Embed Size (px)

Citation preview

JointResearchCentre

1JointResearchCentre

The European Commission’sscience and knowledge service

Joint Research Centre

Fisheries, Aquaculture & Algae Biomass Assessment

BIOMASS Workshop @EUBCE 2017

Jordi Guillen, Gianluca Fiore & Rita AraujoFisheries & Aquaculture Sector

Water and Marine Resources Unit

2

Fisheries is not Forestry or Agriculture

Fisheries are different to other natural renewable-resource systems (more similar to hunting than toagriculture):

Ø Fish are not directly observable (e.g. how many fishare in the sea?). This implies high uncertainty.

Ø Fish are not directly manageable and have weakproperty rights (e.g. we cannot own a fish in the sea,so we cannot decide how to grow a fish).

Ø Analyses are complex (wild ecosystem with manyspecies and relations, as well as the environment).

Ø Main use of fish (seafood) products is foodconsumption (high value). Expressing them as drymatter makes no sense.

Fisheries and aquaculture: where we areFisheries

Ø Data collected and analysis ran using in-house modelling.

Ø Methods developed and tested, and gaps identified (referencepoints for stock without assessment, linking stocks to fishing fleetcomponents).

Aquaculture

Ø Production analysis based on official statistics; economicparameters based on STECF report.

Distribution (supply chain)

Ø Developed and input/output model to explore distribution,processing and usage of fishery products along the supply chain tosee the interactions between sectors and countries.

4

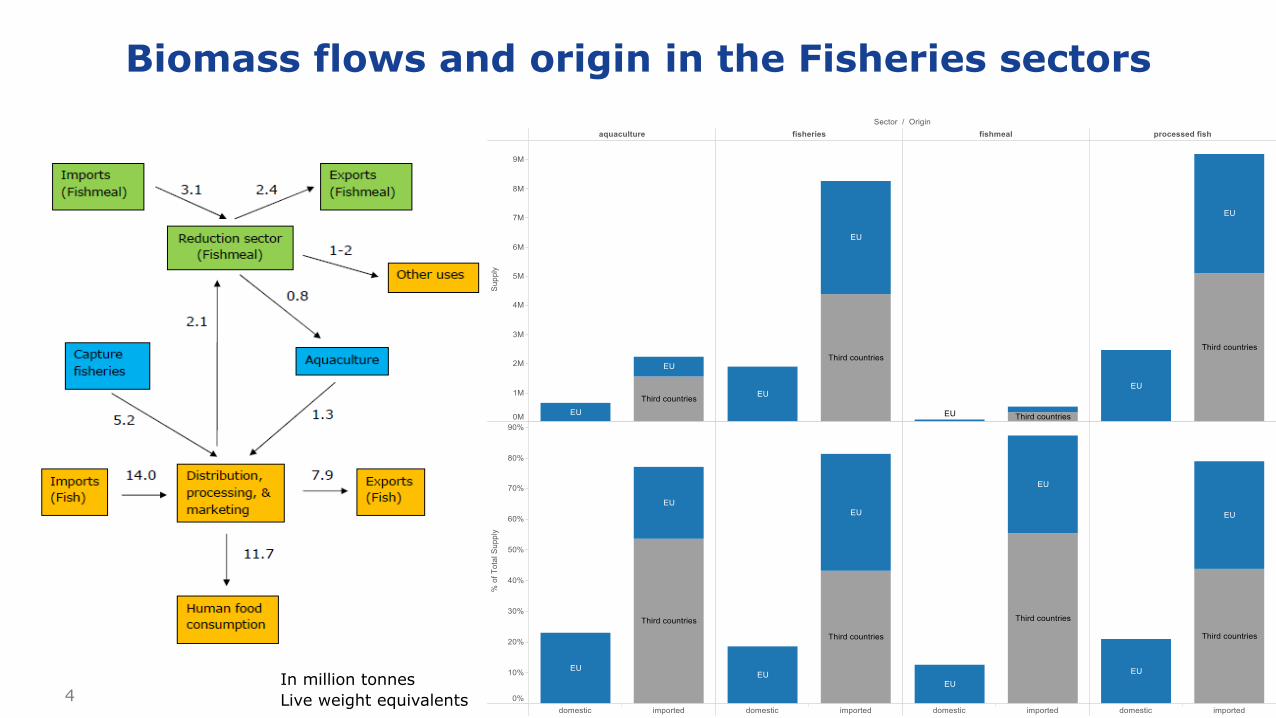

Biomass flows and origin in the Fisheries sectors

In million tonnesLive weight equivalents

5

F & A Main Highlights: Production

Ø EU Fisheries production has been stable/decreasing.

Ø Significant increases in production biomass from wild-capturefisheries in the short term are not expected since most stocks arefully or overexploited.

Ø Aquaculture is the fastest-growing animal food producing sector inthe world, but EU aquaculture production is not increasing.

Ø European Commission (2013) identified four strategic priorities forthe EU aquaculture sector. EU countries estimated that EUaquaculture production could increase 25% by 2020.

Ø Proportion of seafood products traded internationally is high andincreasing. Seafood consumption in EU countries: 21% originatesnationally, 35% in other EU countries and 44% from Third countries.

6

F & A Main Highlights: Distribution

Ø Over the past 50 years, global consumption of seafood percapita has more than doubled. Seafood consumption per capita indeveloping regions has increased even faster.

Ø According to UN, today’s world population of more than 7 billionwill rise to about 9 billion by 2030 and to 10 billion by 2050.

Ø Seafood protein represents an essential nutritional component insome densely populated countries, especially where total proteinintake levels are low.

Ø Demand from emerging economies is increasing and may affectglobal trade.

Ø Aquaculture is a net producer of food and biomass. Butproduction increases from aquaculture may have limits.

F & A Planning for 2017 and onwards

Ø Assessment of current biomass supply and potential:Fisheries stock assessment are essential to any biomass estimatebut often impeded by relevant data gaps. We collaborate withinternational partners by developing, validating and applying newdata poor assessment approaches.

Ø Better understand the origin of supply to the EU and if thesource is in good exploitation status, we will further disaggregatethe non-EU area.

Ø Supply chains: Disaggregation of the intra EU trade at MemberState level and further refinements if needed.

Ø Economic analysis of EU fisheries and aquaculture sectors.

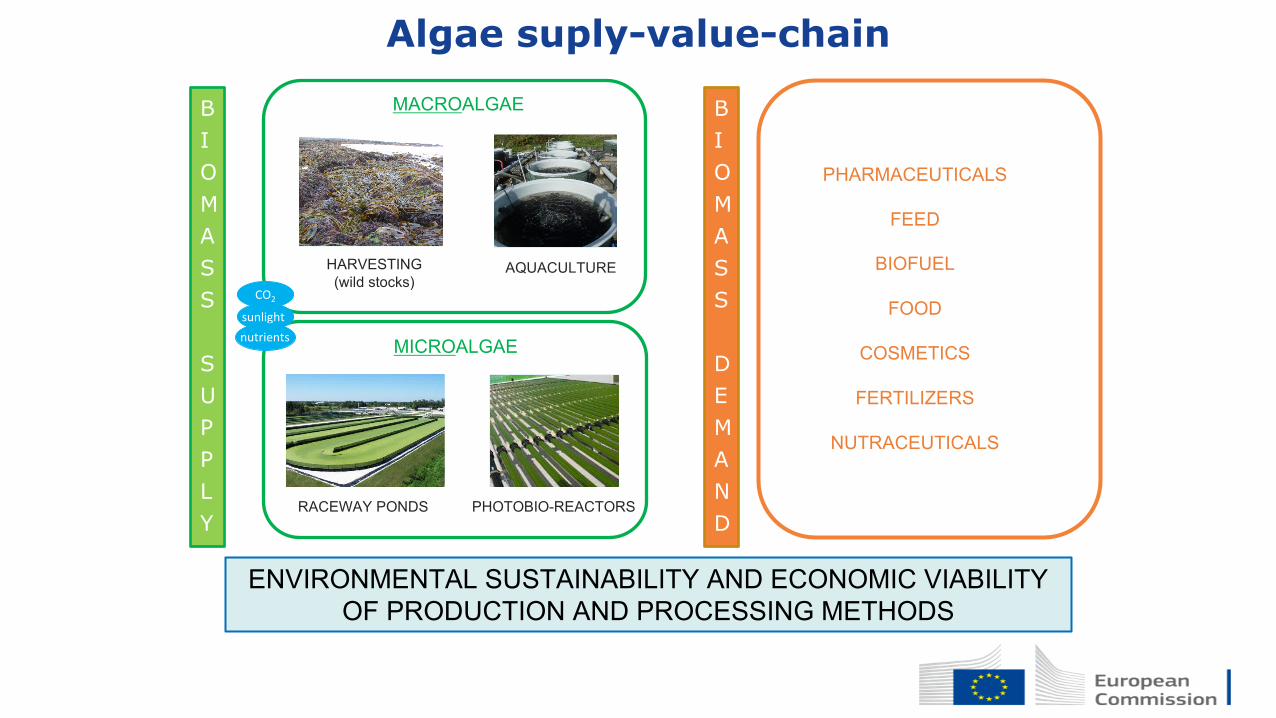

ENVIRONMENTAL SUSTAINABILITY AND ECONOMIC VIABILITY OF PRODUCTION AND PROCESSING METHODS

HARVESTING(wild stocks)

MACROALGAE

AQUACULTURE

RACEWAY PONDS

MICROALGAE

PHOTOBIO-REACTORS

CO2

sunlightnutrients

BIOMASS

SUPPLY

BIOMASSDEMAND

PHARMACEUTICALS

FEED

BIOFUEL

FOOD

COSMETICS

FERTILIZERS

NUTRACEUTICALS

BIOMASS

DEMAND

Algae suply-value-chain

PRODUCTION and SUPPLY CHAIN

Algae biomass: where we are

Ø Available data collected and main knowledge gaps identified

Ø Development of alternative approaches to fill knowledge gaps

Ø Deficient data obtained from official statistics regarding data reporting for

country, year and species resolution

Ø Production and trade volume organized by country and aggregated at the EU and global level

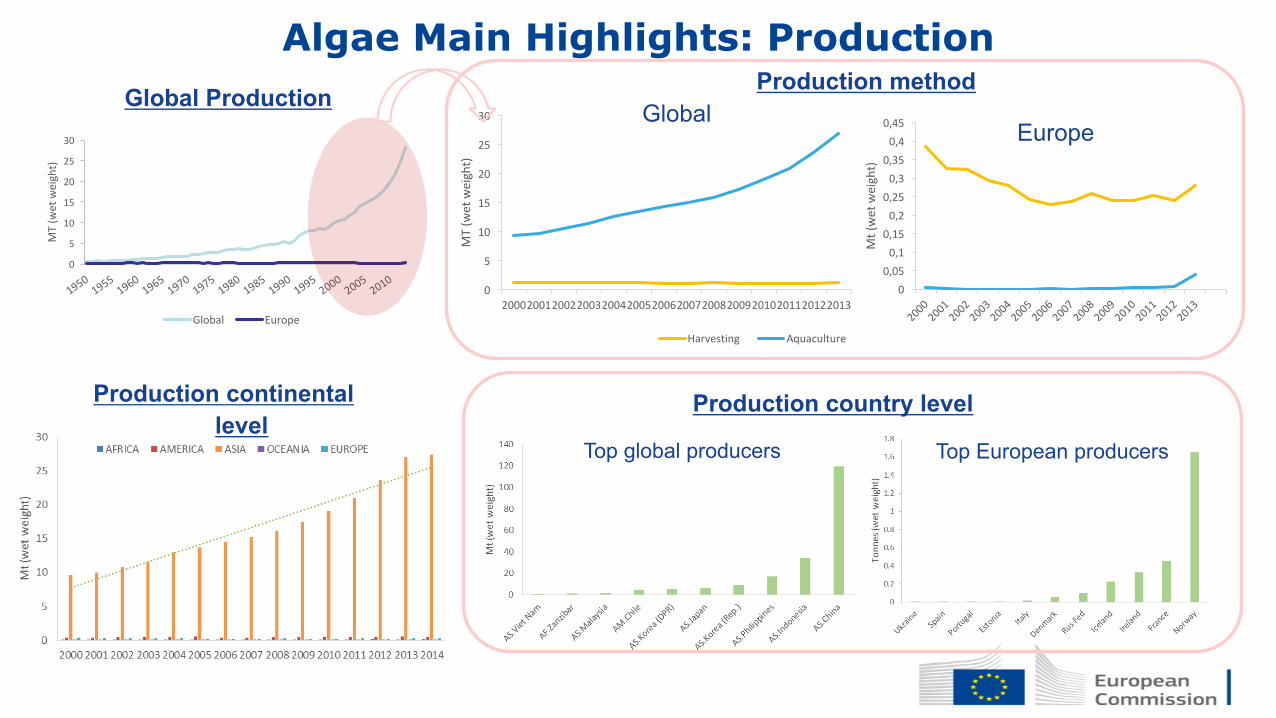

Algae Main Highlights: Production

Europe

0

5

10

15

20

25

30

MT(w

etweight)

Global Europe

00,050,10,150,20,250,30,350,40,45

Mt(wetweight)

Production method

0

5

10

15

20

25

30

20002001200220032004200520062007200820092010201120122013

MT(w

etweight)

Harvesting Aquaculture

Global

Production continental level

Top global producers Top European producers

Production country level

Global Production

0

1

2

3

4

5

6

7

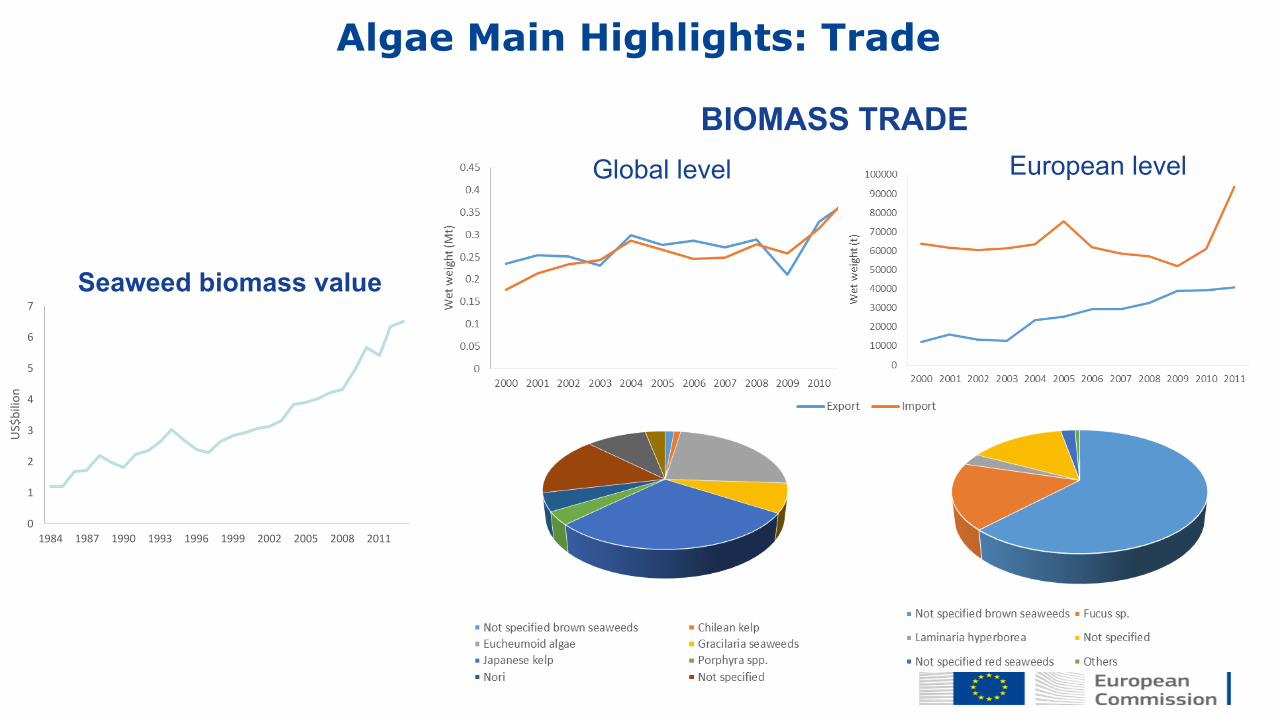

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

US$b

ilion

Seaweed biomass value

Algae Main Highlights: Trade

BIOMASS TRADEGlobal level European level

Thank you very much!

JRCScienceHub:ec.europa.eu/jrc

Twitter:@EU_ScienceHub

Facebook:EUScienceHub– JointResearchCentre

LinkedIn:JointResearchCentre(JRC)- EuropeanCommission'sScienceService

YouTube:JRCAudiovisuals

Vimeo:Science@EC

Fisheries & Aquaculture: Jordi Guillen ([email protected])

Fisheries & Aquaculture: Gianluca Fiore ([email protected])

Algae: Rita Araujo ([email protected])