Embed Size (px)

DESCRIPTION

Â

Citation preview

Electronic copy available at: http://ssrn.com/abstract=2191995

Paper to be presented at the symposium »Insuring against high medical risks from an international historical and social political perspective« in Maastricht on October 26, 2012

FISCAL AND SOCIAL POLICY: FINANCING LONG-TERM CARE IN GERMANY Ralf Götze and Heinz Rothgang

University of Bremen, TranState Research Center, Linzer Str. 9a, D-28359 Bremen (Germany), +49 (0) 421/218-56632, [email protected]

ABSTRACT This paper deals with the coverage of long-term care (LTC) in Germany since the post-war peri-

od. Until the 1990s, long-term care was mainly a task of the family with means-tested, tax-

financed care assistance as a last resort. In 1994, after two decades of political debate, the Ger-

man parliament approved the LTC Insurance Act. This path-breaking reform act introduced a

two-tiered, mandatory long-term care insurance (LTCI) for virtually the entire German popula-

tion. We will capture the genesis of the so-called »fifth pillar« of the social security system from

the initial stage of problem recognition to the agenda-setting period and the decisive implementa-

tion phase. We also shed light on recent reforms of the original LTCI Act. We argue that the

introduction of the LTCI can be explained as an interplay between fiscal and social policy. In

order to mask their financial interests, municipalities and charities acted as advocates for the el-

derly in need of LTC and their families. Summarizing the effects of the LTCI and comparing

them with the initial estimations and targets, we identify unresolved issues and further need for

reform. Even today’s reform debates, however, can be understood as deriving from the tension

between fiscal and social policy, but overshadowed by a revival of ideological debates over pri-

vate vs. public provision.

CONTENTS 1� INTRODUCTION ............................................................................................................................ 2�2� INSTITUTIONS, ACTORS, AND INTERESTS IN GERMAN LTC POLICY ................................... 3�3� THE STONY ROAD TO LONG-TERM CARE INSURANCE IN GERMANY ................................. 5�

3.1� An Uncontested Task of the Family (Until 1974) .................................................................................. 6�

3.2� Recognizing the Long-term Care Problem (1974-83) ............................................................................... 8�

3.3� Setting the Political Agenda (1984-1989) ............................................................................................. 11�

3.4� Finding Consensus in the Decisive Phase (1990-94) .............................................................................. 13�

3.5� Features of the LTCI Act ..................................................................................................................... 16�4� EFFECTS OF THE LTCI ACT ..................................................................................................... 21�5� RECENT DEVELOPMENTS AND UNRESOLVED ISSUES .......................................................... 25�6� CONCLUSION .............................................................................................................................. 29�

Electronic copy available at: http://ssrn.com/abstract=2191995

2

1 INTRODUCTION The following paper1 deals with the coverage of the »new social risk« (Morel 2006: 227), namely

the need for long-term care (LTC)2 in the Federal Republic of Germany3. In legal terms, people

are entitled to benefits if they »are – as a consequence of illness or disability – unable to perform

the activities of daily living independently for an expected period of at least half a year« (§ 14.1

SGB XI, own translation). Though the entitlement is not restricted to the elderly, we nevertheless

focus on LTC for the elderly (i.e. 65 years and older) as it has the highest prevalence in this age

group. We capture changes in the field of LTC policy from the post-war period to the most re-

cent reforms proposals of 2012.

It is important to note that until the 1990s, long-term care was mainly a family task, with

means-tested, tax-financed social assistance as a last resort, particularly in cases of nursing home

care. In 1994, the German parliament approved a bill introducing a two-tiered, mandatory long-

term care insurance scheme (LTCI) for virtually the entire population. Policymakers heralded the

so-called LTCI Act (Pflege-Versicherungsgesetz) as a »comprehensive solution« to the growing long-

term care problem. In a period generally considered an era of austerity, a centre-right government

thus added a new »fifth pillar« to the social security system. In this paper, we argue that the en-

actment can be explained as the result of the interplay between fiscal and social policy. In order

to conceal their financial interests, municipalities and charities acted as advocates for the elderly

in need of LTC and their families. The actual content of the path-breaking reform act, moreover,

is strongly influenced by the veto-ridden institutional setting of the German political system.

State of the art Traditionally in welfare state literature there has not been a strong emphasis on social services in

general or long-term care in particular. While Gøsta Esping-Andersen’s (1990) seminal work

fuelled a rich body of literature focusing on social programmes with cash benefits (e.g. pension,

unemployment, or survivor benefit schemes), social services such as child, health, or long-term

care tended to remain niche topics until the early 2000s. Jens Alber even called LTC the »neglect-

ed dimension« (1995: 277, own translation) of comparative welfare state literature. Since then,

however, a growing interest in new social risks has also shed light on the policy area of LTC.

The number of studies dealing with German LTC policy is thus very limited – this is espe-

cially the case when we turn to English-language publications. The most comprehensive work is

1 We are grateful to the Deutsche Forschungsgemeinschaft for its financial support and to Vicki May for her careful editing. 2 Often used abbreviations: CDU, Christian Democratic Union; CSU, Christian Social Union; FDP, Free Democratic Party;

LTC, long-term care; LTCI, long-term care insurance; SHI, social health insurance; SPD, Social Democratic Party 3 The paper focuses on West Germany until 1990 and on reunited Germany thereafter. Developments within the German

Democratic Republic are neglected. For further reading on the development of East Germany, we recommend volumes 8 to 10 of »Geschichte der Sozialpolitik in Deutschland seit 1945« edited by BMAS and the Bundesarchiv.

3

the dissertation »Der Weg zur Pflegeversicherung« written by Jörg A. Meyer (1996). He captures in

detail the development of the German LTC debate over the 20 years leading up to the enactment

of the LTCI Act from a political-science perspective. In his explanation of the German path to

LTCI he emphasizes the interplay of socio-economic pressures and strong interest groups during

the early stage of the process. In the decisive phase prior to enactment, Meyer’s explanation fo-

cuses more on the political-institutional framework and party politics in a game-theoretical ap-

proach. This combination of socio-economic and actor-centred explanatory factors at different

stages of the LTC debate can also be found in several other studies (Alber and Schölkopf 1999;

Rothgang 1997; Skuban 2004; Strünck 2000). In contrast to this, Ulrike Götting et al. argue

against giving a high weighting to social-demographic factors in a composite explanation:

»The genesis of the long-term care insurance scheme confirms arguments against any socioeconomic perspective in the determination of social policy expansion: social problems which emerge are not quasi-automatically met with state programs serving as functional equivalents to traditional modes of social protection which are no longer effective due to the modernization process« (1994: 305).

Rather, Götting et al. put more emphasis on continuous informal grand coalitions between Chris-

tian and Social Democrats in key social policy issues (such as major pension, unemployment, and

health reforms). This strong tendency towards interparty consensus is fuelled by the veto-ridden

political system of Germany (especially due to strong bicameralism) and explains the path-

dependent design of the new LTC scheme (Götting et al. 1994: 305f).

Structure of this paper This paper is structured as follows. First, we present an outline of the political system in Germa-

ny that is necessary to understand long-term care policy and politics (section 2). In section 3,

which is the main body of our paper, we depict the historical development leading to the intro-

duction of long-term care insurance in Germany. Section 4 deals with the effects of this reform.

In line with our title »Fiscal and Social Policy« we focus on the two main stakeholders: municipal-

ities, and elderly people in need of long-term care. Section 5 then brings us to the recent reforms

addressing some weaknesses of the system, while section 6 concludes the paper.

2 INSTITUTIONS, ACTORS, AND INTERESTS IN GERMAN LTC POLICY For a better understanding of the issue at hand, a basic knowledge of the German political system

is essential. The key political arena for reforms relating to the social risk of LTC is the federal

level, comprising the Parliament (Bundestag), the Council (Bundesrat), and the Government (Bundes-

regierung). While the German constituency elects the members of parliament directly and based on

the principle of proportional representation, the Federal Council represents the governments of

the states (Länder). In general, the Parliament has the superior role as it elects the chancellor, who

4

is the head of government, and has the right to initiate as well as approve legislation. The Council

may initiate drafts, but its approval is only necessary when acts are tangent to Länder rights. The

introduction of a public scheme to cover the LTC risk belongs to those policy fields that need the

approval of both legislative bodies, enhancing the number of veto points.

The main actors within this political system are currently four parties with the potential to

enter a governmental coalition: the Christian Democrats, the Social Democrats, the Liberals, and

the Greens (see Sartori 2005: 108).4 During our observation period the Christian Democratic

Union (CDU) together with its Bavarian sister party, the Christian Social Union (CSU), repre-

sented the mainstream party on the right, emphasizing the primacy of the family in terms of care

activities. With regard to social policy issues the labourite wing of the CDU, the Christlich-

Demokratische Arbeitnehmerschaft, has traditionally played a strong role. Its origin was deeply rooted

in the Catholic social doctrine and it therefore favoured welfare policies supporting the male-

breadwinner model. Its inner-party counterpart was the business wing (Mittelstandsvereinigung),

which holds strong caveats against any form of public spending.

The Social Democratic Party (SPD) represented the mainstream party on the left. While the

SPD favoured more generous social policies, the party also supported the male-breadwinner

model throughout the German economic miracle (until the late 1960s), as »working mothers«

were negatively associated with the demonized German Democratic Republic (Naumann 2005:

51). Due to experiences during the Nazi era, Social Democrats also had much greater reserva-

tions against state interference in family matters than labour parties in France or Northern Eu-

rope (Leitner et al. 2008: 176). In the wake of the protest movements of the late 1960s, the Social

Democrats gradually changed their attitude towards female employment and extramural care and

began to foster policies supporting care activities within families as well as formal care.

With the exception of the legislative period from 1957-1961 no party had an overall majority

in parliament, and until the late 1990s the small Free Democratic Party (FDP) had the role of

kingmaker. This party represented progressive as well as conservative liberalist positions. While

the former were more pronounced up to the early 1980s, the latter became dominant after the

turnaround from the centre-left to the centrist coalition in 1982. Hence, the focus of the Liberals

shifted from egalitarian ideas towards a general reluctance against increased public spending –

with the exception of health expenditure due to strong ties between the medical profession and

the FDP (Rosewitz and Webber 1990: 301).

The fourth and final party with coalition potential during our observation period is the

Green Party (Grüne) founded in 1980. As a political arm of the ecological, peace, and feminist

4 Up to now, the Left Party has not been considered as a potential partner in government by any of the other parties.

5

movement, the Greens initially were a strong left-wing opposition party. During its establishment

as the fourth political power of the Federal Republic, the Green Party gradually lost its strong

leftist notions and filled the niche of a progressive liberal party that had been left open after the

turnaround of the FDP in 1982. From the very beginning, the Greens strongly endorsed female

labour market participation and an expansion of state-sponsored care facilities for children and

the elderly. The Green Party also shared the conservative reluctance against nursing homes but

for different reasons. Rather than large, anonymous care facilities they favoured smaller units that

allowed the residents to mutually help each other, supplemented by professional care in order to

maintain an autonomous lifestyle (Meyer 1996: 295f).

Figure 1: Majorities in the Federal Parliament and the Federal Council

Three minor coalition parties have been neglected as they had vanished from the federal level before LTC entered the political agenda: the German Party (in office: 1949-60), the League of Expellees and Deprived of Rights (1953-56), and the Free People’s Party (1956-57) Own depiction based on www.wahlen-in-deutschland.de

As can be seen in figure 1, the Christian Democrats led most German cabinets throughout our

observation period (1949-1969, 1982-1998, and since 2005). SPD chancellorships are limited to

the Social-Liberal Coalition (1969-1982) and the Red-Green cabinets (1998-2005). The Social

Democrats were also able to influence policies on LTC either at times of so-called Grand Coali-

tions (1966-1969 and 2005-2009) with a CDU chancellor or when a CDU-led government lacked

a majority in the Federal Council (1949-1961, 1991-1998, and in the period since 2010).

3 THE STONY ROAD TO LONG-TERM CARE INSURANCE IN GERMANY The following section deals with the German LTC policy from the post-war period to the intro-

duction of the LTCI Act in 1994. As we analyse changes over a rather long observation period of

more than 40 years, we shall break it down into smaller periods. To set the stage, we first address

the period of development up to 1974 (section 3.1). During this era, often characterized as the

»golden age« of the welfare state, LTC was not affected by welfare state expansion and therefore

remained a private risk for families. In 1974, the reform debate, which led ultimately, after 20

years, to the introduction of LTCI, was triggered by the report of a think tank for the elderly.

Following a rough concept used by several scholars (Rothgang 1997; Skuban 2004), we distin-

CDU FDP

CDU

1949 1957 1961 1966 1969 1982 1990 1998 2005 2009

CDUFDP

CDU SPD

SPDFDP

CDUFDP

CDUFDP

SPD Grüne

CDUSPD

CDUFDP

1949 1957 1961 1966 1969 1982 1990 1998 2005 2009

Federal Parliament (governmental coalitions) Federal Council (white: government holds majority; black: opposition can veto)

6

guish three stages of the policy cycle: problem definition, agenda-setting, and decision making.

The problem definition phase can be dated from the publication of the aforementioned report in

1974 to the presentation, in 1983, of a Joint Proposal by municipalities and charity organizations,

representing powerful stakeholders in the field (section 3.2). The issue then shifted to the decisive

political sphere at federal level, marking the third, agenda-setting phase from 1984 to 1990 (sec-

tion 3.3). During this phase, several alternatives for dealing with the LTC issue competed for

acknowledgment. The fourth, decisive, phase began with Minister Blüm’s proposal for a »social

insurance« solution in 1990, followed by several attempts to secure a political majority and, final-

ly, its enactment in 1994 (section 3.4). The result of this process, i.e. the LTCI Act, is finally de-

scribed in section 3.5.

3.1 An Uncontested Task of the Family (Until 1974) Even at the zenith of the golden age of the welfare state (from 1945 to 1974), West German poli-

cymakers considered long-term care for the elderly a private risk. There was no comprehensive

public system5 to cover the risk of long-term care. In line with the conservative tradition of the

Bismarckian welfare state, caring activities for children as well as old people belonged to the

realm of the family (Morel 2007; Orloff 1996; Pfau-Effinger 2005). As the structure of the taxa-

tion and social security systems favoured male-breadwinner households6, this practically meant

that wives, daughters, and daughters-in-law were expected to provide unpaid LTC at home. The

Christian Democrats, who led various cabinets between 1949 and 1969, strongly supported this

female-caregiver concept. In his first government policy statement on September 20, 1949, Chan-

cellor Konrad Adenauer announced: »As a result of the war, we face a surplus of women. […]

Hence, we have to offer these inevitably single women new occupational opportunities« (Beyme

1979: 65, own translation). In other words, female employment was a symptom of shaken rather

than stable societies. In line with this, Franz-Josef Wuermeling (CDU), Minister of Family Af-

fairs, stated as a policy guideline for his newly founded department in 1953:

»The state cannot and should not take over the burden of family life, but relieve it to some extent. We would also like young married women to take care of their households and raise children, but we cannot arbitrarily prevent them from going into paid employment. We have to find ways of bringing wives from the factories and offices back into their families.« (Der Spiegel 1953: 8, own translation)

5 Apart from social assistance as the safety net of last resort, only minor sections of the population, e.g. civil servants, war

invalids, or accident victims, were entitled to LTC coverage by special public schemes. Moreover, the Länder Berlin, Bremen, and Rhineland-Palatinate had already introduced LTC benefits without means-testing (Roth and Rothgang 2001: 292).

6 Among the measures reinforcing the male-breadwinner model were tax splitting for married couples, the free co-insurance of spouses under social health insurance, and widows' pensions. Up until the first reform of family law in 1977, married women even needed their husbands’ approval to sign an employment contract. Even then, the opening hours at German kindergar-tens and schools often only made part-time work possible (Fagnani 2012).

7

The wording changed when Willy Brandt became the first Social-Democratic Chancellor of the

Federal Republic of Germany. In his government policy statement on October 28, 1969, he em-

phasized: »We will […] support women in fulfilling their equal role in the family, occupation,

politics, and society« (Beyme 1979: 272, own translation). In practical terms, the social-liberal

coalitions led by Brandt made no serious attempts to change the aforementioned incentives fa-

vouring the traditional gender roles.

If families were not able to cope with providing care, their respective municipalities took

over, reflecting the deeply rooted principle of subsidiarity in German social policy (Alber and

Schölkopf 1999: 133). Due to the »conditional priority« of the non-profit sector, local govern-

ments had to contract charity organizations first. Only if they were unable to fulfil this task were

municipalities allowed to operate their own LTC facilities or contract for-profit providers

(Backhaus-Maul and Olk 1994). For this reason, nursing homes were mostly owned by charities

organized under six umbrella associations. They reflected the different ideological strands of

German society and included the catholic Caritas, the protestant Diakonie, the Jewish ZWST, the

social-democratic Arbeiterwohlfahrt (AWO), the conservative Deutsches Rotes Kreuz, and the neutral

Der Paritätische (Strünck 2000: 29ff). As costs for residency in LTC facilities mostly exceeded indi-

vidual pensions, most needy elderly had to apply for »Hilfe zur Pflege« (care assistance) under the

Federal Social Assistance Act (Bundessozialhilfegesetz), which was financed by the municipalities7.

This measure was highly stigmatized, as benefits were means-tested and included the relinquish-

ment of all assets and recourse to family members (Götting et al. 1994: 288).8

Figure 2: Family capacity for long-term care with traditional gender roles in West Germany 1950 1960 1970 1980Women aged 45 to 69 7,897,800 9,142,000 9,778,000 9,251,100Population above the age of 70 2,851,000 3,460,000 4,827,500 6,938,000Capacity quotient 2.770 2.642 2.025 1.333Source: Alber and Schölkopf (1999: 304)

This concept of LTC as a responsibility of female care-givers, with municipalities and charities as

providers of last resort, was increasingly challenged by socio-economic circumstances. First of all,

the capacity of families to provide sufficient care for the elderly in context of the traditional gen-

der role already started to erode in the 1960s. This capacity has often been measured by the ratio

of women between the age of 45 and 69 to overall population aged 70 and over. Although this is

7 The financial responsibility for care assistance differed between Länder. The municipalities either had to bear the cost of

social assistance payments directly or finance commissioned regional social assistance authorities (überörtliche Sozialhilfeträger). 8 In terms of social assistance it is important to distinguish between recipients on account of low income (Hilfe zum Lebensun-

terhalt) and recipients on account of LTC (Hilfe zur Pflege). As recipients of social assistance were stigmatized (Evers 1998: 7), the fallback on Hilfe zur Pflege after a normal working life was regarded as an abnormality of the German welfare state.

8

a rather rough indicator, as it neglects increases in healthy life expectancy as well as developments

in the composition of households, it offers an initial indication of the potential burden of female

care-givers. Compared to other OECD countries, Germany traditionally had a high capacity to

provide long-term care for the elderly within the family owing to the low labour market participa-

tion of married women (Rückert 1989: 122). Between 1960 and 1980, however, this capacity ratio

halved, or – in other words – the potential burden for female care-givers doubled (see figure 2).

Secondly, the long-term projections for the capacity ratio were even worse, as the number of

births had dropped dramatically since the mid-1960s. Since that time, the fertility rate has re-

mained constant at a non-sustainable level, whereas further life expectancy of the elderly grew

steadily. While the Federal Republic witnessed an all-time record of 1.07 million births in 1964

– on the eve of the introduction of the contraceptive pill on the German market – the annual

number of births dropped to 626,000 within a decade (Statistisches Bundesamt 2012). This had a

twofold effect: on the one hand a decreasing number of births directly reduced the potential

number of future females providing long-term care for the baby-boom generation. On the other

hand, women could now decide whether to have children and when, which improved their

chances of staying in or returning to employment. The latter became even more relevant when

the economic crisis of 1974 put an end to the era of full (male) employment and there was a

greater necessity to pool the employment risk between both partners.

As a consequence, the growing demand for long-term care was confronted with a drop in

the number of women exclusively dedicated to informal care activities, and the number of nurs-

ing home residents increased, as did the social assistance payments by the municipalities. In fiscal

terms, this meant an increasing burden on local budgets that was totally beyond the influence of

the municipalities. Although at the end of the day they had to cover the costs, all entitlements

were legislated at federal level. In social policy terms the outcome was a disaster for nursing

home residents: almost all assets were lost and their original pensions, conceived as an acknowl-

edgment of an entire working life record, dwindled to pocket money value.

3.2 Recognizing the Long-term Care Problem (1974-83) The first attempt to increase public awareness of the social risk of long-term care was made by

Peter Galperin, State Secretary of Bremen, with a memorandum in a journal of the powerful cor-

poratist actor, the German Association for Public and Private Welfare (Deutscher Verein für öffen-

tliche und private Fürsorge). He called attention to the widening gap between the moderate growth of

pensions and the soaring costs of social services – especially in LTC facilities. In order to avoid

an increasing number of elderly people having to take recourse to social assistance, Galperin pro-

posed the introduction of a universal social nursing home insurance (1973: 147). While Galperin’s

memorandum was addressed to a small but informed audience, the public debate was triggered in

9

1974 by a report by the German Foundation for the Care of Older People (Kuratorium Deutsche

Altershilfe, KDA) – a think tank for the improvement of living conditions for the elderly, founded

by the presidential couple Heinrich and Wilhelmine Lübke. The foreword to the report put the

entire problem in a nutshell:

»A 70-year-old man, health insured, retired, has a stroke. He is hospitalized at a university clinic and re-ceives state-of-the-art medical treatment. His sickness fund pays everything. His pension stays the same. His assets remain untouched – his family remains unaffected. […] He moves to a nursing home and stays there for the rest of his life. The sickness fund pays nothing. His pension does not cover the costs for residential care. He becomes a social assistance recipient. His assets are sold. His family members face having to cover a large part of the costs themselves« (KDA 1974: 3, own translation).

The KDA criticized the arbitrary distinction between »cure« and »care«. Every sickness resulted in

a certain need for care, and, put the other way round: »No one dies of old age, all elderly people

die from a certain illness« (KDA 1974: 7, own translation). The boundary drawn between medical

treatment and long-term care was only based on different institutional settings rather than on

objective criteria. The report concludes that care activities in nursing-homes fall within the scope

of social health insurance (SHI), as long as the staff is supervised by medical professionals (KDA

1974: 23ff).

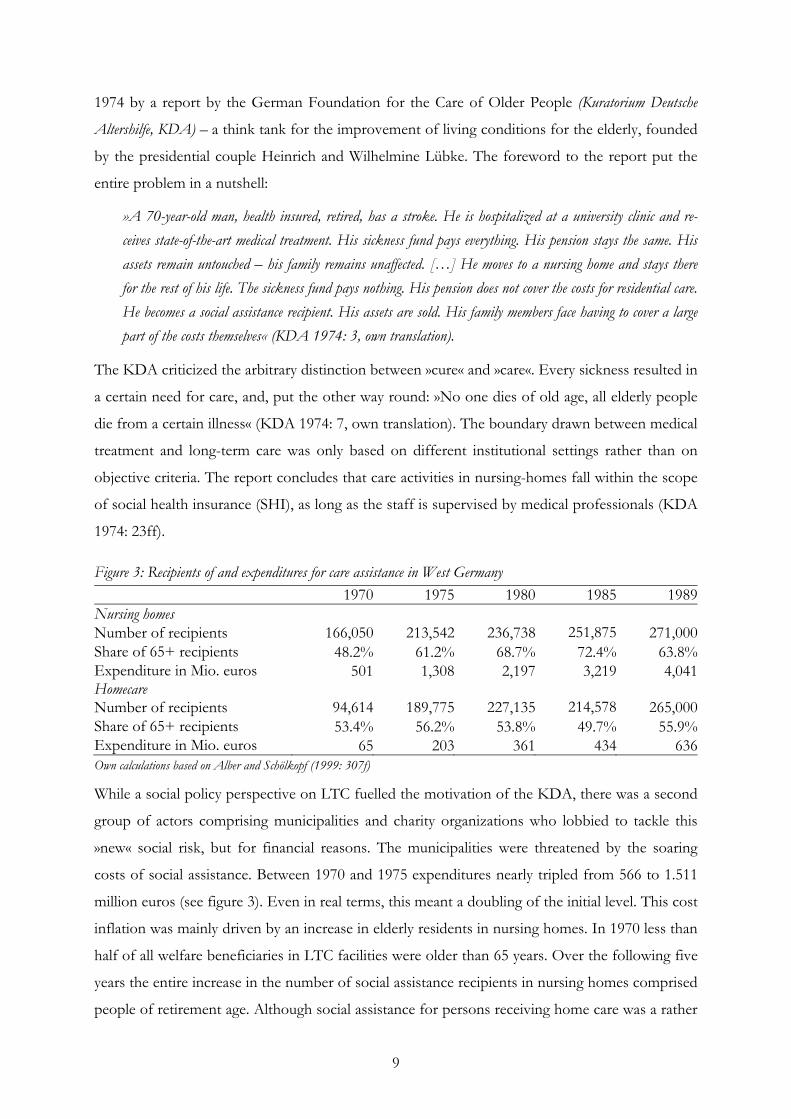

Figure 3: Recipients of and expenditures for care assistance in West Germany 1970 1975 1980 1985 1989Nursing homes Number of recipients 166,050 213,542 236,738 251,875 271,000Share of 65+ recipients 48.2% 61.2% 68.7% 72.4% 63.8%Expenditure in Mio. euros 501 1,308 2,197 3,219 4,041Homecare Number of recipients 94,614 189,775 227,135 214,578 265,000Share of 65+ recipients 53.4% 56.2% 53.8% 49.7% 55.9%Expenditure in Mio. euros 65 203 361 434 636Own calculations based on Alber and Schölkopf (1999: 307f)

While a social policy perspective on LTC fuelled the motivation of the KDA, there was a second

group of actors comprising municipalities and charity organizations who lobbied to tackle this

»new« social risk, but for financial reasons. The municipalities were threatened by the soaring

costs of social assistance. Between 1970 and 1975 expenditures nearly tripled from 566 to 1.511

million euros (see figure 3). Even in real terms, this meant a doubling of the initial level. This cost

inflation was mainly driven by an increase in elderly residents in nursing homes. In 1970 less than

half of all welfare beneficiaries in LTC facilities were older than 65 years. Over the following five

years the entire increase in the number of social assistance recipients in nursing homes comprised

people of retirement age. Although social assistance for persons receiving home care was a rather

10

minor item in local budgets in 1970, it began to burgeon and within five years the number of

beneficiaries had doubled and costs tripled. The rapid increase in elderly social assistance recipi-

ents continued over the subsequent years, making it harder for municipalities to make ends meet,

especially against the background of an economic downturn. They therefore had a strong self-

interest in shifting this financial burden onto social insurance or the federal level.

The charities also favoured shifting the financial burden to a larger risk pool for two main

reasons. Firstly, they feared that local governments might put pressure on them to cut costs and

economize on LTC services. Secondly, municipalities might even lobby against the principle of

»conditional priority«, which safeguarded the quasi-monopolistic power of non-profit organiza-

tions in residential care provision (Rothgang 1997: 13f). Municipalities and charity organizations

masked their contradicting self-interests in the public debate with the social policy argument,

which advocated shifting the risk of LTC to a larger risk pool. Their ostensible objective helped

to bridge their antagonistic interests (Rothgang 1997: 14). Remarkably, despite soaring social as-

sistance costs, cost-containment in LTC did not enter the political agenda in the mid-1970s. This

is even more striking as at the same time the Christian Democratic opposition criticized the

»cost-explosion« in healthcare (see Braun et al. 1998: Chapter 2). Hence, two relevant actors ad-

vocated the concerns of a relatively powerless target group – elderly people in need of care.

In line with this concern, the AWO put the next proposal forward in 1976. Although the

charity organization, which has strong ties to the governing Social Democratic Party, welcomed

the KDA initiative, it underpinned a crucial drawback to the initial concept. If the SHI covered

all nursing-home costs, elderly residents of LTC facilities would have an inappropriate advantage

over healthy retirees who had to pay their rent and sustenance themselves. As an ad-hoc measure,

the AWO (1976: 157) therefore proposed splitting nursing-home costs into three categories:

1. board and lodging, to be paid by the resident, (their dependents, or social assistance),

2. care activities, to be paid by the social health insurance, and

3. social activities, to be paid by the social assistance authorities.

For the long run, the AWO proposed extending the SHI benefit package to cover ambulatory

and institutionalized long-term care. The charity organizations emphasized in this context the

advantage of a single financing source for cure and care to ensure that elderly would get the ap-

propriate services (home, day, hospital, or residential care) according to their needs (AWO 1976:

159). This idea was taken up with considerable interest in the subsequent years. In February 1979,

the German Association of Cities (Deutscher Städtetag) decided to support the AWO proposal.

Despite growing support for this proposal, the Federal Government refrained from setting a

political agenda. Instead, the Ministry for Youth, Family, and Health commissioned a survey

which, published in 1980, offered the first reliable statistics on home care. For the first time, the

11

study made visible the growing burden of long-term care and the shrinking capacity of private

households to cope with it (Socialdata 1980). In the same year a commission of the Federal Gov-

ernment and the Länder elaborated advantages and drawbacks of different concepts addressing

the LTC issue (Meyer 1996: 158f). Their brainstorming led to three competing solutions:

1. extension of the SHI benefit package to cover LTC services,

2. introduction of a social LTCI administered by the sickness funds, and

3. implementation of a LTC law financed by the federal state and the Länder.

On the one hand, the report indicated that the federal level had finally started to recognize the

LTC problem. On the other hand, its open results showed that the relevant policymakers were

not sufficiently interested in tackling it (Meyer 1996: 159). Other actors, by contrast, supported

the idea of a clear proposal. In 1983, this process culminated in a Joint Proposal by three federal

associations representing the municipalities, regional social assistance authorities, and charities as

well as both think tanks Deutscher Verein and KDA. The memorandum also favoured the trisec-

tion idea under the implicit assumption that the municipalities would also cover the investment

costs. Moreover, it proposed the introduction of a social LTCI under the umbrella of the SHI to

finance eldercare (Rothgang 1997: 15). Thus, the Joint Proposal represented exactly the solution

chosen when the LTCI Act was passed eleven years later.

3.3 Setting the Political Agenda (1984-1989) The Joint Proposal pushed the LTC issue to the decisive political arena at federal level. While

most policymakers concurred that there was a problem, there was little consensus as to the right

solution. As the latter would greatly affect the fiscal interdependency between local, regional, and

federal governments, the focus of the discussion shifted in this agenda-setting phase from social

to fiscal policy (Rothgang 1997: 16). As neither the federal state nor the sickness funds were will-

ing to cover costs in order to relieve the municipalities, the reform impetus generated by the Joint

Proposal only lasted a year. In 1984, the Christian-liberal coalition announced that for financial

reasons it would not attempt an extensive LTC reform. As a counter-reaction the Länder took

over the initiative. Within a few weeks, three regional governments drafted competing proposals

to the Federal Council with divergent suggestions both for the kinds of benefits and funding:

1. Hesse (SPD/Grüne) suggested introducing a social LTCI for the entire population funded

by contributions and a Federal subsidy of 30 per cent (BR-Drs. 81/86),

2. Rhineland-Palatinate (CDU) advocated a general LTC allowance paid by the Federal

government (BR-Drs. 137/86), and

3. Bavaria (CSU) put forward a LTC allowance for severe cases as part of the SHI benefit

package financed by contributions and a Federal subsidy (BR-Drs. 138/86).

12

Although the far-left Hessian government made the most comprehensive attempt to tackle the

LTC problem, the other Länder led by Social Democrats supported the Bavarian draft in order to

increase the chances of swift implementation. As a result, the so-called minimal consensus was

approved by the Federal Council and thus brought up for parliamentary discussion with strong

backing (BT-Drs. 10/6135). In addition, the Green Party also presented a draft (BT-Drs.

10/2609) to the Federal Parliament which included tax-financed, universal LTC coverage. The

federal government responded to these legislative initiatives with a draft of their own (BT-Drs.

10/6134). It adopted the idea of extending the SHI benefit package to cover severe LTC cases.

In contrast to the minimal consensus, however, this only included homecare services. This

amendment had a tremendous impact on eligibility and expenses, as most severe cases were treat-

ed in nursing homes. While the minimal consensus of the Länder needed a federal subsidy of

around 1.8 billion euros, the draft put forward by the government only estimated additional fed-

eral expenses of around 50 million euros. In the end, neither of these proposals passed parlia-

ment before the end of the legislative term. The elections of 1987 confirmed the Christian-liberal

government. The Länder refrained from launching an initiative in the Federal Council, as the new

coalition treaty already included the commitment to tackle the still unresolved problem of LTC.

»The coalition parties aim to establish social protection for long-term care. Ambulatory and homecare take priority over inpatient care. As part of a fiscal reform, tax deductions are scheduled to support homecare« (CDU, CSU, and FDP 1987: 13, own translation).

Although the treaty did not specify what kind of cover would be introduced, the CSU, FDP, and

the business wing of the CDU stressed that it would not be a social LTCI (Perschke-Hartmann

1994: 130). In the following year, the Health Reform Act passed parliament including an exten-

sion of SHI benefits to severe LTC services provided at home. This can be considered a result of

a package deal within the coalition. The left-wing of the CDU originally opposed cutbacks in

healthcare, but in the end accepted them in exchange for new LTC benefits. Hence, the govern-

ment traded the SHI extension to LTC services for support for the entire reform package (Alber

and Schölkopf 1999: 130f; Perschke-Hartmann 1994: 131). While the benefits were more gener-

ous than in the prior draft, the limitation to home care remained, narrowing down eligibility. This

reflected the deep concerns of Christian Democrats over state subsidies for LTC within facilities,

as they suspected this would cause a drag towards nursing homes. In addition, the association of

private insurers, the German Medical Association, and even the sickness funds of white-collar

workers lobbied successfully against a more comprehensive solution, evoking the image of a

state-sponsored deportation of elderly people to nursing homes (Dieck 1992: 57). Although the

Healthcare Reform Act only addressed a minor target group, this measure meant the first finan-

cial support for elderly people in need of LTC and their families at the federal level.

13

3.4 Finding Consensus in the Decisive Phase (1990-94) As a step towards resolving the growing LTC problem, the Health Reform Act was a drop in the

ocean right from the beginning. There was still a need for a comprehensive solution. An attempt

by the major CDU stronghold Baden-Wurttemberg to put compulsory private LTCI for people

over 45 years on the agenda failed as the idea gained attention but no interest (Meyer 1996: 163).

The starting point of the decisive phase was a speech by Norbert Blüm, Minister for Labour and

Social Affairs. At the annual general meeting of the sickness funds for white-collar workers on 26

September 1990, he surprisingly announced:

»The next issue on the social policy agenda is long-term care. In the future we will no longer need just four, but five pillars in the social security system. Besides the existing social insurances for casualties, sickness, re-tirement, and unemployment, the fifth pillar must insure the risk of long-term care dependency« (BMAS 1990: own translation).

This was clearly quite contrary to Blüm’s statements of the mid-1980s, when he fiercely sup-

pressed all discussion over a social LTCI (Meyer 1996: 164). At that time he had opposed the idea

of state incentives to put elderly into nursing homes. Years later, Blüm explained his change of

opinion with the rapid erosion of the traditional family model with three generations living under

one roof (Wasem et al. 2007: 702). In his speech, he went on to present an eight-point plan

(BMAS 1990: 19ff) for a »comprehensive solution« to the LTC problem including:

1. support for people in need of LTC, irrespective their grounds or their age,

2. home-care must have first priority,

3. a balance between benefits in cash and benefits in kind,

4. beneficiaries have to pay a reasonable share themselves,

5. one authority must have clear responsibility for the organization of financial assistance,

6. sickness funds are the preferred authority to fulfil this task,

7. organizer does not mean financier; the financial burden should be shared between the

federal level, the social security system and municipalities, and finally

8. proposed entitlements and their financial coverage must complement each other.

Although Blüm refrained from using the term »social insurance for long-term care«, the direction

of his speech was obvious. Otto Graf Lambsdorff (1990: 1), leader of the FDP, harshly criticized

the ideas of their coalition partner as »Traumtänzerei« (wool-gathering). Even within Blüm’s own

party his move was not uncontested. This can be seen in the coalition treaty after the first federal

election in reunified Germany on December 2, 1990, that confirmed the Christian-liberal gov-

ernment. The CDU, CSU, and FDP agreed that »the Federal Government will submit a draft bill

for the coverage of long-term care to the Federal Parliament by June 1, 1992« (1991: 41, own

translation). The coalition parties cautiously used the generic term »Absicherung« (coverage) rather

14

than »Versicherung« (insurance) in order to leave enough scope for the final design. Hence, they

only agreed on what the new scheme should not look like (Jung and Schweitzer 1995: 51).

Only two days after the appointment of Chancellor Helmut Kohl’s fourth cabinet on January

18, 1991, the result of the Hessian state election put an end to the coalition majority in the Feder-

al Council. The government now needed the support of SPD-led Länder for the LTC act to suc-

ceed. In his subsequent government policy statement on January 30, 1991, Chancellor Kohl em-

phasized one word for the proposed solution to the LTC problem: »consensus« (BT-P. 12/5:

83A). Against the background of their newly won influence on federal policy, the Social Demo-

crats, who had toyed with the idea of a tax-financed LTC system in the late 1980s, switched their

opinion in favour of a universal social insurance. In a memorandum published on February 15,

1991, the SPD justified this swing with the enormous burden of German reunification, which left

no scope for LTC coverage through the federal budget (Götting et al. 1994: 294). On the same

day, the FDP announced its rejection of a social insurance for LTC in favour of a private solu-

tion. This approach had already won the support of the business wing of the Christian Demo-

crats (Rothgang 1997: 19; Wasem et al. 2007: 704).

Minister Blüm then put state secretary Karl Jung in charge of drawing up the draft for this

highly controversial issue. In August that year, Jung invited 86 associations to a major LTC con-

gress in Bonn. The vast majority of stakeholders preferred a social insurance for long-term care

on a pay-as-you-go (PAYG) basis, while a minority representing private insurance companies and

the employers’ associations opted for private LTCI based on the funding principle (Meyer 1996:

313). Given the strong backing of the corporate actors, Blüm pushed forward for a fundamental

decision by the Christian Democrats over the LTC roadmap. On September 30, 1991, after a

controversial debate, the federal committee of the CDU announced it would proceed with a so-

cial insurance concept for long-term care based on the PAYG principle (Wasem et al. 2007: 704).

Although at first glance this appeared to be a flawless victory on the part of the Labourites, the

business wing added three important restrictions: the social LTCI should only provide basic ra-

ther than comprehensive coverage, the scheme may not increase the financial burden of employ-

ers, and the contribution rate may not exceed 1.5 percentage points.

While the fundamental decision partly appeased the discussion within the CDU/CSU frac-

tion, it intensified the conflict within the governmental coalition. In October 1991, the Free

Democrats confirmed their commitment to a (compulsory) private LTCI based on the funding

principle. Minister Blüm now had to cut the Gordian knot within the eight remaining months

before the deadline set out in the coalition treaty. He mastered this task with the strategic use of

compromises and threats. First of all, he continuously argued that the Social Democrats, who

controlled the Federal Council, would only accept a social insurance. Secondly, he emphasized

15

the advantages of the reform for the elderly and their families, giving rise to enormous public

expectations forcing the government to succeed. Thirdly, in line with the healthcare system, the

new LTC scheme would become a two-tiered system with a social and substitutive private insur-

ance. Fourthly, Blüm hinted that any additional burden for employers would be compensated.

On June 30, 1992, the coalition parties agreed to introduce a social insurance for long-term

care. The FDP was no longer able to uphold their veto, given a series of defeats in state elections

and the threat of an informal Grand Coalition that had already out-manoeuvred the Liberals in

the field of health policy (Götting et al. 1994: 299; Wasem et al. 2007: 705). The contribution rate

was set at a maximum of 1.7 per cent of income, shared equally between employers and employ-

ees. As a compensation for the employer’s share, the coalition agreed that businesses would no

longer have to pay for the initial day of sick leave (Meyer 1996: 166f). This caused uproar among

the SPD and the trade unions, as it constituted an attack on a key achievement of the labour

movement. Both declared they would block the entire reform package if it included unpaid sick

leave. The Social Democrats threatened with a veto in the Federal Council, while the unions pre-

pared to appeal to the Constitutional Court, as this measure affected existing work contracts and

therefore violated the autonomy of collective bargaining (article 9.3 GG). As even the FDP

acknowledged the latter point, and the labourite wing of the CDU also disliked the deal, Minister

Blüm had to find another way of compensating employers (Götting et al. 1994: 300).

The second promising idea9 was to use public holidays as compensation, either directly by

abolishing them or indirectly by reducing their replacement ratio. The Achilles Heel of the direct

concept was that the federal level could only decide over one nationwide public holiday, namely

Reunification Day. This was unthinkable even for conservative politicians. This left only religious

holidays10, New Year’s Day, and Labour Day, all of which fell under the competences of the Län-

der. The prospect of 16 in all likelihood negative decisions at state level rendered the indirect

concept more attractive. On September 27, 1993, the cabinet finally agreed to reduce the re-

placement ratio for ten common public holidays to 80 per cent (Jung and Schweitzer 1995: 53).

Hence, the coalition finally reached a consensus. Four weeks later, the initial draft (BT-Drs.

12/5617) of the LTCI Act passed the Parliament, backed by CDU/CSU and FDP.

The legislative process came to a halt soon after this initial step when the SPD-governed

Länder rejected the reform package and the draft found no majority in the Federal Council on

November 5, 1993. Moreover, the Council demanded a mediation committee in order to find a

compromise between coalition parties and the Social Democrats. This marked the beginning of 9 The Ministry of Labour and Social Affairs considered a vast number of (short-lived) concepts for compensating employers,

filling 13 volumes in the Federal Archive (Wasem et al. 2007: 706). 10 Due to their distinct protestant or catholic traditions, the number of religious holidays differed among the Länder, ranging

from seven in the Free Hanseatic City of Bremen to eleven in the Free State of Bavaria.

16

the crucial phase, as any concession to the SPD might break the fragile consensus between the

CDU and FDP (Wasem et al. 2007: 708). At the initial meeting of the mediation committee, the

representatives of the Council stipulated several revisions. One of them concerned investment

costs for LTC facilities. The Länder rejected a monistic funding scheme, i.e. operational and in-

vestment financing from one source, and insisted on retaining a dual financing system analogous

to the hospital sector, in which the Länder would be responsible for investment costs, while op-

erational costs would be covered by other sources. In addition, the Social Democrats also de-

manded significantly higher benefits – especially if provided in kind. Finally, the Länder also ad-

vocated maintaining the »conditional priority« of charities, whereas the LTCI Act included the

equal treatment of non- and for-profit providers. The coalition rejected the latter revision but

agreed to various other points, including dualistic funding and increases for several benefits in

kind by about 20 per cent (Jung and Schweitzer 1995: 55ff; Meyer 1996: 358ff).

The revised draft passed parliament on December 10, 1993; again, however, the Council ve-

toed it a couple of days later and appealed to the mediation committee for the second time. The

reason was less the content of the LTCI Act than the compensation for employers. The Social

Democrats claimed that the reduction of the replacement ratio for ten common public holidays,

which in monetary terms meant abolishing two of them, was inacceptable. They hinted that they

would accept the abolition of one public holiday only (Götting et al. 1994: 301). At this point, the

FDP lost its patience. High-ranking party officials doubted that the estimated compensation

would be high enough for employers and demanded an external expertise (Wasem et al. 2007:

709). The Council of Economic Advisors finally made the Solomonic statement that the abolition

of one holiday would be not enough but two would be too much (BT-Drs. 13/3016: 282). In the

end the mediation committee agreed to cancel one holiday, namely Penance Day (Buß- und Bettag).

With the exception of the Free State of Saxony11, all federal states abolished this holiday. The

final version of the LTCI Act passed through parliament with the support of the CDU/CSU,

FDP, and SPD on April 22, 1994. One week later, the Council also accepted the bill. The idea of

a »fifth pillar« within the German social security system had become reality.

3.5 Features of the LTCI Act The LTCI Act was an omnibus bill, establishing the content of the new Social Code Book XI

(Sozialgesetzbuch – Elftes Buch, SGB XI) which became effective on January 1, 1995. It introduced

the regulatory framework for a two-tiered LTCI. In accordance with the principle of aligning

LTC insurance with health insurance (Naegele and Reichert 2002: 124), sickness fund members

11 The Premier of Saxony, Kurt Biedenkopf (CDU), already announced in October 1993 that he would not accept an indirect

compensation for employers. Instead, employees should directly pay the entire contribution (Wasem et al. 2007: 707).

17

were automatically enrolled in the social LTCI (§ 20 SGB XI). Those with private health plans

were obliged to buy private LTCI (§ 23 SGB XI). Right from the beginning, both schemes to-

gether covered almost12 the entire population, since every citizen is legally bound to have a social

or private health insurance, and consequently since 2009 every citizen must also have LTC cover-

age. In contrast to healthcare, LTCI was designed as a partial coverage, as all benefits are capped

(Evers 1998: 8). Therefore, private co-payments remain important, and means-tested social assis-

tance still plays a vital role, especially in residential care. Finally, policymakers removed services

for severe long-term homecare patients from the SHI benefit package, as such cases were hence-

forth covered by the LTCI (Mager 1999: 208).

Entitlement and benefits Since its introduction, eligibility has been independent of the age of the person in need of care.

However, more than 80 per cent of all beneficiaries are aged 65 years or older. In legal terms, the

»need for long-term care« refers to those people who need help to perform their activities of daily

living (ADL) due to physical or mental illness or disability for an expected period of at least half a

year (§ 14.1 SGB XI). The paragraph also defines four ADL groups.

x Hygiene: to wash, shower, bath, shave, brush teeth, comb hair, and use the toilet

x Diet: to prepare and eat food

x Mobility: to leave or enter bed, (un)dress, walk, stand, climb stairs, leave home, and return

x Housekeeping: to shop, cook, tidy up, washing-up, do the laundry, and heat the rooms

The benefits are laid down by law and organized into three dependency levels according to the

need for care. Persons requiring help in at least two basic ADLs (hygiene, diet, or mobility) and

additional housekeeping assistance more than once a week qualify for the lowest benefit level. If

a patient needs help for the basic ADLs at least three different times a day, they receive the sec-

ond level. The third level of benefits addresses the most severe cases, where help must be availa-

ble around the clock. Finally, a limited number of exceptionally needy patients may be acknowl-

edged as hardship cases, which implies the highest level of entitlements. The Medical Review

Board (Medizinischer Dienst der Krankenversicherung, MDK) performs the assessments for members of

the social LTCI, while Medicproof, a private company, carries out this task for private LTC in-

surers. Hence, in the field of long-term care, physicians lost their exclusive authority to define the

severity of illnesses (Naegele and Reichert 2002: 127f; Rothgang 2010: 438).

Persons with a recognized need for care at a specific dependency level may opt to receive

benefits in kind or cash benefits, or a combination of both. Cash benefits are paid directly to the

12 Between 1995 and 2009 the share of uninsured never exceeded the half-per cent level (Greß et al. 2005).

18

beneficiary. The charges for formal providers of benefits are capped by the LTCI funds. In the

original draft, these caps differed according to the three types of care: home, semi-residential (day

or night care), and residential care (figure 4). If the MDK acknowledges a case of hardship, the

benefits in kind are increased to 1,918 euros and 1,688 euros per month for home and residential

care respectively. Cash and in-kind benefits may be combined in levels I to III; e.g. if only half of

benefits in kind are claimed, half of the cash benefits are still available (Rothgang 2010: 439).

Figure 4: Definition and benefits of the three original dependency levels Level I Level II Level III Help for diet, hygiene, or mobility

At least once a day with at least two ADLs

At least 3 times a day at different times

Help must be available around the clock

Help for housekeeping More than once a week More than once a week More than once a weekRequired time per day At least 1.5 hours At least 3 hours At least 5 hours Benefits in euros per month Home care in cash 205 410 665 Home care in kind 384 921 1432 Semi-residential care 384 767 1074 Residential care 1,023 1,279 1,432 Own depiction based on §§ 15, 36, 37, 41, 43 SGB X;

If family care-givers go on holiday, the LTCI covers bills for care by professional providers for a

period of up to four weeks, capped at 1,470 euros per year. Moreover, informal work is acknowl-

edged by other branches of the social security system. For example, family care-givers are cov-

ered under statutory insurance legislation for accidents occurring during care activities. . They

may also apply to the LTCI for contributions to their public or private pension funds. In order to

qualify for this benefit, they have to perform home care for at least 14 hours a week and their

normal employment must not exceed 30 working hours per week. The level of contribution de-

pends on the duration of care for the beneficiary and the dependency level (Meyer 1996: 117f).

All benefits are absolute lump-sums or capped, as defined by law. This means that legislative

procedures are necessary to adjust them. Without adjustment their purchasing power declines

over time as the prices for LTC-related goods and services steadily increase. Hence, the German

LTC benefits are vulnerable to policy drift (see Mahoney and Thelen 2010). Indeed, policymakers

increased benefits for the first time in 2008 as part of a reform package – 13 years after the LTCI

Act came into force. At the same time they introduced a mandatory review of the appropriate-

ness of the benefits every three years (Rothgang 2010: 439f).

Remuneration of formal providers Benefits in kind are provided mostly by private non- or for-profit providers. Public provision is

limited to residential care, which serves members of social and private insurance alike. Even

there, the number of nursing homes owned by public authorities is relatively small and in decline.

19

In 2009, only five per cent of all LTC facilities for the elderly were public – three percentage

points less than at the beginning of the new millennium (Rothgang et al. 2011: 79). Providers

must have a contract with LTCI funds, which they get whenever certain formal criteria are met.

As the benefits are capped, a potential oversupply of providers is not regarded as a problem for

the insurance scheme. Quite to the contrary, it is rather encouraged to increase competition

(Rothgang 2010: 440). In terms of home care by professional providers, the 16 Länder are re-

sponsible for regulating remuneration. Hence, the number and definition of the service complex-

es s vary among Länder. The LTCI funds negotiate the actual level of tariffs with the providers.

Some Länder distinguish between for- and non-profit providers. LTC professionals are not al-

ways interested in higher prices, as they compete with each other on the one hand, and against

informal care-givers on the other. The latter can be explained as an effect of the benefit caps in

the LTCI. If prices for long-term care increase, families with a dependent person have to bear the

remainder. Therefore, they might decide to take the cash instead of the in-kind benefit and pro-

vide the services themselves (Rothgang 2010: 440).

Concerning residential care, the remuneration of providers is split into three different rates

for care, board and lodging (so-called »hotel costs«), as well as investment costs. Rates for care

and hotel costs are negotiated between providers on the one hand, and LTC funds together with

the responsible social assistance authority on the other (Evers 1998: 14). The investment costs

are partly financed by the Länder – this was one of the key amendments in the initial legislative

process. In order to enhance the infrastructure of Eastern Germany as soon as possible, the fed-

eral government set up a special investment programme of about 500 million euros per year. Be-

tween 1996 and 2003, the five new Länder could apply for money from this fund for building or

modernizing nursing homes as long as they covered 20 per cent of the total investment costs

themselves (Rothgang 2010: 440f). Investment costs that are not publicly financed are passed on

to the residents, or ,ultimately to the social assistance.

Financing and Administration As mentioned above, the benefits defined in the SGB XI are administered by the social and pri-

vate LTCI, which differ in terms of their legal status and financing mechanisms. Hence, it is nec-

essary to distinguish these two types of coverage.

We start with the social LTCI, which is administered by several LTC funds. Although for

practical purposes they resemble the sickness funds, they are separate in terms of accounting.

While sickness funds have the financial responsibility for their SHI members, which might lead to

surpluses or deficits, the benefits and administrative costs for long-term care are fully reimbursed

from a common pool. As with all other branches of the German social security system, the LTC

scheme is based on the PAYG principle. It is financed almost exclusively through contributions,

20

which are related to the income of individuals but not to their risk. The level of the contribution

is calculated as a certain share (contribution rate) of certain parts of the income (contributory

income). Employees pay 50 per cent of the contribution themselves, the other half is paid by

their employers. As the Free State of Saxony refused to abolish Penance Day, employees working

in this Land have to pay a higher share of the contribution rate. The contributions of unem-

ployed members are covered by unemployment insurance. The self-employed and, since 2004,

also pensioners have to pay the whole contribution themselves (Rothgang and Igl 2007: 54). Ini-

tially the contribution rate was 1.7 per cent of gross earnings or pension up to an annually adjust-

ed income cap. The income from other sources such as assets, rent, and leases is not considered

as liable to contributions, except for voluntary members. From 2004 onwards, members without

children above the age of 23 had to pay an additional contribution rate of 0.25 per cent. In July

2008, policymakers raised the general contribution rate for social LTCI to 1.95 per cent

(Rothgang 2010: 441). Although until 2009 sickness funds were entitled to determine the contri-

bution rate for SHI themselves, the LTCI contribution rate was fixed by parliament right from

the outset. Hence, unlike the SHI market, sickness funds have neither the opportunity nor the

incentive to compete with each other in the realm of long-term care (Jacobs 1995).

Mandatory Private Long-term Care Insurance Turning now to compulsory private LTCI, it is important to note that private health insurance

(PHI) companies administer this scheme. In other words, for the first time policymakers have

officially assigned a public task to private insurers (Böckmann 2011: 80f). This included the right

to impose the mandate for private LTC plans on their members. At the same time, however, they

had to accept every entitled applicant – irrespective of pre-existing conditions (§ 110.1.1 SGB

XI). Several German scholars interpret this as the highest acknowledgment of private health in-

surers as an essential institution of the German welfare state (Klingenberger 2001: 125; Koch and

Uleer 1997: 129; Wasem 1995). In line with the PHI, private LTCI is a funded scheme, i.e. mem-

bers build up provisions for old-age during their healthy years which should cover the costs for

long-term care in their final stage of life. Premiums are not related to personal income but to

individual risk (Rothgang 2010: 441). Unlike PHI, however, policymakers only allowed much less

comprehensive risk-rating. Private insurers must not use gender and health status for the calcula-

tion of the premium level for existing members. Moreover, they are not allowed to charge more

than the maximum contribution under the social LTC scheme or exclude pre-existing conditions.

Even children have to be co-insured for free (§ 110.1.2 SGB XI). Hence, private LTCI shares a

number of features commonly associated with social LTCI (Böckmann 2011: 81). As regulatory

constraints impede the calculation of risk-equivalent premiums, private insurers have to re-insure

21

their LTC plans with the Federal Financial Supervisory Authority (Bundesanstalt für Fi-

nanzdienstleistungsaufsicht) in order to guarantee their financial solvency (§ 111.2 SGB XI).

When comparing both branches, we nevertheless find a considerable selection bias. Members of

mandatory private LTC insurance are much younger, have lower age-specific dependency rates

and are economically better off. As simulations have shown, the contribution rate for the private-

ly insured would only be one third of the contribution rate for the members of social LTC insur-

ance if the former were also operating a PAYG system with a similar framework.

4 EFFECTS OF THE LTCI ACT Already in the prelude to the LTCI Act, the government labelled the bill »a comprehensive solu-

tion to the long-term care problem« (BT-Drs. 12/5617: 1, own translation). The cabinet estimat-

ed that around 1.65 million people would initially qualify for this new pillar of the social security

system and their number would grow to 1.9 million by the year 2014 (BT Drs. 12/5262: 62). As

the reform took effect in two stages and pending assessments by the Medical Review Board

slowed down the implementation, the year 1997 offers the first figures for the fully implemented

LTCI Act. At that time, the number of beneficiaries already exceeded the estimated level by

about 75,000. The figure grew almost continuously at a high rate over the subsequent years. In

2001 – 13 years earlier than originally expected – the total number of beneficiaries already sur-

passed the level of 1.9 million (see figure 5). In terms of their demographic composition, more

than three out of four recipients for that year are older than 65 and the number of female benefi-

ciaries is more than twice as high as the number of males.

Figure 5: Number and composition of beneficiaries of the social LTCI 1995 1997 1999 2001 2003 2005 2007 2009 2011Beneficiaries in tds. 1,069 1,725 1,889 1,925 1,977 2,005 2,102 2,271 2,360Share of benefit level Level I n/a 43.9% 47.8% 49.8% 51.2% 51.8% 53.1% 54.3% 56.1%Level II n/a 40.7% 38.3% 36.9% 35.8% 35.3% 34.2% 33.3% 32.0%Level III n/a 15.4% 14.0% 13.2% 12.9% 12.9% 12.7% 12.4% 11.9%Share of benefit type Home care in cash 83,0% 56,3% 52,0% 50,0% 49,0% 47,9% 46,9% 45,5% 44,5%Home care in kind 15,4% 16,0% 18,3% 18,9% 18,8% 18,7% 19,1% 20,4% 20,7%Semi-residential care 1,5% 0,8% 1,1% 1,4% 1,7% 2,1% 2,5% 3,5% 4,8%Residential care - 26,9% 28,5% 29,7% 30,5% 31,2% 31,4% 30,5% 29,9%Home care in kind also includes combinations with cash benefits; Semi-residential care includes day, night, short-term, and vacational care Own depiction based on BMG, Pflegestatistik

In addition to the number of beneficiaries, their assigned dependency level and their chosen type

of benefits are also important for the financial impact of the reform. Starting with the level of

dependency assigned by the Medical Review Board, we observe a shift towards less severe levels.

The share of people at the lowest benefit level I increased steadily from 43.9 per cent in 1997 to

22

56.1 per cent in 2011 at the expense of the more generous levels II and III (see figure 5). As this

finding contradicts the general trend of population ageing, it can be assumed that the assessments

have become stricter over time. With regard to types of services, we observe a shift away from

exclusively cash benefits, which represent the cheapest type for the LTC funds. The initial de-

crease is related to the staged implementation of the LTCI Act. Benefits for home care already

came into force in 1995. From the subsequent year on, LTC funds also paid for residential care.

As a consequence, we observe – in relative terms – a sharp decrease in dependent persons choos-

ing cash benefits between 1995 and 1997. Since its peak in 2007, the share of residential care has

decreased slightly. It is therefore likely that the overall shift away from cash benefits is fuelled by

two smaller categories: home care in kind and semi-residential care. Both increased almost con-

tinuously over the last 15 years, reflecting e.g. the development of new care arrangements that lie

between the classic models of family caregiving and nursing homes. Clearly, therefore, the com-

position of the selected benefit types was more expensive prior to 2007. Since then, the picture

has become more complex, as there has been a drop not only in cheap cash benefits but also in

the most expensive type: residential care.

Summing up, we observe a constant increase in beneficiaries and a trend towards more ex-

pensive types of benefits until 2007. As we can see in figure 6, these two cost-inflating develop-

ments outweighed the steady decrease of the average benefit level. Expenses have grown contin-

uously since the inception of the LTCI Act. The tripling of costs between 1995 and 1997 was

related to the staged implementation of the law. Between 1997 and 2007, social LTCI expendi-

tures only increased by 13 per cent – very close to the overall growth in consumer prices. Since

then, expenses have risen sharply due to the first adjustment of benefit levels and a refined ac-

knowledgment of dementia patients.

Figure 6: Revenue, expenses, surpluses, and financial reserves of the social LTCI in billion euros 1995 1997 1999 2001 2003 2005 2007 2009 2011Revenue 8.41 15.94 16.32 16.81 16.86 17.49 18.02 21.31 22.24Expenses 4.97 15.14 16.35 16.87 17.56 17.86 18.34 20.33 21.92Surplus / deficit 3.44 0.80 -0.03 -0.06 -0.70 -0.37 -0.32 0.98 0.32Financial reserve 3.93 3.77 3.61 3.27 2.82 2.01 2.06 2.78 2.93Own depiction based on BMG, Pflegestatistik

Next, we focus on the social LTCI revenue that is mainly fuelled by wage-related social security

contributions. In 1995, right after the first stage of the reform became effective, revenues exceed-

ed expenses by far, leading to a financial reserve of about four billion euros. Since then, this fi-

nancial reserve has slowly but steadily diminished due to deficits from the late 1990s onwards.

While expenses kept pace with overall inflation, contributions developed disappointingly due to a

combination of several socioeconomic factors such as the decreasing role of standard employ-

23

ment13 and low wage increases (Evers 1998: 8). From 1997 to 2004, the average annual growth of

nominal contributions remained at 0.8 per cent, well behind the development of consumer prices.

Thus, it was the poor growth in contributions rather than the soaring costs that caused trouble

(Rothgang 2010: 445). By 2007, only half of the initial financial reserve was left. In the meantime,

due to the increased general contribution rate in 2008 and the fast recovery of the German econ-

omy after the Great Recession, social LTCI generates surpluses again.

The official objective stated in the LTCI Act was that social assistance for long-term care

costs should become an exception rather than a rule (BT-Drs. 12/5262: 61). The latter had been

the case before the implementation of the law, as the vast majority14 of nursing home residents

received social assistance. In line with the two strands of the long debate, the government em-

phasized the twofold effect of fewer welfare recipients. On the one hand there was the social

policy argument that the elderly would preserve their personal dignity and assets. On the other

hand, there was the fiscal argument that municipalities would be relieved of an inappropriate task

and an immense financial burden (BT-Drs. 12/5262: 61f).

Figure 7: Recipients of and expenditure for care assistance in Germany (1994=100)

Own depiction based on Statistisches Bundesamt, Statistik der Sozialhilfe

We therefore take a closer look at the number of social assistance recipients due to LTC at the

end of a calendar year and the related costs in deflated terms. As figure 7 clearly reveals, the index

for both indicators dropped strongly after the introduction of the LTCI Act, although with dif-

ferent timing. The first reform stage in 1995, when the home-care benefits were introduced, had

only a noticeable impact on the number of social assistance recipients, but not on related expend-

13 The decrease in standard employment was fuelled on the one hand by a growing number of social security beneficiaries at

working age (unemployment and early retirement) and on the other by the substitution of standard employment with so-called mini-jobs and/or freelancers who were only partially or not fully liable to contributions.

14 The research institute Infratest estimated that in 1994 around 69 per cent of all residents in the Western Länder had to apply for social assistance and 88 per cent of residents in the Eastern Länder (Schneekloth and Müller 1995: 46).

0

20

40

60

80

100

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Number�of�recipientsDeflated�expenditure

24

itures. While the former decreased by 17 per cent the latter only dropped by three per cent. Re-

garding expenditures for means-tested care assistance, the second stage of the reform, which in-

troduced benefits for residential care in 1996, was far more important. Expenditure rapidly de-

clined to 30 per cent of the pre-reform level and stayed there until 2010, representing a big finan-

cial relief for local budgets. Hence, in terms of the fiscal policy argument the LTCI Act has so far

provided a sustainable success for the municipalities. In contrast to this, the results for the num-

ber of social assistance recipients, constituting the actual social policy motivation for the reform,

are much more ambiguous. At first the LTCI Act fulfilled its promises. By the end of 1998, the

number of recipients was only half of the pre-reform level. But since then, we observe an overall

growth trend with only a minor intermission in the early 2000s. At the end of the year 2010,

around 318,000 people had to apply for social assistance for LTC to make ends meet – 70 per

cent of the pre-reform level (see figure 7).

Figure 8: Share of long-term care patients receiving care assistance

Own depiction based on BMG, Pflegestatistik and Statistisches Bundesamt, Statistik der Sozialhilfe

In order to further elaborate this finding, we compare the number of social assistance recipients

due to LTC with the overall head-count of people receiving home or residential care. We take

1998 as our reference year as it represents the first data point for the fully implemented LTCI

Act. Moreover, as already mentioned, that year is also the turning point for the absolute number

of social assistance recipients due to long-term care. At the end of 1998, only 5.1 per cent of

people being cared for at home received social assistance (see figure 8). Until 2010, the indicator

stays close to the five per cent level. Hence, for elderly receiving LTC services in their home,

social assistance has indeed – as intended – become an exception.

This is far from the case in terms of nursing home residents. In 1998, still 31.3 per cent of

them applied for care assistance as their pension, LTCI benefit, and assets did not cover their

costs (see figure 8). Within two years this indictor gained nearly five percentage points, coming to

a peak in 2000 at 36.1 per cent. By 2004 the share of nursing home residents receiving care assis-

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

1998 2000 2002 2004 2006 2008 2010

Home�care Residential�care

25

tance had bounced back to 30.4 per cent. But since then, the indicator has again increased steadi-

ly. At the end of 2000, over 33 per cent had to apply for care social – well above the reference

year. Clearly, for nursing home residents the proposed »comprehensive solution« was neither

sufficient nor sustainable. The main explanation for this is the devaluation of the LTCI benefits

due to a lack of adjustments before 2008 and insufficient adjustments since then. We observe this