Embed Size (px)

DESCRIPTION

fleet europe 63 OEM Fleet Strategy

Citation preview

Tips for efficient procurement

Athlon Car Lease in partnership with Tesla

E-mobility & the infrastructure equation

ScopeManageMent

car Manufacturers’Fleet Strategytheir fleet strategy,their product & service development,and their view on the future

DoSSIeR

case Studies MSD & almirallLearn from the winners of the Fleet europe awardswith espiri carrasco

ManageMent

March 2013 - # 63

NE

XU

S C

OM

MU

NIC

ATIO

N -

FLE

ET

EU

RO

PE

#63

- P

ER

IOd

IC M

Ag

AzI

NE

- M

AR

Ch

201

3 -

dE

PO

SIT

OF

FIC

E L

Ièg

E X

Save the Date: IFMI SeSSIon on the Do’S & Don’tS oF toDay’SFLeet ManageMent - BRuSSeLS, 29 May 2013.

BuSIneSS

To see the future of your business,

56734_001TOYOTA_FleetEur_189x297.indd 1 __TFG Prepress__ 18/02/2013 13:01

March 2013 - # 63

To see the future of your business,

56734_001TOYOTA_FleetEur_189x297.indd 1 __TFG Prepress__ 18/02/2013 13:01

Toyota Hybrid Range. For your business, Hybrid is a business.

By adding Toyota hybrid range to your fl eet, you’ll be able to achieve signifi cant fi nancial savings, while making a powerful environment statement to your customers. Look back at our 16 years of success to drive your business forward.

Since 1997 we have been continuously improving our hybrid technology, engineering it into the cars of almost 5 million satisfi ed drivers. And guess what? Our Hybrid family is growing all the time, with a portfolio of 6 hybrids available today. Toyota’s hybrid family combines low fuel consumption and emissions with uniquely relaxed, quiet driving.

56734_001TOYOTA_FleetEur_398x297.indd 1 __TFG Prepress__ 18/02/2013 14:42

Toyota Hybrid Range. For your business, Hybrid is a business.

By adding Toyota hybrid range to your fl eet, you’ll be able to achieve signifi cant fi nancial savings, while making a powerful environment statement to your customers. Look back at our 16 years of success to drive your business forward.

Since 1997 we have been continuously improving our hybrid technology, engineering it into the cars of almost 5 million satisfi ed drivers. And guess what? Our Hybrid family is growing all the time, with a portfolio of 6 hybrids available today. Toyota’s hybrid family combines low fuel consumption and emissions with uniquely relaxed, quiet driving.

56734_001TOYOTA_FleetEur_398x297.indd 1 __TFG Prepress__ 18/02/2013 14:42

Toyota Hybrid Range. For your business, Hybrid is a business.

By adding Toyota hybrid range to your fl eet, you’ll be able to achieve signifi cant fi nancial savings, while making a powerful environment statement to your customers. Look back at our 16 years of success to drive your business forward.

Since 1997 we have been continuously improving our hybrid technology, engineering it into the cars of almost 5 million satisfi ed drivers. And guess what? Our Hybrid family is growing all the time, with a portfolio of 6 hybrids available today. Toyota’s hybrid family combines low fuel consumption and emissions with uniquely relaxed, quiet driving.

56734_001TOYOTA_FleetEur_398x297.indd 1 __TFG Prepress__ 18/02/2013 14:42

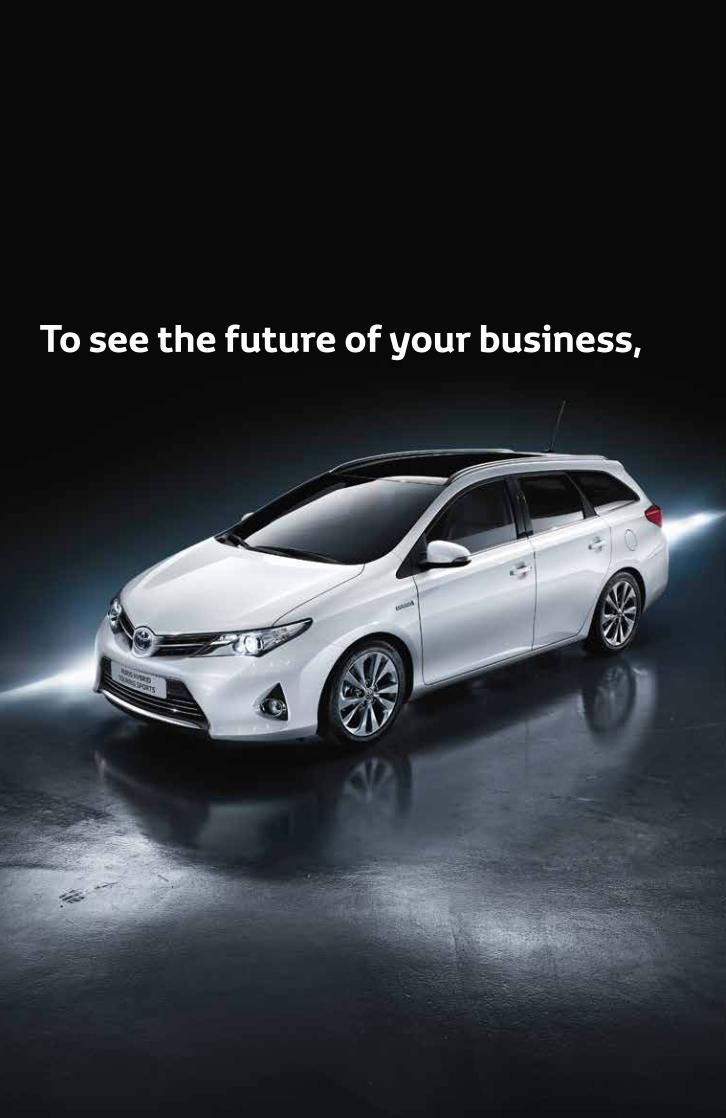

www.skoda-auto.com

SIMPLY CLEVER

ŠKODA Rapid. A great news for your eet.

Combined fuel consumption and CO2 emissions for the Rapid model: 3.9–5.8 l/100 km, 104–134 g/km

Regardless of which angle you look at the new ŠKODA Rapid, you will always discover many good reasons why to make it a member of your company eet. Rapid is a representative as well as a practical car. Behind its elegant clean lines awaits a spacious interior and many clever details that will make traveling pleasant for the entire crew. For example, the side pockets where you can place your cell phone, an ice scraper mounted on the fuel tank lid or the multimedia holder located on the center console. While drivers will enjoy the high performance of TSI engines, eet managers will appreciate their ef ciency. The offer also includes extremely ef cient 1.6 TDI diesel engines. All TDI and TSI engines are also available in Green tec versions that are particularly environmentally friendly. With the new ŠKODA Rapid your eet will reach a completely new level. Contact us as soon as possible. We will gladly introduce you to other ŠKODA models from our eet offer.

Rapid_fleet_A4-sample.indd 1 11.12.12 11:25

P.7FLEET EUROPE # 63www.skoda-auto.com

SIMPLY CLEVER

ŠKODA Rapid. A great news for your eet.

Combined fuel consumption and CO2 emissions for the Rapid model: 3.9–5.8 l/100 km, 104–134 g/km

Regardless of which angle you look at the new ŠKODA Rapid, you will always discover many good reasons why to make it a member of your company eet. Rapid is a representative as well as a practical car. Behind its elegant clean lines awaits a spacious interior and many clever details that will make traveling pleasant for the entire crew. For example, the side pockets where you can place your cell phone, an ice scraper mounted on the fuel tank lid or the multimedia holder located on the center console. While drivers will enjoy the high performance of TSI engines, eet managers will appreciate their ef ciency. The offer also includes extremely ef cient 1.6 TDI diesel engines. All TDI and TSI engines are also available in Green tec versions that are particularly environmentally friendly. With the new ŠKODA Rapid your eet will reach a completely new level. Contact us as soon as possible. We will gladly introduce you to other ŠKODA models from our eet offer.

Rapid_fleet_A4-sample.indd 1 11.12.12 11:25

From Business to Business

To Business to Employee

newsletter Issuu.com calaméo.com

Linkedin twitter

Register to the Fleet Europe Newsletter and receive twice a month the highlights of the in-ternational fleet sector.www.fleeteurope.com

Discover the digital edition of Fleet Europe magazine. Have a look at the more recent edition, or look at our archives.www.issuu.com

Discover the digital edition of Fleet Europe magazine, adapted to be read through your smart-phone and iPad.www.calameo.com

Join the Fleet Europe LinkedIn group and connect with internation-al fleet professionals, fleet decision makers, suppliers and experts. Our LinkedIn Community counts more than 1,780 members. http://www.linkedin.com/ groups?about=&gid =157239

Discover the latest magazine, picture from our events, event announcements… If you like our pages, click on ‘LIKE’ and share it with your contacts!www.facebook.com/Fleet-europe

Follow the latest tweets of @FleetEurope2012 and connect to Chief Editor @StevenSchoefs and Partner Content & Business Development @CarolineThonnon

Fleet europe is a cross-medium platform where analyzes, interviews and factual information go hand in hand with sharing best practices and with the possibility to learn from each other through dedicated training sessions. to optimize this cross-medium sharing expertise we propose different applications and tools to interact with the international fleet community

Join Fleet Europe’s community

The Driver Connection

eDIt

oR

IaL

Although 2013 is only in its first quarter, we can already say that it will be once again be a challenging year t the fleet business has become key to the automotive players as B2B sales guarantee market share and assure sales volumes. And the fleet market is highly appreciated as the ideal arena for introducing and testing new technologies and innovations in terms of sustainability, safety and driver behaviour. B2B clients are early adopters, as we all know. Together with other fleet suppliers the car manufacturers are looking to expand the fleet market in trying to extend their B2B sales with ‘B2E’ sales (Business to Employee). Various car lease companies have also recently launched new initiatives with the fleet driver at the center. A logical step as it is: 1) a must to secure business and thus an opportunity to expand the target group, and 2) it is often the driver that has the power to choose his company car or mobility mode, and it is the driver that has an important impact on the TCO. So it would appear that 2013 brings new business initiatives for fleet suppliers with the driver in the driver’s seat!

But this must not be at the cost of neglecting B2B clients. Because these B2B clients are the basis of the car fleet business, and there is still work to be done here. International fleets need their suppliers to bring realistic innovation and concrete ideas to improve fleet efficiency, along with an easy assessment of performance. So let’s hope that 2013 will not only be the year of the driver connection, but that it will be the year of the fleet connection.

And that is the goal of the Fleet Europe platform: making the connection between all parties and players in the car fleet business in Europe.

Steven Schoefs, Chief Editor

[email protected] : @StevenSchoefs

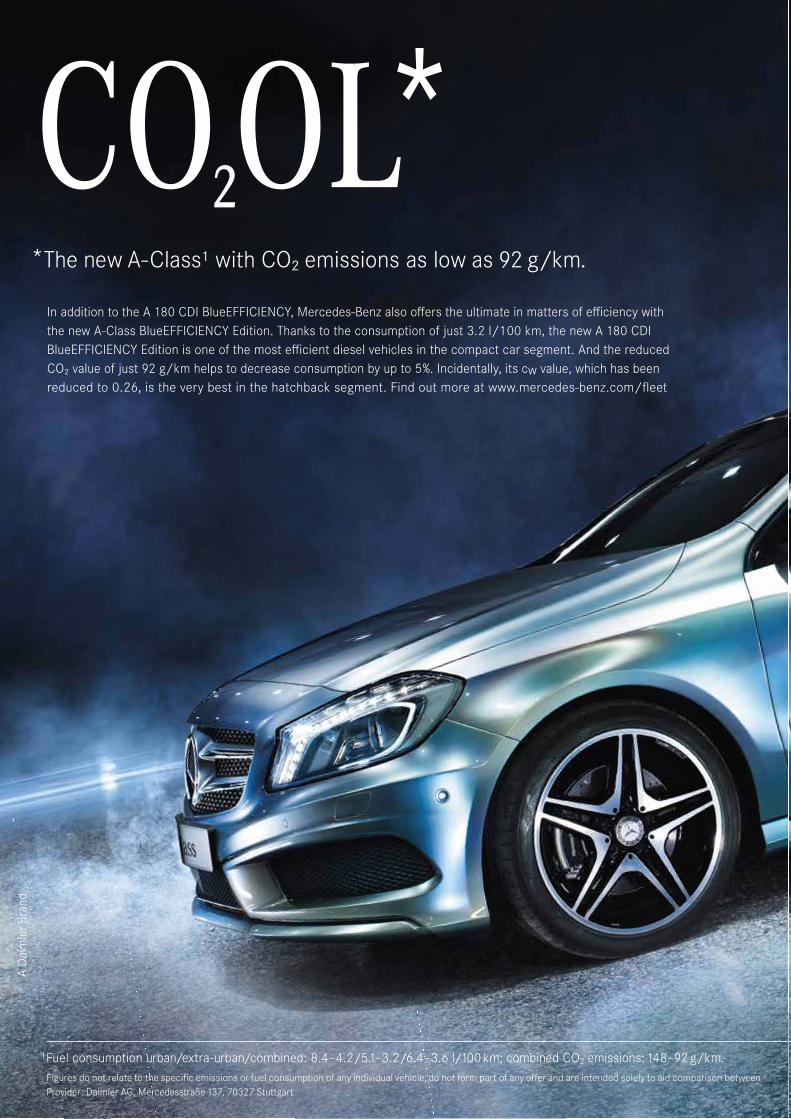

CO²OL* *The new A-Class¹ with CO₂ emissions as low as 92 g/km.

In addition to the A 180 CDI BlueEFFICIENCY, Mercedes-Benz also off ers the ultimate in matters of effi ciency withthe new A-Class BlueEFFICIENCY Edition. Thanks to the consumption of just 3.2 l/100 km, the new A 180 CDIBlueEFFICIENCY Edition is one of the most effi cient diesel vehicles in the compact car segment. And the reducedCO₂ value of just 92 g/km helps to decrease consumption by up to 5%. Incidentally, its cw value, which has beenreduced to 0.26, is the very best in the hatchback segment. Find out more at www.mercedes-benz.com/fl eet

¹Fuel consumption urban/extra-urban/combined: 8.4–4.2/5.1–3.2/6.4–3.6 l/100 km; combined CO₂ emissions: 148–92 g/km.Figures do not relate to the specific emissions or fuel consumption of any individual vehicle, do not form part of any offer and are intended solely to aid comparison between Provider: Daimler AG, Mercedesstraße 137, 70327 Stuttgart

A D

aim

ler B

rand

• Ju

ng v

on M

att

• 4

20 ×

297

mm

•

Kun

de: M

erce

des-

Benz

(Dai

mle

r AG

)•

134

43/2

7/13

001/

07

• 2

/1-S

eite

Ein

zels

eite

n •

Pro

dukt

: A-K

lass

e (W

176)

• D

TP: P

eter

-148

7 •

4C

, Lin

ke S

eite

•

Tite

l/O

bjek

t: F

leet

wor

ld in

tern

atio

nal

Fl

eet E

urop

e M

agaz

in

420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3420x297W176Cool_engl_Flotte.indd 3 14.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:38

Provider: Daimler AG, Mercedesstraße 137, 70327 StuttgartProvider: Daimler AG, Mercedesstraße 137, 70327 Stuttgart

• Ju

ng v

on M

att

• 4

20 ×

297

mm

•

Kun

de: M

erce

des-

Benz

(Dai

mle

r AG

)•

134

43/2

7/13

001/

07

• 2

/1-S

eite

Ein

zels

eite

n •

Pro

dukt

: A-K

lass

e (W

176)

• D

TP: P

eter

-148

7 •

4C

, Rec

hte

Seite

•

Tite

l/O

bjek

t: F

leet

wor

ld in

tern

atio

nal

Fl

eet E

urop

e M

agaz

in

420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4 14.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:38

Provider: Daimler AG, Mercedesstraße 137, 70327 StuttgartProvider: Daimler AG, Mercedesstraße 137, 70327 Stuttgart

• Ju

ng v

on M

att

• 4

20 ×

297

mm

•

Kun

de: M

erce

des-

Benz

(Dai

mle

r AG

)•

134

43/2

7/13

001/

07

• 2

/1-S

eite

Ein

zels

eite

n •

Pro

dukt

: A-K

lass

e (W

176)

• D

TP: P

eter

-148

7 •

4C

, Rec

hte

Seite

•

Tite

l/O

bjek

t: F

leet

wor

ld in

tern

atio

nal

Fl

eet E

urop

e M

agaz

in

420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4420x297W176Cool_engl_Flotte.indd 4 14.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:3814.02.13 11:38

25.09.2012 12:54 PDF_QUADRI_300dpi_txvecto

P.11FLEET EUROPE # 63

25.09.2012 12:54 PDF_QUADRI_300dpi_txvecto

co

nte

nt

ManageMent I case Studiesthe integrated car fleet philosophy at MSD: with Joe carreira and Robert patrick, winners of the International Fleet Managerof the year award.

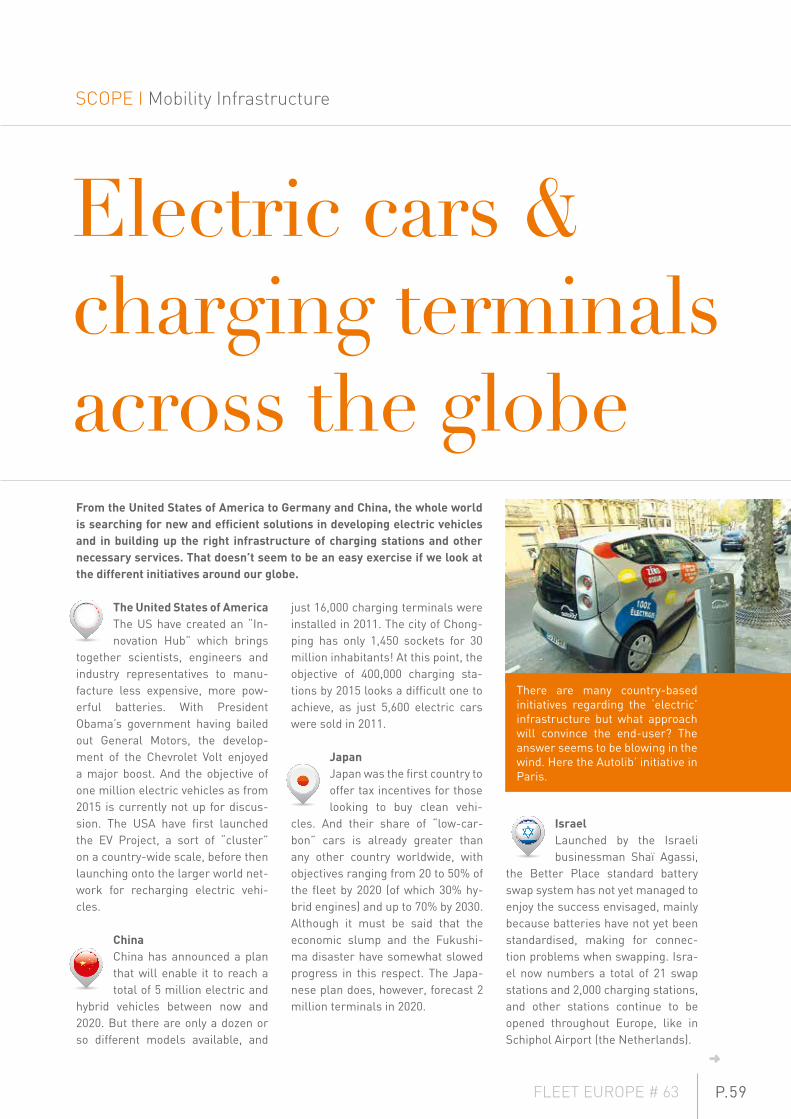

Scope charging stations’ initiativesfor electric cars.

COLOPHONSteven Schoefs - chief editor - Fleet europe([email protected])

caroline thonnon - head of Business Development & global Fleet Leader([email protected])

pierre-yves Simon - It & Web Manager([email protected])

David Baudeweyns - International Sales & Business Development([email protected])

Romina De gregorio - Internal Sales & operations([email protected])

thao van de poel - Internal [email protected]

Kathleen hubert - head of Marketing & Smart Mobility Management Leader([email protected])

Jonathan green - chief editor Smart Mobility [email protected]

contributors: Tim Harrup, Frank Jacobs, Jean-François-Christiaens, Michael Hawking

Special thanks to: Peter Fuβ (Ernst & Young), Professor Peter Cooke (University of Buckingham), Hervé Legenvre (EIPM), Bart Vanham (RBR PwC)

Layout: Un pas plus loin - [email protected]

EDITORthierry Degives, Managing partner at Nexus Communication SA, Parc Artisanal 11-13, 4671 Barchon (Belgium)T. : +32 4 387 87 94 - Fax : +32 4 387 90 63 - www.nexuscommunication.be

FLeet euRopewww.fleeteurope.com - www.fleeteurope.com/shop

I DOSSIER IThe Car Fleet Challenge. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.11

The Changing Business Environment . . . . . . . . . . . . . . . . . . . . . . . P.12

The Race for the Mobility Customer . . . . . . . . . . . . . . . . . . . . . . . . . P.14

B2B is a key area for OEM growth. . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.18

What OEMs can do to help reduce TCO . . . . . . . . . . . . . . . . . . . . . P.24

What does mobility mean for an OEM? . . . . . . . . . . . . . . . . . . . . . P.28

Listen to the car fleet future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.30

Geneva Motor Show 2013 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.34

Going Global . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.38

The driverless car . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.40

I MANAGEMENT ICase study: the fleet philosophy of MSD . . . . . . . . . . . . . . . . . . P.42

Case study: the safety project of Almirall . . . . . . . . . . . . . . . . . P.47

Six tips for efficient fleet procurement . . . . . . . . . . . . . . . . . . . . . P.48

I BUSINESS INews from the world of fleet suppliers . . . . . . . . . . . . . . . . . . . . P.50

Electric partnership between Tesla Motors & Athlon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.52

Fleet Management with TomTom Business Solutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . P.54

I SCOPE I News about the fleet & mobility environment . . . . . . . . . . . P.55Electric cars & Charging terminals . . . . . . . . . . . . . . . . . . . . . . . . . . P.57

DoSSIeR I car Manufacturers’ Fleet Strategy get a clear insight in the organisation,the products and services, andthe new developments for 2013. 11-4057

BuSIneSS athlon car Lease starts partnership withtesla Motors. 52

42

Reproduction rights (texts, advertisements, pictures) reserved for all countries. Received documents will not be returned. By submitting them, the author implicitly authorizes their publication.

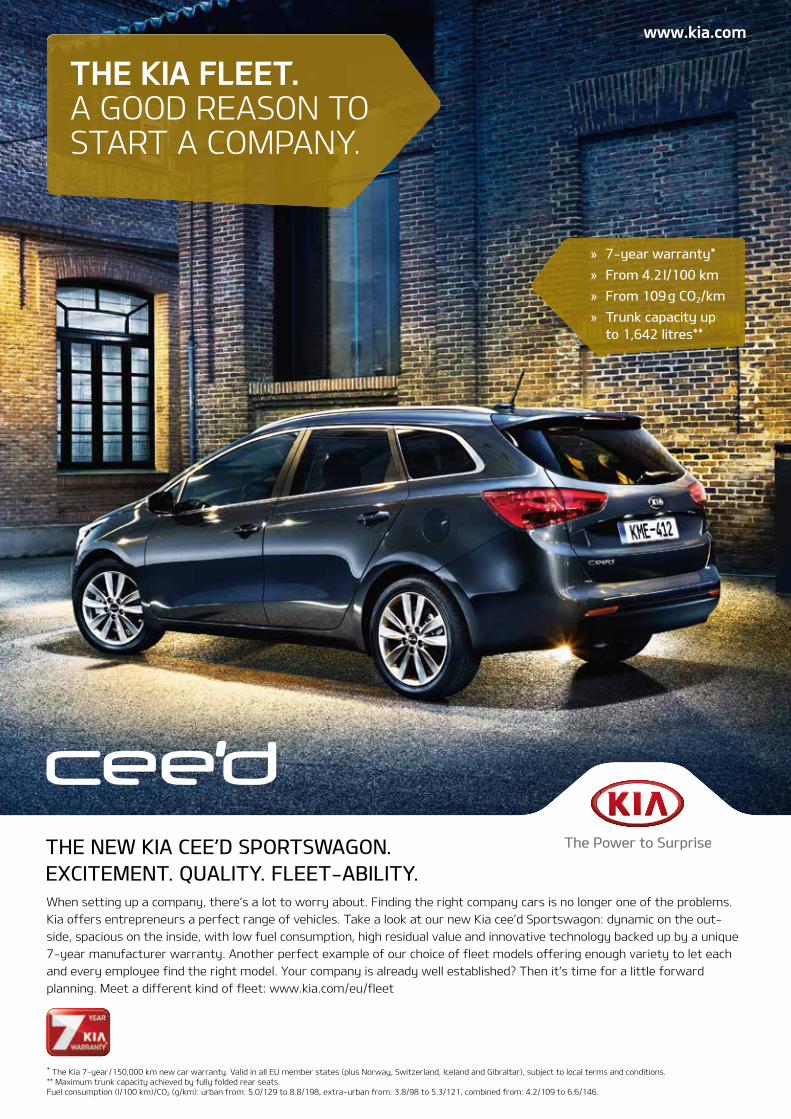

www.kia.com

* The Kia 7-year/150,000 km new car warranty. Valid in all EU member states (plus Norway, Switzerland, Iceland and Gibraltar), subject to local terms and conditions.** Maximum trunk capacity achieved by fully folded rear seats.Fuel consumption (l/100 km)/CO2 (g/km): urban from: 5.0/129 to 8.8/198, extra-urban from: 3.8/98 to 5.3/121, combined from: 4.2/109 to 6.6/146.

When setting up a company, there’s a lot to worry about. Finding the right company cars is no longer one of the problems. Kia offers entrepreneurs a perfect range of vehicles. Take a look at our new Kia cee’d Sportswagon: dynamic on the out-side, spacious on the inside, with low fuel consumption, high residual value and innovative technology backed up by a unique 7-year manufacturer warranty. Another perfect example of our choice of fleet models offering enough variety to let each and every employee find the right model. Your company is already well established? Then it’s time for a little forward planning. Meet a different kind of fleet: www.kia.com/eu/fleet

THE NEW KIA CEE’D SPORTSWAGON.EXCITEMENT. QUALITY. FLEET-ABILITY.

» 7-year warranty*

» From 4.2 l/100 km

» From 109 g CO2/km

» Trunk capacity up to 1,642 litres**

THE KIA FLEET. A GOOD REASON TOSTART A COMPANY.

P.13FLEET EUrOPE # 63

www.kia.com

* The Kia 7-year/150,000 km new car warranty. Valid in all EU member states (plus Norway, Switzerland, Iceland and Gibraltar), subject to local terms and conditions.** Maximum trunk capacity achieved by fully folded rear seats.Fuel consumption (l/100 km)/CO2 (g/km): urban from: 5.0/129 to 8.8/198, extra-urban from: 3.8/98 to 5.3/121, combined from: 4.2/109 to 6.6/146.

When setting up a company, there’s a lot to worry about. Finding the right company cars is no longer one of the problems. Kia offers entrepreneurs a perfect range of vehicles. Take a look at our new Kia cee’d Sportswagon: dynamic on the out-side, spacious on the inside, with low fuel consumption, high residual value and innovative technology backed up by a unique 7-year manufacturer warranty. Another perfect example of our choice of fleet models offering enough variety to let each and every employee find the right model. Your company is already well established? Then it’s time for a little forward planning. Meet a different kind of fleet: www.kia.com/eu/fleet

THE NEW KIA CEE’D SPORTSWAGON.EXCITEMENT. QUALITY. FLEET-ABILITY.

» 7-year warranty*

» From 4.2 l/100 km

» From 109 g CO2/km

» Trunk capacity up to 1,642 litres**

THE KIA FLEET. A GOOD REASON TOSTART A COMPANY.

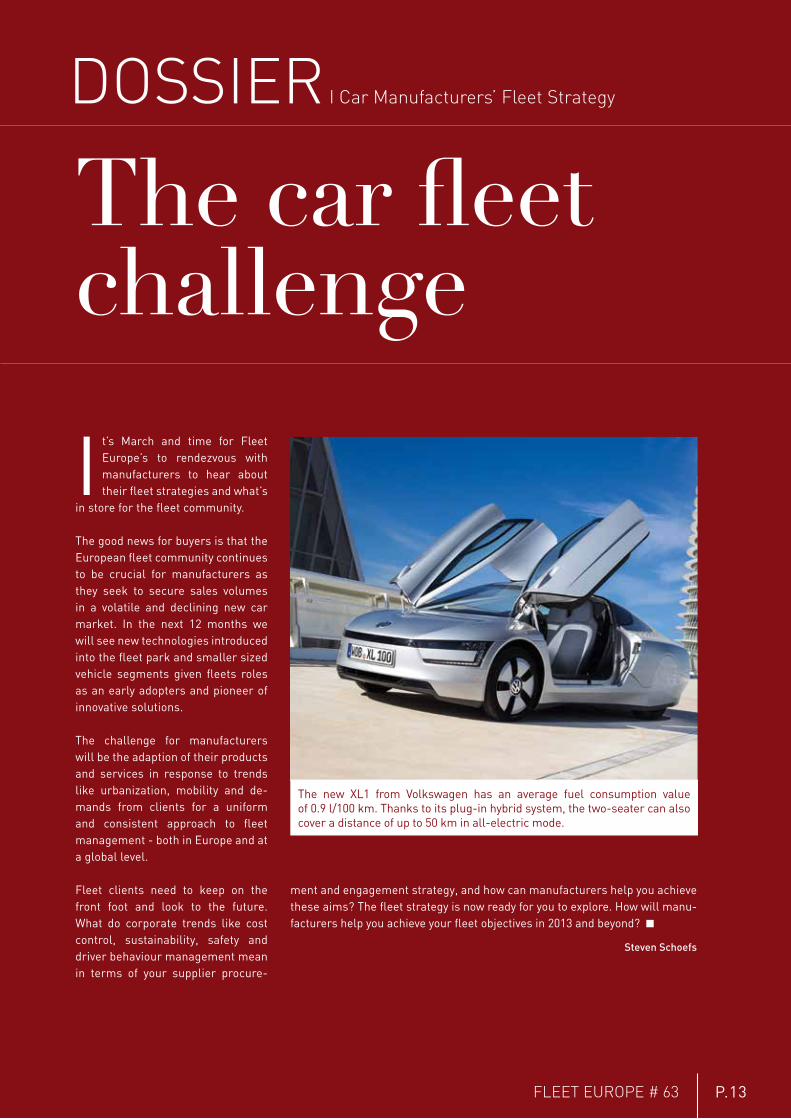

dOssiEr i car Manufacturers’ Fleet strategy

The car fleet challenge

It’s March and time for Fleet Europe’s to rendezvous with manufacturers to hear about their fleet strategies and what’s

in store for the fleet community.

The good news for buyers is that the European fleet community continues to be crucial for manufacturers as they seek to secure sales volumes in a volatile and declining new car market. In the next 12 months we will see new technologies introduced into the fleet park and smaller sized vehicle segments given fleets roles as an early adopters and pioneer of innovative solutions.

The challenge for manufacturers will be the adaption of their products and services in response to trends like urbanization, mobility and de-mands from clients for a uniform and consistent approach to fleet management - both in Europe and at a global level.

Fleet clients need to keep on the front foot and look to the future. What do corporate trends like cost control, sustainability, safety and driver behaviour management mean in terms of your supplier procure-

The new XL1 from Volkswagen has an average fuel consumption value of 0.9 l/100 km. Thanks to its plug-in hybrid system, the two-seater can also cover a distance of up to 50 km in all-electric mode.

Steven Schoefs

ment and engagement strategy, and how can manufacturers help you achieve these aims? The fleet strategy is now ready for you to explore. How will manu-facturers help you achieve your fleet objectives in 2013 and beyond? ■

P.14 FLEET EUROPE # 63

15.115.3 15.3

15.816.0

14.714.5

13.813.6

12.5

10

11

12

13

14

15

16

17

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Mill

ions

of

units

dOssiEr i car Manufacturers’ Fleet strategy

The ChangingBusiness Environmentthe whole dynamic of the motor industry, the relationships between the oeMs, their national sales companies, fleet operators and the economy has changed significantly in the past few years. no wonder that there is a whole new business scenario fleet executives have to come to terms with.

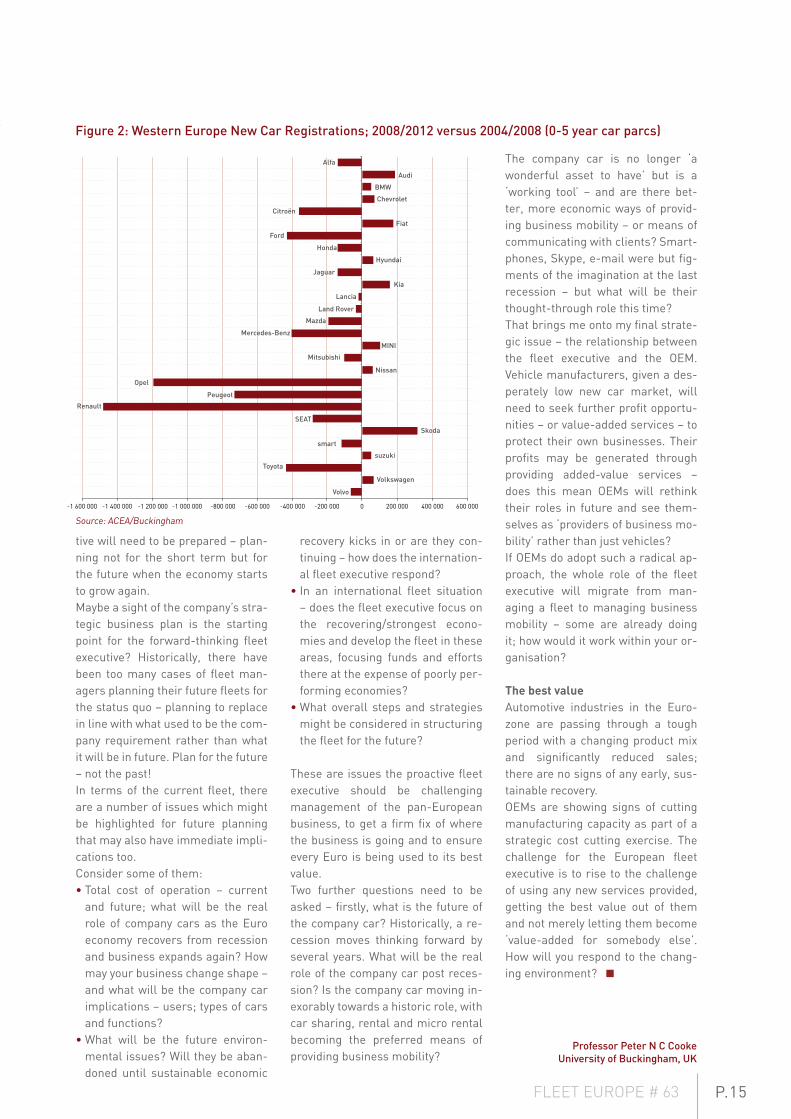

Across the EU new car sales have dropped by some three million units a year from the pre-banking crisis period of economic growth as shown in Figure 1. The decline in new car sales is but a part of the problem; the size of vehicles being sold has been polarising with larger and smaller cars taking precedence. To an OEM, seeking to build profit, this is the worst of both worlds as larger units offer significantly greater profit opportunities than smaller variants.As if that were not enough, the pre-ferred brands acquired in the EU have changed significantly over the past few years as shown in Figure 2. Thus, if a fleet operator has been running with a single brand for a

long period, just how popular is that marque today – and what are the im-plications of the move away by the overall market from that brand?Economic recession, or problems associated with the Euro have caused governments to take strong action to manage economies. As a result, there has been a steady move into a period of economic austerity across the region. In reality, new car sales have dropped in practically ev-ery market in the Eurozone.

a new Business order?Given such a sea change in market conditions, there are many other is-sues which might be raised. The Eu-ropean fleet executive, whether op-

erating in a single market or across the whole region, has a number of new and often fundamental issues they have to deal with.The rapidly changing market may be a mixed blessing. Given the huge excess installed manufacturing ca-pacity in Europe, there may be ex-ceptional deals available for new ve-hicles. However, these new units will be acquired to replace existing ones – just how good are used car prices and how well are they holding up?The used car message is as compli-cated as the new car scenario.If there is a shortage of younger used cars coming to market then, in theo-ry, these used cars might be expect-ed to achieve a good price. Yes, a fine argument – but how is demand for used cars holding? Many traditional new car buyers are either retaining their cars longer or buying younger used cars, or smaller new cars as economic hardship bites.There is an old business adage - ‘never waste a good recession’. Is this what is happening at present with organisations taking the op-portunity to reorganise business, clients, markets and product offer-ings as well as the way they do work – ready for the economic recovery? Any significant downsizing in the Eurozone may well call for reduced company size and new methods of doing business.It is against this slightly scary situ-ation that the European fleet execu-(Source: ACEA 2012)

Figure 1: European New Car Registrations (EFTA)

P.15FLEET EUROPE # 63

-1 600 000 -1 400 000 -1 200 000 -1 000 000 -800 000 -600 000 -400 000 -200 000 200 000 400 000 600 0000

Alfa

Audi

BMW

Chevrolet

Fiat

Citroën

Ford

Honda

Jaguar

Lancia

Land Rover

Mazda

MINI

Mercedes-Benz

Opel

Renault

SEAT

smart

Toyota

Volvo

suzuki

Volkswagen

Peugeot

Mitsubishi

Nissan

Skoda

Hyundai

Kia

Source: ACEA/Buckingham

Figure 2: Western Europe New Car Registrations; 2008/2012 versus 2004/2008 (0-5 year car parcs)

tive will need to be prepared – plan-ning not for the short term but for the future when the economy starts to grow again.Maybe a sight of the company’s stra-tegic business plan is the starting point for the forward-thinking fleet executive? Historically, there have been too many cases of fleet man-agers planning their future fleets for the status quo – planning to replace in line with what used to be the com-pany requirement rather than what it will be in future. Plan for the future – not the past!In terms of the current fleet, there are a number of issues which might be highlighted for future planning that may also have immediate impli-cations too. Consider some of them:• Total cost of operation – current

and future; what will be the real role of company cars as the Euro economy recovers from recession and business expands again? How may your business change shape – and what will be the company car implications – users; types of cars and functions?

• What will be the future environ-mental issues? Will they be aban-doned until sustainable economic

recovery kicks in or are they con-tinuing – how does the internation-al fleet executive respond?

• In an international fleet situation – does the fleet executive focus on the recovering/strongest econo-mies and develop the fleet in these areas, focusing funds and efforts there at the expense of poorly per-forming economies?

• What overall steps and strategies might be considered in structuring the fleet for the future?

These are issues the proactive fleet executive should be challenging management of the pan-European business, to get a firm fix of where the business is going and to ensure every Euro is being used to its best value. Two further questions need to be asked – firstly, what is the future of the company car? Historically, a re-cession moves thinking forward by several years. What will be the real role of the company car post reces-sion? Is the company car moving in-exorably towards a historic role, with car sharing, rental and micro rental becoming the preferred means of providing business mobility?

The company car is no longer ‘a wonderful asset to have’ but is a ‘working tool’ – and are there bet-ter, more economic ways of provid-ing business mobility – or means of communicating with clients? Smart-phones, Skype, e-mail were but fig-ments of the imagination at the last recession – but what will be their thought-through role this time?That brings me onto my final strate-gic issue – the relationship between the fleet executive and the OEM. Vehicle manufacturers, given a des-perately low new car market, will need to seek further profit opportu-nities – or value-added services – to protect their own businesses. Their profits may be generated through providing added-value services – does this mean OEMs will rethink their roles in future and see them-selves as ‘providers of business mo-bility’ rather than just vehicles?If OEMs do adopt such a radical ap-proach, the whole role of the fleet executive will migrate from man-aging a fleet to managing business mobility – some are already doing it; how would it work within your or-ganisation?

the best valueAutomotive industries in the Euro-zone are passing through a tough period with a changing product mix and significantly reduced sales; there are no signs of any early, sus-tainable recovery. OEMs are showing signs of cutting manufacturing capacity as part of a strategic cost cutting exercise. The challenge for the European fleet executive is to rise to the challenge of using any new services provided, getting the best value out of them and not merely letting them become ‘value-added for somebody else’. How will you respond to the chang-ing environment? ■

Professor Peter N C CookeUniversity of Buckingham, UK

P.16 FLEET EUROPE # 63

The race to own the mobility customer

You can compare the automo-tive and fleet business evolution with the evolution in the music business: Our desire to listen to music remains as strong as ever, but the way music is ac-cessed has changed dramati-cally. A similar development can be expected with professional mobility.

With increasing global urbanization, increased traffic vol-umes, more traffic jams and traffic accidents, we need to find a cleverer, safer and more comfortable ways of mov-ing from a to B. no single player holds a dominant position across the transport landscape today and is unlikely to do so in the future. the development of new Mobility con-cepts will force every major player - including oeMs - to work outside its core competency. ............................................................................

dOssiEr i car Manufacturers’ Fleet strategy

P.17FLEET EUROPE # 63

The music industry is a great exam-ple of how business models have evolved over time. For over 50 years people were thrilled to purchase vinyl of their favourite musician. About 30 years ago, vinyl started to be replaced by CDs, which offered better quality of sound. Roll on to the new century and the CD started to be replaced by MP3 players and internet downloads. What does this example tell us? Our desire to listen to music remains as strong as ever, but the way music is accessed has changed dramatical-ly. And the players in this field have changed in the last 20 years. A sim-ilar development can be expected with mobility. Our needs may remain broadly similar, but our behaviour and provision of solutions that will meet de-mand will change.

the age of mobilityparticipantsNo one will argue that megacities in developed economies – like Amster-dam, London, Paris or Vi-enna in Europe – are the largest markets for mobil-ity services, but the mobili-ty needs and behaviours of people in these cities is changing. There are significant changes in the way that people are managing their time. Rising population densities in many regions of this globe, an in-creasing share of inhabitants in older age groups and connection via the in-ternet are changing how people be-have and value their time. Shopping in physical stores is re-placed by virtual shopping and, in turn, stores on the high street are be-coming more of a showroom than a place for a purchasing. The increased usage of the Smartphone will contin-ue to change our behaviours – and not just in megacities. The delivery of goods will be handled differently and require more localised transport than in the past.Further, to avoid congestion and traffic accidents, mobility – wheth-

er individual or public – needs to be organized in a much better way than in the last 127 years (since the pro-motion of the first car , the Benz Pat-ent Motorwagen in 1886). A radical change of urban mobility could mean the following: Individual cars are no longer allowed in cities – only public transportation and vehicles for the transport of merchandise and goods. A significant reduction of emissions, congestion and traffic accidents could be the outcome. The individ-ual’s mobility needs could be met through integrated car sharing or car pooling program. The number of cars in a city would be limited to the mobility needs of its inhabitants. This

could decrease the level of idle cars. This may appear too far removed from how we view mobility today. However the attractiveness of cities is determined by many different fac-tors – availability of affordable apart-ments, environmental considerations and infrastructure - which include the offerings of convenient travel op-tions like subways or buses. Over the last decade, many cities have begun to find ways to reduce traffic in cities – either by congestion charges, limitations of new car reg-istrations or reductions of parking space. In the future, individual mo-bility in Cities may only be allowed by motorbikes, bikes or electric cars. In addition, people who are living and working in megacities may want to have access to different mobility of-ferings with one access and payment system, like an Intermodal Mobility

App via a smartphone with payment per usage or even more aggressive at a flat rate or finally for free.This may sound unrealistic. But look at the music example – the music may have even not changed, but the way to access music and those who are providing the access to the music has. In our case, the car represents the music and the discs and/or the internet download functions repre-sent an access channel like an Urban Mobility Concept.With an ageing society and an in-creasing share of inhabitants in high-er age groups, the question must be asked whether this automatically im-plies future decline of motorization

and mobility. After all, the in-creasing share of older citizens in society will mean a higher average age of mobility partici-pants.Car fleets will be more than hardwareIt is agreed by almost all stake-holders that there is a major challenge for all mobility stake-holders - whether OEMs, sup-pliers, cities, public transport provider, rental companies etc - to identify mobility solutions

and mobile usage concepts which will satisfy future customer de-mands. Further individual car owner-ship may no longer be necessary to consume mobility, and a car may no longer be seen as the status symbol it once was.Possible new mobility demands could also change the relationship with the car. The car could become a place of entertainment and not driving with, a focus on entertainment and commu-nications functions, infotainment & networking.Under such a scenario, only mobility service providers who are able to offer solutions which fit to the changing be-haviour of customers will be relevant.There is no doubt that the mobility spend by person will increase over the next few years – either driven by increased taxation or increased transportation costs (i.e. gasoline

Rental companies could be first to cover the new automotive and mobility market with flexible and efficient usage concepts

P.18 FLEET EUROPE # 63

Automotive industry needs to adopt a service-centric approach to meet shifting mobility preferences

Product configurationand design

Regulatory mandates• Adopt alternative zero-emission powertrain technologies• Develop more fuel-efficient conventional powertrains• Standardize advanced safety and emergency response technologies

Enhanced fuel efficiency• Standardization of engine technologies• Light weight construction

Enhanced safety• ABS, EBD, TPMS• Driving assist applications• Collision avoidance systems

Powertrain electrification• Electric vehicles, hybrids, hydrogen fuel cells• Charging stations

Small and smarter cars• Building cars around cities• More head and leg room• Remote access

Car sharing/leasing• On-demand vehicle access• User created routes and stops• Short-term hire or leasing

Mobility solutions• Option to choose vehicle class as per need/occasion• Linkages with public transport

On-board telematics• Navigation and traffic systems• Web connectivity• Voice recognition technology

Integrated packages• Service, maintenance, insurance, road-side assistance, accidental repair

Shift in personal mobility preferences• Owning personal cars losing attractiveness • Alternate personal mobility solutions gaining competitive strength• Optimized purchase and running cost budgets are becoming more important• Need to stay connected – always and everywhere

Scope of services

Automotive OEMs are transforming their business models to defend leadership in personal mobility market

Value chainimplications / impact

Triggers / factors New value proposition

prices). There may be less people across Europe who can afford to own a car, but they will, in turn, be seeking alter-native mobility options such as car sharing, car pooling or intermodal packages. Under these circumstances, car fleets may become more relevant than in the past; but only if the car fleet product is much broader than just offering “hardware and hardware related services” for a fixed monthly rate. The customer of car fleets (employer) and the end-user (employee) of the fleet products are demanding new offerings like car pool-ing and integrated mobility concepts. This requires more flexible product/service offerings than in the past. Short term rentals like car sharing, combined mobility packages together with long distance train tickets, pre-ferred parking at airports etc. are adding value to custom-ers. To gain a higher share in the total mobility spend of customers is the ultimate goal for any stakeholder in the future mobility market – especially for OEMs.Therefore, car manufacturers must give top priority to the analysis of markets, trends and the competitive situation, with regards to potential future fields of competition.

Potentially serious competition in this field is likely to come from car rental companies. First of all, the concept is threatening their market and secondly, car rental compa-nies have already established global distribution networks across brands, which provide value to their customers. If mobility continues to gain in relevance and the importance of ownership of an automobile continues to lose its impor-tance, rental companies could be first to cover the market with flexible and efficient usage concepts. Automotive manufacturers thus face the challenge to quickly counteract such developments, which requires a dramatic change in their future business model – mov-ing from a premium car maker to a provider of premium mobility services – especially on B2B car fleet business, which will be a key area for corporations to manage their cost base and to become more attractive to employees in providing smart mobility services as a fringe benefit. ■

Peter FuβSenior Advisory Partner Automotive Ernst & Young,

Frankfurt-Germany

P.19FLEET EUROPE # 63

Tame your righT fooT.

The new InsIgnIa BiTurBo

www.opel.com/insignia

Official fuel consumption urban 8.6–6.1 l/100 km, extra-urban 5.4–4.2 l/100 km, combined 6.6–4.9 l/100 km; CO2 emissions combined 174–129 g/km (according to R (EC) No. 715/2007). Efficiency classes C–A

The best car we’ve ever built.now with the powerful and frugal BiTurbo diesel engine.400 nm. 230 km/h. With 4.9 l consumption.

12_SF_in_BiTurbo_Fleetworld_A4.indd 1 17.04.12 12:12

P.20 FLEET EUROPE # 63

dOssiEr i car Manufacturers’ Fleet strategy

B2B is key area for OEM growth

Fiat group automobilesInteRnatIonaL FLeet pRoSpect contact

Francesco Monaco, EMEA Region - Head of International Key Account Managers

car manufacturers’ strategy For FGA the fleet channel is a strategic asset. The fleet business generates high visibility inside private com-panies and public organizations. And the business cus-tomer – by word of mouth – can turn into a voluntary ambassador of the brand he is using towards relatives, friends and colleagues. The most important priorities in terms of fleet development and sales ambitions in 2013 inside Europe are Italy of course, as Fiat is the na-tional manufacturer and leader in the country. Outside Italy, the UK and Germany are important, both for the dimensions of the market and the huge opportunities of products. On top of these come France and the Neth-erlands: in these markets there is a high awareness for ecological issues, so also their legislation is pushing the private and corporate market versus ecological prod-ucts, where FGA is leader. The fleet business is grow-ing noticeably all over the world and the Fiat Group with its organizational structure of four operating regions – NAFTA (U.S., Canada and Mexico), LATAM (Central and South America), APAC (Asia Pacific) and EMEA (Europe, the Middle East and Africa), is able to serve customers everywhere in the world.

Strategy towards fleet clients Each individual market has its own local structure in or-der to handle fleet demand at a national level and to be as close as possible to the customer. On top of this are two other structures: on the one hand the ‘International Key Account Management’ with five International Key Account Managers (one specialized in LCV) – this team being dedicated to corporate customers at an interna-tional level. And on the other hand the ‘LTR Internation-al’ team which is the reference for long term rentals companies’ headquarters and for international tenders.

opeL vauXhaLLInteRnatIonaL FLeet pRoSpect contact

Juan Manuel Sagardoy grawe, Director European Corporate [email protected]

car manufacturers’ strategy For 2013, Opel/Vauxhall is preparing to launch a new prod-uct offensive with new vehicles in new segments, allied to major changes in the powertrain portfolio. With new products and state-of-the-art comfort and assistance sys-tems normally found only in higher vehicle classes Opel/Vauxhall intends to give customers what they want, and to maintain the fast pace of vehicle and technology introduc-tions. The new vehicles to be launched in 2013 include the Adam and the Cascada. Fleet continues to be of strategic importance for Opel/Vauxhall, and for 2013 the company will continue the strategy of improving vehicle residual values, increasing corporate and user-chooser penetra-tion and focusing more on SMEs. Opel/Vauxhall continues to address the traditional big Western European fleet mar-kets, but also sees huge opportunities to develop more in Eastern Europe, especially in Russia and Turkey, as well as in Central and Eastern Europe.

Strategy towards fleet clients To meet the growing demands of European and global fleet customers, Opel/Vauxhall has a pan-European Corporate Account team. Its team of dedicated Corporate Account Managers is based in different European regions (e.g. Ger-many, the UK, Hungary, Belgium and the Netherlands).Whenever a new prospect is interested in a pan-Europe-an or global agreement this international team of fleet professionals will support the customer with its expertise and provide consulting on how the customer can derive the most benefit from the agreement. Opel/Vauxhall has a dealer network of more than 3,750 distributor sites across Europe. The repairer network coverage in Europe of close to 6,500 sites provides customers with the peace of mind that is so vital to their business operations.

In order to give an overview of what the major car manufacturers are expecting to see in 2013, and how they are approach-ing the vital fleet market and its clients, we asked them to outline their views and policies. It is clear that globalization is a reality, and also that despite challenging times, optimism is still there.

P.21FLEET EUROPE # 63

volkswagen groupInteRnatIonaL FLeet pRoSpect contact

Ralf Kostrewa, Head of Volkswagen Group Fleet International

car manufacturers’ strategy The fleet domain is of huge importance to Volkswagen Group, as can be seen in the volumes ordered by large cus-tomers. Large customers also play an important role for the company in oth-er ways. They are traditionally the first to take new technologies on board and the feedback received from these pro-fessional users is used in the develop-ment process for vehicles. Volkswagen Group believes the Western European market will remain challenging but despite this is expecting to see positive progress due to its balanced product portfolio. And while Europe has tra-ditionally been more important for fleets, Volkswagen will also be con-centrating on emerging markets, both areas of business being of importance to the company. There will in particular be a commitment to Brazil, China and Russia. In model terms, in the United States, Volkswagen expects the new Passat to be successful in the fleet domain. Other new models include the Audi A3 Sportback, the SEAT Leon which will also be seen in Combi Ver-sion. Škoda is to have a new version of its best selling Octavia in both sedan and Kombi. And the new Golf is expect-ed to remain as Europe’s best selling fleet car.

Strategy towards fleet clients The Volkswagen Group – through Volkswagen Group Fleet Internation-al – manages large multinationals in cooperation with its importer network. Within Volkswagen Group Fleet Inter-national each customer has a central contact (Key Account Manager) for all international fleet demands. As back office to the Key Account Manager a team of tender coordinators and con-tract managers supports their daily activities. With the International Bonus Agreement (IBA) customers are fur-ther motivated to take on Volkswagen vehicles. An IBA is available to com-panies with at least 2,500 vehicles and which order at least 300 cars annually in more than three countries.

Jaguar Land RoverInteRnatIonaL FLeet pRoSpect contact

Simon Dransfield, General Manager, Corporate Sales Europe

car manufacturers’ strategy Corporate fleet sales represent an extremely important area for Jaguar Land Rover, which is seeing con-tinued investment. New models are being developed with the corporate customer in mind. The company has a focus on reducing CO2 emissions fur-ther, and identifying what the corpo-rate customer wants and needs from a vehicle. Sales growth in 2012 was in excess of 35% for Jaguar Land Rover as many of the SME fleets adopted the Range Rover Evoque and the Jaguar XF 2.2 litre diesel. The UK is the most mature fleet market. Jaguar Land Rover is focusing on key accounts and leasing and is supporting investment by the dealer network to target the SME market. Germany has a signif-icant wagon market where the new Jaguar XF Sportbrake has recently been launched. Italy is Europe’s larg-est Land Rover market and, despite difficult economic conditions, the company has a healthy order bank for Range Rover Evoque and an increase in segment performance for all mod-els. Benelux, France and Spain form the next tier of markets where there are investment and growth opportuni-ties in Corporate Sales. China is now Jaguar Land Rover’s leading market.

Strategy towards fleet clients Research and development has en-abled lower CO2 emission vehicles. The Range Rover Evoque, Jaguar XF and XF Sportbrake are all designed to be more competitive in the fleet world. Jaguar Land Rover has a strong, and growing corporate sales network across Europe, developing fleet spe-cialists within dealerships. The com-pany has an established fleet team in each of the European NSC’s. The in-ternational account relationship is led by the customers ‘home’ market. The European and global team will then support a coordinated response to the client.

InfinitiInteRnatIonaL FLeet pRoSpect contact

carlos Montenegro, Corporate Sales Director [email protected]

car manufacturers’ strategy Corporate sales represent a key topic for Infiniti. The premium car segment is very focused on business channels. The deterioration of the private chan-nel due to the economic situation is making fleet the key channel. This is also reflected in Infiniti’s product port-folio with the introduction last year of the Infiniti M Business edition and the upcoming Q50 that has all the key fea-tures to be successful with corporate fleet operators. International fleet sales represent 3- 5% of overall sales. The range has transformed rapidly from a 100% petrol V6-V8 line up with reduced fleet presence (90% private sales until 2010) to diesel V6 engines, and fleet sales reached 40% in 2011 and 55% 2012, with a forecast of 65% in 2013. The new Infiniti Q50 will com-pete in a core fleet segment with a car that perfectly fits the European fleet market needs; very efficient diesel engine, best in class CO2 and business versions. With this, Infiniti anticipates sales growth in all European markets.

Strategy towards fleet clients There is a growing interest from inter-national customers to move towards global contracts and not remain only with a European scope only. In this sense, Infiniti, as the luxury brand of the Renault-Nissan Alliance, is per-fectly prepared to play this global role for all international customers. The Infiniti fleet structure is in con-stant development and aligned to the overall growth plan of the company in Europe. Currently the European fleet structure is based in France and oversees the European area with fleet managers based in the G5 countries that cover all the Infiniti markets in Europe. Each fleet manager develops the fleet business in the countries he is responsible for and also channels any international fleet demand to cen-tral operations.

P.22 FLEET EUROPE # 63

DaimlerInteRnatIonaL FLeet pRoSpect contact

andre Dutkowski, Manager Coordination International Key Account Management & Leasing

car manufacturers’ strategy Europe is and will remain one of the big-gest automobile markets in the world and will continue to play a key role in the development of new technologies. The factors driving environmental performance and mobility are devel-oped in Europe, and Mercedes-Benz’s technological knowledge and R&D will remain in Europe. With its new compact cars, the OEM plans to fur-ther open up the Eastern European market. Mercedes-Benz is optimistic concerning the development of fleet sales in 2013. With the first complete year of the new A-Class as well as the launch of the new E-Class, a new CLA and a new S-Class the manufacturer offers a highly attractive portfolio to its fleet customers. Mercedes-Benz sees high potential for the Chinese premi-um market in the mid and long terms, and also expects to further boost sales in the US. In December 2012 Daimler AG appointed a new member of the board, responsible for China. The Mer-cedes-Benz International Corporate Sales Team works in close collabo-ration with the colleagues for Mer-cedes-Benz USA and Mercedes-Benz Canada.

Strategy towards fleet clients The Mercedes-Benz International Cor-porate Sales Team offers ‘one-stop shopping’ for large, multinational companies. The manufacturer offers a well-developed infrastructure with market-centric fleet programs in all major countries catering to fleets of all sizes. The international team requests offers and conditions from all involved markets. These are consolidated at the ‘Fleet Floor’ through an integrated approach by Corporate Sales, Daim-ler Financial Services and Global Ser-vices and Parts to provide a customer specific solution or offer. International Framework Agreements (IFA’s) guar-antee worldwide availability. Today, Mercedes-Benz has around 280 such agreements. This has grown from 50 just five years ago.

pSa peugeot citroënInteRnatIonaL FLeet pRoSpect contact

hugues de Laage de Meux, head of International Key Account Sales

car manufacturers’ strategy B2B has become more and more strategic, because it is quite a stable market compared to B2C. In 2012, the B2B sales represented 31% of global PSA sales. Around 38% of global sales are outside Europe, and in B2B terms it is more than 20%. The forecast in Europe is to stay at the same level of market share (15.6%) in B2B. At this point, the objective is to sell around 200,000 cars in B2B overseas. PSA’s priorities in Europe are Germany, the United Kingdom and France. The Southern European markets are fac-ing a very difficult situation. PSA Peu-geot Citroën has an international ap-proach focus on certain markets this year: Russia, China, Turkey and Latin America. In 2013 the group expects a more dynamic market in Eastern Eu-rope and Scandinavia but a volume decrease in Western and Southern Europe. There is an overseas growth strategy (with specific products (Peu-geot 301, Citroën C-Elysee and Citroën C4 L) and a more defensive strategy in Europe during the first half. However, the second semester will see a more offensive phase with the launch of the new Citroën C4 Picasso and the Peu-geot 2008, then the new Peugeot 308 at the end of the year

Strategy towards fleet clients The PSA Corporate Solution organi-sation is customer oriented with an International Key Account Managers (IKAM) team and, in all countries, the National Key Account Managers (NKAM). There are also Leasers Key Account Managers and Citroën Busi-ness Centers and Peugeot Profes-sional Centers in all countries. The operational teams are in the field to help customers and provide all ser-vices according to their needs. The PSA target is to develop business at an international level with a focus on more than 150 Key Account custom-ers (more than 1,000 vehicles in at least 3 countries).

RenaultInteRnatIonaL FLeet pRoSpect contact

emmanuel LongeaRD, Sales Director Corporate Sales Division

car manufacturers’ strategy Corporate fleet sales have always been strategic for Renault. Over 140 multi-national companies around the world already turn to Renault to implement their international car policies. There will be extended volumes and country fleet organizations in 2013. The B2B sales level represents around 30% of all sales. In 2012 there has been strong fleet development in countries or regions such as Latin America, Russia, and Euromed-Africa. Renault will focus on the European fleet mar-kets, whose sales represent around 65% of fleet sales: not only the ‘big 5’ but also for example the Netherlands and Belgium, which offer good sales opportunities in key accounts and the local fleet business. Renault will also pursue the fleet structure develop-ment in countries outside Europe, so as to answer efficiently to corporate and local fleet customer needs and contribute to the effective implemen-tation of international agreements. For 2013, the manufacturer expects to see the development of new fleet opportunities (especially in Asia-Pa-cific). In Europe, thanks to new Captur and new Clio models, it intends to de-velop market share in 2013, which will be also linked to market evolution. The Alliance is developing new com-mon international contracts which will contribute to sales increase.

Strategy towards fleet clients The structure is designed to serve large international clients, with 9 In-ternational Key Accounts Managers (IKAMs) at international level, 3 Fleet Regional Managers dedicated to sales development in and outside Europe and over 100 Key Account Managers (KAMs) at national level. There are also fleet teams in the Renault net-work at local level. International fleet customers obtain the positive eco-nomic benefit and simplicity of global one-stop negotiation, while the Key Account Managers work directly with the customer subsidiaries.

P.23FLEET EUROPE # 63

toyotaInteRnatIonaL FLeet pRoSpect contact

International Key Account Managers: tine poels, emrah [email protected]

car manufacturers’ strategy In 2012 Toyota Motor Europe (TME) achieved a 2% sales increase. The market share increase was a balanced re-sult of both retail and fleet sales. The target is sustainable growth in retail and corporate fleet business with a focus on fleet customers benefiting from the competitive TCO. Important contributors to growth were the built-in-France Toyota Yaris with sales up of 27% thanks to the strong launch of the Yaris Hybrid and the Toyota Camry with sales up 68%, a segment-leader in Russia and the Ukraine. Toy-ota also expects to benefit from the growing success of its full hybrid range with sales up 29% and exceeding 100,000 units sold in a year for the first time in Europe. In 2013 Toyota sales are expected to further increase in fleet and retail thanks to a product offensive in the crucial C- seg-ment with the introduction of the new Auris, Auris Touring Sports, the new Verso, and the fourth generation RAV 4.

Strategy towards fleet clients The TME fleet division includes IKAMs (International Key Account Managers) and 1 back-office support. The IKAMs follow up international clients based on the client fleet rep-resentatives’ country. The IKAMs act as the single point-of-contact and will provide the client with a consolidated European proposal. TME has an on-going agreement with all its NMSCs for 56 countries in Europe (including Russia, Turkey, Israel). For RFPs that hold specific, non-standard requests, the IKAM will secure with the relevant NMSC an appropriate local solution is provided. TME will further strengthen the IKAM team with additional headcount mid 2013.

Car manufacturers are developing new fleet services to enhance the connectivity with the fleet driver.

volvo carsInteRnatIonaL FLeet pRoSpect contact

Javier vazquez, Global Accounts [email protected]

car manufacturers’ strategy Corporate and fleet sales are vital for Volvo Cars, account-ing for over 35% of global volume. In Europe, the share exceeds 50% in many markets. This year Volvo is review-ing its fleet business around the world, starting with its 15 largest markets. It has established a new Global Fleet Op-erations function based in Gothenburg and will be work-ing with markets to understand the opportunities, finding ways to better support them in delivering excellence to fleet customers and drivers. This global view enables Vol-vo to offer help and advice to customers looking outside of the traditional European markets. Volvo expects to contin-ue to grow market and segment share in key EU markets. Last year, with the launch of the V40, the company saw all time record market shares in some markets. It ex-pects to continue this trend with further product launches throughout the year. Outside of Europe, Volvo anticipates growth in the US and Asia during 2013 and recently signifi-cantly expanded its fleet organisation in China to support international clients in that region.

Strategy towards fleet clients Volvo has a global account team at a corporate level. It has regular live meetings and has commenced workshops to ensure sharing best practice towards international cus-tomers. There are dedicated fleet managers in all EU mar-kets serving both international and national fleet clients. Volvo has over 110 international agreements with implan-tation in all regions of the world. The company is aiming at being closer to customers by understanding their needs and motivations and delivering excellence.

P.24 FLEET EUROPE # 63

nissanInteRnatIonaL FLeet pRoSpect contact

emmanuel Bussiere, International Fleet Sales [email protected]

car manufacturers’ strategy Corporate sales represent a key pillar of Nissan strategy for growth in 2013 and for the coming years. At Nissan, mid term planned sales growth is coming from the introduction of new models but also through the sales increase towards fleet customers. In 2013 Nissan expects to grow Europe-an sales in the UK, France, Germany, Russia, the Nordics, the Benelux and Poland. To answer to customer needs and to make them benefit from Nis-san’s global presence in the world it has developed a global approach to International Key Customers. The In-ternational Key Account team is work-ing with every Nissan Local Corporate Sales department. The manufacturer is in a position to offer to all Global Key Accounts a single contact person within the organisation.

Strategy towards fleet clients Nissan’s team of Fleet Specialists is composed of 5 people. There are one International fleet Sales Manager, two International Key Accounts managers in charge of developing internation-al sales, two back office in charge of customer follow up, call for tender and international relationships.Nissan only started to develop inter-national fleet sales agreements in 2012, and now has 20 international fleet agreements signed, including world contract and solus. Although relatively new to this domain, the re-ception from global companies has been exceptional. A main asset is world presence, a strong M/S posi-tion in most of the important mar-kets, products developed locally for local needs, local production helping Nissan to react quickly to customer orders and the flexibility of the cor-porate sales team across the world to support all international customers specific requirements.

KIaInteRnatIonaL FLeet pRoSpect contact chan uk Jun, Manager Fleet and Remarketing

car manufacturers’ strategy Growing fleet sales is on top of Kia’s strategic agenda. Long term fleet sales have increased by more than 30% over recent years. To become one of the 10 mainstream brands in Europe, Kia will grow the fleet mar-kets share more strongly than the retail share. In 2012 the share of fleet sales was 38% of total sales in 14 Kia subsidiary markets. Overall market share in Europe was 2.7% in the passenger car market, increas-ing sales by 17% over 2011. The 2012 sales result was an increase of 17% compared to 2011. Kia expects to con-tinue to ‘buck the trend’ in recording positive sales growth in 2013. Kia’s most remarkable sales growth was in Italy, where it experienced a 30% increase in sales. It also grew 27% in Germany, 24% in the UK and 20 % in Ireland. Its 2012 performance con-tinues a long-term trend: over the past four years Kia has recorded growth of 50% in the European market. In Ger-many and Italy Kia still has a huge op-portunity in the SME segment.

Strategy towards fleet clients Kia has dedicated Key Account Man-agers at European level coordinating international tenders and the rela-tionship with the major leasing com-panies. It has white label partnerships with leasing companies in more than 10 countries. Markets have had a pro-fessional national fleet organisation for several years to cope with large customer demand. The manufacturer offers a strong focus on managing re-sidual values and service costs, while offering a 7 year manufacturer war-ranty.

Tim Harrup & Steven Schoefs

BMW groupInteRnatIonaL FLeet pRoSpect contact

astrid Schneider, Prospective Customer [email protected]

car manufacturers’ strategy Corporate Sales represent an import-ant sales channel for the BMW Group, not only in mature European Markets but also globally. Over recent years the company has seen constant and steady growth in fleet sales for both BMW and Mini. This development is thanks to corporate customers who recognize and reward BMW Group’s efforts in terms of sustainability not only with regard to automobiles but also with regard to the whole supply chain starting from R&D up to pro-duction and ultimately recycling. In the fleet industry a clear commitment to sustainability combined with a fo-cus on TCO has become increasingly important in customers’ fleet policies. BMW Group corporate customers val-ue the combination of fuel efficiency and driving pleasure offered through BMW Efficient Dynamics and ‘mini-malism’ technology. The BMW Group has been named the world’s most sustainable automotive company for the eighth consecutive year in the ranking published by the SAM Group for the Dow Jones Sustainability In-dexes (DJSI).

Strategy towards fleet clients BMW International Corporate Sales provides companies with a global point of contact The team of Interna-tional Key Account Managers helps customers to set up business rela-tions with the global network of sub-sidiaries and dealers, and optimize fleet operations. Within their mar-ket / region specific responsibilities the Key Account Managers ensure a smoothly running relationship to lay the foundation for successful long-term cooperation. Whenever possible, International Key Account Managers will visit international customers to-gether with the national Key Account Manager. ■

Decision time for fleet managers 7 reasons why you shoulD consiDer Kia.

We would like you to meet a fleet designed to match your needs. A complete model range that will satisfy the employees and

even the CFO. A fleet that is as unique in terms of its model line-up as it is in terms of its service approach. A fleet focused on

design and quality, aligned to value for money. A fleet that will give you peace of mind for at least 7 years. And these are not

just all promises. They are the commitments and key objectives of one of the fastest-growing mainstream brands in Europe.

A brand that renewed its entire product range within 24 months, with new product launches in the A, B, C, C-MPV and D segments.

1 High value

When it comes to residual value

(RV), you will hardly find a fleet

that performs better. Purchasing a

Kia is the best choice you can make,

thanks to our competitive prices and

high RVs. On top of that, we are also

able to provide you with 5 to 10%

more value than our competitors in

terms of equipment and technology.

2 Low emissions and

low fuel consumption

We do more than just meet

industry standards. Eco-friendliness

for us is a long-term company strat-

egy. By providing the latest fuel-saving

technologies, Kia is, on average, overall

one of the best in terms of CO2 emis-

sions. The Kia Rio with its 85 g/km is

a perfect example. Your fleet will thus

be both friendly to the environment

and your budget, because low fuel

consumption and emission rates will

result in tax benefits in many countries.

3Low maintenance costs

Our excellent product quality,

durable parts and constant

product improvements show how it

is possible to further reduce operating

costs. Service intervals of up to 2 years/

30,000 km have already been imple-

mented in most of our models with

diesel engines. And the cost of insur-

ance for every Kia model is highly

competitive.

4Made in Europe

The modern car and engine

manufacturing plant in Žilina,

Slovakia, fulfils our commitment to

exceptional quality. Here, we have set

new standards for vehicle quality and

productivity, and achieved a level of

product quality that gives us the reas-

surance to provide each and every Kia

with a 7-year industry-leading manu-

facturer’s warranty.

5A design that inspires

Thanks to our European Design

Centre, our cars are fresh and

bold, and could not be mistaken

for anything other than a Kia. The

Kia cee’d Sportswagon is an excellent

example of our design philosophy.

Because of our outstanding product

design, we are actually one of the main

winners in the first-ever Automotive

Brand Contest and are ranked “Best of

the Best” in the Brand Design category.

6Global brand

Kia Motors is a modern, dynamic

and enthusiastic company with a

strong focus on quality and design. We

are one of the fastest-growing inter-

national carmakers, with over 47,000

employees across the globe. We are

one of the world’s five largest car

manufacturers. Over 2.5 million

Kia vehicles a year are produced in

15 manufacturing plants and sold in

149 countries around the world.

7 The Kia 7-year warranty

An industry-leading and unique

7-year/150,000 km manufac-

turer’s warranty, which supports our

entire model range

and offers peace

of mind for fleet

managers.

Do you need a model portfolio that

meets all kinds of functional needs

plus the expectations of user-

choosers? all things considered, we

are offering you forward-looking

and inspiring new fleet models with

superior levels of quality and design,

and a very special team behind it.

feel free to test us!

meet a different kind of fleet at www.kia.com/eu/fleet

advertisement

the new Kia cee’D sportswagon.ExCiTEMEnT. QuAliTY. FlEET-ABiliTY.

P.26 FLEET EUROPE # 63

What OEMs can do to help reduce TCOonce the vehicle is on the road it is not out of the fleet manager’s mind. the use phase accounts for the greatest impacts in terms of costs, as well as fleet safety considerations and environmental performance. What are oeM’s doing to help fleet managers in this critical area?

dOssiEr i car Manufacturers’ Fleet strategy

Choosing the right vehicles and implementing a best in class fleet strategy are two of the ‘big’ three factors that lead to best practice fleet management. The third and perhaps the most

challenging area of optimisation is the creation of a cul-ture where driver behaviour is aligned with fleet manage-ment priorities. Drivers are human beings and changing human behaviour is perhaps the ultimate challenge.

Supporting behavioural changeWhen choosing an OEM a fleet manager needs to appraise more than the vehicle specifications or the maintenance offered in the garage, but how the OEM will support op-timisation on the road. An OEM in today’s fleet world is more than simply a provider of vehicles.

the driver is the keyThe driver is the key to the optimisation. Once the vehicle is on the road the best planned fleet management prac-tices are dependent on how a driver responds to them. The challenge for a fleet manager is two fold. Firstly, find-ing effective ways to engage with and then raise aware-ness amongst drivers of their role in fleet optimisation, and secondly communicating with drivers to achieve the behavioural changes that are desired.

Raising awarenessAwareness is the first step on the ladder of change. Once there is awareness of a particular issue or risk a discus-sion can ensue on whether a response is necessary and who should take the lead in attempting to change be-haviour.OEM’s are supporting fleet managers build knowledge and raise awareness in three key areas (i) Before the Tip (ii) During the trip (iii) After the trip.

Before the trip – the right choice of vehicleOEM’s are designing vehicles that result in optimised per-formance with no action from the driver. Toyota told Fleet Europe that research and development in the design of a vehicle, so that it intelligently and intuitively support drivers, is a critical success factor for a progressive OEM. The first step of optimising performance therefore, is the domain of the fleet specialist and in the procurement of vehicles. The culture of the fleet programme will influ-ence how drivers use and maintain a vehicle. By commu-nicating this through a procurement strategy a driver will be encouraged to behave in a particular manner.

Before the trip – educating the driverThe cost of fuel is a constant challenge. Educating the driver about improved driving styles, safety and well-being is moving up the agenda because of the need to manage fuel. Mercedes-Benz is one of a number of OEMs offering support. Drivers participating in its EcoTrain-ing programme learn how to drive efficiency and results show up to 15% reduction in fuel consumption can be achieved. PSA Peugeot Citroën also offers training and explains that better driver behaviour also reduces main-tenance impacts and costs, as well as reducing driver stress-levels. Renault’s DrivingEco2 programme offers similar opportunities and its risk assessment profiling helps identify drivers that are in need of support based on pre-selected criteria. By risk profiling fleet managers can prioritise areas of action. This systematic approach enables metrics to be created that measure performance and evidence the benefit of changed behaviours.

Before and during the trip: planningAs the car becomes increasingly connected more tools and features will enter the market to aid route optimisa-

P.27FLEET EUROPE # 63

What OEMs can do to help reduce TCO

tion and in use driver performance, and OEMs will be deploying these to show differentiation from competi-tors and increase potential revenue opportunities.Volvo explained that telematics, HMI and the connected car will deliver an improved driver experience as well as reduce accidents and risks for fleet managers. The on-going enhancements to its Sensus driver interface provide drivers with intui-tive navigation advice and access to support and information helps driv-ers ‘do the right thing’.

During and after the tripTelematics offers granular big data like never before. Tools like GPS trackers and OEM vehicle manage-ment systems can be configured to highlight risks and opportunities – and estimate the potential return of changing behaviour. Renaults Fleet Assessment Management Service enables real-time management of fleets, providing daily updates on up

to 60 different areas of information like the daily distance travelled, en-ergy consumption and, in the case of EV, battery updates.The information on vehicle use is not just available for the fleet manager- perhaps seen by some drivers as a

big brother in the sky that is ready to pounce on poor behaviour. Telemat-ics puts the information in the hands and at the feet of a driver in real time or post travel allowing them to re-view their own performance.

Fiat eco:Drive system analyses how the vehicle is being driven in real time and enables a driver to review his or her own performance. Jaguar Land Rover advanced safety features such as emergency brake assist and dynamic stability control through to tyre pressure monitoring, are exam-ples of how OEM are automatically helping the driver and educating the driver when an action is required to improve vehicles performance.

creating the changeyou want to seeSuccessful behavioural change means getting to know your drivers, how they react in certain situations and being supportive. The tools, fea-tures and resources offered by OEM can help fleet managers get to know their drivers – and from this change can happen. ■

Successful behavioural change means getting to know your drivers, and being supportive.

Tim Harrup

Educating the driver about

improved driving styles, safety

and wellbeing is moving up the fleet manager’s

agenda

Think Again.

Fuel consumption in MPG (l/100km) for New Generation i30: Urban 29.7-68.9 (9.5-4.1), Extra Urban 51.4-80.7 (5.5 - 3.5), Combined 40.9 -76.3 (6.9-3.7), CO2 Emissions 162-97g/km.

Think you can have too much of a good thing?

Hyundai understands everyone is unique and that different people need different solutions. That’s why we’re proud to announce the arrival of our newest model, the all new Hyundai i30 3 door. More options for you to choose from, the same quality for you to enjoy. For more information, please proceed to Hyundai.com/eu

DPS_i30_Range_Think_WC_420x297_Fleet_Europe_March_39l.indd 1 15.02.13 08:54

Think Again.

Fuel consumption in MPG (l/100km) for New Generation i30: Urban 29.7-68.9 (9.5-4.1), Extra Urban 51.4-80.7 (5.5 - 3.5), Combined 40.9 -76.3 (6.9-3.7), CO2 Emissions 162-97g/km.

Think you can have too much of a good thing?