Embed Size (px)

Citation preview

DEL MAR SCHOOLS EDUCATION FOUNDATION Financial Statements and Supplemental Information

Year Ended June 30, 2020

FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2020

DEL MAR SCHOOLS EDUCATION FOUNDATION Financial Statements and Supplemental Information

Year Ended June 30, 2020

TABLE OF CONTENTS

INDEPENDENT AUDITOR’S REPORT 1

FINANCIAL STATEMENTS 3

Statement of Financial Position ......................................................................................................................... 3

Statement of Activities ....................................................................................................................................... 4

Statement of Functional Expenses ..................................................................................................................... 5

Statement of Cash Flows ................................................................................................................................... 6

Notes to the Financial Statements ...................................................................................................................... 7

Independent Auditor’s Report

To the Board of Trustees of Del Mar Schools Education Foundation Rancho Santa Fe, California Report on the Financial Statements

We have audited the accompanying financial statements of Del Mar Schools Education Foundation (DMSEF), which comprise the statement of financial position as of June 30, 2020, and the related statements of activities, functional expenses, and cash flows for the year then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

2

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Del Mar Schools Education Foundation as of June 30, 2020, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Emphasis of Matter – COVID-19

As more fully described in Note G to the financial statements, the Del Mar Schools Education Foundation may be materially impacted by the outbreak of the novel coronavirus (COVID-19), which was declared a global pandemic by the World Health Organization in March 2020.

El Cajon, California July 31, 2020

Financial Statements

The accompanying notes are an integral part of this statement. 3

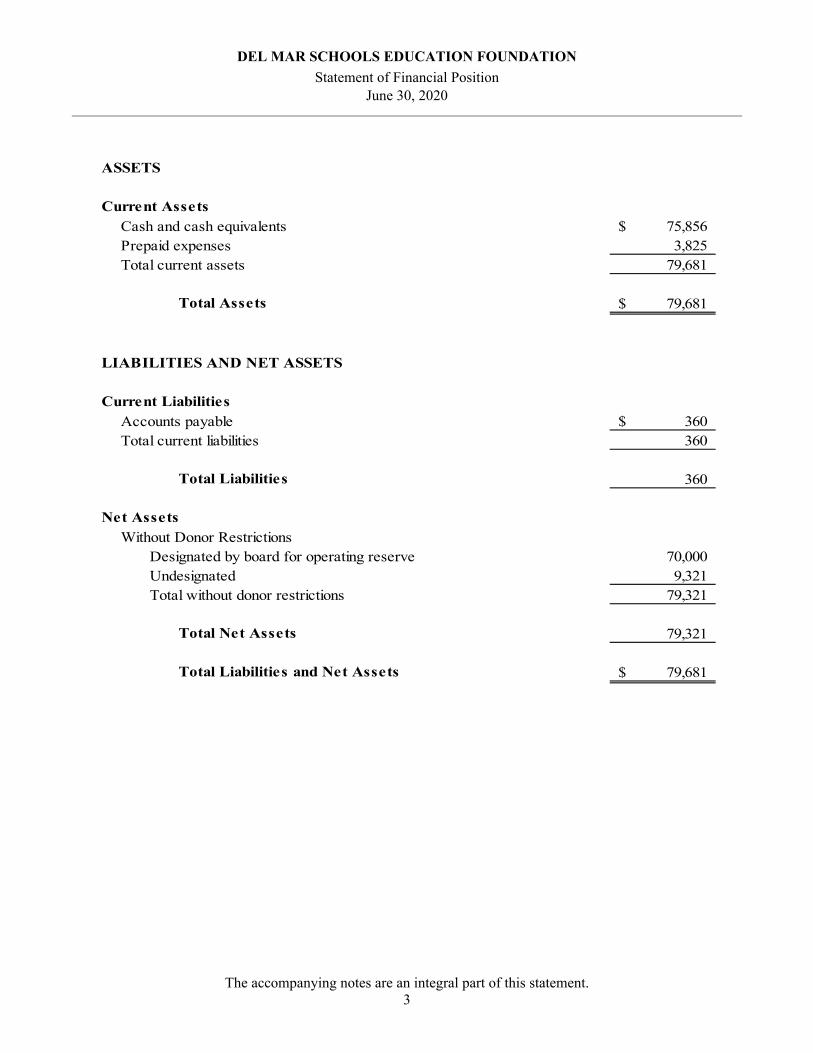

DEL MAR SCHOOLS EDUCATION FOUNDATION

Statement of Financial Position June 30, 2020

ASSETS

Current AssetsCash and cash equivalents 75,856$ Prepaid expenses 3,825 Total current assets 79,681

Total Assets 79,681$

LIABILITIES AND NET ASSETS

Current LiabilitiesAccounts payable 360$ Total current liabilities 360

Total Liabilities 360

Net AssetsWithout Donor Restrictions

Designated by board for operating reserve 70,000 Undesignated 9,321 Total without donor restrictions 79,321

Total Net Assets 79,321

Total Liabilities and Net Assets 79,681$

The accompanying notes are an integral part of this statement. 4

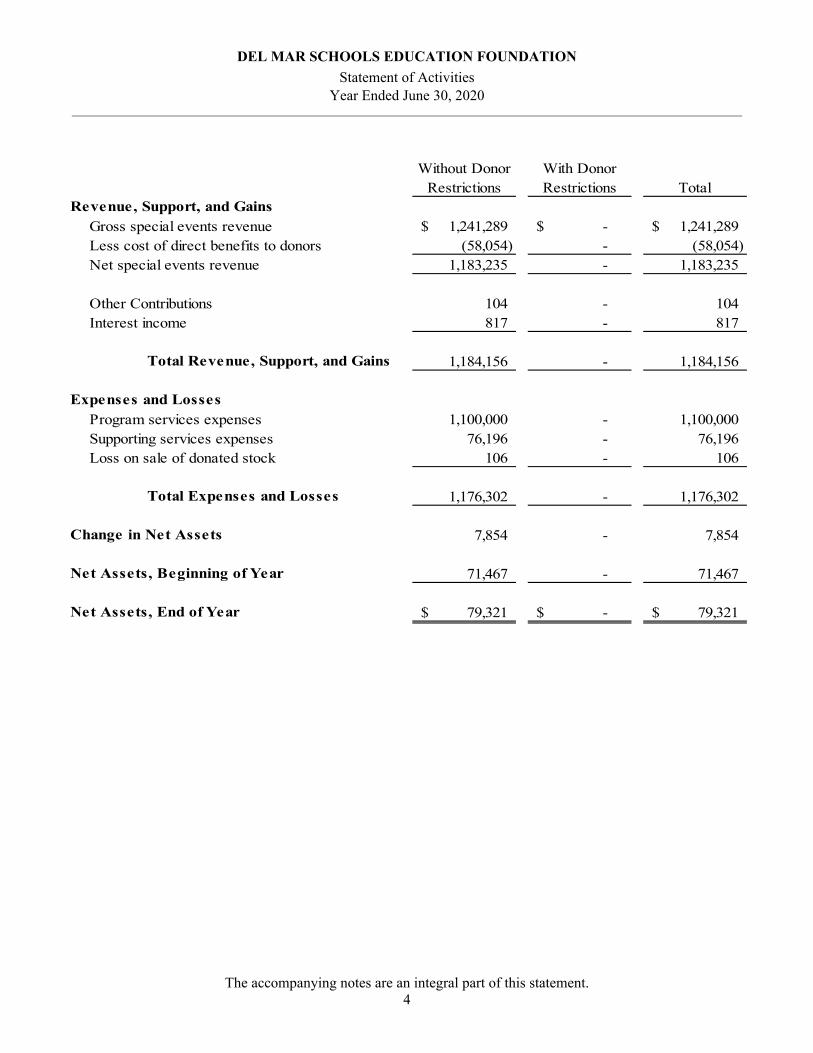

DEL MAR SCHOOLS EDUCATION FOUNDATION

Statement of Activities Year Ended June 30, 2020

Without Donor Restrictions

With Donor Restrictions Total

Revenue, Support, and GainsGross special events revenue 1,241,289$ -$ 1,241,289$ Less cost of direct benefits to donors (58,054) - (58,054) Net special events revenue 1,183,235 - 1,183,235

Other Contributions 104 - 104 Interest income 817 - 817

Total Revenue, Support, and Gains 1,184,156 - 1,184,156

Expenses and LossesProgram services expenses 1,100,000 - 1,100,000 Supporting services expenses 76,196 - 76,196 Loss on sale of donated stock 106 - 106

Total Expenses and Losses 1,176,302 - 1,176,302

Change in Net Assets 7,854 - 7,854

Net Assets, Beginning of Year 71,467 - 71,467

Net Assets, End of Year 79,321$ -$ 79,321$

The accompanying notes are an integral part of this statement. 5

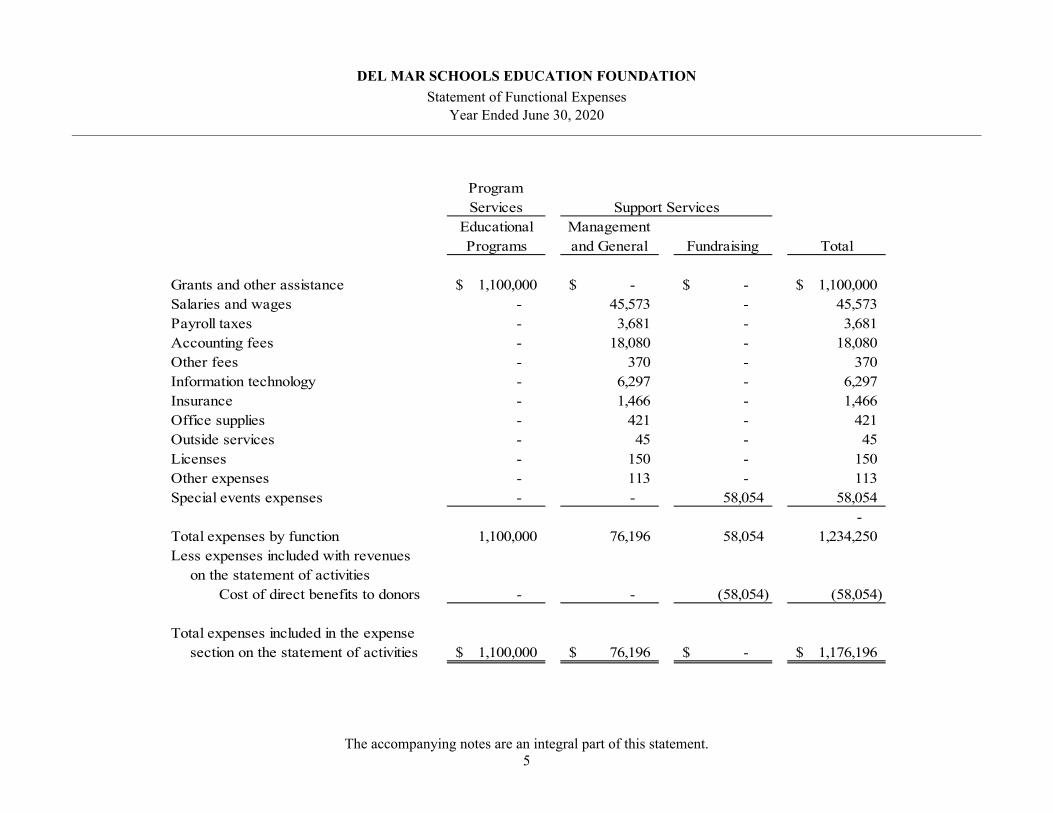

DEL MAR SCHOOLS EDUCATION FOUNDATION

Statement of Functional Expenses Year Ended June 30, 2020

Program Services

Educational Programs

Management and General Fundraising Total

Grants and other assistance 1,100,000$ -$ -$ 1,100,000$ Salaries and wages - 45,573 - 45,573 Payroll taxes - 3,681 - 3,681 Accounting fees - 18,080 - 18,080 Other fees - 370 - 370 Information technology - 6,297 - 6,297 Insurance - 1,466 - 1,466 Office supplies - 421 - 421 Outside services - 45 - 45 Licenses - 150 - 150 Other expenses - 113 - 113 Special events expenses - - 58,054 58,054

- Total expenses by function 1,100,000 76,196 58,054 1,234,250 Less expenses included with revenues

on the statement of activitiesCost of direct benefits to donors - - (58,054) (58,054)

Total expenses included in the expensesection on the statement of activities 1,100,000$ 76,196$ -$ 1,176,196$

Support Services

The accompanying notes are an integral part of this statement. 6

DEL MAR SCHOOLS EDUCATION FOUNDATION

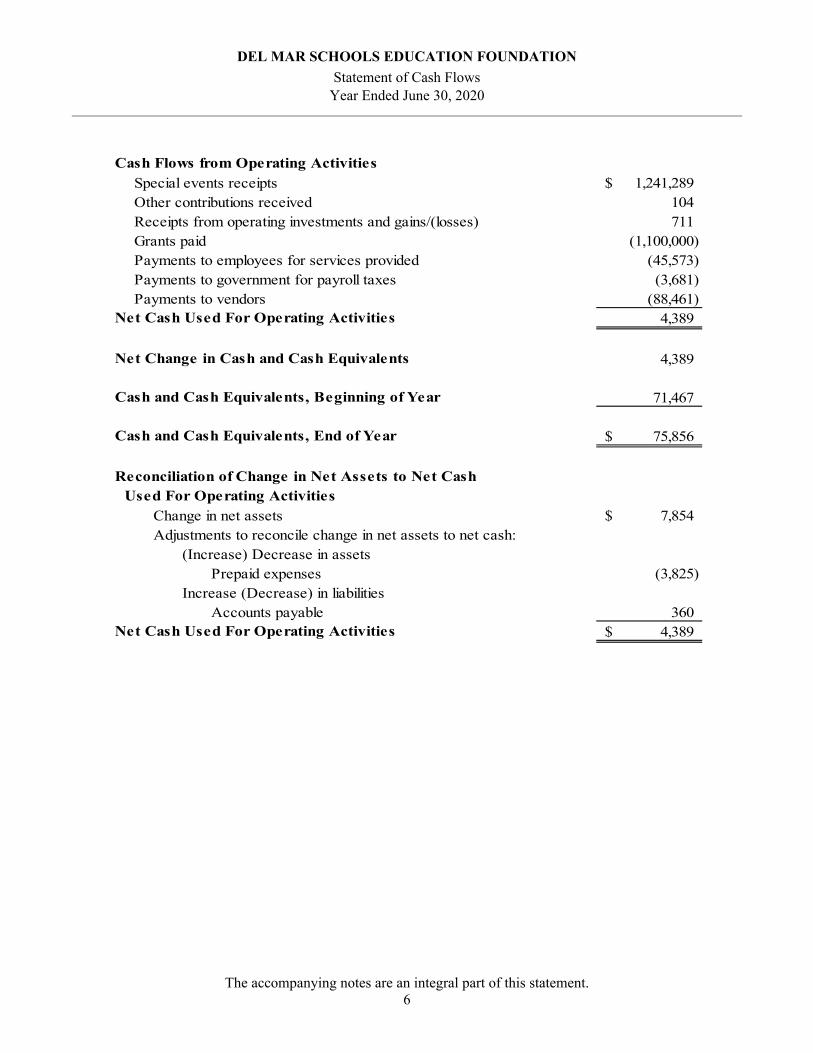

Statement of Cash Flows Year Ended June 30, 2020

Cash Flows from Operating ActivitiesSpecial events receipts 1,241,289$ Other contributions received 104 Receipts from operating investments and gains/(losses) 711 Grants paid (1,100,000) Payments to employees for services provided (45,573) Payments to government for payroll taxes (3,681) Payments to vendors (88,461)

Net Cash Used For Operating Activities 4,389

Net Change in Cash and Cash Equivalents 4,389

Cash and Cash Equivalents, Beginning of Year 71,467

Cash and Cash Equivalents, End of Year 75,856$

Reconciliation of Change in Net Assets to Net Cash Used For Operating Activities

Change in net assets 7,854$ Adjustments to reconcile change in net assets to net cash:

(Increase) Decrease in assetsPrepaid expenses (3,825)

Increase (Decrease) in liabilitiesAccounts payable 360

Net Cash Used For Operating Activities 4,389$

7

DEL MAR SCHOOLS EDUCATION FOUNDATION

Notes to the Financial Statements Year Ended June 30, 2020

A. Principal Activity and Summary of Significant Accounting Policies Organization The Del Mar Schools Education Foundation (the Foundation), a California nonprofit public benefit corporation, was organized with the purpose of providing benefits to the education programs and services of the Del Mar Union School District (the District). Educational Programs The Foundation’s primary purpose is to support and enrich the educational programs provided to students in the District. Each year the Foundation provides the District a grant in order to meet the following objectives:

Reduce class sizes so children receive individualized instruction on a regular basis, Provide enrichment offerings at all grade levels such as art programs, athletics, language programs,

STEAM and more, and

Provide specialized teachers for art, language, literacy, math, music, physical education, science and technology.

Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting period. Accordingly, actual results could differ from those estimates. Cash and Cash Equivalents The Foundation considers all cash and highly liquid financial instruments with original maturities of three months or less, which are neither held for nor restricted by donors for long-term purposes, to be cash and cash equivalents. Cash and highly liquid financial instruments restricted for endowments that are perpetual in nature, or other long-term purposes are excluded from this definition. Net Assets Net assets, revenues, gains, and losses are classified based on the existence or absence of donor or grantor-imposed restrictions. Accordingly, net assets and changes therein are classified and reported as follows: Net Assets Without Donor Restrictions – Net assets are available for use in general operations and not subject to donor restrictions. The governing board has designated, from net assets without donor restrictions, net assets for an operating reserve. Net Assets With Donor Restrictions – Net assets subject to donor imposed restrictions. Some donor-imposed restrictions are temporary in nature, such as those that will be met by the passage of time or other events specified by the donor. Other donor-imposed restrictions are perpetual in nature, where the donor stipulates that resources be maintained in perpetuity. Donor-imposed restrictions are released when a restriction expires, that is, when the stipulated time has elapsed, when the stipulated purpose for which the resource was restricted has been fulfilled, or both.

8

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

Revenue and Revenue Recognition Revenue is recognized when earned. Program service fees and payments received in advance are deferred to the applicable period in which the related services are performed, or expenditures are incurred, respectively. Contributions are recognized when cash, securities or other assets, an unconditional promise to give, or notification of a beneficial interest is received. Conditional promises to give are not recognized until the conditions on which they depend have been substantially met. Donated Services and In-Kind Contributions Volunteers contribute significant amounts of time to our program services, administration, and fundraising and developing activities; however, the financial statements do not reflect the value of these contributed services because they do not meet recognition criteria prescribed by generally accepted accounting principles. Advertising Advertising costs are expensed as incurred and approximated $0 during the year ended June 30, 2020. Functional Allocation of Expenses The costs of program and supporting services activities have been summarized on a functional bases in the statement of activities. The statement of functional expenses presents the natural classification detail of expenses by function. Accordingly, certain costs have been allocated among the program and supporting services benefited. Income Taxes The Del Mar Schools Education Foundation is organized as a California nonprofit corporation and is recognized by the IRS as exempt from federal income taxes under IRC Section 501(a) as organizations described in IRC Section 501(c)(3). Contributions to the Foundation qualify for the charitable contribution under IRC Sections 170(b)(1)(A)(vi) and have been determined not to be private foundations under IRC Sections 509(a)(1) and (3). The Foundation is required to file an annual Return of Organization Exempt from Income Tax (Form 990) with the IRS. In addition, the Foundation is subject to income tax on net income that is derived from business activities that are unrelated to their exempt purposes. We have determined that the Foundation is not subject to unrelated business income tax and therefore have not filed an Exempt Organization Business Income Tax Return (Form 990-T) with the IRS. The federal income tax and informational returns are subject to examination by the Internal Revenue Service for three years after the returns are filed. The Foundation is also exempt from California franchise or income tax under Section 23701d of the California Revenue and Taxation Code. The Foundation is required to file a California Exempt Organization Annual Information Return (Form 199) each fiscal year with the California Franchise Tax Board. In addition, the Foundation is required to file an Annual Registration Renewal Fee Report to Attorney General of California (Form RRF-1) to the California Registry of Charitable Trusts. The state income tax and informational returns are subject to examination by the California Franchise Tax Board for four years after the returns are filed. The Foundation follows provisions of uncertain tax positions as addressed in ASC 958. The Foundation recognizes accrued interest and penalties associated with uncertain tax positions as part of the income tax provision, when applicable. There are no amounts accrued in the financial statements related to uncertain tax positions for the year ended June 30, 2020.

9

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

Financial Instruments and Credit Risk The Foundation manages deposit concentration risk by placing cash, money market accounts, and certificates of deposit with financial institutions believed by the Foundation to be creditworthy. At times, amounts on deposit may exceed insured limits or include uninsured investments in money market mutual funds. To date, the Foundation has not experienced losses in any of these accounts. Credit risk associated with contributions receivable is considered to be limited due to high historical collection rates and because substantial portions of the outstanding amounts are due from board members and individuals supportive of the Foundations mission. Investments are made by diversified investment managers whose performance is monitored by the board of directors for the Foundation. Although fair values of investments are subject to fluctuation on a year-to-year basis, the Foundation believes that the investment policies and guidelines are prudent for the long-term welfare of the Foundation. New Accounting Guidance The Financial Accounting Standards Board (FASB) has issued the following Accounting Standards Updates (ASU) that became effective during the 2019-20 fiscal year: 1. FASB ASU 2014-09 Revenue from Contracts with Customers (Topic 606) 2. FASB ASU 2015-14 Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date 3. FASB ASU 2016-01 Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of

Financial Assets and Financial Liabilities. 4. FASB ASU 2016-04 Liabilities – Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage

for Certain Prepaid Stored-Value Products (a consensus of the Emerging Issues Task Force). 5. FASB ASU 2016-08 Revenue from Contracts with Customers (Topic 606): Principal versus Agent

Considerations (Reporting Revenue Gross versus Net). 6. FASB ASU 2016-10 Revenue from Contracts with Customers (Topic 606): Identifying Performance

Obligations and Licensing. 7. FASB ASU 2016-12 Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements

and Practical Expedients. 8. FASB ASU 2016-15 Statement of Cash Flows (Topic 230) Classification of Certain Cash Receipts and Cash

Payments (a consensus of the Emerging Issues Task Force). 9. FASB ASU 2016-16 Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other than Inventory 10. FASB ASU 2016-20 Technical Corrections and Improvements to Topic 606, Revenue from Contracts with

Customers. 11. FASB ASU 2017-01 Business Combinations (Topic 805): Clarifying the Definition of a Business 12. FASB ASU 2017-05 Other Income – Gains and Losses from the Derecognition of Nonfinancial Assets

(Subtopic 610-20): Clarifying the Scope of Asset Derecognition Guidance and Accounting for Partial Sales of Nonfinancial Assets.

13. FASB ASU 2017-07 Compensation – Retirement Benefits (Topic 715): Improving Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost.

14. FASB ASU 2018-03 Technical Corrections and Improvements to Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities.

15. FASB ASU 2018-09 Codification Improvements 16. FASB ASU 2020-04 Reference Rate Reform (Topic 848) Facilitation of the Effects of Reference Rate Reform

on Financial Reporting. 17. FASB ASU 2020-05 Revenue from Contracts with Customers (Topic 606) and Leases (Topic 842): Effective

Dates for Certain Entities.

10

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

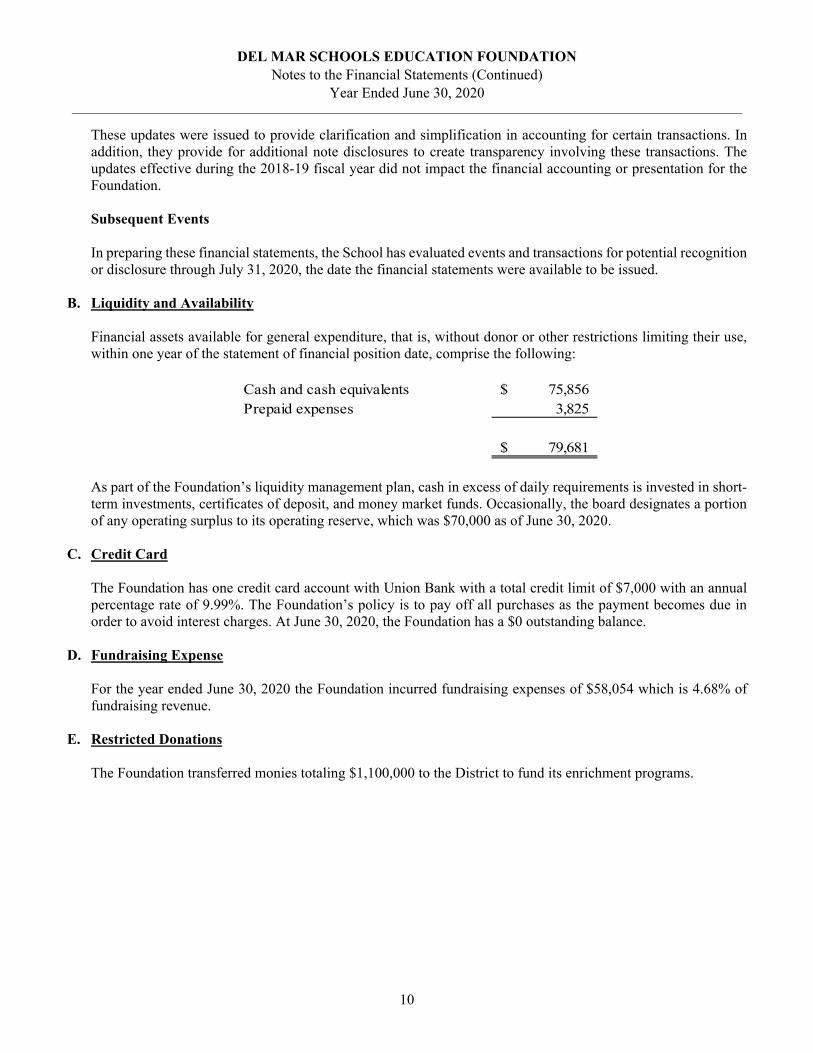

These updates were issued to provide clarification and simplification in accounting for certain transactions. In addition, they provide for additional note disclosures to create transparency involving these transactions. The updates effective during the 2018-19 fiscal year did not impact the financial accounting or presentation for the Foundation. Subsequent Events In preparing these financial statements, the School has evaluated events and transactions for potential recognition or disclosure through July 31, 2020, the date the financial statements were available to be issued.

B. Liquidity and Availability Financial assets available for general expenditure, that is, without donor or other restrictions limiting their use, within one year of the statement of financial position date, comprise the following:

Cash and cash equivalents 75,856$ Prepaid expenses 3,825

79,681$

As part of the Foundation’s liquidity management plan, cash in excess of daily requirements is invested in short-term investments, certificates of deposit, and money market funds. Occasionally, the board designates a portion of any operating surplus to its operating reserve, which was $70,000 as of June 30, 2020.

C. Credit Card The Foundation has one credit card account with Union Bank with a total credit limit of $7,000 with an annual percentage rate of 9.99%. The Foundation’s policy is to pay off all purchases as the payment becomes due in order to avoid interest charges. At June 30, 2020, the Foundation has a $0 outstanding balance.

D. Fundraising Expense For the year ended June 30, 2020 the Foundation incurred fundraising expenses of $58,054 which is 4.68% of fundraising revenue.

E. Restricted Donations The Foundation transferred monies totaling $1,100,000 to the District to fund its enrichment programs.

11

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

F. Upcoming Changes in Accounting Pronouncements The Financial Accounting Standards Board (FASB) has issued the following Accounting Standards Updates (ASU) that become effective over the next few fiscal years: 1. FASB ASU 2016-02 Leases (Topic 842) – Effective Fiscal Year Ending June 30, 2022 2. FASB ASU 2016-13 Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on

Financial Instruments – Effective Fiscal Year Ending June 30, 2024 3. FASB ASU 2017-04 Intangibles – Goodwill and Other (Topic350): Simplifying the Test for Goodwill

Impairment – Effective Fiscal Year Ending June 30, 2024 4. FASB ASU 2017-08 Receivables – Nonrefundable Fees and Other Costs (Subtopic 310-20): Premium

Amortization on Purchased Callable Debt Securities – Effective Fiscal Year Ending June 30, 2021 5. FASB ASU 2017-11 Earnings Per Share (Topic 260); Distinguising Liabilities from Equity (Topic 480);

Derivatives and Hedging (Topic 815): (Part I) Accounting for Certain Financial Instruments with Down Round Features, (Part II) Replacement of the Indefinite Deferral for Mandatorily Redeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests with a Scope exception. – Effective Fiscal Year Ending June 30, 2021

6. FASB ASU 2017-12 Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities – Effective Fiscal Year Ending June 30, 2022

7. FASB ASU 2018-01 Leases (Topic 842): Land Easement Practical Expedient for Transition to Topic 842 – Effective Fiscal Year Ending June 30, 2022

8. FASB ASU 2018-07 Compensation – Stock Compensation (Topic 718): Improvements to Nonemployee Share Based Payment Accounting. – Effective Fiscal Year Ending June 30, 2021.

9. FASB ASU 2018-08 Not-for-Profit Entities (Topic 958): Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. – Effective Fiscal Year Ending June 30, 2021

10. FASB ASU 2018-10 Codification Improvements to Topic 842, Leases – Effective Fiscal Year Ending June 30, 2022

11. FASB ASU 2018-11 Leases (Topic 842): Targeted Improvements – Effective Fiscal Year Ending June 30, 2022

12. FASB ASU 2018-12 Financial Service – Insurance (Topic 944): Targeted Improvements to the Accounting for Long-Duration Contracts – Effective Fiscal Year Ending June 30, 2025

13. FASB ASU 2018-13 Fair Value Measurement (Topic 820): Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement – Effective Fiscal Year Ending June 30, 2021

14. FASB ASU 2018-14 Compensation – Retirement Benefits – Defined Benefit Plans – General (Subtopic 715-20): Disclosure Framework – Changes to the Disclosure Requirements for Defined Benefit Plans – Effective Fiscal Year Ending June 30, 2023

15. FASB ASU 2018-15 Intangibles – Goodwill and Other – Internal Use Software (Subtopic 350-40): Customer’s Accounting for Implementation Costs Incurred ina Cloud Computing Arrangement That is a Service Contract (a consensus of the FASB Emerging Issues Task Force) – Effective Fiscal Year Ending June 30, 2022

16. FASB ASU 2018-16 Derivatives and Hedging (Topic 815): Inclusion of the Secured Overnight Financing Rate (SOFR) Overnight Index Swap (OIS) Rate as a Benchmark Interest Rate for Hedge Accounting Purposes – Effective Fiscal Year Ending June 30, 2022

17. FASB ASU 2018-17 Consolidation (Topic 810): Targeted Improvements to Related Party Guidance for Variable Interest Entities – Effective Fiscal Year Ending June 30, 2021

18. FASB ASU 2018-18 Collaborative Arrangements (Topic 808): Clarifying the Interaction between Topic 808 and Topic 606 – Effective Fiscal Year Ending June 30, 2022

19. FASB ASU 2018-19 Codification Improvements to Topic 326, Financial Instruments – Credit Losses – Effective Fiscal Year Ending June 30, 2024

20. FASB ASU 2018-20 Leases (Topic 842): Narrow Scope Improvements for Lessors – Effective Fiscal Year Ending June 30, 2022

12

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

21. FASB ASU 2019-01 Leases (Topic 842): Codification Improvements – Effective Fiscal Year Ending June 30, 2022.

22. FASB ASU 2019-02 Entertainment – Films – Other Assets – Film Costs (Subtopic 926-20) and Entertainment – Broadcasters – Intangibles – Goodwill and Other (Subtopic 920-350): Improvements to Accounting for Costs of Films and License Agreements for Program Materials (a consensus of the Emerging Issues Task Force – Effective Fiscal Year Ending June 30, 2022

23. FASB ASU 2019-03 Not-For-Profit Entities (Topic 958): Updating the Definition of Collections – Effective Fiscal Year Ending June 30, 2021

24. FASB ASU 2019-04 Codification Improvements to Topic 326, Financial Instruments – Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments – Effective Fiscal Year Ending June 30, 2021

25. FASB ASU 2019-05 Financial Instruments – Credit Losses (Topic 326): Targeted Transition Relief – Effective Fiscal Year Ending June 30, 2021

26. FASB ASU 2019-08 Compensation – Stock Compensation (Topic 718) and Revenue from Contracts with Customers (Topic 606): Codification Improvements – Share Based Consideration Payable to a Customer – Effective Fiscal Year Ending June 30, 2021

27. FASB ASU 2019-09 Financial Services – Insurance (Topic 944): Effective Date – Effective Fiscal Year Ending June 30, 2025

28. FASB ASU 2019-10 Financial Instruments – Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates - Effective Fiscal Years Ending June 30, 2022 and June 30, 2024

29. FASB ASU 2019-11 Codification Improvements to Topic 326, Financial Instruments – Credit Losses – Effective Fiscal Year Ending June 30, 2024

30. FASB ASU 2019-12 Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes – Effective Fiscal Year Ending June 30, 2024

31. FASB ASU 2020-01 Investments – Equity Securities (Topic 321), Investments – Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815) – Clarifying the Interactions between Topic 321, Topic 323, and Topic 815 (a consensus of the Emerging Issues Task Force). – Effective Fiscal Year Ending June 30, 2022

32. FASB ASU 2020-03 Codification Improvements to Financial Instruments – Effective Fiscal Years Ending June 30, 2021 and June 30, 2024

These updates were issued to provide clarification and simplification in accounting for certain transactions. In addition, they provide for additional note disclosures to create transparency involving these transactions. The updates effective during the future fiscal years are not expected to impact the financial accounting or presentation for the Foundation.

G. COVID-19 Impact and Considerations In March 2020 the World Health Organization declared the outbreak of the novel coronavirus COVID-19 a global pandemic. The nature of the pandemic resulted in a mandatory school property closure affecting the Del Mar Union School District from March 2020 and continuing into the Fall of 2020-21 school year. California Governor Gavin Newsom issued a state-wide executive order mandating that schools remain closed until the county in which the school is located is off the COVID-19 watch list for fourteen consecutive days. At this point in time, the Del Mar Union School District campuses remain closed until San Diego County meets the benchmark requirements. The circumstances surrounding COVID-19 create uncertainty in expectations for future donations and contributions to the Foundation. The Foundation expects a reduction in donations for the 2020-21 fiscal year, and consequently expects to reduce amounts donated to the Del Mar Union School District accordingly. The Foundation believes sufficient donations along with established reserves will allow for a continuation of operations.

13

DEL MAR SCHOOLS EDUCATION FOUNDATION Notes to the Financial Statements (Continued)

Year Ended June 30, 2020

H. Subsequent Event On July 24, 2020 the Del Mar Schools Education Foundation was approved for $11,330 in Paycheck Protection Program (PPP) Loan from the Small Business Administration. The PPP, established as part of the Coronavirus Aid, Relief and Economic Securities Act (CARES Act), provides for loans to qualifying businesses for amounts up to 2.5 times of the average monthly payroll expenses of the qualifying business. The loans and accrued interest are forgivable after 24 weeks as long as the borrower uses the loan proceeds for eligible purposes, including payroll, benefits, rent and utilities, and maintains its payroll levels. The amount of loan forgiveness will be reduced if the borrower terminates employees or reduces salaries. The unforgiven portion of the PPP loan is payable over two years at an interest rate of 1%, with a deferral of payments for the first six months. The Foundation intends to use the proceeds for purposes consistent with the PPP. While the Foundation currently believes that its use of the loan proceeds will meet the conditions for forgiveness of the loan, there is not a guarantee that the Foundation will not take actions that could cause the Foundation to be ineligible for forgiveness of the loan, in whole or in part.