Embed Size (px)

Citation preview

Fleet Management in Central & Eastern Europe

Challenges & Opportunities

By Thomas Schroeder, Business Development Director Central Europe

� About LeasePlan

� Challenges & Opportunities

� Funding and fleet strategy

� CO2

� Taxation

� Summary

� Changing car policy

Fleet europe forum

CONTENT

About LeasePlan

Global market leader in fleet and vehicle management

� Founded in 1963 in The Netherlands

� Owned by a consortium of :� Volkswagen Bank GmbH (50%� Fleet Investments B.V. (50%)

� Global presence with offices in 30 countries� 1.3 million cars managed

� Well-diversified corporate customer base

� Manufacturer independent

� Universal banking license, supervised by the

Dutch Central Bank

� Proven track record in managing risk

� About LeasePlan

� Challenges & Opportunities

� Funding and fleet strategy

� Environmental approach

� Taxation

� Summary

� Changing car policy

Fleet europe forum

CONTENT

CHALLENGES & OPPORTUNITIES

Economic & political climate

� EUROPE – Moderate recovery

� Supported by global trade and policy

stimulus

� Savings measures

� Slow recovery employment market

� Interest rates are expected to

increase

� Changing taxation

� CENTRAL / EASTERN EUROPE –

Higher inflation

� Russia, fragile recovery

Increase of policy rate with 25 bps

� Poland continues to out perform

� CZ, manufacturer PMI at record high

� HU, reform plan to reduce budget

deficit and public debt

CHALLENGES & OPPORTUNITIES

Funding

� Low liquidity affecting both consumers, clients and fleet management companies;

�Collapse of car market (e.g. up to 60% less cars in HU)

�Decline of resale values and second hand car market demands

�Fleet Management Market

�Consolidation of the lease market is continuing

� Less local market players

� Increasing presence of global fleet management companies

CHALLENGES & OPPORTUNITIES

Fleet strategy

�Outright purchase � Financial lease � Operational lease

�Companies are focusing on price more than before and trying various purchasing strategies

� Lease Accounting Standards (IFRS)

�Commercial car market opening up for operational lease

�Car policy subject to change

CHALLENGES & OPPORTUNITIES

Fleet cost control and the rising price of fuel

� Our life is almost entirely oil dependent

� Crude oil price climbed by over 35% since last low in May 2010

� Various measures taken by governments

� Diversifying oil distribution across countries

� Financial measures like in Saudi Arabia

� Speed limits like in Spain

� Considerations for fleet

� Look at emerging technologies

� Choose fuel efficient vehicles

� Review vehicle allocation policy

� Downsizing company cars

� Fuel management

� Look at driving habits (e.g. Driver training)

€0

€500

€1,000

€1,500

€2,000

€2,500

€3,000

€3,500

€4,000

Average annual fuel cost per car

fuel price anticipated price increase

€0

€500

€1,000

€1,500

€2,000

€2,500

€3,000

€3,500

€4,000

Average annual fuel cost per car

fuel price anticipated price increase

source: ConsultPlus, data for Slovenia

Increase

23%

� About LeasePlan

� Challenges & Opportunities

� Funding and fleet strategy

� Environmental approach

� Taxation

� Summary

� Changing car policy

Fleet europe forum

CONTENT

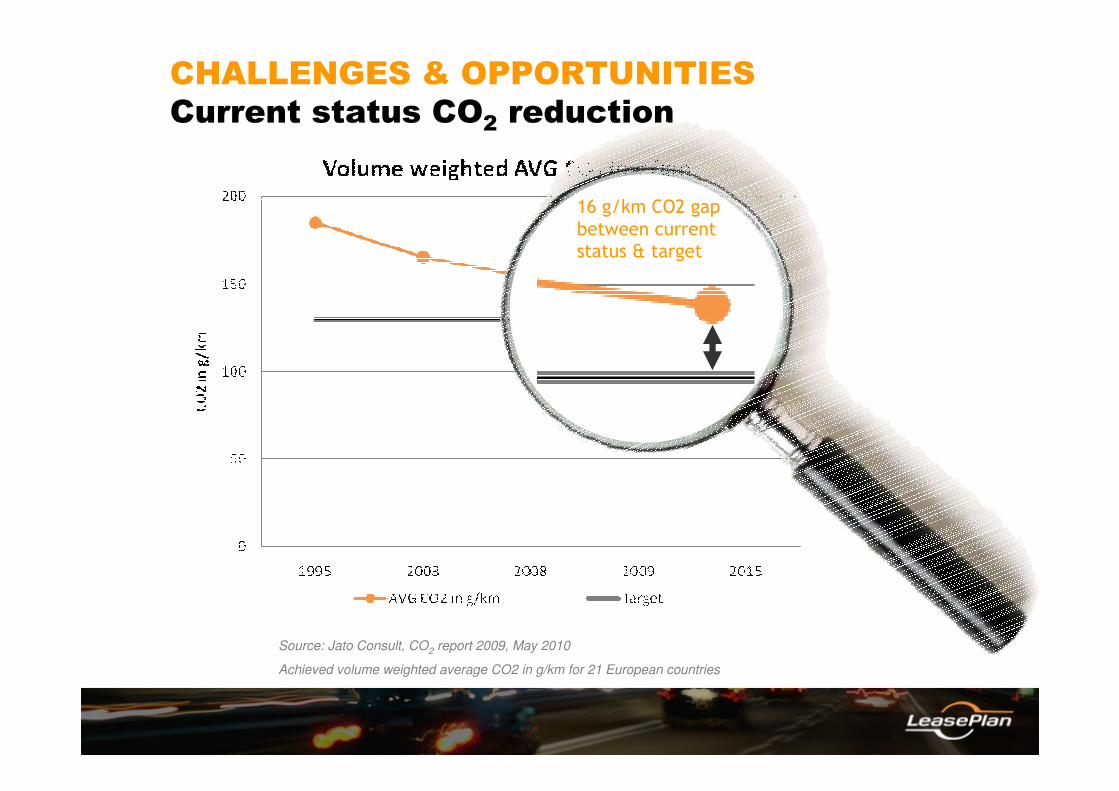

CHALLENGES & OPPORTUNITIES

Current status CO2 reduction

•Source: Jato Consult, CO2 report 2009, May 2010

•Achieved volume weighted average CO2 in g/km for 21 European countries

16 g/km CO2 gap

between current

status & target

CHALLENGES & OPPORTUNITIESCO2 reduction – how the industry achieved this…

1. Technical developments

2. Economic pressure

3. Fiscal regulation & scrappage schemes

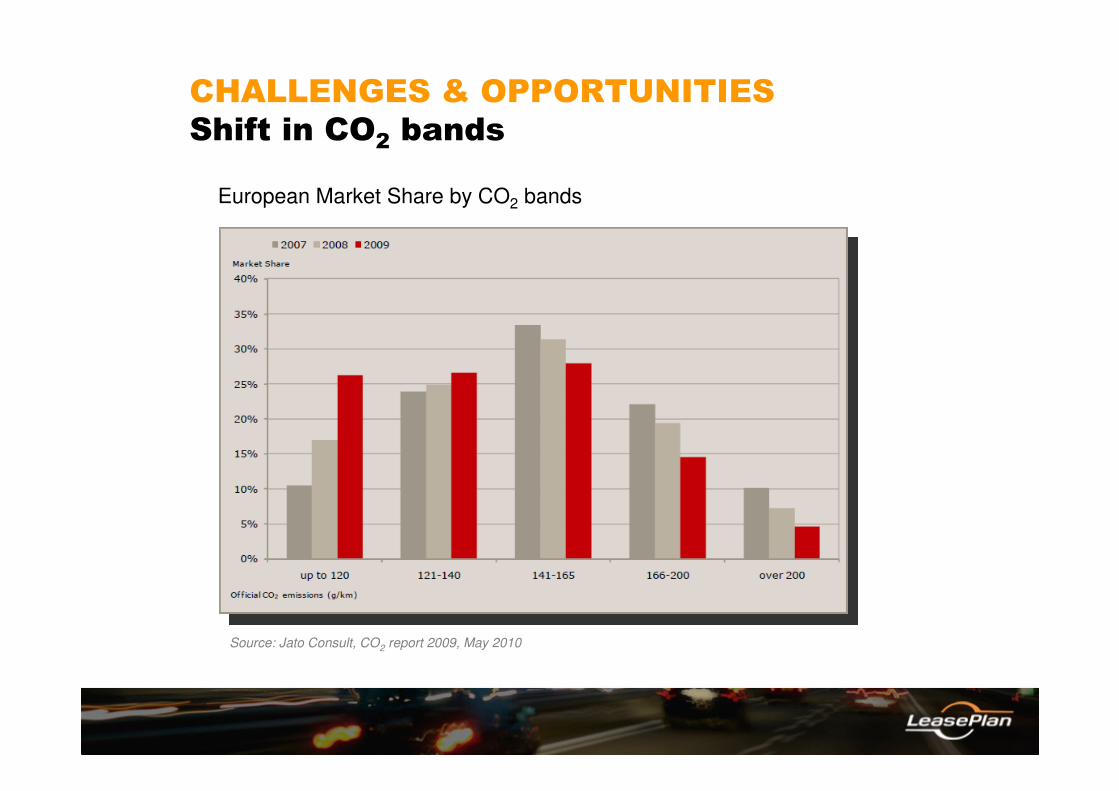

•European Market Share by CO2 bands

•Source: Jato Consult, CO2 report 2009, May 2010

CHALLENGES & OPPORTUNITIES

Shift in CO2 bands

CHALLENGES & OPPORTUNITIES

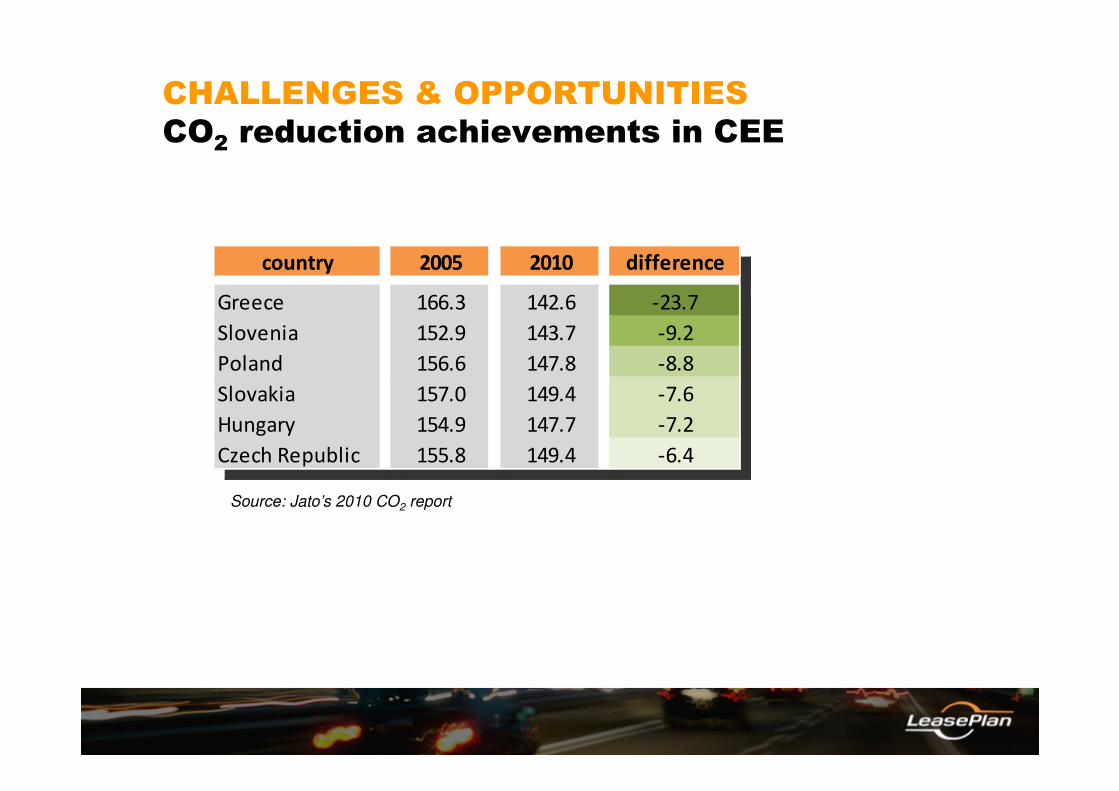

CO2 reduction achievements in CEE

country 2005 2010 difference

Greece 166.3 142.6 -23.7

Slovenia 152.9 143.7 -9.2

Poland 156.6 147.8 -8.8

Slovakia 157.0 149.4 -7.6

Hungary 154.9 147.7 -7.2

Czech Republic 155.8 149.4 -6.4

country 2005 2010 difference

Greece 166.3 142.6 -23.7

Slovenia 152.9 143.7 -9.2

Poland 156.6 147.8 -8.8

Slovakia 157.0 149.4 -7.6

Hungary 154.9 147.7 -7.2

Czech Republic 155.8 149.4 -6.4

Source: Jato’s 2010 CO2 report

� About LeasePlan

� Challenges & Opportunities

� Funding and fleet strategy

� Environmental approach

� Taxation

� Summary

� Changing car policy

Fleet europe forum

CONTENT

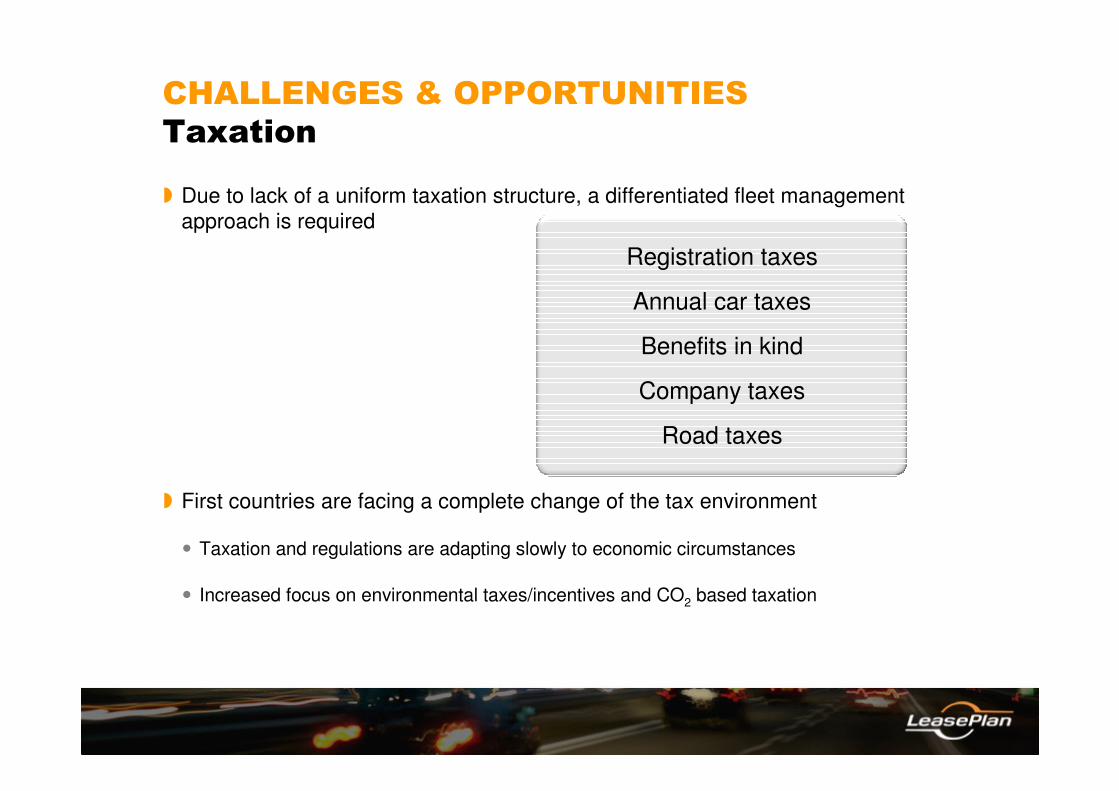

� Due to lack of a uniform taxation structure, a differentiated fleet management

approach is required

� First countries are facing a complete change of the tax environment

� Taxation and regulations are adapting slowly to economic circumstances

� Increased focus on environmental taxes/incentives and CO2 based taxation

Registration taxes

Annual car taxes

Benefits in kind

Company taxes

Road taxes

CHALLENGES & OPPORTUNITIES

Taxation

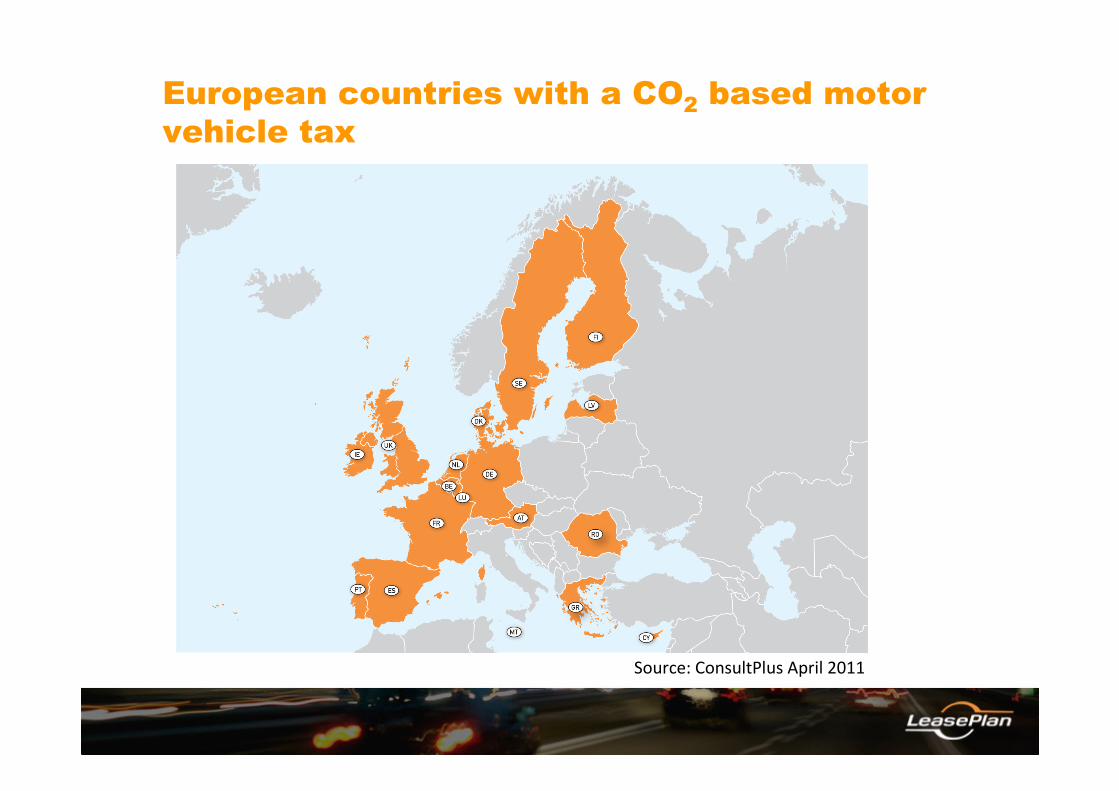

European countries with a CO2 based motor

vehicle tax

•Source: ConsultPlus April 2011

� About LeasePlan

� Challenges & Opportunities

� Company Car, Strategy, Cost

� Environmental approach

� Taxation

� Summary

� Changing car policy

Fleet europe forum

CONTENT

CHALLENGES & OPPORTUNITIES

Changing car policy

�Changes in company car policies

� Increased focus on cost and cost reduction opportunities

� Pro-active fleet management

� Upfront pricing and TCO

� Increased focus on environmental aspects

� CO2 thresholds

� Budgets including fuel

� Incentives to motivate BIK drivers

� Fuel management and influencing driver behaviour

�Harmonisation with other countries/subsidiaries

� Alignment of allocation