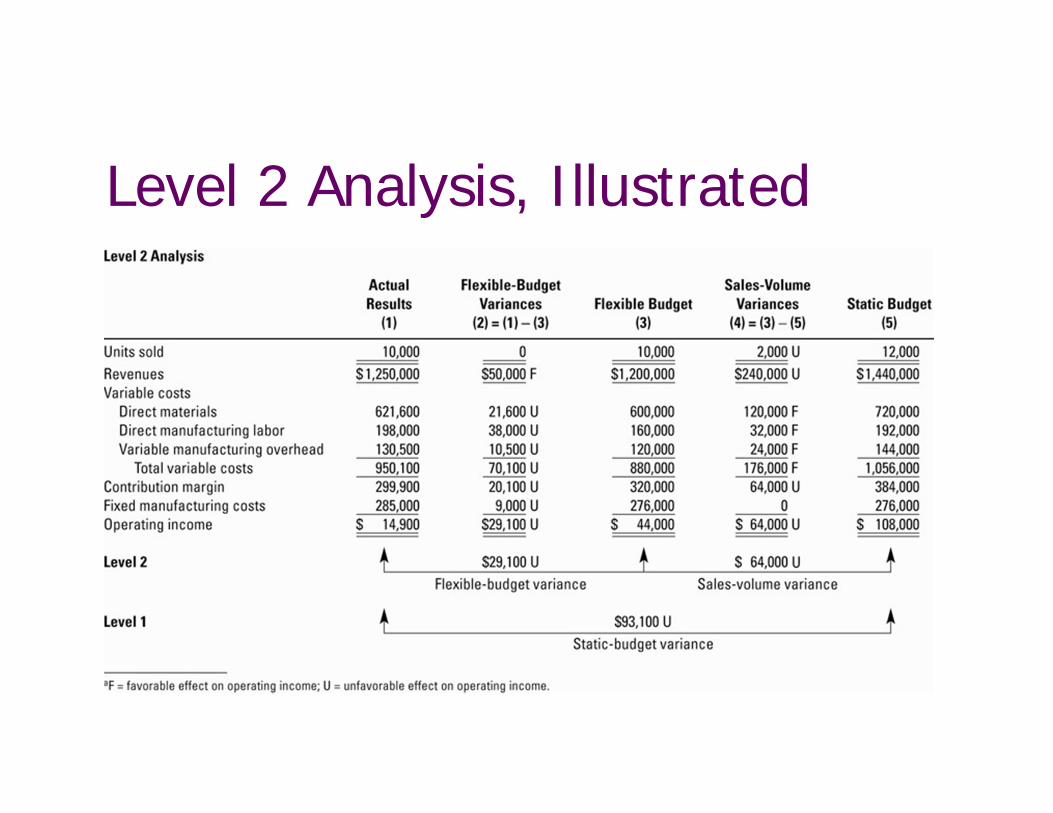

view of operating results. The Level 1 analysis is nothing more than the difference between actual and static-budgetFurther analysis decomposes (breaks down) the Level 0 analysis down into progressively smaller and smaller components Answers: “How much were we off?”

Levels 2, and 3 examine the Level 1 variance into progressively more-detailed levels of analysis Answers: “Where and why were we off?”

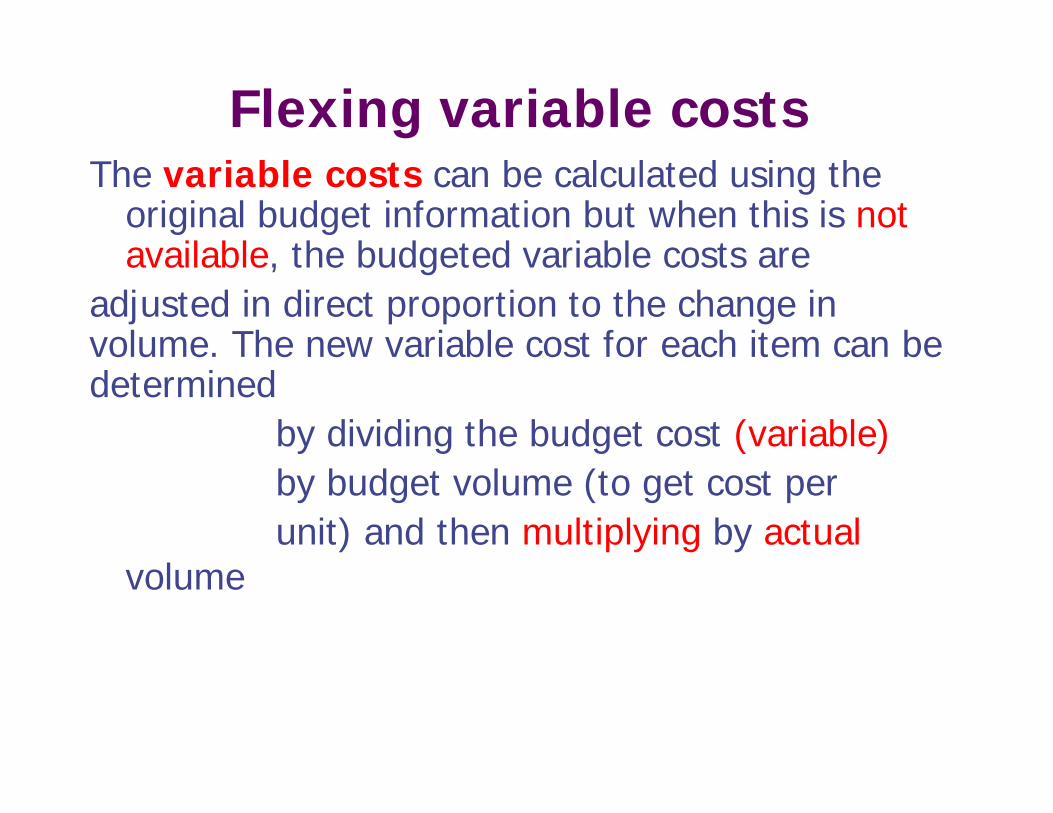

Flexing variable costsThe variable costs can be calculated using the

original budget information but when this is not available, the budgeted variable costs are

adjusted in direct proportion to the change in volume. The new variable cost for each item can be determined

by dividing the budget cost (variable)by budget volume (to get cost per unit) and then multiplying by actual

volume

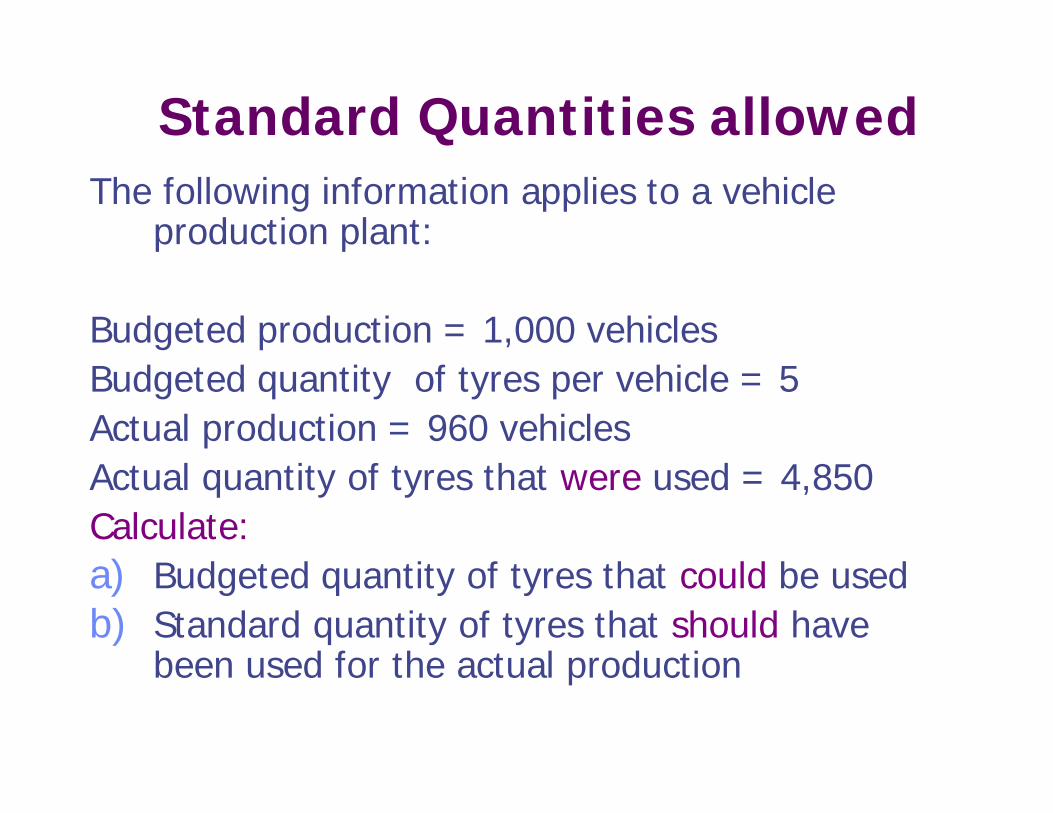

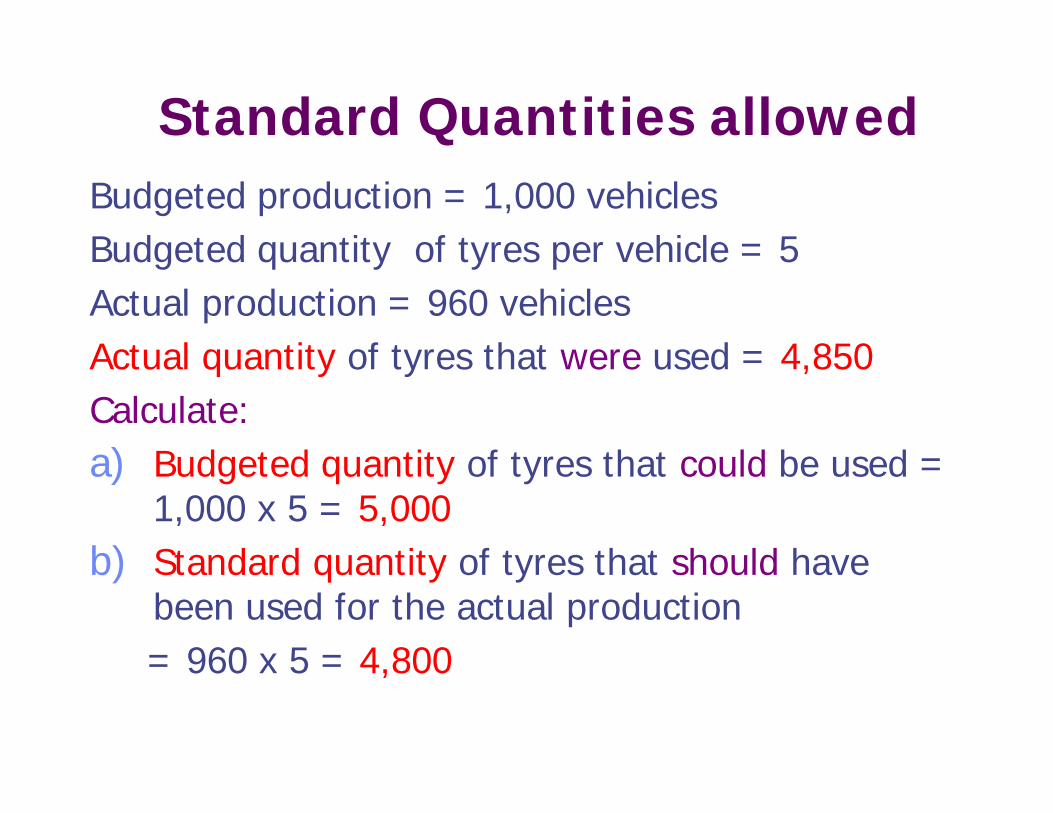

Standard Quantities allowedThe following information applies to a vehicle

production plant:

Budgeted production = 1,000 vehiclesBudgeted quantity of tyres per vehicle = 5Actual production = 960 vehiclesActual quantity of tyres that were used = 4,850Calculate:a) Budgeted quantity of tyres that could be usedb) Standard quantity of tyres that should have

been used for the actual production

Standard Quantities allowedBudgeted production = 1,000 vehiclesBudgeted quantity of tyres per vehicle = 5Actual production = 960 vehiclesActual quantity of tyres that were used = 4,850Calculate:a) Budgeted quantity of tyres that could be used =

1,000 x 5 = 5,000b) Standard quantity of tyres that should have

been used for the actual production= 960 x 5 = 4,800

Level 1 Analysis, Illustrated

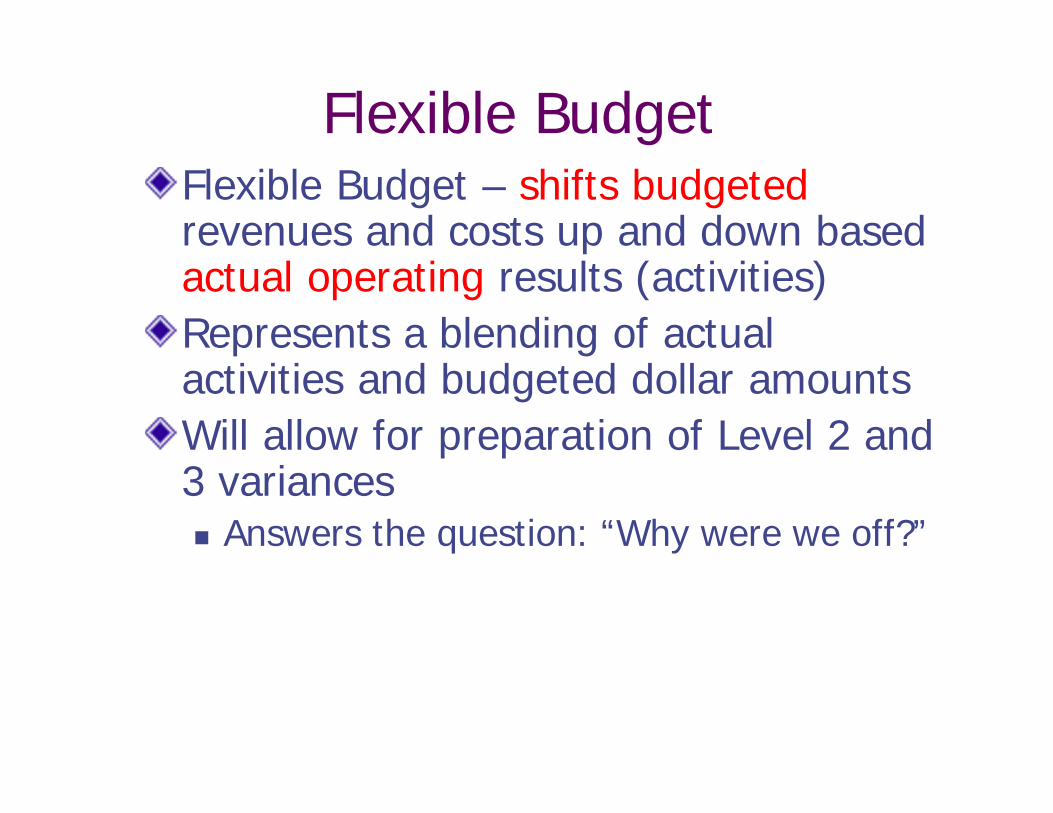

Flexible BudgetFlexible Budget – shifts budgeted revenues and costs up and down based actual operating results (activities)Represents a blending of actual activities and budgeted dollar amountsWill allow for preparation of Level 2 and 3 variances Answers the question: “Why were we off?”

Level 2 Analysis, Illustrated

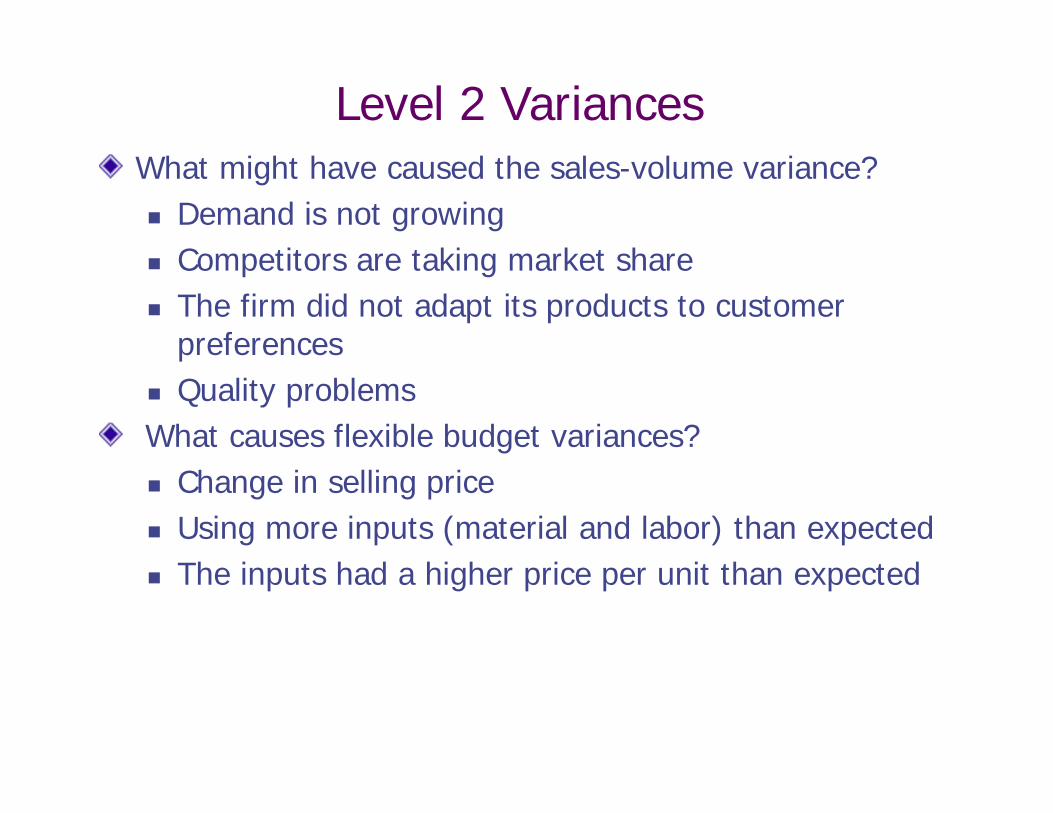

Level 2 VariancesWhat might have caused the sales-volume variance? Demand is not growing Competitors are taking market share The firm did not adapt its products to customer

preferences Quality problemsWhat causes flexible budget variances? Change in selling price Using more inputs (material and labor) than expected The inputs had a higher price per unit than expected

Level 3 VariancesDeals with the variances of cost items (e.g. labor, material and overhead).

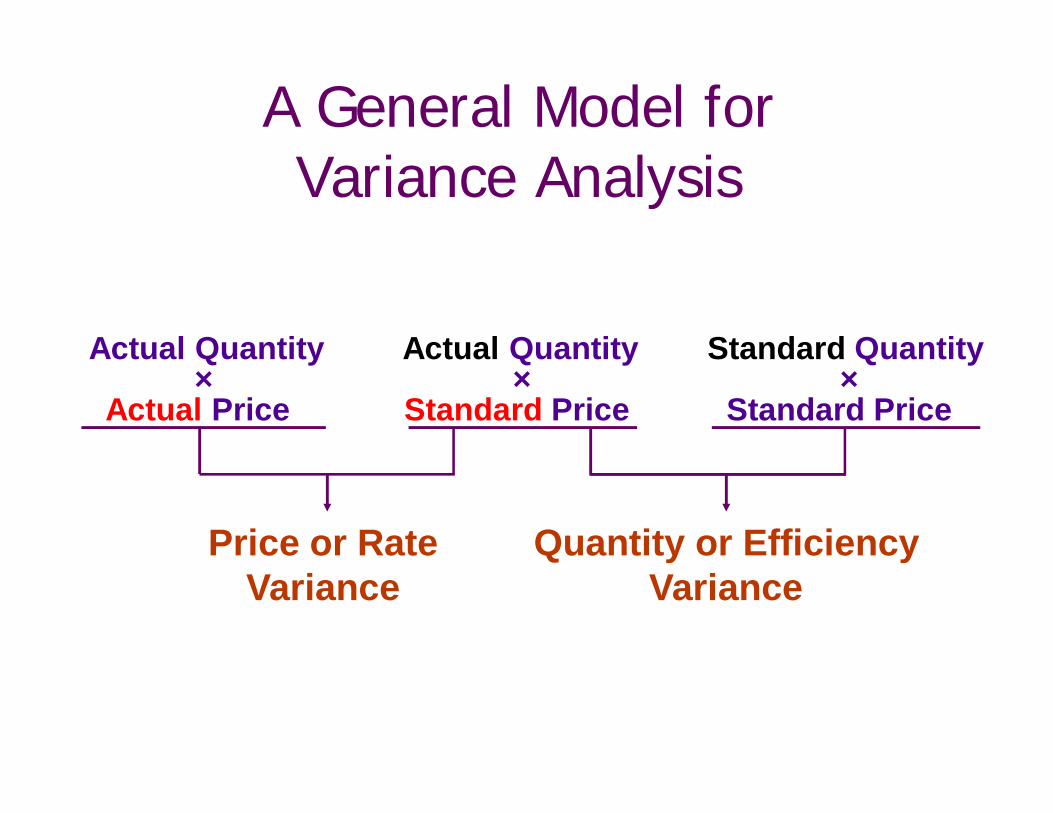

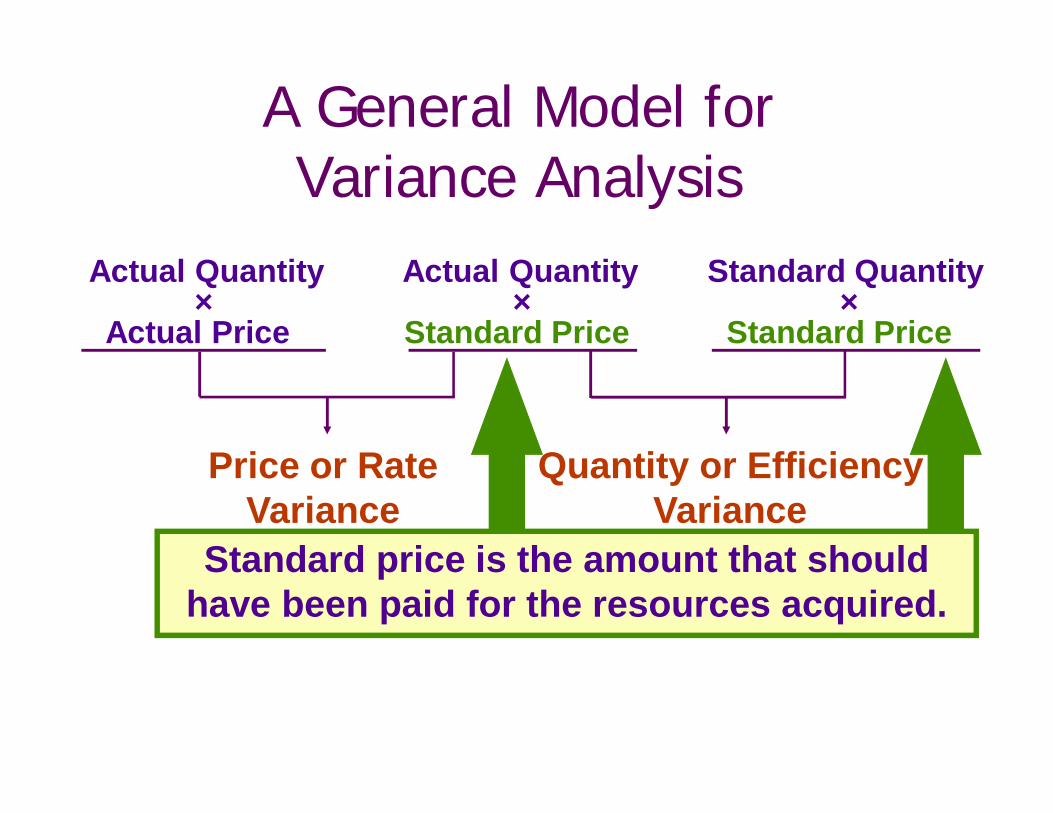

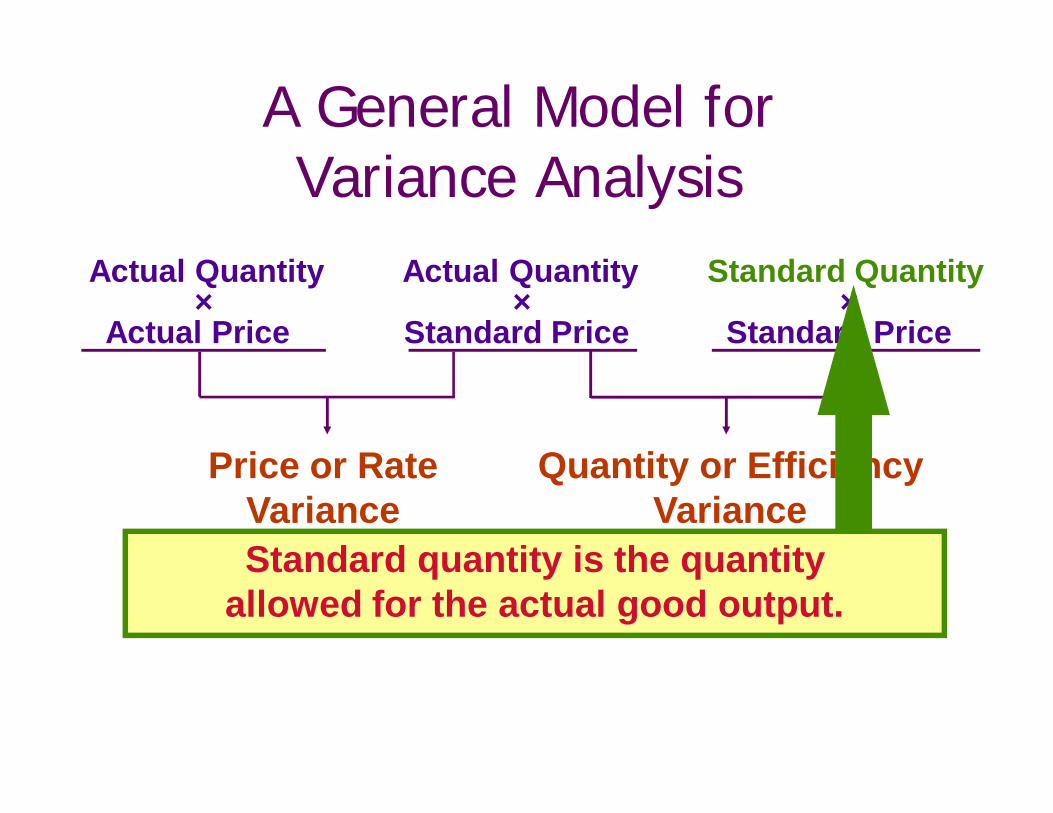

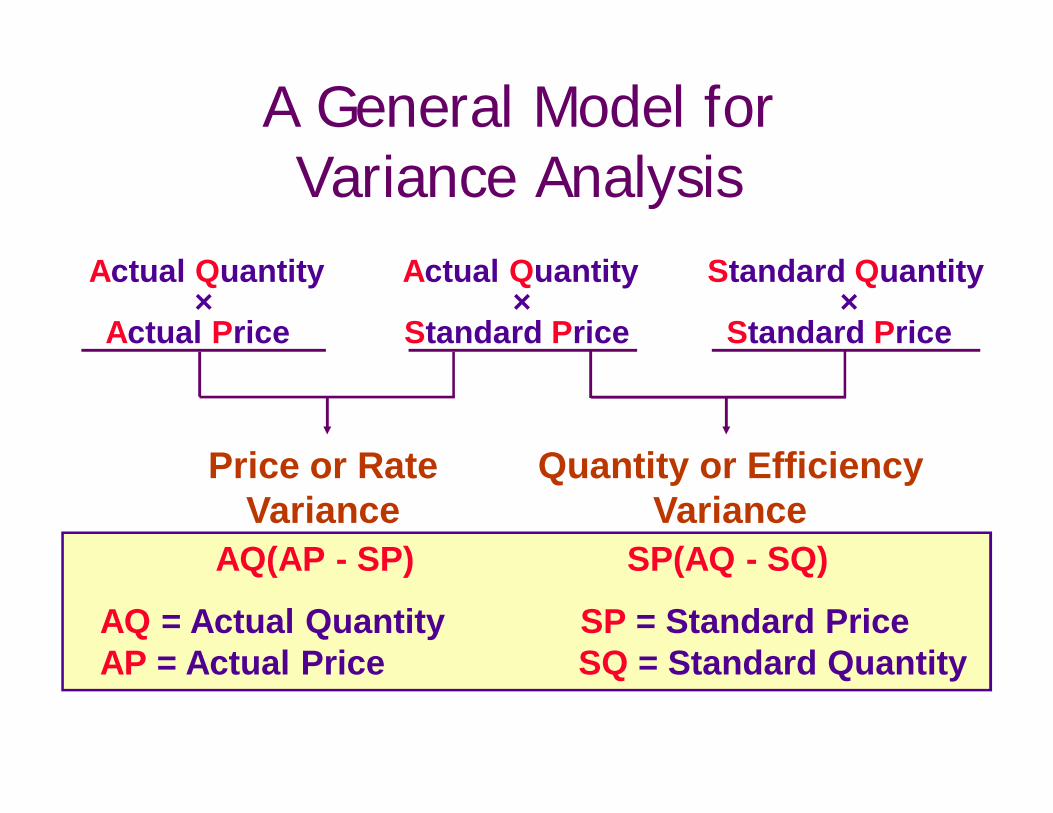

A General Model for Variance Analysis

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Price or RateVariance

Quantity or Efficiency Variance

A General Model forVariance Analysis

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Standard price is the amount that should have been paid for the resources acquired.

Price or RateVariance

Quantity or Efficiency Variance

Quantity or Efficiency Variance

Price or RateVariance

A General Model forVariance Analysis

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Standard quantity is the quantityallowed for the actual good output.

A General Model forVariance Analysis

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Materials price variance Materials quantity varianceLabor rate variance Labor efficiency varianceVariable overhead Variable overhead spending variance efficiency variance

AQ(AP - SP) SP(AQ - SQ)

AQ = Actual Quantity SP = Standard PriceAP = Actual Price SQ = Standard Quantity

Price or RateVariance

Quantity or Efficiency Variance

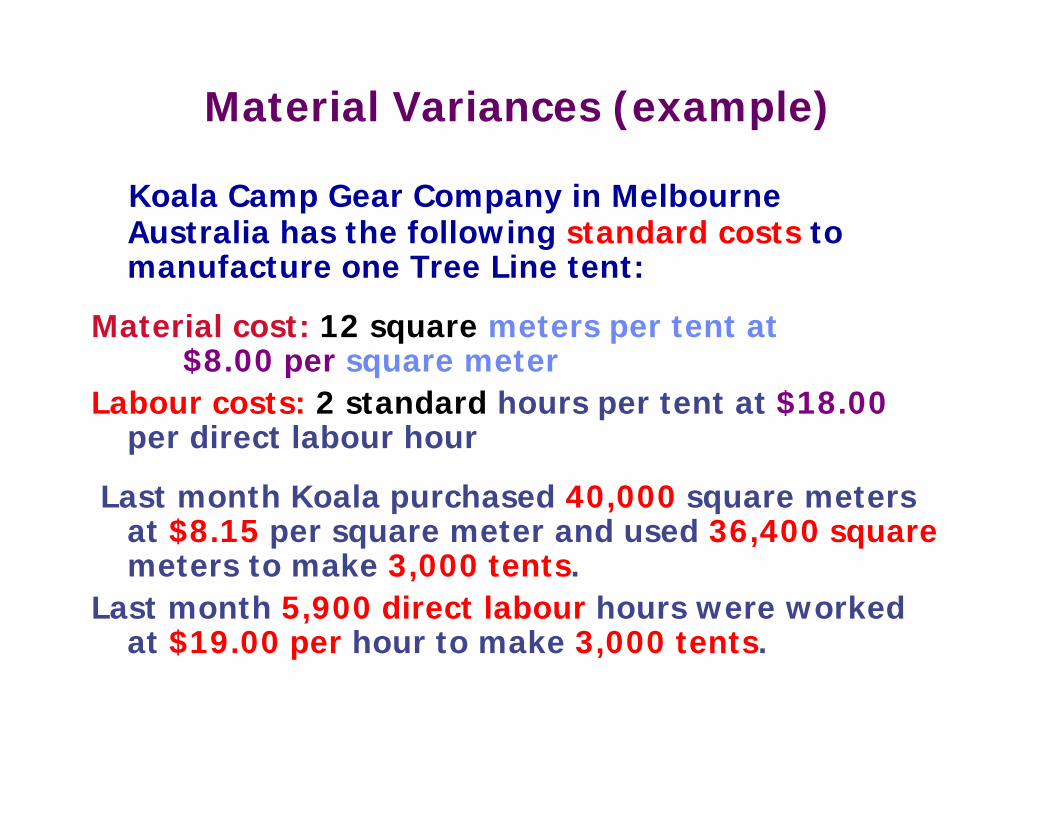

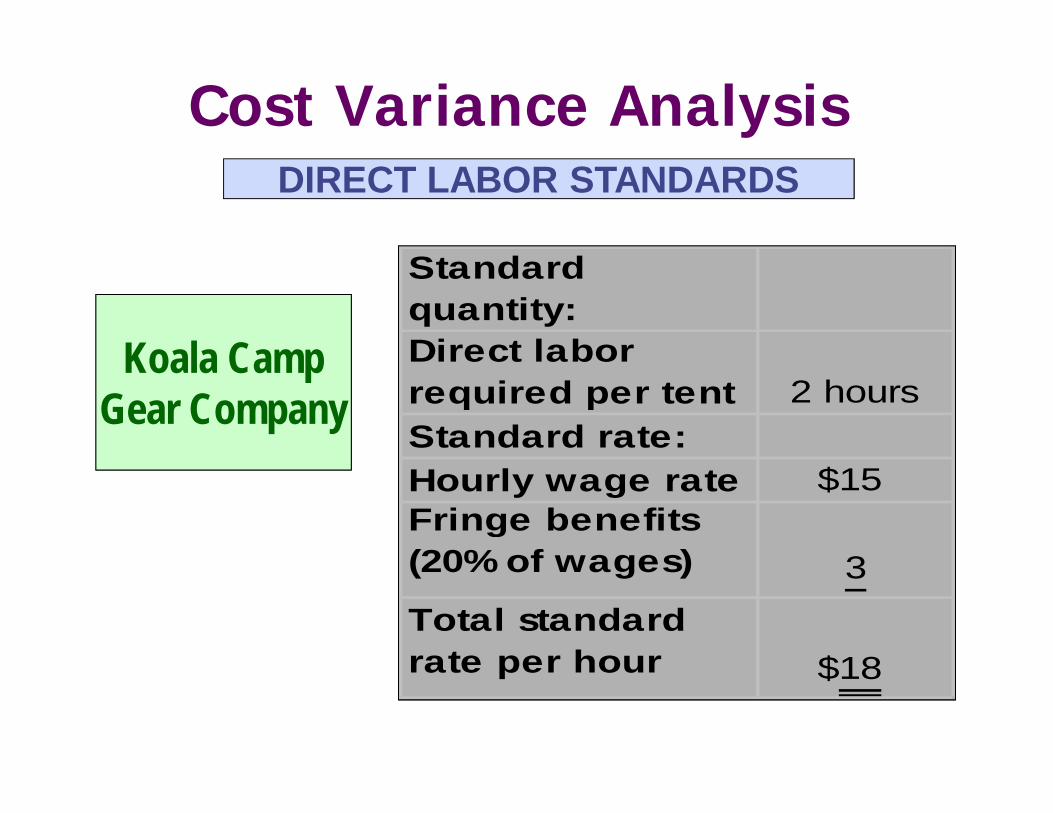

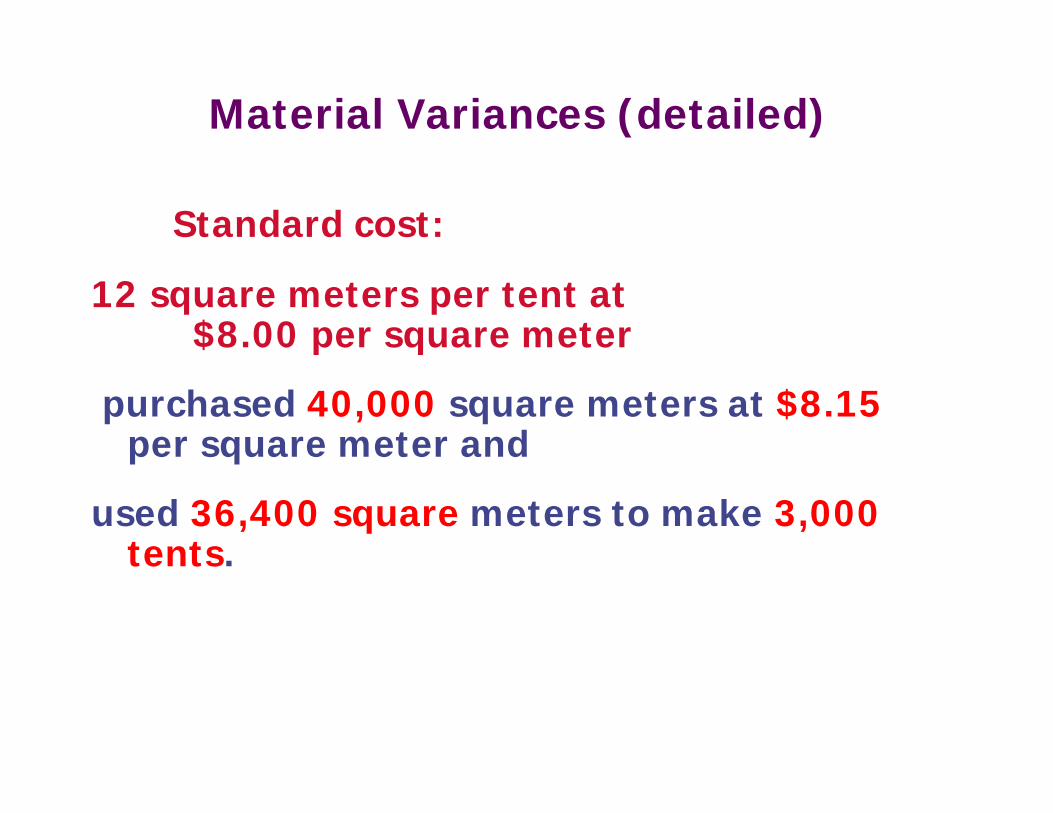

Koala Camp Gear Company in MelbourneAustralia has the following standard costs to manufacture one Tree Line tent:

Material cost: 12 square meters per tent at$8.00 per square meter

Labour costs: 2 standard hours per tent at $18.00per direct labour hour

Last month Koala purchased 40,000 square meters at $8.15 per square meter and used 36,400 squaremeters to make 3,000 tents.

Last month 5,900 direct labour hours were worked at $19.00 per hour to make 3,000 tents.

Material Variances (example)

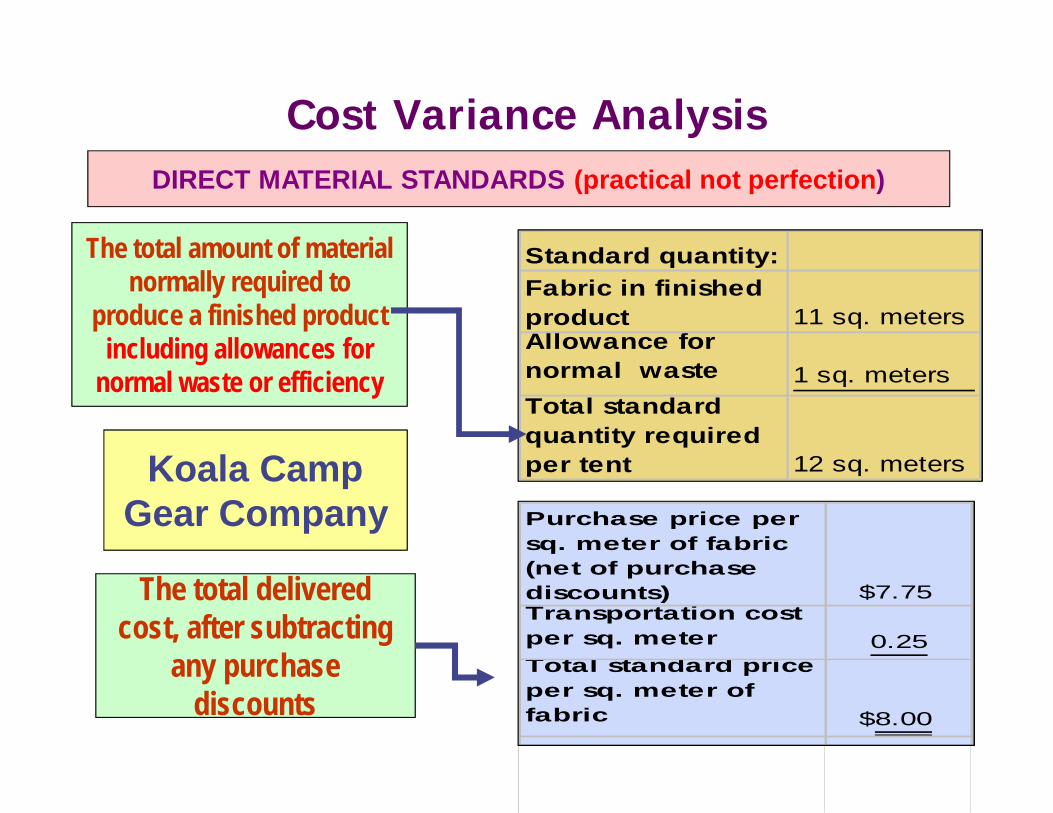

Standard quantity:Fabric in finished product 11 sq. metersAllowance for normal waste 1 sq. metersTotal standard quantity required per tent 12 sq. meters

Standard quantity:Fabric in finished product 11 sq. metersAllowance for normal waste 1 sq. metersTotal standard quantity required per tent 12 sq. meters

Purchase price per sq. meter of fabric (net of purchase discounts) $7.75Transportation cost per sq. meter 0.25Total standard price per sq. meter of fabric $8.00

Purchase price per sq. meter of fabric (net of purchase discounts) $7.75Transportation cost per sq. meter 0.25Total standard price per sq. meter of fabric $8.00

Koala CampGear Company

DIRECT MATERIAL STANDARDS (practical not perfection)

The total amount of material normally required to

produce a finished product including allowances for

normal waste or efficiency

The total delivered

discounts

The total delivered cost, after subtracting

any purchase discounts

Cost Variance Analysis

Koala CampGear Company

DIRECT LABOR STANDARDSDIRECT LABOR STANDARDS

Standard quantity:Direct labor required per tent 2 hoursStandard rate:Hourly wage rate $15Fringe benefits (20% of wages) 3Total standard rate per hour $18

Standard quantity:Direct labor required per tent 2 hoursStandard rate:Hourly wage rate $15Fringe benefits (20% of wages) 3Total standard rate per hour $18

Cost Variance Analysis

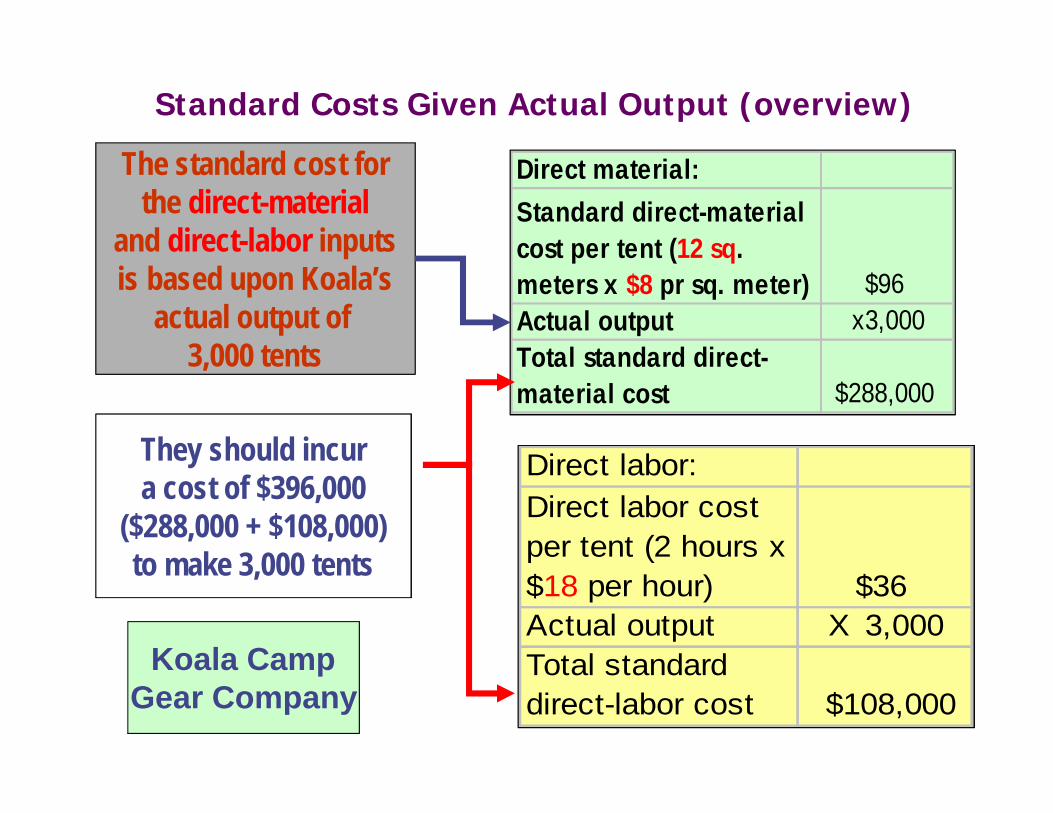

Direct material: Standard direct-material cost per tent (12 sq. meters x $8 pr sq. meter) $96Actual output x3,000Total standard direct-material cost $288,000

Direct material: Standard direct-material cost per tent (12 sq. meters x $8 pr sq. meter) $96Actual output x3,000Total standard direct-material cost $288,000

Direct labor:Direct labor cost per tent (2 hours x $18 per hour) $36Actual output X 3,000Total standard direct-labor cost $108,000

Direct labor:Direct labor cost per tent (2 hours x $18 per hour) $36Actual output X 3,000Total standard direct-labor cost $108,000

Koala CampGear Company

The standard cost forthe direct-material

and direct-labor inputsis based upon Koala’s

actual output of 3,000 tents

They should incura cost of $396,000

($288,000 + $108,000)to make 3,000 tents

Standard Costs Given Actual Output (overview)

Standard cost:

12 square meters per tent at$8.00 per square meter

purchased 40,000 square meters at $8.15per square meter and

used 36,400 square meters to make 3,000 tents.

Material Variances (detailed)

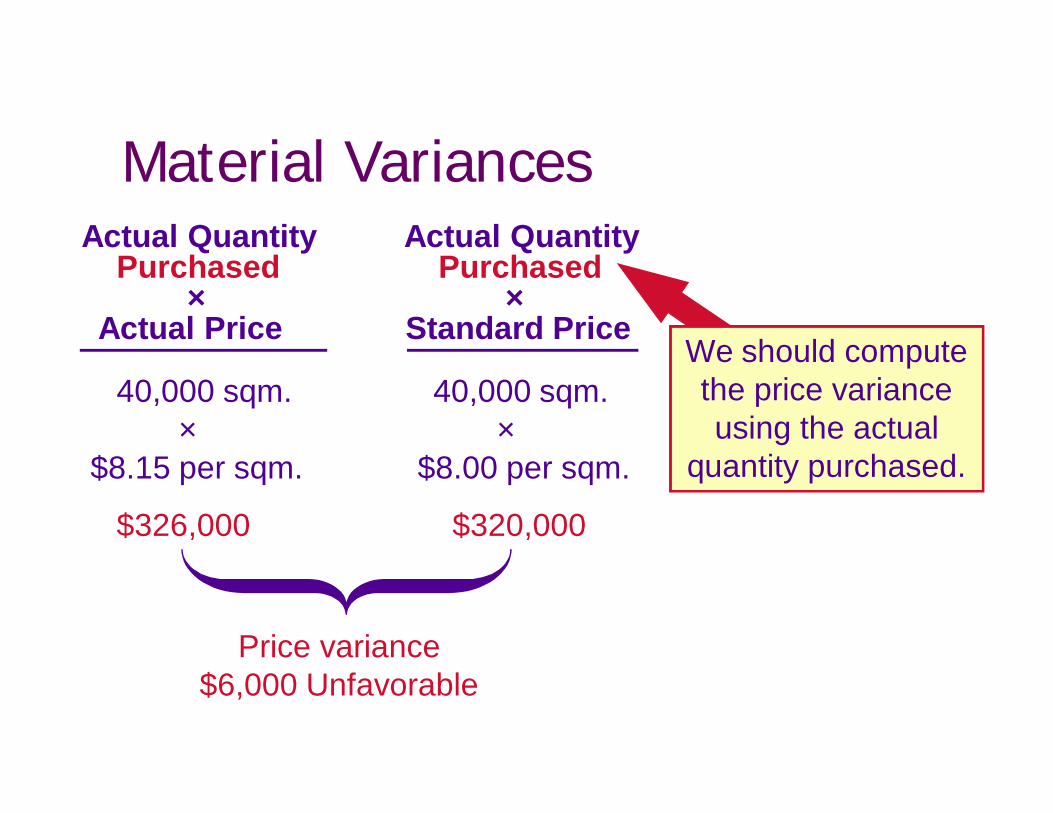

We should compute the price variance using the actual

quantity purchased.

Price variance$6,000 Unfavorable

40,000 sqm. 40,000 sqm. × ×

$8.15 per sqm. $8.00 per sqm.

$326,000 $320,000

Actual Quantity Actual QuantityPurchased Purchased

× ×Actual Price Standard Price

Material Variances

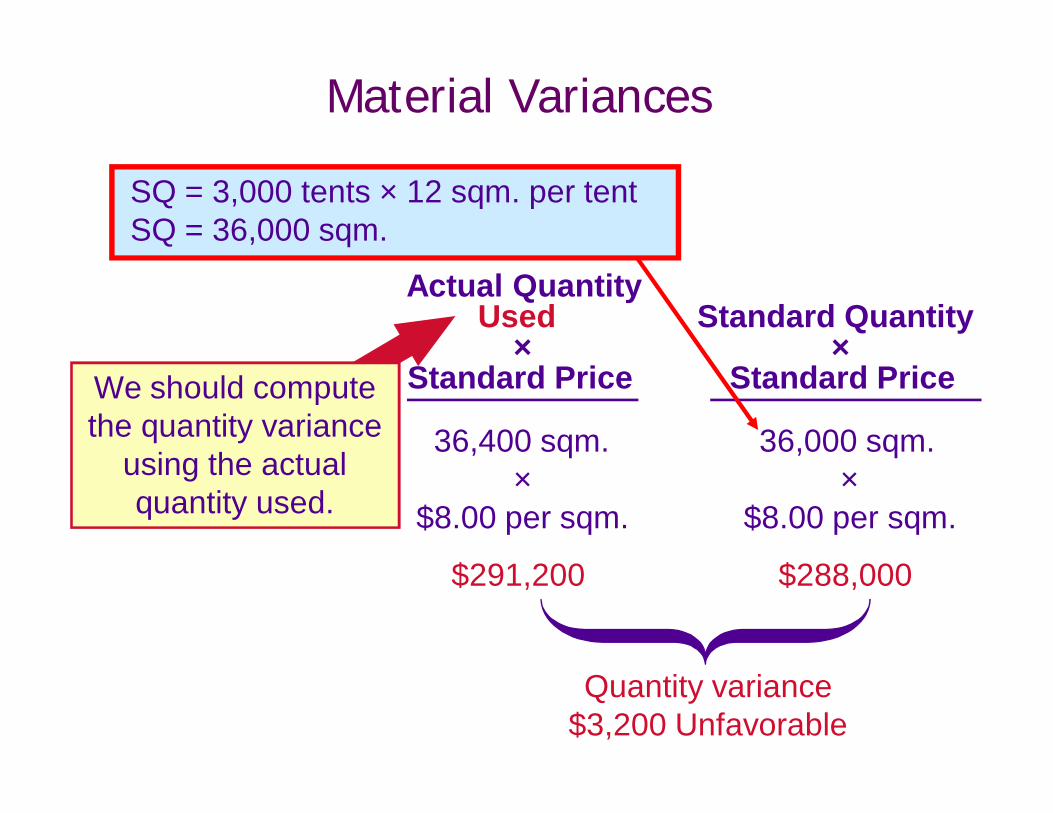

We should compute the quantity variance

using the actual quantity used.

Quantity variance$3,200 Unfavorable

36,400 sqm. 36,000 sqm.× ×

$8.00 per sqm. $8.00 per sqm.

$291,200 $288,000

Actual QuantityUsed Standard Quantity

× ×Standard Price Standard Price

SQ = 3,000 tents × 12 sqm. per tentSQ = 36,000 sqm.

Material Variances

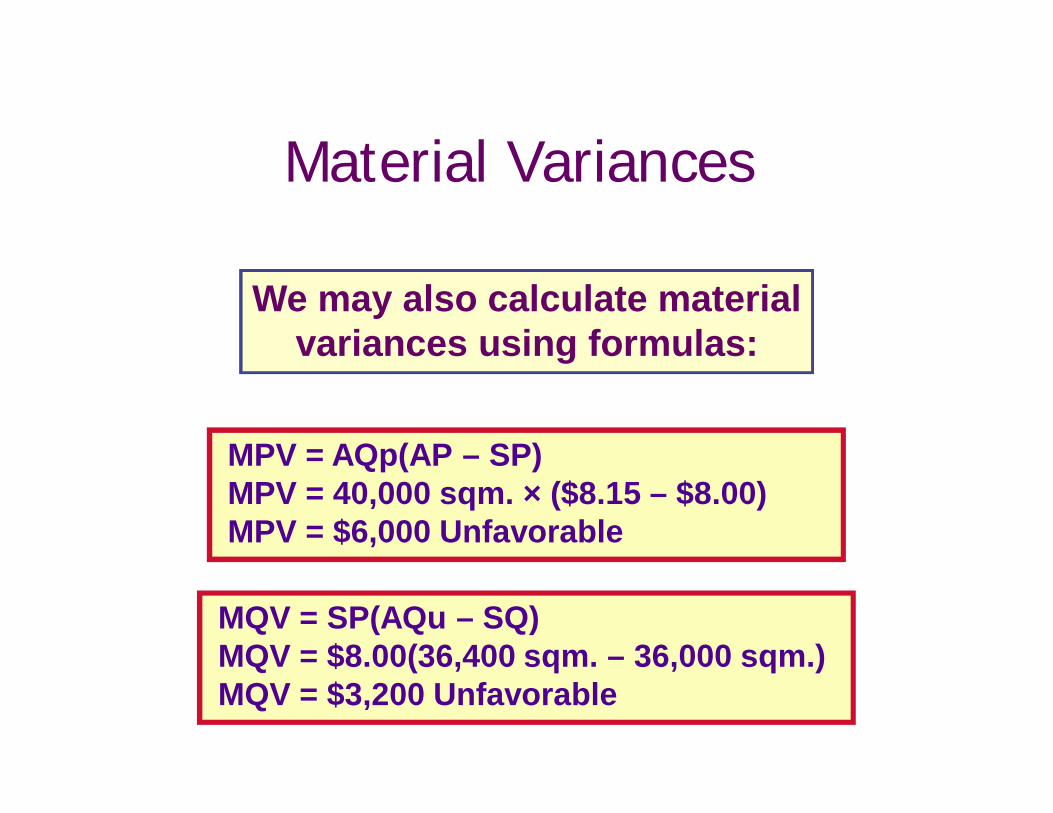

MPV = AQp(AP – SP)MPV = 40,000 sqm. × ($8.15 – $8.00)MPV = $6,000 Unfavorable

MQV = SP(AQu – SQ)MQV = $8.00(36,400 sqm. – 36,000 sqm.)MQV = $3,200 Unfavorable

We may also calculate materialvariances using formulas:

Material Variances

40,000 sq.meters

purchased

$8.15 persq. meter

40,000 sq.meters

purchased

$8.00 persq. meter

36,000sq. meters

allowed

$8.00 per sq. meter

$326,000 $320,000 $288,000

$6,000U

36,400 sq.meters

used

$8.00per sq.meter

$291,200

Direct-material price variance

$3,200U

Direct-materialquantity variance

xx x

Analysis Of Material VariancesActual

quantityActualprice

Actualquantity

Standardprice

Standardquantity

Standardpricexx x

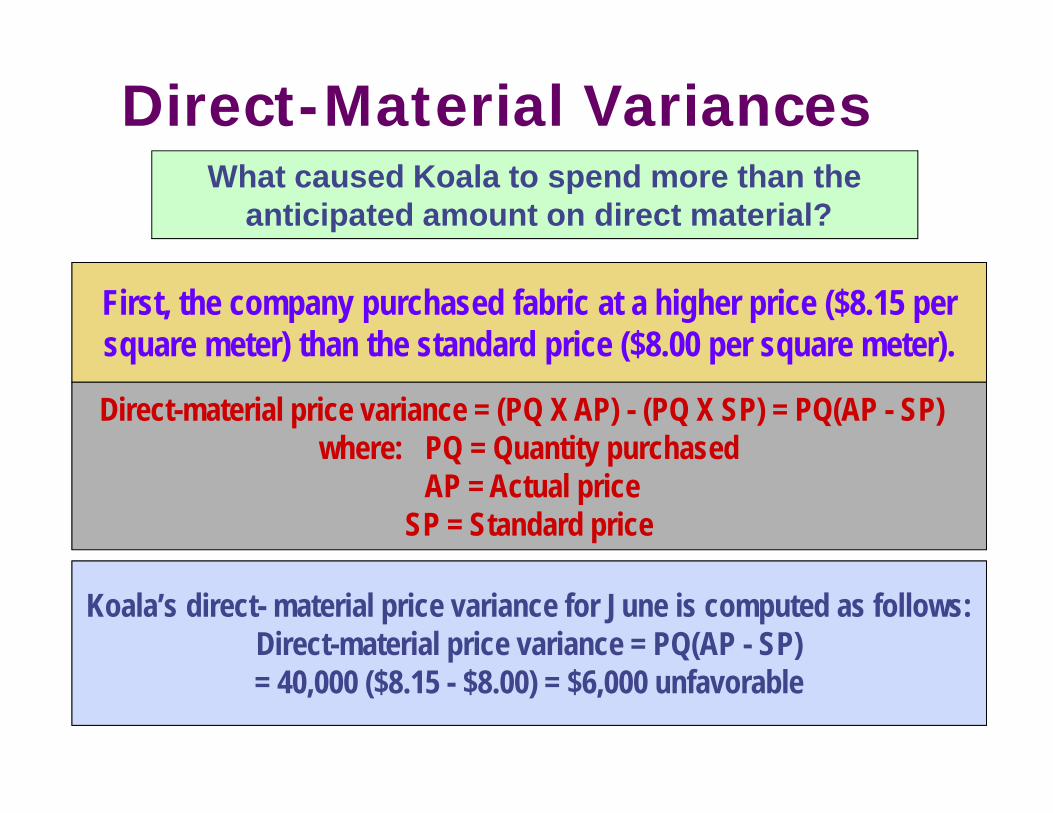

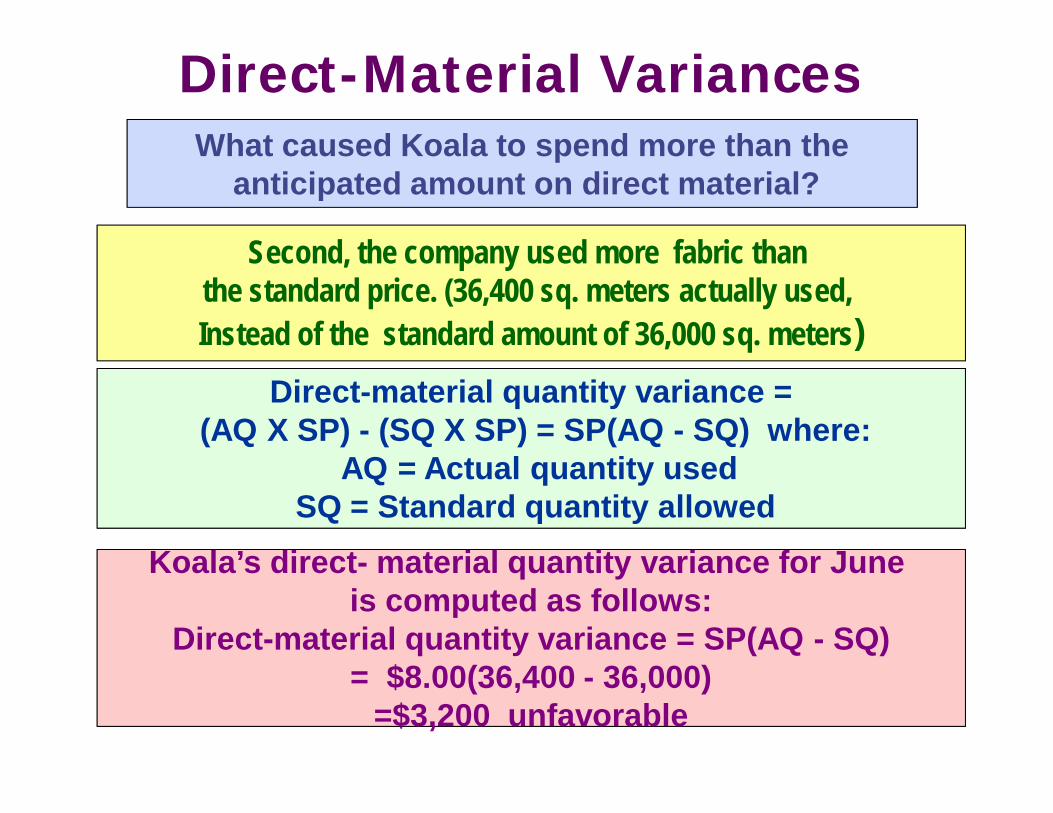

What caused Koala to spend more than theanticipated amount on direct material?

First, the company purchased fabric at a higher price ($8.15 persquare meter) than the standard price ($8.00 per square meter).

Direct-material price variance = (PQ X AP) - (PQ X SP) = PQ(AP - SP) where: PQ = Quantity purchased

AP = Actual priceSP = Standard price

Koala’s direct- material price variance for June is computed as follows:Direct-material price variance = PQ(AP - SP)= 40,000 ($8.15 - $8.00) = $6,000 unfavorable

Direct-Material Variances

Second, the company used more fabric than the standard price. (36,400 sq. meters actually used, Instead of the standard amount of 36,000 sq. meters)

Direct-material quantity variance =(AQ X SP) - (SQ X SP) = SP(AQ - SQ) where:

AQ = Actual quantity used SQ = Standard quantity allowed

Koala’s direct- material quantity variance for June

=$3,200 unfavorable

Koala’s direct- material quantity variance for June is computed as follows:

Direct-material quantity variance = SP(AQ - SQ)= $8.00(36,400 - 36,000)

=$3,200 unfavorable

What caused Koala to spend more than theanticipated amount on direct material?

Direct-Material Variances

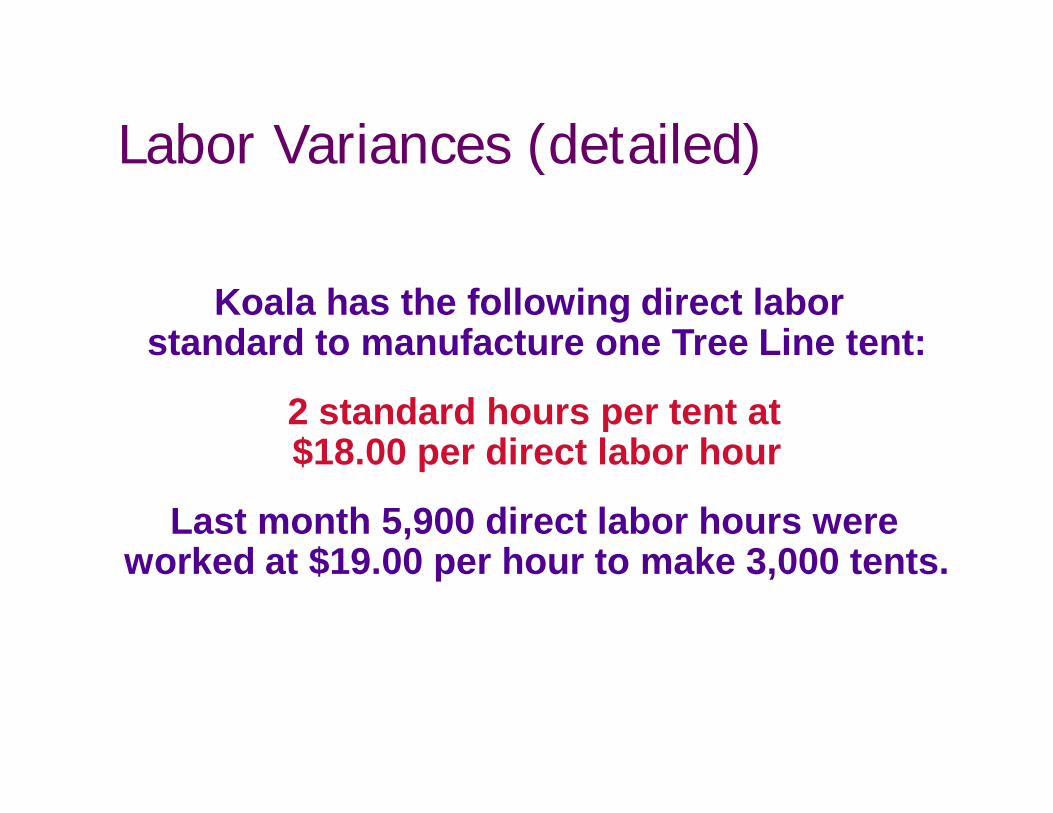

Koala has the following direct laborstandard to manufacture one Tree Line tent:

2 standard hours per tent at$18.00 per direct labor hour

Last month 5,900 direct labor hours were worked at $19.00 per hour to make 3,000 tents.

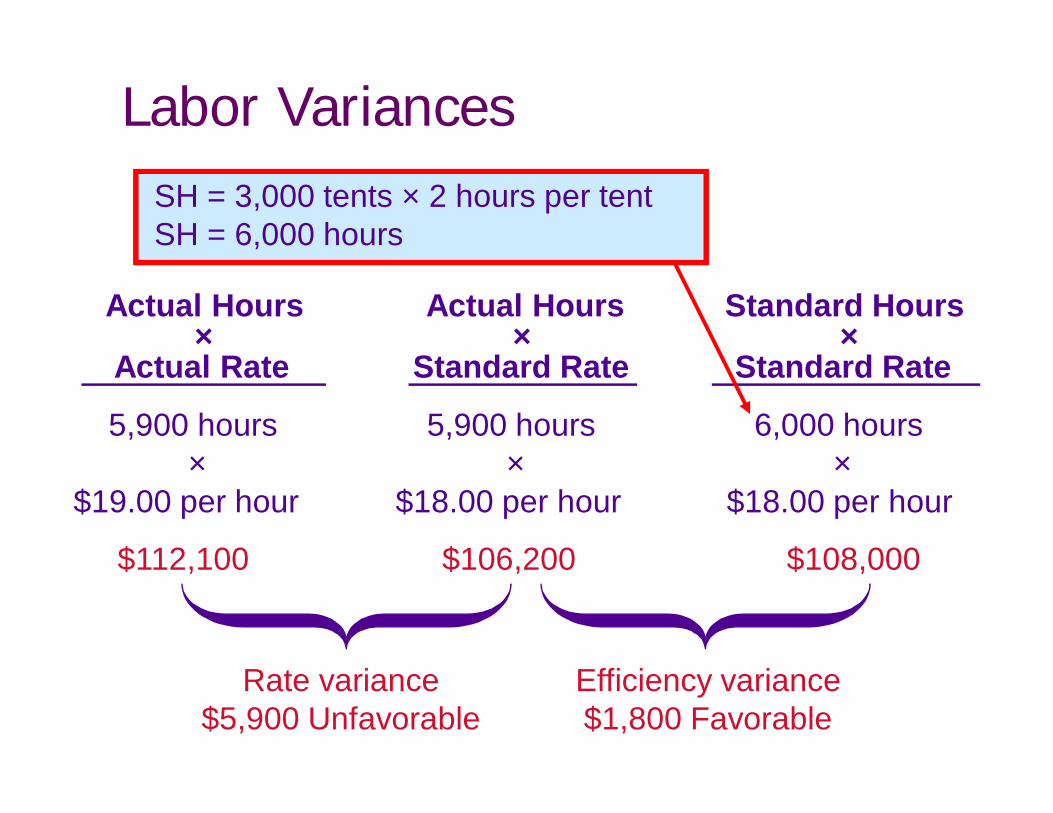

Labor Variances (detailed)

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

Rate variance$5,900 Unfavorable

Efficiency variance$1,800 Favorable

5,900 hours 5,900 hours 6,000 hours× × ×

$19.00 per hour $18.00 per hour $18.00 per hour

$112,100 $106,200 $108,000

SH = 3,000 tents × 2 hours per tentSH = 6,000 hours

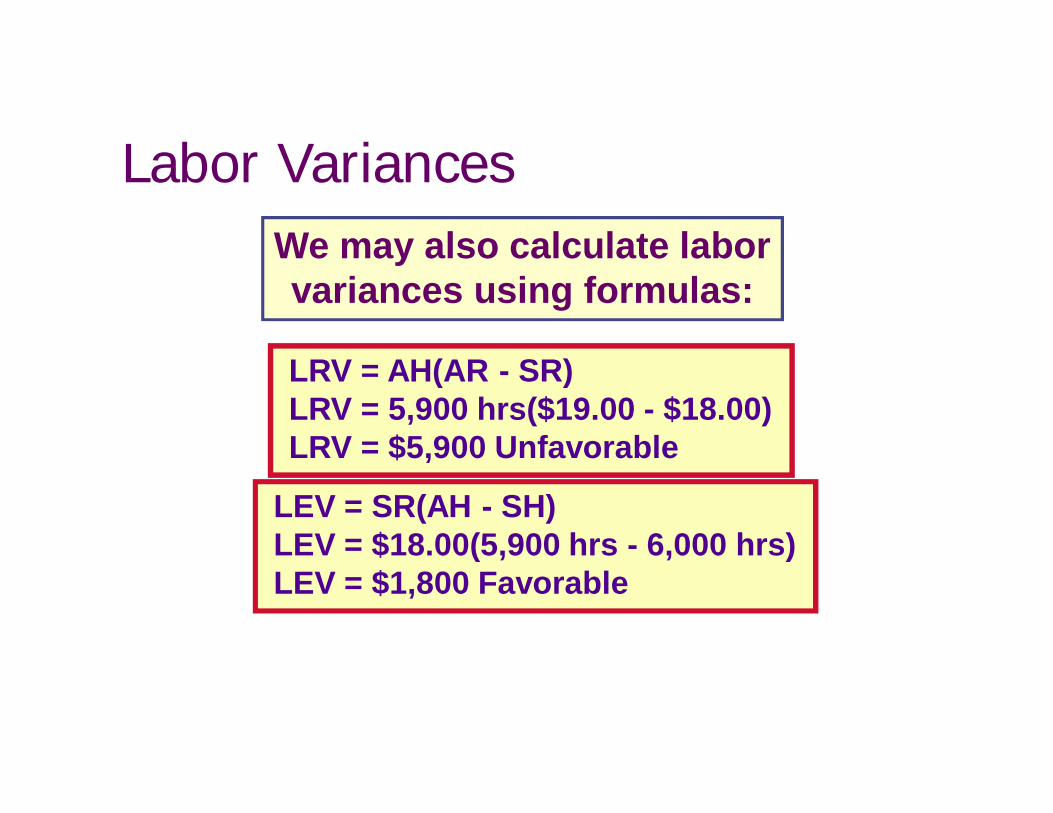

Labor Variances

LRV = AH(AR - SR)LRV = 5,900 hrs($19.00 - $18.00)LRV = $5,900 Unfavorable

LEV = SR(AH - SH)LEV = $18.00(5,900 hrs - 6,000 hrs)LEV = $1,800 Favorable

We may also calculate laborvariances using formulas:

Labor Variances

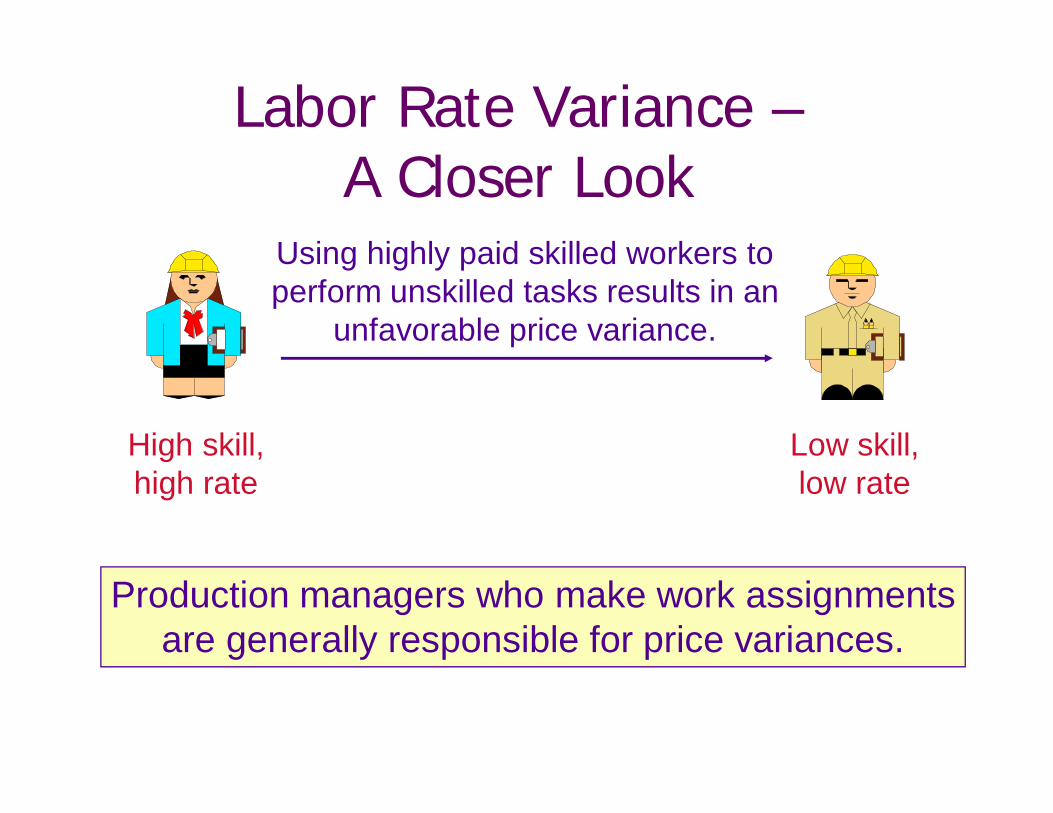

Labor Rate Variance –A Closer Look

Production managers who make work assignmentsare generally responsible for price variances.

High skill,high rate

Low skill,low rate

Using highly paid skilled workers toperform unskilled tasks results in an

unfavorable price variance.

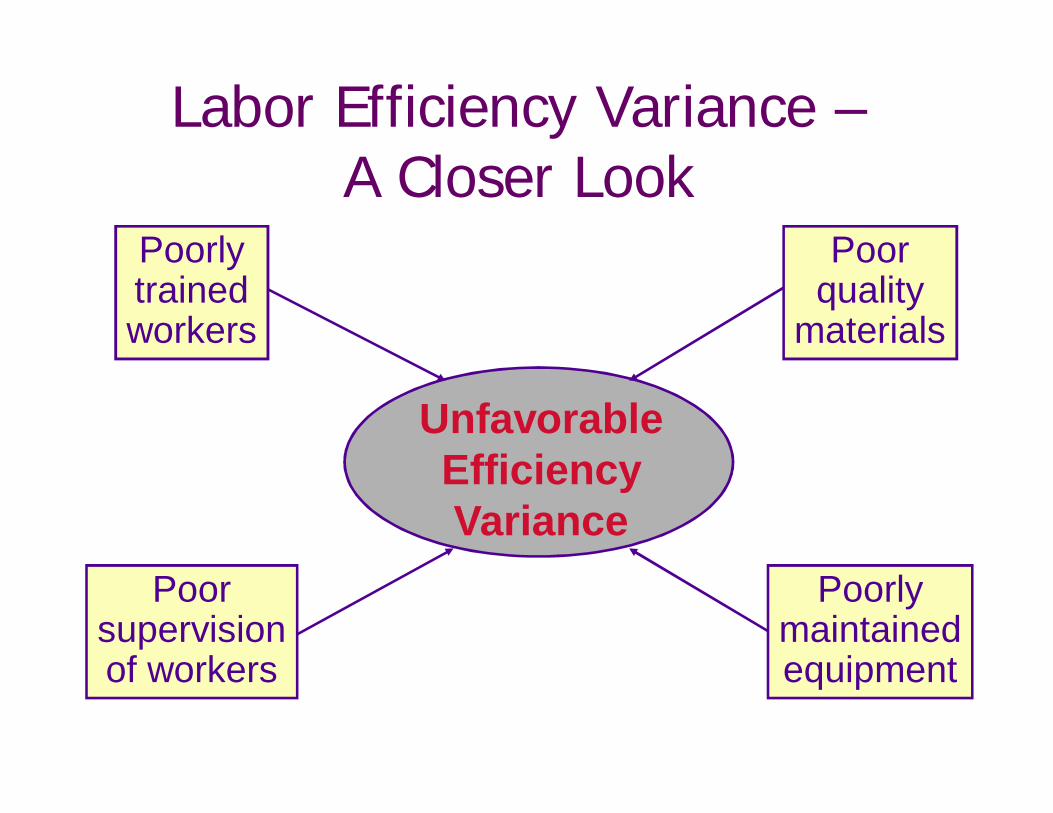

Labor Efficiency Variance –A Closer Look

UnfavorableEfficiencyVariance

Poorlytrainedworkers

Poorquality

materials

Poorlymaintainedequipment

Poorsupervisionof workers

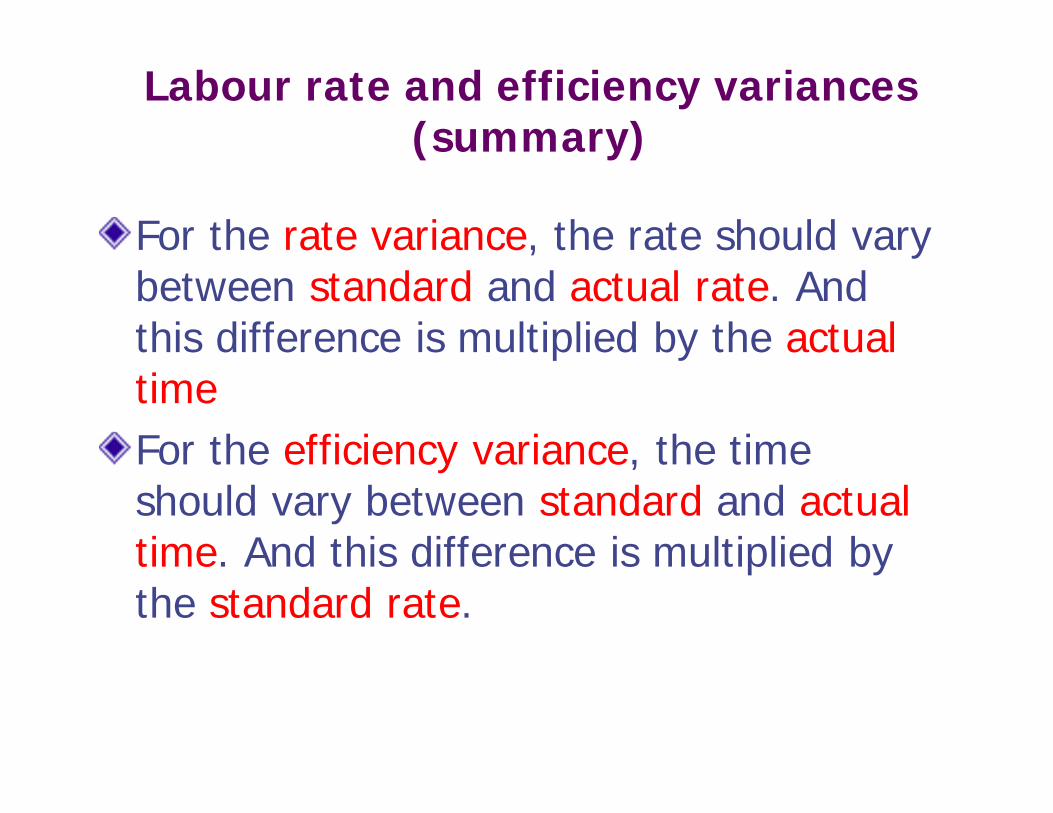

Labour rate and efficiency variances (summary)

For the rate variance, the rate should vary between standard and actual rate. And this difference is multiplied by the actual timeFor the efficiency variance, the time should vary between standard and actual time. And this difference is multiplied by the standard rate.

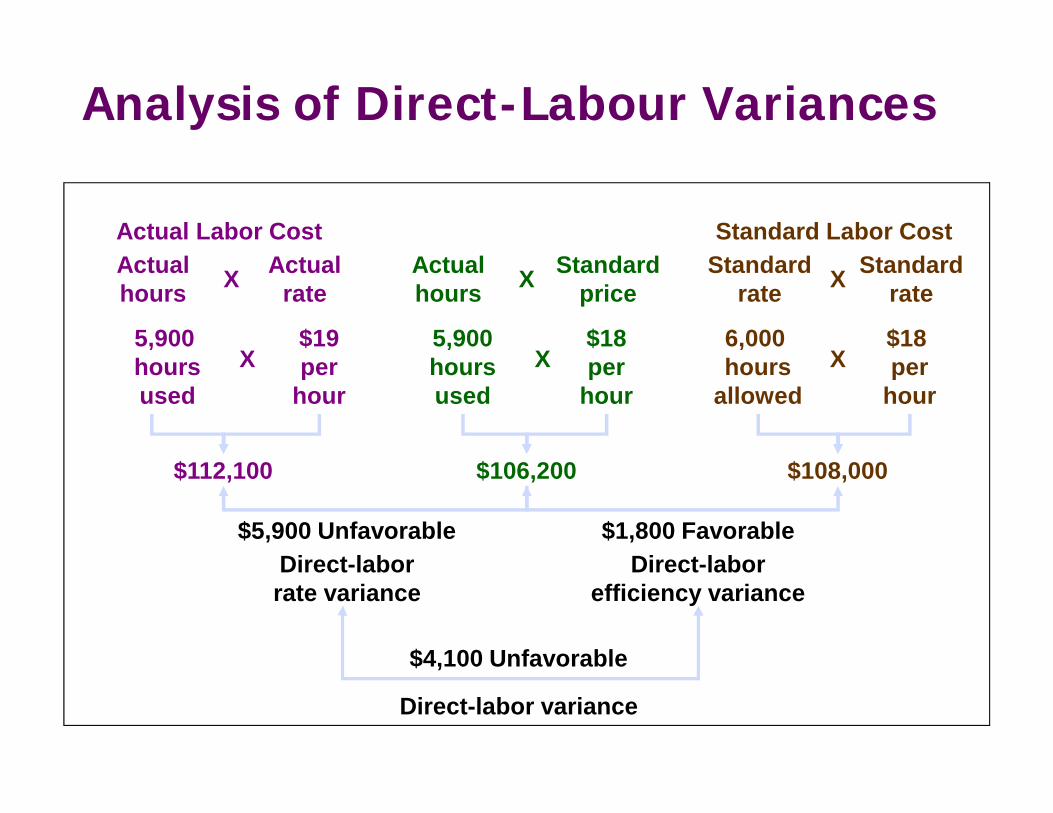

X X X

Actual Labor Cost Standard Labor CostActualhours

Standardprice

Actualrate

Actualhours

Standardrate

StandardrateXXX

5,900 hoursused

$19per

hour

5,900hoursused

$18per

hour

6,000 hours

allowed

$18 per

hour

$112,100 $106,200 $108,000

$5,900 Unfavorable $1,800 FavorableDirect-laborrate variance

Direct-laborefficiency variance

$4,100 Unfavorable

Direct-labor variance

Analysis of Direct-Labour Variances

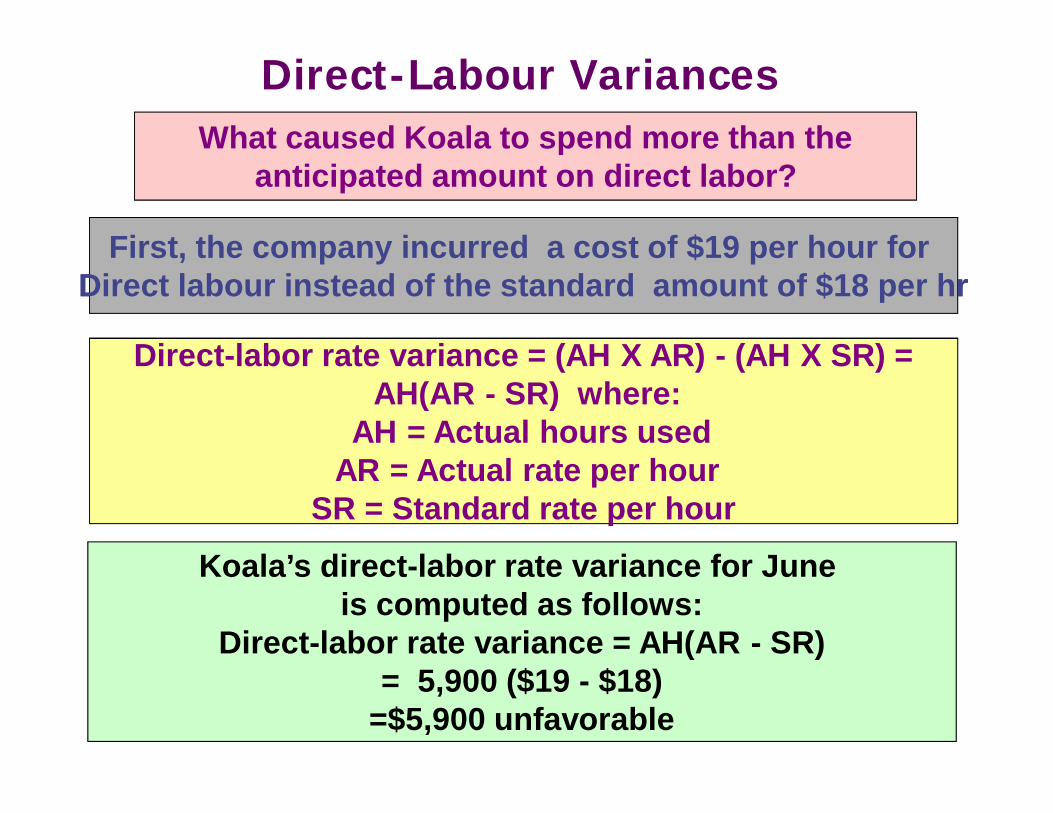

What caused Koala to spend more than theanticipated amount on direct labor?

Direct instead of the standard amount of $18 per hrFirst, the company incurred a cost of $19 per hour for

Direct labour instead of the standard amount of $18 per hr

Direct-labor rate variance = (AH X AR) - (AH X SR) =

SR = Standard rate per hour

Direct-labor rate variance = (AH X AR) - (AH X SR) =AH(AR - SR) where:

AH = Actual hours used AR = Actual rate per hour

SR = Standard rate per hour

Koala’s direct-labor rate variance for June is computed as follows:

Direct-labor rate variance = AH(AR - SR)= 5,900 ($19 - $18)

=$5,900 unfavorable

Direct-Labour Variances

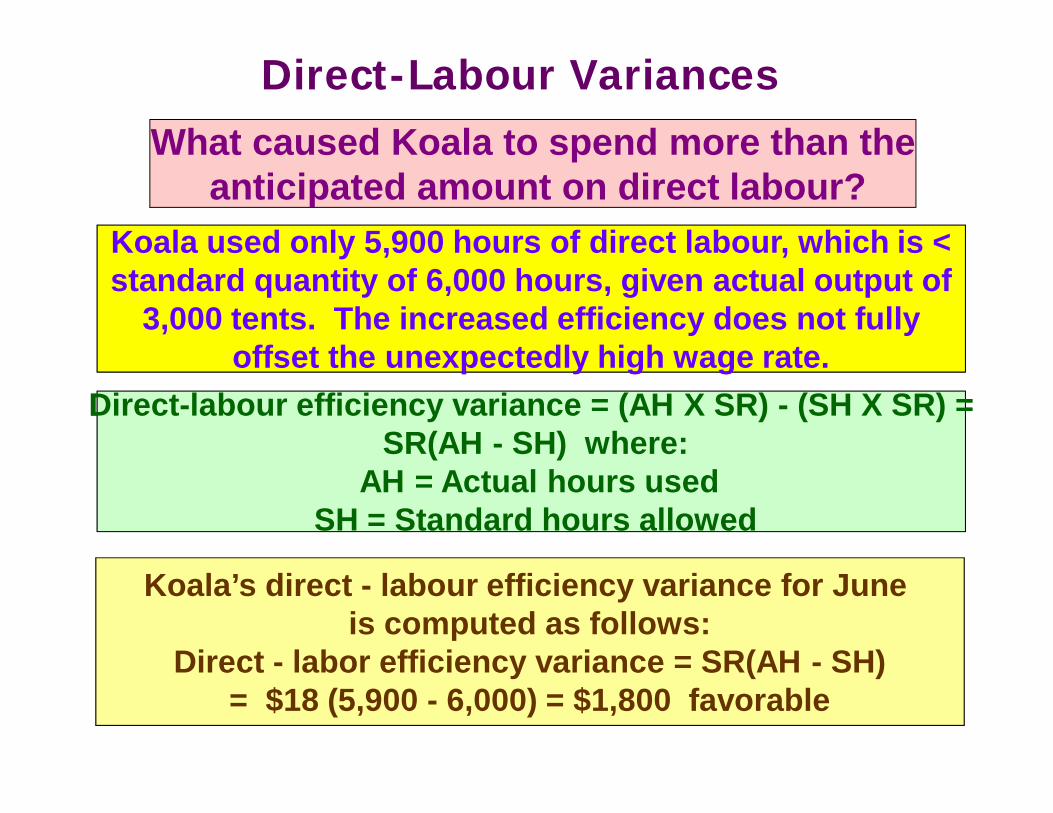

Koala used only 5,900 hours of direct labour, which is <

offset the unexpectedly high wage rate.

Koala used only 5,900 hours of direct labour, which is < standard quantity of 6,000 hours, given actual output of

3,000 tents. The increased efficiency does not fully offset the unexpectedly high wage rate.

Direct-labour efficiency variance = (AH X SR) - (SH X SR) =

SH = Standard hours allowed

Direct-labour efficiency variance = (AH X SR) - (SH X SR) =SR(AH - SH) where:

AH = Actual hours used SH = Standard hours allowed

Koala’s direct - labour efficiency variance for June is computed as follows:

Direct - labor efficiency variance = SR(AH - SH)= $18 (5,900 - 6,000) = $1,800 favorable

anticipated amount on direct labour?What caused Koala to spend more than the

anticipated amount on direct labour?

Direct-Labour Variances

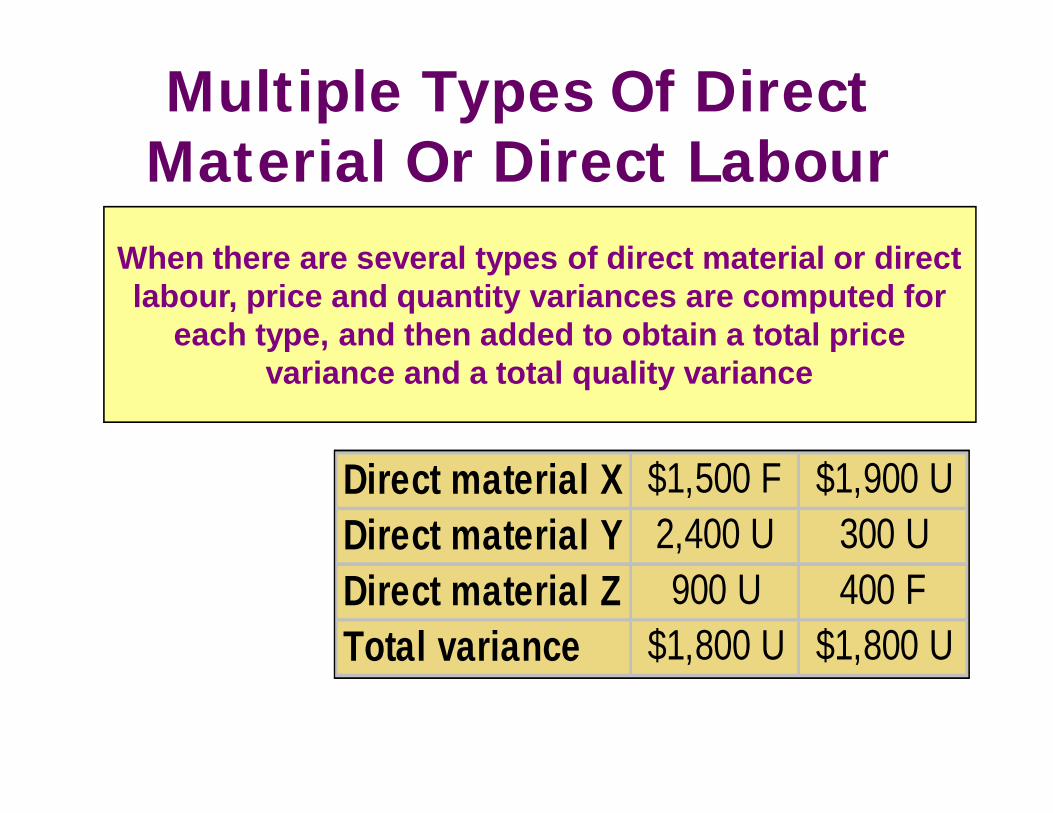

Direct material X $1,500 F $1,900 UDirect material Y 2,400 U 300 UDirect material Z 900 U 400 FTotal variance $1,800 U $1,800 U

Direct material X $1,500 F $1,900 UDirect material Y 2,400 U 300 UDirect material Z 900 U 400 FTotal variance $1,800 U $1,800 U

When there are several types of direct material or direct labour, price and quantity variances are computed for

each type, and then added to obtain a total price variance and a total quality variance

Multiple Types Of Direct Material Or Direct Labour

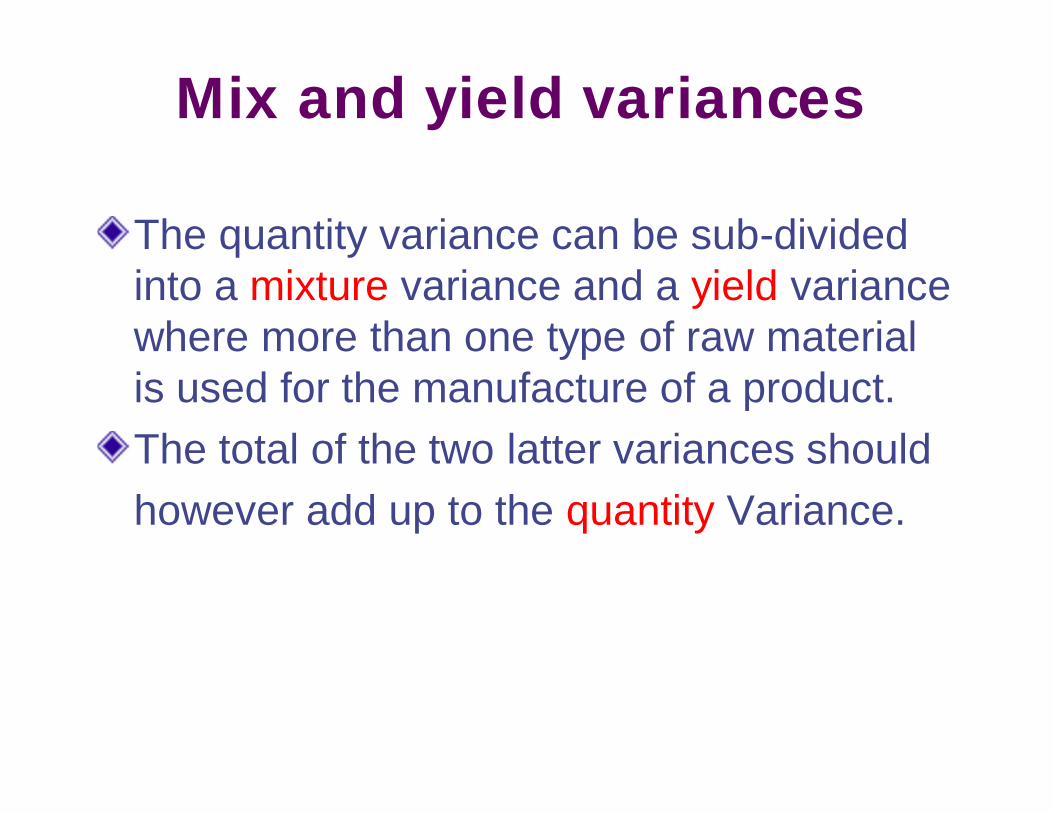

Mix and yield variances

The quantity variance can be sub-divided into a mixture variance and a yield variance where more than one type of raw material is used for the manufacture of a product. The total of the two latter variances should however add up to the quantity Variance.

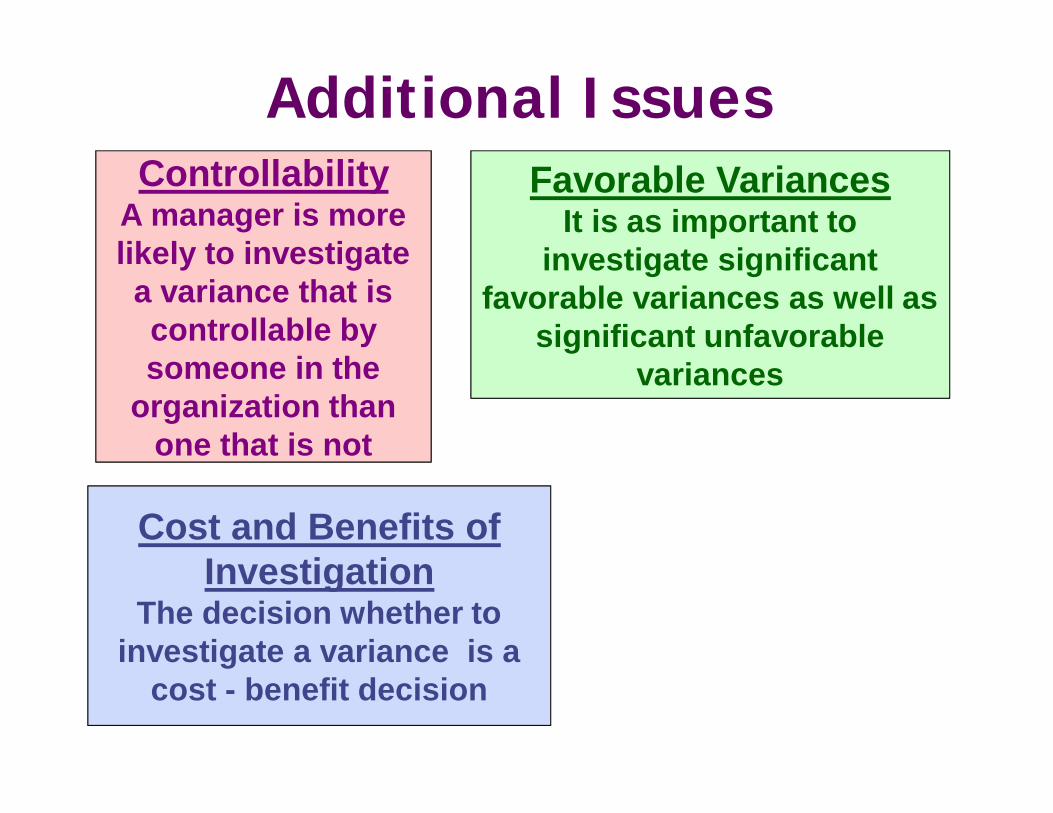

one that is not

ControllabilityA manager is more likely to investigate a variance that is controllable by someone in the

organization than one that is not

Favorable VariancesIt is as important to

investigate significant favorable variances as well as

significant unfavorable variances

Cost and Benefits of Investigation

The decision whether to investigate a variance is a

cost - benefit decision

Additional Issues

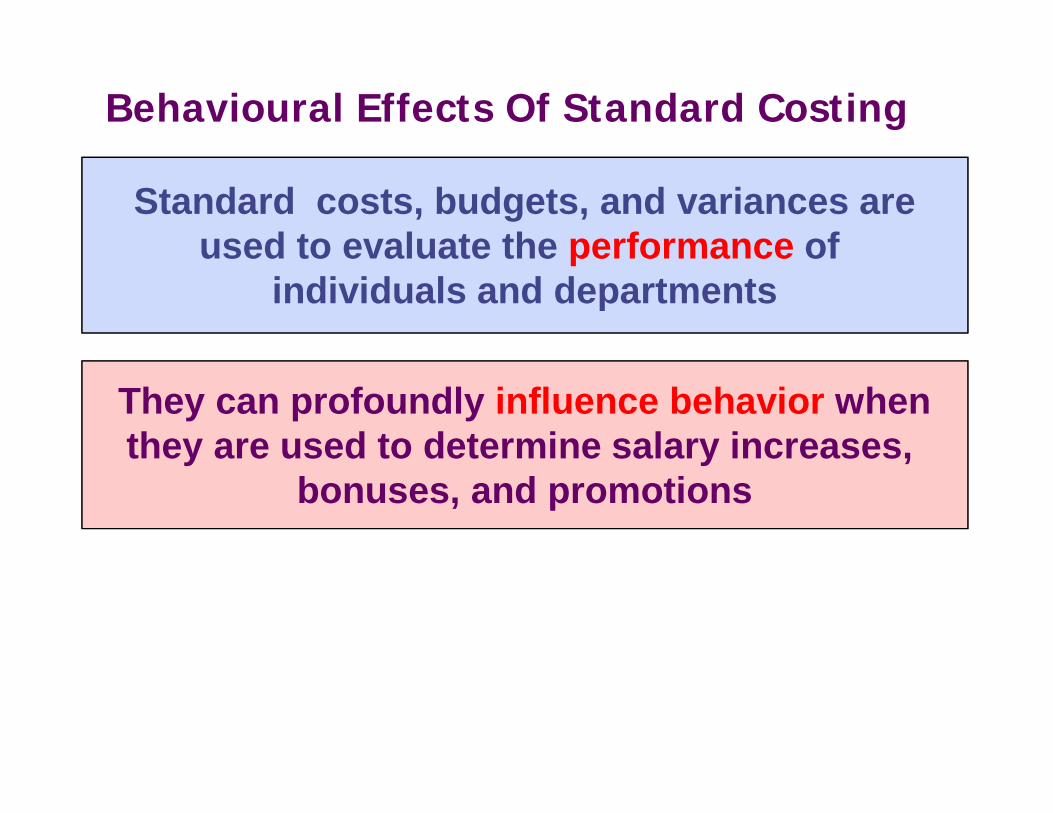

Behavioural Effects Of Standard Costing

Standard costs, budgets, and variances areused to evaluate the performance of

individuals and departments

They can profoundly influence behavior whenthey are used to determine salary increases,

bonuses, and promotions

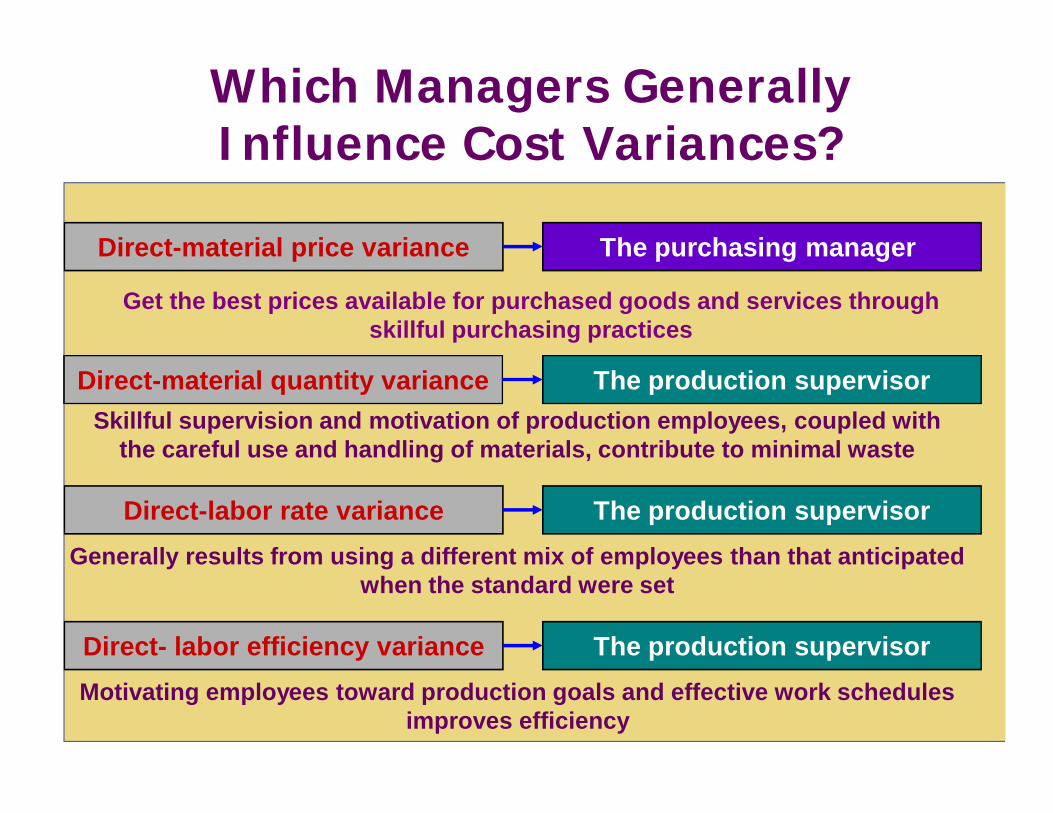

Direct-material price variance

Direct-material quantity variance

Direct-labor rate variance

Direct- labor efficiency variance

The purchasing manager

The production supervisor

The production supervisor

The production supervisor

Get the best prices available for purchased goods and services throughskillful purchasing practices

Skillful supervision and motivation of production employees, coupled withthe careful use and handling of materials, contribute to minimal waste

Generally results from using a different mix of employees than that anticipatedwhen the standard were set

Motivating employees toward production goals and effective work schedulesimproves efficiency

Which Managers Generally Influence Cost Variances?

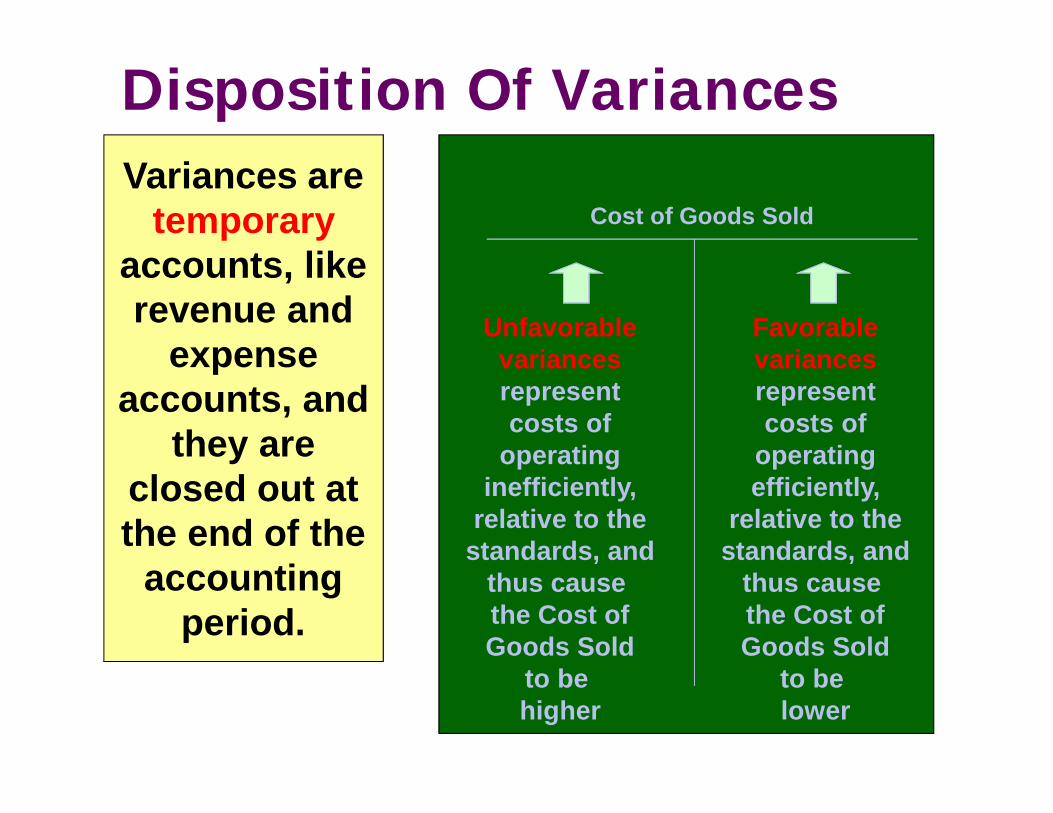

Variances are temporary

accounts, like revenue and

expense accounts, and

they are closed out at the end of the

accountingperiod.

Cost of Goods Sold

Unfavorablevariancesrepresentcosts of

operatinginefficiently,

relative to thestandards, and

thus cause the Cost ofGoods Sold

to be higher

Favorablevariancesrepresentcosts of

operatingefficiently,

relative to thestandards, and

thus cause the Cost ofGoods Sold

to be lower

Disposition Of Variances