Embed Size (px)

Citation preview

Fixed assets

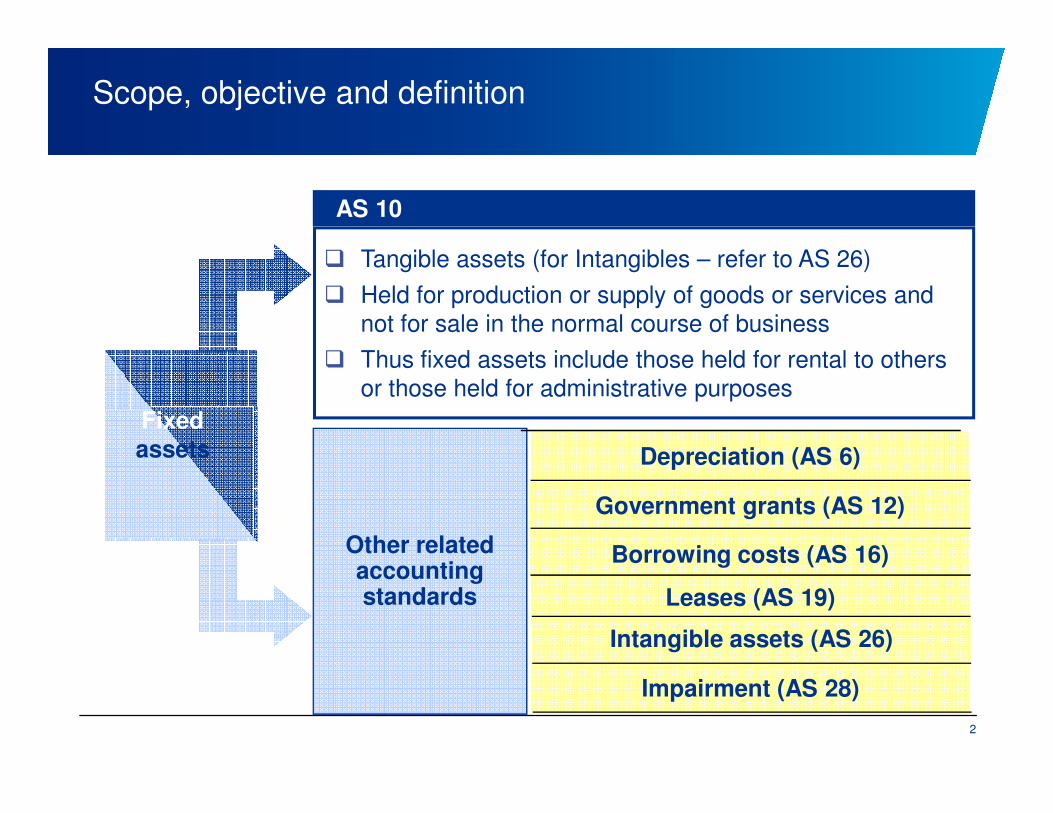

Scope, objective and definition

AS 10

Fixed

� Tangible assets (for Intangibles – refer to AS 26)

� Held for production or supply of goods or services and

not for sale in the normal course of business

� Thus fixed assets include those held for rental to others

or those held for administrative purposes

2

Other related accounting standards

Fixed assets Depreciation (AS 6)

Borrowing costs (AS 16)

Government grants (AS 12)

Leases (AS 19)

Impairment (AS 28)

Intangible assets (AS 26)

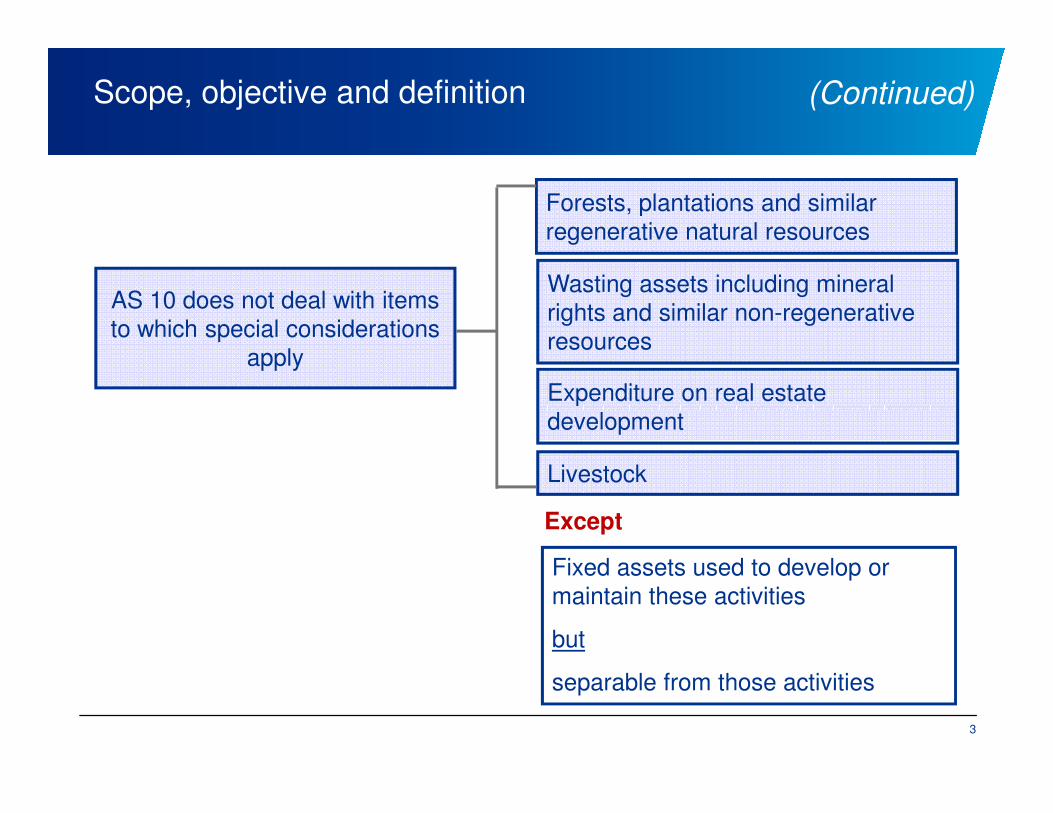

Scope, objective and definition

AS 10 does not deal with items

to which special considerations

apply

Forests, plantations and similar

regenerative natural resources

Wasting assets including mineral

rights and similar non-regenerative

resources

Expenditure on real estate

(Continued)

3

development

Livestock

Except

Fixed assets used to develop or

maintain these activities

but

separable from those activities

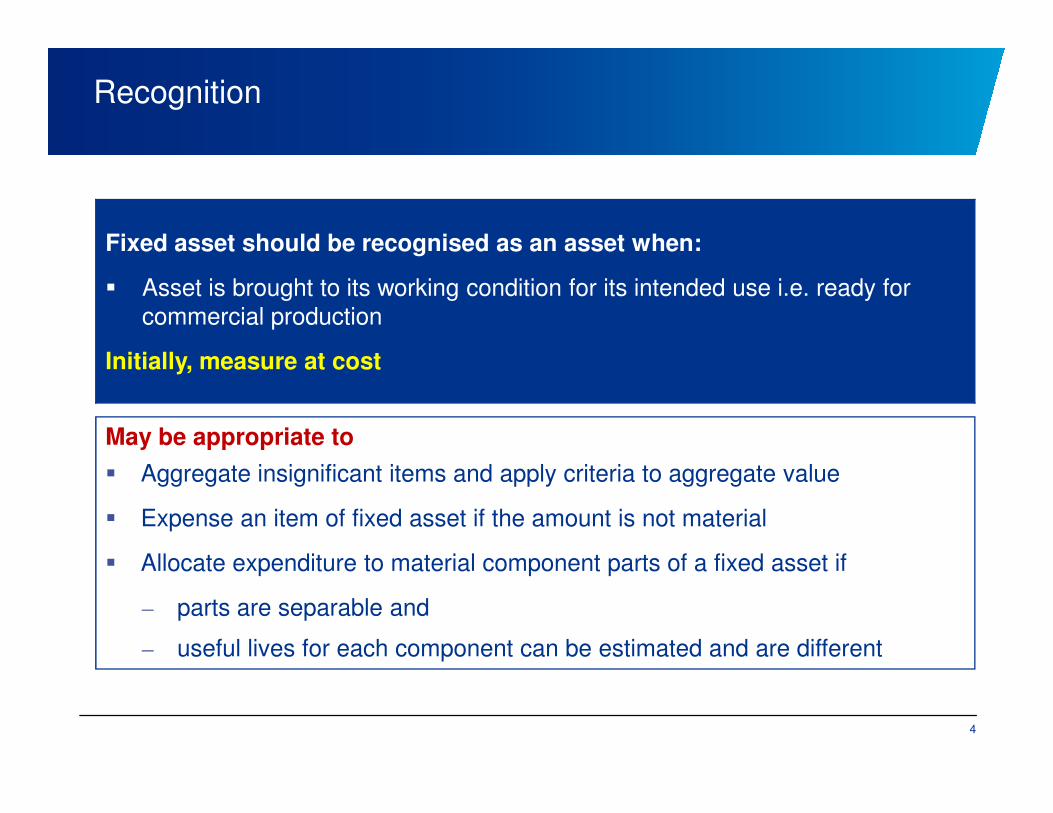

Recognition

Fixed asset should be recognised as an asset when:

� Asset is brought to its working condition for its intended use i.e. ready for

commercial production

Initially, measure at cost

4

May be appropriate to

� Aggregate insignificant items and apply criteria to aggregate value

� Expense an item of fixed asset if the amount is not material

� Allocate expenditure to material component parts of a fixed asset if

– parts are separable and

– useful lives for each component can be estimated and are different

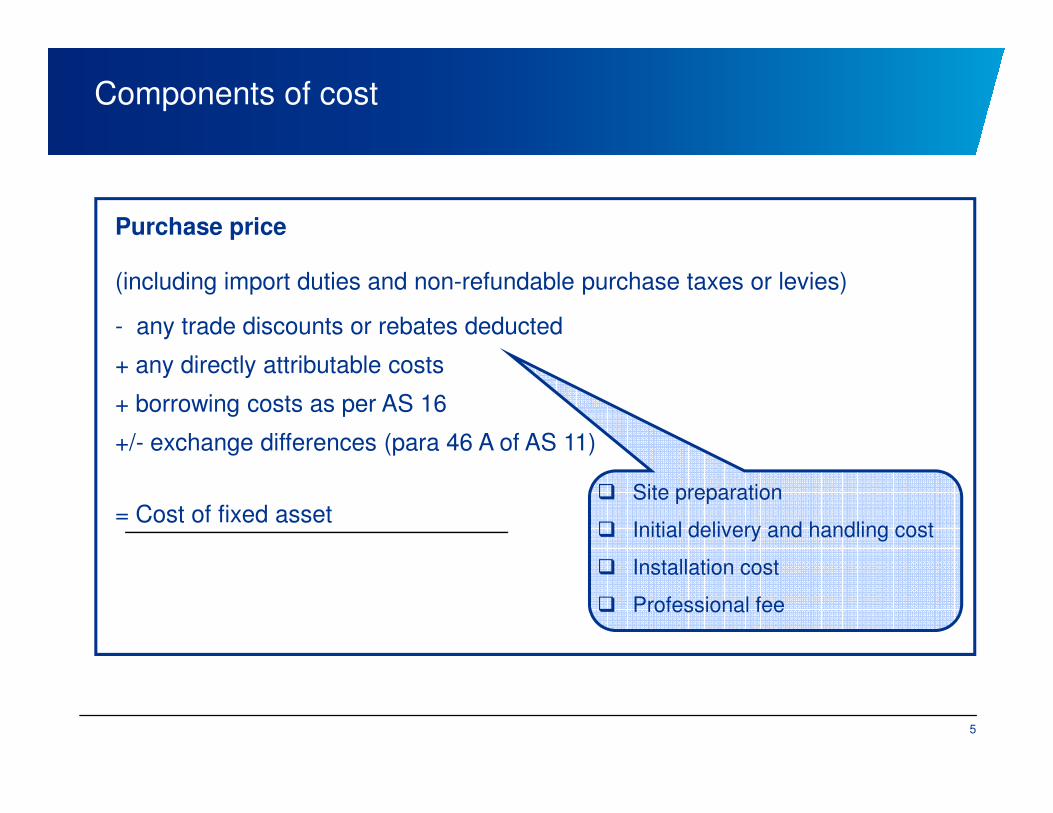

Components of cost

Purchase price

(including import duties and non-refundable purchase taxes or levies)

- any trade discounts or rebates deducted

+ any directly attributable costs

+ borrowing costs as per AS 16

5

+ borrowing costs as per AS 16

+/- exchange differences (para 46 A of AS 11)

= Cost of fixed asset� Site preparation

� Initial delivery and handling cost

� Installation cost

� Professional fee

Other expenses

Administration and other general overhead costs not included

unless

Such expenses are specifically attributable

� to construction of a project or

� to acquisition of fixed asset or

6

� to acquisition of fixed asset or

� bringing it to its working condition

Start-up, test runs and similar pre-production costs

� Included only till asset is ready for commercial production

� Not included if incurred after commercial production even if the plant will be

taken over after satisfactory completion of guarantee period

Expenditure during period of delayed commercial production

Self constructed fixed assets

Same principles as stated earlier

� Direct costs

� Costs attributable to construction which can be allocated

to the asset

� Internal profits are eliminated

7

Cost

Can the following costs be capitalised?

� Administrative, selling and general overheads which cannot

be attributed to making the asset ready for use

� Clearly identified abnormal costs including those of

inefficiencies

8

� Expenditure on training the staff to operate the asset

Impact of withdrawal of Guidance Note on Expenditure incurred during pre-construction period

Cost

The cost may change subsequently due to:

� Changes in duties

� Other similar factors

� Exchange fluctuations

� Price adjustments

(Continued)

9

� Price adjustments

Component accounting - Paragraph 8.3 states ‘the accounting for an item of fixed asset may

be improved if the total expenditure thereon is allocated to its component parts, provided they are in practice separable, and estimates are made of the useful lives of these components’ – recommendatory

provision’.

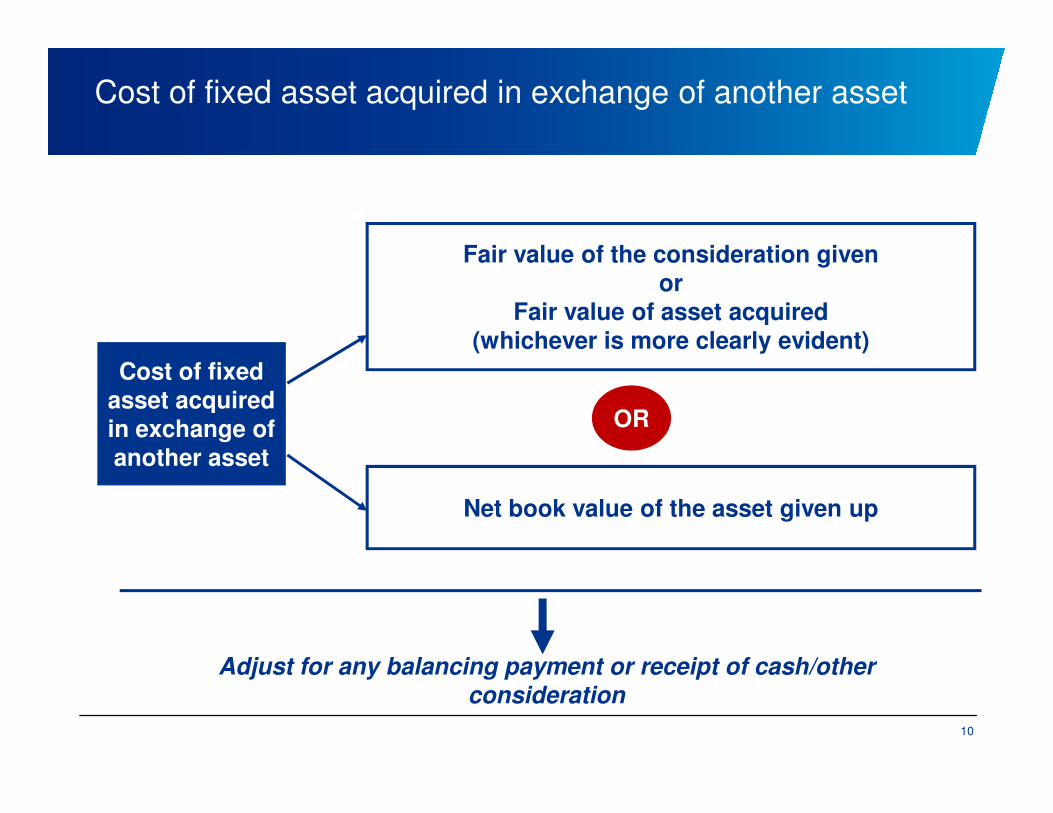

Cost of fixed asset acquired in exchange of another asset

Fair value of the consideration given or

Fair value of asset acquired (whichever is more clearly evident)

Cost of fixed asset acquired

OR

10

asset acquired in exchange of another asset

Net book value of the asset given up

OR

Adjust for any balancing payment or receipt of cash/other consideration

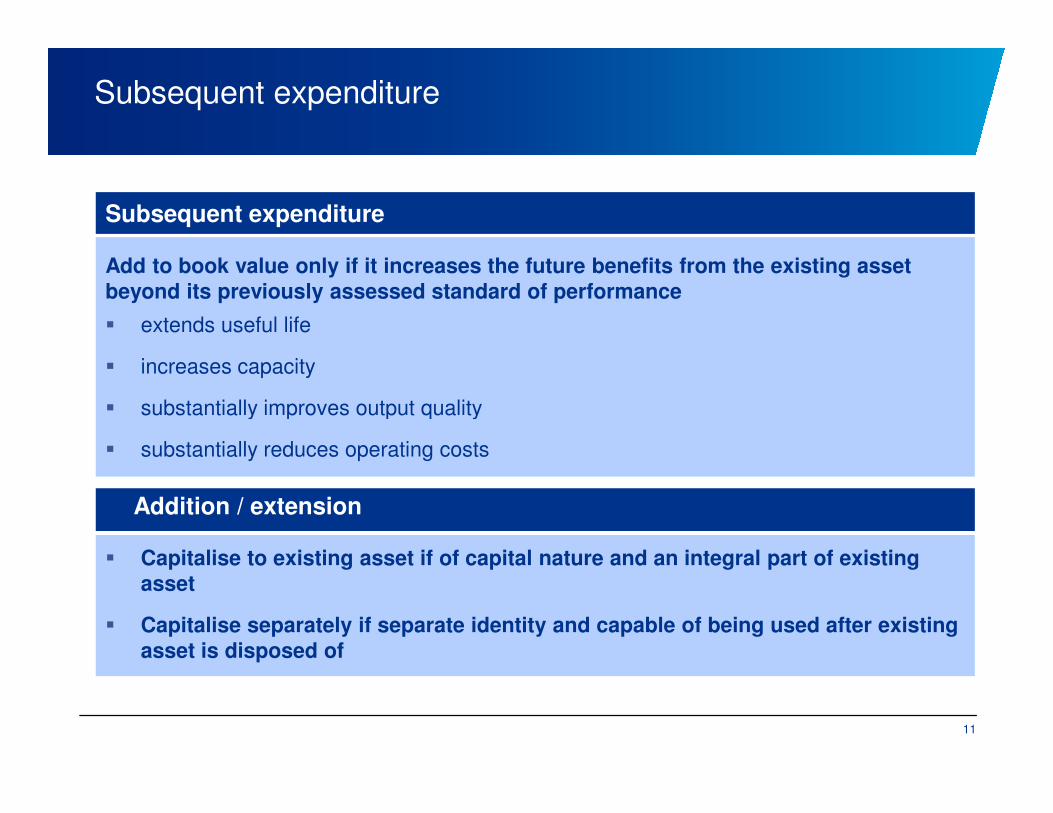

Subsequent expenditure

Add to book value only if it increases the future benefits from the existing asset beyond its previously assessed standard of performance

� extends useful life

� increases capacity

� substantially improves output quality

Subsequent expenditure

11

� substantially improves output quality

� substantially reduces operating costs

� Capitalise to existing asset if of capital nature and an integral part of existing asset

� Capitalise separately if separate identity and capable of being used after existing asset is disposed of

Addition / extension

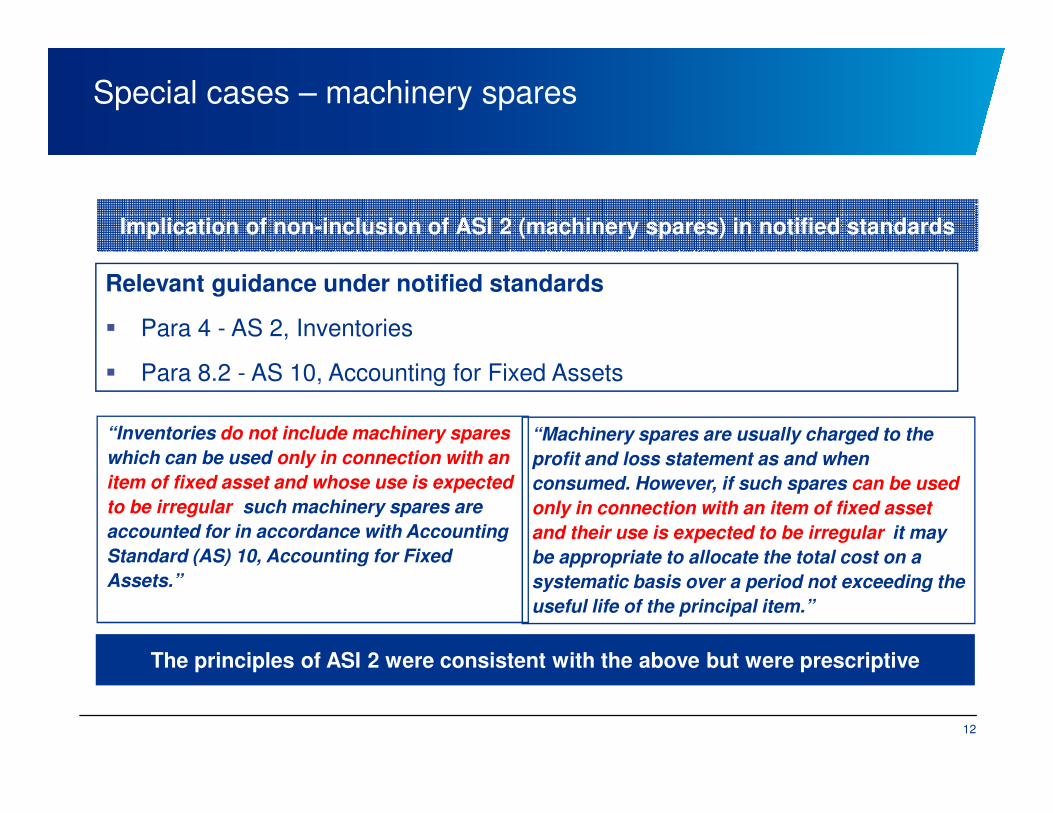

Special cases – machinery spares

Implication of non-inclusion of ASI 2 (machinery spares) in notified standards

Relevant guidance under notified standards

� Para 4 - AS 2, Inventories

� Para 8.2 - AS 10, Accounting for Fixed Assets

“Inventories do not include machinery spares

which can be used only in connection with an

item of fixed asset and whose use is expected

to be irregular; such machinery spares are

accounted for in accordance with Accounting

Standard (AS) 10, Accounting for Fixed

Assets.”

“Machinery spares are usually charged to the

profit and loss statement as and when

consumed. However, if such spares can be used

only in connection with an item of fixed asset

and their use is expected to be irregular, it may

be appropriate to allocate the total cost on a

systematic basis over a period not exceeding the

useful life of the principal item.”

The principles of ASI 2 were consistent with the above but were prescriptive

12

Special cases – machinery spares

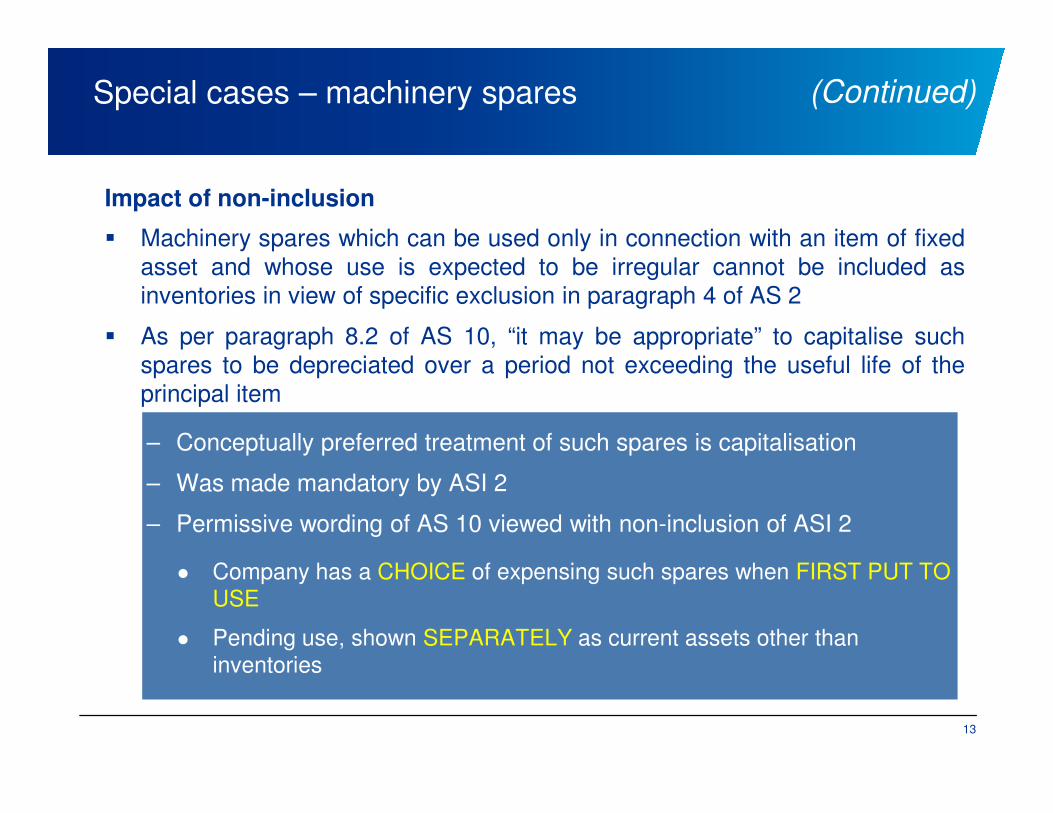

Impact of non-inclusion

� Machinery spares which can be used only in connection with an item of fixed

asset and whose use is expected to be irregular cannot be included as

inventories in view of specific exclusion in paragraph 4 of AS 2

� As per paragraph 8.2 of AS 10, “it may be appropriate” to capitalise such

spares to be depreciated over a period not exceeding the useful life of the

principal item

(Continued)

– Conceptually preferred treatment of such spares is capitalisation

– Was made mandatory by ASI 2

– Permissive wording of AS 10 viewed with non-inclusion of ASI 2

� Company has a CHOICE of expensing such spares when FIRST PUT TO USE

� Pending use, shown SEPARATELY as current assets other than inventories

13

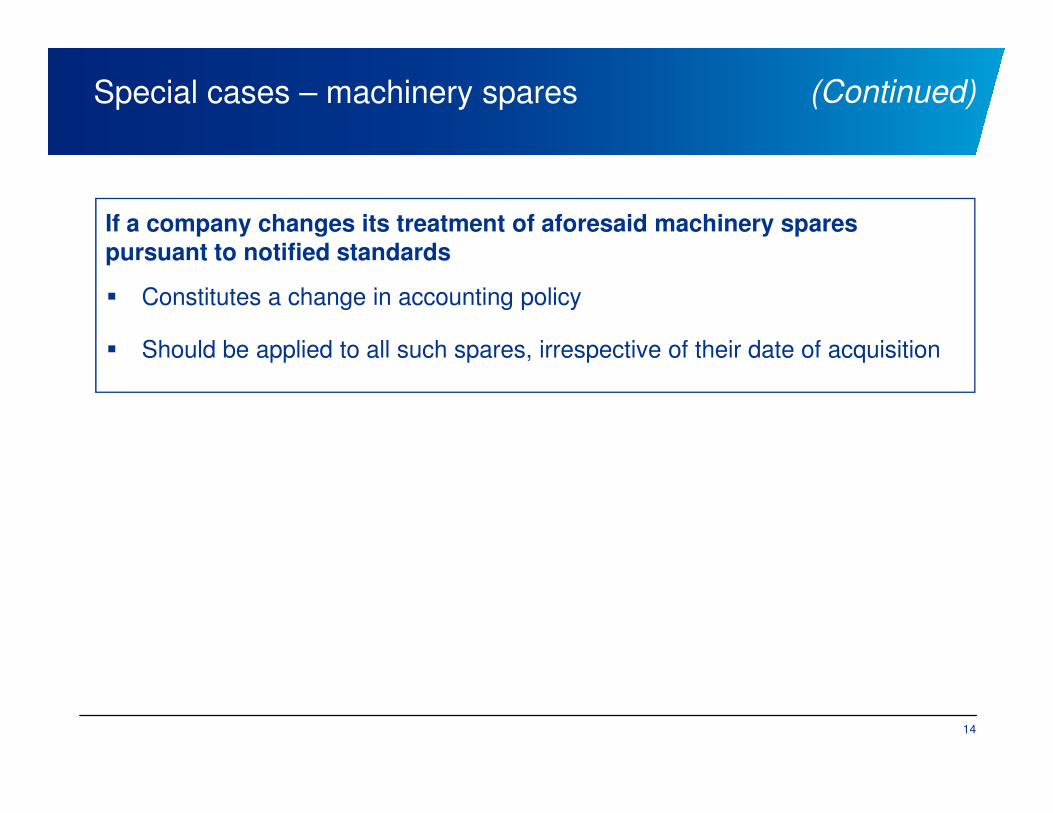

Special cases – machinery spares

If a company changes its treatment of aforesaid machinery spares pursuant to notified standards

� Constitutes a change in accounting policy

� Should be applied to all such spares, irrespective of their date of acquisition

(Continued)

14

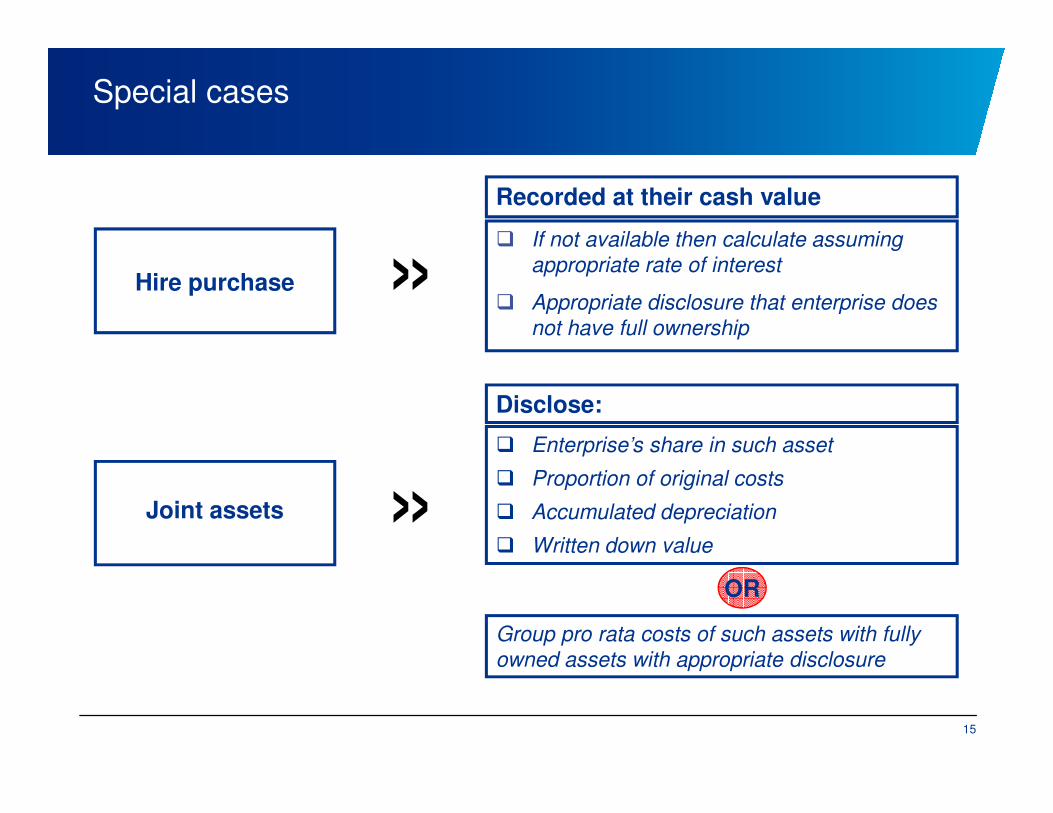

Special cases

Disclose:

Hire purchase

Recorded at their cash value

� If not available then calculate assuming

appropriate rate of interest

� Appropriate disclosure that enterprise does

not have full ownership

»Disclose:

Joint assets

� Enterprise’s share in such asset

� Proportion of original costs

� Accumulated depreciation

� Written down value

Group pro rata costs of such assets with fully

owned assets with appropriate disclosure

OR

»

15

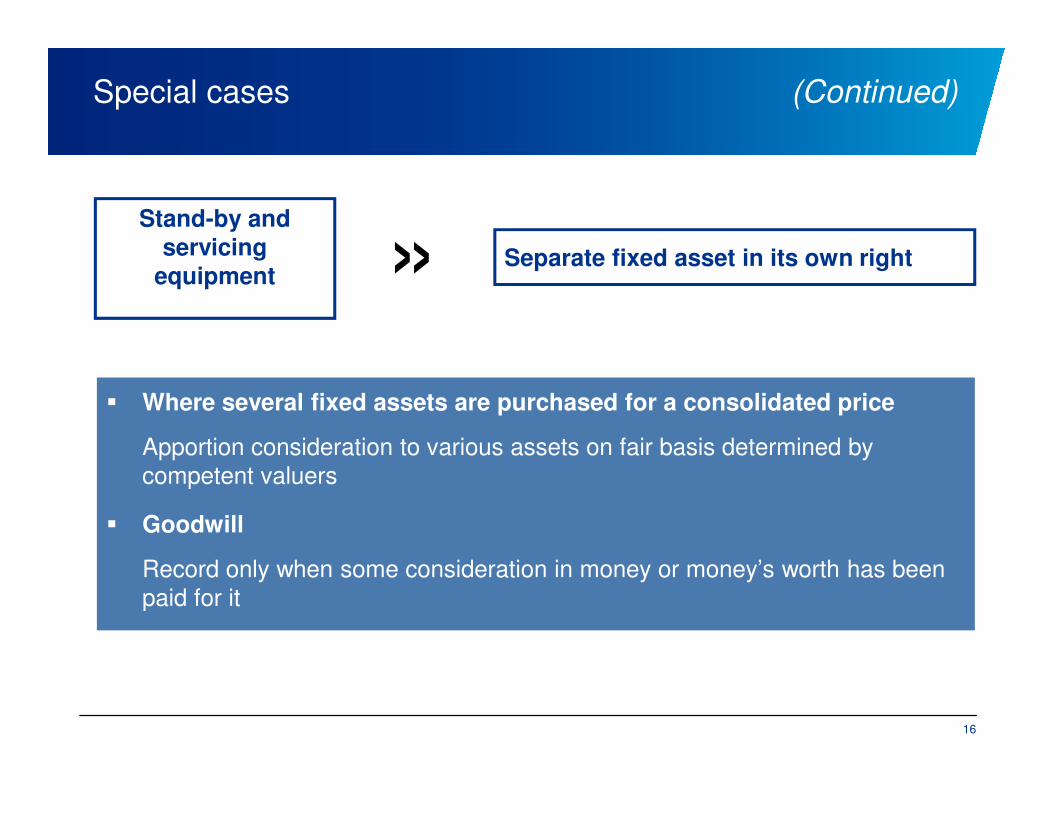

Special cases

� Where several fixed assets are purchased for a consolidated price

Separate fixed asset in its own right

Stand-by and servicing

equipment »

(Continued)

� Where several fixed assets are purchased for a consolidated price

Apportion consideration to various assets on fair basis determined by

competent valuers

� Goodwill

Record only when some consideration in money or money’s worth has been

paid for it

16

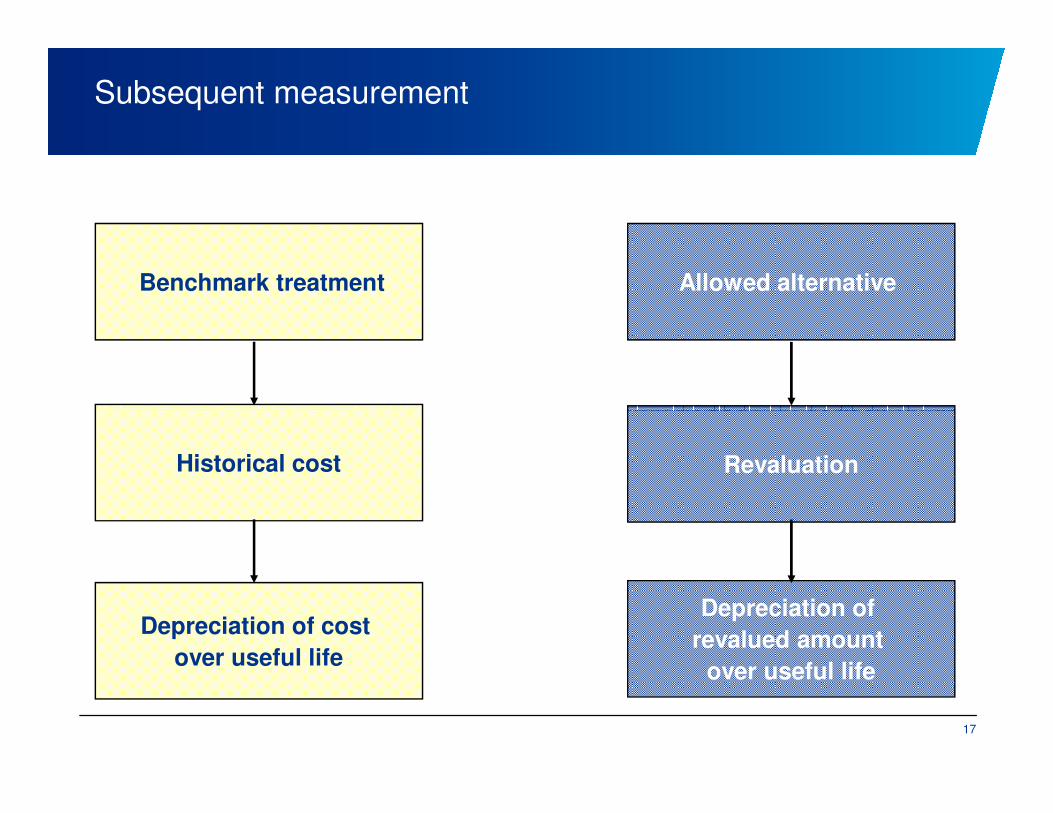

Subsequent measurement

Allowed alternative Benchmark treatment

Revaluation

Depreciation of

revalued amount

over useful life

Depreciation of cost

over useful life

Historical cost

17

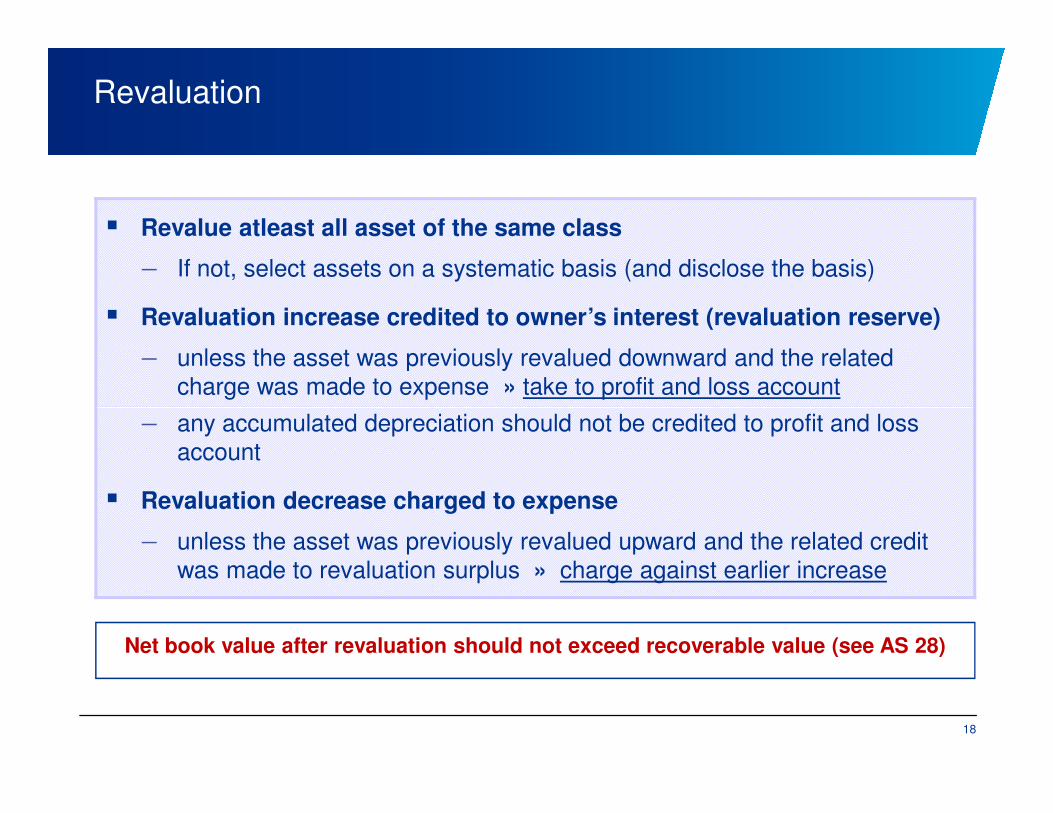

Revaluation

� Revalue atleast all asset of the same class

– If not, select assets on a systematic basis (and disclose the basis)

� Revaluation increase credited to owner’s interest (revaluation reserve)

– unless the asset was previously revalued downward and the related

charge was made to expense » take to profit and loss account

–

18

– any accumulated depreciation should not be credited to profit and loss

account

� Revaluation decrease charged to expense

– unless the asset was previously revalued upward and the related credit

was made to revaluation surplus » charge against earlier increase

Net book value after revaluation should not exceed recoverable value (see AS 28)

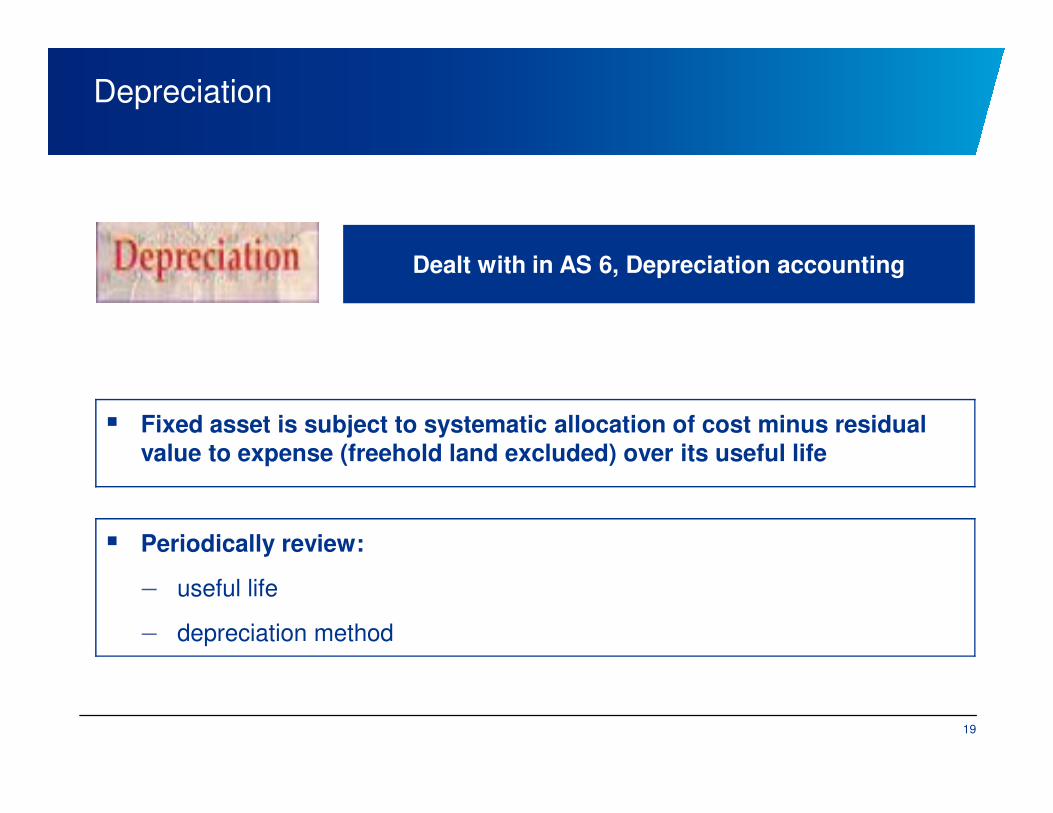

Depreciation

�

Dealt with in AS 6, Depreciation accounting

19

� Fixed asset is subject to systematic allocation of cost minus residual value to expense (freehold land excluded) over its useful life

� Periodically review:

– useful life

– depreciation method

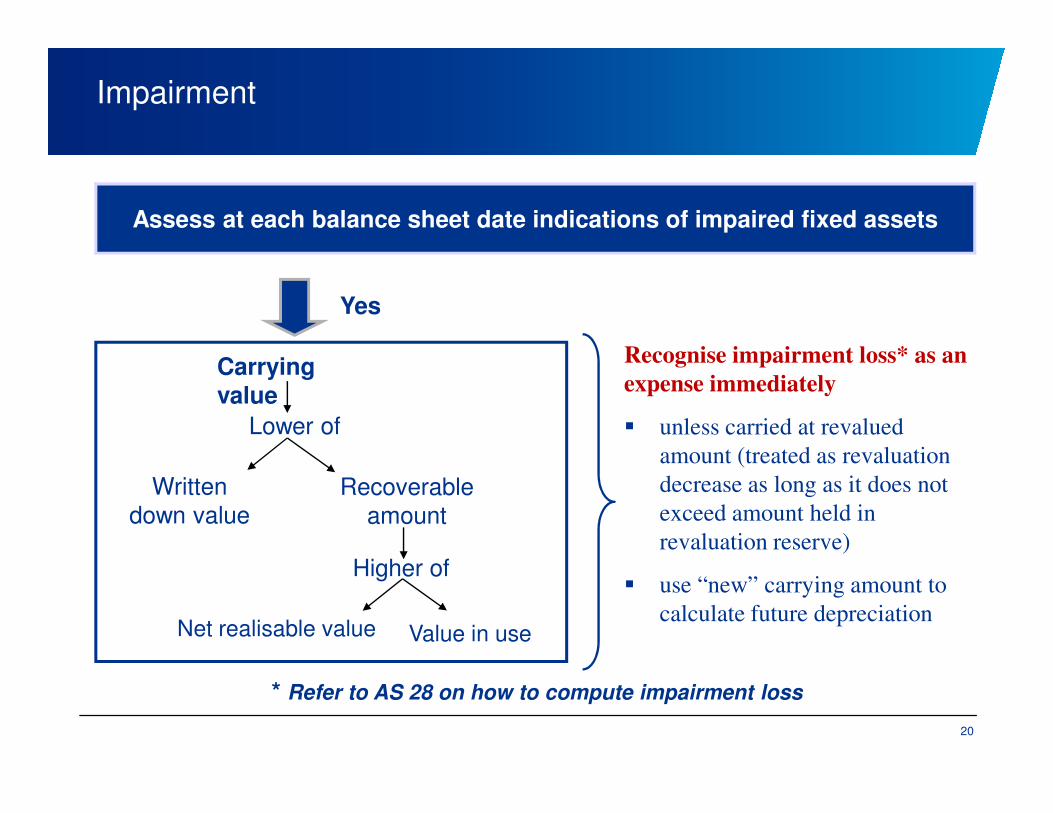

Impairment

Assess at each balance sheet date indications of impaired fixed assets

Yes

Carrying value

Recognise impairment loss* as an

expense immediatelyvalue

Lower of

Written

down valueRecoverable

amount

Net realisable value Value in use

Higher of

� unless carried at revalued

amount (treated as revaluation

decrease as long as it does not

exceed amount held in

revaluation reserve)

� use “new” carrying amount to

calculate future depreciation

* Refer to AS 28 on how to compute impairment loss

20

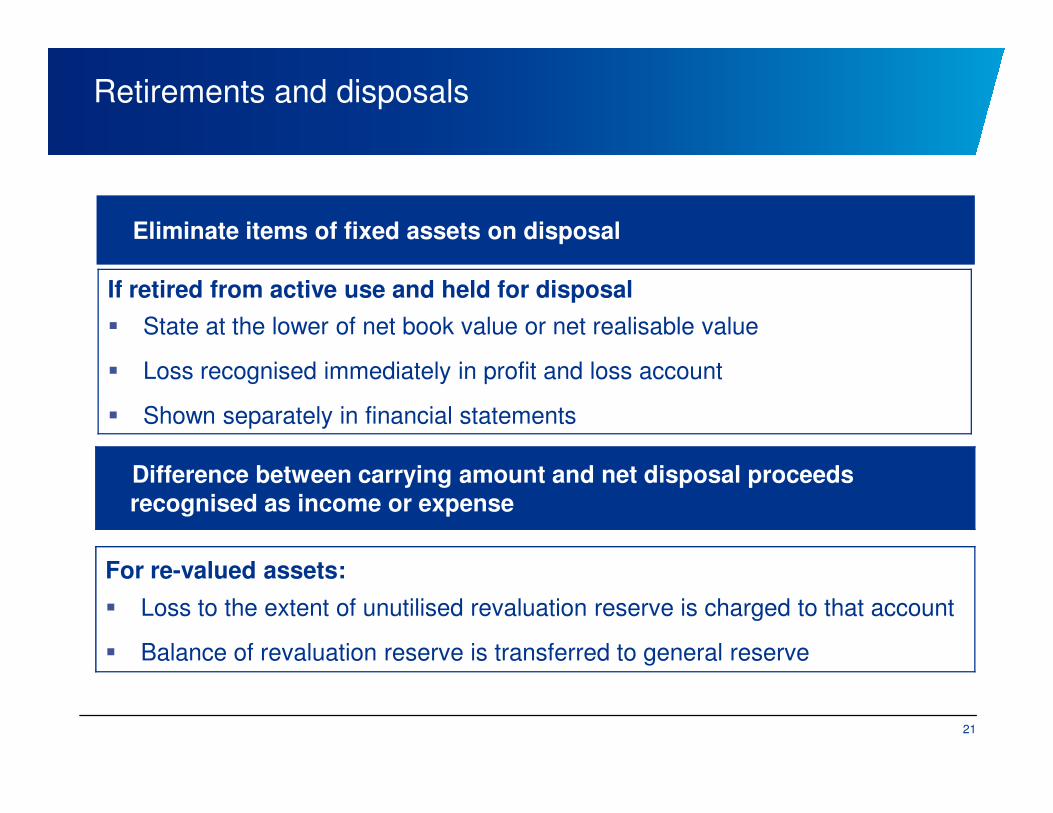

Retirements and disposals

�Eliminate items of fixed assets on disposal

If retired from active use and held for disposal

� State at the lower of net book value or net realisable value

� Loss recognised immediately in profit and loss account

� Shown separately in financial statements

21

� Shown separately in financial statements

�Difference between carrying amount and net disposal proceeds recognised as income or expense

For re-valued assets:

� Loss to the extent of unutilised revaluation reserve is charged to that account

� Balance of revaluation reserve is transferred to general reserve

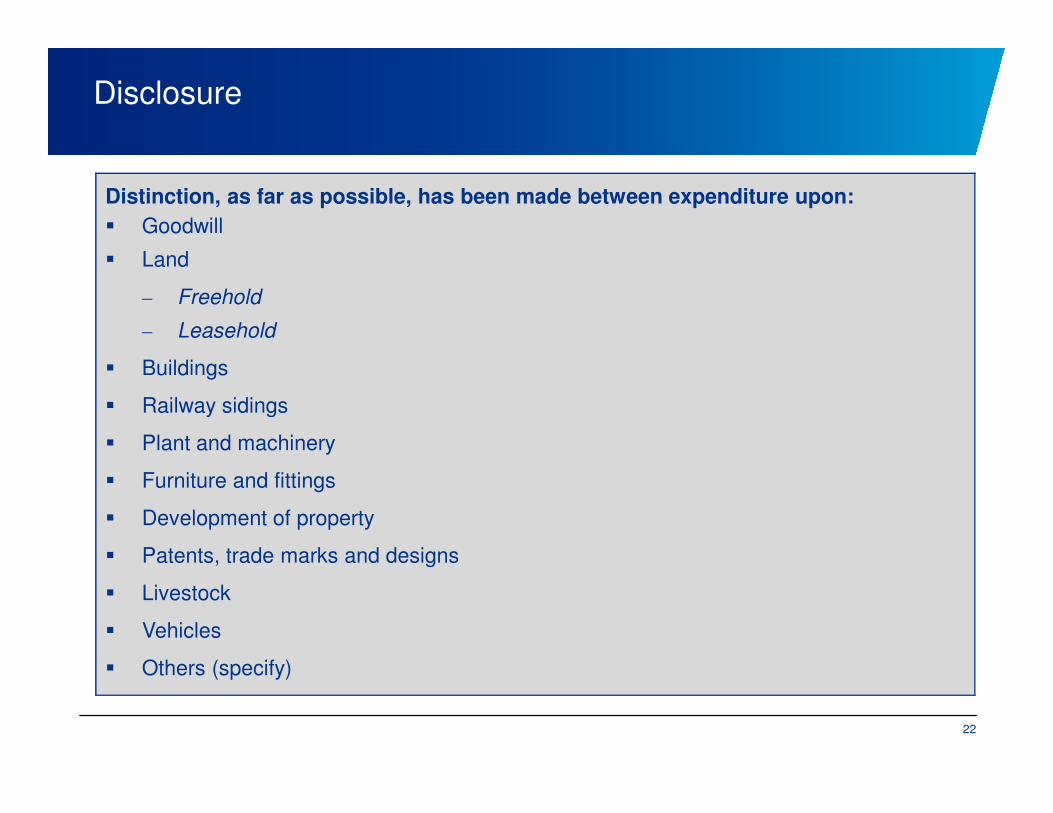

Disclosure

Distinction, as far as possible, has been made between expenditure upon:

� Goodwill

� Land

– Freehold

– Leasehold

� Buildings

� Railway sidings

22

� Railway sidings

� Plant and machinery

� Furniture and fittings

� Development of property

� Patents, trade marks and designs

� Livestock

� Vehicles

� Others (specify)

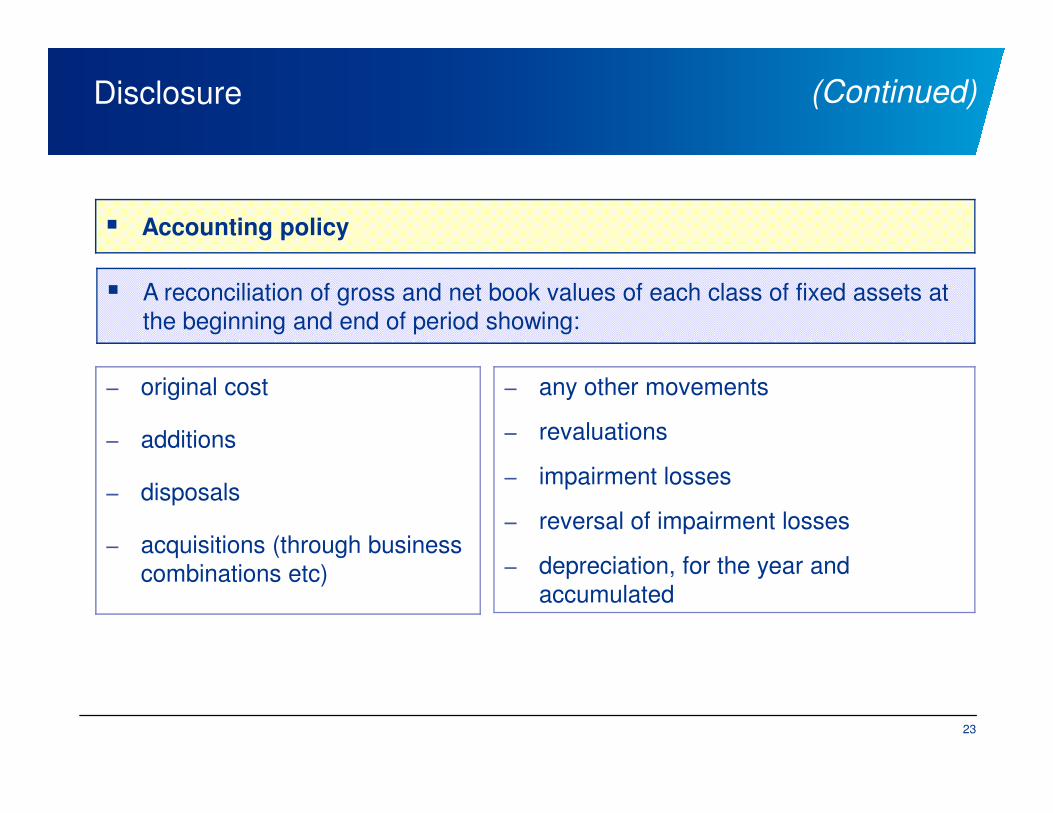

Disclosure

� Accounting policy

− any other movements − original cost

� A reconciliation of gross and net book values of each class of fixed assets at

the beginning and end of period showing:

(Continued)

23

− revaluations

− impairment losses

− reversal of impairment losses

− depreciation, for the year and

accumulated

− additions

− disposals

− acquisitions (through business

combinations etc)

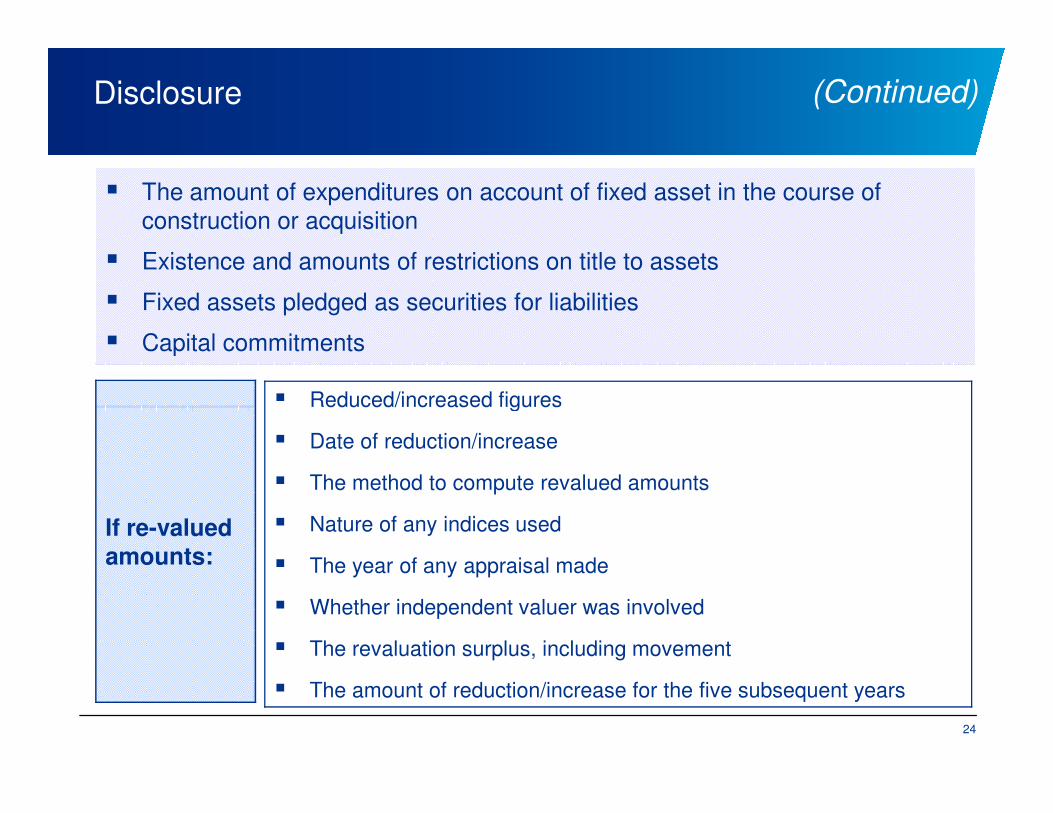

Disclosure

� The amount of expenditures on account of fixed asset in the course of

construction or acquisition

� Existence and amounts of restrictions on title to assets

� Fixed assets pledged as securities for liabilities

� Capital commitments

� Reduced/increased figures

(Continued)

24

� Reduced/increased figures

� Date of reduction/increase

� The method to compute revalued amounts

� Nature of any indices used

� The year of any appraisal made

� Whether independent valuer was involved

� The revaluation surplus, including movement

� The amount of reduction/increase for the five subsequent years

If re-valued amounts:

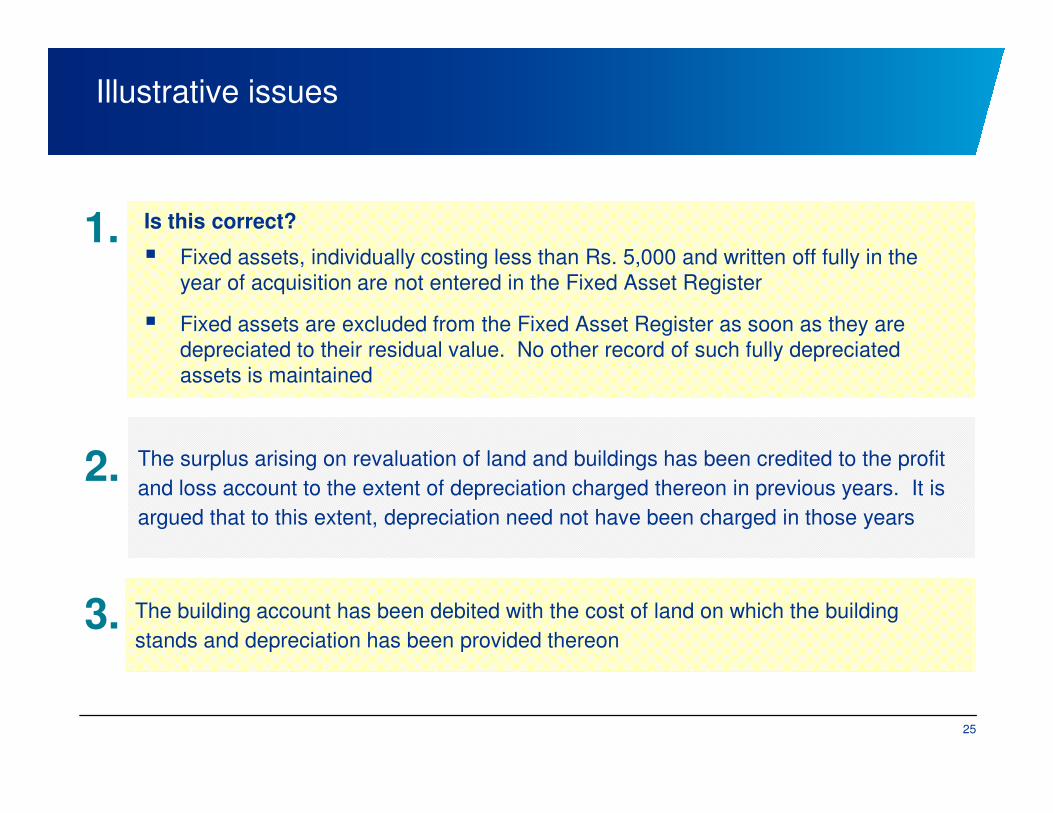

Illustrative issues

Is this correct?

� Fixed assets, individually costing less than Rs. 5,000 and written off fully in the

year of acquisition are not entered in the Fixed Asset Register

� Fixed assets are excluded from the Fixed Asset Register as soon as they are

depreciated to their residual value. No other record of such fully depreciated

assets is maintained

1.

The surplus arising on revaluation of land and buildings has been credited to the profit

and loss account to the extent of depreciation charged thereon in previous years. It is

argued that to this extent, depreciation need not have been charged in those years

2.

The building account has been debited with the cost of land on which the building

stands and depreciation has been provided thereon3.

25

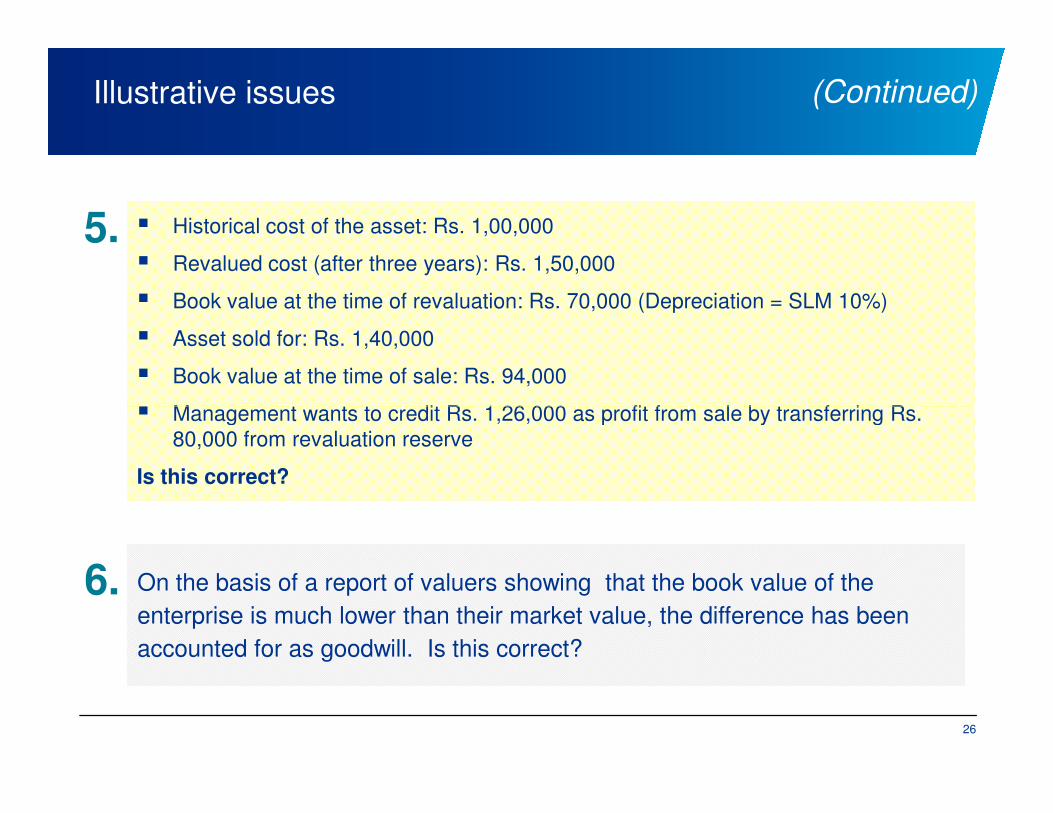

Illustrative issues

� Historical cost of the asset: Rs. 1,00,000

� Revalued cost (after three years): Rs. 1,50,000

� Book value at the time of revaluation: Rs. 70,000 (Depreciation = SLM 10%)

� Asset sold for: Rs. 1,40,000

� Book value at the time of sale: Rs. 94,000

� Management wants to credit Rs. 1,26,000 as profit from sale by transferring Rs.

5.

(Continued)

� Management wants to credit Rs. 1,26,000 as profit from sale by transferring Rs.

80,000 from revaluation reserve

Is this correct?

On the basis of a report of valuers showing that the book value of the

enterprise is much lower than their market value, the difference has been

accounted for as goodwill. Is this correct?

6.

26

Illustrative issues

Deferred revenue expenditure

Paragraph 9.2 of AS 10

However, expenditure incurred during this (‘construction) period is also sometimes treated as

deferred revenue expenditure to be amortised over a period not exceeding 3 to 5 years after

the commencement of commercial production.

Paragraphs 55(a) and 56 of AS 26

Expenditure on an intangible item should be recognised as an expense when it is incurred

7.

(Continued)

Expenditure on an intangible item should be recognised as an expense when it is incurred

unless: (a) it forms part of the cost of an intangible asset that meets the recognition criteria

(see paragraphs 19-54).

EAC Opinion – Query 10 – Volume XXIII

The expenditure incurred between the date the project is ready to commence commercial

production and the date at which the commercial production actually begins cannot be treated

as deferred revenue expenditure pursuant to the requirements of paragraphs 55 and 56, since

such an expenditure does not create an intangible asset, and, therefore, will have to be

expensed.

27

AS-6 Depreciation

Non - Applicability of Standard

� Forests, plantations and similar regenerative natural resources

� Wasting assets including expenditure on the exploration for and extraction of

minerals, oils, natural gas and similar non-regenerative resources;

� Expenditure on research and development;

� Goodwill and other intangible assets; � Goodwill and other intangible assets;

� Livestock.

� This standard also does not apply to land unless it has a limited useful life for

the enterprise.

29

Meaning of depreciation

� Depreciation is a measure of the wearing out, consumption or other loss of

value of a depreciable asset arising from use, effluxion of time or

obsolescence through technology and market changes. Depreciation is

allocated so as to charge a fair proportion of the depreciable amount in each

accounting period during the expected useful life of the asset. Depreciation

includes amortization of assets whose useful life is pre-determined.

30

Meaning of depreciable asset

Depreciable assets are assets which

� are expected to be used during more than one accounting period; and

� have a limited useful life; and

� are held by an enterprise for use in the production or supply of goods and

services, for rental to others, or for administrative purposes and not for the services, for rental to others, or for administrative purposes and not for the

purpose of sale in the ordinary course of business.

31

Meaning of useful life of depreciable asset

Useful life is either

(i) the period over which a depreciable asset is expected to be used by the

enterprise; or

(ii) the number of production or similar units expected to be obtained from the

use of the asset by the enterprise.

Factors to be considered

1. Pre-determined by legal or contractual limits

2. Directly governed by extraction or consumption

3. Dependent on the extent of use and physical deterioration

4. Obsolescence etc.

32

Methods of Depreciation

Straight Line Method(SLM)

Written Down Method(WDV)

Basis of selection of most appropriate method are:

1.Type of asset

2. the nature of the use of such asset

3. circumstances prevailing in the business

33

Straight Line Method (SLM)

� Depreciation =

Original Cost – Estimated Scrap Value

------------------------------------------------------------

Estimated useful life

1. Original Cost: Cost of acquisition, installation and commissioning as well as 1. Original Cost: Cost of acquisition, installation and commissioning as well as

for additions to or improvement thereof

2. Scrap Value: Estimated residual value of asset at the end of useful life.

(Generally assumed as ‘Nil’).

3. As explained in earlier slide

34

Written Down Method (WDV)

� Under this method depreciation is calculated on the reduced balance of the

fixed asset. Reduced balance is calculated by deducting accumulated

depreciation from the original cost or revalued amount.

� The statute governing an enterprise may provide the basis for computation of

the depreciation. For example, the Companies Act, 2013 lays down the rates

of depreciation in respect of various assets.

� Depreciation for the year = WDV * Rate

1. WDV : Original cost – Accumulated depreciation

2. Rate : Prescribed by the governing statue

35

Change in Depreciation Method

� Required by statute

� Required by accounting standard

Conditions

� Management judgment

36

Effect of Change in Depreciation Method

Recalculation of depreciation from the date of put to use to the date of

Change of method

Actual Depreciation Charged till date – Depreciation should be charged

Surplus Deficiency

Should be adjusted in the statement of profit & loss in the year in which the

Method of depreciation Is changed.

37

Change in Useful Life

� In case of useful life of the depreciable asset then it is necessary to charge

the depreciation on the basis of remaining useful life of the asset as per the

re-estimated useful life. The change should be given effect prospectively.

� What would be the treatment in the event of remaining useful life of an asset

being increased as compared to the original estimate.

38

being increased as compared to the original estimate.

� Can there be an scenario where the method of depreciation changes and

there is also a change in the estimate of remaining useful life?

Capitalization of Foreign Exchange Loss/Gain

� Where the historical cost of a depreciable asset has undergone a change due

to increase or decrease in long term liability on account of exchange

fluctuations, the depreciation on the revised unamortized depreciable amount

should be provided prospectively over the useful life of the asset.

� At point in time do you recognize and capitalize exchange differences (where

an enterprise elects to apply paragraph 46A of AS 11 – whether monthly,

quarterly, half-yearly or annually?quarterly, half-yearly or annually?

� Practical difficulty in maintaining trail of exchange differences which were

capitalised at the respective period-end and depreciating such differences at

a rate which is different from the rate being applied to the base cost originally

capitalised.

� Whether the fixed asset accounting is in an ERP environment or is it done on

MS Excel sheets, practical difficulties in maintaining audit trail.

39

Revaluation and depreciation

� In case of revaluation of depreciable asset, the depreciation charge should be

based on the revalued amount.

Revaluation

Upward Downward

Depreciation will be charged onrevalued amount of asset and anequal amount will be transferredfrom revaluation reserve to profit

& loss account.

Depreciation will be charged onrevalued amount of asset.

40

Disclosures

The following information should be disclosed in the financial statements :

� the historical cost or other amount substituted for historical cost of each class

of depreciable assets;

� total depreciation for the period for each class of assets; and

� the related accumulated depreciation.� the related accumulated depreciation.

� depreciation methods used; and

� depreciation rates or the useful lives of the assets, if they are different from

the principal rates specified in the statute governing the enterprise.

41

Accounting Standard 16 - Accounting for Borrowing Costs

Capitalised

� Borrowing costs directly attributable to acquisition, construction or production

of a qualifying asset to be capitalised as part of cost of that asset. Borrowing

costs capitalised as part of cost of qualifying asset when probable that they

will result in future economic benefits to enterprise and costs measured

reliably

AS 16 – Recognition

� Amount of borrowing costs eligible for capitalisation to be determined in

accordance with Statement.

Charged Off

� Other borrowing costs recognised as expenses in period incurred.

43

� Concept of qualifying assets – whether land can be a qualifying asset? What

if an enterprise has borrowings to set up a power project and a portion of

such borrowings are used to acquire land (on which a power plant will be

constructed)? Should such interest be capitalised to land?

� Practical challenges in allocating interest cost to different components of

qualifying assets which take a long gestation period to construct, for e.g. a

period of 3-5 years, how would one allocate interest to different classes of

AS 16 – Qualifying assets

period of 3-5 years, how would one allocate interest to different classes of

assets which got constructed at different points of time during the period of

construction?

� Whether a period less than 1 year can be considered – what about interest on

loans taken by a company for opening retail outlets which usually take 6-9

months to construct.

44

� Where funds borrowed generally and used for obtaining a qualifying asset,

borrowing costs eligible for capitalisation to be determined by applying a

capitalisation rate to expenditure on that asset.

� Capitalisation rate should be weighted average of borrowing cost applicable

to borrowings outstanding during the period other than borrowings specifically

for obtaining a qualifying asset.

AS 16 – Borrowing costs eligible for capitalisation

� Amount of borrowing costs capitalised during a period not to exceed

borrowing costs incurred during period.

� Borrowing costs for the period where there is cessation of construction

activity? How about costs where such cessation is necessary and incidental

to such construction.

45

� When carrying amount or expected ultimate cost of qualifying asset exceeds

recoverable amount or net realisable value, carrying amount written down/off

in accordance with other Accounting Standards.

� In certain circumstances, amount of write down/off is written back in

accordance with those other Accounting Standards.

As 16 – Excess of carrying amount of qualifying asset over

recoverable amount

46

AS 26 Intangible assets

Applicability

� Mandatory in nature for all enterprises

� Notified by Central Government w.e.f. accounting periods commencing on or

after 7 December 2006

What is the purpose of the Standard?

� To set forth criteria for recognition, measurement and disclosures about� To set forth criteria for recognition, measurement and disclosures about

intangible assets

48

Effect on other standards

� From the date of the Standard becoming mandatory:

− AS 8 (R & D) to stand withdrawn fully

− AS 6, Depreciation Accounting, to stand superseded with respect to the

amortisation of intangible assets

− Paragraphs 16.3 to 16.7, 37 and 38 of AS 10, which deal with expenditure− Paragraphs 16.3 to 16.7, 37 and 38 of AS 10, which deal with expenditure

on patents and know-how, to stand withdrawn

49

Exclusions from scope of standard

� Standard does not apply to –

– Intangible assets covered by another Accounting Standard

– Financial assets

– Mineral rights and expenditure on exploration, development or extraction

of minerals, oil, natural gas and similar non-regenerative resourcesof minerals, oil, natural gas and similar non-regenerative resources

– Intangible assets arising in insurance enterprises from contracts with

policyholders

– Expenditure in respect of termination benefits

– Discount or premium relating to borrowings and ancillary costs incurred in

connection with arrangement of borrowings, share issue expenses and

discount allowed on issue of shares

50

What is an ‘Intangible Asset’

� ‘Intangible asset’ is “an identifiable non-monetary asset, without physical

substance, held for use in the production or supply of goods or services, for

rental to others, or for administrative purposes”

� An asset is a resource controlled by an enterprise from which future

economic benefits are expected to flow to the enterprise

51

Criteria

� Identifiability

� Control

� Future benefits

� Without substance but non monetary

52

Identifiability

� Clearly distinguished from goodwill

� Enterprise can rent/sell/exchange/distribute future benefits

� Asset is identifiable even if it generates future benefits in combination with

other assets

53

Control

� Power to obtain future benefits

� Also can restrict access of others to those benefits

� Normally stems from legal rights

� In absence of legal rights, more difficult to demonstrate control

54

Future economic benefits

� Revenue

� Cost savings

� Other benefits from the use of asset

55

Composite assets

� Intangible assets contained in or on a physical substance, e.g. software

contained on a CD, motion picture contained on celluloid film

� Assets incorporating both intangible and tangible elements e.g, computer

hardware containing also the operating system as well as applications

software

56

What qualifies as intangible asset

� AS 26 applies to expenditure on advertising, training, start-up, research and

development activities, rights under licensing agreements (for items such as

motion picture films, video recordings, plays, manuscripts)

� AS 26 also covers intangible resources such as scientific or technical

knowledge, design and implementation of new processes or systems,

expenditure on prototypes, licences, intellectual property, market knowledge

and trademarks (including brand names and publishing titles). Common and trademarks (including brand names and publishing titles). Common

examples of items encompassed by these broad headings are computer

software, patents, copyrights, motion picture films, customer lists, mortgage

servicing rights, fishing licences, import quotas, franchises, customer or

supplier relationships, customer loyalty, market share and marketing rights

� Not all the items described above will meet the definition of an intangible

asset

57

Recognition of intangible assets

� An intangible asset to be recognised if,

– it is probable that the future economic benefits that are attributable to the

asset will flow to the enterprise; and

– the cost of the asset can be measured reliably.

58

Recognition of intangible assets

� An intangible asset should be measured initially at cost. After initial

recognition, an intangible asset should be carried at its cost less any

accumulated amortisation and any accumulated impairment losses.

� Per AS 10 (para 15.3) - where several assets are purchased for a

consolidated price, the consideration is apportioned to the various assets on

a fair basis as determined by competent valuers (eg. Assets/business

purchase on ‘Slump’ basis)purchase on ‘Slump’ basis)

� As per AS 26 (para 27), an intangible asset acquired in an amalgamation in

the nature of purchase is accounted for in accordance with Accounting

Standard 14

� Indian GAAP does not permit Revaluation of Intangibles; under IFRS,

intangibles which have an active market (eg. Emission allowance) may be

revalued to fair value; US GAAP does not permit revaluation of intangibles.

59

Cost of an intangible asset

� Acquired in exchange for shares or other securities of the reporting enterprise

- cost is asset’s fair value, or fair value of securities issued, whichever is more

clearly evident.

� Acquired in exchange for another asset - apply AS 10

� Acquired by way of government grants - apply AS 12

� Acquired in an amalgamation in the nature of purchase

– Record at existing carrying amount or

– Allocate consideration based on fair values at amalgamation date.

60

Internally generated assets

� Internally generated goodwill not to be recognised as an asset

� Internally generated brands, mastheads, publishing titles, customer lists, etc.

not to be recognised as intangible assets

� For other internally generated assets, generation of asset to be classified into:

– Research phase– Research phase

– Development phase

61

Research phase

� Examples of research phase activities

– Activities aimed at obtaining new knowledge

– Search for, evaluation and final selection of, applications of research

findings or other knowledge

– Search for alternatives for materials, devices, products, processes,

systems or servicessystems or services

– Formulation, design, evaluation and final selection of possible alternatives

for new or improved materials, devices, products, processes, systems or

services

� Research phase costs to be expensed in all cases

62

Development phase

Examples of development phase activities:

� Design, construction and testing of pre-production or pre-use prototypes and

models

� Design of tools, jigs, moulds and dies involving new technology

� Design, construction and operation of a pilot plant that is not of a scale� Design, construction and operation of a pilot plant that is not of a scale

economically feasible for commercial production

� Design, construction and testing of a chosen alternative for new or improved

materials, devices, products, processes, systems or services

63

Development phase

� An intangible asset should be recognised if enterprise can demonstrate thefollowing:

– Technical feasibility of completing the asset

– Its intention to complete the asset and use/sell it

– Its ability to use or sell the intangible asset

– How the asset will generate probable future economic benefits

(Continued)

– How the asset will generate probable future economic benefits

– Availability of adequate technical, financial and other resources to complete the

development and to use or sell the intangible asset and

– its ability to measure the expenditure attributable to the intangible asset during its

development reliably

� Cost of internally generated intangible asset comprises expenditure incurredfrom the time when it first meets the recognition criteria

64

Exclusions from cost of internally generated intangible assets

� Selling, administrative, other general overheads unless they can be directly

attributed to making the asset ready for use

� Clearly identified inefficiencies and initial operating losses incurred before an

asset achieves planned performance

� Expenditure on training the staff to operate the asset

65

Recognition as expense

� Expenditure on an intangible item to be expensed when incurredunless:

– it forms part of the cost of an intangible asset that meets the recognition

criteria or

– the item is acquired in an amalgamation in the nature of purchase and

cannot be recognised as an intangible asset. In this case, the expenditurecannot be recognised as an intangible asset. In this case, the expenditure

(included in the cost of acquisition) should form part of goodwill/capital

reserve

66

Examples of expenditure to be expensed

� Expenditure on research

� Start-up costs other than

– Expenditure which can be capitalised as per AS 10

– Share/debenture issue expenses

– Discount on shares/debentures (Preliminary expenses other than the – Discount on shares/debentures (Preliminary expenses other than the

above are to be expensed)

� Expenditure on training activities

� Expenditure on advertising/promotional activities

� Expenditure on relocation/re-organisation

� Expenditure initially recognised as expense in previous annual/interim

financial reports cannot later be recognised as part of cost of an intangible

asset

67

Subsequent expenditure

� To be expensed unless -

– it is probable that the expenditure will result in future economic benefits in

excess of its originally assessed standard of performance and

– the expenditure can be measured and attributed to the asset reliably

� Only rarely will subsequent expenditure be added to the cost of the � Only rarely will subsequent expenditure be added to the cost of the intangible asset

68

Amortisation

� Depreciable amount to be amortised over useful life

� Amortisation should commence when the asset is available for use

� Requirements concerning amortisation method, useful life and depreciable

amount are significantly at variance from those of AS 6

69

Amortisation method

� Should reflect the pattern in which the asset's economic benefits are

consumed

� If that pattern cannot be determined reliably, straight-line method should be

used

� There will rarely, if ever, be persuasive evidence to support an amortisation

method that results in a lower amount of accumulated amortisation thanmethod that results in a lower amount of accumulated amortisation than

under straight-line method

� Eg. Extractive industry - Costs incurred to gain access to mineral reserves

are capitalised and amortised over the life of the quarry, which is based on

the estimated tonnes of raw materials to be extracted from the reserves

Eg. Pharma - Intangible assets comprise patents, trademarks, designs and

licenses and computer software which are stated at cost less accumulated

amortization (determined on a straight line basis) and impairment losses, if

any

70

Useful life

� Rebuttable presumption that the useful life of an intangible asset will not

exceed ten years. Reasons for taking useful life exceeding ten years to be

disclosed highlighting the factors that played a significant role in determining

useful life

� Computer software and many other intangible assets are susceptible to

technological obsolescence and their useful life is thus likely to be short

� If control is achieved through legal rights granted for limited period, useful life

not to exceed the period of the legal rights unless:

– the legal rights are renewable and

– renewal is virtually certain

71

Useful life

� Eg. Consumer goods - For various brands acquired by the Company,

estimated useful life has been determined ranging between 20 to 25 years.

The Company believes this based on number of factors including the

competitive environment, market share, brand history, product life cycles,

operating plan, no restrictions on title and the macroeconomic environment of

the countries in which the brands operate. Accordingly, such intangible assets

are being amortised over the determined useful life.are being amortised over the determined useful life.

72

� Computer software and many other intangible assets are susceptible totechnological obsolescence and their useful life is thus likely to be short

– Eg. Mfg co. Expenditure on computer software is amortised on straight line method

over the period of expected benefit not exceeding five years

� If control is achieved through legal rights granted for limited period, useful lifenot to exceed the period of the legal rights unless:

(Continued)Useful life

– the legal rights are renewable and renewal is virtually certain

Eg. Mfg co. - Licenses for Technical know-how have been amortised on a straight line

basis over the License term of forty two months

Eg. Telecom - Bandwidth / Fibre taken on Indefeasible Right of Use (IRU) is amortised

over twenty years being the agreement period

� Under International GAAP (IFRS/US GAAP), Intangibles can also have indefiniteuseful life (eg Brands)

73

Residual value

� In determining depreciable amount, residual value should be assumed to be

zero unless:

– there is a commitment by a third party to purchase the asset at the end of

its useful life or

– there is an active market for the asset and:

� residual value can be determined by reference to that market and� residual value can be determined by reference to that market and

� it is probable that such a market will exist at the end of the asset's useful life

74

Review of amortisation period/method

� Amortisation period to be reviewed at least at each financial year end and to

be changed if expected useful life is significantly different from previous

estimates, the amortisation period should be changed accordingly

� Amortisation method to be similarly changed if there has been a significant

change in expected pattern of economic benefits

� Both are changes in accounting estimates� Both are changes in accounting estimates

75

Impairment losses

� Recoverable amount of following assets to be determined at least at each

financial year end even if there is no indication of impairment:

– intangible assets not yet available for use

– intangible assets being amortised over a period exceeding ten years from the date

when they became available for use

– Intangible assets with indefinite useful life (under International GAAP)– Intangible assets with indefinite useful life (under International GAAP)

76

Derecognition

� Asset to be derecognised on disposal or when no future economic benefits

are expected from its use and subsequent disposal.

77

Transitional provisions

� Assess remaining useful life (as per standard) of each intangible item on the

date of initial application of standard (say 3 years in the case of Asset A and 4

years in the case of Asset B and 6 years for Asset C)

� Determine remaining amortisation period as per books of account (say 4

years for each)

� In case of Assets B and C write off net book value in 4 years� In case of Assets B and C write off net book value in 4 years

� In case of Asset A, increase accumulated amortisation so that it can be

written off in 3 years. Increase to be adjusted against opening revenue

reserves

78

Transitional provisions - another example

� Amortisation period 10 years, 6 years have elapsed

� Remaining life as per AS 26 is 3 years. Hence total life as per AS 26 is

9 years. Hence amortisation for each year would be 100/9 or Rs 67 should

have been written off. Adjust Rs 7 against opening reserve

79

Case study on intangible assets

� Facts

During the year ended 31 March X3, Company A purchased intellectual

property rights (IPR) in the Product X, a treasury management product, from

Company B for use by its Banking group. The aggregate consideration paid

for the IPR is Rs. 5 crores. Management estimates the useful life of the IPR

as two years

� Analysis of the case

Applicability of AS 26 – Intangible assets to the above case

− In accordance with the definition of intangible assets in para 6 of AS 26 on

Intangible Assets, the IPR above constitutes an identifiable non-monetary

asset without physical substance, held for use in the supply of the services

to others. Further, intellectual property is explicitly included in examples of

intangible resources in Para 7 of the standard.

80

Case study on intangible assets

� Recognition and initial measurement of the asset

− The facts above represent a case of separate acquisition. Accordingly

the consideration paid to Company B for the acquisition of the IPR has

been used for recording the asset in the books.

� Amortisation

− Management of Company A believes that the economic benefits

(Continued)

− Management of Company A believes that the economic benefits

embodied in the IPR shall be received over a period of two year which

represent the best estimate of the useful life of the IPR. Further, this

estimate does not exceed the period of the legal rights. In accordance

with Para 63, amortisation has commenced from the date when asset is

available for use to Company A. The amortisation is performed in

accordance with Para 72 using the straight-line method over the

estimated useful life

81

Case study on accounting for software development

Stage Examples Accounting treatment

Preliminary stage

� Strategic decision to

allocate resources

� Determination of

performance requirements

� Payroll costs

� Administration costs –

eg. traveling, rent,

communications

� Recognised as expense

as incurred

� Reason – enterprises

cannot demonstrate performance requirements

� Exploration of alternative

performance requirements

� Determination of

technology

� Appointment of consultant

for development/

installation of software

communications

� External consultants

� Purchase of software

� Cost of external

software services

cannot demonstrate

that an asset exists

from which future

economic benefits are

probable

82

Case study on accounting for software development

Stage Examples Accounting treatment

Development stage

� Software including program design

� Coding of computer software

� Same as above –

Costs not considered for capitalisation

� Selling, administration and

� Recognised as assets, if & only if:

� Technical feasibility has been achieved

� Enterprise has intention to

(Continued)

� Beta testing (initial testing)

� Testing of function, feature and technical performance of product design

� Selling, administration and other general overhead expenditure

� Clearly defined ineffectiveness and initial operating losses before software achieves planned performance

� Staff training costs

� Enterprise has intention to complete software project and use it for intended purpose

� Enterprise has ability to use the software

� Software will generate future economic benefits

� Availability of adequate technical, financial and other resources to complete development and use software

– Expenditure can be measured

83

� Costs incurred subsequent to development of software shall becapitalised if

− probable that future economic benefits are in excess of originally

assessed standards of performances

− expenditure can be reliably measured and attributed to software

development

Case study on accounting for software development(Continued)

development

� Amortisation period

− 3 to 5 years or if useful life is a shorter period or software is susceptible to

technological obsolescence. Testing for impairment to be carried out

annually

84

IPR – Definition

As per World Trade Organisation

Intellectual Property Rights (IPR) are the rights given to persons over the creations of their minds. They

usually give the creator an exclusive right over the use of his/her creation for a certain period of time

I Copyright and rights related to copyright

� The rights of authors of literary and artistic works (such as books and other writings, musical

compositions, paintings, sculpture, computer programs and films) are protected by copyright, for a

minimum period of 50 years after the death of the author

� Also protected through copyright and related (sometimes referred to as “neighbouring”) rights are the� Also protected through copyright and related (sometimes referred to as “neighbouring”) rights are the

rights of performers (e.g. actors, singers and musicians), producers of phonograms (sound recordings)

and broadcasting organizations. The main social purpose of protection of copyright and related rights

is to encourage and reward creative work

II Industrial property

� One area can be characterized as the protection of distinctive signs, in particular trademarks (which

distinguish the goods or services of one undertaking from those of other undertakings) and

geographical indications (which identify a good as originating in a place where a given characteristic of

the good is essentially attributable to its geographical origin)

� Other types of industrial property are protected primarily to stimulate innovation, design and the

creation of technology. In this category fall inventions (protected by patents), industrial designs and

trade secrets

85

As per Development Commissioner - Micro, Small and Medium Enterprises

Intellectual Property Rights (IPR) are legal rights, which result from intellectual activity in

industrial, scientific, literary & artistic fields. These rights safeguard creators and other

producers of intellectual goods & services by granting them certain time-limited rights to

control their use. Protected IP rights like other property can be a matter of trade, which

can be owned, sold or bought

Types of IPR

(Continued)IPR – Definition

a. Patents

b. Trademarks/ Brands

c. Copyrights and related rights

d. Geographical Indications

e. Industrial Designs

f. Trade Secrets

g. Layout Design for Integrated Circuits

h. Protection of New Plant Variety

86

IPR accounting – relevance and challenges

� As corporations around the world are awakening to the revenue-generating

potential of intangible assets, the issue of accounting for intellectual property

gains importance

� Varying accounting practices are prevalent resulting in differing Balance

sheets and Profit and loss accounts

� Due to absence of organised and transparent markets, and subjectivity

involved, there are difficulties in determining value of IPRsinvolved, there are difficulties in determining value of IPRs

� Accounting rules are evolving to enhance reporting/disclosures of IPR

� Differences between economic framework of accounting and legal framework

lead to disparity between what Companies show in the balance sheet and

own. Therefore, not all IPR are recognised as intangible assets in accounting

and some intangible assets considered as IP are not recognised as IPR by

law

� Is IP Report a need of the hour (in case of internally generated IPs)??

87

IPR recorded on the balance sheets….

� Pepsi has perpetual brands of USD 4,839 million representing 6% of its total

assets

� Walt Disney has copyrights and trademarks aggregating USD 4,273 million

representing 6% of its total assets

� Microsoft has technology based and marketing related intangibles of USD

3,083 million representing 2% of its total assets3,083 million representing 2% of its total assets

� Coca Cola has perpetual trademarks of USD 6,527 million representing 8% of

its total assets

� Google has patents and developed technology of USD 5,987 million

representing 6% of its total assets

88

Applicability of accounting literature for IPR

� Under Indian GAAP, accounting for IPR is guided by:

- Accounting Standard 26 ‘Intangible Assets’

- Accounting Standard 10 ‘Fixed assets’ –

• As per AS 10, assets are grouped into various categories, such as

land, buildings, plant and machinery, vehicles, furniture and fittings,

goodwill, patents, trade marks and designsgoodwill, patents, trade marks and designs

� Accounting Standard 14 ‘Accounting for Amalgamations’

� Typical industries with IPRs

- Technology - Microsoft, IBM, Google, Wipro

- Pharma - Ranbaxy, Pfizer

- Media and Entertainment – Time Warner, Walt Disney

- Manufacturing - Pepsi, Coca Cola, Nokia

89

Impairment losses

� Recoverable amount of following assets to be determined at least ateach financial year end even if there is no indication of impairment:

– intangible assets not yet available for use

– intangible assets being amortised over a period exceeding ten years from

the date when they became available for use

– Intangible assets with indefinite useful life (under International GAAP)– Intangible assets with indefinite useful life (under International GAAP)

90

Derecognition

� Asset to be derecognised

– on disposal or

– when no future economic benefits are expected from its use and

subsequent disposal

91

AS 28 – Impairment of Assets

Angry young man

Sober old man

Tiger in the Woods

What is Impairment?

96

What is Impairment?(Continued)

At 60, Dadi

At 40, Bhabhi

At 16, Heroine

97

Again a new

You areBeautifulWith this dress

What is Impairment?(Continued)

Married since 7 months

Again a newdress ?

Married since 7 years

How much ?

Married since 7 days

98

w.e.f April 1, 2004

� Listed & in process of listing

� Turnover > 500 Mn

w.e.f April 1, 2005All Enterprises

Applicability

Excludes

Inventory

Financial Assets

Construction

contracts

Deferred Tax Asset

99

Recoverable

amount is greater

of:

Impairment Loss = Carrying Amount - Recoverable Amount

Impairment Concept

Net Selling Price (NSP)

determined by either of:

Binding Sale

Bid price in

Active Market

Best Estimate

Value in Use: NPV of

Cash Flows

Number

of Years

Discount

Rate

100

Impairment

Indications exist

No

Impairment

Review

Identify Asset

No Yes

Impairment Concept (Continued)

Review

Determine Recoverable

Amount

If indeterminate,

identify Cash-

Generating Unit

(CGU)

101

� A land is rented as a parking space as a result of which there is impairment.

However the land owner argues that an impairment provision is not required

since the land will soon be converted into a bowling alley, a highly profitable

business. Is that argument acceptable for not making an impairment

provision?

Case # 1 – Recoverability / Fair value

− Recoverability Test – Continuing use of asset

− Not a Fair Value Test – Market place assumption

− Future change – Not yet committed

102

70% of the Printing Press – New Plant has been completed. Due to some

financial problems further work came to a halt since the past one year. Is

impairment required to be provided on capital work-in-progress?

� Yes, Impairment is required.

Case # 2 – Impairment - CWIP

� Existing Carrying Amount is without expected future cash outflows

� Value in use to include future cash outflows before use/sale

103

Walt Disney Company

Amusement Park

Film ProductionMerchandise

104

� The Roller coaster in a theme park is damaged and is to be repaired

� This ride generates independent cash inflows

� The ride’s NSP (which is negligible) < Carrying Amount

� Value in use can be estimated

� The smallest identifiable CGU is the Theme park ? Or the ride? The Theme park taken

as a whole is not impaired

Case # 3A – Identification of CGU

as a whole is not impaired

� Assume no commitment to sell & replace the machine

� What is impaired?

� Recoverable Amount – Can be estimated for machine as well as the Theme Park

� However, Theme Park is not impaired

Only reassess depreciation method/period for machine

105

� Now assume, a commitment to sell and replace the machine

� Also, Cash flows from continuing use to be negligible

� What is impaired?

Case # 3B – Identification of CGU

� Machine

� Recoverable Amount – Can be estimated for machine

− Commitment to sell the machine &

− NSP > Value in Use

� Hence, no consideration to CGU

106

Admin++= Roller Coaster Ferry Wheel

How to arrive at Carrying Amount of CGU?

Admin+

Allocable Assets

-

Liabilities on Disposal

+

Assets Under CGU

= Roller Coaster Ferry Wheel

107

� While doing cash projection of following CGU that has assets with different remaining useful lives, how is the maximum period, up to which the cash flows should be projected is determined?

� Identify Primary asset of the CGU

� The Primary Asset is Rides, since

− Availability of Rides determines possibility of cash generation of the CGU

− No need of other assets unless entity has exciting Rides

Case # 4 – Useful life of CGU

− No need of other assets unless entity has exciting Rides

� Cannot be the asset not being amortized e.g. Land

Assets Balance Life Carrying Amt.

Sets 8 100 Mn

Building 6 20 Mn

Rides 10 85 Mn

Furniture 12 50 Mn

Computer 3 2 Mn

108

Admin Roller Coaster Ferry Wheel

Level at which Impairment required...

NilImpairment

60 MnNPV of rentals

50 MnCarrying Amount

Admin Roller Coaster Ferry Wheel

20 MnImpairment

230 MnNPV of Business Income

200 MnCarrying Amount of Others

50 MnCarrying Amount of Admin

109

Goodwill allocated, if any

Other assets: Pro-rata

Allocation of Impairment Loss on CGU

Ensure, Carrying Amount = Recoverable Amount

Else, balance Loss to be allocated to other assets

Other assets: Pro-rata

110

External Sources

Market Value ↓

Adverse External Env

Internal Sources

Physical Damage

Indicators

Adverse External Env

↑ Market ROI

Book Value > Mkt. Cap.

Poor Economic performance

Adv chg in Asset use

Formally estimate Recoverable Amount

111

Apply Bottom-Up test, if allocable

How is Impairment determined for Goodwill and

Corporate Asset?

Else, apply both Bottom-Up & Top-Down Tests

112

Application of Top-Down Test

(Rs in Mn) Goodwill Total

Carrying Amount 250 100 20 370

Impairment Loss for A under

Bottom up test

(20) - - (20)

Carrying Amount after loss 230 100 20 350

Recoverable Amount 340

Impairment Loss - Top Down (10)

113

Accounting Treatment

� Initial Losses to be adjusted against opening revenue reserves

� The Loss should be recognised as

− Revaluation decrease if asset was revalued earlier, else

− Expense in P&L

� After recognition, revise depreciation charge� After recognition, revise depreciation charge

� Recognise liability if, Loss > Carrying Amount

114

Treatment of Reversals

� Annually identify if Loss recognised earlier no longer exists

� Reversal if change in Cash Flow or Discount rate

� Carrying Amount <= original amortised Carrying Amount

� The Reversal should be recognised as

− Revaluation Increase if asset was revalued earlier, else

− Income in P&L

115

Disclosure requirements

� For each class of assets and reportable Segment, seperately

− Loss / Reversals recognised in P&L Account

− Loss / Reversals recognised against Revaluation Reserves

116

If material to the financial statements as a whole:

Relevant events and circumstances

Nature of asset / CGU

Disclosure requirements (Continued)

Nature of asset / CGU

Reportable Segment

Reasons for change, current and former CGU

Measurement of Recoverable Amount

117

Im p a irm e n t

In d ic a tio n s e x is t

N oIm p a irm e n t

R e v ie w

Id e n tify A s s e t

D e te rm in eR e c o ve ra b le A m o u n t

R e c o ve ra b leA m o u n t is g re a te r

o f:

N o

Y e s

If U n d e te rm in e d , id e n tifyC a s h -G e n e ra tin g U n it

V e r ify

Summary

N e t S e llin g P ric ed e te rm in e d b y

e ith e r o f:

B in d in gS a le

B id p ric e in

A c tiveM a rk e t

B e s tE s tim a te

V a lu e in U s e :N P V o f C F

C a rry in g A m o u n t >R e c o ve ra b le A m o u n t

N oIm p a irm e n t

P ro v is io n

Im p a irm e n t L o s s =C a rry in g A m o u n t - N e t

R e c o ve ra b le A m o u n t

T o b e fo llo w e d u p b yA n n u a l Im p a irm e n t

R e v ie w

N o

Y e s

N u m b e r o f

Y e a rs

D is c o u n tR a te

118

Key practice management issues

119

� Financial forecasts for maximum 5 years

� Steady / declining growth rate for extrapolating

� Do not consider

− Financial activities, receivables, payables and provisions

− Income tax receipts and payments

Cash Flows

− Income tax receipts and payments

− Non-committal future restructuring

− Proposed capital expenditure

� Foreign currency cash flows discounted at a rate appropriate to such currency. NPV to

be translated using the exchange rate at balance sheet date

� Cash Flow & Discount rate must reflect consistent assumptions about Inflation

120

� A pre-tax rate that reflects current time value of money and asset specific

risks

� Ignore risks for which future Cash Flows have been adjusted

� Rate of return that investors would expect from similar asset

� Weighted Average Cost of Capital (WACC) of a listed entity with similar

Discount Rate

� Weighted Average Cost of Capital (WACC) of a listed entity with similar

service potential and risks

� If benchmark not available, then consider entity’s own WACC or incremental

borrowing rate adjusted for:

− asset-specific risks

− country risks

− currency risks

121