Embed Size (px)

Citation preview

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

FinancialAccounting 2INSTRUCTIONS:

Please read the following instructions carefully before attempting any question:

• The duration of this examination is 150 minutes .• All questions are compulsory. • This exam consists of 5 Multiple Choice Questions (MCQ's) carrying

2 marks each, 6 Short questions carrying 5 marks each and 2 Descriptive questions carrying 10 marks.

• You are required to show all the working of short questions as well as Descriptive questions.

• This examination is closed book, closed notes, closed neighbors. • Do not ask any questions about the contents of this examination from anyone. • The use of calculator is allowed. • You may wish to pace yourself with your own watch, but the Supervisor

will be the official timekeeper of the test. • Failure to comply with the Supervisor's directions will result in your test

being cancelled. Please comply with supervisor's directions to avoid any unpleasant event.

pg. 1

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

1. Mahler Company began the accounting period with a $5,000 debit balance in its accounts receivable account. During the accounting period Mahler recorded revenue on account amounting to $17,000. The accounts receivable account at the end of the accounting period contained a $8,000 debit balance. Based on this information alone, the cash collected from accounts receivables during the period is A) $14,000 B) $17,000 C) $20,000 D) $22,000

2. Credit entries will: A) increase contributed capital accounts. B) decrease asset accounts. C) increase liability accounts. D) All of the above.

3. On January 1, 20X1 the Green Acre Company purchased an tractor that cost $25,000; had a five year useful life; and a $5,000 salvage value. Which of the following is the correct general journal entry to record depreciation expense for the 20X2 fiscal year? A) Depreciation Exp. 4,000

Acc. Depreciation 4,000 B) Acc. Depreciation 4,000

Depreciation Exp. 4,000 C) Depreciation Exp. 8,000

Acc. Depreciation 8,000 D) Acc. Depreciation 8,000

Depreciation Exp. 8,000

4. On November 1, 20X2, Jackson Company paid $2,400 in advance for an insurance policy that covered the company for six months. Assuming that Howard recorded this purchase as an asset, the adjusting entry required on December 31, 20X2 would include: A) a debit to prepaid insurance for $2,400. B) a credit to prepaid insurance for $800. C) a credit to insurance expense for $800. D) a credit to insurance expense for $1,600

5. Sullivan Company issued a $10,000 face value note to the First Bank on September 1, 20X3. The note carried a 12% annual rate of interest and a one year term. Which of the following general journal entries would be necessary to record accrued interest on December 31, 20X3? A) Interest Expense 800

Interest Payable 800

pg. 2

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

B) Interest Payable 800 Interest Expense 800

C) Interest Expense 400 Interest Payable 400

D) Interest Payable 400 Interest Expense 400

6. The following is a trial balance of RS Company as of December 31, 20X2:

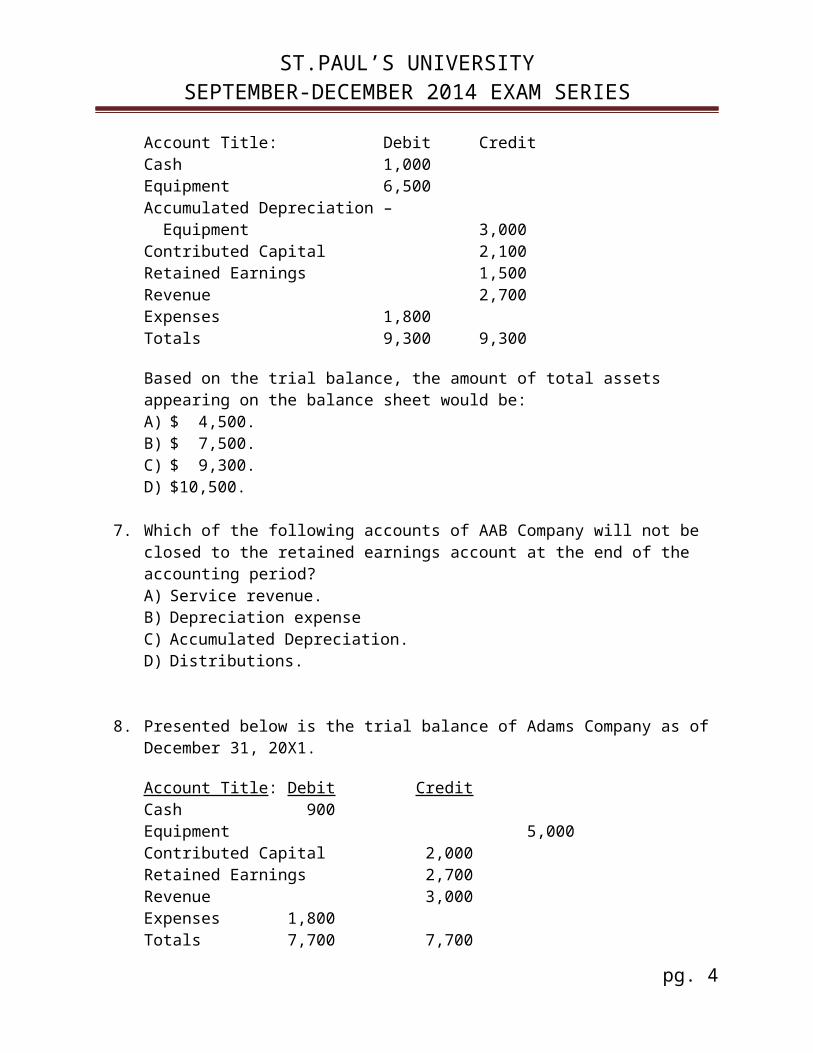

Account Title: Debit CreditCash 1,000Equipment 6,500Accumulated Depreciation – Equipment 3,000Contributed Capital 2,100Retained Earnings 1,500Revenue 2,700Expenses 1,800Totals 9,300 9,300

Based on the trial balance, the amount of total assets appearing on the balance sheet would be: A) $ 4,500. B) $ 7,500. C) $ 9,300. D) $10,500.

7. Which of the following accounts of AAB Company will not be closed to the retained earnings account at the end of the accounting period? A) Service revenue. B) Depreciation expense C) Accumulated Depreciation. D) Distributions.

8. Presented below is the trial balance of Adams Company as of December 31, 20X1.

Account Title: Debit CreditCash 900Equipment 5,000Contributed Capital 2,000Retained Earnings 2,700Revenue 3,000Expenses 1,800Totals 7,700 7,700

pg. 3

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

After the closing entries have been posted to the accounts, the retained earnings account will have a balance of A) $2,700.B) $3,900.C) $4,500. D) $5,700.

9. WAM Company borrowed $40,000 on October 1, 20X4. The company issued a one-year note with a 6% annual interest rate. The adjusting entry necessary to record accrued interest on December 31, 20X4 would include a: A) debit to interest expense for $600. B) debit to interest payable for $2,400. C) debit to notes payable for $40,000. D) None of the above.

10. The information in the following T-accounts indicates that:

A) owners invested $500 cash in the business. B) the company repaid a $500 debt. C) the company borrowed $500. D) None of the above.

11. The employees of Elgar Company have worked the last two weeks of 20X2, but the employees' wages have not been paid nor recorded as of December 31, 20X2. The adjusting entry that Elgar should make for these unpaid wages on December 31, 20X2 is: A) debit to wage expense and credit to wages payable. B) debit to wage expense and credit to cash. C) debit to wages payable and credit to wages expense. D) no entry is required until the employee is paid next period.

12. During a company's first year, the asset account, office supplies, was debited for $1,400 for the purchases of supplies. At year end, office supplies on hand were counted and determined to be $500. The proper adjusting entry for supplies will A) have no effect on net income B) decrease assets by $500 C) increase liabilities by $900 D) increase expenses by $900

13. The following transactions apply to Sue's Lawn and Garden Service for the year 20X2.(1) Sue invested $5,000 cash in a her new business.(2) Purchased land for $3,000 cash that will be used as a parking lot.(3) Performed services on account for $6,000.

pg. 4

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

(4) Collected $5,000 of the amount owed on accounts receivable.(5) Paid operating expense of $4,500.

Required:

(1) Draw T-accounts and post the above transactions to the appropriate T-accounts.(2) Prepare a balance sheet and statement of cash flow for Sue's Word Processing Service for the period ended December 31, 20X2.

14. Flint Company uses the perpetual inventory system. The company purchased $6,000 of merchandise from JX Company under the terms 2/10, net/30. Flint paid for the merchandise within 10 days and also paid $150 freight to obtain the goods under terms FOB Shipping Point. All of the merchandise purchased was sold for $9,000 cash. The amount of gross margin for this merchandise is: A) $ 2,550 B) $ 2,970 C) $ 3,150 D) $ 5,880

15. The following information for the year 20X6 is taken from the accounts of GG Company. The company uses the periodic inventory method.

Inventory, December 31, 20X5 $2,000Purchases 9,000Purchases Returns.and allow. 200Purchase Discounts 100Freight on goods purchased under terms FOB shipping point 300Freight on goods sold under terms FOB destination 400Cost of Goods Sold 7,600

Based on this information, the inventory at December 31, 20X6 is A) $3,800 B) $3,400 C) $3,300 D) $3,000

16. The following data is from the income statement of Peach Company:Sales $ 800 Cost of goods sold (500)Other expenses (200)Net earnings $ 100

The company's gross profit percentage is: A) 12.5%. B) 37.5%.

pg. 5

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

C) 62.5%. D) 60.0%.

17. The following are account balances from the accounts of LL Company at December 31, 20X1:

Cash $181,500Building 232,550Accumulated Depreciation. 150,000Inventory 192,950Supplies 7,100Contributed Capital 250,000Distributions 50,000Salaries Expense 72,500Operating Expense 108,200Retained Earnings 192,500Salaries Payable 3,100Sales 980,700Cost of Goods Sold 698,500Accounts Payable 17,500Depreciation Expense 50,000

(1) After the temporary accounts are closed, what is the balance in retained earnings?(2) From the above information, prepare an income statement.

18. At the beginning of the year, Jay's Sales had $2,400 of merchandise inventory. During the year, Jay purchased $22,000 of inventory. At the end of the year, a count of the inventory revealed that Jay had $1,600 of inventory on hand.

(a.) What is cost of goods sold for the year?(b.) What is the amount of goods available for sale?(c.) What amount of inventory will be shown on the year end balance sheet?

19. Walden Company uses the perpetual inventory method. On January 1, 20X2 Walden purchased 300 units of inventory that cost $2.00 each. On January 10, 20X2 the company purchased an additional 400 units of inventory that cost $2.50 each. If Walden uses a weighted average cost flow method, and sells 400 units of inventory, the amount of cost of goods sold appearing on the income statement will be: A) $900.B) $914.C) $964. D) $1,000.

20. Martin Company uses the perpetual inventory method. Martin purchased 400 units of inventory that cost $4.00 each. At a later date the company purchased an additional 500 units of inventory that cost $5.00 each. Martin sold 700 units of inventory for $7.00. If

pg. 6

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

Martin uses a FIFO cost flow method, the amount of gross margin appearing on the income statement will be: A) $1,800.B) $2,400.C) $3,100. D) $4,900.

21. XYZ Company uses the periodic inventory system and desires to prepare quarterly financial statements. Gross margin is normally 40% of sales. Information taken from the company's records revealed first quarter sales of $40,000; beginning inventory of $6,000 and purchases of $30,000. The estimated amount of ending inventory would be: A) .$12,000. B) $14,000.C) $16,000. D) $24,000.

22. The ABC Company has four different categories of inventory. Quantity, cost, market value for each inventory category is shown below:Item Quantity Cost Per Unit Market Value Per Unit1 220 $4.40 $4.602 130 $6.20 $6.003 100 $10.00 $9.254 25 $20.50 $25.00

The company carries inventory at lower-of-cost-or-market applied to each individual category. The implementation of the lower-of-cost-or-market rule would act to: A) reduce assets and equity by $99.50. B) reduce assets and equity by $79.00. C) increase assets and equity by $79.00. D) increase assets and equity by $99.50.

23. When prices are falling: A) LIFO will result in higher income and a higher inventory valuation than will FIFO. B) LIFO will result in higher income and a lower inventory valuation than will FIFO. C) LIFO will result in lower income and a higher inventory valuation than will FIFO. D) LIFO will result in lower income and a lower inventory valuation than will FIFO.

24. When prices are rising, which method of inventory, if any, will result in the lowest relative net cash outflow (including the effects of taxes, if any)? A) FIFO. B) LIFO. C) weighted average. D) None of these; inventory methods cannot affect cash flows.

25. During 20X3, Cramer Sales sold 180 units @ $320 each. Cash selling and administrative

pg. 7

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

expenses were $15,000. The following information is also available:

Beginning inventory 30 units @ $180Feb 3 purchase 60 units @ $190June 2 purchase 70 units @ $220Oct 1 purchase 40 units @ $230

The company's income tax rate is 40%.

Required:(a.) Determine the amount of cost of goods sold using:

FIFOLIFOWeighted Average

(b.) Determine the amount of ending inventory using:FIFOLIFOWeighted Average

(c.) Determine the company's net income after tax using:FIFOLIFO

26. Hill Company purchased investment securities at a cost of $7,000. At the end of the accounting period the securities had a market value of $7,600. Indicate whether each of the following statements is true or false assuming the securities areclassified as available-for-sale._____ a. The unrealized gain would cause net income to increase._____ b. The unrealized gain would cause equity to increase._____ c. The securities would be carried at $7,600 on the balance sheet._____ d. A $7,600 cash outflow would be shown in the investing activities section of the statement of cash flows._____ e. The unrealized gain would not be recognized in the financial statements.

27. Investment securities that cost $6,300 have a market value of $6,900. Show the effects of the appropriate accounting treatment to the unrealized gain assuming the securities are classified a trading securities.

28. James Company purchased an asset with a list price of $35,000. James received a 2% cash discount. The asset was delivered under terms FOB shipping point and freight costs amounted to $700. James paid $800 to have the asset installed. Insurance costs to protect the asset from fire and theft amounted to $400 for the first year of operations. Based on this information, the cost capitalized in the asset account would be:

pg. 8

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

A) $35,000.B) $35,800.C) $36,500. D) $36,900.

29. On January 1, 20X1 NCAA Company purchased a truck that cost $24,000. The truck had an expected useful life of 5 years and a $4,000 salvage value. The amount of depreciation expense recognized in 20X3 assuming that NCAA uses the double declining balance method is: A) $8,000.B) $4,000.C) $3,456. D) $2,880.

30. CosbyCompany purchased a truck that cost $26,000. The company expected to drive the truck 100,000 miles. The truck had an estimated salvage value of $2,000. If the truck is driven 36,000 miles in the current accounting period, which of the following amounts should be recognized as depreciation expense? A) $8,000.B) $8,280.C) $8,640. D) $9,360.

31. Scott Company purchased a producing oil well for $2,000,000. The well was expected to produce 500,000 barrels of oil over its useful life. During 20X4 the company extracted 120,000 barrels of oil. The oil was sold for $20 per barrel. Assume that the company incurred $1,440,000 in operating expenses during 20X4. Based on this information, how much net income would Scott report in 20X4? A) $1,920,000.B) $1,680,000.C) $400,000. D) $480,000.

32. ClarkCompany owned an asset that had cost $32,000. The company sold the asset on January 1, 20X2 for $8,000. Accumulated depreciation on the day of sale amounted to $26,000. Based on this information, the sale would result in: A) a $2,000 gain in the operating activities section of the statement of cash flows. B) an $8,000 cash inflow in the investing activities section of the cash flow statement. C) an $8,000 increase in total assets. D) a $6,000 cash inflow in the financing activities section of the cash flow statement.

33. On January 1, 20X1, Staton Company paid $160,000 to obtain a patent. Staton expected to use the patent for 5 years before it became technologically obsolete. Based on this information, the amount of amortization expense on the December 31, 20X3 income statement and the book value of the patent on the December 31, 20X3 balance sheet

pg. 9

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

would be: A) $32,000 / $96,000.B) $32,000 / $54,000.C) $54,000 / $96,000. D) $54,000 / $54,000.

34. Redstorm Company purchased a new machine on January 1, 20X1, at a cost of $150,000. The machine is expected to have an eight-year life and a $15,000 salvage value. The machine is expected to produce 675,000 finished products during its eight-year life. Production during 20X1 was 70,000 units and during 20X2 110,000 units

Required: Determine the amount of depreciation expense to be recorded on the machine for the years 20X1 and 20X2 under each of the following methods:

20X1 20X2(1.)Straight-line ________ ________(2.)Units of production method ________ ________(3.)Double-declining-balance ________ ________

pg. 10

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

Answer Key --

1. A2. D3. A4. B5. C6. A7. C8. B9. A

10. C11. A12. D13. T-Accounts

(2) Balance Sheet

Assets Cash $2,500 Land 3,000 Accounts Receivable 1,000Total Assets $6,500

Liabilities $ -0-

Equity Contributed Capital $5,000 Retained Earnings 1,500Total Equity $6,500

Total Liabilities and Equity $6,500

Statement of Cash Flows

pg. 11

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

Cash Flow from Operating Activities: Inflow from Customers $ 5,000 Outflow from Operating Expenses (4,500)Net Cash Flow from Operations $ 500

Cash Flow from Investing Activities: Outflow from Purchase of Land (3,000)

Cash Flow from Financing Activities: Inflow from Owner Investment 5,000

Net Change in Cash $ 2,500

14. B15. B16. B17. 1) Retained Earnings, beginning balance $192,500

Add, Sales 980,700 Less, Cost of Goods Sold ( 698,500) Less, Expenses (72,500 + 108,200 + 50,000) (230,700) Less, Distributions ( 50,000) Retained Earnings, ending balance $194,000

2) Income Statement Net Sales $980,700 Cost of Goods Sold (698,500) Gross Margin $282,200 Operating Expenses Salaries Expense $ 72,500 Operating Expense 108,200 Depreciation Expense 50,000 Total Expenses (230,700) Net Income $ 51,500

18. Question: Computation:Beginning inventory $ 2,400Purchases 22,000

(b) Goods available for sale 24,400 (c) Less, ending inventory ( 1,600) (a) Cost of Goods sold $22,800

19. B20. A21. B22. A

pg. 12

ST.PAUL’S UNIVERSITYSEPTEMBER-DECEMBER 2014 EXAM SERIES

23. A24. B25. d(a) Cost of Goods Sold

FIFO LIFO30 @ $180 = 5,400 40 @ 230 = 9,20060 @ $190 = 11,400 70 @ 220 = 15,40070 @ $220 = 15,400 60 @ 190 = 11,40020 @ $230 = 4,600 10 @ 180 = 1,800Total $36,800 Total $37,800

Weighted Average = $41,400 ÷ 200 = $207 per unit180 X $207 = $37,260

(b) FIFO = 20 @ $230 = $4,600LIFO = 20 @ $180 = $3,600Weighted Average = 20 @ $207 = $4,140

(c) FIFO LIFOSales (180 X $320) $57,600 $57,600Cost of Goods Sold (36,800) (37,800)Selling & Administration Expenses (15,000) (15,000)Net Income Before Taxes 5,800 4,800Taxes (2,320) (1,920)Net Income After Taxes $3,480 $2,880

26. (a.) F (b.)T (c.)T (d.)F (e.) F 27. I N I I N I N 28. B29. C30. C31. D32. B33. B34. 20X1 20X2

(a.) $150,000 - $15,000 = $135,000 / 8 = $16,875 per year $16,875 $16,875(b.) $150,000 - $15,000 = $135,000/ 675,000 =

.20 per unit $14,000 $22,000(c.) $150,000 x (2 x .125) = 37,500 $37,500 112,500 x (2 x .125) = 28,125 $28,125

pg. 13