Embed Size (px)

Citation preview

FINANCIAL STATEMENTSFINANCIAL STATEMENTS

Why Use Financial Why Use Financial Statements?Statements?

Investors and bankersInvestors and bankersSuppliers and creditorsSuppliers and creditorsYou and managementYou and management

Types of Financial Types of Financial StatementsStatements

Cash Flow StatementCash Flow Statement Income Statement Income Statement

(aka Profit-and-Loss)(aka Profit-and-Loss) Balance SheetBalance Sheet Personal Financial StatementPersonal Financial Statement

Cash Flow Cash Flow StatementStatement

Describes the flow of cash in and Describes the flow of cash in and out of a businessout of a business

Created at end of each monthCreated at end of each month

$$

Why is a Cash Flow Why is a Cash Flow Statement Important?Statement Important?

Expenses are paid with Expenses are paid with CASH not salesCASH not sales

Helps you estimate salesHelps you estimate sales Helps you estimate Helps you estimate

operating expensesoperating expenses

Constructing a Cash Flow Constructing a Cash Flow StatementStatement

Cash receipts - Disbursements = Net cash Cash receipts - Disbursements = Net cash flowflow

(inflow)(inflow) (outflow)(outflow)

Example:Example:A business took in $23,000.A business took in $23,000.

It spent $16,620.It spent $16,620.What is its cash flow? What is its cash flow?

$23,000 - $16,620 = $6380$23,000 - $16,620 = $6380

Positive cash flowPositive cash flow

Example:Example:For the month of March, a For the month of March, a business took in $18,920. business took in $18,920.

It spent $19,340. It spent $19,340. What is its monthly cash What is its monthly cash

flow? flow?

$18,920 - $19,340 = -$18,920 - $19,340 = -$420.00$420.00

Negative cash flowNegative cash flow

CASH FLOW STATEMENT

March 31, 2002

Cash Receipts $23,000

Disbursements

Equipment $12,000

Cost of goods 2,500

Selling Expense 200

Salaries 700

Advertising 130

Office Supplies 20

Rent 500

Utilities 90

Insurance 170

Taxes 70

Loan principal and interest 240

Total disbursements $ 16,620

NET CASH FLOW 6,380

Income StatementIncome Statement(Profit-and-loss Statement)(Profit-and-loss Statement)

Compares revenues and expenses over a Compares revenues and expenses over a specific period of time (usually monthly)specific period of time (usually monthly)

Revenue – Expenses = Net Profit (Loss)Revenue – Expenses = Net Profit (Loss) In a retail or wholesale business, In a retail or wholesale business,

expenses include “cost of goods sold”expenses include “cost of goods sold”

INCOME STATEMENT- Year ended December 31, 2001

Revenue

Sales $450,000

Cost of goods sold 250,000

Gross Profit $200,000

Operating Expenses

Salaries $70,000

Advertising 12,000

Rent 14,000

Utilities 3,600

Maintenance 1,200

Insurance 1,500

Miscellaneous 1,000

Total Expenses $103,300

NET PROFIT (before taxes) $ 96,700

Balance SheetBalance Sheet Tells entrepreneur what Tells entrepreneur what

the business is worth.the business is worth. Includes Includes assets assets and and

liabilitiesliabilities Asset – things of value Asset – things of value

that belong to the that belong to the businessbusiness

Liability – things that are Liability – things that are owed to othersowed to others

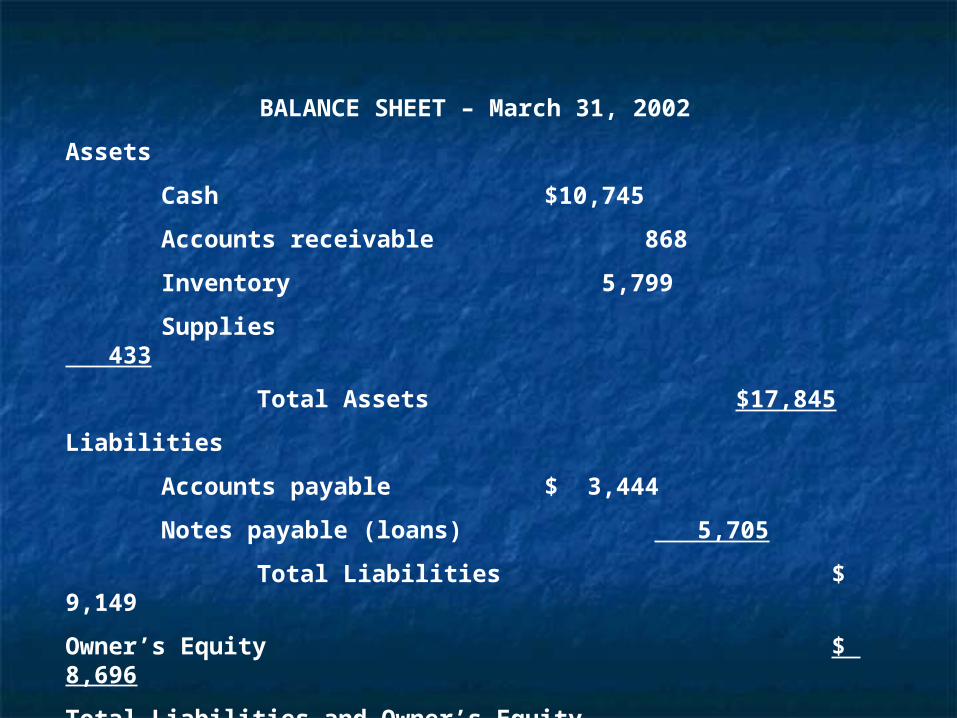

BALANCE SHEET – March 31, 2002

Assets

Cash $10,745

Accounts receivable 868

Inventory 5,799

Supplies 433

Total Assets $17,845

Liabilities

Accounts payable $ 3,444

Notes payable (loans) 5,705

Total Liabilities $ 9,149

Owner’s Equity $ 8,696

Total Liabilities and Owner’s Equity $17,845

Personal Financial Personal Financial StatementStatement

Potential investorsPotential investors Personal assetsPersonal assets

Savings accountSavings account Equity in houseEquity in house

Personal liabilitiesPersonal liabilities Credit cardsCredit cards House paymentHouse payment Car paymentCar payment

Net WorthNet Worth

Managing Your FinancesManaging Your Finances

Forecasting sales – you must Forecasting sales – you must predict what your business will do. predict what your business will do. You can use industry data or You can use industry data or actual sales data once your actual sales data once your company is operating.company is operating.

Evaluating profit potential – Evaluating profit potential – Fixed cost/selling price – variable cost Fixed cost/selling price – variable cost

= break even point= break even point Variable costs: expenses that changeVariable costs: expenses that change Fixed costs: expenses that don’t Fixed costs: expenses that don’t

changechange

Controlling CostsControlling Costs

Lease instead of buying an office or Lease instead of buying an office or warehouse.warehouse.

Lease equipment or purchase used Lease equipment or purchase used equipmentequipment

Hire part time help or use free Hire part time help or use free lancerslancers

Monitor and control utility costsMonitor and control utility costs

Managing Cash FlowManaging Cash Flow

Budget (put it in writing)Budget (put it in writing) Improve cash flowImprove cash flow

Tighten up credit and collectionsTighten up credit and collections Set up cash reserve for bad debtsSet up cash reserve for bad debts Take advantage of credit termsTake advantage of credit terms Offer cash discountsOffer cash discounts Manage inventory carefullyManage inventory carefully Put cash surpluses to workPut cash surpluses to work Keep payroll under controlKeep payroll under control Cut expensesCut expenses

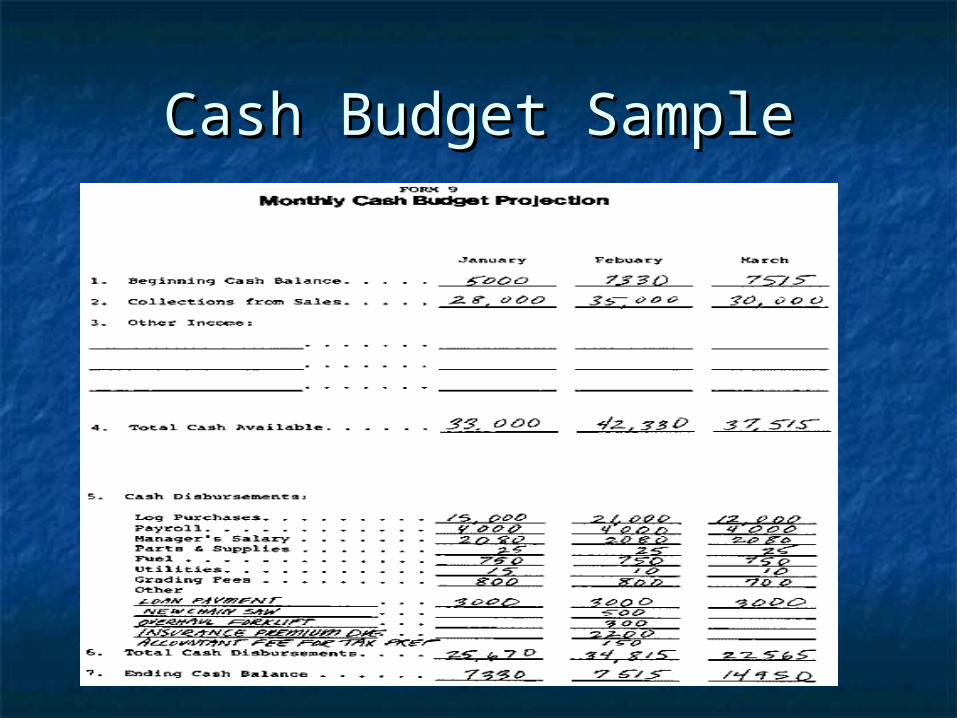

Cash Budget SampleCash Budget Sample

Plan for Capital Plan for Capital ExpendituresExpenditures

Long-term commitments of Long-term commitments of large sums of money to buy large sums of money to buy new equipment or replace new equipment or replace old equipment.old equipment.

Create savings accounts or Create savings accounts or plans to cover these to limit plans to cover these to limit your borrowing needs.your borrowing needs.

Managing TaxesManaging Taxes

Time income so you can control when it Time income so you can control when it is taxes (schedule sales for beginning of is taxes (schedule sales for beginning of new year will defer taxes)new year will defer taxes)

Time deductionsTime deductions Choose the depreciation method that is Choose the depreciation method that is

most beneficial to your specific situation.most beneficial to your specific situation. Write off bad debt.Write off bad debt. Claim research and development costs.Claim research and development costs. Keep expense records.Keep expense records. Keep current with tax laws.Keep current with tax laws.

Managing CreditManaging Credit

Granting credit involves 5 steps:Granting credit involves 5 steps:

Obtain information from customers.Obtain information from customers. Checking credit and background before you extend creditChecking credit and background before you extend credit Evaluating credit applicationsEvaluating credit applications Making your decisionMaking your decision ClosingClosing

Collect on accountsCollect on accounts