Embed Size (px)

Citation preview

First Discussion PaperOn

Goods and Services TaxIn India

The Empowered CommitteeOf

State Finance Ministers

New Delhi

November 10 , 2009

First Discussion PaperOn

Goods and Services TaxIn India

The Empowered CommitteeOf

State Finance Ministers

New Delhi

November 10 , 2009

Contents

Pages

Foreword i-iv

Introduction 1-11

Preparation for GST 11-13

Goods & Services Tax Model for India 13-27

Annexure on Frequently Asked 29-53Questions and Answers on GST

i

Foreword

If the Value Added Tax (VAT) is considered to bea major improvement over the pre-existing Centralexcise duty at the national level and the sales tax systemat the State level, then the Goods and Services Tax(GST) will be a further significant breakthrough - thenext logical step - towards a comprehensive indirect taxreform in the country.

Keeping this overall objective in view, anannouncement was made by Shri P. Chidambaram, thethen Union Finance Minister in the Central Budget(2007-2008) to the effect that GST would be introducedfrom April 1, 2010 and that the Empowered Committeeof State Finance Ministers, on his request, wouldwork with the Central Government to prepare a roadmap for introduction of GST in India. After thisannouncement, the Empowered Committee of StateFinance Ministers decided to set up a Joint WorkingGroup (May 10, 2007), with the then Adviser to theUnion Finance Minister and the Member-Secretary ofEmpowered Committee as Co-convenors and theconcerned Joint Secretaries of the Department ofRevenue of Union Finance Ministry and all FinanceSecretaries of the States as its members. This JointWorking Group, after intensive internal discussions as

ii

well as interaction with experts and representatives ofChambers of Commerce and Industry, submitted itsreport to the Empowered Committee (November 19,2007).

This report was then discussed in detail in themeeting of Empowered Committee (November 28, 2007).On the basis of this discussion and written observationsof the States, certain modifications were made and afinal version of the views of Empowered Committeeat that stage was prepared and was sent to theGovernment of India (April 30, 2008). The commentsof the Government of India were received on December12, 2008 and were duly considered by the EmpoweredCommittee (December 16, 2008). It was decided thata Committee of Principal Secretaries /Secretariesof Finance / Taxation and Commissioners of TradeTaxes of the States would be set up to consider thesecomments, and submit their views. These viewswere submitted and were accepted in principle bythe Empowered Committee (January 21, 2009).Consequent upon this in-principle acceptance, aWorking Group, consisting of the concerned officials ofthe State Governments was formed who, in close associationwith senior representatives of the Government of India,submitted their recommendations in detail on thestructure of GST. An important interaction has alsorecently taken place between Shri Pranab Mukherjee,the Union Finance Minister and the Empowered

iii

Committee (October 19, 2009) on the related issue ofcompensation for loss of the States on account ofphasing out of CST. The Empowered Committee hasnow taken a detailed view on the recommendations ofthe Working Group of officials and other related matters.This detailed view of the Empowered Committee onthe structure of GST is now presented in terms of theFirst Discussion Paper, along with an Annexure onFrequently Asked Questions and Answers on GST, fordiscussions with industry, trade, agriculture and peopleat large.

The Discussion Paper is divided into four sections.Since GST would be further improvement over the VAT,Section 1 begins with a brief reference to the process ofintroduction of VAT at the Centre and the States andalso indicates the precise points where there is a needfor further improvement. This section also showshow the GST can bring about this improvement.With this as the background for justification of GST,Section 2 then describes the process of preparation forGST. Thereafter, Section 3 presents in detail thecomprehensive structure of the GST model. Forillustrating this GST model further, there is in the endan Annexure on Frequently Asked Questions andAnswers.

This Discussion Paper has been the result of trulycollective efforts on the basis of hardwork of all the

iv

concerned officials of the States, the officials ofEmpowered Committee Secretariat and the Adviser andofficials of the Union Finance Ministry, the counsel andactive participation of Finance Ministers and concernedSenior Ministers of the States at each stage, and theencouragement and advice of the Union FinanceMinister.

With the release of this First Discussion Paper andthe Annexure on Frequently Asked Questions andAnswers, we now sincerely invite interaction with therepresentatives of industry, trade, agriculture andcommon people. This interaction and campaign willimmediately start at the national level and at the Statelevels. As a part of this interaction, we look forward toreceiving the views of industry, trade, agriculture aswell as consumers in a time-bound manner.

Asim Kumar DasguptaChairman,

Empowered Committee ofState Finance Ministers

&Minister of Finance & Excise,Government of West Bengal

New Delhi,November 10, 2009

1

1. Introduction

1.1 Introduction of the Value Added Tax (VAT) atthe Central and the State level has been considered to bea major step – an important breakthrough – in the sphereof indirect tax reforms in India. If the VAT is a majorimprovement over the pre-existing Central excise duty atthe national level and the sales tax system at the Statelevel, then the Goods and Services Tax (GST) will indeedbe a further significant improvement – the next logicalstep – towards a comprehensive indirect tax reforms inthe country.

1.2 Keeping this objective in view, an announcementwas made by the then Union Finance Minister in theCentral Budget (2007-08) to the effect that GST would beintroduced with effect from April 1, 2010 and that theEmpowered Committee of State Finance Ministers, on hisrequest, would work with the Central Government toprepare a road map for introduction of GST in India. Afterthis announcement, the Empowered Committee of StateFinance Ministers decided to set up a Joint WorkingGroup (May 10, 2007), with the then Adviser to the UnionFinance Minister and Member-Secretary of theEmpowered Committee as its Co-convenors and concernedfour Joint Secretaries of the Department of Revenue ofUnion Finance Ministry and all Finance Secretaries ofthe States as its members. This Joint Working Group gotitself divided into three Sub-Groups and had several

2

rounds of internal discussions as well as interaction withexperts and representatives of Chambers of Commerce& Industry. On the basis of these discussions andinteraction, the Sub-Groups submitted their reports whichwere then integrated and consolidated into the report ofJoint Working Group (November 19, 2007).

1.3 This report was discussed in detail in the meetingof the Empowered Committee on November 28, 2007, andthe States were also requested to communicate theirobservations on the report in writing. On the basis ofthese discussions in the Empowered Committee and thewritten observations, certain modifications wereconsidered necessary and were discussed with theCo-convenors and the representatives of the Departmentof Revenue of Union Finance Ministry. With themodifications duly made, a final version of the views ofEmpowered Committee on the model and road map forthe GST was prepared (April 30, 2008). These views ofEmpowered Committee were then sent to the Governmentof India, and the comments of Government of India werereceived on December 12, 2008. These comments were dulyconsidered by the Empowered Committee (December 16,2008), and it was decided that a Committee of PrincipalSecretaries/Secretaries of Finance/Taxation andCommissioners of Trade Taxes of the States would be setup to consider these comments, and submit their views.These views were submitted and were accepted in principleby the Empowered Committee (January 21, 2009). As

3

a follow-up of this in-principle acceptance, a WorkingGroup consisting of the concerned officials of the StateGovernments was formed who, in association with seniorrepresentatives of Government of India, submittedtheir recommendations in detail on the structure of GST.An important interaction has also recently takenplace between Shri Pranab Mukherjee, the UnionFinance Minister and the Empowered Committee(October 19, 2009) on the related issue of compensationfor loss of the States on account of phasing out of CST.The Empowered Committee has now taken a detailed viewon the recommendations of the Working Group of officialsand other related matters. This detailed view is nowpresented in terms of the First Discussion Paper, alongwith an Annexure on Frequently Asked Questions andAnswers on GST, for discussion with industry, trade,agriculture and people at large. Since the GST at theCentre and States would be a further improvement overthe VAT, a brief recalling of the process of introduction ofVAT in India is worthwhile.

Value Added Tax at the Central and the State level

1.4 Prior to the introduction of VAT in the Centreand in the States, there was a burden of multiple taxationin the pre-existing Central excise duty and the State salestax systems. Before any commodity was produced, inputswere first taxed, and then after the commodity got producedwith input tax load, output was taxed again. This wascausing a burden of multiple taxation (i.e. “tax on tax”)

4

with a cascading effect. Moreover, in the sales taxstructure, when there was also a system of multi-pointsales taxation at subsequent levels of distributive trade,then along with input tax load, burden of sales tax paidon purchase at each level was also added, thus aggravatingthe cascading effect further.

1.5 When VAT is introduced in place of Central exciseduty, a set-off is given, i.e., a deduction is made from theoverall tax burden for input tax. In the case of VAT inplace of sales tax system, a set-off is given from tax burdennot only for input tax paid but also for tax paid on previouspurchases. With VAT, the problem of “tax on tax” andrelated burden of cascading effect is thus removed.Furthermore, since the benefit of set-off can be obtainedonly if tax is duly paid on inputs (in the case of CentralVAT), and on both inputs and on previous purchases (inthe case of State VAT), there is a built-in check in theVAT structure on tax compliance in the Centre as well asin the States, with expected results in terms ofimprovement in transparency and reduction in taxevasion. For these beneficial effects, VAT has now beenintroduced in more than 150 countries, including severalfederal countries. In Asia, it has now been introduced inalmost all the countries.

1.6 In India, VAT was introduced at the Central levelfor a selected number of commodities in terms ofMODVAT with effect from March 1, 1986, and in a

5

step-by-step manner for all commodities in terms ofCENVAT in 2002-03. Subsequently, after ConstitutionalAmendment empowering the Centre to levy taxes onservices, these service taxes were also added to CENVATin 2004-05. Although the growth of tax revenue from theCentral excise has not always been specially high, therevenue growth of combined CENVAT and service taxeshas been significant.

1.7 Introduction of VAT in the States has been a morechallenging exercise in a federal country like India, whereeach State, in terms of Constitutional provision, issovereign in levying and collecting State taxes. Beforeintroduction of VAT, in the sales tax regime, apart fromthe problem of multiple taxation and burden of adversecascading effect of taxes as already mentioned, there wasalso no harmony in the rates of sales tax on differentcommodities among the States. Not only were the ratesof sales tax numerous (often more than ten in severalStates), and different from one another for the samecommodity in different States, but there was also anunhealthy competition among the States in terms of salestax rates – so-called “rate war” – often resulting in,revenue-wise, a counter-productive situation.

1.8 It is in this background that attempts were madeby the States to introduce a harmonious VAT in theStates, keeping at the same time in mind the issue ofsovereignty of the States regarding the State tax matters.

6

The first preliminary discussion on State-level VAT tookplace in a meeting of Chief Ministers convened byDr. Manmohan Singh, the then Union Finance Ministerin 1995. In this meeting, the basic issues on VAT werediscussed in general terms and this was followed upby periodic interactions of State Finance Ministers.Thereafter, in a significant meeting of all theChief Ministers, convened on November 16, 1999 byShri Yashwant Sinha, the then Union Finance Minister,two important decisions, among others, were taken. First,before the introduction of State-level VAT, the unhealthysales tax “rate war” among the States would have to end,and sales tax rates would need to be harmonised byimplementing uniform floor rates of sales tax for differentcategories of commodities with effect from January 1, 2000.Secondly, on the basis of achievement of the first objective,steps would be taken by the States for introductionof State-level VAT after adequate preparation. Forimplementing these decisions, a Standing Committeeof State Finance Ministers was formed which was thenmade an Empowered Committee of State FinanceMinisters.

1.9 Thereafter, the Empowered Committee has metregularly. All the decisions were taken on the basis ofconsensus. On the strength of these repeated discussionsand collective efforts, involving the Ministers and theconcerned officials, it was possible within a period of about

7

a year and a half to achieve nearly 98 per cent success inthe first objective, namely, harmonisation of sales taxstructure through implementation of uniform floor ratesof sales tax.

1.10 After reaching this stage, steps were initiatedfor systematic preparation for introduction of State-levelVAT. In order again to avoid any unhealthy competitionamong the States which may lead to distortions inmanufacturing and trade, attempts have been made fromthe very beginning to harmonise the VAT design in theStates, keeping also in view the distinctive features of eachState and the need for federal flexibility. This has beendone by the States collectively agreeing, throughdiscussions in the Empowered Committee, to certaincommon points of convergence regarding VAT, andallowing at the same time certain flexibility toaccommodate the local characteristics of the States. Inthe course of these discussions, references to the TenthFive Year Plan Report of the Advisory Group on TaxPolicies & Tax Administration (2001) and the report ofKelkar (Chairman) Task Force were helpful.

1.11 Along with these measures, steps were taken fornecessary training, computerization and interaction withtrade and industry. While these preparatory steps weretaken, the Empowered Committee got a significantsupport from Shri P. Chidambaram, the then Union

8

Finance Minister, when he responded positively inproviding Central financial support to the States inthe event of loss of revenue in transitional years ofimplementation of VAT.

1.12 As a consequence of all these steps, the Statesstarted implementing VAT beginning April 1, 2005. Afterovercoming the initial difficulties, all the States andUnion Territories have now implemented VAT. TheEmpowered Committee has been monitoring closely theprocess of implementation of State-level VAT, anddeviations from the agreed VAT rates has been containedto less than 3 per cent of the total list of commodities.Responses of industry and also of trade have been indeedencouraging. The rate of growth of tax revenue has nearlydoubled from the average annual rate of growth in thepre-VAT five year period after the introduction of VAT.

Justification of GST

1.13 Despite this success with VAT, there are stillcertain shortcomings in the structure of VAT both at theCentral and at the State level. The shortcoming inCENVAT of the Government of India lies in non-inclusionof several Central taxes in the overall framework ofCENVAT, such as additional customs duty, surcharges,etc., and thus keeping the benefits of comprehensive inputtax and service tax set-off out of reach for manufacturers/dealers. Moreover, no step has yet been taken to capturethe value-added chain in the distribution trade below the

9

manufacturing level in the existing scheme of CENVAT.The introduction of GST at the Central level will not onlyinclude comprehensively more indirect Central taxesand integrate goods and service taxes for the purpose ofset-off relief, but may also lead to revenue gain for theCentre through widening of the dealer base by capturingvalue addition in the distributive trade and increasedcompliance.

1.14 In the existing State-level VAT structure thereare also certain shortcomings as follows. There are, forinstance, even now, several taxes which are in the natureof indirect tax on goods and services, such as luxury tax,entertainment tax, etc., and yet not subsumed in the VAT.Moreover, in the present State-level VAT scheme,CENVAT load on the goods remains included in the valueof goods to be taxed under State VAT, and contributingto that extent a cascading effect on account of CENVATelement. This CENVAT load needs to be removed.Furthermore, any commodity, in general, is produced onthe basis of physical inputs as well as services, and thereshould be integration of VAT on goods with tax on servicesat the State level as well, and at the same time thereshould also be removal of cascading effect of service tax.In the GST, both the cascading effects of CENVAT andservice tax are removed with set-off, and a continuouschain of set-off from the original producer’s point andservice provider’s point upto the retailer’s level isestablished which reduces the burden of all cascadingeffects. This is the essence of GST, and this is why GST

10

is not simply VAT plus service tax but an improvementover the previous system of VAT and disjointed servicetax. However, for this GST to be introduced at the State-level, it is essential that the States should be given thepower of levy of taxation of all services. This power of levyof service taxes has so long been only with the Centre.A Constitutional Amendment will be made for giving thispower also to the States. Moreover, with the introductionof GST, burden of Central Sales Tax (CST) will also beremoved. The GST at the State-level is, therefore, justifiedfor (a) additional power of levy of taxation of services forthe States, (b) system of comprehensive set-off relief,including set-off for cascading burden of CENVAT andservice taxes, (c) subsuming of several taxes in the GSTand (d) removal of burden of CST. Because of the removalof cascading effect, the burden of tax under GST on goodswill, in general, fall.

1.15 The GST at the Central and at the State levelwill thus give more relief to industry, trade, agricultureand consumers through a more comprehensive andwider coverage of input tax set-off and service tax set-off, subsuming of several taxes in the GST and phasingout of CST. With the GST being properly formulatedby appropriate calibration of rates and adequatecompensation where necessary, there may also berevenue/ resource gain for both the Centre and the States,primarily through widening of tax base and possibility of

11

a significant improvement in tax-compliance. In otherwords, the GST may usher in the possibility of a collectivegain for industry, trade, agriculture and commonconsumers as well as for the Central Government andthe State Governments. The GST may, indeed, lead tothe possibility of collectively positive-sum game.

2. Preparation for GST

2.1 Keeping this significance of GST in view, anannouncement was made by the then Union FinanceMinister in the Union Budget, as mentioned before, tothe effect that GST would be introduced from April 1, 2010,and that the Empowered Committee of State FinanceMinisters would work with the Central Government toprepare a road map for introduction of the GST. Afterthis announcement, the Empowered Committee, as statedearlier, had set up a Joint Working Group which submitteda report on a model and road map for GST. Afteraccommodating the views of the States appropriately onthis report, the views of the Empowered Committee onthe model and road map were sent to the Government ofIndia on 30th April, 2008. The comments of theGovernment of India were received on 12th December,2008. These comments were duly considered by theEmpowered Committee in its meeting held on 16th

December, 2008 and it was decided that a Committeeof Principal Secretaries/Secretaries (Finance/Taxation) and

12

Commissioners of Trade Taxes should consider thecomments received from the Government of India andsubmit its views and also work out the Central GSTand State GST rates. The Committee held detaileddeliberations on 5th and 6th January, 2009, andsubmitted its recommendations to the EmpoweredCommittee. The Empowered Committee consideredthese recommendations in its meeting held on 21st

January, 2009 and accepted them in principle. TheEmpowered Committee also decided to constitute aWorking Group consisting of Principal Secretaries/Secretaries (Finance/Taxation) and Commissioners ofTrade Taxes of all States/UTs to give theirrecommendations on (a) the commodities and servicesthat should be kept in the exempted list, (b) the rulesand principles of taxing the transactions of servicesincluding the transactions in inter-State services, and(c) finalization of the model suggested for inter-statetransaction/movement of goods including stock transfersin consultation with the State Bank of India and someother nationalized banks. It was also decided that thesenior representatives from the Government of Indiamay also be associated. The Working Group deliberatedon the issues on 10th February, 2009 and decided toform three Sub Working Groups to deliberate each itemin depth. The Reports of the Working Group on thethree issues have already been received, and theEmpowered Committee has taken a view on theserecommendations for concluding the details of GSTstructure.

13

2.2 While making this preparation of GST, it wasalso necessary, as mentioned earlier, to phase out the CST,because it did not carry any set-off relief and therewas a distortion in the VAT regime due to export of taxfrom one State to other State. The Empowered Committeeaccordingly took a decision to phase out CST on theunderstanding with the Centre that, since phasing out ofCST would result in a loss of revenue to the States on apermanent basis, an appropriate mechanism tocompensate the States for such loss would be worked out.The rate of CST has already been reduced to 2% and willbe phased out with effect from the date of introduction ofGST on the basis of such GST structure which, withnecessary financial support to the States, shouldadequately compensate for the loss of the States on apermanent basis. With these steps at preparation in mind,it is important now to turn to the proposed model of GST.

3. Goods & Services Tax Model For India

3.1 It is important to take note of the significantadministrative issues involved in designing an effectiveGST model in a federal system with the objective ofhaving an overall harmonious structure of rates. Togetherwith this, there is a need for upholding the powers ofCentral and State Governments in their taxation matters.Further, there is also the need to propose a model thatwould be easily implementable, while being generallyacceptable to stakeholders.

14

Salient features of the GST model

3.2 Keeping in view the report of the Joint WorkingGroup on Goods and Services Tax, the views receivedfrom the States and Government of India, a dual GSTstructure with defined functions and responsibilities ofthe Centre and the States is recommended. An appropriatemechanism that will be binding on both the Centre andthe States would be worked out whereby the harmoniousrate structure along with the need for further modificationcould be upheld, if necessary with a collectively agreedConstitutional Amendment. Salient features of theproposed model are as follows:

(i) The GST shall have two components: one leviedby the Centre (hereinafter referred to as Central GST),and the other levied by the States (hereinafter referred toas State GST). Rates for Central GST and State GSTwould be prescribed appropriately, reflecting revenueconsiderations and acceptability. This dual GST modelwould be implemented through multiple statutes (one forCGST and SGST statute for every State). However, thebasic features of law such as chargeability, definition oftaxable event and taxable person, measure of levyincluding valuation provisions, basis of classification etc.would be uniform across these statutes as far aspracticable.

(ii) The Central GST and the State GST would beapplicable to all transactions of goods and services made

15

for a consideration except the exempted goods andservices, goods which are outside the purview of GSTand the transactions which are below the prescribedthreshold limits.

(iii) The Central GST and State GST are to be paid tothe accounts of the Centre and the States separately. Itwould have to be ensured that account-heads for allservices and goods would have indication whether itrelates to Central GST or State GST (with identificationof the State to whom the tax is to be credited).

(iv) Since the Central GST and State GST are to betreated separately, taxes paid against the Central GSTshall be allowed to be taken as input tax credit (ITC) forthe Central GST and could be utilized only against thepayment of Central GST. The same principle will beapplicable for the State GST. A taxpayer or exporter wouldhave to maintain separate details in books of account forutilization or refund of credit. Further, the rules for takingand utilization of credit for the Central GST and the StateGST would be aligned.

(v) Cross utilization of ITC between the CentralGST and the State GST would not be allowed except inthe case of inter-State supply of goods and services underthe IGST model which is explained later.

(vi) Ideally, the problem related to credit accumulationon account of refund of GST should be avoided by both theCentre and the States except in the cases such as exports,

16

purchase of capital goods, input tax at higher rate thanoutput tax etc. where, again refund/adjustment should becompleted in a time bound manner.

(vii) To the extent feasible, uniform procedure forcollection of both Central GST and State GST would beprescribed in the respective legislation for Central GSTand State GST.

(viii) The administration of the Central GST to theCentre and for State GST to the States would be given.This would imply that the Centre and the States wouldhave concurrent jurisdiction for the entire value chain andfor all taxpayers on the basis of thresholds for goods andservices prescribed for the States and the Centre.

(ix) The present threshold prescribed in differentState VAT Acts below which VAT is not applicablevaries from State to State. A uniform State GST thresholdacross States is desirable and, therefore, it is consideredthat a threshold of gross annual turnover of Rs.10 lakhboth for goods and services for all the States and UnionTerritories may be adopted with adequate compensationfor the States (particularly, the States in North-EasternRegion and Special Category States) where lowerthreshold had prevailed in the VAT regime. Keeping inview the interest of small traders and small scaleindustries and to avoid dual control, the States alsoconsidered that the threshold for Central GST for goods

17

may be kept at Rs.1.5 crore and the threshold for CentralGST for services may also be appropriately high. It maybe mentioned that even now there is a separate thresholdof services (Rs. 10 lakh) and goods (Rs. 1.5 crore) in theService Tax and CENVAT.

(x) The States are also of the view that Composition/Compounding Scheme for the purpose of GST should havean upper ceiling on gross annual turnover and a floor taxrate with respect to gross annual turnover. In particular,there would be a compounding cut-off at Rs. 50 lakh ofgross annual turn over and a floor rate of 0.5% across theStates. The scheme would also allow option for GSTregistration for dealers with turnover below thecompounding cut-off.

(xi) The taxpayer would need to submit periodicalreturns, in common format as far as possible, to both theCentral GST authority and to the concerned State GSTauthorities.

(xii) Each taxpayer would be allotted a PAN-linkedtaxpayer identification number with a total of 13/15 digits.This would bring the GST PAN-linked system in linewith the prevailing PAN-based system for Income tax,facilitating data exchange and taxpayer compliance.

(xiii) Keeping in mind the need of tax payer’sconvenience, functions such as assessment, enforcement,

18

scrutiny and audit would be undertaken by the authoritywhich is collecting the tax, with information sharingbetween the Centre and the States.

Central and State Taxes to be subsumed under GST

3.3 The various Central, State and Local levies wereexamined to identify their possibility of being subsumedunder GST. While identifying, the following principleswere kept in mind:

(i) Taxes or levies to be subsumed should beprimarily in the nature of indirect taxes, either on thesupply of goods or on the supply of services.

(ii) Taxes or levies to be subsumed should be part ofthe transaction chain which commences with import/manufacture/ production of goods or provision of servicesat one end and the consumption of goods and services at theother.

(iii) The subsumation should result in free flow of taxcredit in intra and inter-State levels.

(iv) The taxes, levies and fees that are not specificallyrelated to supply of goods & services should not besubsumed under GST.

(v) Revenue fairness for both the Union and theStates individually would need to be attempted.

19

3.4 On application of the above principles, it isrecommended that the following Central Taxes should be,to begin with, subsumed under the Goods and ServicesTax:

(i) Central Excise Duty

(ii) Additional Excise Duties

(iii) The Excise Duty levied under the Medicinal andToiletries Preparation Act

(iv) Service Tax

(v) Additional Customs Duty, commonly known asCountervailing Duty (CVD)

(vi) Special Additional Duty of Customs - 4% (SAD)

(vii) Surcharges, and

(viii) Cesses.

Following State taxes and levies would be, to begin with,subsumed under GST:

(i) VAT / Sales tax

(ii) Entertainment tax (unless it is levied by the localbodies).

(iii) Luxury tax

(iv) Taxes on lottery, betting and gambling.

(v) State Cesses and Surcharges in so far as theyrelate to supply of goods and services.

(vi) Entry tax not in lieu of Octroi.

20

Purchase tax: Some of the States felt that they aregetting substantial revenue from Purchase Tax and,therefore, it should not be subsumed under GST whilemajority of the States were of the view that no suchexemptions should be given. The difficulties of thefoodgrains producing States and certain other Stateswere appreciated as substantial revenue is being earnedby them from Purchase Tax and it was, therefore, felt thatin case Purchase Tax has to be subsumed then adequateand continuing compensation has to be provided to suchStates. This issue is being discussed in consultation withthe Government of India.

Tax on items containing Alcohol: Alcoholicbeverages would be kept out of the purview of GST. SalesTax/VAT can be continued to be levied on alcoholicbeverages as per the existing practice. In case it has beenmade Vatable by some States, there is no objection to that.Excise Duty, which is presently being levied by the Statesmay not be also affected.

Tax on Tobacco products: Tobacco products wouldbe subjected to GST with ITC. Centre may be allowed tolevy excise duty on tobacco products over and above GSTwithout ITC.

Tax on Petroleum Products: As far as petroleumproducts are concerned, it was decided that the basket ofpetroleum products, i.e. crude, motor spirit (including

21

ATF) and HSD would be kept outside GST as is theprevailing practice in India. Sales Tax could continue tobe levied by the States on these products with prevailingfloor rate. Similarly, Centre could also continue its levies.A final view whether Natural Gas should be kept outsidethe GST will be taken after further deliberations.

Taxation of Services : As indicated earlier, both theCentre and the States will have concurrent power to levytax on all goods and services. In the case of States, theprinciple for taxation of intra-State and inter-State hasalready been formulated by the Working Group ofPrincipal Secretaries/Secretaries of Finance/Taxationand Commissioners of Trade Taxes with seniorrepresentatives of Department of Revenue, Governmentof India. For inter-State transactions an innovative modelof Integrated GST will be adopted by appropriatelyaligning and integrating CGST and SGST. The workingof this model is elaborated below.

3.5 Inter-State Transactions of Goods and Services

The Empowered Committee has accepted therecommendations of the Working Group of concernedofficials of Central and State Governments for adoptionof IGST model for taxation of inter-State transactionof Goods and Services. The scope of IGST Model is thatCentre would levy IGST which would be CGST plus SGSTon all inter-State transactions of taxable goods and

22

services with appropriate provision for consignment orstock transfer of goods and services. The inter-State sellerwill pay IGST on value addition after adjusting availablecredit of IGST, CGST, and SGST on his purchases. TheExporting State will transfer to the Centre the credit ofSGST used in payment of IGST. The Importing dealerwill claim credit of IGST while discharging his output taxliability in his own State. The Centre will transfer to theimporting State the credit of IGST used in payment ofSGST. The relevant information will also be submittedto the Central Agency which will act as a clearing housemechanism, verify the claims and inform the respectivegovernments to transfer the funds.

The major advantages of IGST Model are:

a) Maintenance of uninterrupted ITC chain on inter-State transactions.

b) No upfront payment of tax or substantial blockageof funds for the inter-State seller or buyer.

c) No refund claim in exporting State, as ITC is usedup while paying the tax.

d) Self monitoring model.

e) Level of computerization is limited to inter-Statedealers and Central and State Governmentsshould be able to computerize their processesexpeditiously.

23

f) As all inter-State dealers will be e-registered andcorrespondence with them will be by e-mail, thecompliance level will improve substantially.

g) Model can take ‘Business to Business’ as well as‘Business to Consumer’ transactions into account.

3.6 GST Rate Structure

The Empowered Committee has decided to adopt atwo-rate structure –a lower rate for necessary items andgoods of basic importance and a standard rate for goodsin general. There will also be a special rate for preciousmetals and a list of exempted items. For upholding ofspecial needs of each State as well as a balanced approachto federal flexibility, and also for facilitating theintroduction of GST, it is being discussed whether theexempted list under VAT regime including Goods of LocalImportance may be retained in the exempted list underState GST in the initial years. It is also being discussedwhether the Government of India may adopt, to beginwith, a similar approach towards exempted list under theCGST.

The States are of the view that for CGST relating togoods, the Government of India may also have a two-ratestructure, with conformity in the levels of rate under theSGST. For taxation of services, there may be a single ratefor both CGST and SGST.

The exact value of the SGST and CGST rates,including the rate for services, will be made known dulyin course of appropriate legislative actions.

24

3.7 Zero Rating of Exports

Exports would be zero-rated. Similar benefits maybe given to Special Economic Zones (SEZs). However, suchbenefits will only be allowed to the processing zones ofthe SEZs. No benefit to the sales from an SEZ to DomesticTariff Area (DTA) will be allowed.

3.8 GST on Imports: The GST will be levied onimports with necessary Constitutional Amendments. BothCGST and SGST will be levied on import of goods andservices into the country. The incidence of tax will followthe destination principle and the tax revenue in case ofSGST will accrue to the State where the imported goodsand services are consumed. Full and complete set-off willbe available on the GST paid on import on goods andservices.

3.9 Special Industrial Area Scheme

After the introduction of GST, the tax exemptions,remissions etc. related to industrial incentives should beconverted, if at all needed, into cash refund schemes aftercollection of tax, so that the GST scheme on the basis of acontinuous chain of set-offs is not disturbed. RegardingSpecial Industrial Area Schemes, it is clarified that suchexemptions, remissions etc. would continue up tolegitimate expiry time both for the Centre and the States.Any new exemption, remission etc. or continuation ofearlier exemption, remission etc. would not be allowed.

25

In such cases, the Central and the State Governmentscould provide reimbursement after collecting GST.

3.10 IT Infrastructure

After acceptance of IGST Model for Inter-Statetransactions, the major responsibilities of ITinfrastructural requirement will be shared by the CentralGovernment through the use of its own IT infrastructurefacility. The issues of tying up the State Infrastructurefacilities with the Central facilities as well as furtherimprovement of the States’ own IT infrastructure,including TINXSYS, is now to be addressed expeditiouslyand in a time bound manner.

3.11 Constitutional Amendments, Legislationsand Rules for administration of CGST and SGST

It is essential to have Constitutional Amendmentsfor empowering the States for levy of service tax, GST onimports and consequential issues as well as correspondingCentral and State legislations with associated rules andprocedures. With these specific tasks in view, a JointWorking Group has recently been constituted (September30, 2009) comprising of the officials of the Central andState Governments to prepare, in a time bound mannera draft legislation for Constitutional Amendment, draftlegislation for CGST, a suitable Model Legislation forSGST and rules and procedures for CGST and SGST.Simultaneous steps have also been initiated for drafting

26

of a legislation for IGST and rules and procedures. Asa part of this exercise, the Working Group will alsoaddress the issues of dispute resolution and advanceruling.

3.12 Harmonious structure of GST and theStates’ autonomy in a Federal Framework

As a part of the exercise on Constitutional Amendment,a special attention would be given, as mentioned earlierin para 3.2, to the formulation of a mechanism forupholding the need for a harmonious structure for GSTalong with the concern for the States’ autonomy in afederal structure.

3.13 Dispute Resolution and Advance Ruling

As a part of the exercise on drafting of legislation,rules and procedures for the administration of CGST andSGST, specific provisions would also be made to the issuesof dispute resolution and advance ruling.

3.14 Need for compensation duringimplementation of GST

Despite the sincere attempts being made by theEmpowered Committee on the determination of GST ratestructure, revenue neutral rates, it is difficult to estimateaccurately as to how much the States will gain fromservice taxes and how much they will lose on account of

27

removal of cascading effect, payment of input tax creditand phasing out of CST. In view of this, it would beessential to provide adequately for compensation forloss that might emerge during the process ofimplementation of GST for the next five years. Thisissue may be comprehensively taken care of in therecommendations of the Thirteenth FinanceCommission. The payment of this compensation willneed to be ensured in terms of special grants to bereleased to the States duly in every month on the basisof neutrally monitored mechanism.

3.15 With the release of this First Discussion Paperand the Annexure on Frequently Asked Questions andAnswers on GST, interaction with the representatives ofindustry, trade and agriculture would begin immediatelyat the national level, and then also simultaneously at theState levels. Similarly awareness campaign for commonconsumers would also be initiated at the same time. As apart of the discussion and campaign, the views of theindustry, trade and agriculture as well as consumers arebeing sought in a structured and time bound manner.

29

Annexure

Frequently Asked Questions and Answers on GST

Question 1 : What is the justification of GST ?

Answer : There was a burden of “tax on tax” inthe pre-existing Central excise duty of theGovernment of India and sales tax system of the StateGovernments. The introduction of Central VAT(CENVAT) has removed the cascading burden of“tax on tax” to a good extent by providinga mechanism of “set off” for tax paid on inputs andservices upto the stage of production, and has beenan improvement over the pre-existing Central exciseduty. Similarly, the introduction of VAT in the Stateshas removed the cascading effect by giving set-offfor tax paid on inputs as well as tax paid on previouspurchases and has again been an improvement overthe previous sales tax regime.

But both the CENVAT and the State VAThave certain incompleteness. The incompleteness inCENVAT is that it has yet not been extended toinclude chain of value addition in the distributive

30

trade below the stage of production. It has alsonot included several Central taxes, such as AdditionalExcise Duties, Additional Customs Duty, Surchargesetc. in the overall framework of CENVAT, and thuskept the benefits of comprehensive input tax andservice tax set-off out of the reach of manufacturers/dealers. The introduction of GST will not only includecomprehensively more indirect Central taxes andintegrate goods and services taxes for set-off relief,but also capture certain value addition in thedistributive trade.

Similarly, in the present State-level VATscheme, CENVAT load on the goods has not yet beenremoved and the cascading effect of that part of taxburden has remained unrelieved. Moreover, there areseveral taxes in the States, such as, Luxury Tax,Entertainment Tax, etc. which have still not beensubsumed in the VAT. Further, there has also notbeen any integration of VAT on goods with tax onservices at the State level with removal of cascadingeffect of service tax. In addition, although the burdenof Central Sales Tax (CST) on inter-State movementof goods has been lessened with reduction of CSTrate from 4% to 2%, this burden has also not beenfully phased out. With the introduction of GST atthe State level, the additional burden of CENVATand services tax would be comprehensively removed,

31

and a continuous chain of set-off from the originalproducer’s point and service provider’s point upto theretailer’s level would be established which wouldeliminate the burden of all cascading effects,including the burden of CENVAT and service tax.This is the essence of GST. Also, major Central andState taxes will get subsumed into GST which willreduce the multiplicity of taxes, and thus bring downthe compliance cost. With GST, the burden of CSTwill also be phased out.

Thus GST is not simply VAT plus servicetax, but a major improvement over the previoussystem of VAT and disjointed services tax – a justifiedstep forward.

Question 2. What is GST? How does it work ?

Answer : As already mentioned in answer toQuestion 1, GST is a tax on goods and services withcomprehensive and continuous chain of set-offbenefits from the producer’s point and serviceprovider’s point upto the retailer’s level. It isessentially a tax only on value addition at each stage,and a supplier at each stage is permitted to set-off,through a tax credit mechanism, the GST paid onthe purchase of goods and services as available forset-off on the GST to be paid on the supply of goods

32

and services. The final consumer will thus bear onlythe GST charged by the last dealer in the supplychain, with set-off benefits at all the previous stages.

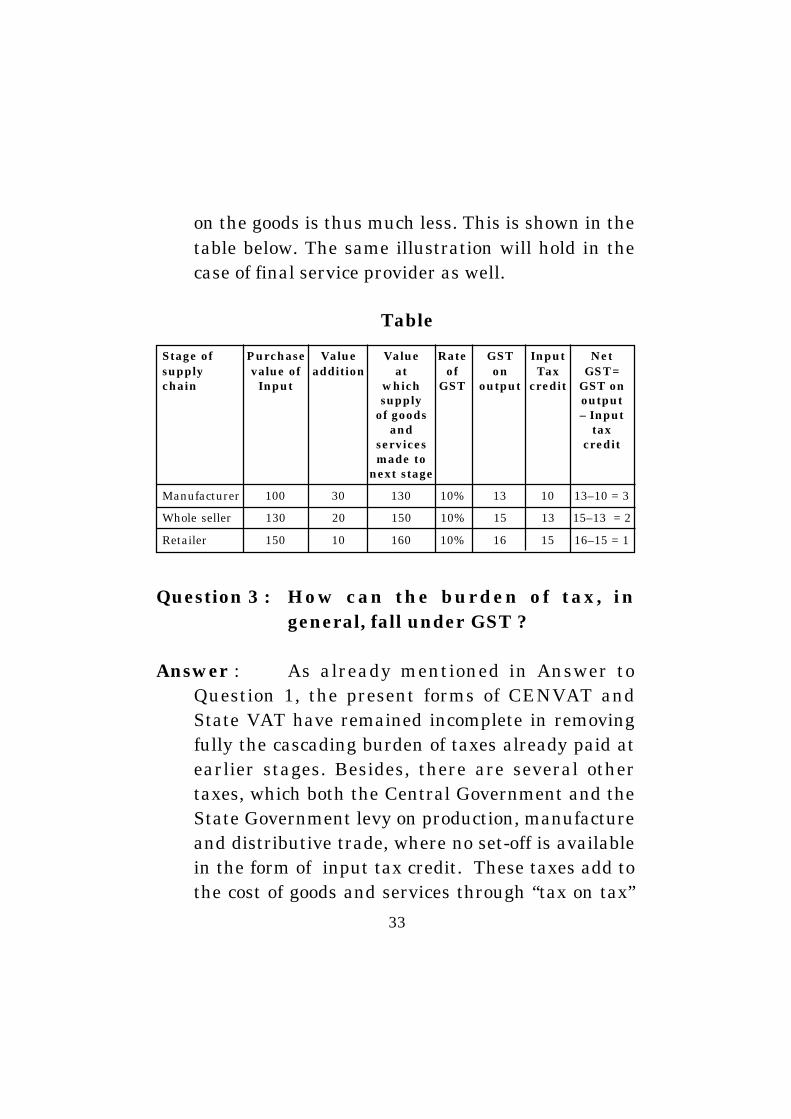

The illustration shown below indicates, interms of a hypothetical example with a manufacturer,one wholeseller and one retailer, how GST will work.Let us suppose that GST rate is 10%, with themanufacturer making value addition of Rs.30 on hispurchases worth Rs.100 of input of goods and servicesused in the manufacturing process. The manufacturerwill then pay net GST of Rs. 3 after setting-off Rs. 10as GST paid on his inputs (i.e. Input Tax Credit) fromgross GST of Rs. 13. The manufacturer sells the goodsto the wholeseller. When the wholeseller sells thesame goods after making value addition of (say), Rs.20, he pays net GST of only Rs. 2, after setting-off ofInput Tax Credit of Rs. 13 from the gross GST ofRs. 15 to the manufacturer. Similarly, when a retailersells the same goods after a value addition of (say)Rs. 10, he pays net GST of only Re.1, after setting-offRs.15 from his gross GST of Rs. 16 paid to wholeseller.Thus, the manufacturer, wholeseller and retailerhave to pay only Rs. 6 (= Rs. 3+Rs. 2+Re. 1) as GSTon the value addition along the entire value chainfrom the producer to the retailer, after setting-off GSTpaid at the earlier stages. The overall burden of GST

33

on the goods is thus much less. This is shown in thetable below. The same illustration will hold in thecase of final service provider as well.

Table

Stage of Purchase Value Value Rate GST Input Netsupply value of addition at of on Tax GST=chain Input which GST output credit GST on

supply outputof goods – Input

and taxservices creditmade to

next stage

Manufacturer 100 30 130 10% 13 10 13–10 = 3

Whole seller 130 20 150 10% 15 13 15–13 = 2

Retailer 150 10 160 10% 16 15 16–15 = 1

Question 3 : How can the burden of tax, ingeneral, fall under GST ?

Answer : As already mentioned in Answer toQuestion 1, the present forms of CENVAT andState VAT have remained incomplete in removingfully the cascading burden of taxes already paid atearlier stages. Besides, there are several othertaxes, which both the Central Government and theState Government levy on production, manufactureand distributive trade, where no set-off is availablein the form of input tax credit. These taxes add tothe cost of goods and services through “tax on tax”

34

which the final consumer has to bear. Since, withthe introduction of GST, all the cascading effects ofCENVAT and service tax would be removed with acontinuous chain of set-off from the producer’s pointto the retailer’s point, other major Central and Statetaxes would be subsumed in GST and CST will alsobe phased out, the final net burden of tax on goods,under GST would, in general, fall. Since there wouldbe a transparent and complete chain of set-offs,this will help widening the coverage of tax base andimprove tax compliance. This may lead to highergeneration of revenues which may in turn lead to thepossibility of lowering of average tax burden.

Question 4 : How will GST benefit industry, tradeand agriculture ?

Answer : As mentioned in Answer to Question 3,the GST will give more relief to industry, trade andagriculture through a more comprehensive andwider coverage of input tax set-off and service taxset-off, subsuming of several Central and Statetaxes in the GST and phasing out of CST. Thetransparent and complete chain of set-offs which willresult in widening of tax base and better taxcompliance may also lead to lowering of tax burdenon an average dealer in industry, trade andagriculture.

35

Question 5 : How will GST benefit the exporters?

Answer : The subsuming of major Central andState taxes in GST, complete and comprehensive set-off of input goods and services and phasing out ofCentral Sales Tax (CST) would reduce the cost oflocally manufactured goods and services. This willincrease the competitiveness of Indian goods andservices in the international market and give boostto Indian exports. The uniformity in tax rates andprocedures across the country will also go a long wayin reducing the compliance cost.

Question 6 : How will GST benefit the smallentrepreneurs and small traders?

Answer : The present threshold prescribed indifferent State VAT Acts below which VAT is notapplicable varies from State to State. The existingthreshold of goods under State VAT is Rs. 5 lakhsfor a majority of bigger States and a lower thresholdfor North Eastern States and Special CategoryStates. A uniform State GST threshold across Statesis desirable and, therefore, the EmpoweredCommittee has recommended that a threshold ofgross annual turnover of Rs. 10 lakh both for goodsand services for all the States and Union Territoriesmay be adopted with adequate compensation for theStates (particularly, the States in North-Eastern

36

Region and Special Category States) where lowerthreshold had prevailed in the VAT regime. Keepingin view the interest of small traders and small scaleindustries and to avoid dual control, the Statesconsidered that the threshold for Central GST forgoods may be kept at Rs.1.5 crore and the thresholdfor services should also be appropriately high. Thisraising of threshold will protect the interest of smalltraders. A Composition scheme for small traders andbusinesses has also been envisaged under GST aswill be detailed in Answer to Question 14. Both thesefeatures of GST will adequately protect the interestsof small traders and small scale industries.

Question 7 : How will GST benefit the commonconsumers?

Answer : As already mentioned in Answer toQuestion 3, with the introduction of GST, all thecascading effects of CENVAT and service tax will bemore comprehensively removed with a continuouschain of set-off from the producer’s point to theretailer’s point than what was possible under theprevailing CENVAT and VAT regime. Certain majorCentral and State taxes will also be subsumed in GSTand CST will be phased out. Other things remainingthe same, the burden of tax on goods would, ingeneral, fall under GST and that would benefit theconsumers.

37

Question 8 : What are the salient features of theproposed GST model?

Answer : The salient features of the proposed modelare as follows:

(i) Consistent with the federal structure of thecountry, the GST will have two components:one levied by the Centre (hereinafter referredto as Central GST), and the other levied by theStates (hereinafter referred to as State GST).This dual GST model would be implementedthrough multiple statutes (one for CGST andSGST statute for every State). However, thebasic features of law such as chargeability,definition of taxable event and taxable person,measure of levy including valuation provisions,basis of classification etc. would be uniformacross these statutes as far as practicable.

(ii) The Central GST and the State GST wouldbe applicable to all transactions of goods andservices except the exempted goods andservices, goods which are outside the purviewof GST and the transactions which are belowthe prescribed threshold limits.

38

(iii) The Central GST and State GST are to be paidto the accounts of the Centre and the Statesseparately.

(iv) Since the Central GST and State GST are tobe treated separately, in general, taxes paidagainst the Central GST shall be allowed to betaken as input tax credit (ITC) for the CentralGST and could be utilized only against thepayment of Central GST. The same principlewill be applicable for the State GST.

(v) Cross utilisation of ITC between the CentralGST and the State GST would, in general, notbe allowed.

(vi) To the extent feasible, uniform procedure forcollection of both Central GST and State GSTwould be prescribed in the respectivelegislation for Central GST and State GST.

(vii) The administration of the Central GST wouldbe with the Centre and for State GST with theStates.

(viii) The taxpayer would need to submit periodicalreturns to both the Central GST authority andto the concerned State GST authorities.

39

(ix) Each taxpayer would be allotted a PAN-linked taxpayer identification number witha total of 13/15 digits. This would bring theGST PAN-linked system in line with theprevailing PAN-based system for Income taxfacilitating data exchange and taxpayercompliance. The exact design would be workedout in consultation with the Income-TaxDepartment.

(x) Keeping in mind the need of tax payersconvenience, functions such as assessment,enforcement, scrutiny and audit would beundertaken by the authority which is collectingthe tax, with information sharing between theCentre and the States.

Question 9 : Why is Dual GST required ?

Answer : India is a federal country where both theCentre and the States have been assigned the powersto levy and collect taxes through appropriatelegislation. Both the levels of Government havedistinct responsibilities to perform according tothe division of powers prescribed in the Constitutionfor which they need to raise resources. A dual GSTwill, therefore, be in keeping with the Constitutionalrequirement of fiscal federalism.

40

Question 10 : How would a particular transactionof goods and services be taxedsimultaneously under Central GST(CGST) and State GST (SGST)?

Answer : The Central GST and the State GSTwould be levied simultaneously on every transactionof supply of goods and services except the exemptedgoods and services, goods which are outside thepurview of GST and the transactions which are belowthe prescribed threshold limits. Further, both wouldbe levied on the same price or value unlike State VATwhich is levied on the value of the goods inclusive ofCENVAT. While the location of the supplier and therecipient within the country is immaterial for thepurpose of CGST, SGST would be chargeable onlywhen the supplier and the recipient are both locatedwithin the State.

Illustration I : Suppose hypothetically that the rateof CGST is 10% and that of SGST is 10%. When awholesale dealer of steel in Uttar Pradesh suppliessteel bars and rods to a construction company whichis also located within the same State for , say Rs.100, the dealer would charge CGST of Rs. 10 andSGST of Rs. 10 in addition to the basic price of thegoods. He would be required to deposit the CGSTcomponent into a Central Government account while

41

the SGST portion into the account of the concernedState Government. Of course, he need not actuallypay Rs. 20 (Rs. 10 + Rs. 10 ) in cash as he would beentitled to set-off this liability against the CGST orSGST paid on his purchases (say, inputs). But forpaying CGST he would be allowed to use only thecredit of CGST paid on his purchases while for SGSThe can utilize the credit of SGST alone. In otherwords, CGST credit cannot, in general, be used forpayment of SGST. Nor can SGST credit be used forpayment of CGST.

Illustration II: Suppose, again hypothetically, thatthe rate of CGST is 10% and that of SGST is 10%.When an advertising company located in Mumbaisupplies advertising services to a companymanufacturing soap also located within the State ofMaharashtra for, let us say Rs. 100, the ad companywould charge CGST of Rs. 10 as well as SGST ofRs. 10 to the basic value of the service. He would berequired to deposit the CGST component into aCentral Government account while the SGST portioninto the account of the concerned State Government.Of course, he need not again actually pay Rs. 20 (Rs.10+Rs. 10) in cash as it would be entitled to set-offthis liability against the CGST or SGST paid on hispurchase (say, of inputs such as stationery, officeequipment, services of an artist etc). But for paying

42

CGST he would be allowed to use only the credit ofCGST paid on its purchase while for SGST he canutilise the credit of SGST alone. In other words, CGSTcredit cannot, in general, be used for payment ofSGST. Nor can SGST credit be used for payment ofCGST.

Question 11 : Which Central and State taxes areproposed to be subsumed under GST ?

Answer : The various Central, State and Locallevies were examined to identify their possibility ofbeing subsumed under GST. While identifying, thefollowing principles were kept in mind:

(i) Taxes or levies to be subsumed should beprimarily in the nature of indirect taxes, eitheron the supply of goods or on the supply ofservices.

(ii) Taxes or levies to be subsumed should be partof the transaction chain which commences withimport/ manufacture/ production of goods orprovision of services at one end and theconsumption of goods and services at the other.

(iii) The subsumation should result in free flow oftax credit in intra and inter-State levels.

43

(iv) The taxes, levies and fees that are notspecifically related to supply of goods & servicesshould not be subsumed under GST.

(v) Revenue fairness for both the Union and theStates individually would need to be attempted.

On application of the above principles, theEmpowered Committee has recommended that thefollowing Central Taxes should be, to begin with,subsumed under the Goods and Services Tax:

(i) Central Excise Duty

(ii) Additional Excise Duties

(iii) The Excise Duty levied under the Medicinaland Toiletries Preparation Act

(iv) Service Tax

(v) Additional Customs Duty, commonly known asCountervailing Duty (CVD)

(vi) Special Additional Duty of Customs - 4% (SAD)

(vii) Surcharges, and

(viii) Cesses.

44

The following State taxes and levies would be, tobegin with, subsumed under GST:

(i) VAT / Sales tax

(ii) Entertainment tax (unless it is levied by thelocal bodies).

(iii) Luxury tax

(iv) Taxes on lottery, betting and gambling.

(v) State Cesses and Surcharges in so far as theyrelate to supply of goods and services.

(vi) Entry tax not in lieu of Octroi.

Purchase tax: Some of the States felt that they aregetting substantial revenue from Purchase Tax and,therefore, it should not be subsumed under GST whilemajority of the States were of the view that no suchexemptions should be given. The difficulties of thefoodgrain producing States was appreciated assubstantial revenue is being earned by them fromPurchase Tax and it was, therefore, felt that in casePurchase Tax has to be subsumed then adequate andcontinuing compensation has to be provided to suchStates. This issue is being discussed in consultationwith the Government of India.

45

Tax on items containing Alcohol: Alcoholicbeverages would be kept out of the purview of GST.Sales Tax/VAT could be continued to be levied onalcoholic beverages as per the existing practice. Incase it has been made Vatable by some States, thereis no objection to that. Excise Duty, which is presentlylevied by the States may not also be affected.

Tax on Tobacco products: Tobacco productswould be subjected to GST with ITC. Centre may beallowed to levy excise duty on tobacco products overand above GST with ITC.

Tax on Petroleum Products: As far as petroleumproducts are concerned, it was decided that the basketof petroleum products, i.e. crude, motor spirit(including ATF) and HSD would be kept outside GSTas is the prevailing practice in India. Sales Tax couldcontinue to be levied by the States on these productswith prevailing floor rate. Similarly, Centre could alsocontinue its levies. A final view whether Natural Gasshould be kept outside the GST will be taken afterfurther deliberations.

Taxation of Services : As indicated earlier, boththe Centre and the States will have concurrent powerto levy tax on goods and services. In the case of States,the principle for taxation of intra-State and inter-

46

State has already been formulated by the WorkingGroup of Principal Secretaries /Secretaries ofFinance / Taxation and Commissioners of TradeTaxes with senior representatives of Department ofRevenue, Government of India. For inter-Statetransactions an innovative model of Integrated GSTwill be adopted by appropriately aligning andintegrating CGST and IGST.

Question 12 : What is the rate structure proposedunder GST ?

Answer : The Empowered Committee has decidedto adopt a two-rate structure –a lower rate fornecessary items and items of basic importance and astandard rate for goods in general. There will also bea special rate for precious metals and a list ofexempted items. For upholding of special needs ofeach State as well as a balanced approach to federalflexibility, it is being discussed whether the exemptedlist under VAT regime including Goods of LocalImportance may be retained in the exempted listunder State GST in the initial years. It is also beingdiscussed whether the Government of India mayadopt, to begin with, a similar approach towardsexempted list under the CGST.

For CGST relating to goods, the Statesconsidered that the Government of India might also

47

have a two-rate structure, with conformity in thelevels of rate with the SGST. For taxation ofservices, there may be a single rate for both CGSTand SGST.

The exact value of the SGST and CGSTrates, including the rate for services, will be madeknown duly in course of appropriate legislativeactions.

Question 13: What is the concept of providingthreshold exemption for GST?

Answer : Threshold exemption is built into a taxregime to keep small traders out of tax net. This hasthree-fold objectives:

a) It is difficult to administer small traders andcost of administering of such traders is veryhigh in comparison to the tax paid by them.

b) The compliance cost and compliance effortwould be saved for such small traders.

c) Small traders get relative advantage over largeenterprises on account of lower tax incidence.

The present thresholds prescribed in different StateVAT Acts below which VAT is not applicable varies

48

from State to State. A uniform State GST thresholdacross States is desirable and, therefore, as alreadymentioned in Answer to Question 6, it has beenconsidered that a threshold of gross annual turnoverof Rs. 10 lakh both for goods and services for all theStates and Union Territories might be adopted withadequate compensation for the States (particularly,the States in North-Eastern Region and SpecialCategory States) where lower threshold had prevailedin the VAT regime. Keeping in view the interest ofsmall traders and small scale industries and to avoiddual control, the States also considered that thethreshold for Central GST for goods may be keptRs.1.5 Crore and the threshold for services shouldalso be appropriately high.

Question 14 : What is the scope of composition andcompounding scheme under GST?

Answer : As already mentioned in Answer toQuestion 6, a Composition/Compounding Scheme willbe an important feature of GST to protect theinterests of small traders and small scale industries.The Composition/Compounding scheme for thepurpose of GST should have an upper ceiling on grossannual turnover and a floor tax rate with respect togross annual turnover. In particular there will be acompounding cut-off at Rs. 50 lakhs of the gross

49

annual turnover and the floor rate of 0.5% across theStates. The scheme would allow option for GSTregistration for dealers with turnover below thecompounding cut-off.

Question 15 : How will imports be taxed under GST ?

Answer : With Constitutional Amendments, bothCGST and SGST will be levied on import of goodsand services into the country. The incidence of taxwill follow the destination principle and the taxrevenue in case of SGST will accrue to the Statewhere the imported goods and services are consumed.Full and complete set-off will be available on the GSTpaid on import on goods and services.

Question 16 : Will cross utilization of creditsbetween goods and services beallowed under GST regime?

Answer : Cross utilization of credit of CGSTbetween goods and services would be allowed.Similarly, the facility of cross utilization of credit willbe available in case of SGST. However, the crossutilization of CGST and SGST would generally notbe allowed except in the case of inter-State supply ofgoods and services under the IGST model which isexplained in answer to the next question.

50

Question 17 : How will be Inter-State Transactionsof Goods and Services be taxed underGST in terms of IGST method ?

Answer : The Empowered Committee has acceptedthe recommendation for adoption of IGST model fortaxation of inter-State transaction of Goods andServices. The scope of IGST Model is that Centrewould levy IGST which would be CGST plus SGSTon all inter-State transactions of taxable goods andservices. The inter-State seller will pay IGST onvalue addition after adjusting available credit ofIGST, CGST, and SGST on his purchases. TheExporting State will transfer to the Centre the creditof SGST used in payment of IGST. The Importingdealer will claim credit of IGST while discharginghis output tax liability in his own State. The Centrewill transfer to the importing State the credit of IGSTused in payment of SGST. The relevant informationis also submitted to the Central Agency which willact as a clearing house mechanism, verify the claimsand inform the respective governments to transferthe funds.

The major advantages of IGST Model are:

a) Maintenance of uninterrupted ITC chain oninter-State transactions.

51

b) No upfront payment of tax or substantialblockage of funds for the inter-State seller orbuyer.

c) No refund claim in exporting State, as ITC isused up while paying the tax.

d) Self monitoring model.

e) Level of computerisation is limited to inter-Statedealers and Central and State Governmentsshould be able to computerise their processesexpeditiously.

f) As all inter-State dealers will be e-registered andcorrespondence with them will be bye-mail, the compliance level will improvesubstantially.

g) Model can take ‘Business to Business’ as well as‘Business to Consumer’ transactions intoaccount.

Question 18 : Why does introduction of GST requirea Constitutional Amendment?

Answer : The Constitution provides fordelineation of power to tax between the Centre andStates. While the Centre is empowered to tax services

52

and goods upto the production stage, the States havethe power to tax sale of goods. The States do not havethe powers to levy a tax on supply of services whilethe Centre does not have power to levy tax on thesale of goods. Thus, the Constitution does not vestexpress power either in the Central or StateGovernment to levy a tax on the ‘supply of goods andservices’. Moreover, the Constitution also does notempower the States to impose tax on imports.Therefore, it is essential to have ConstitutionalAmendments for empowering the Centre to levy taxon sale of goods and States for levy of service tax andtax on imports and other consequential issues.

As part of the exercise on ConstitutionalAmendment, there would be a special attention tothe formulation of a mechanism for upholding theneed for a harmonious structure for GST along withthe concern for the powers of the Centre and theStates in a federal structure.

Question 19: How are the legislative steps beingtaken for CGST and SGST ?

Answer : A Joint Working Group has recently beenconstituted (September 30, 2009) comprising of theofficials of the Central and State Governments toprepare, in a time-bound manner a draft legislationfor Constitutional Amendment.

53

Question 20: How will the rules for administrationof CGST and SGST be framed?

Answer : The Joint Working Group, as mentionedabove, has also been entrusted the task of preparingdraft legislation for CGST, a suitable ModelLegislation for SGST and rules and procedures forCGST and SGST. Simultaneous steps have also beeninitiated for drafting of legislation for IGST and rulesand procedures. As a part of this exercise, theWorking Group will also address to the issues ofdispute resolution and advance ruling.