Embed Size (px)

Citation preview

Financial Stewardship

<>

A practical approach

Robert Sterling CPA, CA, FCCA

YOUR CURRENT FINANCIAL POSITION

Gather the facts (current position)

Assess your current position

Set/adjust objectives & expectations

Work on your objectives & expectations

Regularly review results with

expectations

Personal budget and cash flow statement

Personal budget or a home budget is a finance plan that allocates future income towards expenses, debt repayment and savings.

Example of personal budget: Personal monthly budget1.xlsx

Personal cash flow statement – measures cash inflows and outflows in order to show your net cash flow for a specific period of time.

Example of a cash flow statement: Personal cash flow statement.xlsx

DEBT MANAGEMENT Loan and Credit

Credit Scores

Using Credit Wisely

Last strategy to settle debt•Debt counselling

•Consumer proposal or

•Bankruptcy

LOAN & CREDIT

LOAN – Money borrowed to be repaid with or without INTEREST (Bank loan, loan from family member, friend or peer).

CREDIT – Goods, services or money received for a promise to repay a definite sum of money back at a future date, (Credit card or consumer credit).

Classification of

Loan/Credit

SECURED UNSECUREDOPEND-ENDED

CLOSED -ENDED

LOAN & CREDIT

Secured loan – Borrower pledges asset (e.g. property or other valuables) as collateral. Interest rate is usually lower than unsecured loan. E.g. A mortgage is a secured loan.

Unsecured loan – No collateral is needed. Normally rely on credit history and current income level to qualify for unsecured loan. E.g. Lineof credit, bank overdrafts and some credit cards.

Opened-ended loan – Loan you can borrow over and over again. E.g. credit card and lines of credit are the most common types.

Closed-ended loans – Once repaid the loan is closed. E.g. mortgage or auto and student loan.

LOAN & CREDIT

Pay Day Loan

Consolidated Loan

TYPES OF

LOANS

Business Loan

Personal Loan

Education Loan

Vehicle Loan

Mortgage/Home

Loan

Consumer Credit/Loan

Policy Loan

Investment Loan

Term Loan

Vacation Loan

Advance Loan

CREDIT SCORE

What is a credit score?

• A NUMBER that is derived through calculation of various factors, that helps alender predict how likely an individual can or will repay a loan, or make creditpayments on time.

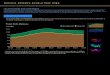

Factors used in the calculation:

Payment History,

35%

Current Debt, 30%

Credits used, 10%

Request new

credits, 10%

Credit History, 15%

CREDIT SCORE

What does the NUMBER reveals?

CREDIT SCORE

Obtain your score from:

•Equifax – Beacon Score, range between 300 – 850 (www.Equifax.ca ; telephone 1-800-465-7166)

• TransUnion – Empirica Score, range between 150 – 934 (www.transunion.ca ; telephone 1-800-663-990)

•Experian – FICO Score, range between 330 and 830 (www.Experian.com ; telephone 1-877-284-7942)

USING CREDIT

Bad Credit Purchases

• Credit card purchases - unplanned

• Consumer debt – unplanned

• Financing asset (eg. A car) for longer than its useful life.

• Financing a vacation trip using credit.

Good Credit Purchases

• Buy a house on credit. A smart investment.

• Financing education using credit.

• Buying a car using credit can also be a good purchase, if planned.

USING CREDIT

IMPROVE YOUR CREDIT SCORE

• Always (not sometime) pay your bills on time.

• pay your bills in full by the DUE DATE.

• Keep low balances credit card and line of credit.

• Do not open many credit accounts too quickly.

• Do not go over your credit limit on your credit card.

• Correct mistakes on your credit file.

• Ensure you have a credit history.

• Check your credit report.

USING CREDIT

Last strategies to settle outstanding debt

• Seek debt counselling:o To structure a repayment plan

o For debt consolidation

• Consumer Proposal:o Required to repay all outstanding debts but at a reduced amounts.

o Reduced amounts have to be repaid monthly until completed.

o A fee is charged to prepare a consumer proposal.

o Stays on your credit report 3 years after completion.

• Bankruptcy:o Last strategic arrangement.

o Usually gain full relief from unsecured debts, not secured debts

o A fee is charged to prepare a bankruptcy arrangement.

o Stays on your credit report 6 to 7 years after completion

o Affects your future dealings with financial institutions and employment

Savings and Investment Options

ComparisonFEATURES RRSP TFSA Chequing/saving

Main features • Registered

Retirement Saving

plan.

• Need earned

income to create

Contribution room.

• Must file a tax return.

• A registered

investment plan.

• Withdrawal of

investment &

interest are tax free

• Non-registered

account.

• Different accounts

• Any Interest

earned is taxable.

Age limit • None: Need earned

income to 71.

• 18 years old. • No limit.

Account ownership • Individual • Individual Individual and entities

Main purpose • Save for retirement.

• Optional usage

before retirement.

• Save/use for

anything you want.

• Short or long term.

• Save/use for

anything you want.

• Short or long term.

Tax treatment • Contributions are

tax-deductible in the

year of purchase.

• No tax treatment

required. Tax free

account.

• Interest earned is

taxable.

Savings and Investment Options

Comparison (continues)

FEATURES RRSP TFSA Chequing/saving

Withdrawals • Taxed. Withdrawal

added to income in

the year the amount

is withdrawn and

taxed.

• Never taxed. TFSA

is a tax free

account.

• No tax on

withdrawals.

Contribution limit

and room

• 18% of previous

year’s income.

• Less any pension

adjustment.

• Contribution is based

on the accumulated

available RRSP room.

• Started in 2009 with

$5,000 per year up

to year 2012.

• From 2013 to 2018

is $5,500 per year.

• Total room

available $53,000.

• No limit on deposits

• Cash deposit of

$10,000 or more

require source of

funds.

Carry forward

unused contribution

room

• Yes, until the year

you turn 71.

• Yes, indefinitely. • No limit.

Savings and Investment Options

Comparison (continues)

FEATURES RRSP TFSA Chequing/saving

Types of Investment • Invest in

1. GICs

2. Stocks

3. Mutual Funds

4. ETFs

• Earnings will be

taxed at date of

withdrawal.

• Invest in

1. GICs

2. Stocks

3. Mutual Funds

4. ETFs

• Earnings will NOT

be taxed at date

of withdrawal.

• Invest in

1. GICs

2. Stocks

3. Mutual Funds

4. ETFs

• Earnings taxed

when investment

cashed in.

Over-contribution

penalty tax

• Yes, 1% per month if

you exceed lifetime

over contribution

limit of $2000.

• Yes, 1% per month

on excess

contribution.

• No penalty on

deposit.

Contribute after

year 71

• No. Must convert to

a RRIF or annuity

when you turn 71 or

close the plan.

• Yes. There is no

ending date.

• Yes. There is no

ending date.

Financial stewardship <> A practical approach

End of presentation

Q & A