Embed Size (px)

Citation preview

Report No. 6082

Financing Adjustment With Growthin Sub-Saharan Africa, 1986-90

February 1986

FOR OFFICIAL USE ONLY

Document of the U4rId Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. its contents may not otherwísebedisclosed without Worid Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

THE WORLD BANKWashngtUonID. C. 20433

U.5.A.

A.W. CLAUSENPheit ~February 21, 1986

MRMORANDUM TO THE EXECUTIVE DIRECTORS

Subject: Financing Adjustment with Growth in Sub-Saharan Africa, 1986-90

This i8 the World Bank's fourth report focusíng on developmentissues and requirements in sub-Saharan Africa. Since 1981, the developmentstrategíes of many African countries have changed dramatically. Majorstructural reforms are being uindertaken and some promising results arealready evident. The tragedy of drought and famíne heightened the urgencyof these reforms while often weakening the capacity to implement them.Nevertheless, many African policy-makers have demonstrated farsighteddetermination in pursuing necessary reforms. While much remains to bedone, especially in addressing long-term issues of human and naturalresource development, there has been marked progress by many Africancountries in redressing major macro-economic and sectoral distortions.

The response of the donor community to Africa's famine wasgenerous and effectíve, and represe.ated a heartening example of how a widearray of donors can pursue a shared obiective to the great benefit of thepeople of Africa.

However, the major structural reforms undertaken by many Africancountries to address their long-term development problems have not receivedadequate donor support. As noted in the Report, growth and equityenhancing reform programs already under way are foundering because ofinadequate donor fundlng, which ís often inappropriate in form andtiming. Countríes consídering major reform programs can find littleencouragement from the donor support demonstrated for those countries withreforms under way. In the absence of adequate financial support,structural reforms cannot be achieved with growth. Adjustment throughfurther economíc contraction ls not a feasible alternatíve in a continentwhere per capita income levels today are no higher than they were twentyyears ago.

-2-

In the past, the Bank has argued that resource availability isonly one element ín addressing Africa's development; the political will ofAfrican leaders, essential to effectively utilize both domestic and foreignresources, is also critical. But there is now growing evidence that manyAfrican countries are exercising this political will. Theír comnitment andefforts must be matched now by the political will of the donor community toincrease the resources available to implement growth-oriented adjustment 3programs.

The resources needed to restore growth prospects in Africa are notlarge but they exceed by far those currently available or envisaged. Theseresource requirements reflect the deepening debt problem _n Africa, with arapidly increasing share of resource flows required to service debt, aswell as a decline in non-concessional flows due to the deterioratingcreditworthiness of the region. While-some increases in bilateral andmultilateral flows are foreseen, because of an enlarged Lome III and theSpecial Facility for Sub-Saharan Africa, a further US$2.5 billion per yearin concessional flows and debt relief is required ín 1986-90 to restoreAfrican import capacity per capita to its 1980-82 level, even assuming asignificant increase in exnorts. The increased flows from multilateralagencies including an enlarged IDA-8, IMF Trust Fund reflows, and anenhanced replenishment of the African Development Fund, when due, mightprovide up to $1 biLlion per year of these additional funds. For theremainder, a major effort is required in bilateral assistance -- whetherthrough new money or more liberal debt relief.

Donor action is also required in several areas to enhance theeffectiveness of assistance to Africa. Many of these actions are not new;they have been discussed and agreed upon in principle in various fora.However, their implementation has lagged far behind the implementation ofstructural reforms by many African countries, and urgent action is nowrequired on matters relating to the quality, form, timeliness andcoordination of aid. Action in the following areas would do much tostrengthen the system:

- Donors must be willing to work within coherent and realisticadjustment and investment programs designed by African governments.Projects outside thcese programs are of lower priority and should not befinanced unless the agreed prioríty program is also fully financed.

- Donor decisions on aid and debt relief must be made together inlight of an overall financial package and a program of adjustment withgrowth. This could be achieved Sn the context of adapted consultativegroup meetings or roundtables.

- To enhance the effectiveness of aid group meetings, the ¡najorparticipants should discuss the key elements of the financial package andadjustment program required for the country, in advance of the meeting, andarrangements should be made to monitor implementation of aid commitments insupport of each adjustment program.

- Donors should provide meaningful medium-term indications of aidand debt relief levels-, to enable countries to program their investmentstrategies in light of an indicative resource envelope.

For its part, the World Bank stands ready to further strengthenits role in assisting countries to design programs of growth-orientedadjustnent and in their funding. In addition, as requested by theDevelopment Committee, the Bank will continue to exercise a leading role inestablishing mechanisms to enhance the effectiveness of aid flows throughimproved coordination and monitoring.

There are opportunities ahead to restore many African countries toa sustainable growth path. But substantially increased donor support isessentlal to capitalize on these opportunities.

FOR OFFICIAL USK ONLY

Financing adjustment with growthin Sub-Saharan Africa, 1986-90

The World BankWashington, D.C.February 1986

This document has a restricted distribution and may be used by recipientsonly in the performance of their offícial dutíes. Its contents may notothervise be dísclosed without World Bank authorization.

.i

Contento

Country coverage y

Acrongym aud definitiona vi

Sumuary aUd conclusion. 1

Progreso in domestic policy reform 1Resource scarcity 2Measuring the resource gap 2Bridging the resource gap 3Improving aid coordination 4A year of opportunity 4

1 Introduction 5

The end of the drought 5Continuing long-term decline 7The deepening debt problem 8A strategy of adjustment with growth 9

2 Adjusttent programa 11

Correcting overvalued exchange rates 12Correcting urban-rural bias 14Rationalizing the public sector 17

3 Long-ter= constrainta on growth 20

Population 20Human resources 23

Health 23Education 24

Deforestatíon 25Agricultural research 26 _

4 External capital and aid coordination 30

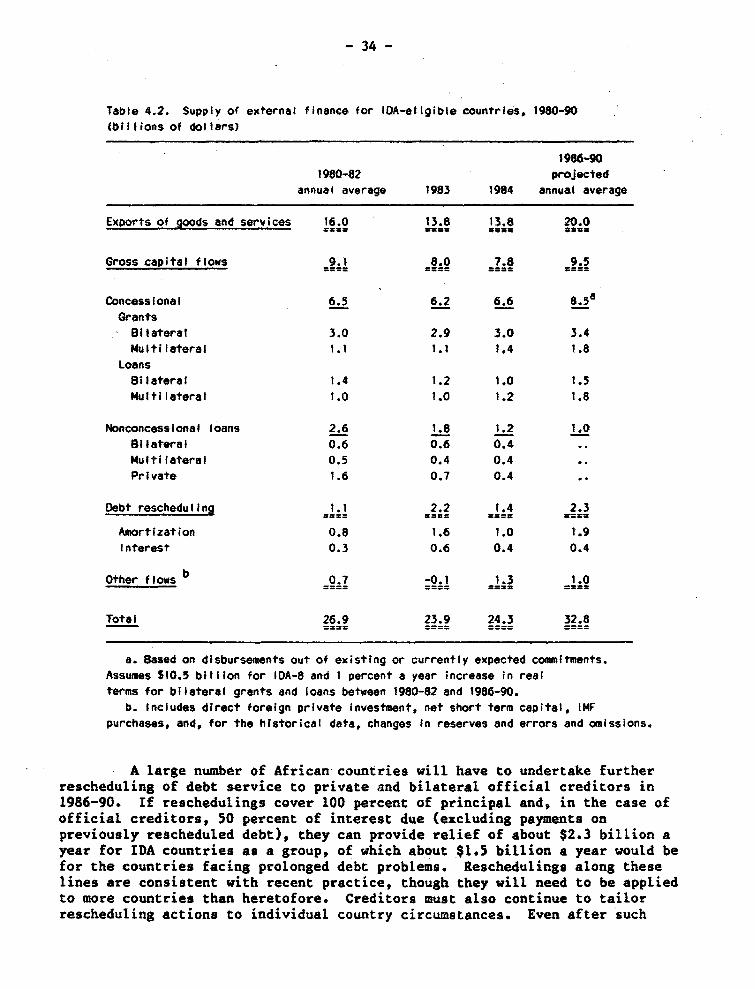

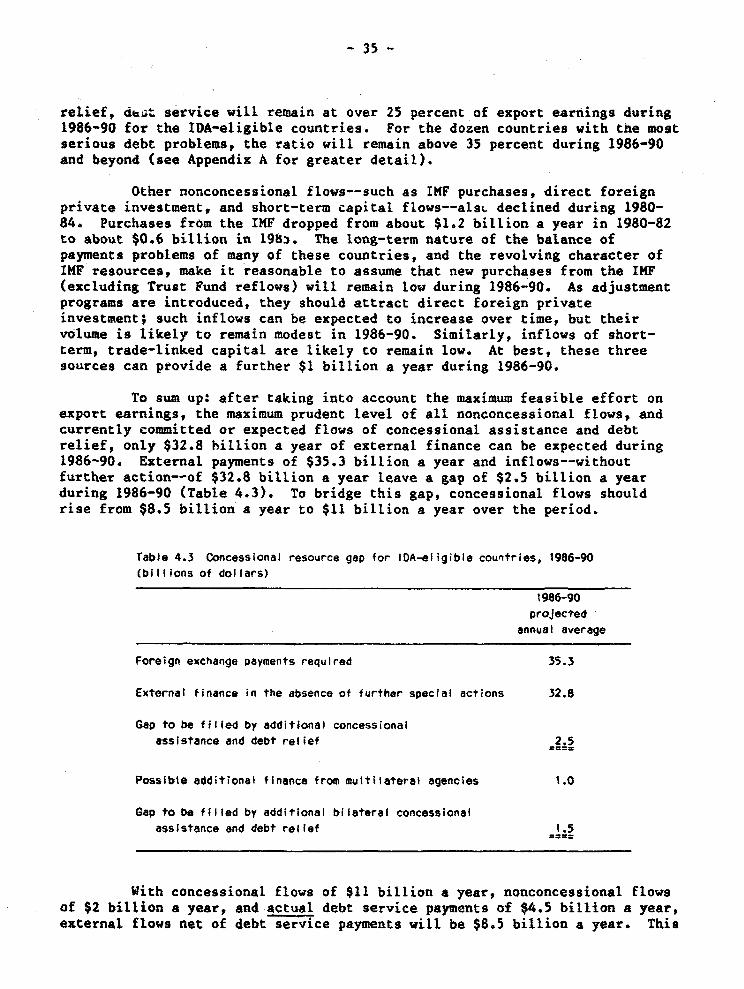

External resource flows, 1986-90 30Foreign exchange requirements 31Sources of external finance 33Bridging the resource gap 36

Institutional reforms in aid coordination 37Recent progress 37Further reforms 38

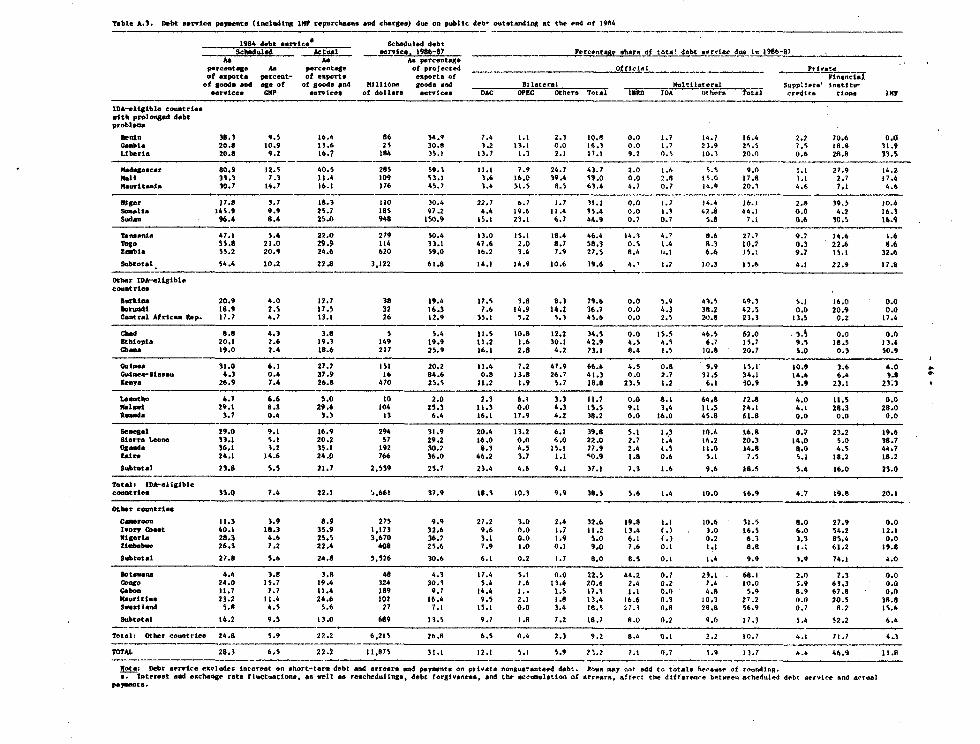

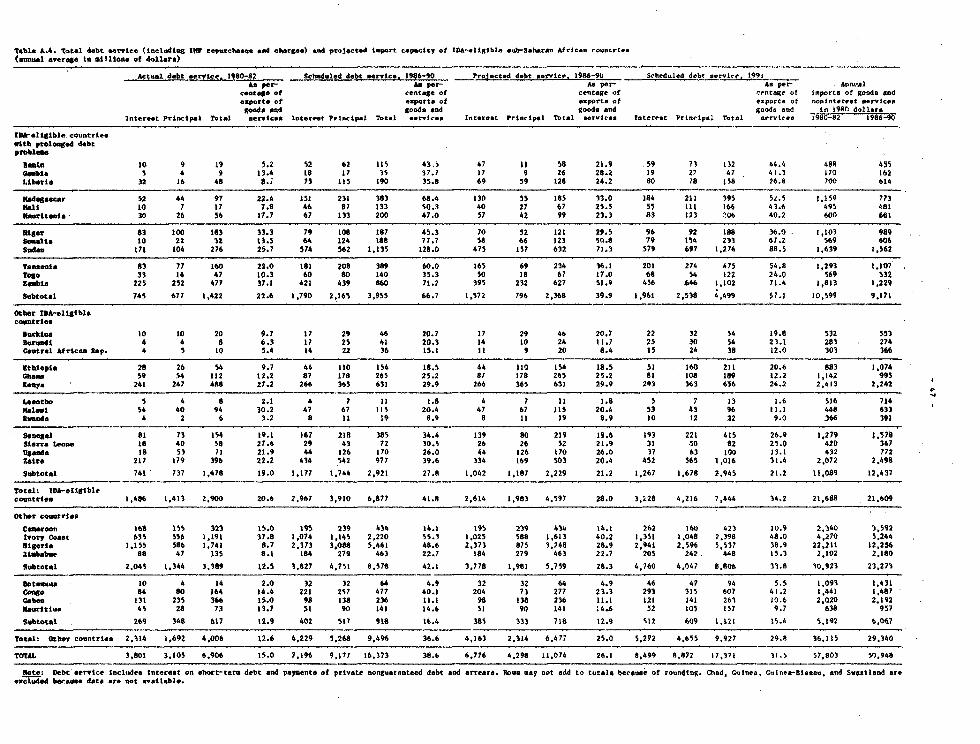

Appendix A: The debt problea and ita implications for import capacity 41

Profile of the African debt problem 41Projected debt-service burden and ímport capacity 42

Appendix B: Macroeconomic indicators 48

Statistical Annez 51

Kap 109

- ív

Text tables

1.1. Develop¡Aents vi the trade environmentof IDA-eligible countries, 1970-86 6

1.2* Output, populecion, income, andconsumption in IDA-elígible countries, 1960-86 7

1.3. Availabilíty of resourcesin IDA-eligible countries, 1960-84 8

2.1. Earnings as a multiple of per capitaGDP: Sub-Saharan Africa and Asia 16

3.1. Desired family size and actual fertility rates 22

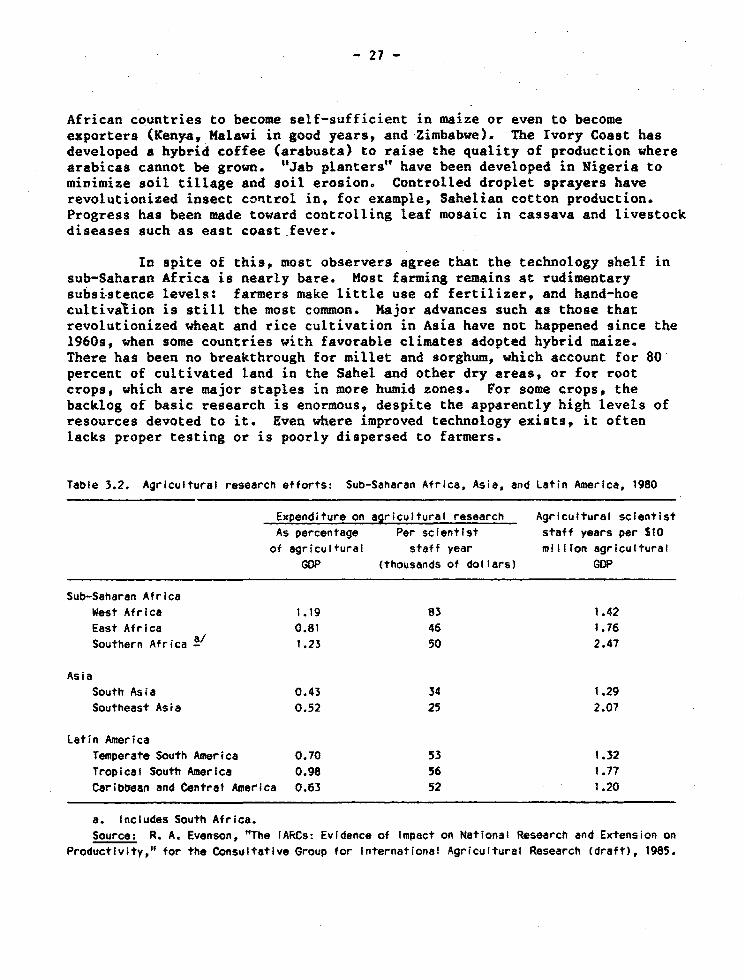

3.2. Agricultural research efforts:Sub-Saharan Africa, Asia, and Latin America, 1980 27

4.1. Foreign exchange paymentsby IDA-elígible countríes, 1980-90 32

4.2. Supply of external finance for IDA-eligiblecountries, 1980-90 34

4.3. Concessional resource gap forIDA-eligible countries, 1986-90 35

Text figures

2.1. Real effective exchange rate indexesin developing countríes, 1971-84 13

This Report was prepared by a team led by Ramgopal Agarwala and comprisingCharles Humphreys, Kathie Krumm, and John Underwood, with the assistance ofmany World Bank staff members and Stanley Please, principal consultant. Itdraws heavily on the ideas and views expressed by scholars and officials inAfrica and in donor countries. The work was carried out under the generaldirection of Xavier de la Renaudiere. Sang Lee, in collaboration with RameshChander and with the assistance of Zafar Ahmed and Maria Cristina Germany andothers, prepared the Statistical Annex. Clive Crook was principal editor andJane Carroll and Carol Rosen were technical editors. Special thanks go to thesupport staff, headed by Jean Ponchamni and including Lynn CIark-MCCarthy andAnn Van Aken.

v

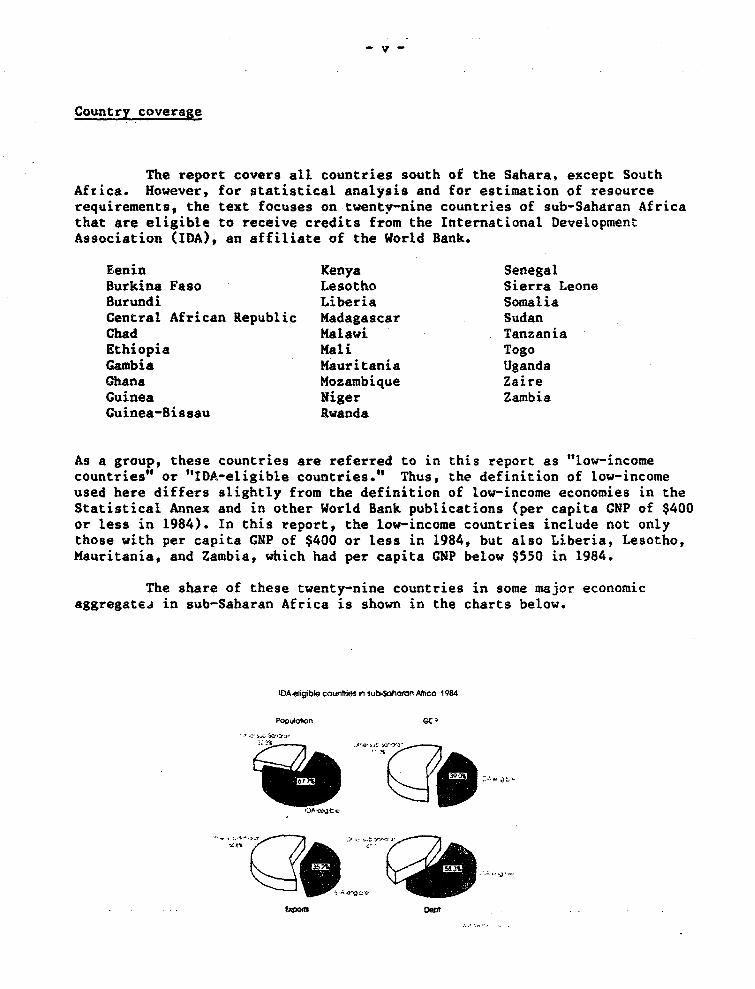

Country coverage

The report covers all countries south of the Sahara, except SouthAfrica. However, for statistical analyuis and for estimation of resourcerequirementa, the text focuses on twentv-nine countries of sub-Saharan Africathat are eligible to receive credíts from the International DevelopmentAssociation (IDA>, an affiliate of the World Bank.

Eenin Kenya SenegalBurkina Faso Lesotho Sierra LeoneBurundi Liberia SomaliaCentral African Republic Madagascar SudanChad Malawi TanzaniaEthiopia Mali TogoGambia Mauritania UgandaGhana Mozambíque ZaireGuinea Niger ZambiaGuinea-Bissau Rwanda

As a group, these countries are referred to in this report as tlow-íncomecountries" or "IDA-eligible countries." Thus, the definition of low-incomeused here differs slightly from the definition of low-income economies in theStatistical Annex and in other World Bank publications (per capita GNP of $400or less in 1984). In this report, the low-income countries include not onlythose with per capita GNP of $400 or less in 1984, but also Liberia, Lesotho,Mauritania, and Zambia, which had per capita CNP below $550 in 1984.

The share of these twenty-nine countries in some major economicaggregate.i in sub-Saharan Africa is shown in the charts below.

IDA eigibte counhGs in sub-Soharan Alico 1984

popuúon hGC

e7-a,

Eagofts DeS-

- ví -

Acronyms and defiuitions

DAC Development Assistance Committee of the OECDFAO Food and Agriculture OrganizationIDA International Development AseociationILO InLernational Labour OrganisationIMF International Monetary FundODA Official development assistanceOECD Organisaton for Economic Co-operation and DevelopmeatOPEC Organization of the Petroleum Exporting CountriesUNICEI United Nations Children's FundUNCTAD United Nations Conference on Trade and DevelopmentUnesco United Nations Educational, Scientific and Cultural OrganizationUNIDO United Nations Industrial Development OrganizationWHO World Health Organization

Unless otherwise indicated, tables and figures in the text andappendices are based on World Bank data. Growth rates are least-squaresestimates in constant prices unless otherwise stated.

Billíon is 1,000 million.

Dollars are US dollars.

.. Not available.

.) Less than half the unit shown.

Summary and conclusiona

Sub-Saharan Africa ia emergín& from one of the worst famines inrecent history. Cood rainas have come to much of the region. Per copitaincomes should rise this year for the first time since 1980. Even so, thereis little cause to celebrate. Low-income Africa ¡s poorer ín 1986 than it wasa generation aga in 1960. And though the recent good news interrupts thetrend of chronic economic decline, it will not be enoug- to reverse it.Population growth is largely unchecked, productivity all but stagnant. Ifpresent trends continue, the human disaster of 1983-84 in sub-Saharan Africavill return to haunt the world community.

This year gives a breathing opace. Africa shoutd use it to makeatructural adjustmenta aimed at reviving growth, especially in agriculture,and to halt the deterioration in basic health and education services. Donorcountries, for their part, must not see 1986 as a time to relax. Theprincipal theme of this report ¡s that Africa's attempts to help itself willfail with"u additional resources in the form of new aid and debt relief.

Progreuo la domestic policl refor.

Many Afri-an goverments are now making significant progresain structural adjustmen.. Sut they atill have much to do tocorrect the accumulated policy distortiona of the past.

In many African countries, government policy has long discriminatedagainst agriculture--the sector which ¡a not only crucial for any attempt toraise output and exporte, but whích also gives most of the poor theirlivelihood. Dismantling such policies will hela the region to increase outputand exporte, and help the poor at the same time. Thís proceso has begun.Goveramenta have started to reduce the overvaluation cf their currencíes--oneway in which agriculture had been penalized. They have increased adrículturalprices and lowered real urban wages. They have reduced public spending, vitbite bias toward expanding employment in urban areas.

These are welcome reformst but no more than the first steps.Exchange retes remain severely overvalued in many African countries.Producers' shares of export yrices are still too low. Urban wages are higherthan in other low-income developing countries.

Africa's governnments have done even less to overcome the region'slonger-term obstacles to development. Family planning, education and health,resource conservation and agricultural research are vital in this respect. Insome cases, however, services have declined, canceling out progress made inearlier years. And governments still have much to do to improve theallocation of resources--by giving a greater role to prices, markets and theprivate sector, by increasing the supply of domestic savings, and by runningpublic enterpríses more efficiently.

Resource scarcity

Declining importa and investment threaten to undermine atructuraladjustment in low-income Africa.

Adjustment with growth requíres extra resources, but the recent trendin resource flows has been just the opposite. The investment rate in low-íncome Africa has been falling sínce 1980 and ¡a now the lowest amongdeveloping regíons. It is not sufficíent to maintain and rehabilitateexisting productive capacity, nor to provide for new capacity. This declinein investment mirrors declines in Afríca's supply of both domestic and foreign.savings; the shortfall in foreign savings in turn reflecta a worsening debtcrisis and a diminishing flow of commercial capítal. A dozen countries nowface acute debt difficulties, with little prospect of improvement.,

Africa needs more imports, not just of investment goods, but also ofessential consumer goods and raw materials. Importa per capita have beendeclíníng since 1970s and the rate of decline has accelerated in the 1980s.In spite of hígher coffee prices and lower oil prices, the outlook for theterms of trade is poor. Without new aid and debt relie4, imports per capitawill contínue to fall for the rest of this decade and beyond.

Measuring the resource gap

To continue its progreso toward economic adjustment, lov-income Africa vill need at least $11 billion a year inconcessional flows during 1986-90. Alloving for known andexpected aid comhnitents, a gap of $2.5 billion remains.

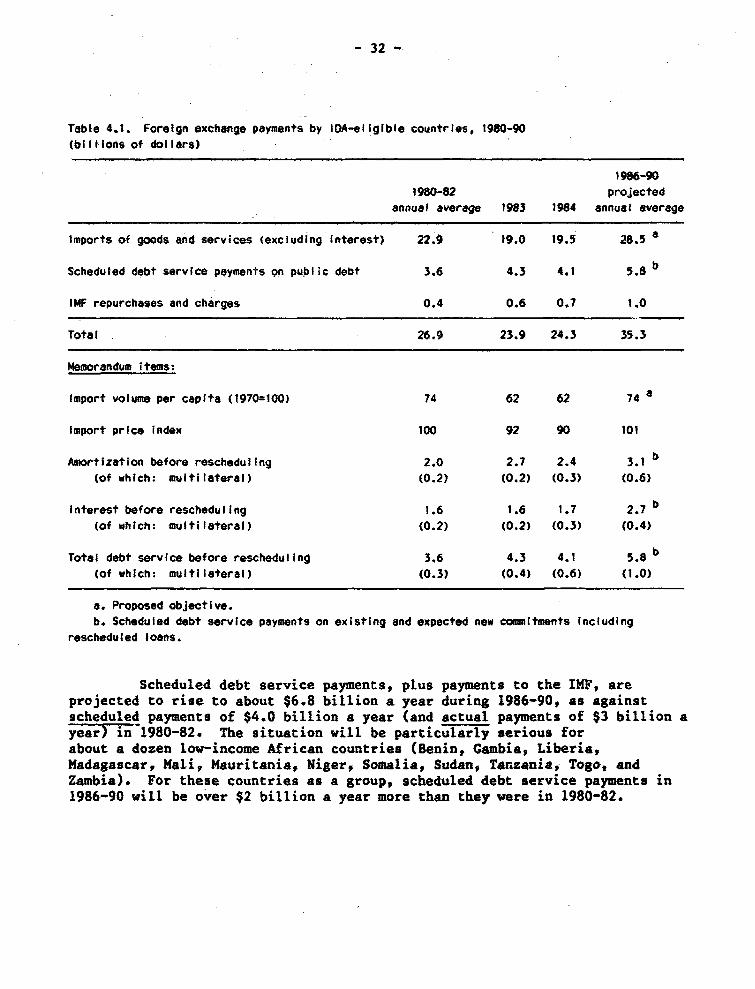

In calculating external resource requirements, the objective is tohalt the trend of decline in per capíta consumption by 1990 and achieve somegrowth thereafter. This minimum objective would require a GDP growth rate ofat least 3-4 percent a year by 1990. Qn the basis of the Bank's countryexperience, it is unlikely that such growth rates can be achieved, unless thedecline in import capacity is reversed. At a mninimum, imports per capitashould return to theír level of 1980-82. This implies imports of $28.5billion a year in current prices during 1986-90. Provision must also be madefor debt-service payments that are projected to rise to an average of $6.8billion a year over the períod. Altogether, then, the region needs $35.3billion a year for the next five years.

The possible sources of that finance are as foLlows. Exports mightprovíde at best $20 bíllíon a year--and this assumes that governments continueto adopt export-oriented policíes. New bank borrowing on commercial termsmight provide $1 billion a year; in view of the region's poor debt-servícingcapacity, it would be imprudent to seek more. In aLl, another $1 billion ayear ín nonconcessional finance might come from the IMF, froma direct privateforeign investment, and ín short-term capital flows. Debt. reschedulings,under existing procedures, should provide around $2.3 bíllion a year. Knownand expected aid commítments imply concessional flows of $8.5 biíLion a year--an increase of about 25 percent from tte level of 1980-82. Altogether, theregion might tap $32.8 bíLlion, leaving a resource gap of $2.5 billion a year.

-3-

1986-90

projected

annual average

(bilitons of dollars)

Forcign exchange requirements for IDA-eligible countries

Imports of go"d end services (excluding Interest> 28.5

Debt service payments (plus payments to IMF) 6.8

Total 35.

Sources of f¡nance

Exports of goods and services 20.0

Nonconcessional flows 2.0

Debt rescheduling (based on existing practices) 2.3

Concesslonal flows (based an existing and expected commitments> 8.5

Total 32.8

Resource gapTo be fWiled by additional concessional flows

and debt rescheduling 2.5

Bridgíng the resource gap

Multilateral agencies might provide $1 bíllion of the

resource gap of $2.5 billion a year. This leaves $1.5

bhllion a year to be met from new bilateral aid and

additional debt relief.

Multilateral agencies could, at best, meet about $1 billion of the

gap íf the IDA-8 replenishment is st least $12 billíon and low-income Africa

receives a large part of the SDR 2.7 billion expected in the IMF Trust Fund

reflows. Bilateral aid and additional debt relief must bridge the remaining

gap of $1.5 billion a year. That vould mean an increase of 30 percent over

the aid and debt relíef given in 1984 and a 20 percent increase over the

levels currently projected.

The additional resources will be needed to pay for importe during

1986-90 and to cover debt service payments, so they must be in quick-

disbursing form. The correct pattern of assistance--in particular, the split

between quick-disbursing aid and debt relief--will vary from case to case.

But one general rule should be observed: no donor country should be a net

recipient of resource flows fros any African country undertaking credible

economic reforma.

Donors might provide new bilateral assistance in several ways, for

example:

o By converting exísting official loans into grants, through retroactive

termsa adjustment, as proposed in the UNCTAD declaration of 1977

-4-

O By enabling their export credit agencies to refinance debt servicepayments on more concessional termo

o By widening the circLe of creditors that participates in debt rescheduling

o By increasing their ai* 5udgets, and especially by increasing quick-disbursing funde avíilLole in support of atructural adjustment.

Improving aid coordination

Dovora must act more in concert-vith each other and vithrecipiente. This report suggests cix vaya to improvecoordinastioQ.

First, donora must be willing to work within adjustment programadesigned by African governments. Second, they should bring decisions on aidand debt relief together, using the existing framework of consultative groupmeetings. Third, the major participants should discuss the elements of therequired financial package in advance of full-scale aid coordinatíonmeetings. Fourth, to provide effective support for medium-term adjustment,donors should be more willing to give medium-term indications of aid. Fifth,secretariats should be established to monitor progress toward economic reformand toward implementing governments' and donors' agreements. Sixth, themultilateral agencies must assume a larger role in orchestrating donorassistance--both in designing adjustment programs and in financing them. TheWorld Bank and the IMF, in particular, must work together with Africangovernments, first to develop adjustment and investment programe aimed atrestoring growth, and second to assess the requirements for, and sources of,external finance.

A year of opportunity

Recovery from the drought has brought lower food prices, and importedpetroleum will be cheaper because of the decline in oil prices. This makes1986 a good year for Africa to accelerate ite procese of correcting overvaluedexchange rateg: lower food and petroleum prices will soften the inflationaryimpact of devaluation on urban dwelLers; at the same time, devaluation wouldhelp raise the farm prices of agricultural exporta and partly offset theeffects of lower food prices on farmere. Lover food prices have alzo createdan opportunity for Africa to dismantle, without undue hardship, more of itacontrole on food pricing and marketing.

It ¡J a year of opportunity for donors too. Decisions on the IDA-8replenishment and on the IMF Trust Fund reflows will affect the resourcesavailable for Africa over the next five years. The Development Comnittee'smeeting in April and the epecial session of the UN General Assembly in May canestablish the principles on which the concerted effort of the Africancountries and the international community can be based.

1. Introduction

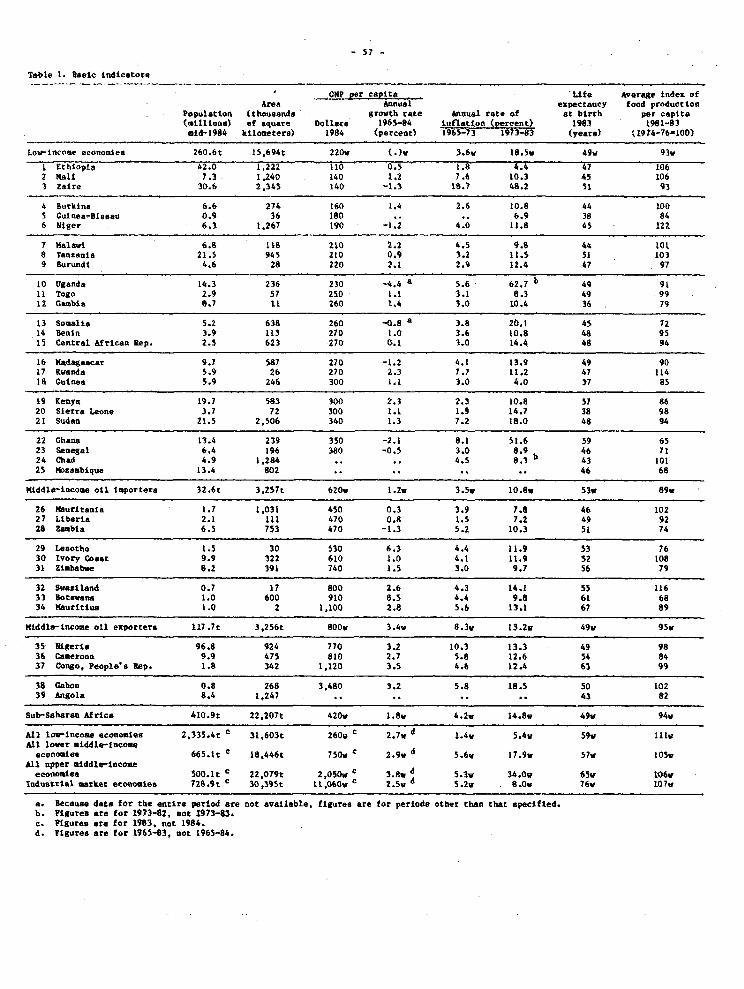

The famine of 1983-84 ín sub-Saharan Africa ¡i videly recognized 8sbeing part of a longer-term production crisis. The World Bank's previousreport on the region argued that this deeper problem has ite roots in high andaccelerating pqpulation growth and in low and declining efficiency in the useof resources. _ The report predieted that, without additional donor support,inadequate resources vould soon become another major constraint, and Africa'sdecline would continue.

This year has brought some velcome signs of relief. Most of Africahas had good rainfall. An increasing number of countries are starting torecognize the policy mistakes of the p8st and are taking steps to correctthem.- Por low-income Africa, termo of trade have improved because of highercoffee prices and lower oil prices.

However, the long-term tren¿ of decline persists. As yet, too fewcountríes are embarking upon the atructural adjustment process; those thathave begun atill have far to go. Only a handful of countries are seriouslytrying to control extremely high rates of population growth. The availabilityof resources in Africa ¡a shrinking, and without additional donor support,will continue to do so.

The challenge for Africa and the donor countries ¡i to reverse thelong-term trend of decline. Adjustment with growth must become a realistictheme for the lov-income countries of the region--as for the high-debt middle-income developing countries. Over the next five years, this calls both fornational programa of policy reform and for substantially higher donorasmistance: each will fail without the other. To achieve adjustment withgrowth during this period, decisions must be made in 1986 on the level snd theform of assistance that the developnment community will provide. The focus ofthis report is on the needs of low-income African countries eligible to borrowfrom IDA, '2ut many of íts conclusions hold for the other sub-Saharan countriesas vell. -

The end of the drought

Sub-Saharan Africa ¡i emerging from one of the worst famines inrecent history. The drought that began in southern Africa in 1983 went on toaffect more than twenty countries and 35 million people by 1985. Theínternational community responded on an unprecedented scale, vithcontributions of food, medicine, and other critical supplies. Relief workersfrom donor and recipient governments and from prívate agencies moved massive

1. Tovard Sustained Development in Sub-Sahsran Africa: A Joint Programof Actíon (Washington, D.C., 1984>.

2. Por a list of the IDA-eligible countríes, see the note on countrycoverage at the beginning of this report. In this report, the terms "IDA-eligible" and 'lov-income" countries are synonymous.

-6-

samounts of material under extremely difficult condítíons, helping to savethousands, if not millions, of líves. Yet the famiíne took its toll. Manyfarmers and nomads have joined the ranks of the urban poor. Families havebroken up, systems of community support have weakened, and the strain on over-stretched goverrment servi'es has increased still further. In these difficultcircumstances, people are sL.dggling, with remarkable spirit, to resume theirnormal lives.

Fortunately, most of Africa received good rainfall in 1985. In spiteof the famine's devastation, agriculture is recovering. According to the FAO,agricultural output in 1196 will equal or exceed pre-drought levels in mostIDA-eligible countries. - The main exceptiona are Ethiopia, vhere faminepersists in some areas, and Mozambique; both will need special assístance thisyear, according to the UN Office for Emergency Operations in Africa. Most ofthe region, however, shares in a sense of relíef.

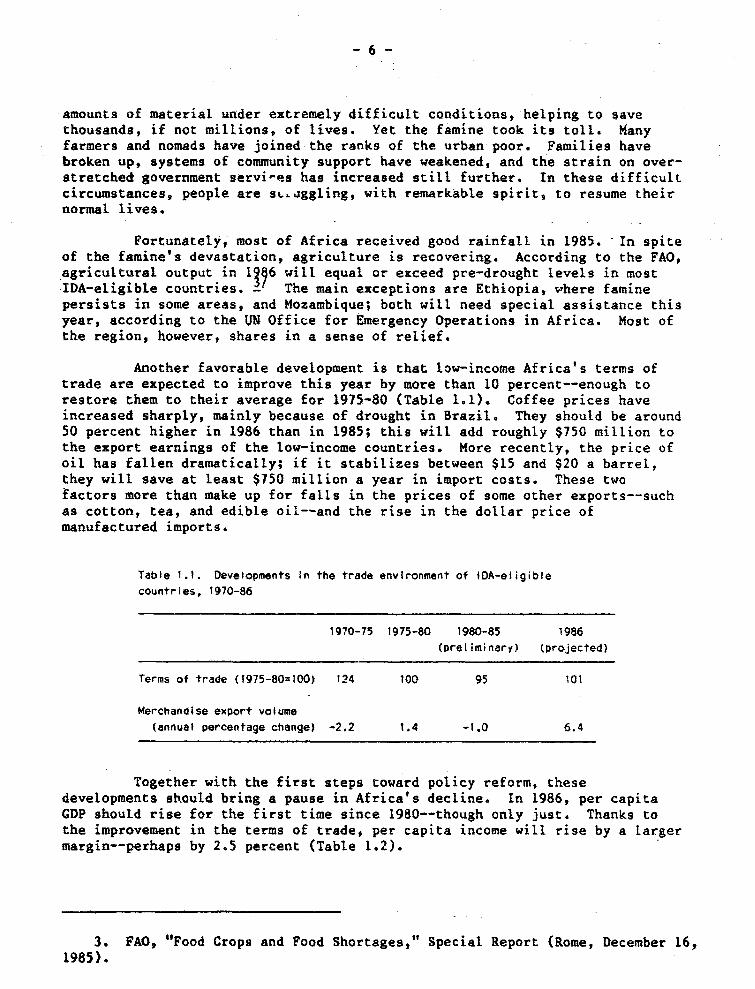

Another favorable development is that low-income Africa' s terms of

trade are expected to improve this year by more than 10 percent--enough torestore them to their average for 1975-80 (Table 1.1). Coffee prices haveíncreased sharply, mainly because of drought in Brazil. They should be around50 percent higher in 1986 than in 1985; this vill add roughly $750 million tothe export earnings of the low-income countries. More recently, the price ofoil has fallen dramatically; if it stabilizes between $15 and $20 a barrel,they will save at least $750 million a year in import costs. These twofactors more than make up for falls in the prices of some other exports--suchas cotton, tea, and edible oil--and the rise in the dollar price ofmanufactured imports.

Table 1.1. Developments in the trade environment of fDA-eligible

countries, 1970-86

1970-75 1975-80 1980-85 1986

(prel iminary) (projected)

Terms of trade (1975-80=100) 124 100 95 101

Merchandise export volume

(annual percentage changeJ -2.2 1.4 -1.0 6.4

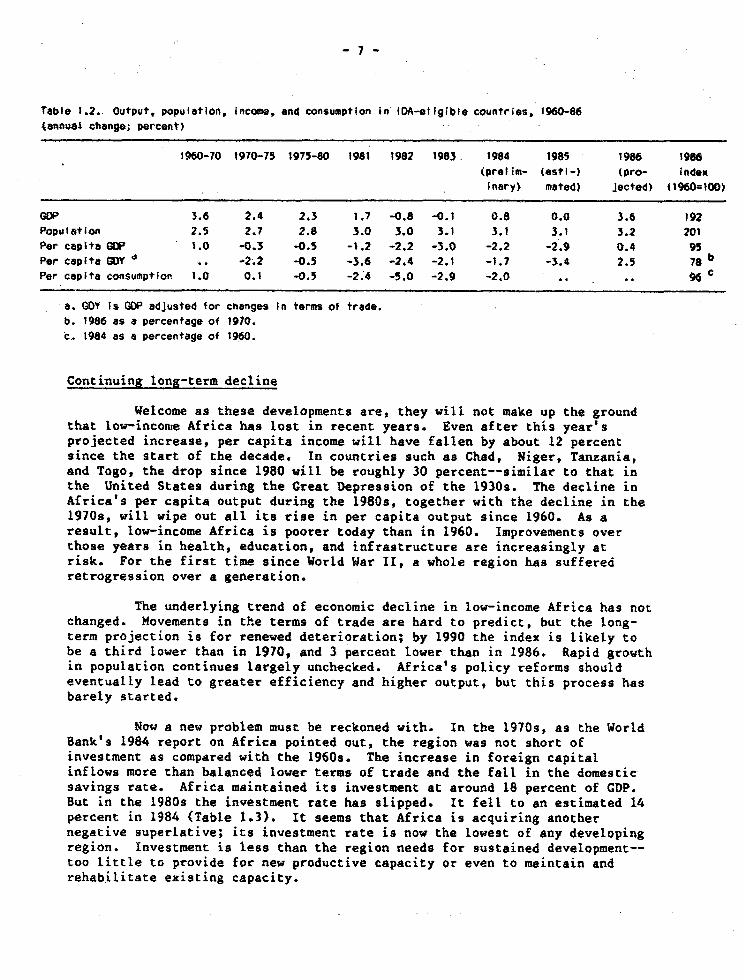

Together with the first steps toward policy reform, thesedevelopments should bring a pause in Africa's decline. In 1986, per capitaGDP should rise for the first time since 1980--though only just. Thanks tothe improvement in the terms of trade, per capita income will rise by a largermargin--perhaps by 2.5 percent (Table 1.2).

3. FAO, "Food Cropa and Food Shortages," Special Report (Rome, December 16,1985).

-7-

Table 1.2. Output, popufation, incomo, end consumption in IDA-etlgible countries" 1960-86

<ennuel chango; percent)-

1960-70 1970-75 1975-80 1981 1982 1983 1984 1985 1986 1986

(prelim- (esti-> (pro- Index

Inary> mnted) jecte4) 01960=100>

GDP 3.6 2.4 2.3 1.7 -0.8 -0.1 0.8 0.0 3.6 192PopuIation 2.5 2.7 2.8 3.0 3.0 3.1 3.1 3.1 3.2 201Por capita GDP 1.0 -0.3 -0.5 -1.2 -2.2 -3.0 -2.2 -2.9 0.4 95Por cepita GDY .. -2.2 -0.5 -3.6 -2.4 -2.1 -1.7 -3.4 2.5 78 bPer cepita consueption 1.0 0.1 -0.3 -2.4 -5.0 -2.9 -2.0 .. C

e. GDY Is GDP adjusted for changes i¡ teras of trade.

b. 1986 es a percentage of 1910.c. 1984 es a percentege of 1960.

Continuing long-term decline

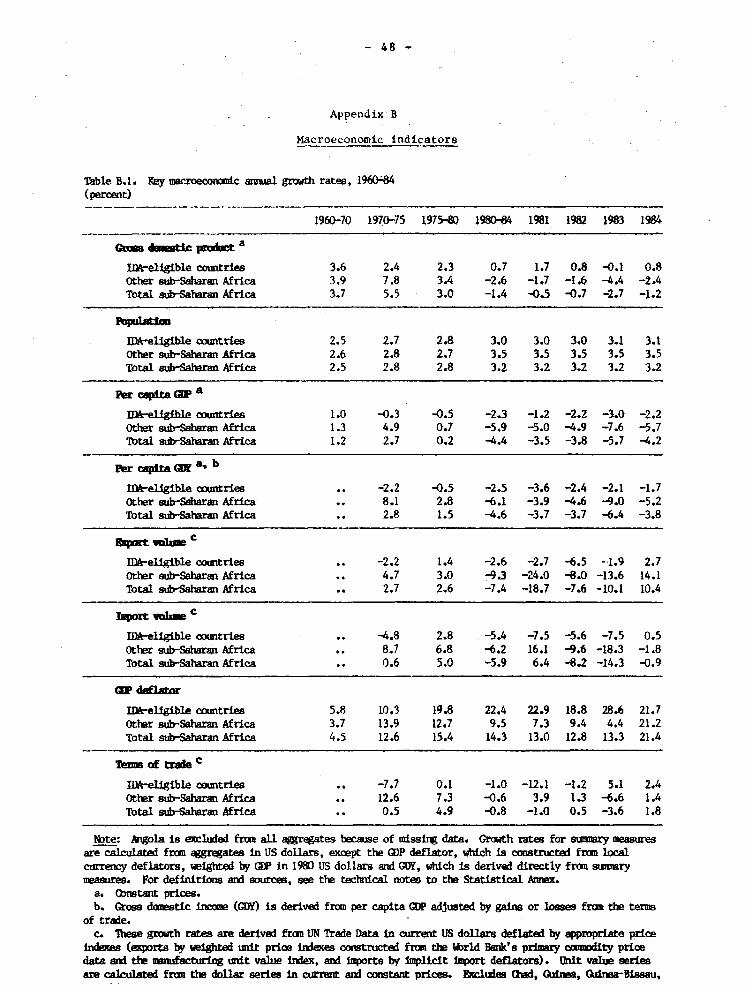

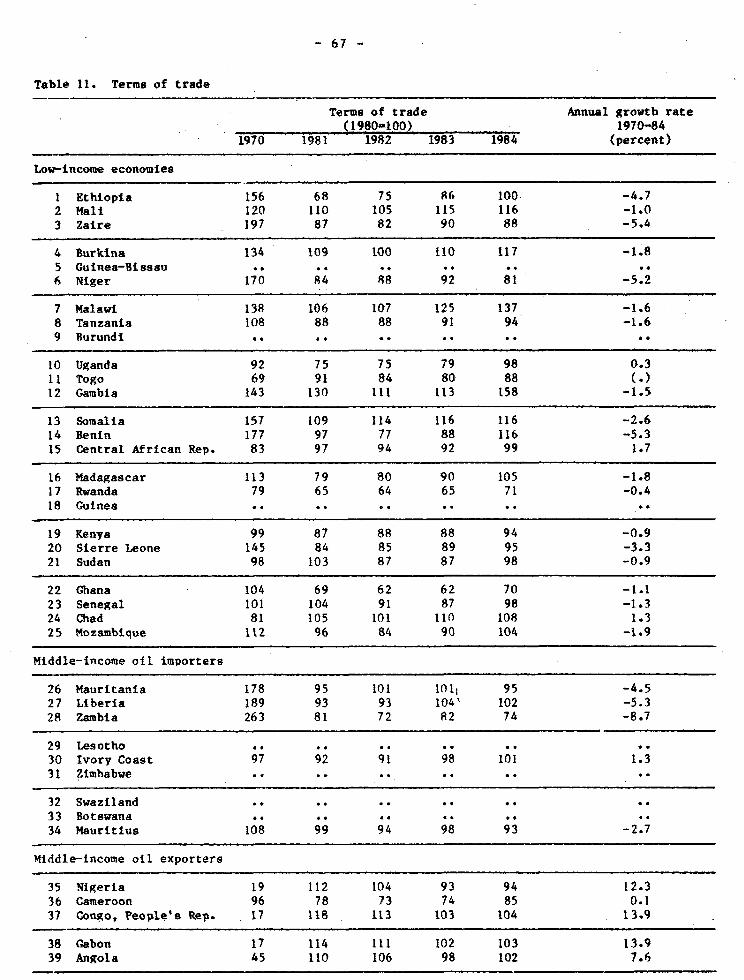

Welcome as these developments are, they wíll not make up the groundthat low-inconie Africa has loSt in recent years. Even after thís year'sprojected increase, per capita income will have fallen by about 12 percentsince the atart of the decade. In countries such as Chad, Niger, Tanzania,and Togo, the drop since 1980 will be roughly 30 percent--similar to that inthe United States during the Creat Depression of the 1930s. The decline inAfrica's per capita output during the 1980s, together with the decline in the19709, will wipe out all ita rise in per capita output since 1960. As aresult, low-income Africa is poorer today than in 1960. Improvements overthose years ín health, education, and infrastructure are increasingly atrísk. For the first time since World War II, a whole region has sufferearetrogression over a generation.

The underlyíng trend of economic decline in low-income Africa has notchanged. Movementa in the terms of trade are hard to predict, but the long-term projection is for renewed deterioration; by 1990 the index is likely tobe a third lower than in 1970, and 3 percent lower than in 1986. Rapid growthin population continues largely unchecked. Afríca's policy reforms shouldeventually lead to greater efficiency and higher output, but this process hasbarely started.

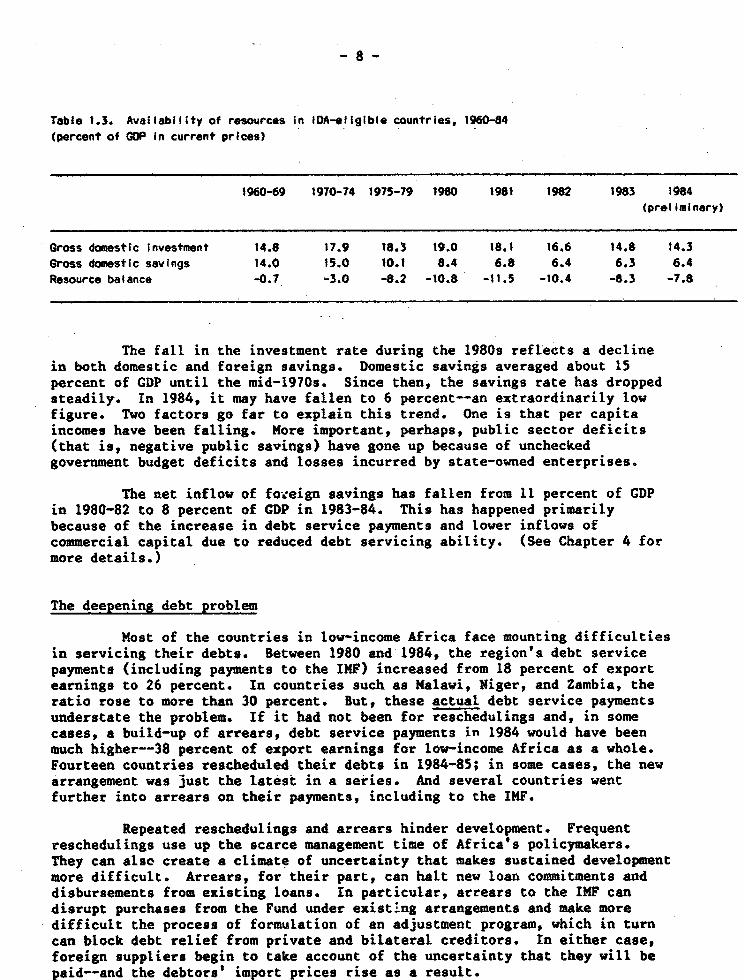

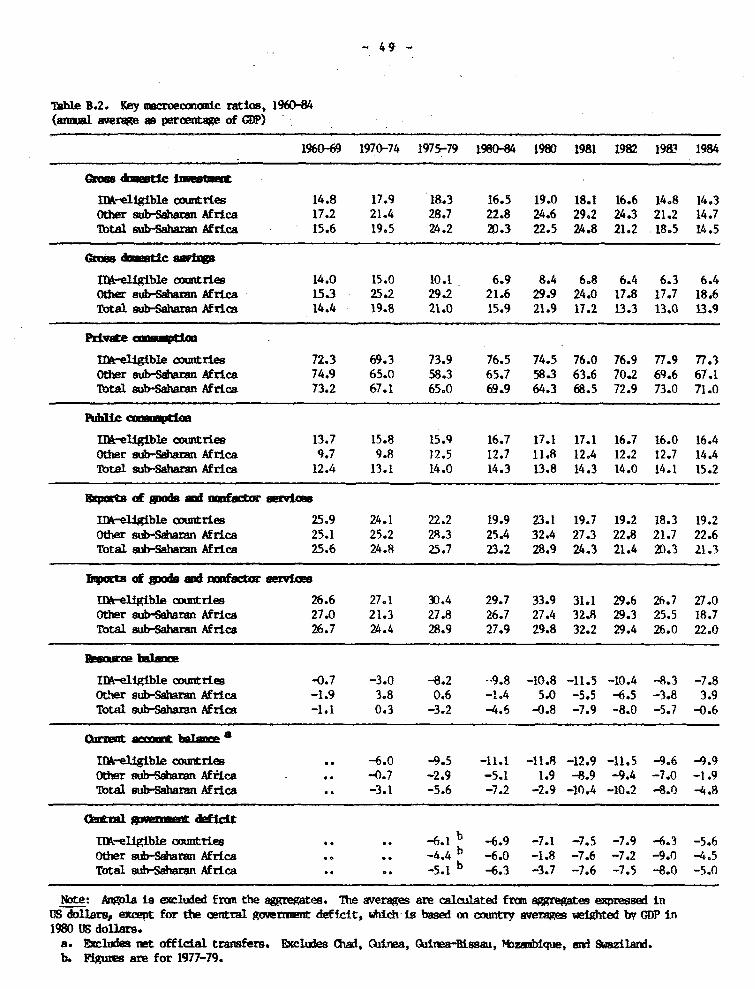

Now a new problem must be reckoned with. In the 1970s, as the WorldBank's 1984 report on Africa poínted out, the region was not short ofinvestment as compared with the 1960s. The increase in foreign capitalinflows more than balanced lower terms of trade and the fall in the domesticsavings rate. Africa maintained its investment at around 18 percent of GDP.But in the 19809 the investment rate has slipped. It fell to an estimated 14percent in 1984 (Table 1.3). It seems that Africa is acquiring anothernegative superlative; its investment rate ja now the lowest of any developingregion. Investment ¡a leas than the region needa for sustained development--too little to provide for new productive capacity or even to maintain andrehabilitate existing capacity.

Table 1.3. Avallability of resaurces in ¡DA-elígible countries, 1960-84

(percent of GDP in current prices)

1960-69 1970-74 1975-79 1980 1981 1982 1983 1984

(preliminary)

Gross domesttc investment 14.8 17.9 18.3 19.0 18.1 16.6 14.8 14.3

Gross daomestic sevings 14.0 15.0 10.1 8.4 6.8 6.4 6.3 6.4

Resource balance -0.7 -3.0 -8.2 -10.8 -11.5 -10.4 -8.3 -7.8

The fall in the investment rate during the 1980s reflects a declinein both domestic and foreign savings. Domestic savings averaged about 15percent of GDP until the mid-1970s. Since then, the savings rate has droppedsteadily. In 1984, it may have fallen to 6 percent--an extraordinarily lowfigure. Two factors go far to explain this trend. One js that per capítaincomes have been falling. More important, perhaps, public sector def£cita(that is, negative public savings) have gone up because of uncheckedgovernment budget deficits and losses incurred by state-owned enterprises.

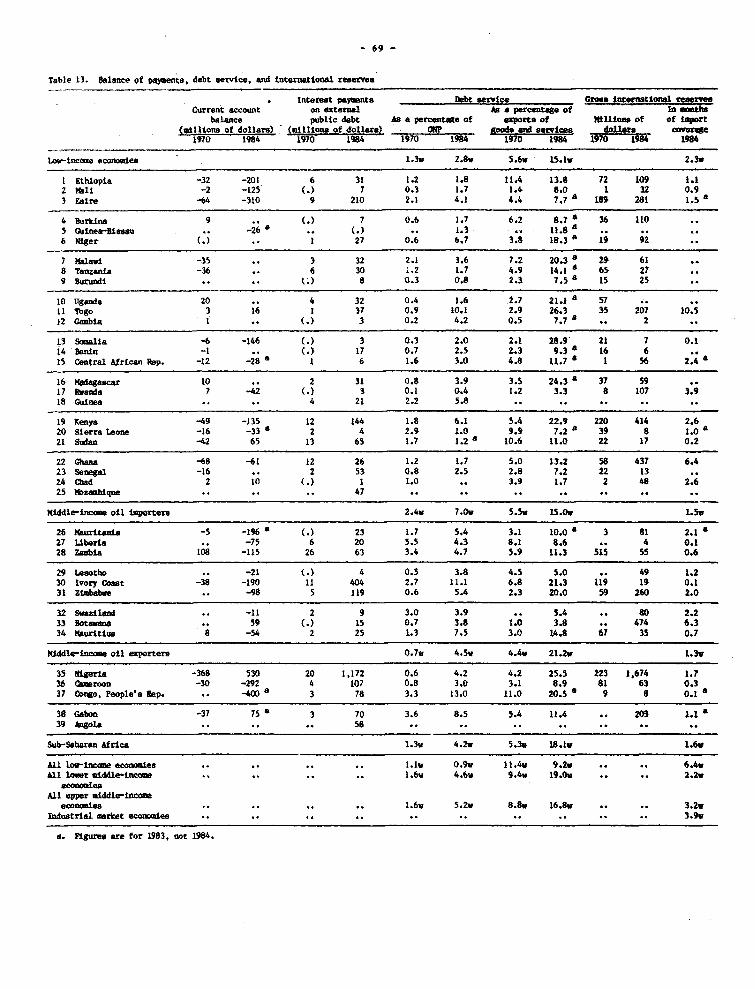

The net inflow of fo-.eign savings has fallen from 11 percent of GDPin 1980-82 to 8 percent of CDP in 1983-84. This has happened primarilybecause of the increase in debt service payments and lower inflows ofcoomnercial capital due to reduced debt servicing ability. (See Chapter 4 formore details.)

The deepening debt problem

Most of the countries in low-income Africa face mounting difficultiesin servicing theír debts. Between 1980 and 1984, the region's debt servicepayments (including payments to the INF) increased from 18 percent of exportearnings to 26 percent. In countries such as Malawi, Niger, and Zambia, theratio rose to more than 30 percent. But, these actual debt service paymentsunderstate the problem. If it had not been for reschedulings and, in somecases, a build-up of arrears, debt service payments in 1984 would have beenmuch higher--38 percent of export earnings for low-income Africa as a whole.Fourteen countries rescheduled their debts in 1984-85; in some cases, the newarrangement was just the latest in a series. And several countries wentfurther into arreara on their payments, including to the IMF.

Repeated reschedulings and arrears hinder development. Frequentreschedulinga use up the scarce management time of Africa's policymakers.They can also create a climate of uncertainty that makes sustained developmentmore difficult. Arreara, for their part, can halt new loan commitments anddisbursements from existing loans. In particular, arrears to the IMF candisrupt purchases from the Fund under existing arrangements and make moredifficult the process of formulation of an adjustment program, which in turncan block debt relíef from private and bilateral creditora. In either case,foreign suppliers begin to take account of the uncertainty that they will benaid--and the debtors' imDort Drices rise as a result.

-9-

Without action by the development community, these problems willmount during the next few years (see Chapter 4 and Appendix A). A dozen low-income countries face particularly severe debt problems and for them presentrescheduling arrangements will be inadequate. - Even with rescheduling onconventional termo during the next few years, their debt burden will still behigh at the end of the century.

A strategy of adjustment with growth

If Africa's decline ís to be reversed, action is needed on threefronts. First, the region needs more resources for investment--both foreignand domestic. Second, it must use new and existing resources moreefficiently. Third, it must curb its growth in population.

The basic objective of further adjustment is to stimulate growth.Thar requires more resources. Some of the additional resources can come fromhigher domestic savings. Prudent fiscal and monetary polícies are essentialfor that purpose. But domestic savings cannot carry the whole burden.

A consensus is emerging in the international community thatconcessional capital inflows to the low-income countries of Africa shouldrise, at least for the rest of this decade. To make medium-term programa ofadjustment with growth feasible, donors must give medium-term indications oftheir plans for aid and debt relief. Programs can then be designed on alonger-term basis to give adequate attention to the tasks of developing humanresources, conserving natural resources, and maintaining or extendinginfrastructure. A clearer picture of the resources to be available would alsopromote stability in trade and credit regimes. Domestic and foreign privatesectors would then feel more confident about the outlook for imports mdcredit and could play a more active role in stimulating growth.

In judging the prospecto for adjustment with growth ín low-incomeAfrica, it is important to realize that the region's performance has not beenuniformly poor. The region has its succesa storíes, some of which are betterthan average for the developir.g world. This is true both for sustaineddevelopment and for medium-term adjustment. At least seven countries in sub-Saharan Africa (Botswana, Cameroon, Ivory Coast, Kenya, Malawi, Nauritius, andRwanda) achieved significant growth ín per capita income over the last twenty-five years; four of them (Botswanas Cameroon, Ivory Coast, and Mauritius) havegraduated from low-income status. Some (Ivory Coast, Kenya, Malawi, andMauritius) launched unsustainable public expenditure programs during theperiod of commodity price boom in the mid-1970s, but then adopted atructuraladjustment programs in the early 1980s and by 1985 had made substantialprogress. For each area of policy Africa can report some success. Forexample, exchange rate policy in Malawi; food marketing in Cameroon; exportcrop pricíng in Kenya; export promotion in Mauritius; family planning inMauritius and Zimbabwe; and management of windfall income and technicalassistance in Botswana.

4. Benin, Gambia, Liberia, Madagascar, Mali, Mauritania, Miger, Somalia,Sudan. Tanzania. Toto. and Zambia.

- 10 -

A detailed strategy for 1986-90, which translates general aims intospecific programs, can be formulated only at a country level--but someelements that all such programs should include are discussed in the chaptersthat follow. Two sets of issues are important. The first, discussed inChapter 2, concerns the effíciency of reesorce use. It involves three mainareas of policy that were highlighted in earlier reports:

o Exchange rateso Urban-rural biaso - Public sector management.

The second set of issues, discussed in Chapter 3, covers longer-termconstraints on development; these were also identified in earlier reports:

o Population growtho Healtho Educationo Deforestationo Agricultural research.

Chapter 4 then goes on to assess the external capital and donorinstitutíonal reforms required to support these programs of adjustment withgrowth.

A crucIal objective of the proposed programs is to stimulate outputand exports by correcting discrímination agaínst the rural sector. This is tobe done through reduction ín price distortions and in urban bias in theallocation of government and aid expenditures. Most of the poor in low-incomeAfrica live in rural areas; so these improvements should promote equity asvell as growth. Rarely will the poor be the principal losers from suchprogramse

- 11 -

2. Adjustment programs

For some time Africa's own regional institutions have been leading achange in attítudes toward development policy. The most recent jointreport by the Ec omic Comnission for Africa and the African Development Bankas one example. - It argued that mistaken policies have depressedagricultural output and industrial productivity, promoted inefficiency instate-owned enterprises, and damaged incentives for the domestic privatesector. The Organisation of African Unity's summit meeting in July 1985echoed the theme by adopting "Africa's Priority Programme for EconomicRecovery, 1986-90." This too stressed the importance of agriculture, and theneed for new industrial policies that give the private sector a largereconomic role, and for more active population programs. This shift in Africanthinkiug toward a more pragmatic approach to development. is important andencouraging.

But new thinking is only a first step. Successful adjustment meansadopting new policies, not merely agreeing that they are desirable. How muchhas the region actually achieved? Thia is hard to answer precisely, becauseimprovemento consist of many different changes in many dífferent countries.Nonetheless, progress ¡a clearly under way.

Especially in the past two years, more countries have started toact, and the changes they are making go deeper than before. Several countriesillustrate the trend. Togo, Ghana, and Zaire have reinforced thecomprehensive economic and financial reforme which they introduced in 1983.In 1984-85, Senegal, Mauritania, Zambia, and Guinea adopted similar policies--aiming to improve broad macroeconomic performance, as well as to assistindividual economic sectors. Other countries, such as Niger, Mali andMadagascar, continue to adopt important policy reforms, though more slowly.The reform movement seems likely to endure, and perhaps to gather pace, asmore countríes see the resulta in those that have ted the way.

These reforma cover a wide range of measures aimed at giving príces,marketa, and the private sector a greater role in promoting development inAfrica. In particular, they reflect a desire to reduce administrativeintervention in setting prices; to end monopolies on trade and marketing; andto reduce the government's role in allocating credit and to increase the scopefor prívate sector activity. Changes are needed on a broad front, but thischapter focusea on three areas which were highlighted in the World Bank'sprevious Africa report: exchange rates, urban-rural bias, and public sectormanagement.

1. Economic Report on Africa, 1985.

-12-

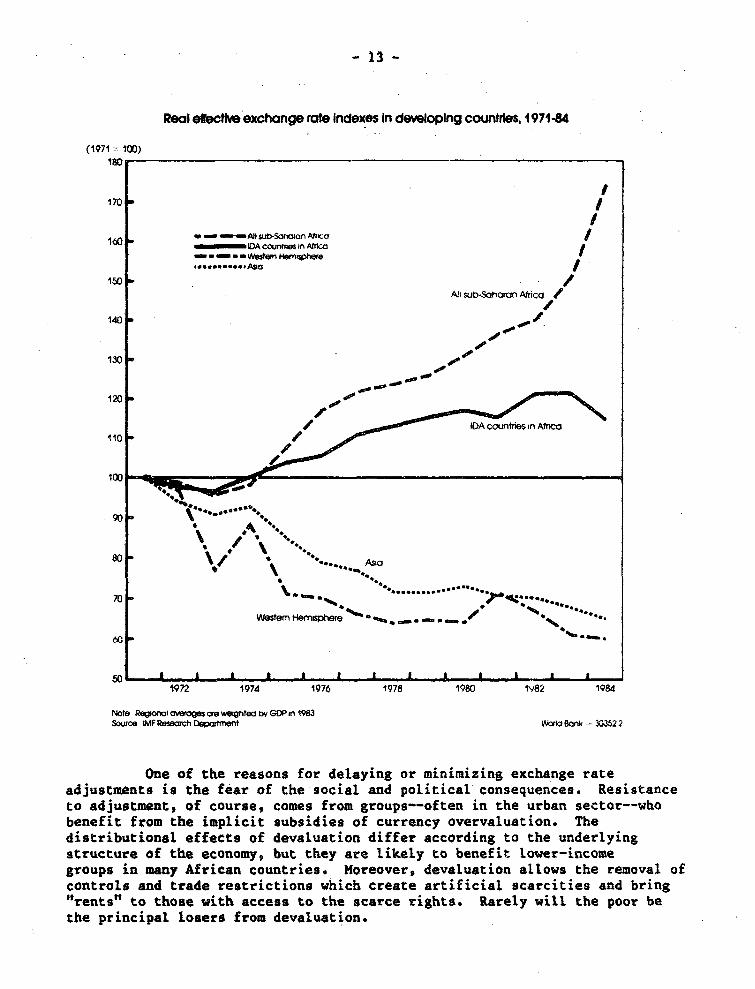

Correcting overvalued exçhange rates

Correcting overvaluation of currencies helpa to reduce balance ofpayments deficita. Equally important, it also shifts the internal termsa oftrade in favor of those who produce for export (often mainly rural households)and away from those who consume imports (often predominantly urbanhouseholda). In the past two years, several countries have made progress inthis area. After more than a decade of creeping appreciation, the averagereal effective exchange rate for the IDA-eligible countríes in Africa began todepreciate ín 1984, and this trend seema to have continued into 1985. Agrowing number of governments have adopted more flexible exchange rateregimes, which rely on supply and demand in the foreign exchange market todetermine the exchange rate.

Following a huge devaluation, Zaire introduced a floating ratesystem in 1983, and by 1984 the exchange rate was freely determined ín aninterbank market. By the end of 1984, the real effective exchange rate hadfallen by three-quarters znd the premium on the parallel market was no morethan 10 percent, roughly in line with the cost of bank commissions. In late1985, Zambia introduced an auction system for most trade-related exchangetransactions. Although the government and selected public enterprisescontinue to receive an administrative allocation of foreign exchange, thevalue of foreign exchange is determined by the auction. After theintroduction of the new system, the nominal exchange rate fell by two-thirdsin three weeks.

Guinea and Gambia are establíshing similar systems intended to leadto a unified. market-determined exchange rate; as an interim measure inGuinea, the new rate has been devalued to less than 10 percent of the oldofficial rate. Madagascar took a step toward more flexible exchange rates inMarch 1984; it began to adjust the Malagasy franc every quarter in line withthe change ín the consumer price index during the previous quarter. Betweenthen and the third quarter of 1985, the real effective exchange ratedepreciated by about 15 percent and was brought in line wíth its 1978 level.Other countríes (Ghana and Mauritania) have made substantial devaluationswithin their existing exchange rate systems, by combining vigorous nominaldevaluations with effective measures to contain inflation.

These are promising developments. However, for the low-íncomecountries as a group, the average real effective exchange tate appreciatedsignificantly in the 1970s and early 1980s--a marked contrast to theperformance of Asian and Latir American countries (see Figure 2.1>. As oflate 1985, in spite of the recent adjustments, the real effective exchangerate was about 15 percent above ita 1970-72 levels. Moreover, even the 1970-72 level ¡a too high for some countries, especially where terms of tradeshifts have been large and negative. Por example, in Zaire and Zambia,market-determined real effective exchange rates had fallen at the end of 1985by over 40 percent from their level in 1970-72. The progreso observed in1984-85 is important, but only part of a long proceso that still has far togo.

- 13 -

Real efecthe exchange rte Indoxes In devMeoping countrles, 1971-84

(1971 = 100)

170 u

160 - ~ -A1i su-tSafaan ~co atO - iD A cournes ín Af

_ * _ * _ I.Ist6Y emli1erre<,o --- ,ss..ee.e.ASI/

150 b...

Ait sub-Sahoran Africa /

140

130 --

120 -» --

- «/ IDA countriesb Afnca110

100

-

i ,

o~~ S

80 < s *'-",."..A5se

70 '

Western HeiBmsphee %. * _ '41 _ *o

1972 1974 1976 1978 1980 1V82 1984

Note Regional ove s ae weghted by GDP in 1983Sourca iMF Prch m WoW Bank - 3352 2

One of the reasons for delaying or minímizing exchange rate

adjustments is the fear of the social and political consequences. Resistance

to adjustment, of course, comes from groups--often in the urban sector--who

benefit from the implicit subsidies of currency overvaluation. The

dístributional effects of devaluation diffet aecording to the underlyingatructure of the economy, but they are likely to benefit lower-income

groups in many African countries. Moreover, devaluation allows the removal of

controls and trade restrictiona which create artificial scarcities and bring"rents" to those with acceso to the acarce rights. Rarely will the poor be

the principal losera from devaluation.

- 14 -

However, because of the impact on the urban population, it isimport-ant to time devaluations with care. The economic developuients of1985-86 make 1986 a good year to act decisively on exchange rate adjustment.Lower food prices, following recovery from the drought, together with lowerpetroleum import prices, can cushion the impa,t of devaluation on the towns;at the same time, devaluation would help raise the farm prices of agriculturalexports and partly offset the effects of lower food prices on farmers.

Correcting urban-rural bias

There is a growing consensus in Africa that policies whichdiscriminate against ag-riculture and favor the urban sector must be changed.There are at least three links between farming and development in low-incomeAfrica. First, the largest part of the population and the majority of thepoor depend on agriculture for a living. It will therefore be difficult toattack poverty on a broad front so long as the sector ¡a discriminatedagainat. Second, the region's output ís still heavily agricultural. Higheroutput will require incentives for improved productivity in farming. Third,exporta, too, will be mostly agricultural for the medium term. But they willbe slow to rise as long as governments channel the profits mostly to benefittheir urban populatíons.

Devaluation, as noted earlier, can be a powerful instrument toredress the urban-rural bias. It can simultaneously mean higher farm pricesfor agricultural exports and higher prices for the imported goods that areconsumed mostly in the towns. But correcting the urban bias requirescomplementary changes in domestic policy. These include hígher farm prices,lower agricultural taxation, more flexíble marketing arrangements, and wagerestraint in the urban sector, as well as more public expenditure in the ruralareas. Over the past two to three years, many governments in low-incomeAfrica have introduced reforms in these areas.

Many governments have improved agricultural incentives by increasingoffícial príces ín conjunction with a currency devaluation. Some have done itby deregulating markets, to give farmers access to higher prices on parallelmarkets. Others are introducing more flexible systems of offícial pricing asa step toward lifting controls on agricultural trade.

There ís a clear trend toward higher food-crop prices, In 1984,following substantíal devaluations, the government of Zambia raised theofficial producer price of maize by over 35 percent (a 12 percent increase inreal terms). In Tanzania, the government more than doubled the controlledproducer price of maize between 1983 and 1985 (a one-third increase in realterms). In 1985, Mauritanía set ration shop cereal prices in líne with theprice of imported grain. In Zaire following devaluation and deregulation offood marketing, producer prices are estimated to have doubled for maize andtripled for cassava between 1983 and 1984 (which amounted to at least adoubling of these prices in real terms since 1980). As part of a reformpackage including massive devaluation, in early 1986 Guinea decontrolledproducer prices for food crops and quadrupled the official wholesale price ofimported ríce.

*- 15 -

A number of countries are making similar efforts to improveincentives for export crops. Ghana, after large devaluationa in 1984-85,tripled the price of cocoa between 1983 and 1985 (a 50 percent íncrease inreal terms). Zambia raised the price of cotton, and Zaire raised the pricesof both coffee and cotton; in both countries, these price increases followedsubstantial currency devaluatíons.

Another clear illustration of this trend is that the countriesimplementing reforms duríng the 1980s have seen crop prices rise much fasterthan urban incomes. The disparity was sometimes dramatic--as in the case ofmaize in Zaire and rice in Madagascar. In most cases, farm prices foz exportcrops also improved relative to urban incomes, though less so than food-cropprices.

Examples of some dramatic shifts in urban-rural íncome ratíosinclude Tanzania during 1980-84, when real farm incomes are estimated to haverisen by 5 percent, while urban vage earners faced a decline of 50 percent.In Ghana, during the same petiod, farm incomes stagnated but urban incomesfell by 40 percent in real terms. Per capita incomes have fallen in low-income Africa during the 1980s, while real producer prices have risen or atleast remained constant ini most of the countries that have adopted reformprograma. This leaves little doubt that the reforming governments have helpedto raise the terma of trade between the countryside and the city.

In agriculture, it is hard to separate the effects of better weatherfrom the effects of better prices and better policy. But the response ofagriculture in the countries that have adopted improved incentives has beentoo dramatic to dismiss. In Ghana, cocoa output in 1985-86 is expected to be25 percent above the level of two years earlier--though it will still be lowerthan the pre-drought level of 1981-82. After a price increase of over 300percent in 1983, maize production tripled in 1984, rising above the pre-drought level by almost two-thirds. In Zambia, cotton and maize prodxctionrose by over 20 percent during 1983-85. The amount of maize marketed lsestimated to have risen by over 55 percent during 1984-85; it came close tomeeting Zambia's domestic consumption requirementa for the first time since1976. In Togo, cotton production is estimated to have doubled between 1984and 1985.

Incentives for farmers have improved, but there is room for furtherprogreso. The producer ahare of the international price of exports remainsrelatively love For coffee, cocoa, and cotton--low-income Africa's principalagricultural exports-farmers in the main exporting countries generallyreceived only about half of the export unit value in 1984. Coffee farmers inKenya were an important exception, usually receiving as much as 90 percent ofthe export price. By contrast, in Tanzania, the producer share for coffee was40-50 percent, and in Madagascar it was only about 20 percent in 1984-85.During these years, for cocoa, the share ín Togo was about 40 percent, and forcotton, the share in Mali and Togo was as low as 30 percent.

Two recent reforma in this area may be a guide for othercountries. in 1984-85, Cameroon's national marketing board atartedímplementing a system of rebates to coffee and cocoa farmers; it is estimated

- 16 -

that ít will increase theír share of the export price by 7-8 perce.nt. In late1985, Guinea said the state marketing agency would pay coffee and palmproducera 80 percent of export prices, and raised official buying pricessubstantially.

Conditions in 1986 seem right not just for initiatives on exchangerate policy, but also for other policies to correct the urban-rural bias.Higt food output has helped ease consumer prices in many countries. Thiscreites an opportunity for governments to dismantle price and marketingcontrols an¿ to eliminate food marketing subsidies with fewer fears of theeffects on inflation. Lower prices for food and petroleum should also dampeninflation. Hence, 1986 will be a good year to try to restrain urban andpublic sector wage increases. Furthermore, in those areas where excessproduction threatens to depress the market, deregulation, incl.uding freerintr¿regional trade, could help to maintain producer pricés and at the sametime help consurmera in areas with shortages.

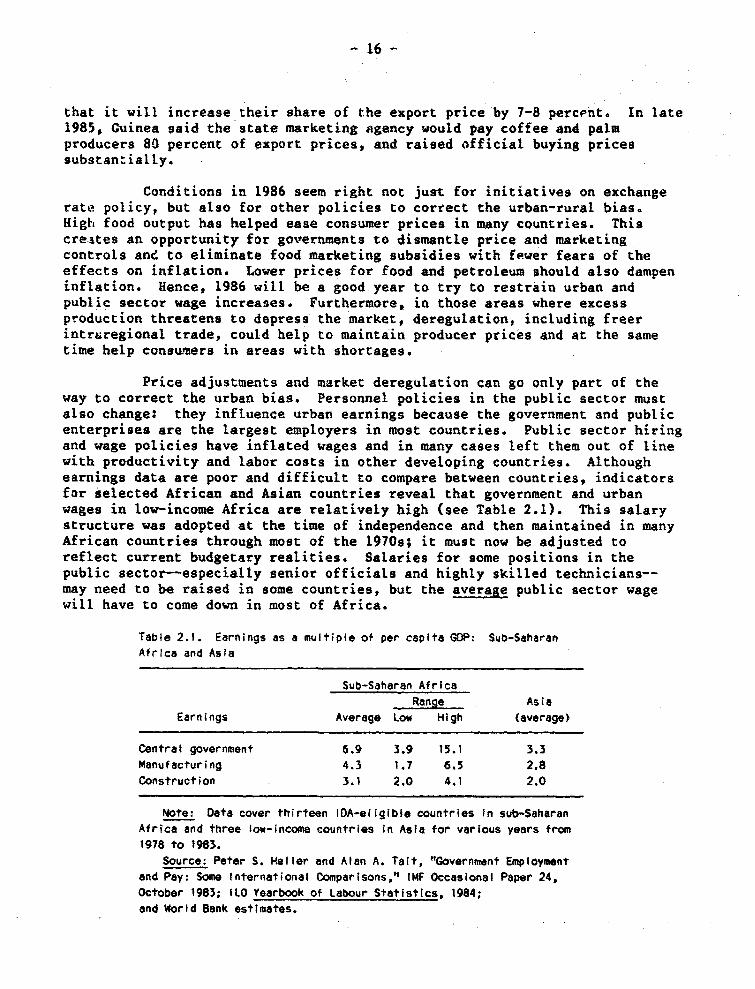

Price adjustments and market deregulation can go only part of theway to correct the urban bias. Personnel policies in the public sector mustalso change: they influence urban earnings because the government and publicenterprises are the largest employers in most countries. Public sector hiringend wage policies have ínflated wages and in many cases left them out of línewith productivity and labor costa in other developing countries. Althoughearnings data are poor and difficult to compare between countries, indicatorsfor selected African and Asian countries reveal that government and urbanwages in low-income Africa are relatively high (see Table 2.1). This salarystructure was adopted at the time of independence and then maintained in manyAfrican countries through most of the 1970s; it must now be adjusted toreflect current budgetary realities. Salaries for some positions in thepublic sector--especially senior offícials and highly skilled technicians--may need to be raised in some countries, but the average public sector wagewill have to come down in most of Africa.

Table 2.1. Earnings as a multipie of per capita GDP: Sub-SaharanAfrica and Asia

Sub-Saharan AfricaRange Asia

Earnings Average Low High (average>

Central government 6.9 3.9 15.1 3.3Manufacturing 4.3 1.7 6.5 2.8Construction 3.1 2.0 4.1 2.0

Note: Data cover thirteen IDA-eligible countries in sub-SaharanAfrica and three low-income countries in Asia for various years from1978 to 1983.

Source: Petar S. Heller end Alan A. Tait, "Government Employmentand Pay: Some International Comparisons," IMF Occasional Papar 24,October 1983; 110 Yearbook of Labour Statistlcs, 1984;and World Bank estimates.

- 17

Rationalízing the public sector

The role of the atate in the economies of sub-Saharan Africa islarger than in other regions. Public sector employment is half of all modernsector employment, compared with only one-third in Asia. Allowing for countrysize, public enterprises are more numerous than in most other developingcountries, and they engage in a wider array of activities. Public investmentaccounts for the bulk of investment in the formal sector.

As the Bank's previous reports on Africa have argued, the rapidgrowth of the pubLic sector, along with its inefficient management andoverambitious public investment programs, are ímportant reasons for theeconomic difficulties facing sub-Saharan Africa today. In addition, the scopeof public sector activities and the operating subsidies to which publicenterprises had access atifled private entrepreneurial activity inagriculture, industry and commerce. Many governments in sub-Saharan Africanow face financial dífficulties and are therefore trying to reduce the size ofthe public sector and to improve its management. However, these reforms arestill at an early stage.

Financial stabilization programa are begínning to reduce governmentexpenditures. Public consumption as a percentage of GDP in low-income Africadeclined from 17.1 percent in 1980-81 to 16.2 percent in 1983-84. Thisdecline happened alongside the fall in GDP. As a result, public consumptiondeclined by 1.5 percent a year in real terms during 1980-84, compared with anincrease of almost 5 percent a year in 1975-80. These cuts have beenachieved, in part, by restraints on public employment. In the past few years,Rwanda, Mali, Somalia, and Togo have abandoned their policy of automaticemployment of secondary school and university graduates. In 1984, the shareof personnel ín total central government expenditures declined for the firsttime in several years in Mali because of slower growth in governmentemployment as a result of the introduction of competitive examinations forentry to the civil service. The SomaLi government froze government empLoymentin 1985. Togo reduced total government employment by 1.6 percent in 1984.

Budget restraint, reflected in lower public employment, is desirablein much of Africa, but ín some cases it has led to excessive cuts in financingfor equipment, maintenance, operating costs, and materials. The result hasbeen a steady deterioration in the quaLity of public services and furtherdeclines in the productiíity of public employees. The impact is plain whenroad maintenance crews lack fuel and bitumen to accomplish their work, whenteachers lack books, chalk, and even classrooms for their students, and whenhealth workers have no medicines to distribute. This deterioration in publicservices is especially disruptive for programs designed to deal with the basicconstrainta on development. Unless a better balance is established betweenpersonnel and other expenditures, these programs are in jeopardy. To maintainnonwage expenditures, most countries must reduce government employment and, insome instances, civil service wages.

Efforts to rationalize the public enterprise sector have focused onimproving management as well as reducing it9 size. Studies and audits aregenerally followed by closure of nonviable enterprises, by divestiture of

- 18 -

nonstrategic enterprises, or by carefully taílored rehabilitation ofenterprises (such as utility companies) -selected to remain ín the publicsector. Most of these efforts involve institutional reforms to strengthengovernment supervision.

Low-income Africa's governments have closed down or divested about 5percent of their public enterprises during the 19809. For many of those thatremain, better management has cut operating losses--through hígher prices,better cost accounting, and (usually) reduced employment. In Ghana, theaggregate net loases (before taxes) of approximately a hundred publicenterprises felL in 1983 to 20 percent of their 1982 level. In the Gambia,net losses after taxes of seventeen public enterprises fell in 1984 to about30 percent of the 1982-83 level. Be en 1981 and 1984, the operatingdeficita of thirteen key public ente.prises in Mali fell by over 50 percent.In 1985, Ghana's Cocoa Marketing Board--the country's largest public sectoremployer--dísmiased 19,000 employees, a third of its payroll. In Mali, about10 percent of public enterprise employees were fired in early 1984. However,reductions made in one area can sometimes be offset by increased employmentelsewhere. In Benin, for example, the central government rehired many of theworkers who lost their jobs when some provincial public enterprises closeddown.

Of the countríes that are trying to reform their public enterprises,Senegal and Zaire are especially interesting. In Senegal, the government andaix public enterprises have signed formal agreemento (contract programs) whichestablish objectives and performance indicators and set out the reciprocalobligations of the government and the enterprises. Compared with other publicenterprises, these firma have had higher sales growth and lower personnelcosta.

In 1984, Zaire introduced a series of reforms, and for some largepublic enterprises, these measures have started to bear fruit. Substantialrestructuring of the mining sector, together with devaluation and tax reforms,have vastly improved the financial situation of CECAMINES. After two years ofsubstantial losses, and despite the continuing loa price of copper, profitsafter taxes amounted to $45 million in 1984 and are expected to have been muchhigher in 1985. In Zairels transport sector, ONATRA--the company responsiblefor river and rail transport between Kinshasa and the port of Matadi--tooksteps to reduce wage costs and raise tariffs. Nov it ía paying divídends tothe treasury for the fírst time in several years. And Zaire's nationalraílway company reduced its losses by over two-thirds since 1983.

The region s governmento have made efforta to reduce the size oftheir public investment programa and to improve the allocation of public fundsto sound, high-priority projectc. Some of the discipline results fromunavoidable financíal austerity. Much of it, though, reflects a greaterappreciation of the importance of including rehabilitation in publicinvestment programa, of keeping investments in line wíth the capacity tofinance recurrent costa, and of using existing productive capacity beforebuilding more. There ja also a growing awareness that amall-scaleinvestments, especially in agriculturea may be more productive than large-acale investments and that large projects of great political appeal butdoubtful economic viability are best postponed or dropped altogether.

-19 -

However, doubtful projects continue to be financed--ostentatiousuniversítiest overdesigned highways, luxury sports stadiums, and uncompetitiveagroindustrial ventures. Often these are financed by donors responding topolitical requests. Sometimes donors fail to appreciate the scarcity ofinvestable funds and the need to devote aid resources to projects that areeconomically sound. And it is odd that finance ¡a sometimes easier to findfor a politically sttractive project of doubtful viability than for support ofexchange and trade adjustment programs or for maintenance and rehabilitationprojects. Most African countries atilL need to strengthen the authority ofthe government agencies that are in charge of planning and project evaluation.

This year, strengthening the planning process is all the moreurgent. The coffee price boom will augment resources availahle to manyAfrican governments. It ís essential that mistakes of the miu-1970s followingcommodity price booms are not repeated, and that extra resources be used tostimulate growth in the near term and to attack the basic constraints todevelopment in the long term. In most of low-income Africa in 1986-90,rehabilitation and maintenance should remain the focus for expenditures oninfrastructure, agriculture, and industry--together with some carefully chosennew investments to remove bottlenecks. However, as the next chapter explaina,in areas concerned with overcoming long-term constraints on growth, it isnecessary to go beyond rehabilitation and maintenance and finance new projectscovering both capital and recurrent expenditure. Projects of doubtfulviability--"white elephants," as the 1984 report called them--must not beallowed to reappear.

- 20 -

3. Long-term constraints on growth

The thrust of structural adjustment in Africa has been toward agreater role for prices, markets, and the private sector in promotingdevelopment. This emphasis needs to continue. However, in areas such asfamíly planning, human resource development, natural resource conservation,and agricultural research, governments must play a larger and more effectiverole. Sub-Saharan Africa has made little progresa in these areas in recentyears. In some cases, services have declined, undoing earlier progresa.

On issues such as family planning, resource conservation, andagricultural research, governments must commit themselves to change andpromote a social consensus in its favor. Consensus must spring from a clearerunderstanding of the link between these long-term factors and prospects for abetter quality of life.

Policy can then build on this by giving programs in these areasgreater priority in the allocation of scarce budgetary and human resources, bystrengthening public institutions where necessary, and by giving privateagencies (including nongovernmental organizations) a much larger role.Increased health and education coverage for a growing population requires,when resources are short, restructured programs which emphasize low-costpreventive health care, primary education, and greater efficiency. Withoutnew policies, the quality and relevance of these services will decline, andthe objectives of universal literacy and greater technical and managerialíndependence will be out of reach.

Population

Lower rates of population growth may well be one of the mostimportant requirements for sustained development in Africa. A recent paperfrom the Worldwatch Institute stated the problem graphically:

If African governments take a serious look at futurepopulation/resource balances...they may discover thatthey are forced to choose between a sharp reduction inbirth rates or falling living standards and, in somecases, rísing death rates. If [they] choose to donothing, the "demographic transition" that has marked theadvance of all developed countries may be reversed forthe first time in modern history. -

1. L. R. Brown and E. C. Wolf, Reversing Africa's Decline (Washington,D.C.: Worldwatch Institute, June 1985), pp. 31-32.

-- 21 -

Until recently, very few African governments recognized theimportance of family planning. Africa's vast empty spaces suggest that manymore people can be accommodated. The problem,-however, ja not that Africalacks the land to support a larger population, but that substantial investmentand other inputs will be needed to make that land sufficiently productive. Ittakes time to mobilize these resources and use them effectívely. The existingrate of population growth is higher than the rate at which the supply ofnutrition, water, health, and education can be increased.

In 1984, at both the Second African Population Conference in Tanzaniaand at the UN International Population Conference in Mexico, Africangovernments appeared ready to adopt a new approach to their policy onpopulation. A recent World Bank study found that about three-quarters ofAfrican countries now endorse family planning, at least fo health reasona,and some have set explicit targets for population growth. _ Increasingly,national leaders are ready to discuss the population problem and the need foraction to deal with it--as, for example, the presidents of Nigeria and Kenyahave done in recent apeeches.

In some cases, such as Malawi, the turnaround in official attitudeshas happened remarkably quickly. In Zimbabwe, provision of contraceptiveservices has expanded rapidly in the past five years, and contraceptive usehas more than doubled. Kenya and Botswana have programs well under way, andseveral other countries--for example, Tanzania, Liberia, Nigeria, Rwanda,Burundi and Malawi--have recently started programs too. As a result, fertilityseens to be falling in some countries. Birth rate- are starting to drop inZimbabwe, which provides good access to family planning services in ruralareas. Kenya, one of the first countries with a major population program,received considerable aid for family planning in the 1970s; ita most recentpopulation surveys show that fertility rates have declined, though onlymarginally, from 8.0 in 1977 to 7.7 ín 1984.

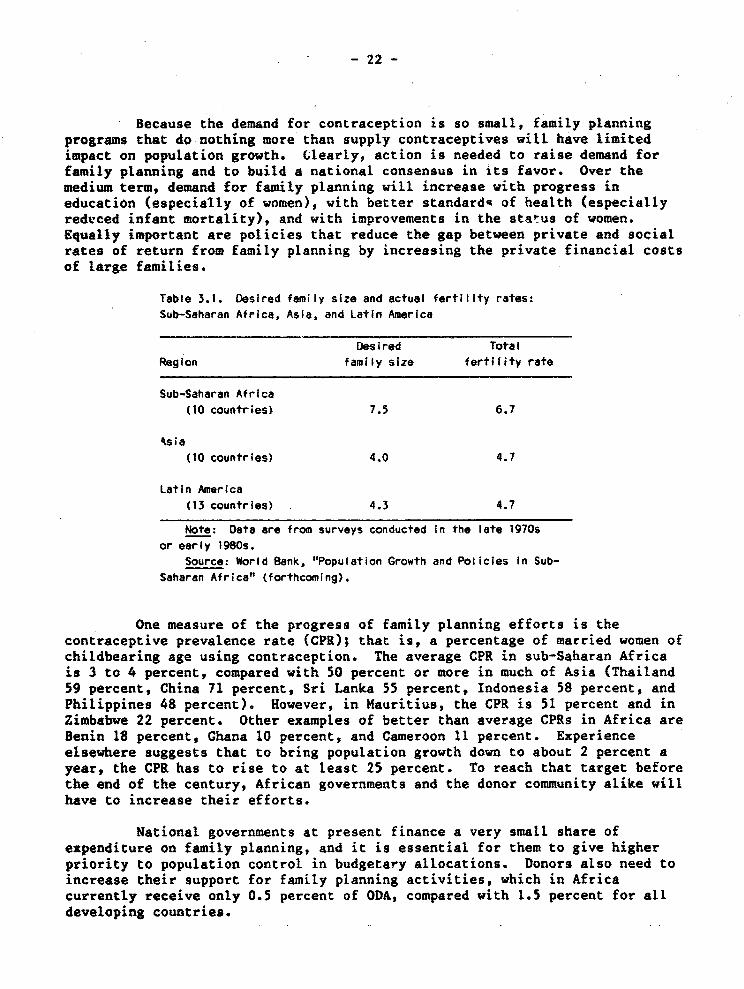

However, the progress achieved so far in sub-Saharan Africa as awhole is small in relation to the task of achieving viable populationgrowth. First, several African countries still take a pronatalist position orshow virtually no support for population control. Second, experience aroundthe world shows that in the difficult area of family planning, governmentsupport is only a begínning. It is not encugh to widen contraceptive choiceand expand channels of access to family planning assistance, however importantthat may be. Poor people in Africa, as elsewhere, find it in their interestto have large families. Desired family size in Africa is the highest in theworld (Table 3.1); in contrast wíth Asia and Latin America, it is higher thanthe fertility rate.

2. World Bank, "Population Growth and Policies in Sub-Saharan Africa"(forthcoming).

-22-

Because the demand for contraceptíon is so small, family planningprogramo that do nothing more than supply contraceptives will have limitedímpact on population growth. Clearly, action is needed to raise demand forfamily planning and to build a national consensus in itS favor. Over themedium term, demand for family planning will increase with progress ineducation (especially of women), with better standardq of health (especiallyredvced infant mortality), and with improvements in the status of women.Equally important are policies that reduce the gap between private and socialrates of return from family planning by increasing the private financial costsof large families.

Table 3.1. Desired fam¡iy slze and actual fert¡llty rates:Sub-Saharan Africa, Asia, and Latin America

Des Ired TotalRegion fam;ly size fertility rate

Sub-Saharan Africa(10 countries> 7.5 6.7

s¡a(10 countries> 4.0 4.7

Latin America(13 countries . 4.3 4.7

Note: Data are from surveys conducted in the late 1970sor early 1980s.

Source: Worid Bank, "Population Growth and Policies in Sub-Saharan Africa" (forthcomíng).

One measure of the progress of family planning efforts is thecontraceptive prevalence rate (CPR); that ¡s, a percentage of married women ofchíldbearing age using contraception. The average CPR in sub-Saharan Africai9 3 to 4 percent, compared with 50 percent or more ín much of Asia (Thailand59 percent, China 71 percent, Sri Lanka 55 percent, Indonesia 58 percent, andPhilippines 48 percent). However, in Mauritius, the CPR is 51 percent and inZimbabwe 22 percent. Other examples of better than average CPRs in Africa areBenin 18 percent, Ghana 10 percent, and Cameroon 11 percent. Experienceelsewhere suggests that to bring population growth down to about 2 percent ayear, the CPR has to ríse to at teast 25 percent. To reach that target beforethe end of the century, African governments and the donor community alike willhave to increase their efforts.

National governments at present finance a very small share ofexpenditure on family planning, and it is essential for them to give higherpriority to population control in budgetary allocations. Donors also need toincrease their support for famíly planning activities, which in Africacurrently receive only 0.5 percent of ODA, compared with 1.5 percent for alldeveloping countries.

- 23 -

Human resources

Pespite the recognized need to develop human resources in Afríca,there have recently been signs of shrínking access to, and a deterioration inthe quality of, services for health and education--especially in ruralareas. Basic policy reforms, as well as additional resources, will be neededto reverse this trend.

Health

Health conditions in sub-Saharan Africa have improved over the pastfew decades, but they remain among the worst in the world. In most Africancountries, acceas to health care is extremely limited. According to 1985estimates by U14ICEF and WHO, childhood imzunization levels, for example, arethe lowest in tLe world: polio 32 percent, measles 35 percent, tuberculosis41 percent, and diphtheria, pertussis, and tetanus 33 percent. An immuni-zation level of about 80 percent is generally considered necessary to controlthe transmissíon of these diseases, so there is still a long way to go.

The 1980s have seen decline, not improvement, in health services.Despite the lack of reliable and timely statístics, most observers report thatpublic health delivery systems have deteriorated in the past few years,particularly in rural areas. In many countries, thís has meant a loweroverall standard of health. Immunization levels have actually dropped inrecent years in countries such as Zambia, Tanzania, and Ghana. One reason forthis dismal picture is a worseníng shortage of financíal resources. Healthexpenditures are often vulnerable to cuts during períods of fiscal austerity;in some West African countries the share of public health in the nationalbudget fell in the early 1980s.

Inefficient use of the resources that are available has aggravatedthe problem. Government policy has contributed to this in three ways. First,at times of budget austerity, growth of employment in the health sector hasbeen maintained, so a rising salary bill has crowded out funding for essentialsupplies, transport, and maintenance of facilities. Second, most governmentscontinue the practice of concentrating health care facilities in urban areas(and especially in high-cost hospitals), neglecting peripheral facilities thatare much more cost-effective for treating the vast mejority of diseases.This, together with the policy of providing such facilities free or at anominal charge, puto pressure on high-cost urban facilities and leavessecondary facilities underused. Third, some governments have reduced thesupply of private health services by making medical facilities a publicmonopoly.

Raising the standard of health in Africa wíll require several policyreforms to increase the efficiency of resource use. The first step is to aimto deliver a minimum package of health care--especially immunization againstmajor communicable diseases, oral rehydration therapy, early diagnosis and

- 24 -

treatment of acute respiratory infections and malaria in chíldren under five,and other elemento of mother and child health cave. To do this, governmentsneed to reorient their public health systems by expanding access to community-based, primary health care, particularly in rural areas. These communityprogramo must then be backed up by institutions to monitor public health.

Covernments nust also change their hiring and cost recovery policiesto ensure that they have adequate funding to cover their nonlabor costa.Several governments are already emphasizing primary health care programs thatwill help to correct the urban bias of past policies. Many have introducedco0t recovery measures. Senegal, for instance, has a program in which userfees are collected and managed by community heaith committees. Othercountries--Ghana, Malawi, and Zambia, for example--are seriously consideringvarious schemes for user charges and community financing. Some have takensteps to reduce unit costs--for example, Mali now imports generic drugs.

Reforms to improve the level and use of resources are important; theymust be supported by donor financial assistance. Donors should coordinatetheir efforta not only in financing projects, but also in promotíng policyreforme that emphasize primary health care, cost recovery, and funding forrecurrent costs. Donora should also consid2r funneling a larger ehare oftheir resources through nongovernmental organizations. These are already theprincipal providera of health care in many rural areas, where they can serveas a well-developed vehicle for targeted primary health care.

Education

In many African countries, the education sector expanded afterindependence. Now it is suffering a reversal in both the quality and thequantity of the services it provides. According to the most recent Unescodata, primary enrollment ratios declined during 1980-83 in twelve IDAcountries in sub-Saharan Africa. In some cases (Somalia, Togo, andMozambique), the decline in these three years was 10 percentage points ormore. Evidence of declining quality ¡8 more scattered and anecdotal, but thefact that spending--on items other than teachers' pay--has fallen in the pastthree years is an indication. A lower qualíty of education in turndiscourages families from sending their children to school--especially whenthe decline happens alongside higher school fees and other charges.

To restore the momentum of primary education, African governmentswill have to allocate additional resources to the sector. This iS necessarynot only to meet the enrollment requirements of a rapidly growing population,but aleo teo ensure that students have basic books and supplies. Some savingsmay be possible on primary teacher salaries--without jeopardizing either thequality or quantity of primary educati,n--through increased qualitydifferentials in the salary structure, increases in teachers' working hours(to bring them more in line wíth civil service norms), and, in some cases,higher student-teacher ratios.

- 25 -

In postsecondary education, the immediate prierity ja to reduce thepublic costs-per student. In sub-Saharan Africa, the annual pubLíc cost ofhigher education amounts to almost $3,000 per studert. Thit ís eight timeshigher than the cost of higher education ín Asia and aimost double its cost inLatin America. The costs are high for several reasons. Student-teacherratios are only seven to one, compared with twelve or fifteen to one in Europeand the United States. Nonteaching costs and student subsidies are aliohigh: a recent survey of twenty-four African countries showed that twenty-twoprovide free tuition, twenty-one cover board aid lodgíng for most studenta,and sixteen provide additional cash allowances. Covernments can reduce thesepublic costs in several ways. For example, they should close or consolidotesmall or low-priority programs (for example, the degrees in Spanish and Polishgranted by Ghana's universities). They should spend leas on arta andhumanities and more on scientific and engineering training. They shouldinstitute tuition charges and provide fewer subsidized services and studentstipends. Some countries, such as Cameroon, Ghana, Malawi, and Nigeria, areworking on programs to cut costs in their universities.

Donors should coordinate their efforts to ensure that scholarships,technical assistance, and construction programs are consistent with thenational objectives discussed above. External assístance to education ls atpresent heavily skewed to postsecondary education. Bilateral assistance isconcentrated in technical assistance and scholarships, multilateral aid incivil works and construction. Only 14 percent of ODA for education :.s spenton operating costS and supplies, and only 11 percent of total foreigi.assistance for education is channeled to primary education. Foreign donorsundoubtedly have a comparative advantage in supplying higher education andcapital assistance, but they need to restructure their assistance to avoid adeterioration in the primary schools: they should increase the share ofasaistance for school supplies at the primary level.

Deforestation

Deforestation and, more broadly, degradation of the land--soilerosion, declíning soil fertílity, and desertification--are serious andmounting problems over large parts of Africa. The area of forest and savannahwoodland has halved since the turn of the century, and there have been majorlosses in farm tree stocks. The decline in tree stocks ís accelerating underseveral influences: consumption of fuelwood ís rising with population growth;land clearance has removed trees from farm boundaries and groves that wereneeded to maintain soil moisture and nutrient contents or to protect soalsfrom erosion; seedlings and mature trees have been lost to ill-managedlivestock; commercial logging in the higher rainfall zones goes on withoutadequate reinvestment in, or maíntenance of, forest reserves; and the meanannual yield of tree stocks has rallen in proportion to the decline in thestocks themselves.