Embed Size (px)

Citation preview

FISCAL POLICY IN SOUTH AFRICA: AN INTERTEMPORAL

CGE ANALYSIS

Margaret Chitiga, Ramos Mabugu, Hélène Maisonnave and Véronique Robichaud

For an Equitable Sharing of National Revenue

OUTLINE OF THE PRESENTATION

• Aims and Objectives• Methodology• Results• Conclusion

2Workshop Name

Date 2011

AIMS AND OBJECTIVES

• New Growth Plan involves accelerated investment program in social and economic infrastructure and general government spending

• These expansionary fiscal strategies raise a number of critical policy questions:– composition of spending – financing strategies (taxation or increased debt)

• How would these policies and their financing affect the South African economy in the short, medium and long run?

• CGE analysis in a forward-looking perspective3

Workshop NameDate 2011

METHODOLOGY - JUSTIFICATION

• CGE analysis that allows taking into account all the linkages between productive sectors, demand, international trade and macroeconomic constraints

• As measures are known in advance, a forward-looking behaviour (for firms and households) is more suitable

• Impact of infrastructure on economic growth is taken into account

4Workshop Name

Date 2011

METHODOLOGY - OVERVIEW

• Multi-sector analysis (19 industries and commodities)

• Intertemporal framework: all current and future prices are known and affect firms investment decision and households consumption pattern

• Taxation options: many tax instruments are explicitly modelled to allow for a wide variety of policy responses

5Workshop Name

Date 2011

METHODOLOGY - FIRMS

• Representative firm in each industry that combines labour, capital and intermediate inputs to produce composite commodities that can be sold either locally or exported.

• Constant returns to scale technology • Competitive environment in the good markets, as

well as in factor markets.

6Workshop Name

Date 2011

METHODOLOGY - FIRMS

• Nested structure:

7Workshop Name

Date 2011

Total output

Value added Total intermediate cons.

Capital Labour Int. cons. by commodity

Leontief

LeontiefCES

METHODOLOGY - FIRMS

• Nested structure:

8Workshop Name

Date 2011

Total output

Value added Total intermediate cons.

Capital Labour Int. cons. by commodity

j

tj

j

tjtj io

CI

v

VAXST

,,, ,min

VAj

VAj

VAjINF

tjVAjtj

VAj

VAj

INFttj KDLDBKDVA

1

,,, 1

ji

tjitj aij

DICI

,

,,, min

METHODOLOGY - FIRMS

9Workshop Name

Date 2011

VAj

VAj

VAjINF

tjVAjtj

VAj

VAj

INFttj KDLDBKDVA

1

,,, 1

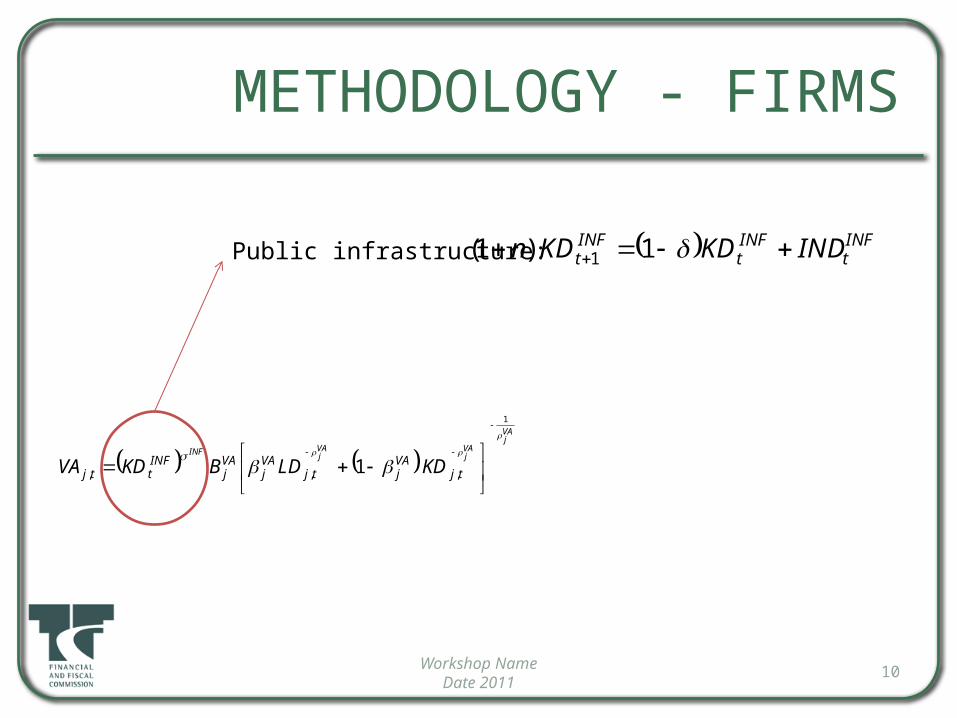

Public infrastructure:

METHODOLOGY - FIRMS

10Workshop Name

Date 2011

VAj

VAj

VAjINF

tjVAjtj

VAj

VAj

INFttj KDLDBKDVA

1

,,, 1

Public infrastructure: INFt

INFt

INFt INDKDKDn 1)1( 1

METHODOLOGY - FIRMS

• Standard static optimization problem yields the first order conditions:

11Workshop Name

Date 2011

tjjtj XSTvVA ,,

tjjtj XSTioCI ,, VAj

tj

tj

VAj

VAj

tj

tj

WTI

RTI

KD

LD

,

,

,

,

1

tjjitji CIaijDI ,,,,

METHODOLOGY - FIRMS

• Intertemporal optimization: the representative forward-looking firm maximizes the actualized value of profits net of investment expenditures:

subject to:– Profits

12Workshop Name

Date 2011

T

t

Ttjttjtj

t

t

INDPKKDrir1

,,,1

1max

tjtji

tjititjtjttjtjtjtj KDttikDIPCLDttiwwXSPPKDr ,,,,,,,,,,, )1(

METHODOLOGY - FIRMS

– Capital stock accumulation:

– Adjustment cost function (Hayashi 1982):

13Workshop Name

Date 2011

tjtjjtj INDKDKDn ,,1, 1)1(

tjtj

tjjTtj IND

KD

INDIND ,

,

,, 2

1

METHODOLOGY - FIRMS

From the first order conditions, we find:– Optimum level of investment:

– Desired future capital stock:

14Workshop Name

Date 2011

tbus

tbusbusttbus KD

INDPKq

,

,, 1

2

1,

1,11,1,,1, 2

111

tbus

tbusbusttbustbusttbusbustbus KD

INDPKttikrirqq

METHODOLOGY - HOUSEHOLDS

• Finite number of infinitely-lived households• The representative household makes

consumption and savings decisions • It derives its current income from wages and

profits paid by firms, and pays income tax. • It maximizes an intertemporal utility function

subject to a sequence of budget constraints and an intertemporal solvency constraint.

15Workshop Name

Date 2011

METHODOLOGY - HOUSEHOLDS

• The intertemporal utility function is additively separable, features a constant rate of time preference and an instantaneous logarithmic utility function that is weakly separable and defined over aggregate consumption CTH.

from which we derive the trade-off between consumption in two consecutive periods (Euler equation):

16Workshop Name

Date 2011

T

tt

t

HCTHu

1

ln1

1max

ttH

t irCTHCTH 111

METHODOLOGY - HOUSEHOLDS

• Based on the optimal path for aggregate consumption consumption expenditures, the representative household allocates in each period these expenditures among the available commodities (Ci).

• A Linear Expenditure System (LES) function is used as the aggregator function to specify the relation between aggregate consumption and the quantities of various commodities consumed by the representative household.

17Workshop Name

Date 2011

ijtij

MINtijt

LESiti

MINtititi PCCCTHPCCPCC ,,,,,,

METHODOLOGY - GOVERNMENT

• The government collects various direct and indirect taxes:– Income taxes (firms and households)– Taxes on production and on factors of production– Import duties and export taxes– Taxes on commodities

• It receives and pays transfers, and consumes goods and services (current and investment).

• It also pays interest on the public domestic and foreign debt for which interests rates can differ and are exogenous

18Workshop Name

Date 2011

METHODOLOGY - GOVERNMENT

• The government finances the excess of its current and investment expenditures over its revenue by issuing bonds (SG).

• A positive balance implies that the government would reimburse part of its debt, whereas a negative balance would increase it.

19Workshop Name

Date 2011

PUBt

ROWt

DOMtt

agngtGVTagngtt ITINTINTGTRYGSG ,,

t

DOMt

ROWt

ROWt

DOMtt

DOMt

DOMt

ROWt

ROWt

TOTt

SGDebtDebt

INTINTSGDebtirDebtirDebtn

111 1

METHODOLOGY - CLOSURES

• Small open economy hypothesis (world prices are given)• Constant current account balance• Fixed repartition between domestic and foreign debt• Nominal exchange rate is the numéraire

20Workshop Name

Date 2011

RESULTS-SIMULATIONS

• Two simulations:– Increased current public spending

• 10% in 2011 and 2012 • 2% in 2013,2014 and 2015• back to BAU in 2016

– Increased public investment • 10% in 2011 and 2012 • 2% in 2013,2014 and 2015• back to BAU in 2016

21Workshop Name

Date 2011

RESULTS-SIMULATIONS

• Under three financing mechanisms:– Increased income tax rate on households’ income– Increased indirect tax rate on commodities– Increased debt

• Caveats:– Public investment in infrastructure is assumed to increase total factor

productivity– But public current spending does not affect productivity (period of

increased spending is assumed too short to significantly impact productivity)

22Workshop Name

Date 2011

RESULTS-SIMULATION 1

• Increased public expenditures has little impact on GDP, regardless of the timeframe.

23Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 1.18% 0.07% -0.10% -0.54% -0.42% -0.23% 1.14% 0.04% -0.12%

GDP deflator 1.19% 0.38% 0.11% -0.56% 0.15% 0.16% 1.15% 0.35% 0.10%

Real GDP -0.01% -0.31% -0.20% 0.02% -0.57% -0.39% -0.01% -0.32% -0.21%

Real consumption -1.07% -0.71% -0.24% -1.65% -0.81% -0.40% -1.09% -0.74% -0.27%

Real investment -5.56% -0.77% -0.05% -2.54% -1.27% -0.28% -5.69% -0.81% -0.07%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 1.97% 2.08%

Gov. expenditures 5.92% 1.22% 0.03% 6.23% 1.36% 0.07% 5.91% 1.43% 0.25%

Increase in tax rate 2.65% 0.63% 0.06% 1.01% 0.26% 0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 1

• Affects negatively real investment, especially in the short run and under direct tax and debt financing.

24Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 1.18% 0.07% -0.10% -0.54% -0.42% -0.23% 1.14% 0.04% -0.12%

GDP deflator 1.19% 0.38% 0.11% -0.56% 0.15% 0.16% 1.15% 0.35% 0.10%

Real GDP -0.01% -0.31% -0.20% 0.02% -0.57% -0.39% -0.01% -0.32% -0.21%

Real consumption -1.07% -0.71% -0.24% -1.65% -0.81% -0.40% -1.09% -0.74% -0.27%

Real investment -5.56% -0.77% -0.05% -2.54% -1.27% -0.28% -5.69% -0.81% -0.07%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 1.97% 2.08%

Gov. expenditures 5.92% 1.22% 0.03% 6.23% 1.36% 0.07% 5.91% 1.43% 0.25%

Increase in tax rate 2.65% 0.63% 0.06% 1.01% 0.26% 0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 1

• Implies increased income tax rates by 2.65 or increased indirect tax rates by 1 (temporary tax)

25Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 1.18% 0.07% -0.10% -0.54% -0.42% -0.23% 1.14% 0.04% -0.12%

GDP deflator 1.19% 0.38% 0.11% -0.56% 0.15% 0.16% 1.15% 0.35% 0.10%

Real GDP -0.01% -0.31% -0.20% 0.02% -0.57% -0.39% -0.01% -0.32% -0.21%

Real consumption -1.07% -0.71% -0.24% -1.65% -0.81% -0.40% -1.09% -0.74% -0.27%

Real investment -5.56% -0.77% -0.05% -2.54% -1.27% -0.28% -5.69% -0.81% -0.07%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 1.97% 2.08%

Gov. expenditures 5.92% 1.22% 0.03% 6.23% 1.36% 0.07% 5.91% 1.43% 0.25%

Increase in tax rate 2.65% 0.63% 0.06% 1.01% 0.26% 0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 1

• Debt financing mechanism implies greater debt-to GDP ratio, even in the very long run

26Workshop Name

Date 2011

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2056

2057

2058

2059

2060

0.98

0.985

0.99

0.995

1

1.005

1.01

1.015

1.02

1.025

1.03BAU SIM1-direct tax SIM1-indirect tax SIM1-Debt

Direct tax financing Indirect tax financing Debt financing

2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 0.02% 0.15% 0.17% -0.22% 0.16% 0.26% 0.02% 0.15% 0.17%

GDP deflator 0.02% -0.34% -0.27% -0.22% -0.33% -0.25% 0.02% -0.34% -0.27%

Real GDP 0.00% 0.49% 0.44% 0.00% 0.49% 0.51% 0.00% 0.49% 0.44%

Real consumption 0.07% 0.30% 0.37% -0.09% 0.23% 0.37% 0.07% 0.30% 0.38%

Real investment -0.21% 0.89% 0.51% 0.46% 1.12% 0.79% -0.25% 0.88% 0.51%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.17% -0.15%

Gov. expenditures 0.73% 0.07% -0.07% 0.76% 0.06% -0.10% 0.73% 0.08% -0.08%

Increase in tax rate 0.34% -0.03% -0.11% 0.13% -0.01% -0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 2

• Increased public investment has greater impact on GDP, especially in the long run (TFP effect)

27Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing

2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 0.02% 0.15% 0.17% -0.22% 0.16% 0.26% 0.02% 0.15% 0.17%

GDP deflator 0.02% -0.34% -0.27% -0.22% -0.33% -0.25% 0.02% -0.34% -0.27%

Real GDP 0.00% 0.49% 0.44% 0.00% 0.49% 0.51% 0.00% 0.49% 0.44%

Real consumption 0.07% 0.30% 0.37% -0.09% 0.23% 0.37% 0.07% 0.30% 0.38%

Real investment -0.21% 0.89% 0.51% 0.46% 1.12% 0.79% -0.25% 0.88% 0.51%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.17% -0.15%

Gov. expenditures 0.73% 0.07% -0.07% 0.76% 0.06% -0.10% 0.73% 0.08% -0.08%

Increase in tax rate 0.34% -0.03% -0.11% 0.13% -0.01% -0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 2

• Stimulates real consumption (especially in the longer run)

28Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing

2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 0.02% 0.15% 0.17% -0.22% 0.16% 0.26% 0.02% 0.15% 0.17%

GDP deflator 0.02% -0.34% -0.27% -0.22% -0.33% -0.25% 0.02% -0.34% -0.27%

Real GDP 0.00% 0.49% 0.44% 0.00% 0.49% 0.51% 0.00% 0.49% 0.44%

Real consumption 0.07% 0.30% 0.37% -0.09% 0.23% 0.37% 0.07% 0.30% 0.38%

Real investment -0.21% 0.89% 0.51% 0.46% 1.12% 0.79% -0.25% 0.88% 0.51%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.17% -0.15%

Gov. expenditures 0.73% 0.07% -0.07% 0.76% 0.06% -0.10% 0.73% 0.08% -0.08%

Increase in tax rate 0.34% -0.03% -0.11% 0.13% -0.01% -0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 2

• Affects real investment negatively in the short run, but positively in the medium and long run

29Workshop Name

Date 2011

Direct tax financing Indirect tax financing Debt financing

2011 2015 2025 2011 2015 2025 2011 2015 2025

GDP 0.02% 0.15% 0.17% -0.22% 0.16% 0.26% 0.02% 0.15% 0.17%

GDP deflator 0.02% -0.34% -0.27% -0.22% -0.33% -0.25% 0.02% -0.34% -0.27%

Real GDP 0.00% 0.49% 0.44% 0.00% 0.49% 0.51% 0.00% 0.49% 0.44%

Real consumption 0.07% 0.30% 0.37% -0.09% 0.23% 0.37% 0.07% 0.30% 0.38%

Real investment -0.21% 0.89% 0.51% 0.46% 1.12% 0.79% -0.25% 0.88% 0.51%

Debt 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.17% -0.15%

Gov. expenditures 0.73% 0.07% -0.07% 0.76% 0.06% -0.10% 0.73% 0.08% -0.08%

Increase in tax rate 0.34% -0.03% -0.11% 0.13% -0.01% -0.04% n.a. n.a. n.a.

RESULTS-SIMULATION 2

• Would require small tax increase in the short run but translate into tax reduction in the longer term

30Workshop Name

Date 2011

RESULTS-SIMULATION 2

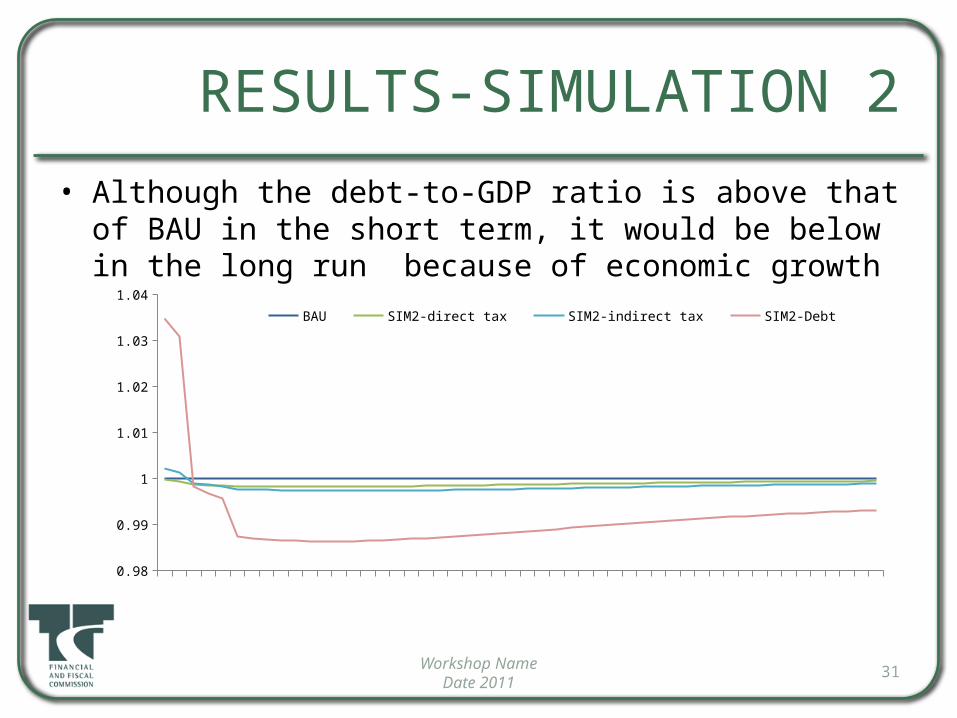

• Although the debt-to-GDP ratio is above that of BAU in the short term, it would be below in the long run because of economic growth

31Workshop Name

Date 2011

20112013

20152017

20192021

20232025

20272029

20312033

20352037

20392041

20432045

20472049

20512053

20552057

20590.98

0.99

1

1.01

1.02

1.03

1.04

BAU SIM2-direct tax SIM2-indirect tax SIM2-Debt

RESULTS-SIMULATION 2

• Different values of elasticity would change the amplitude of the impact on GDP by less than 1%.

32Workshop Name

Date 2011

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2056

2057

2058

2059

99.4

99.6

99.8

100

100.2

100.4

100.6

100.8

101

101.2

BAU 0.1-direct tax 0.1-indirect tax0.1-Debt 0.3-direct tax 0.3-indirect tax0.3-Debt 0.6-direct tax 0.6-indirect tax0.6-Debt

RESULTS-SIMULATION 2

• Similar conclusion for the debt-to-GDP ratio

33Workshop Name

Date 2011

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2056

2057

2058

2059

0.970000000000001

0.975000000000001

0.980000000000001

0.985000000000001

0.990000000000001

0.995000000000001

1

1.005

BAU 0.1-direct tax 0.1-indirect tax0.1-Debt 0.3-direct tax 0.3-indirect tax0.3-Debt 0.6-direct tax 0.6-indirect tax0.6-Debt

CONCLUSIONS

• Current expenditures:– Increase in current expenditures has little impact on the economy– Including TFP impact would significantly change the results.

(Would a 5-year increase be sufficient to impact TFP?)– Debt financing would require future intervention in order to go

back to the initial debt-to-GDP ratio.

34Workshop Name

Date 2011

CONCLUSIONS

• Investment expenditures:– Short term public investment in infrastructure would affect TFP– Positive impact on macroeconomic impacts, especially in the

medium run– Reduces the debt-to-GDP ratio, regardless of the financing

mechanism (economic growth).

35Workshop Name

Date 2011