Embed Size (px)

Citation preview

1

Financial Year 2004 Final Results Presentation

19 August 2004

2

Market Overview and Financial Results

Tom HonanChief Financial Officer

3

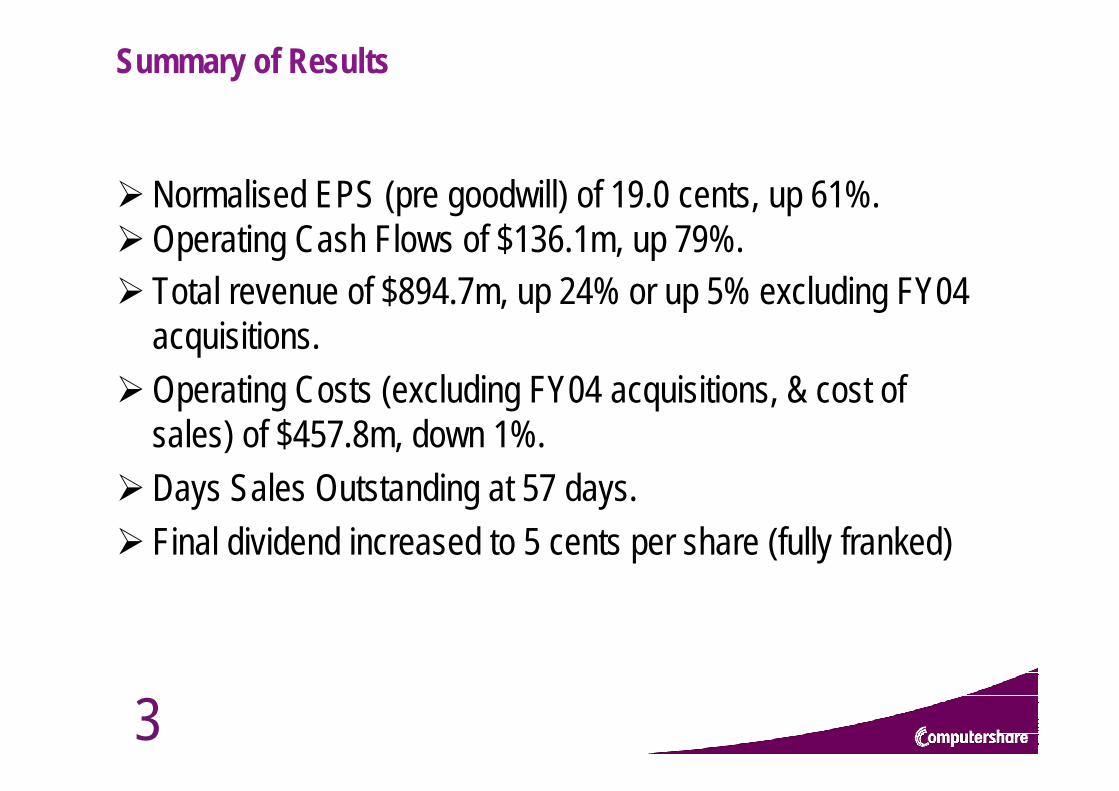

Summary of Results

Normalised EPS (pre goodwill) of 19.0 cents, up 61%.Operating Cash Flows of $136.1m, up 79%.Total revenue of $894.7m, up 24% or up 5% excluding FY04 acquisitions.Operating Costs (excluding FY04 acquisitions, & cost of sales) of $457.8m, down 1%.Days Sales Outstanding at 57 days.Final dividend increased to 5 cents per share (fully franked)

4

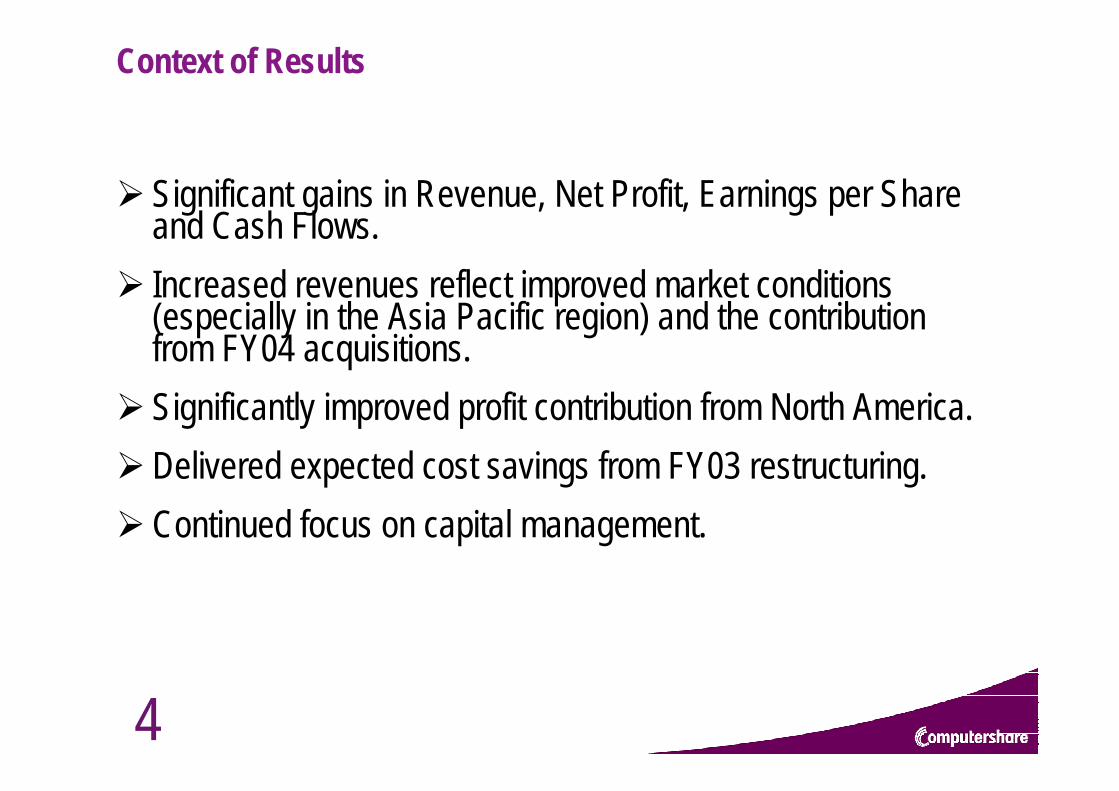

Context of Results

Significant gains in Revenue, Net Profit, Earnings per Share and Cash Flows.Increased revenues reflect improved market conditions (especially in the Asia Pacific region) and the contribution from FY04 acquisitions.Significantly improved profit contribution from North America. Delivered expected cost savings from FY03 restructuring.Continued focus on capital management.

5

This presentation is structured around the following framework

MarketOverview

FinancialResults

CEO’s Report

6

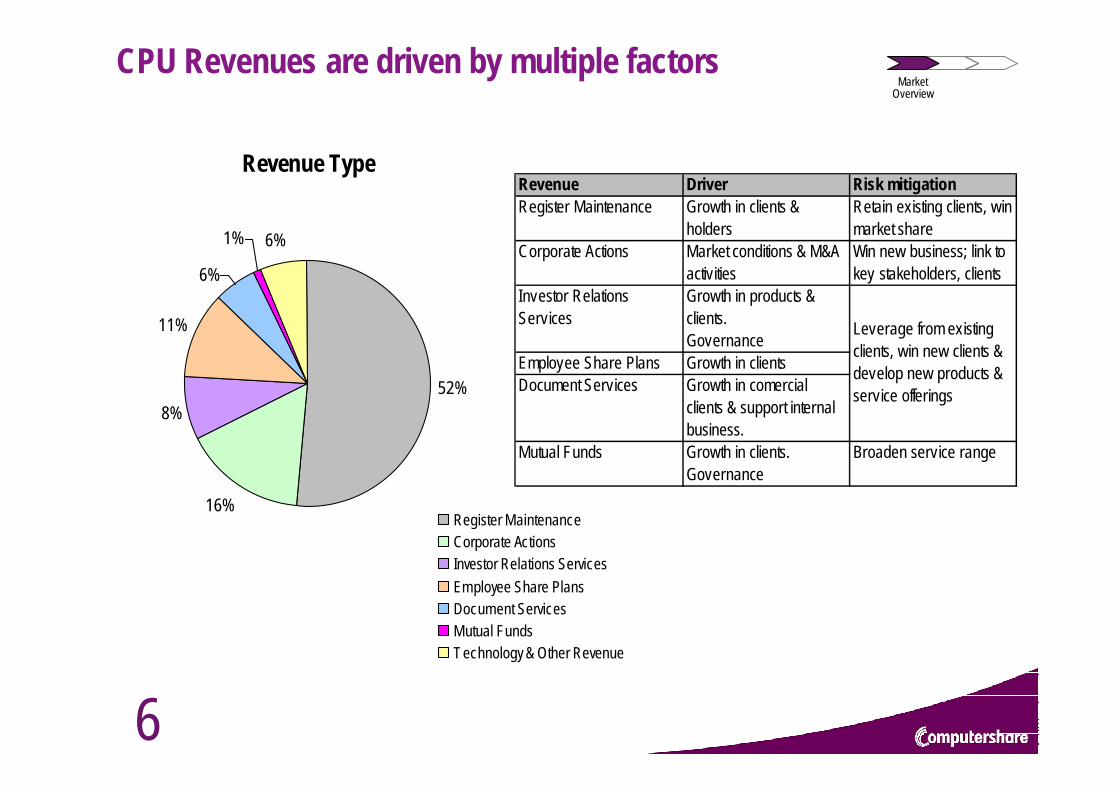

CPU Revenues are driven by multiple factorsMarket

Overview

Revenue Type

52%

16%

11%

6%

1% 6%

8%

Register MaintenanceCorporate ActionsInvestor Relations ServicesEmployee Share PlansDocument ServicesMutual FundsTechnology & Other Revenue

Revenue Driver Risk mitigationRegister Maintenance Growth in clients &

holdersRetain existing clients, win market share

Investor Relations Services

Growth in products & clients.Governance

Employee Share Plans Growth in clientsDocument Services Growth in comercial

clients & support internal business.

Mutual Funds Growth in clients.Governance

Broaden service range

Corporate Actions Market conditions & M&A activities

Win new business; link to key stakeholders, clients

Leverage from existing clients, win new clients & develop new products & service offerings

7

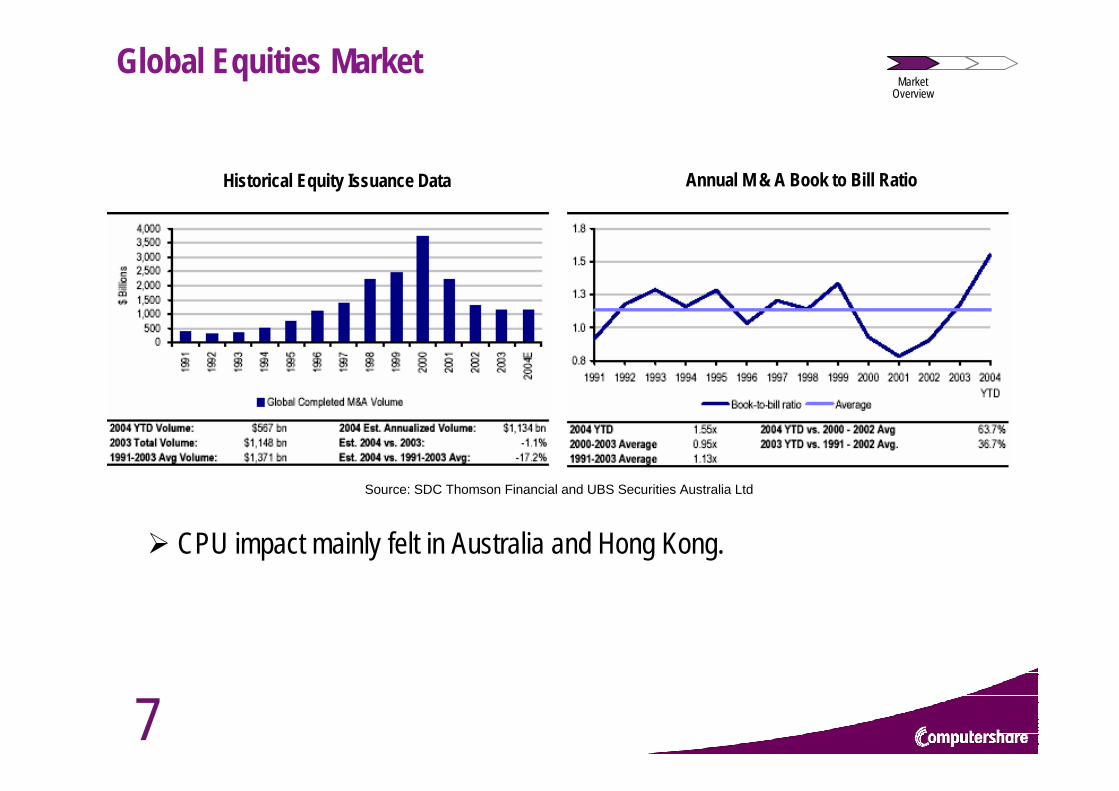

Global Equities MarketMarket

Overview

CPU impact mainly felt in Australia and Hong Kong.

Historical Equity Issuance Data Annual M & A Book to Bill Ratio

Source: SDC Thomson Financial and UBS Securities Australia Ltd

8

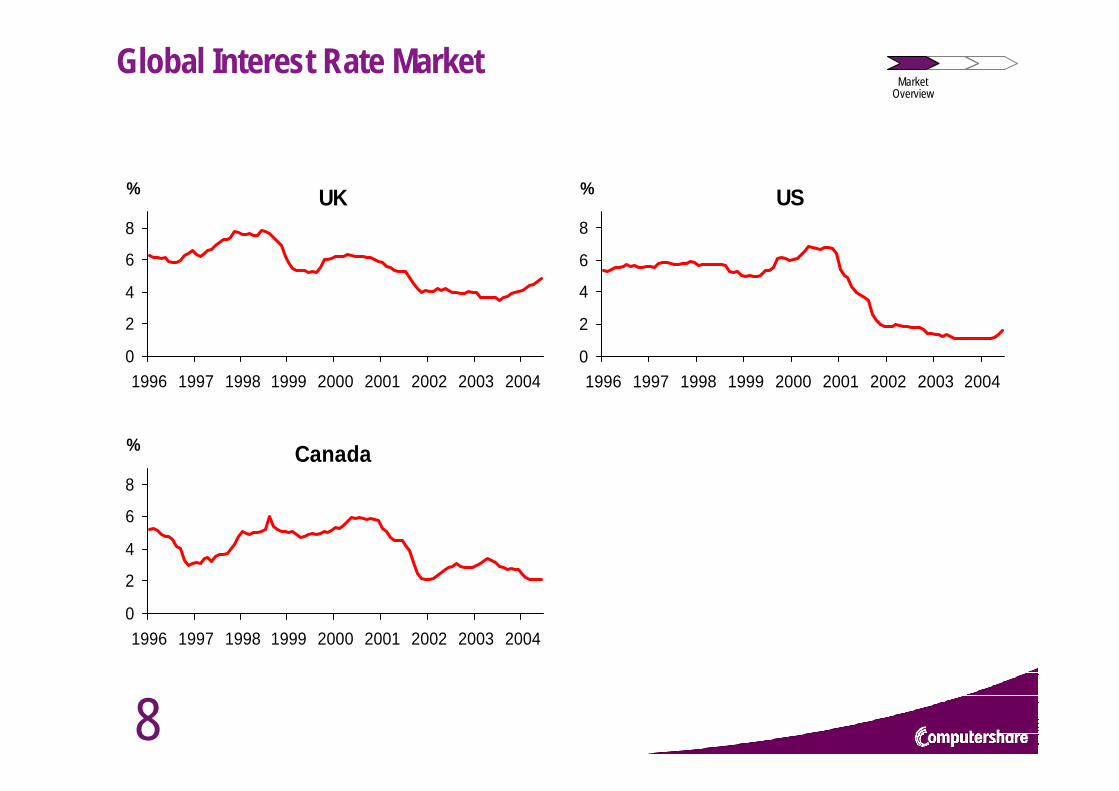

Global Interest Rate MarketMarket

Overview

US

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003 2004

%UK

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003 2004

%

Canada

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003 2004

%

9

Computershare Strengths

Recurring Revenue - >70% of revenue is of a recurring nature.Global Diversification – across more than 15 countries.High Margins – EBITDA margins > 20% and increasing.Low Capital Requirements – Capex < depreciation expense.Profit increases deliver substantial free cash flow increases.Exposure to northern hemisphere interest rates.

Market Overview

10

MarketOverview

FinancialResults

CEO’s Report

11

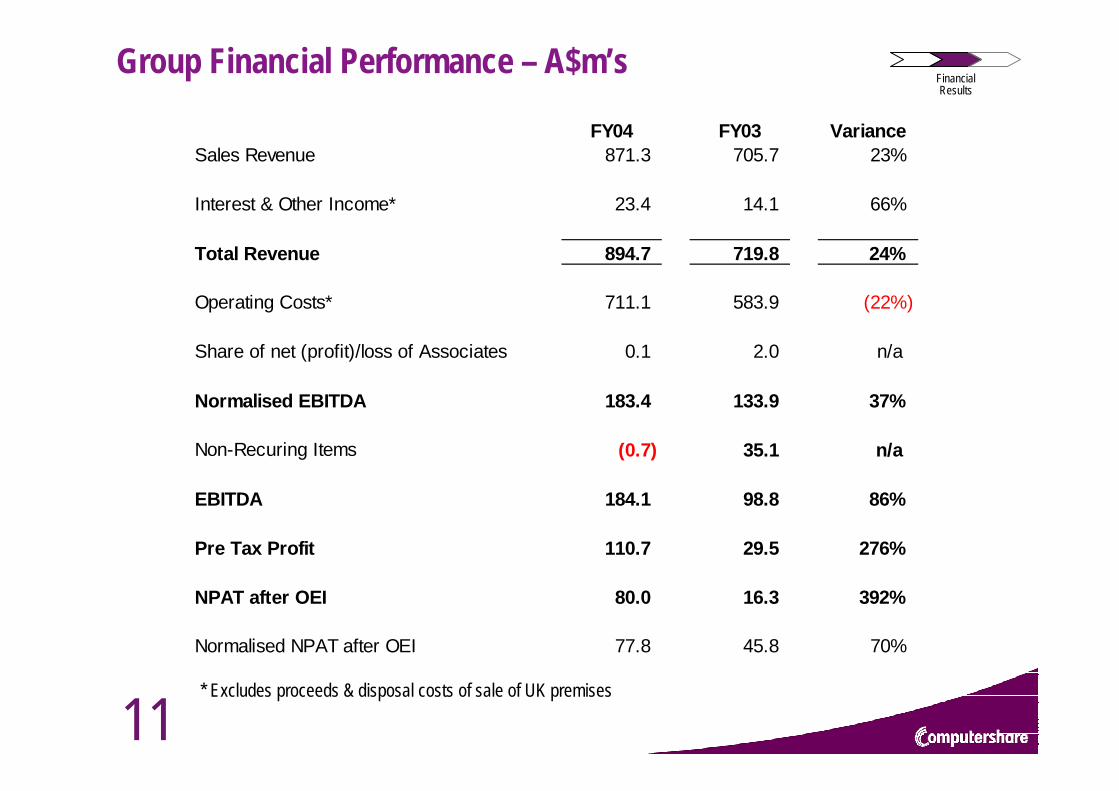

Group Financial Performance – A$m’sFinancialResults

FY04 FY03 VarianceSales Revenue 871.3 705.7 23%

Interest & Other Income* 23.4 14.1 66%

Total Revenue 894.7 719.8 24%

Operating Costs* 711.1 583.9 (22%)

Share of net (profit)/loss of Associates 0.1 2.0 n/a

Normalised EBITDA 183.4 133.9 37%

Non-Recuring Items (0.7) 35.1 n/a

EBITDA 184.1 98.8 86%

Pre Tax Profit 110.7 29.5 276%

NPAT after OEI 80.0 16.3 392%

Normalised NPAT after OEI 77.8 45.8 70%

* Excludes proceeds & disposal costs of sale of UK premises

12

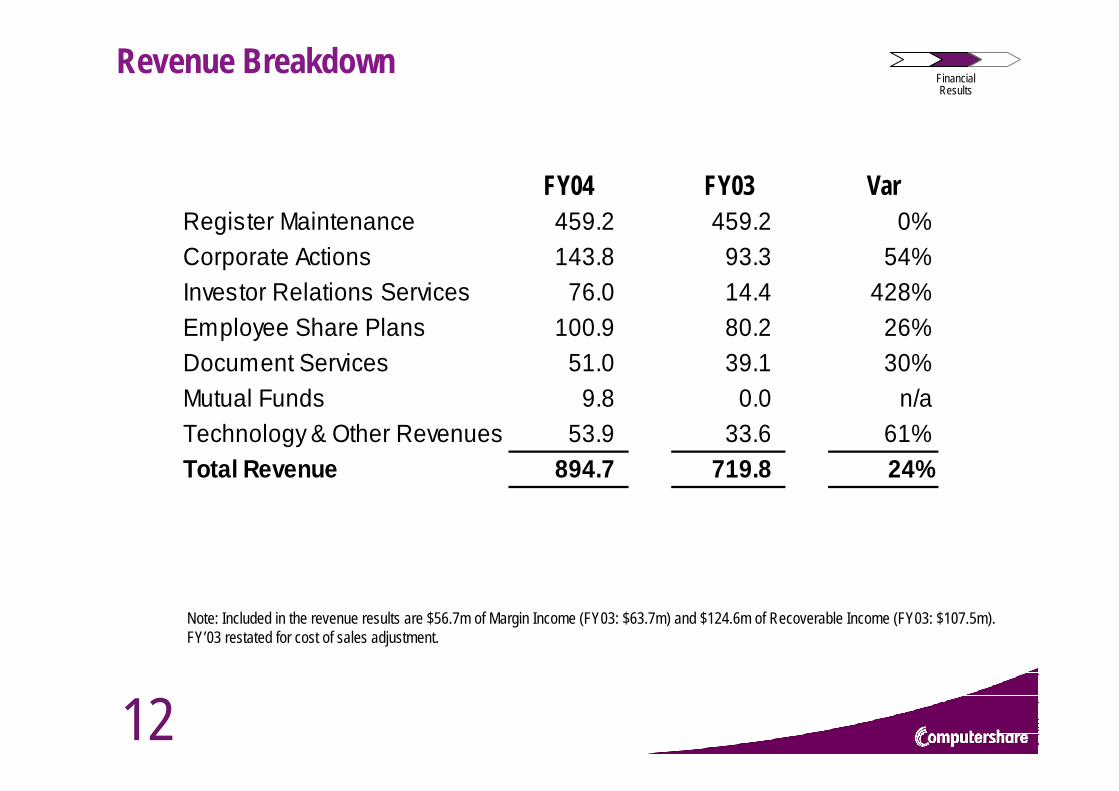

Revenue Breakdown

FY04 FY03 VarRegister Maintenance 459.2 459.2 0%Corporate Actions 143.8 93.3 54%Investor Relations Services 76.0 14.4 428%Employee Share Plans 100.9 80.2 26%Document Services 51.0 39.1 30%Mutual Funds 9.8 0.0 n/aTechnology & Other Revenues 53.9 33.6 61%Total Revenue 894.7 719.8 24%

Note: Included in the revenue results are $56.7m of Margin Income (FY03: $63.7m) and $124.6m of Recoverable Income (FY03: $107.5m).FY’03 restated for cost of sales adjustment.

FinancialResults

13

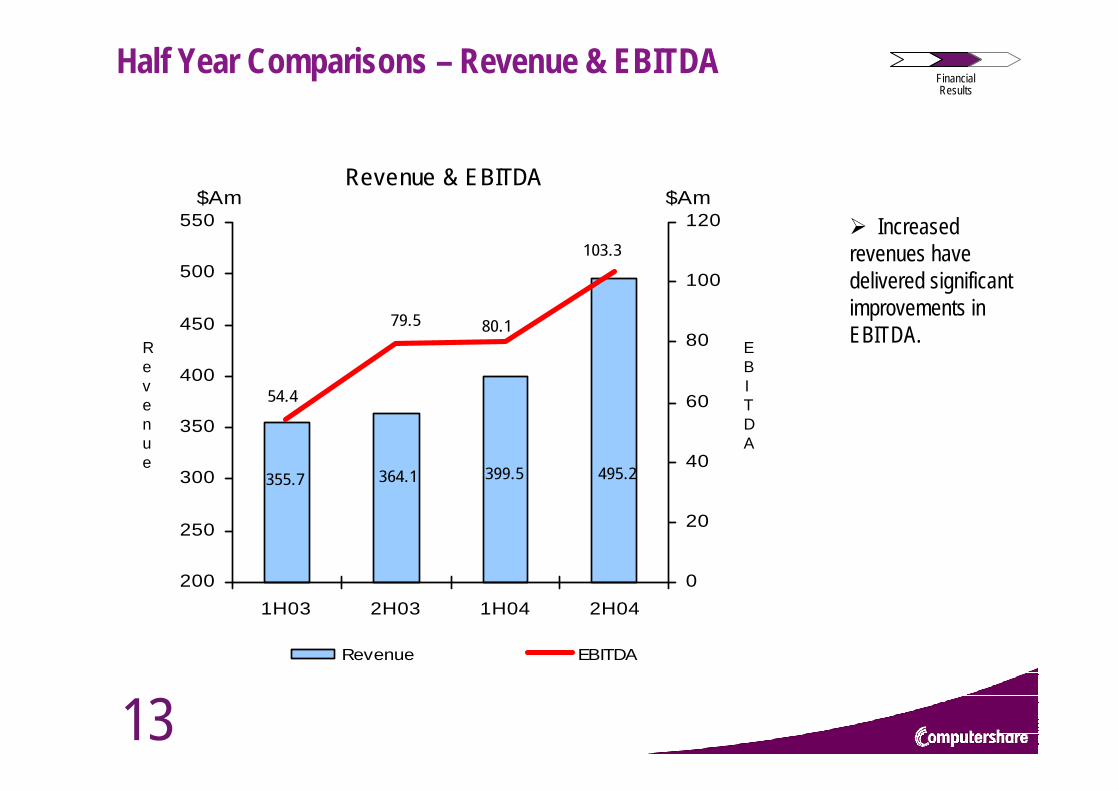

Half Year Comparisons – Revenue & EBITDAFinancialResults

Revenue & EBITDA

355.7 495.2399.5364.1

80.1

103.3

79.5

54.4

200

250

300

350

400

450

500

550

1H03 2H03 1H04 2H04

$Am

0

20

40

60

80

100

120$Am

Revenue EBITDA

Revenue

EBITDA

Increased revenues have delivered significant improvements in EBITDA.

14

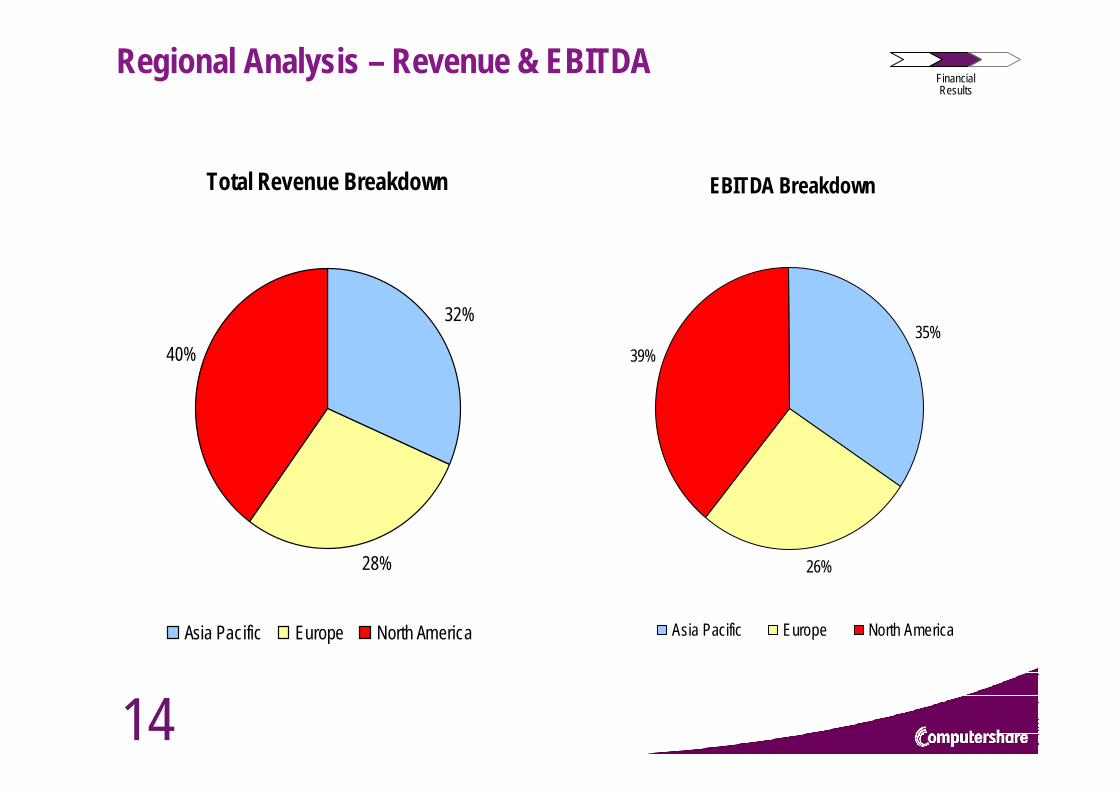

Regional Analysis – Revenue & EBITDA

Total Revenue Breakdown

32%

28%

40%

Asia Pacific Europe North America

EBITDA Breakdown

35%

26%

39%

Asia Pacific Europe North America

FinancialResults

15

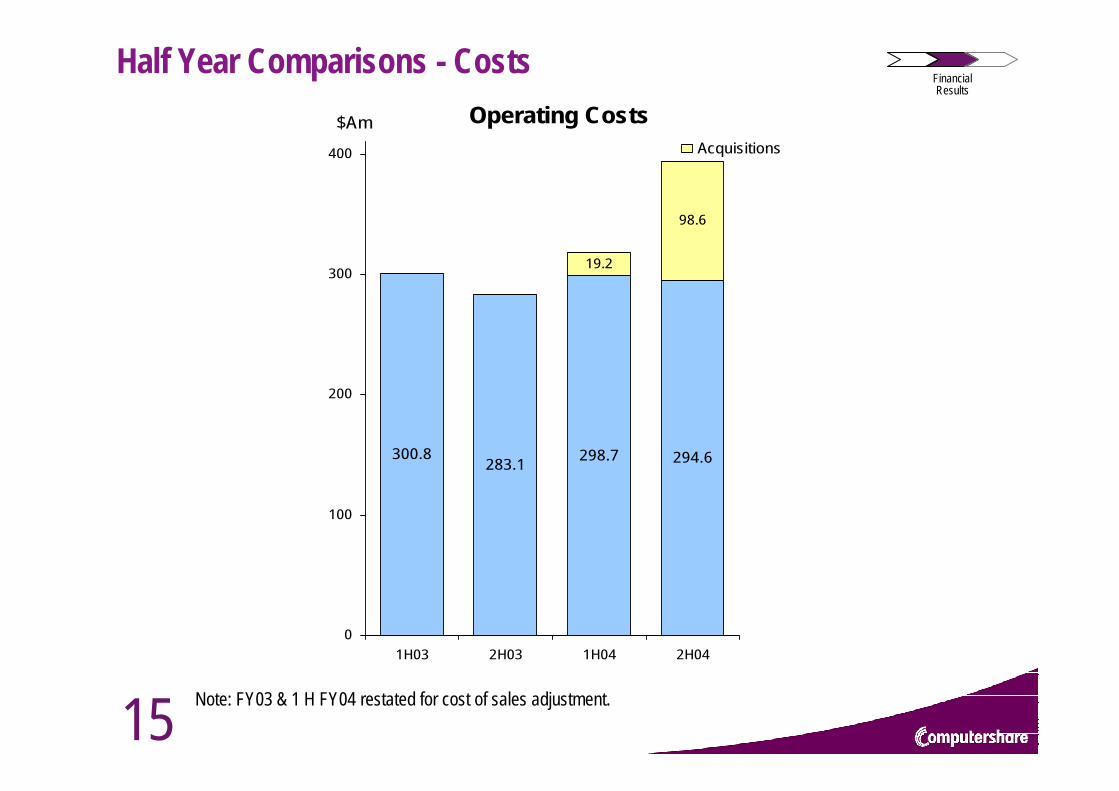

Half Year Comparisons - CostsOperating Costs

300.8283.1 294.6

19.2

98.6

298.7

0

100

200

300

400

1H03 2H03 1H04 2H04

$AmAcquisitions

FinancialResults

Note: FY03 & 1 H FY04 restated for cost of sales adjustment.

16

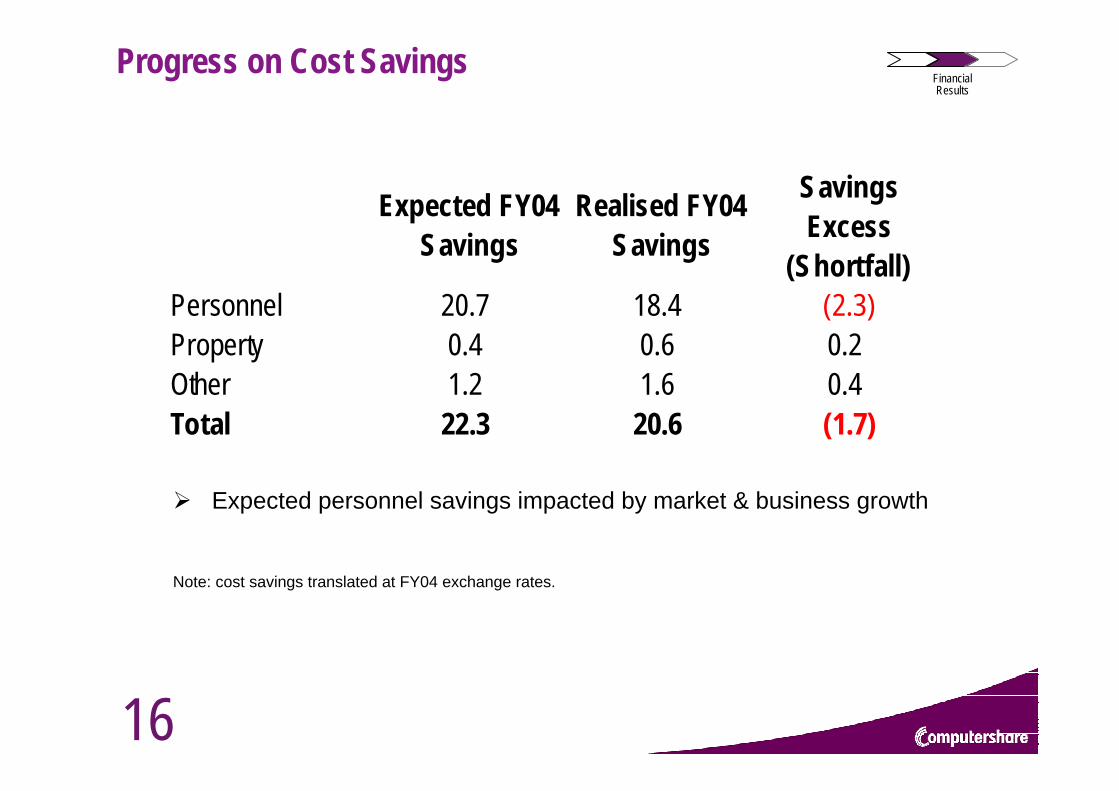

Progress on Cost Savings

Expected FY04 Savings

Realised FY04 Savings

Savings Excess

(Shortfall)Personnel 20.7 18.4 (2.3)Property 0.4 0.6 0.2Other 1.2 1.6 0.4Total 22.3 20.6 (1.7)

Expected personnel savings impacted by market & business growth

Note: cost savings translated at FY04 exchange rates.

FinancialResults

17

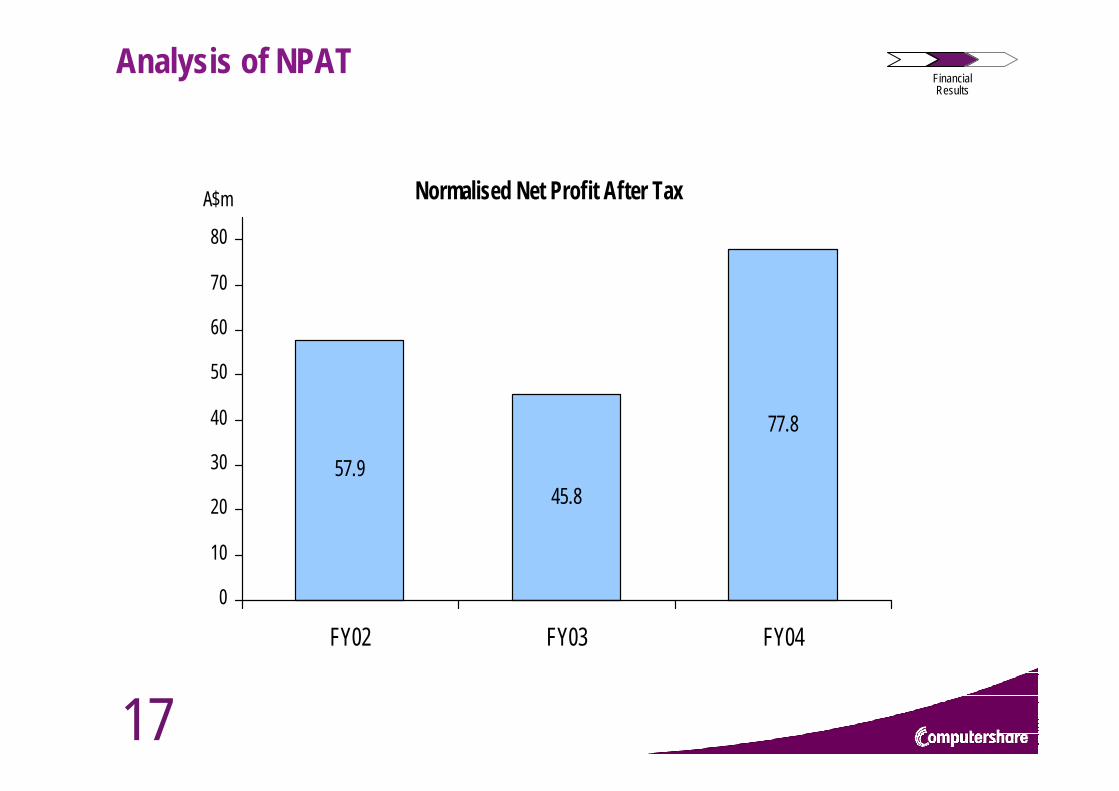

Analysis of NPATFinancialResults

Normalised Net Profit After Tax

57.945.8

77.8

0

10

20

30

40

50

60

70

80

FY02 FY03 FY04

A$m

18

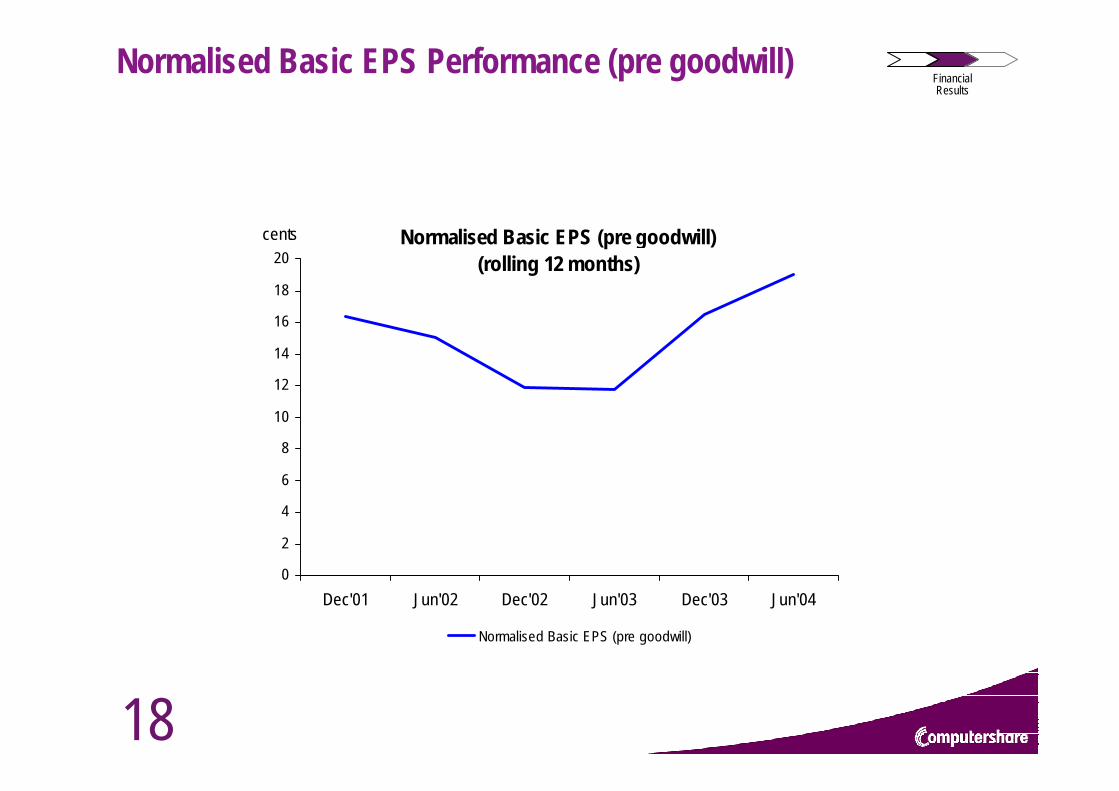

Normalised Basic EPS Performance (pre goodwill)FinancialResults

Normalised Basic EPS (pre goodwill) (rolling 12 months)

0

2

4

6

8

10

12

14

16

18

20

Dec'01 Jun'02 Dec'02 Jun'03 Dec'03 Jun'04

cents

Normalised Basic EPS (pre goodwill)

19

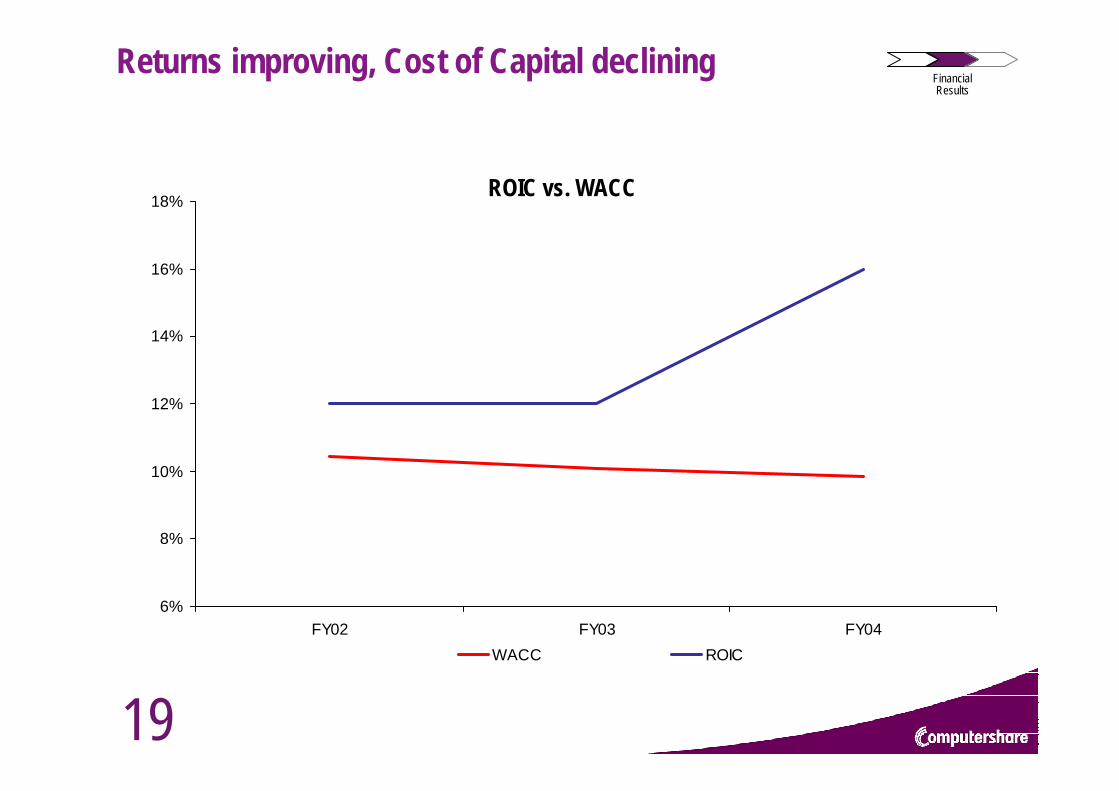

Returns improving, Cost of Capital declining

ROIC vs. WACC

FinancialResults

6%

8%

10%

12%

14%

16%

18%

FY02 FY03 FY04WACC ROIC

20

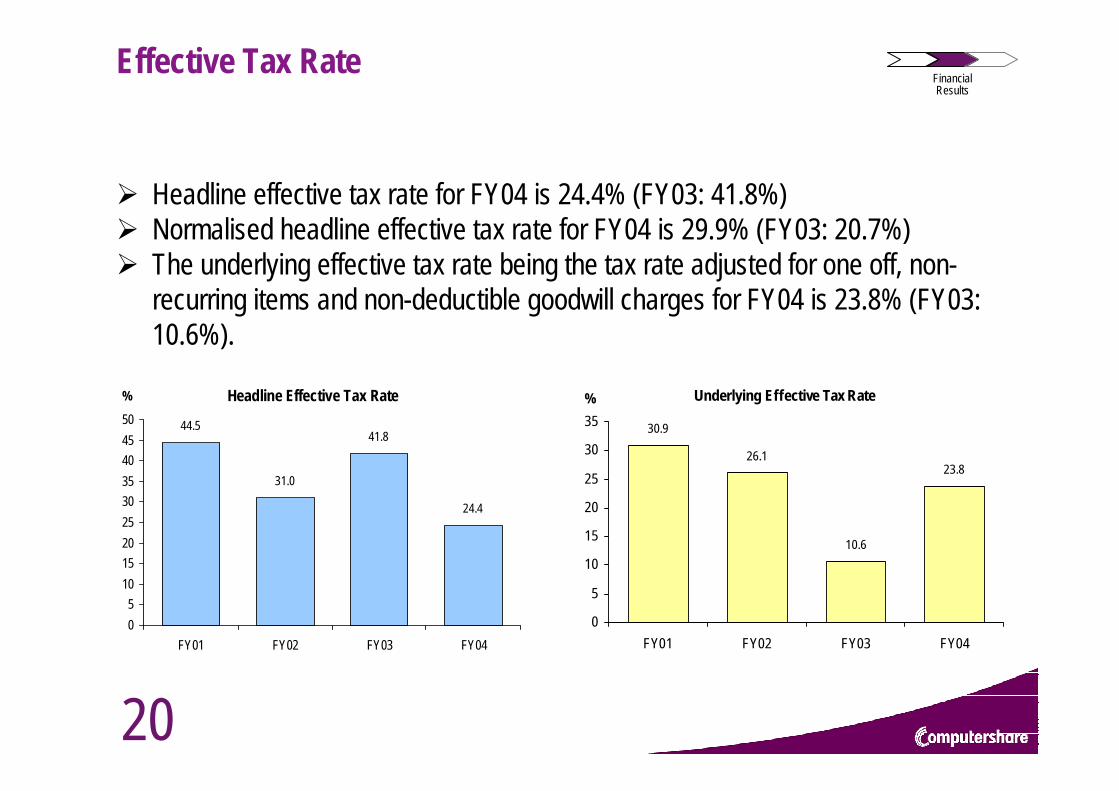

Effective Tax Rate

Headline effective tax rate for FY04 is 24.4% (FY03: 41.8%)Normalised headline effective tax rate for FY04 is 29.9% (FY03: 20.7%)The underlying effective tax rate being the tax rate adjusted for one off, non-recurring items and non-deductible goodwill charges for FY04 is 23.8% (FY03: 10.6%).

FinancialResults

Headline Effective Tax Rate

44.5

31.0

41.8

24.4

05

101520253035404550

FY01 FY02 FY03 FY04

% Underlying Effective Tax Rate

30.9

26.1

10.6

23.8

0

5

10

15

20

25

30

35

FY01 FY02 FY03 FY04

%

21

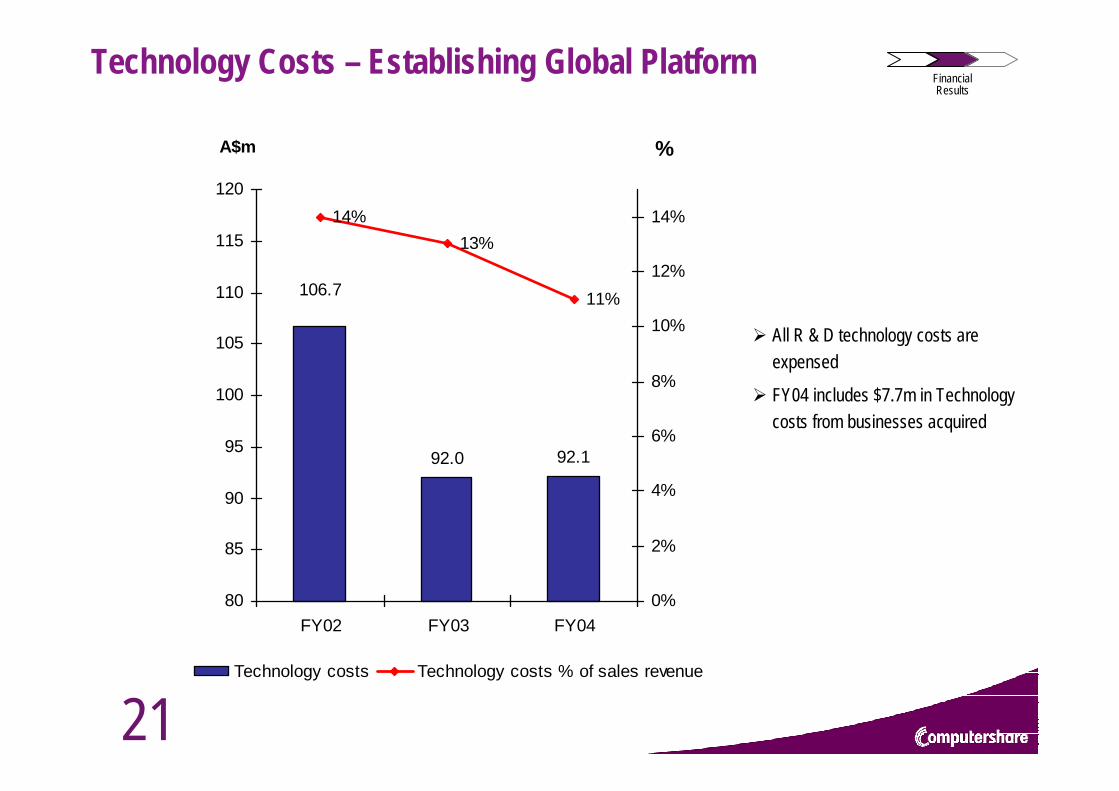

Technology Costs – Establishing Global PlatformFinancialResults

92.0 92.1

106.7

14%13%

11%

80

85

90

95

100

105

110

115

120

FY02 FY03 FY04

A$m

0%

2%

4%

6%

8%

10%

12%

14%

%

Technology costs Technology costs % of sales revenue

All R & D technology costs are expensed

FY04 includes $7.7m in Technology costs from businesses acquired

22

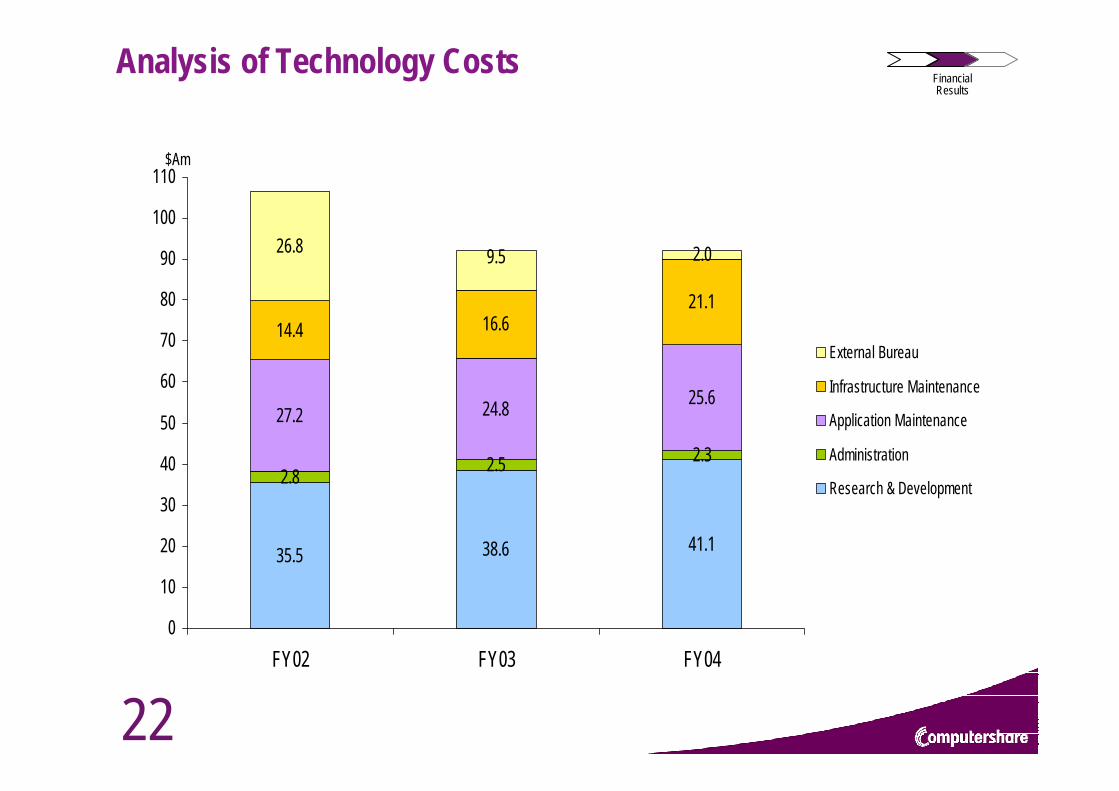

Analysis of Technology CostsFinancialResults

35.5 38.6 41.1

2.8 2.5 2.3

27.2 24.8 25.6

14.4 16.621.1

26.8 2.09.5

0

10

20

30

40

50

60

70

80

90

100

110

FY02 FY03 FY04

$Am

External Bureau

Infrastructure Maintenance

Application Maintenance

Administration

Research & Development

23

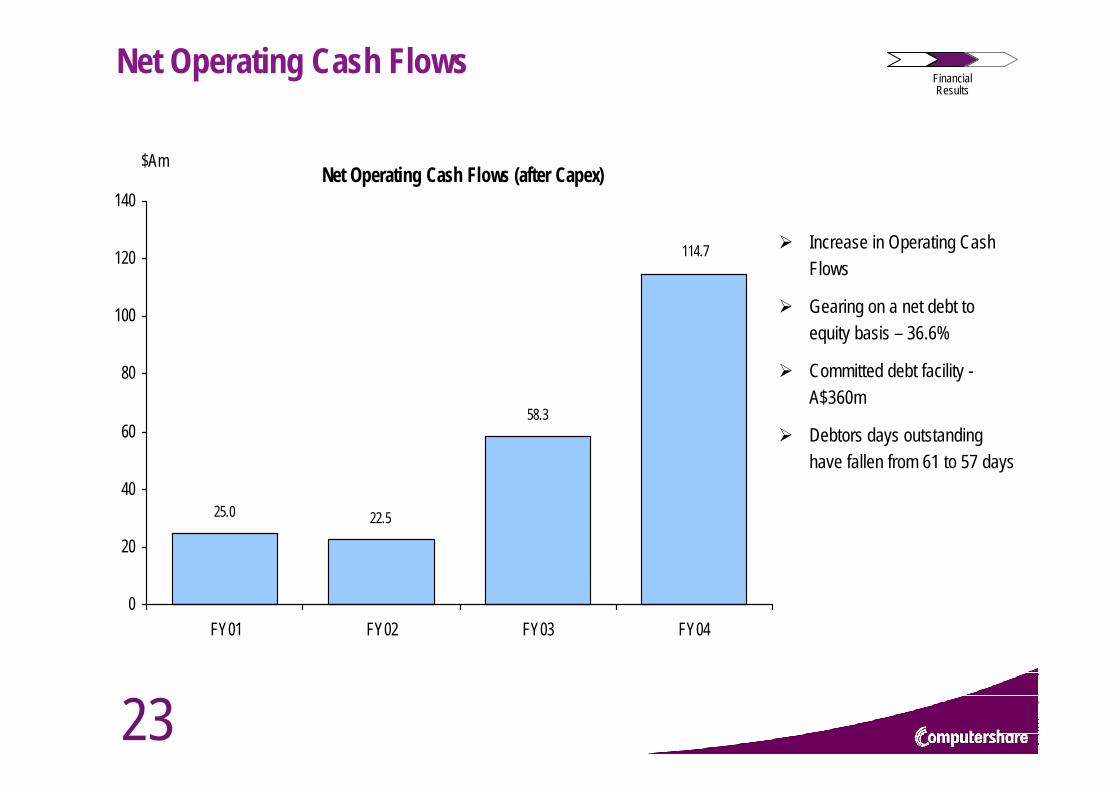

Net Operating Cash FlowsFinancialResults

Increase in Operating Cash Flows

Gearing on a net debt to equity basis – 36.6%

Committed debt facility -A$360m

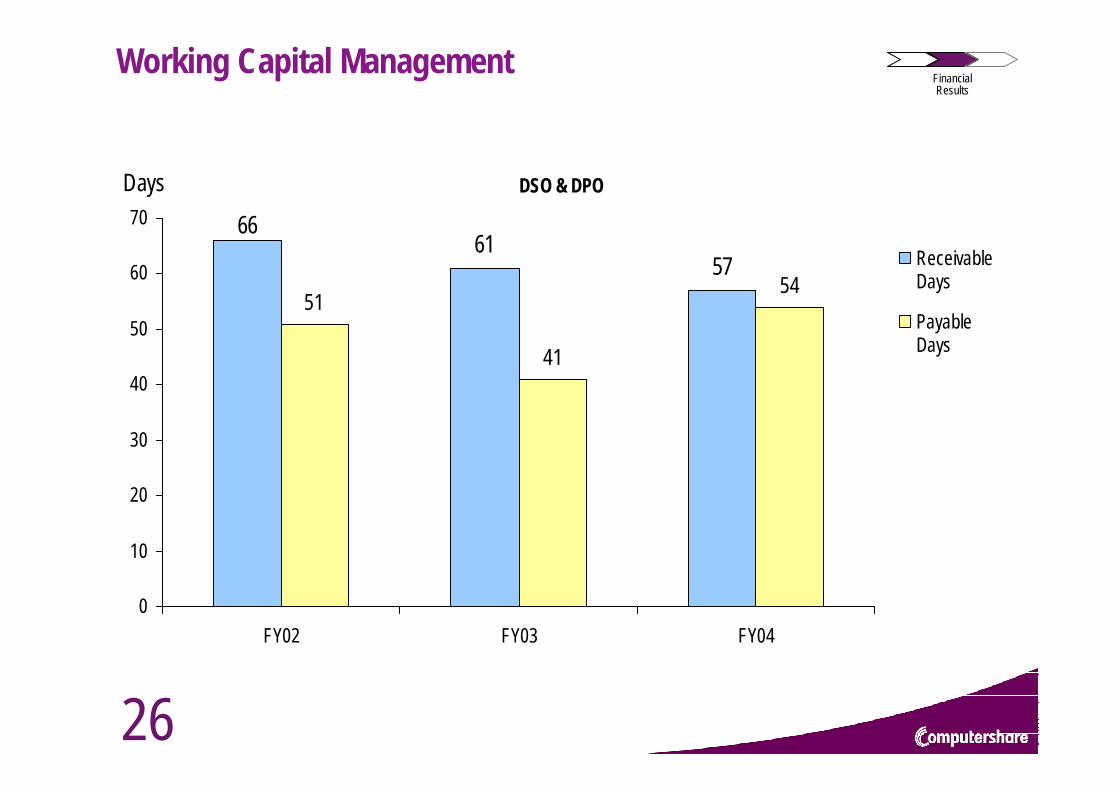

Debtors days outstanding have fallen from 61 to 57 days

Net Operating Cash Flows (after Capex)

25.0 22.5

58.3

114.7

0

20

40

60

80

100

120

140

FY01 FY02 FY03 FY04

$Am

24

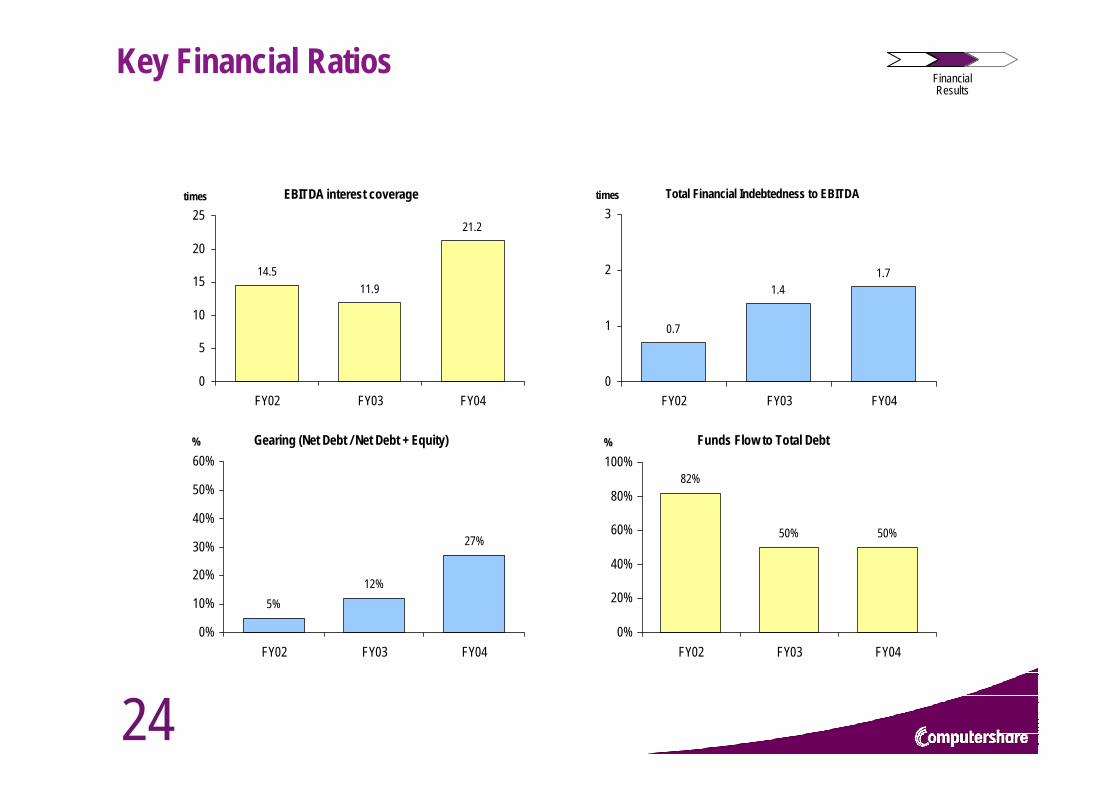

Key Financial Ratios

EBITDA interest coverage

14.511.9

21.2

0

5

10

15

20

25

FY02 FY03 FY04

times Total Financial Indebtedness to EBITDA

0.7

1.41.7

0

1

2

3

FY02 FY03 FY04

times

Gearing (Net Debt / Net Debt + Equity)

5%12%

27%

0%

10%

20%

30%

40%

50%

60%

FY02 FY03 FY04

% Funds Flow to Total Debt

82%

50% 50%

0%

20%

40%

60%

80%

100%

FY02 FY03 FY04

%

FinancialResults

25

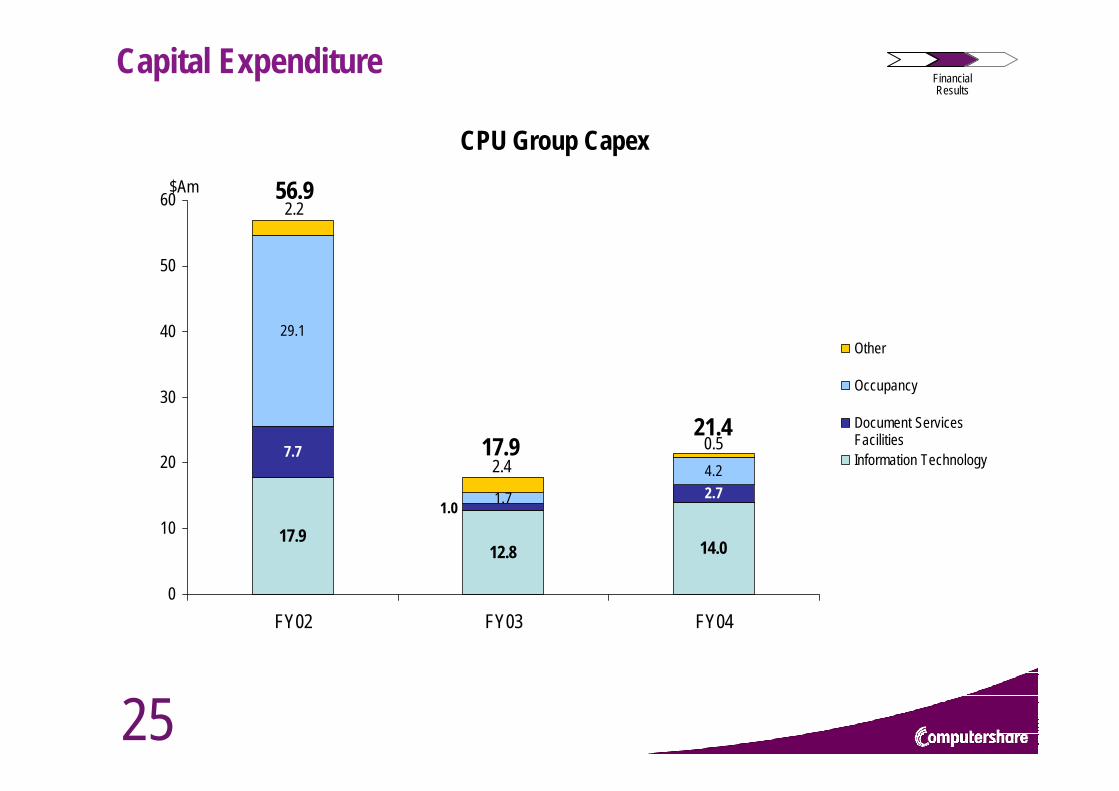

Capital Expenditure FinancialResults

17.912.8 14.0

7.7

2.7

29.1

1.7

4.2

1.0

0.52.4

2.2

0

10

20

30

40

50

60

FY02 FY03 FY04

$Am

Other

Occupancy

Document ServicesFacilitiesInformation Technology

CPU Group Capex

56.9

17.921.4

26

Working Capital ManagementFinancialResults

DSO & DPO

6157

51

41

54

66

0

10

20

30

40

50

60

70

FY02 FY03 FY04

Days

ReceivableDays

PayableDays

27

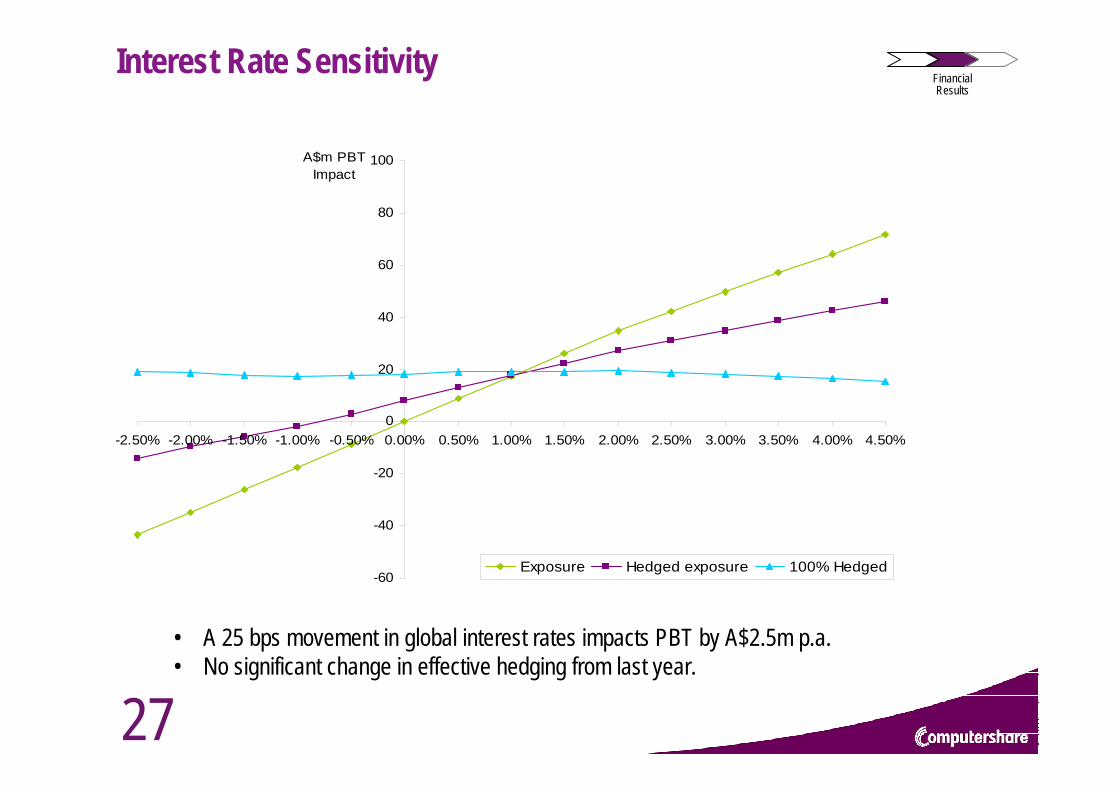

Interest Rate SensitivityFinancialResults

-60

-40

-20

0

20

40

60

80

100

-2.50% -2.00% -1.50% -1.00% -0.50% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50%

A$m PBTImpact

Exposure Hedged exposure 100% Hedged

• A 25 bps movement in global interest rates impacts PBT by A$2.5m p.a.• No significant change in effective hedging from last year.

28

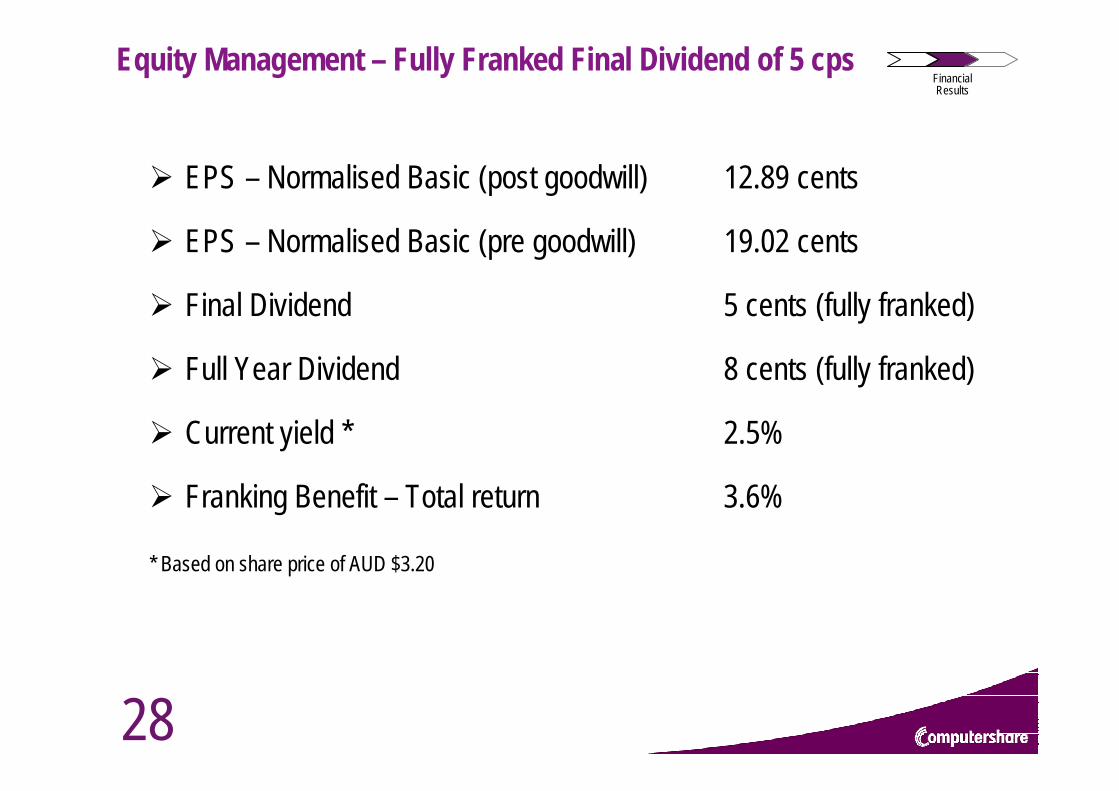

Equity Management – Fully Franked Final Dividend of 5 cps

EPS – Normalised Basic (post goodwill) 12.89 cents

EPS – Normalised Basic (pre goodwill) 19.02 cents

Final Dividend 5 cents (fully franked)

Full Year Dividend 8 cents (fully franked)

Current yield * 2.5%

Franking Benefit – Total return 3.6%

* Based on share price of AUD $3.20

FinancialResults

29

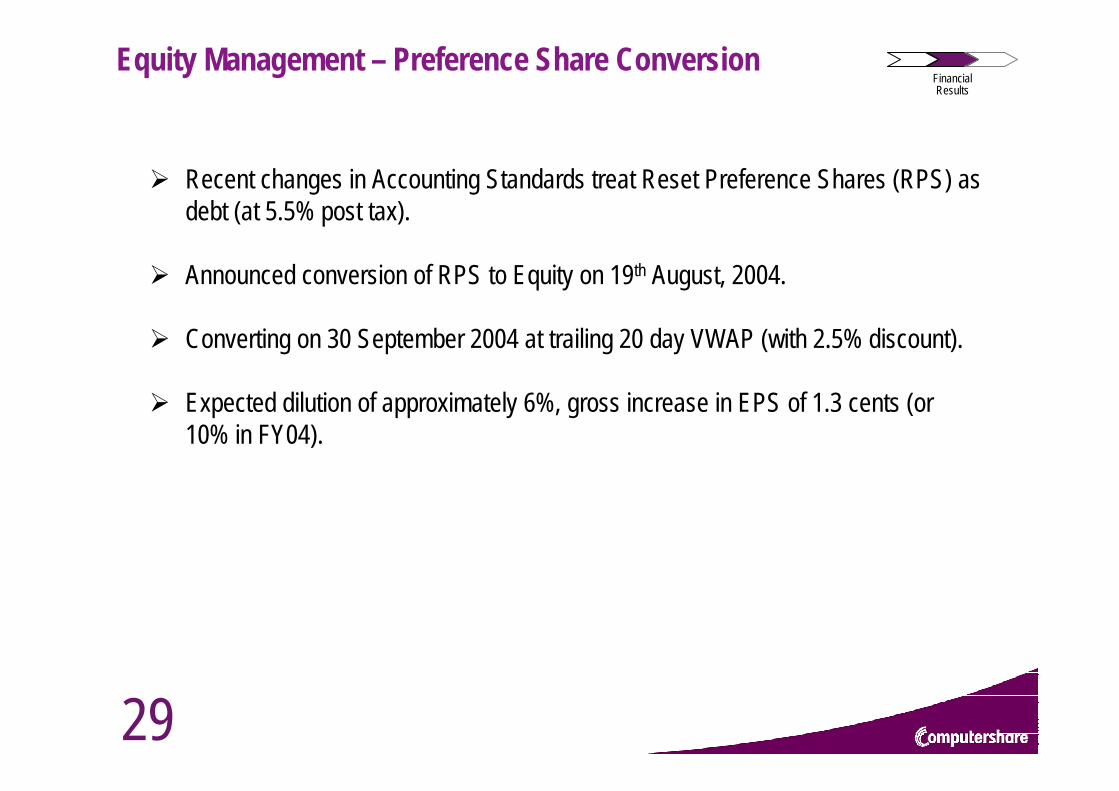

Equity Management – Preference Share ConversionFinancialResults

Recent changes in Accounting Standards treat Reset Preference Shares (RPS) as debt (at 5.5% post tax).

Announced conversion of RPS to Equity on 19th August, 2004.

Converting on 30 September 2004 at trailing 20 day VWAP (with 2.5% discount).

Expected dilution of approximately 6%, gross increase in EPS of 1.3 cents (or 10% in FY04).

30

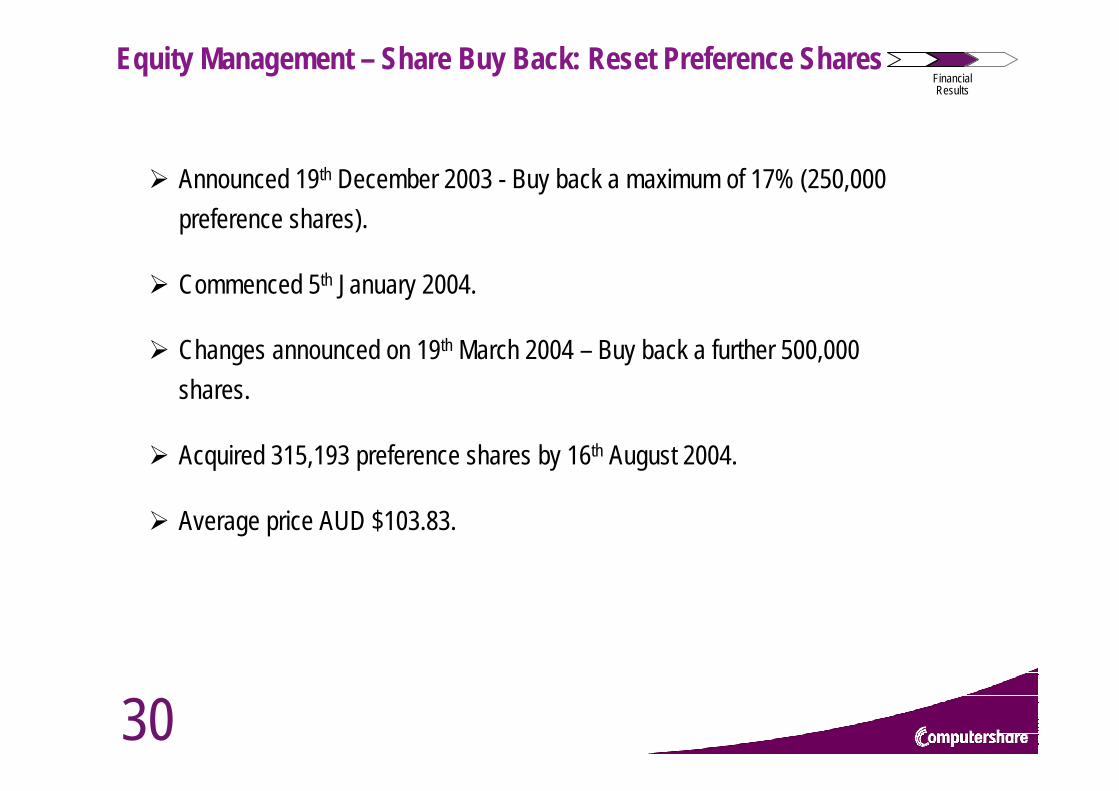

Equity Management – Share Buy Back: Reset Preference SharesFinancialResults

Announced 19th December 2003 - Buy back a maximum of 17% (250,000 preference shares).

Commenced 5th January 2004.

Changes announced on 19th March 2004 – Buy back a further 500,000 shares.

Acquired 315,193 preference shares by 16th August 2004.

Average price AUD $103.83.

31

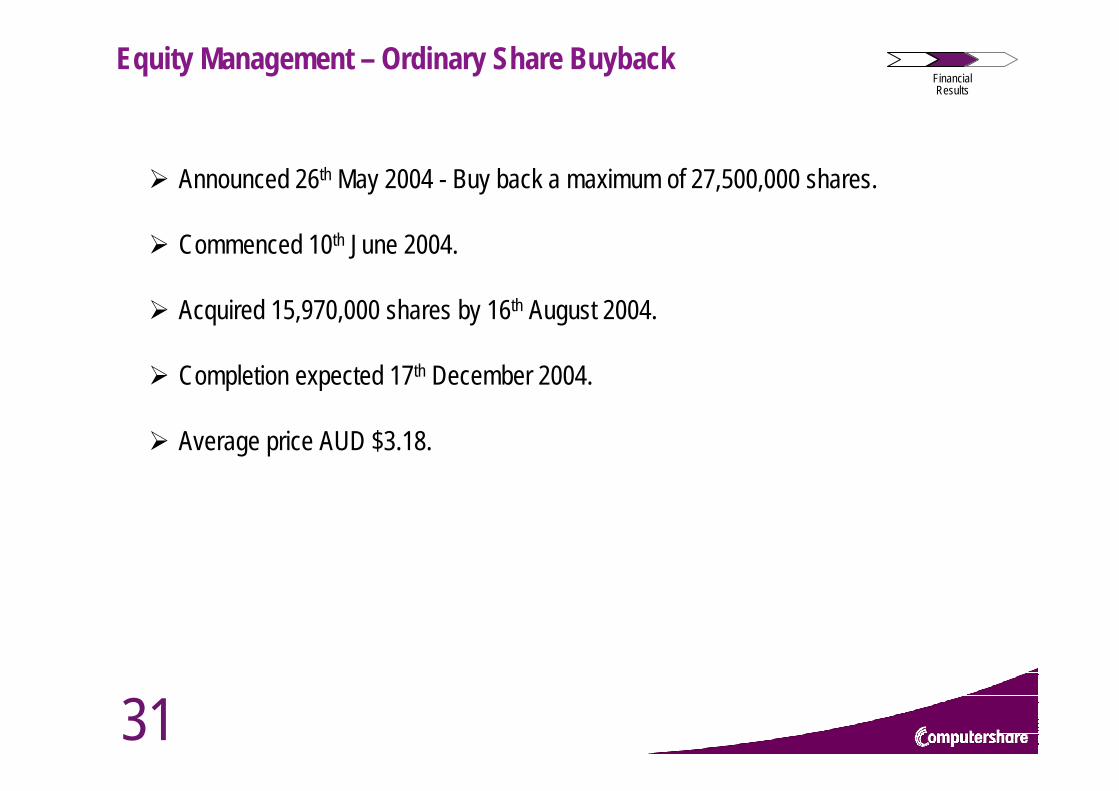

Equity Management – Ordinary Share BuybackFinancialResults

Announced 26th May 2004 - Buy back a maximum of 27,500,000 shares.

Commenced 10th June 2004.

Acquired 15,970,000 shares by 16th August 2004.

Completion expected 17th December 2004.

Average price AUD $3.18.

32

Financial SummaryFinancialResults

Normalised Earnings per Share (pre goodwill) rose from 11.79 to 19.02 cents per share.

Net operating Cash Flows were $136.1m (an increase of 79% on FY 2003).

Revenues increased 24% to $894.7m.

Normalised EBITDA up 37% to $183.4m

Operating expenses were $711.1m (inclusive of cost of sales). Excluding cost of sales & acquisitions, operating costs declined 1%.

Days Sales Outstanding were 57 days, down 4 days from June 2003.

Capital Expenditure was in line with expectation at $21.4 million.

33

MarketOverview

FinancialPerformance CEO’s Report

34

Increased Revenue & Profit

Major focus on capital management

Capital Expenditure

Cash Flow

Focus on EPS for future reporting

CEO’sReport

Highlights - Financial

35

Regional Highlights – Asia/Pacific

India Hong KongPhilippines

Australia New Zealand

36

Relocated to Global Headquarters

Regional Highlights – Asia/Pacific CEO’sReport

37

Call Centre (from worst to first)

Regional Highlights – Asia/Pacific CEO’sReport

38

Regional Highlights – Asia/Pacific

Australia: Significant improvement in productivity, accuracy and efficiency

Introduction of Workflow / EDC resulted in 65% productivity improvement over 18 monthsIAG significant winMore than 75% of clients have taken our integrated offering

India – Results better than budgetConsistent flows in IPOs from mainland China into Hong Kong with 23 IPOs won between February and July 2004

CEO’sReport

39

Ireland United Kingdom

Germany South AfricaRussia

Regional Highlights - EMEA

40

Regional Highlights - EMEA

South Africa significant turnaround in EBITDAGermany

Design and implementation of new registry systemAll companies migrated from Deutsche Bourse systemCreation of Plans divisionNow operating profitably

Gilts & NHS in UKAppointed Geoff Price, Managing Director Plans

CEO’sReport

41

Regional Highlights – North America

United States of America Canada

CEO’sReport

42

GeorgesonIntegration benefits better than expectedMajor synergies starting to be realisedRationalization of offices underwaySignificant savings in operational areasNow have 35 people in sales force in USInherited great staff who have added to management strengthPlenty of upside to comeAcquisition of Alamo to merge with GSC, creating end-to-end proxy service for Mutual Funds (print/solicitation/tabulation)

Regional Highlights – North America CEO’sReport

43

Regional Highlights – North America

TranscentiveLes Trachtman, Global head of business development for PlansExpanding their products globally

EuropeHong Kong, ChinaIndia

Selling web-based solutions hosted in USA22 New clients have been signed since acquisitionExceeding financial forecast

CEO’sReport

44

Growing our Cross-Sell opportunities in North AmericaNew Business from cross sales $15.1 million

Benefits spread across all business solutionsAnalytics $0.4 millionCorporate Actions $1.0 millionPlans $0.1 millionPost Merger Clean-up $3.2 millionDocument Services $4.0 millionProxy Solicitation $1.7 millionSmall Shareholder Plans $3.7 millionTransfer Agency (Registrar) $1.0 million

Regional Highlights – North America CEO’sReport

45

Canada efficiency gains (overtime 5% of a year ago)

Restructured Canadian Trust business - now showing solid growth

Centralization of sales and marketing in North America

Significant business wins in the US include:News CorporationAlltel

Regional Highlights – North America CEO’sReport

46

Document ServicesBrilliant resultsThe only global print/mail operationSeeking opportunities to expand in

PerthSouth AfricaIreland

Alamo gives us an East coast facility

Highlights - Global CEO’sReport

47

AnalyticsIntegration into Georgesons’ Stock ID completedAppointed Paul Conn as Global Managing DirectorIR Track released Deal with NASDAQ and in discussions with other major exchangesSome work outsourced to our Philippine businessGlobal development completed

Highlights - Global CEO’sReport

48

Highlights - Global

PepperERM forecast revenues this year > $15m plus + $$ to Plan ManagersCRM expanded to Asia Pacific and North America: revenues now over $25m per yearSRM strong in the UK and Australia, first clients signed up in the US, adds significant value to our other businesses like SSPeTree

Australia – Landcare Australia32 Major Australian companies participating446,000 trees planted or planned

US – American ForestsCanada – Tree Canada FoundationUK – Future Forests

CEO’sReport

49

WHERE TO FROM HERE?

CEO’sReport

50

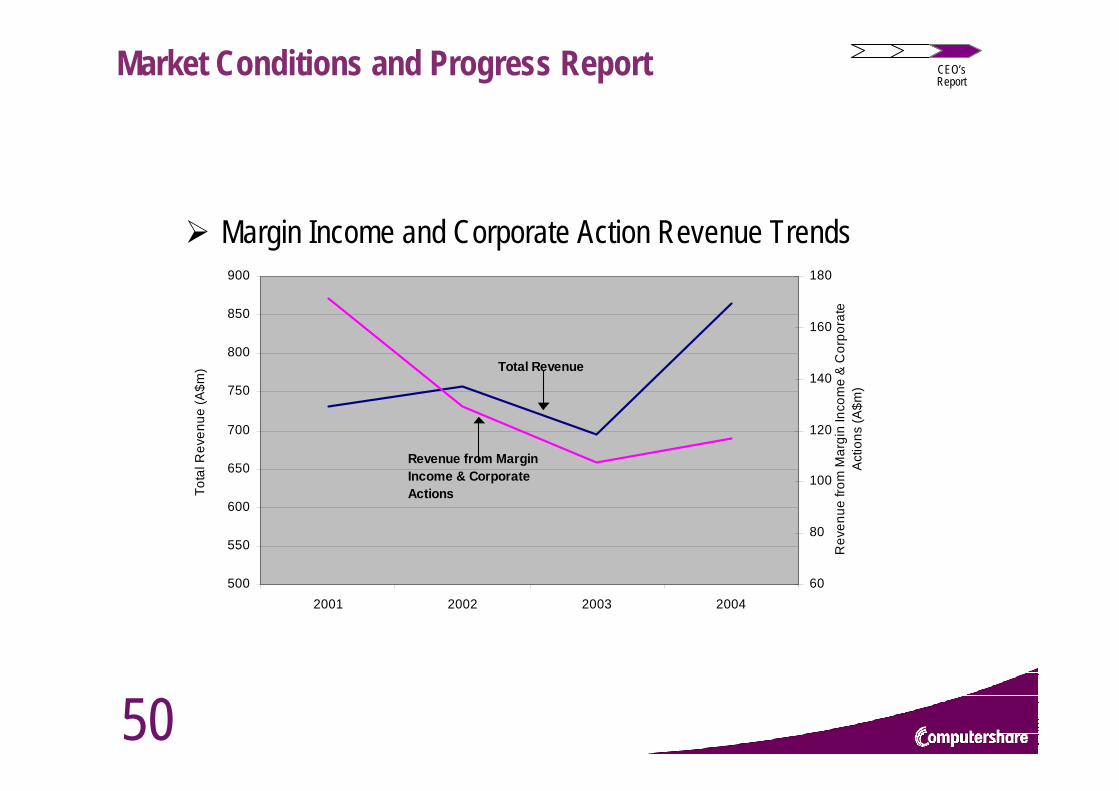

Margin Income and Corporate Action Revenue Trends

500

550

600

650

700

750

800

850

900

2001 2002 2003 2004

Tota

l Rev

enue

(A$m

)

60

80

100

120

140

160

180

Rev

enue

from

Mar

gin

Inco

me

& C

orpo

rate

A

ctio

ns (A

$m)

Total Revenue

Revenue from Margin Income & Corporate Actions

Market Conditions and Progress Report CEO’sReport

51

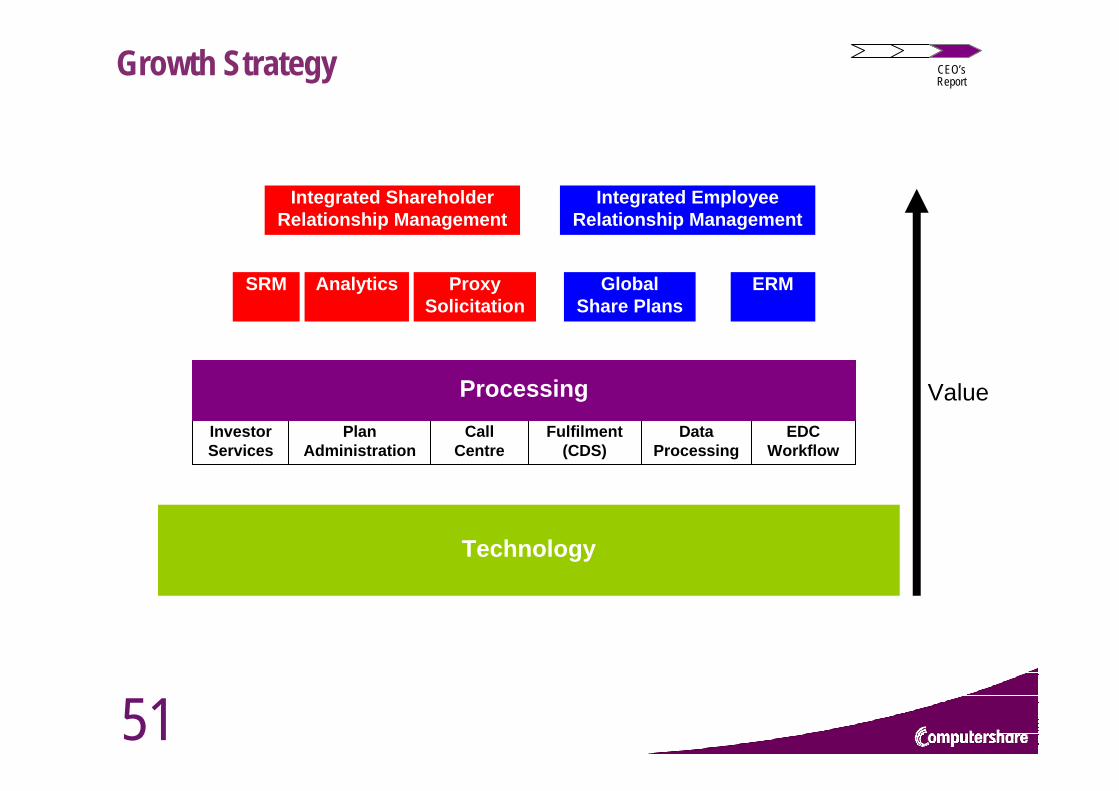

Integrated Shareholder Relationship Management

Integrated Employee Relationship Management

SRM ProxySolicitation

Analytics ERMGlobal Share Plans

Investor Services

Plan Administration

Call Centre

Fulfilment (CDS)

Data Processing

EDC Workflow

Technology

ValueProcessing

Growth Strategy CEO’sReport

52

Revenue growth > 10%

Growth in EPS > 20%

Guidance for FY 2005 will be established within the context of these metrics

Outlook CEO’sReport

53

QUESTIONS?

CEO’sReport

54

Financial Year 2004 Final Results Presentation

19 August 2004

FinancialResults

55

Appendix 1: Group ComparisonsFinancialResults

Group Comparisons

56

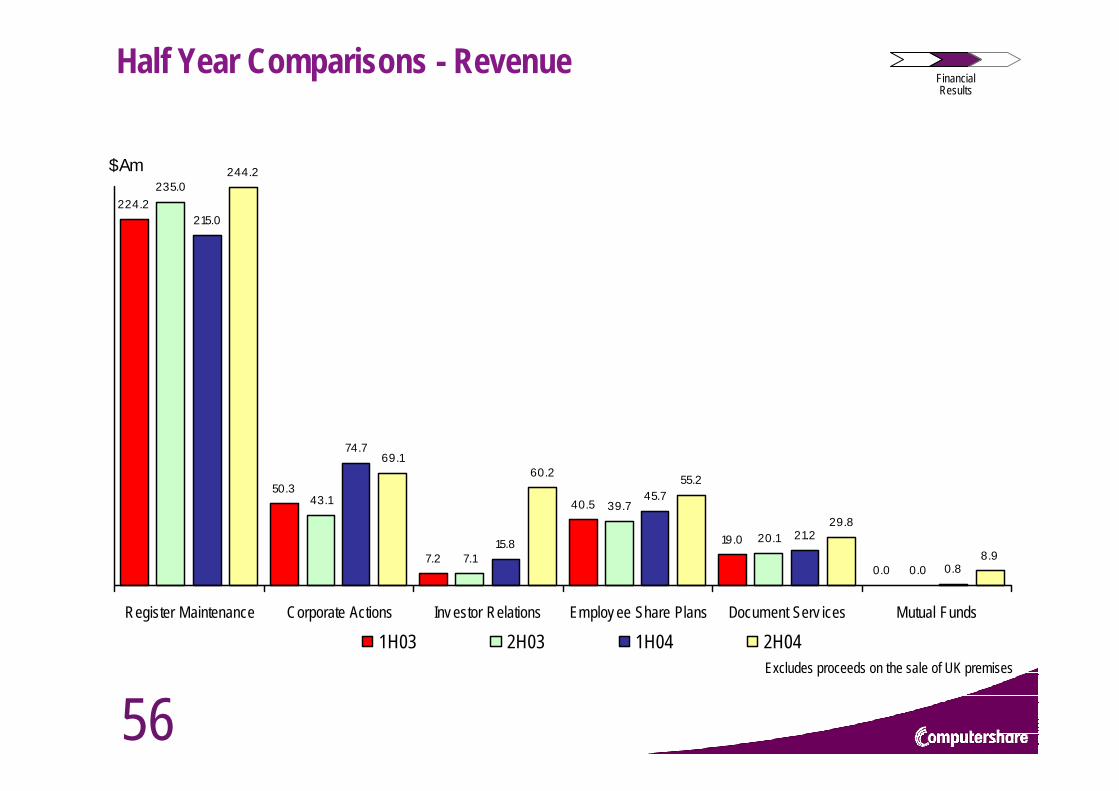

Half Year Comparisons - RevenueFinancialResults

224.2

50.3

7.2

40.5

19.0

0.0

235.0

43.1

7.1

39.7

20.1

0.0

215.0

74.7

15.8

45.7

21.2

0.8

244.2

69.1

55.2

29.8

8.9

60.2

Register Maintenance Corporate Actions Inv estor Relations Employ ee Share Plans Document Serv ices Mutual Funds

$Am

1H03 2H03 1H04 2H04Excludes proceeds on the sale of UK premises

57

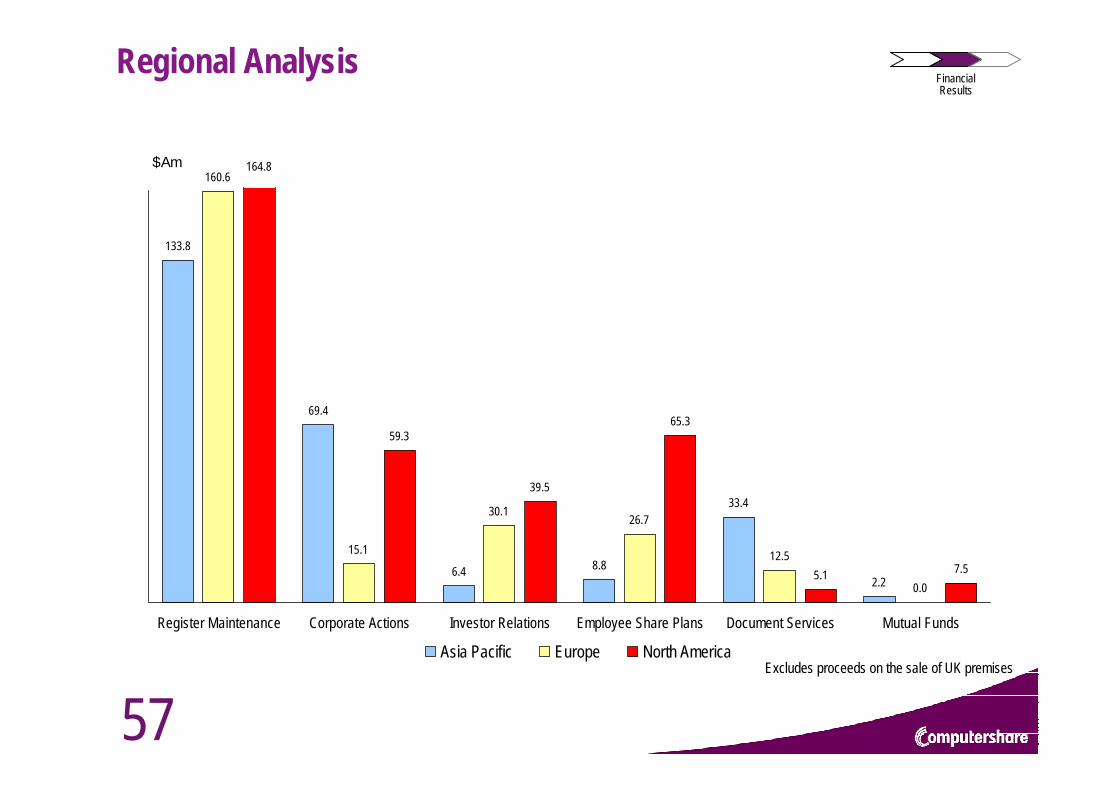

Regional AnalysisFinancialResults

133.8

69.4

6.4 8.8

33.4

2.2

160.6

15.1

30.126.7

12.5

0.0

164.8

59.3

39.5

65.3

5.1 7.5

Register Maintenance Corporate Actions Investor Relations Employee Share Plans Document Services Mutual Funds

$Am

Asia Pacific Europe North AmericaExcludes proceeds on the sale of UK premises

58

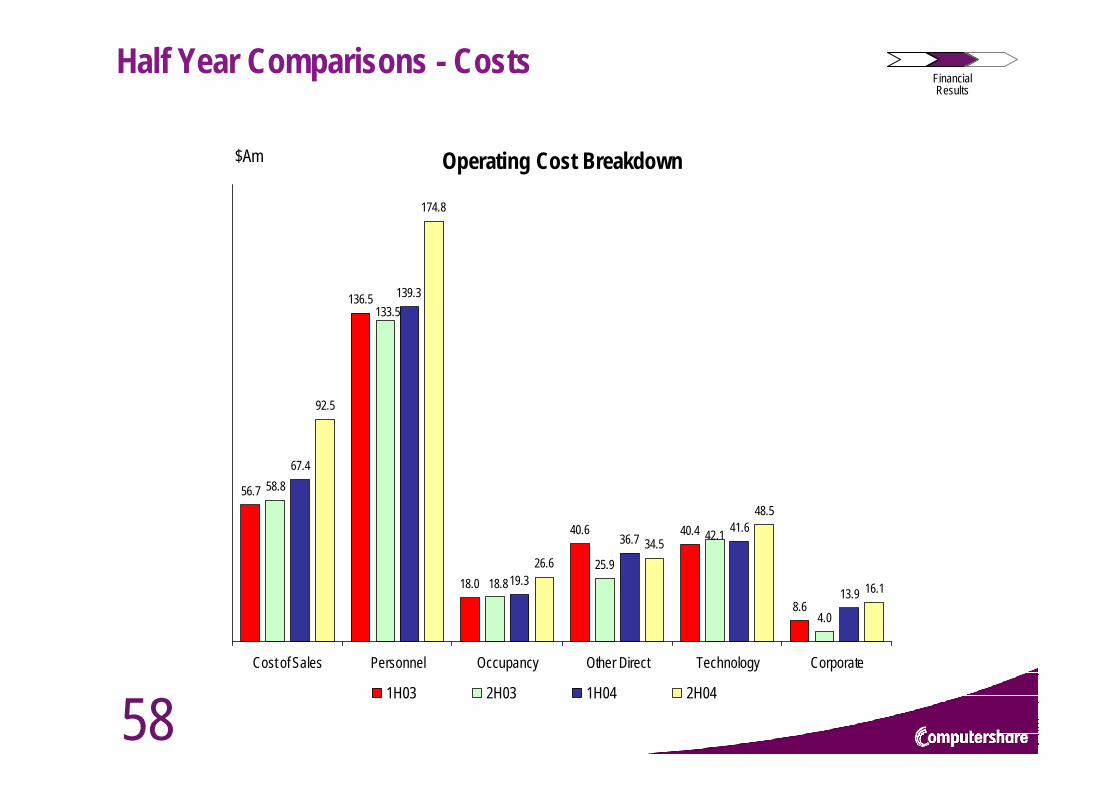

Half Year Comparisons - CostsFinancialResults

Operating Cost Breakdown

56.7

136.5

18.0

40.6 40.4

8.6

58.8

25.9

4.0

67.4

139.3

19.3

36.741.6

13.9

92.5

174.8

26.634.5

48.5

16.1

42.1

133.5

18.8

Cost of Sales Personnel Occupancy Other Direct Technology Corporate

$Am

1H03 2H03 1H04 2H04

59

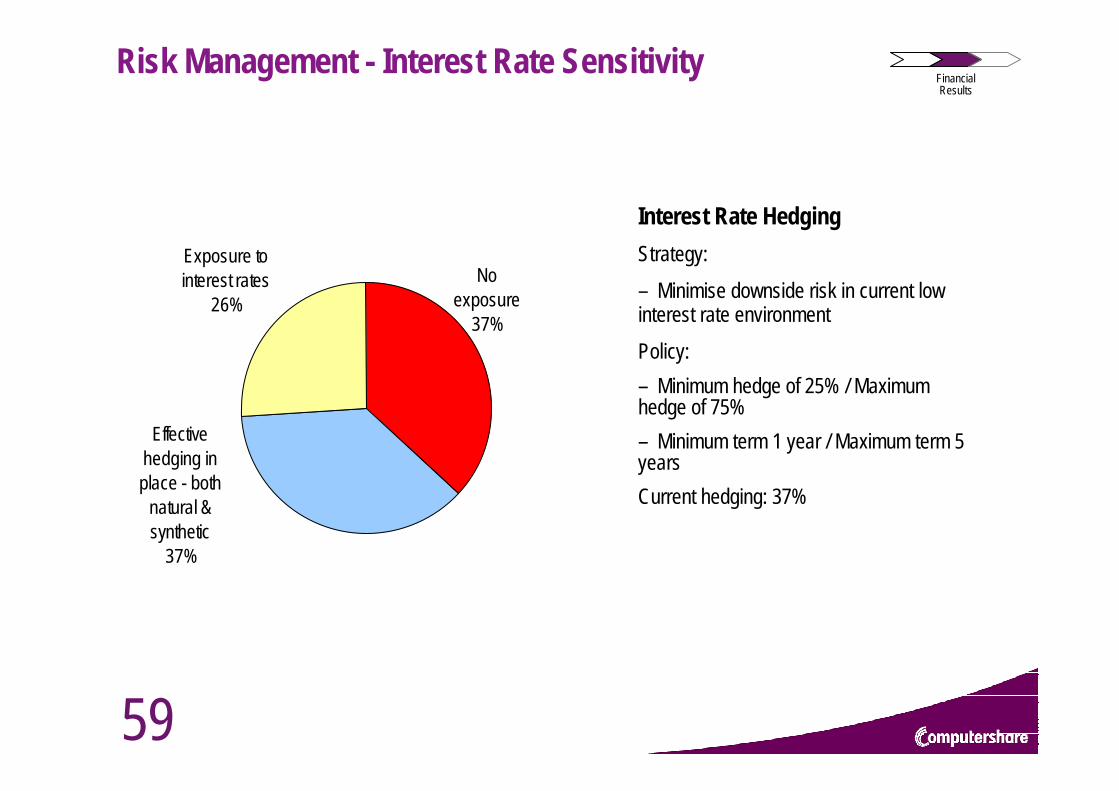

Risk Management - Interest Rate Sensitivity

Exposure to interest rates

26%

Effective hedging in place - both

natural & synthetic

37%

No exposure

37%

Interest Rate HedgingStrategy:– Minimise downside risk in current low interest rate environmentPolicy:– Minimum hedge of 25% / Maximum hedge of 75%– Minimum term 1 year / Maximum term 5 yearsCurrent hedging: 37%

FinancialResults

60

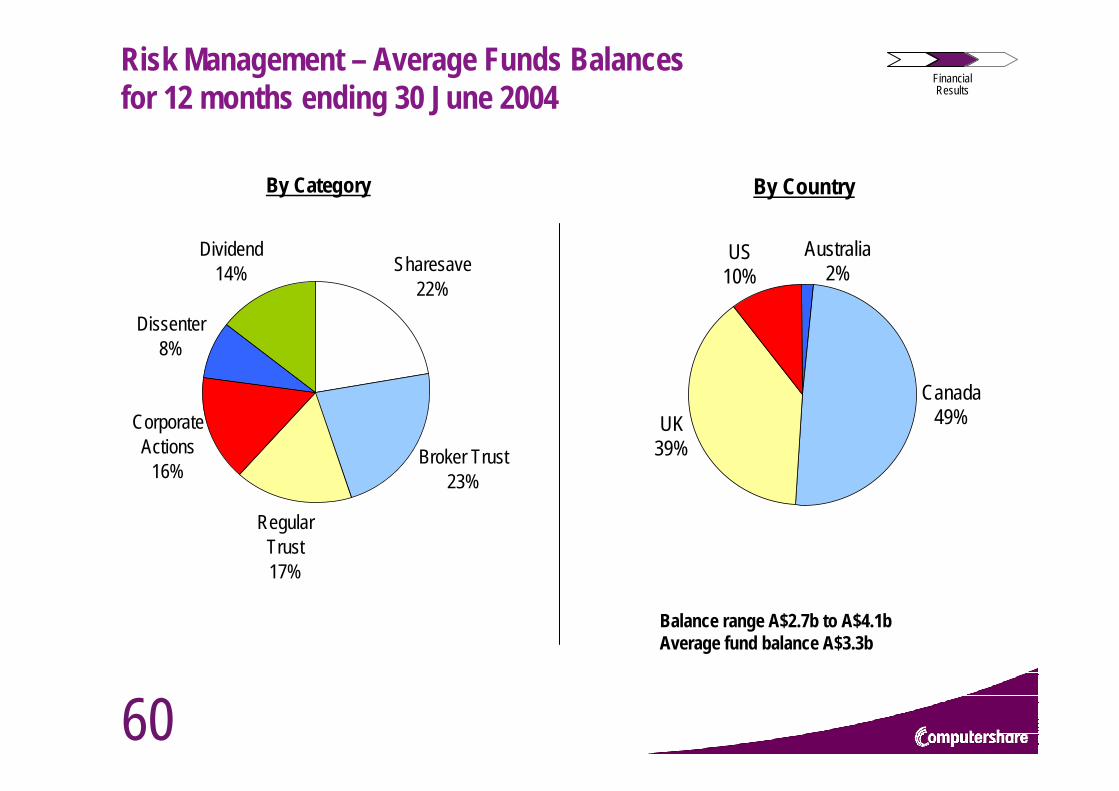

Risk Management – Average Funds Balances for 12 months ending 30 June 2004

Balance range A$2.7b to A$4.1bAverage fund balance A$3.3b

FinancialResults

By Category

Sharesave22%

Broker Trust23%

Corporate Actions

16%

Dissenter8%

Dividend14%

Regular Trust17%

By Country

Canada49%UK

39%

US10%

Australia2%

61

Appendix 2: Country SummariesFinancialResults

Country Summaries

62

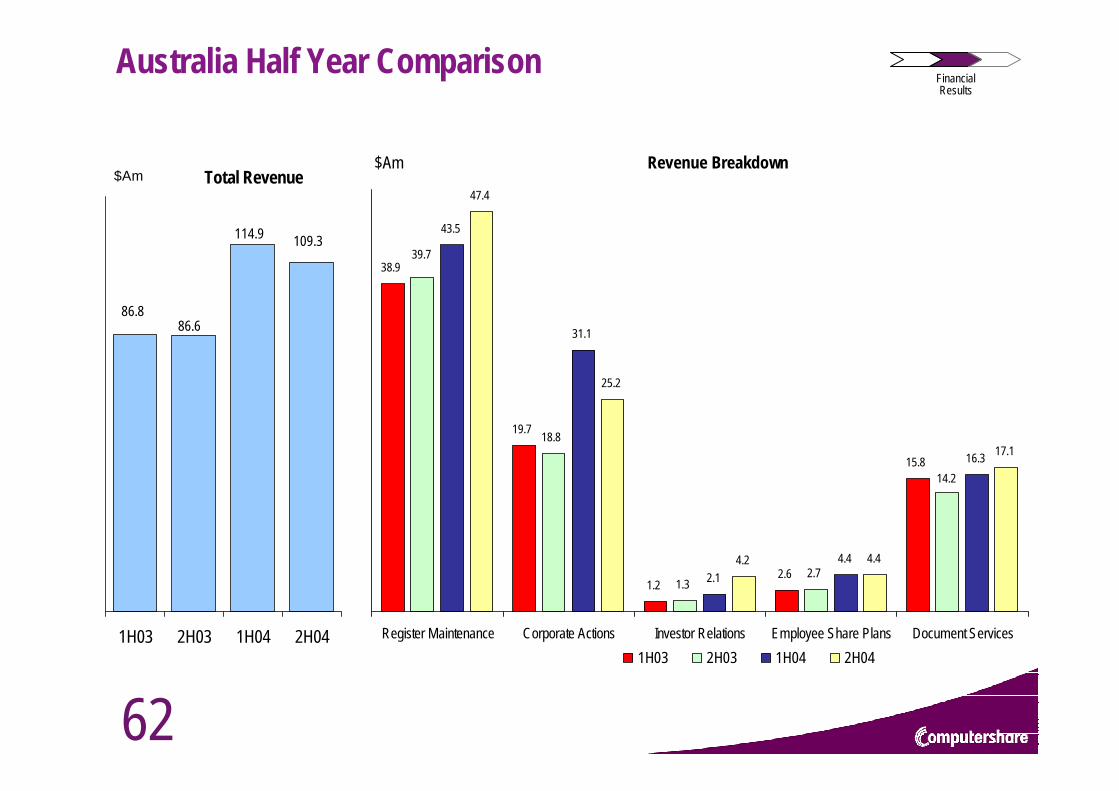

Australia Half Year Comparison

Revenue Breakdown

38.9

19.7

1.22.6

15.8

18.8

1.32.7

43.5

31.1

2.14.4

16.3

47.4

25.2

4.2 4.4

17.1

39.7

14.2

Register Maintenance Corporate Actions Investor Relations Employee Share Plans Document Services

$Am

1H03 2H03 1H04 2H04

Total Revenue

86.886.6

109.3114.9

1H03 2H03 1H04 2H04

$Am

FinancialResults

63

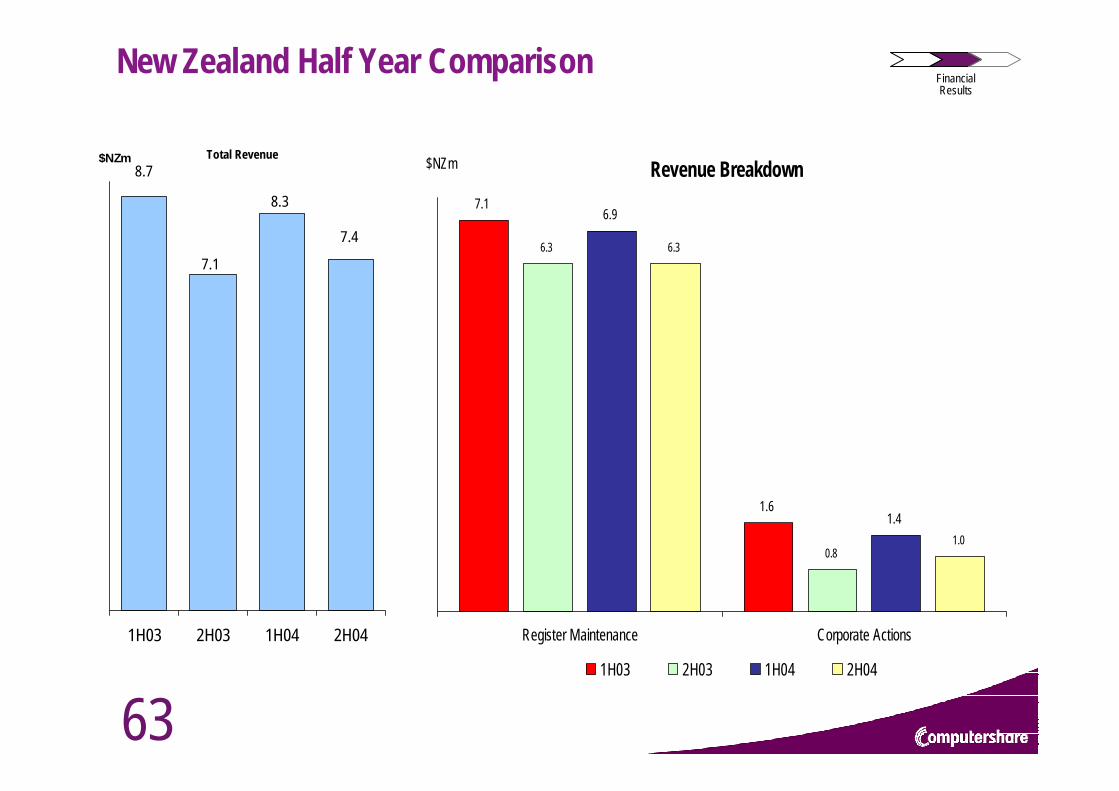

New Zealand Half Year Comparison

Revenue Breakdown7.1

1.6

6.3

0.8

6.9

1.4

6.3

1.0

Register Maintenance Corporate Actions

$NZm

1H03 2H03 1H04 2H04

Total Revenue8.7

7.1

7.4

8.3

1H03 2H03 1H04 2H04

$NZm

FinancialResults

64

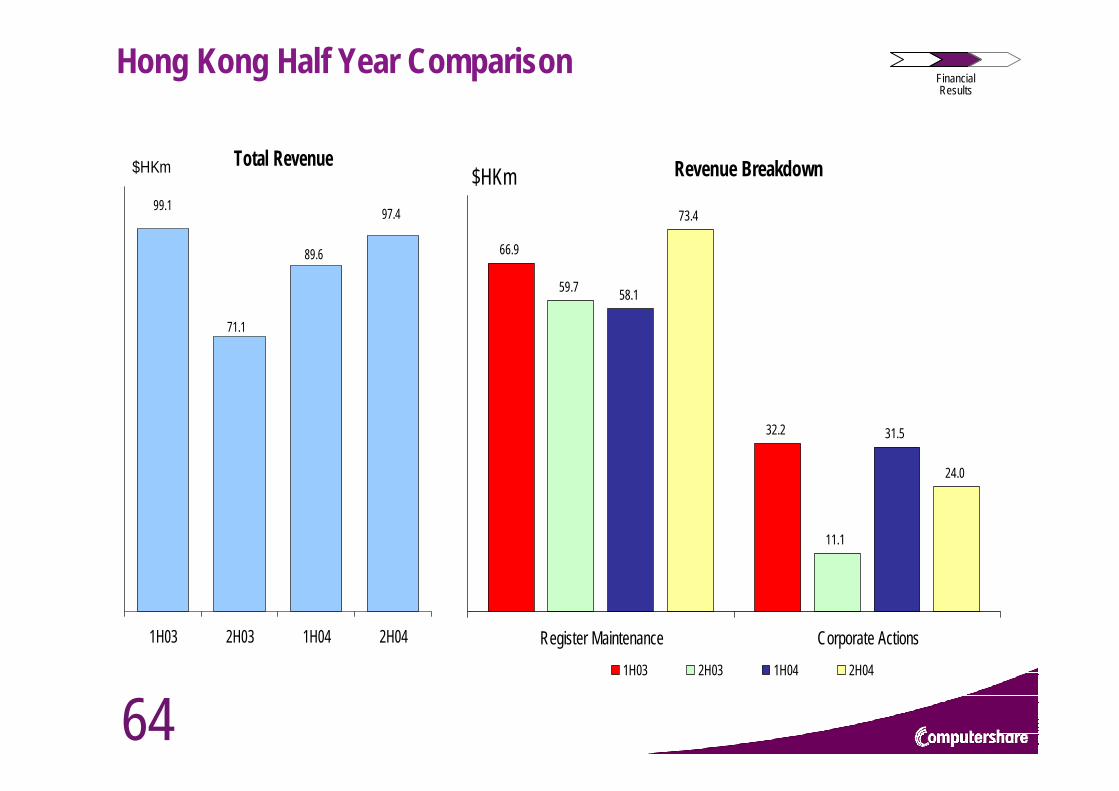

Hong Kong Half Year Comparison

Total Revenue

89.6

97.4

71.1

99.1

1H03 2H03 1H04 2H04

$HKm Revenue Breakdown

66.9

32.2

59.7

11.1

58.1

31.5

24.0

73.4

Register Maintenance Corporate Actions

$HKm

1H03 2H03 1H04 2H04

FinancialResults

65

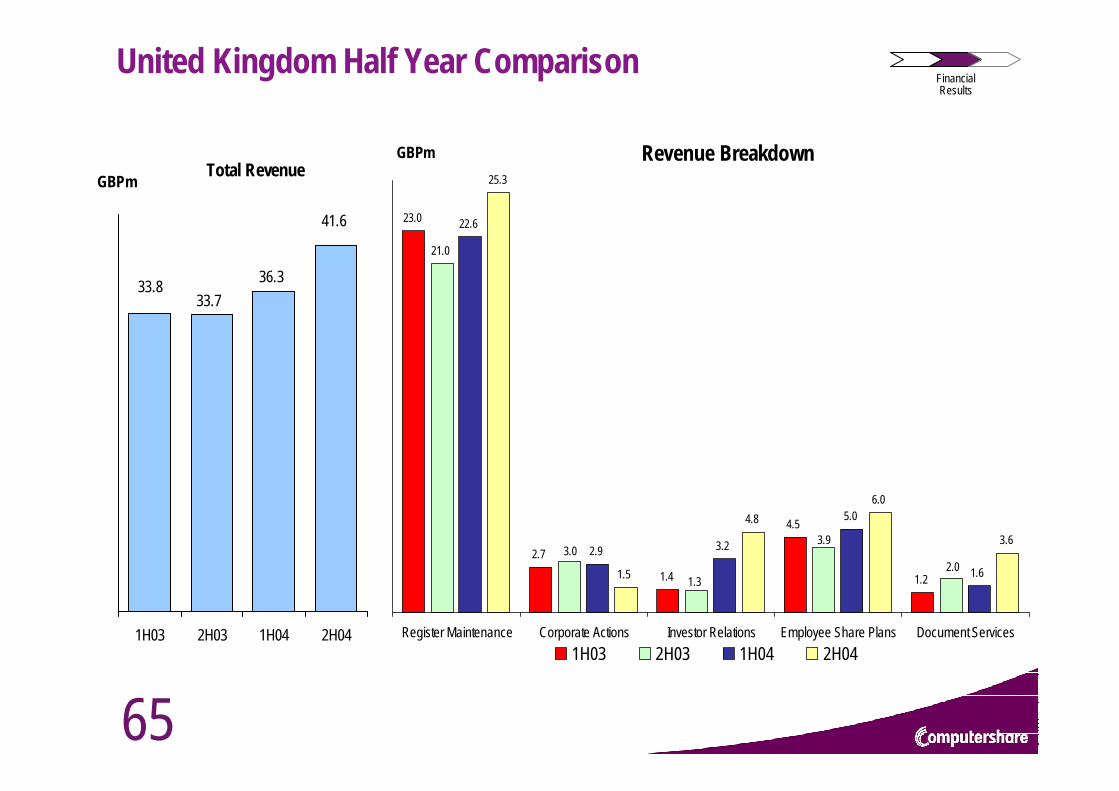

United Kingdom Half Year Comparison

Revenue Breakdown

23.0

2.7

1.4

4.5

1.2

21.0

22.6

2.9 3.2

5.0

1.6

25.3

1.5

4.86.0

3.63.0

2.0

3.9

1.3

Register Maintenance Corporate Actions Investor Relations Employee Share Plans Document Services1H03 2H03 1H04 2H04

GBPmTotal Revenue

33.833.7

41.6

36.3

1H03 2H03 1H04 2H04

GBPm

FinancialResults

66

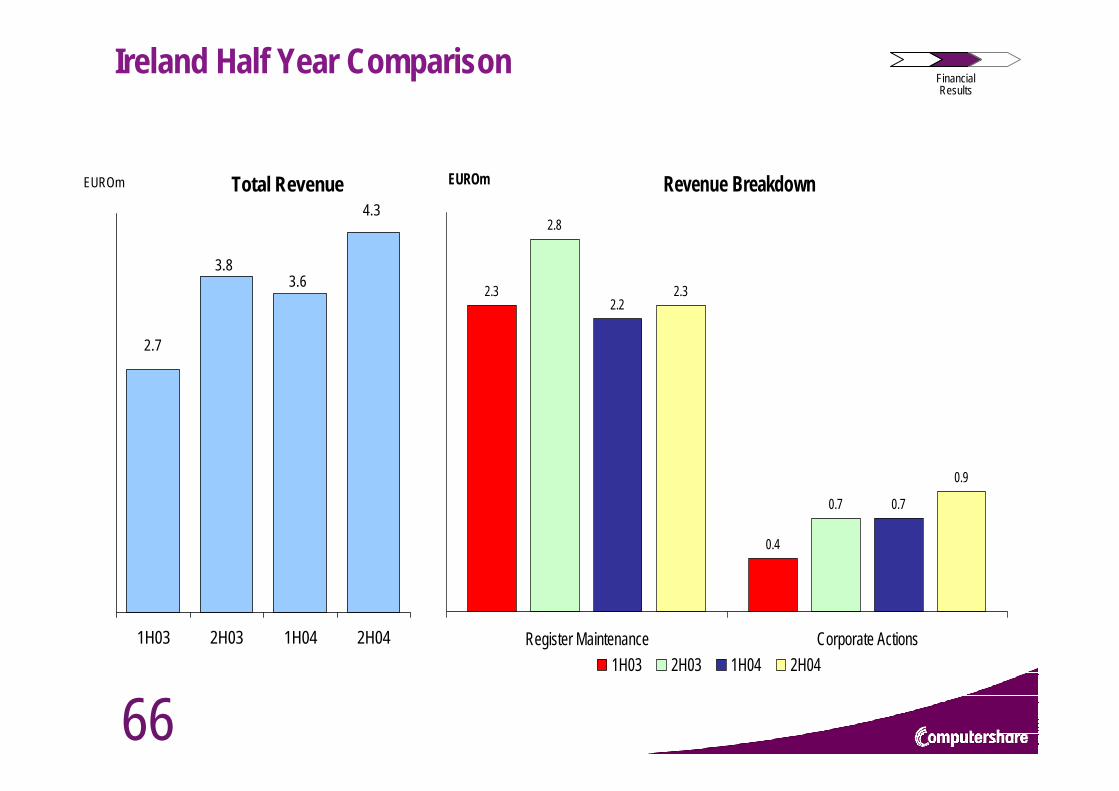

Ireland Half Year Comparison

Revenue Breakdown

2.3

0.4

2.8

0.7

2.2

0.7

2.3

0.9

Register Maintenance Corporate Actions

EUROm

1H03 2H03 1H04 2H04

Total Revenue

2.7

3.8

4.3

3.6

1H03 2H03 1H04 2H04

EUROm

FinancialResults

67

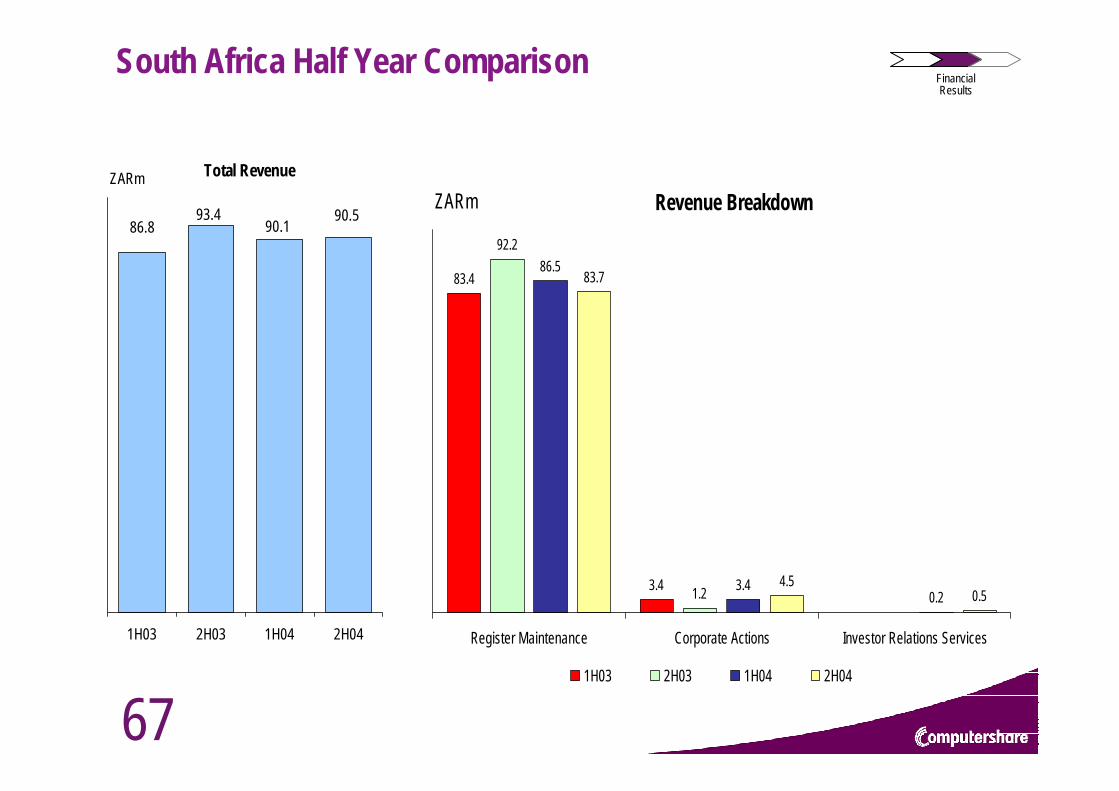

South Africa Half Year Comparison

Revenue Breakdown

83.4

3.4

92.2

1.2

86.5

3.40.2

83.7

4.50.5

Register Maintenance Corporate Actions Investor Relations Services

ZARm

1H03 2H03 1H04 2H04

Total Revenue

86.893.4 90.5

90.1

1H03 2H03 1H04 2H04

ZARm

FinancialResults

68

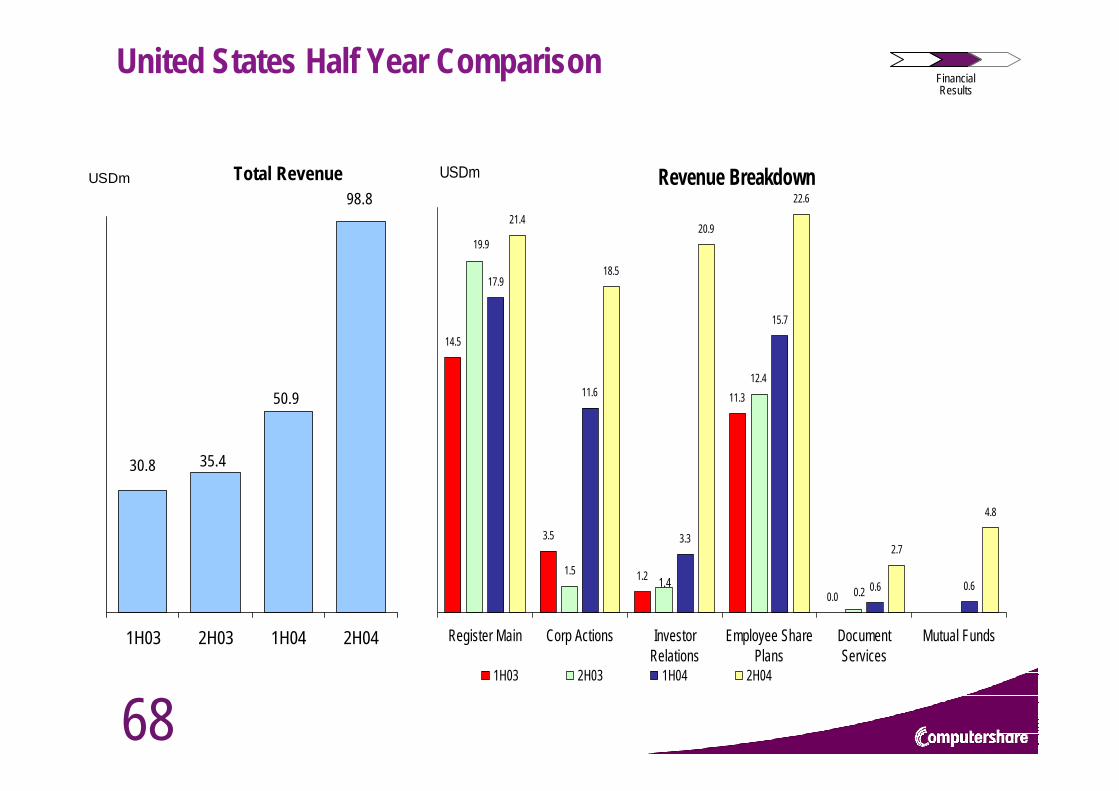

United States Half Year Comparison

Revenue Breakdown

14.5

3.5

1.2

11.3

0.0

1.5

12.4

17.9

11.6

3.3

15.7

0.6 0.6

21.4

18.5

20.9

22.6

2.7

4.8

1.40.2

19.9

Register Main Corp Actions InvestorRelations

Employee SharePlans

DocumentServices

Mutual Funds

USDm

1H03 2H03 1H04 2H04

Total Revenue

30.8 35.4

98.8

50.9

1H03 2H03 1H04 2H04

USDm

FinancialResults

69

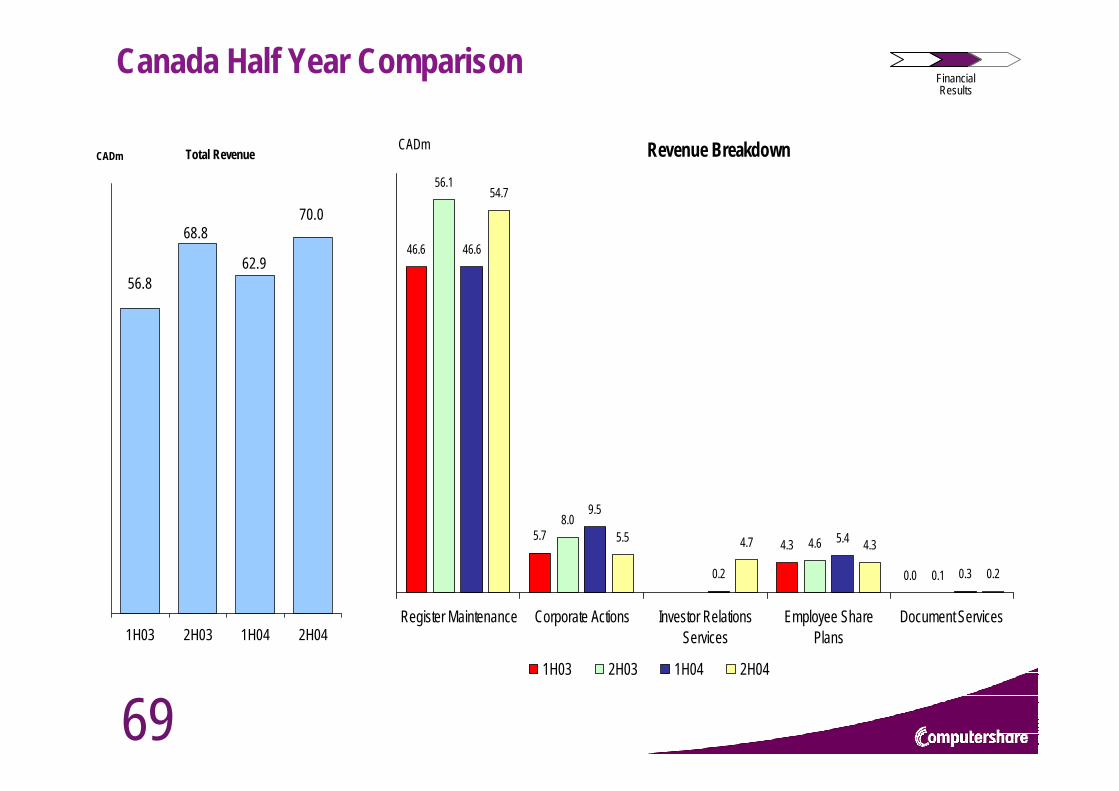

Canada Half Year Comparison

Revenue Breakdown

46.6

5.74.3

0.0

8.0

4.6

0.1

46.6

9.5

0.2

5.4

0.3

54.7

5.5 4.7 4.3

0.2

56.1

Register Maintenance Corporate Actions Investor RelationsServices

Employee SharePlans

Document Services

CADm

1H03 2H03 1H04 2H04

Total Revenue

56.8

68.870.0

62.9

1H03 2H03 1H04 2H04

CADm

FinancialResults