Embed Size (px)

Citation preview

November 5, 2018

FinTech & InsurTech : cooperation or competitionwith the large financial institutions ?

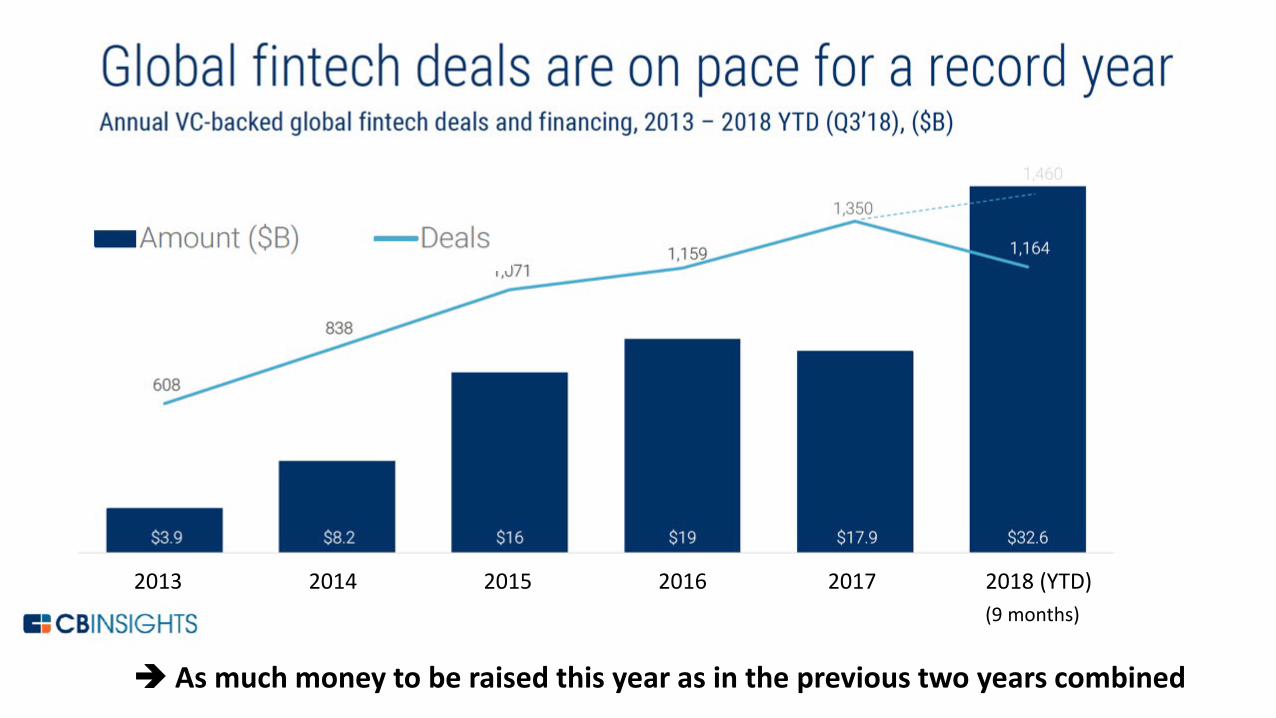

(9 months)2013 2014 2015 2016 2017 2018 (YTD)

As much money to be raised this year as in the previous two years combined

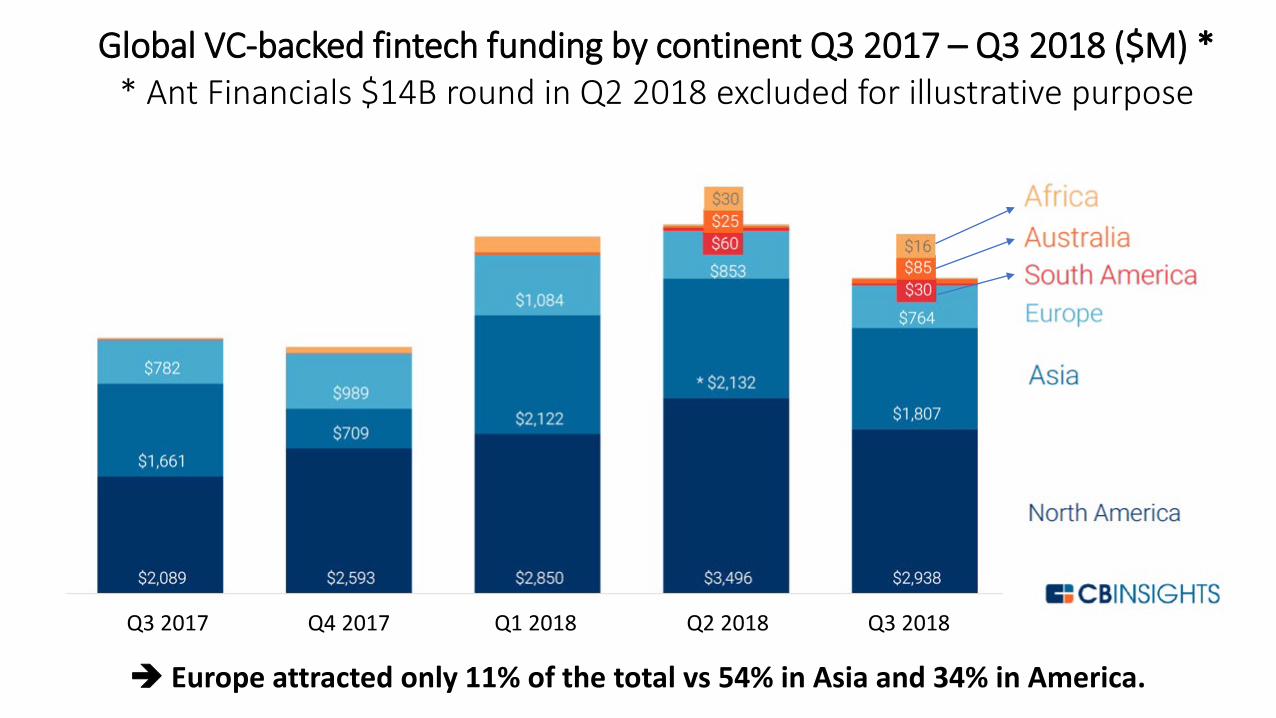

Global VC-backed fintech funding by continent Q3 2017 – Q3 2018 ($M) ** Ant Financials $14B round in Q2 2018 excluded for illustrative purpose

Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018

Europe attracted only 11% of the total vs 54% in Asia and 34% in America.

PROGRAM• Quentin Colmant,

co-founder and managing director of Qover (InsurTech)• Bart Vanhaeren,

co-founder and CEO of InvestSuite (robo advisers)• Prof. Georges Hubner,

co-founder of Gambit (AI for investment advice)• Jean-Louis Van Houwe,

founder and CEO of Monizze (digital vouchers)• Fabian Vandenreydt,

executive chairman at B-Hive Europe (incubator)

• Panel dicussion

• Question time

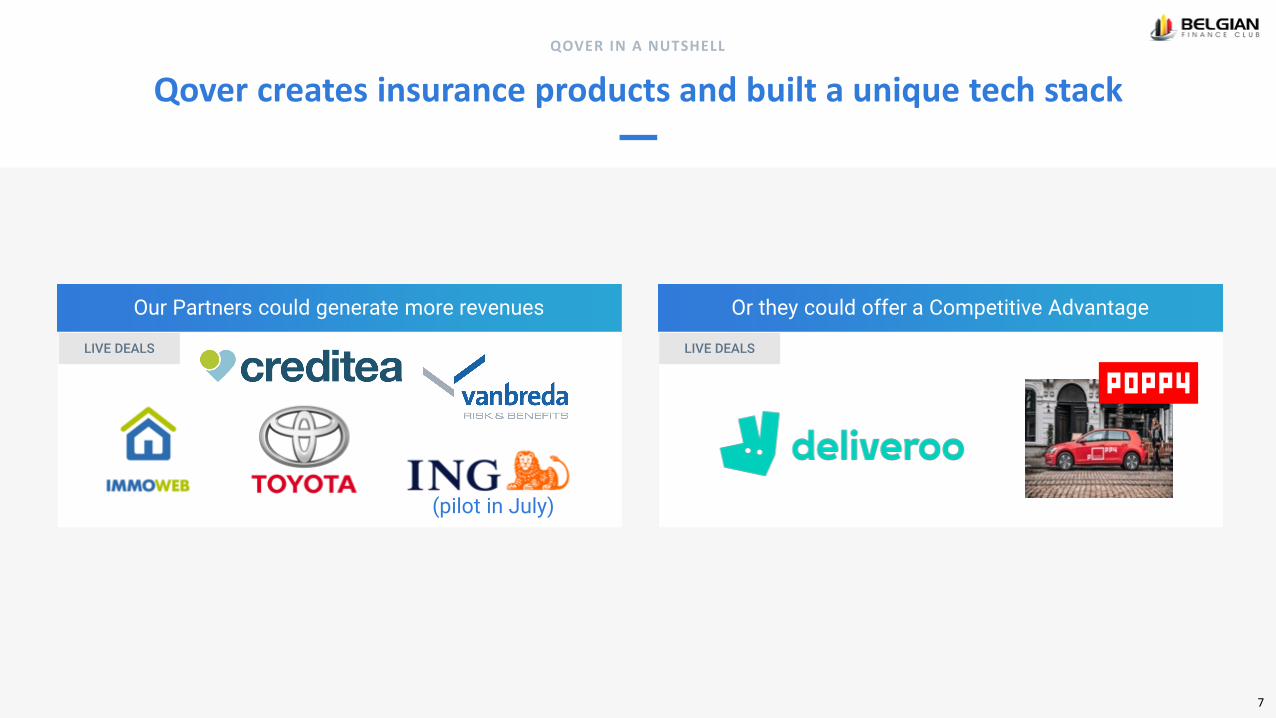

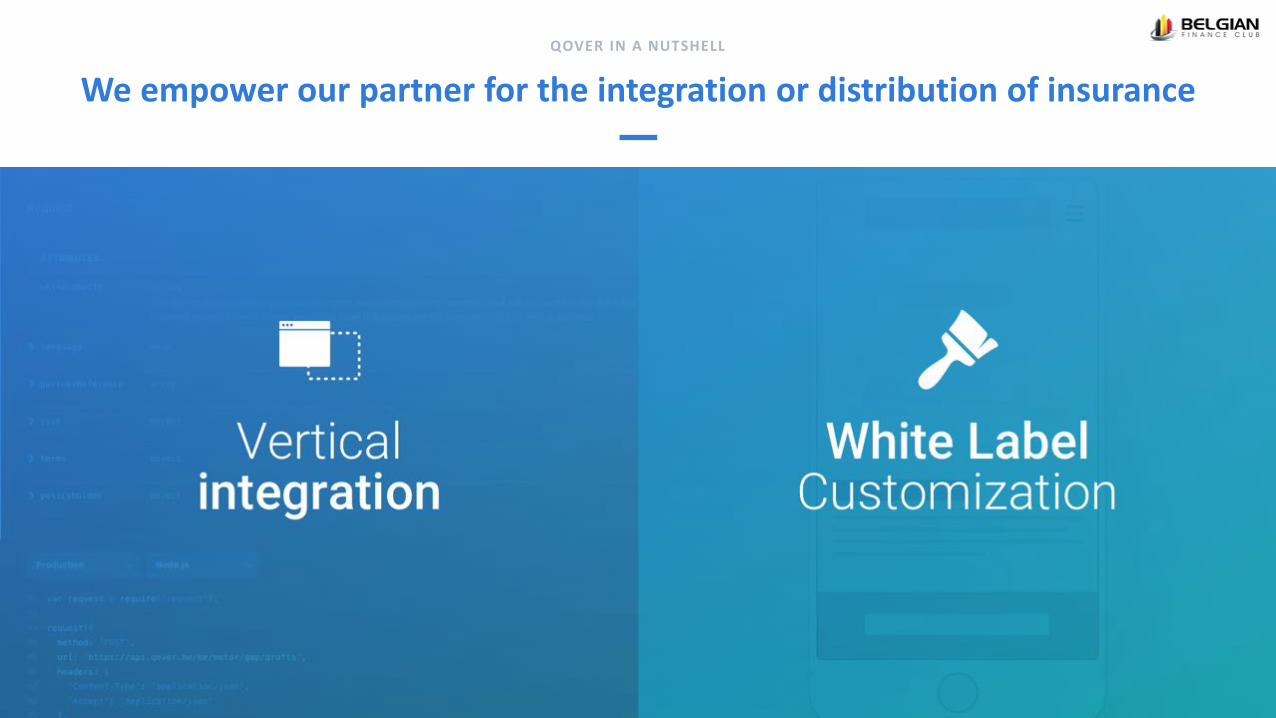

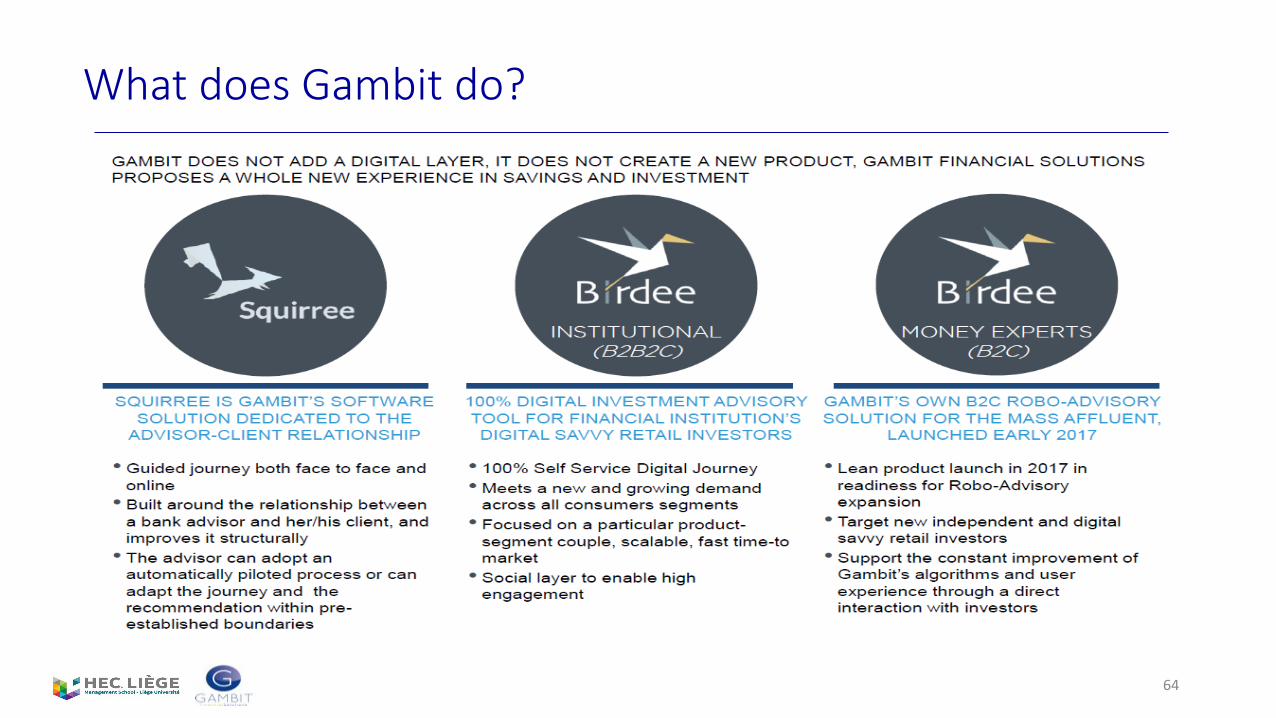

Qover creates insurance products and built a unique tech stack QOVER IN A NUTSHELL

LIVE DEALS LIVE DEALS

Our Partners could generate more revenues Or they could offer a Competitive Advantage

7

(pilot in July)

QOVER IN A NUTSHELL

We empower our partner for the integration or distribution of insurance

QOVER IN A NUTSHELL

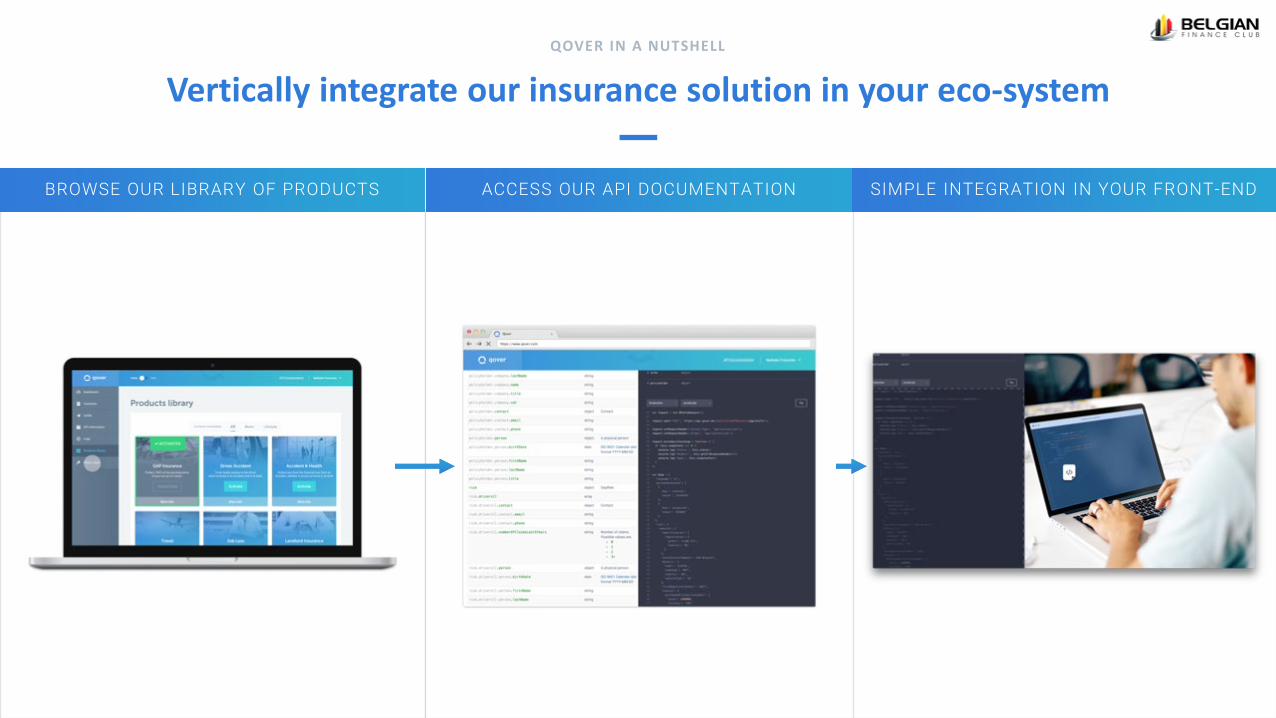

Vertically integrate our insurance solution in your eco-system

BROWSE OUR LIBRARY OF PRODUCTS ACCESS OUR API DOCUMENTATION SIMPLE INTEGRATION IN YOUR FRONT-END

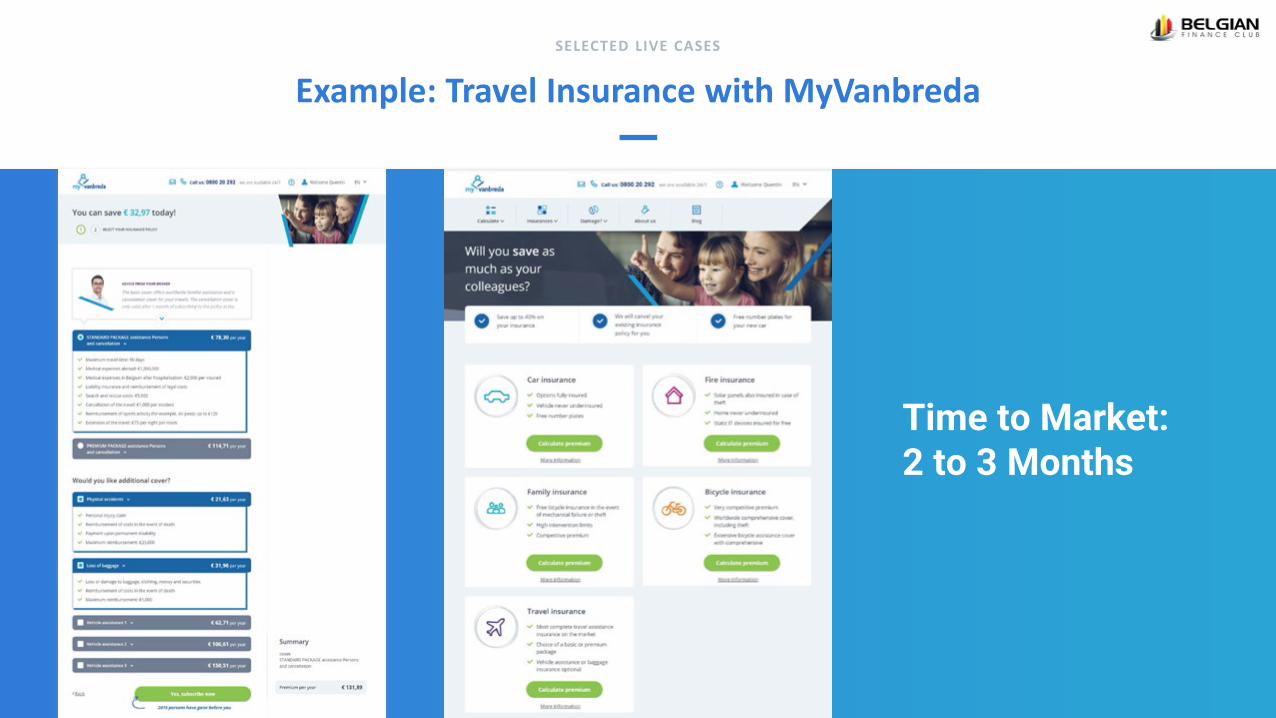

Example: Travel Insurance with MyVanbredaSELECTED LIVE CASES

Time to Market: 2 to 3 Months

QOVER IN A NUTSHELL

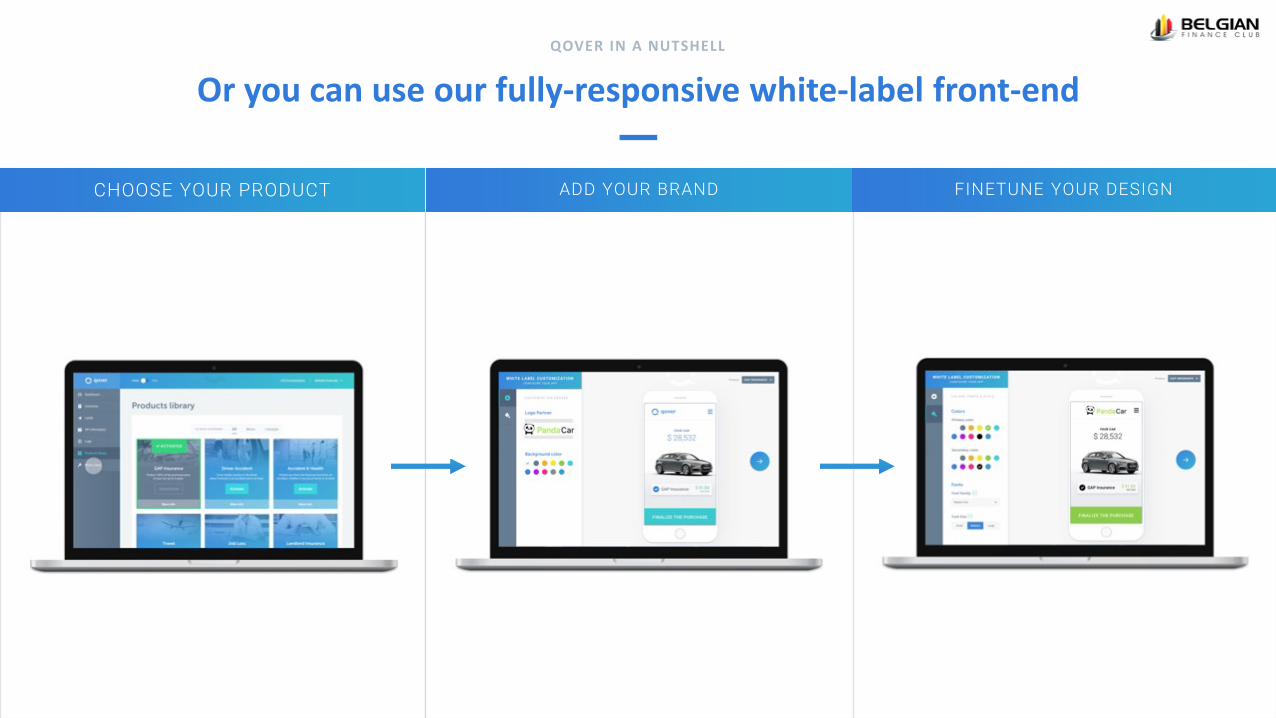

Or you can use our fully-responsive white-label front-end

CHOOSE YOUR PRODUCT ADD YOUR BRAND FINETUNE YOUR DESIGN

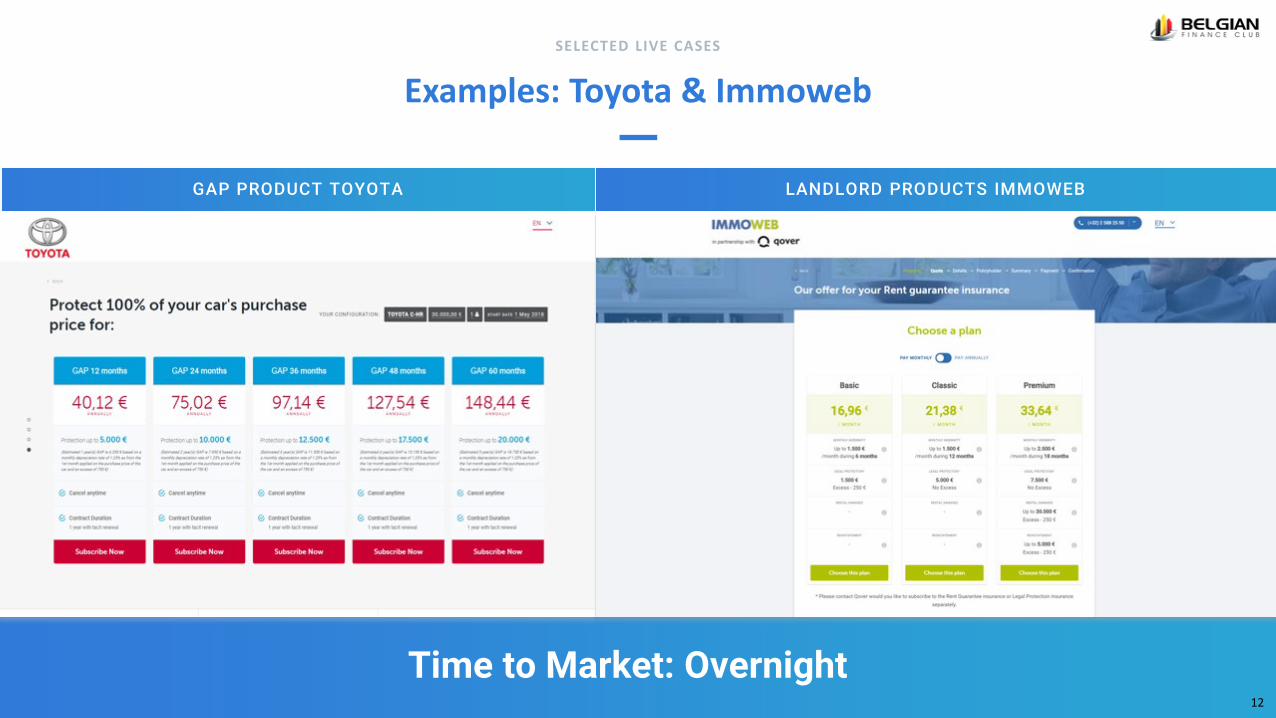

Examples: Toyota & ImmowebSELECTED LIVE CASES

GAP PRODUCT TOYOTA LANDLORD PRODUCTS IMMOWEB

12

Time to Market: Overnight

QOVER IN A NUTSHELL

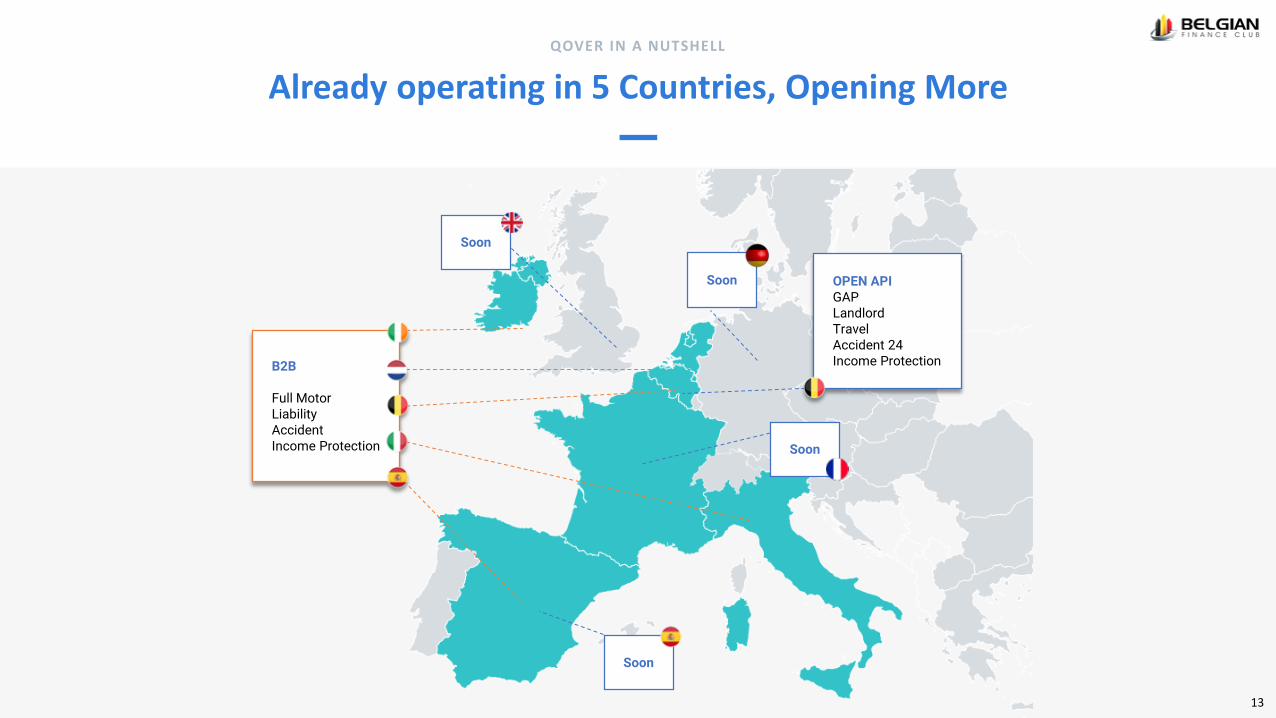

Already operating in 5 Countries, Opening More

Soon

B2B

Full MotorLiabilityAccidentIncome Protection

OPEN APIGAPLandlordTravelAccident 24Income Protection

Soon

13

Soon

Soon

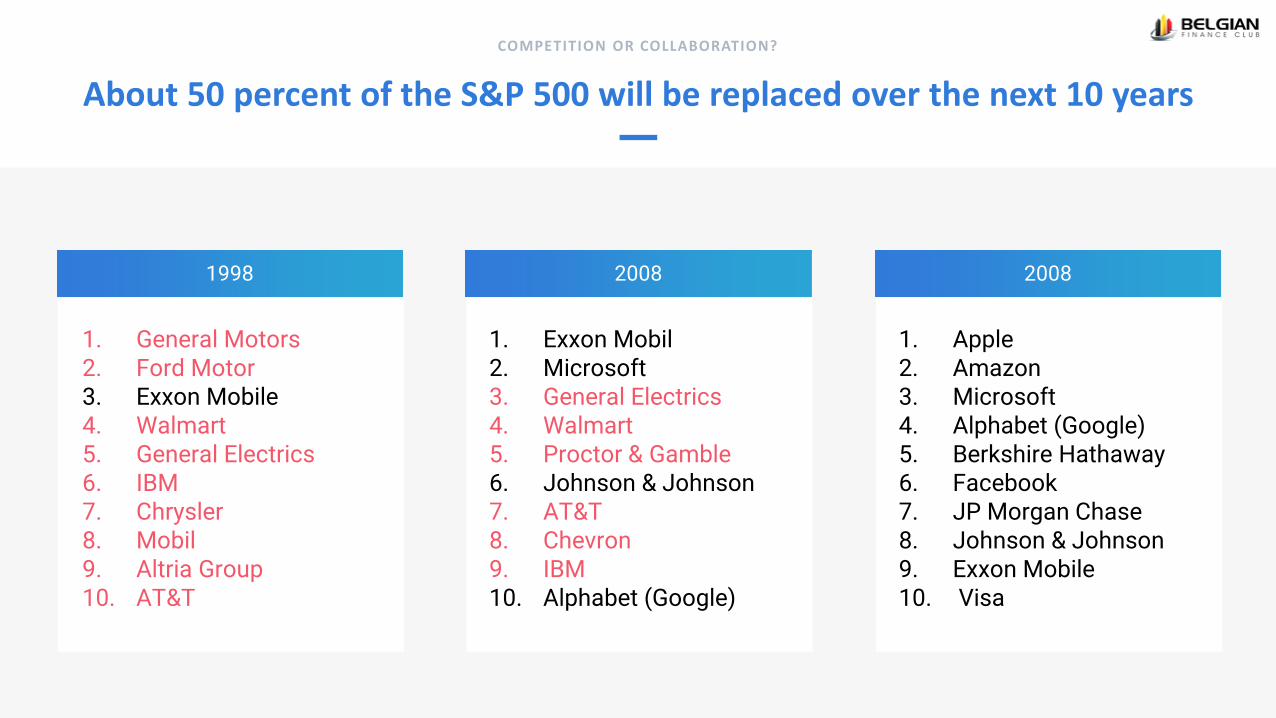

About 50 percent of the S&P 500 will be replaced over the next 10 yearsCOMPETITION OR COLLABORATION?

1998

1. General Motors2. Ford Motor3. Exxon Mobile4. Walmart5. General Electrics6. IBM7. Chrysler8. Mobil9. Altria Group10. AT&T

2008

1. Exxon Mobil2. Microsoft3. General Electrics4. Walmart5. Proctor & Gamble6. Johnson & Johnson7. AT&T8. Chevron9. IBM10. Alphabet (Google)

2008

1. Apple2. Amazon3. Microsoft4. Alphabet (Google)5. Berkshire Hathaway6. Facebook7. JP Morgan Chase8. Johnson & Johnson9. Exxon Mobile10. Visa

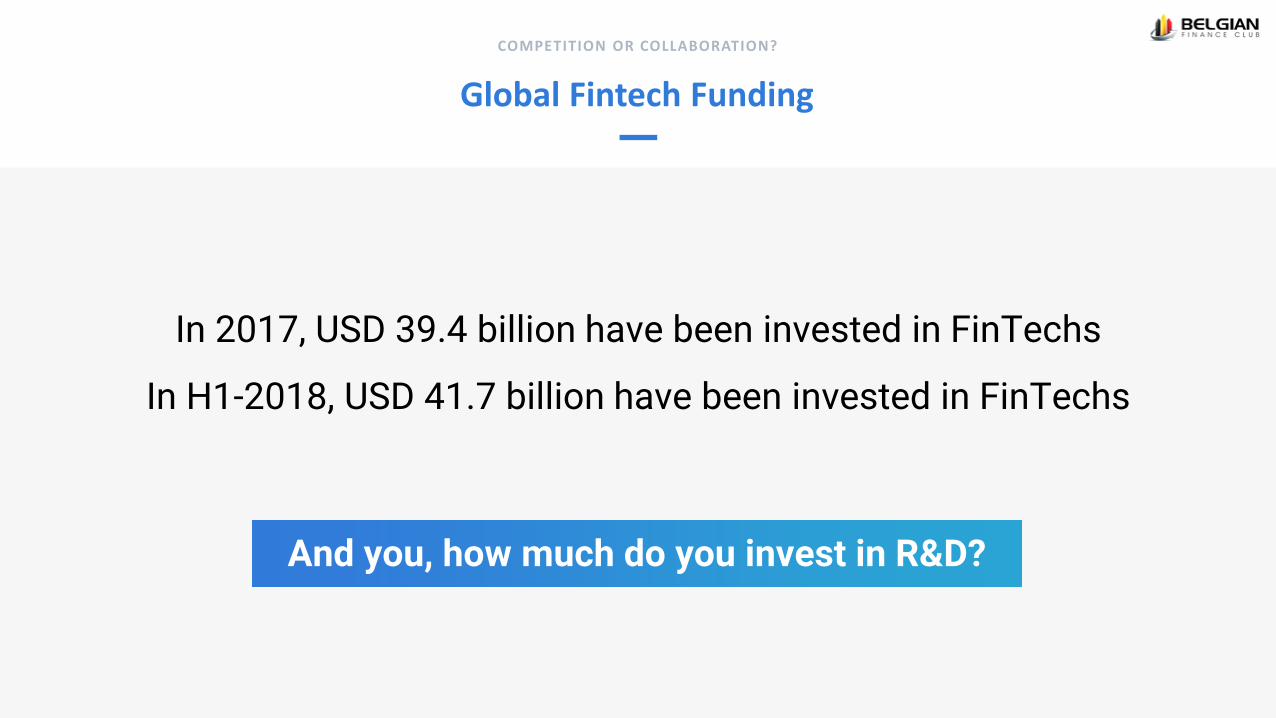

Global Fintech Funding

In 2017, USD 39.4 billion have been invested in FinTechs

In H1-2018, USD 41.7 billion have been invested in FinTechs

COMPETITION OR COLLABORATION?

And you, how much do you invest in R&D?

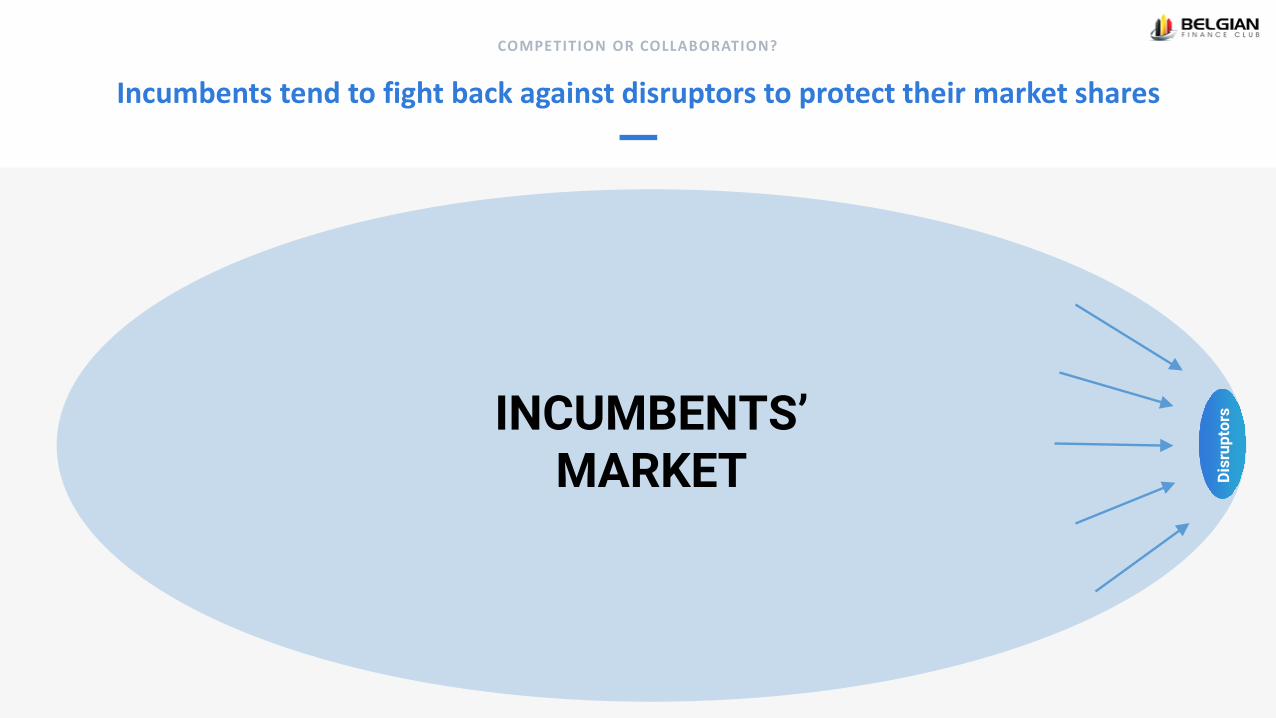

Incumbents tend to fight back against disruptors to protect their market shares

INCUMBENTS’ MARKET Di

srup

tors

COMPETITION OR COLLABORATION?

Instead of collaborating to benefit from new market opportunities

INCUMBENTS’ MARKET

NEW MARKET OPPORTUNITIES

COMPETITION OR COLLABORATION?

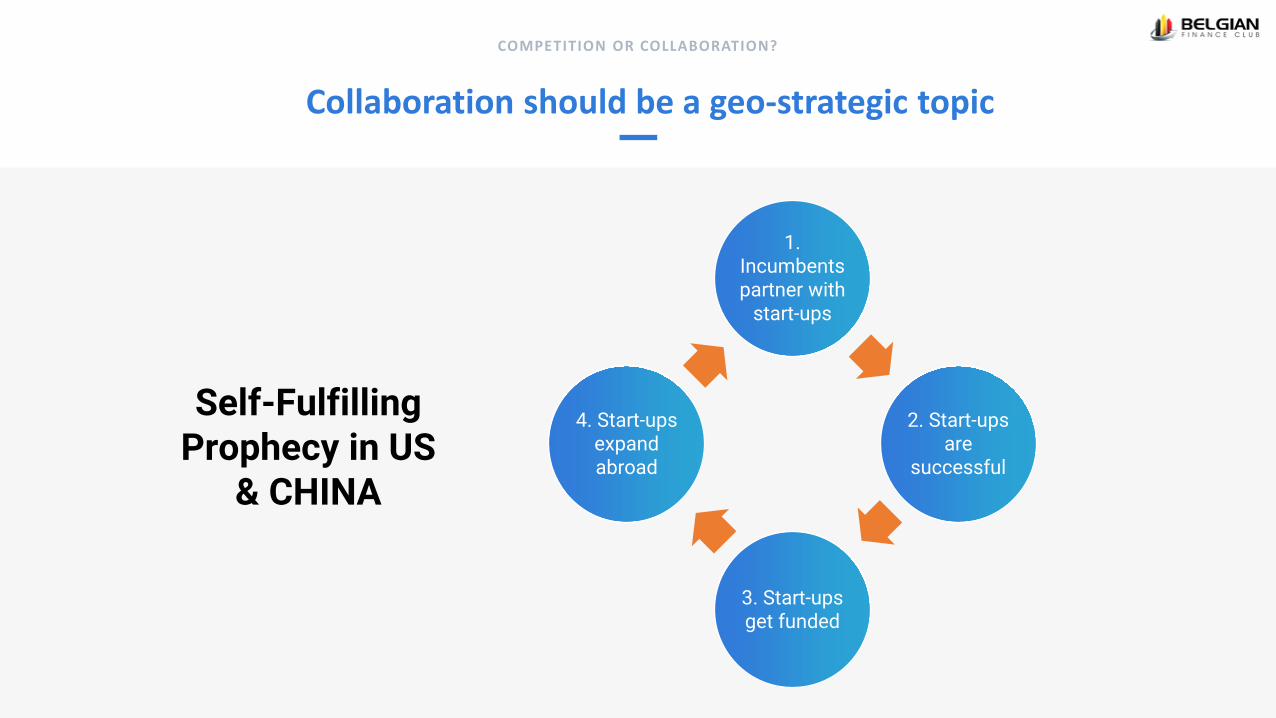

Collaboration should be a geo-strategic topic

Self-Fulfilling Prophecy in US

& CHINA

1. Incumbents partner with

start-ups

2. Start-ups are

successful

3. Start-ups get funded

4. Start-ups expand abroad

COMPETITION OR COLLABORATION?

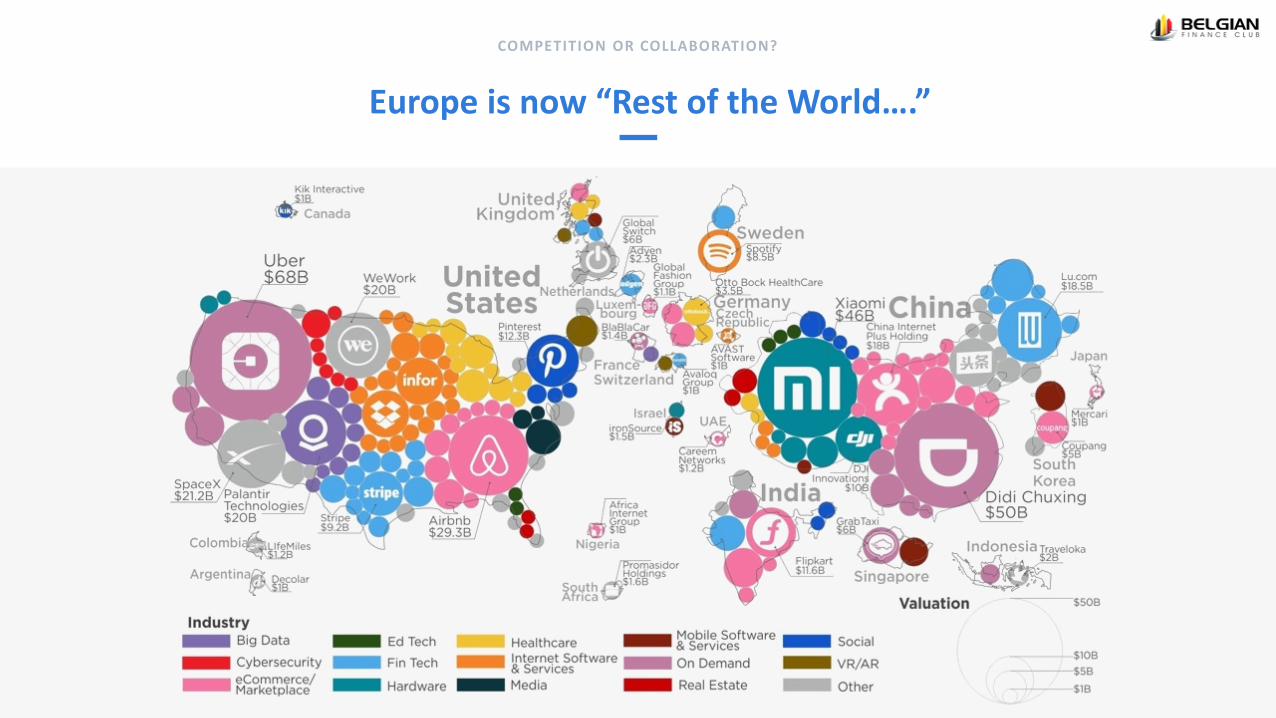

Europe is now “Rest of the World….”

COMPETITION OR COLLABORATION?

Question / Answer

ANSWER

A REAL-LIFE CASE IN BELGIUM

QUESTION

How many full digital insurance with banking APPS?

Question / AnswerA REAL-LIFE CASE IN BELGIUM

ANSWER

QUESTION

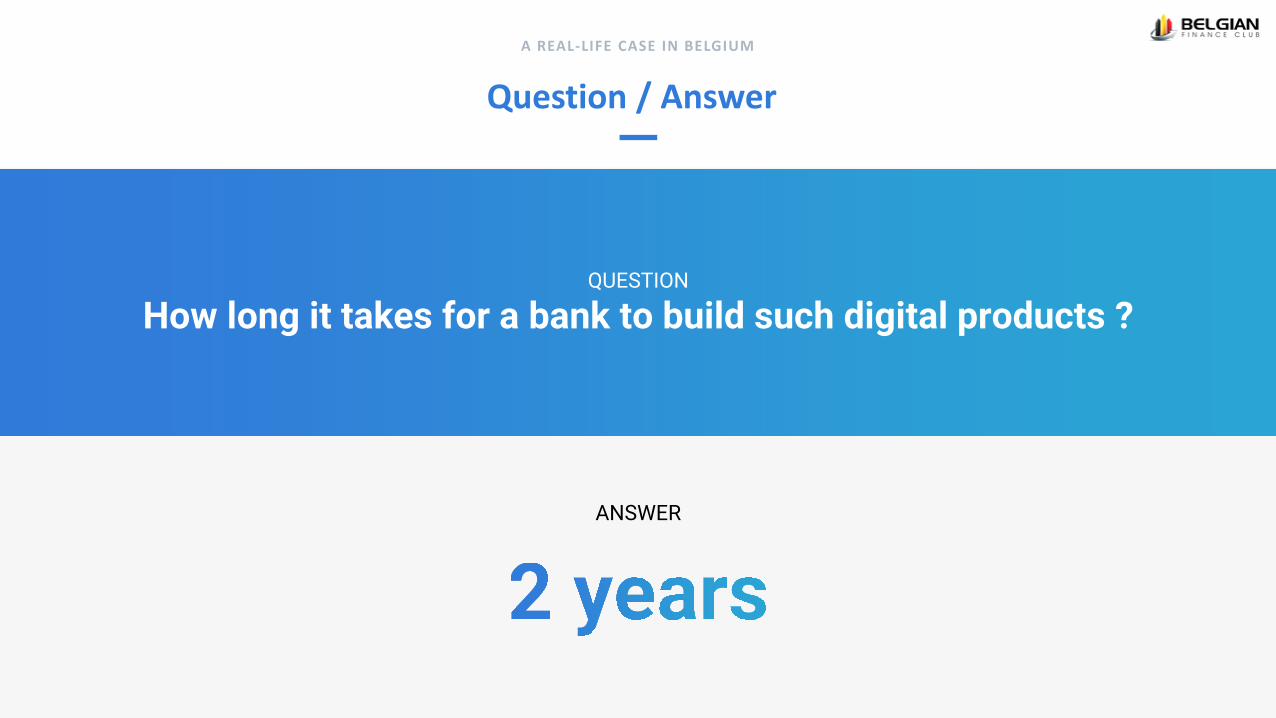

How long it takes for a bank to build such digital products ?

Question / AnswerA REAL-LIFE CASE IN BELGIUM

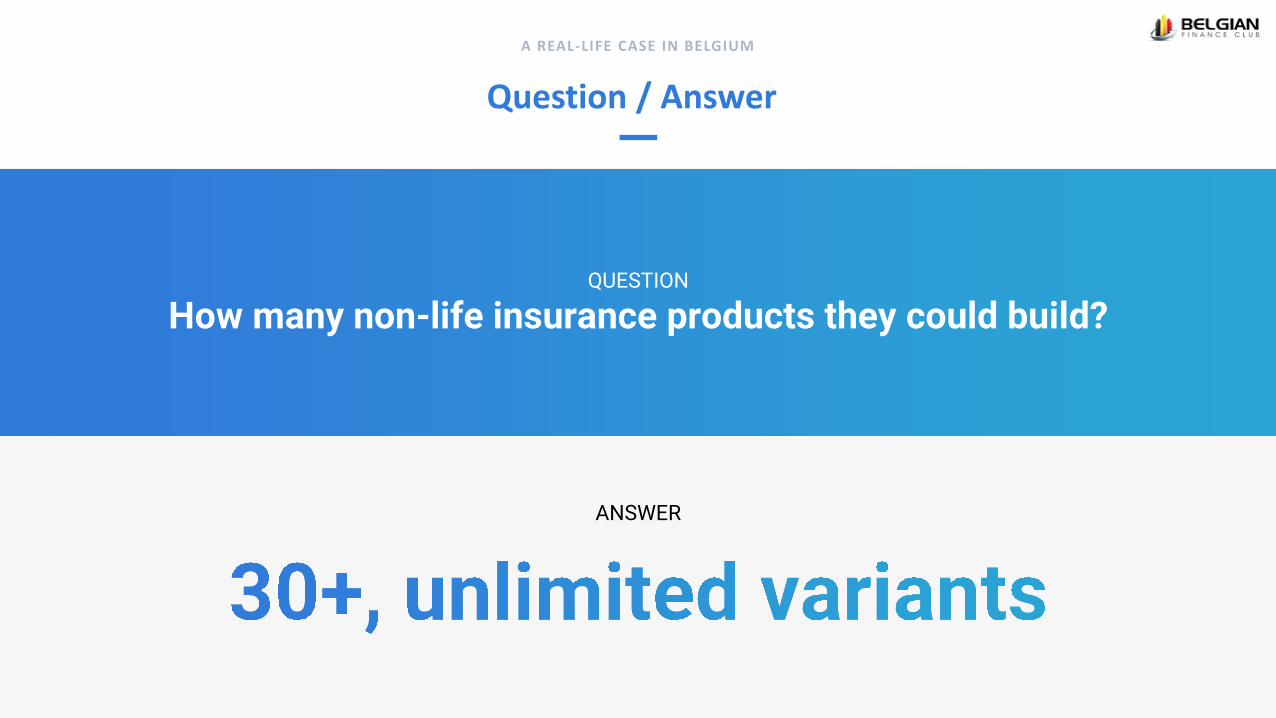

ANSWER

QUESTION

How many non-life insurance products they could build?

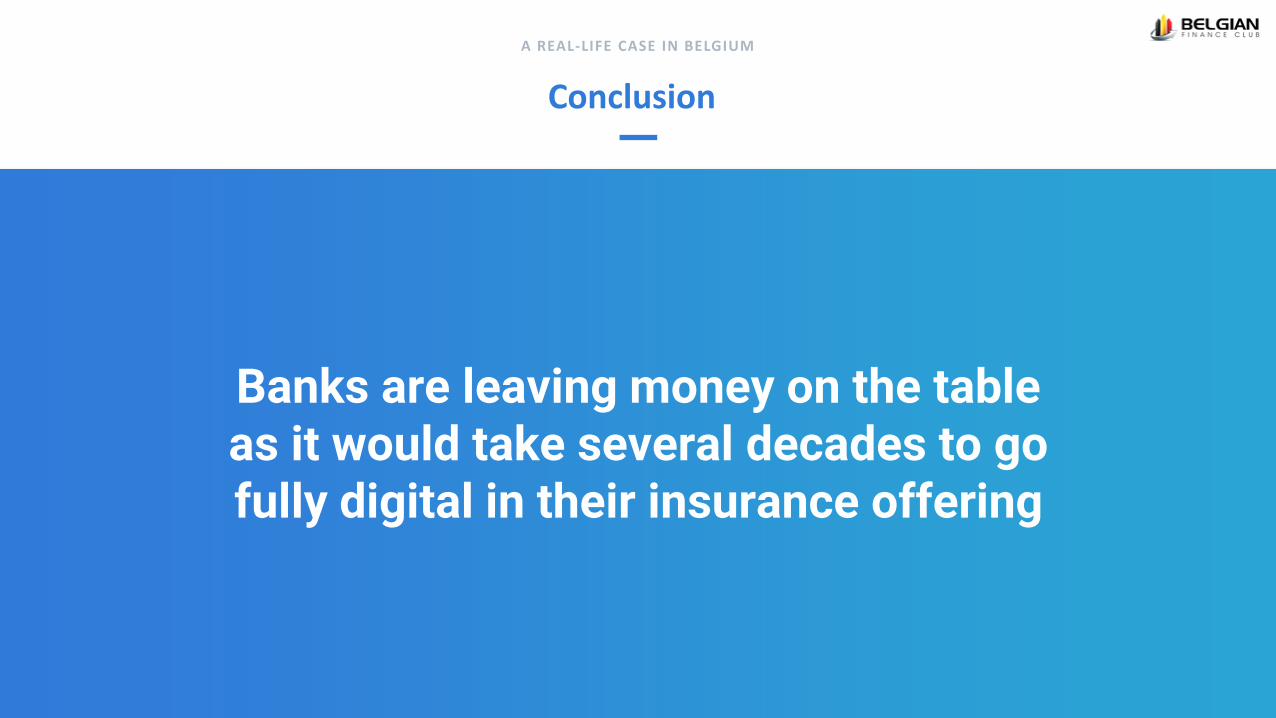

ConclusionA REAL-LIFE CASE IN BELGIUM

Banks are leaving money on the table as it would take several decades to go fully digital in their insurance offering

What they should do?

Each Belgian banks, could offer at least 6 insurance products (fully digital) from Qover

And about 15+ in 2020…

A REAL-LIFE CASE IN BELGIUM

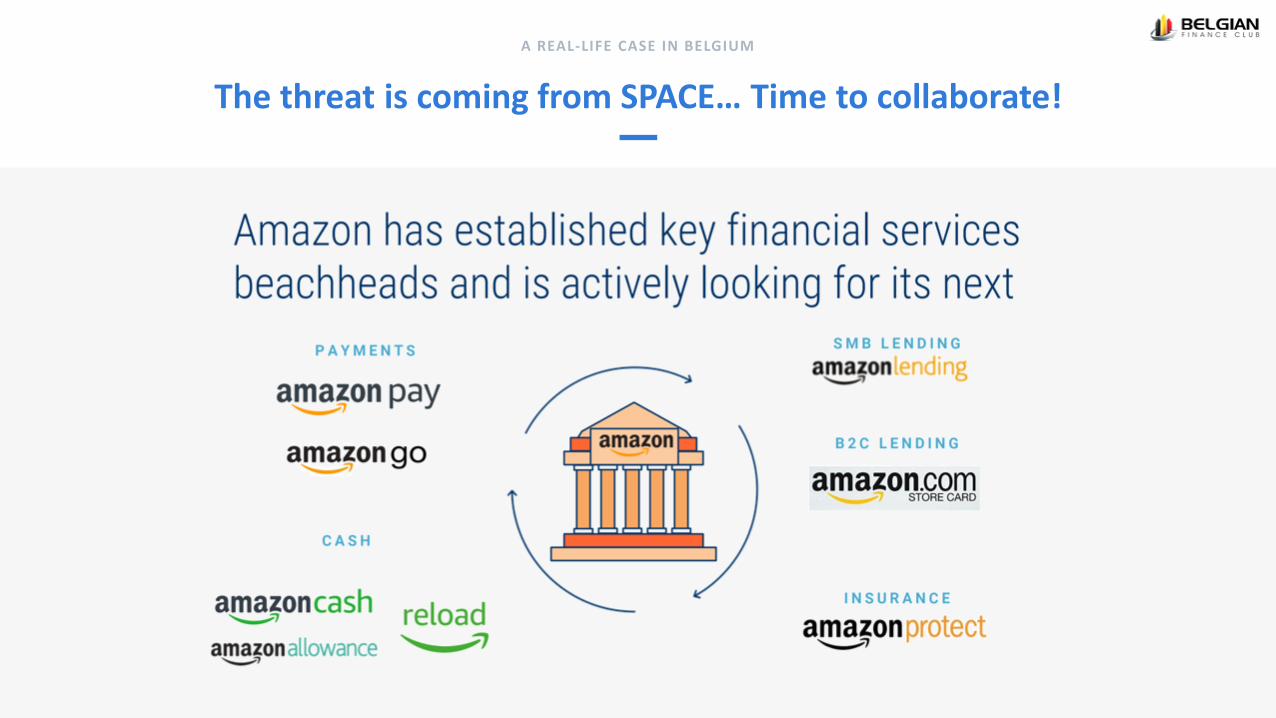

The threat is coming from SPACE… Time to collaborate!A REAL-LIFE CASE IN BELGIUM

INNOVATION AS A SERVICE

WE ARE A EUROPEAN B2B FINTECH AIMING FOR

LEADERSHIP IN THE DIGITAL RETAIL WEALTH

MANAGEMENT AND INVESTMENT SPACE

WE LAUNCHED IN JUNE 2018

BART VANHAERENCEO

Seasoned Banking Executive

Founded 3 businesses

20 years banking experience

Ex GE Capital; Arthur D. Little; KBC Securities

MBA IMD/Lausanne

EMMANUEL WILDIERSHEAD PRODUCT R&D

Master in Electrotechnical Engineering

CFA charterholder

Head Portfolio Construction at KBC Asset Management

Senior Quantitative Equity Analyst/ Portfolio Manager at Schroders, London

LAURENT SORBERCTO / CO-FOUNDER

Ph.D. in Mathematical Engineering, Summa cum Laude

Founder of B2C roboadvisory

Founder of AI & machine learning consultancy

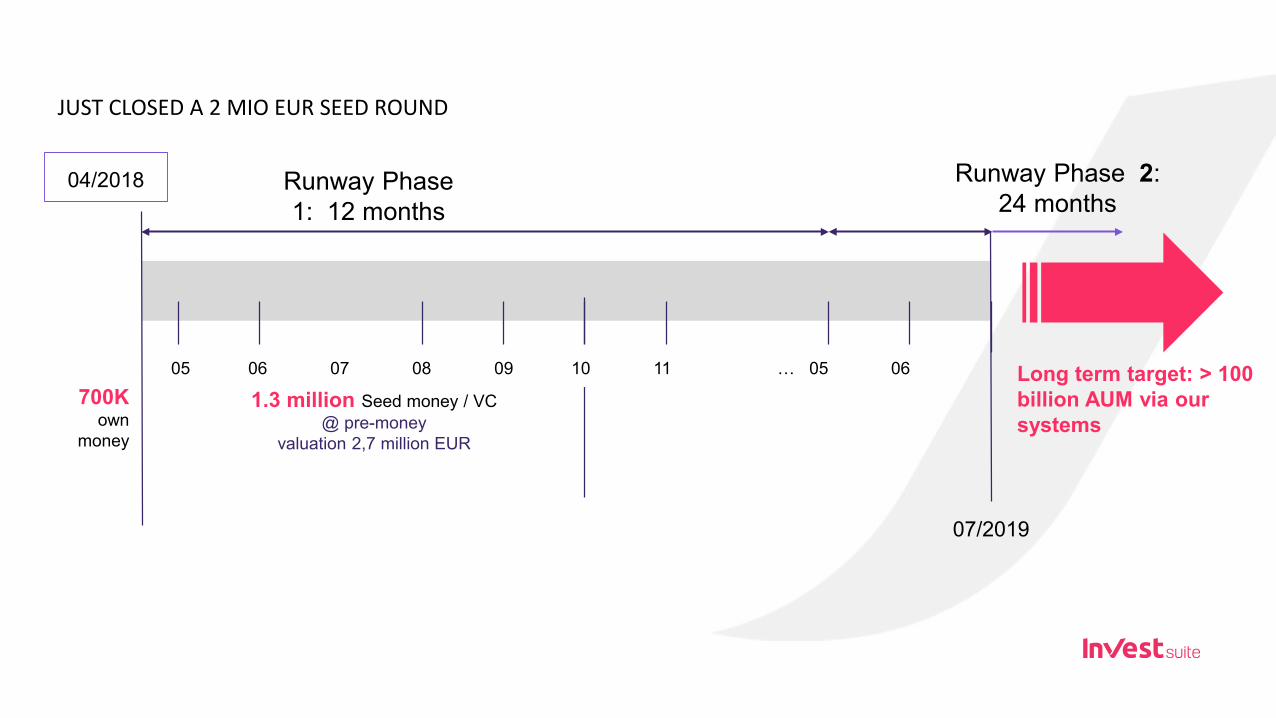

JUST CLOSED A 2 MIO EUR SEED ROUND

07/2019

04/2018

700K own

money

Runway Phase 1: 12 months

Runway Phase 2: 24 months

1.3 million Seed money / VC@ pre-money

valuation 2,7 million EUR

Long term target: > 100 billion AUM via our systems

05 06 07 08 09 10 11 … 05 06

LEUVEN

LUXEMBOURG

WARSAW

FIRST LOI

35

WE ALSO HAVE A SECOND PRODUCT IN THE MAKING: A NEXT GENERATION ONLINE INVESTMENT PLATFORM NOT AIED AT ‘TRADERS’ BUT AT NORMAL RETAIL CLIENTS

INTUITIVE TO USE –LIMITED MARKETS –SIMPLE BUT POWERFULL

Is there a Tsunami on its way in

the world of wealth management

and investments?

Is the old cosy world of face

to face ‘offline’ banking a

picture of the past?

ANOTHER ROBOADVISOR?

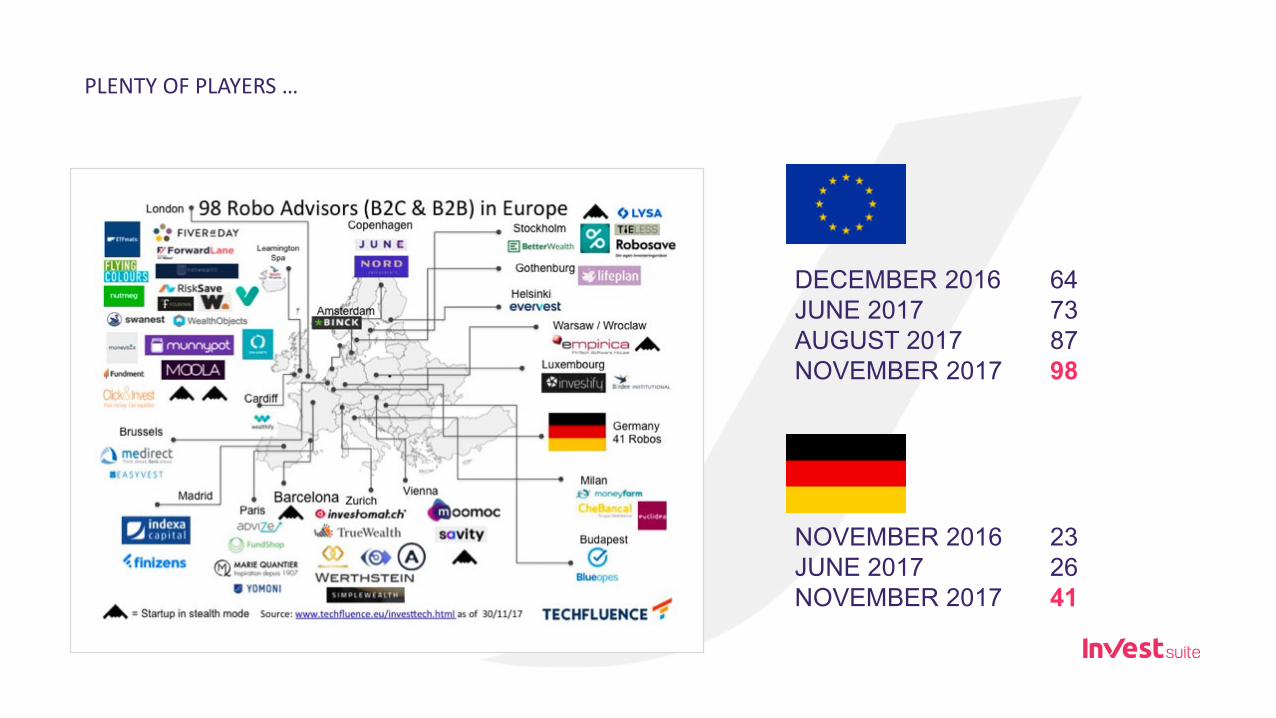

PLENTY OF PLAYERS …

DECEMBER 2016JUNE 2017AUGUST 2017NOVEMBER 2017

NOVEMBER 2016JUNE 2017NOVEMBER 2017

64738798

232641

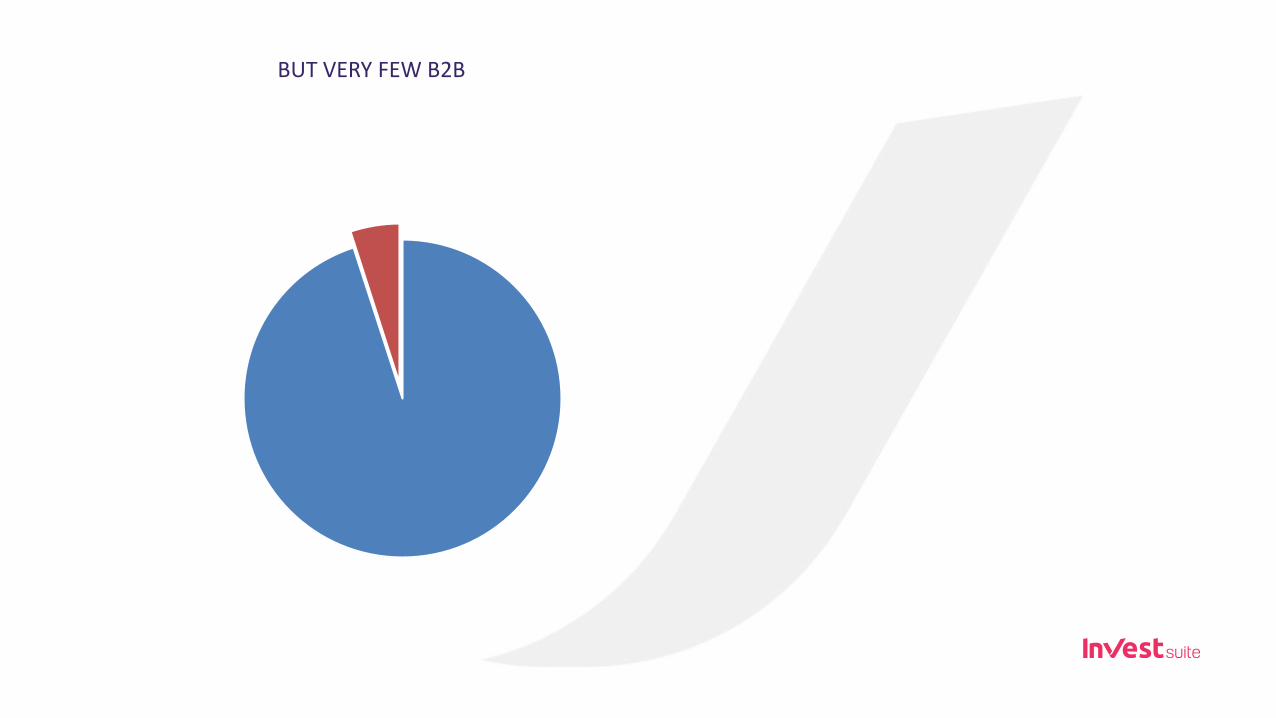

BUT VERY FEW B2B

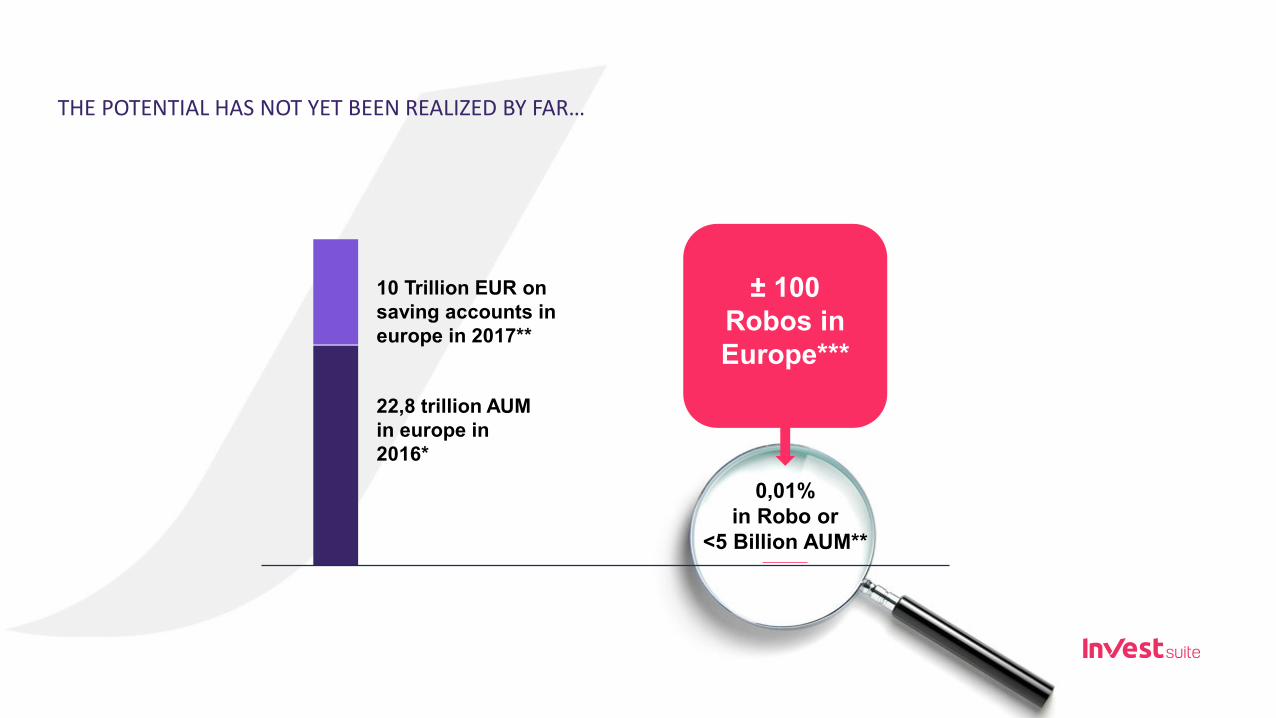

THE POTENTIAL HAS NOT YET BEEN REALIZED BY FAR…

± 100 Robos in Europe***

22,8 trillion AUM in europe in 2016*

0,01%in Robo or

<5 Billion AUM**

10 Trillion EUR on saving accounts in europe in 2017**

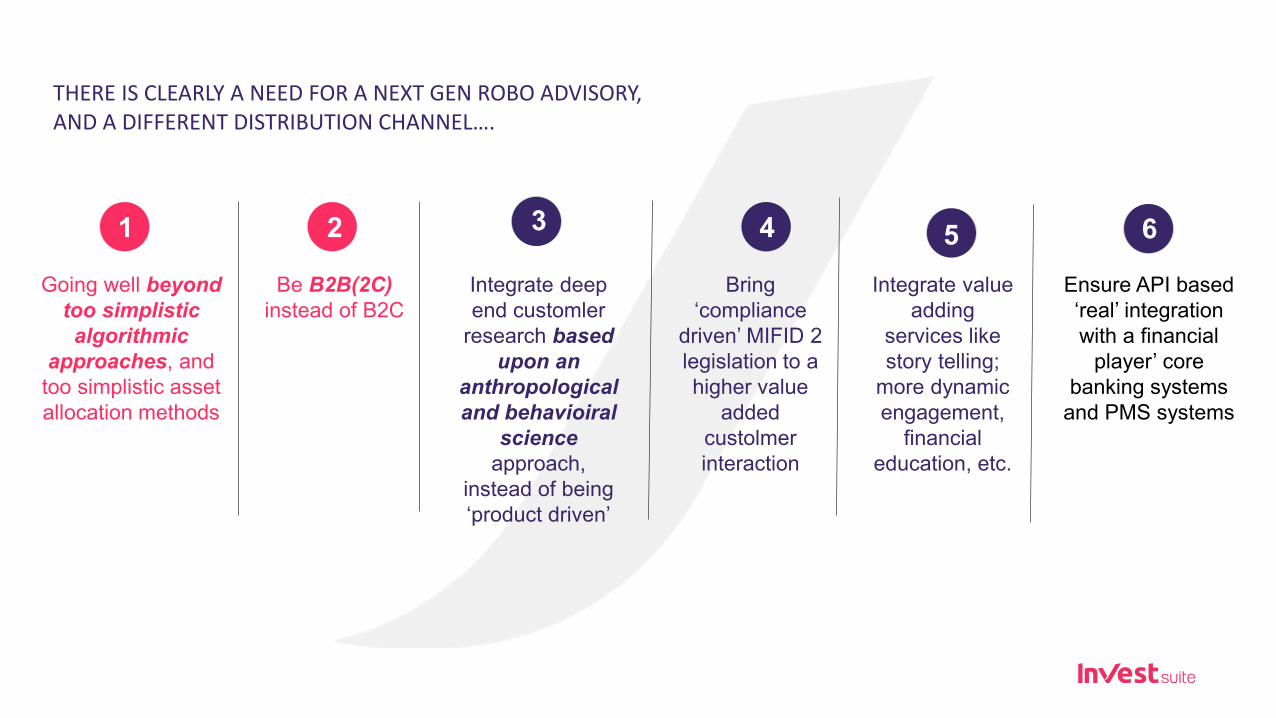

THERE IS CLEARLY A NEED FOR A NEXT GEN ROBO ADVISORY, AND A DIFFERENT DISTRIBUTION CHANNEL….

Going well beyond too simplistic algorithmic

approaches, and too simplistic asset allocation methods

Be B2B(2C) instead of B2C

Ensure API based ‘real’ integration with a financial

player’ core banking systems

and PMS systems

Bring ‘compliance

driven’ MIFID 2 legislation to a higher value

added custolmer interaction

4 6

Integrate deep end customler

research based upon an

anthropological and behavioiral

science approach,

instead of being ‘product driven’

3

Integrate value adding

services like story telling;

more dynamic engagement,

financial education, etc.

51 2

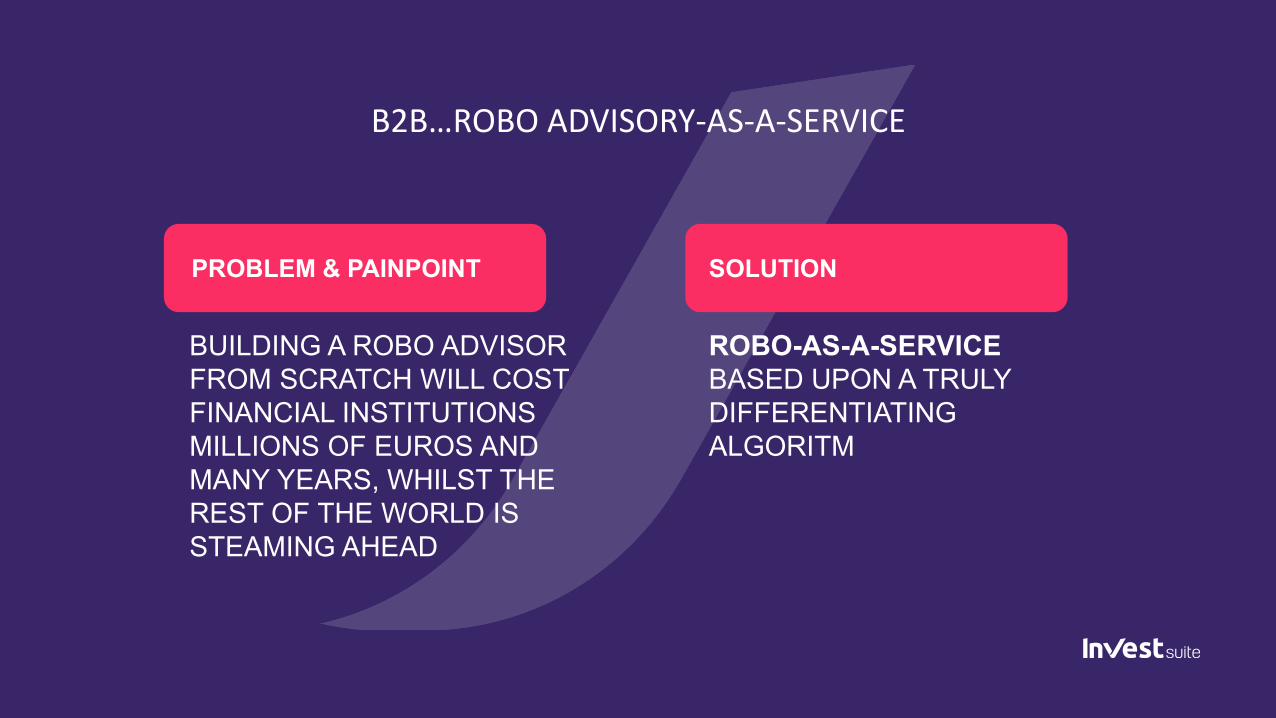

B2B…ROBO ADVISORY-AS-A-SERVICE

BUILDING A ROBO ADVISOR FROM SCRATCH WILL COST FINANCIAL INSTITUTIONS MILLIONS OF EUROS AND MANY YEARS, WHILST THE REST OF THE WORLD IS STEAMING AHEAD

PROBLEM & PAINPOINT SOLUTION

ROBO-AS-A-SERVICE BASED UPON A TRULY DIFFERENTIATING ALGORITM

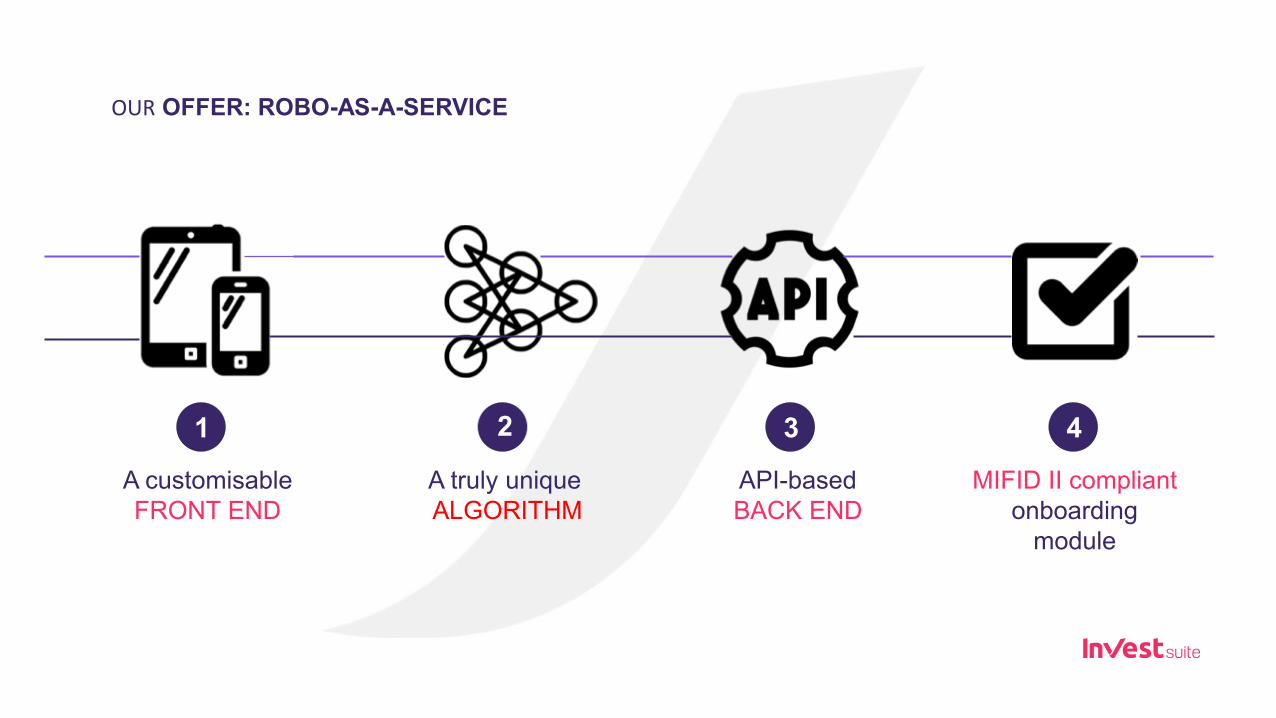

OUR OFFER: ROBO-AS-A-SERVICE

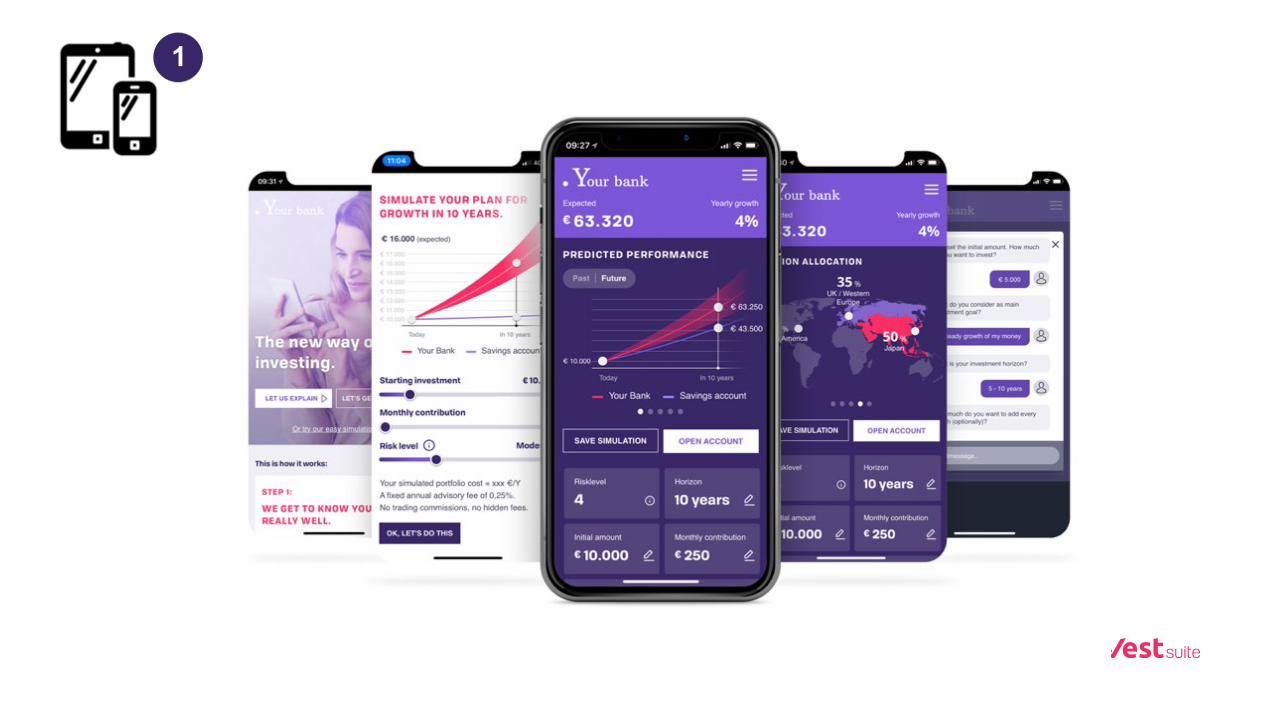

A customisable FRONT END

A truly uniqueALGORITHM

MIFID II compliantonboarding

module

API-based BACK END

1 2 3 4

1

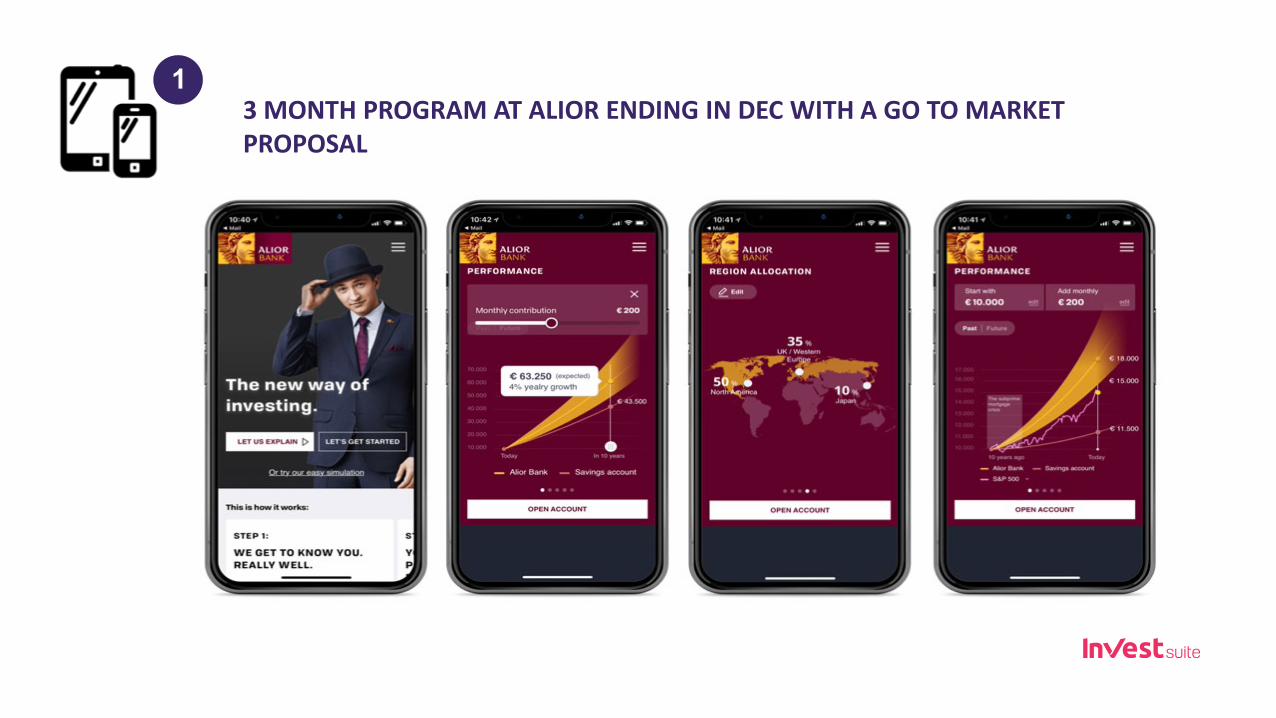

13 MONTH PROGRAM AT ALIOR ENDING IN DEC WITH A GO TO MARKET PROPOSAL

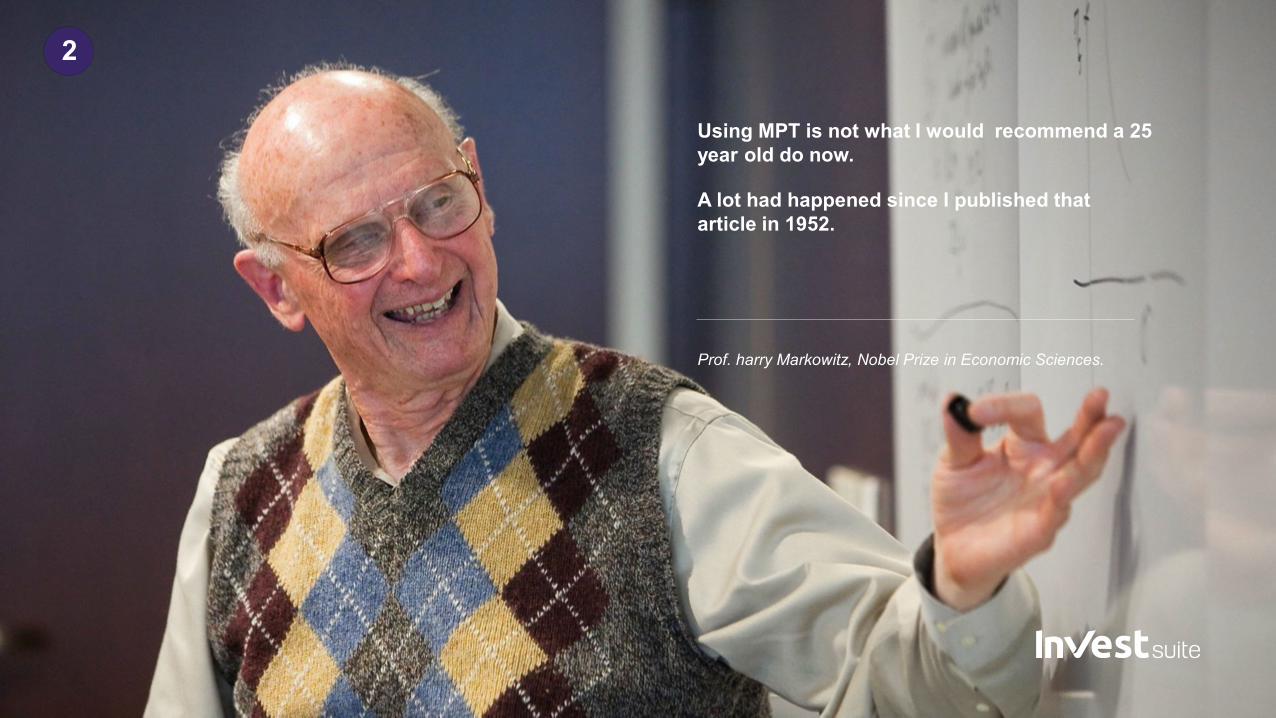

Using MPT is not what I would recommend a 25 year old do now.

A lot had happened since I published that article in 1952.

Prof. harry Markowitz, Nobel Prize in Economic Sciences.

2

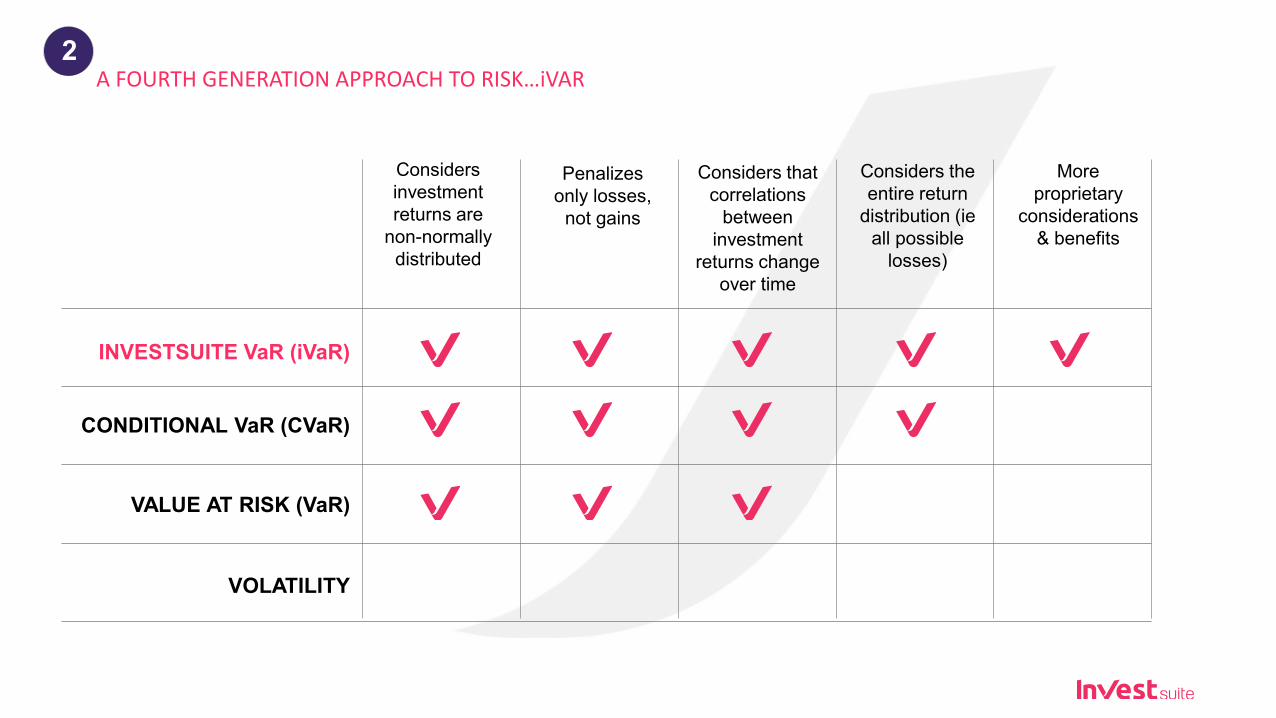

A FOURTH GENERATION APPROACH TO RISK…iVAR

VOLATILITY

VALUE AT RISK (VaR)

CONDITIONAL VaR (CVaR)

INVESTSUITE VaR (iVaR)

Considers investment returns are

non-normally distributed

Penalizes only losses,

not gains

Considers that correlations

between investment

returns change over time

Considers the entire return

distribution (ie all possible

losses)

More proprietary

considerations & benefits

2

2

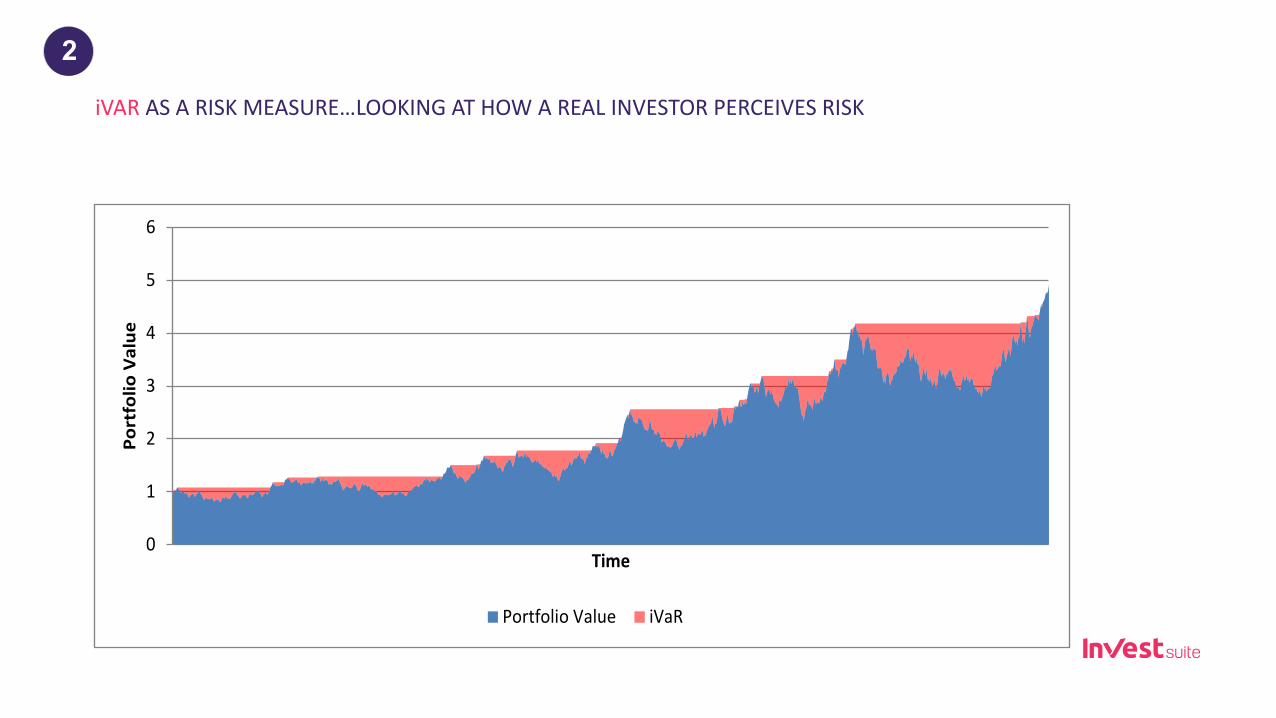

iVAR AS A RISK MEASURE…LOOKING AT HOW A REAL INVESTOR PERCEIVES RISK

0

1

2

3

4

5

6

Port

folio

Val

ue

Time

Portfolio Value iVaR

2

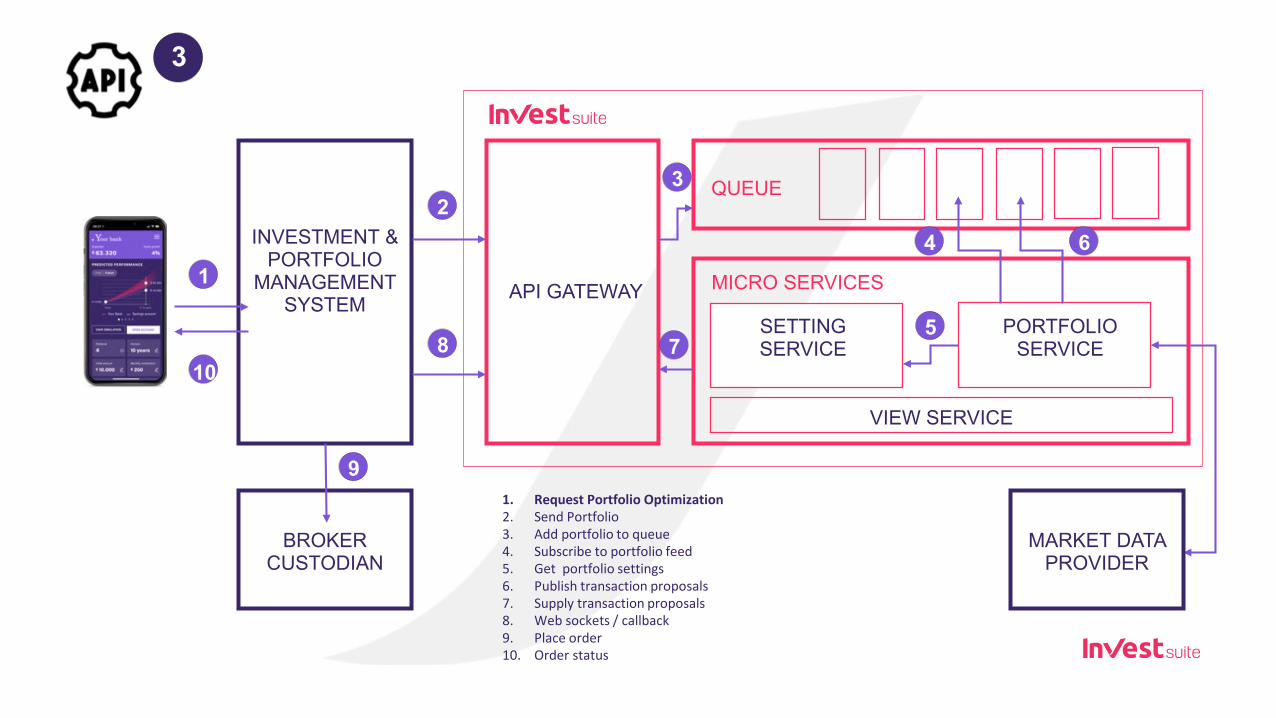

INVESTMENT & PORTFOLIO

MANAGEMENT SYSTEM API GATEWAY

QUEUE

SETTING SERVICE

PORTFOLIO SERVICE

VIEW SERVICE

MICRO SERVICES

BROKER CUSTODIAN

MARKET DATA PROVIDER

1. Request Portfolio Optimization2. Send Portfolio3. Add portfolio to queue4. Subscribe to portfolio feed5. Get portfolio settings6. Publish transaction proposals7. Supply transaction proposals8. Web sockets / callback9. Place order10. Order status

1

2

8

3

4 6

57

9

3

10

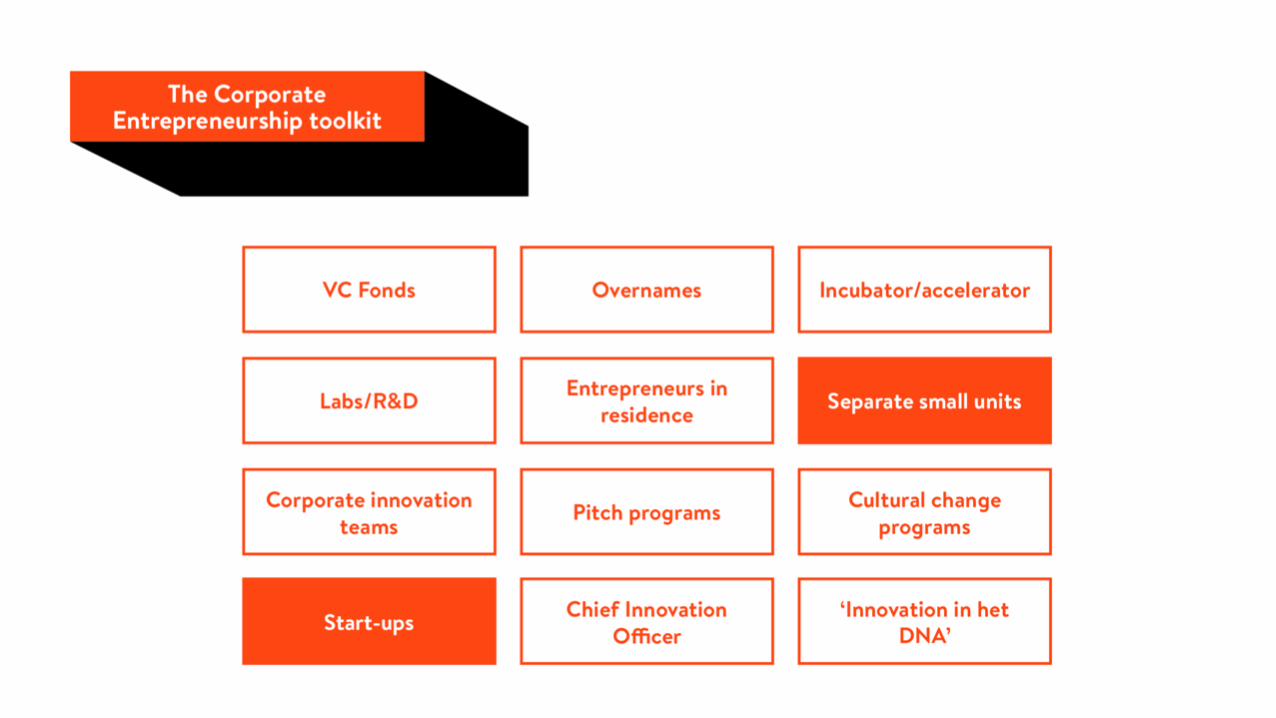

A FEW REFLECTIONS ON CORPORATE ENTREPRENEURSHIPS & STARTUPS

EVERYBODY WANTS TO BE VERY BIG AND IMPORTANT

± 100 Robos in Europe***

1. The average entrepreneur is 40 years old

2. More than 80% of new business started by people older than 35

3. There are more entrepreneurs over 55 starting business than under 35

4. Chances of survival increase with age

FinTech & InsurTech: Cooperation or competition with the large financial institutions?

Gambit Financial SolutionsA teenager FinTech’s experience

Georges HübnerProfessor of Finance, HEC Liège, Liège University

Founder, Gambit Financial SolutionsBelgian Finance ClubBrussels, 5/11/2018

64

What does Gambit do?

65

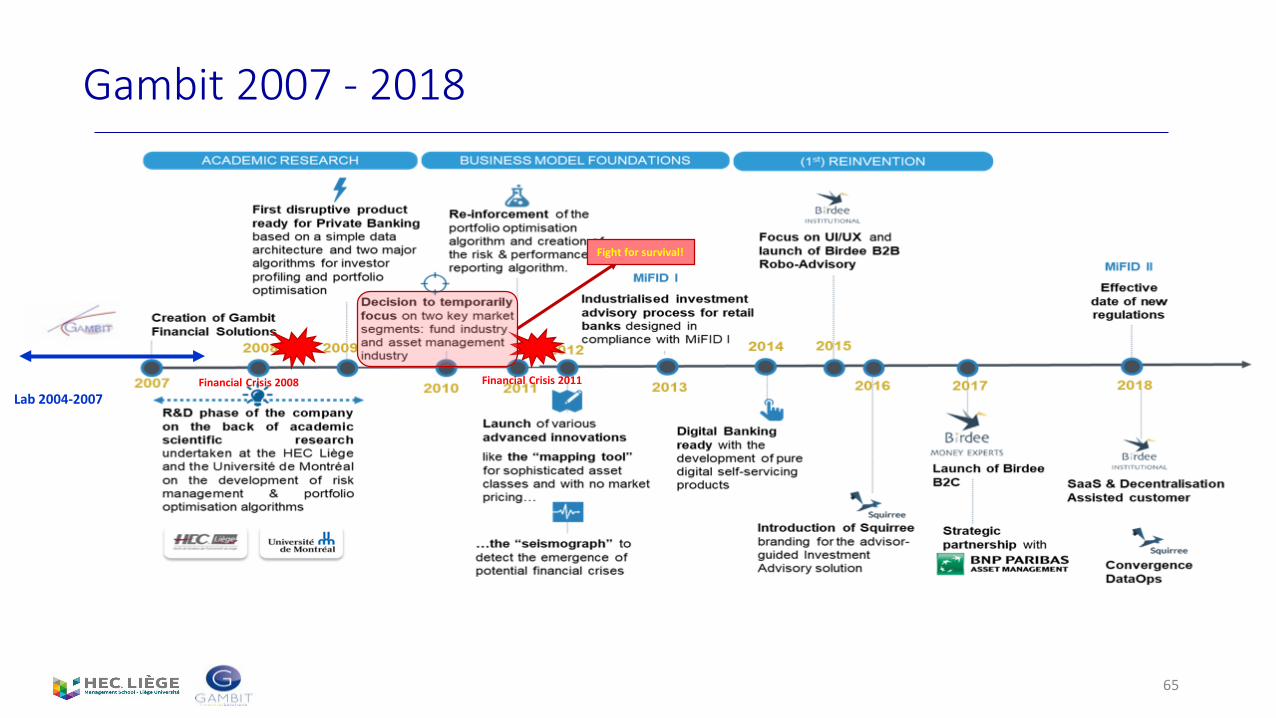

Gambit 2007 - 2018

Lab 2004-2007Financial Crisis 2008 Financial Crisis 2011

Fight for survival!

66

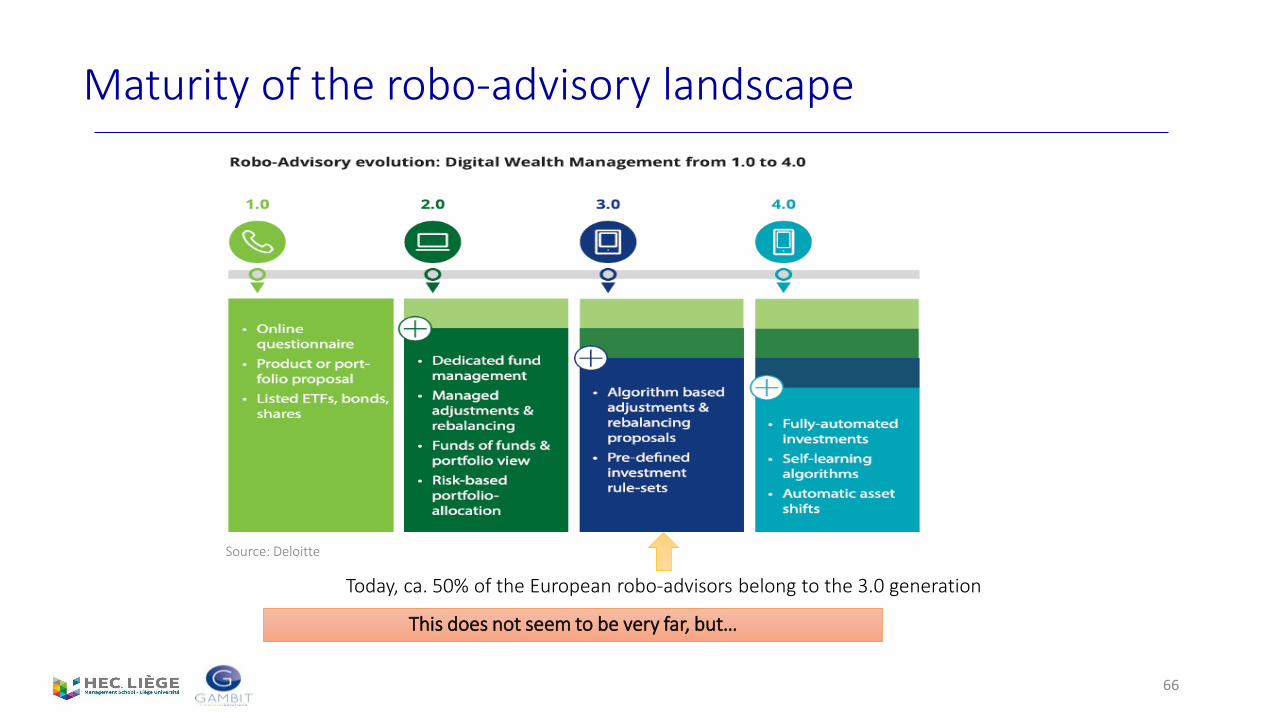

Maturity of the robo-advisory landscape

Source: Deloitte

Today, ca. 50% of the European robo-advisors belong to the 3.0 generation

This does not seem to be very far, but…

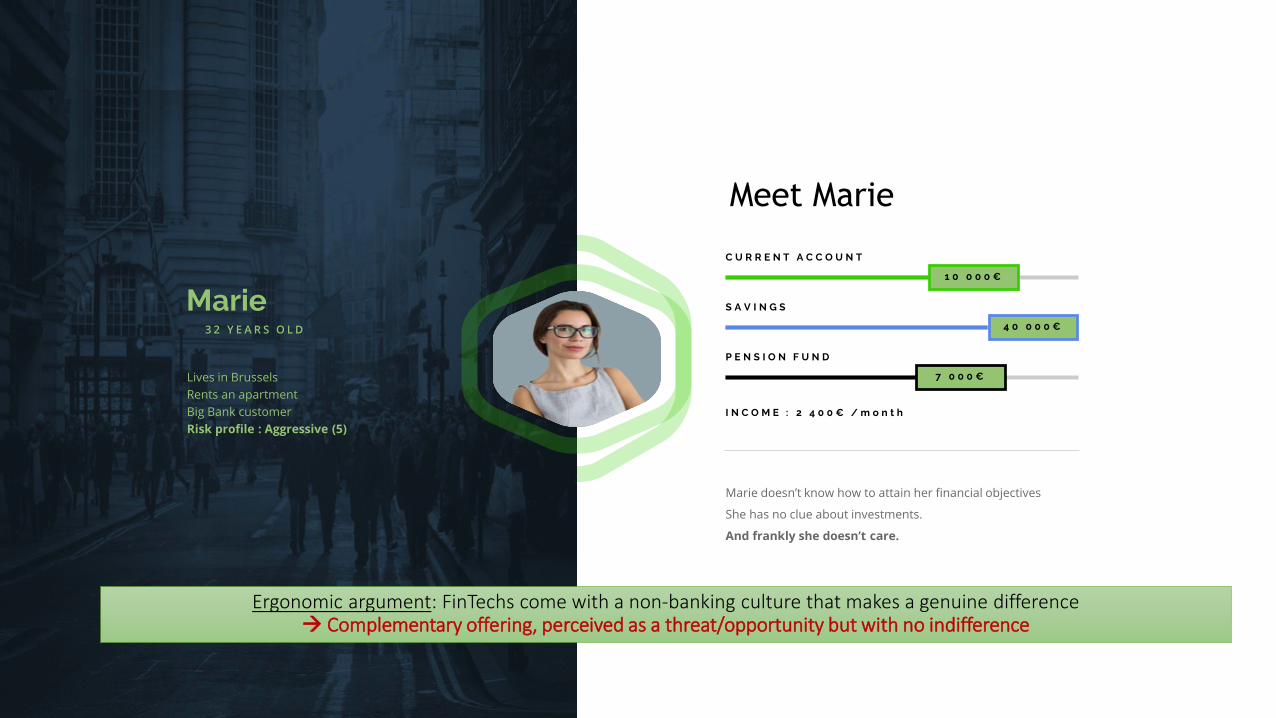

Marie3 2 Y E A R S O L D

P E N S I O N F U N D

7 0 0 0 €

I N C O M E : 2 4 0 0 € / m o n t h

S A V I N G S

4 0 0 0 0 €

C U R R E N T A C C O U N T

1 0 0 0 0 €

Lives in BrusselsRents an apartmentBig Bank customerRisk profile : Aggressive (5)

Meet Marie

Ergonomic argument: FinTechs come with a non-banking culture that makes a genuine difference Complementary offering, perceived as a threat/opportunity but with no indifference

68

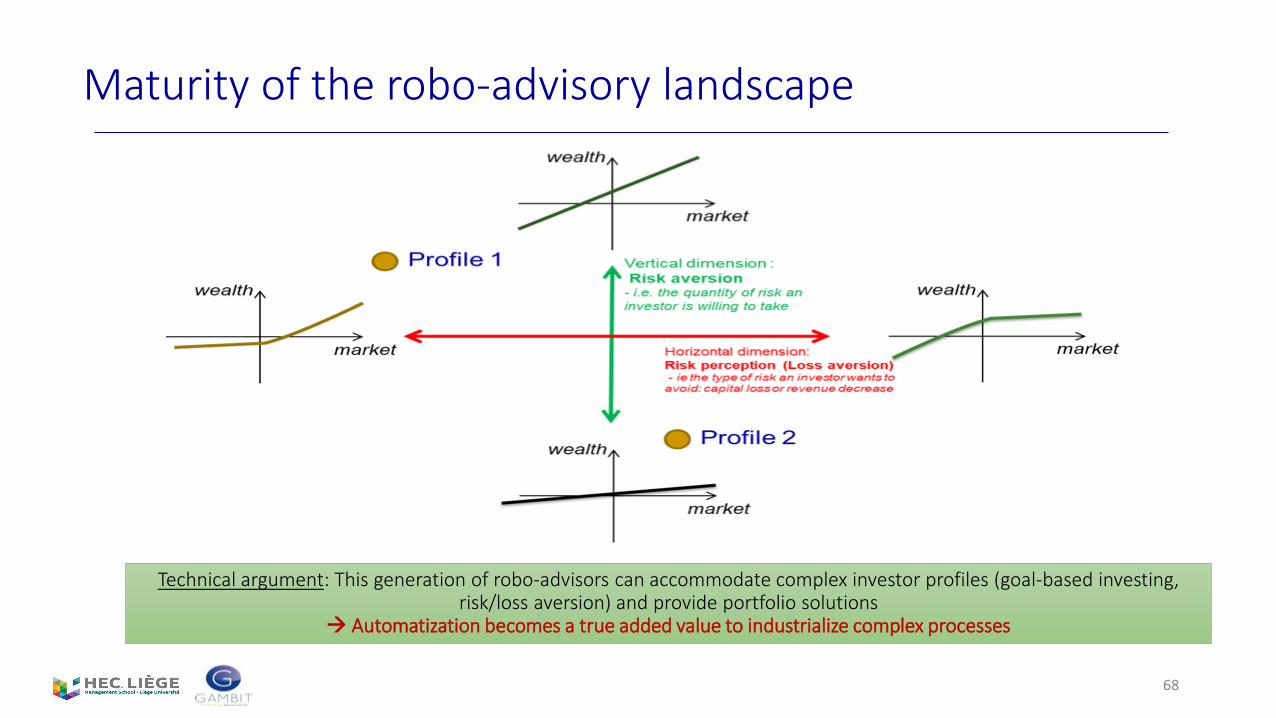

Maturity of the robo-advisory landscape

Technical argument: This generation of robo-advisors can accommodate complex investor profiles (goal-based investing, risk/loss aversion) and provide portfolio solutions

Automatization becomes a true added value to industrialize complex processes

69

Gambit’s answer to today’s question

http://www.bankingtech.com/978992/gambit-acquisition-offers-bnp-paribas-robo-advisory-opening/https://www.finextra.com/newsarticle/31041/bnp-paribas-buys-majority-stake-in-robo-advisor-gambithttp://www.mondovisione.com/media-and-resources/news/bnp-paribas-asset-management-acquires-a-majority-stake-in-gambit-financial-solut/https://www.thetradenews.com/Technology/BNP-Paribas-Asset-Management-acquires-stake-in-robo-advisor/http://www.privatebankerinternational.com/news/robo-advice-gambit-bnp-paribas-belgian-fintech/http://www.international-adviser.com/news/1037946/bnp-paribas-buys-majority-stake-belgian-robo-adviserhttps://www.fundstrategy.co.uk/bnp-paribas-acquires-majority-stake-robo-adviser/http://www.automatedtrader.net/news/at/158025/bnp-paribas-acquires-majority-stake-in-gambit-financial-solutionshttps://www.lesechos.fr/finance-marches/gestion-actifs/010219199760-bnp-paribas-am-fait-lacquisition-du-robo-advisor-gambit-2112506.phphttps://www.investmentweek.co.uk/investment-week/news/3016863/bnp-paribas-am-acquires-majority-stake-in-robo-adviserhttps://www.zonebourse.com/BNP-PARIBAS-4618/actualite/BNP-Paribas-prise-de-participation-majoritaire-dans-Gambit-25076643/http://www.roboadvicenews.com/1045_bnp-paribas-asset-management-snaps-up-stake-in-robo-advice-firmhttp://citywireselector.com/news/bnp-paribas-am-acquires-stake-in-fintech-firm/a1047225https://www.boursedirect.fr/fr/actualites/categorie/actualites-financieres/bnp-paribas-am-prend-le-controle-de-la-fintech-gambit-aof-480983c57e617dd107b7cfc8dc19040fde69e4f8http://bourse.lefigaro.fr/fonds-trackers/actu-conseils/bnp-paribas-am-prend-le-controle-de-la-fintech-gambit-6182880

http://votreargent.lexpress.fr/bourse-de-paris/bnp-paribas-prise-de-participation-majoritaire-dans-gambit_1941358.htmlhttp://www.corporatenews.lu/fr/archives-shortcut/archives/article/2017/09/bnp-paribas-asset-management-prend-une-participation-majoritaire-dans-gambit-financial-solutions-fournisseur-europeen-de-premier-plan-de-solutions-digitales-de-conseil-en-investissementhttps://fr.finance.yahoo.com/quote/BNP.PA/http://www.belga.be/fr/press-release/details-64161/?langpr=FRhttp://www.investmenteurope.net/regions/france/bnp-acquires-robo-advisory-investment-solutions-provider/http://citywire.it/news/robo-advisory-bnp-paribas-am-acquisisce-la-maggioranza-di-gambit-financial-solutions/a1047218?ref=international_Italy_latest_news_listhttp://www.tijd.be/ondernemen/financiele-diensten-verzekeringen/BNP-Paribas-slokt-Belgische-fintechspeler-op/9930091?ckc=1&ts=1504845907https://www.financialinvestigator.nl/nieuws/20170907-bnpp-am-neemt-meerderheidsbelang-in-gambit-financial-solutionshttps://fr.investing.com/news/actualit%C3%A9s-bourse/bnp-paribas-prise-de-participation-majoritaire-dans-gambit-508041http://www.combourse.com/Societe/BNP_Paribas_prise_de_participation_majoritaire_dans_Gambit__BNP_PARIBAS__FR0000131104__2219796.htmlhttp://www.financialstandard.com.au/news/bnp-paribas-am-acquires-fintech-103276734https://www.fintastico.com/fintech-news/http://es.fundspeople.com/news/bnp-paribas-am-adquiere-una-adquisicion-mayoritaria-en-el-roboasesor-gambithttps://www.fnlondon.com/articles/bnp-paribas-buys-a-robo-adviser-20170907http://www.cbanque.com/actu/rss/les-echos-finances/713801-bnp-paribas-am-fait-acquisition-du-robo-advisor-gambithttp://www.finanzen.nl/aandelen/nieuws/BNP-Paribas-slokt-Belgische-fintechspeler-op-5678622

70

9

>1 000 000

€ 50

>100

2010

4Robo-advice & Portfolio Mgmt

Investment AdvisoryRisk Management

GAMBITSpecialized in Digital Investment

Solutions

© 2018 Gambit | All rights reserved

CM Arkea

Formerly: Delta Lloyd Bank

CMNE

Trusted by:

New in 2019: Singapore

€ 10Mio (+250%

71

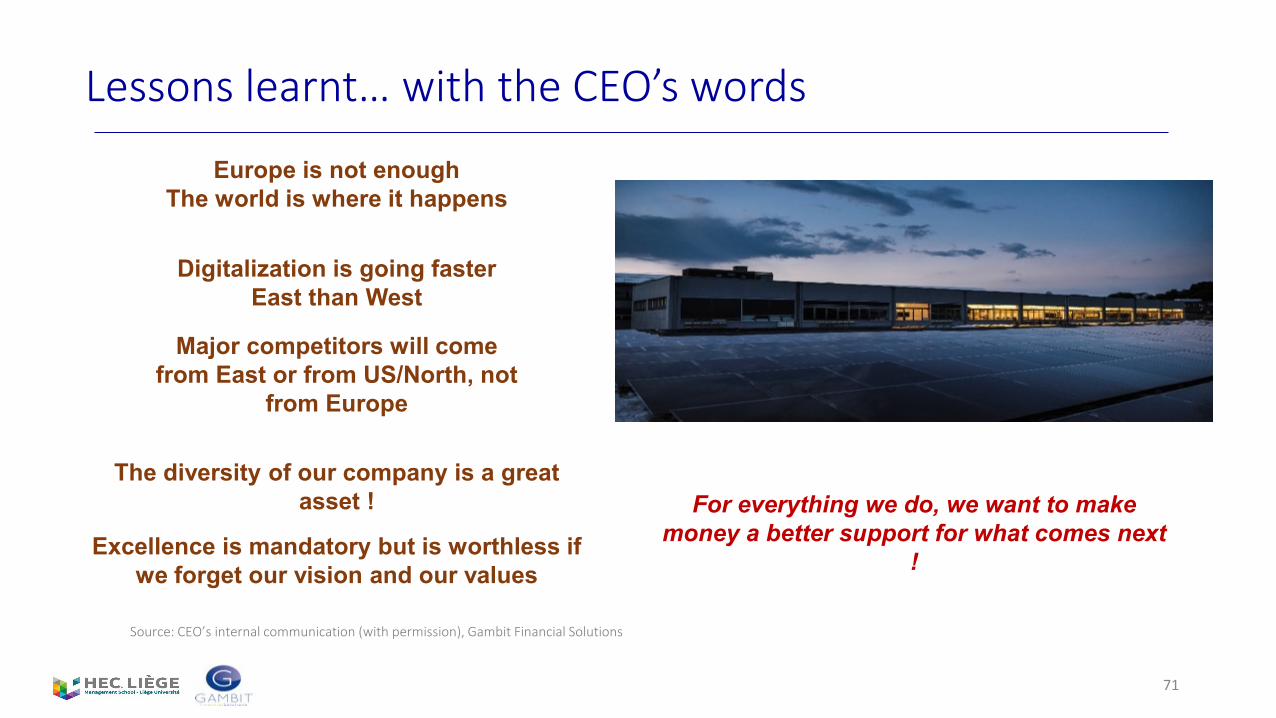

Lessons learnt… with the CEO’s words

Europe is not enoughThe world is where it happens

Digitalization is going faster East than West

The diversity of our company is a great asset !

Major competitors will come from East or from US/North, not

from Europe

Excellence is mandatory but is worthless if we forget our vision and our values

For everything we do, we want to make money a better support for what comes next

!

Source: CEO’s internal communication (with permission), Gambit Financial Solutions

Monizze“The innovative multi-wallet payment solutions in the e-voucher space”

Jean-Louis Van HouweBrussels 5/11/2018

Belgian Finance Club Conference“FinTech & InsurTech : cooperation or competition

with the large financial institutions ”

Who we are – what we do

What is our ecosystem

Why and How do we collaborate with the banks

The next steps and conclusions

Q&A

Topic

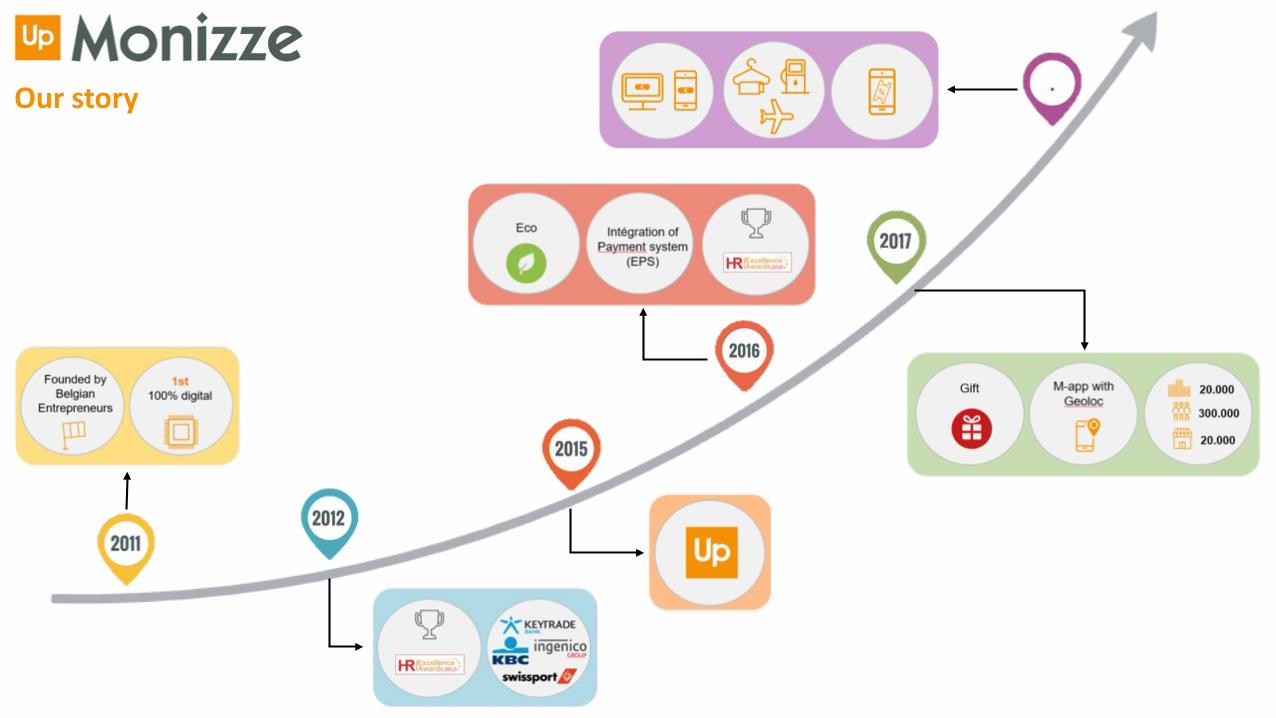

Our story

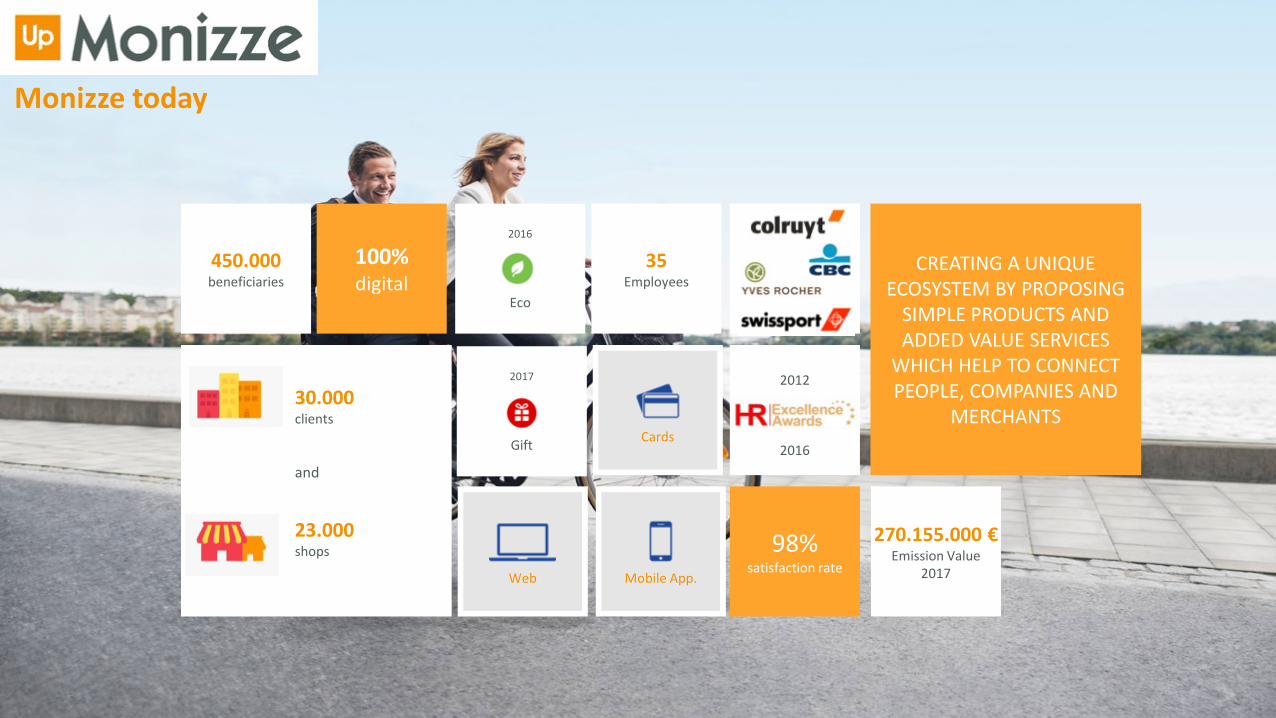

450.000beneficiaries

35Employees

98%satisfaction rate

CREATING A UNIQUE ECOSYSTEM BY PROPOSING

SIMPLE PRODUCTS AND ADDED VALUE SERVICES

WHICH HELP TO CONNECT PEOPLE, COMPANIES AND

MERCHANTS

2012

2016

30.000clients

and

23.000shops

270.155.000 €Emission Value

2017Web Mobile App.

Cards

100%digital

2016

Eco

2017

Gift

Monizze today

Userexperience

Impression

Transport

NotificationE-mailSMS

Windowsticker On field

Affiliate search

Online order, delivery, …

On field On field

Cash system Various

tools: promotion, loyalty, …

CRT/UP Coupons

Up

Issuance

Valu

e

Deliv

ery

Transaction

Acce

ptan

ce/

paym

ent

Auth

oriza

-tio

n

Post-Transaction

Regu

latio

n

Inte

ract

ion

Pre-transaction

Rese

arch

Sele

ctio

nIntermediary

UP/ Intermediary

The Integrated Digital Offer – Our eco system

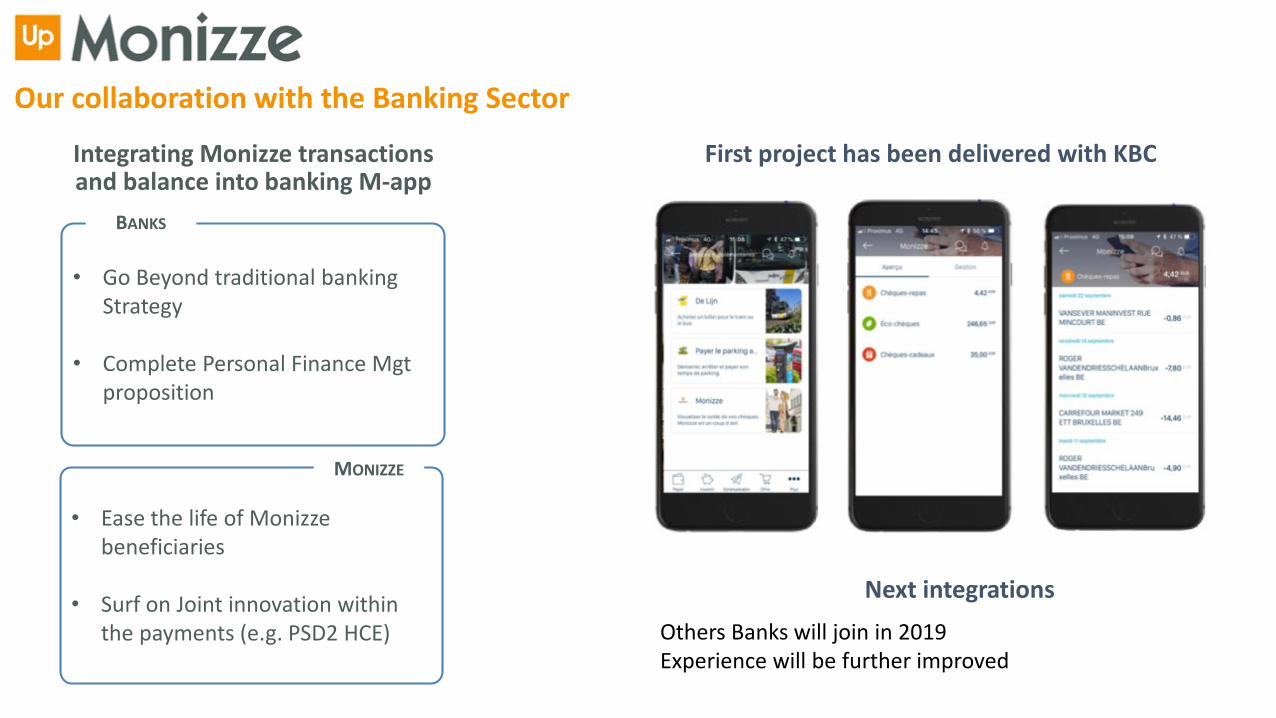

Integrating Monizze transactions and balance into banking M-app

• Go Beyond traditional banking Strategy

• Complete Personal Finance Mgtproposition

• Ease the life of Monizze beneficiaries

• Surf on Joint innovation within the payments (e.g. PSD2 HCE)

BANKS

MONIZZE

First project has been delivered with KBC

Next integrationsOthers Banks will join in 2019Experience will be further improved

Our collaboration with the Banking Sector

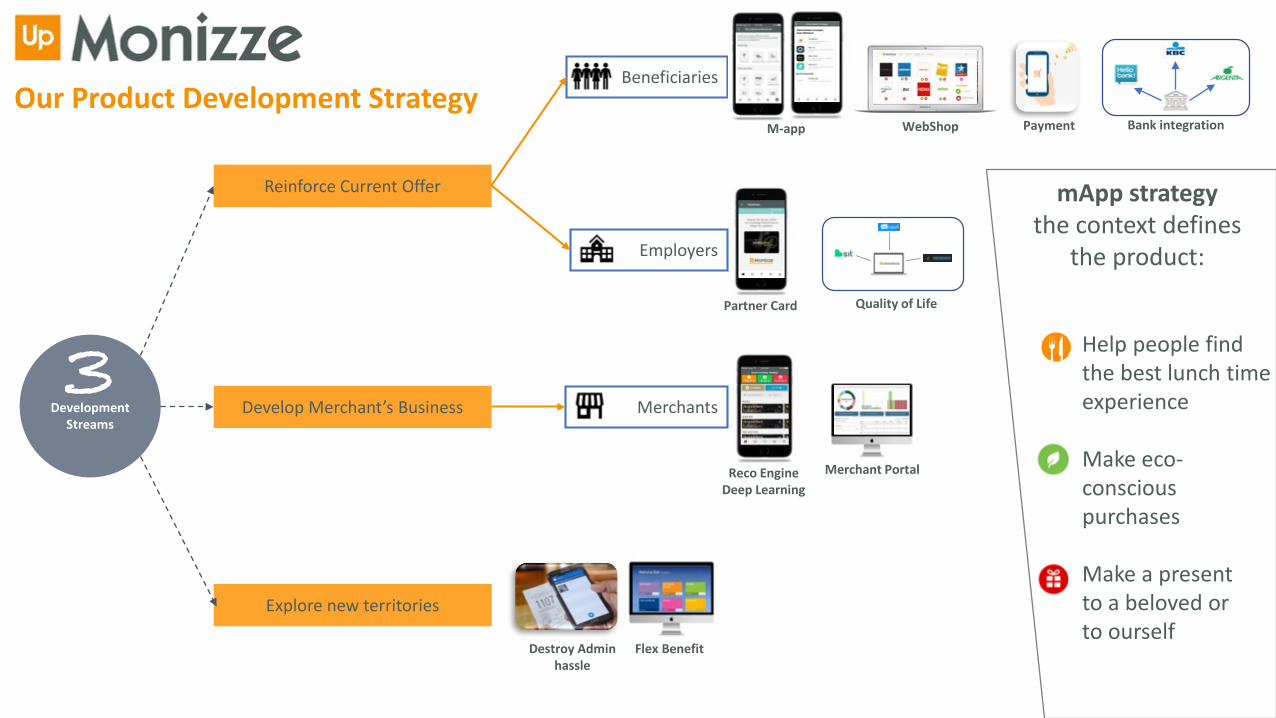

Development Streams

Reinforce Current Offer

Develop Merchant’s Business

Explore new territories

Beneficiaries

Employers

3Merchants

Merchant Portal

M-app WebShop

Reco EngineDeep Learning

Quality of LifePartner Card

Payment Bank integration

Destroy Adminhassle

Flex Benefit

Help people find the best lunch time experience

Make eco-conscious purchases

Make a presentto a beloved orto ourself

Our Product Development Strategy

mApp strategythe context defines

the product:

Jean-Louis Van HouweMonizze – Founder & CEOFintech Belgium – Chairman of the Board+32 498 44 57 [email protected]

Thank you for your attention!

B-Hive EuropeFinTech & InsurTech: cooperation or competition with the large financial institutions

Fabian VandenreydtExecutive Chairman

Belgian Finance Club5 November 2018

Compete vs. Collaborate ?

Compete or Collaborate... On What? (i)

84

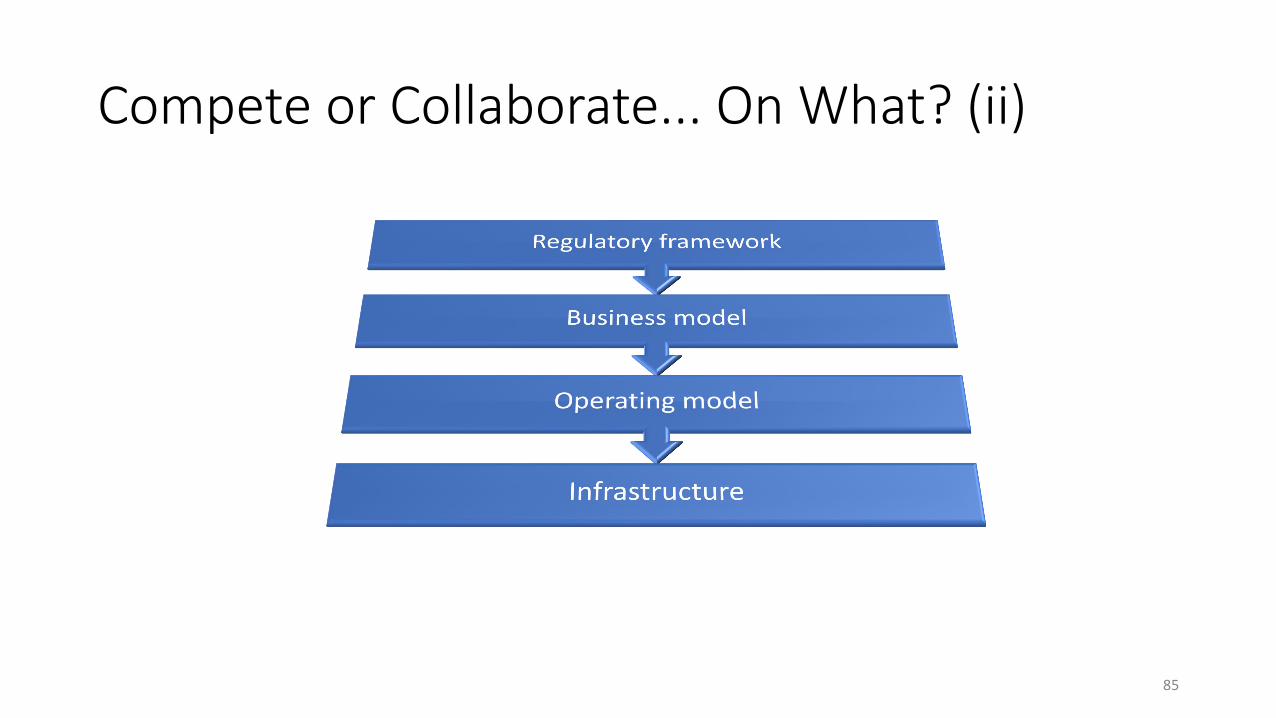

Compete or Collaborate... On What? (ii)

85

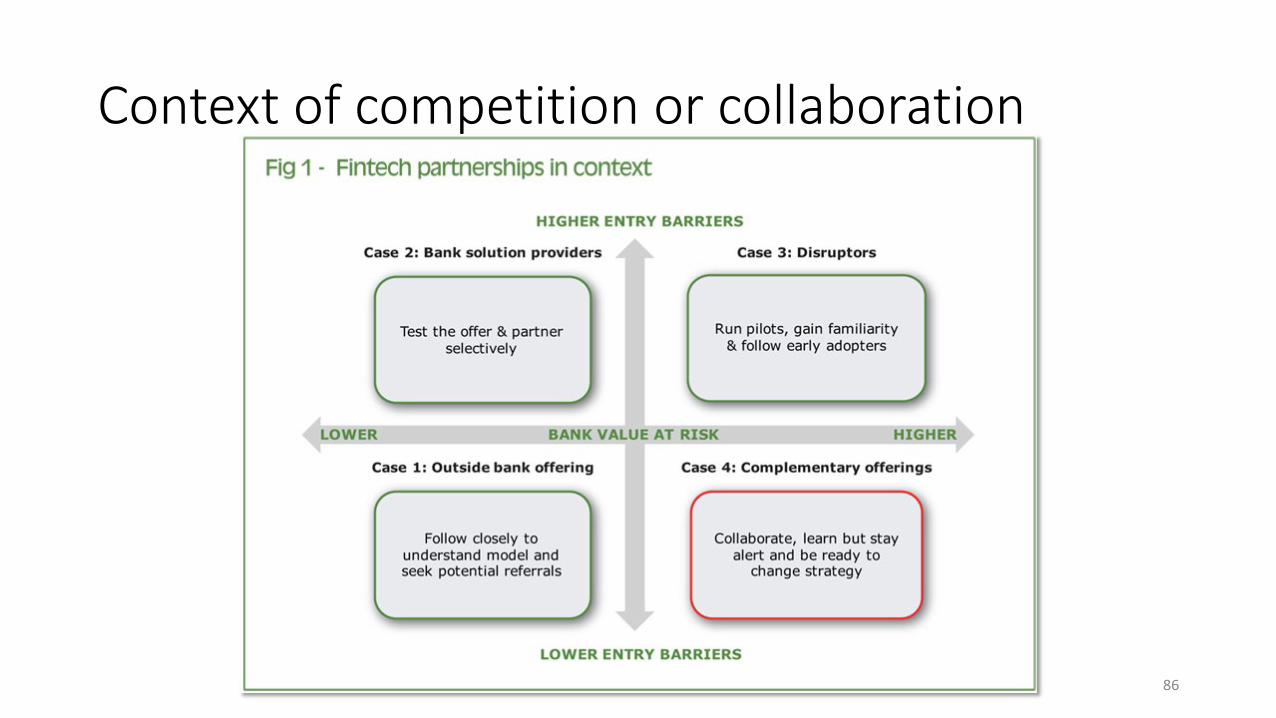

Context of competition or collaboration

86

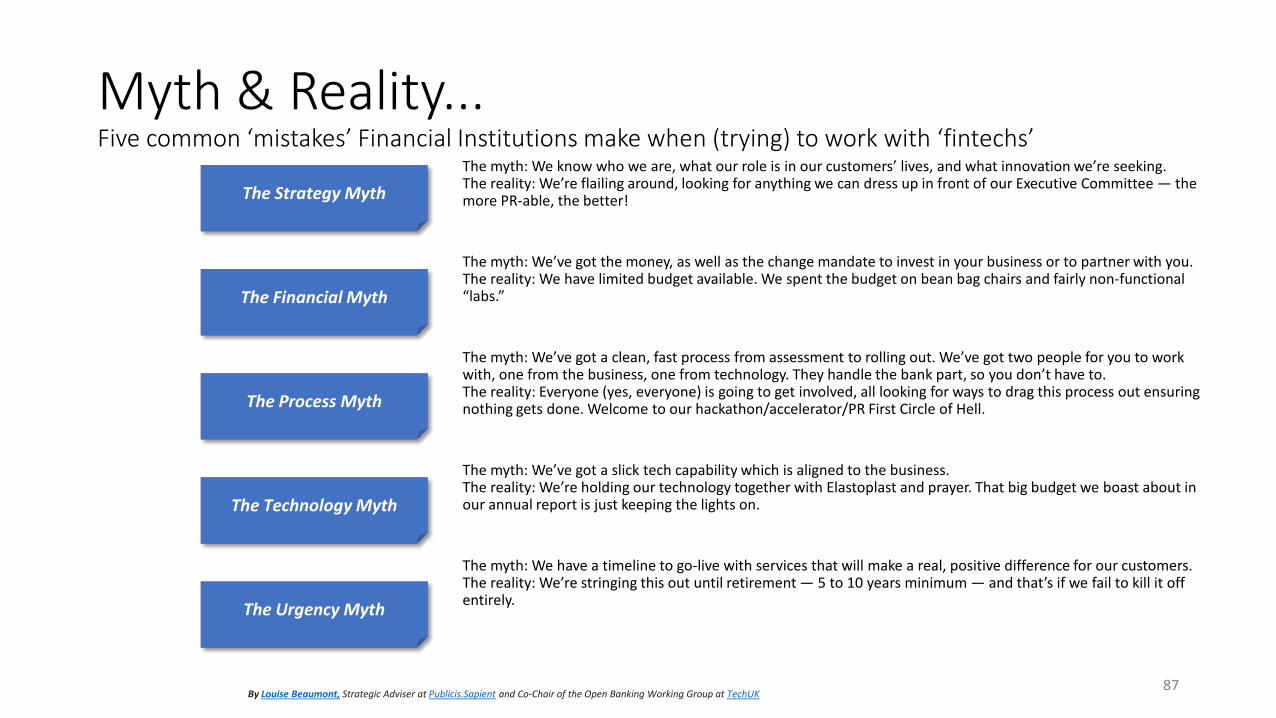

Myth & Reality...Five common ‘mistakes’ Financial Institutions make when (trying) to work with ‘fintechs’

The myth: We know who we are, what our role is in our customers’ lives, and what innovation we’re seeking.The reality: We’re flailing around, looking for anything we can dress up in front of our Executive Committee — the more PR-able, the better!

The myth: We’ve got the money, as well as the change mandate to invest in your business or to partner with you.The reality: We have limited budget available. We spent the budget on bean bag chairs and fairly non-functional “labs.”

The myth: We’ve got a clean, fast process from assessment to rolling out. We’ve got two people for you to work with, one from the business, one from technology. They handle the bank part, so you don’t have to.The reality: Everyone (yes, everyone) is going to get involved, all looking for ways to drag this process out ensuring nothing gets done. Welcome to our hackathon/accelerator/PR First Circle of Hell.

The myth: We’ve got a slick tech capability which is aligned to the business.The reality: We’re holding our technology together with Elastoplast and prayer. That big budget we boast about in our annual report is just keeping the lights on.

The myth: We have a timeline to go-live with services that will make a real, positive difference for our customers.The reality: We’re stringing this out until retirement — 5 to 10 years minimum — and that’s if we fail to kill it off entirely.

87By Louise Beaumont, Strategic Adviser at Publicis.Sapient and Co-Chair of the Open Banking Working Group at TechUK

The Strategy Myth

The Financial Myth

The Process Myth

The Technology Myth

The Urgency Myth

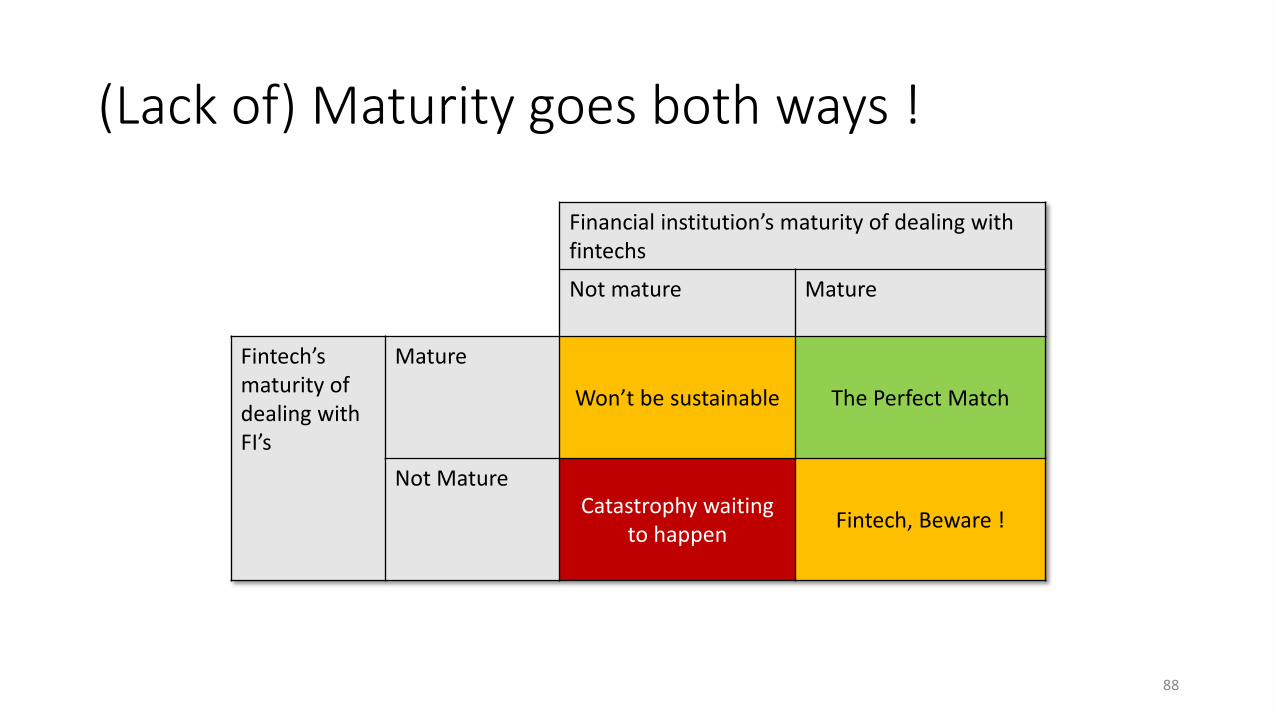

(Lack of) Maturity goes both ways !

Financial institution’s maturity of dealing with fintechs

Not mature Mature

Fintech’s maturity of dealing with FI’s

Mature

Won’t be sustainable The Perfect Match

Not MatureCatastrophy waiting

to happen Fintech, Beware !

88

Who We Are & What We Do

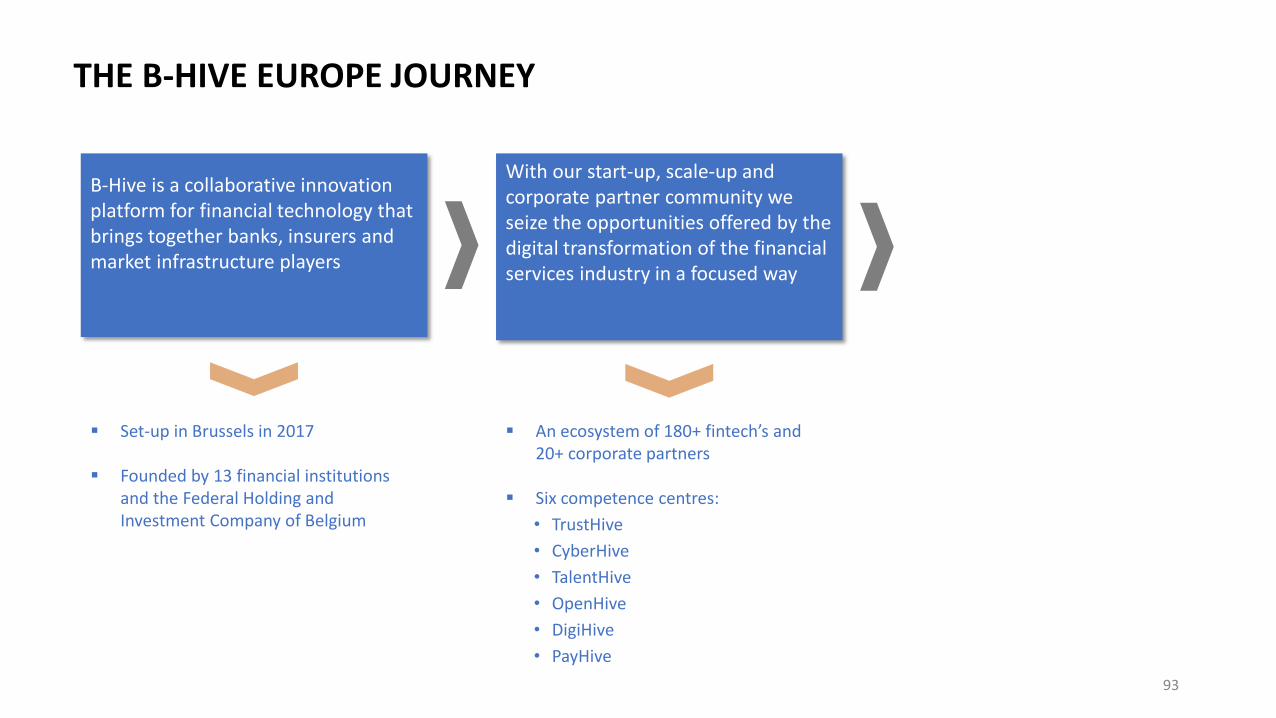

B-Hive Europe is a collaborative innovation platform for financial technology that brings together banks, insurers and market infrastructure players

Set-up in Brussels in 2017

Founded by 13 financial institutions and the Federal Holding and Investment Company of Belgium

THE B-HIVE EUROPE JOURNEY

90

CURRENT B-HIVE SHAREHOLDERS

91

B-Hive MembersSept 2018

LendingAsset Management Insurance Cybersecurity/ID management

Banking Platforms

Business Solutions

Full list on b-hive.eu/membersRisk ManagementPaymentsBlockchain

E-Invoicing / Accounting

Analytics/Data Management

Consulting

92

B-Hive is a collaborative innovation platform for financial technology that brings together banks, insurers and market infrastructure players

Set-up in Brussels in 2017

Founded by 13 financial institutions and the Federal Holding and Investment Company of Belgium

With our start-up, scale-up and corporate partner community we seize the opportunities offered by the digital transformation of the financial services industry in a focused way

An ecosystem of 180+ fintech’s and 20+ corporate partners

Six competence centres:• TrustHive• CyberHive• TalentHive• OpenHive• DigiHive• PayHive

THE B-HIVE EUROPE JOURNEY

93

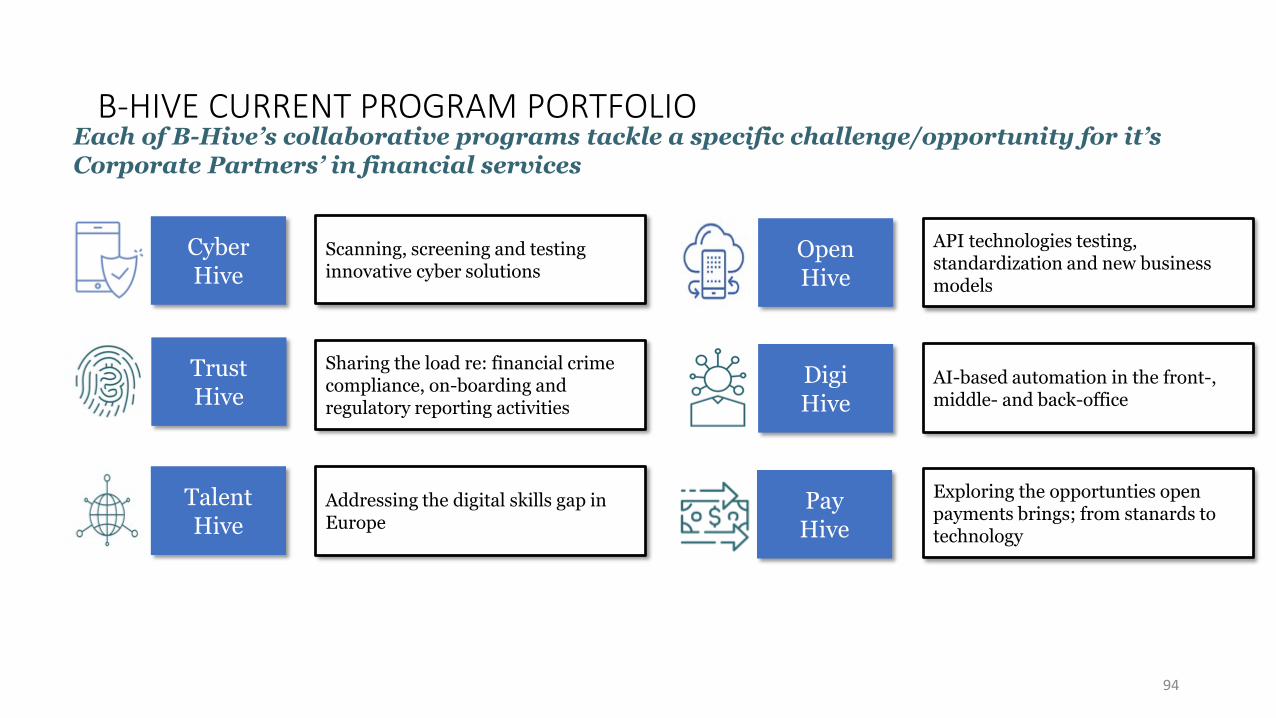

B-HIVE CURRENT PROGRAM PORTFOLIO

94

Each of B-Hive’s collaborative programs tackle a specific challenge/opportunity for it’s Corporate Partners’ in financial services

Cyber Hive

TrustHive

DigiHive

OpenHive

TalentHive

Scanning, screening and testinginnovative cyber solutions

Sharing the load re: financial crime compliance, on-boarding andregulatory reporting activities

Addressing the digital skills gap in Europe

API technologies testing, standardization and new business models

AI-based automation in the front-, middle- and back-office

PayHive

Exploring the opportunties open payments brings; from stanards to technology

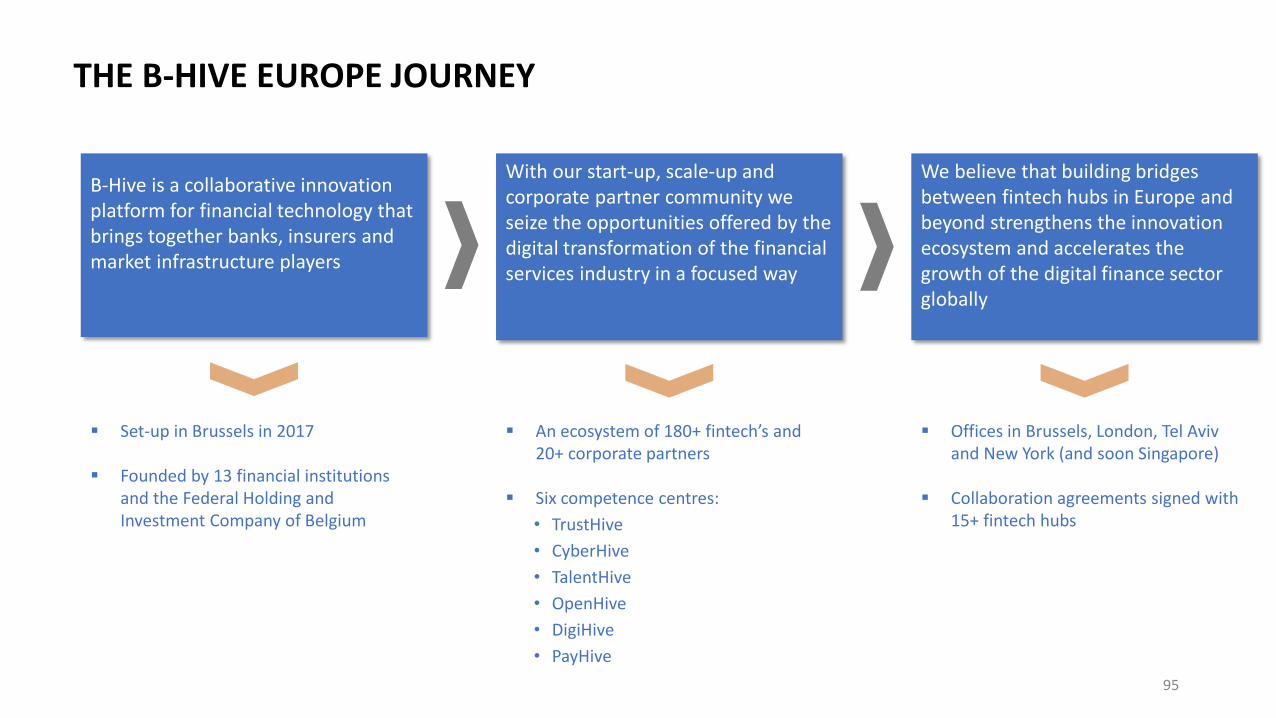

B-Hive is a collaborative innovation platform for financial technology that brings together banks, insurers and market infrastructure players

Set-up in Brussels in 2017

Founded by 13 financial institutions and the Federal Holding and Investment Company of Belgium

With our start-up, scale-up and corporate partner community we seize the opportunities offered by the digital transformation of the financial services industry in a focused way

An ecosystem of 180+ fintech’s and 20+ corporate partners

Six competence centres:• TrustHive• CyberHive• TalentHive• OpenHive• DigiHive• PayHive

We believe that building bridges between fintech hubs in Europe and beyond strengthens the innovation ecosystem and accelerates the growth of the digital finance sector globally

Offices in Brussels, London, Tel Aviv and New York (and soon Singapore)

Collaboration agreements signed with 15+ fintech hubs

THE B-HIVE EUROPE JOURNEY

95

96

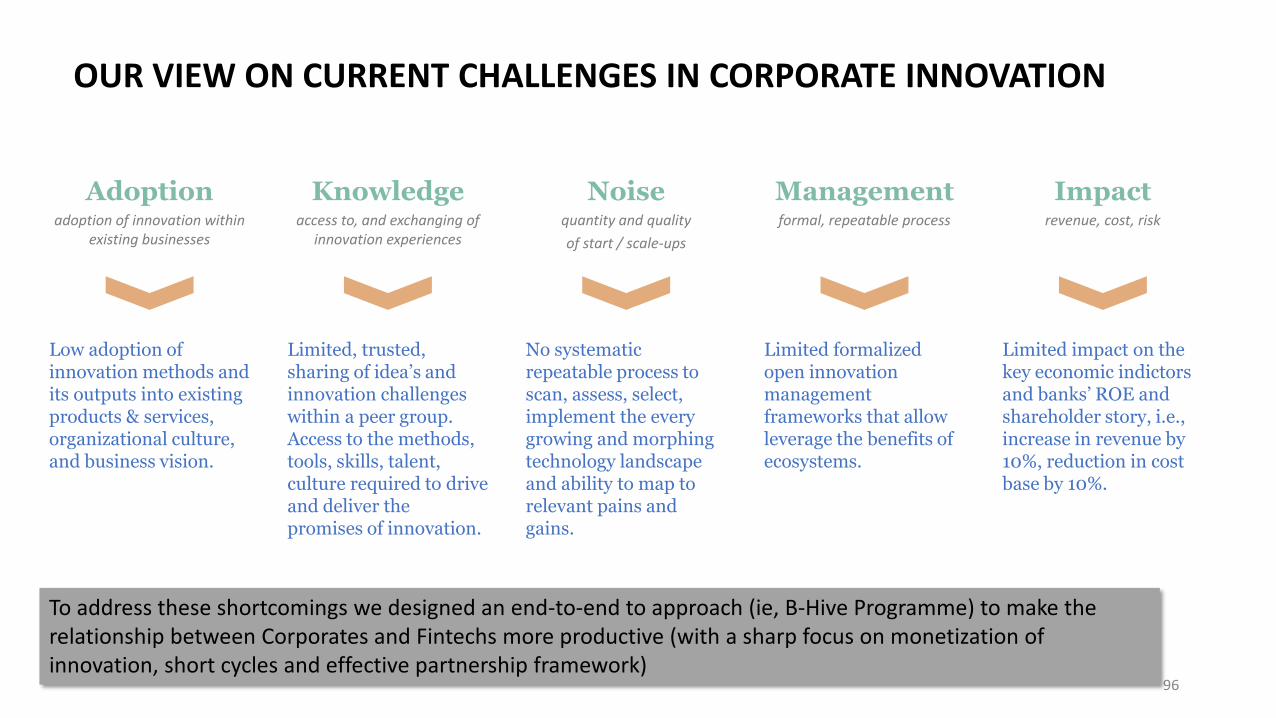

OUR VIEW ON CURRENT CHALLENGES IN CORPORATE INNOVATION

Knowledgeaccess to, and exchanging of

innovation experiences

Limited, trusted, sharing of idea’s and innovation challenges within a peer group. Access to the methods, tools, skills, talent, culture required to drive and deliver the promises of innovation.

Noisequantity and quality of start / scale-ups

No systematic repeatable process to scan, assess, select, implement the every growing and morphing technology landscape and ability to map to relevant pains and gains.

Impactrevenue, cost, risk

Limited impact on the key economic indictors and banks’ ROE and shareholder story, i.e., increase in revenue by 10%, reduction in cost base by 10%.

Managementformal, repeatable process

Limited formalized open innovation management frameworks that allow leverage the benefits of ecosystems.

Adoptionadoption of innovation within

existing businesses

Low adoption of innovation methods and its outputs into existing products & services, organizational culture, and business vision.

To address these shortcomings we designed an end-to-end to approach (ie, B-Hive Programme) to make the relationship between Corporates and Fintechs more productive (with a sharp focus on monetization of innovation, short cycles and effective partnership framework)

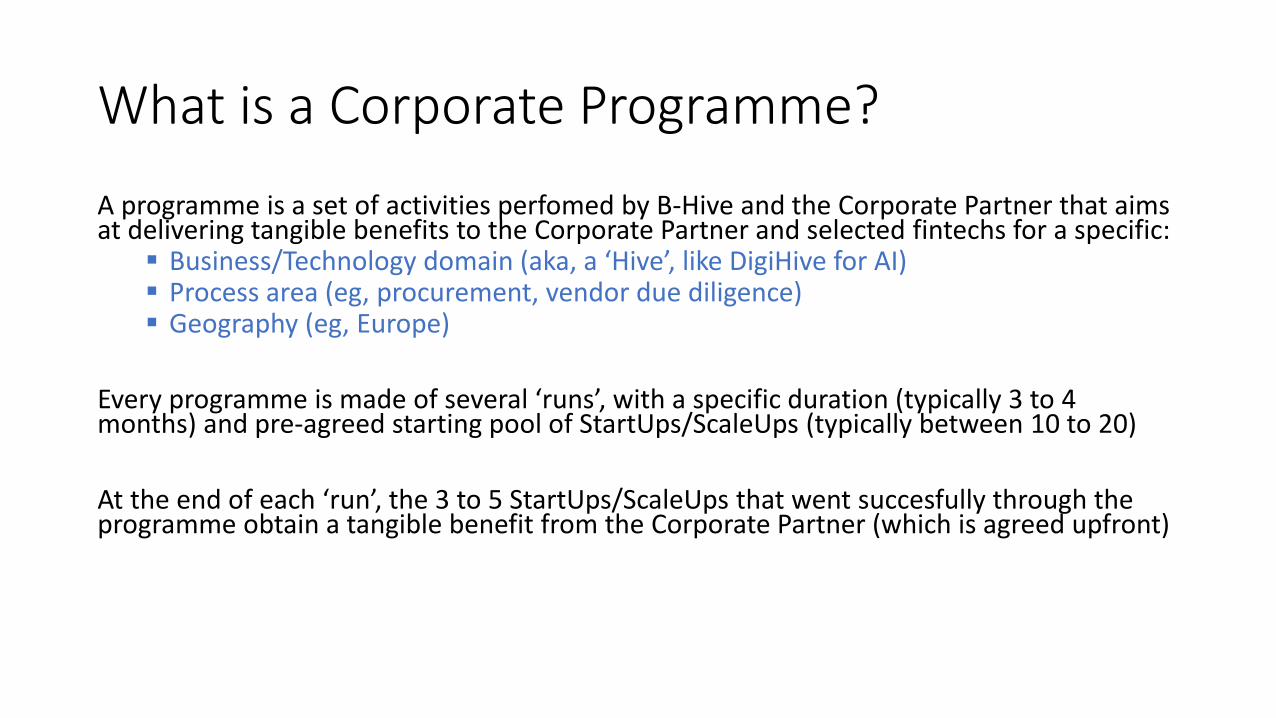

What is a Corporate Programme?

A programme is a set of activities perfomed by B-Hive and the Corporate Partner that aims at delivering tangible benefits to the Corporate Partner and selected fintechs for a specific: Business/Technology domain (aka, a ‘Hive’, like DigiHive for AI) Process area (eg, procurement, vendor due diligence) Geography (eg, Europe)

Every programme is made of several ‘runs’, with a specific duration (typically 3 to 4 months) and pre-agreed starting pool of StartUps/ScaleUps (typically between 10 to 20)

At the end of each ‘run’, the 3 to 5 StartUps/ScaleUps that went succesfully through the programme obtain a tangible benefit from the Corporate Partner (which is agreed upfront)

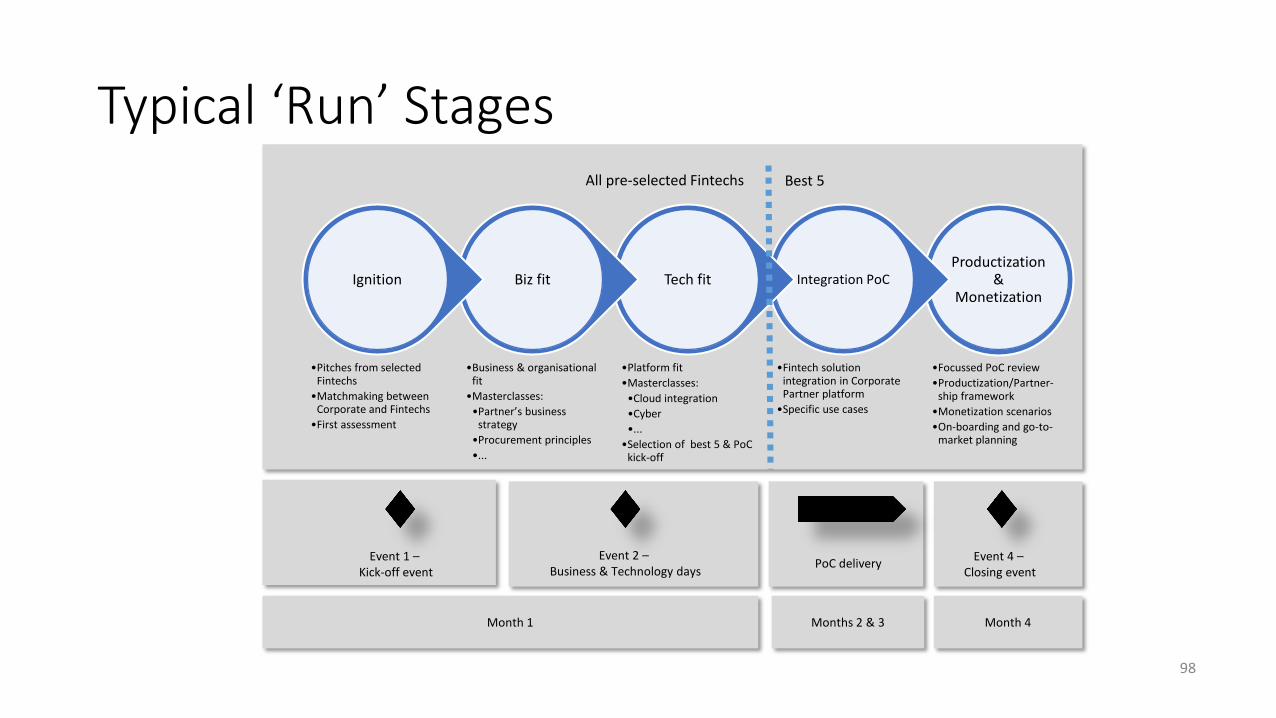

Typical ‘Run’ Stages

Productization &

Monetization

•Focussed PoC review•Productization/Partner-

ship framework•Monetization scenarios•On-boarding and go-to-

market planning

Integration PoC

•Fintech solution integration in Corporate Partner platform

•Specific use cases

Tech fit

•Platform fit•Masterclasses:

•Cloud integration•Cyber•...

•Selection of best 5 & PoC kick-off

Biz fit

•Business & organisational fit

•Masterclasses:•Partner’s business

strategy•Procurement principles•...

Ignition

•Pitches from selected Fintechs

•Matchmaking between Corporate and Fintechs

•First assessment

98

All pre-selected Fintechs Best 5

Event 1 –Kick-off event

Event 2 –Business & Technology days

Event 4 –Closing event

Month 1 Month 4

PoC delivery

Months 2 & 3

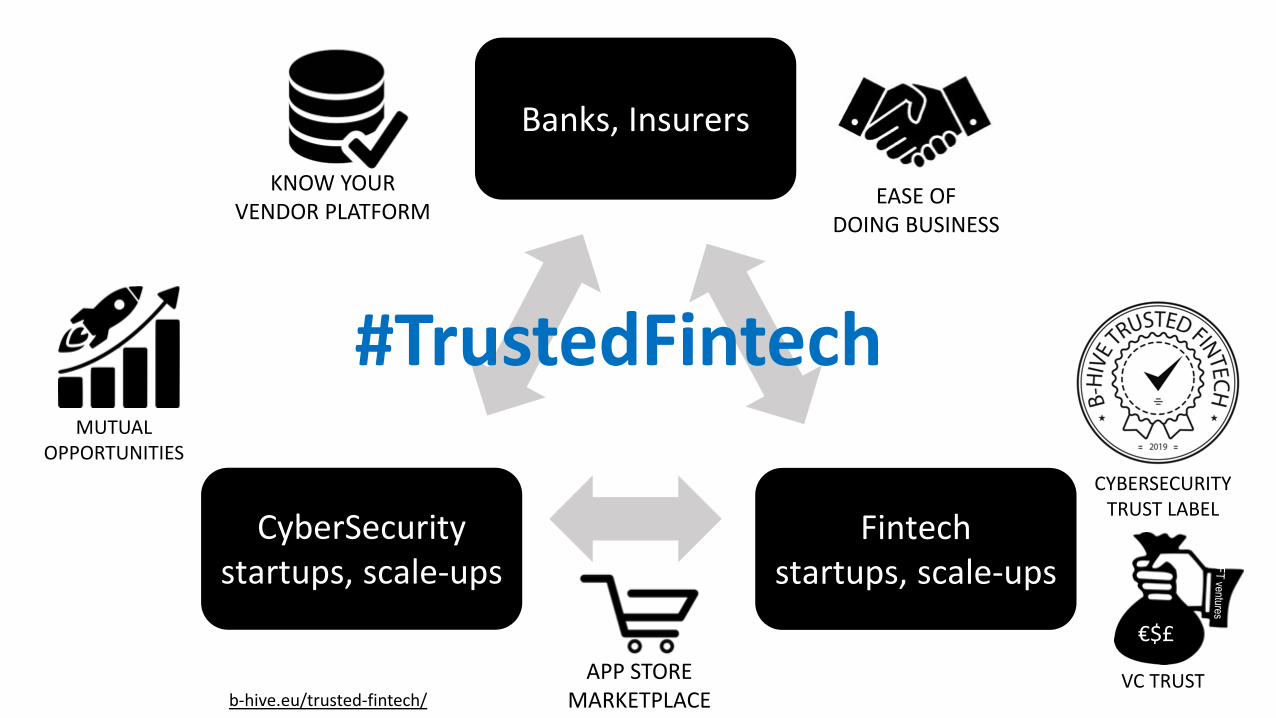

CYBERSECURITYTRUST LABEL

APP STOREMARKETPLACE

EASE OFDOING BUSINESS

MUTUALOPPORTUNITIES

Banks, Insurers

Fintechstartups, scale-ups

#TrustedFintech

CyberSecuritystartups, scale-ups

KNOW YOURVENDOR PLATFORM

VC TRUST

€$£

b-hive.eu/trusted-fintech/

Content is provided by our community

b-hive.eu/trusted-fintech/

PANEL• Quentin Colmant,

co-founder and managing director of Qover (InsurTech)

• Bart Vanhaeren, co-founder and CEO of InvestSuite (robo advisers)

• Prof. Georges Hubner, co-founder of Gambit (AI for investment advice)

• Jean-Louis Van Houwe, founder and CEO of Monizze (digital vouchers)

• Fabian Vandenreydt, executive chairman at B-Hive Europe (incubator)

Next conferences

Monday 10 December 2018: "The stability of the financial system”o Prof. Willem Buiter, Special Economic Advisor at Citi

o Prof. Dr. Bruno Colmant from Bank Degroof Petercam

Monday 21 January 2019: BFC New Year Party:

“Fintech missions in China (2018) and Korea (2019)”

o Thierry Janssen (Just in Time Management)

o Yannick Vandecapelle (Bank Delen)