Embed Size (px)

Citation preview

FINN DIXON & HERLING LLP

U.S. Carried Interest Legislation and its Impact on International Private Investment Fund Structures

Michael Spiro

International Fiscal Association

USA Branch, Westchester County, NY/Connecticut Region

Sheraton Stamford Hotel, CT

February 10, 2016

2

WHAT IS “CARRIED INTEREST”?

n An interest in a partnership (private investment fund) that entitles the fund manager (or its affiliate) to receive a disproportionate share of fund profits.

n Often equal to 20% of fund profits.q In the buyout fund context, generally 20% in excess of an

8% coupon on invested capital.

q VC context generally does not include a coupon.

q Hedge funds vary, but traditionally did not include a “hurdle.”

n Fund managers also usually charge an annual fee based on assets under management (“AUM”). (2% is standard.)

Partnership Tax

n Income of partnership is allocated according to the partnership agreement.

n Character of income (ordinary income or loss, long-term capital gain or loss, short term capital gain or loss) determined at partnership level.

n Allocations must have “substantial economic effect”—i.e. track economic entitlements to partnership income in liquidation.

3

Grant of a Partnership Interest

n “Capital Interest” is property under Section 83 of the Internal Revenue Code. Recipient is taxed on the fair market value of the partnership interest.

n Receipt of a “profits interest” is not taxable (Rev. Proc. 93-27).

4

Taxation of Carried Interest

n Carried interest is a partnership “profits interest.”

n Rev. Proc. 93-27:

q A capital interest is an interest that would give the holder a share of the proceeds if the partnership's assets were sold at fair market value and then the proceeds were distributed in a complete liquidation of the partnership. This determination generally is made at the time of receipt of the partnership interest.

q A profits interest is a partnership interest other than a capital interest.

5

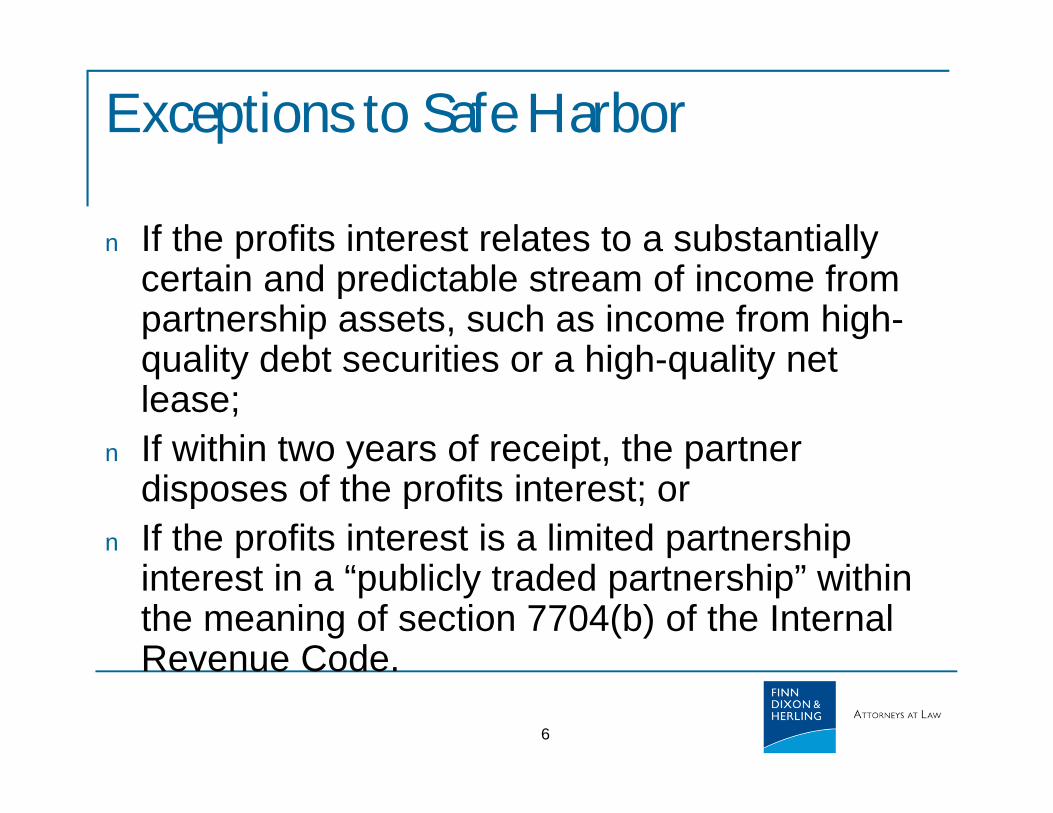

Exceptions to Safe Harbor

n If the profits interest relates to a substantially certain and predictable stream of income from partnership assets, such as income from high-quality debt securities or a high-quality net lease;

n If within two years of receipt, the partner disposes of the profits interest; or

n If the profits interest is a limited partnership interest in a “publicly traded partnership” within the meaning of section 7704(b) of the Internal Revenue Code.

6

Benefits of Carried Interest

n No tax at grant.

n Character of income determined at partnership level.

q In private equity fund context, vast majority of income is either long-term capital gains or qualified dividend income.

q When 20% of long-term capital gains or QDI is allocated to the fund manager to compensate for management services, it retains its character.

7

TYPICAL 1 ENTITY FUND STRUCTURE

8

Private Investment Fund, LP

(Delaware)

General Partner (LP

or LLC)Investment Manager

Management fee (2% of AUM)

LP Investors

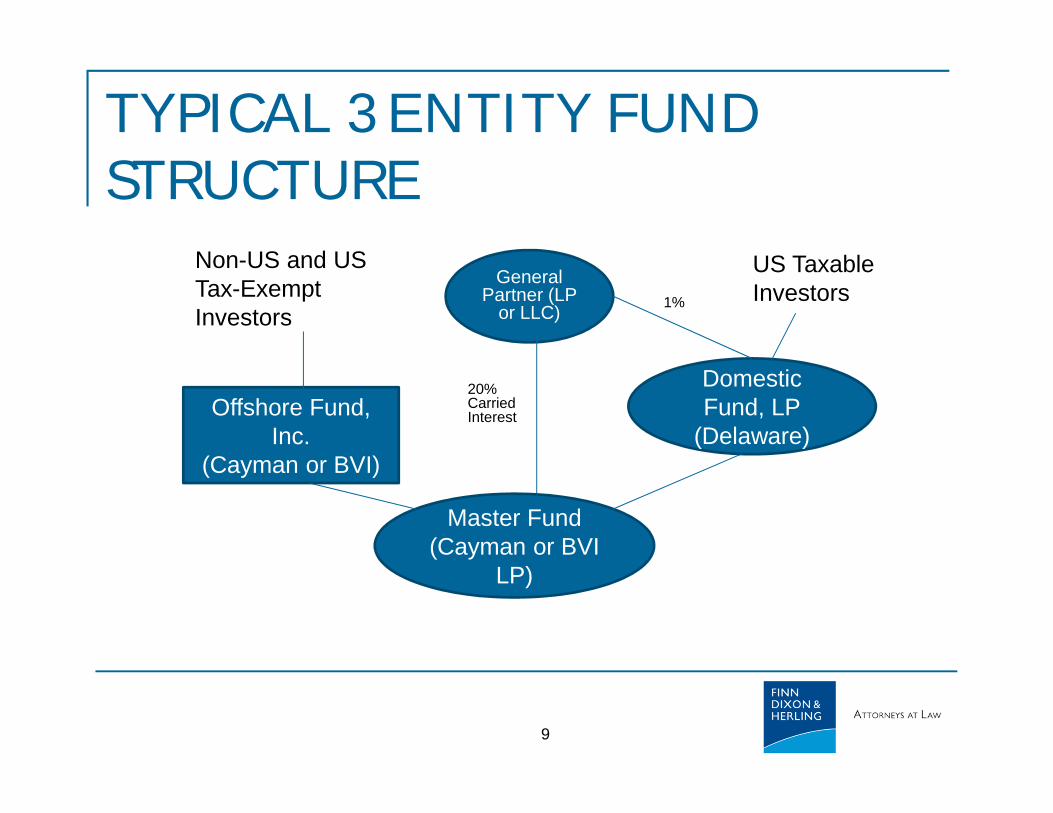

TYPICAL 3 ENTITY FUND STRUCTURE

9

Master Fund (Cayman or BVI

LP)

Offshore Fund, Inc.

(Cayman or BVI)

Domestic Fund, LP

(Delaware)

General Partner (LP

or LLC)

20% Carried Interest

1%

Non-US and US Tax-Exempt Investors

US Taxable Investors

CONGRESSIONAL PROPOSALS TO CLOSE THE “CARRIED INTEREST LOOPHOLE”

n 2007—HR 2834

n 2010—American Jobs and Closing Tax Loopholes Act”

n 2012—Carried Interest Fairness Act

n 2014—Dave Camp Discussion Draft

n 2015—Carried Interest Fairness Act

10

2007, 2010, 2012 and 2015 LEGISLATION (THE LEVIN BILL)

n Introduces a new Section 710 of the Internal Revenue Code which recharacterizes income with respect to an “Investment Services Partnership Interest” (“ISPI”), as ordinary income.q 2007 iteration included the words “for the performance of

services.” This language does not appear in subsequent iterations.

q After being passed by the House in 2010, the 2010 Senate bill considered a blended rate for certain income rather than all ordinary.

q 2015 iteration only recharacterizes net capital gain so short-term capital gain retains its character as capital.

n Gain on the disposition of an ISPI is treated as ordinary income.

11

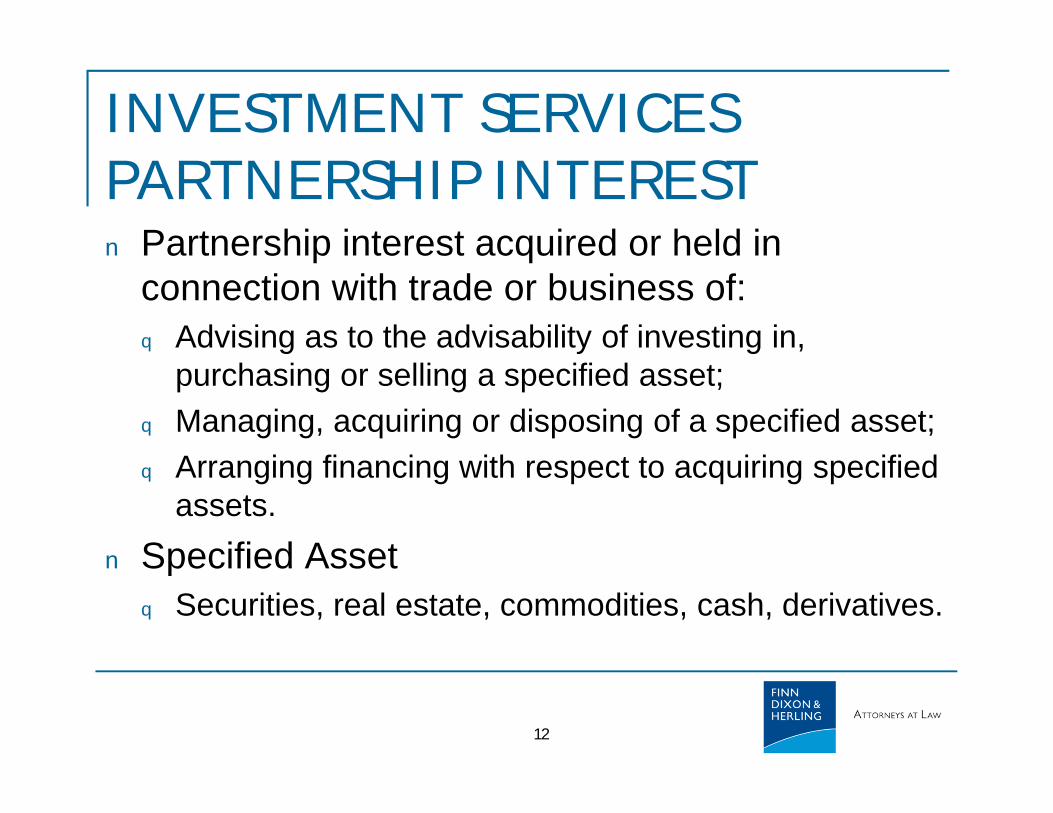

INVESTMENT SERVICES PARTNERSHIP INTERESTn Partnership interest acquired or held in

connection with trade or business of:

q Advising as to the advisability of investing in, purchasing or selling a specified asset;

q Managing, acquiring or disposing of a specified asset;

q Arranging financing with respect to acquiring specified assets.

n Specified Asset

q Securities, real estate, commodities, cash, derivatives.

12

SIGNIFICANT ISSUES

n Ordinary incomeq Sourcing

n Does income that is recharacterized as ordinary retain its character for other purposes?

n If a fund manager who is not a US taxpayer receives a share of net capital gain as carried interest, this would typically be sourced to his country of residence (and not be subject to US tax).

n Does this sourcing apply under 710 or is it recast as service income that is sourced according to where services provided?q Removal of “performance of services” language from 2007 legislation

suggests the former, but no clarity. It is treated as net earnings from self-employment.

n Coordination with tax credit regimes in other jurisdictions.

q 409A/457An Does recharacterized income retain its character as a partnership

allocation that is exempt from 409A/457A?

13

SIGNIFICANT ISSUES (CONT.)

n Enterprise Valueq 2007 and 2010 iterations would have treated equity interests in

an entity engaged in fund management as ISPIs.q Sale proceeds from sale of equity of the manager would be

ordinary—taxing “enterprise value” of the manager itself as ordinary.

q 2015 iteration changes this so that to be an ISPI, the interest must be an interest in an “investment partnership”n Partnership substantially all of the assets of which are specified assets;

andn Less than 75% of the capital is attributable to invested capital and held in

connection with a trade or business of the owner of the interest (i.e. not an operating entity).

n This allows continued capital gains treatment of goodwill/enterprise value of investment management businesses.

14

THE CAMP PROPOSAL

n 2014 Discussion Draftn No tractionn Treats the holder of carried interest as having borrowed

partnership capital used to fund carried interest share of profit.n Interest that the GP would have had to pay on the loan is tracked

to establish “recharacterization account balance” and partnership net capital gain income allocated to carried interest is treated as ordinary to extent of this account (effectively treating imputed interest as compensatory to carried interest holder).

n Also applies only to investment management services (not real estate).

n Rate of imputed interest is high (and complex).n Raises similar questions about sourcing—is the

“recharacterization account” service income sourced based on where services are provided?

15

REGULATORY ACTIONS—DISGUISED PAYMENTS FOR SERVICES

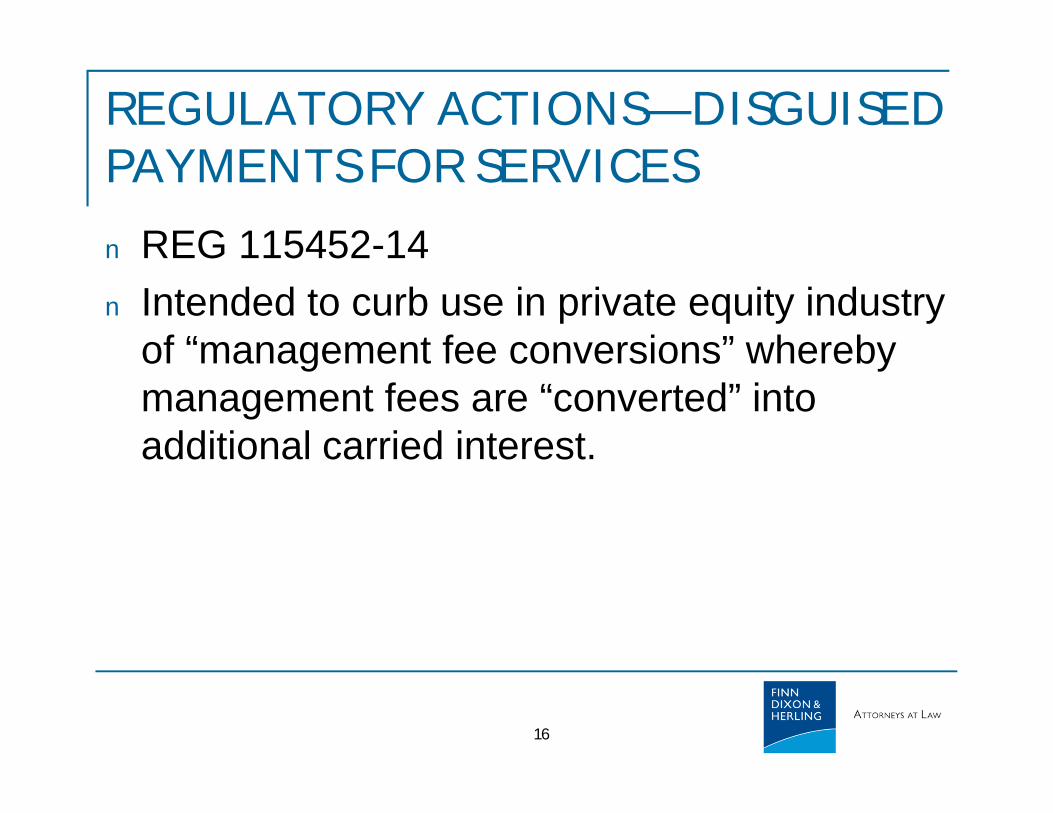

n REG 115452-14

n Intended to curb use in private equity industry of “management fee conversions” whereby management fees are “converted” into additional carried interest.

16

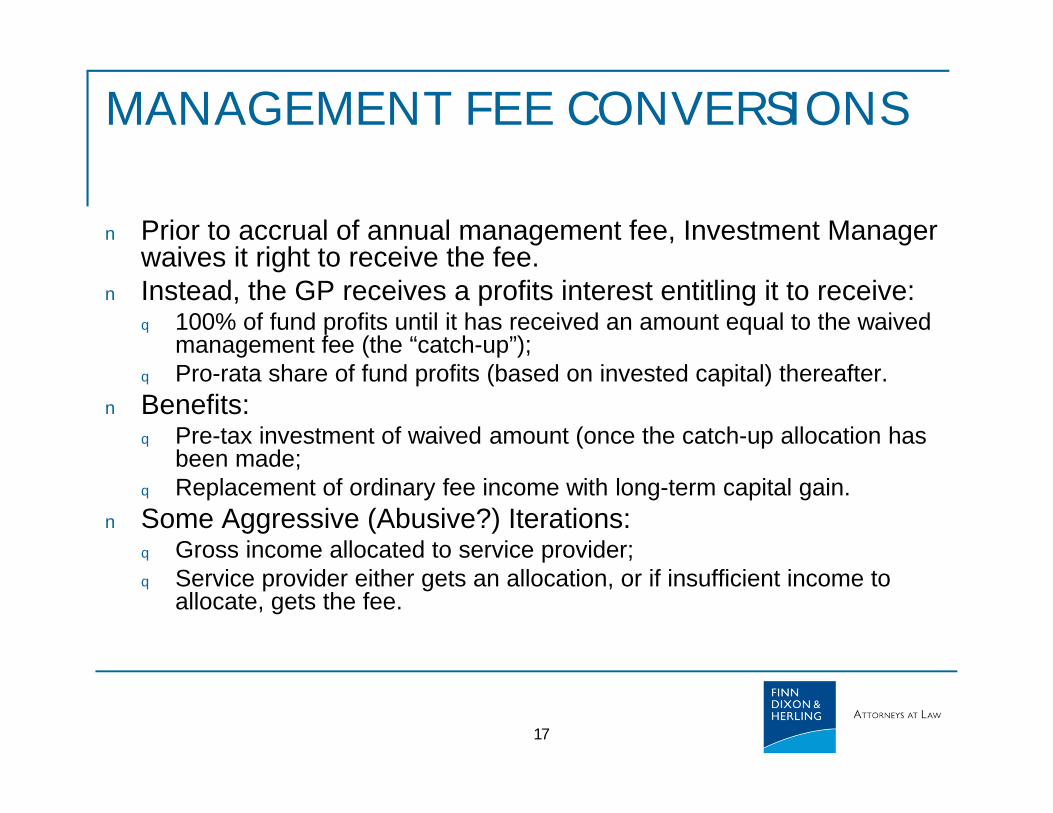

MANAGEMENT FEE CONVERSIONS

n Prior to accrual of annual management fee, Investment Manager waives it right to receive the fee.

n Instead, the GP receives a profits interest entitling it to receive:q 100% of fund profits until it has received an amount equal to the waived

management fee (the “catch-up”);q Pro-rata share of fund profits (based on invested capital) thereafter.

n Benefits:q Pre-tax investment of waived amount (once the catch-up allocation has

been made;q Replacement of ordinary fee income with long-term capital gain.

n Some Aggressive (Abusive?) Iterations:q Gross income allocated to service provider;q Service provider either gets an allocation, or if insufficient income to

allocate, gets the fee.

17

18

CODE SECTION 707(A)(2)(A)

If—

(i) a partner performs services for a partnership or transfers property to a partnership,

(ii) there is a related direct or indirect allocation and distribution to such partner, and

(iii) the performance of such services (or such transfer) and the allocation and distribution, when viewed together, are properly characterized as a transaction occurring between the partnership and a partner acting other than in his capacity as a member of the partnership,

such allocation and distribution shall be treated as a transaction described in paragraph (1) [as compensation paid to a non-partner]

PROPOSED REGULATIONS

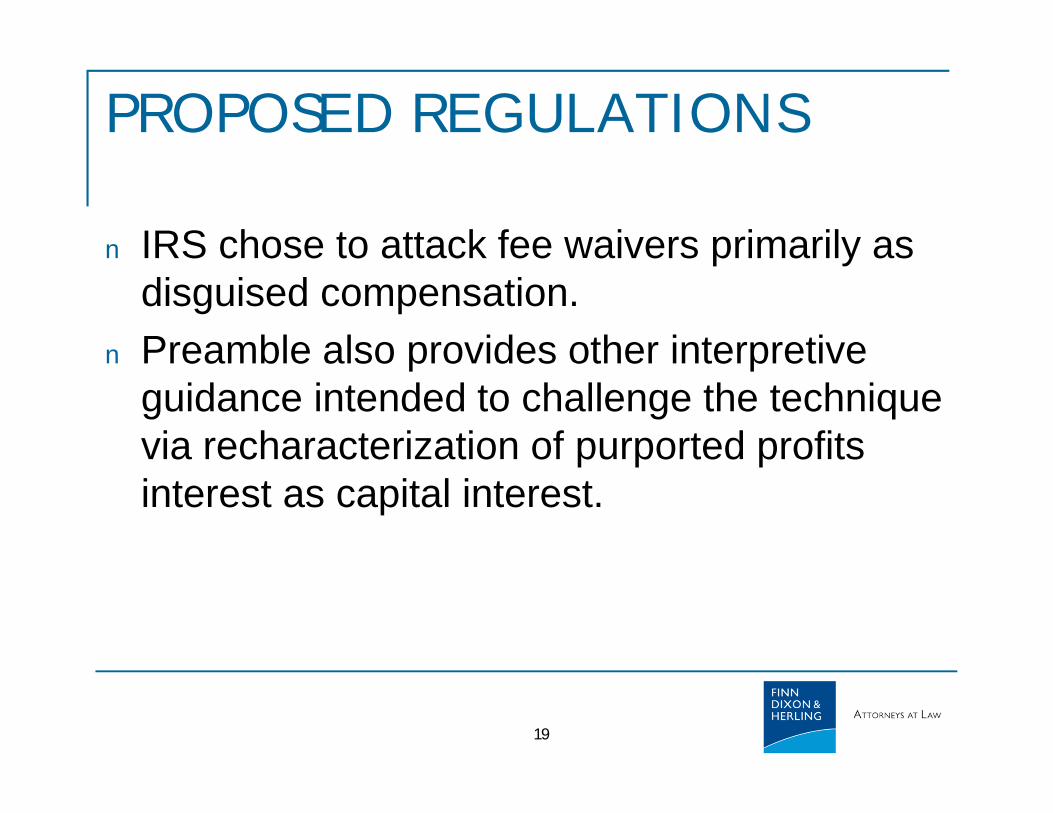

n IRS chose to attack fee waivers primarily as disguised compensation.

n Preamble also provides other interpretive guidance intended to challenge the technique via recharacterization of purported profits interest as capital interest.

19

THE PROPOSED REGULATIONS

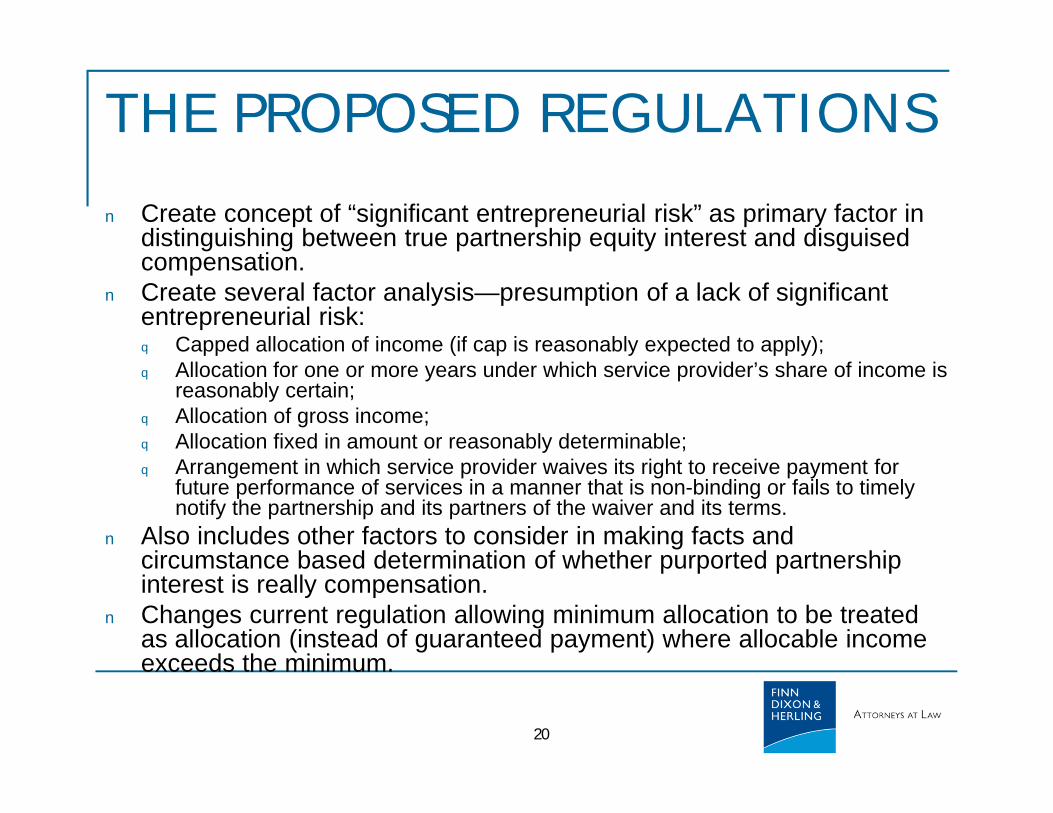

n Create concept of “significant entrepreneurial risk” as primary factor in distinguishing between true partnership equity interest and disguised compensation.

n Create several factor analysis—presumption of a lack of significant entrepreneurial risk:q Capped allocation of income (if cap is reasonably expected to apply);q Allocation for one or more years under which service provider’s share of income is

reasonably certain;q Allocation of gross income;q Allocation fixed in amount or reasonably determinable;q Arrangement in which service provider waives its right to receive payment for

future performance of services in a manner that is non-binding or fails to timely notify the partnership and its partners of the waiver and its terms.

n Also includes other factors to consider in making facts and circumstance based determination of whether purported partnership interest is really compensation.

n Changes current regulation allowing minimum allocation to be treated as allocation (instead of guaranteed payment) where allocable income exceeds the minimum.

20

Consequences of Recharacterization

n 409A/457A apply;

n Sourcing is based on where services provided—same as if the amount had been paid as management fee.

21

Questions?

Michael P. Spiro

FINN DIXON & HERLING LLP

177 Broad Street

Stamford, CT 06901

Phone: (203) 325-5067

Fax: (203) 325-5001

Email: [email protected]

www.fdh.com

22

![U.S. v. Dixon, 509 U.S. 688 (1993) - Columbus School of Lawclinics.law.edu/res/docs/US-v-Dixon.pdfU.S. v. Dixon, 509 U.S. 688 (1993) Dixon, Dixon. and [1] Dixon. *698. order. Dixon](https://img.pdfslide.us/doc/110x75/5ac1e6007f8b9ad73f8d6ea8/us-v-dixon-509-us-688-1993-columbus-school-of-v-dixon-509-us-688.jpg)