Embed Size (px)

Citation preview

FIRST TELECOMMUNICATION REGULATORY MEETING FOR THE ARAB REGION

CORPORATE NETWORKS AND OPENING OF FIXED SERVICES

Mostafa TERRAB

Lead Regulatory Specialist

ALGIERS, April 19, 2003

OUTLINE

• Why are competitive fixed-services and corporate networks important?

• Regional telecom specificities

• Options for improving fixed-services and corporate network provision

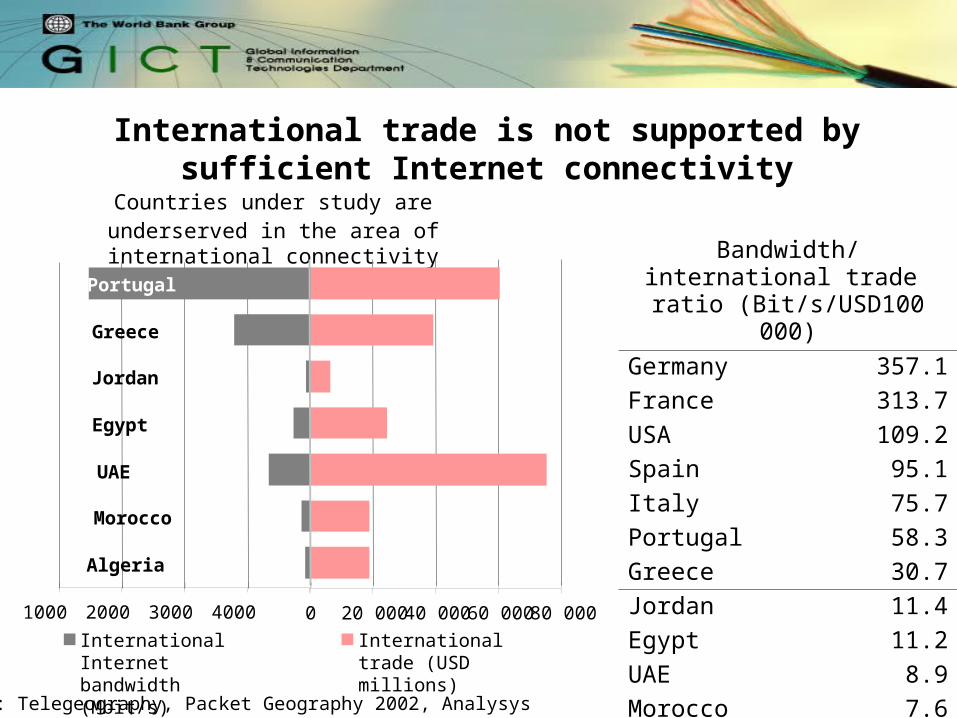

International trade is not supported by sufficient Internet connectivity

Countries under study are underserved in the area of international connectivity

Source: Telegeography, Packet Geography 2002, Analysys

0 20 000 40 000 60 000 80 000

Algeria

Morocco

UAE

Egypt

Jordan

Greece

Portugal

1000 2000 3000 4000

International trade (USD millions)

International Internet bandwidth (Mbit/s)

Bandwidth/international trade ratio (Bit/s/USD100 000)

Germany 357.1

France 313.7

USA 109.2

Spain 95.1

Italy 75.7

Portugal 58.3

Greece 30.7

Jordan 11.4

Egypt 11.2

UAE 8.9

Morocco 7.6

Algeria 4.6

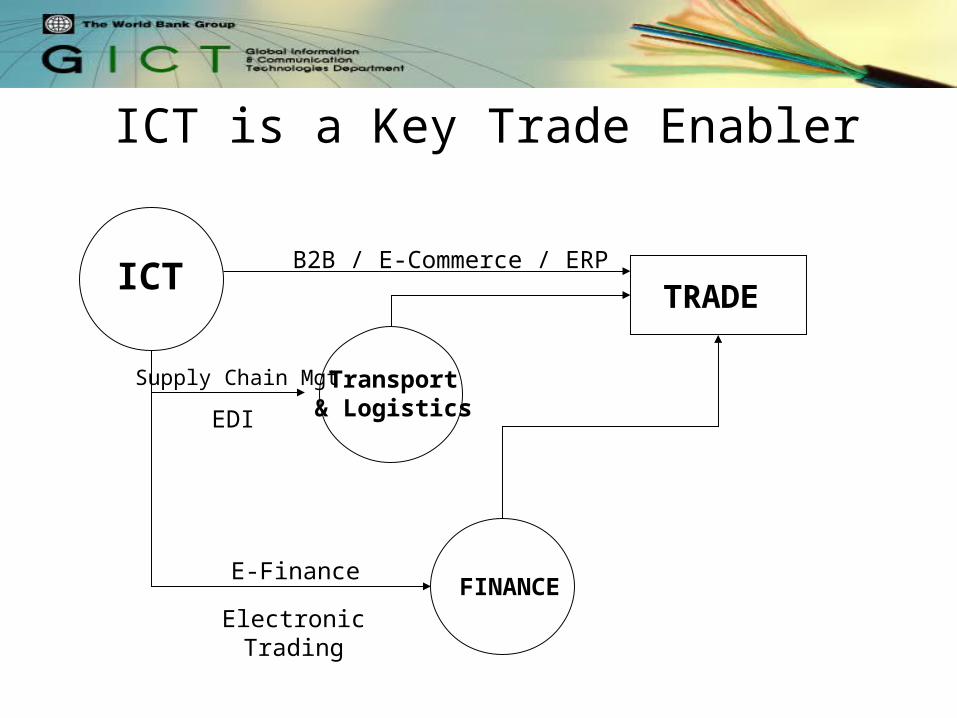

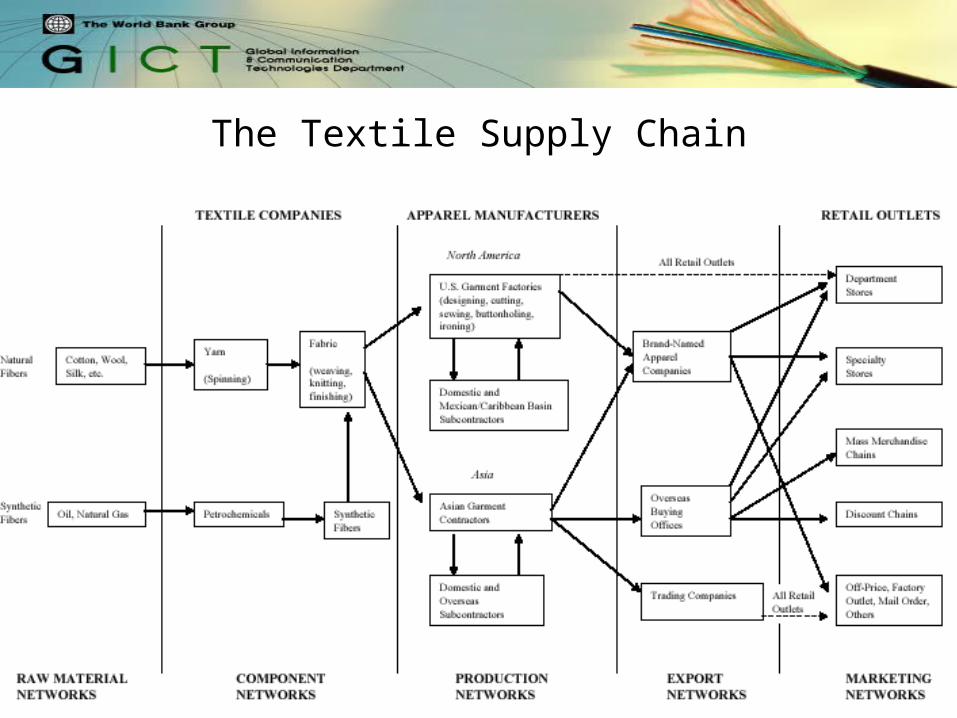

ICT is a Key Trade Enabler

ICTTRADE

FINANCE

Transport& Logistics

B2B / E-Commerce / ERP

E-Finance

Supply Chain Mgt

EDI

ElectronicTrading

The Textile Supply Chain

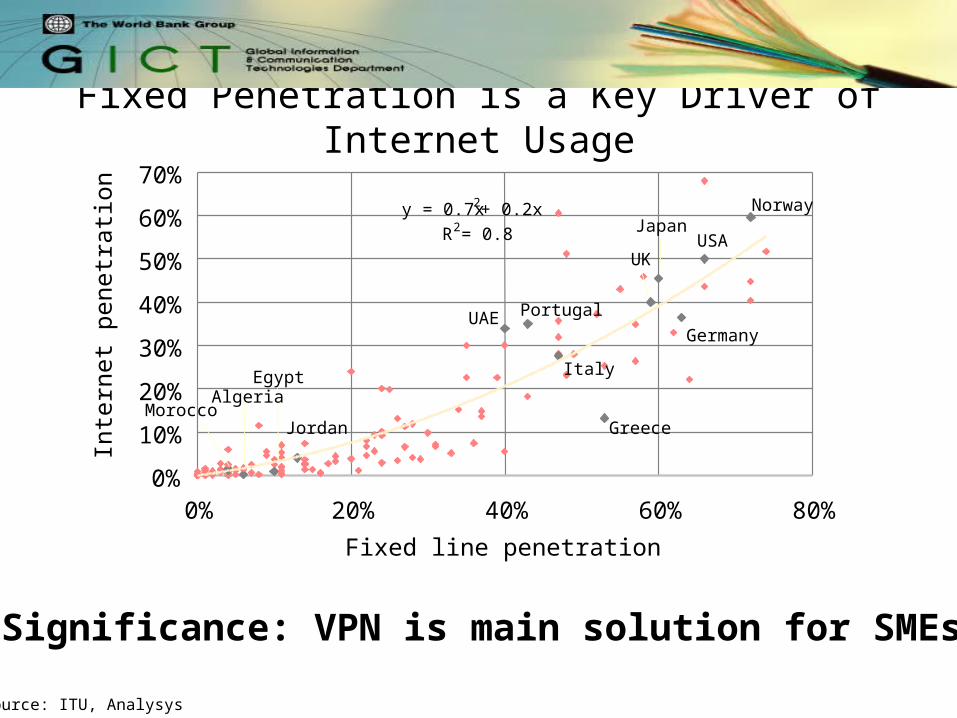

Fixed Penetration is a Key Driver of Internet Usage

Source: ITU, Analysys

y = 0.7x2 + 0.2x

R2 = 0.8

0%

10%

20%

30%

40%

50%

60%

70%

0% 20% 40% 60% 80%

Fixed line penetration

Inte

rnet

pen

etra

tion

AlgeriaMorocco

Egypt

Jordan

UAE

Greece

Germany

Italy

Portugal

UKUSA

JapanNorway

Significance: VPN is main solution for SMEs

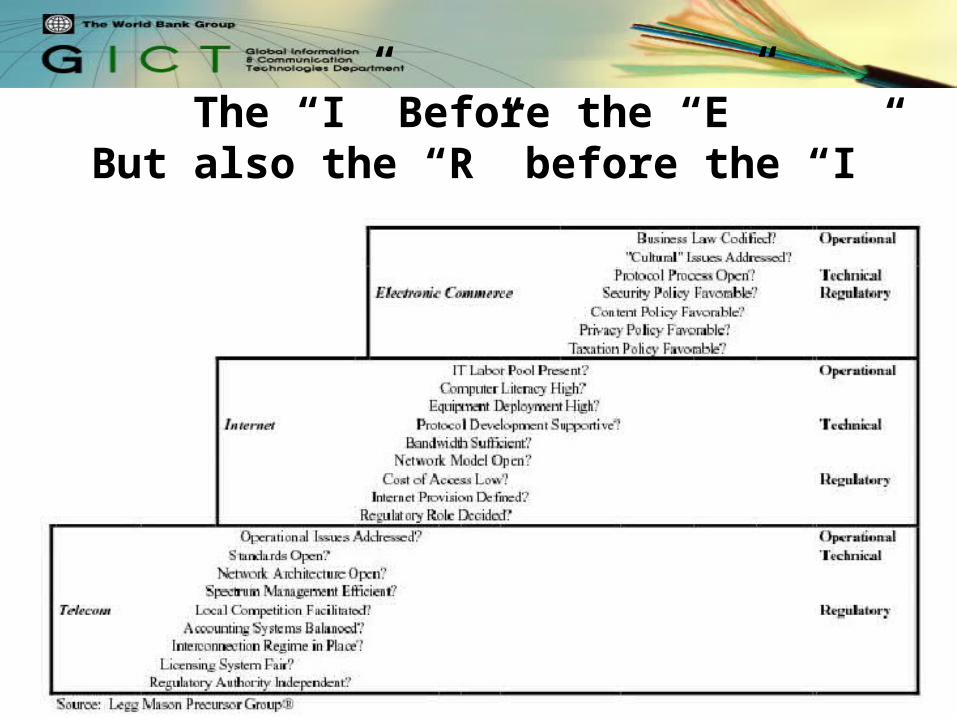

The “I” Before the “E” But also the “R” before the “I”

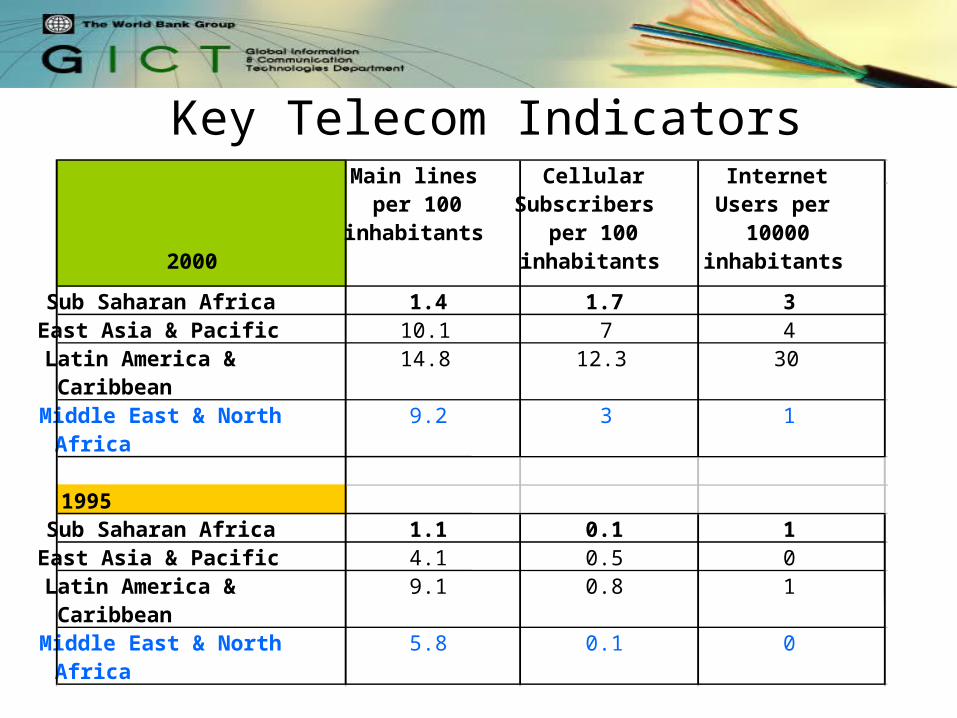

Key Telecom Indicators

Sub Saharan Africa 1.4 1.7 3East Asia & Pacific 10.1 7 4Latin America & Caribbean

14.8 12.3 30

Middle East & North Africa

9.2 3 1

1995Sub Saharan Africa 1.1 0.1 1East Asia & Pacific 4.1 0.5 0Latin America & Caribbean

9.1 0.8 1

Middle East & North Africa

5.8 0.1 0

2000

Main lines per 100

inhabitants

Cellular Subscribers

per 100 inhabitants

Internet Users per

10000 inhabitants

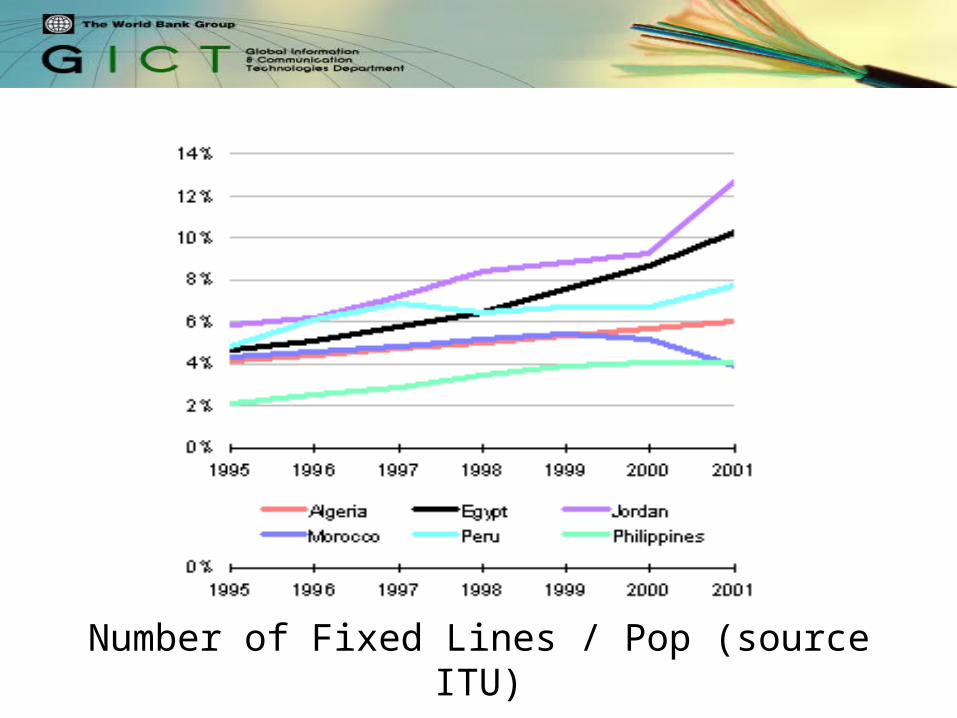

Number of Fixed Lines / Pop (source ITU)

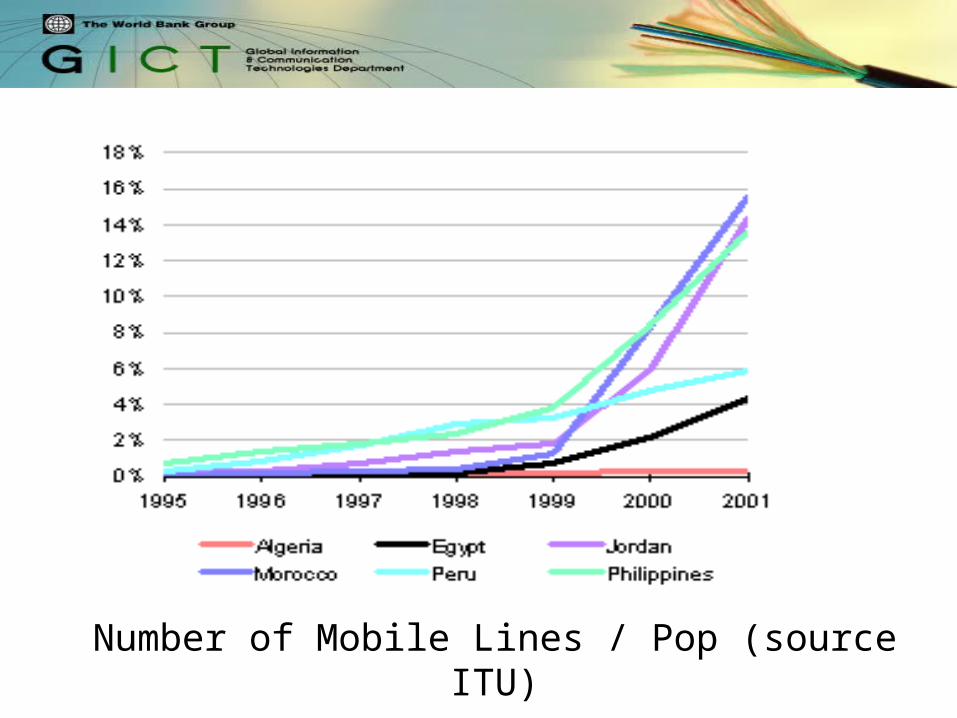

Number of Mobile Lines / Pop (source ITU)

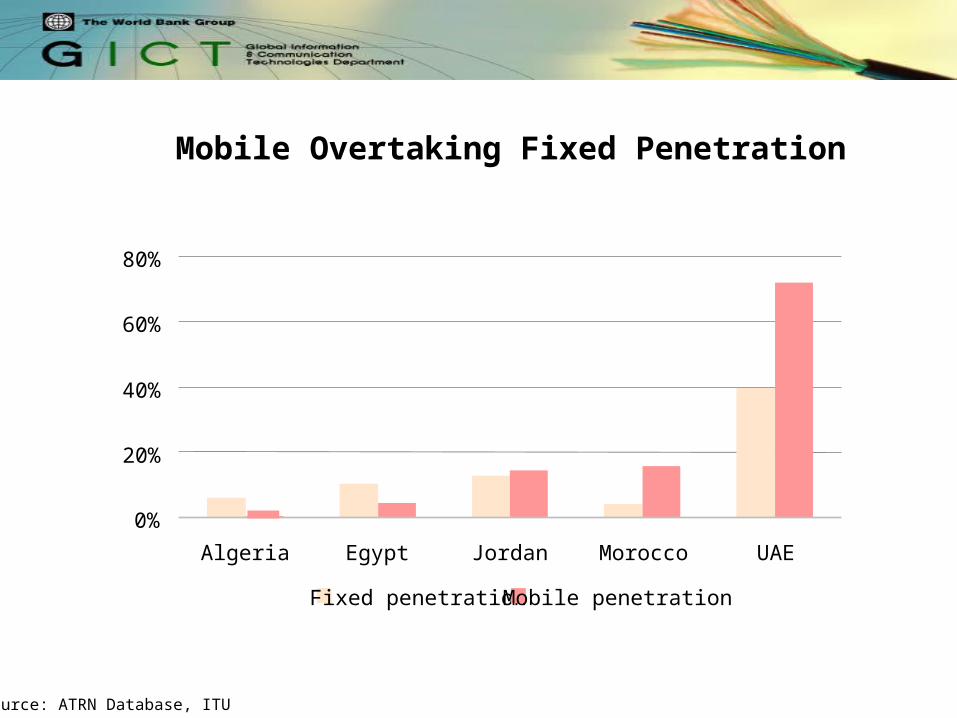

Source: ATRN Database, ITU

Mobile Overtaking Fixed Penetration

0%

20%

40%

60%

80%

Algeria Egypt Jordan Morocco UAE

Fixed penetration Mobile penetration

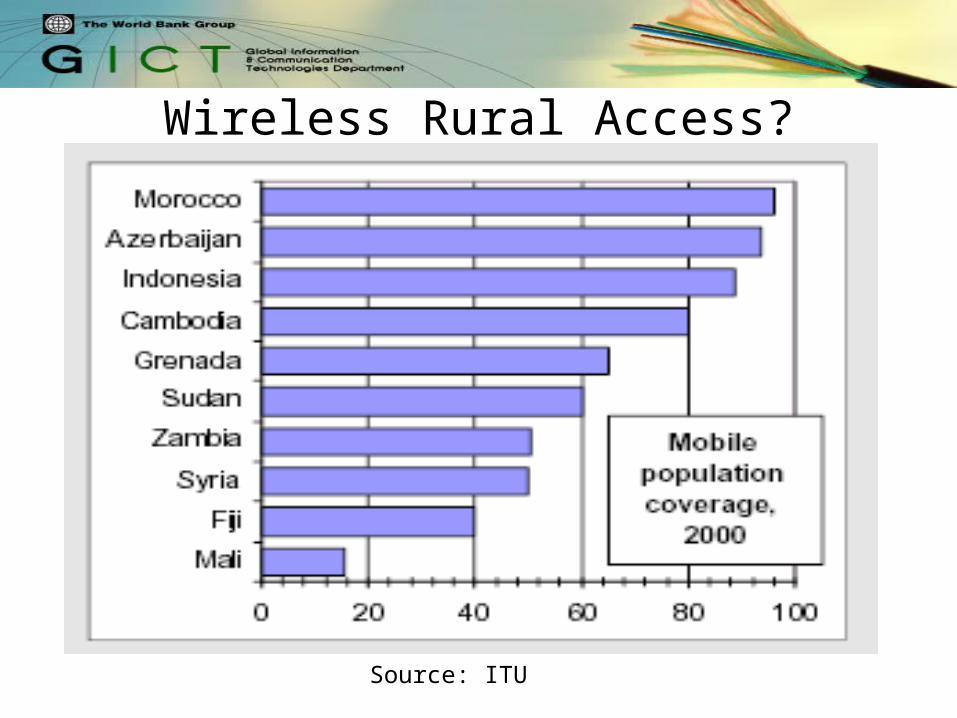

Wireless Rural Access?

Source: ITU

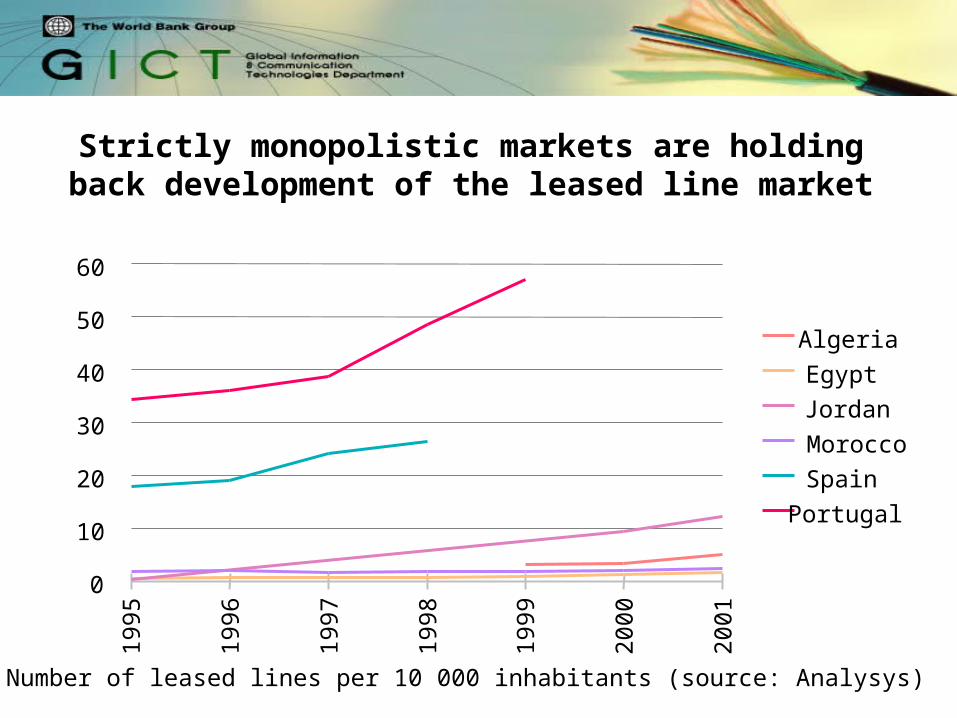

Strictly monopolistic markets are holding back development of the leased line market

Number of leased lines per 10 000 inhabitants (source: Analysys)

0

10

20

30

40

50

60

1995

1996

1997

1998

1999

2000

2001

Algeria

Egypt

Jordan

Morocco

Spain

Portugal

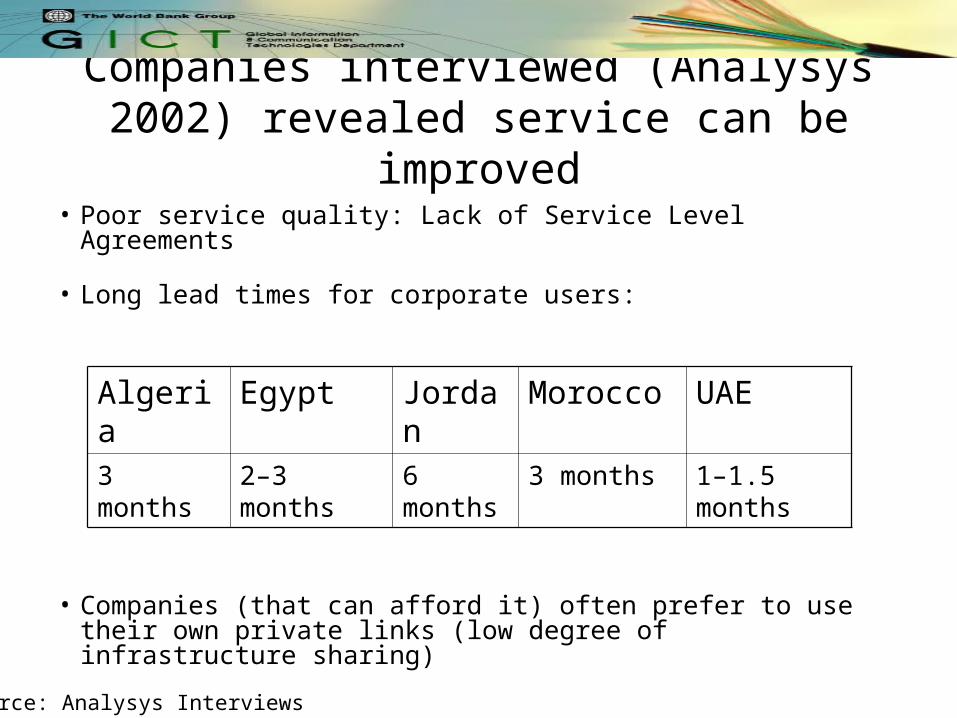

Companies interviewed (Analysys 2002) revealed service can be improved

• Poor service quality: Lack of Service Level Agreements

• Long lead times for corporate users:

• Companies (that can afford it) often prefer to use their own private links (low degree of infrastructure sharing)

Algeria Egypt Jordan Morocco UAE3 months 2–3 months 6

months3 months 1–1.5

months

Source: Analysys Interviews

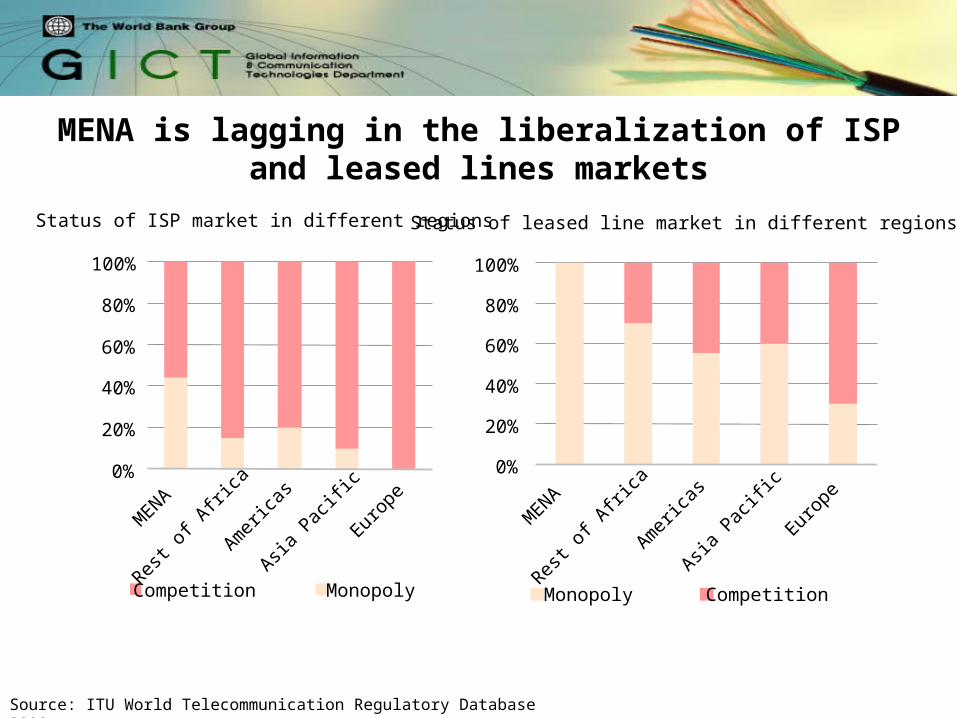

MENA is lagging in the liberalization of ISP and leased lines markets

Source: ITU World Telecommunication Regulatory Database 2000

Status of leased line market in different regions

0%

20%

40%

60%

80%

100%

MENA

Rest o

f Afri

ca

Amer

icas

Asia P

acific

Europ

e

Monopoly Competition

Status of ISP market in different regions

0%

20%

40%

60%

80%

100%

MENA

Rest o

f Afri

ca

Amer

icas

Asia P

acific

Europ

e

Competition Monopoly

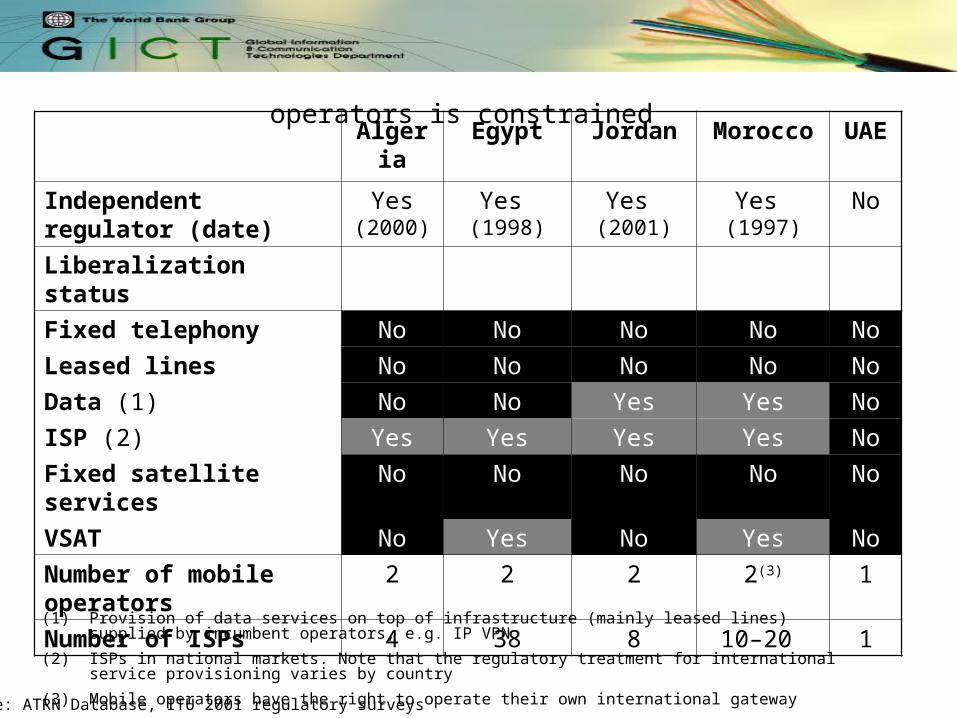

Data and leased lines delivery by alternative operators is constrained Algeria Egypt Jordan Morocco UAE

Independent regulator (date)

Yes (2000)

Yes (1998)

Yes (2001)

Yes (1997)

No

Liberalization status

Fixed telephony No No No No No

Leased lines No No No No No

Data (1) No No Yes Yes No

ISP (2) Yes Yes Yes Yes No

Fixed satellite services No No No No No

VSAT No Yes No Yes No

Number of mobile operators

2 2 2 2(3) 1

Number of ISPs 4 38 8 10–20 1

Source: ATRN Database, ITU 2001 regulatory surveys

(1) Provision of data services on top of infrastructure (mainly leased lines) supplied by incumbent operators, e.g. IP VPN

(2) ISPs in national markets. Note that the regulatory treatment for international service provisioning varies by country

(3) Mobile operators have the right to operate their own international gateway

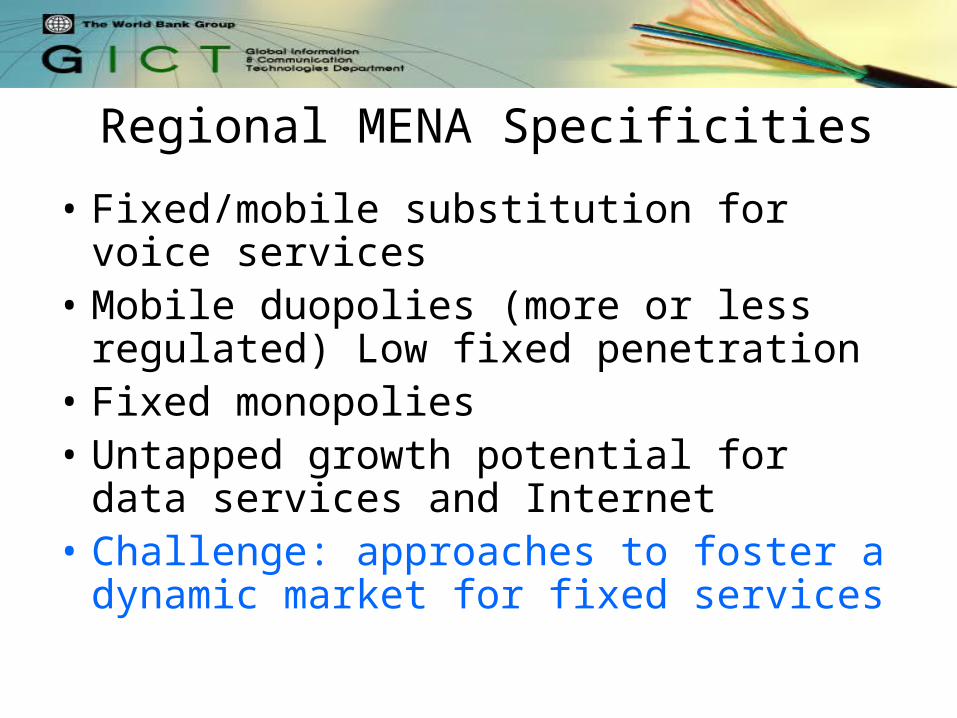

Regional MENA Specificities

• Fixed/mobile substitution for voice services

• Mobile duopolies (more or less regulated) Low fixed penetration

• Fixed monopolies• Untapped growth potential for data

services and Internet• Challenge: approaches to foster a

dynamic market for fixed services

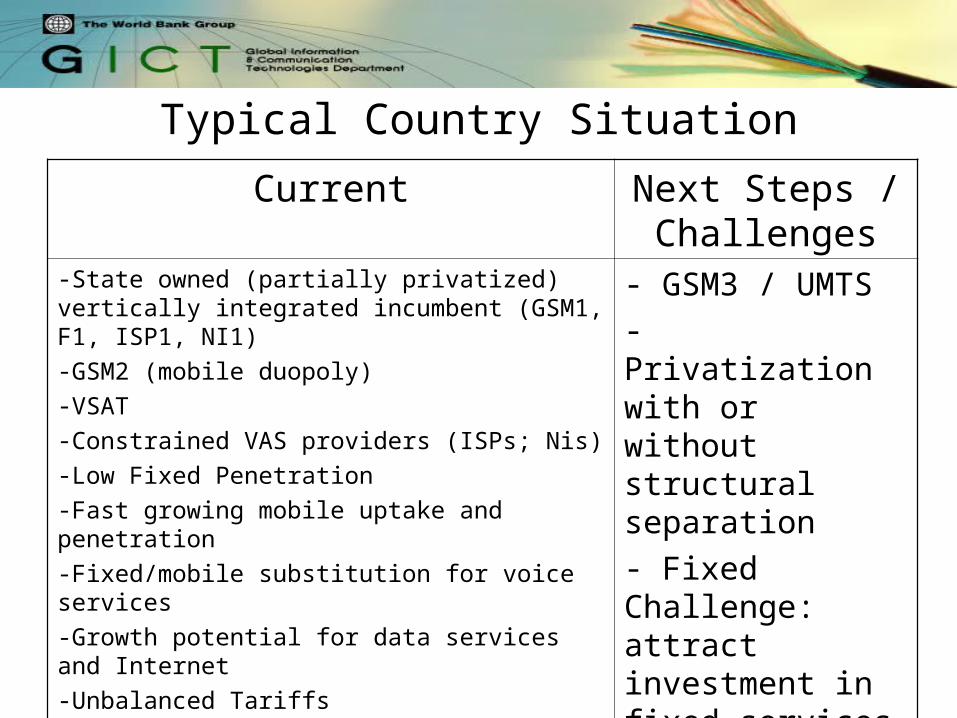

Typical Country Situation

Current Next Steps / Challenges

-State owned (partially privatized) vertically integrated incumbent (GSM1, F1, ISP1, NI1)

-GSM2 (mobile duopoly)

-VSAT

-Constrained VAS providers (ISPs; Nis)

-Low Fixed Penetration

-Fast growing mobile uptake and penetration

-Fixed/mobile substitution for voice services

-Growth potential for data services and Internet

-Unbalanced Tariffs

-High international tariffs

- GSM3 / UMTS- Privatization with or without structural separation- Fixed Challenge: attract investment in fixed services

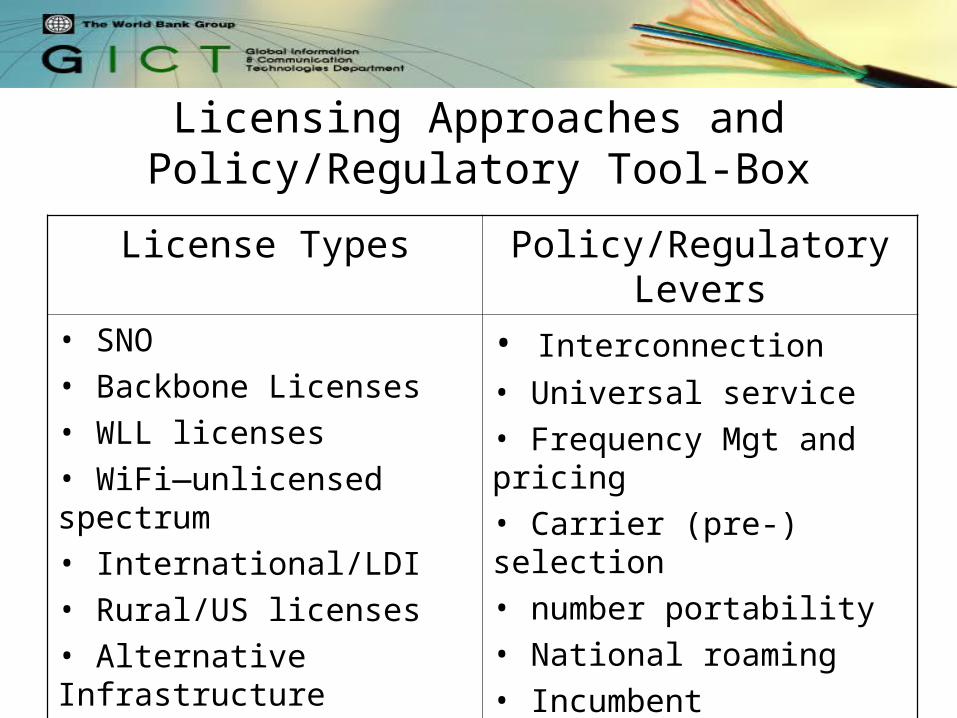

Licensing Approaches and Policy/Regulatory Tool-Box

License Types Policy/Regulatory Levers• SNO• Backbone Licenses• WLL licenses• WiFi—unlicensed spectrum• International/LDI• Rural/US licenses• Alternative Infrastructure licenses• Privatization approach• Structural Separation

• Interconnection

• Universal service• Frequency Mgt and pricing• Carrier (pre-) selection• number portability• National roaming• Incumbent regulation• Regulation of dominance• Market structure

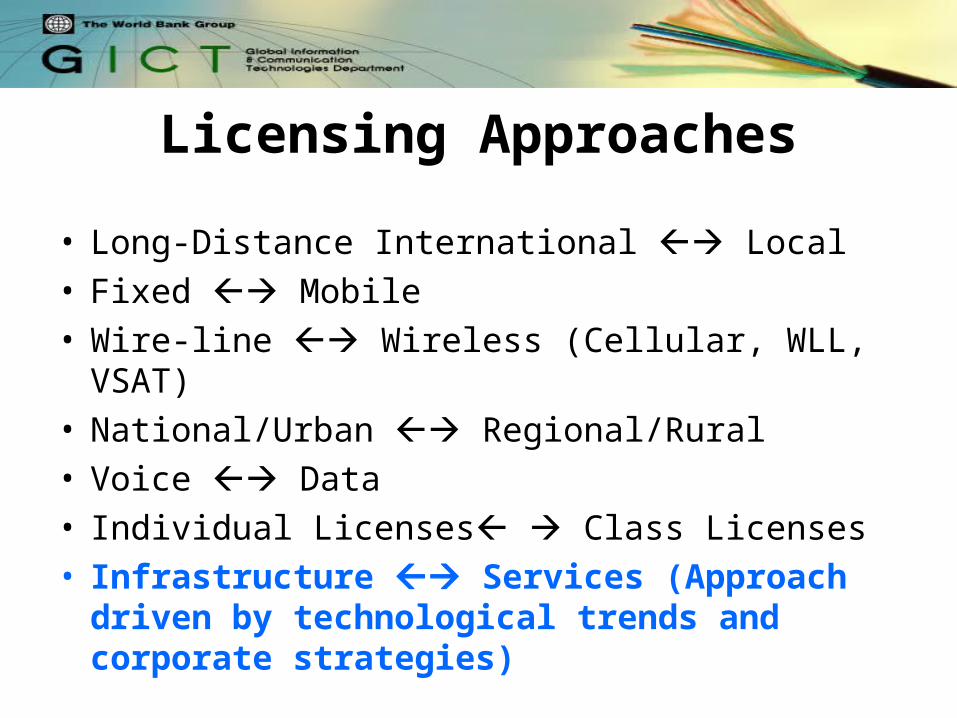

Licensing Approaches

• Long-Distance International Local• Fixed Mobile • Wire-line Wireless (Cellular, WLL, VSAT)• National/Urban Regional/Rural• Voice Data• Individual Licenses Class Licenses• Infrastructure Services (Approach

driven by technological trends and corporate strategies)

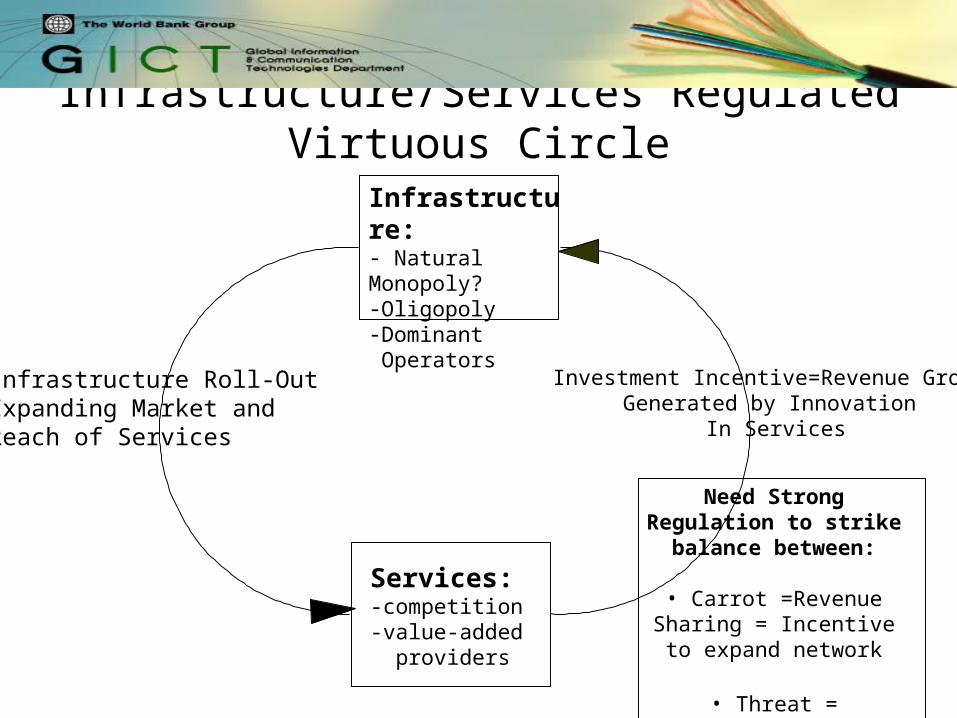

Infrastructure/Services Regulated Virtuous Circle

Investment Incentive=Revenue GrowthGenerated by Innovation

In Services

Need Strong Regulation to strike balance between:

• Carrot =Revenue Sharing = Incentive to expand

network

• Threat = Conditional right to infrastructure

Infrastructure:- Natural Monopoly?-Oligopoly-Dominant Operators

Services:-competition-value-added providers

Infrastructure Roll-OutExpanding Market andReach of Services

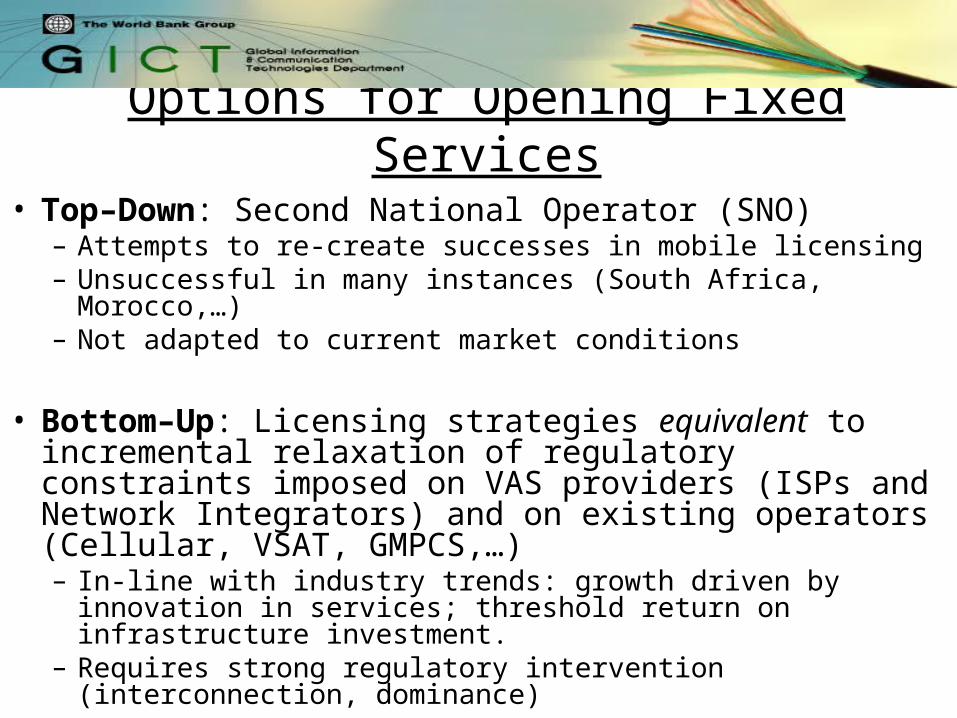

Options for Opening Fixed Services

• Top–Down: Second National Operator (SNO)– Attempts to re-create successes in mobile licensing– Unsuccessful in many instances (South Africa, Morocco,…)– Not adapted to current market conditions

• Bottom–Up: Licensing strategies equivalent to incremental relaxation of regulatory constraints imposed on VAS providers (ISPs and Network Integrators) and on existing operators (Cellular, VSAT, GMPCS,…)– In-line with industry trends: growth driven by innovation in

services; threshold return on infrastructure investment.– Requires strong regulatory intervention (interconnection,

dominance)

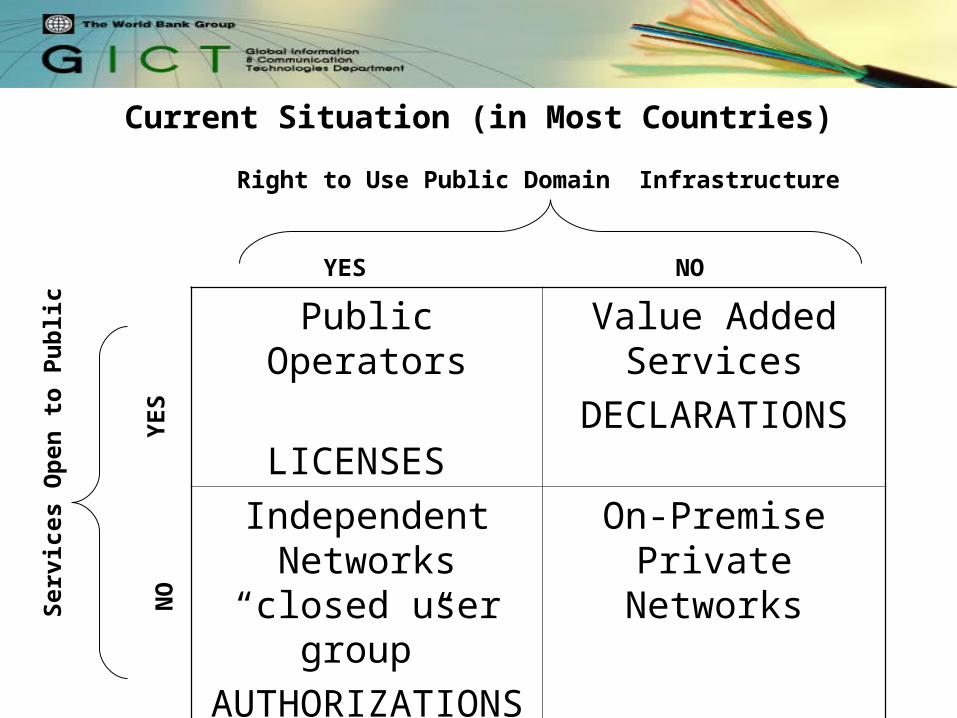

Current Situation (in Most Countries)

Public Operators

LICENSES

Value Added Services

DECLARATIONS

Independent Networks “closed

user group”

AUTHORIZATIONS

On-Premise Private Networks

Right to Use Public Domain Infrastructure

YES

NO

Y

ES

NO

Ser

vice

s O

pen

to

Pu

bli

c

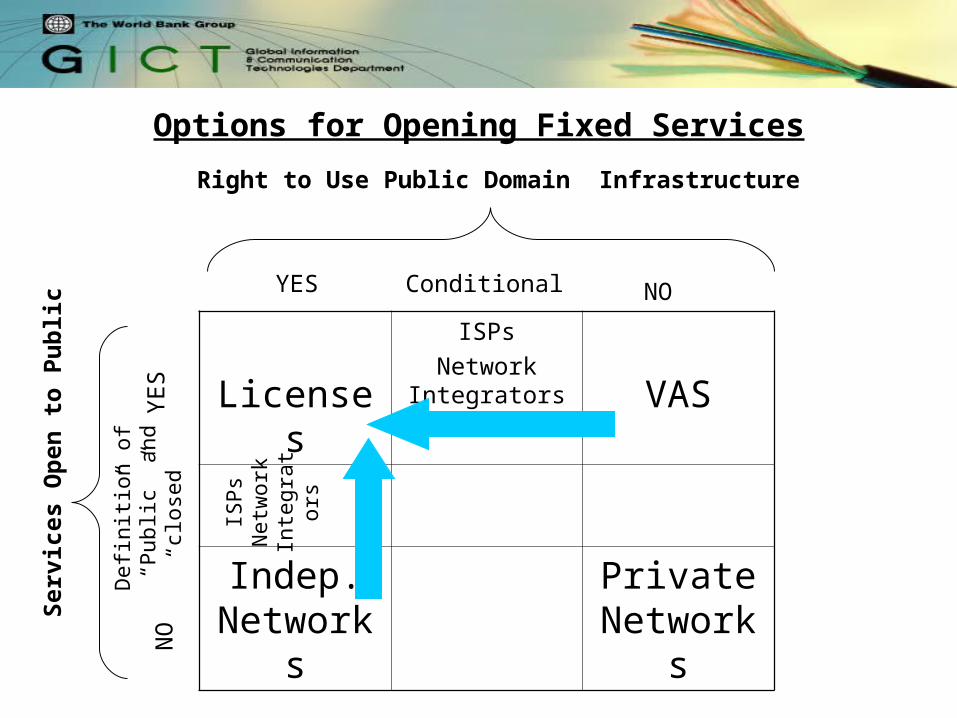

Options for Opening Fixed Services

Right to Use Public Domain Infrastructure

YES

NO

Y

ES

NO

Ser

vice

s O

pen

to

Pu

bli

c

Licenses

ISPs

Network Integrators VAS

Indep. Networks

Private Networks

Conditional

Def

initi

on o

f “

Pub

lic”

and

“clo

sed”

ISP

sN

etw

ork

Inte

grat

ors

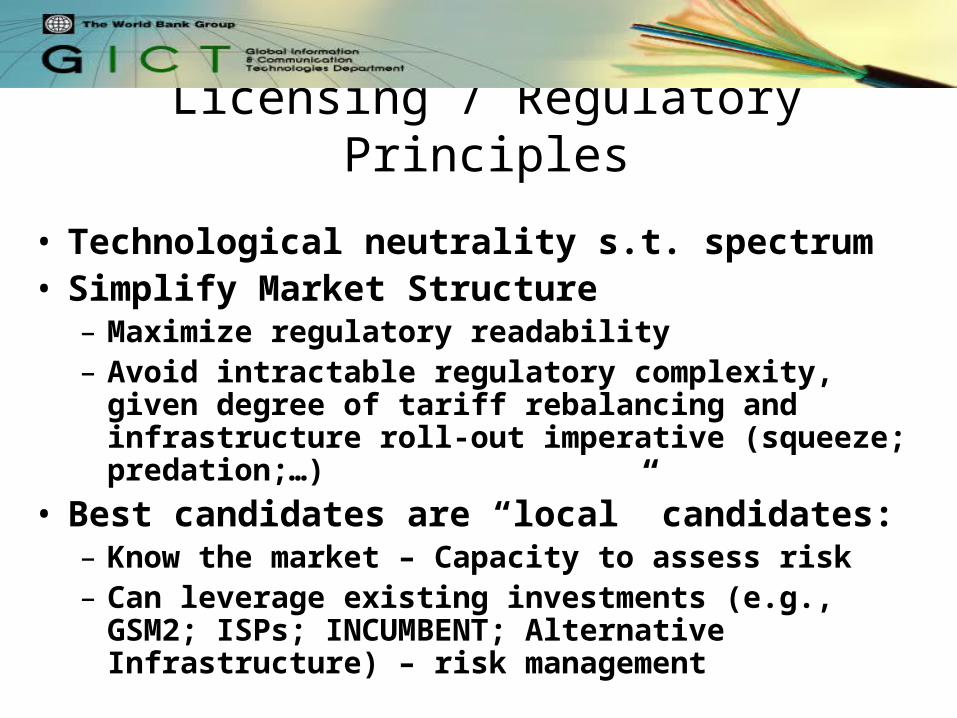

Licensing / Regulatory Principles

• Technological neutrality s.t. spectrum• Simplify Market Structure

– Maximize regulatory readability – Avoid intractable regulatory complexity, given

degree of tariff rebalancing and infrastructure roll-out imperative (squeeze; predation;…)

• Best candidates are “local” candidates:– Know the market – Capacity to assess risk– Can leverage existing investments (e.g., GSM2; ISPs;

INCUMBENT; Alternative Infrastructure) – risk management