Embed Size (px)

Citation preview

12

CHAPTER II

CAPITAL EXPENDITURES – A THEORITICAL FRAMEWORK

Capital expenditure decisions are one of the most important decisions for the

growth of a company. The success of long term investment decisions of the

companies is crucial for economy’s growth. These decisions pertain to building up the

infrastructural base of the company by investing in land, building, plant and

machinery, furniture, transportation and such other assets for utilizing them in their

physical form throughout their working life.

Business fixed investment is either intended to replace the old utilities or

create new capacity in the firm. It is, however, difficult to separately analyze the

investments incurred for replacement or expansion on account of data unavailability.

Various studies in the past have considered either gross or net investment (net of

depreciation) as the dependent variable in estimating the impact of financing on

investment decisions. The studies with gross investment (Krishnamurty and Sastry

(1975)1, Hoshi, Kashyap and Scharfstein (1991)2, Athey and Laumas (1994)3 etc.) as

the dependent variable consider total increase in business investment including

replacement and expansion investments. Moreover, such studies have taken

depreciation as an independent variable to study its impact and significance on change

in gross investment. On the other hand, various other studies have taken net

investment as the dependent variable. In any case, the objective of the study still holds

good and the present analysis is confined to study of change in net fixed investment

(change in net fixed assets). Replacement and expansion investments are usually

complementary and are undertaken together. Replacement investment is of routine

nature and needs to be carried out by all organizations on a recurring basis. On the

other hand, expansionary investments are aimed at enlarging the scale of operations

by either investing in new products or new markets or deeper penetration in existing 1 Krishnamurthy, K. and Sastry, D.U. Investment and Financing in the Corporate Sector in India,

Tata McGraw-Hill Publishing Company Ltd, New Delhi, 1975 2 Hoshi, Takeo; Kashyap, Anil and Scharfstein, David, “Corporate Structure, Liquidity, and

Investment: Evidence from Japanese Industrial Groups,” The Quarterly Journal of Economics, Volume 106, No. 1., Feb., 1991, p.p. 33-60

3 Athey, M. J. and Laumas, P. S., "Internal Funds and Corporate Investment in India", Journal of Development Economics, Vol. 45, 1994, pp. 287-303

13

markets. The period covered in the study represents a growing phase of Indian

economy due to liberalization and it would be an interesting proposition to study the

exact nature of investments during this phase. The net investments are expected to

exhibit greater consistency than the gross impact of replacement and expansion

investments. Moreover, there is a need to study the impact of availability or non-

availability of internal or external funds while meeting corporate objectives and any

particular financing hierarchy.

This chapter aims to provide theoretical support for the empirical analysis to

be performed in later chapters. It has been divided into five sections. Section 2.1

discusses capital expenditure decision and Section 2.2 highlights the capital

expenditure decision making process. Investment theories have been explained in

Section 2.3 and Section 2.4 deals with external sources of finance. Section 2.5

establishes the link between financing sources and investment. The last Section 2.6

concludes the chapter.

2.1 CAPITAL EXPENDITURE DECISION

The success of a company lies in optimum utilization of funds to achieve the

widely accepted objective of the shareholder’s wealth maximization. The capital

expenditure decisions play a key role in this process because of their magnitude and

impact on company’s overall performance. Wealth maximization is a preferred

objective over profit maximization and earnings per share (which is at times

considered as an improved version of profit maximization). It takes into account the

present and expected future earnings per share along with timing of benefits,

qualitative factors (risk attached to expected earnings), dividend policy of the

company and various other factors. Hence, the management should evaluate the

investment, financing and asset management decisions on the yardstick of

shareholder’s value maximization. This objective can further be broadened by adding

other stake holders (such as managers, creditors, customers, suppliers and society as a

whole) into the ambit.

14

“Investing is commitment of resources made with the expectation of realizing

future benefits over a reasonably long period.”4

In other words, an investment refers to the outlay of funds in physical,

financial or intangible assets to reap benefits in the future. Capital expenditures

primarily relate to commitment of a part of total funds permanently or for long-term

to work towards the accomplishment of company’s objectives. It represents a sizeable

outlay of funds for the company. These investments include new building, major

repairs and renovations. Further, equipments and infrastructure may be required for

new products, for greater production volume, replacements for various reasons, for

cost reduction, and major overhauling. As this study aims at understanding capital

expenditure behavior of major Indian companies, these expenditures may be referred

to as business fixed investment or corporate investment. Corporate investment is in

turn a significant barometer of growth and development in an economy and involves

huge stakes. Different companies have varied reasons for incurring these expenditures.

The next section describes the standard capital expenditure decision making process

followed by companies.

2.2 CAPITAL EXPENDITURE DECISION MAKING PROCESS

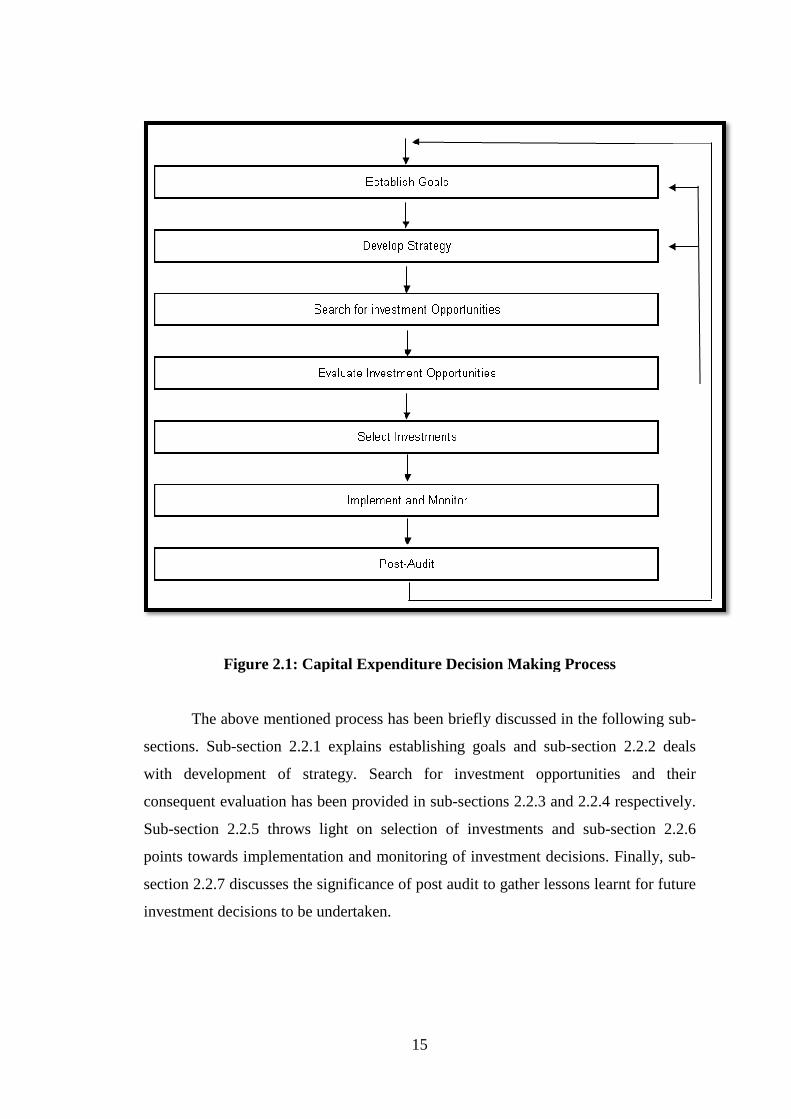

Capital Expenditure decision making involves the scrutiny, review, analysis,

implementation and follow-up of such long-term investments to achieve the goal of

shareholder’s wealth maximization. In the words of Gitman (2001)5 , “Capital

budgeting is the process of evaluating and selecting long-term investments consistent

with the firm’s goal of owner’s wealth maximization.”

The decision process typically follows the following displayed route:

4 Kreps, Clifton H. Jr. and Wacht, Richard F., Financial Administration, The Dryden Press, Illinois,

1975, p. 369 5 Gitman, Lawrence J., Principles of Managerial Finance, Ninth Edition, Pearson Education Asia,

2001, p 332

Figure 2.1: Capital Expen

The above mentioned process has been briefly discussed in the following sub

sections. Sub-section 2.2.1 explains establishing goals and sub

with development of strategy. Search for investment opportuniti

consequent evaluation has been provided in sub

Sub-section 2.2.5 throws light on selection of investments and sub

points towards implementation and monitoring of investment decisions. Finall

section 2.2.7 discusses the significance of post audit to gather lessons learnt for future

investment decisions to be undertaken.

15

.1: Capital Expenditure Decision Making Process

The above mentioned process has been briefly discussed in the following sub

section 2.2.1 explains establishing goals and sub-section 2.2.2 deals

with development of strategy. Search for investment opportuniti

consequent evaluation has been provided in sub-sections 2.2.3 and 2.2.4 respectively.

section 2.2.5 throws light on selection of investments and sub

points towards implementation and monitoring of investment decisions. Finall

section 2.2.7 discusses the significance of post audit to gather lessons learnt for future

investment decisions to be undertaken.

diture Decision Making Process

The above mentioned process has been briefly discussed in the following sub-

section 2.2.2 deals

with development of strategy. Search for investment opportunities and their

sections 2.2.3 and 2.2.4 respectively.

section 2.2.5 throws light on selection of investments and sub-section 2.2.6

points towards implementation and monitoring of investment decisions. Finally, sub-

section 2.2.7 discusses the significance of post audit to gather lessons learnt for future

16

2.2.1 Establish Goals

As previously discussed, maximization of share holder’s wealth is the overall

objective of financial management. However, the same may be inferred more

precisely for operational decisions. Moreover, the operational objectives also indicate

the motive for investment. The growth plans of an existing firm require the

acquisition of new fixed assets. The expansion plans may involve either tapping of

new markets with existing products or penetrating deeper in existing markets with

advanced or new products. On the other hand, a newly incorporated firm needs to

build resources to implement its initial plans. Further, when a budding firm is

progressing towards its goals, it requires replacing or renewing the obsolete or worn-

out assets. Costs and benefits of repairs and replacements have to be compared.

Renewal, an alternative to replacement, may involve rebuilding, overhauling or

retrofitting an existing fixed asset to improve its efficiency. Some other capital

expenditure decisions require long-term commitment of funds in expectation of a

future return.

2.2.2 Develop Strategy

Strategy is an organization’s response to environmental opportunities and

threats. It is the framework within which resources are to be marshaled to pursue

predefined goals. Each strategic decision is in itself a general capital budgeting

decision, in that it is based on the estimate of wealth creation and other contributions

to company goals that can be expected from later capital investments in pursuit of a

particular strategy. Goal setting and strategy choice are interactive processes because

goals usually require to be fine-tuned in response to information about practicability

gained in the assessment of alternatives. Now-a-days, strategic business units are set-

up within companies for achieving organizational goals.

17

2.2.3 Search for Investment Opportunities

Horne and Wachowicz 6 classifies the sources of investment project proposals

into five categories, namely, new products or expansion of existing products,

replacement of equipment or buildings, research and development, exploration and

other. Another useful classification has been discussed below7.

• Replacement Investment

It involves outlay for a new equipment for the purpose of replacing an existing

but discarded equipment. The need may arise either due to wear and tear during

normal course of business or due to obsolescence. Wearing of machinery is a usual

phenomenon over an asset’s life. Parts wear out one at a time and are replaced.

Capital additions are made to replace major components.

However, obsolescence refers to discarding of equipment due to the

introduction of alternative and more effective methods of production (in terms of

quality or economy). The asset turns out to be obsolete if the product it produces

becomes obsolete. If technological development is fast and changes in customer

preferences are frequent, the obsolescence rate tends to be higher. Obsolescence does

not put a question on the make, performance or economic life of the asset.

Moreover, replacement takes place at individual machine level and in case the

overall plant requires overhauling and change, such investment is categorized under

modernization category. This method is adopted to absorb the advanced technology in

the organizational set-up and to cope up with the dynamic and competitive business

environment.

• Expansion Investment

The capital expenditure decisions to buy equipments for expansion of

production of existing products fall under this category. New Industrial Policy, 1991

6 Horne, Van J.C. and Wachowicz, Jr., John M., Fundamentals of Financial Management, Eleventh

Edition, Pearson Education Asia, India, 2001, p 316 7 Kishore, Ravi M., Financial Management, Sixth Edition, Taxmann, 2007, p 609

18

brought tremendous changes in Indian corporate sector. Economic growth rate and

increased per capita output during the study period clearly indicate that companies

have grown at a fast pace to keep up with complex corporate scenarios after

liberalization and globalization. Hence such types of investments have been in vogue

in India. They include a wide variety of proposals ranging from increasing the number

of existing machines to opening multiple branches as the increase in demand is of

permanent nature.

• Balancing Investment

At times the capacity utilization of plant and machinery remains unbalanced

due to under-utilization of existing capacity. Initial increase in demand is usually met

through installation of relevant machinery to complement the existing structure and

achieve full plant capacity utilization. The value addition that takes place due to

addition of balancing equipment is considered as incremental cash inflow.

• Diversification Investment

This implies adding up an entirely new business with the existing line after

strategic considerations. This leads to minimization of total risk of the company due

to portfolio diversification. It leads to widening of asset base, increase in turnover and

profits, optimum utilization of managerial capacity and implementation of latest

technologies.

• Modernization Investment

This type of investment is required to be carried out in case of high cost of

production, frequent interruptions in plant running, high maintenance cost and such

other reasons attached with old set-up. Investment in new machineries helps in

improving productivity as well as product quality.

Based on this premise, the potential capital investments have to be identified.

The remainder of the process can only assure that the best of the proposed

investments are selected. The search for investment opportunities must be supported

by a corporate culture that encourages creativity; otherwise, there will be no good

proposals to evaluate. A successful search process generally requires the commitment

19

of resources. Research, product development, and consumer attitude surveys are all

ways to identify investment opportunities. If the strategy involves acquisition of other

companies, an acquisition group may be responsible for searching out and evaluating

opportunities. These various approaches have in common the willingness to spend

money on people to search for attractive capital investments.

Training in support of strategy is another example of organization for a

successful search. Executives are increasingly realizing that training of employees is

not a sideline activity but an important part of strategy implementation. A successful

search for investment opportunities will be carried out at all levels of the organization.

Major capital investments that involve a change in strategy will probably be identified

at a top management level. Major investments in support of existing strategy will

typically be developed at a high level, such as the senior executive in charge of

marketing or production. Smaller investments are identified and given preliminary

screening by the person in a position to perceive a risk. Efforts to encourage the

search for attractive investments must reach people at all levels of the organization.

2.2.4 Evaluate Investment Opportunities

This is the most important step of capital budgeting process. Numerous capital

expenditure proposals developed during above mentioned step have to be evaluated

by use of various capital budgeting techniques. Cash flow estimation is usually

considered as the most difficult stage of capital expenditure decisions. This step

involves cash flow estimations and application of capital budgeting techniques along

with risk incorporation resulting in the calculation of the expected net present value of

cash flows from different proposals.

2.2.5 Select Investments

Final decision making power is usually spread across the company depending

on the magnitude of investment. The larger investment opportunities are chosen by

corporate capital budgeting committee and the smaller ones may be assigned to

middle level management. At times, the managers are faced with more than one

20

feasible proposals but the funds fall short of requirements. Hence, the next step in

capital expenditure decision making process is rationing the available funds among

the feasible proposal (s) optimally. In other words, “capital rationing requires the

investor to reject investment projects that otherwise meet his financial or non financial

requirements for acceptance”8. This situation complicates the investment decision

process. The company must not merely identify profitable investment opportunities,

but must also rank them in relation to one another.

Capital rationing may be caused by conditions external to the firm, by internal

factors or by a combination of both. During the period of rationing, it is advisable to

use the internal rate of return criterion for project ranking as it ranks the projects on

the basis of project yield irrespective of company’s cut-off rate. The firm will start at

the top of the list and work downward until its available funds have been exhausted.

The top management team entrusted with this task includes finance head and the

concerned departmental heads to take the final decisions in this regard.

2.2.6 Implement and Monitor

Finally, the implementation and monitoring process begins once a capital

investment proposal has been approved. Capital investments are monitored during the

actual period of acquisition or construction because deviations, either good or bad,

should be recognized, taken into consideration, and dealt with. Cost overruns are the

most common deviations during construction or acquisition and are dealt with by

changing control procedures or taking another look at the attractiveness of the

investment. Likewise, the capital investment should be monitored as it goes into

operation to spot deviations and take timely corrective action.

2.2.7 Post-Audit

Post-audit of the decisions taken and implemented is primarily a learning tool

because it is carried out at the end of a capital investment’s life or after the investment

8 Fremgen, J.M., “Capital Budgeting Practice – A Survey,” Management Accounting, May, 1973, p

19

21

has matured to a stable level of activity and profitability. The post-audit includes an

assessment of the actual performance of the investment and a comparison with

forecasted performance. Reasons for deviation from anticipated performance are

sought. Post-audits allow identifying the strengths and weakness of the capital

budgeting systems. The information garnered from a series of post-audits can result in

a new look at goals and strategies.

Consequently, the capital investment process is dynamic, with the entire

process being continually reviewed and modified as and when new information

becomes available.

2.3 THEORIES OF INVESTMENT

Investment implies an incremental flow to the existing stock of capital. This

addition may be fixed (long-term) or inventory (short-term), replacement or

expansionary. The different theories of investment primarily revolve around the

writings of Fisher9 and Keynes10 and primarily involve the concepts like marginal

efficiency of capital (MEC) or marginal efficiency of investment (MEI). MEC of an

investment as per Keynes is the discount rate at which the demand price exactly

equals the supply price. This concept is quite equivalent to Fisher’s internal rate of

return. MEC schedule presents the optimal level of capital stock as a function of rate

of interest. MEI schedule shows how much investment would be profitable to carry

out in current period for different levels of cost of capital given the initial level of

capital stock. The other notable factors affecting investment are:

• Expectations regarding demand factors which determine the position of MEC

schedule are to be specified.

• Adjustment of capital stock to the desired level cannot be instantaneous for a

variety of reasons.

• The presumption with MEI schedule is regarding infinitely elastic supply of

funds at a given rate of interest. 9 Fisher, The Theory of Interest, New York, 1930 10 Keynes, J. Maynard, The General Theory of Employment, Interest and Money , New York,

Harcourt Brace Jovanovich, 1936

22

Thus a lag structure needs to be specified. The models of business fixed

investment are discussed below to highlight their method of tackling the above

mentioned issues and the factors pertinent as per them in determining corporate fixed

investment.

This section presents five theories of investment developed over a period of time.

These theories have been briefly discussed in the following sub-sections. Sub-section

2.3.1 throws light on accelerator theory and accelerator- cashflow model has been

provided in sub-section 2.3.2. The next two sub-sections 2.3.3 and 2.3.4 deal with

permanent income theory and neo-classical theory. The last sub-section 2.3.5 presents

security value model.

2.3.1 Accelerator Theory

Accelerator model was initially proposed by J. M. Clark11 in early twentieth

century which was later modified by a number of economists especially Koyck12 and

Chenery13. The model displays a linear relation of current investment with current and

past changes in output. The underlying assumption of any accelerator model is that

the desired capital stock at any point of time is a constant multiple of output, Y.

Hence, if output is growing, an increase in capital stock is required. Simply stated,

accelerator principle implies

K*t = αYt 2.1

Where K*t is the planned capital stock, Yt is the output and α is the capital-output

ratio. The model is based on the assumption that capital stock is optimally adjusted in

the unit period and an increase in output leads to increase in capital stock,

K*t+1 = αYt+1 2.2

And therefore,

11 Clark J. Maurice, "Business Acceleration and the Law of Demand: A Technical Factor in

Economic Cycles", Journal of Political Economy, 25, 1917, pp 217–235. 12 Koyck, L.M. "Distributed Lags and Investment Analysis", Amsterdam, North-Holland Pub. Co.,

1954 in Bhattacharyya, Surajit, "Determinants of Private Corporate Investment: Evidence from Indian Manufacturing Firms', Economic Society of South Africa, Conference, 2007

13 Chenery, H B, “Over Capacity and the Acceleration Principle”, Econometrica, Vol. 20, 1952, pp. 1-28

23

K*t+1 - K

*t = I t = α (Yt+1 - Yt) = α ∆Yt 2.3

However, it presumes that capital stock is always fully utilized but the model can

be reformulated to allow for capacity under-utilization and deviations from capital

stock in the previous period. Further, the assumption that capital stock is optimally

adjusted in the unit period ignores the importance of lags in investment decisions and

expectations formation. In the real world scenario, the adjustments in capital stock

take place over a period of time. The huge monetary expenditures, administrative

approvals and long gestation periods make it infeasible to relate current investment to

current change in output. Keeping in mind the shortcomings of simple accelerator

model, Goodwin14 and Chenery15 formulated ‘flexible accelerator’ models. This is

written as

I t = β (K*t - Kt-1) 2.4

Where β is a positive constant between zero and one and K*t equals αYt. The

equation implies that the adjustment path of actual stock is asymptotic. Chenery

extended Goodwin’s work by introducing ‘reaction lags’ to highlight the interval

between changes in demand and response in terms of new investment activity. In

these models, the expected future output is taken as the weighted average of past

output to allow for partial and delayed adjustment. The lags are expected to be longer

for large scale projects and shorter for small-scale projects. These lags may be

encountered due to a variety of reasons like gestational delays, planning, ordering,

delivery and delays in decision making. Moreover, the formation of expectations is

also captured by the same. However, the source of a particular lag may still remain

unidentified. The econometric evidence of accelerator theory has been impressive

though not free from criticism.

2.3.2 Accelerator – Cashflow Model

The theoretical base for adding a profit or cashflow variant to the investment

equation arises primarily on two grounds. Firstly, profits not only represent the

14 Goodwin, R.M., "The Non-linear Acceleration and the Persistence of Business Cycles,"

Econometrica, Vol. 19, 1951, pp: 1-17 15 Chenery, 1952, op. cit.

24

current status of excess revenue over costs but also act as a signal of future

profitability of the firm probably through increasing expected future output and

boosting optimal capital stock as well. Secondly, market imperfections may lead to

higher cost of external funds as compared to internally generated funds, thereby

creating the financing hierarchy. And cashflow as a proxy for internal funds may

yield some interesting results to dwell upon. Larger amounts of internal funds may

therefore be required to lower the cost of financing on one hand and to boost

investment on the other. This theory of investment was initially proposed by

Tinbergen (1938)16 and subsequently developed by Klien (1950)17. It upholds that the

amount of investment spending depends on the amount of profit that a firm is earning.

An increase in level of profits would increase the desired level of capital stock at all

levels of interest. Thus, firms invest with the expectation of earning profits in the

future on the basis of past and present profit levels. Moreover, the theory gets support

from the existence of capital market imperfections. In the strong version of this theory,

financing constraints usually operate at all times leading to restricted access to

external funds. Even in the weaker version of the theory, the financing constraints

operate at low levels of capacity utilization where extreme pressure on capacity may

result in procuring funds from outside (Meyer and Kuh, 1957)18. However, this view

is in sharp contrast with Modigliani and Miller’s independence hypothesis. Some of

the firm level studies using profit as a determinant of investment include that of

Grunfeld (1960)19, Kuh (1963)20 and Eisner (196721, 7822). Grunfeld23 and Kuh24

suggest that profit expectation cannot be adequately represented by current realized

16 Tinbergen, J., "Statistical Evidence on the Acceleration Principle," Economica, May 1938 in

Dhrymes, Phoebus, and Kurz, Mordecai, “Investment, Dividend, and External Finance Behavior of Firms”, 1979

17 Klein, E., “On Econometric Studies of Investment” , Journal of Economic Literature, 44-49, 1950 18 Meyer, John R and Edwin Kuh, “The Investment Decision: An Empirical Study”, Cambridge,

Harvard University Press, 1957 19 Grunfeld, Yehuda, "The Determinants of Corporate Investment," in The Demand for Durable

Goods, Ed. Arnold C. Harberger, Chicago, University of Chicago Press, 1960, pp 211-266 20 Kuh, Edwin, Capital Stock Growth: A Microeconomic Approach, Amsterdam, 1963. 21 Eisner, R., "A Permanent Theory for Investment: Some Empirical Explorations," American

Economic Review 57, 1967, pp 363–390. 22 Eisner, R., Factors in Business Investment, Ballinger Publishing Company, Cambridge,

Massachusetts, 1978. 23 Grunfeld, 1960, op. cit. 24 Kuh, 1963, op. cit.

25

profits. However, Eisner (1967)25 showed both profit and rate of growth of sales as

significant determinants of desired capital. In his later work (1978)26 he suggested that

it is in the timing of investment rather than in its long-run magnitude that profits play

a greater role. The empirical specification of the accelerator cashflow model is

identical to accelerator model except the addition of distributed lag on the level of

cashflow as an explanatory variable. In India, Bagchi (1962)27, Krishnamurty (1964)28,

Sarkar (1970)29 and certain other researchers have applied profit theory on empirical

data. Hence, there are an identifiable number of studies which have used some variant

of profit in their investment equations.

2.3.3 Permanent Income Theory

From the preceding paragraphs it is clear that accelerator and accelerator-

cashflow model emphasize on the possibility of rightward shift in the MEC schedule

due to actual and/or expected changes in the output. Further, an increase in the desired

capital stock boosts the level of investment in the economy. However, permanent or

moving average theory of investment proclaims that,

K*t = ���� 2.5

Where ��� is the weighted average of past values of output, i.e. ��� = (1-µ) ∑ µ Yt-1

Hence, the theory stresses on a significant relationship between current capital

expenditures and rate of change in demand over a number of periods in the past. It has

been supported by Birch and Siebert (1976)30 who have concluded that sales

expectations have some role in explaining investment over and above the ones

provided by current and lagged values.

25 Eisner, 1967, op. cit. 26 Eisner, 1978, op. cit. 27 Bagchi, A.K., " Investment by Privately Owned Joint Stock Companies in India", Arthaniti July,

1962 in Sarkar, D., “Capital Formation in Indian Industries: An Empirical Application of Investment Theories,” Economic and Political Weekly, Vol. V(9), 1970

28 Krishnamurthy K., "Private Investment behavior in India: A Macro Time Series Study", Arthaniti, 1964, In: Krishnamurthy, K. and Sastry, D.U., Investment and Financing in the Corporate Sector in India, 1975, Tata McGraw-Hill Publishing Company Ltd, New Delhi.

29 Sarkar, D., “Capital Formation in Indian Industries: An Empirical Application of Investment Theories,” Economic and Political Weekly, Vol. V (9), 1970, pp.M-29 – M-38

30 Birch, M. and Siebert, Calvin D., "Uncertainty, Permanent Demand, and Investment Behavior ", The American Economic Review, Vol. 66, No. 1, Mar., 1976, pp. 15-27

26

2.3.4 Neo-Classical Theory

In addition to the previously specified models where investment was measured as

a function of output, relative cost of capital is also added to this model. Jorgenson

(1963)31 in his neo-classical model of investment describes a process of capital stock

adjustment to an optimal level with emphasis on relative factor costs. He used

marginalist approach where marginal productivity of capital and marginal cost are in

balance and also included depreciation, expected capital value changes and interest

rates into his concept of capital. His model was based on the assumption that

investment by perfectly competitive firms’ takes place without any cost and there is

instantaneous adjustment of optimal capital stock period with that of previous period.

Further he added that the future expectations were unnecessary as the capital stock

adjusted in no time. He asserted that optimal capital stock will be determined at a

point where the value of the firm’s productive activities is maximized i.e. where

marginal productivity of capital, MPK, is equal to the marginal cost of capital. He

titled marginal cost of capital as the ‘user cost of capital’ which included opportunity

cost of investing in real assets, rate of depreciation for the existing capital stock and

capital gains/losses from change in value of capital stock. He derived MPK from

Cobb-Douglas production of the firm:

Y = AKαLβ 2.6

In this equation, Y, K, and L are output, capital and labor respectively. While A is

a constant, α and β represent elasticity of output with respect to capital and labor

respectively. Further,

MPK = dY

= αKα-1Lβ = α Y

dK K

Hence, optimal capital stock would be arrived when

α Y

= C K*

31 Jorgenson, Dale, W., “Capital Theory and Investment Behavior,” American Economic Review,

Vol. 53, May 1963, pp. 247-259

27

C denotes the user cost of capital.

Net Investment (IN) is therefore defined as a function of disequilibrium in capital

stock.

IN = α (Y/C)t - α (Y/C)t-1 2.7

IN = α∆ (Y/C) 2.8

However, this model presumes that capital stock was at optimal level in the

previous period. Jorgenson32 build this premise on various simplifying assumptions

like static expectations, instantaneous capital stock adjustment, no adjustment costs

and completely reversible investment decisions. These assumptions served as weak

links in his model. He also assumed financial neutrality, i.e., sources of finance and

their availability were not significant in investment determination.

Bischoff (1971)33 has analyzed a widely accepted variant of Jorgenson’s neo-

classical model in various articles. These are hybrid models called putty clay. These

models allow that the production processes are like putty in planning stage as well as

in the long run but like clay in the short run. The drift from the neo-classical model

arises from the empirical observations that most modifications in capital output ratio

are relating to new equipment and structures and that existing capital goods are less

frequently modified in response to fluctuations in relative prices of inputs. The

performance of these models has been mixed. Though the evidence usually supported

a response in investment due to output growth but there are varied results ranging

from close to zero to close to one for the magnitude of elasticity of factor substitution.

2.3.5 The Securities Value Model

The preceding sub sections have presented four models as variations to a

single theme of investment being a function of output. The securities value (Q) model

however, attempts to explain investment on a financial basis in terms of portfolio

balance. Such models assert the relationship between investment and ratio of market-

32 Ibid. 33 Bischoff W. Charles, "Business Investment in the 1970s: A Comparison of Models", Brookings

Papers on Economic Activity, 1, 1971, pp: 13-58

28

value to replacement cost (Q). They have been based around the premise that although

investor’s judgments of marginal productivity of capital are unobservable, stock

market valuations may act as a good proxy for marginal benefits of investment.

Broadly speaking, if the market value of a firm exceeds its replacement cost of assets,

it can increase its market value by investing more in fixed capital. Conversely, if

market value of a firm is less than replacement cost of its assets it can increase the

value of shareholders equity by reducing its stock of fixed assets. Hence, stock market

capitalization of firm can be balanced against replacement cost to measure the

incentive to investment.

These models supplement the output based models because both investment

and ratio of market value to replacement cost react similarly to long-run expectations

about future output and process. The Q theories have been developed to encounter the

restrictive assumptions embedded in Jorgenson’s Neo-classical model. He had

assumed instantaneous and costless capital stock adjustment. However, Q theories

introduced the concept of adjustment costs to frame a model in which the rate of

investment is defined over time. External adjustment costs reflect macro economic

factors and internal ones relate to factors affecting an individual firm. Average Q is

defined as the ratio of market value of the firm to current replacement cost of the

firm’s capital stock. Hence,

Q = MV

= Market Value Capitalization

CRC Current replacement cost of the capital stock

This was based on the assumption of efficient capital markets which follows

that the asset prices (here, share prices) fully reflect all available information and

respond instantaneously to new information. Therefore, they serve as a rational

indicator of fundamental value of firms. The empirical problems in adjustment cost

theories surfaced while capturing rational expectations. A number of limitations

encountering this model include serial correlation and mis-measurement of

components of Q. Moreover, the stock markets in India are not efficient in strong

form which renders the measurement of accurate Q very difficult.

Hence, these five basic models of investment highlight the relative importance

of the various factors (output, cashflows, cost of capital, and so on) in shaping up the

29

investment decision. Moreover, they also bring to light the role of a single factor

subject to the exclusion of all other factors as a determinant of investment expenditure.

Certain composite models like accelerator cashflow, Q - cashflow have also been

tested to recognize the complexities and interdependence present in investment

decision making. The early work on investment (Clark, 191734 and others) has

emphasized on accelerator approach. The next theory of investment has stressed that

investment depends primarily on cashflows (internal finance) or more precisely

retained earnings and depreciation. Hence, the discussion on financial constraints on

investment due to limited availability of internal funds becomes the central point for

research. Past profits have also been taken as a proxy for internal funds. Attempts

have been made to bring out the preferred ordering of sources of finance resorted by

the companies facing financial constraints. Meanwhile, Grunfeld (1960)35 proposed

the use of firm’s market value as a proxy for expected profitability. In a way, the

market value approach of Grunfeld could be viewed as a pioneer to Tobin’s Q theory.

This was followed by neoclassical model formulation by Jorgensen and revival of

accelerator approach by Eisner and his associates. Following this was Q-theory of

investment by Brainard and Tobin (1968)36 and Tobin (1969)37 which was in sharp

contrast to the output-oriented models developed earlier in that it attempted to explain

investment on a financial basis in terms of portfolio balance, i.e., based on the ratio of

market value of capital to its replacement cost. Bischoff (1971)38 proposed modified

neoclassical model and indicated that it is often easier to modify factor proportions

and thus the capital-output ratio ex ante; ex post, the substitution between factors is

zero. Consequently, investment may be more responsive to changes in output

compared to changes in cost of capital. As far as the composite models are concerned,

the accelerator-profit (cashflow) model has been used by Eisner (1978)39 and others.

Eisner has taken gross capital expenditure as a function of sales, depreciation and

34 Clark, 1917, op. cit. 35 Grunfeld, 1960, op. cit. 36 Brainard, W.C. and Tobin, J., "Pitfalls in Financial Model Building," American Economic Review,

58(2), 1968, pp 99-122 37 Tobin, J., "A General Equilibrium Approach to Monetary Theory", Journal of Money, Credit and

Banking 1, 1969, 15-29. 38 Bischoff, 1971, op. cit. 39 Eisner, 1978, op. cit.

30

profit. He has argued that rate of expected output should be the primary determinant

of investment which practically translates into a distributed lag function of current and

past changes in sales.

The effectiveness of any model of investment lies in its ability to explain past

data as well as make future predictions. Jorgensen and Siebert (1968)40 have

empirically tested accelerator, neoclassical, liquidity, and market value – at the firm

level and has found neoclassical model to be the best. The results have been based on

a sample of fifteen large manufacturing companies over the period from 1949 to 1963.

However, Elliot’s (1973)41 estimates using the same dataset suggested cashflow

model to be the best for cross-section and accelerator model in time-series data.

Eisner’s studies have consistently indicated the superiority of accelerator and/or

accelerator-cashflow models over neoclassical model in various attempts.

Furthermore, Bischoff’s (1971)42 comparison of various models has found modified

neoclassical model to be the best fit followed by accelerator model. He has used

quarterly data for US economy for the period of 1953-1968. Clark et al (1979)43 has

also compared various models with similar data over 1954-1973 and confirmed

Bischoff’s results. Hence, he has concluded output to be the primary determinant of

non-residential fixed investment in the economy and variables like the rental price of

capital services, interest rate and tax rates have been insignificant as per empirical

findings. The results of Samuel (1996)44 sustain the need for an eclectic approach to

the study of capital expenditure decisions at the firm level. Neoclassical model has

been ranked first as per time-series analysis and cashflow model as per cross-sectional

data. Cashflows have appeared to be the single most important determinant of

investment if cross section results were assumed to be representing the long-run

scenario. 40 Jorgenson, Dale, W. and Siebert, Calvin, D., "A Comparison of Alternative Theories of Corporate

Investment Behavior", American Economic Review, LVIII (4) 1968, pp 681-712. 41 Elliot J. W, "Theories of Corporate Investment Behavior Revisited", American Economic Review,

63, 1973, pp 195-207. 42 Bischoff, 1971, op. cit. 43 Clark, Peter K.; Greenspan, Alan and Goldfeld, Stephan M., “Investment in the 1970s: Theory,

Performance and Prediction” Brookings Papers on Economic Activity, Volume 1979, No. 1, 1979, p.p. 73-124

44 Samuel, Cherian, "The Investment Decision: A Re-examination of Competing Theories using Panel Data", Policy Research Working Paper 1656, Washington, D.C.: The World Bank, Operations Policy Department, Operations Policy Group, Sep., 1996, pp. 1-56

31

Bagchi’s (1962)45 study has been the first major attempt to analyze the factors

affecting investment decisions. He has tested the role of accelerator and profitability

during the period from 1950 to 1960, thereby covering the first two five-year plans.

Profitability has been found to exert a strong influence but not accelerator during the

first plan period. Both the factors have a combined effect in the second plan period.

He suggested taking current profits as a proxy for future profitability. Krishnamurty

and Sastry (1975)46 have analyzed the determinants of fixed investment expenditure

for chemical industry using the data of 40 companies from chemical industry with

accelerator model. The results have indicated that financial variables are significant

and accelerator principle has been evident in selective years. In another work by them

(1975)47, accelerator model has an important influence on fixed investment except in

sugar and cement industries. Although availability of internal and external funds has

been found to be significant, external funds have a greater impact on investment. “On

the whole, accelerator, financial variables and inventory investment were the

significant factors influencing corporate investment.” Rajakumar (2005)48 has

examined the relationship between corporate financing and investment behavior using

Fazzari et al’ (1988)49 model which integrated accelerator, Tobin’s Q and internal

liquidity. He has divided the firms into equity financed and debt financed by

introducing dummy variable for capturing growth of investment. Panel regression

over the period of 1988-89 to 1998-99 has indicated that demand was the most

important factor irrespective of the mode of financing. Tobin’s Q representing

investment opportunities and internal liquidity were found significant for equity

45 Bagchi, 1962, op. cit. 46 Krishnamurthy, K. and Sastry, D.U., “Some Aspects of Corporate Behaviour in India: A Cross-

section Analysis of investment, Dividends and External finance for the Chemical Industry, 1962-70,”1975, In: Krishnamurthy, K. and Sastry, D.U., Investment and Financing in the Corporate Sector in India, 1975, Tata McGraw-Hill Publishing Company Ltd, New Delhi.

47 Krishnamurthy, K. and Sastry, D.U., Investment and Financing in the Corporate Sector in India, 1975, Tata McGraw-Hill Publishing Company Ltd, New Delhi.

48 Rajakumar, Dennis J., "Corporate Financing and Investment Behaviour in India" , Economic and Political Weekly Vol. 40, No. 38, Sep. 17-23, 2005, pp. 4159-4165

49 Fazzari, Steven, Hubbard, R. Glenn and Petersen, Bruce C., “Financing Constraints and Corporate Investment," NBER Working Papers 2387, National Bureau of Economic Research, Inc., September 1988

32

financed firms only. Gangopadhyay, Lensink and Molen (2001)50 have examined the

effect of business group affiliation on corporate investment behavior in India using

standard accelerator cum cash-flow investment model. In their study net investment

scaled by beginning of the period total assets has been explained by sales scaled by

beginning of the period total assets and cashflow scaled by beginning of the period

total assets. Nair (2004)51 has used augmented accelerator model and Bhattacharyya

(2007)52 has attempted to examine the role of accelerator and financial factors,

individually and collectively affecting business fixed investment. The details of these

studies have been provided in the chapter on literature review.

The present study plans to use accelerator- cashflow model as the basic model

of analysis as change in output and internal funds seem to be the most significant

factors in explaining investment as per the foregoing description. Most of the studies

of Indian origin have used accelerator, accelerator cashflow models due to data

availability constraints attached to user cost of capital concept of neoclassical model.

Moreover, markets in India are not efficient enough to reflect the true value of firms

and thereby restrict the usage of Tobin’s Q.

2.4 EXTERNAL SOURCES OF FUNDS

This is the next major decision-making area to be focused by a finance

manager. Business requires money which can either be of the entrepreneur or

borrowed from some other source. As the business expands, owner’s funds (equity)

are not enough and the managers usually resort to borrowed funds (debt). This

introduction of leverage in the capital structure is done by the manager either for the

sheer need of funds or for increasing the profits due to equity holders. This happens

because the tax advantage attached to interest paid on debt leaves greater funds at the

50 Gangopadhyay, S., Lensink, R. and Van, Der, Molen, R., "Business Groups, Financing Constraints

and Investment", CCSO Quarterly Journal, Vol. 3., No. 4, 2001 51 Nair, V.R. Prabhakaran, "Financial Liberalization and Determinants of Investment: An Enquiry

into Indian Private Corporate Manufacturing Sector", 8th Capital Markets Conference, Indian Institute of Capital Markets Paper, December 20, 2004, Available at SSRN: http://ssrn.com/abstract=872268 or http://dx.doi.org/10.2139/ssrn.872268

52 Bhattacharyya, Surajit, "Determinants of Private Corporate Investment: Evidence from Indian Manufacturing Firms', Economic Society of South Africa, Conference, 2007

33

disposal of equity shareholders. An optimum degree of financial leverage depends on

various factors including, size and nature of the firm and/or industry and public

accountability. The capital structure at which the weighted average cost of capital is

minimized, thereby maximizing the firm’s value is called optimal capital structure.

Close to fifty years ago, Modigliani and Miller (1958)53 demonstrated that, in a

perfect market setting, capital structure decision would be irrelevant, as the weighted

average cost of capital would be constant irrespective of the level of gearing. Since

then, an extensive literature has been developed on this issue but the research for a

universally acceptable optimal capital structure is still on.

The following sub-sections discuss the broad observations of theorists. Sub-

section 2.4.1 deals with residual demand theory and sub-section 2.4.2 provide trade-

off theory. The next sub-section 2.4.3 highlight salient features of agency model and

asymmetric information model.

2.4.1 Residual Demand Theory

Flow of internal funds is usually represented by gross retained profits.

Normally, the firms retain a substantial portion of net profit for reinvestment purposes

in their business. The rationale for preferring internal funds over external funds is the

lower cost of internal funds, less risk and no fear of loss of control. Further, trading on

equity produces an expanded stream of income to the shareholders (provided the

number of shares remains constant). However, the availability of internal funds is

limited as the company needs to divide the net profits between dividends and retained

earnings. Dividends, being the income of shareholders cannot be completely sufficed

in order to meet the investment requirements. For a given profit margin and desired

capital-output ratio, firms choose long-run dividend-payout ratio and reaction

coefficients that are compatible with internal financing exclusively. Demand for

external funds arises when the desired increase in assets is more than the available

internal funds. In this sense, the demand for external funds is a residual demand.

53 Modigliani, F. and M. Miller, "The Cost of Capital, Corporation Finance and the Theory of

Investment", American Economic Review 48, 1958, 261-297

34

Hence, the residual demand theory suggests that a company continues with a given

capital structure until the need for additional funds surpasses the internally generated

funds and available free reserves.

2.4.2 Trade-off Theory / Capital Structure Theory

Trade-off theory is based on the assumption that capital structure is optimized

by management by comparing the relative tax advantage of tax-shield benefits of debt

with the increased likelihood of incurring debt related bankruptcy costs. It argues that

debt being a cheaper source of finance (because interest on debt is fixed and tax-

deductible) helps in raising shareholder value but increasingly high levels of debt

moves up the risk of bankruptcy in the event of non-payment of interest. Hence the

management weighs both the alternatives and achieves a trade-off, keeping in mind a

number of factors which are particular to each firm.

2.4.3 Agency Model and Asymmetric Information Model

The other school of thought studies the effect of separation of ownership and

management on capital structure. Two models of management behavior have been

presented which can affect this decision, namely, agency model and asymmetric

information model. Agency models stress that the use of debt finance can reduce

agency costs between managers and shareholders. Firstly, by increasing the manager’s

share of equity and secondly, by reducing the free cash flow available at manager’s

discretion. This model shows the desire of management to ameliorate conflicts of

interest among groups (including managers) with claims to firm’s resources by use of

debt. Till the time a firm is running into profits and it can comfortably meet its debt

service requirements and investment schedule, there is a likelihood of manager’s

consuming perquisites and not investing in activities which will maximize firm’s

value. The managers can capture only a fraction of firm’s gains while bearing the

entire cost if they do not invest in personal-gain enhancing activities. This

inefficiency is reduced when a larger fraction of the firm’s equity is owned by the

manager. Increase in debt ratio increases the manager’s share of equity and mitigate

35

the loss from conflict between the management and the shareholders. Moreover, since

the debt commits the firm to pay out of cash, it reduces the amount of free cash flow

available to managers to engage in self-interest activities. The lessening of conflicts

between managers and shareholders constitutes the benefits of debt financing.

The asymmetric model on the other hand shows the desire of management to

convey information to the capital market. It rests on the assumption of asymmetric

information and heterogeneous expectations between insiders and outsiders. It argues

that investors generally believe that firms will only issue equity when prospects are

poor. As a result, the share prices tend to decline, which makes issuing equity an

extremely expensive way of funding investment project. Hence, if firms finance new

projects by issuing equity, under-pricing may be so severe that new investors gain

more of the net present value (NPV) to the detriment of existing shareholders. This

may lead to an ‘under investment’ problem since such projects will be rejected even if

the net present value (NPV) is positive. This under investment can be reduced by

financing the project using a security that is less likely to be mis-priced by the market.

Internal funds involve no under valuation and even debt that is not too risky will be

preferred to equity. This preference leads the firm to adopt dividend policies that

reflect their anticipated need for investment funds, policies which managers are

reluctant to substantially change. If retained profits exceed investment needs, then

debt can be repaid. If external finance is required, firms tend first to issue the safest

security, debt, and only issue equity as a last resort.

The capital structure designing process starts with the estimation of total funds

required to start a business and is continuously upgraded with the changing need of

funds. The finance executives need to look at all the relative alternatives available

such as raising domestic equity, preference shares, debentures, bonds (short term and

long term), foreign equity, convertible debentures and the like. These options are

broadly divided into owned and borrowed funds and the managers need to find an

optimal mix of debt and equity as per the company’s requirements.

36

2.5 FINANCING OF INVESTMENT (CAPITAL EXPENDITURE)

DECISIONS

The previous sections have built up a platform to bring up a discussion on

investment and financing decisions. The various models of investment theory

highlight the relative importance of various factors as explanatory variables for

defining investment. Moreover, the different sources available with firms’ for raising

funds have also been provided. The aim of this section is to theoretically explain the

importance of various factors as explanatory variables in investment equation. The

propositions laid by Modigliani and Miller (hereafter referred as MM) in their seminal

article of 195854 have proved to be a landmark in the literature of corporate finance.

They showed that a firm’s financial policy was irrelevant for taking investment and

dividend decisions by proving that the market value of the firm depends only on its

profits and is independent of its capital structure. They argued that internal and

external funds are perfect substitutes. This separation of investment and financing

decisions was presented with the underlying assumptions of perfect and symmetric

information.

However, a vast empirical literature supports the model about the hierarchy of

financing which expects that the investment expenditure of some firms may be

constrained by lack of internally generated funds. Various factors like access to

markets, availability of information and transaction costs make internal sources of

finance preferred over external sources for a number of firms. For such firms, the cost

of external capital does indeed seem to exceed the cost of internal funds. Differing

views on the riskiness of investment projects between shareholders and management

and hence on the relevant discount rate may result in good investment projects being

rejected. Myers and Majluf (1984)55 have tagged this as hierarchy of financing -

driven by asymmetric information and/or the real direct and indirect costs of different

sources of financing - the pecking order theory. The firms utilize internal finances for

positive net present value projects in the first instance, subsequently with debt (as the

54 Modigliani and Miller, op. cit. 55 Myers, Stewart. C. and Nicholas S. Majluf, “Corporate Financing and Investment Decisions When

Firms have Information that Investors do not”, Journal of Financial Economics, 13, 1984, pp. 187-221.

37

least risky form of external financing) followed by all kinds of hybrid debt with equity

components and finally with external equity as a last resort.

Accordingly, a positive relation between investment and internal funds may

result from asymmetric information because the lack of internal capital and the ‘high

cost’ of external capital create an underinvestment problem (Goergen and Renneboog,

2000)56. To put it in another way, the positive relation may also be the outcome of an

abundance of retained earnings which makes internal funds too inexpensive (from the

management’s point of view). In certain firms agency costs also impact the relation

between investment and internal funds. In such cases, managers’ interests are not

perfectly aligned with those of the shareholders, (Bernanke and Gertler 198957):

managerial decision-making may be motivated by ‘empire building’ and lead to

overinvestment. In this setting, managers may place a discount on internal funds and

may overspend by undertaking even negative NPV projects as long as there is

excessive liquidity in the firm because managers may derive more private benefits by

increasing their firm’s size (Hart and Moore 1995)58.

The question whether or not the level of investment depends on sources of

finance has drawn substantial attention over the recent decades. The seminal paper of

Fazzari, Hubbard and Petersen (1988)59 rekindled the interest in the determinants of

investments. However, relatively few studies tested the investment-financing relation

in Indian context. Notable Indian contributions include, Krishnamurty and Sastry

(1975)60 , Athey and Laumas (1994)61 , Purohit, Lall and Panda (1994)62 ,

56 Goergen M. and L. Renneboog, "Investment Policy, Internal Financing and Ownership

Concentration in the UK", Centre for Economic Research, November, 2000 57 Bernanke, B. and Gertler, M., "Agency Costs, Net Worth and Business Fluctuations," American

Economic Review, 73, 1989, pp 257 - 276 58 Hart, Oliver, and John Moore, “Debt and Seniority: An Analysis of the Role of Hard Claims in

Constraining Management”, American Economic Review 85 (Issue 3, June), 1995, pp. 567-586 59 Fazzari, Hubbard and Petersen, 1988, op. cit. 60 Krishnamurty and Sastry, 1975, op. cit. 61 Athey and Laumas, 1994, op. cit. 62 Purohit, Badri Narayan; Lall, Gouri Shankar and Panda, Jagannath, Capital Budgeting in India,

Kanishka Publishers Distributors, 1994

38

Gangopadhyay, Lensink and Molen (2001)63, Athukorala and Sen (2002)64, Nair

(2004)65, Bhaduri (2005)66 and Bhattacharyya (2007)67.

2.6 CONCLUSION

This chapter outlines the capital expenditure decision making process

generally used by various companies. Moreover, it also throws light on theories of

investment and various studies related to external sources of funds. The present study

intends to analyze financing of capital expenditures in Indian corporate sector to

understand the relative importance of internal and external sources of finance in

explaining investment equation. The next chapter focuses on literature review of

various researches conducted in India and abroad on this vital topic.

63 Gangopadhyay, Lensink and Molen, 2001, op. cit. 64 Athukorala, P.C. and K. Sen, ''Liberalization and Business Investment in India'', Australian and

East Anglian Universities: Research School of Pacific and Asian Studies Press, 2002 65 Nair, 2004, op. cit. 66 Bhaduri, Saumitra N., "Investment, Financial Constraints and Financial Liberalization: Some

Stylized Facts from a Developing Economy", India, Journal of Asian Economics, Volume 16, Issue 4, August 2005, pp 704-718

67 Bhattacharyya, Surajit, 2007, op. cit.